Schedules of Employer Allocations and Schedules of Pension ...

Reporting templates and schedules (participating entity)

General guidelines

Disclosures per reporting template should include all taxes attributed to taxable year 2012 irrespective of whether these were settled or paid in 2011 (advance payments) or 2013 (post settlement). Essentially, accrual basis will be adopted; hence taxes disclosed should correspond to reported amounts per audited financial statements. Reporting templates should present the total taxes/fees for the year with corresponding schedules disclosing the breakdown with the required level of detail (e.g. per frequency, receiving office) indicated in each. Reporting templates should be completed and provided no later than 30 June 2014. Based on accomplished reporting templates, the IA will communicate the results three (3) days thereafter (i.e., 3 July) and require participating entities to submit corresponding schedules for those taxes with noted differences. Schedules should be endorsed to the IA after two weeks or no later than 15 July 2014. During the said period, the IA will communicate proposed fieldwork dates to test reconciliation and examine sample documents. Please provide any relevant information for reconciliation process under remarks column. For example, participating entities may disclose if there were subsequent amendments made to initial filings and tax returns, or deficiency taxes (penalties, surcharges, interest) paid that may be included by government agencies in their respective reporting templates. Reporting templates should be signed by an authorized representative of senior management such as President and Chief Finance Officer. For queries and concerns, you may directly reach Isla Lipana & Co., Independent Administrator, or the PH-EITI Secretariat.

2 of 29 pages

1. Reporting templates

A. Bureau of Internal Revenue (BIR)

Type of tax Period covered (Cut-off date) Amount paid Remarks

Excise tax on minerals Jan–Dec 2012 80,488,050.03

Corporate income tax Jan–Dec 2012 2,329,562.99

Withholding tax Jan–Dec 2012 45,279,965.38

Foreign shareholder dividends

Profit remittance to principal

Royalties to claim owners

Improperly accumulated retained earnings tax (IAET)

B. Bureau of Customs (BOC)

Type of tax Period covered (Cut-off date) Amount paid Remarks

Customs duties Jan–Dec 2012 6,392,341.63

VAT on imported materials and equipment

Excise tax on imported goods (e.g. petroleum products)

3 of 29 pages

C. Philippine Ports Authority (PPA)

Type of tax Period covered (Cut-off date) Amount paid Remarks

Wharfage fees

D. Department agency

Mines and Geosciences Bureau (MGB)

Type of payment Period covered (Cut-off date) Amount paid Remarks

Royalty in mineral reservation

Occupation fees (only applicable to OG)

Others (e.g. penalties, fines, etc.)

E. Local government unit (LGUs)

i. Main taxes/fees

Type of taxes Period covered (Cut-off date) Amount paid Remarks

Local business tax (paid either in mine site or head office) Jan- Dec 2012 P14,376,627.12

