Residential Real Estate - teja8.kuikr.com · PDF fileestate developers.The sector is expected...

66

INDIA RESIDENTIAL REAL ESTATE I RESEARCH ANNUAL REPORT 2016 India Residential Real Estate BENGALURU I NCR I MMR I PUNE I CHENNAI I HYDERABAD I KOLKATA

Transcript of Residential Real Estate - teja8.kuikr.com · PDF fileestate developers.The sector is expected...

INDIA RESIDENTIAL REAL ESTATE I RESEARCH

ANNUAL

REPORT

2016

I nd i a

Res iden t i a l

Rea l E s t a te

BENGALURU I NCR I MMR I PUNE I CHENNAI I HYDERABAD I KOLKATA

INDIA RESIDENTIAL REAL ESTATE I RESEARCH

F O R E W O R D

The year 2016 was yet another lackluster year for the Indian Real Estate Industry in terms of sales and new

launches. However, the flurry of policy announcements in the form of RERA, GST, Demonetization, and Benami

act made during the year have ensured that 2016 will be remembered as a year of reincarnation of the Indian Real

Estate Industry.

The perennial issues of transparency that had severely impacted buyers sentiment were addressed by the

government by making RERA into a reality. Passing of RERA was welcomed by almost all the recognized builders.

It helps weed out the bad apples of the developer community, that normally tarnishes the image of the entire real

estate developers. The sector is expected to witness consolidation in the coming years, predominantly due to the

smaller players who may find complying with RERA norms difficult as well as expensive and may end up merging

with a stronger entity.

Having said that, well established developers too will now have to re-look at their strategy of new launches,

project planning and execution. Not to mention the importance of better capital deployment will gain the center

stage. With the vigil increasing on Benami transaction and black money, the early stage investors and speculators

almost abandoned the pre-launch and early stage construction projects. However, there has been a gradual

increase in the enquiries of ready-to-move-in projects. This is a good sign for the industry, as it clearly indicates

that the interest of genuine end users that stands to gain momentum over a period of time.

Overall, in 2016, the rules of the games were reset, but, its evident that all the policy development and

announcements made during the year have laid down a very strong ground for the revival of industry.

Prashant Kumar Thakur Head of Research & Data Services

INDIA RESIDENTIAL REAL ESTATE I RESEARCH

E X E C U T I V E S U M M A R Y

• In 2016, the top seven cities in the country have recorded a decline of nearly 40 percent in the new launch

supply compared to its preceding year. The major reason behind this turmoil can be attributed to the huge

stock of unsold inventory in the primary market, low sales velocity and negative buyer sentiments due to high

property prices. Moreover, developers in these cities started focusing on clearing the existing stock by

providing lucrative offers to home buyers, instead of infusing new launch supply.

• The top seven cities across India have witnessed launch of approximate 2.25 Lac residential dwelling units in

2016. MMR contributed a maximum share of this new launch supply, at 28 percent, followed by Pune,

Bengaluru and NCR at 18,17 & 16 percent, respectively.

• The residential market of National Capital Region (NCR) was the the worst affected in terms of new launch

supply in 2016, an approximate 61 percent decline recorded compared to the new launch supply of 2015,

followed by Bengaluru, Chennai and Kolkata, at 41, 37 and 33 percent, respectively. Negative investor

sentiment coupled with enormous quantum of under construction supply in Greater Noida and Gurgaon has

restricted the developer focus on new launch projects.

• Q4 2016 has recorded a sharp decline of 58 percent in new launch supply compared to Q4 2015. The

demonetization drive by the central government has restricted developers to launch new projects in the cash

crunch market. This is because the pre launch and new launch are the only stages, where developers get

maximum traction from the consumer due to low ticket price.

• In 2016, in the top seven cities, an approximate 66 percent unit launched were under the budget of 60 Lacs

ticket price properties. The new launch supply trend clearly connotes that developers in top cities started

aligning with the consumer demand for affordable and mid segment properties.

• Interestingly, the premium residential market of the country (MMR) has recorded 57 percent launches under

the ticket price of 60 Lacs. The above price bracket has been primarily chosen to cater the demand of those

home buyers who are holding their purchase decision due to skyrocketing prices and non-availability of

affordable property options in the region.

• Fewer new launches in the last quarter of 2016 have helped in bringing down the unsold inventory level in top

seven cities. Unsold inventory decreased by 3 percent, from 7,56,373 units in Q3 2016 to 7,34,610 units in Q4

2016. Lucrative offers and easy payment plans on ready to move in properties and mid stage construction

properties have marginally helped developers to clear their existing stock.

• The year 2016 witnessed active participation from Private equity players in the Indian real estate industry.

Approximately $5.5 billion was pumped in through the private equity route, which was an increase of 40

percent as compared to 2011.

INDIA RESIDENTIAL REAL ESTATE I RESEARCH

H I G H L I G H T S O F U N I O N B U D G E T 2 0 1 7 - 1 8 A N D I T S I M P A C T O N R E A L E S T A T E S E C T O R

Announcement Impact

Infrastructure Status to Affordable

Housing

Reduces the cost of borrowing for real estate developers, Provides easy

access to finance and spur investments, Opening of External Commercial

Borrowing (ECB) route and Taxation benefits for the developers.

An increase in budget allocation under

PMAY from 15,000 Cr to 23,000 Cr to

complete 1 Crore houses by 2019

Increased PMAY will provide budget housing segment with a cheaper

source of finance and increase employment opportunities in rural area

which extends supports to the "Housing For All By 2022" mission.

Revising the size of carpet area for low

income group houses

Will enhance uniformity in market measurement and thereby easing the

decision making process for the homebuyers. The buyer will now get a

spacious house of carpet area 30 to 60 Sq.mt. instead of built up area. The

30 sq.m limit will apply only in case of municipal limits of 4 metropolitan

cities and for the rest of the country, the limit is 60 sq.m

Revising the holding period for capital

gain tax from 3 years to 2 years

This move will reduce the capital gain tax liability while encouraging the

mobility of assets. It will also make the real estate sector more attractive

for investors.

Boost in home loans

The refinancing of individual housing loans of 20,000 crore by the National

Housing Bank (NHB) will aid the housing finance companies and low

income borrowers.

Special benefit for AMRUT and Smart

Cities

An increased fund allocation of 9,000 crore for AMRUT and Smart Cities

will boost the real estate development, especially in tier 2 and tier 3 cities

falling under this scheme.

Ease in FDI Norms

FDI can now be bought into the construction sector in any amount and

for any size of project. This decision will help in strengthening those

projects that could not receive capital due to conditions applicable for

attracting FDI.

Tax relaxation for JDA developed

properties

For Joint Development Projects, the payment of capital gain tax will be in a

year after the project is completed.

Interest subsidy for lower income

group home buyers

Interest subsidy of 3% and 4% for housing loans of up to INR 12 Lacs and

INR 9 Lacs was announced for middle-income group segment. In rural

areas, 3% subsidy was announced for loans of up to INR 2 Lacs to build

and expand existing housing unit.

Tax relief for developers holding

unsold stock

The developer will now pay capital gain tax only in the year when the

project is completed. This will reduce the tax burden of the developer and

encourage to liquidate inventory at a faster rate.

INDIA RESIDENTIAL REAL ESTATE I RESEARCH

CONTENTS

PAN INDIA

6

BENGALURU

11

43

CHENNAI

HYDERABADKOLKATA

MMR

PUNE

27

36

NCR

19

5851

INDIA RESIDENTIAL REAL ESTATE I RESEARCH

INDIA RESIDENTIAL REAL ESTATE I RESEARCH

No. o

f U

nits

R E S I D E N T I A L S U P P L Y - 2 0 1 5 V S 2 0 1 6

2016 ended with the lowest number of new launches

across the top seven cities of India since 2012. There

has been a 40 percent decline in the new launch supply

recorded in the year 2016 compared to the previous

year.

Q4 2016, considered as the worst time-frame in 2016,

has recorded nearly 58 percent whopping decline in

new launch supply when compared to Q4-2015.

Due to demonetization drive by the Central

Government, most of the developers restricted to

infuse new launch supply in the market. Even festive

season couldn't boost the market sentiments in the last

quarter of the year 2016. Additionally, the sales volume

in top cities also impacted badly in the Q4- 2016.

** Source: QuikrHomes Data – Values excluding layout and plots

Note: The Top seven cities are Bengaluru, Chennai, National Capital Region(NCR), Hyderabad, Kolkata, Mumbai Metropolitan Region(MMR) and Pune.

Time-frame Q1 2016 Q2 2016 Q3 2016 Q4 2016

% Change -2015 vs 2016 -33% -36% -35% -58%

R E S I D E N T I A L S U P P L Y – T O P C I T I E S

National Capital Region witnessed the sharpest

drop in new launch supply by 61 percent in 2016,

compared to the preceding year. This was

followed by Bengaluru, Chennai and Kolkata by

41, 37 and 33 percent, respectively.

However, Hyderabad is the only city, which has

witnessed a marginal drop in new launch supply

by just 4 percent.

Post formation of the separate state, the realty

sentiments in Hyderabad are heading towards

the north and showing a marginal increase in

capital price and new launch supply.

