REPORT OF THE 1ST HALF YEAR 2005 - Morningstar, Inc.

22

REPORT OF THE 1ST HALF YEAR_ 2005

Transcript of REPORT OF THE 1ST HALF YEAR 2005 - Morningstar, Inc.

REPORT OF THE 1ST HALF YEAR_ 2005

_ 2

O million

Order intake

Sales (net)

of which international (in %)

Gross profit

EBITDA

EBIT

EBIT margin (in % of sales)

EBT

Net income for the period

Earnings per share in L (DVFA/SG)

Shares in circulation (in million)

Cash flow from ordinary operations

Key data as at June 30

Working capital

Long term liabilities to banks

Net liquidity

Shareholders’ equity

Balance sheet total

Equity ratio (in %)

Employees (excluding apprentices)

1st half 2004

77.0

62.7

63.7

22.1

6.9

5.8

9.3

4.0

2.9

0.32

9.2

6.6

12.4

25.5

7.9

26.4

115.5

22.9

725

1st half 2005

84.9

76.2

66.6

27.4

9.8

8.6

11.3

7.4

5.3

0.58

9.2

- 0.5

11.8

14.1

8.6

35.2

111.8

31.5

752

The elexis Group at a glance (unaudited in accordance with IFRS/IAS)

The

elex

is G

roup

at

a gl

ance

_ 3

1.0_ Report of the 1st half year 2005

1.1_ Summary of the first six months

The 1st half year 2005 for the elexis Group was characterised in particular by a strong development of the operating business, the broad approval of the shareholders with regard to all items on the agenda at the general meeting of shareholders held at the end of June as well as by a positive development of the share price.

Both during the first six months of the current fiscal year as well as during the second quarter of 2005 the elexis group achieved significant growth rates with regard to all relevant financial data. Order intake increased during the first half of the current year to L 84.9 million. This represents an increase of 10% versus the comparative prior year amount. During the first half year 2005 sales increased by 22% to L 76.2 million. Incoming orders thus exceed sales by a good 11% (book to bill ratio: 1.11). The high level of incoming orders and the orders on hand resulting there from, the continuation of the extensive project list as well as the strong profitability achieved in the meantime permit the Management Board to raise yet again its forecast for the full year, which was last increased only in May (see "1.9_ Outlook").

The earnings data also developed positively without exception during the period under report. The growth rates achieved in this respect were substantially higher than those of sales and order intake. This supports the corporate strategy which is directed at profitable growth. Earnings before interest and taxes (EBIT) grew by 48% to L 8.6 million. The EBIT margin amounted to 11.3% and was thus higher than the range of eight to ten percent which the Management Board had hitherto aimed for at the latest by 2006. The net income for the period increased to L 5.3 million and thus exceeded the amount of the 1st half year 2004 by 83%. During the first six months of 2005 earnings per share amounted to L 0.58. In the first half of the prior year the elexis Group reported earnings per share of L 0.32.

At its meeting at the beginning of June the Supervisory Board extended until 2010 the appointment of the two members of the Management Board, Messrs Koepp and Schäfer. It has thus assured for the elexis Group the continuity of the successful work of the Management Board for the next few years.

At the general meeting of shareholders held at Wenden at the end of June 2005 the shareholders gave a unanimous discharge both to the Supervisory Board as well as to the Management Board in respect of the fiscal year 2004. Furthermore, they also gave the management the possibility of increasing the share capital by up to 50% until June 2010 through a capital increase in cash or in kind. This possible capital measure is subject to the approval of the Supervisory Board. At the same time the shareholders authorised the Management Board to repurchase up to ten percent of the elexis shares. These shares can subsequently be used for the acquisition of companies or parts of companies. The securities can also be withdrawn after repurchase and thus complement a dividend payment. The capital measure is limited up to December 2006 and is also sub-ject to the approval of the Supervisory Board. The objective of these so-called inventory resolutions is to increase further the corporate value as well as the value of the elexis share. Various strategic options are available to the Management Board in this respect.

The report of the 1st half year 2005 has been drawn up in accordance with the accounting standards of the International Accounting Standard Board (IAS). The effects which result from the change in the accounting standards from HGB (German Commercial Code) to IFRS/IAS are shown in the reconciliations in Section "1.10_ Explanatory notes on the half year financial statements as at June 30, 2005“.

_ 3

1.0_

Re

port

of

the

1st

half

yea

r 20

05

1.

1_

Sum

mar

y of

the

fir

st s

ix m

onth

s

The elexis share

The elexis shares developed in accordance with that of the operating business. During the first six months of the current year it rose from L 8.29 (Xetra closing price on 31.12.2004) to L 12.94 (Xetra closing price on 30.06.2005), representing growth of 56%.

The market capitalisation of the elexis Group, i.e. the share price multiplied by the number of shares in cir-culation amounted to L 119.0 million as at June 30, 2005. This represented the highest value since the first listing in May, 1999. During the six years from the stock market floatation in may 1999 until the end of the 1st half year 2005 the elexis share has increased on average by 11% per annum.

_ 4

1.1_

Su

mm

ary

of t

he f

irst

six

mon

ths

Jan. – June,

2005

12.94

7.53

9.2

119.0

Jan. – June,

2004

6.11

3.11

9.2

55.2

Summary of the elexis share

elexis vs. SDAX (Perf.) O

01.01.2005 - 30.06.2005

13,00

12,00

11,00

10,00

9,00

8,00

Stock market price (XETRA-closing price) in O

High

Low

Number of shares (in million)

Market capitalisation 30.6. in L million

January February March April May June

_ 5

1.2_

Th

e in

divi

dual

div

isio

ns

1.2_ The individual divisions

Both the Factory Automation, Steel and Printing division as well as the Factory Automation, Plastics division exceeded during the first six months of 2005 the comparative performance of the prior year.