Real property tax Jan- Dec 2012 P15,648,114.88

4 of 29 pages

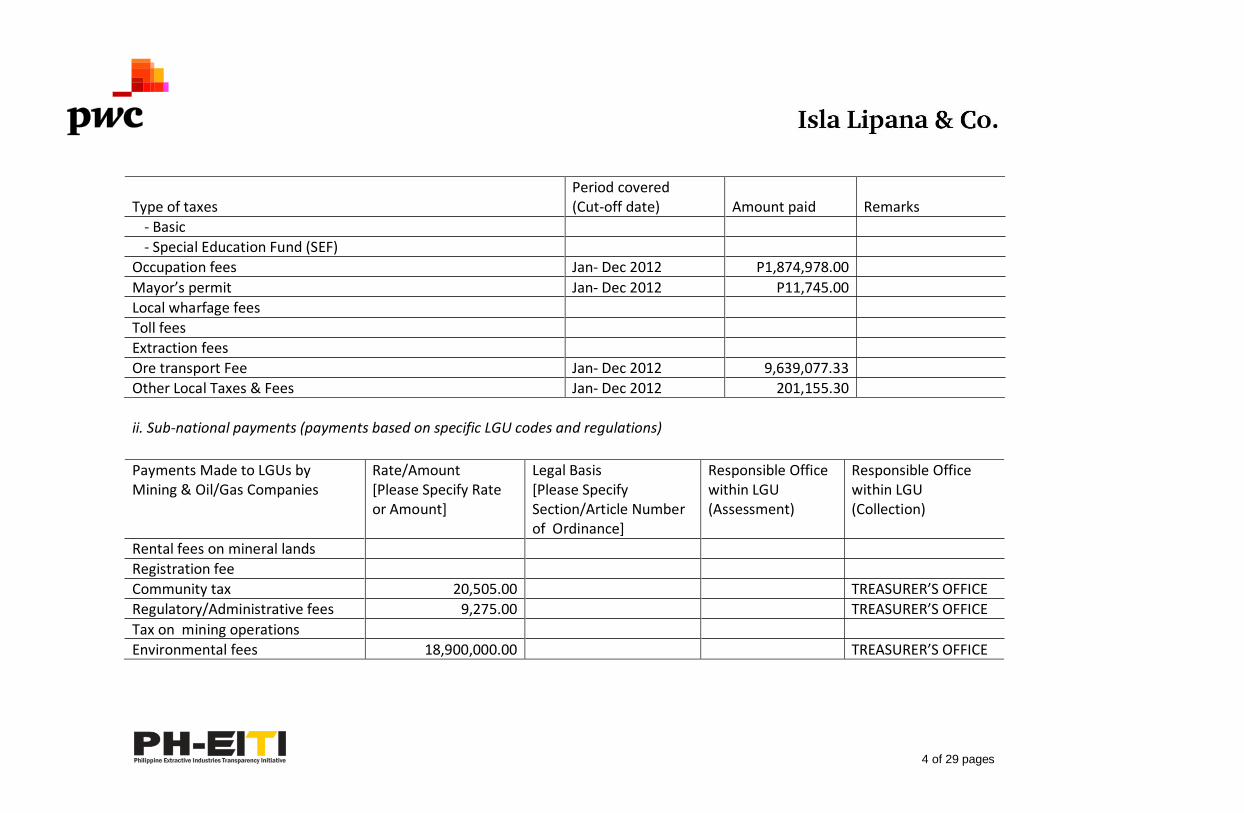

Type of taxes Period covered (Cut-off date) Amount paid Remarks

- Basic

- Special Education Fund (SEF)

Occupation fees Jan- Dec 2012 P1,874,978.00

Mayor’s permit Jan- Dec 2012 P11,745.00

Local wharfage fees

Toll fees

Extraction fees

Ore transport Fee Jan- Dec 2012 9,639,077.33

Other Local Taxes & Fees Jan- Dec 2012 201,155.30

ii. Sub-national payments (payments based on specific LGU codes and regulations)

Payments Made to LGUs by Mining & Oil/Gas Companies

Rate/Amount [Please Specify Rate or Amount]

Legal Basis [Please Specify Section/Article Number of Ordinance]

Responsible Office within LGU (Assessment)

Responsible Office within LGU (Collection)

Rental fees on mineral lands

Registration fee

Community tax 20,505.00 TREASURER’S OFFICE

Regulatory/Administrative fees 9,275.00 TREASURER’S OFFICE

Tax on mining operations

Environmental fees 18,900,000.00 TREASURER’S OFFICE

5 of 29 pages

Payments Made to LGUs by Mining & Oil/Gas Companies

Rate/Amount [Please Specify Rate or Amount]

Legal Basis [Please Specify Section/Article Number of Ordinance]

Responsible Office within LGU (Assessment)

Responsible Office within LGU (Collection)

Mine wastes & Tailing fees

Authority to Construct pollution devices

Other payments/ Imposed by the LGU (please list and enumerate all that apply)

F. Social funds (Mining)

1. Mandatory expenditures

Type Administrator

Basis of calculation Total actual expenditures

Remarks Reference Amount Amount spent Currency Period covered

Annual EPEP Company 3-5% of the mining and/or milling cost

19,867,000.00 29,838,414.00 PhP CY 2012

6 of 29 pages

Community Development Program

Company

CDP EP NO. XIII-031 Annual Accomplishment Report Covering January to December Total Exploration cost Total 10% Community Development 75% for the development of Host and Neighboring Communities 15% for the promotion of the public awareness and education on mining technology and Geosciences (DMTG) 10% for the Development of mining technology and Geosciences (DMTG)

2,040,400.00 204,040.00 153,030.00 30,606.00 20,404.00

204,040.00 153,030.00 30,606.00 20,404.00

PhP

CY 2012

7 of 29 pages

CDP EP NO. XIII-032 Annual Accomplishment Report Covering January to December Total Exploration cost Total 10% Community Development 75% for the development of Host and Neighboring Communities 15% for the promotion of the public awareness and education on mining technology and Geosciences (DMTG) 10% for the Development of mining technology and Geosciences (DMTG) CDP MPSA No. 343-2010-

1,693,400.00 169,340.00 127,005.00 25,401.00 16,934.00

139,705.50 127,005.00 12,700.50 0

8 of 29 pages

XIII-Guinhalinan, Javier, Barobo and Mahayahay, Lingig, Surigao dcel Sur Annual Accomplishment Report Covering January to December Total Exploration cost Total 10% Community Development 75% for the development of Host and Neighboring Communities 15% for the promotion of the public awareness and education on mining technology and Geosciences (DMTG) 10% for the Development of mining technology and Geosciences (DMTG) CDP MPSA No. 344-2010-

2,311,000.00 231,100.00 173,325.00 34,665.00 23,110.00

129,129.81 99,317.66 29,812.15 0

9 of 29 pages

XIII-Tambis, Barobo, Surigao del Sur Annual Accomplishment Report Covering January to December Total Exploration cost Total 10% Community Development 75% for the development of Host and Neighboring Communities 15% for the promotion of the public awareness and education on mining technology and Geosciences (DMTG) 10% for the Development of mining technology and Geosciences (DMTG)

2,540,011.00 254,001.10 190,500.83 38,100.17 25,400.11

223,601.00 190,500.83 18,100.17 15,000.00

10 of 29 pages

Social Development Management Program

Company SDMP ANNUAL ACCOMPLISHMENT REPORT Total IEC, MTGR & SDMP Budget CY 2012 (1.5% of Operating Cost) IEC Budget (15%) Mining Technology Geo research Budget (10%) SDMP Budget (75%)

20,461,278.00 3,069,191.70 2,046,127.80 15,345,958.50

15,831,668.62 1,765,730.26 0 14,065,938.36

PhP CY 2012

Safety and Health Program Safety Department

Annual Safety and Health Program

5,882,000.00 5,882,000.00 PhP C.Y. 2012

Environmental Work Program Company 10% of the exploration cost 9,605,000.00 10,264,000.00 PhP FY July 2011-June 2012 and July 2012-June 2013

Guidelines/Reminders

Administrator - Identify the entity that manages the fund (i.e. Company, government institutions/units, officers or representatives)

Basis of calculation - Describe how total amount of the fund was calculated (e.g. as percentage of revenue/operating costs, as specified in Memorandum of Agreement (MOA) or mining contract, etc.).