INDIA RESIDENTIAL REAL ESTATE I RESEARCH

C I T Y W I S E S P L I T O F R E S I D E N T I A L L A U N C H E S - 2 0 1 6

B U D G E T W I S E S P L I T O F N E W L A U N C H E S - T O P C I T I E S 2 0 1 6

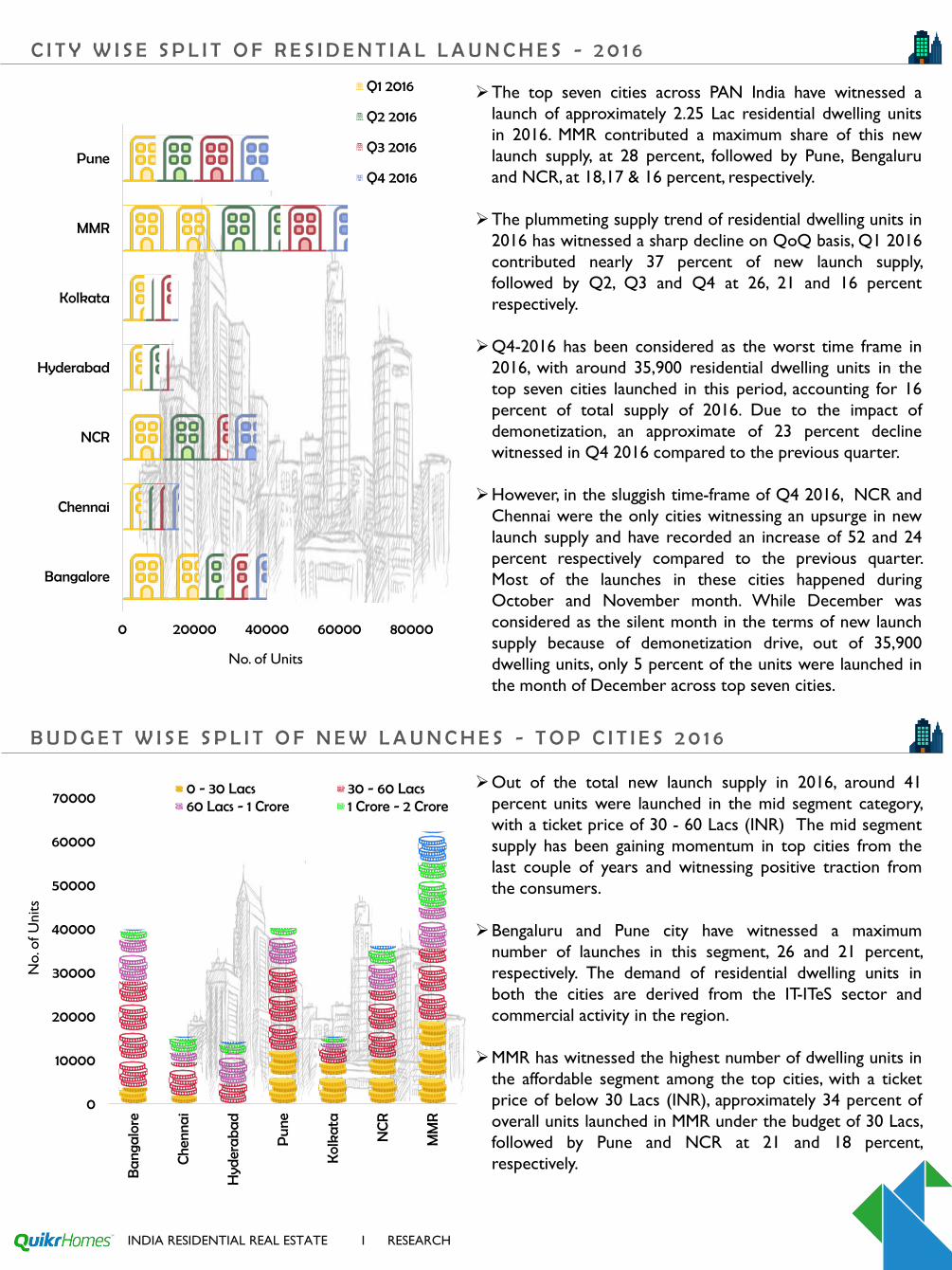

The top seven cities across PAN India have witnessed a

launch of approximately 2.25 Lac residential dwelling units

in 2016. MMR contributed a maximum share of this new

launch supply, at 28 percent, followed by Pune, Bengaluru

and NCR, at 18,17 & 16 percent, respectively.

The plummeting supply trend of residential dwelling units in

2016 has witnessed a sharp decline on QoQ basis, Q1 2016

contributed nearly 37 percent of new launch supply,

followed by Q2, Q3 and Q4 at 26, 21 and 16 percent

respectively.

Q4-2016 has been considered as the worst time frame in

2016, with around 35,900 residential dwelling units in the

top seven cities launched in this period, accounting for 16

percent of total supply of 2016. Due to the impact of

demonetization, an approximate of 23 percent decline

witnessed in Q4 2016 compared to the previous quarter.

However, in the sluggish time-frame of Q4 2016, NCR and

Chennai were the only cities witnessing an upsurge in new

launch supply and have recorded an increase of 52 and 24

percent respectively compared to the previous quarter.

Most of the launches in these cities happened during

October and November month. While December was

considered as the silent month in the terms of new launch

supply because of demonetization drive, out of 35,900

dwelling units, only 5 percent of the units were launched in

the month of December across top seven cities.

0 20000 40000 60000 80000

Bangalore

Chennai

NCR

Hyderabad

Kolkata

MMR

Pune

No. of Units

Q1 2016

Q2 2016

Q3 2016

Q4 2016

Out of the total new launch supply in 2016, around 41

percent units were launched in the mid segment category,

with a ticket price of 30 - 60 Lacs (INR) The mid segment

supply has been gaining momentum in top cities from the

last couple of years and witnessing positive traction from

the consumers.

Bengaluru and Pune city have witnessed a maximum

number of launches in this segment, 26 and 21 percent,

respectively. The demand of residential dwelling units in

both the cities are derived from the IT-ITeS sector and

commercial activity in the region.

MMR has witnessed the highest number of dwelling units in

the affordable segment among the top cities, with a ticket

price of below 30 Lacs (INR), approximately 34 percent of

overall units launched in MMR under the budget of 30 Lacs,

followed by Pune and NCR at 21 and 18 percent,

respectively.

0

10000

20000

30000

40000

50000

60000

70000

Ba

nga

lore

Che

nna

i

Hyd

era

ba

d

Pu

ne

Kol

kata

NC

R

MM

R

No. o

f U

nits

0 - 30 Lacs 30 - 60 Lacs60 Lacs - 1 Crore 1 Crore - 2 Crore

INDIA RESIDENTIAL REAL ESTATE I RESEARCH

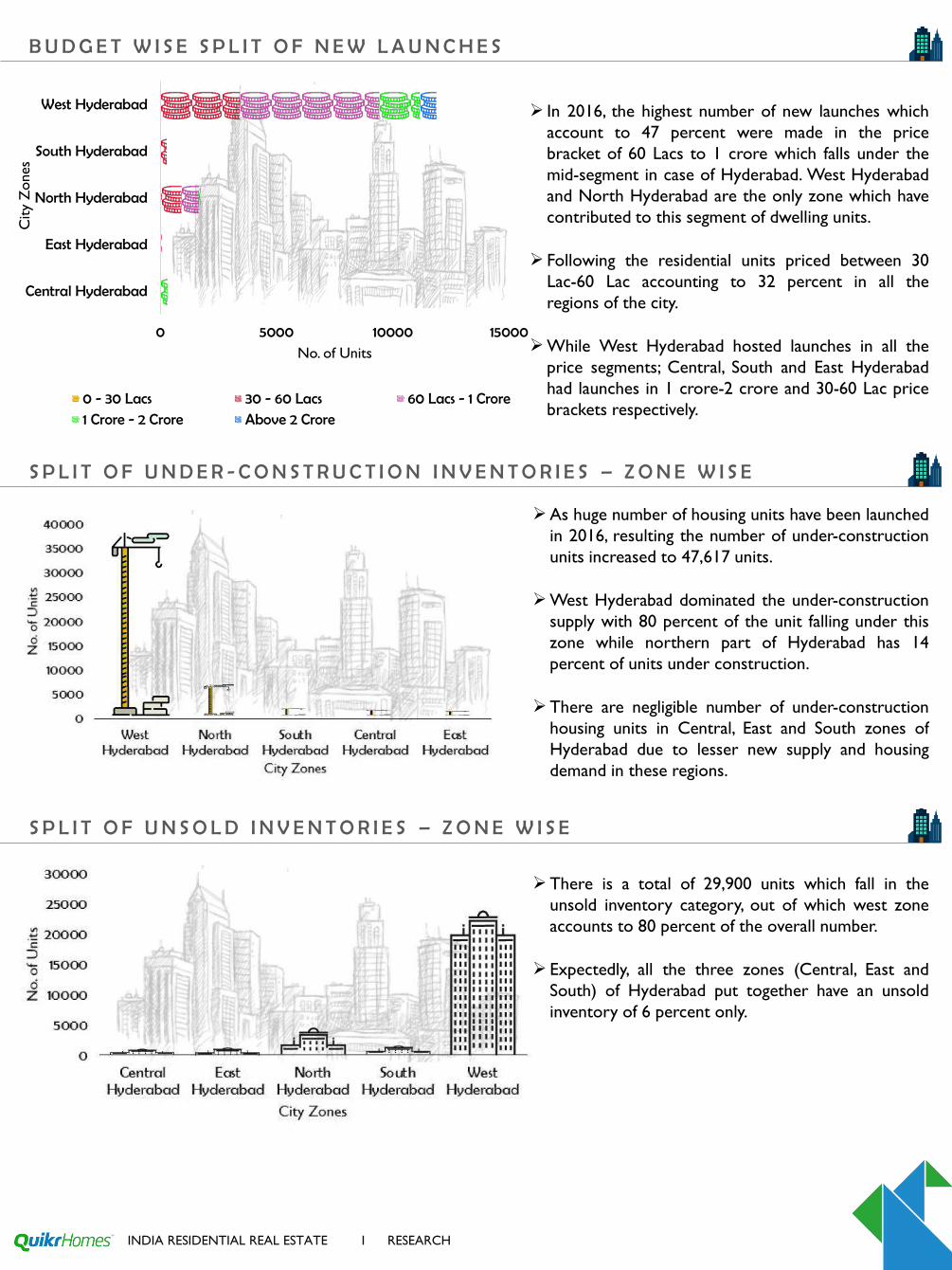

Most of the launches in this segment happened in the peripheral regions of the city. Zones such as Mumbai Beyond

Thane and Mumbai Beyond Mira Road were the biggest contributors in this supply. High property prices and shortage of

land bank within the city center have forced the developer interest to focus on these areas for their portfolio expansion.

Additionally, easy accessibility and connectivity to city commercial hub has made these zones one of the most sought

after.

MMR is the hub of premium segment properties, out of total supply in the premium segment (above 2 crore (INR)),

nearly 68 percent units were launched in the micro markets of Western suburbs, Central suburbs and South zone of

MMR region, followed by NCR and Hyderabad, at 10 and 7 percent, respectively.

Fewer new launches in the last quarter of 2016 have helped in bringing down the unsold inventory level in top seven cities.

Unsold inventory decreased by 3 percent, from 7,56,373 units in Q3 2016 to 7,34,610 units in Q4 2016.

On an average basis, the current unsold stock in the top seven cities will take nearly 47 months to absorb in the primary

market. The calculation of inventory overhang is arrived from the average sales velocity of last 12 months in the primary

market in the respective city.