Factory Automation, Steel and Printing

Following the extremely strong performance during the 1st quarter the Factory Automation, Steel and Printing division continued its high rate of growth also during the months from April to June. In total, the division acquired new orders in the amount of L 60.4 million during the first six months of 2005. Versus the comparative amounts of the prior year this represents an increase of twelve percent. Significant orders could be obtained in particular in Asia, Eastern Europe and also increasingly in the domestic market. Sales also increased substantially during the period under report by 14%, to L 55.8 million. The growth in the earnings data was even more significant. EBIT grew during the 1st half year by 27% to L 6.6 million versus the first six months of the prior year. The EBIT margin of 11.8%, which was considerably in excess of plan, was attributable not only to the increasing sales of fault detection systems for the printing industry but also to the high level of sales of quality control systems to customers in the steel industry. During the 1st half year 2005 elexis sold a higher volume of the IMPOC and Sorm3Plus systems than in the full prior year. Earnings after interest and taxes, i.e. the net income for the period, also increased substantially. It increased by 37% to L 5.9 million.

Summary of the Factory Automation, Steel and Printing division (unaudited for IFRS/IAS))

O million

Order intake

Sales (net)

EBITDA

EBIT

EBIT margin (in % of sales)

Net income for the period

Employees *

Jan. – June,

2005

60.4

55.8

7.6

6.6

11.8

5.9

598

Change

+ 12 %

+ 14 %

+ 27 %

+ 27 %

+ 37 %

+ 1 %

Jan. – June,

2004

53.7

48.8

6.0

5.2

10.7

4.3

590

* As at June 30 excluding apprentices

The 1st half year 2005

O million

Order intake

Sales (net)

EBITDA

EBIT

EBIT margin (in % of sales)

Net income for the period

April – June,

2005

29.3

29.5

3.9

3.4

11.5

2.8

Change

+ 11 %

+ 18 %

+ 30 %

+ 31 %

+ 56 %

April – June,

2004

26.4

25.0

3.0

2.6

10.4

1.8

The 2nd quarter 2005

_ 6

1.2_

Th

e in

divi

dual

div

isio

ns

Factory Automation, Plastics

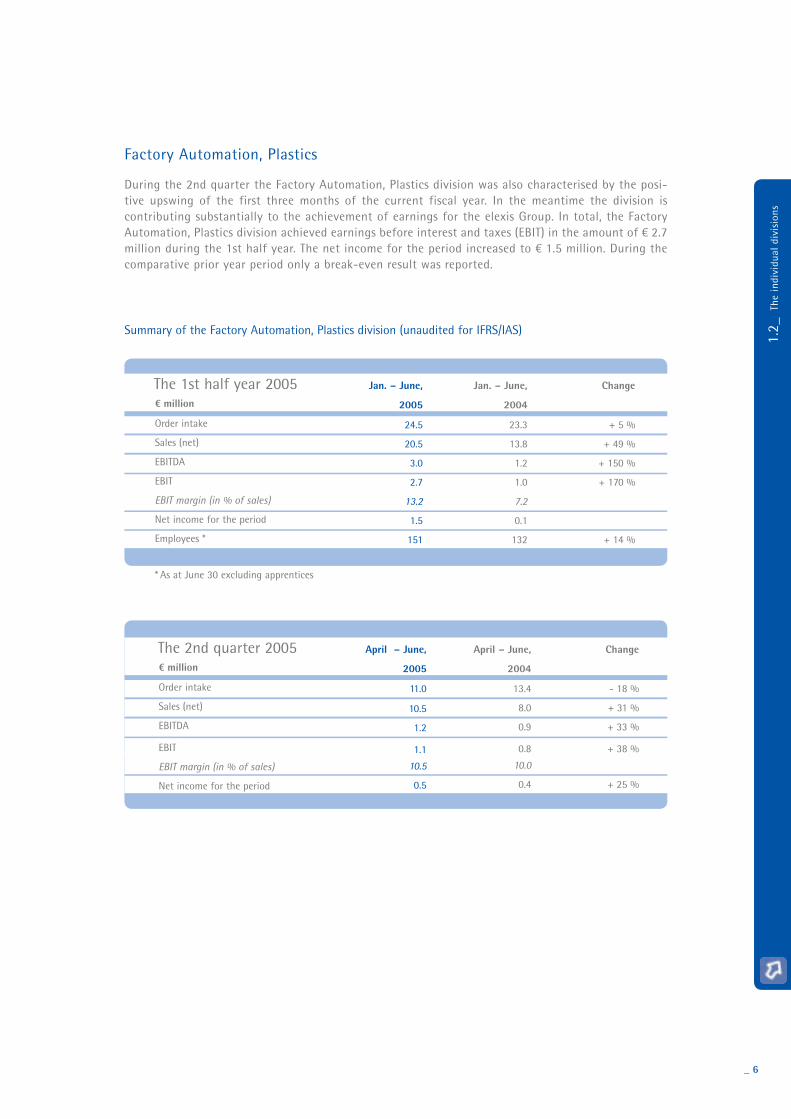

During the 2nd quarter the Factory Automation, Plastics division was also characterised by the posi-tive upswing of the first three months of the current fiscal year. In the meantime the division is contributing substantially to the achievement of earnings for the elexis Group. In total, the Factory Automation, Plastics division achieved earnings before interest and taxes (EBIT) in the amount of L 2.7 million during the 1st half year. The net income for the period increased to L 1.5 million. During the comparative prior year period only a break-even result was reported.

