Research Report - APTARE

59

Research Report 2012 Storage Market Survey By Bill Lundell, Senior Research Analyst and Mark Peters, Senior Analyst With Jennifer Gahm November 2012 © 2012, The Enterprise Strategy Group, Inc. All Rights Reserved.

Transcript of Research Report - APTARE

Research Report

2012 Storage Market Survey

By Bill Lundell, Senior Research Analyst and Mark Peters, Senior Analyst

With Jennifer Gahm

November 2012

© 2012, The Enterprise Strategy Group, Inc. All Rights Reserved.

Research Report: 2012 Storage Market Survey 2

© 2012 by The Enterprise Strategy Group, Inc. All Rights Reserved.

Contents

List of Figures ................................................................................................................................................ 3

List of Tables ................................................................................................................................................. 4

Executive Summary ...................................................................................................................................... 5 Report Conclusions ................................................................................................................................................. 5

Introduction .................................................................................................................................................. 8 Research Objectives ............................................................................................................................................... 8

Research Findings ......................................................................................................................................... 9 General Storage Environments ............................................................................................................................... 9 Storage Spending Trends ...................................................................................................................................... 21 Storage Challenges ............................................................................................................................................... 27 The Impact of Virtualization Technology and Cloud Services on Storage Infrastructure ...................................... 31 Storage Media ...................................................................................................................................................... 36 Storage Requirements and Buying Criteria........................................................................................................... 43

Conclusion ................................................................................................................................................... 47 Research Implications for Technology Vendors.................................................................................................... 49 Research Implications for IT Professionals ........................................................................................................... 49

Research Methodology ............................................................................................................................... 50

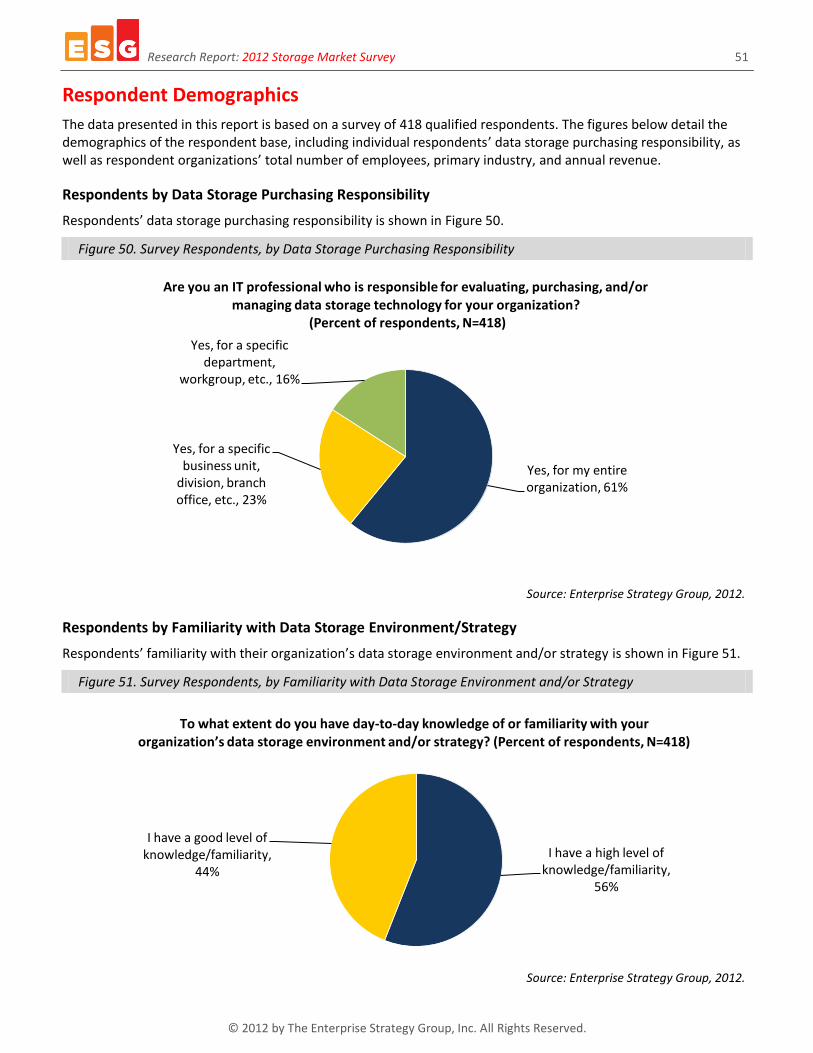

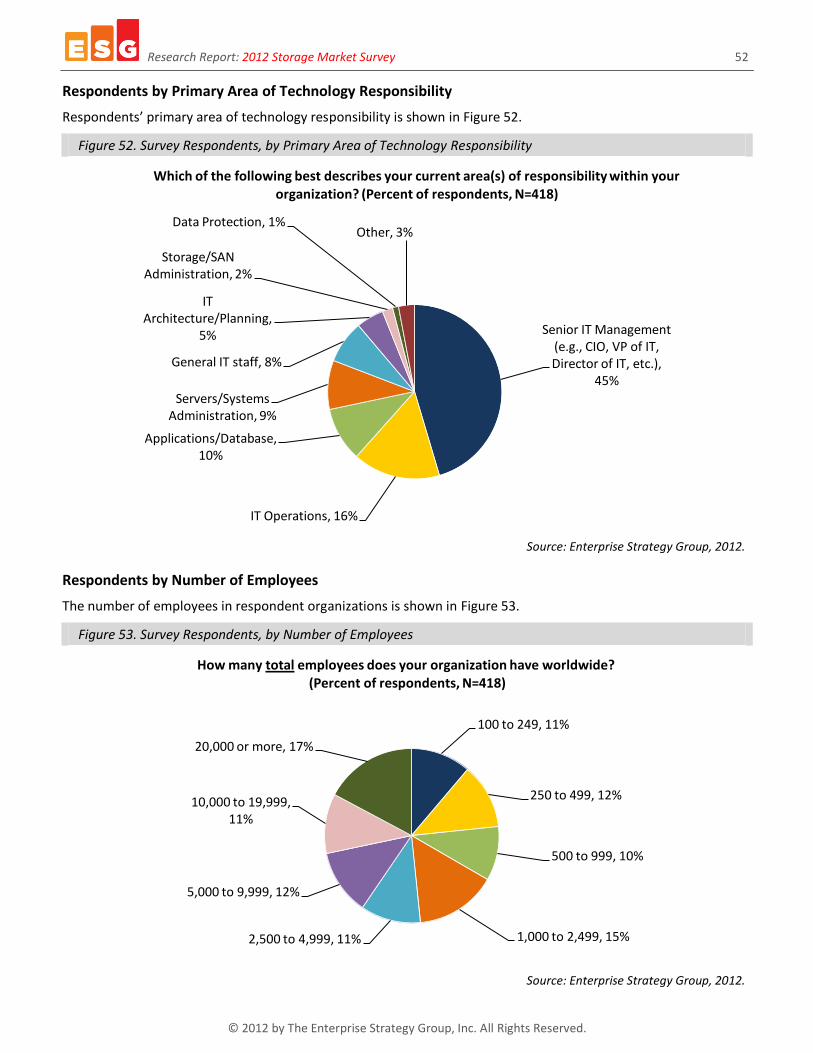

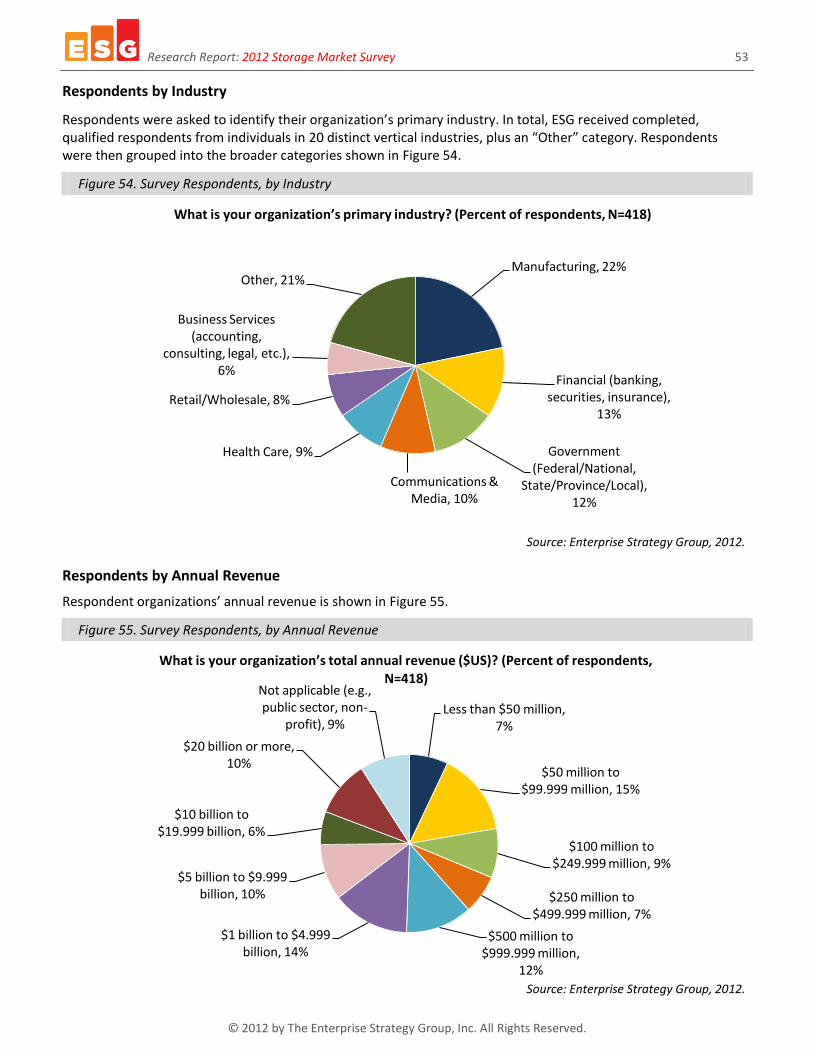

Respondent Demographics......................................................................................................................... 51

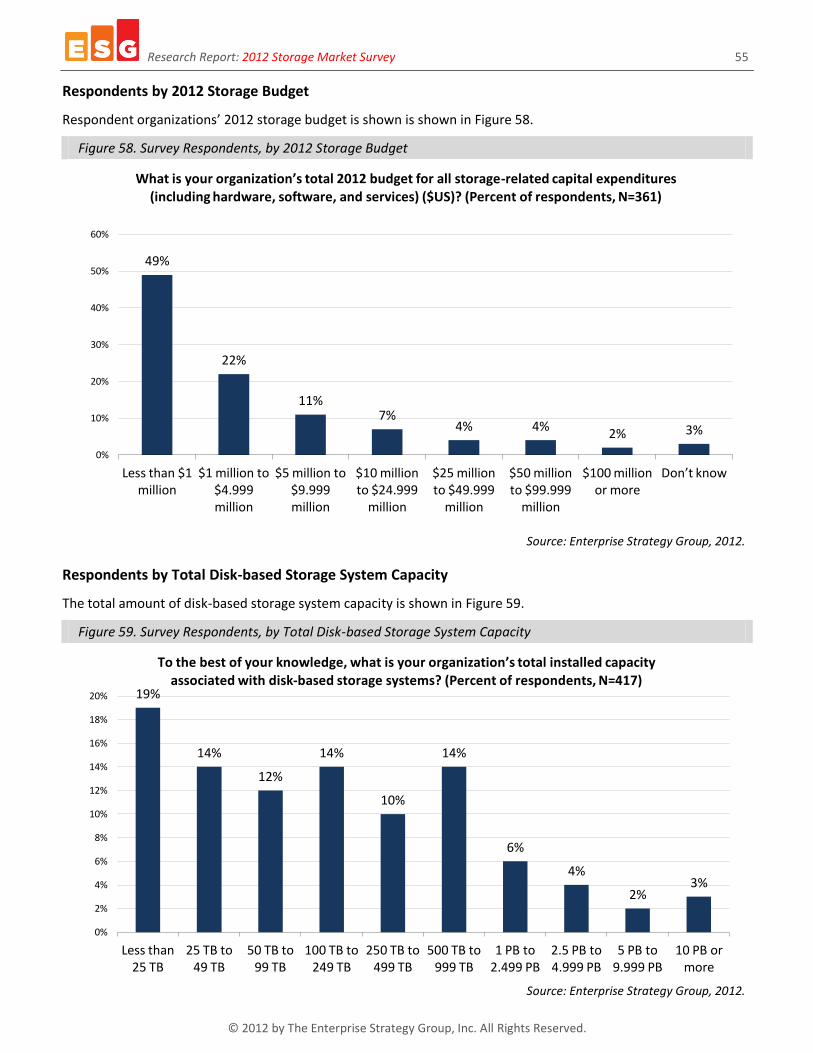

Respondents by Data Storage Purchasing Responsibility ..................................................................................... 51 Respondents by Familiarity with Data Storage Environment/Strategy ................................................................ 51 Respondents by Primary Area of Technology Responsibility ................................................................................ 52 Respondents by Number of Employees................................................................................................................ 52 Respondents by Industry ...................................................................................................................................... 53 Respondents by Annual Revenue ......................................................................................................................... 53 Respondents by 2012 IT Budget ........................................................................................................................... 54 Respondents by Number of Production Servers................................................................................................... 54 Respondents by 2012 Storage Budget .................................................................................................................. 55 Respondents by Total Disk-based Storage System Capacity ................................................................................. 55 Respondents by Server Virtualization Usage ........................................................................................................ 56 Respondents by Percentage of x86 Servers Virtualized ........................................................................................ 56 Respondents by Total Number of Virtual Machines ............................................................................................. 57 Respondents by Total Storage Capacity Used to Support Virtual Server Environments ....................................... 57 Respondents by Role of Data Storage Technology in IT and Business Operations ............................................... 58 Respondents by Importance of Data .................................................................................................................... 58

Research Report: 2012 Storage Market Survey 3

© 2012 by The Enterprise Strategy Group, Inc. All Rights Reserved.