Pune continues to be among the best performing residential markets in the country, with lowest inventory overhang,

followed by Kolkata and Bengaluru.

NCR and MMR remained the worst performing market in terms of unsold inventory. Out of total unsold inventory, nearly

31 percent of unsold stock is available in NCR at the different stages of construction, followed by MMR and Bengaluru, at

25 and 15 percent, respectively.

To liquidate current unsold inventory, NCR residential market will take an approximate 70 months and MMR will take an

approximate 60 months, while Bengaluru residential market will take 40 odd months to absorb the current unsold

inventory.

U N S O L D I N V E N T O R Y I N T O P C I T I E S

INDIA RESIDENTIAL REAL ESTATE I RESEARCH

REGULATORY UPDATES

Proposals for reduction of stamp duty on registration of houses has come up to reduce burden to the home buyers

as 2508 cities in 26 states have been shortlisted by the GoI under the 'Pradhan Mantri Awas Yojana' for providing

affordable houses to the urban poor

The Securities and Exchange Board of India (Sebi) has relaxed rules on Real Estate Investment Trusts (REITs) by

allowing high investments in under-construction projects, rationalised unit holder consent on related transactions and

removed restrictions on special purpose vehicle (SPV)

INFRASTRUCTURE UPDATES

Monetization of completed public funded national highway projects through Toll-Operate Transfer mode based on the

predicted collection of user fee receivables, through private sector efficiency and expertise has been proposed and

the proceeds shall be utilised for construction, operation and maintenance of national highways

A 1,400-km long highway which starts in the eastern region of India from Moreh and ends in Myanmar’s Tamu city

aids in linking India with Southeast Asia by land which will boost the trade and cultural exchanges between the three

countries

MAJOR DEALS

About Rs 7,296 crore has been allocated for two central schemes -- Atal Mission for Rejuvenation and Urban

Transformation (AMRUT) and 'Smart Cities' Mission with focus on provision of clean drinking water, setting up of

sanitation and solid waste management systems, efficient mobility and public transportation and affordable housing

Tata Value Homes, a 100 per cent subsidiary of Tata Housing Development Company, has raised USD 25 million i.e. Rs

168 crore for construction of affordable housing projects through CDC, UK's Development Finance Institution (DFI)

and IFC, a member of the World Bank group

R E A LT Y N E W S

INDIA RESIDENTIAL REAL ESTATE I RESEARCH

INDIA RESIDENTIAL REAL ESTATE I RESEARCH

POPULATION

CITY

OVERVIEW

709 km2 8.42 Million

AREA

ABOUT CITY

Third most populous city and fifth most populous urban

agglomeration in India

POPULATION GROWTH RATE

38% 10.3%

ECONOMIC GROWTH RATE

*As of year 2008

RESIDENTIAL MARKET GROWTH DRIVERS

East Bengaluru: Whitefield, ITPL, Marathahalli-Sarjapur Road

West Bengaluru: Peenya Industrial Area.

North Bengaluru: Manyata Tech Park, Kempegowda

International Airport, Bagalur Tech Park (Under Construction)

South Bengaluru: Electronic City and Hosur Road

INFRASTRUCTURE

Existing: Namma Metro Phase 1, Signal Free Bellary Road, Outer Ring Road

Upcoming: Peripheral Ring Road (PPR), Namma Metro Phase 3

RESIDENTIAL UNITS LAUNCHED

39,935 units

PREDOMINANT BUDGET RANGE

30 Lac - 60 Lac

*Constitutes 61 % of total Supply

HIGHEST NUMBER OF LAUNCHES

East Bengaluru (13,308 units)

% CHANGE IN PRICE 2015 vs 2016

% CHANGE IN NEW LAUNCH SUPPLY – 2015 vs 2016

41%

UNSOLD STOCK

1,09,452 units

CITY INVENTORY OVERHANG

UNDER CONSTRUCTION

UNITS

1,98,711 units

*As per Census 2011

Icons Source: Flaticon

40 Months

3%

INDIA RESIDENTIAL REAL ESTATE I RESEARCH

N E W L A U N C H S U P P L Y T R E N D - 2 0 1 5 V S 2 0 1 6

Bengaluru, one of the best performing residential market

among top cities has witnessed a decline of 41 percent in

new launch supply in 2016 compared to its preceding year.

The decline in new launch supply in the residential market

is directly related to piled up stock in the primary market.

Moreover, developers are also focusing to clear the piled

up stock, instead of infusing new supply in the market.

Demonetization has badly impacted the residential supply

in the last quarter of 2016, a whopping 74 percent decline

was recorded in new launch supply in Q4 2016, compared

to Q4 2015. The drive not only halted the new launch

supply trend in the city, but also impacted the sales

volume dreadfully.

Z O N E W I S E S P L I T O F R E S I D E N T I A L L A U N C H E S

0 5000 10000 15000

Central Bangalore

East Bangalore

North Bangalore

South Bangalore

West Bangalore

No. of units

City

Zones

Q1 2016 Q2 2016 Q3 2016 Q4 2016

East Bengaluru accounted for 33 percent of new launch

supply in 2016, followed by South and North Bengaluru,

30 and 24 percent respectively.

East Bengaluru is one of the prominent zones of the

Bengaluru city. The zone has witnessed the whopping

decline of 55 percent in new launch supply in 2016 over

2015. Well established offices spaces in Whitefield and

commercial developments along Marathahalli - Sarjapur

Road stretch have made this zone one of the most sought

after in the city and attracted lot of developers for their

portfolio expansion. Micro Market such as Whitefield,

Varthur and Sarjapur road are persistently witnessing new

launch supply due to their proximity to the commercial

hub of the city and improved physical and social

infrastructure.

South Bengaluru recorded the decline of 40 percent in new launch supply compared to previous year. The peripheral

boundaries of the zone are slowly gaining the momentum in new launch supply from past couple of years Micro markets

such as Chandapura Anekal Road, Jigani, Attibele and Chandapura have witnessed the launch of nearly 25 percent of

dwelling units out of total supply launched in the South Bengaluru in 2016. Commercial office spaces in Electronic city

and commercial corridor along with the Bannerghatta Road and Hosur Road have derived the realty sentiments in the

zone and boosted the real estate activity in and around the South Bengaluru.

North Bengaluru is one of the most sought after zone of the Bengaluru city because of the presence of Kempegowda

International Airport in the vicinity and the upcoming Bagalur Tech Park. The zone has witnessed a decline of nearly 23

percent in new launch supply compared to previous year because of the high number of unsold inventory in the primary

market.

The North Zone of Bengaluru has been witnessing traction from the developer from 2012 onwards and has completely

transformed the realty landscape, nearly 67,753 dwelling units has been infused in the North Bengaluru, since then. Micro

Markets such as Hebbal, Thanisandra Main Road, Hennur Main Road, Yelahanka, and Jakkur are the key micro market of

this zone and hold strong future growth potential because of the availability of ample land bank, proximity to Manyata

Tech Park and easy accessibility and connectivity to Kempegowda International Airport.Continued..

INDIA RESIDENTIAL REAL ESTATE I RESEARCH

T O P M I C R O M A R K E T S O F 2 0 1 6 - B A S E D O N N E W L A U N C H S U P P L Y

0 1000 2000 3000 4000

Sarjapur Road

Kengeri

Chandapura Anekal Road

Panathur

Devanahalli

Kanakapura Road

No. of Units

Mic

ro M

arke

ts

Located in south east Bengaluru, Sarjapur Road has

emerged as one of the most prominent residential

destination in the city over the last decade. The

micro market has witnessed the launch of 3,611

dwelling units in the year 2016. The locality is

strategically located between two major IT hotspots

of the city – Outer Ring Road (ORR) on one side

and Electronic City on the other. The micro market

has witnessed the launch of 13 projects in the year

2016. Additionally, the 16 km stretch offers excellent

property options for all segments of home buyers.

Kengeri and Chandapura Road are the emerging

micro market in the city. Both the micro markets

offer affordable property options and hold strong

future growth potential.

Devanahalli, Kanakapura Road and Panathur are the fastest developing micro market in the city, The IT/ITeS services in the

region has derived the realty sentiments in these micro markets and has boosted real estate development. Devanahalli and

Panathur holds strong growth potential due to ample availability of land bank and proximity to the key commercial hub,

while Kanakapura Road has witnessed a positive traction from the developers for the last couple of years and has a

presence of improved physical and social infrastructure, making it more viable for the end use purpose.

The western quadrant of the city has witnessed an upsurge in new launch supply, an approximate 31 percent increase is

recorded in 2016 compared to the previous year. The zone is slowly gaining momentum and transforming it into a

residential market from the industrial area status.

Central Bengaluru, the high end residential market of the city has witnessed a limited number of residential supply in

2016 due to unavailability of land bank.

B U D G E T W I S E S P L I T O F N E W L A U N C H E S

0 5000 10000 15000

CentralBangalore

EastBangalore

NorthBangalore

SouthBangalore

WestBangalore

No. of Units

City

Zones

0 - 30 Lacs 30 - 60 Lacs 60 Lacs - 1 Crore

1 Crore - 2 Crore Above 2 Crore

The southern and the eastern zones of the city have

witnessed a maximum number of launches under the

budget of 30 - 60 Lacs in 2016, accounting for 36

percent and 32 percent, respectively.

North Bengaluru has witnessed maximum number of

launches under the budget range of 60 Lacs - 1

crore, with approximately 40 percent out of total

supply of 60 Lacs - 1 crore budget properties,

followed by East and South Bengaluru, at 30 and 15

percent, respectively.

East Bengaluru has witnessed most of the launches in

the luxury segment properties. Out of the overall

supply of 1 crore – 2 crore ticket price properties,

nearly 87 percent have been launched in the eastern

quadrant of the city.

INDIA RESIDENTIAL REAL ESTATE I RESEARCH

S P L I T O F U N D E R - C O N S T R U C T I O N I N V E N T O R I E S – Z O N E W I S E

S P L I T O F U N S O L D I N V E N T O R I E S – Z O N E W I S E

East Bengaluru accounts for the major share of the

total number of under construction dwelling units, to

the tune of 35 percent, given the fact that the region

has been continuously witnessing launches of

residential projects from Category A developers in

the past years. The region is preferred by potential

home buyers due to the presence of commercial

hubs and its improved social and physical

infrastructure. Additionally, the region is easily

accessible from the city center and has excellent

property options for the all segments of home

buyers.

