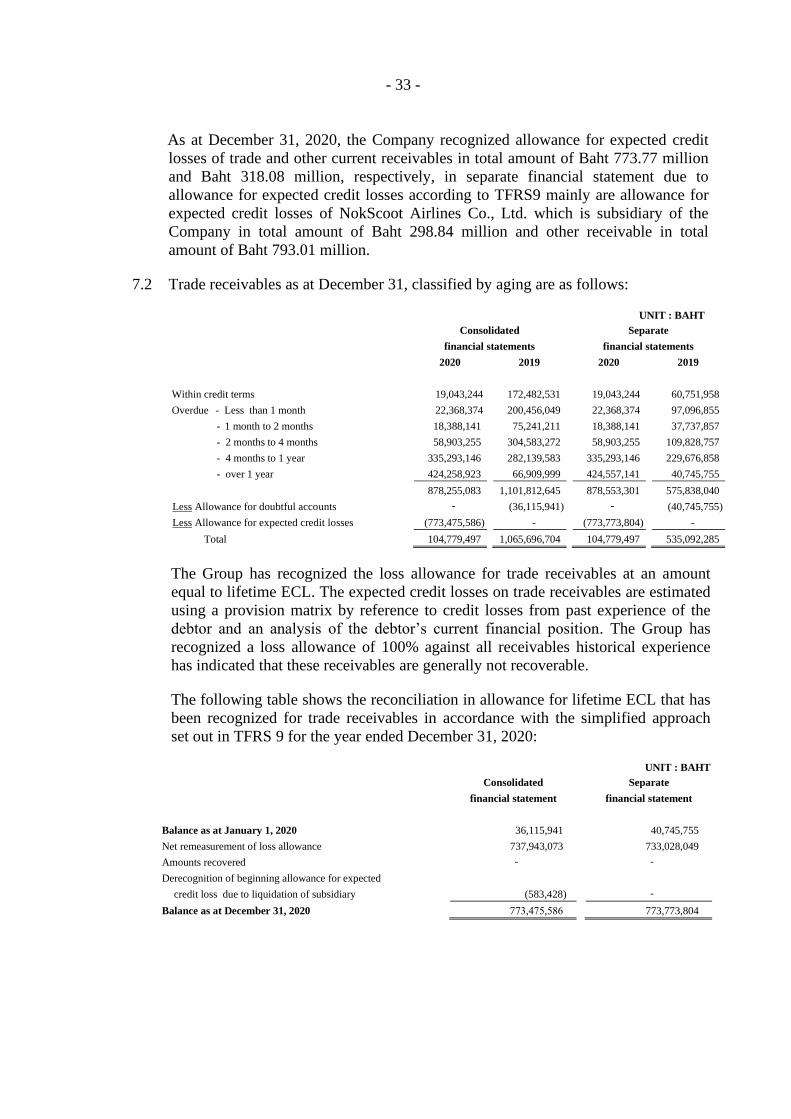

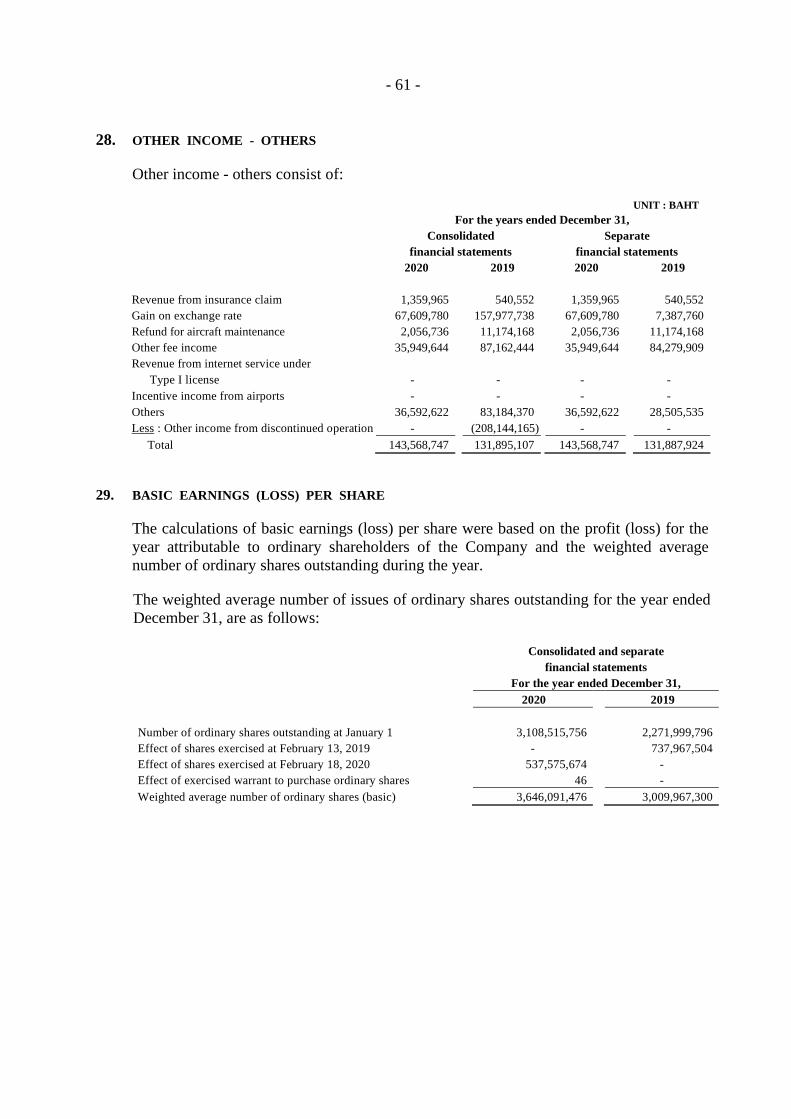

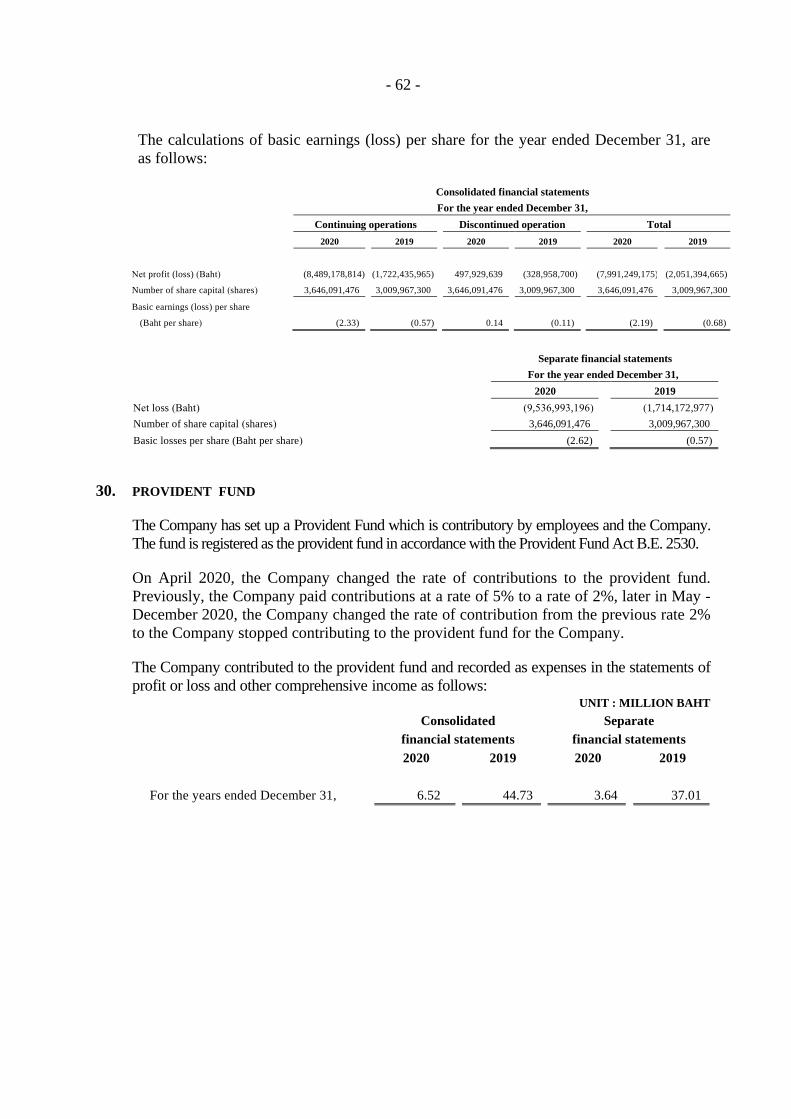

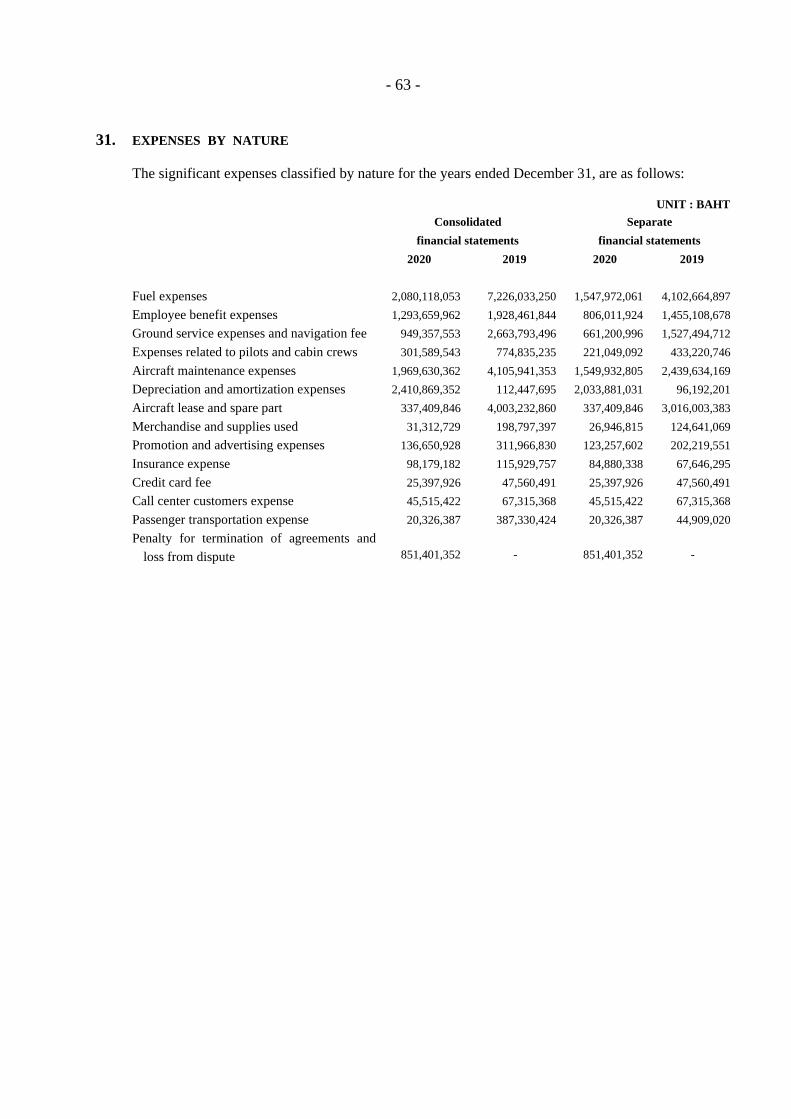

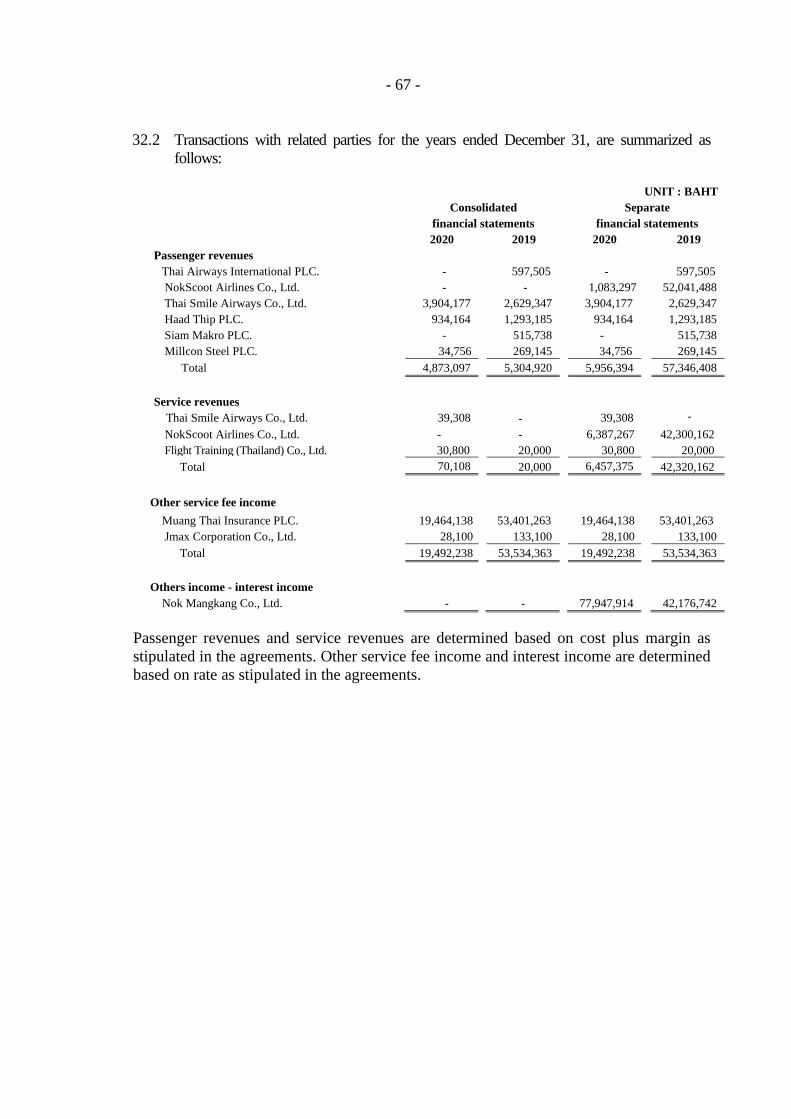

REPORT OF THE INDEPENDENT CERTIFIED PUBLIC …

94

REPORT OF THE INDEPENDENT CERTIFIED PUBLIC ACCOUNTANTS TO THE PLANNERS NOK AIRLINES PUBLIC COMPANY LIMITED Disclaimer of Opinion We were engaged to audit the consolidated financial statements of Nok Airlines Public Company Limited and its subsidiaries (“the Group”) and the separate financial statements of Nok Airlines Public Company Limited (“the Company”), which comprise the consolidated and separate statements of financial position as at December 31, 2020, and the related consolidated and separate statements of profit or loss and other comprehensive income, changes in shareholders’ equity and cash flows for the year then ended, and notes to the consolidated and separate financial statements, including a summary of significant accounting policies. We do not express an opinion on the accompanying consolidated and separate financial statements. Because of the significance of the matters described in the Basis for Disclaimer of Opinion section of our report, we have not been able to obtain sufficient appropriate audit evidence to provide a basis for an audit opinion on these consolidated and separate financial statements. Basis for Disclaimer of Opinion As we considered the conditions of uncertainty that had impact to the future outcomes of the Group’s and the Company’s operations as follows: 1. Lack of financial liquidity and debt default As disclosed in Note 1.2.1 to the financial statements regarding the financial position of the Group and the Company as at December 31, 2020, the Group had significant current liabilities in excess of current assets by Baht 16,194.30 million and had capital deficiency of Baht 8,002.15 million in the consolidated financial statements and the Company had current liabilities in excess of current assets by Baht 16,193.29 million and had capital deficiency of Baht 7,972.81 million in the separate financial statements. In the third quarter of year 2020, the Company was under the Automatic Stay status according to the Order to accept the rehabilitation petition of the Central Bankruptcy Court on July 30, 2020. As a result, the Company has triggered the event of default of outstanding liabilities and inability to pay liabilities when due, which consisted of trade account payables, short-term borrowings and lease liabilities. The ability to repay outstanding liabilities due within one year is depended on the creditors’ approval of the rehabilitation plan and the successful implementation of the rehabilitation plan.