11 of 29 pages

Social Development Management Program (SDMP)

Program

Allocation per current mandate*

Mandated expenditures

Actual expenditures Period covered Remarks

Social Development & Management (host and neighboring communities) 75% 15,345,958.50 14,065,938.36 CY 2012

Mining Technology and Geosciences advancement 10% 2,046,127.80 0 CY 2012

Information, Education & Communication (IEC) 15% 3,069,191.70

1,765,730.26 CY 2012

Other information

Entities are requested to attach their 2012 Annual SDMP Report (as submitted to the MGB) as part of the completed reporting template. The said Report is expected to detail or enumerate expenditures or projects sourced from the SDMP.

Who is the implementer/contractor? Please see attached report.

Who are the partner organizations? Please see attached report.

2. Environmental funds

Fund Actual expenditures

Fund balance at the end of 2012 Remarks Type

Fund in the name of Administrator

Amount (in total) Currency

Period covered

12 of 29 pages

Fund Actual expenditures

Fund balance at the end of 2012 Remarks Type

Fund in the name of Administrator

Amount (in total) Currency

Period covered

Contingency Liability and Rehabilitation Fund

1.Mine rehabilitation fund PMC Final Mine Rehabilitation and Decommissioning Fund (FMRDF)

CLRF-SC /MRFC 10,000,000.00 Philippine Peso

Php 10,000,000.00 Deposited at DBP, San Francisco, Agusan del Sur

2.Mine monitoring trust fund

PMC MTF MRFC 150,000.00 Philippine Peso

Php 150,000.00 Deposited at DBP, San Francisco, Agusan del Sur

3.Rehabilitation cash fund PMC RCF MRFC 5,000,000.00 Philippine Peso

Php 5,000,000.00 Deposited at DBP, San Francisco, Agusan del Sur

Mine Waste and Tailings Reserve

CLRF-SC

Final Mine Rehabilitation and Decommissioning Fund

PMC FMRDF CLRF-SC /MRFC 10,000,000.00 Philippine Peso

Php 10,000,000.00 Deposited at DBP, San Francisco, Agusan del Sur

3. Other allowances

13 of 29 pages

Type Date paid

Basis of calculation Total actual expenditure

Remarks Reference Amount Amount Currency

Special allowance to claim owners and surface right holders

G. National Commission on Indigenous People (NCIP)

Type Administrator

Basis of calculation

Actual expenditures Remarks Reference Amount

Royalty for IPs 35,879,293.45

FPIC expenditure

Field Based Investigation Fee

H. Project registration

Indicate existing registration (e.g. BOI, PEZA)

Confirmation of fiscal incentives availed in 2012

Incentive Yes No Amount

Income tax

Duty free - importations

Real property

Any preferential tax rates applied

Others (to enumerate)