Summary of the Factory Automation, Plastics division (unaudited for IFRS/IAS)

O million

Order intake

Sales (net)

EBITDA

EBIT

EBIT margin (in % of sales)

Net income for the period

Employees *

Jan. – June,

2005

24.5

20.5

3.0

2.7

13.2

1.5

151

Change

+ 5 %

+ 49 %

+ 150 %

+ 170 %

+ 14 %

Jan. – June,

2004

23.3

13.8

1.2

1.0

7.2

0.1

132

* As at June 30 excluding apprentices

The 1st half year 2005

O million

Order intake

Sales (net)

EBITDA

EBIT

EBIT margin (in % of sales)

Net income for the period

April – June,

2005

11.0

10.5

1.2

1.1

10.5

0.5

Change

- 18 %

+ 31 %

+ 33 %

+ 38 %

+ 25 %

April – June,

2004

13.4

8.0

0.9

0.8

10.0

0.4

The 2nd quarter 2005

_ 7

1.3_

In

vest

men

ts

1.

4_

Rese

arch

and

dev

elop

men

t

1.5

_ P

erso

nnel

1.

6_

Bala

nce

shee

t si

tuat

ion

of t

he G

roup

elexis AG

The operating costs of the holding company, i.e. the AG itself, developed as planned. EBIT before the result of participations amounted to L -0.7 million during the 1st half year.

1.3_ Investments

Investments amounting to L 1.3 million during the period under report exceeded the comparative amount of the prior year by over eight percent. The emphases of these investments were on IT infrastructure and on manufacturing.

1.4_ Research and development

During the first six months of the current year L 2.7 million was invested for research and development. The increase versus the 1st half of the past fiscal year amounted to 59%. A large part of the R&D activities was attributable to further developments and product innovations.

1.5_ Personnel

The number of employees increased by 27 to 752 in comparison with the prior year period. The major part of the increase in personnel took place in the Factory Automation, Plastics division, in order to cope with the high growth in that division. Both sales as well as value added per employee increased substantially during the 1st half year 2005 in comparison with the first six months of the prior year. This proves that productivity and efficiency in the Company could also be increased further in parallel with the increase in sales.

1.6_ Balance sheet situation of the Group

During the first six months of the current year the shareholders’ equity grew to L 35.2 million. As at June 30, 2005 the equity margin amounted to 31.5%. The long-term liabilities to banks could be reduced to L 14.1 million in accordance with plan. These had still amounted to L 16.2 million at the beginning of the year. Thanks to the application of an efficient inventory management system in all business units it was possible to reduce inventories to L 17.5 million in spite of the increase in production. This represents a decline of L 0.7 million versus the beginning of the year. The higher level of sales as well as the simultaneous increase in the export quota led to an increase in trade receivables.

_ 8

1.6_

Ba

lanc

e sh

eet

situ

atio

n of

the

Gro

up

Consolidated balance sheet

IFRS/IAS (unaudited)

Fixed assets

Long term assets

Long term receivables and other assets

Deferred tax claims

Short term assets

Inventories (net)

Trade receivables

Other short term receivables and assets

Cash on hand and at banks

Deferred charges

Total assets

Shareholders’ equity

Shareholders’ equity excluding minority interests

Minority interests

Long term provisions and liabilities

Provisions for pensions

Deferred tax liabilities

Liabilities to banks

Short term provisions and liabilities

Provisions

Financial liabilities

Taxes on income

Other liabilities

Total liabilities

June 30, 2005in %

40.0

7.7

0.6

7.1

52.0

15.7

22.5

3.2

10.6

0.3

100.0

31.5

31.3

0.2

29.5

13.5

3.4

12.6

39.0

8.0

9.6

0.4

21.0

100.0

O million

44.7

8.6

0.7

7.9

58.1

17.5

25.2

3.6

11.8

0.4

111.8

35.2

35.0

0.2

33.0

15.1

3.8

14.1

43.6

8.9

10.7

0.5

23.5

111.8

Dec. 31, 2004in %

38.5

8.1

0.4

7.7

53.1

15.6

20.1

2.4

15.0

0.3

100.0

25.7

25.5

0.2

29.5

12.9

2.7

13.9

44.8

8.5

10.5

0.3

25.5

100.0

O million

44.8

9.4

0.5

8.9

61.8

18.2

23.4

2.8

17.4

0.4

116.4

29.9

29.7

0.2

34.4

15.0

3.2

16.2

52.1

9.9

12.2

0.3

29.7

116.4

June 30, 2004in %

40.7

8.1

0.5

7.6

50.9

16.8

20.4

2.6

11.1

0.3

100.0

22.8

22.6

0.2

37.3

12.9

2.3

22.1

39.9

6.7

10.5

0.3

22.4

100.0

O million

47.0

9.3

0.5

8.8

58.8

19.4

23.6

3.0

12.8

0.4

115.5

26.4

26.2

0.2

43.1

14.9

2.7

25.5

46.0

7.7

12.1

0.3

25.9

115.5

_ 9

1.6_

Ba

lanc

e sh

eet

situ

atio

n of

the

Gro

up

O million

Status as at 01.01.2005

Other changes

Consolidated net income

Currency differences

Total consolidated result

Status as at 30.06.2005

Consolidated shareholders’ equity earned

1,4

5,3

5,3

6,7

Effect of currency conversion

1,1

1,1

Minority interests

0,2

0,2

Consolidated shareholders’

equity

29,9

5,3

5,3

35,2

Sub-scribed capital

23,6

23,6

Capital reserve

3,6

3,6

Development of shareholders’ equity in the 1st half year 2005 (unaudited for IFRS/IAS)