Transcript of REPORT OF THE INDEPENDENT CERTIFIED PUBLIC …

REPORT OF THE INDEPENDENT CERTIFIED PUBLIC ACCOUNTANTS

TO THE PLANNERS

NOK AIRLINES PUBLIC COMPANY LIMITED

Disclaimer of Opinion

We were engaged to audit the consolidated financial statements of Nok Airlines Public

Company Limited and its subsidiaries (“the Group”) and the separate financial statements

of Nok Airlines Public Company Limited (“the Company”), which comprise the consolidated

and separate statements of financial position as at December 31, 2020, and the related

consolidated and separate statements of profit or loss and other comprehensive income, changes

in shareholders’ equity and cash flows for the year then ended, and notes to the consolidated and

separate financial statements, including a summary of significant accounting policies.

We do not express an opinion on the accompanying consolidated and separate financial

statements. Because of the significance of the matters described in the Basis for Disclaimer

of Opinion section of our report, we have not been able to obtain sufficient appropriate

audit evidence to provide a basis for an audit opinion on these consolidated and separate

financial statements.

Basis for Disclaimer of Opinion

As we considered the conditions of uncertainty that had impact to the future outcomes of

the Group’s and the Company’s operations as follows:

1. Lack of financial liquidity and debt default

As disclosed in Note 1.2.1 to the financial statements regarding the financial position of

the Group and the Company as at December 31, 2020, the Group had significant current

liabilities in excess of current assets by Baht 16,194.30 million and had capital deficiency

of Baht 8,002.15 million in the consolidated financial statements and the Company had

current liabilities in excess of current assets by Baht 16,193.29 million and had capital

deficiency of Baht 7,972.81 million in the separate financial statements.

In the third quarter of year 2020, the Company was under the Automatic Stay status

according to the Order to accept the rehabilitation petition of the Central Bankruptcy Court

on July 30, 2020. As a result, the Company has triggered the event of default of outstanding

liabilities and inability to pay liabilities when due, which consisted of trade account payables,

short-term borrowings and lease liabilities. The ability to repay outstanding liabilities

due within one year is depended on the creditors’ approval of the rehabilitation plan

and the successful implementation of the rehabilitation plan.

Deloitte Touche Tohmatsu Jaiyos Audit

ดีลอยท ์ทูช้ โธมทัสุ ไชยยศ สอบบญัชี

- 2 -

2. Effect of Coronavirus Disease 2019 Pandemic to the operations of the Group

As disclosed in Note 1.2.1 to the financial statements, the Coronavirus disease 2019

(“COVID-19”) pandemic is continuing to evolve, resulting in an economic slowdown

and adversely impacting most businesses and industries, especially aviation industry.

This affect to the Company and the subsidiary to close overseas routes since March 2020

onwards. For domestic routes, the Company normally operates with adjustments on

frequency of flights has been reduced as appropriate under the Emergency Situation Act.

This situation may have a significant impact on the flight plan, the financial position, the

ability to generate revenues and the current and future cash flows of the Group.

3. Entering into the rehabilitation process

As disclosed in Note 4 to the financial statements, on July 30, 2020, the Company

submitted a petition to enter into a business rehabilitation process and propose the

rehabilitation planners to the Central Bankruptcy Court under the Bankruptcy Act B.E. 2483.

The Central Bankruptcy Court issued an order to accept the rehabilitation petition of the

Company on the same day. On November 4, 2020, the Central Bankruptcy Court granted

the Company’s business rehabilitation petition and appointed the Planners as nominated

by the Company. Currently, the Company is under rehabilitation plan and the Planners

is in process of submitting the rehabilitation plan for requesting approval from the

creditors. The Company’s business plan, including flight plan and the ability to continue

as a going concern depends on several internal and external factors, economic condition

and aviation industry, including the creditors’ approval of the rehabilitation plan as well

as the successful implementation of the rehabilitation plan and the Company’s ability to

continue to operate the business.

The aforementioned situations in No. 1 to No. 3 have impact on and are inter-related

reflecting the material uncertainty to the ability to continue as going concern of the

Company which may affect valuation of significant assets and liabilities to the consolidated

and separate financial statements for the year ended December 31, 2020.

Emphasis of Matter

We draw attention to the following notes to the financial statements as follows:

1. Note 1.2.3 and 2.3 to the financial statements that on July 14, 2020, the Annual General

Meeting of Shareholders for the year 2020 of NokScoot Airlines Company Limited (the

“subsidiary”) approved the dissolution of the subsidiary. The subsidiary registered the

dissolution with the Department of Business Development on July 29, 2020. Currently,

the subsidiary is undergoing the liquidation process. The subsidiary appointed a liquidator

to manage the liquidation process and the determination of operating policy is subject to

direction by the liquidator. As a result, the Company lost control of such subsidiary. The Company derecognized the assets and liabilities of the subsidiary at their carrying

amounts, and non-controlling interests in the former subsidiary at their carrying amount

and recognized resulting difference as a gain on dissolution of the subsidiary in the

consolidated financial statements of the Group.

Deloitte Touche Tohmatsu Jaiyos Audit

ดีลอยท ์ทูช้ โธมทัสุ ไชยยศ สอบบญัชี

- 3 -

2. Note 2.6 to the financial statements that the Group has adopted the Group of Financial

Instruments Standards and Thai Financial Reporting Standard No. 16 “Leases” which

become effective for fiscal years beginning on or after January 1, 2020 The Group elected

to recognize the cumulative effect of initially applying such Standards as an adjustment

to the beginning balances of retained earnings of the reporting period. In addition, the

Group elected to adopt the Accounting Treatment Guidance on the temporary relief

measures for additional accounting alternatives to alleviate the impact of the COVID-19

outbreak issued by the Federation of Accounting Professions.

However, such matters did not affect our disclaimer of opinion.

Responsibilities of Management and Those Charged with Governance for the

Consolidated and Separate Financial Statements

Management is responsible for the preparation and fair presentation of the consolidated and

separate financial statements in accordance with Thai Financial Reporting Standards

(“TFRSs”), and for such internal control as management determines is necessary to enable

the preparation of consolidated and separate financial statements that are free from material

misstatement, whether due to fraud or error.

In preparing the consolidated and separate financial statements, management is responsible

for assessing the Group’s and the Company’s ability to continue as a going concern,

disclosing, as applicable, matters related to going concern and using the going concern

basis of accounting unless management either intends to liquidate the Group and the

Company or to cease operations, or has no realistic alternative but to do so.

Those charged with governance are responsible for overseeing the Group’s financial

reporting process.

Auditor’s Responsibilities for the Audit of the Consolidated and Separate Financial

Statements

Our responsibility is to conduct an audit of the consolidated and separate financial

statements in accordance with Thai Standards on Auditing and to issue an auditor's report.

However, because of the matters described in the Basis for Disclaimer of Opinion section

of our report, we were not able to obtain sufficient appropriate audit evidence to provide a

basis for an audit opinion on these financial statements.

Deloitte Touche Tohmatsu Jaiyos Audit

ดีลอยท ์ทูช้ โธมทัสุ ไชยยศ สอบบญัชี

- 4 -

We are independent of the Group in accordance with the Federation of Accounting Professions’

Code of Ethics for Professional Accountants together with the ethical requirements that are

relevant to the audit of the consolidated and separate financial statements, and we have

fulfilled our other ethical responsibilities in accordance with these requirements.

Dr. Suphamit Techamontrikul

Certified Public Accountant (Thailand)

BANGKOK Registration No. 3356

August 31, 2021 DELOITTE TOUCHE TOHMATSU JAIYOS AUDIT CO., LTD.

Notes

2020 2019 2020 2019

ASSETS

CURRENT ASSETS

Cash and cash equivalents 5.1 1,405,561,027 1,233,787,384 1,404,419,500 362,394,166

Current investments 6 - 42,878,939 - 42,261,195

Current investments in financial assets 6 541,235,949 - 541,235,949 -

Trade and other current receivables 7.1 255,160,170 2,493,338,355 256,943,929 1,036,373,329

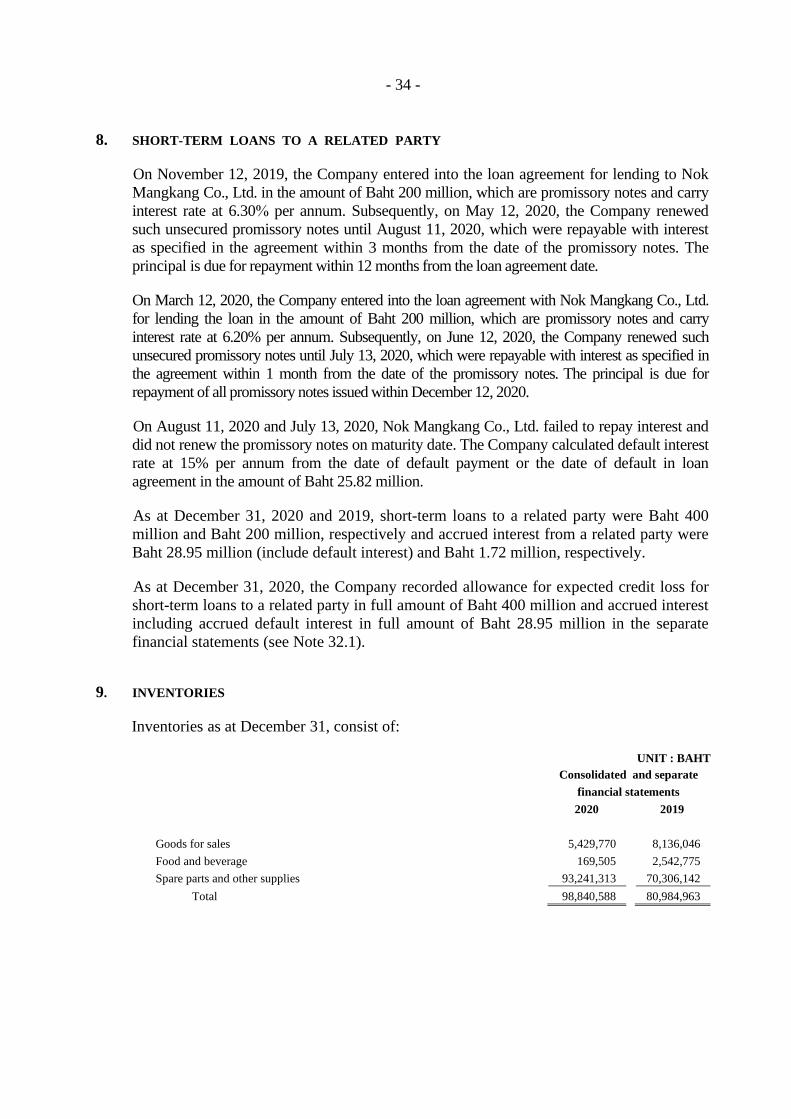

Short-term loans to a related party 8 - - - 200,000,000

Inventories 9 98,840,588 80,984,963 98,840,588 80,984,963

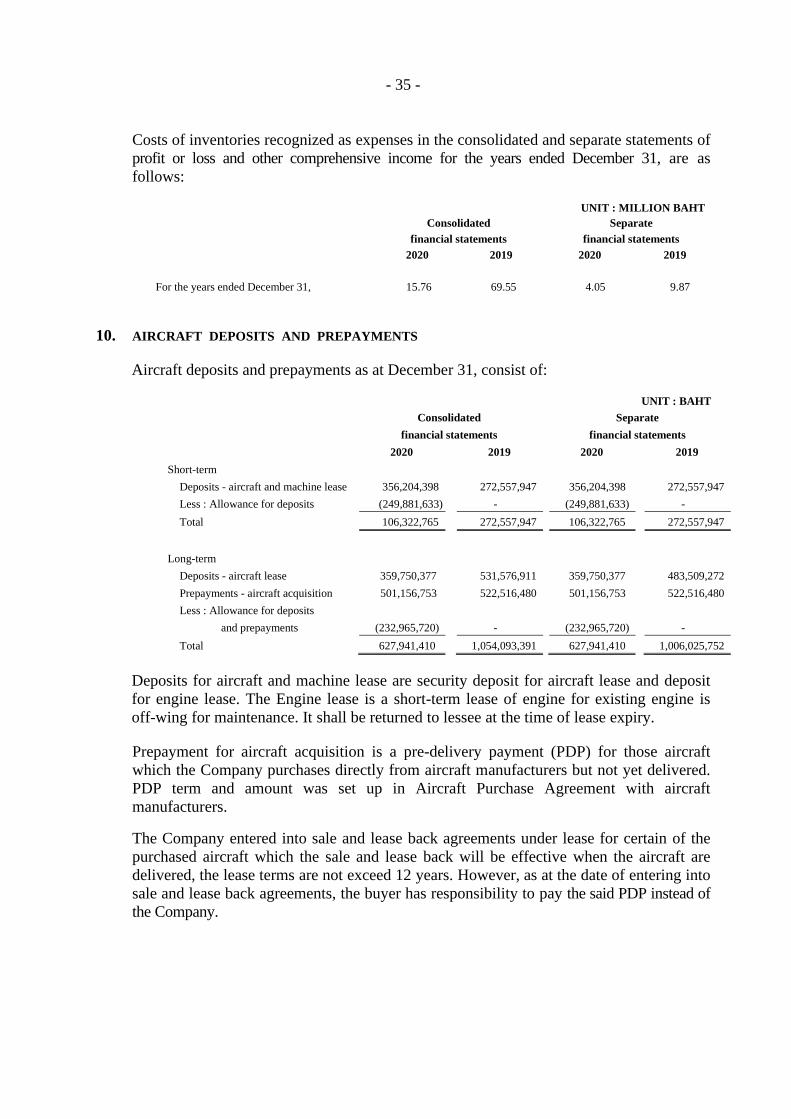

Short-term aircraft deposits and prepayments 10 106,322,765 272,557,947 106,322,765 272,557,947

Other current assets 175,456,342 123,046,016 175,362,853 62,844,945

Total Current Assets 2,582,576,841 4,246,593,604 2,583,125,584 2,057,416,545

NON-CURRENT ASSETS

Deposits at bank pledged as collateral 33.4 110,246,299 1,153,058,005 110,246,299 960,659,498