14 of 29 pages

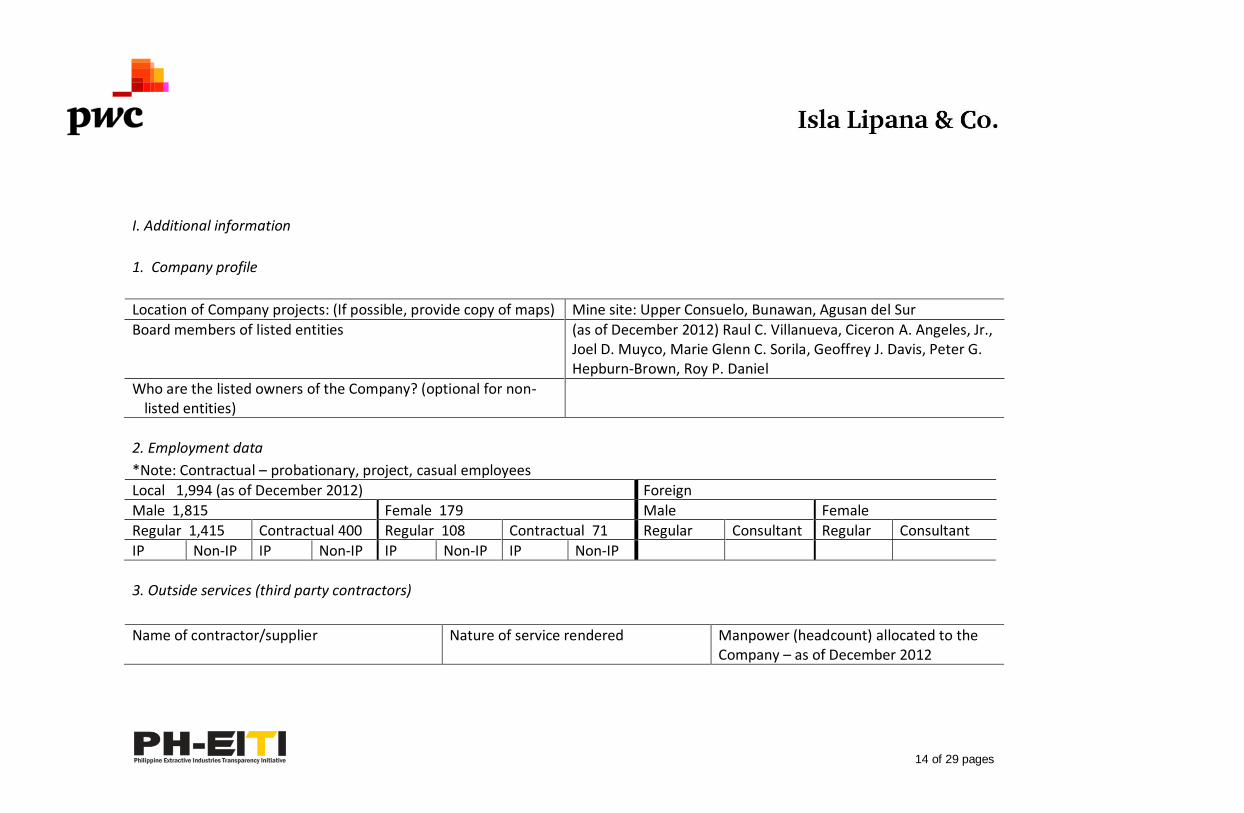

I. Additional information

1. Company profile

Location of Company projects: (If possible, provide copy of maps) Mine site: Upper Consuelo, Bunawan, Agusan del Sur

Board members of listed entities (as of December 2012) Raul C. Villanueva, Ciceron A. Angeles, Jr., Joel D. Muyco, Marie Glenn C. Sorila, Geoffrey J. Davis, Peter G. Hepburn-Brown, Roy P. Daniel

Who are the listed owners of the Company? (optional for non-listed entities)

2. Employment data

*Note: Contractual – probationary, project, casual employees

Local 1,994 (as of December 2012) Foreign

Male 1,815 Female 179 Male Female

Regular 1,415 Contractual 400 Regular 108 Contractual 71 Regular Consultant Regular Consultant

IP Non-IP IP Non-IP IP Non-IP IP Non-IP

3. Outside services (third party contractors)

Name of contractor/supplier Nature of service rendered Manpower (headcount) allocated to the Company – as of December 2012

15 of 29 pages

Shepherd Boy Service Contracting and Consultancy

Mine Contractor 1,335

Skaff Eximport & Services, Inc. Construction Contractor 210

SBF Philippines Drilling Resources Corporation Drilling Contractor 309

EEI Corporation Construction Contractor 74

Prochina Company Civil Works Contractor 35

Bussbarr Corporation Electrical Works Contractor 40

4. Gross production in metric tons (M/T) – as processed by affiliate company Mindanao Mineral Processing & Refining Corporation

Mineral Product

Local Export

Country of Destination

Company to whom minerals are exported

Related to mining company (Y/N)

Price (Average/ Range) Forex

Value

Volume Value Volume In PHP In US$

Gold Dore (kgs):

Contained gold (kgs)

1,644.93 7,278,982,835.66 HONGKONG HERAEUS 2,259.00

Contained silver (kgs)

Copper Concentrate (DMT)

697.02 29,417,704.45 HONGKONG HERAEUS 42.48

Contained gold (kgs)

Contained silver

16 of 29 pages

Mineral Product

Local Export

Country of Destination

Company to whom minerals are exported

Related to mining company (Y/N)

Price (Average/ Range) Forex

Value

Volume Value Volume In PHP In US$

(kgs)

Nickel Direct Shipping Ore (DMT)

Chromite Ore/ Concentrate (DMT)

Zinc Concentrate (DMT)

Iron Ore/ Concentrate (DMT)

Others: (Specify)

*For nickel DSO, kindly specify type of ore 5. Grants and donations

Recipient/s Donation Amount (monetary equivalent)

LGUs Typhoon Pablo donations (cash and building materials) to various municipalities in Compostela Valley