O million

Status as at 01.01.2004

Other changes

Consolidated net income

Currency differences

Total consolidated result

Status as at 30.06.2004

Consolidated shareholders’ equity earned

-4,9

2,9

2,9

-2,0

Effect of currency conversion

1,0

1,0

Minority interests

0,2

0,2

Consolidated shareholders’

equity

23,5

2,9

2,9

26,4

Sub-scribed capital

23,6

23,6

Capital reserve

3,6

3,6

Development of shareholders’ equity in the 1st half year 2004 (unaudited for IFRS/IAS)

1.7_

Fi

nanc

ial s

itua

tion

of

the

Gro

up

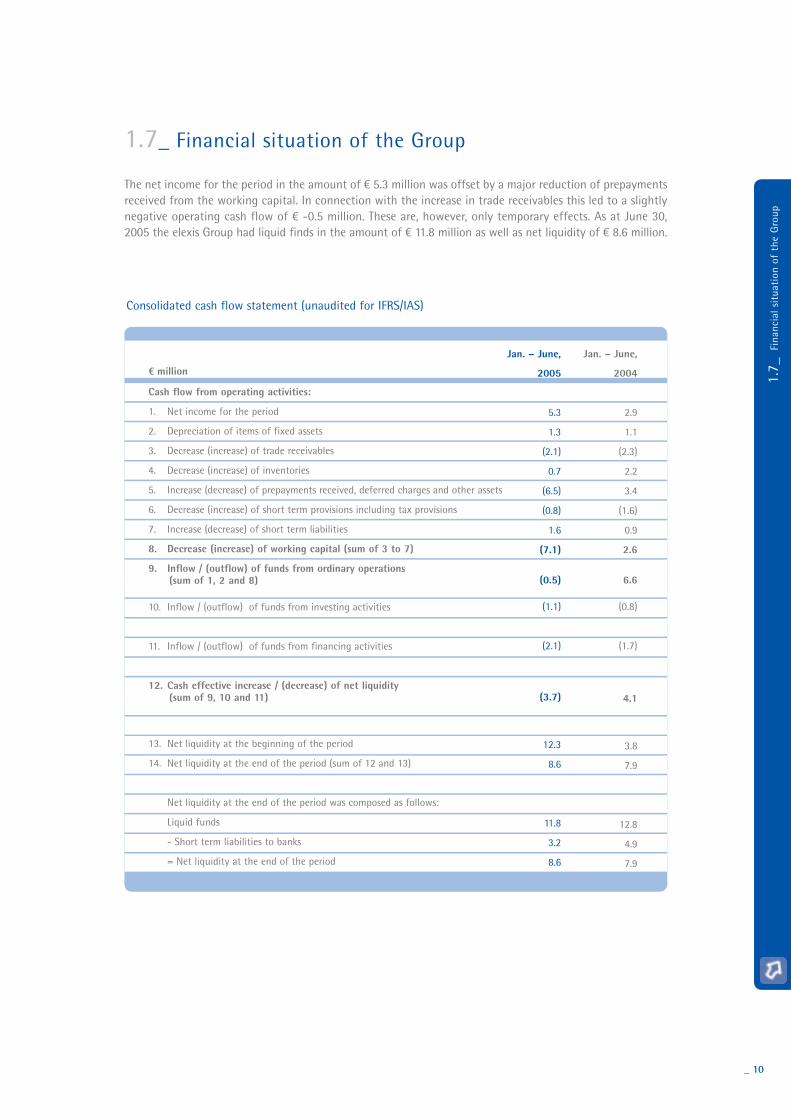

1.7_ Financial situation of the Group

The net income for the period in the amount of L 5.3 million was offset by a major reduction of prepayments received from the working capital. In connection with the increase in trade receivables this led to a slightly negative operating cash flow of L -0.5 million. These are, however, only temporary effects. As at June 30, 2005 the elexis Group had liquid finds in the amount of L 11.8 million as well as net liquidity of L 8.6 million.

Consolidated cash flow statement (unaudited for IFRS/IAS)

_ 10

O million

Cash flow from operating activities:

1. Net income for the period

2. Depreciation of items of fixed assets

3. Decrease (increase) of trade receivables

4. Decrease (increase) of inventories

5. Increase (decrease) of prepayments received, deferred charges and other assets

6. Decrease (increase) of short term provisions including tax provisions

7. Increase (decrease) of short term liabilities

8. Decrease (increase) of working capital (sum of 3 to 7)

9. Inflow / (outflow) of funds from ordinary operations (sum of 1, 2 and 8)

10. Inflow / (outflow) of funds from investing activities

11. Inflow / (outflow) of funds from financing activities

12. Cash effective increase / (decrease) of net liquidity (sum of 9, 10 and 11)

13. Net liquidity at the beginning of the period

14. Net liquidity at the end of the period (sum of 12 and 13)

Net liquidity at the end of the period was composed as follows:

Liquid funds

- Short term liabilities to banks

= Net liquidity at the end of the period

Jan. – June,

2005

5.3

1.3

(2.1)

0.7

(6.5)

(0.8)

1.6

(7.1)

(0.5)

(1.1)

(2.1)

(3.7)

12.3

8.6

11.8

3.2

8.6

Jan. – June,

2004

2.9

1.1

(2.3)

2.2

3.4

(1.6)

0.9

2.6

6.6

(0.8)

(1.7)

4.1

3.8

7.9

12.8

4.9

7.9

1.

8_

Prof

itab

ility

of

the

Gro

up

Consolidated profit and loss account (unaudited for IFRS/IAS)

_ 11

1.8_ Profitability of the Group

The increases in efficiency which were achieved by the elexis Group during the 1st half year are reflected in the higher gross margin as well as in the decline in the selling and administration expense ratio. The EBIT margin of 11.3%, which was achieved during the first six months, supports the profitability of the Company. Due to the usual fluctuations in the engineering sector the quarterly results cannot be guaranteed to continue.