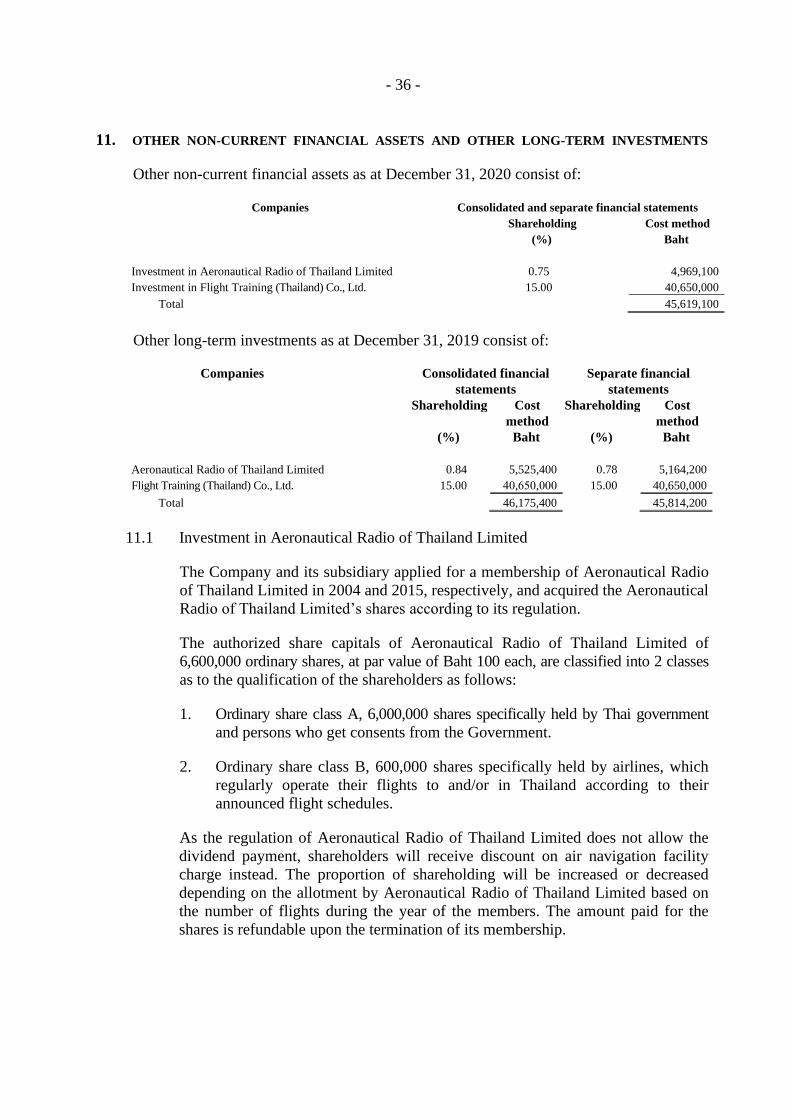

Other non-current financial assets 11 45,619,100 - 45,619,100 -

Investments in subsidiaries 12 - - 99,990 4,999,990

Investment in joint venture 14 - 8,119,200 28,420,554 28,420,554

Other long-term investments 11 - 46,175,400 - 45,814,200

Long-term loans to a related party 15 - - - 1,460,000,000

Maintenance reserve 22.1 6,292,715,783 8,342,408,284 6,292,715,783 5,650,730,869

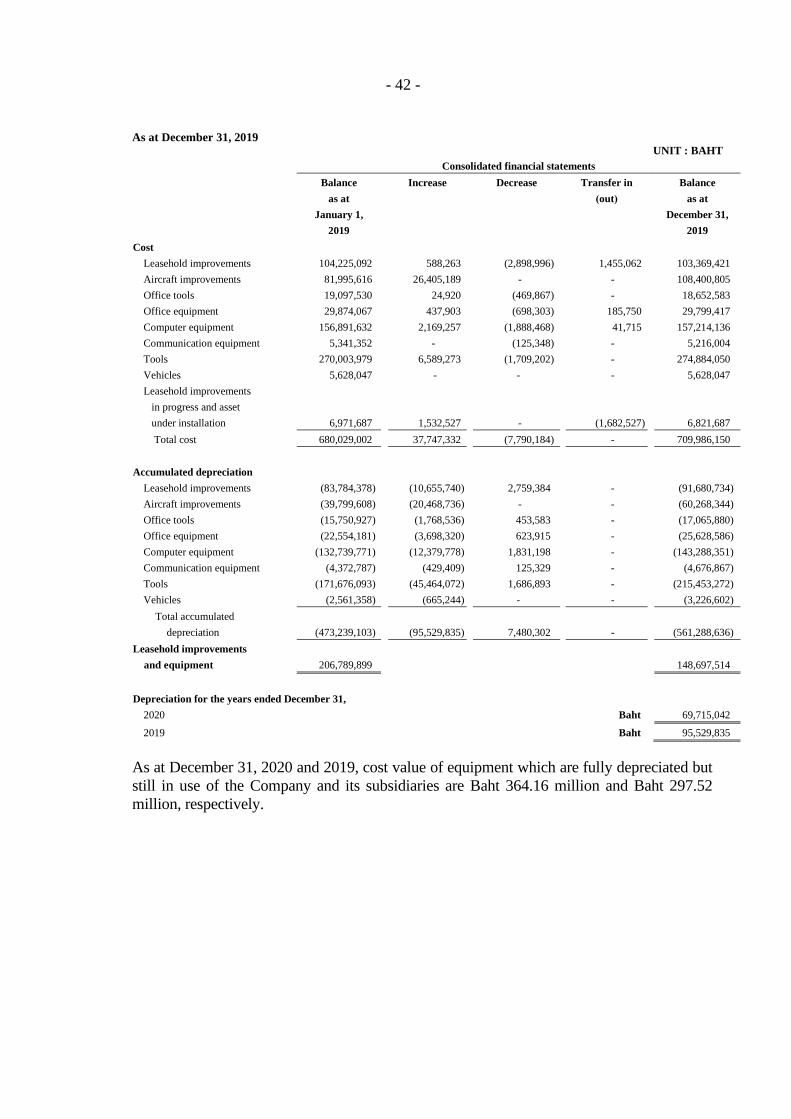

Leasehold improvements and equipment 16 66,442,758 148,697,514 66,442,758 115,762,339

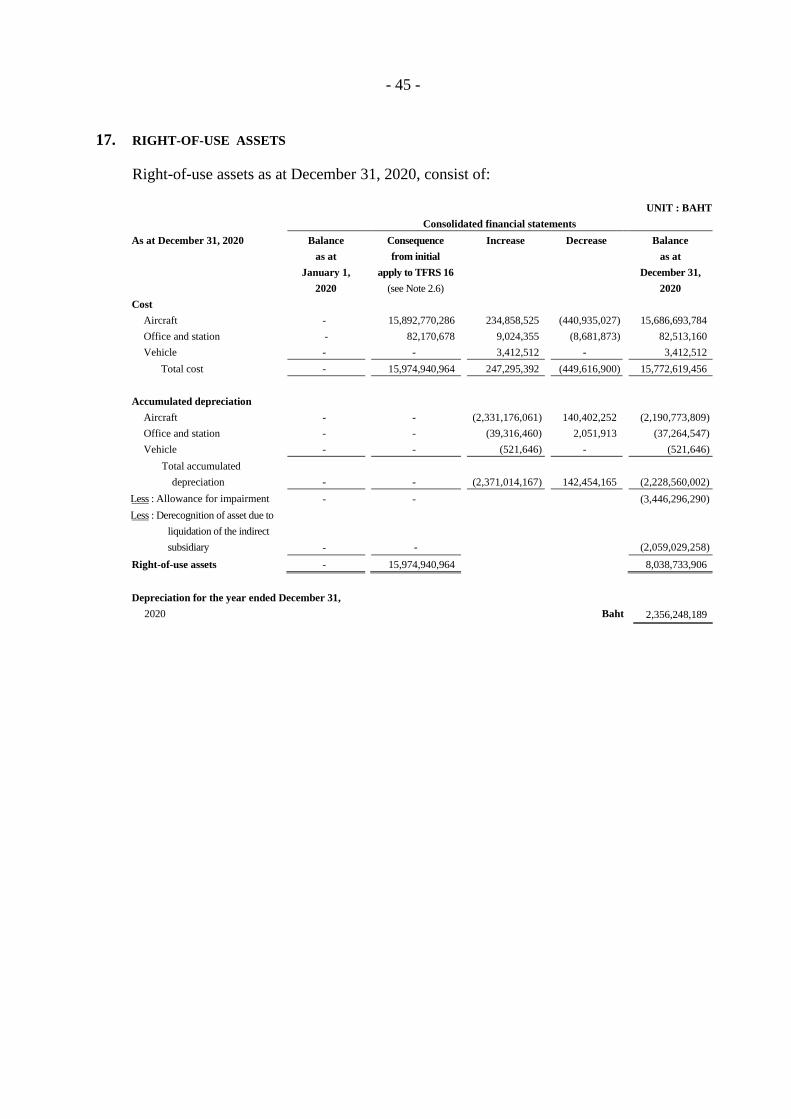

Right-of-use assets 17 8,038,733,906 - 8,038,733,906 -

Intangible assets 18 27,432,477 48,916,514 27,244,357 36,269,947

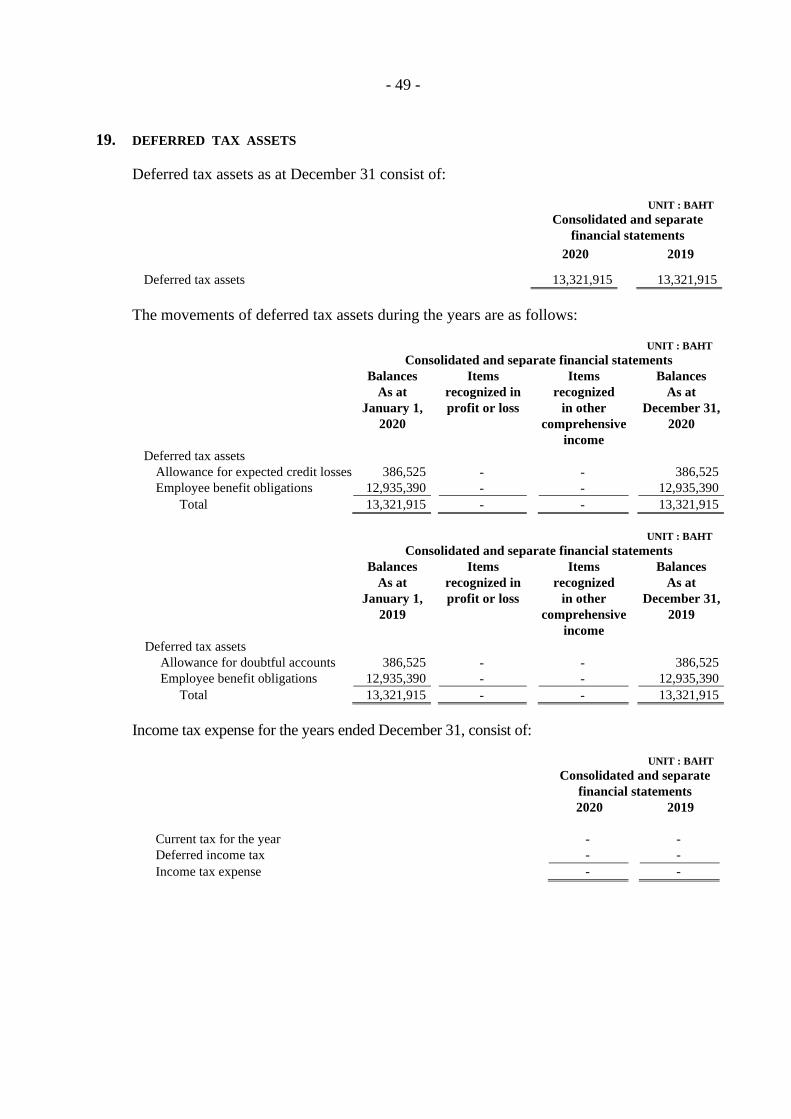

Deferred tax assets 19 13,321,915 13,321,915 13,321,915 13,321,915

Long-term aircraft deposits and prepayments 10 627,941,410 1,054,093,391 627,941,410 1,006,025,752

Other non-current assets 89,894,181 109,571,430 89,894,181 158,875,441

Total Non-current Assets 15,312,347,829 10,924,361,653 15,340,680,253 9,480,880,505

TOTAL ASSETS 17,894,924,670 15,170,955,257 17,923,805,837 11,538,297,050

Notes to the financial statements form an integral part of these statements

...........................................................

Mr. Tai Chong Yih (Director) Mr. Wutthiphum Jurangkool (Director)

FINANCIAL STATEMENTS FINANCIAL STATEMENTS

...........................................................

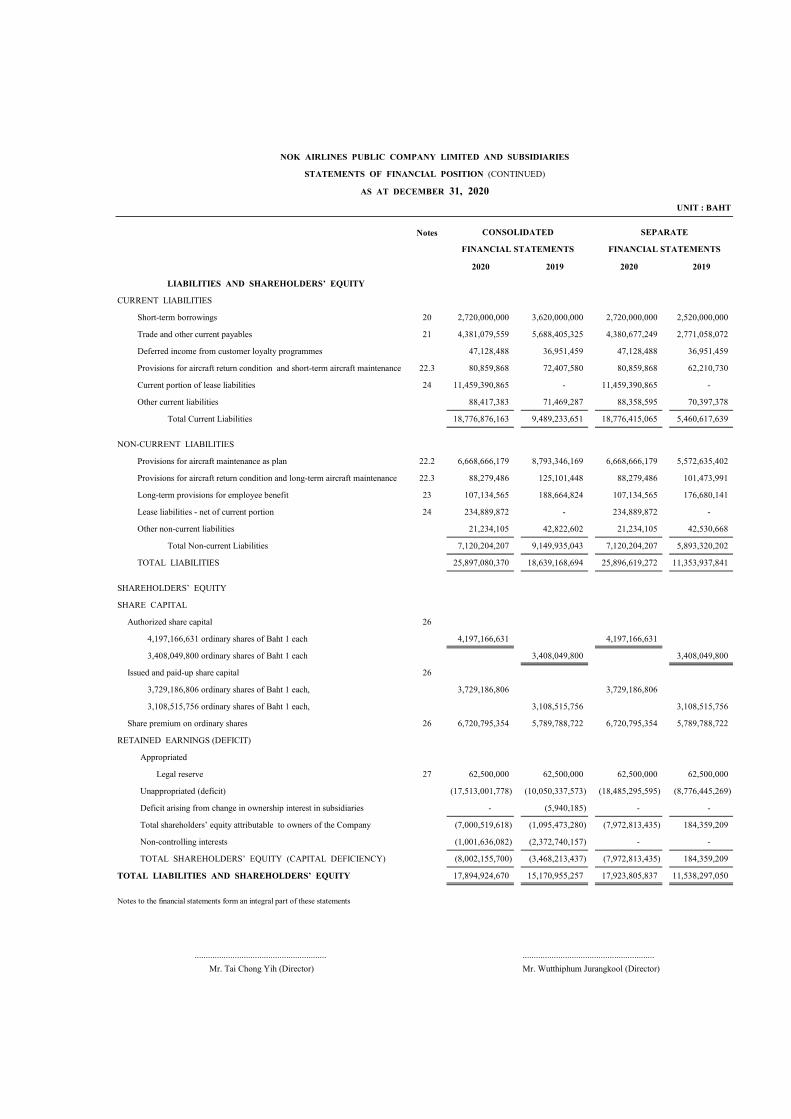

NOK AIRLINES PUBLIC COMPANY LIMITED AND SUBSIDIARIES

STATEMENTS OF FINANCIAL POSITION

AS AT DECEMBER 31, 2020

UNIT : BAHT

CONSOLIDATED SEPARATE

Notes

2020 2019 2020 2019

LIABILITIES AND SHAREHOLDERS’ EQUITY

CURRENT LIABILITIES

Short-term borrowings 20 2,720,000,000 3,620,000,000 2,720,000,000 2,520,000,000

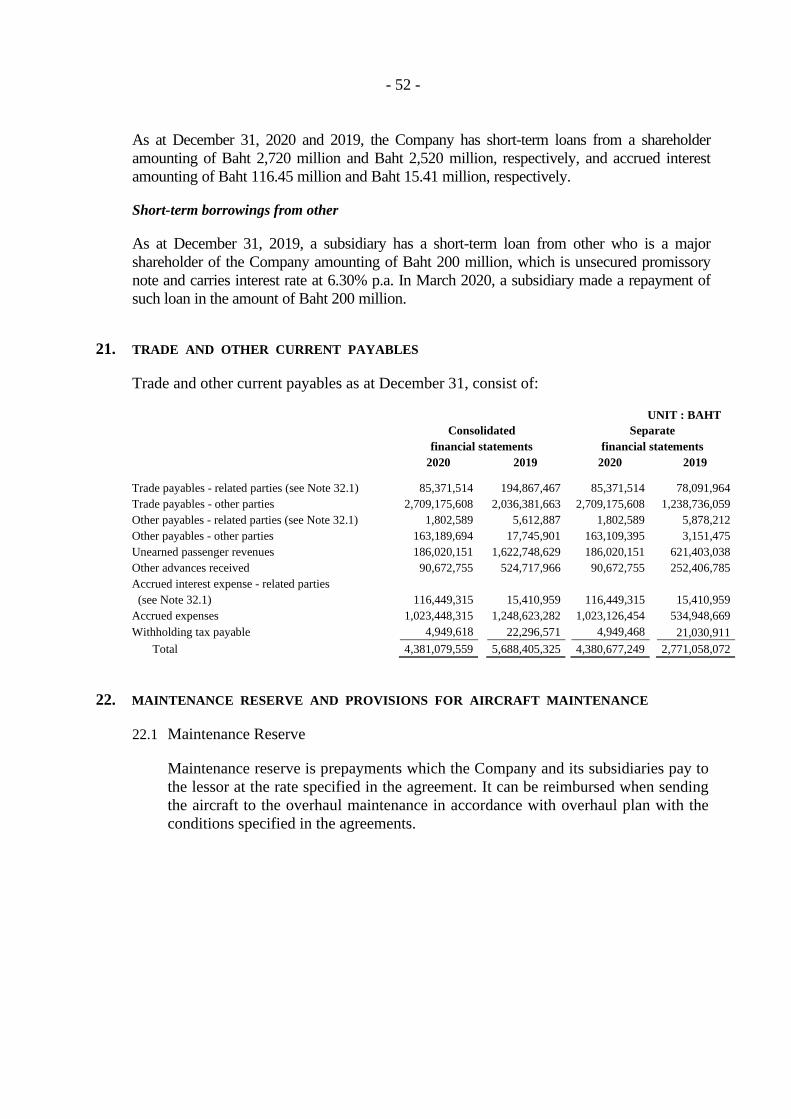

Trade and other current payables 21 4,381,079,559 5,688,405,325 4,380,677,249 2,771,058,072