List of Figures Figure 1. Total Disk-based Storage System Capacity, by Company Size .................................................................... 9 Figure 2. Total Installed Disk-Based Storage System Capacity, by Total Number of Production Servers ................ 10 Figure 3. Percent of Organizations with Disk-based Storage System Capacity of 500 TB or More, 2010 vs. 2012 .. 10 Figure 4. Annual Data Storage Capacity Growth Rate ............................................................................................. 11 Figure 5. Annual Data Storage Capacity Growth Rates, by Total Disk-based Storage System Capacity .................. 11 Figure 6. Applications Responsible for Storage Growth .......................................................................................... 12 Figure 7. Most Common Reason for Adding New Storage Systems ........................................................................ 13 Figure 8. All Disk-based Storage Technologies in Use ............................................................................................. 14 Figure 9. All Disk-based Storage Technologies in Use, by Company Size ................................................................ 15 Figure 10. Primary Disk-based Storage Technology in Use, by Company Size ......................................................... 15 Figure 11. All Disk-based Storage Technologies in Use, by Total Disk-based Storage System Capacity .................. 16 Figure 12. Primary Disk-based Storage Technology in Use, by Total Disk-based Storage System Capacity............. 16 Figure 13. Primary Disk-based Storage Technology in Use, by Total Disk-based Storage System Capacity............. 17 Figure 14. Number of Storage Administrators, by Company Size ........................................................................... 18 Figure 15. Number of Storage Administrators, by Total Disk-based Storage System Capacity ............................... 19 Figure 16. Number of Storage Administrators, by Role of Data Storage Technology in IT and Business Operations

................................................................................................................................................................... 19 Figure 17. Ability to Support Storage with Current Staff ......................................................................................... 20 Figure 18. 2012 Storage Budget Levels, by Company Size ...................................................................................... 21 Figure 19. 2012 Storage Budget Levels, by Total Installed Disk-Based Storage System Capacity ............................ 22 Figure 20. 2012 Storage Budget Levels, by Role of Data Storage Technology in IT and Business Operations ......... 22 Figure 21. Expected 2013 Storage Budget Levels .................................................................................................... 23 Figure 22. Expected 2013 Storage Budget Levels, by Company Size ....................................................................... 24 Figure 23. Expected 2013 Storage Budget Levels, by Role of Data Storage Technology in IT and Business

Operations ................................................................................................................................................. 24 Figure 24. IT Initiatives Expected to Significantly Impact Storage Spending over the Next 12-18 Months ............. 25 Figure 25. IT Initiatives Expected to Significantly Impact Storage Spending over the Next 12-18 Months, by

Company Size ............................................................................................................................................. 26 Figure 26. The Progression of Managing Data Storage Technology ........................................................................ 27 Figure 27. Storage Challenges ................................................................................................................................. 28 Figure 28. Satisfaction Level with Storage Hardware Utilization Rate .................................................................... 29 Figure 29. The Impact of Desktop Virtualization on Storage Infrastructure ............................................................ 30 Figure 30. Total Storage Capacity Currently Used to Support Virtual Server Environment ..................................... 31 Figure 31. Total Storage Capacity Currently Used to Support Virtual Server Environment, by Company Size ........ 32 Figure 32. Total Storage Capacity Currently Used to Support Virtual Server Environments, by Total Number of

Virtual Machines ........................................................................................................................................ 32 Figure 33. Storage Challenges Stemming from Server Virtualization Usage ........................................................... 33 Figure 34. Storage Challenges Stemming from Server Virtualization Usage, by Total Storage Capacity Currently

Used to Support Virtual Server Environment ............................................................................................. 34 Figure 35. Expected Impact of Public Cloud Computing Services to Onsite Storage Infrastructure and Processes 35 Figure 36. Solid-state Storage Usage Trends ........................................................................................................... 36 Figure 37. Significant Increase in Solid-state Storage Usage among Enterprise Organizations since 2008 ............. 37 Figure 38. Solid-state Storage Implementation Types among Current Users .......................................................... 38 Figure 39. All Solid-state Storage Implementation Types among Current Users, by Company Size ........................ 39 Figure 40. Solid-state Storage Implementation Types among Potential Adopters .................................................. 39 Figure 41. Allocation of Disk-based Storage Capacity across Disk Drive Types, Now vs. 24 Months from Now ...... 40 Figure 42. Overall Solid-state Storage Footprint Now and 24 Months from Now, by 2012 Storage Budget ........... 40 Figure 43. Tape Usage Trends and Future Plans ..................................................................................................... 41 Figure 44. How Organizations Currently Use Tape .................................................................................................. 42 Figure 45. Must-have Storage Features and Capabilities ........................................................................................ 43

Research Report: 2012 Storage Market Survey 4

© 2012 by The Enterprise Strategy Group, Inc. All Rights Reserved.

Figure 46. Important Criteria When Selecting Storage Vendors/Solutions ............................................................. 44 Figure 47. Most Important TCO Cost Considerations .............................................................................................. 45 Figure 48. Long-term View of Data Storage Technology ......................................................................................... 48 Figure 49. Long-term View of Data Storage Technology, by Role of Data Storage Technology in IT and Business

Operations ................................................................................................................................................. 48 Figure 50. Survey Respondents, by Data Storage Purchasing Responsibility .......................................................... 51 Figure 51. Survey Respondents, by Familiarity with Data Storage Environment and/or Strategy........................... 51 Figure 52. Survey Respondents, by Primary Area of Technology Responsibility ..................................................... 52 Figure 53. Survey Respondents, by Number of Employees ..................................................................................... 52 Figure 54. Survey Respondents, by Industry ........................................................................................................... 53 Figure 55. Survey Respondents, by Annual Revenue .............................................................................................. 53 Figure 56. Survey Respondents, by 2012 IT Budget ................................................................................................ 54 Figure 57. Survey Respondents, by Number of Production Servers ........................................................................ 54 Figure 58. Survey Respondents, by 2012 Storage Budget ....................................................................................... 55 Figure 59. Survey Respondents, by Total Disk-based Storage System Capacity ...................................................... 55 Figure 60. Survey Respondents, by Usage of Server Virtualization Technology ...................................................... 56 Figure 61. Survey Respondents, by Percentage of x86 Servers Virtualized ............................................................. 56 Figure 62. Survey Respondents, by Total Number of Virtual Machines .................................................................. 57 Figure 63. Survey Respondents, by Total Storage Capacity Used to Support Virtual Server Environments ............ 57 Figure 64. Survey Respondents, by Role of Data Storage Technology in Business and IT Operations..................... 58 Figure 65. Survey Respondents, by Importance of Data ......................................................................................... 58

List of Tables Table 1. Applications Responsible for Storage Growth, by Company Size .............................................................. 13 Table 2. Primary Disk-based Storage Technology in Use, by Role of Data Storage Technology in IT and Business

Operations ................................................................................................................................................. 17 Table 3. Overall Storage Hardware Utilization Rates Are Higher among Organizations Citing Networked Storage as

Their Primary Disk-based Storage Technology ........................................................................................... 18 Table 4. Storage Challenges, by Company Size ....................................................................................................... 29 Table 5. Overall Storage Hardware Utilization Rates Are Lower among Organizations Citing Poor Storage

Hardware Utilization as a Challenge .......................................................................................................... 30 Table 6. Expected Impact of Public Cloud Computing Services to Onsite Storage Infrastructure and Processes, by

Total Disk-based Storage System Capacity ................................................................................................. 35 Table 7. Current Usage of Solid-state Storage, by Role of Data Storage Technology in IT and Business Operations

................................................................................................................................................................... 36 Table 8. Tape Usage Trends and Future Plans, by Company Size ............................................................................ 41 Table 9. How Organizations Currently Use Tape, by Total Disk-based Storage System Capacity ............................ 42 Table 10. Must-have Storage Features and Capabilities, by Total Disk-based Storage System Capacity ................ 44 Table 11. Important Criteria When Selecting Storage Vendors/Solutions, by Company Size.................................. 45 Table 12. Most Important Message Storage Vendors Can Deliver .......................................................................... 46 Table 13. Most Important Message Storage Vendors Can Deliver, by Role of Data Storage Technology in IT and

Business Operations ................................................................................................................................... 46

All trademark names are property of their respective companies. Information contained in this publication has been obtained by sources The Enterprise Strategy Group (ESG) considers to be reliable but is not warranted by ESG. This publication may contain opinions of ESG, which are subject to change from time to time. This publication is copyrighted by The Enterprise Strategy Group, Inc. Any reproduction or redistribution of this publication, in whole or in part, whether in hard-copy format, electronically, or otherwise to persons not authorized to receive it, without the express consent of The Enterprise Strategy Group, Inc., is in violation of U.S. copyright law and will be subject to an action for civil damages and, if applicable, criminal prosecution. Should you have any questions, please contact ESG Client Relations at 508.482.0188.

Research Report: 2012 Storage Market Survey 5

© 2012 by The Enterprise Strategy Group, Inc. All Rights Reserved.

Executive Summary

Report Conclusions

ESG conducted an in-depth survey of 418 IT and data storage professionals concerning their organizations’ current data storage environments including current storage resources, challenges, purchase criteria, as well as forward-looking data storage plans. Survey participants represented midmarket (100 to 999 employees) and enterprise-class (1,000 employees or more) organizations in North America (United States and Canada).

Based on the data collected from this survey, ESG concludes:

Total installed disk-based storage system capacity continues to grow. More than one-quarter of organizations have at least 500 TB of disk-based storage system capacity deployed. From a company size perspective, nearly two-thirds (63%) of midmarket organizations (i.e., 100 to 999 employees) manage less than 50 TB of total disk-based storage system capacity; conversely, more than one in five enterprises (i.e., 1,000 or more employees) have 1 PB or more deployed, while 8% of these larger organizations reported having at least 5 PB of total disk-based storage system capacity. The majority of respondents cited overall annual storage capacity growth rates in the 1%-20% range, with more than one-quarter reporting that their data is growing in excess of 20% per year. Organizations with at least 500 TB of disk-based storage capacity are almost three times as likely as those with less than 100 TB to anticipate growth rates exceeding 20%.

The biggest application drivers of storage growth include business intelligence/data warehousing, ERP, and e-mail. While half of respondents believe that e-mail will be responsible for storage growth over the next two years, 12% believe that business intelligence and/or data analytics will be the application most responsible for storage growth over that same period. Other applications expected to have a significant impact on storage growth included enterprise resource planning systems, office productivity applications, and digital images. When analyzed by company size, enterprises are more likely than their midmarket counterparts to see data growth associated with business intelligence and data analytics, as well as web serving and e-commerce applications. For their part, midmarket organizations were more likely to cite e-mail, office productivity applications (i.e., Excel, PowerPoint, etc.), and video surveillance as more common application data storage growth sources.

Networked storage is the preferred infrastructure choice of large and more sophisticated organizations. The majority of users still leverage internal server storage (82%) and/or direct-attached storage (57%) to some extent. However, nearly two-thirds of users cite networked storage—whether network-attached storage (NAS), Fibre Channel and iSCSI SAN, or unified storage—as their primary disk-based storage technology (measured by percentage of total disk-based capacity). Networked storage systems were more likely to be identified as the primary underlying infrastructure for larger organizations—whether measured by employees, total disk-based capacity, or production servers—and those that view data storage as strategic to both IT and business operations. Organizations using networked storage were also more likely to report higher overall storage hardware utilization rates.

Size and importance of data storage technology dictates extent of support headcount. More than one-quarter (29%) of respondents have at least five storage full time equivalents (FTEs). Viewing the data based on company size—both number of employees and disk-based storage system capacity—reveals significant differences. Specifically, 59% of enterprises have at least four dedicated administrators in place to manage their storage environments compared to only 18% of midmarket organizations; similarly, nearly three-quarters (73%) of organizations with at least 500 TB of disk-based storage system capacity employ four or more administrators to manage these environments as opposed to 27% of those with less than 100 TB. Organizations that consider storage to be strategic to IT and business operations are more than twice as likely as those that view storage more tactically to have six or more FTEs focused on storage management activities. However, more than half (55%) of respondent organizations believe that they have some level of shortage when it comes to storage management headcount.

Research Report: 2012 Storage Market Survey 6

© 2012 by The Enterprise Strategy Group, Inc. All Rights Reserved.

Organizations expect to maintain healthy 2012 storage spending levels in 2013. Using $1 million as the line of delineation for 2012 storage spending levels, more than three-quarters (79%) of midmarket organizations found themselves below that line while nearly two-thirds (64%) of enterprise organizations came in above it. Organizations with at least 500 TB of total disk-based storage system capacity were more than six times as likely as those with less than 100 TB to have allocated $5 million or more for storage-related capital expenditures. Looking ahead, 59% of respondents expect to see an increase in 2013 storage spending relative to 2012 levels. Nearly two-thirds (65%) of enterprise-class organizations expect to increase their 2013 storage spending levels compared to 48% of midmarket respondents.

Cloud storage and server virtualization are expected to impact storage spending over the next 12-18 months. The use of cloud storage services to source storage capacity in lieu of buying new onsite infrastructure was the most commonly cited IT initiative with storage spending implications. More than one-third (35%) of organizations expect that supporting server virtualization implementations and/or technology refreshes will influence storage spending decisions. In addition to cloud storage and server virtualization, other IT initiatives most likely to impact storage spending among enterprise organizations included business intelligence/data analytics activities and data center initiatives.

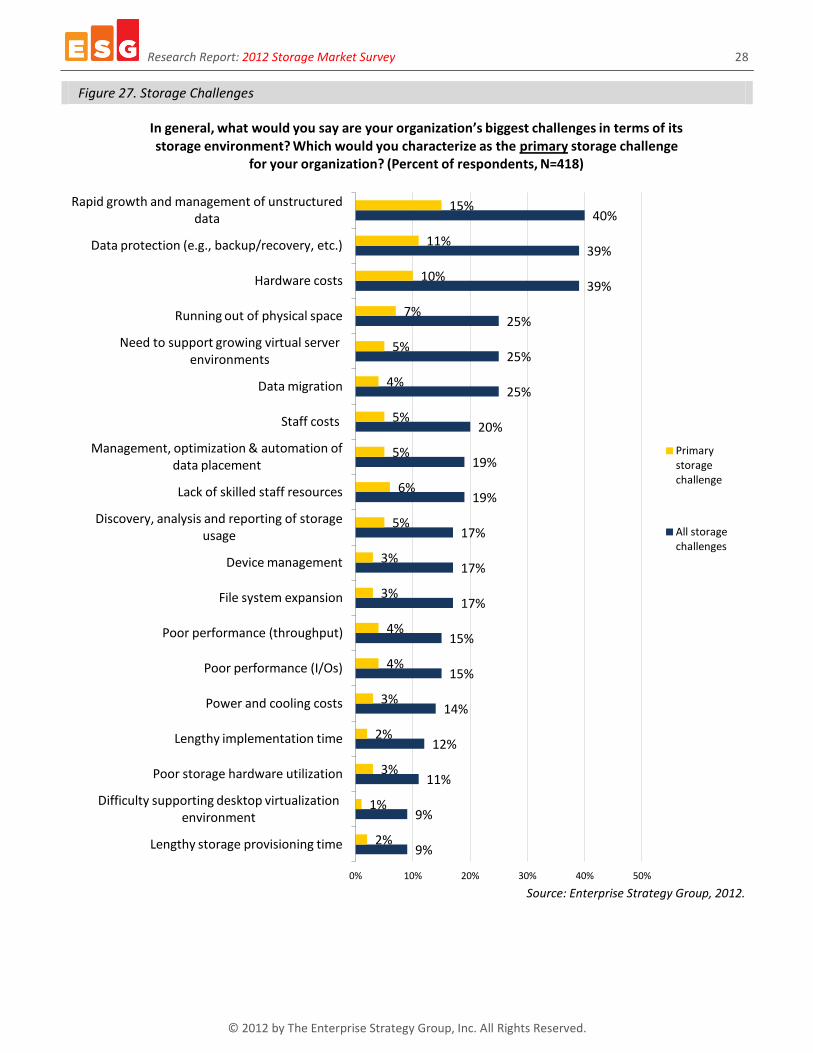

Challenges associated with storage environments span a wide spectrum of issues. When asked to assess the process of managing data storage technology, more than half (57%) of survey respondents indicated that it has actually become easier over the last five years. However, that does not mean that organizations don’t still encounter issues with their storage environments. In fact, respondents clearly acknowledge a wide variety of ongoing challenges based on the fact that every one of the issues provided as an option was cited by at least one respondent organization as their primary challenge. Storage costs are clearly a key consideration for IT organizations, with more than half citing capital expense (i.e., hardware) and/or operational expense (i.e., largely staff) as a storage challenge. Additionally, 15% of organizations cited cost as their primary challenge, whether related to CAPEX or OPEX. The rapid growth—and subsequent management—of unstructured data was also identified as a challenge by 40% of all respondents, with 15% singling it out as their primary challenge.