10,846,373.99

17 of 29 pages

and Caraga Region

6. Other withholding taxes

Type of withholding tax Cutoff date (Period covered) Amount remitted Remarks

ITW @ compensation & WAGES Jan-Dec 2012 36,212,401.79

ITW @ compensation & RENTAL

Other National taxes (royalty) Jan-Dec 2012 8,675,050.17

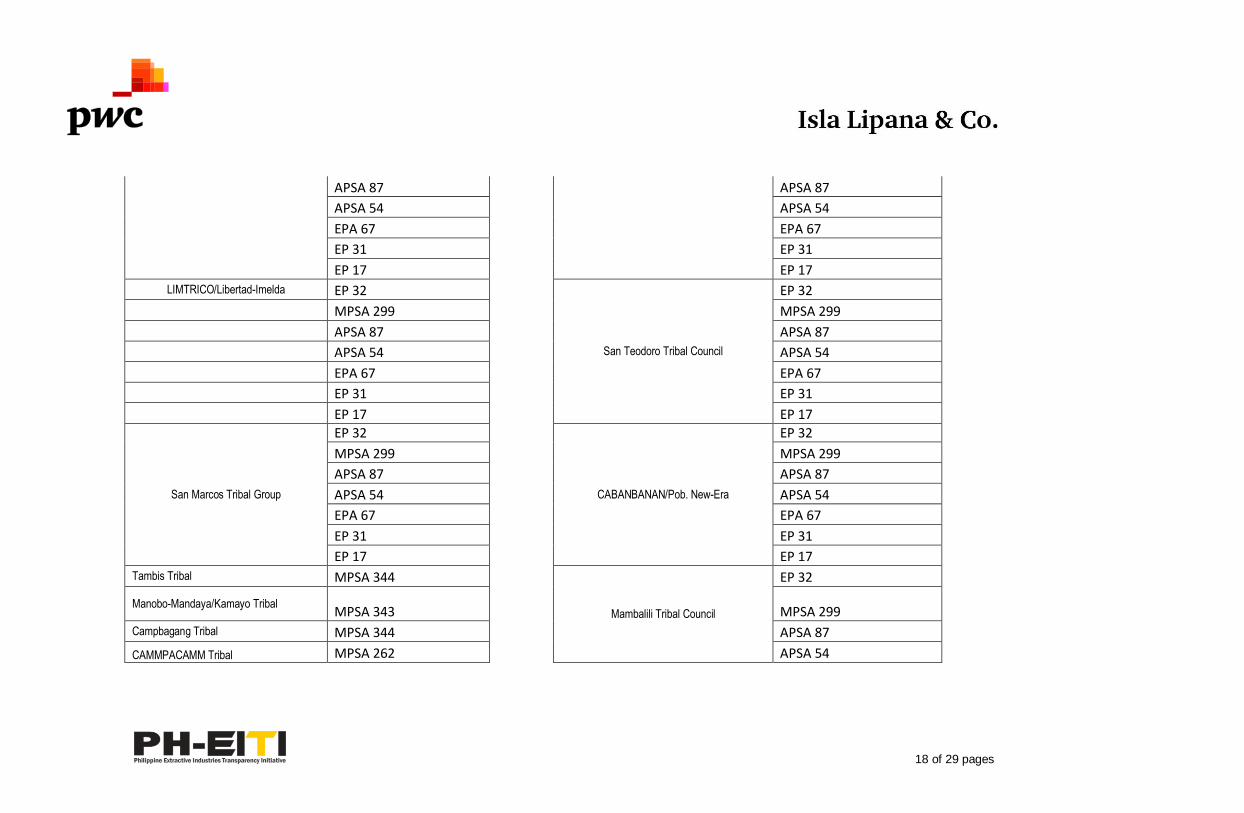

7. Enumeration of existing MOAs with IPs

IP GROUP Tenement Application

IP GROUP Tenement Application

BTCBDI/BMADMC

EP 32

San Andres Tribal Council

EP 32

MPSA 299

MPSA 299

APSA 87

APSA 87

APSA 54

APSA 54

EPA 67

EPA 67

EP 31

EP 31

EP 17

EP 17

BMTCE(Bunawan Brook) EP 32

COTAMPCO/Consuelo Tribal Group

EP 32

MPSA 299

MPSA 299

18 of 29 pages

APSA 87

APSA 87

APSA 54

APSA 54

EPA 67

EPA 67

EP 31

EP 31

EP 17

EP 17

LIMTRICO/Libertad-Imelda EP 32

San Teodoro Tribal Council

EP 32

MPSA 299

MPSA 299

APSA 87

APSA 87

APSA 54

APSA 54

EPA 67

EPA 67

EP 31

EP 31

EP 17

EP 17

San Marcos Tribal Group

EP 32

CABANBANAN/Pob. New-Era

EP 32

MPSA 299

MPSA 299

APSA 87

APSA 87

APSA 54

APSA 54

EPA 67

EPA 67

EP 31

EP 31

EP 17

EP 17

Tambis Tribal MPSA 344

Mambalili Tribal Council

EP 32

Manobo-Mandaya/Kamayo Tribal MPSA 343

MPSA 299

Campbagang Tribal MPSA 344

APSA 87

CAMMPACAMM Tribal MPSA 262

APSA 54

19 of 29 pages

CAMMPACAMM Tribal APSA 77

EPA 67

CAMMPACAMM Tribal MPSA 299

EP 31

Manobo-Mandaya/Kamayo Tribal MPSA 343

EP 17

Bitan-Agan Tribal MPSA 344

8. Details of CSR projects undertaken

List of activities undertaken, materials/supplies procured and facilities constructed during the year

If possible, to attach available reports submitted to regulatory bodies (e.g. MGB/DENR)

PARTICULARS AMOUNT (PhP)

ADOPT A FOREST PROJECT 212,336.68

ADOPT A MOUNTAIN FOREST PROJECT 2,947,858.05

ADOPT A SCHOOL 2,851,475.15

PHILSAGA HIGHSCHOOL 6,340,110.38

CORPORATE SOCIAL PROGRAMS – DAVAO REGION (financial assistance, medical assistance, solicitations) 11,067,733.85

CORPORATE SOCIAL PROGRAMS – CARAGA REGION (financial assistance, medical assistance, solicitations) 5,130,468.85

RUBBER TREES PROPAGATION 2,618,072.06

VERMICULTURE 898,048.08

PUBLIC RELATIONS COST 7,330,253.85

GRAND TOTAL 39,396,357.40

20 of 29 pages

Certification

I hereby certify the following:

I am the duly authorized and designated representative of Philsaga Mining Corporation with office address at C.P. Garcia Highway, Brgy. Sasa, Buhangin District, Davao City; and

All information disclosed and documents to be submitted in satisfaction of the EITI initiative are considered authentic and complete, and all statements and information provided therein are true and correct.

ATTY. RAUL C. VILLANUEVA/President 3 July 2014 Authorized representative Date

21 of 29 pages

2. Schedules

A. BIR

Type of tax

Cutoff date (Period covered) Date paid

Filing reference no.

