Report on standard-setting activities - Ian Carruthers, John Stanford, , IPSASB

24

IPSASB Update Ian Carruthers IPSASB Chair John Stanford Technical Director OECD 17 th Annual Accruals Symposium Paris 2 March 2017

-

Upload

oecd-governance -

Category

Government & Nonprofit

-

view

20 -

download

0

Transcript of Report on standard-setting activities - Ian Carruthers, John Stanford, , IPSASB

Page 1 | Proprietary and Copyrighted Information

IPSASB Update

Ian Carruthers

IPSASB Chair

John Stanford

Technical Director

OECD 17th Annual Accruals Symposium

Paris

2 March 2017

Page 2 | Proprietary and Copyrighted Information

IPSASB progress during 2016

Final pronouncements approved:

• Applicability of IPSASs

• Minor Improvements

• Impairment of Revalued Assets

• Update of IPSAS 25 Employee Benefits – IPSAS 39

• Public Sector Combinations - IPSAS 40

Consultation paper issued for comment:

• Public Sector Financial Instruments – monetary authority issues

Staff Paper issued:

• Emissions Trading Schemes

Consultations closed - responses being analysed:

• Update of Cash Basis IPSAS ED 61 (July 31st)

• Social Benefits Consultation Paper (January 31st) – ED being developed

Page 3 | Proprietary and Copyrighted Information

• Amalgamation or

Acquisition

• Control essential for

acquisition, but not

conclusive

• Economic substance

– Consideration

– Decision Making

• Carrying amounts for

amalgamations vs fair

value for acquisitions

IPSAS 40 Public Sector Combinations:

Classification

No Yes

No Yes

Does one party to the public sector

combination gain control of operations?

Is the economic substance of the public sector

combination that of an amalgamation?

Amalgamation Acquisition

Page 4 | Proprietary and Copyrighted Information

Current IPSASB work programme:

Key projects 2016 - 2018

Project Public sector

specific

IFRS

convergence

Social Benefits

Revenue & Non-Exchange Expenditure

Heritage

Leases

Financial Instruments

Public Sector Measurement (starting March 2017)

Infrastructure Assets (starting June 2017)

Cash Basis IPSAS (limited-scope update)

Page 5 | Proprietary and Copyrighted Information

Revenue and Non-Exchange Expenditure

• Current global literature on Revenue

– IPSAS 23 (Non-Exchange Revenue: Taxes and Transfers)

– IPSAS 9 (Revenue from Exchange Transactions)

– IPSAS 11 (Construction Contracts)

– IFRS 15 (Revenue from Contracts with Customers)

• Single CP to address need for common approach between

Non-Exchange Revenue and Expenditure (e.g. grants)

• Replace IPSASs 9 & 11 with IFRS 15-based standard

• Retain IPSAS 23-based standard - address application issues

• Assess extent to which public sector version of IFRS 15

performance obligation approach can help

Page 6 | Proprietary and Copyrighted Information

Category C

Converged IFRS 15

Sale of goods or services

on commercial terms

e.g. fees from

professional services

provided at market rates

Category B

Stretched Performance

Obligation Approach?

Satisfaction of

performance obligations

but does not include all

the characteristics of a

commercial based

transaction

e.g. fees in exchange for

the delivery of subsidised

health services

Category A

IPSAS 23 based

standard

No performance

obligations

e.g. taxes, transfers,

grants with no restrictions

over use

Transaction ‘categories’

Current classification

Potential re-classification

Description (in summary)