O million

Sales (net)

Cost of goods sold

Gross profitGross profit margin (in % of sales)

Selling expensesSelling expense ratio (in % of sales)

General administration expensesAdministration expense ratio (in % of sales)

Other income/expense

EBITEBIT margin (in % of sales)

Net interest expense

EBT

Taxes on income*

Net income for the period

Jan. – June, 2005

76,2

48,8

27,4 36,0

13,918,2

5,26,8

0,3

8,611,3

- 1,2

7,4

2,1

5,3

Jan. – June, 2004

62,7

40,6

22,135,2

12,219,5

4,97,8

0,8

5,89,3

- 1,8

4,0

1,1

2,9

* Incl. effect of deferred taxes

The 1st half year 2005

1.

8_

Prof

itab

ility

of

the

Gro

up

1.

9_

Out

look

1.9_ Outlook

The book to bill ratio of 1.11 at the end of the first six months indicates continuing organic growth during the 2nd half year. On the basis of the exceptionally successful performance during the 1st half year these positive forecasts permit the Management Board to increase once again the forecast for the full year, which was last raised in May. For the full year 2005 the management now expects incoming orders totalling between L 150 and 160 million (last forecast: L 142 to 155 million). The growth in order intake will be driven in particular by comparatively young products. Whereas the share of product innovations, which have been on the market only since 2001, represented less than a third of order intake in 2004, new innovative products will probably contribute more than 40% to incoming orders during the current year. Sales will probably rise to between L 142 to 150 million during 2005 (last forecast: L 138 to 142 million). Furthermore, the Manage-ment Board expects that its forecast of the whole Group achieving an EBIT margin of eight to ten percent in 2006 will already be achieved and/or exceeded during the current fiscal year.

_ 12

O million

Sales (net)

Cost of goods sold

Gross profitGross profit margin (in % of sales)

Selling expensesSelling expense ratio (in % of sales)

General administration expensesAdministration expense ratio (in % of sales)

Other income/expense

EBITEBIT margin (in % of sales)

Net interest expense

EBT

Taxes on income*

Net income for the period

April – June, 2005

39,9

26,1

13,8 34,6

7,518,8

2,76,6

0,5

4,110,3

- 0,8

3,3

1,2

2,1

April – June, 2004

33,1

21,5

11,635,0

6,519,6

2,78,2

0,7

3,19,4

- 1,1

2,0

0,6

1,4

* Incl. effect of deferred taxes

The 2nd quarter 2005

1

.10_

Ex

plan

ator

y no

tes

on t

he h

alf

year

fin

anci

al s

tate

men

ts

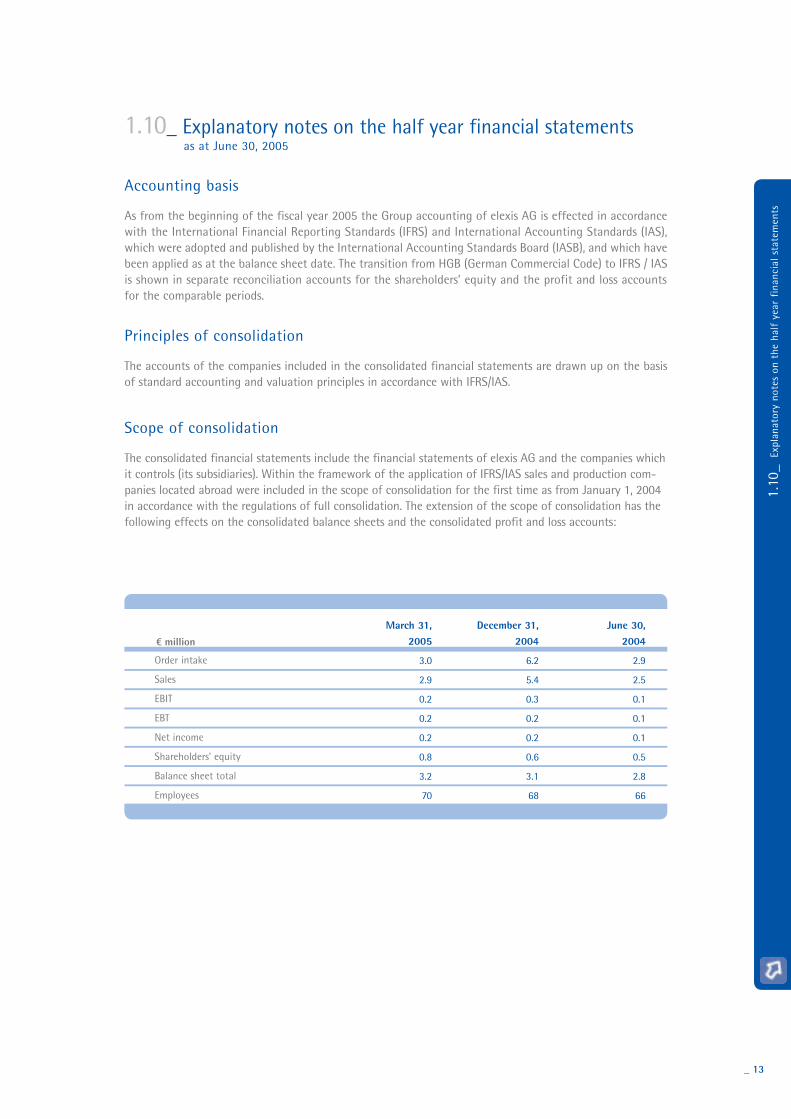

1.10_ Explanatory notes on the half year financial statements

Accounting basis

As from the beginning of the fiscal year 2005 the Group accounting of elexis AG is effected in accordance with the International Financial Reporting Standards (IFRS) and International Accounting Standards (IAS), which were adopted and published by the International Accounting Standards Board (IASB), and which have been applied as at the balance sheet date. The transition from HGB (German Commercial Code) to IFRS / IAS is shown in separate reconciliation accounts for the shareholders’ equity and the profit and loss accounts for the comparable periods.