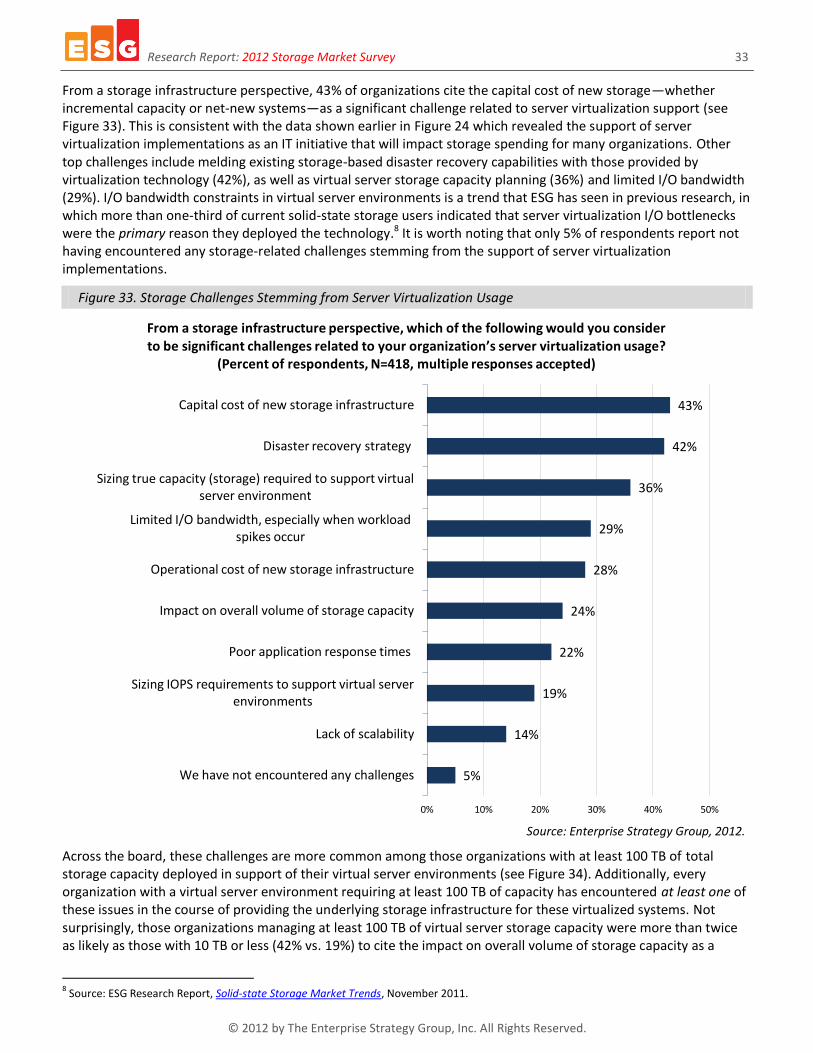

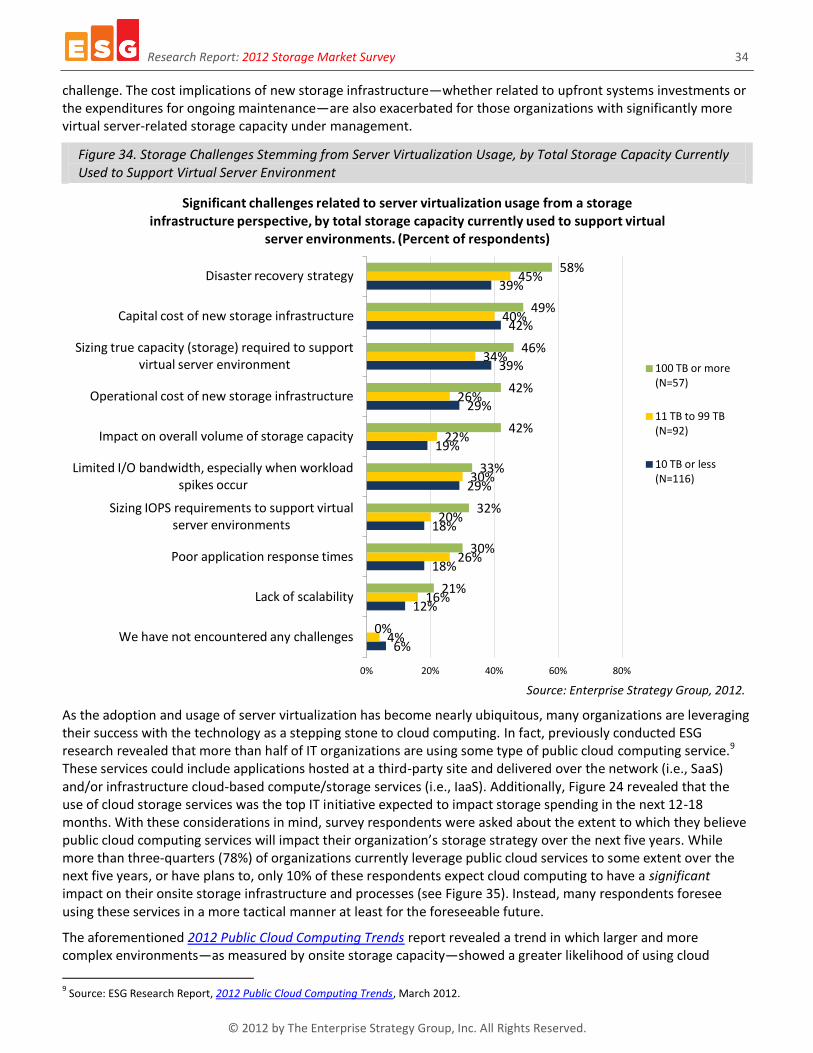

Cost of new infrastructure is the biggest server virtualization-related storage challenge. Of the organizations with server virtualization technology deployed, 38% report that virtual machine images, applications, and associated data combine to consume 10 TB of storage capacity or less. While just 30% of enterprise organizations allocate at least 100 TB of storage capacity to support their virtual server environments, more than three-quarters (76%) of those organizations with more than 500 virtual machines have at least 100 TB of storage capacity associated with their virtual server environments. As such, it is not surprising that from a storage infrastructure perspective, 43% of organizations cite the capital cost of new storage-—whether incremental capacity or net-new systems—as a significant challenge related to server virtualization support.

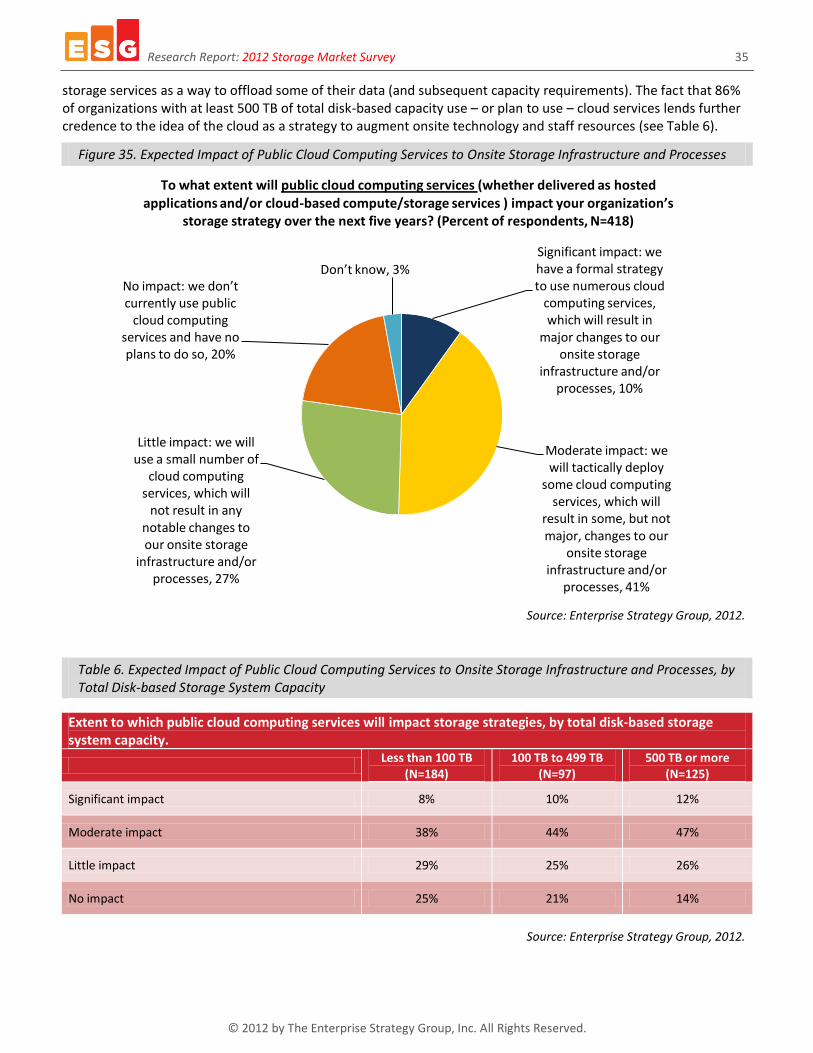

The impact of public cloud services on storage infrastructure will remain limited for most users. While more than three-quarters (78%) of organizations currently leverage public cloud computing services—or have plans to—to some extent over the next five years, only 10% of these respondents expect cloud computing to have a significant impact on their onsite storage infrastructure and processes. Instead, many respondents foresee using these services in a more tactical manner as a way to offload the burden on both technology and personnel resources, at least for the foreseeable future.

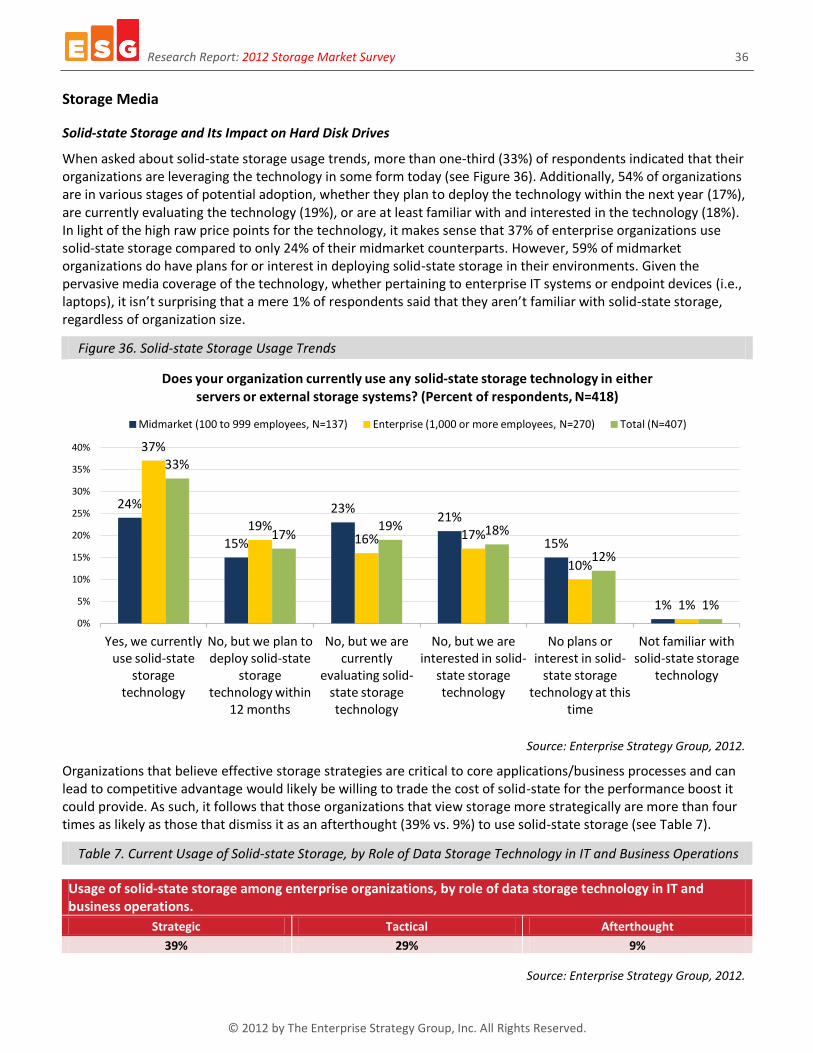

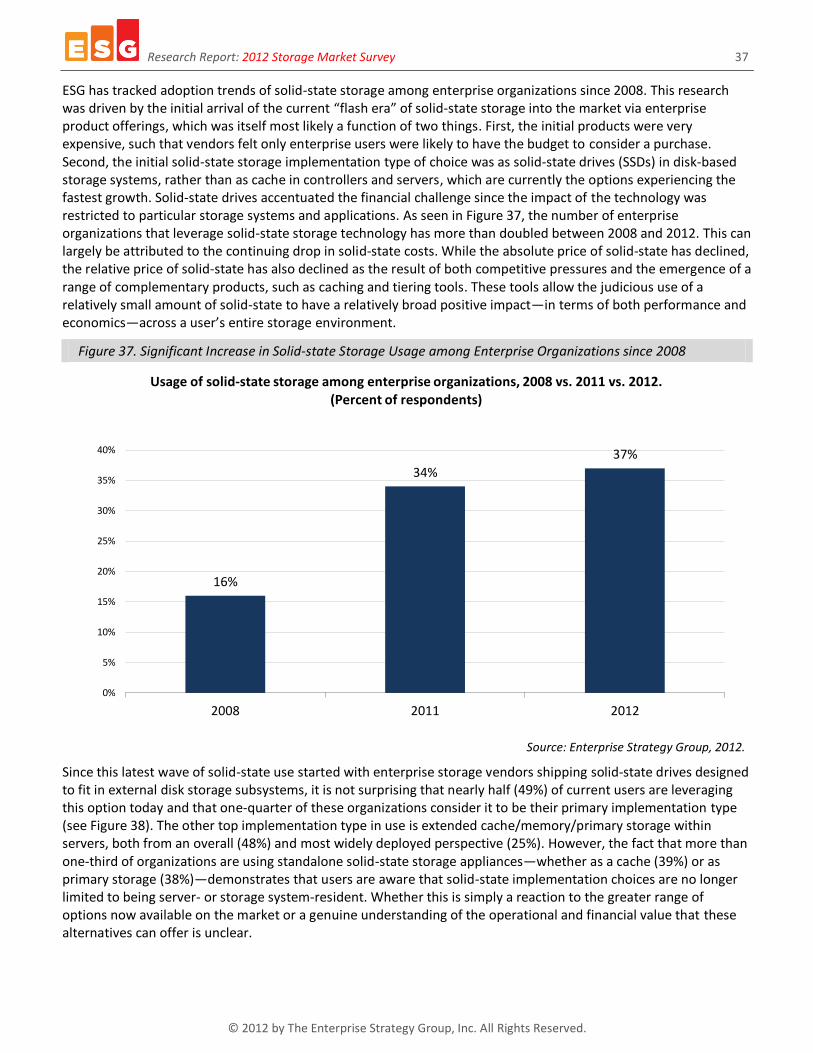

Solid-state storage usage is increasing. More than one-third (33%) of respondents indicated that their organizations are leveraging solid-state storage technology in some form today. In light of the high raw price points for the technology, it makes sense that 37% of enterprise organizations—compared to 16% in 2008—use solid-state storage compared to only 24% of their midmarket counterparts. Those organizations that view data storage more strategically are more than four times as likely as those that dismiss it as an afterthought (39% vs. 9%) to use solid-state storage.

Research Report: 2012 Storage Market Survey 7

© 2012 by The Enterprise Strategy Group, Inc. All Rights Reserved.