The Southern and Northern markets contributes 32

and 25 percent of the supply of under construction

dwelling units, while West Bengaluru is yet to catch

up on the residential market scene.

East Bengaluru accounts for the major share of the

total number of unsold inventory in the city, nearly

36 percent, followed by South and North Bengaluru

at 33 and 22 percent, respectively.

High property prices, delay in execution and

negative market sentiments were the major reasons

behind the doldrums and pilled up inventory.

However, the initiatives announced by the

government, to make real estate more transparent

and viable will bring back the consumer confidence

towards the real estate market and solve the

problem of huge unsold stocks.

INDIA RESIDENTIAL REAL ESTATE I RESEARCH

Area/Locality

Price Q4 2016

Rate Per Sqft

(INR)

% Change

(Q3 vs.

Q4)

1BHK Rental Range

(INR)

2 BHK Rental

Range (INR)

3 BHK Rental

Range (INR)

HSR Layout 3,650-5,732 -0.10 9,500-15,750 11,500-18,800 16,200-31,500

Bannerghatta 3,594-4,700 -0.08 7,500-12,500 11,800-19,000 14,500-32,000

Hebbal 3,788-6,124 -0.75 7,500-15,000 12,000-25,000 20,000-40,000

Indira Nagar 9,710-12,083 0.36 11,500-19,000 15,000-27,777 21,000-45,000

Jayanagar 7,504-10,338 1.65 10,000-17,500 13,500-26,700 16,300-40,000

Koramangala 7,370-9,350 0.56 11,500-13,700 12,000-26,000 15,000-39,000

Marathahalli 4,066-5,342 1.73 11,200-14,000 12,000-22,000 14,600-30,000

Sarjapur Road 3,530-5,800 -1.00 10,000-14,500 11,000-20,000 16,500-29,200

Whitefield 3,748-6,204 0.00 9,900-14,000 12,400-26,000 15,300-32,100

Yelahanka 3,824-5,657 5.70 7,500-11,500 11,500-20,200 12,500-31,500

Electronic City 3,176-5,034 -5.15 9,200-16,000 11,000-26,000 15,500-30,000

Jakkur 3,969-6,100 0.57 7,800-12,000 10,500-24,000 14,000-25,000

Banaswadi 3,825-6,077 5.61 7,200-13,000 10,500-15,000 15,000-25,000

Domlur 4,566-8,192 -3.18 9,500-16,000 14,000-20,000 14,500-22,000

Project Name LocalityDeveloper

Name

Possession

Date

No. of Units

(Approx.)

Lump sum

Price (INR)BHK Type

BHK Sizes

(Sqft)

Assetz 63 Degree

East

Sarjapur

RoadAssetz Homes Dec-19 1608

40.93Lac to

41.26 Lac1,2

685 Sqft - 1157

Sqft

Bren Champion

Square

Sarjapur

Road

Bren

CorporationApr-18 401

35.11 Lac to

57.24 Lac1,2,3

733 Sqft - 1644

Sqft

Sobha Gateway Of

DreamsPanathur Sobha Limited Jun-19 1800

34.41 Lac to

64.05 Lac1,2

650 Sqft - 1210

Sqft

Sipani Royal

Heritage

Chandapura

Anekal Road

Sipani

Properties

Private

Limited

Dec-18 128414.37 Lac to

27.87 Lac1,2,3

575 Sqft - 1115

Sqft

Godrej EternityKanakapura

Road

Godrej

Properties

Limited

Dec-18 180044.04 Lac to

79.78 Lac2,3

1049 Sqft - 1900

Sqft

Salarpuria Sattva

Park CubixDevanahalli

Salarpuria

Sattva GroupJun-21 1620

26.93 Lac to

60.88 Lac1,2,3

657 Sqft - 1485

Sqft

Bhagini RJM

EnclaveKengeri

Bhagini

DevelopersDec-20 1150

56.04 Lac to

1.22 Crore2,3

927 Sqft - 2450

Sqft

T O P L A U N C H E S O F 2 0 1 6 - B A S E D O N N E W L A U N C H S U P P L Y

P R I C E M O V E M E N T A N D R E N T A L P R I C E S O F K E Y M I C R O M A R K E T S

INDIA RESIDENTIAL REAL ESTATE I RESEARCH

T O P L A U N C H E S O F 2 0 1 6 - B A S E D O N N E W L A U N C H S U P P L Y

INDIA RESIDENTIAL REAL ESTATE I RESEARCH

REGULATORY UPDATES

Bengaluru Development Authority (BDA) has reduced the property tax by 50 per cent for vacant sites while hiking

the tax for buildings. The revised property tax for BDA Layouts and BDA-approved Layouts has been fixed as

1/2000th of the Guidance Value for sites of higher dimensions and 1/4000th of the Guidance Value for sites of small

dimensions

Department of rural development and Panchayat raj (RDPR) has passed an order that handwritten khatas are illegal

as touts and agents have been forging the property documents and using handwritten khatas to get legal sanctity for

their transactions

INFRASTRUCTURE UPDATES

Feasibility study for running high-speed trains in the southern corridor of Chennai-Bengaluru-Mysore has been taken

up by Germany. Discussions were made on various issues involving running high-speed train, raising speed on the

existing track to 200kmph and redevelopment of stations

The Bengaluru Metro Rail Corporation Ltd (BMRCL) has plans on linking the city with the Kempegowda International

Airport by extending the Phase II Metro line from Nagawara all the way to the airport

MAJOR DEALS

RMZ Corp has acquired Bengaluru’s Shangri-La hotel for over $100 million (Rs 700 crore) to build an additional 2.5

million sqft office space in the city's IT suburbs at Ecoworld business park on Outer Ring Road

Indiabulls has loaned Rs.800 crore to Embassy Group to help the southern property developer acquire the listed Mac

Charles, which owned the Le Meridien hotel

R E A LT Y N E W S

INDIA RESIDENTIAL REAL ESTATE I RESEARCH

INDIA RESIDENTIAL REAL ESTATE I RESEARCH

POPULATION

CITY

OVERVIEW

58332 km2 46.07 Million

AREA

ABOUT CITY

India's largest agglomeration and one of the world's largest

agglomerations

POPULATION GROWTH RATE

20.96 % 8.40 %

ECONOMIC GROWTH RATE

*As of year 2008

RESIDENTIAL MARKET GROWTH DRIVERS

Gurgaon- Cyber City, Golf Course Road, Sohna Road, UdyogVihar Ph- 1,2,3,4,5

Noida- Sector-18, Sector-63, Sector-62 Delhi- Connaught PLace, Bhikaji Cama PLace, Nehru PLace,

Netaji Subash PLace Ghaziabad- Sahibabad Industrial Area, kaushambi

INFRASTRUCTURE

Existing: NH-8, Rapid Metro, Delhi Metro

Upcoming: Delhi-Mumbai Industrial Corridor Project (DMIC), Faridabad-Noida-Ghaziabad Corridor (FNG)

RESIDENTIAL UNITS LAUNCHED

36,997 units

PREDOMINANT BUDGET RANGE

30 Lac - 60 Lac

*Constitutes 43% of total Supply

HIGHEST NUMBER OF LAUNCHES

Greater Noida(9,921 units)

% CHANGE IN PRICE 2015 vs 2016

% CHANGE IN NEW LAUNCH SUPPLY – 2015 vs 2016

61%

UNSOLD STOCK

2,26,981 units

CITY INVENTORY OVERHANG

UNDER CONSTRUCTION

UNITS

4,91,712 units

*As per Census 2011

Icons Source: Flaticon

70 Months

0.38%

INDIA RESIDENTIAL REAL ESTATE I RESEARCH

N E W L A U N C H S U P P L Y T R E N D - 2 0 1 5 V S 2 0 1 6

Predominantly an investor-driven market, NCR is

losing its shine in new launch supply, an approximate

61 percent decline in new launch supply was

recorded in 2016 compared to supply of 2015. This

is the lowest number of launches happened in NCR

from last 7 years, the reason, clearly identified as the

huge piled up unsold inventory in the region,

execution delays in a micro markets of Greater

Noida, Noida and Gurgaon along with high property

prices and litigation issues in the sectors of Dwarka

expressway.

Moreover, potential buyers and investors are also

holding their purchase decision and opting the wait

and watch approach, while developers are struggling

to deliver the project in the cash crunch market.

Third quarter of 2016 witnessed the lowest number of new launch supply in 2016, nearly 76 percent decline recorded in

new launch supply compared to same quarter previous year. On the contrary, Q4 2016 recorded an increase of 34

percent in new launch supply over Q3 2016, despite of demonetization and sluggish market condition.

Z O N E W I S E S P L I T O F R E S I D E N T I A L L A U N C H E S

0 2000 4000 6000 8000 10000 12000

Delhi

Dharuhera

Faridabad

Ghaziabad

Greater Noida

Gurgaon

Noida

No. of Units

Citie

s

Q1 2016 Q2 2016 Q3 2016 Q4 2016

Greater Noida is the major contributor in the

new launch supply in the National Capital

Region in the year 2016. The city has

witnessed launch of nearly 27 percent

dwelling units out of total supply i.e. 36,997

units, followed by Gurgaon, Ghaziabad and

Noida, at 25, 20 and 16 percent, respectively.

Meanwhile, Delhi, Faridabad and Dharuhera

witnessed limited supply in the year 2016.

Ghaziabad, the end user driven market of

NCR has recorded a supply of 35 percent in

Q4 2016, highest among all cities of NCR,

followed by Greater Noida and Noida, at 23

and 16 percent, respectively.

On the other hand, Gurgaon, the most active

market of NCR in the large scale residential

development has witnessed a plummeting

supply trend in Q4 2016 and has recorded a

whopping decline of nearly 61 percent in new

launch supply compared to the previous

quarter of the same year.

Moreover, Gurgaon residential market is

going through a tough time in this sluggish

market condition, where investors are taking

an exit mode, while end users are preferring

to buy ready to move in properties.

INDIA RESIDENTIAL REAL ESTATE I RESEARCH

T O P M I C R O M A R K E T S O F 2 0 1 6 - B A S E D O N N E W L A U N C H S U P P L Y

0 500 1000 1500 2000 2500 3000

Yamuna Expressway

Sector 76 - Noida

Sector 144 - Noida

L Zone

Knowledge Park-5

No. of Units

Mic

ro M

arke

ts

Yamuna Expressway in Greater Noida has witnessed

the launch of 2,421 dwelling units supply in 2016,

highest among all micro markets of NCR. The stretch is

witnessing the rapid real estate development and has

attracted several property developers and investors to

bring new setups in commercial, residential, industrial

and institutional sectors. Being developed by Yamuna

Expressway Industrial Development Authority the

locality holds strong growth potential due to the large-

scale residential development, fast connectivity and

upcoming world-class projects in the micro market.