Principles of consolidation

The accounts of the companies included in the consolidated financial statements are drawn up on the basis of standard accounting and valuation principles in accordance with IFRS/IAS.

Scope of consolidation

The consolidated financial statements include the financial statements of elexis AG and the companies which it controls (its subsidiaries). Within the framework of the application of IFRS/IAS sales and production com-panies located abroad were included in the scope of consolidation for the first time as from January 1, 2004 in accordance with the regulations of full consolidation. The extension of the scope of consolidation has the following effects on the consolidated balance sheets and the consolidated profit and loss accounts:

_ 13

Order intake

Sales

EBIT

EBT

Net income

Shareholders’ equity

Balance sheet total

Employees

June 30, 2004

2.9

2.5

0.1

0.1

0.1

0.5

2.8

66

O million

March 31, 2005

3.0

2.9

0.2

0.2

0.2

0.8

3.2

70

December 31, 2004

6.2

5.4

0.3

0.2

0.2

0.6

3.1

68

as at June 30, 2005

_ 14

Currency conversion

The conversion of the accounts of the subsidiaries, which are drawn up in foreign currency, is carried out in accordance with IAS 21 following the concept of the functional currency. In the elexis Group foreign subsidiaries are considered as economically independent partial units. For this reason the conversion of the balance sheet items takes place in principle at the rates prevailing at the balance sheet date. An exception to this is the shareholders’ equity of the subsidiaries included, which is converted at the historical rate. Items of expense and income are converted at annual average rates. The conversion differences resulting from the application of different exchange rates for items of the balance sheet and the profit and loss account are booked to shareholders’ equity without any effect on the profit and loss account.

In the individual accounts of the companies transactions in foreign currency are converted at the exchange rates prevailing at the date of the transaction. Monetary assets and liabilities, the value of which is indicated in a foreign currency, are valued as at the balance sheet date. Capital gains and losses are booked to the profit and loss account.

Capital consolidation

The initial consolidation of the companies first consolidated prior to January 1, 2004 was carried out on the basis of the book value method in accordance with Article 301, Paragraph 1, No. 1 of the HGB. In this respect the Group’s interests in the shareholders’ equity of the consolidated subsidiary was set off against the acquisition/establishment costs. Goodwill which arose was capitalized within the framework of the previous accounting principles in accordance with HGB and was subject to straight line amortisation over a period of 20 years. The valuation of the goodwill, which was previously capitalised in accordance with HGB accounting principles, was carried out for the fiscal year 2005 as well as for the prior year in accordance with the regulations of IAS 36. As a result goodwill was frozen at the amount of its value at the date of transition from HGB to IFRS/IAS as at January 1, 2004 and amortised only in the event of actual loss of value. For subsidiaries included in the consolidated financial statements for the first time after December 31, 2003 the capital consolidation was carried out in accordance with the acquisition method in the form of the book value method.

Consolidation of liabilities and income

Receivables and liabilities between the consolidated companies as well as internal Group sales, income and expenses are eliminated. In this respect the internal sales have been set off against the cost of goods sold of the work performed for the generation of these sales.

1

.10_

Ex

plan

ator

y no

tes

on t

he h

alf

year

fin

anci

al s

tate

men

ts

_ 15

Accounting and valuation methods

Recognition of income and expense

The recognition of sales and other operating income is carried out in principle when the work is performed, when the amount of the income can be reliably established and when the economic benefit will probably accrue to the Group. Operating expenses are charged to the profit and loss account when the expense occurs or at the date of their being caused. Sales and expenses from long term production contracts are recognised in accordance with the percentage of completion method, provided that the amount of the income can be reliably measured and that it is probable that the economic benefit from the transaction will accrue to the Group, and provided that the costs incurred for the transaction and the costs to be expected up to its full execution can be established reliably.

Fixed assets

Purchased intangible assets are stated at their cost of acquisition and are subject to straight line amortisation over a maximum period of five years depending on their expected economic life.

The goodwill from the individual accounts and from the consolidation was capitalised at its acquisition cost and was subject to scheduled amortisation up to December 31, 2003 in compliance with the accounting regulations of the German Commercial Code. The value of the goodwill stated as at December 31, 2003 was fixed as at January 1, 2004 at the date of the transition from HGB to IFRS/IAS. The valuation of the goodwill in the accounts is monitored once per annum by means of an impairment test. In the event of an indication of reduction in value unscheduled amortisation is charged.

Tangible fixed assets are valued at acquisition or manufacturing cost less scheduled and unscheduled depre-ciation. Apart from individual specific costs the manufacturing costs include an appropriate share of the allocable material and production overheads. Third party capital costs are not included in the manufacturing costs. Scheduled depreciation is charged in principle in accordance with the straight line method. Office and factory buildings are depreciated over a maximum period of 40 years, technical equipment and machinery over a period of between 10 and 15 years and other equipment, factory and office equipment mainly over a period of 5 years. Items of minor value are depreciated fully in the year of acquisition. Tangible fixed assets are subject to unscheduled depreciation in the event that there are indications of a reduction in value and if the realisable market value is lower than the depreciated acquisition or manufacturing cost.

Leased tangible fixed assets, which are considered economically to be purchases of equipment with long term financing (financial leasing), are included in the balance sheet at market value in accordance with IAS 17, insofar as the discounted value of the leasing installments are not lower. The depreciation methods and the economic lives correspond to those of similar acquired assets. The resulting payment liabilities from future leasing installments are included under short term liabilities. The capitalised items leased include real estate, machinery and office equipment.