Proof of payment

RDO/Bank branch receiving payment

Basis of calculation

Amount paid Remarks Reference Tax base

Tax rate

Excise tax on minerals JAN 12/29/2011 241200005425499 BIR-EFPS 3,487,196.41

JAN 1/31/2012 241200005567814 BIR-EFPS 1,405,454.98

FEB 1/31/2012 241200005567814 BIR-EFPS 2,094,545.02

FEB 3/1/2012 241200005681461 BIR-EFPS 3,500,000.00

FEB 3/6/2012 241200005695378 BIR-EFPS 1,013,040.31

MAR 3/13/2012 241200005736494 BIR-EFPS 5,064,925.13

MAR 4/16/2012 241200005833293 BIR-EFPS 2,204,322.01

APR 4/2/2012 241200005780055 BIR-EFPS 5,000,000.00

APR 4/26/2012 241200005880145 BIR-EFPS 1,852,823.87

MAY 4/26/2012 241200005880370 BIR-EFPS 5,000,000.00

MAY 5/30/2012 241200005988558 BIR-EFPS 1,372,188.88

JUNE 6/11/2012 241200006035498 BIR-EFPS 6,000,000.00

JUL 7/23/2012 241200006167145 BIR-EFPS 5,000,000.00

AUG 8/29/2012 241200006299336 BIR-EFPS 5,000,000.00

SEP 9/26/2012 241200006402279 BIR-EFPS 5,000,000.00

AUG-OCT 10/15/2012 241200006469987 BIR-EFPS 5,442,473.10

NOV 10/31/2012 241200006505850 BIR-EFPS 5,000,000.00

NOV 12/3/2012 241200006622426 BIR-EFPS 3,427,476.56

DEC 12/3/2012 241200006622426 BIR-EFPS 1,572,523.44

DEC 12/27/2012 241200006714054 BIR-EFPS 5,000,000.00

22 of 29 pages

DEC 1/14/2013 241300006787178 BIR-EFPS 1,431,041.11

DEC 1/14/2013 241300006787178 BIR-EFPS 5,620,039.21

Corporate income tax JUL11-June12 10/06/2012 121200006410334 BIR-EFPS 2,329,562.99

Withholding tax – 1601E JAN 2/13/2012 BIR-EFPS 4,160,577.68

FEB 3/14/2012 BIR-EFPS 2,141,697.06

MAR 4/16/2012 BIR-EFPS 5,252,923.38

APR 5/14/2012 BIR-EFPS 3,053,593.10

MAY 6/13/2012 BIR-EFPS 4,665,945.08

JUN 7/12/2012 BIR-EFPS 3,495,839.44

JULY 8/14/2012 BIR-EFPS 4,578,671.49

AUG 9/11/2012 BIR-EFPS 3,514,543.35

SEPT 10/12/2012 BIR-EFPS 3,934,523.13

OCT 11/13/2012 BIR-EFPS 4,154,785.40

NOV 12/14/2012 BIR-EFPS 2,268,932.26

DEC 1/14/2013 BIR-EFPS 4,257,934.01

Withholding tax - Compensation JAN 2/14/2012

BIR-EFPS

2,839,352.79

FEB 3/13/2012 BIR-EFPS 2,842,317.47

MAR 4/12/2012 BIR-EFPS 2,922,067.62

APR 5/14/2012 BIR-EFPS 3,232,781.00

MAY 6/11/2012 BIR-EFPS 3,288,611.00

JUN 7/12/2012 BIR-EFPS 3,077,626.00

JULY 8/14/2012 BIR-EFPS 3,381,673.33

AUG 9/13/2012 BIR-EFPS 3,077,724.00

SEPT 10/10/2012 BIR-EFPS 2,686,405.00

OCT 11/13/2012 BIR-EFPS 2,806,718.00

NOV 12/14/2012 BIR-EFPS 2,817,717.00

23 of 29 pages

DEC 1/14/2012 BIR-EFPS 2,834,995.79

Final tax JAN 2/14/2012 BIR-EFPS 723,122.35

FEB 3/12/2012 BIR-EFPS 647,543.36

MAR 4/11/2012 BIR-EFPS 712,386.22

APR 5/10/2012 BIR-EFPS 1,125,792.63

MAY 6/13/2012 BIR-EFPS 624,474.51

JUN 6/30/2012 BIR-EFPS 261,206.83

JULY 7/30/2012 BIR-EFPS 576,016.58

AUG 9/13/2012 BIR-EFPS 732,497.36

SEPT 10/9/2012 BIR-EFPS 1,027,291.70

OCT 11/13/2012 BIR-EFPS 607,372.41

NOV 12/4/2012 BIR-EFPS 825,892.70

DEC 1/14/2013 BIR-EFPS 784,349.33

Foreign shareholder dividends

Profit remittance to principal

Royalties to claim owners

Improperly accumulated retained earnings tax (IAET)

Guidelines/Reminders

Reference pertains to the basis of calculation used by the Company in determining tax to be paid. Tax base is the quantitative equivalent of said reference. Example as follows: Type of tax: Excise tax | Reference: Gross market value of shipments | Tax base: PHP XXX.XX

24 of 29 pages

B. BOC

Type of tax

Cutoff date (Period covered) Date paid

Filing reference no.