With the launch of Amrapali Adarsh Awas Yojna a large

scale residential development project consisting 2,000

units, Sector 76 Noida holds the second position

among the top localities in 2016, based on the units

launched. The Micro market has been already house of

several big ticket size projects such as Supertech Cape

town and Prateek Wisteria.

L Zone located in the South West of Delhi is persistently witnessing the developer focus, the micro market has

witnessed the launch of nearly 20,000 dwelling units in last 4 years. Under the jurisdiction of Delhi Development

Authority, the micro market is considered as the largest zone of Delhi with 22,840 hectares.

B U D G E T W I S E S P L I T O F N E W L A U N C H E S

0 5000 10000 15000

Delhi

Dharuhera

Faridabad

Ghaziabad

Greater Noida

Gurgaon

Noida

No. of Units

Citie

s

0 - 30 Lacs 30 - 60 Lacs 60 Lacs - 1 Crore

1 Crore - 2 Crore Above 2 Crore

The residential market of NCR has witnessed

maximum launches in affordable and mid segment of

properties. Out of total new launch supply in 2016, an

approximate 43 percent unit launched under the

budget range of 30 - 60 Lacs, followed by below 30

Lacs and 60 Lacs - 1 crore budget properties, at 29

and 16 percent, respectively. Surprisingly, out of overall

supply in 2016, nearly 88 percent unit launched under

the ticket price of 1 crore, which clearly indicates that

developers in NCR are catering the demand of those

home buyers who are looking property under the

affordable and mid segment category.

Greater Noida is the hub of mid segment budget

properties, an approximate 42 percent unit launched

in the city under the budget range of 30 Lacs - 60

Lacs. Additionally, out of total new launch supply in

Greater Noida, nearly 89 percent dwelling units falls

under the budget of below 60 Lacs. The residential

market of Greater Noida is slowly gaining the

momentum backed by improved social and physical

infrastructure.

In line with the trend of other metro cities, Gurgaon

has witnessed the launch of 31 percent dwelling units

under the budget of 30 Lacs, followed by Ghaziabad

and Greater Noida.

INDIA RESIDENTIAL REAL ESTATE I RESEARCH

S P L I T O F U N D E R - C O N S T R U C T I O N I N V E N T O R I E S – Z O N E W I S E

S P L I T O F U N S O L D I N V E N T O R I E S – Z O N E W I S E

The major chunk of the under construction dwelling unit is lying in the micro-markets of Greater Noida, Gurgaon,

Ghaziabad and Noida. Out of the overall supply of under construction dwelling units, an approximate 83 percent falls

under the micro markets of these regions. Greater Noida accounts for 36 percent of under construction dwelling units,

highest among of all cities of NCR, followed by Gurgaon, Ghaziabad and Noida at 21,13 and 12 percent, respectively.

The execution delays in the major micro market of Greater Noida (Noida Extension) and Gurgaon (Dwarka Expressway)

due to litigation, were the major reasons behind this turmoil and increasing under construction units.

With nearly 2.26 Lac unsold inventory in the region, NCR is leading the pack. The residential market of NCR is at its all

time low with the decline in new launch supply trend and plummeting sales velocity. In order to liquidate the current flow

of unsold inventory, it will take almost 70 odd months.

In NCR, Greater Noida hold the highest sum of unsold inventory at 33 percent, followed by Gurgaon, Ghaziabad and

Noida at 19,18 and 13 percent, respectively. Yamuna Expressway and Noida Extension are the biggest contributors in

unsold supply in the Greater Noida City, an approximate 44 percent of unsold stock lies in these 2 micro markets, out of

total unsold stock in the city. The sum of unsold inventory in NCR region is directly related to the sum of under

construction supply in these cities, the highest the under construction supply, higher the unsold units, vice -versa.

INDIA RESIDENTIAL REAL ESTATE I RESEARCH

T O P L A U N C H E S O F 2 0 1 6 - B A S E D O N N E W L A U N C H S U P P L Y

P R I C E M O V E M E N T A N D R E N T A L P R I C E S O F K E Y M I C R O M A R K E T S

CityProject

NameLocality

Developer

Name

Possessio

n Date

No. of Units

(Approx.)

Lump sum

Price (INR)

BHK

Type

BHK Sizes

(Sqft)

DelhiJay Kay

GreensL Zone Jaykay Buildtech May-19 350

35.93 Lac to

1.08 Crore2,3,4

980 Sqft - 2950

Sqft

Ghaziabad

UPAVP

Gulmohar

Enclave

Tronica City UPAVP Dec-20 195111.40 Lac to

18.80 Lac1,2

366 Sqft - 603

Sqft

Greater NoidaLe Solitairian

Estate

Yamuna

Expressway

Le Solitairian

GroupMay-19 1900

22.44 Lac to

47.73 Lac1,2,3

670 Sqft - 1425

Sqft

Greater NoidaAarcity

Foreste

Knowledge

Park-5

Aarcity

Infrastructure

Pvt Ltd.

Dec-19 167722.75 Lac. to

61.59 Lac2,3,3.5

875 Sqft - 2360

Sqft

Noida

Amrapali

Adarsh Awas

Yojna

Sector 76 Amrapali Group Feb-21 200035.09 Lac to

71.34 Lac2,3,4

1070 Sqft -

2175 Sqft

NoidaShantiniketan

PrakritiSector 144

Shantiniketan

Buildcon Pvt.

Ltd

Sep-19 108848.30 Lac to

1.49 Crore2,3,4

1150 Sqft -

3550 Sqft

City Area/Locality

Price Q4 2016

Rate Per Sqft

(INR)

%

Change

(Q3 vs.

Q4)

1BHK Rental

Range (INR)

2 BHK Rental

Range (INR)

3 BHK Rental

Range (INR)

Faridabad Sector-86 2,906-4,421 1.48 3,500-8,000 8,500-11,000 9,000-16,500

Faridabad Sector-88 2,906-4,005 2.96 4,000-5,000 8,000-12,500 12,000-14,000

Faridabad Sector-82 3,445-4,439 2.47 3,500-4,000 9,800-16,000 10,500-21,500

Ghaziabad Raj Nagar Extension 2,401-3,079 -0.90 4,000-7,000 6,000-9,000 7,500-10,000

Ghaziabad Crossing Republik 2,925-3,344 -1.00 4,500-5,500 8,000-16,000 9,000-19,000

Ghaziabad Indirapuram 4,168-5,248 0.29 9,500-12,500 11,000-18,000 15,000-28,000

Ghaziabad Vasundhara 3,844-5,042 -0.24 9,000-12,500 11,000-18,000 9,000-21,000

Ghaziabad Vaishali 4,983-6,004 0.15 9,000-12,000 12,500-19,000 13,500-22,000

Greater Noida Noida Extension 2,803-4,103 4.70 3,000-6,000 5,000-10,000 8,000-12,000

Greater Noida Tech Zone IV 3,022-3,432 -1.06 5,500-9,000 8,000-10,000 10,000-14,000

Gurgaon Sector-54 11,255-14,437 -1.76 15,000-18,000 22,000-40,000 35,000-85,000

Gurgaon Sector-50 6,814-9,267 -1.09 12,000-15,000 23,000-32,000 30,000-40,000

Gurgaon Sector-25 9,064-14,240 -2.82 12,000-15,000 30,000-45,000 36,000-55,000

Gurgaon Sector-86 3,631-5,299 0.60 6,000-7,000 8,100-12,500 10,000-14,000

Gurgaon Sushant Lok I 7,445-10,513 -2.50 10,000-13,000 18,000-40,000 28,000-60,000

Gurgaon Golf Course Road 9,244-14,700 -2.38 15,000-18,000 22,000-40,000 35,000-85,000

Gurgaon Sohna Road 5,938-9,523 -1.31 7,000-15,000 18,000-28,000 25,000-48,000

Noida Sector-119 4,036-5,604 1.78 7,500-10,000 10,000-16,500 11,000-25,000

Noida Sector-129 3,895-5,409 0.48 7,500-15,000 11,000-16,000 13,200-18,000

Noida Sector-76 4,390-5,942 6.05 7,500-13,000 11,500-16,000 13,500-17,500

Noida Sector-50 5,526-8,662 -0.13 7,500-12,000 15,000-20,000 18,000-35,000

INDIA RESIDENTIAL REAL ESTATE I RESEARCH

M A P O F N C R

INDIA RESIDENTIAL REAL ESTATE I RESEARCH

REGULATORY UPDATES

Construction sites above 20,000 square metres will be fined Rs 5 Lac for causing dust pollution and flouting

environmental norms. Similarly, buildings of plot size 200 to 500 sq.m will pay Rs 30,000 while sites of 500 to 20,000

sq.m will pay Rs 50,000 as environmental compensation

CREDAI- NCR has started encouraging builders to adapt green building norms, especially norms pertaining to the

inclusion of the differently-abled. Upon adhering to the norms, the builders automatically get benefit of increased

floor area ratio (FAR)

INFRASTRUCTURE UPDATES

The 600m bridge which was proposed to link Noida’s Sector 150 with Faridabad’s Tilori village, will be completely

funded by the Noida Authority and the second proposed bridge between the FNG expressway from Noida’s Sector

168 with Faridabad in Haryana will be constructed by the NHAI

Delhi Development Authority (DDA) has formed a Special Purpose Vehicle for the maintenance and development of

green zones at par with international parks like London's Hyde Park, NewYork's Central park

MAJOR DEALS

Gurgaon-based real estate developer M3M India has raised Rs 1,250 crore from Indiabulls Housing Finance through a

structured debt transaction

Realty developer Lodha Group has raised single largest debt transaction of Rs 2,320 crore from Piramal Fund

Management, the realty investment arm of Piramal Enterprises, for a portfolio of projects in south and central Mumbai

includingThe World Towers

R E A LT Y N E W S

INDIA RESIDENTIAL REAL ESTATE I RESEARCH

INDIA RESIDENTIAL REAL ESTATE I RESEARCH

POPULATION

CITY

OVERVIEW

603 km2 12.47 Million

AREA

ABOUT CITY

A Metropolitan area in Maharashtra state, consisting of the state

capital Mumbai and its satellite towns.

