REPORT OF THE AUDITOR GENERAL ON THE FINANCIAL STATEMENTS ... · PDF filereport of the auditor...

27

` THE REPUBLIC OF UGANDA REPORT OF THE AUDITOR GENERAL ON THE FINANCIAL STATEMENTS OF UGANDA POST LIMITED FOR THE YEAR ENDED 30 TH JUNE 2015 OFFICE OF THE AUDITOR GENERAL KAMPALA, UGANDA

Transcript of REPORT OF THE AUDITOR GENERAL ON THE FINANCIAL STATEMENTS ... · PDF filereport of the auditor...

`

THE REPUBLIC OF UGANDA

REPORT OF THE AUDITOR GENERAL ON THE FINANCIAL STATEMENTS OF

UGANDA POST LIMITED

FOR THE YEAR ENDED 30TH JUNE 2015

OFFICE OF THE AUDITOR GENERAL

KAMPALA, UGANDA

ii

TABLE OF CONTENTS

LIST OF ACRONYMS ...................................................................................................... iii

REPORT OF THE AUDITOR GENERAL ON THE FINANCIAL STATEMENTS OF UGANDA POST

LIMITED FOR THE YEAR ENDED 30TH JUNE, 2015 ........................................................... iv

1.0 INTRODUCTION ................................................................................................. 1

2.0 BACKGROUND INFORMATION ............................................................................. 1

3.0 ENTITY FINANCING ............................................................................................ 1

4.0 OBJECTIVES OF THE COMPANY ........................................................................... 2

5.0 AUDIT SCOPE .................................................................................................... 2

6.0 AUDIT PROCEDURES PERFORMED ....................................................................... 3

7.0 CATEGORIZATION AND SUMMARY OF FINDINGS .................................................. 4

7.1 Categorization of findings .................................................................................... 4

7.2 Summary of Findings .......................................................................................... 4

8.0 DETAILED FINDINGS .......................................................................................... 4

8.1 Sustainability of services –Liquidity analysis .......................................................... 4

8.2 Long overdue Trade and other Receivables ........................................................... 5

8.3 Trade and Other Payables ................................................................................... 6

8.4 Prior year adjustments ........................................................................................ 7

8.5 Lack of documented credit and debt policies ......................................................... 7

8.6 Revenue ............................................................................................................ 8

8.7 Statutory deduction remittances ......................................................................... 10

8.8 Budget Performance .......................................................................................... 12

8.9 Field inspections ................................................................................................ 14

8.10 Status of prior year audit recommendations ......................................................... 16

iii

LIST OF ACRONYMS

Acronym Meaning

NSSF National Social Security Fund

EMS Express Mail Services

DPO District Post Office

ICT Information and Communications Technology

LST Local Service Tax

MoFPED Ministry of Finance, Planning and Economic Development

MoWT Ministry of Works and Transport

NSSF National Social Security Fund

PAYE Pay As You Earn

PBU Post Bank Uganda Limited

UCC Uganda Communications Commission

UGX Uganda Shillings

UPL Uganda Post Limited

UPTC Uganda Posts and Telecommunications Corporation

URA Uganda Revenue Authority

UTL Uganda Telecommunications Limited

Cap Chapter

VAT Value Added Tax

IAS International Accounting Standard

WHT Withholding Tax

UPU Universal Postal Union

PFMA Public Finance Management Act, 2015

iv

REPORT OF THE AUDITOR GENERAL ON THE FINANCIAL STATEMENTS OF

UGANDA POST LIMITED

FOR THE YEAR ENDED 30TH JUNE, 2015

THE RT. HON. SPEAKER OF PARLIAMENT

I have audited the financial statements of Uganda Post Limited for the year ended 30th June

2015. These financial statements comprise of the statement of financial position as at 30th

June 2015, Statement of comprehensive income, statement of changes in equity and cash

flow statement together with other accompanying schedules, notes and accounting policies.

Management Responsibility

Under section 17 of the Public Enterprises Reform and Divesture (PERD) Act and the

Company’s Act (Cap 98, Laws of Uganda), the Directors of the company are responsible for

the preparation of the financial statements which give a true and fair view of the Company’s

state of affairs and its profit or loss in accordance with International Financial Reporting

Standards. This responsibility includes designing implementing and maintaining internal

controls relevant to the preparation and fair presentation of financial statements that are

free from material misstatement, whether due to fraud or error, selecting and applying

appropriate accounting policies and making accounting estimates that are reasonable in the

circumstances.

Auditor’s Responsibility

My responsibility as required by Article 163 of the Constitution of the Republic of Uganda,

1995 (as amended), Section 17 of the Public enterprises Reform and Divesture Act (Cap 98)

and Sections 13 and 19 of the National Audit Act, 2008 is to audit and express an opinion on

these statements based on my audit. I conducted the audit in accordance with International

Standards on Auditing. Those standards require that I comply with the ethical requirements

and plan and perform the audit to obtain reasonable assurance whether the financial

statements are free from material misstatement.

An audit involves performing audit procedures to obtain evidence about the amounts and

disclosures in the financial statements as well as evidence supporting compliance with

relevant laws and regulations. The procedures selected depend on the Auditor’s judgment

including the assessment of risks of material misstatement of financial statements whether

due to fraud or error. In making those risk assessments, the Auditor considers internal

control relevant to the entity’s preparation and fair presentation of financial statements in

order to design audit procedures that are appropriate in the circumstances but not for

purposes of expressing an opinion on the effectiveness of the entity’s internal control. An

v

audit also includes evaluating the appropriateness of accounting policies used and the

reasonableness of accounting estimates made by management as well as evaluating the

overall presentation of the financial statements. I believe that the audit evidence I have

obtained is sufficient and appropriate to provide a basis for my audit opinion.

Part ‘‘A’’ of this report sets out my opinion on the financial statements. Part “B” which forms

an integral part of this report presents in detail all the significant audit findings made during

the audit which have been brought to the attention of management.

PART “A”

Opinion

In my opinion, the financial statements of Uganda Post Limited, for the year ended 30th

June, 2015 are prepared, in all material respects, in accordance with the International

Financial Reporting Standards and the PERD Act (Cap 98, Laws of Uganda).

Emphasis of matter

Without qualifying my opinion, I draw your attention to the following matters disclosed in

the financial statements that, in my judgment, are of such importance and fundamental to

the user’s understanding of the financial statements, which are also included in part “B” of

this report.