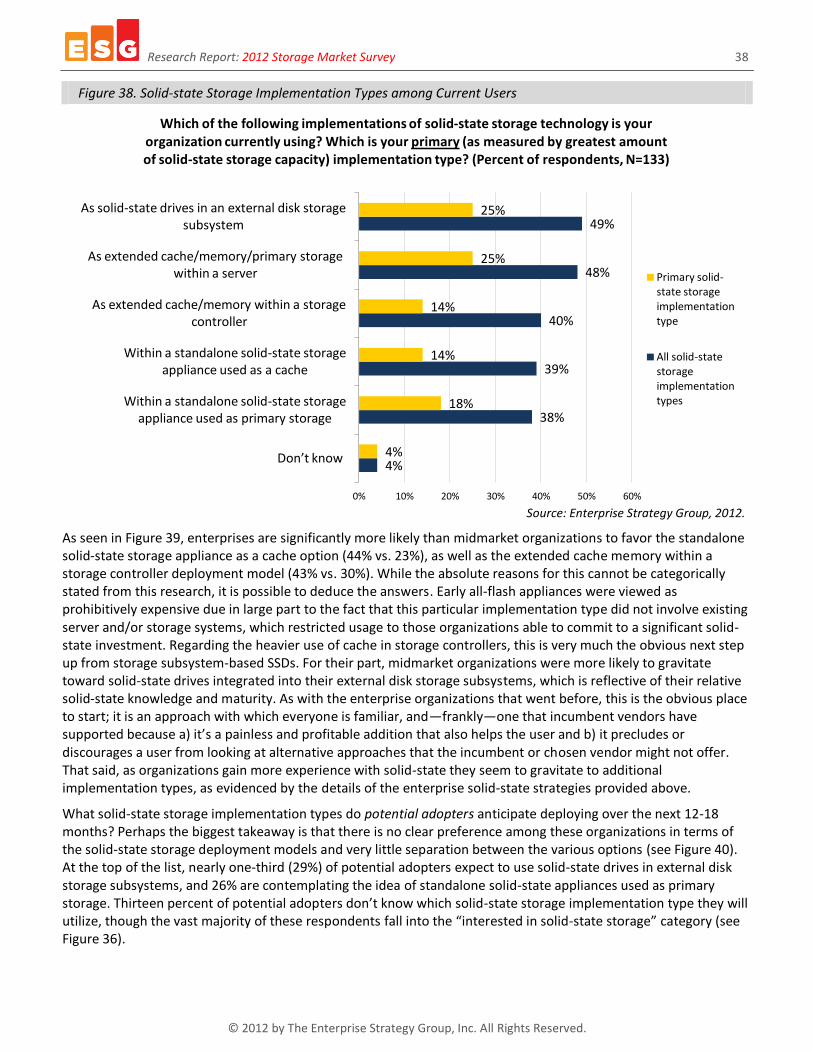

Solid-state drives (SSDs) are still the most common solid-state storage implementation type. Since the latest wave of solid-state usage started with enterprise storage vendors shipping external disk storage subsystems with solid-state drives, it is not surprising that nearly half of current solid-state users are leveraging this option today and that one-quarter of these organizations consider it to be their primary implementation type. The other top implementation type in use is extended cache/memory/primary storage within servers, both from an overall (48%) and most widely deployed perspective (25%). Among potential adopters, solid-state drives in an external disk storage subsystem are the most commonly cited implementation type.

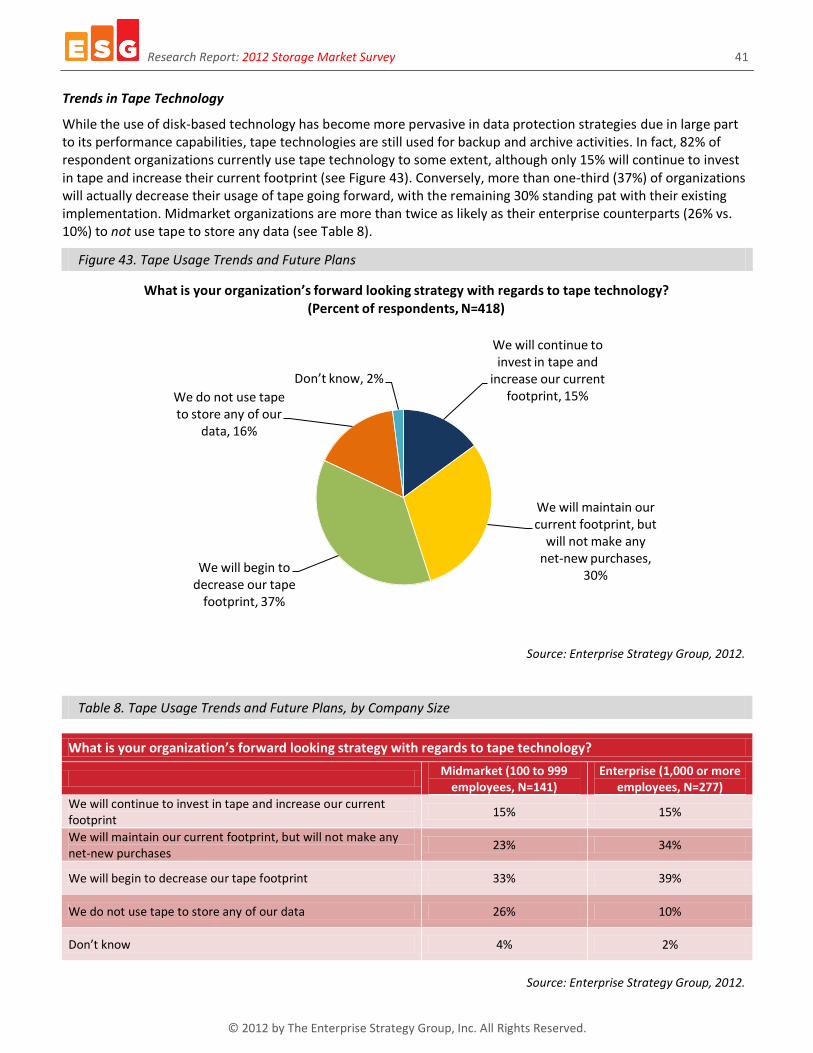

Tape won’t disappear anytime soon, but it’s not a top priority. While the use of disk-based technology has become more pervasive in data protection strategies due in large part to its performance capabilities, tape technologies are still used for backup and archive activities. In fact, 82% of respondent organizations currently use tape technology to some extent, although only 15% will continue to invest in tape and increase their current footprint. Conversely, more than one-third (37%) of organizations will actually decrease their usage of tape going forward, with the remaining 30% standing pat with their existing implementation. Midmarket organizations are more than twice as likely as their enterprise counterparts (26% vs. 10%) to not use tape to store any data.

High availability is most commonly cited as a “must have” storage system feature. Respondents were asked to identify up to five features they would classify as “must have” when purchasing a storage system. Considering downtime tolerance windows continue to shrink, especially for tier-1 and mission-critical applications and data, it makes sense that the majority of organizations gravitate to storage systems that can deliver high availability. The fact that 41% of organizations would expect their storage systems to provide 10 Gigabit Ethernet support is not surprising given that the increasing use of server virtualization is leading many organizations to re-architect their data center networks to accommodate increased throughput requirements. Data reduction technologies such as data deduplication (37%), storage tiering (33%), and unified storage (23%) were other top must-have storage system attributes identified by respondents, especially those with at least 500 TB of disk-based storage system capacity.

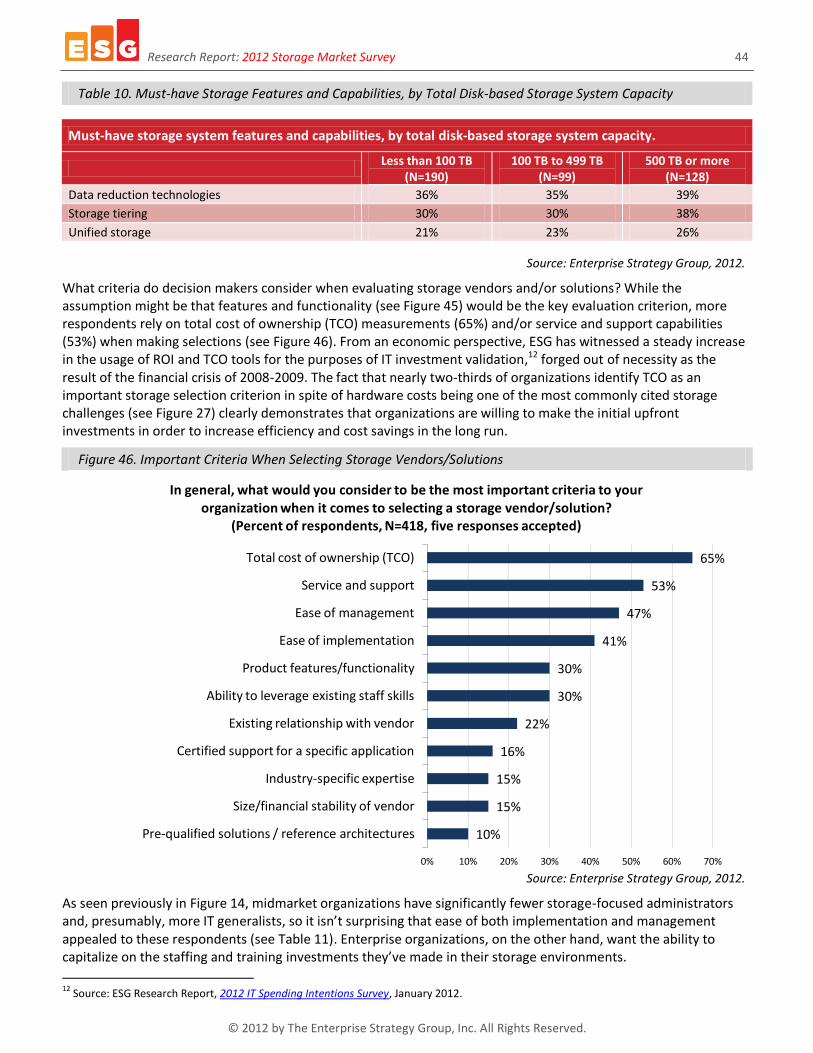

TCO and service and support are what organizations look for when making product/vendor selections. The majority of organizations rely on total cost of ownership (TCO) measurements and/or service and support capabilities when evaluating storage vendors/solutions. The fact that nearly two-thirds of organizations identify TCO as an important storage selection criterion, in spite of hardware costs being one of the most commonly cited storage challenges, clearly demonstrates that organizations are willing to make the initial upfront investments in order to increase efficiency and cost savings in the long run. The majority of those organizations that consider total cost of ownership when evaluating storage vendors/solutions gravitated toward the reduced cost of storage hardware and software as the most important cost consideration factoring into TCO calculations.

Storage performance and cost are the key messages vendors can deliver. When respondents were asked about the key messages that storage vendors should emphasize, performance and cost were ranked as the top two value propositions. Considering that hardware costs are among the top storage challenges and TCO is the most commonly leveraged storage vendor/solution selection criterion, it is not surprising that users put such a premium on cost. Among those organizations that view data storage as an afterthought in terms of the role it plays in IT and business operations, cost—both CAPEX and OPEX—actually supersedes storage performance. Additionally, these organizations put a slightly higher premium on a vendor’s cloud vision.

Research Report: 2012 Storage Market Survey 8

© 2012 by The Enterprise Strategy Group, Inc. All Rights Reserved.

Introduction

Research Objectives

In order to assess the current state and future direction of the data storage technology market, ESG recently surveyed 418 North American-based IT and data storage professionals representing midmarket (100 to 999 employees) and enterprise-class (1,000 employees or more) organizations. All respondents were personally responsible for evaluating, purchasing, and managing data storage technology for their organization and were familiar with their organization’s data storage environment and/or strategy—including topics such as storage technology types in use, current storage challenges, and forward looking data storage plans.

The survey was designed to answer the following questions:

How large is a typical storage environment in terms of disk-based storage system capacity?

At what rate are organizations adding storage capacity on an annual basis?

What applications are most responsible for data storage capacity growth?

What types of disk-based storage systems do organizations use? How does this vary according to size and complexity of IT and storage environments?

How many storage administrators do organizations employ? Are they satisfied with storage-focused headcount they have in place?

How much did organizations spend on data storage technology in 2012? How do they expect that to change in 2013?

What IT initiatives will have the greatest impact on storage spending over the next 12-18 months?

What challenges do organizations face in terms of their data storage environments? Is it getting easier to manage data storage?

What kind of impact has server virtualization technology had on data storage?

How do organizations expect public cloud computing services to affect their onsite storage infrastructure and processes?

How pervasive is the adoption of solid-state storage technology?

How extensive are current solid-state storage deployments? At what rate will solid-state storage erode the footprint of hard disk drives (HDDs)?

What solid-state storage implementation types have current users deployed? What do potential adopters expect to use?

What are the future plans for tape technology? How are current tape users leveraging the technology today?

What are viewed as “must have” storage features and functions? What criteria do organizations use when evaluating storage vendors/solutions?

What is the most important message storage vendors can deliver to their customers?

Survey participants represent a wide range of industries including manufacturing, financial services, communications and media, health care, retail, government, and business services. For more details, please see the Research Methodology and Respondent Demographics sections of this report.

Research Report: 2012 Storage Market Survey 9

© 2012 by The Enterprise Strategy Group, Inc. All Rights Reserved.

Research Findings

General Storage Environments

Capacity and Infrastructure

ESG regularly conducts research on the topic of data storage, and has consistently found that IT organizations are managing large and continually growing storage environments. In fact, managing data growth was cited as a top five overall IT priority by one-quarter of those surveyed in ESG’s 2012 IT Spending Intentions Survey.1 This is significant because it reflects the opinions of general IT professionals and not just storage managers and administrators, which would seem to indicate that storage is being more broadly acknowledged as strategically important at an organization-wide level.

As shown in Figure 1, more than one-quarter (29%) of organizations have at least 500 TB of disk-based storage system capacity deployed. From a company size perspective, nearly two-thirds (63%) of midmarket organizations (i.e., 100 to 999 employees) manage less than 50 TB of total disk-based storage system capacity; conversely, more than one in five enterprises (i.e., 1,000 or more employees) have 1 PB or more deployed, while 8% of these larger organizations reported having at least 5 PB of total disk-based storage system capacity.

Figure 1. Total Disk-based Storage System Capacity, by Company Size

Source: Enterprise Strategy Group, 2012.

This data becomes more meaningful when analyzed based on the scope of onsite IT infrastructure—as measured by the number of production servers—already deployed. Indeed, there is a direct relationship between the amount of disk-based storage system capacity and the number of production servers. Figure 2 reveals that nearly two-thirds (61%) of organizations with more than 500 production servers have at least 500 TB of disk-based storage system capacity as opposed to only 11% of those with 100 or fewer production servers. When compared to storage environments from 2010, there has been a significant increase in the number of organizations with 500 TB or more

1 Source: ESG Research Report, 2012 IT Spending Intentions Survey, January 2012.

40%

23%

11% 10%

6% 8%

2% 0% 0% 0%

8% 10%

13% 16%

12%

18%

9% 7%

3% 5%

19%

14% 12%

14%

10%

14%

6% 4%

2% 3%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

Less than 25 TB

25 TB to 49 TB

50 TB to 99 TB

100 TB to 249 TB

250 TB to 499 TB

500 TB to 999 TB

1 PB to 2.499 PB

2.5 PB to 4.999 PB

5 PB to 9.999 PB

10 PB or more

To the best of your knowledge, what is your organization’s total installed capacity associated with disk-based storage systems? (Percent of respondents)

Midmarket (100 to 999 employees, N=141) Enterprise (1,000 or more employees, N=276) Total (N=417)

Research Report: 2012 Storage Market Survey 10

© 2012 by The Enterprise Strategy Group, Inc. All Rights Reserved.

of total disk-based storage system capacity, especially in the midmarket and small enterprise segments (see Figure 3).

Figure 2. Total Installed Disk-Based Storage System Capacity, by Total Number of Production Servers

Source: Enterprise Strategy Group, 2012.