Proof of payment

BOC office (Port) receiving payment

Basis of calculation

Amount paid Remarks Reference

Tax base Tax rate

Customs duties JAN 68,490.04 Various transactions

FEB 101,818.00 Various transactions

MAR 153,054.50 Various transactions

APR 249,998.43 Various transactions MAY 160,468.91 Various transactions

JUN 903,744.67 Various transactions

JULY 372,140.06 Various transactions

AUG 390,820.02 Various transactions

SEPT 578,585.97 Various transactions

OCT 363,678.81 Various transactions

NOV 1,099,347.00 Various transactions

DEC 146,389.40 Various transactions

VAT on imported materials and equipment

Excise tax on imported goods (e.g. petroleum products)

Guidelines/Reminders

Filing reference no. refers to Import Entry and Internal Revenue Declaration No.

Reference primarily pertains to dutiable value and may include landed cost for duties, market value of imported acquisitions for VAT, and others. Tax base represents the equivalent monetary value of disclosed reference.

25 of 29 pages

C. PPA

Type of tax Date paid Proof of payment

Port Management Office (PMO)

Basis of calculation Amount paid Remarks Tax base Tax rate

Wharfage fees

Guidelines/Reminders

If possible, to disclose payments on a per PMO and port/terminal basis specifically for those operating at multi locations (provinces).

D. Department agency - MGB

Type of tax

Date paid Proof of payment

MGB office receiving payment

Basis of calculation Amount paid

Remarks

Reference Tax rate

Royalty in mineral reservation

Occupation fees

Others (e.g. penalties, fines, etc.)

For occupation fees, to disclose to which project this relates to under the remarks column to facilitate reconciliation with the MGB.

Likewise, if the entity is operating a number of projects across various locations, the reporting template should disclose royalty payments to each area.

26 of 29 pages

E. Local government unit

Type of tax Date paid Proof of payment LGU Receiving payment

Reference Tax base Tax rate Amount paid Remarks

Local business tax (paid either in mine site or head office) 1. Davao City Head

Office 2. Agusan del Sur Site

Office

01.20.2012 04.20.2012 07.16.2012 10.05.2012 02.09.2012

OR#4200737

DAVAO CITY BUNAWAN, AGUSAN DEL SUR

PhP72,255,842.00

P100,726.78 P100,726.78 P100,726.78 P100,726.78 P13,973,720

1ST QTR 2ND QTR 3RD QTR 4TH QTR

Real property tax Agusan del Sur Site Office

Various dates

BUNAWAN and ROSARIO, AGUSAN DEL SUR

P15,648,114.88

Occupation fees 1. Davao City Head Office 2. Agusan del Sur Site Office

01.20.2012

DAVAO CITY

P2,100.00

27 of 29 pages

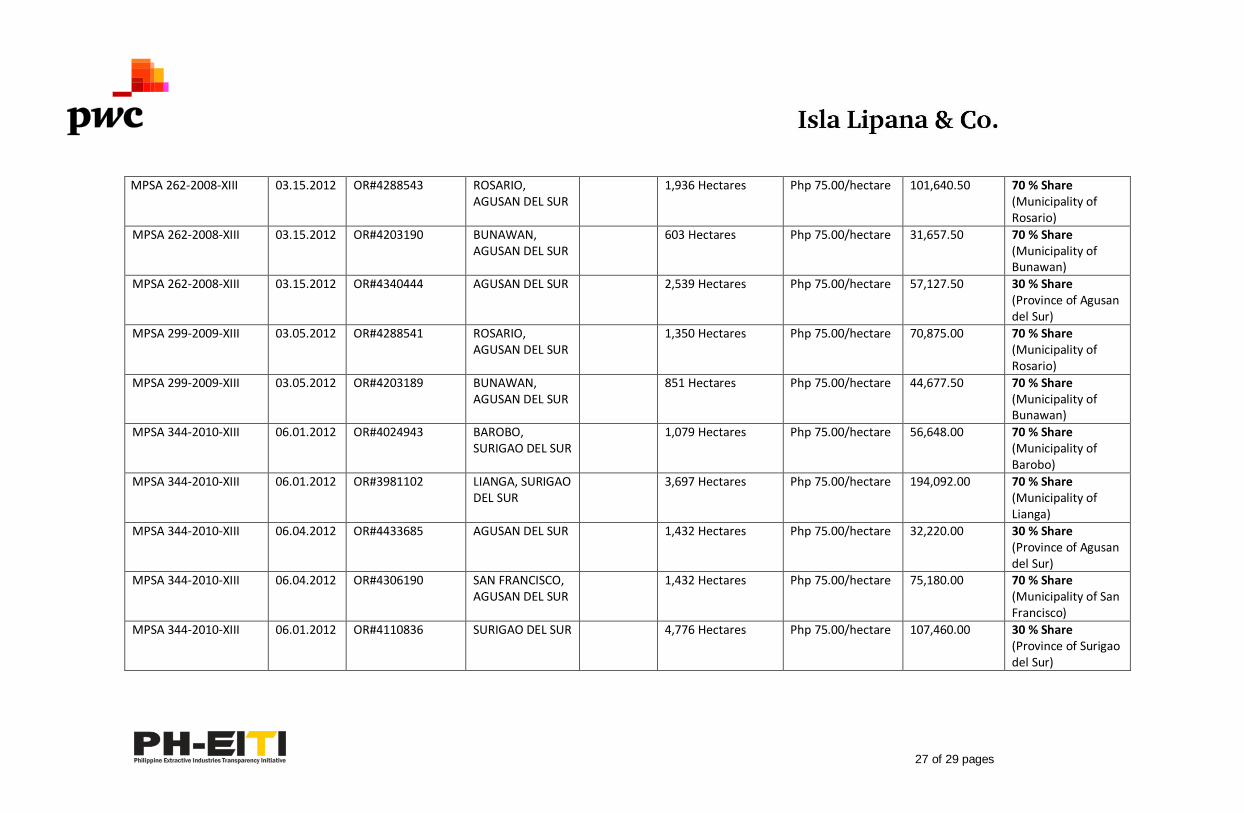

MPSA 262-2008-XIII 03.15.2012 OR#4288543 ROSARIO, AGUSAN DEL SUR

1,936 Hectares Php 75.00/hectare 101,640.50 70 % Share (Municipality of Rosario)