1

.10_

Ex

plan

ator

y no

tes

on t

he h

alf

year

fin

anci

al s

tate

men

ts

_ 16

Current assets

The raw material, supplies and merchandise included in inventories are valued at their average cost of acquisition or at the lower net disposal value. The valuation of unfinished and finished goods is based on the manufacturing costs. The manufacturing costs include, apart from specific individual costs, appropriate shares of the allocable material and production overheads. General administrative expenses are not included in the manufacturing costs. Risks, which result from reduced usability, are taken into consideration through specific provisions for bad debts.

Receivables and other assets are stated at acquisition cost. If there are doubts with regard to collectability these are stated at nominal value less an appropriate specific provision. Deliveries and services charged to the customers are shown under trade receivables. This item also includes the work performed under long term production contracts, which are not yet invoiced, and which are valued in accordance with the percentage of completion method. The liquid funds are stated at their nominal value.

Deferred taxes

Deferred taxes are accounted for in accordance with IAS 12 by applying the balance sheet based liability method with regard to the temporary differences, which may occur from the differing amounts between the book value of the assets and liabilities in the consolidated financial statements and with regard to the calculation of the corresponding tax value to be used for the taxable result. Furthermore, deferred taxes are set up in respect of tax loss carry forwards. Deferred taxes are taken into consideration both at the level of the individual companies as well as with respect to consolidation events. The establishment of the deferred taxes is based on the application of the tax rates to be expected at the date of realization. Deferred tax claims and tax debts are not discounted. The book value of deferred tax provisions is monitored regularly and adjusted.

Provisions

The valuation of provisions for pensions are carried out in accordance with the actuarial projected unit credit method for performance based pension plans as stipulated in IAS 19.

Other provisions were set up insofar as an obligation towards a third party resulting from a past event might exist, which indicates an outflow of assets, which can be reliably established. These represent uncertain obligations, which are stated at the best possible estimated amount. Provisions with a maturity of more than one year are stated at their discounted value.

Liabilities

Liabilities from financial leasing contracts are shown at the discounted value of the leasing installments or the lower market value of the capitalised leased item. The other liabilities are shown at their repayment amount.

1

.10_

Ex

plan

ator

y no

tes

on t

he h

alf

year

fin

anci

al s

tate

men

ts

_ 17

Notes on the Group quarterly financial statements

Goodwill

The goodwill stated in the fixed assets in the amount of a total of L 27,162,000 includes in particular the following companies: HEKUMA GmbH (L 22,940,000), BST Pro Mark Inc. (L 3,486,000) und AViTEQ Vibrationstechnik GmbH (L 360,000). No unscheduled amortisation was carried out during the current period under report.

Trade receivables

The trade receivables in the amount of L 25,161,000 include receivables from long term production contracts in the amount of L 1,292,000, which were not partially or finally accounted for at the quarterly balance sheet date. The long term production contracts are taken into consideration in accordance with IAS 11 corresponding to the percentage of completion method. Insofar as the accumulative work performed (contract costs and partially realized profits) exceed the prepayments received in an individual case, the production contracts must be shown as an asset under trade liabilities. If a negative amount remains after deduction of the prepayments received, the item must be included under liabilities from long term production contracts.

Provisions

The other short term provisions in the amount of L 8,882,000 (December 31, 2004: L 9,858,000) are attributable in particular to structural measures, guarantees and obligations towards employees.

Financial liabilities

The short term financial liabilities include liabilities to banks in the amount of L 3,179,000 (December 31, 2004: L 5,090,000), liabilities from leasing and rental contracts in the amount of L 7,537,000 (December 31, 2004: L 7,113,000) and liabilities in respect of personnel in the amount of L 3,344,000 (December 31, 2004: L 2,287,000).

Other liabilities

The other liabilities as at June 30, 2005 include in particular trade liabilities of L 7,217,000 (December 31, 2004: L 7,518,000) and liabilities from long term contract production in the amount of L 5,451,000 (December 31, 2004: L 11,977,000).

1

.10_

Ex

plan

ator

y no

tes

on t

he h

alf

year

fin

anci

al s

tate

men

ts

_ 18

Separate notes on the first time application of IFRS/IAS

In accordance with IFRS 1 the first time application of IFRS/IAS takes place retrospectively. Thereafter the necessary adjustments of the accounting and valuation methods for the first time application of IFRS must be taken retroactively as if the accounting had always been based on IFRS/IAS.

These consolidated quarterly financial statements include the following major accounting and valuation methods which differ from HGB:

• Goodwill is subjected to a regular impairment test. No scheduled amortisation is charged.

• Leasing contracts, with regard to which the lessee is considered to be the economic owner of the leased item, are included in the balance sheet as assets and as leasing liabilities.

• Value adjustments and provisions on inventories and receivables are carried out for recognisable individual risks. No general provisions are made.

• Sales and expenses from long term production contracts are recognised in accordance with the degree of completion. Insofar as the accumulated work performed at the balance sheet date (manufacturing costs incurred plus related profits or less any losses to be taken into consideration) exceed the value of the prepayments received, the production contracts must be stated as an asset under trade receivables. Should a negative amount remain, they must be stated under the liabilities.

• Deferred taxes are calculated in accordance with the liability method based on the balance sheet. Deferred taxes on loss carry forwards are capitalised if it is expected that they can be used.

• Provisions for pensions are established in accordance with the projected unit credit method.

• Provisions are set up only if obligations exist towards third parties. Medium and long term provisions are stated at their discounted value. No provisions are set up for expenses.