Figure 3. Percent of Organizations with Disk-based Storage System Capacity of 500 TB or More, 2010 vs. 2012

Source: Enterprise Strategy Group, 2012.

At what rate is storage capacity increasing annually to at least try to keep pace with continually growing volumes of data? ESG research found that the majority of respondents (70%) cited overall annual storage capacity growth rates in the 1%-20% range, with more than one-quarter reporting that their data is growing in excess of 20% per year

11%

33%

61%

18%

33%

23%

72%

34%

16%

0% 20% 40% 60% 80% 100%

100 or fewer production servers (N=180)

101 to 500 production servers (N=123)

More than 500 production servers (N=112)

Total installed disk-based storage system capacity, by total number of production servers. (Percent of respondents)

500 TB or more 100 TB to 499 TB Less than 100 TB

2%

9%

33%

50%

10%

24%

49%

57%

0% 10% 20% 30% 40% 50% 60%

100 to 999 employees

1,000 to 4,999 employees

5,000 to 19,999 employees

20,000 or more employees

Percent of organizations with external disk-based storage capacity of 500 TB or more, by number of employees—2010 vs. 2012. (Percent of respondents)

2012 (N=418)

2010 (N=271)

Research Report: 2012 Storage Market Survey 11

© 2012 by The Enterprise Strategy Group, Inc. All Rights Reserved.

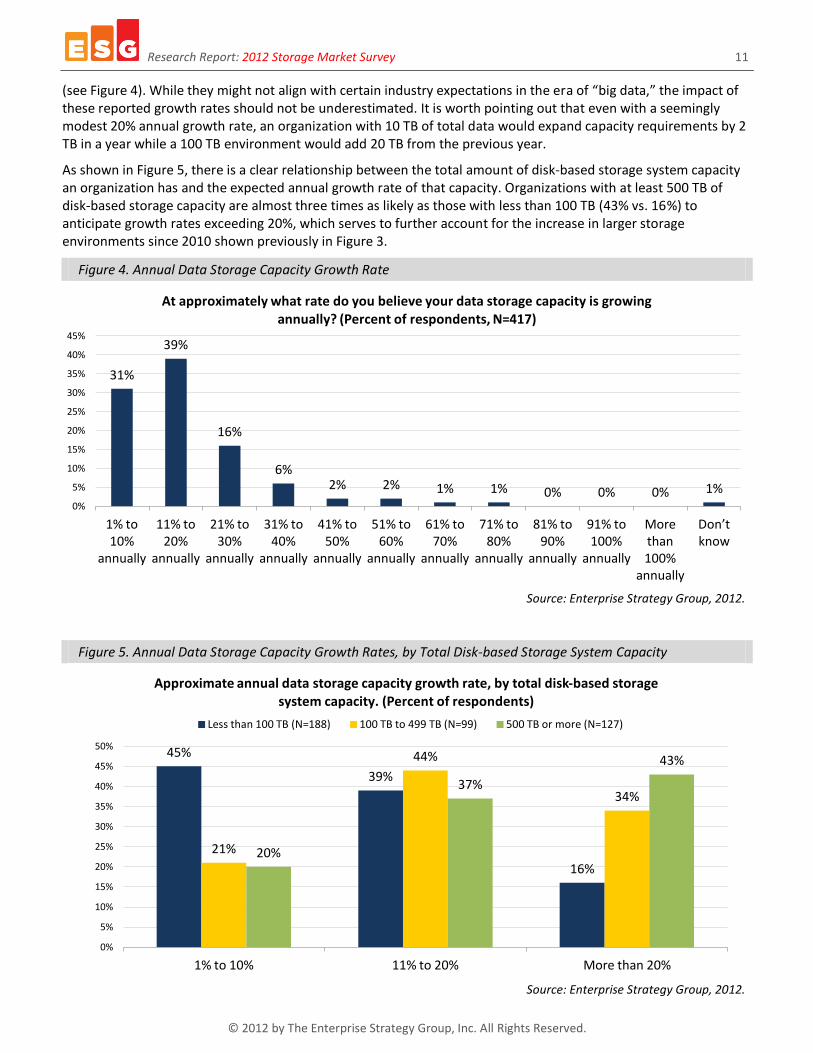

(see Figure 4). While they might not align with certain industry expectations in the era of “big data,” the impact of these reported growth rates should not be underestimated. It is worth pointing out that even with a seemingly modest 20% annual growth rate, an organization with 10 TB of total data would expand capacity requirements by 2 TB in a year while a 100 TB environment would add 20 TB from the previous year.

As shown in Figure 5, there is a clear relationship between the total amount of disk-based storage system capacity an organization has and the expected annual growth rate of that capacity. Organizations with at least 500 TB of disk-based storage capacity are almost three times as likely as those with less than 100 TB (43% vs. 16%) to anticipate growth rates exceeding 20%, which serves to further account for the increase in larger storage environments since 2010 shown previously in Figure 3.

Figure 4. Annual Data Storage Capacity Growth Rate

Source: Enterprise Strategy Group, 2012.

Figure 5. Annual Data Storage Capacity Growth Rates, by Total Disk-based Storage System Capacity

Source: Enterprise Strategy Group, 2012.

31%

39%

16%

6% 2% 2% 1% 1% 0% 0% 0% 1%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

1% to 10%

annually

11% to 20%

annually

21% to 30%

annually

31% to 40%

annually

41% to 50%

annually

51% to 60%

annually

61% to 70%

annually

71% to 80%

annually

81% to 90%

annually

91% to 100%

annually

More than 100%

annually

Don’t know

At approximately what rate do you believe your data storage capacity is growing annually? (Percent of respondents, N=417)

45%

39%

16%

21%

44%

34%

20%

37%

43%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

1% to 10% 11% to 20% More than 20%

Approximate annual data storage capacity growth rate, by total disk-based storage system capacity. (Percent of respondents)

Less than 100 TB (N=188) 100 TB to 499 TB (N=99) 500 TB or more (N=127)

Research Report: 2012 Storage Market Survey 12

© 2012 by The Enterprise Strategy Group, Inc. All Rights Reserved.

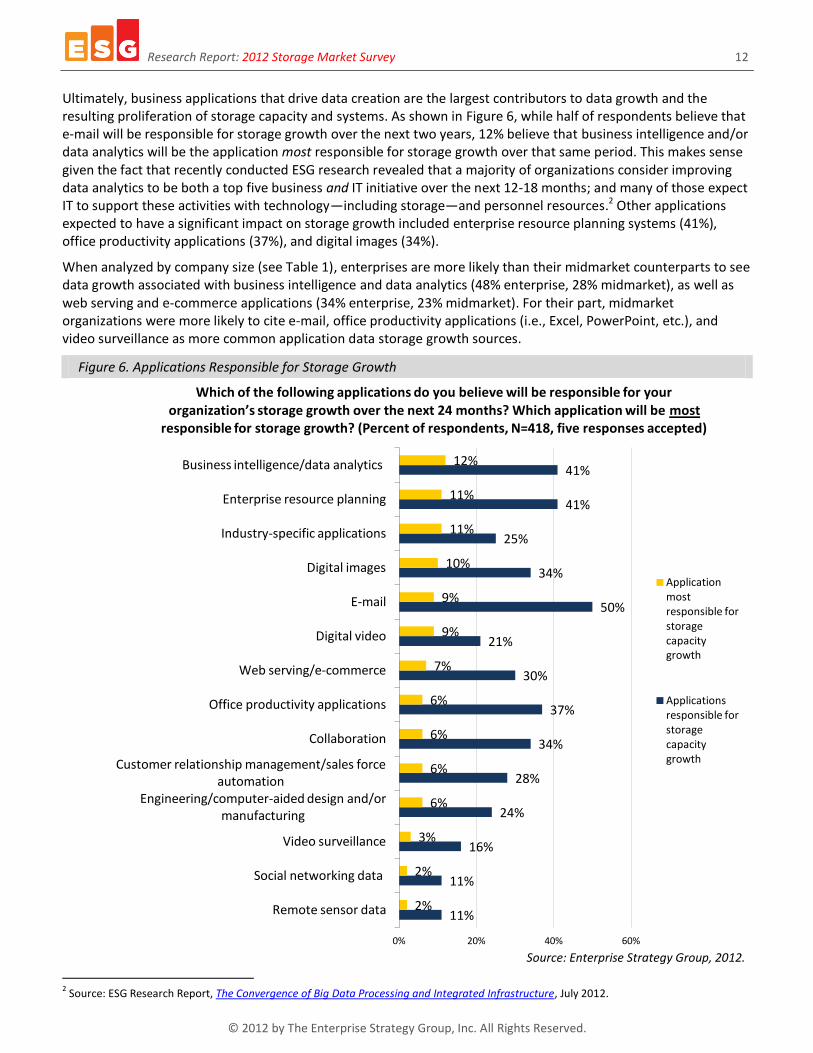

Ultimately, business applications that drive data creation are the largest contributors to data growth and the resulting proliferation of storage capacity and systems. As shown in Figure 6, while half of respondents believe that e-mail will be responsible for storage growth over the next two years, 12% believe that business intelligence and/or data analytics will be the application most responsible for storage growth over that same period. This makes sense given the fact that recently conducted ESG research revealed that a majority of organizations consider improving data analytics to be both a top five business and IT initiative over the next 12-18 months; and many of those expect IT to support these activities with technology—including storage—and personnel resources.2 Other applications expected to have a significant impact on storage growth included enterprise resource planning systems (41%), office productivity applications (37%), and digital images (34%).

When analyzed by company size (see Table 1), enterprises are more likely than their midmarket counterparts to see data growth associated with business intelligence and data analytics (48% enterprise, 28% midmarket), as well as web serving and e-commerce applications (34% enterprise, 23% midmarket). For their part, midmarket organizations were more likely to cite e-mail, office productivity applications (i.e., Excel, PowerPoint, etc.), and video surveillance as more common application data storage growth sources.

Figure 6. Applications Responsible for Storage Growth

Source: Enterprise Strategy Group, 2012.

2 Source: ESG Research Report, The Convergence of Big Data Processing and Integrated Infrastructure, July 2012.

11%

11%

16%

24%

28%

34%

37%

30%

21%

50%

34%

25%

41%

41%

2%

2%

3%

6%

6%

6%

6%

7%

9%

9%

10%

11%

11%

12%

0% 20% 40% 60%

Remote sensor data

Social networking data

Video surveillance

Engineering/computer-aided design and/or manufacturing

Customer relationship management/sales force automation

Collaboration

Office productivity applications

Web serving/e-commerce

Digital video

Digital images

Industry-specific applications

Enterprise resource planning

Business intelligence/data analytics

Which of the following applications do you believe will be responsible for your organization’s storage growth over the next 24 months? Which application will be most

responsible for storage growth? (Percent of respondents, N=418, five responses accepted)

Application most responsible for storage capacity growth

Applications responsible for storage capacity growth

Research Report: 2012 Storage Market Survey 13

© 2012 by The Enterprise Strategy Group, Inc. All Rights Reserved.

Table 1. Applications Responsible for Storage Growth, by Company Size

Which of the following applications do you believe will be responsible for your organization’s storage growth over the next 24 months?

Midmarket (100 to 999

employees, N=141) Enterprise (1,000 or more

employees, N=277)

Business intelligence/data analytics 28% 48%

E-mail 58% 46%

Web serving/e-commerce 23% 34%

Office productivity applications 42% 34%

Video surveillance 20% 14%

Source: Enterprise Strategy Group, 2012.

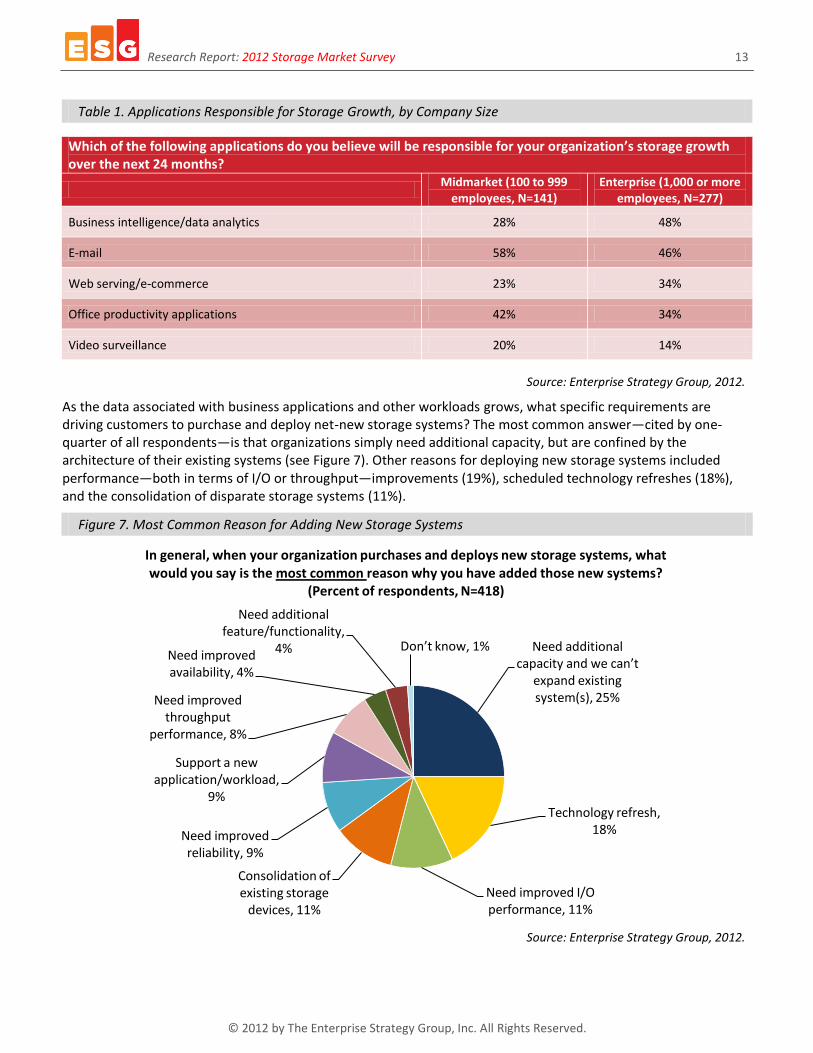

As the data associated with business applications and other workloads grows, what specific requirements are driving customers to purchase and deploy net-new storage systems? The most common answer—cited by one-quarter of all respondents—is that organizations simply need additional capacity, but are confined by the architecture of their existing systems (see Figure 7). Other reasons for deploying new storage systems included performance—both in terms of I/O or throughput—improvements (19%), scheduled technology refreshes (18%), and the consolidation of disparate storage systems (11%).

Figure 7. Most Common Reason for Adding New Storage Systems

Source: Enterprise Strategy Group, 2012.

Need additional capacity and we can’t

expand existing system(s), 25%

Technology refresh, 18%

Need improved I/O performance, 11%

Consolidation of existing storage

devices, 11%

Need improved reliability, 9%

Support a new application/workload,

9%

Need improved throughput

performance, 8%

Need improved availability, 4%

Need additional feature/functionality,

4% Don’t know, 1%

In general, when your organization purchases and deploys new storage systems, what would you say is the most common reason why you have added those new systems?

(Percent of respondents, N=418)

Research Report: 2012 Storage Market Survey 14

© 2012 by The Enterprise Strategy Group, Inc. All Rights Reserved.