MPSA 262-2008-XIII 03.15.2012 OR#4203190 BUNAWAN, AGUSAN DEL SUR

603 Hectares Php 75.00/hectare 31,657.50 70 % Share (Municipality of Bunawan)

MPSA 262-2008-XIII 03.15.2012 OR#4340444 AGUSAN DEL SUR 2,539 Hectares

Php 75.00/hectare 57,127.50 30 % Share (Province of Agusan del Sur)

MPSA 299-2009-XIII 03.05.2012 OR#4288541 ROSARIO, AGUSAN DEL SUR

1,350 Hectares

Php 75.00/hectare 70,875.00 70 % Share (Municipality of Rosario)

MPSA 299-2009-XIII 03.05.2012 OR#4203189 BUNAWAN, AGUSAN DEL SUR

851 Hectares Php 75.00/hectare 44,677.50 70 % Share (Municipality of Bunawan)

MPSA 344-2010-XIII 06.01.2012 OR#4024943 BAROBO, SURIGAO DEL SUR

1,079 Hectares

Php 75.00/hectare 56,648.00 70 % Share (Municipality of Barobo)

MPSA 344-2010-XIII 06.01.2012 OR#3981102 LIANGA, SURIGAO DEL SUR

3,697 Hectares

Php 75.00/hectare 194,092.00 70 % Share (Municipality of Lianga)

MPSA 344-2010-XIII 06.04.2012 OR#4433685 AGUSAN DEL SUR 1,432 Hectares Php 75.00/hectare 32,220.00 30 % Share (Province of Agusan del Sur)

MPSA 344-2010-XIII 06.04.2012 OR#4306190 SAN FRANCISCO, AGUSAN DEL SUR

1,432 Hectares

Php 75.00/hectare 75,180.00 70 % Share (Municipality of San Francisco)

MPSA 344-2010-XIII 06.01.2012 OR#4110836 SURIGAO DEL SUR 4,776 Hectares

Php 75.00/hectare

107,460.00

30 % Share (Province of Surigao del Sur)

28 of 29 pages

MPSA 343-2010-XIII 06.01.2012 OR#4024944 BAROBO, SURIGAO DEL SUR

1,100 Hectares

Php 75.00/hectare 57,750 70 % Share (Municipality of Barobo)

MPSA 343-2010-XIII 06.01.2012 OR#3944370 LINGIG, SURIGAO DEL SUR

2,710 Hectares

Php 75.00/hectare 142,275.00 70 % Share (Municipality of Lingig)

MPSA 343-2010-XIII 06.01.2012 OR#3944370 SURIGAO DEL SUR 3.810 Hectares

Php 75.00/hectare

142,275.00

30 % Share (Province of Surigao del Sur)

EP No. 17-XIII 06.01.2012 OR#4320818 BUNAWAN, AGUSAN DEL SUR

3,133 Hectares Php 75.00/hectare 164,482.50 70 % Share (Municipality of Bunawan)

EP No. 17-XIII 06.04.2012 OR#4433683 AGUSAN DEL SUR 3,133 Hectares Php 75.00/hectare 70,492.50 30 % Share (Province of Agusan del Sur)

EP No. 31-XIII 06.01.2012 OR#4320819 BUNAWAN, AGUSAN DEL SUR

3,631 Hectares Php 75.00/hectare 190,627.50 70 % Share (Municipality of Bunawan)

EP No. 31-XIII 06.01.2012 OR#4439639 TRENTO, AGUSAN DEL SUR

348 Hectares Php 75.00/hectare 18,270.00 70 % Share (Municipality of Trento)

EP No. 31-XIII 06.04.2012 OR#4433682 AGUSAN DEL SUR 3,979 Hectares Php 75.00/hectare 89,527.50 30 % Share (Province of Agusan del Sur)

EP No. 32-XIII 06.01.2012 OR#4320817 BUNAWAN, AGUSAN DEL SUR

2,949 Hectares Php 75.00/hectare 154,822.50 70 % Share (Municipality of Bunawan)

EP No. 32-XIII 06.01.2012 OR#4439638 TRENTO, AGUSAN DEL SUR

99 Hectares Php 75.00/hectare 5,197.50 70 % Share (Municipality of Trento)

29 of 29 pages

EP No. 32-XIII 06.04.2012 OR#4433683 AGUSAN DEL SUR 3,048 Hectares Php 75.00/hectare 68,580.00 30 % Share (Province of Agusan del Sur)

Mayor’s permit and other regulatory fees

1. Davao City Head Office

2. Agusan del Sur Site

Office

01.20.2012 02.09.2012

OR# 0005892054A OR#4200737

DAVAO CITY BUNAWAN, AGUSAN DEL SUR

P4,745.00

P7,000.00

Local wharfage fees

Toll fees

Extraction fees