Sustainability of services

Ratio analysis of the financial information revealed that Uganda Post Limited current ratio

and quick ratio were not healthy and yet the company’s total liabilities had increased from

the previous year by 12%. Furthermore, Uganda Post Limited has a contingent liability of

UGX.1,663,800,000 in which former employees sued for pension claims and Judgment was

entered in their favour.

Long overdue receivables

The trade and other receivables increased from UGX.8,677,115,840 to UGX.12,727,659,700

(representing 47% increase from the previous year’s balance) contrary to Paragraph 8.4.4 of

the Posta Uganda financial manual that requires all invoices to be collected within sixty days

from date of invoicing.

vi

Trade and Other Payables UGX.15,549,969,730

The trade and other payables increased by 29% from UGX.12,052,739,660 in 2014 to

UGX.15,549,969,730 in the current year which is quite significant besides, 71% of the

Payables (UGX.8,235,411,925) were well beyond 180 days against which creditors should

have been settled promptly.

Report on other Legal Requirements

As required by the Companies Act, I report based on the audit that;

(i) All information and explanations which to the best of my knowledge and belief was

necessary for the purposes of the audit was obtained.

(ii) proper books of account have been kept by the Company, so far as appears from my

examination of those books, and

(iii) The Company’s statement of financial position and statement of comprehensive income

are in agreement with the books of account.

John F.S. Muwanga

AUDITOR GENERAL

KAMPALA

15th December, 2015

REPORT OF THE AUDITOR GENERAL AND SUPPLEMENTARY INFORMATION

1

PART "B"

DETAILED REPORT OF THE AUDITOR GENERAL ON THE FINANCIAL STATEMENTS

OF UGANDA POST LIMITED FOR THE YEAR ENDED 30TH JUNE, 2015

This Section outlines the detailed audit findings, management responses, and my

recommendations in respect thereof.

1.0 INTRODUCTION

Article 163 (3) of the Constitution of the Republic of Uganda, 1995 (as amended)

requires me to audit and report on the public accounts of Uganda and all public

offices including the courts, the central and local government administrations,

universities, and public institutions of the like nature and any public corporation or

other bodies or organizations established by an Act of Parliament. Accordingly, I

carried out the audit of Uganda Post Limited (UPL) to enable me report to

Parliament.

2.0 BACKGROUND INFORMATION

Uganda Post Limited (UPL) trading as M/s Posta Uganda was established in 1998

under the Communications Act 1997 when the then Uganda Posts and

Telecommunications Corporation (UPTC) was unbundled into four entities namely:

Uganda Post Ltd (UPL), Uganda Telecommunications Ltd (UTL), Post Bank Uganda

Ltd (PBU), and Uganda Communications Commission (UCC). Uganda Post Limited

was incorporated as a limited liability company on 19th February 1998 to take over as

a going concern, the postal activities of the former UPTC. In November 2002, UPL

under new management launched the new trade name “Posta Uganda” and logo in a

bid to restore customer confidence and satisfaction in the services rendered by the

company.

The shareholders of Posta Uganda are the Ministry of Finance, Planning and

Economic Development (MoFPED) with 999,999 ordinary shares and Ministry of

Works and Transport (MoWT) with 1 (one) ordinary share. However, operationally,

the company reports to the Ministry of Information and Communications Technology.

The Head Office is located on Plot 35 Kampala Road with over 300 branches located

across the country in 30 major towns.

3.0 ENTITY FINANCING

The entity was financed by internally generated revenue. Revenue amounting to

UGX.18,984,688,000 was received. Expenses of UGX.18,456,395,000 were incurred,

2

leaving a profit for the year of UGX.528,293,000. The entity also carried out

revaluation of its non-current assets from which a net revaluation reserve of

UGX.1,880,000,000 was realized.

4.0 OBJECTIVES OF THE COMPANY

The Company was created with the following objectives:-

Enhancing national coverage of the communications services.

Reducing Government direct role as an operator in the sector.

Encouraging the participation of private investors in the development of the

sector.

Minimizing all direct and indirect subsidies paid by Government to the

communications sector and for communications services.

The Company offers a wide range of postal, communications, financial and logistical

services to domestic and international customers and clients. The services offered

include:-

Private (written) communications;

Business communications (business mail, bank statements, invoices,

advertisements;

Courier services (EMS);

Counter services (traditional counter and agency services);

Financial services (Money orders);

Logistics (passenger and parcel transport services);

Post Shop;

Post Box Rentals.

5.0 AUDIT SCOPE

The audit was carried out in accordance with International Standards on Auditing and

accordingly included a review of the accounting records and agreed procedures as

was considered necessary. In conducting my reviews, special attention was paid to

establish whether:-

a. The financial statements have been prepared in accordance with consistently

applied Accounting Policies and fairly present the revenues and expenditures

for the period and of the financial position as at the end of the period.

b. All Company funds were utilized with due attention to economy and efficiency

and only for the purposes for which the funds were provided.

3

c. Goods and services financed have been procured in accordance with the

Government of Uganda procurement regulations.

d. To evaluate and obtain a sufficient understanding of the internal control

structure of the company, assess control risk and identify reportable

conditions, including material internal control weaknesses.

e. The Company Management was in compliance with the Government of

Uganda financial regulations and guidelines.

f. All necessary supporting documents, records and accounts have been kept in

respect of all Company activities, and are in agreement with the financial

statements presented.

6.0 AUDIT PROCEDURES PERFORMED

The following audit procedures were undertaken:-

a. Revenue/Receipts

Obtained all schedules of receipts and reconciled the amounts to the Company

cashbooks and bank statements.

b. Expenditure

Vouched transactions to establish whether documentation in support of

expenditure agreed with the amount and description on the vouchers and/or

applications and bank statements, and was properly controlled and accounted

for.

c. Internal Control System

Reviewed the internal control system and its operations to establish whether

sound controls were applied throughout the period.

d. Procurement

Reviewed the procurement of goods and services under the Company during the

period under review and reconciled with the approved procurement plan.

e. Fixed Assets Management

Reviewed the use and management of the assets of the Company during the

period under review.

f. Financial Statements

Examined, on a test basis, evidence supporting the amounts and disclosures in

the financial statements; assessed the accounting principles used and significant

estimates made by management; as well as evaluating the overall financial

statement presentation.