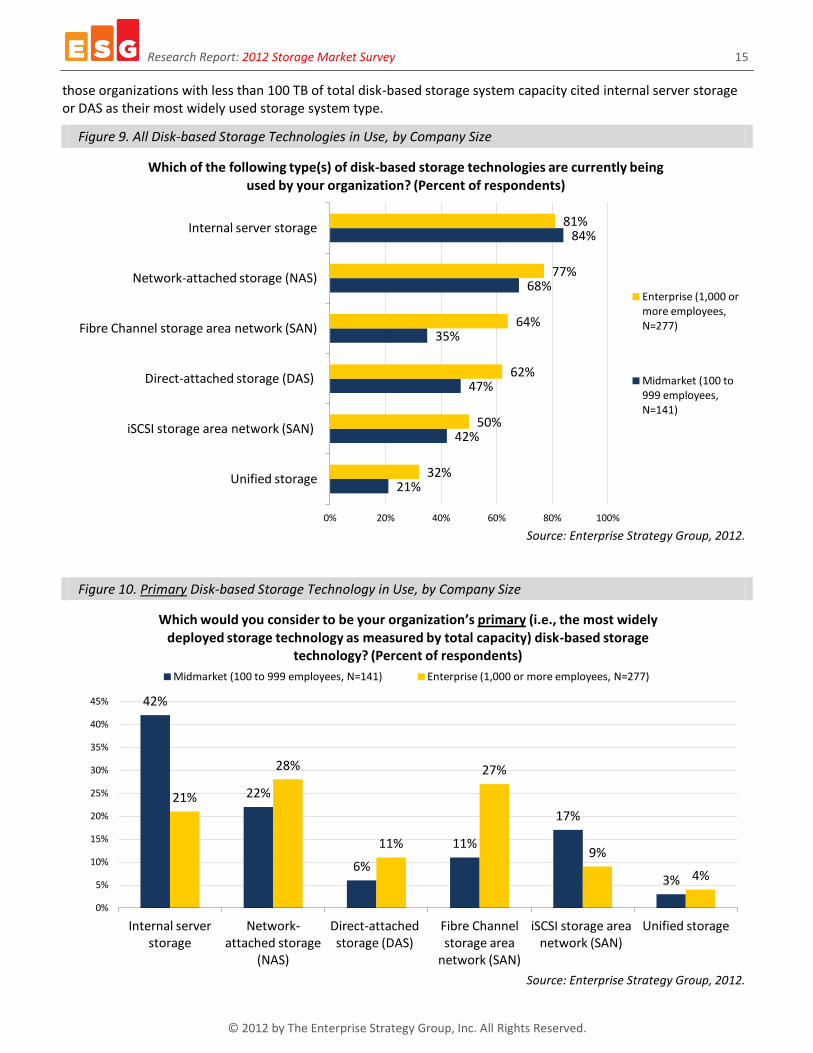

There is a wide array of data storage system options with various features and performance capabilities available to support the needs of IT environments. While the focus of a lot of industry commentary concerns the various forms of networked storage, Figure 8 reveals that the majority of users still leverage internal server storage (82%) and/or direct-attached storage (57%). Of course, the former comes as part of a delivered system, so its existence doesn’t automatically equate to its use or value. Indeed, when all the various forms of networked (i.e., shared or at least shareable) storage are added together, nearly two-thirds (64%) of users attest to such an approach as their primary disk-based storage technology, as measured by percentage of total disk-based capacity. This makes sense, given the benefits of shared access to data across systems and applications that networked storage invariably delivers, together with the improved utilization rates that tend to follow more of a pooled approach. It is worth noting that 54% of all respondent organizations use Fibre Channel SAN-based systems to some extent, with 22% singling it out as their primary storage infrastructure. What this says simply is that—relative to all other disk-based storage options—those organizations using Fibre Channel SAN technology were more likely to recognize it as their most widely deployed storage platform.

Figure 8. All Disk-based Storage Technologies in Use

Source: Enterprise Strategy Group, 2012.

When viewed by company size—whether measured by the number of employees or total disk-based storage system capacity—some interesting trends emerge (see Figure 9 and Figure 11). The first obvious takeaway is that larger organizations are more likely to have each of the various storage options deployed, which is likely a function of more diversified environments—either by design, ability, and/or acquisition—in terms of applications and data with varying underlying storage system requirements. Looking at all of the storage system types that organizations have in place, internal server storage is still the most commonly deployed storage type regardless of company size, and usage does not vary much between large and small organizations; however, there is a significant difference in Fibre Channel SAN usage. Specifically, nearly two-thirds (64%) of enterprise organizations have Fibre Channel SAN technology implemented compared to only 35% of their midmarket counterparts; likewise, more than two-thirds (68%) of organizations with more than 500 TB of disk-based storage capacity are Fibre Channel SAN users as opposed to only 41% of those with less than 100 TB. According to Figure 10 and Figure 12, in terms of the depth of usage, smaller organizations are significantly more likely to report that the largest portion of their overall storage capacity is provided by internal server storage or DAS. Indeed, nearly half (48%) of midmarket respondents identified these “non-networked” options as their organization’s primary storage infrastructure; similarly, 48% of

28%

47%

54%

57%

74%

82%

4%

12%

22%

9%

26%

28%

0% 20% 40% 60% 80% 100%

Unified storage

iSCSI storage area network (SAN)

Fibre Channel storage area network (SAN)

Direct-attached storage (DAS)

Network-attached storage (NAS)

Internal server storage

Which of the following type(s) of disk-based storage technologies are currently being used by your organization? Which would you consider to be your organization’s primary

disk-based storage technology? (Percent of respondents, N=418)

Primary disk-based storage technology

All disk-based storage technologies

Research Report: 2012 Storage Market Survey 15

© 2012 by The Enterprise Strategy Group, Inc. All Rights Reserved.

those organizations with less than 100 TB of total disk-based storage system capacity cited internal server storage or DAS as their most widely used storage system type.

Figure 9. All Disk-based Storage Technologies in Use, by Company Size

Source: Enterprise Strategy Group, 2012.

Figure 10. Primary Disk-based Storage Technology in Use, by Company Size

Source: Enterprise Strategy Group, 2012.

21%

42%

47%

35%

68%

84%

32%

50%

62%

64%

77%

81%

0% 20% 40% 60% 80% 100%

Unified storage

iSCSI storage area network (SAN)

Direct-attached storage (DAS)

Fibre Channel storage area network (SAN)

Network-attached storage (NAS)

Internal server storage

Which of the following type(s) of disk-based storage technologies are currently being used by your organization? (Percent of respondents)

Enterprise (1,000 or more employees, N=277)

Midmarket (100 to 999 employees, N=141)

42%

22%

6%

11%

17%

3%

21%

28%

11%

27%

9%

4%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

Internal server storage

Network-attached storage

(NAS)

Direct-attached storage (DAS)

Fibre Channel storage area

network (SAN)

iSCSI storage area network (SAN)

Unified storage

Which would you consider to be your organization’s primary (i.e., the most widely deployed storage technology as measured by total capacity) disk-based storage

technology? (Percent of respondents)

Midmarket (100 to 999 employees, N=141) Enterprise (1,000 or more employees, N=277)

Research Report: 2012 Storage Market Survey 16

© 2012 by The Enterprise Strategy Group, Inc. All Rights Reserved.

Figure 11. All Disk-based Storage Technologies in Use, by Total Disk-based Storage System Capacity

Source: Enterprise Strategy Group, 2012.

Figure 12. Primary Disk-based Storage Technology in Use, by Total Disk-based Storage System Capacity

Source: Enterprise Strategy Group, 2012.

21%

40%

53%

41%

72%

85%

24%

49%

56%

62%

69%

76%

43%

56%

64%

68%

80%

80%

0% 20% 40% 60% 80% 100%

Unified storage

iSCSI storage area network (SAN)

Direct-attached storage (DAS)

Fibre Channel storage area network (SAN)

Network-attached storage (NAS)

Internal server storage

Type(s) of disk-based storage technologies currently being used, by total disk-based storage system capacity. (Percent of respondents)

500 TB or more (N=128)

100 TB to 499 TB (N=99)

Less than 100 TB (N=190)

39%

9%

21%

16% 13%

2%

22%

11%

22%

29%

11%

4%

16%

9%

38%

23%

10%

5%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

Internal server storage

Direct-attached storage (DAS)

Network-attached storage

(NAS)

Fibre Channel storage area

network (SAN)

iSCSI storage area network (SAN)

Unified storage

Primary disk-based storage technology currently being used, by total disk-based storage system capacity. (Percent of respondents)

Less than 100 TB (N=190) 100 TB to 499 TB (N=99) 500 TB or more (N=128)

Research Report: 2012 Storage Market Survey 17

© 2012 by The Enterprise Strategy Group, Inc. All Rights Reserved.

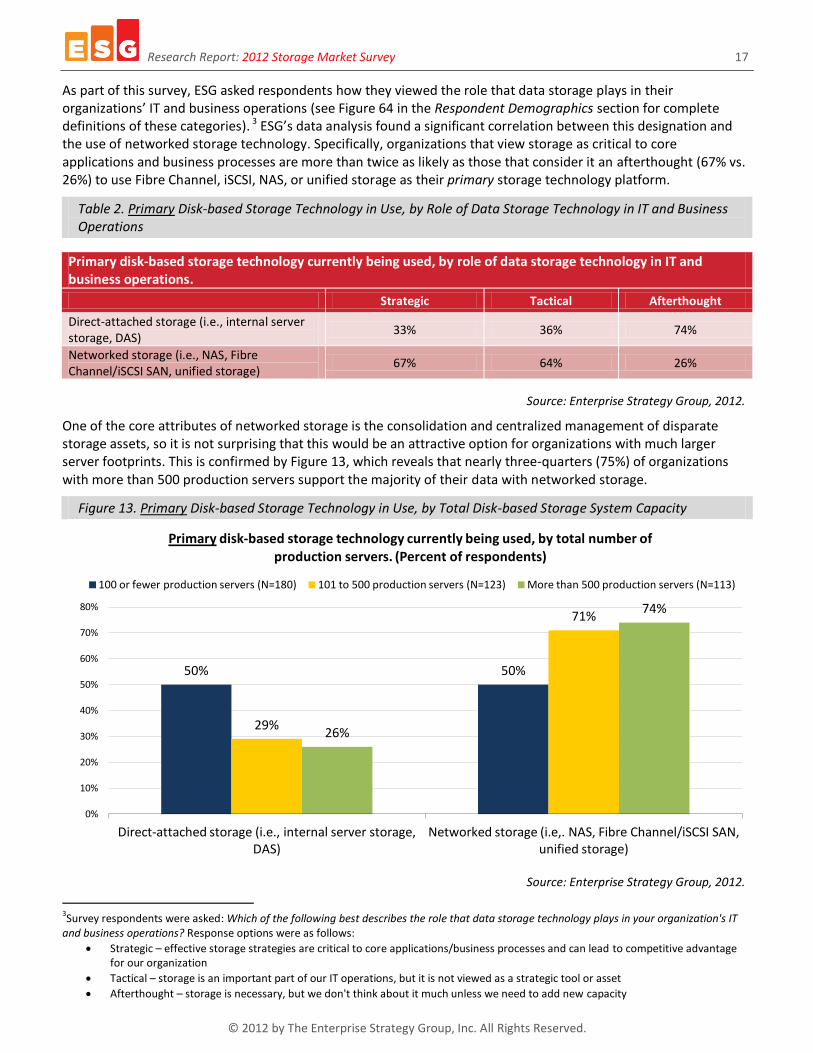

As part of this survey, ESG asked respondents how they viewed the role that data storage plays in their organizations’ IT and business operations (see Figure 64 in the Respondent Demographics section for complete definitions of these categories). 3 ESG’s data analysis found a significant correlation between this designation and the use of networked storage technology. Specifically, organizations that view storage as critical to core applications and business processes are more than twice as likely as those that consider it an afterthought (67% vs. 26%) to use Fibre Channel, iSCSI, NAS, or unified storage as their primary storage technology platform.

Table 2. Primary Disk-based Storage Technology in Use, by Role of Data Storage Technology in IT and Business Operations

Primary disk-based storage technology currently being used, by role of data storage technology in IT and business operations.

Strategic Tactical Afterthought

Direct-attached storage (i.e., internal server storage, DAS)

33% 36% 74%

Networked storage (i.e., NAS, Fibre Channel/iSCSI SAN, unified storage)

67% 64% 26%

Source: Enterprise Strategy Group, 2012.

One of the core attributes of networked storage is the consolidation and centralized management of disparate storage assets, so it is not surprising that this would be an attractive option for organizations with much larger server footprints. This is confirmed by Figure 13, which reveals that nearly three-quarters (75%) of organizations with more than 500 production servers support the majority of their data with networked storage.

Figure 13. Primary Disk-based Storage Technology in Use, by Total Disk-based Storage System Capacity

Source: Enterprise Strategy Group, 2012.

3Survey respondents were asked: Which of the following best describes the role that data storage technology plays in your organization's IT

and business operations? Response options were as follows:

Strategic – effective storage strategies are critical to core applications/business processes and can lead to competitive advantage for our organization

Tactical – storage is an important part of our IT operations, but it is not viewed as a strategic tool or asset

Afterthought – storage is necessary, but we don't think about it much unless we need to add new capacity

50% 50%

29%

71%

26%

74%

0%

10%

20%

30%

40%

50%

60%

70%

80%

Direct-attached storage (i.e., internal server storage, DAS)

Networked storage (i.e,. NAS, Fibre Channel/iSCSI SAN, unified storage)

Primary disk-based storage technology currently being used, by total number of production servers. (Percent of respondents)

100 or fewer production servers (N=180) 101 to 500 production servers (N=123) More than 500 production servers (N=113)

Research Report: 2012 Storage Market Survey 18

© 2012 by The Enterprise Strategy Group, Inc. All Rights Reserved.

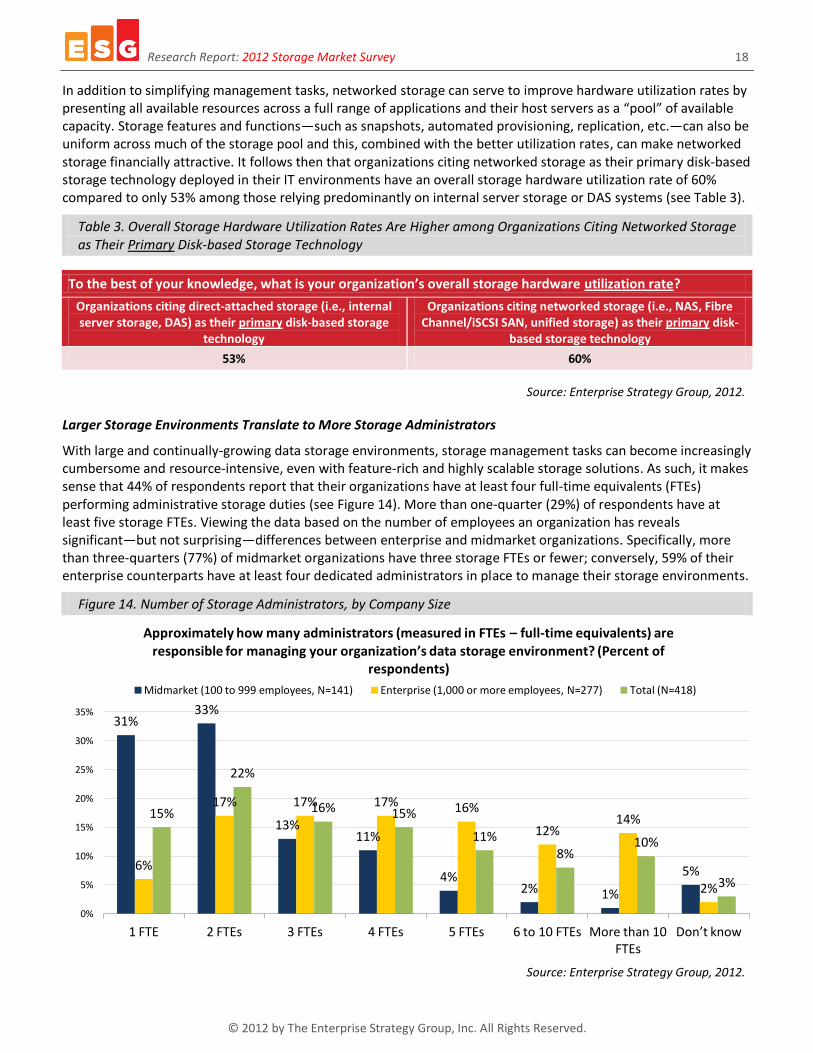

In addition to simplifying management tasks, networked storage can serve to improve hardware utilization rates by presenting all available resources across a full range of applications and their host servers as a “pool” of available capacity. Storage features and functions—such as snapshots, automated provisioning, replication, etc.—can also be uniform across much of the storage pool and this, combined with the better utilization rates, can make networked storage financially attractive. It follows then that organizations citing networked storage as their primary disk-based storage technology deployed in their IT environments have an overall storage hardware utilization rate of 60% compared to only 53% among those relying predominantly on internal server storage or DAS systems (see Table 3).