Example

Non-Performance

obligation

Performance Obligation

Exchange

Non-Exchange

Revenue reporting options

Page 7 | Proprietary and Copyrighted Information

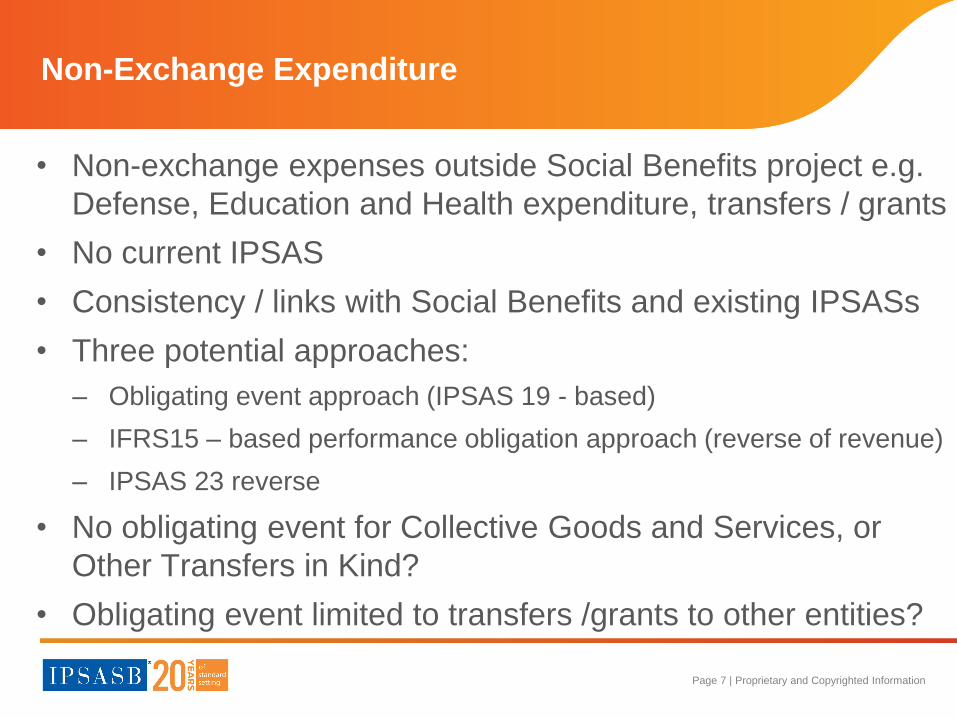

Non-Exchange Expenditure

• Non-exchange expenses outside Social Benefits project e.g.

Defense, Education and Health expenditure, transfers / grants

• No current IPSAS

• Consistency / links with Social Benefits and existing IPSASs

• Three potential approaches:

– Obligating event approach (IPSAS 19 - based)

– IFRS15 – based performance obligation approach (reverse of revenue)

– IPSAS 23 reverse

• No obligating event for Collective Goods and Services, or

Other Transfers in Kind?

• Obligating event limited to transfers /grants to other entities?

Page 8 | Proprietary and Copyrighted Information

Leases

• Existing IPSAS 13 based on IAS 17

• IFRS convergence project – responding to new IFRS 16

• Changes lessee recognition model

• More on balance sheet – fiscal impact?

• Retention of IPSAS 17 not an option – mixed groups

• Public Sector needs symmetry between lessee and lessor

accounting – lessor / lessee arrangements common e.g.

property

• Board view that IFRS 16 lessor accounting inappropriate for

public sector due to lack of symmetry

• ‘Right of use’ model under consideration for lessor accounting

Page 9 | Proprietary and Copyrighted Information

Lessor Accounting—Context of Development of

Options

Lessor accounting – Alternative options

IPSAS 32

Service Concessions:

Grantor

IPSASB

“Rules of the Road”

IPSASB

Conceptual Framework

New

IPSASB

lessor

guidance?

Consistency

with

IPSASB

literature

Page 10 | Proprietary and Copyrighted Information

Public Sector Measurement (1):

CF measurement bases

Assets Liabilities

Historical Cost Historical Cost

Current Value measures

• Market Value

• Replacement Cost

• Net Selling Price

• Value in Use

Current Value measures

• Market Value

• Cost of Fulfilment

• Cost of Release

• Assumption Price

Page 11 | Proprietary and Copyrighted Information

Public Sector Measurement (2)

• Combined impact on IPSASs of CF and IFRS 13:

– Service potential - need for entry-based values

– Existing measurement requirements not consistent with CF

– Fair value references inconsistent with IFRS 13 (exit-based)

• Other key issues:

– Transaction costs treatment (including borrowing costs)

– Consistency with GFS and IVSC guidance

– Further Implementation Guidance needed?

• Task Force to include GFS and IVSC representatives

• Preliminary analysis stage before deciding next steps

Page 12 | Proprietary and Copyrighted Information

Developing the next IPSASB Strategy and Work Plan

Multi-year Strategy (2019-2023), Work

Plan to implement/operationalize Strategy

PIC

advice

CAG input

Public consultation 2018

Stakeholder outreach 2017

Page 13 | Proprietary and Copyrighted Information

• Complexity of PFM landscape

• Coordination with other stakeholders?

• Relative balance between:

– Addressing public sector-specific issues?

– Maintaining (increasing?) IFRS convergence?

– Relationship with Government Finance Statistics?

– Improving communication of financial information?