POPULATION GROWTH RATE

3.87 % 8.50 %

ECONOMIC GROWTH RATE

*As of year 2008

RESIDENTIAL MARKET GROWTH DRIVERS

Central Mumbai: Dadar, Lower Parel, Parel, Prabhadevi, Wadala,Worli

Mumbai West: Andheri MIDC South Mumbai: Nariman Point, Bandra Kurla Complex Navi Mumbai: CBD Belapur, Taloja MIDC, Mindspace (Airoli) Thane: Waghle Industrial Estate, Ghodbunder Road

INFRASTRUCTURE

Existing: Bandra-Worli Sea Link (BWSL), Eastern Express Highway,Mumbai Eastern Freeway, Santacruz – Chembur Link Road (SCLR),Sahar Elevated Road, Western Express Highway, Monorail

Upcoming: Mumbai Trans Harbour Link, Navi Mumbai InternationalAirport, Mumbai Metro Phase-2)

RESIDENTIAL UNITS LAUNCHED

62,271 units

PREDOMINANT BUDGET RANGE

0 Lac - 30 Lac

*Constitutes 31% of total Supply

HIGHEST NUMBER OF LAUNCHES

Mumbai Beyond

Thane (24,882 units)

% CHANGE IN PRICE 2015 vs 2016

% CHANGE IN NEW LAUNCH SUPPLY – 2015 vs 2016

30%

UNSOLD STOCK

1,87,198 units

CITY INVENTORY OVERHANG

UNDER CONSTRUCTION

UNITS

3,62,776 units

*As per Census 2011

Icons Source: Flaticon

60 Months

20%

INDIA RESIDENTIAL REAL ESTATE I RESEARCH

Z O N E W I S E S P L I T O F R E S I D E N T I A L L A U N C H E S

N E W L A U N C H S U P P L Y T R E N D - 2 0 1 5 V S 2 0 1 6

The premium residential market of the country

witnessed a serious setback, with high unsold

inventory, skyrocketing prices, lower sales velocity

and shrinking new launch supply. The residential

market of MMR has recorded a decline of nearly 30

percent in new launch supply compared to the

preceding year 2015.

The demonetization drive has severely impacted

the residential market of MMR. Q4 2016 witnessed

a whopping decline of 73 percent in new launch

supply, compared to the previous year same period

and 53 percent decline over Q3-2016. The sales

velocity in the region has also been badly impacted

post demonetization, as the cash component in

most of the transaction remains high. Additionally,

investors have taken the back seat and opted the

wait and watch approach, while end users are

holding their purchase decision for price

correction in the coming time frame.

0 5000 10000 15000 20000 25000 30000

Mumbai Beyond Thane

Mumbai Western Suburbs

Mumbai Central Suburbs

Mumbai Harbour

Mumbai South

Mumbai Mira Road & Beyond

Mumbai Others

NaviMumbai

Thane

No. of Units

City

Zones

Q1 2016 Q2 2016 Q3 2016 Q4 2016

The Mumbai Beyond Thane zone emerged as the largest market, with 40 percent of all new launches in 2016, followed by

Thane and Navi Mumbai city, at 22 and 13 percent respectively. The premium residential zones of MMR, such as Mumbai

South, Mumbai Central Suburbs and Mumbai Harbour have recorded a limited new launch supply in 2016.

Mumbai Beyond Thane is most sought after zone of the region and holds strong growth potential. From 2013 onwards,

the zone has recorded a supply of around 1.03 Lac dwelling units and is coined as one of the most active zone in terms of

new launch supply. Because of its improved connectivity to the city center and affordability, most of the top category

developers have launched large scale residential projects in the vicinity. Moreover, limited availability of land bank within

the city center has shifted the developer interest to these peripheral locations of the city, making them most preferred

for large scale residential development. Localities such as Dombivli, Badlapur, Kalyan, Bhiwandi and Karjat are persistently

getting traction from the developers.

INDIA RESIDENTIAL REAL ESTATE I RESEARCH

B U D G E T W I S E S P L I T O F N E W L A U N C H E S

T O P M I C R O M A R K E T S O F 2 0 1 6 - B A S E D O N N E W L A U N C H S U P P L Y

0 1000 2000 3000 4000 5000

Dombivli East

Neral

Kharghar

BadlapurWest

Karjat

GhodbunderRoad

No. of units

Mic

ro M

arke

ts

Dombivli East, Neral, Badlapur West and Karjat

altogether have recorded a supply of 14,313 dwelling

units. All the mentioned micro markets falls under

Mumbai Beyond Thane zone and offer excellent

affordable property options. Dombivli has an added

advantage of close proximity to the satellite cities of

Mumbai, the micro market shares excellent

connectivity to the commercial hub of the Navi

Mumbai and Thane city. Moreover, the micro market is

already witnessing capital value appreciation and a rise

in rental demand.

Ghodbunder Road emerged as the favored destination

in the Thane city. The stretch provides excellent

connectivity and quick accessibility to Mira Road from

Thane, and to other micro markets such as Mulund,

Bhandup and Ghatkopar. The road is witnessing rapid

development, and has attracted several developers for

their portfolio expansion, along with several initiatives

by MMRDA to improve the connectivity. The micro

market is on the verge of becoming a realty hotspot in

the city.

0 5000 10000 15000 20000 25000 30000

Mumbai Beyond Thane

Mumbai Central Suburbs

Mumbai Harbour

Mumbai Mira Road & Beyond

Mumbai Others

Mumbai South

Mumbai Western Suburbs

Navi Mumbai

Thane

No. of Units

City

Zones

0 - 30 Lacs 30 - 60 Lacs 60 Lacs - 1 Crore 1 Crore - 2 Crore Above 2 Crore

Affordability is the new mantra in MMR for the developers to cater the residential demand of end users. Out of the total

supply in 2016, nearly 31 percent units were launched in below 30 Lacs ticket price properties, followed by 30 Lacs - 60

Lacs, 1 crore - 2 crore and 60 Lacs - 1 crore budget properties, at 26,17 and 15 percent, respectively. Interestingly, the

premium residential market of the country has witnessed 72 percent units launched under the ticket price of 1 crore. The

new launch supply trend clearly connotes that developers in MMR have started tapping the market sentiments and infusing

more supply in affordable and mid segment of properties. Mumbai beyond Thane zone is the biggest contributor in low

ticket price supply. Out of the total units launched under the ticket price of 30 Lacs, Mumbai Beyond Thane zone

contributes an approximate 84 percent units alone.

MMR has witnessed nearly 6,976 dwelling units launched under the premium categories, i.e. properties above the 2 crore

ticket price. Out of overall supply of 2 crore and above ticket price properties, nearly 38 percent units were launched in

Mumbai Western Suburbs followed by Mumbai Central (20 %), Mumbai Harbour (18%) and Mumbai South (18%). Mumbai

South, Mumbai Harbour and Mumbai Central, the relatively premium markets of the MMR, have witnessed a sharp decline

in new launches in 2016.

INDIA RESIDENTIAL REAL ESTATE I RESEARCH

S P L I T O F U N D E R - C O N S T R U C T I O N I N V E N T O R I E S – Z O N E W I S E

The Mumbai Beyond Thane zone, contributing 24 percent of over all supply of under construction unit in 2016, is the

largest residential market in the MMR in terms of the quantum of under-construction dwelling units. Relatively affordable

property prices and improved connectivity to commercial hubs in Mumbai make this zone an attractive choice for home

buyers.

The residential micro markets of Navi Mumbai and Thane holds the second and third position in terms of under

construction dwelling units, at 18 and 15 percent respectively. The micro markets in these cities relatively offers lower

prices besides good connectivity to the commercial hub of the Western Suburbs, Central Mumbai and South Mumbai.

The Western Suburb ranks fourth in terms of under construction dwelling units, at 14 percent. Andheri, Borivali,

Goregaon and Dahisar are the major micro markets in this zone and have witnessed decent supply of residential units in

past years.Altogether, the zone has around 49,205 units under construction supply at the different stages of construction.

Navi Mumbai has witnessed launch of around 7,799 dwelling units in 2016. An approximate 48 percent unit in the city

have been launched under the budget range of 1 crore - 2 crore which indicates that the city is slowly gaining the

moment in luxury segment supply. Kharghar has witnessed launch of nearly 3,621 dwelling units in this segment. Based on

the new launch supply, the second most happening segment in the city is the mid segment, nearly 30 percent unit

launched under the budget range of 30 Lacs - 60 Lacs, followed by properties below 30 Lac ticket price , which accounts

for 17 percent of total supply of 2016. Micro market such as Dronagiri, Khalapur, Panvel and Taloja have witnessed

launches under the budget of 60 Lacs ticket size properties.

Thane city, predominantly known as an industrial estate, has transformed itself in to an upscale residential destination.

IT/ITeS services in the region and improved rail-road connectivity have derived the realty sentiments in the city and

boosted the real estate activity. In 2016, the city has recorded launch of around 13,765 dwelling units. An approximate 34

percent new supply launch in the budget range of 30 Lacs - 60 Lacs, followed by 60 Lacs - 1 crore and 1 crore - 2 crore

ticket price properties, at 29 and 27 percent, respectively.

INDIA RESIDENTIAL REAL ESTATE I RESEARCH

S P L I T O F U N S O L D I N V E N T O R I E S – Z O N E W I S E

The Mumbai Metropolitan Region (MMR) has an approximate 1.87 Lac unsold inventory available in the primary market.

The MMR region has the second highest unsold inventory among all top cities, followed by the National Capital Region,

which will take an approximate 5 years to offload.

Unsold inventories, high property prices, low sales velocity and Lack of transparency in real estate sector has created this

doldrums, with the market reaching the stagnant position, and for developers it is getting hard to offload their current

pilled up stock. Moreover, the property developers are focusing on clearing existing unsold stock, instead of infusing new

supply in the market.

INDIA RESIDENTIAL REAL ESTATE I RESEARCH

T O P L A U N C H E S O F 2 0 1 6 - B A S E D O N N E W L A U N C H S U P P L Y

P R I C E M O V E M E N T A N D R E N T A L P R I C E S O F K E Y M I C R O M A R K E T S

CityProject

NameLocality

Developer

Name

Possession

Date

No. of Units

(Approx.)