Table 3. Overall Storage Hardware Utilization Rates Are Higher among Organizations Citing Networked Storage as Their Primary Disk-based Storage Technology

To the best of your knowledge, what is your organization’s overall storage hardware utilization rate?

Organizations citing direct-attached storage (i.e., internal server storage, DAS) as their primary disk-based storage

technology

Organizations citing networked storage (i.e., NAS, Fibre Channel/iSCSI SAN, unified storage) as their primary disk-

based storage technology

53% 60%

Source: Enterprise Strategy Group, 2012.

Larger Storage Environments Translate to More Storage Administrators

With large and continually-growing data storage environments, storage management tasks can become increasingly cumbersome and resource-intensive, even with feature-rich and highly scalable storage solutions. As such, it makes sense that 44% of respondents report that their organizations have at least four full-time equivalents (FTEs) performing administrative storage duties (see Figure 14). More than one-quarter (29%) of respondents have at least five storage FTEs. Viewing the data based on the number of employees an organization has reveals significant—but not surprising—differences between enterprise and midmarket organizations. Specifically, more than three-quarters (77%) of midmarket organizations have three storage FTEs or fewer; conversely, 59% of their enterprise counterparts have at least four dedicated administrators in place to manage their storage environments.

Figure 14. Number of Storage Administrators, by Company Size

Source: Enterprise Strategy Group, 2012.

31% 33%

13% 11%

4% 2% 1%

5% 6%

17% 17% 17% 16%

12% 14%

2%

15%

22%

16% 15%

11% 8%

10%

3%

0%

5%

10%

15%

20%

25%

30%

35%

1 FTE 2 FTEs 3 FTEs 4 FTEs 5 FTEs 6 to 10 FTEs More than 10 FTEs

Don’t know

Approximately how many administrators (measured in FTEs – full-time equivalents) are responsible for managing your organization’s data storage environment? (Percent of

respondents)

Midmarket (100 to 999 employees, N=141) Enterprise (1,000 or more employees, N=277) Total (N=418)

Research Report: 2012 Storage Market Survey 19

© 2012 by The Enterprise Strategy Group, Inc. All Rights Reserved.

This data becomes more meaningful when analyzed from the perspective of both storage environment size and strategic relevance. Not surprisingly, there is a direct correlation between the number of storage FTEs an organization has and the amount of disk-based capacity requiring management. Indeed, more than one-third (38%) of organizations with at least 500 TB of disk-based storage system capacity employ six or more administrators to manage these environments. On the other hand, nearly three-quarters (73%) of those organizations with disk-based storage footprints of less than 100 TB have three or fewer storage FTEs (see Figure 15). While organizations that place a greater emphasis on storage technology are much more likely to have more advanced storage systems deployed in their environments (as seen in Table 2), it is also important to consider the human element. Indeed, organizations that consider storage to be strategic to IT and business operations are more than twice as likely as those that view storage more tactically (27% vs. 10%) to have six or more FTEs focused on storage management activities (see Figure 16).

Figure 15. Number of Storage Administrators, by Total Disk-based Storage System Capacity

Source: Enterprise Strategy Group, 2012.

Figure 16. Number of Storage Administrators, by Role of Data Storage Technology in IT and Business Operations

Source: Enterprise Strategy Group, 2012.

9%

11%

38%

5%

14%

20%

13%

21%

15%

15%

17%

16%

30%

27%

10%

28%

9%

1%

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Less than 100 TB (N=182)

100 TB to 499 TB (N=98)

500 TB or more (N=124)

Number of administrators (measured in FTEs) responsible for managing data storage environments, by total disk-based storage system capacity. (Percent of respondents)

6 or more FTEs 5 FTEs 4 FTEs 3 FTEs 2 FTEs 1 FTE

10%

27%

5%

13%

12%

10%

19%

13%

10%

15%

19%

25%

29%

18%

50%

15%

11%

0% 20% 40% 60% 80% 100%

Afterthought – storage is necessary but we don't think about it much unless we need to add new capacity

(N=20)

Tactical – storage is an important part of our IT operations but it is not viewed as a strategic tool or

asset (N=172)

Strategic – effective storage strategies are critical to core applications/business processes and can lead to competitive advantage for our organization (N=205)

Number of administrators (measured in FTEs) responsible for managing data storage environments, by role of data storage technology in IT and business operations. (Percent of

respondents)

6 or more FTEs 5 FTEs 4 FTEs 3 FTEs 2 FTEs 1 FTE

Research Report: 2012 Storage Market Survey 20

© 2012 by The Enterprise Strategy Group, Inc. All Rights Reserved.

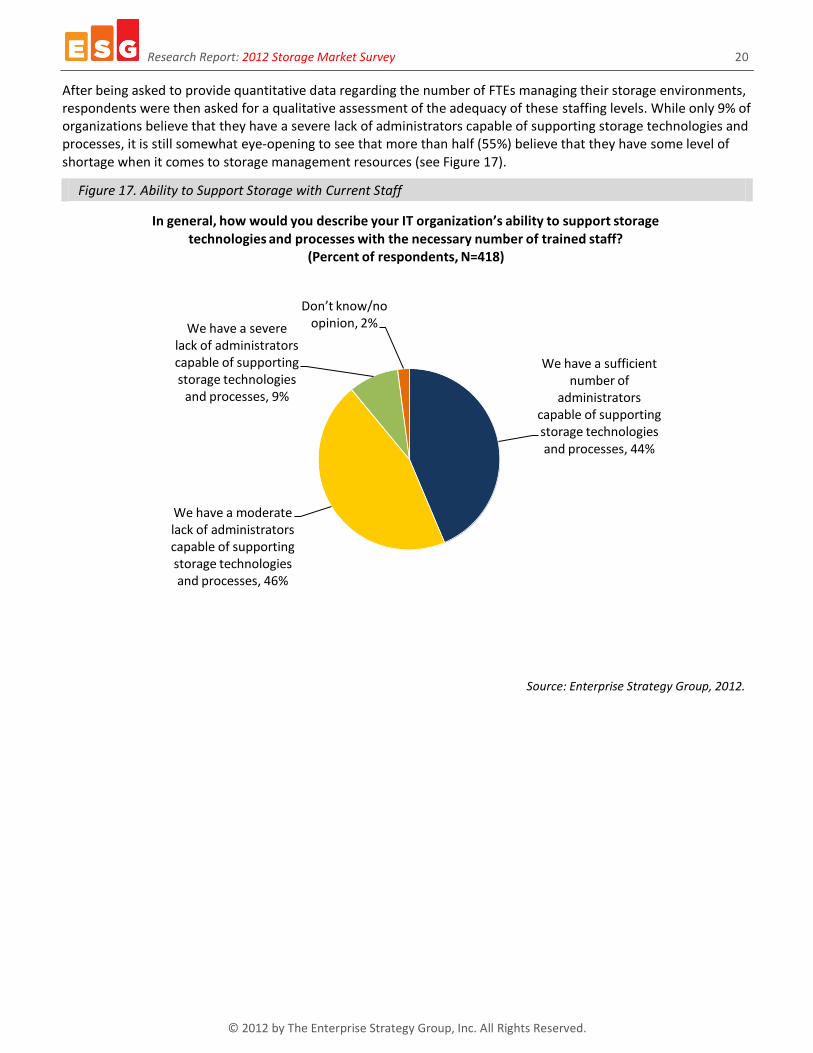

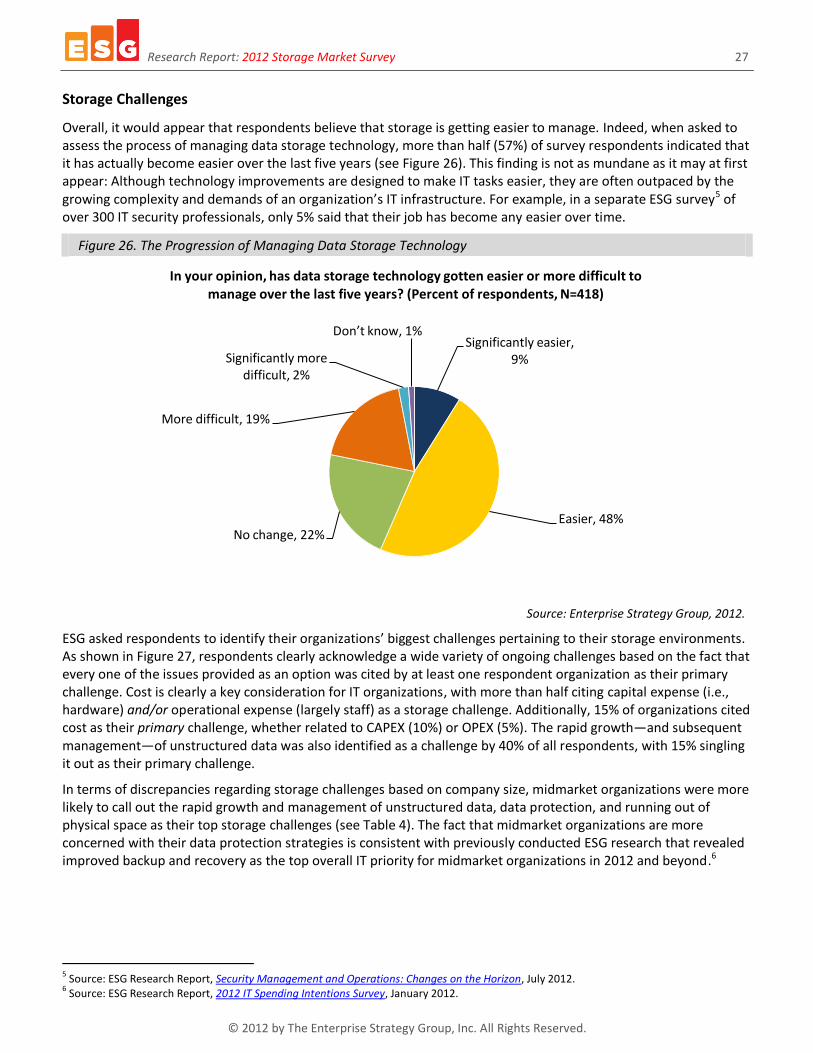

After being asked to provide quantitative data regarding the number of FTEs managing their storage environments, respondents were then asked for a qualitative assessment of the adequacy of these staffing levels. While only 9% of organizations believe that they have a severe lack of administrators capable of supporting storage technologies and processes, it is still somewhat eye-opening to see that more than half (55%) believe that they have some level of shortage when it comes to storage management resources (see Figure 17).

Figure 17. Ability to Support Storage with Current Staff

Source: Enterprise Strategy Group, 2012.

We have a sufficient number of

administrators capable of supporting storage technologies and processes, 44%

We have a moderate lack of administrators capable of supporting storage technologies and processes, 46%

We have a severe lack of administrators capable of supporting storage technologies

and processes, 9%

Don’t know/no opinion, 2%

In general, how would you describe your IT organization’s ability to support storage technologies and processes with the necessary number of trained staff?

(Percent of respondents, N=418)

Research Report: 2012 Storage Market Survey 21

© 2012 by The Enterprise Strategy Group, Inc. All Rights Reserved.

Storage Spending Trends

What Organizations Spent in 2012…

Respondents were asked about their organizations’ total 2012 budget for storage-related capital expenditures for any hardware, software, and/or services purchased over the course of the year. More than three-quarters (79%) of midmarket organizations reported spending less than $1 million on storage technology (see Figure 18). Conversely, nearly two-thirds (64%) of enterprise organizations allocated more than $1 million to storage-related investments in 2012, with one-quarter allotting at least $10 million for storage CAPEX.

Figure 18. 2012 Storage Budget Levels, by Company Size

Source: Enterprise Strategy Group, 2012.

Not surprisingly, there is a strong correlation between the amount of money an organization spent on storage hardware, software, and service in 2012 and the total amount of disk-based storage system capacity it has deployed. According to Figure 19, organizations with at least 500 TB of total disk-based storage system capacity were more than six times as likely as those with less than 100 TB (52% vs. 8%) to have allocated $5 million or more for storage-related capital expenditures. On the flip side, more than three-quarters (77%) of organizations with a disk-based storage footprint of less than 100 TB did not exceed the $1 million threshold in terms of their 2012 storage spending.

The role that data storage technology plays in an organization’s IT and business operations is also a good indicator of storage budget levels. One-third of respondents that believe effective storage strategies are critical to core applications/business processes and can lead to competitive advantage for their organization reported making investments of at least $5 million in storage technology in 2012 (see Figure 20). Of the organizations that consider storage to be necessary but don't think about it unless they need to add new capacity, 94% spent less than $1 million.

79%

12% 6%

1% 0% 0% 0% 2%

33% 27%

13% 10% 6% 6% 3% 3%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

Less than $1 million

$1 million to $4.999 million

$5 million to $9.999 million

$10 million to $24.999

million

$25 million to $49.999

million

$50 million to $99.999

million

$100 million or more

Don’t know

To the best of your knowledge, what is your organization’s total 2012 budget for all storage-related capital expenditures (including hardware, software, and services)?

(Percent of respondents)

Midmarket (100 to 999 employees, N=126) Enterprise (1,000 or more employees, N=235)

Research Report: 2012 Storage Market Survey 22

© 2012 by The Enterprise Strategy Group, Inc. All Rights Reserved.

Figure 19. 2012 Storage Budget Levels, by Total Installed Disk-Based Storage System Capacity

Source: Enterprise Strategy Group, 2012.

Figure 20. 2012 Storage Budget Levels, by Role of Data Storage Technology in IT and Business Operations

Source: Enterprise Strategy Group, 2012.

8%

34%

52%

16%

24%

33%

77%

43%

15%

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Less than 100 TB (N=166)

100 TB to 499 TB (N=80)

500 TB or more (N=100)

Total 2012 budget for all storage-related capital expenditures (including hardware, software, and services), by total installed disk-based storage system capacity.

(Percent of respondents)

$5 million or more $1 million to $4.999 million Less than $1 million

6%

24%

33%

24%

23%

94%

52%

44%

0% 20% 40% 60% 80% 100%

Afterthought – storage is necessary but we don't think about it much unless we need to add new capacity

(N=17)

Tactical – storage is an important part of our IT operations but it is not viewed as a strategic tool or

asset (N=152)

Strategic – effective storage strategies are critical to core applications/business processes and can lead to competitive advantage for our organization (N=176)

Total 2012 budget for all storage-related capital expenditures (including hardware, software, and services), by role of data storage technology in IT and business

operations. (Percent of respondents)

$5 million or more $1 million to $4.999 million Less than $1 million

Research Report: 2012 Storage Market Survey 23

© 2012 by The Enterprise Strategy Group, Inc. All Rights Reserved.