Deferred income from customer loyalty programmes 47,128,488 36,951,459 47,128,488 36,951,459

Provisions for aircraft return condition and short-term aircraft maintenance 22.3 80,859,868 72,407,580 80,859,868 62,210,730

Current portion of lease liabilities 24 11,459,390,865 - 11,459,390,865 -

Other current liabilities 88,417,383 71,469,287 88,358,595 70,397,378

Total Current Liabilities 18,776,876,163 9,489,233,651 18,776,415,065 5,460,617,639

NON-CURRENT LIABILITIES

Provisions for aircraft maintenance as plan 22.2 6,668,666,179 8,793,346,169 6,668,666,179 5,572,635,402

Provisions for aircraft return condition and long-term aircraft maintenance 22.3 88,279,486 125,101,448 88,279,486 101,473,991

Long-term provisions for employee benefit 23 107,134,565 188,664,824 107,134,565 176,680,141

Lease liabilities - net of current portion 24 234,889,872 - 234,889,872 -

Other non-current liabilities 21,234,105 42,822,602 21,234,105 42,530,668

Total Non-current Liabilities 7,120,204,207 9,149,935,043 7,120,204,207 5,893,320,202

TOTAL LIABILITIES 25,897,080,370 18,639,168,694 25,896,619,272 11,353,937,841

SHAREHOLDERS’ EQUITY

SHARE CAPITAL

Authorized share capital 26

4,197,166,631 ordinary shares of Baht 1 each 4,197,166,631 4,197,166,631

3,408,049,800 ordinary shares of Baht 1 each 3,408,049,800 3,408,049,800

Issued and paid-up share capital 26

3,729,186,806 ordinary shares of Baht 1 each, 3,729,186,806 3,729,186,806

3,108,515,756 ordinary shares of Baht 1 each, 3,108,515,756 3,108,515,756

Share premium on ordinary shares 26 6,720,795,354 5,789,788,722 6,720,795,354 5,789,788,722

RETAINED EARNINGS (DEFICIT)

Appropriated

Legal reserve 27 62,500,000 62,500,000 62,500,000 62,500,000

Unappropriated (deficit) (17,513,001,778) (10,050,337,573) (18,485,295,595) (8,776,445,269)

Deficit arising from change in ownership interest in subsidiaries - (5,940,185) - -

Total shareholders’ equity attributable to owners of the Company (7,000,519,618) (1,095,473,280) (7,972,813,435) 184,359,209

Non-controlling interests (1,001,636,082) (2,372,740,157) - -

TOTAL SHAREHOLDERS’ EQUITY (CAPITAL DEFICIENCY) (8,002,155,700) (3,468,213,437) (7,972,813,435) 184,359,209

TOTAL LIABILITIES AND SHAREHOLDERS’ EQUITY 17,894,924,670 15,170,955,257 17,923,805,837 11,538,297,050

Notes to the financial statements form an integral part of these statements

...........................................................

Mr. Tai Chong Yih (Director) Mr. Wutthiphum Jurangkool (Director)

...........................................................

FINANCIAL STATEMENTS FINANCIAL STATEMENTS

NOK AIRLINES PUBLIC COMPANY LIMITED AND SUBSIDIARIES

STATEMENTS OF FINANCIAL POSITION (CONTINUED)

AS AT DECEMBER 31, 2020

UNIT : BAHT

CONSOLIDATED SEPARATE

Notes

2020 2019 2020 2019

CONTINUING OPERATIONS

REVENUES

Passenger revenues 5,784,220,942 11,163,363,866 5,784,220,942 11,227,896,366

Service revenues 777,090,636 1,248,906,861 777,090,636 1,291,538,531

Other income

Interest income 30,510,904 15,138,428 84,781,679 57,312,124

Others 28 143,568,747 131,895,107 143,568,747 131,887,924

Total Revenues 6,735,391,229 12,559,304,262 6,789,662,004 12,708,634,945

EXPENSES

Costs of passenger and services 7,439,347,381 13,468,472,422 7,439,347,381 13,566,220,821

Selling expenses 37,039,055 102,983,739 37,039,055 102,978,998

Administrative expenses 1,236,435,402 648,624,796 1,236,036,685 670,766,323

Finance costs 910,014,166 81,033,562 910,014,166 82,841,780

Impairment loss on right-of-use assets 17 3,446,296,290 - 3,446,296,290 -

Expected credit losses 3,104,616,061 - 3,257,921,624 -

Total Expenses 16,173,748,355 14,301,114,519 16,326,655,201 14,422,807,922

SHARE OF LOSS FROM INVESTMENT IN A JOINT VENTURE - (1,409,685) - -

LOSS BEFORE INCOME TAX EXPENSES (9,438,357,126) (1,743,219,942) (9,536,993,197) (1,714,172,977)

INCOME TAX EXPENSES 19 - - - -

LOSS FOR THE PERIODS FROM CONTINUING OPERATIONS (9,438,357,126) (1,743,219,942) (9,536,993,197) (1,714,172,977)

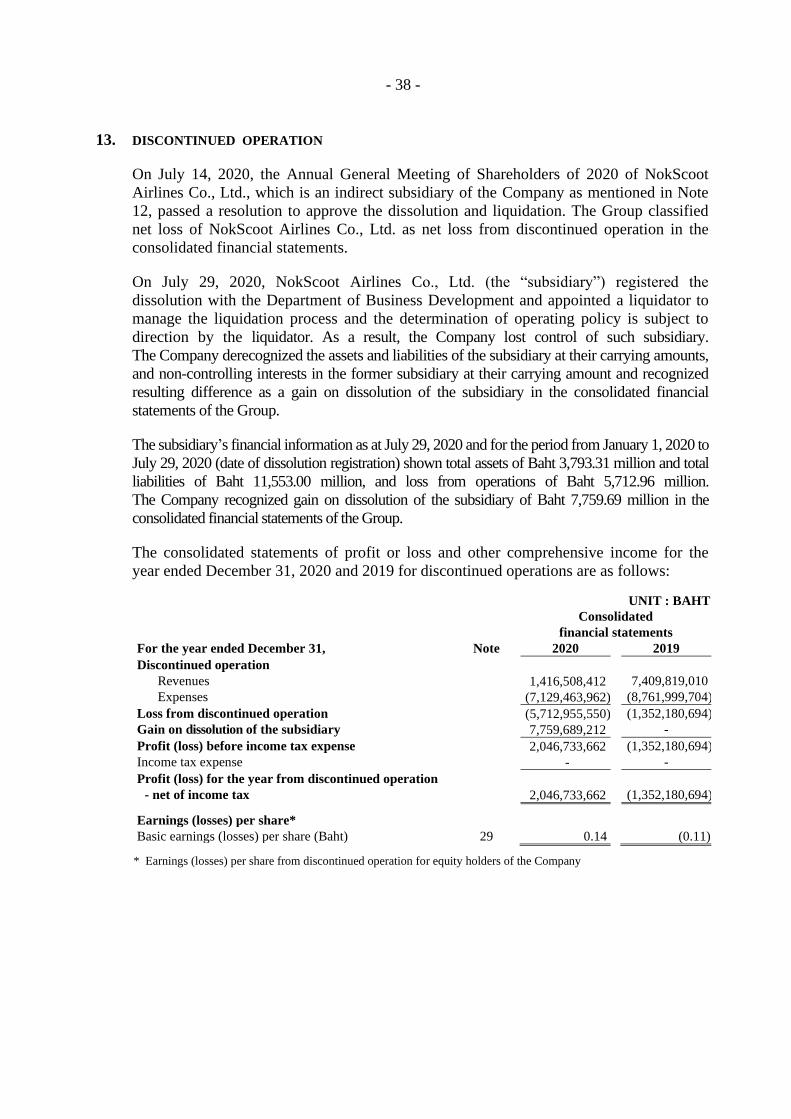

DISCONTINUED OPERATION

Profit (loss) from discontinued operation - net of tax 13 2,046,733,662 (1,352,180,694) - -

TOTAL LOSS FOR THE YEARS (7,391,623,464) (3,095,400,636) (9,536,993,197) (1,714,172,977)

OTHER COMPREHENSIVE INCOME

Item that will not be reclassified subsequently to profit or loss

Actuarial gain on defined employee benefit plans 95,758,709 123,056,465 95,758,709 123,056,465

OTHER COMPREHENSIVE INCOME FOR THE YEARS 95,758,709 123,056,465 95,758,709 123,056,465

TOTAL COMPREHENSIVE LOSS FOR THE YEARS (7,295,864,755) (2,972,344,171) (9,441,234,488) (1,591,116,512)

...........................................................

Mr. Tai Chong Yih (Director) Mr. Wutthiphum Jurangkool (Director)

FINANCIAL STATEMENTS FINANCIAL STATEMENTS

NOK AIRLINES PUBLIC COMPANY LIMITED AND SUBSIDIARIES

STATEMENTS OF PROFIT OR LOSS AND OTHER COMPREHENSIVE INCOME (CONTINUED)

...........................................................

CONSOLIDATED SEPARATE

NOK AIRLINES PUBLIC COMPANY LIMITED AND SUBSIDIARIES

STATEMENTS OF PROFIT OR LOSS AND OTHER COMPREHENSIVE INCOME

FOR THE YEAR ENDED DECEMBER 31, 2020

UNIT : BAHT

Notes

2020 2019 2020 2019

Profit (loss) for the year attributable to:

Equity holders of the Company

From continuing operations (8,489,178,814) (1,722,435,965) (9,536,993,197) (1,714,172,977)

From discontinued operation 497,929,639 (328,958,700)

(7,991,249,175) (2,051,394,665)

Non-controlling interests of the subsidiaries

From continuing operations (949,178,312) (20,783,977)

From discontinued operation 1,548,804,023 (1,023,221,994)

599,625,711 (1,044,005,971)

(7,391,623,464) (3,095,400,636)

Total comprehensive income (loss) for the year attributable to:

Equity holders of the Company

From continuing operations (8,393,420,105) (1,599,379,500) (9,441,234,488) (1,591,116,512)

From discontinued operation 497,929,639 (328,958,700)

(7,895,490,466) (1,928,338,200)

Non-controlling interests of the subsidiaries

From continuing operations (949,178,312) (20,783,977)

From discontinued operation 1,548,804,023 (1,023,221,994)

599,625,711 (1,044,005,971)

(7,295,864,755) (2,972,344,171)

EARNINGS (LOSSES) PER SHARE 29

Basic earnings (losses) per share (Baht)

From continuing operations (2.33) (0.57)

From discontinued operation 13 0.14 (0.11)

Basic losses per share for the years (2.19) (0.68) (2.62) (0.57)

Notes to the financial statements form an integral part of these statements

........................................................... ...........................................................

Mr. Tai Chong Yih (Director) Mr. Wutthiphum Jurangkool (Director)

UNIT : BAHT

CONSOLIDATED SEPARATE

FINANCIAL STATEMENTS FINANCIAL STATEMENTS

FOR THE YEAR ENDED DECEMBER 31, 2020

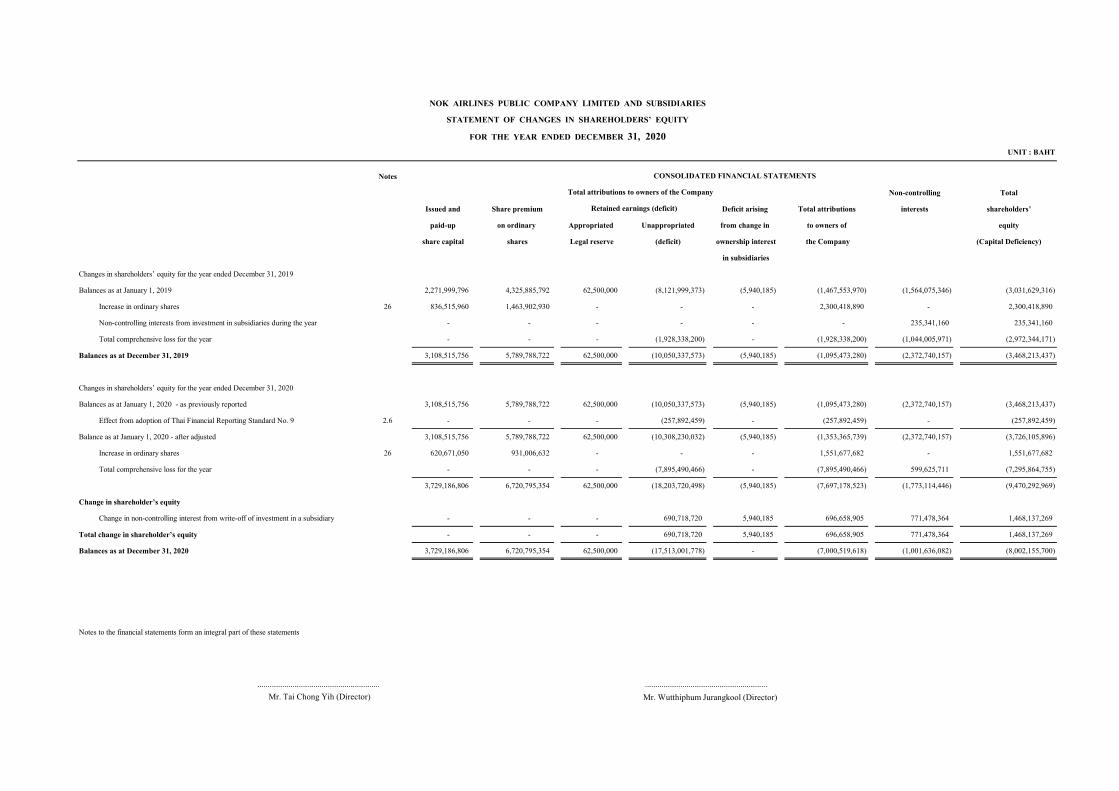

Notes

Non-controlling Total

Issued and Share premium Deficit arising Total attributions interests shareholders’

paid-up on ordinary Appropriated Unappropriated from change in to owners of equity

share capital shares Legal reserve (deficit) ownership interest the Company (Capital Deficiency)

in subsidiaries

Changes in shareholders’ equity for the year ended December 31, 2019

Balances as at January 1, 2019 2,271,999,796 4,325,885,792 62,500,000 (8,121,999,373) (5,940,185) (1,467,553,970) (1,564,075,346) (3,031,629,316)

Increase in ordinary shares 26 836,515,960 1,463,902,930 - - - 2,300,418,890 - 2,300,418,890

Non-controlling interests from investment in subsidiaries during the year - - - - - - 235,341,160 235,341,160

Total comprehensive loss for the year - - - (1,928,338,200) - (1,928,338,200) (1,044,005,971) (2,972,344,171)

Balances as at December 31, 2019 3,108,515,756 5,789,788,722 62,500,000 (10,050,337,573) (5,940,185) (1,095,473,280) (2,372,740,157) (3,468,213,437)

Changes in shareholders’ equity for the year ended December 31, 2020

Balances as at January 1, 2020 - as previously reported 3,108,515,756 5,789,788,722 62,500,000 (10,050,337,573) (5,940,185) (1,095,473,280) (2,372,740,157) (3,468,213,437)

Effect from adoption of Thai Financial Reporting Standard No. 9 2.6 - - - (257,892,459) - (257,892,459) - (257,892,459)

Balance as at January 1, 2020 - after adjusted 3,108,515,756 5,789,788,722 62,500,000 (10,308,230,032) (5,940,185) (1,353,365,739) (2,372,740,157) (3,726,105,896)

Increase in ordinary shares 26 620,671,050 931,006,632 - - - 1,551,677,682 - 1,551,677,682