Lump sum

Price (INR)BHK Type

BHK Sizes

(Sqft)

MumbaiLodha Palava

- Casa Bella

Dombivli

EastLodha Group Jan-19 2592

46.98 Lac to

89.64 Lac1,2,3

783 Sqft -

1494 Sqft

Mumbai KK Ashray NeralKK

DevelopersJan-19 1650

12.60 Lac to

24.64 Lac1,2

450 Sqft -

880 sqft

Mumbai Maple cityBadlapur

West

Abhishek

Shelters

Limited

Jan-19 350016.14 Lac to

22.73 Lac1

600 Sqft -

845 Sqft

MumbaiNK Neel

EmpireKarjat

NK

EnterprisesDec-19 2300

15.20 Lac to

34.80 Lac1,2

380 Sqft -

870 Sqft

Navi MumbaiSai World

EmpireKharghar

Paradise

GroupDec-18 1600

1 Crore to

2.52 Crore2,3,4

1240 Sqft -

3120 Sqft

ThaneGodrej

Emerald

Ghodbunder

Road

Godrej

Properties

Limited

Jun-19 140075 Lacs to

1.42 Crore1.5,2,3

500 Sqft -

950 Sqft

City Name Area/Locality

Price Q4 2016

Rate Per Sqft

(INR)

% Change

(Q3 vs.

Q4)

1BHK Rental

Range (INR)

2 BHK Rental

Range (INR)

3 BHK Rental

Range (INR)

Mumbai Badlapur East 2,984-3,010 1.03 2,000-6,000 4,000-8,000 6,000-15,000

Mumbai Andheri West 19,648-21,220 0.72 20,000-45,000 36,000-60,000 55,000-100,000

Mumbai Mira Road 5,938-8,859 4.92 9,250-15,000 10,000-25,500 13,000-30,000

Mumbai Borivali West 12,559-16,827 0.42 10,000-15,000 12,200-32,000 25,000-55,000

Mumbai Chembur 15,353-19,053 1.54 14,000-33,000 21,000-59,000 33,000-82,000

Mumbai Dombivli East 4,559-5,364 -5.34 8,200-12,000 12,000-30,000 25,000-95,000

Mumbai Powai 15,433-20,405 -2.07 25,000-35,000 36,000-50,000 52,000-100,000

Navi Mumbai Ulwe 5,059-5,605 -1.17 6,500-10,000 9,000-11,000 9,500-16,000

Navi Mumbai Panvel 4,977-6,327 3.42 8,500-13,000 9,500-20,500 11,000-22,000

Navi Mumbai Taloje 3,668-5,542 -3.03 4,000-6,000 7,500-10,000 8,000-12,000

Navi Mumbai Kharghar 6,488-10,056 2.74 9,500-13,000 11,800-28,000 13,000-37,000

Navi Mumbai Roadpali 5,616-7,546 1.98 6,500-8,500 8,500-14,000 11,000-25,000

Navi Mumbai Nerul 9,225-15,366 3.43 12,500-14,000 16,500-38,000 19,000-43,000

Navi Mumbai Airoli 8,187-12,820 3.00 11,000-16,000 17,000-32,000 20,000-38,000

Navi Mumbai Ulwe 5,059-7,105 2.56 8,000-10,000 8,500-11,000 9,000-14,000

Navi Mumbai Seawoods 8,554-13,361 0.08 11,500-16,000 21,000-44,000 26,000-50,000

Thane Ghodbunder Road 7,453-11,867 0.99 8,000-10,500 11,000-18,000 16,000-25,000

Thane Vartak Nagar 8,498-13,588 0.94 12,000-20,000 22,000-32,000 25,000-40,000

Thane Kasarvadavali 6,822-9,997 0.77 10,500-16,000 12,500-22,000 13,000-25,000

Thane Manpada 9,357-13,450 1.78 9,500-14,000 10,000-22,000 17,000-31,000

Thane Majiwada 9,808-13,887 1.38 14,000-18,000 15,000-24,000 21,000-38,000

INDIA RESIDENTIAL REAL ESTATE I RESEARCH

M A P O F M M R

INDIA RESIDENTIAL REAL ESTATE I RESEARCH

REGULATORY UPDATES

Brihanmumbai Municipal Corporation (BMC) proposed that builders must allocate 30% of every building's

recreational open spaces (ROS) on the ground in its natural state i.e. without pavements, to ensure rain water

percolation and maintenance of the ground water level

Maharashtra Urban Development Department (UDD) has directed Navi Mumbai Municipal Corporation (NMMC) to

ensure that 15% of the plot area meant for residences is kept for open recreational space for public use as per

Development Control Regulations of NMMC

INFRASTRUCTURE UPDATES

Construction of Metro line 2B (From DN Nagar to Mandala) and Metro line 4 (From Wadala to Kasarwadavli) have

been approved which would be operational (tentative) by 2021-22. Other Metro corridors that have been approved

for Mumbai include Dahisar to DN Nagar (Metro-2A), Colaba-Bandra-Seepz (Metro-3) and Dahisar-East to Andheri-

East (Metro-7)

Maharashtra government allowed the use of plastic waste, other than bLack plastic and PVC, in building asphalt roads,

thereby increasing their durability or longevity by three years

MAJOR DEALS

Ajay Piramal's Piramal Fund Management and Shapoorji Pallonji Real Estate Development will pump in about Rs 300

crore in a 1 million sq.ft residential projectTowers launched by Mumbai-based developer Ornate Spaces

Maharashtra government has signed a MoU with Korea Land & Housing Corporation (KLHC) of the Republic of

Korea to build a strategic partnership for smart cities, roads and bridges

R E A LT Y N E W S

INDIA RESIDENTIAL REAL ESTATE I RESEARCH

INDIA RESIDENTIAL REAL ESTATE I RESEARCH

POPULATION

CITY

OVERVIEW

479 km2 2.53 Million

AREA

ABOUT CITY

Third most populous city and fifth most populous urban

agglomeration in India

POPULATION GROWTH RATE

30.34% 7.40%

ECONOMIC GROWTH RATE

*As of year 2008

RESIDENTIAL MARKET GROWTH DRIVERS

Central Pune: Ashok Nagar, Prabhat Road, Shivaji Nagar,Deccan Gymkhana

East Pune: Hadapsar, Kharadi, Wagholi, Koregaon Park, KalyaniNagar

West Pune: Hinjewadi, Aundh, Wakad. North Pune: Talegaon MIDC, Charholi, Pimple Nilakh, Pimple

Saudagar South Pune: Vadgaon Budruk, Kondhwa, Bibvewadi.

INFRASTRUCTURE

Existing: University Flyovers -Pune, Pune Ring Road, Pune – Mumbaihighway (NH-4), Nashik Highway

Upcoming: Outer Ring Road (ORR), Bus Rapid Transit System (BRTS),PCMC Infrastructure

RESIDENTIAL UNITS LAUNCHED

40,420 units

PREDOMINANT BUDGET RANGE

30 Lac - 60 Lac

*Constitutes 49% of total Supply

HIGHEST NUMBER OF LAUNCHES

North Pune(15,247 units)

% CHANGE IN PRICE 2015 vs 2016

% CHANGE IN NEW LAUNCH SUPPLY – 2015 vs 2016

32%

UNSOLD STOCK

97,637 units

CITY INVENTORY OVERHANG

UNDER CONSTRUCTION

UNITS

1,83,540 units

*As per Census 2011

Icons Source: Flaticon

35 Months

2%

INDIA RESIDENTIAL REAL ESTATE I RESEARCH

Z O N E W I S E S P L I T O F R E S I D E N T I A L L A U N C H E S

N E W L A U N C H S U P P L Y T R E N D - 2 0 1 5 V S 2 0 1 6

The year 2016 has seen a downfall in the supply of new

residential launches in Pune by 32 percent when

compared to the previous year. Unlike the residential

supply in the preceding year, the third quarter of 2016 has

seen the highest number of new launches.

On QoQ basis, there has been a drop in the launches

observed in the Q1 (49 percent) and Q2 (33 percent) due

to the increased unsold inventory pressure on the

builders. While Q3 2016 witnessed positive launches

(16%) compared to the previous year attributing to the

developers making a comeback with revival in market

momentum, but the launches in forth quarter of 2016

again slumped by 42 percent.

North Pune has witnessed the highest number of

residential launches (38 percent) in 2016 while the eastern

part of Pune contributed the least number of launches(14

percent). West and South Pune stand in the mid-way with

27 percent and 21 percent of new residential unit launches.

Interestingly, North Pune is the only zone in the city which

has recorded an upsurge in residential properties during

the last quarter of the year in spite of the demonetization

effect. Micro markets such as Chikhali, Ravet and Dhanori

are in high demand among the home buyers.

Chikhali in the North zone stands ahead of the other

localities in Pune in terms of new launch supply. This

micro market turned into a premier residential area with

the advent of the IT/ITeS establishments and multi-

national companies in the proximity, well- laid

infrastructure with excellent connectivity. In addition to

the above, the reason behind high unit launches is that the

micro market is witnessing huge price appreciation in the

recent past.

Undri, Hinjewadi, Wagholi and Wakad are the other top

performing micro-markets in terms of new launch supply

due to the availability of affordable housing units, good

connectivity and employment generating centres.

0 5000 10000 15000 20000

NorthPune

WestPune

SouthPune

EastPune

No of Units

City

Zones

Q1 2016 Q2 2016 Q3 2016 Q4 2016

0 1000 2000 3000 4000

Chikhali

Undri

Hinjewadi

Wagholi

Wakad

No. of Units

Mic

ro M

arke

ts

T O P M I C R O M A R K E T S O F 2 0 1 6 - B A S E D O N N E W L A U N C H S U P P L Y

INDIA RESIDENTIAL REAL ESTATE I RESEARCH

B U D G E T W I S E S P L I T O F N E W L A U N C H E S

All the zones of Pune except Central Pune have good

number of under-construction housing units, because of

high demand for enormous number of housing units by

the students and private sector employees working in

these regions.

The central part of Pune has vey limited land availability

which restricted major residential development.

As expected, North Pune has the maximum unsold

inventory (34 percent) while West and South Pune each

contribute approx. 24% of unsold inventory in 2016.

Central Pune and East Pune have recorded minimal

unsold stock compared to other zones of the city due

to the reduced number of unit launches during the year.