…And What They Expect to Spend in 2013

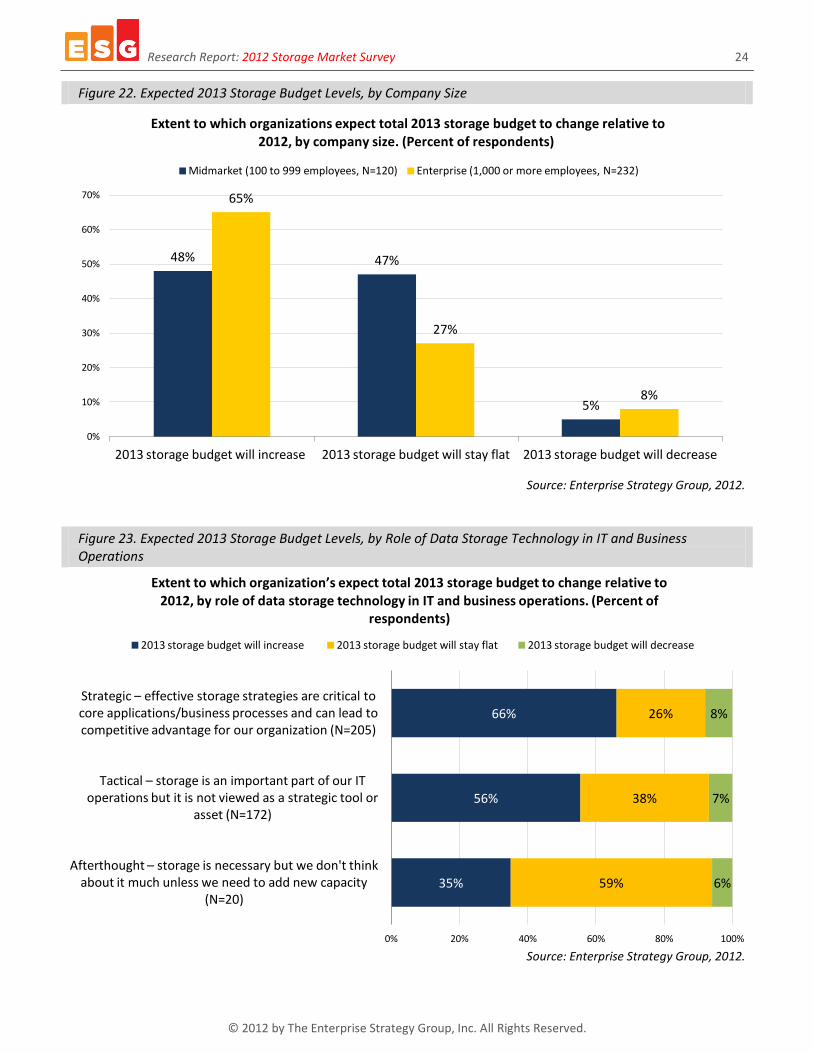

What is the outlook for 2013 storage budgets? Figure 21 reveals that 59% of respondents expect to see an increase in 2013 storage spending relative to 2012 levels. Those organizations planning to increase storage spending project an estimated average year-over-year budget increase of 5.41%, while ESG’s respondent base as a whole (i.e., organizations with increasing, flat, or declining storage budgets) expects an estimated average spending increase of 2.89% in 2013. A mere 6% expect to decrease their 2013 storage budgets, but not a single organization expects those cuts to exceed 10%. It is also worth noting that 2% of organizations had not begun their 2013 storage planning at the time of the survey.

Figure 21. Expected 2013 Storage Budget Levels

Source: Enterprise Strategy Group, 2012.

Nearly two-thirds (65%) of enterprise-class organizations expect to increase their 2013 storage spending levels compared to 48% of midmarket respondents (see Figure 22). Midmarket organizations, for their part, are more likely to hold the line, with nearly half (47%) reporting that 2013 storage budgets will remain flat relative to 2012. Overall, ESG estimates that the average expected net change in 2013 storage spending is 2.82% for midmarket organizations and 2.93% for enterprises.

According to Figure 23, organizations that consider data storage to be strategic to IT and business operations were nearly twice as likely as those characterizing the technology as an afterthought to be increasing 2013 storage budgets (66% vs. 35%). Overall, ESG estimates that organizations that view data storage technology as being strategic, tactical, or an afterthought will see a net year-over-year storage spending increase (2.82%, 2.53%, and 1.09%, respectively).

1%

14% 16%

12% 15%

33%

2% 2% 1% 1% 0% 2%

0%

5%

10%

15%

20%

25%

30%

35%

Increase more

than 10%

Increase 8% to 10%

Increase 5% to 7%

Increase 3% to 4%

Increase 1% to 2%

Stay flat Decrease 1% to 2%

Decrease 3% to 4%

Decrease 5% to 7%

Decrease 8% to 10%

Decrease more

than 10%

We have not

begun our

storage planning for 2013

at this point

At this point, to what extent do you believe your organization’s total 2013 storage budget will change relative to 2012? (Percent of respondents, N=361)

Research Report: 2012 Storage Market Survey 24

© 2012 by The Enterprise Strategy Group, Inc. All Rights Reserved.

Figure 22. Expected 2013 Storage Budget Levels, by Company Size

Source: Enterprise Strategy Group, 2012.

Figure 23. Expected 2013 Storage Budget Levels, by Role of Data Storage Technology in IT and Business Operations

Source: Enterprise Strategy Group, 2012.

48% 47%

5%

65%

27%

8%

0%

10%

20%

30%

40%

50%

60%

70%

2013 storage budget will increase 2013 storage budget will stay flat 2013 storage budget will decrease

Extent to which organizations expect total 2013 storage budget to change relative to 2012, by company size. (Percent of respondents)

Midmarket (100 to 999 employees, N=120) Enterprise (1,000 or more employees, N=232)

35%

56%

66%

59%

38%

26%

6%

7%

8%

0% 20% 40% 60% 80% 100%

Afterthought – storage is necessary but we don't think about it much unless we need to add new capacity

(N=20)

Tactical – storage is an important part of our IT operations but it is not viewed as a strategic tool or

asset (N=172)

Strategic – effective storage strategies are critical to core applications/business processes and can lead to competitive advantage for our organization (N=205)

Extent to which organization’s expect total 2013 storage budget to change relative to 2012, by role of data storage technology in IT and business operations. (Percent of

respondents)

2013 storage budget will increase 2013 storage budget will stay flat 2013 storage budget will decrease

Research Report: 2012 Storage Market Survey 25

© 2012 by The Enterprise Strategy Group, Inc. All Rights Reserved.

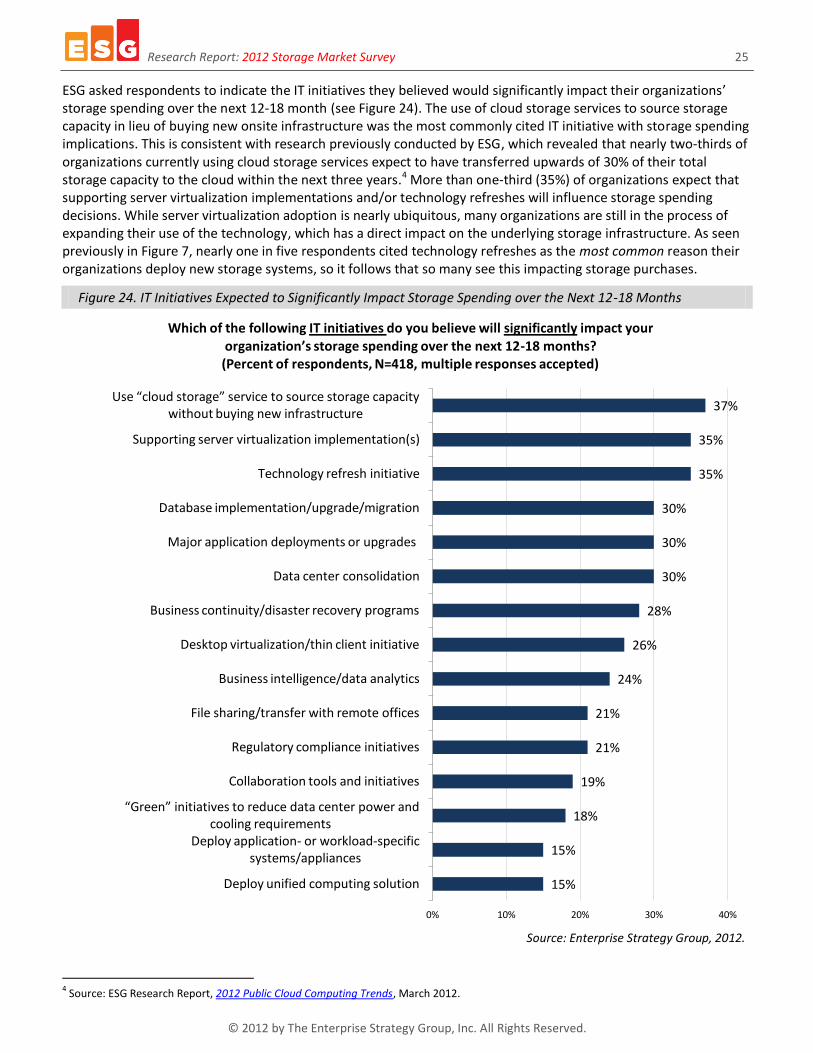

ESG asked respondents to indicate the IT initiatives they believed would significantly impact their organizations’ storage spending over the next 12-18 month (see Figure 24). The use of cloud storage services to source storage capacity in lieu of buying new onsite infrastructure was the most commonly cited IT initiative with storage spending implications. This is consistent with research previously conducted by ESG, which revealed that nearly two-thirds of organizations currently using cloud storage services expect to have transferred upwards of 30% of their total storage capacity to the cloud within the next three years.4 More than one-third (35%) of organizations expect that supporting server virtualization implementations and/or technology refreshes will influence storage spending decisions. While server virtualization adoption is nearly ubiquitous, many organizations are still in the process of expanding their use of the technology, which has a direct impact on the underlying storage infrastructure. As seen previously in Figure 7, nearly one in five respondents cited technology refreshes as the most common reason their organizations deploy new storage systems, so it follows that so many see this impacting storage purchases.

Figure 24. IT Initiatives Expected to Significantly Impact Storage Spending over the Next 12-18 Months

Source: Enterprise Strategy Group, 2012.

4 Source: ESG Research Report, 2012 Public Cloud Computing Trends, March 2012.

15%

15%

18%

19%

21%

21%

24%

26%

28%

30%

30%

30%

35%

35%

37%

0% 10% 20% 30% 40%

Deploy unified computing solution

Deploy application- or workload-specific systems/appliances

“Green” initiatives to reduce data center power and cooling requirements

Collaboration tools and initiatives

Regulatory compliance initiatives

File sharing/transfer with remote offices

Business intelligence/data analytics

Desktop virtualization/thin client initiative

Business continuity/disaster recovery programs

Data center consolidation

Major application deployments or upgrades

Database implementation/upgrade/migration

Technology refresh initiative

Supporting server virtualization implementation(s)

Use “cloud storage” service to source storage capacity without buying new infrastructure

Which of the following IT initiatives do you believe will significantly impact your organization’s storage spending over the next 12-18 months? (Percent of respondents, N=418, multiple responses accepted)

Research Report: 2012 Storage Market Survey 26

© 2012 by The Enterprise Strategy Group, Inc. All Rights Reserved.

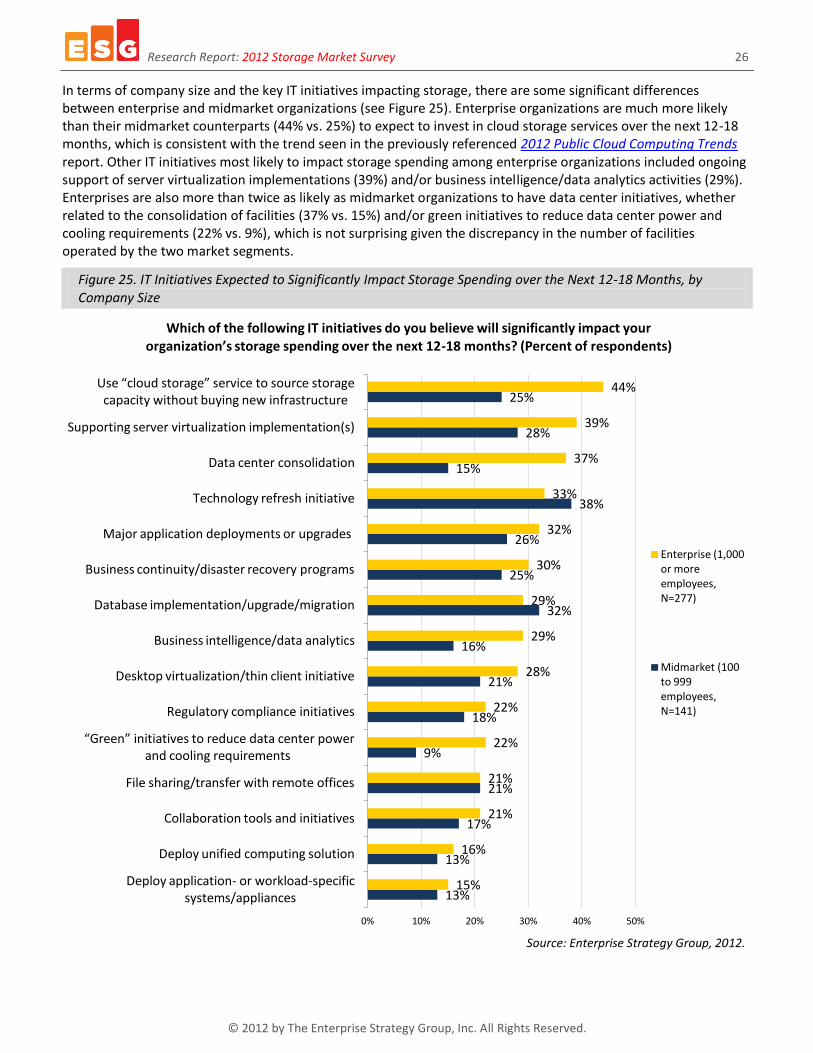

In terms of company size and the key IT initiatives impacting storage, there are some significant differences between enterprise and midmarket organizations (see Figure 25). Enterprise organizations are much more likely than their midmarket counterparts (44% vs. 25%) to expect to invest in cloud storage services over the next 12-18 months, which is consistent with the trend seen in the previously referenced 2012 Public Cloud Computing Trends report. Other IT initiatives most likely to impact storage spending among enterprise organizations included ongoing support of server virtualization implementations (39%) and/or business intelligence/data analytics activities (29%). Enterprises are also more than twice as likely as midmarket organizations to have data center initiatives, whether related to the consolidation of facilities (37% vs. 15%) and/or green initiatives to reduce data center power and cooling requirements (22% vs. 9%), which is not surprising given the discrepancy in the number of facilities operated by the two market segments.

Figure 25. IT Initiatives Expected to Significantly Impact Storage Spending over the Next 12-18 Months, by Company Size

Source: Enterprise Strategy Group, 2012.

13%

13%

17%

21%

9%

18%

21%

16%

32%

25%

26%

38%

15%

28%

25%

15%

16%

21%

21%

22%

22%

28%

29%

29%

30%

32%

33%

37%

39%

44%

0% 10% 20% 30% 40% 50%

Deploy application- or workload-specific systems/appliances

Deploy unified computing solution

Collaboration tools and initiatives

File sharing/transfer with remote offices

“Green” initiatives to reduce data center power and cooling requirements

Regulatory compliance initiatives