Total comprehensive loss for the year - - - (7,895,490,466) - (7,895,490,466) 599,625,711 (7,295,864,755)

3,729,186,806 6,720,795,354 62,500,000 (18,203,720,498) (5,940,185) (7,697,178,523) (1,773,114,446) (9,470,292,969)

Change in shareholder’s equity

Change in non-controlling interest from write-off of investment in a subsidiary - - - 690,718,720 5,940,185 696,658,905 771,478,364 1,468,137,269

Total change in shareholder’s equity - - - 690,718,720 5,940,185 696,658,905 771,478,364 1,468,137,269

Balances as at December 31, 2020 3,729,186,806 6,720,795,354 62,500,000 (17,513,001,778) - (7,000,519,618) (1,001,636,082) (8,002,155,700)

Notes to the financial statements form an integral part of these statements

Mr. Wutthiphum Jurangkool (Director)Mr. Tai Chong Yih (Director)

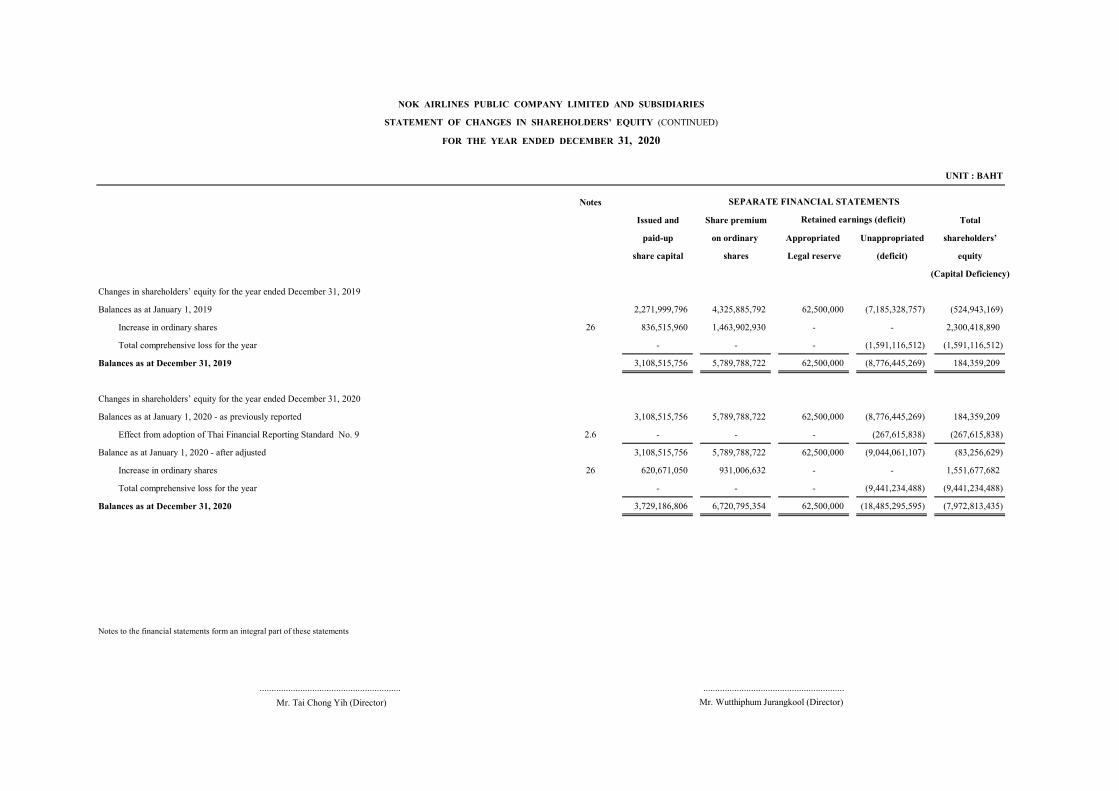

NOK AIRLINES PUBLIC COMPANY LIMITED AND SUBSIDIARIES

STATEMENT OF CHANGES IN SHAREHOLDERS’ EQUITY

FOR THE YEAR ENDED DECEMBER 31, 2020

UNIT : BAHT

CONSOLIDATED FINANCIAL STATEMENTS

Total attributions to owners of the Company

Retained earnings (deficit)

........................................................... ...........................................................

Notes

Issued and Share premium Total

paid-up on ordinary Appropriated Unappropriated shareholders’

share capital shares Legal reserve (deficit) equity

(Capital Deficiency)

Changes in shareholders’ equity for the year ended December 31, 2019

Balances as at January 1, 2019 2,271,999,796 4,325,885,792 62,500,000 (7,185,328,757) (524,943,169)

Increase in ordinary shares 26 836,515,960 1,463,902,930 - - 2,300,418,890

Total comprehensive loss for the year - - - (1,591,116,512) (1,591,116,512)

Balances as at December 31, 2019 3,108,515,756 5,789,788,722 62,500,000 (8,776,445,269) 184,359,209

Changes in shareholders’ equity for the year ended December 31, 2020

Balances as at January 1, 2020 - as previously reported 3,108,515,756 5,789,788,722 62,500,000 (8,776,445,269) 184,359,209

Effect from adoption of Thai Financial Reporting Standard No. 9 2.6 - - - (267,615,838) (267,615,838)

Balance as at January 1, 2020 - after adjusted 3,108,515,756 5,789,788,722 62,500,000 (9,044,061,107) (83,256,629)

Increase in ordinary shares 26 620,671,050 931,006,632 - - 1,551,677,682

Total comprehensive loss for the year - - - (9,441,234,488) (9,441,234,488)

Balances as at December 31, 2020 3,729,186,806 6,720,795,354 62,500,000 (18,485,295,595) (7,972,813,435)

Notes to the financial statements form an integral part of these statements

...........................................................

Mr. Tai Chong Yih (Director) Mr. Wutthiphum Jurangkool (Director)

...........................................................

SEPARATE FINANCIAL STATEMENTS

Retained earnings (deficit)

NOK AIRLINES PUBLIC COMPANY LIMITED AND SUBSIDIARIES

STATEMENT OF CHANGES IN SHAREHOLDERS’ EQUITY (CONTINUED)

FOR THE YEAR ENDED DECEMBER 31, 2020

UNIT : BAHT

Notes

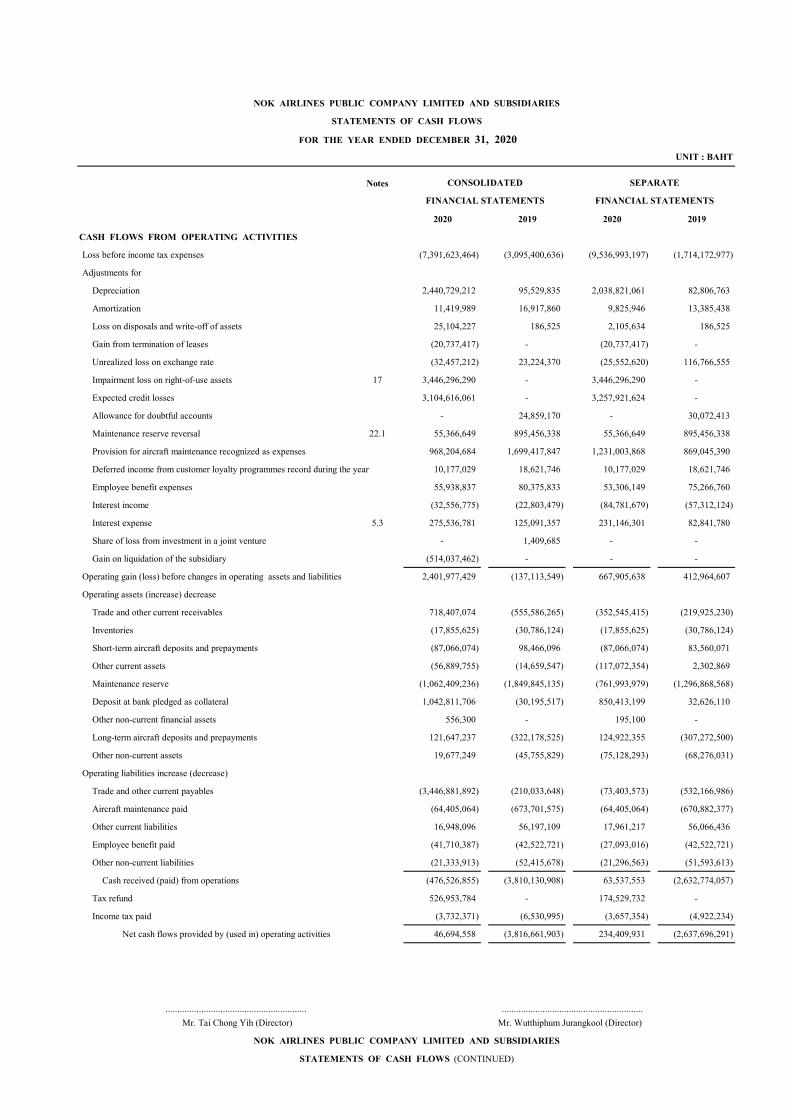

2020 2019 2020 2019

CASH FLOWS FROM OPERATING ACTIVITIES

Loss before income tax expenses (7,391,623,464) (3,095,400,636) (9,536,993,197) (1,714,172,977)

Adjustments for

Depreciation 2,440,729,212 95,529,835 2,038,821,061 82,806,763

Amortization 11,419,989 16,917,860 9,825,946 13,385,438

Loss on disposals and write-off of assets 25,104,227 186,525 2,105,634 186,525

Gain from termination of leases (20,737,417) - (20,737,417) -

Unrealized loss on exchange rate (32,457,212) 23,224,370 (25,552,620) 116,766,555

Impairment loss on right-of-use assets 17 3,446,296,290 - 3,446,296,290 -

Expected credit losses 3,104,616,061 - 3,257,921,624 -

Allowance for doubtful accounts - 24,859,170 - 30,072,413

Maintenance reserve reversal 22.1 55,366,649 895,456,338 55,366,649 895,456,338

Provision for aircraft maintenance recognized as expenses 968,204,684 1,699,417,847 1,231,003,868 869,045,390

Deferred income from customer loyalty programmes record during the year 10,177,029 18,621,746 10,177,029 18,621,746

Employee benefit expenses 55,938,837 80,375,833 53,306,149 75,266,760

Interest income (32,556,775) (22,803,479) (84,781,679) (57,312,124)

Interest expense 5.3 275,536,781 125,091,357 231,146,301 82,841,780

Share of loss from investment in a joint venture - 1,409,685 - -

Gain on liquidation of the subsidiary (514,037,462) - - -

Operating gain (loss) before changes in operating assets and liabilities 2,401,977,429 (137,113,549) 667,905,638 412,964,607

Operating assets (increase) decrease

Trade and other current receivables 718,407,074 (555,586,265) (352,545,415) (219,925,230)

Inventories (17,855,625) (30,786,124) (17,855,625) (30,786,124)

Short-term aircraft deposits and prepayments (87,066,074) 98,466,096 (87,066,074) 83,560,071

Other current assets (56,889,755) (14,659,547) (117,072,354) 2,302,869

Maintenance reserve (1,062,409,236) (1,849,845,135) (761,993,979) (1,296,868,568)

Deposit at bank pledged as collateral 1,042,811,706 (30,195,517) 850,413,199 32,626,110

Other non-current financial assets 556,300 - 195,100 -

Long-term aircraft deposits and prepayments 121,647,237 (322,178,525) 124,922,355 (307,272,500)

Other non-current assets 19,677,249 (45,755,829) (75,128,293) (68,276,031)

Operating liabilities increase (decrease)

Trade and other current payables (3,446,881,892) (210,033,648) (73,403,573) (532,166,986)

Aircraft maintenance paid (64,405,064) (673,701,575) (64,405,064) (670,882,377)

Other current liabilities 16,948,096 56,197,109 17,961,217 56,066,436

Employee benefit paid (41,710,387) (42,522,721) (27,093,016) (42,522,721)

Other non-current liabilities (21,333,913) (52,415,678) (21,296,563) (51,593,613)

Cash received (paid) from operations (476,526,855) (3,810,130,908) 63,537,553 (2,632,774,057)

Tax refund 526,953,784 - 174,529,732 -

Income tax paid (3,732,371) (6,530,995) (3,657,354) (4,922,234)

Net cash flows provided by (used in) operating activities 46,694,558 (3,816,661,903) 234,409,931 (2,637,696,291)

FINANCIAL STATEMENTS FINANCIAL STATEMENTS

...........................................................

NOK AIRLINES PUBLIC COMPANY LIMITED AND SUBSIDIARIES

Mr. Tai Chong Yih (Director) Mr. Wutthiphum Jurangkool (Director)

...........................................................

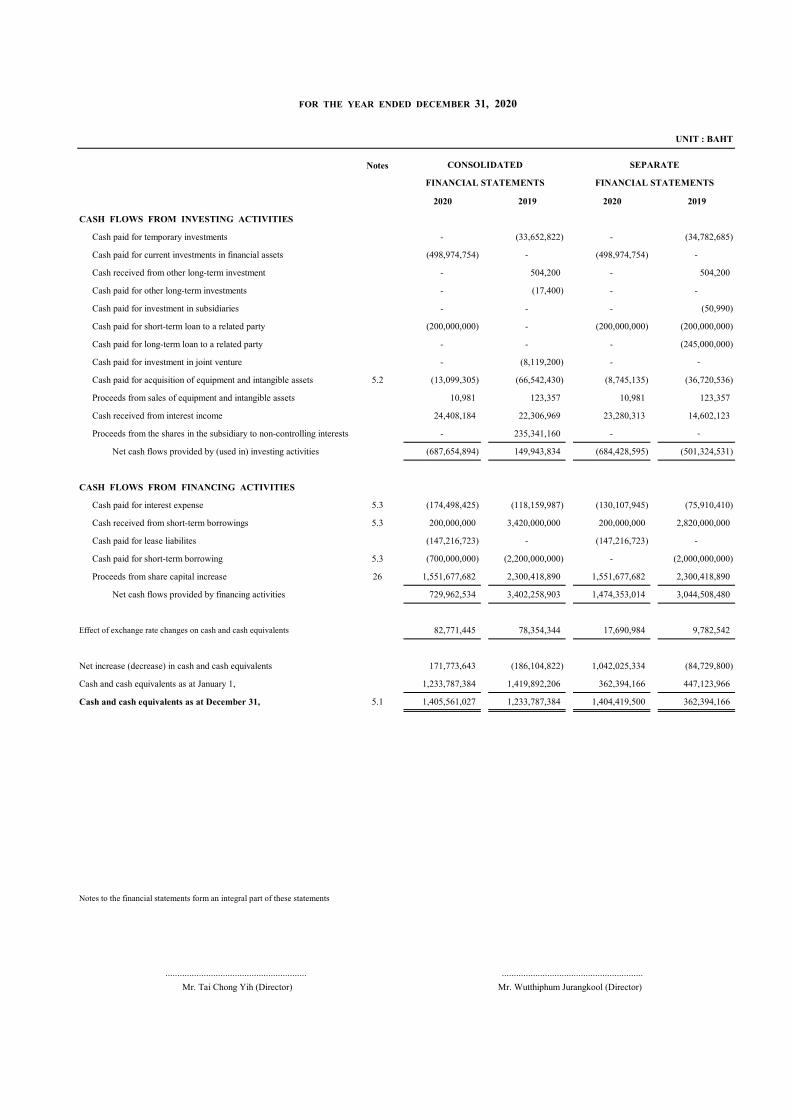

NOK AIRLINES PUBLIC COMPANY LIMITED AND SUBSIDIARIES

STATEMENTS OF CASH FLOWS

FOR THE YEAR ENDED DECEMBER 31, 2020

UNIT : BAHT

CONSOLIDATED SEPARATE

STATEMENTS OF CASH FLOWS (CONTINUED)

Notes

2020 2019 2020 2019

CASH FLOWS FROM INVESTING ACTIVITIES

Cash paid for temporary investments - (33,652,822) - (34,782,685)

Cash paid for current investments in financial assets (498,974,754) - (498,974,754) -

Cash received from other long-term investment - 504,200 - 504,200

Cash paid for other long-term investments - (17,400) - -

Cash paid for investment in subsidiaries - - - (50,990)

Cash paid for short-term loan to a related party (200,000,000) - (200,000,000) (200,000,000)

Cash paid for long-term loan to a related party - - - (245,000,000)

Cash paid for investment in joint venture - (8,119,200) - -

Cash paid for acquisition of equipment and intangible assets 5.2 (13,099,305) (66,542,430) (8,745,135) (36,720,536)

Proceeds from sales of equipment and intangible assets 10,981 123,357 10,981 123,357

Cash received from interest income 24,408,184 22,306,969 23,280,313 14,602,123

Proceeds from the shares in the subsidiary to non-controlling interests - 235,341,160 - -

Net cash flows provided by (used in) investing activities (687,654,894) 149,943,834 (684,428,595) (501,324,531)

CASH FLOWS FROM FINANCING ACTIVITIES

Cash paid for interest expense 5.3 (174,498,425) (118,159,987) (130,107,945) (75,910,410)

Cash received from short-term borrowings 5.3 200,000,000 3,420,000,000 200,000,000 2,820,000,000

Cash paid for lease liabilites (147,216,723) - (147,216,723) -

Cash paid for short-term borrowing 5.3 (700,000,000) (2,200,000,000) - (2,000,000,000)

Proceeds from share capital increase 26 1,551,677,682 2,300,418,890 1,551,677,682 2,300,418,890

Net cash flows provided by financing activities 729,962,534 3,402,258,903 1,474,353,014 3,044,508,480

Effect of exchange rate changes on cash and cash equivalents 82,771,445 78,354,344 17,690,984 9,782,542

Net increase (decrease) in cash and cash equivalents 171,773,643 (186,104,822) 1,042,025,334 (84,729,800)

Cash and cash equivalents as at January 1, 1,233,787,384 1,419,892,206 362,394,166 447,123,966

Cash and cash equivalents as at December 31, 5.1 1,405,561,027 1,233,787,384 1,404,419,500 362,394,166

- -

Notes to the financial statements form an integral part of these statements

........................................................... ...........................................................