4

7.0 CATEGORIZATION AND SUMMARY OF FINDINGS

7.1 Categorization of findings

The following system of profiling of the audit findings is used to prioritise the

implementation of audit recommendations:

No Category Description

1 High significance Has a significant/material impact, has a high likelihood of

reoccurrence, and in the opinion of the Auditor General, it

requires urgent remedial action. It is a matter of high risk or

high stakeholder interest.

2 Moderate significance Has a moderate impact, has a likelihood of reoccurrence,

and in the opinion of the Auditor General, it requires

remedial action. It is a matter of medium risk or moderate

stakeholder interest.

3 Low significance Has a low impact, has a remote likelihood of reoccurrence,

and in the opinion of the Auditor General, may not require

much attention, though its remediation may add value to the

entity. It is a matter of low risk or low stakeholder interest.

7.2 Summary of Findings

No Finding Significance

8.1 Sustainability of services –Liquidity analysis High

8.2 Trade and other Receivables- UGX.12,727,659,700 High

8.3 Trade and Other Payables -UGX.15,549,969,730 High

8.4 Misstatement of prior year balances–UGX 906,151,209 High

8.5 Lack of documented credit and debt policies Moderate

8.6 Revenue Moderate

8.7 Statutory deductions remittances Moderate

8.8 Budget performance Moderate

8.9 Field inspections Moderate

8.10 Status of prior year audit recommendations Moderate

8.0 DETAILED FINDINGS

8.1 Sustainability of services –Liquidity analysis

I carried out ratio analysis of financial information and the following were observed

for the attention of management for improvement purposes and ensure sustainability

of services:

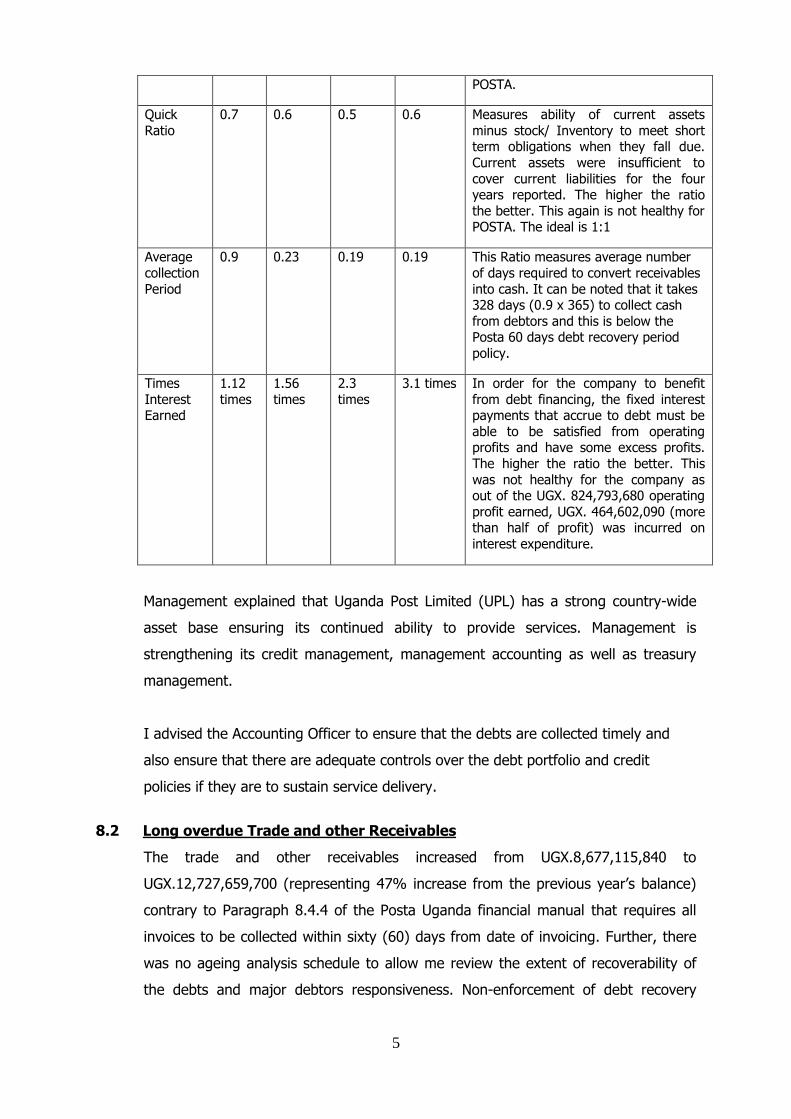

YEAR 2015 2014 2013 2012 IMPLICATIONS AND REMARKS

Current Ratio

1.08 times

1.04 times

1.01 times

0.90 times

Measures company’s ability to meet short term liabilities when they fall due.

Current assets were not adequate to cover current liabilities in all the years.

The higher the ratio the better and

ideal is 2:1 This is not healthy for

5

POSTA.

Quick

Ratio

0.7 0.6 0.5 0.6 Measures ability of current assets

minus stock/ Inventory to meet short term obligations when they fall due.

Current assets were insufficient to

cover current liabilities for the four years reported. The higher the ratio

the better. This again is not healthy for POSTA. The ideal is 1:1

Average

collection

Period

0.9 0.23 0.19 0.19 This Ratio measures average number

of days required to convert receivables

into cash. It can be noted that it takes 328 days (0.9 x 365) to collect cash

from debtors and this is below the Posta 60 days debt recovery period

policy.

Times

Interest Earned

1.12

times

1.56

times

2.3

times

3.1 times In order for the company to benefit

from debt financing, the fixed interest payments that accrue to debt must be

able to be satisfied from operating profits and have some excess profits.

The higher the ratio the better. This

was not healthy for the company as out of the UGX. 824,793,680 operating

profit earned, UGX. 464,602,090 (more than half of profit) was incurred on

interest expenditure.

Management explained that Uganda Post Limited (UPL) has a strong country-wide

asset base ensuring its continued ability to provide services. Management is

strengthening its credit management, management accounting as well as treasury

management.

I advised the Accounting Officer to ensure that the debts are collected timely and

also ensure that there are adequate controls over the debt portfolio and credit

policies if they are to sustain service delivery.

8.2 Long overdue Trade and other Receivables

The trade and other receivables increased from UGX.8,677,115,840 to

UGX.12,727,659,700 (representing 47% increase from the previous year’s balance)

contrary to Paragraph 8.4.4 of the Posta Uganda financial manual that requires all

invoices to be collected within sixty (60) days from date of invoicing. Further, there

was no ageing analysis schedule to allow me review the extent of recoverability of

the debts and major debtors responsiveness. Non-enforcement of debt recovery

6

measures hampers service delivery and affects the Company’s debt servicing which

may attract interest on late payments.