0 5000 10000 15000 20000

East Pune

North Pune

South Pune

West Pune

No. of Units

City

Zones

0 - 30 Lacs 30 - 60 Lacs 60 Lacs - 1 Crore1 Crore - 2 Crore Above 2 Crore

An approximate 49 percent dwelling unit launched

under the budget range of 30 Lacs – 60 Lacs in the

residential market of Pune city, North Pune recorded

nearly 35 percent of dwelling supply under this

budget, followed by South and West Pune, at 26 and

23 percent, respectively.

The price brackets 0-30 Lacs and 30-60 Lacs are the

most preferred ones among the Punekars because of

IT/ITeS employees are in search of affordable housing

units which offer decent amenities rather than luxury

and ultra-luxury properties.

S P L I T O F U N D E R - C O N S T R U C T I O N I N V E N T O R I E S – Z O N E W I S E

S P L I T O F U N S O L D I N V E N T O R I E S – Z O N E W I S E

INDIA RESIDENTIAL REAL ESTATE I RESEARCH

T O P L A U N C H E S O F 2 0 1 6 - B A S E D O N N E W L A U N C H S U P P L Y

P R I C E M O V E M E N T A N D R E N T A L P R I C E S O F K E Y M I C R O M A R K E T S

Project Name Locality Developer NamePossession

Date

No. of Units

(Approx)

Lumpsum

Price (INR)BHK Type

BHK Sizes

(Sqft)

Aishwaryam Hamara Chikhali Essen Group Apr-19 200012.28 Lac to

28 Lacs1,2

351 Sqft -

800 Sqft

Kolte Patil R1 Life

RepublicHinjewadi

Kolte Patil

Developers LtdDec-19 1000

52 Lacs to 77

Lacs2,3

1030 Sqft -

1545 Sqft

Pristine Prolife Phase III Wakad Pristine Builders Dec-18 28261.88 Lac to

69.80 Lac2

935 Sqft -

1069 Sqft

Dynamic Grandeur UndriDynamic Realty

VenturesMay-19 1200

32 Lacs to

69.29 Lac1,2,3

697 Sqft -

1550 Sqft

Gagan Adira WagholiGagan

ConstructionDec-19 345

48.67 Lac to

91.69 Lac2,3

930 Sqft -

2090 Sqft

Area/LocalityPrice Q4 2016

Rate Per Sqft (INR)

% Change

(Q3 vs. Q4)

1BHK Rental Range

(INR)

2 BHK Rental Range

(INR)

3 BHK Rental Range

(INR)

Wagholi 3,520-4,121 0.28 8,500-14,500 11,000-20,000 12,500-21,000

Wakad 5,123-5,574 0.17 7,500-14,000 12,000-22,000 15,000-32,000

Baner 5,667-7,092 1.33 10,500-15,500 12,700-25,000 14,999-30,000

Kharadi 4,732-5,720 -0.69 8,000-13,800 11,250-21,000 17,000-31,800

Undri 3,797-4,025 0.41 7,800-10,000 10,000-14,000 14,000-22,000

Hadapsar 4,544-5,932 3.45 10,000-15,000 16,000-25,000 15,000-30,000

Talegaon 3,127-4,651 0.49 4,000-8,000 6,500-10,000 9,000-12,000

Moshi 3,506-4,839 1.46 6,000-8,500 8,000-13,000 11,000-18,000

Hinjewadi 4,786-5,321 1.95 10,500-15,000 16,000-25,000 22,500-35,000

Kondhwa 4,162-5,371 -3.43 10,000-12,000 15,000-22,000 20,000-25,000

Chakan 2,843-4,093 2.41 8,000-11,000 9,000-12,000 12,000-15,000

Ravet 4,614-6,612 2.96 9,500-11,000 12,000-16,000 15,000-19,000

Dhanori 4,099-6,312 3.39 9,500-12,000 11,000-16,000 15,000-20,000

Lohegaon 3,937-5,489 3.49 8,000-10,000 11,500-15,000 15,000-18,000

INDIA RESIDENTIAL REAL ESTATE I RESEARCH

M A P O F P U N E

INDIA RESIDENTIAL REAL ESTATE I RESEARCH

REGULATORY UPDATES

Rain water harvesting has been made compulsory in Pimpri Chinchwad for all new residential and commercial

buildings with an area of 20,000 sq. m. and a rebate is given in property tax to housing societies where rain water

harvesting is being implemented

Builders of Pune who do not replant the trees they cut during their previous projects will find it hard to get projects

cleared in the future by Pune Municipal Corporation (PMC)

INFRASTRUCTURE UPDATES

A new Greenfield international airport is proposed to come up at Purandar Taluk, which will be spread over 2400

hectares, and the new airport would be named as Chhatrapati Sambhaji Raje International Airport

Pune railway station and adjoining areas are being re-developed by enhancing the passenger amenities, enabling

optimal utilization of land at railway stations and improving of integrated public transport hub as a part of smart city

development program

MAJOR DEALS

Global private equity major KKR's non-banking financial company (NBFC) invested Rs 300 crore in two residential

projects (Abitante and Aldea Espanola) of realty developer Puranik Builders

Realty developer Kumar Urban has raised Rs 300 crore to refinance existing lenders and project construction from

Altico Capital for its township KUL Ecoloch near Hinjewadi

R E A LT Y N E W S

INDIA RESIDENTIAL REAL ESTATE I RESEARCH

INDIA RESIDENTIAL REAL ESTATE I RESEARCH

POPULATION

CITY

OVERVIEW

426 km2 4.34 Million

AREA

ABOUT CITY

Located on the Coromandel Coast off the Bay of Bengal, Chennai is

capital of Tamil Nadu

POPULATION GROWTH RATE

7.7 % 6.20 %

ECONOMIC GROWTH RATE

*As of year 2008

RESIDENTIAL MARKET GROWTH DRIVERS

Central Chennai: Nungambakkam, Anna Salai, Alwarpet ,T.Nagar

West Chennai: Anna Nagar, Ambattur, Sriperumbudur (IndustrialArea), Oragadam (Industrial Area)

North Chennai: Perambur South Chennai: Old Mahabalipuram Road (OMR), Guindy,

Nandambakkam, Perungudi, Thuraipakkam, Sholinganallur,Siruseri, Maraimalai Nagar

INFRASTRUCTURE

Existing: Old Mahabalipuram Road, East Coast Road, Outer RingRoad

Upcoming: Ponneri Smart City, Greenfield Airport, ChennaiBengaluru Industrial Corridor (CBIC)

RESIDENTIAL UNITS LAUNCHED

15,691 units

PREDOMINANT BUDGET RANGE

30 Lac - 60 Lac

*Constitutes 50% of total Supply

HIGHEST NUMBER OF LAUNCHES

South Chennai(9,074 units)

% CHANGE IN PRICE 2015 vs 2016

% CHANGE IN NEW LAUNCH SUPPLY – 2015 vs 2016

36.87 %

UNSOLD STOCK

32,038 units

CITY INVENTORY OVERHANG

UNDER CONSTRUCTION

UNITS

52,145 units

*As per Census 2011

Icons Source: Flaticon

42 Months

6.37 %

INDIA RESIDENTIAL REAL ESTATE I RESEARCH

Chennai has seen a high slump in the supply of new

residential units in the year 2016. Chennai city witnessed

a dip of 38 percent in the new launch supply when

compared to the previous year 2015.

New launches have come down at faster rates as the

market sentiments fell till the third quarter of the year

due to various aspects such as impact of 2015 floods and

RERA.

Residential realty in Q4 2015 has faced tough times due

to the impact of floods and the same quarter in 2016 has

seen a comeback with 57 percent more new residential

dwelling unit launches.

South Chennai is ahead of the other zones of Chennai

in terms of new launch supply in 2016 with 9074 new

unit launches i.e. 58 percent of overall new units supply

in the city.

South Chennai alone contributed more than half to the

new unit launch figure in the first quarter (Q1) and the

fourth quarter (Q4) contributing to whopping 63

percent and 35 percent of the new units. The IT

establishments along the OMR Road and GST Road,

improved physical and social infrastructure along with

the presence of major transportation corridors made

South Chennai the most favoured residential

destination.

The Western zone of Chennai recorded considerable

number (5,277 units i.e. 34 percent) of new residential

launches in 2016 with the advent of numerous global

manufacturing companies and presence of industrial

belts.

While North Chennai has recorded 7 percent of new

launches, Central Chennai, expectedly, recorded mere 1

percent of new dwelling units launch in spite of the huge

demand for residential properties in the region. This is

because the price per square feet is very high and the

shortage of developable land prevents sizeable

development activity

0 2000 4000 6000 8000 10000

Central Chennai

North Chennai

South Chennai

West Chennai

No. of Units

City

Zones

Q1 2016 Q2 2016 Q3 2016 Q4 2016

Z O N E W I S E S P L I T O F R E S I D E N T I A L L A U N C H E S

N E W L A U N C H S U P P L Y T R E N D - 2 0 1 5 V S 2 0 1 6

INDIA RESIDENTIAL REAL ESTATE I RESEARCH

Situated in the heart of the city and located in the

western Chennai, Vadapani has recorded the maximum

unit launch figure of 1,044 units. This is due to the

booming IT development and improved infrastructure

along with availability of huge land bank in this region.

Maramalai Nagar, one of the IT and educational hubs of

Chennai has grabbed a lot of attention with 908 units

launched in 2016, one main reason being its strategic

location on the Grand Southern Trunk (GST) Road. In

addition to these, there are numerous manufacturing and

industrial units which are driving the residential demand

in and around this micro-market.

Ponneri smart city, proposed 400-ft Outer Ring Road and

the upcoming Chennai-Bengaluru Industrial Corridor

(CBIC) are few important aspects which are responsible

for the increasing housing demand in Ponneri.

Vanagaram and Mahindra World City evolved as the top

micro-markets due to existence of industrial parks and

proximity to commercial hubs.0 200 400 600 800 1000 1200

Vadapalani

Maraimalai Nagar

Ponneri

Vanagaram

Mahindra World City

No. of Units

Mic

ro M

arke

ts

0 1000 2000 3000 4000 5000 6000 7000 8000 9000 10000

Central Chennai

North Chennai

South Chennai

West Chennai

No. of Units

City

Zones

0 - 30 Lacs 30 - 60 Lacs 60 Lacs - 1 Crore 1 Crore - 2 Crore Above 2 Crore

B U D G E T W I S E S P L I T O F N E W L A U N C H E S

Chennai's residential market has witnessed half of the new launches in the mid segment, specifically in the price bracket of