Mr. Tai Chong Yih (Director) Mr. Wutthiphum Jurangkool (Director)

FOR THE YEAR ENDED DECEMBER 31, 2020

UNIT : BAHT

CONSOLIDATED SEPARATE

FINANCIAL STATEMENTS FINANCIAL STATEMENTS

NOK AIRLINES PUBLIC COMPANY LIMITED AND SUBSIDIARIES

NOTES TO THE FINANCIAL STATEMENTS

FOR THE YEAR ENDED DECEMBER 31, 2020

1. GENERAL INFORMATION AND OPERATIONS OF THE COMPANY AND SUBSIDIARIES

1.1 General information of the Company and subsidiaries (the “Group”)

1.1.1 Nok Airlines Public Company Limited (the “Company”) was incorporated as

a limited company under Thai laws on February 27, 2004. The registered

office is located at 3 Rajanakarn Building, 17th Floor, South Sathorn Road,

Yannawa, Sathorn, Bangkok, and its principal activity is to provide air

transport services for passengers. On January 18, 2013, the Company registered

to convert the Company from a limited company to a public limited company

and registered the change of the Company’s name from Nok Airlines Company

Limited to Nok Airlines Public Company Limited with the Ministry of

Commerce. On June 20, 2013, the Company had been approved by the Stock

Exchange of Thailand to be a listed company in the Stock Exchange of Thailand.

On January 1, 2021, the Company registered the change of address of new head

office to 222 Don Mueang International Airport, Central Building, Room No. 4235,

4th Floor, Vibhavadi Rangsit Road, Sanambin Sub-district, Don Mueang District, Bangkok.

As at December 31, 2020, the Company’s major shareholders were Mrs. Hatairatn

Jurangkool, Mr. Nattapol Jurangkool, Mr. Taveechat Jurangkool and Thai

Airways International Public Company Limited, which are Thai shareholders,

holding 26.38%, 26.07%, 22.51% and 13.28%, respectively, of the Company’s

issued and paid-up share capital.

As at December 31, 2019, the Company’s major shareholders were Mrs.

Hatairatn Jurangkool, Mr. Nattapol Jurangkool, Mr. Taveechat Jurangkool and

Thai Airways International Public Company Limited which are Thai shareholders,

holding 24.37%, 24.32%, 20.98% and 15.94%, respectively, of the Company’s

issued and paid-up share capital.

1.1.2 Nok Holidays Company Limited was incorporated as a limited company

under Thai laws on April 4, 2014. The registered office is located at 3 Rajanakarn

Building, 17th Floor, South Sathorn Road, Yannawa, Sathorn, Bangkok and its

principal activity is to provide tourism and other relevant business.

On January 1, 2021, the Company registered the change of address of new office

to 222 Don Mueang International Airport, Central Building, Room No. 4235,

4th Floor, Vibhavadi Rangsit Road, Sanambin Sub-district, Don Mueang

District, Bangkok.

- 2 -

1.1.3 Nok Mangkang Company Limited was incorporated as a limited company

under Thai laws on June 13, 2014. The registered office is located at 3 Rajanakarn

Building, 17th Fl., South Sathorn Road, Yannawa, Sathorn, Bangkok, and its

principal activity is to provide air transport service for passengers, parcel and

parcel post.

On January 28, 2021, the Company registered the change of address of new

office to 222 Don Mueang International Airport, Central Building, Room No.4235,

4th Floor, Vibhavadi Rangsit Road, Sanambin Sub-district, Don Mueang District, Bangkok.

1.1.4 NokScoot Airlines Company Limited was incorporated as a limited company

under Thai laws on October 30, 2013. The current registered office is located at

999/9 The Offices at Central World Building, 26th Floor, Rama 1 Road,

Pathumwan Sub-district, Pathumwan District, Bangkok, and its principal activity

is to provide air transport service for passengers, parcel and parcel post.

On July 29, 2020, NokScoot Airlines Co., Ltd. registered the dissolution

with the Department of Business Development (see Note 1.2.3).

1.2 Operations of the Company and subsidiaries

1.2.1 Operations of the Company and subsidiaries

For the year ended December 31, 2020, the consolidated and separate financial

statements of the Company shown net loss of Baht 7,391.62 million and

Baht 9,536.99 million, respectively. As at December 31, 2020, the consolidated

and separate financial statements shown total current liabilities exceeded total current

assets of Baht 16,194.30 million and Baht 16,193.29 million and shown capital

deficiency of Baht 8,002.15 million and Baht 7,972.81 million, respectively.

Impact from Coronavirus Disease 2019 Pandemic to Nok Airlines Public

Company Limited (the “Company”) and NokScoot Airlines Company Limited

(the “subsidiary”).

The Coronavirus disease 2019 pandemic is continuing to evolve, resulting in

an economic slowdown and adversely impacting most businesses and

industries especially aviation industry. This affect to the Company and the

subsidiary to close oversea routes since March 2020 onwards. For domestic

routes, the Company normally operates with adjustments on frequency of

flights has been reduced as appropriate under the Emergency Situation Act.

On July 1, 2020, the Company continued their operation in accordance with

the Civil Aviation Authority of Thailand hereby issued the notification on

the conditions for permitting aircrafts to fly over, fly into or out of, and take

off or land in the Kingdom, dated June 29, 2020.

- 3 -

1.2.2 Management plan of Nok Airlines Public Company Limited (the “Company”)

On January 14, 2020, the Extraordinary General Meeting of Shareholders No.

1/2020 has resolved to approve the increase of registered capital of 888.15 million

shares at an offering price of Baht 2.50 per share. The Company determined the

allocation ratio as 3.50 existing shares to 1 newly-issued ordinary share. On

February 11, 2020, the Company received subscriptions in the amount of Baht

1,551.68 million from issued and paid-up share capital totaling 620.67 million shares

at an offering price of Baht 2.50 per share with a par value of Baht 1 per share.

On June 30, 2020, the Board of Director Meeting on special No. 6/2020 has

resolved to approve to renew the term of a connected transaction with a

connected person in relation to a receipt of financial assistance of the credit

limit of Baht 3,000 million, which extended the term from 1 year to 3 years

under the existing credit limit and conditions from October 1, 2020 to May 14,

2023 and grant the rights for the lender to terminate the agreement and/or

immediately cancel the outstanding credit limit. This connected transaction was

approved by the Annual General Meeting of Shareholders of 2020 on August 6,

2020.

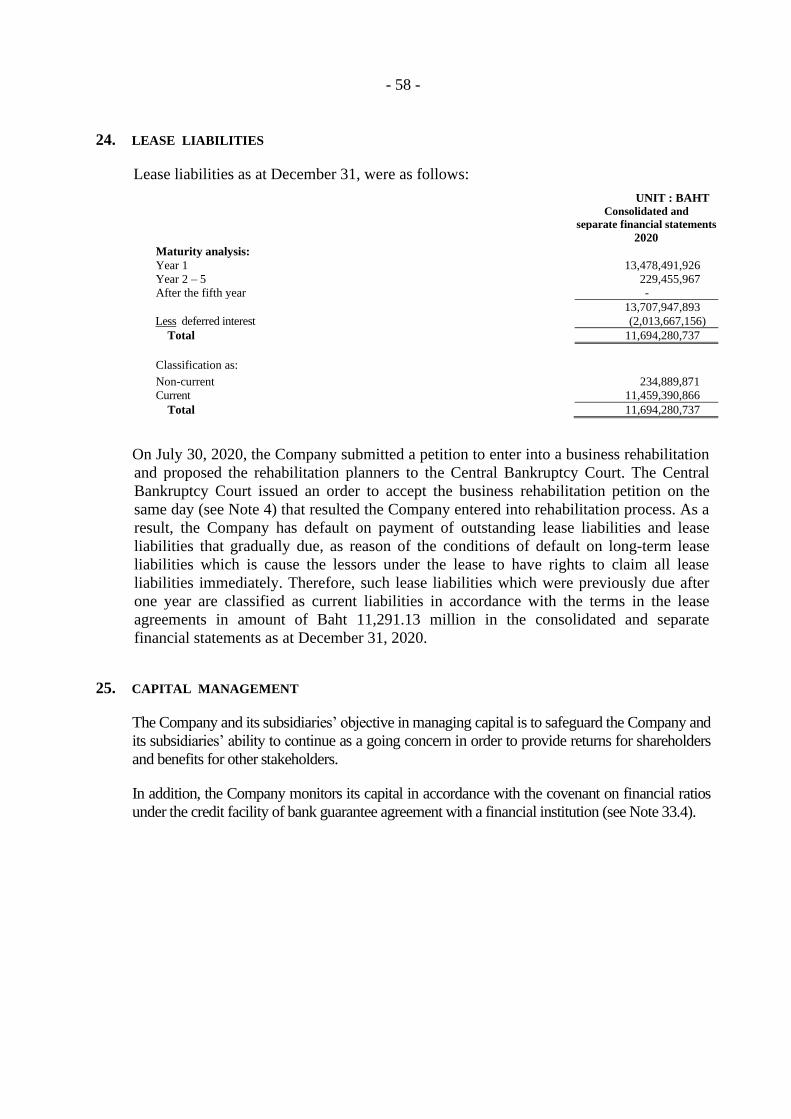

On July 30, 2020, the Company submitted a petition to enter into a business

rehabilitation process and proposed the rehabilitation planners (the

“Planners”) to the Central Bankruptcy Court. The Central Bankruptcy Court

accepted the business rehabilitation petition for further consideration on the

same day (see Note 4). As a result, the Company is under the automatic stay

provisions under the Bankruptcy Act B.E. 2483. Such situation may affect to

the recorded assets and liabilities as at December 31, 2020. However, the

Company’s management considered that the preparation of financial statements

on a going concern basis is still appropriate because the Company prepared

and submitted the rehabilitation plan to request for approved from creditors

and the Central Bankruptcy Court during the year 2021. During this period,

the Company is able to continue its necessary activities for operation as

usual in order to enable the Company to continue as a going concern for at

least 12 months from the date in the statement of financial position.

However, the Company’s ability to continue as going concern depends on

the creditors’ approval of the rehabilitation plan as well as the successful

implementation of the rehabilitation plan.

1.2.3 Operations of NokScoot Airlines Company Limited (the “subsidiary”)

NokScoot Airlines Co., Ltd. has been experiencing continuous financial

losses and has worsened by the Coronavirus Disease 2019 (“COVID-19”)

Pandemic because routes are oversea routes, such as China, Taiwan, Japan,

which have been affected by COVID-19 severely. Therefore, this affected

significantly to NokScoot Airlines Co., Ltd. in order that they cannot operate

on a going concern.

- 4 -

On June 26, 2020, the Board of Directors’ meeting on special No. 5/2020 of

Nok Airlines Public Company Limited (the “Company”) acknowledged the

business termination and liquidation of NokScoot Airlines Co., Ltd. of which

Nok Mangkang Co., Ltd., a subsidiary of the Company, holds 49.65% of its

registered shares. On July 14, 2020, Annual General Meeting of Shareholders

of 2020 approved the dissolution and liquidation along with appointing the

liquidator of NokScoot Airlines Co., Ltd. Subsequently, the subsidiary

registered the dissolution with the Department of Business Development on

July 29, 2020.

The NokScoot Airlines Co., Ltd. (the “subsidiary”)’s financial information as

at July 29, 2020 and for the period from January 1, 2020 to July 29, 2020

(date of dissolution registration) shown net loss of Baht 5,712.96 million,

and total current liabilities exceeded total current assets of Baht 7,759.69

million and shown capital deficiency of Baht 10,720.47 million.

2. BASIS FOR PREPARATION AND PRESENTATION OF THE FINANCIAL STATEMENTS

2.1 The Company and subsidiaries maintain its accounting records in Thai Baht and

prepares its statutory financial statements in the Thai language in conformity with

Thai Financial Reporting Standards and accounting practices generally accepted in

Thailand.

The financial statements in Thai language are the official statutory financial

statements of the Company. The financial statements in English language have been

translated from the Thai language financial statements. In the event of any conflict

or different interpretation in the two languages, the Thai version of the financial

statements, in accordance with Thai laws will prevail.

2.2 The Company and subsidiaries’ financial statements have been prepared in accordance

with the Thai Accounting Standard (TAS) No. 1 “Presentation of Financial Statements”,

which was effective for financial periods beginning on or after January 1, 2020 onward,

and the Regulation of The Stock Exchange of Thailand (SET) dated October 2, 2017,

regarding “The preparation and submission of financial statements and reports for the

financial position and results of operations of the listed companies B.E. 2560” and the

Notification of the Department of Business Development regarding “The Brief Particulars

in the Financial Statement (No.3) B.E. 2562” dated December 26, 2019.

2.3 The financial information of NokScoot Airlines Co., Ltd. (the “subsidiary”) as at July 29,

2020 and for the period from January 1, 2020 to July 29, 2020 (date of dissolution

registration) has been prepared on the basis of measuring asset items at the lower of

carrying amount or net realizable values and measuring liability items at values or

other considerations to be paid, and classified all asset and liability items as current items

in accordance with the clarification regarding the preparation of the financial statements

in accordance with the basis other than going concern basis issued by the Federation

of Accounting Professions on October 11, 2018. This is because the subsidiary

registered the dissolution with the Department of Business Development on July 29,

2020. The Clarification is effective for the financial statements for the period ending

on or after January 1, 2019 onwards, applying the prospective method.

- 5 -

The subsidiary appointed a liquidator to manage the liquidation process and the

determination of operating policy is subject to direction by the liquidator. As a result,

the Company lost control of such subsidiary. The Company derecognized the assets and

liabilities of the subsidiary at their carrying amounts, and non-controlling interests in the

former subsidiary at their carrying amount and recognized resulting difference as a gain

on dissolution of the subsidiary in the consolidated financial statements of the Group.

2.4 The consolidated financial statements included the accounting records of the Company and

its subsidiaries by eliminating of the intercompany significant transactions and balances.