Management explained that a debtor Management policy was formulated and

approved by the Board Committee of Finance and this will be effective beginning of

2016. Reconciliation of receivables was ongoing with a view of writing off long

overdue accounts. Management further explained that they had engaged a debt

collection firm to collect overdue accounts. Management has also set up an in-house

debt collection unit to collect recurring debts.

I advised the Accounting Officer to formulate a comprehensive debt policy that gives

adequate guidance on debt management. I also advised that all receivables should

be reconciled with a view of writing off long overdue accounts that are considered

irrecoverable after undertaking some recovery options

8.3 Trade and Other Payables - UGX.15,549,969,730

The trade and other payables increased by 29% from UGX.12,052,739,660 in 2014

to UGX.15,549,969,730 in the current year which is quiet significant and it was

noted that 71% of the Payables (UGX.8,235,411,925) were well beyond 180 days

contrary to the financial regulations that require that creditors to be settled promptly.

Further, contrary to paragraph 2.5.4 (iii) of the financial manual that requires

suppliers accounts to be reconciled monthly, the company was not compliant and

this has created a numbr of adjustments relating to prior-year periods thus casting

doubt as to the accuracy and completeness of the current year creditors balances.

Without monthly reconciliations, I was not able to confirm that the company’s trade

payables were complete, accurate and properly measured which could be misleading

to the users. Further, the company is at risk of litigation for delays to settle their

accounts.

Management explained that a draft Credit Management Policy was to be presented to

the Board Committee of Finance for approval. Further, management explained that

remedial action had been taken to correct book keeping errors and ledger

adjustments were made to match payments to accruals.

I advised the Accounting Officer to settle obligations as they fall due and ensure that

regular reconciliations of payables accounts are undertaken to eliminate the

misstated and misleading balances. I await the results of management’s efforts in

regard to approval of a credit policy.

7

8.4 Prior year adjustments

Prior year adjustments of UGX.906,151,210 were made to the retained earnings

brought forward from 2013/14 financial year with authorization of Head of Finance

and approval by the Managing Director. At the time of writing this report,

reconciliations were still on-going. A review of the journal vouchers relating to the

adjustments revealed the following;

Recognition of Electricity expenses for Prior Years

UGX.710,185,429 was recognition of Electricity expenses for Prior Years. This was

due to the fact that Posta did not have a separate meter and was deposing cash with

UTL and not recognizing it as an expense in prior years but as a prepayment. This

has an effect on profits reported in prior years as they were overstated thus

misleading the users.

Misstatement of prior year receivables and payables:

It was noted that a number of other adjustments apart from the one above were a

result of non-recognition of revenue earned and expenses incurred in prior years

with some dating back to the period 2008. Others were due to over invoicing of

clients, invoicing non-existent clients, non-reconciliation of clients’ accounts on

settlement of invoices, and as a result several debtors and creditors on the

company’s books in the previous years could have been misstated.

I noted that such cases may continue to surface in subsequent years especially with

long overdue receivables and payables. The errors impact on current years balances

as comparatives for the prior years are misstated.

Management explained that the errors were a result of past capacity gaps in

accounts section and the need to recognize revenue banked to UPL accounts by

clients which had earlier not been captured in UPL books.

I advised the Accounting Officer to undertake a final review of the receivables and

payable balances so as to present a true position probably through circularizing with

a view of writing off the long overdue unsupported receivables and payables.

8.5 Lack of documented credit and debt policies

UPL did not have a credit and approved debt management policies documented for

the staff to manage credit offered to the Company and debts owed to the Company

by its clients contrary to Paragraph 8.2 of the UPL revised Financial Manual that

8

requires the Head of Finance department in consultation with the Accounting Officer

to be responsible for developing and maintaining the company’s credit policy with its

clients. Further, contrary to section 8.3.2(e) of UPL’s Finance policies and procedures

manual that requires management to fix credit limits for all customers who have

been granted credit facility that in any case should not go beyond three months UPL

had no credit limits set for the customers as the credit facility for most customers

were found to have exceeded the three months.

Lack of an approved debt policy has caused accumulation of uncollected revenue

which has been increasing for the past years with a high possibility of debts

becoming bad. Lack of a credit policy has also caused an accumulation of unsettled

debt obligations which may lead into legal suits to the company.

Management explained that there is a Debtor Management Policy approved by the

Board Committee of Finance. A credit Policy is being formulated and shall be laid

before the Board Committee of Finance at its next scheduled meeting in February

2016.

I advised the Accounting Officer to have the debt policy approved by the Board and

expedite the formulation and documentation of the credit policy.

8.6 Revenue

8.6.1 Rental Revenue - Un-occupied rentable space

A review of the UPL register of rentable space and Internal Audit reports revealed

that the company had 41 un-occupied Rooms/space as at the close of the year which

needed to be rented-out as soon as possible contrary to Paragraph 7.1 (a) of the

Estates Management policy 2012 that requires any property or space that is not

immediately required for use or occupancy by Uganda Post Limited to be rented or

leased. This space would have earned the Company UGX.78,102,392 per quarter if

tenants had been sourced by the business services unit. Details of this are

presented in table below:

No. Location Average period

Remark Area(Sq Metre)/Rate Amount

1 GPO Counters 1 year 5 counters

500,000 per counterx5x3 7,500,000

2 GPO Rooms 30 months 26 27,551,792

3 Postel 1st floor 1 year 9 228.6sqmX$12X3000 24,688,800

4 Jinja DPO 6 months 1 164.9X3000X$4 6,892,200

5 Entebbe DPO 2 years 1 30 sqmX3000X$4 2,880,000

6 Bombo DPO. 6 months 5 rooms 117sqm/100,000x5x3 1,500,000

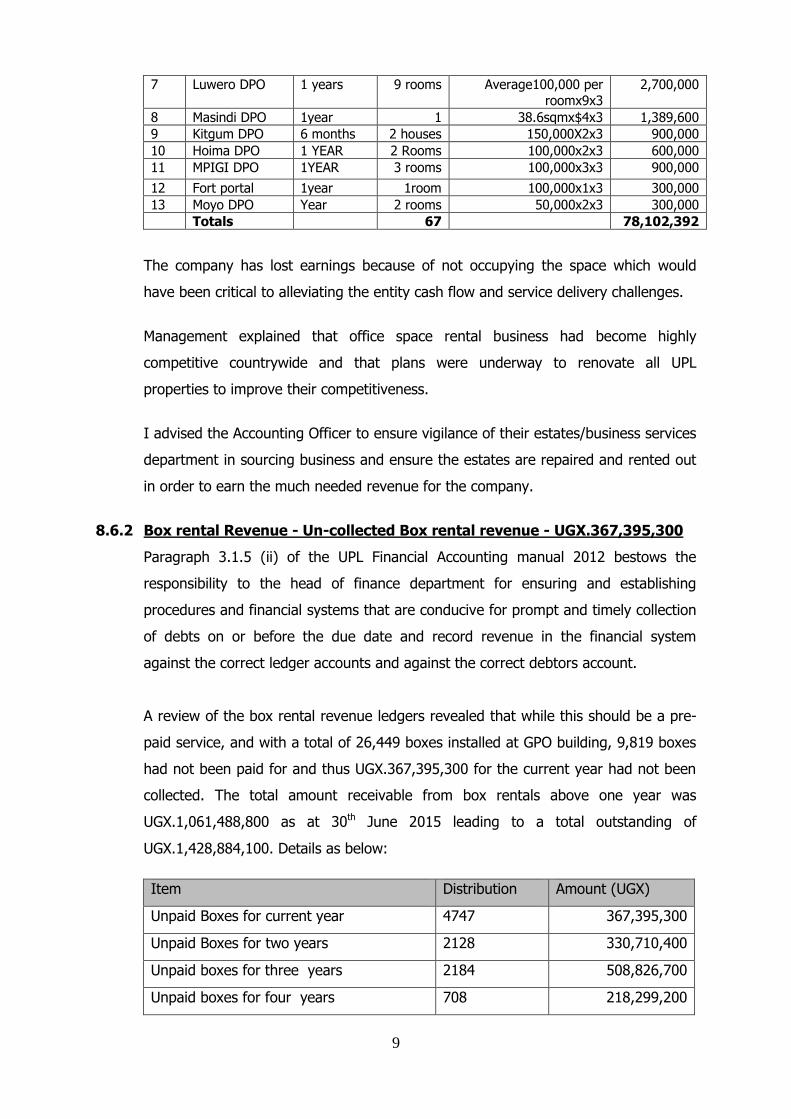

9

7 Luwero DPO 1 years 9 rooms Average100,000 per

roomx9x3

2,700,000

8 Masindi DPO 1year 1 38.6sqmx$4x3 1,389,600

9 Kitgum DPO 6 months 2 houses 150,000X2x3 900,000

10 Hoima DPO 1 YEAR 2 Rooms 100,000x2x3 600,000

11 MPIGI DPO 1YEAR 3 rooms 100,000x3x3 900,000

12 Fort portal 1year 1room 100,000x1x3 300,000

13 Moyo DPO Year 2 rooms 50,000x2x3 300,000

Totals 67 78,102,392

The company has lost earnings because of not occupying the space which would

have been critical to alleviating the entity cash flow and service delivery challenges.

Management explained that office space rental business had become highly

competitive countrywide and that plans were underway to renovate all UPL

properties to improve their competitiveness.

I advised the Accounting Officer to ensure vigilance of their estates/business services

department in sourcing business and ensure the estates are repaired and rented out

in order to earn the much needed revenue for the company.

8.6.2 Box rental Revenue - Un-collected Box rental revenue - UGX.367,395,300

Paragraph 3.1.5 (ii) of the UPL Financial Accounting manual 2012 bestows the

responsibility to the head of finance department for ensuring and establishing

procedures and financial systems that are conducive for prompt and timely collection

of debts on or before the due date and record revenue in the financial system

against the correct ledger accounts and against the correct debtors account.

A review of the box rental revenue ledgers revealed that while this should be a pre-

paid service, and with a total of 26,449 boxes installed at GPO building, 9,819 boxes

had not been paid for and thus UGX.367,395,300 for the current year had not been

collected. The total amount receivable from box rentals above one year was

UGX.1,061,488,800 as at 30th June 2015 leading to a total outstanding of

UGX.1,428,884,100. Details as below:

Item Distribution Amount (UGX)

Unpaid Boxes for current year 4747 367,395,300

Unpaid Boxes for two years 2128 330,710,400

Unpaid boxes for three years 2184 508,826,700

Unpaid boxes for four years 708 218,299,200

10

Unpaid boxes for five years and above 7 3,652,500

Total Amount in arrears 1,428,884,100

Non enforcement of the pre-payment policy for box rentals is likely to cause

accumulation of rental arrears which may never be recovered resulting into loss to

the company.

Management explained that they had heightened enforcement of prepaid policy and

unsubscribed post boxes had been reallocated to available demand.

I advised the Accounting Officer to enforce the pre-payment policy and be more

vigilant in enforcing recovery of the already accumulated arrears.

8.7 Statutory deduction remittances

8.7.1 Pay As You Earn (PAYE)-UGX.1,913,730,580

UGX.1,423,893,470 was deducted and withheld as PAYE from staff emoluments for

the year under review, however, out of the amounts withheld only UGX.99,874,857

was remitted leaving UGX.1,324,018,613 outstanding contrary to Section 124(1) of

the Income Tax Act requires that requires a withholding agent to pay to the

Commissioner any tax that has been withheld or that should have been withheld

under this section within fifteen days after the end of the month in which the

payment subject to withholding tax was made by the withholding agent. Given the

fact that UGX.589,711,967 remained outstanding in the previous years, total

outstanding arrears stood at UGX.1,913,730,580. Details in table below;

Staff Number MONTH/DATE Cheque no. PAYE Amount Amount Paid

318 July 2014 103,187,934

312 August 2014 100,802,303

312 September 2014 99,969,539

313 October 2014 108,634,491

308 November 2014 99,874,760

304 December 2014 116,765,384

28/11/2014 Chq12787 0 99,874,857

306 January 2015 108,381,078

298 February 2015

106,382,295

294 March 2015

136,066,148

292 April 2015

111,933,759

294 May 2015

196,667,613

11

294 June 2015

135,228,166

1,423,893,470 99,874,857

Violation of the Income Tax laws attracts fines and penalties which make an already

bad cash flow situation worse.