• Monetary positions in foreign currencies are valued at the balance sheet date; the exchange rate differences resulting from this are booked to the profit and loss account.

The effects of the conversion of the accounting from HGB to IFRS/IAS on the shareholders’ equity and the result of the comparative periods of the prior year are shown as follows:

1

.10_

Ex

plan

ator

y no

tes

on t

he h

alf

year

fin

anci

al s

tate

men

ts

_ 19

Reconciliation of shareholders’ equity from HGB to IFRS/IAS

O 000

Shareholders’ equity in accordance with HGB

Goodwill

Inventories

Recognition of sales in accordance with degree of completion accounting

Receivables and other assets

Deferred taxes stated as assets

Provisions for pensions

Other provisions

Deferred taxes stated as liabilities

Leasing liabilities

Change from the inclusion of hitherto non-consolidated foreign companies

Shareholders’ equity in accordance with IFRS/IAS

Shareholders’ equity as at December 31, 2004

21.196

+ 1.669

+ 2.964

+ 806

+ 152

+ 8.900

- 3.175

+ 396

- 2.623

- 917

+ 568

29.936

Shareholders equity as at June 30, 2004

17.123

+ 945

+ 2.843

+ 1.070

+ 318

+ 8.807

- 2.934

+ 670

- 2.050

- 877

+ 479

26.394

Notes

(1)

(2)

(3)

(4)

(5)

(6)

(7)

(5)

(8)

O 000

Net income for the period in accordance with HGB

Correction of scheduled amortisation of goodwill

Leasing liabilities

Valuation of inventories

Recognition of sales in accordance with degree of completion accounting

Valuation of receivables and other assets

Valuation of provisions for pensions

Valuation of other provisions

Deferred taxes

Change from the inclusion of hitherto non-consolidated foreign companies

Net income for the period in accordance with IFRS/IAS

Net income for the period as at Dec. 31, 2004

+ 6.127

+ 1.669

- 84

+ 165

+ 549

- 72

- 278

- 415

- 1.525

+ 193

+ 6.329

Net income for the period as at June 30, 2004

+ 2.074

+ 945

- 44

+ 44

+ 813

+ 94

- 37

- 141

- 993

+ 104

+ 2.859

Reconciliation of the net income for the period from HGB to IFRS/IAS

Notes

(1)

(8)

(2)

(3)

(4)

(6)

(7)

(5)

1

.10_

Ex

plan

ator

y no

tes

on t

he h

alf

year

fin

anci

al s

tate

men

ts

_ 20

Notes on the reconciliation from HGB to IFRS/IAS

(1) In application of IFRS 3 the scheduled amortisation on goodwill from the individual accounts and the consolidation was discontinued as from January 1, 2004. Goodwill is subject only to unscheduled amortisation in the event that indications for a reduction in value exist.

(2) The increase in the inventories is attributable primarily to the non-inclusion of general risk provisions.

(3) The sales recognised partially on the basis of the application of the percentage of completion method including the margin from long term production contracts are stated under trade receivables.

(4) The higher valuation of the receivables and other assets is attributable to the non-inclusion of general provisions on receivables, which are overdue. The increase resulting from this is compensated for partially by the discounting of longer term receivables.

(5) The capitalised deferred taxes concern primarily deferred taxes on tax loss carry forwards and provisions. The deferred taxes stated as liabilities are attributable primarily to the discontinuation of the amortisation of goodwill in the individual accounts and the valuation of long term production contracts in accordance with the percentage of completion method.

(6) The calculation of the provisions for pensions on the basis of the projected unit credit method in accordance with IAS 19 leads to a higher valuation of the pension obligations in the IFRS statement than in the HGB statements. This is on the one hand attributable to the fact that on establishing the pension obligations in accordance with IFRS/IAS future payment increases and pension adjustments must be taken into con-sideration. Moreover, the interest rates applied for the calculation vary from the interest rate of 6 % to be applied for German calculation purposes.

(7) The non-inclusion of expense provisions in the IFRS/IAS statements leads to a decline in the other provisions.

(8) Leased items, which economically are attributable to the lessee, are stated under tangible fixed assets. The discounted value of the future leasing installments is shown in the short term liabilities.

1

.10_

Ex

plan

ator

y no

tes

on t

he h

alf

year

fin

anci

al s

tate

men

ts

_ 21

Other notes and explanations

Other notes and explanations

The obligations from leasing contracts in terms of IAS 17 within the non-terminable maturity period amount to a total of L 4,734,000. No major financial obligations existed as at March 31, 2005 in connection with investment projects. Supplier contracts exist with selected suppliers, which depend on requirements, to a normal business extent. Within the framework of long term credit financing there exist possible obligations towards a bank from a debtor warrant in the maximum amount of up to L 4,500,000, which in the event of a sale of a participation and / or on a going concern basis could lead to a payment within the context of an excess cash flow regulation.

Management Board and Supervisory Board

The members of the Supervisory Board and the Management Board as at June 30, 2005 have not changed versus December 31, 2004.

Other notes

Up to the end of the drawing up of this interim report there were no significant changes of a legal or economic nature following the balance sheet date (30.06.2005).

We draw attention to the fact that differences can occur due to the rounding in the tables and summaries presented in respect of the use of rounded amounts and percentages.

Interim report 1-9/2005 November 2005

Analysts’ conferences November and December 2005

Annual report 2005 March 2006

Interim report 1-3/2006 May 2006

General meeting of shareholders May 2006

Corporate calendar

1.1

0_

Expl

anat

ory

note

s on

the

hal

f ye

ar f

inan

cial

sta

tem

ents

elexis AGIndustriestr. 157482 WendenTel. (02762) 612 - 130Fax (02762) 612 - 135

www.elexis.de