As at December 31, 2020, and 2019, the Company has shareholding portion in the

subsidiaries as follows:

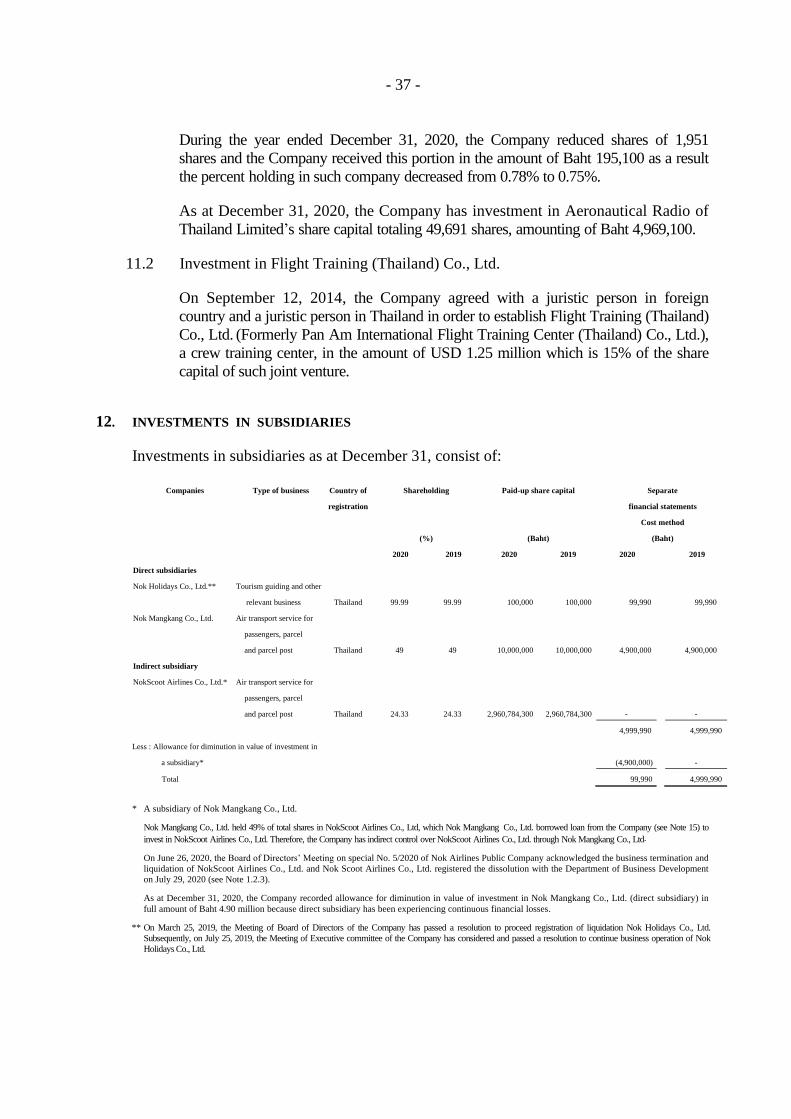

Subsidiaries Type of business Country of Registration Shareholdings

registration date (%)

As at As at

December 31, December 31,

2020 2019

Direct subsidiaries

Nok Holidays Co., Ltd. Tourism and other relevant Thailand April 4, 2014 99.99 99.99

businesses

Nok Mangkang Co., Ltd. Air transport service for Thailand June 13, 2014 49 49

passengers, parcel and

parcel post

Indirect subsidiary

NokScoot Airlines Air transport service for Thailand October 30, 2013 24.33 24.33

Co., Ltd.(1), (2) passengers, parcel and

parcel post

(1) A subsidiary of Nok Mangkang Co., Ltd. (2) On June 26, 2020, the Board of Directors’ meeting on special No. 5/2020 of Nok Airlines Public Company

Limited acknowledged the business termination and liquidation of NokScoot Airlines Co., Ltd. and NokScoot

Airlines Co., Ltd. registered the dissolution with the Department of Business Development on July 29, 2020 (see

Note 1.2.3).

2.5 The financial statements have been prepared under the historical cost convention

except as disclosed in the significant accounting policies (see Note 3).

2.6 Thai Financial Reporting Standards affecting the presentation and disclosure in the

current period financial statements

During the year, the Group has adopted the revised and new financial reporting

standards and guidelines on accounting issued by the Federation of Accounting

Professions which become effective for fiscal years beginning on or after January 1, 2020.

These financial reporting standards were aimed at alignment with the corresponding

International Financial Reporting Standards, with most of the changes directed towards

revision of wording and terminology, and provision of interpretations and accounting

guidance to users of standards. The adoption of these financial reporting standards does

not have any significant impact on the Group’s financial statements, except the following

financial reporting standards:

- 6 -

Group of Financial Instruments Standards

Thai Accounting Standards (“TAS”) TAS 32 Financial Instruments: Presentation Thai Financial Reporting Standards (“TFRS”) TFRS 7 Financial Instruments: Disclosures TFRS 9 Financial Instruments Thai Financial Reporting Standard Interpretations (“TFRIC”) TFRIC 16 Hedges of a Net Investment in a Foreign Operation TFRIC 19 Extinguishing Financial Liabilities with Equity Instruments

These group of Standards make stipulations relating to the classification of financial

instruments and their measurement at fair value or amortized cost; taking into account the

type of instrument, the characteristics of the contractual cash flows and the Company’s

business model, the calculation of impairment using the expected credit loss method, and

the concept of hedge accounting. These include stipulations regarding the presentation

and disclosure of financial instruments.

Thai Financial Reporting Standard No. 16 “Leases” (“TFRS 16”)

TFRS 16 “Leases” provides a comprehensive model for the identification of lease

arrangements and their treatment in the financial statements of both lessees and lessors.

This TFRS superseded the following lease Standards and Interpretations upon its effective

date, which are Thai Accounting Standard No.17 “Leases”, Thai Accounting Standard

Interpretation No.15 “Operating Lease - Incentives”, Thai Accounting Standard

Interpretation No.27 “Evaluating the Substance of Transactions involving the Legal Form

of a Lease” and Thai Financial Reporting Standard Interpretation No.4 “Determining

whether on Arrangement contains a Lease”.

For lessee accounting, there are significant changes to lease accounting in this TFRS by

removing the distinction between operating and finance leases under TAS 17 and

requiring a lessee to recognize a right-of-use asset and a lease liability at commencement

for all leases, except for short-term leases and leases of low value assets. However, the

lessor accounting treatment continues to require a lessor to classify a lease either as an

operating lease or a finance lease, using the same concept as TAS 17.

The Group adopted the Group of Financial Instruments Standards and Thai Financial

Reporting Standards No.16 has been applied, recognizing the cumulative effect of the

initial application of these Thai Financial Reporting Standards which is adjusted to

retained earnings on January 1, 2020 and don’t restate the previous year’s financial

statements that presented for comparison.

- 7 -

The impacts on the beginning balance of the year of 2020 due to the adoption of

these standards are presented as follows:

UNIT : BAHT

Consolidated financial statements

Effect from Thai Financial Reporting Standards

As at Group of TFRS 16 As at

December 31, financial January 1,

2019 instruments 2020

Statements of financial position

Assets

Current assets

Current investments 42,878,939 (42,878,939) - -

Trade and other current receivables 2,493,338,355 (257,892,459) - 2,235,445,896

Other current financial assets - 42,878,939 - 42,878,939

Non-current assets

Other long-term investment 46,175,400 (46,175,400) - -

Right-of-use assets - - 15,974,940,964 15,974,940,964

Deposits at bank pledged as collateral 1,153,058,005 (1,153,058,005) - -

Other non-current financial assets - 1,199,233,405 - 1,199,233,405

Liabilities

Current liabilities

Current portion of lease liabilities - - 2,683,865,349 2,683,865,349

Non-current liabilities

Lease liabilities - - 13,291,075,615 13,291,075,615

Shareholders’ equity

Retained deficit - unappropriated 10,050,337,573 257,892,459 - 10,308,230,032

UNIT : BAHT

Separate financial statements

Effect from Thai Financial Reporting Standards

As at Group of TFRS 16 As at

December 31, financial January 1,

2019 instruments 2020

Statements of financial position

Assets

Current assets

Current investments 42,261,195 (42,261,195) - -

Trade and other current receivables 1,036,373,329 (267,615,838) - 768,757,491

Other current financial assets - 42,261,195 - 42,261,195

Non-current assets

Other long-term investment 45,814,200 (45,814,200) - -

Right-of-use assets - - 13,522,274,385 13,522,274,385

Deposits at bank pledged as collateral 960,659,498 (960,659,498) - -

Other non-current financial assets - 1,006,473,698 - 1,006,473,698

Liabilities

Current liabilities

Current portion of lease liabilities - - 1,860,528,351 1,860,528,351

Non-current liabilities

Lease liabilities - - 11,661,746,034 11,661,746,034

Shareholders’ equity

Retained deficit - unappropriated 8,776,445,269 267,615,838 - 9,044,061,107

- 8 -

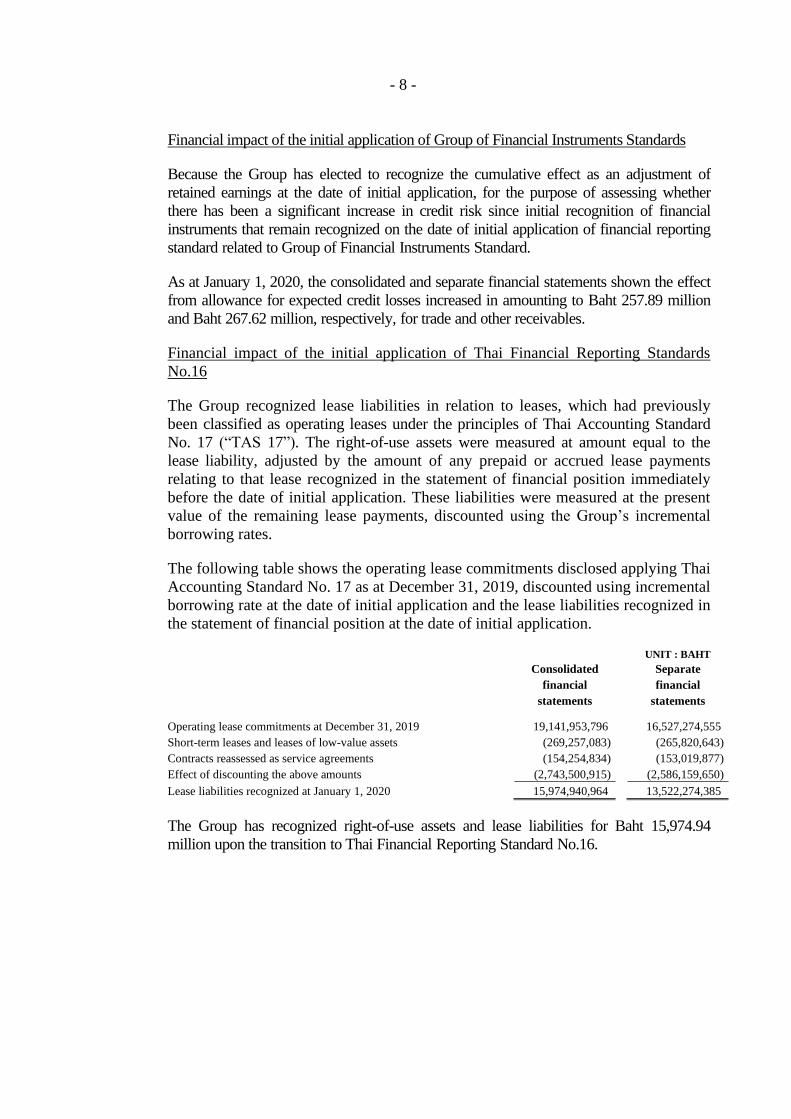

Financial impact of the initial application of Group of Financial Instruments Standards

Because the Group has elected to recognize the cumulative effect as an adjustment of

retained earnings at the date of initial application, for the purpose of assessing whether

there has been a significant increase in credit risk since initial recognition of financial

instruments that remain recognized on the date of initial application of financial reporting

standard related to Group of Financial Instruments Standard.

As at January 1, 2020, the consolidated and separate financial statements shown the effect

from allowance for expected credit losses increased in amounting to Baht 257.89 million

and Baht 267.62 million, respectively, for trade and other receivables.

Financial impact of the initial application of Thai Financial Reporting Standards

No.16

The Group recognized lease liabilities in relation to leases, which had previously

been classified as operating leases under the principles of Thai Accounting Standard

No. 17 (“TAS 17”). The right-of-use assets were measured at amount equal to the

lease liability, adjusted by the amount of any prepaid or accrued lease payments

relating to that lease recognized in the statement of financial position immediately

before the date of initial application. These liabilities were measured at the present

value of the remaining lease payments, discounted using the Group’s incremental

borrowing rates.

The following table shows the operating lease commitments disclosed applying Thai

Accounting Standard No. 17 as at December 31, 2019, discounted using incremental

borrowing rate at the date of initial application and the lease liabilities recognized in

the statement of financial position at the date of initial application.

UNIT : BAHT Consolidated Separate

financial financial

statements statements

Operating lease commitments at December 31, 2019 19,141,953,796 16,527,274,555

Short-term leases and leases of low-value assets (269,257,083) (265,820,643)

Contracts reassessed as service agreements (154,254,834) (153,019,877)

Effect of discounting the above amounts (2,743,500,915) (2,586,159,650)

Lease liabilities recognized at January 1, 2020 15,974,940,964 13,522,274,385

The Group has recognized right-of-use assets and lease liabilities for Baht 15,974.94

million upon the transition to Thai Financial Reporting Standard No.16.

- 9 -

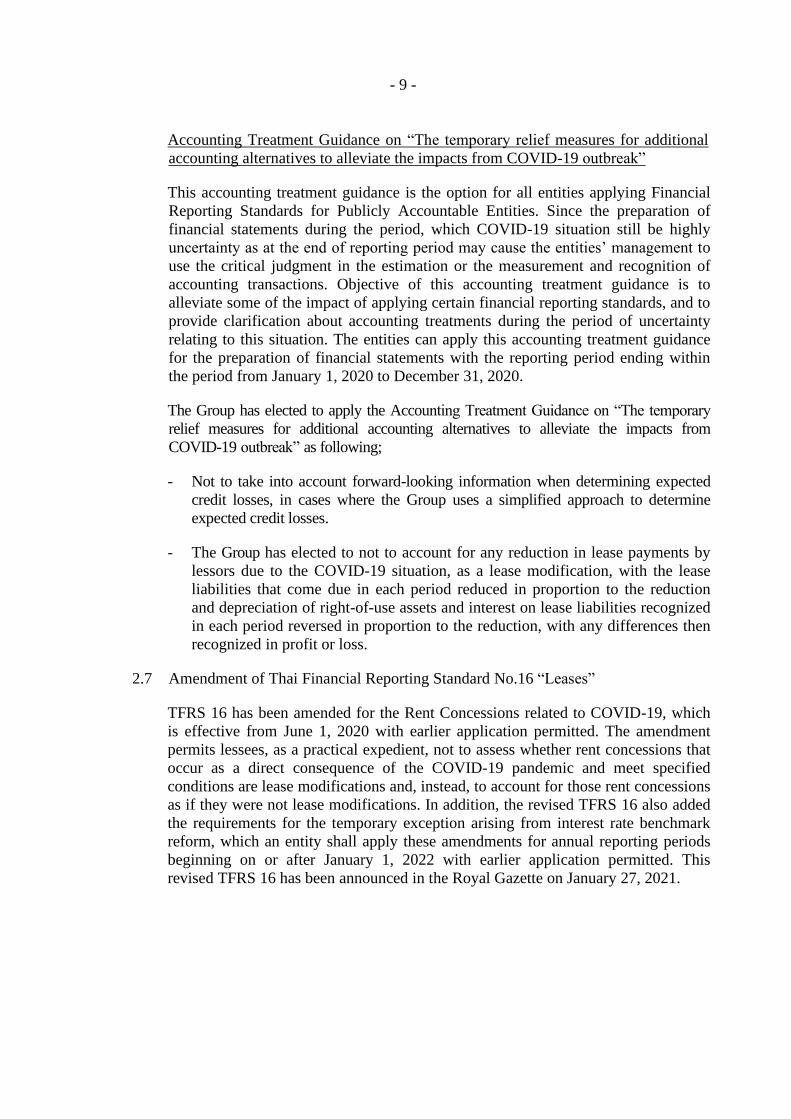

Accounting Treatment Guidance on “The temporary relief measures for additional

accounting alternatives to alleviate the impacts from COVID-19 outbreak”

This accounting treatment guidance is the option for all entities applying Financial

Reporting Standards for Publicly Accountable Entities. Since the preparation of

financial statements during the period, which COVID-19 situation still be highly

uncertainty as at the end of reporting period may cause the entities’ management to

use the critical judgment in the estimation or the measurement and recognition of

accounting transactions. Objective of this accounting treatment guidance is to

alleviate some of the impact of applying certain financial reporting standards, and to

provide clarification about accounting treatments during the period of uncertainty

relating to this situation. The entities can apply this accounting treatment guidance

for the preparation of financial statements with the reporting period ending within

the period from January 1, 2020 to December 31, 2020.