Management explained that the cash flow of the company does not allow instant

settlement of obligations to cover both the recurrent and long term liabilities and that

this challenge was brought to the attention of the Board, who instructed

management to negotiate for installment payments pending capitalization of the

company. Management further explained that URA has been engaged and small

installments had been agreed.

I advised the Accounting Officer to always adhere to the requirements under the

Income Tax Act to avoid fines and penalties.

8.7.2 Non remittances of VAT - UGX.2,004,986,000.

A review of the trial balance revealed that while invoicing UPL services to clients, the

company collected 18% VAT on receipts, however, despite filling monthly returns,

VAT amounting to UGX.2,004,986,000 due to Uganda Revenue Authority was still

outstanding contrary to section 31 (1) of the VAT Act that requires a taxable person

to lodge a tax return for each tax period with the Commissioner General within

fifteen days after the end of the period. Non-remittance of VAT funds is a violation of

the Tax laws (VAT Act) which may lead to fines and penalties.

Management explained as noted in 8.7.1 above.

I advised the Accounting Officer to ensure that VAT funds are strictly remitted within

the timelines of the law and all outstanding amounts should be remitted to Uganda

Revenue Authority.

8.7.3 Non remittances of 15% NSSF deductions UGX.1,789,995,000.

Section 10 (1) of the National Social Security Fund Act, 1985 requires that every

contributing employer shall for every month for which he pays wages to every

eligible employee, pay to the fund, within 15 days next following the last day of the

12

month for which the relevant wages are paid a standard contribution of 15%

calculated on the total wages paid for that month to that employee.

During the year under review, the company did not remit UGX.808,767,310 to the

National Social Security Fund, (NSSF) as required by the law. Details are as below.

Amount in UGX

Annual 5% NSSF deducted 291,171,732

Add 10% Annual Employer contribution 582,346,955

TOTAL 15% Due to NSSF for the year 873,518,687

LESS: Remitted 64,751,377

NOT REMITTED 808,767,310

Further, there was also an outstanding balance from the previous years of

UGX.981,227,690 which has been pending for over one year and is now attracting

interest. Non remittance of statutory deductions may lead to imposition of fines and

penalties by the statutory bodies. Further, employees are denied their interest due

on savings.

Management explained that NSSF has been engaged and small installments have

been agreed.

I advised the Accounting Officer to ensure that NSSF deductions are remitted

promptly as required by the law.

8.7.4 Non-remittance of Withholding Tax - UGX.233,816,000

UGX.233,816,000 withheld from local suppliers as required by the Income Tax Act,

was not remitted to URA contrary to section 123 (1) of the Income Tax Act. The

company is exposed to a risk of fines and penalties imposed by URA for late

remittances.

Management explained as noted in 8.7.1 above.

I advised the Accounting Officer to ensure that all taxes due are remitted to URA

timely.

8.8 Budget Performance

The Board of Directors is entrusted with powers to approve the company’s budget

and the Accounting Officer is entrusted with the responsibility of ensuring that all

total controls such as those contained in the approved estimates are strictly

observed. Budget estimates are based on outputs to be achieved for the financial

13

year and during implementation, effort is required to be made to achieve the agreed

objectives or targets of the entity within the availed resources.

A review of the budget performance for the year revealed that some targets were

partially or not achieved despite collection of funds. Details are as below;

Item description

Planned outputs/Quantity

Amount (UGX) budgeted

Amount spent (UGX)

Actual output/ Quantity

Remarks

Purchase of Computers & Peripherals

Desktops 20

Laptops 10

Inverters 5

Scanners 15

91,500,000 43,129,197 1-APS SMART UPS 2.2KV, 4-Lap tops, 1 Desk Top Computer,

1 APC 2.2KVA Smart UPS, 3 dell Optiplex Gx Computers, 10 Dell mouse & 10 Keyboards, 1 Cisco 2951 ISR G2 Router, 1 Galaxy Grand i-phone, 1 Barcode Scanner.

16 Desktops were not bought 6 Laptops were not bought

No inverter was bought. 14 Scanners were not bought Bought but not planned for: 2 UPS

10 PCS

Mouse

10

Keyboard

1 Router

I I-phone

Purchase of Computer Software

2 HR Software and Dot Post

36,603,334 Not Bought All Items were not purchased

Purchase of Machinery and Equipment

5pcs of counting machines

10,000,000 1,746,073

One Counting Machine for Money

4 Money Counting machines were not bought.

Purchase of Furniture and fittings

5 Desks 6 Chairs 10 Shelves

30,833,333 12,764,732

6 chairs and 8 Post shop Shelves

5 Desks were not bought 2 Shelves were not bought

Purchase of

Automobile

2 M/cycles 5,000,000 Not Bought All Items were

not purchased

Purchase of Office Equipment

10 Money Detectors 5 Weighing scales 20 VOIP Telephone handsets

30,000,000 Not Bought All Items were not purchased

Purchase of Boxes

3 nests of 100 boxes each

36,412,323 Not Bought All Items were not purchased

Service delivery is hampered and the Company objectives may not be met.

14

Management explained that the cash flow challenge of the company compels

continuous review of planned activity against competing priorities in the financial

year.

I advised the Accounting Officer to ensure adequate supervision of the projects being

undertaken.

8.9 Field inspections

During the year, inspections were carried out at various up country postal offices in

Western, Eastern and North-Eastern regions. It was noted that there was a total of

7,993 Boxes in seven post offices indicated in the table below:

Station Total post boxes

Bushenyi 399

Ntungamo 399

Mbale 2698

Soroti 899

Arua 1500

Gulu 998

Lira 1,100

TOTAL 7,993

The following key highlights were noted during inspection.

Non-functional/damaged rental boxes: A total of 21 boxes were found in

Bushenyi-1, Ntungamo-7; Soroti-1 and Arua-12.

A number of Box rentals were in arrears to the tune of UGC.348,802,500 i.e.

Mbale-UGX.88,205,500, Soroti-UGX.67,774,000, Arua-UGX.151,666,000, Lira-

UGX.25,041,000 and Gulu-UGX.16,116,000.

A number of boxes with rental arrears were noted in Bushenyi 178; Ntungamo

286; Arua 758 and Gulu 316.

Office space rental arrears from tenants to the tune of Shs. 35,064,966 were

noted in Mbale - UGX.6,280,000, Soroti-UGX.2,201,711 and Gulu -

UGX.26,583,255.

In Mbale it was noted that out of the 2,698 boxes at the station 1,040 boxes

were dormant.