• IPSASB’s role in relation to adoption and implementation?

• How do these demands fit with available resources?

• Development work during 2017

• Public consultation H1 2018 – Finalise H2 2018.

2019-2023 Strategy / Work Plan challenges

Page 14 | Proprietary and Copyrighted Information

Social Benefits: Project Timeline

• 2013

Project Reactivated

• 2015

CP Issued

• 2017

ED Expected

• 2018

IPSAS Expected

Page 15 | Proprietary and Copyrighted Information

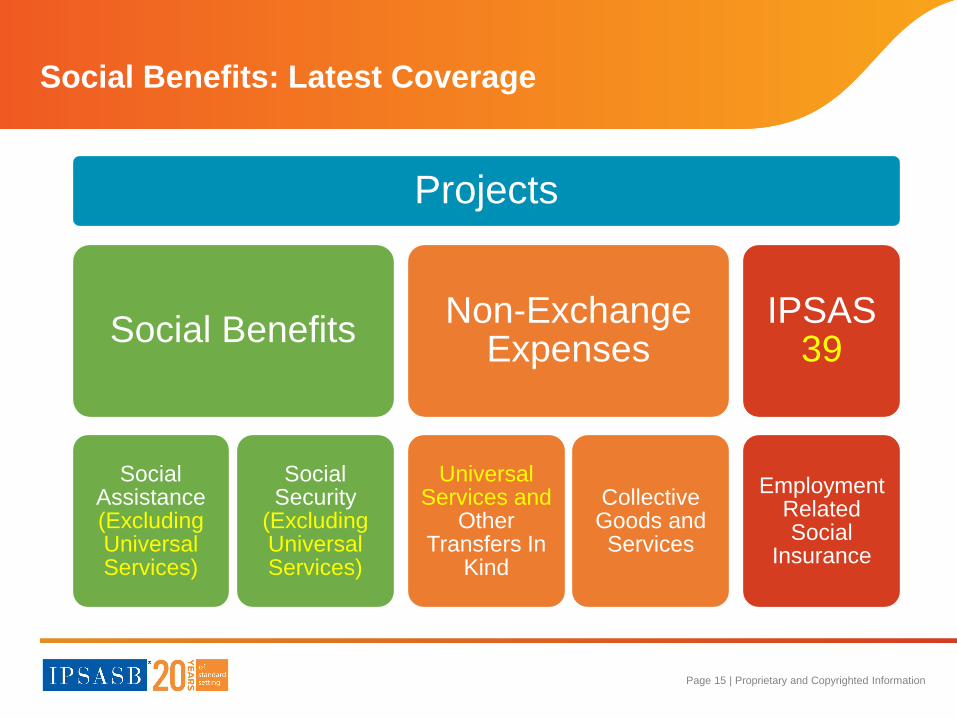

Social Benefits: Latest Coverage

Projects

Social Benefits

Social Assistance (Excluding Universal Services)

Social Security

(Excluding Universal Services)

Non-Exchange Expenses

Universal Services and

Other Transfers In

Kind

Collective Goods and Services

IPSAS 39

Employment Related Social

Insurance

Page 16 | Proprietary and Copyrighted Information

Option 1

• Obligating Event Approach

Option 2

• Social Contract Approach

Option 3

• Insurance Approach

CP: Recognition and Measurement Options

Page 17 | Proprietary and Copyrighted Information

Option 1

• Obligating Event Approach

Option 2

• Social Contract Approach

Option 3

• Insurance Approach

CP: Recognition and Measurement Options

Page 18 | Proprietary and Copyrighted Information

Social Benefits: Insurance Approach

Apply forthcoming IFRS on insurance contracts

• Intended to be fully funded from contributions

• Managed in the same way as an insurer manages insurance contracts

• Limited ability to change scheme

• Separate fund or earmarked asset

• Participants have enforceable rights

• Separate entity strengthens case

Use insurance approach when:

Page 19 | Proprietary and Copyrighted Information

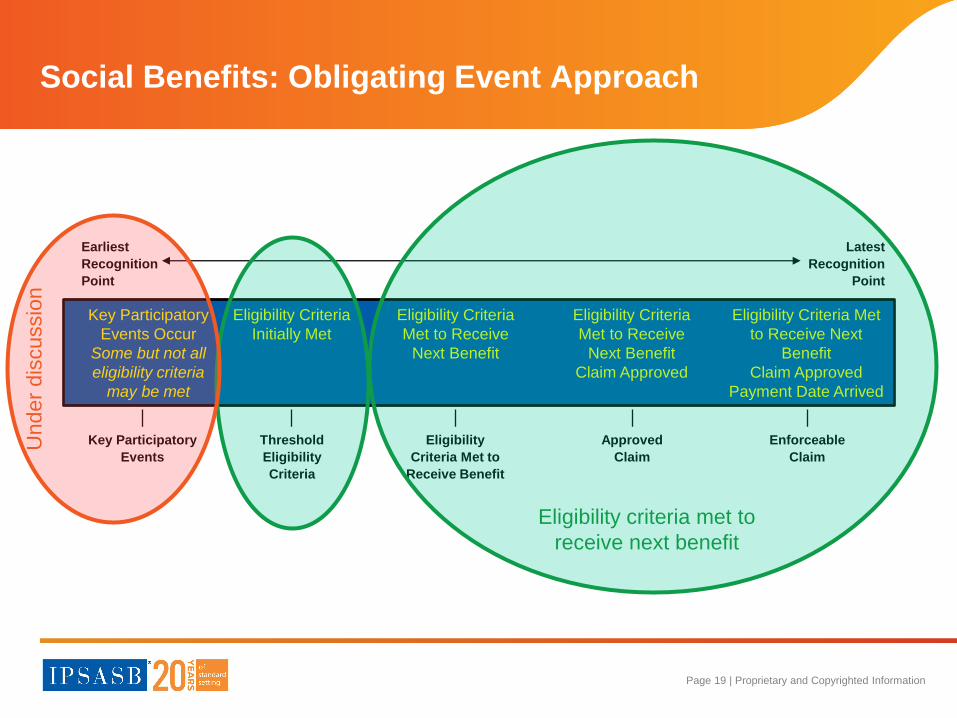

Social Benefits: Obligating Event Approach

Eligibility Criteria Met

to Receive Next

Benefit

Claim Approved

Payment Date Arrived

Eligibility Criteria

Met to Receive

Next Benefit

Claim Approved

Eligibility Criteria

Met to Receive

Next Benefit

Eligibility Criteria

Initially Met

Key Participatory

Events Occur

Some but not all

eligibility criteria

may be met

Key Participatory

Events

Eligibility

Criteria Met to

Receive Benefit

Threshold

Eligibility

Criteria

Approved

Claim

Enforceable

Claim

Earliest

Recognition

Point

Latest

Recognition

Point

Eligibility criteria met to

receive next benefit

Under

dis

cussio

n

Page 20 | Proprietary and Copyrighted Information

Heritage: Project Timeline

• 2015

Project Activated

• 2017

CP Projected

• 2018

ED Possible?

• 2020

IPSAS/Amendment/Other Output Possible ?

Page 21 | Proprietary and Copyrighted Information

Description of Heritage Items

• Items that are intended to be held indefinitely and

preserved for the benefit of present and future generations

because of their rarity and/or significance in relation, but

not limited, to their archeological, architectural,

agricultural, artistic, cultural, environmental, historical,

natural, scientific or technological features.

Page 22 | Proprietary and Copyrighted Information

Heritage Assets—Draft Consultation Paper

proposes:

• Heritage items can be assets

• Recognize heritage items if they meet recognition criteria:

– Asset definition

– Able to be measured

• Measurement bases:

– Historical cost

– Replacement cost

– Market value

• Acknowledge non-recognition and recognition at

symbolic/nominal value but question conceptual validity

Page 23 | Proprietary and Copyrighted Information

Heritage Liabilities—Draft Consultation Paper:

• Do heritage preservation intentions give rise to present

obligations and liabilities?

– Special characteristics of heritage items do not, of themselves,

result in a present obligation

– Entity is able to avoid an outflow of resources

– Do not recognize a liability based only on intentions

Page 24 | Proprietary and Copyrighted Information

Questions, discussion & further information

• Visit our webpage http://www.ipsasb.org/

• Or contact us by e-mail : IPSASB Chair: [email protected] Technical Director: [email protected]

![The Methodological Puzzle of Phenomenal Consciousness Ian … · 2020. 3. 19. · Carruthers [4] accepts that working memory is capacity limited but denies that cognitive access equates](https://static.fdocuments.in/doc/165x107/5fe274c00931cf048d46be15/the-methodological-puzzle-of-phenomenal-consciousness-ian-2020-3-19-carruthers.jpg)