The Group has elected to apply the Accounting Treatment Guidance on “The temporary

relief measures for additional accounting alternatives to alleviate the impacts from

COVID-19 outbreak” as following;

- Not to take into account forward-looking information when determining expected

credit losses, in cases where the Group uses a simplified approach to determine

expected credit losses.

- The Group has elected to not to account for any reduction in lease payments by

lessors due to the COVID-19 situation, as a lease modification, with the lease

liabilities that come due in each period reduced in proportion to the reduction

and depreciation of right-of-use assets and interest on lease liabilities recognized

in each period reversed in proportion to the reduction, with any differences then

recognized in profit or loss.

2.7 Amendment of Thai Financial Reporting Standard No.16 “Leases”

TFRS 16 has been amended for the Rent Concessions related to COVID-19, which

is effective from June 1, 2020 with earlier application permitted. The amendment

permits lessees, as a practical expedient, not to assess whether rent concessions that

occur as a direct consequence of the COVID-19 pandemic and meet specified

conditions are lease modifications and, instead, to account for those rent concessions

as if they were not lease modifications. In addition, the revised TFRS 16 also added

the requirements for the temporary exception arising from interest rate benchmark

reform, which an entity shall apply these amendments for annual reporting periods

beginning on or after January 1, 2022 with earlier application permitted. This

revised TFRS 16 has been announced in the Royal Gazette on January 27, 2021.

- 10 -

In addition, the 2021 amendment to TFRS 16 - Phase 2 has been announced in the

Royal Gazette on May 13, 2021, which permits a lessee to apply the practical

expedient regarding COVID-19-related rent concessions to rent concessions for

which any reduction in lease payments affects only payments originally due on or

before June 30, 2022. lessee shall apply this amendment for annual reporting

periods beginning on or after April 1, 2021 with earlier application is permitted.

The Group’s management will adopt such TFRSs in the preparation of the company’s

financial statements when it becomes effective. Also, the Group’s management is in the

process to assess the impact of these TFRSs on the financial statements of the Group in

the period of initial application.

2.8 Thai Financial Reporting Standards announced in the Royal Gazette but not yet effective

The Federation of Accounting Professions has issued the Notification regarding Thai

Accounting Standards, Thai Financial Reporting Standards, Thai Accounting Standards

Interpretation and Thai Financial Reporting Standard Interpretation, which have been

announced in the Royal Gazette and will be effective for the financial statements for the

period beginning on or after January 1, 2021 onwards. These financial reporting standards

were aimed at alignment with the corresponding International Financial Reporting

Standards, with most of the changes directed towards revisions to references to the

Conceptual Framework in TFRSs, the amendment for definition and accounting

requirements as follows:

Conceptual Framework for Financial Reporting

The revised Conceptual Framework for Financial Reporting consisted of the revised

definitions and recognition criteria of asset and liability as well as new guidance on

measurement, derecognition of asset and liability, presentation and disclosure. In addition,

this Conceptual Framework for Financial Reporting clearly clarifies management’s

stewardship of the entity’s economic resources, prudence, and measurement uncertainty

of financial information.

Definition of Business

The revised Thai Financial Reporting Standard No.3 “Business Combinations”

clearly clarifies the definition of business and introduce an optional concentration

test. Under the optional concentration test, the acquired set of activities and assets is

not a business if substantially all of the fair value of the gross assets acquired is

concentrated in a single identifiable asset or group of similar assets. This revised

financial reporting standard requires prospective method for such amendment.

Earlier application is permitted.

- 11 -

Definition of Materiality

The revised definition of materiality resulted in the amendment of Thai Accounting

Standards No.1 “Presentation of Financial Statements” and Thai Accounting

Standards No.8 “Accounting Policies, Changes in Accounting Estimates and

Errors”, including other financial reporting standards which refer to materiality. This

amendment is intended to make the definition of material to comply with the

Conceptual Framework which requires prospective method for such amendment.

Earlier application is permitted.

The Interest Rate Reform

Due to the interest rate reform, there are the amendments of specific hedge

accounting requirements in Thai Financial Reporting Standard No.9 “Financial

Instruments” and Thai Financial Reporting Standard No.7 “Financial Instruments:

Disclosures”.

In addition, the Federation of Accounting Professions has issued the Notification

regarding Thai Financial Reporting Standards (“TFRSs”) that are relevant to Interest

Rate Benchmark Reform Phase 2 amendments (“Phase 2 amendments”) and amends

Thai Financial Reporting Standards No. 4 “Insurance Contracts”, Thai Financial

Reporting Standards No. 7 “Financial Instruments: Disclosures” and Thai Financial

Reporting Standards No. 9 “Financial Instruments”. The Phase 2 amendments

address issues that might affect financial reporting during the reform of an interest

rate benchmark, including the effects of changes to contractual cash flows or

hedging relationships arising from the replacement of an interest rate benchmark

with an alternative benchmark rate. Such TFRSs have been announced in the Royal

Gazette on June 28, 2021 and will be effective for the financial statements for the

periods beginning on or after January 1, 2022 onwards with earlier application

permitted.

The Group’s management will adopt such TFRSs in the preparation of the company’s

financial statements when it becomes effective. Also, the Group’s management is in the

process to assess the impact of these TFRSs on the financial statements of the Group

in the period of initial application.

3. SIGNIFICANT ACCOUNTING POLICIES

3.1 Basis of preparation of the consolidation financial statements

The Consolidated financial statements comprise the Company and its subsidiaries’

financial statements and the Group’s interest in associates and joint ventures.

Transactions eliminated on consolidation financial statements

Significant intra-group balances and transactions have been eliminated in the preparation

of the consolidated financial statements. The consolidated financial statements for the

years ended December 31, 2020 and 2019 were prepared by using the financial statements

of its subsidiaries, associates and joint ventures as of the same date.

- 12 -

3.2 Foreign currencies

Transactions in foreign currencies incurred during the year are converted to Baht at

the exchange rate of the transaction date. Monetary assets and liabilities

denominated in foreign currencies at the reporting date are converted into Baht at

the reference exchange rates established by the Bank of Thailand at that date.

Gain or loss from settlements and conversion are recognized in the statement of

profit or loss and other comprehensive income.

3.3 Cash and cash equivalents

Cash and cash equivalents consist of cash on hand and all types of deposit at

financial institution and certificate of deposits with maturity date within 3 months,

excluding deposits at financial institution used as collateral.

3.4 Trade and other current receivables

a) Policies applicable prior to January 1, 2020

Trade receivables and other receivables are stated at their invoice value less allowance

for doubtful accounts.

The Group are accounted allowance for doubtful debts is provided for the estimated

collection losses that may incur in collection of receivables. The allowance for

doubtful accounts is based on collection experience and current status of receivables

outstanding at the statement of financial position date.

b) Policies applicable from January 1, 2020

Trade receivables and other receivables are stated at their invoice value less

allowance for expected credit losses.

The allowance for expected credit losses has disclosed in Note 3.7.

3.5 Inventories

Inventories are stated at the lower of cost or net realizable value.

Cost is determined by weighted average method. Net realizable value is the estimate of

the selling price in the ordinary course of business less the estimated costs necessary

to make sale.

3.6 Current investments and other long-term investments

a) Policies applicable prior to January 1, 2020

Current investment

Current investment consisting of deposit at banks having a maturity exceeding

3 months but less than 12 months is presented at cost and is not used as collateral.

- 13 -

Other long-term investments

Other long-term investments are non-marketable equity securities which are

stated at cost less any impairment losses (if any).

Disposal of investments

On disposal of an investment, the difference between net disposal proceeds and

the carrying amount is recognized as profit or loss in the statement of profit or loss

and other comprehensive income.

If the Group disposes of a partial of its holding investment, the deemed cost of

the sold investment and holding investment is determined using the weighted-

average method applied to the carrying value of the total holding of the

investment.

b) Policies applicable from January 1, 2020, has disclosed in Note 3.7.

3.7 Financial instruments

Policies applicable from January 1, 2020

Financial assets and financial liabilities are initially measured at fair value. Transaction

costs that are directly attributable to the acquisition or issuance of financial assets and

financial liabilities (other than financial assets and financial liabilities at fair value

through profit or loss) are added to or deducted from the fair value of the financial assets

or financial liabilities, as appropriate, on initial recognition. Transaction costs directly

attributable to the acquisition of financial assets or financial liabilities at fair value

through profit or loss are recognized immediately in profit or loss.

Financial assets

All recognized financial assets are measured subsequently in their entirely at either

amortized cost or fair value, depending on the classification of the financial assets.

Classification of financial assets

Debt instruments that meet the following conditions are measured subsequently at

amortized cost;

• The financial asset is held within a business model whose objective is to hold

financial assets in order to collect contractual cash flows; and

• The contractual terms of the financial asset give rise on specified dates to cash flows

that are solely payments of principal and interest on the principal amount

outstanding.

- 14 -

By default, all other financial assets are measured subsequently at fair value through

profit or loss (FVTPL).

Impairment of financial assets

The Group recognizes a loss allowance for expected credit losses on investments in debt

instruments that are measured at amortized cost or at FVTOCI, lease receivables, trade

receivables and contract assets. The amount of expect credit losses is updated at each

reporting period date to reflect changes in credit risk since initial recognition of the

respective financial instrument.

The Group always recognizes allowance for lifetime ECL for trade receivables, contract

assets and lease receivables. The expected credit losses on these financial assets are

estimated using a provision matrix based on the Group’s historical credit loss

experience, adjusted for factors that are specific to the debtors, general economic

conditions and an assessment of both the current as well as the forecast direction of

conditions at the reporting date, including time value of money where appropriate.

For all other financial instruments, the Group recognizes allowance for lifetime ECL

when there has been a significant increase in credit risk since initial recognition.

However, if the credit risk on the financial instrument has not increased significantly

since initial recognition, the Group measures the loss allowance for that financial

instrument at an amount equal to 12-month ECL.

Lifetime ECL represents the expected credit losses that will result from all possible

default events over the expected life of a financial instrument. In contrast, 12-month

ECL represents the portion of lifetime ECL that is expected to result from default events

on a financial instrument that are possible within 12 months after the reporting date.

(i) Write-off policy

The Group writes off a financial asset when there is information indicating that the

debtor is in severe financial difficulty and there is no realistic prospect of

recovery. Financial assets written off may still be subject to enforcement activities

under the Group’s recovery procedures, taking into account legal advice where

appropriate. Any recoveries made are recognized in profit or loss.

(ii) Measurement and recognition of expected credit losses

The measurement of expected credit losses is a function of the probability of default,

loss given default (i.e. the magnitude of the loss if there is a default) and the

exposure at default. The assessment of the probability of default and loss given

default is based on historical data adjusted by forward-looking information. As for

the exposure at default, for financial assets, this is represented by the asset’s gross

carrying amount at the reporting date, the Group’s understanding of the specific

future financing needs of the debtors, and other relevant forward-looking

information.

- 15 -

For financial assets, the expected credit loss is estimated as the difference between all

contractual cash flows that are due to the Group in accordance with the contract and all

the cash flows that the Group expects to receive, discounted at the original effective

interest rate. For a lease receivable, the cash flows used for determining the expected

credit losses is consistent with the cash flows used in measuring the lease receivable in

accordance with TFRS 16 “Leases”.

The Group recognizes an impairment gain or loss in profit or loss for all financial

instruments with a corresponding adjustment to their carrying amount through a loss

allowance account, except for investments in debt instruments that are measured at

FVTOCI, for which the loss allowance is recognized in other comprehensive income

and accumulated in the investment revaluation reserve, and does not reduce the carrying

amount of the financial asset in the statement of financial position.

Derecognition of financial assets

The Group derecognizes a financial asset only when the contractual rights to the cash

flows from the asset expire, or when it transfers the financial asset and substantially all

the risks and rewards of ownership of the asset to another entity. If the Group neither

transfers nor retains substantially all the risks and rewards of ownership and continues to

control the transferred asset, the Group recognizes its retained interest in the asset and an

associated liability for amounts it may have to pay. If the Group retains substantially all

the risks and rewards of ownership of a transferred financial asset, the Group continues

to recognize the financial asset and also recognizes a collateralized borrowing for the

proceeds received.

On derecognition of a financial asset measured at amortized cost, the difference between

the asset’s carrying amount and the sum of the consideration received and receivable is

recognized in profit or loss. In addition, on derecognition of an investment in a debt

instrument classified as at FVTOCI, the cumulative gain or loss previously accumulated

in the investments revaluation reserve is reclassified to profit or loss. In contrast, on

derecognition of an investment in equity instrument which the Group has elected on

initial recognition to measure at FVTOCI, the cumulative gain or loss previously

accumulated in the investments revaluation reserve is not reclassified to profit or loss,

but is transferred to retained earnings.

Financial liabilities

All financial liabilities are measured subsequently at amortized cost using the effective

interest method or at FVTPL.

However, financial liabilities that arise when a transfer of a financial asset does not

qualify for derecognition or when the continuing involvement approach applies.

- 16 -

Financial liabilities are measured subsequently at amortized cost

Financial liabilities that are not; (i) contingent consideration of an acquirer in a business

combination (ii) held for trading or (iii) it is designated as at FVTPL or measured

subsequently at amortized cost using the effective interest method.

The effective interest method is a method of calculating the amortized cost of a financial

liability and of allocating interest expense over the relevant period. The effective interest

rate is the rate that exactly discounts estimated future cash payments (including all fees

and points paid or received that form an integral part of the effective interest rate,

transaction costs and other premiums or discounts) through the expected life of the

financial liability, or (where appropriate) a shorter period, to the amortized cost of a

financial liability.

Derecognition of financial liabilities

The Group derecognizes financial liabilities when, and only when, the Group’s

obligations are discharged, cancelled or have expired. The difference between the

carrying amount of the financial liability derecognized and the consideration paid and

payable is recognized in profit or loss.

When the Group exchanges with the existing lender one debt instrument into another

one with the substantially different terms, such exchange is accounted for as an

extinguishment of the original financial liability and the recognition of a new financial

liability. Similarly, the Group accounts for substantial modification of terms of an

existing liability or part of it as an extinguishment of the original financial liability and

the recognition of a new liability. It is assumed that the terms are substantially different

if the discounted present value of the cash flows under the new terms, including any fees

paid net of any fees received and discounted using the original effective rate is at least

10 percent different from the discounted present value of the remaining cash flows of

the original financial liability. If the modification is not substantial, the difference

between; (1) the carrying amount of the liability before the modification; and (2) the

present value of cash flows after modification should be recognized in profit or loss as

the modification gain or loss within other gains and losses.

3.8 Investments in subsidiaries, associates and joint ventures

Investments in subsidiaries, associates and joint ventures in the separate financial

statements of the Company are accounted for using the cost, less impairment losses

(if any). Investments in associates and joint ventures in the consolidated financial

statements are accounted for using the equity method.

An associate is an entity which the Group has significant influence. Significant

influence is the power to participate in the financial and operating policy decisions of

the investee but is not control or joint control over those policies.

- 17 -

A joint venture is a joint arrangement whereby the parties that have joint control of the

arrangement have rights to the net assets of the joint arrangement. Joint control is the

contractually agreed sharing of control of an arrangement, which exists only when

decisions about the relevant activities require unanimous consent of the parties sharing

control.

Under the equity method, an investment in an associate or a joint venture is initially

recognized in the consolidated statement of financial position at cost and adjusted

thereafter to recognize the Group’s share of the profit or loss and other comprehensive

income of the associate or joint venture. When the Group’s share of losses of an

associate or a joint venture equals or exceeds the Group’s interest in that associate or

joint venture (which includes any long-term interests that, in substance, form part of the

Group’s net investment in the associate or joint venture), the Group discontinues

recognizing its share of further losses. Additional losses are recognized only to the

extent that the Group has incurred legal or constructive obligations or made payments