It was further noted that a number of structures were dilapidated as in the

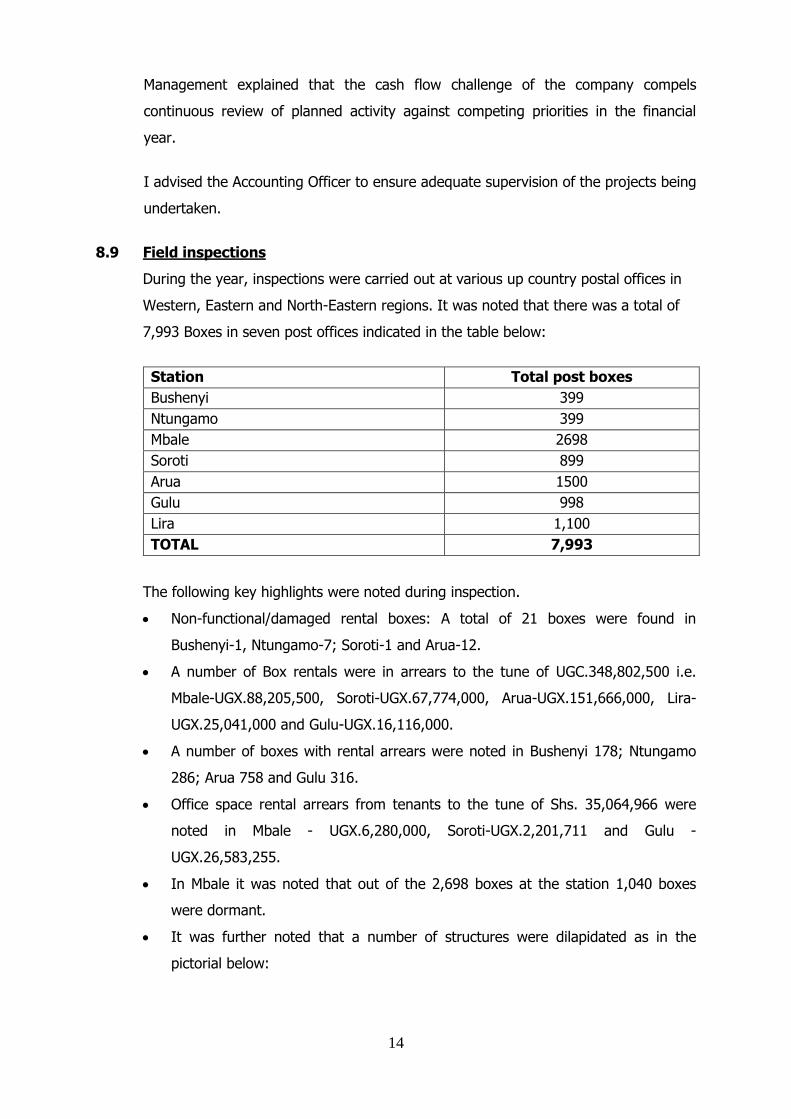

pictorial below:

15

Above: Posta Soroti building is old with a lot of leakage

Above: Gulu Postal offices have no toilets for both staff and tenants. The existing toilets

blocked 2 years ago and staff had erected a makeshift as a place for convenience

Lira Post Office. The roof in the manager’s office was leaking.

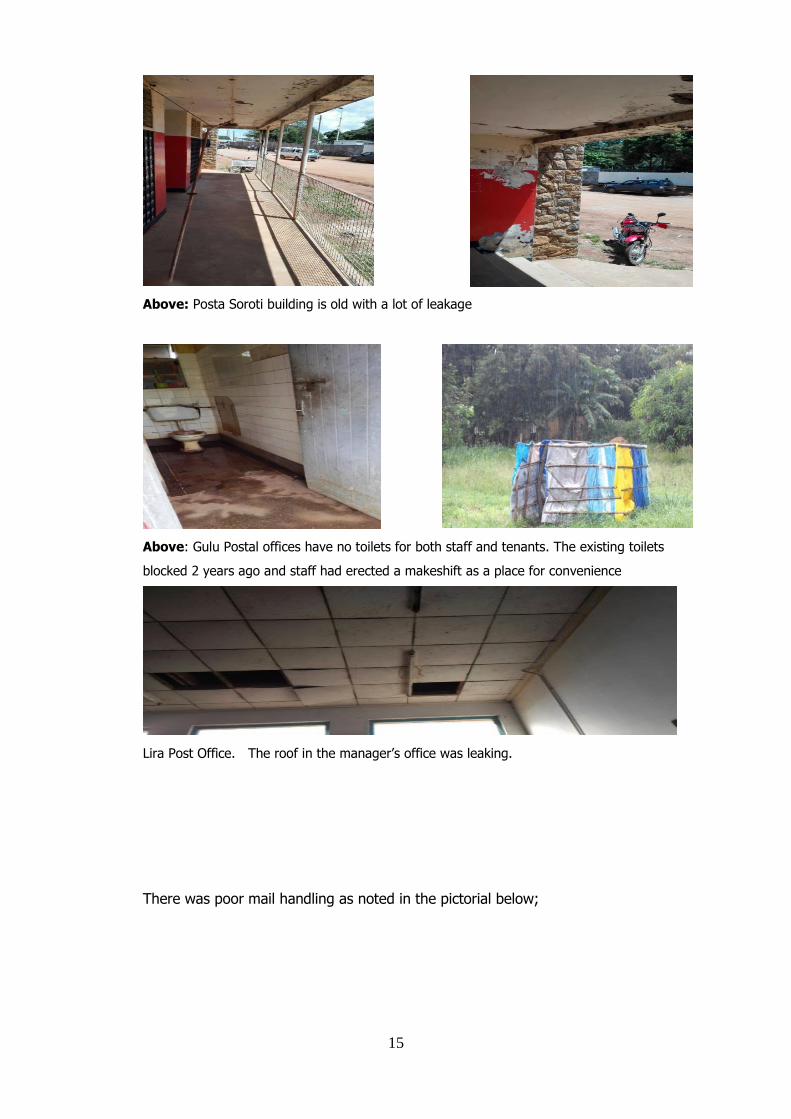

There was poor mail handling as noted in the pictorial below;

16

Above Left: Lira Post Office - rental boxes had got damaged due to the leaking roof

Above Right: Gulu Post Office sorting room was not well organized as mail was just

scattered in the room without lights.

Management acknowledged the observation and indicated that once the funds are

availed, some of the activities will be handled.

I advised the Accounting Officer to address the above anomalies to improve service

delivery.

8.10 Status of prior year audit recommendations

The status of the issues raised in my prior year audit report is summarized as below;

No. Issue Recommendation Status

8.10.1 Sustainability of services-Liquidity analysis: Financial

analysis of the company’s financial information was undertaken and it

was noted that Posta’s financial

standing was not healthy. Management needed to improve its

competitiveness and ensure survival.

Management advised to ensure that debts are

collected timely and also ensure that there are

adequate controls over

their debt portfolio and credit policies if they are to

sustain service delivery

Repeated

8.10.2 Misstatement of prior year receivables:

It was noted that the bulk of the adjustments were a result of non-

recognition of revenue earned in prior years with some dating back to

the period 2005 to 2008. As a result

several debtors on the company’s books in the previous year were

actually not indebted thus overstating the receivables position.

Management advised to continue undertaking a

review of their receivables and also circularize with a

view of writing off the long overdue receivables

Repeated

8.10.3 Confirmation and effect of

receivables balance: I noted that several such cases will

continue to surface in subsequent years especially with long overdue

Management advised to

continue undertaking a review of their receivables

and also circularize with a view of writing off the long

Repeated

17

receivables and as such I could not

confirm with certainty the receivables position of the company

as at close of the financial year as

receivables accounts were never reconciled with customers in prior

years. The errors impact on current years balances as comparatives for

the prior year are misstated.

overdue receivables

8.10.4 Post box rental revenue – lack of updated database

UGX.2,324,659,800 was revenue earned from the rented postal

boxes. However, I could not

ascertain the revenue performance from 82,000 boxes because POSTA

did not keep and maintain a database for all the rentable boxes

in the various centers detailing numbers, boxes in use, boxes paid

for and unused boxes per station.

Management advised to ensure that a database is

kept and maintained showing the status of

boxes at each postal office

which should be the source of data for

budgeting.

Addressed

8.10.5 Incomplete rental files: A review of tenants’ files revealed a

number of tenants but there were

no valid Tenancy contract agreements to bind the two parties

(POSTA Uganda as Landlord and the firms/ individuals as Tenants).

Further, there was no evidence to prove that all rent was based on

regular valuations to determine the

rent payable.

Management advised to ensure that all tenants

have valid tenancy

agreements and also carry out regular valuations of

rentable space as required by the estates policy

Addressed

8.10.6 Failure to settle overdraft

facility:

The facility was originally for one year running up to 31st July 2013,

and as such it should have been fully settled by August 2013.

However, it was noted that there

was no compliance to settle the facility and as such the amount was

still outstanding one year after expected retirement of the facility.

Management advised to

ensure settlement of the

facility as a priority to avoid the unnecessary

charges

Converted to

loan

8.10.7 Interest expense incurred: As a

result of the above, the company incurred interest to the tune of

UGX.338,159,790 during the year. This would have been avoided if

efforts had been undertaken to

repay the amount in installments as had earlier been planned.

Not repeated

8.10.8 Inadequate Credit Control: Sections 8.3.2(e) of UPL’s Finance

Policies and Procedures Manual

requires management to fix credit limits for all customers who have

been granted credit facility and that in any case should not go beyond

three months.

Management advised to expedite the policy

approval and have it

implemented

Repeated

18

On the contrary, it was noted that

UPL had no credit limits set for its customers and further still, the

credit facility for most customers

were found to exceed the three months and as a result debts had

accumulated to UGX.8,149,437,849.

8.10.9 Statutory deduction

remittances:

1. Paye-1,314,224,990 total outstanding

2. VAT -1,807,845,280 outstanding 3. NSSF- 877,455,255 outstanding

4. Withholding tax -113, 224,079

outstanding 5. LST- 105,306,630 outstanding

Management advised to

undertake necessary

efforts to have the outstanding obligations

settled.

Repeated

8.10.10 Absence of a transport management policy information

system:

The transport management policy for UPL requires the company to

develop a transport management policy information system, which

should be kept and regularly

checked for consistency, completeness and accuracy.

However no such system was developed by the entity and as a

result there is no coordination to relate vehicle movements, repairs

and servicing, fuel utilization and

boarding off of vehicles. This may lead to increased cost of repairs for

vehicles as some may be very old, storage or parking costs for vehicles

fit for boarding off, wasteful

expenses on redundant drivers and conductors, uneconomical travel

routes, and other related issues.

Management advised to initiate the system

development by

benchmarking with other statutory bodies. This

system should be comprehensive enough to

cover all transport related

information for the fleet

Repeated

8.10.11 Inspections:

1 Unutilised equipment and

property:

It was observed that in some stations there were equipment and

properties that were not being utilized due to reasons such as non-

maintenance, lack of passwords, resignation of staff previously

managing the equipment, high

rental values, power bills and incomplete structures.

Management advised to

ensure that the equipment

is fully utilized for maximization of revenues

and efficient service delivery

Repeated to

some extent

2 Rental revenue and Liabilities:

It was noted that some stations had tenants occupying postal premises

but the tenants had left the buildings after accumulation of

rental arrears yet the tenancy agreements at Head Office require

Management efforts

awaited in regard to strengthened estates

department charged with the responsibility of

collection of upcountry rental revenue.

Repeated

19

that rent is paid upfront whenever it

falls due.

I await the results of management efforts

3 Parcel and mail handling:

I observed that in several stations parcel and mail handling was not

well managed and could lead to loss and destruction of mails and parcels.

This was basically due to small office

space, poor box maintenance, lack of safe storage facilities and

incompetent staff.

Management effort waited

in regard to the internal training on postal

operations being conducted to equip staff

with necessary skills in

handling mail and parcels.

Repeated

4 Dilapidated buildings: Physical inspection of the various

postal office branches revealed deteriorating infrastructure of both

the owned and rented buildings. This was exhibited by leaking roofs

and ceilings, broken verandahs,

blocked sewage lines among others.

Management advised to continue with the

maintenance of the buildings and consider

renting habitable premises

Repeated

5 Rental boxes:

A sample of the inspected offices

revealed that the status of the rental boxes were in a poor state. These

range from non-operations boxes, lack of locks and damaged boxes.

The rental boxes were therefore not adequately maintained.

Management advised to

maintain the box rentals in

good shape in order to attract more revenue, and

enhance the marketing campaign to attract more

clients

Repeated

APPENDIX 1

20

FINANCIAL STATEMENTS