REPORT No. 505...Ltd (Feng Hsin)) and the Kingdom of Thailand (Thailand) to Australia is justified....

80

PUBLIC RECORD CUSTOMS ACT 1901 - PART XVB REPORT No. 505 CONTINUATION INQUIRY INTO ANTI-DUMPING MEASURES APPLYING TO CERTAIN HOT ROLLED STRUCTURAL STEEL SECTIONS EXPORTED TO AUSTRALIA FROM JAPAN, THE REPUBLIC OF KOREA, TAIWAN (EXCEPT FOR EXPORTS BY FENG HSIN STEEL CO LTD) AND THE KINGDOM OF THAILAND 11 October 2019

Transcript of REPORT No. 505...Ltd (Feng Hsin)) and the Kingdom of Thailand (Thailand) to Australia is justified....

PUBLIC RECORD

CUSTOMS ACT 1901 - PART XVB

REPORT No. 505

CONTINUATION INQUIRY INTO ANTI-DUMPING MEASURES APPLYING TO CERTAIN

HOT ROLLED STRUCTURAL STEEL SECTIONS

EXPORTED TO AUSTRALIA FROM

JAPAN, THE REPUBLIC OF KOREA, TAIWAN (EXCEPT FOR EXPORTS BY FENG HSIN STEEL CO LTD) AND THE

KINGDOM OF THAILAND

11 October 2019

PUBLIC RECORD

Continuation Inquiry 505 — HRS from Japan, Korea, Taiwan and Thailand

i

CONTENTS

CONTENTS .................................................................................................................................................................. I

ABBREVIATIONS ....................................................................................................................................................... III

1 SUMMARY ....................................................................................................................................................... 1

1.1 INTRODUCTION ........................................................................................................................................................ 1 1.2 LEGISLATIVE FRAMEWORK .......................................................................................................................................... 1 1.3 THE STATEMENT OF ESSENTIAL FACTS ........................................................................................................................... 2 1.4 THE PUBLIC RECORD ................................................................................................................................................. 2 1.5 SUBMISSIONS RECEIVED FROM INTERESTED PARTIES ........................................................................................................ 2 1.6 FINAL REPORT ......................................................................................................................................................... 3 1.7 FINDINGS ............................................................................................................................................................... 3 1.8 THE COMMISSIONER’S RECOMMENDATIONS ................................................................................................................. 3

2 BACKGROUND .................................................................................................................................................. 5

2.1 APPLICATION AND INITIATION ..................................................................................................................................... 5 2.2 SUBMISSION RECEIVED REGARDING THE APPLICATION ...................................................................................................... 6 2.3 HISTORY OF THE EXISTING ANTI-DUMPING MEASURES...................................................................................................... 6 2.4 REVIEW 499 ........................................................................................................................................................... 8 2.5 NOTIFICATION AND PARTICIPATION IN THE INQUIRY ........................................................................................................ 9 2.6 DUMPING MARGINS ................................................................................................................................................. 9

3 THE GOODS, LIKE GOODS AND THE AUSTRALIAN INDUSTRY .......................................................................... 11

3.1 LEGISLATIVE FRAMEWORK ........................................................................................................................................ 11 3.2 THE GOODS SUBJECT TO THE ANTI-DUMPING MEASURES ................................................................................................ 11 3.3 TARIFF CLASSIFICATION ........................................................................................................................................... 11 3.4 OTHER INFORMATION – AUSTRALIAN STEEL STANDARD ................................................................................................. 12 3.5 THE AUSTRALIAN INDUSTRY ..................................................................................................................................... 12 3.6 LIKE GOODS .......................................................................................................................................................... 12

4 THE AUSTRALIAN MARKET ............................................................................................................................. 14

4.1 SUPPLY OF THE AUSTRALIAN HRS MARKET .................................................................................................................. 14 4.2 SUBSTITUTABLE PRODUCTS ...................................................................................................................................... 14 4.3 IMPORTERS ........................................................................................................................................................... 14 4.4 EXPORTERS TO AUSTRALIA ....................................................................................................................................... 14 4.5 MARKET SIZE......................................................................................................................................................... 15 4.6 DEMAND IN THE AUSTRALIAN HRS MARKET ................................................................................................................ 15 4.7 IMPORT PARITY PRICING .......................................................................................................................................... 16

5 ECONOMIC CONDITION OF THE AUSTRALIAN INDUSTRY ............................................................................... 18

5.1 APPROACH TO ANALYSIS .......................................................................................................................................... 18 5.2 FINDINGS IN THE ORIGINAL INVESTIGATION.................................................................................................................. 18 5.3 THE COMMISSION’S ANALYSIS – CONTINUATION INQUIRY 505 ....................................................................................... 18 5.4 CONCLUSION ........................................................................................................................................................ 26

6 VARIABLE FACTORS ........................................................................................................................................ 27

7 LIKELIHOOD THAT DUMPING WILL CONTINUE OR RECUR .............................................................................. 28

7.1 AUSTRALIAN INDUSTRY’S CLAIMS .............................................................................................................................. 28 7.2 LIKELIHOOD OF CONTINUATION OR RECURRENCE OF DUMPING ........................................................................................ 32 7.3 SUMMARY ............................................................................................................................................................ 39

8 LIKELIHOOD THAT MATERIAL INJURY WILL CONTINUE OR RECUR? ................................................................ 40

8.1 AUSTRALIAN INDUSTRY’S CLAIMS .............................................................................................................................. 40 8.2 THE COMMISSION’S ANALYSIS .................................................................................................................................. 40

PUBLIC RECORD

Continuation Inquiry 505 — HRS from Japan, Korea, Taiwan and Thailand

ii

8.3 SUMMARY ............................................................................................................................................................ 46

9 SUBMISSIONS – DUMPING AND MATERIAL INJURY ....................................................................................... 47

9.1 SUBMISSIONS FROM HYUNDAI .................................................................................................................................. 47 9.2 SUBMISSIONS FROM LIBERTY STEEL IN RESPONSE TO HYUNDAI ........................................................................................ 49 9.3 THE COMMISSION’S ANALYSIS .................................................................................................................................. 50 9.4 SUBMISSIONS BY LIBERTY STEEL IN RESPECT OF SYS ...................................................................................................... 53 9.5 SUBMISSIONS BY SYS.............................................................................................................................................. 54 9.6 SUBMISSIONS ON MATERIAL INJURY BY DRAGON STEEL .................................................................................................. 57 9.7 SUBMISSION FROM LIBERTY STEEL IN RESPONSE TO TUNG HO......................................................................................... 61 9.8 SUBMISSION FROM TUNG HO IN RESPONSE TO LIBERTY STEEL......................................................................................... 61

10 SUMMARY AND CONCLUSION ....................................................................................................................... 62

10.1 SUMMARY ............................................................................................................................................................ 62 10.2 CONCLUSION ........................................................................................................................................................ 62

11 RECOMMENDATIONS ..................................................................................................................................... 64

12 LIST OF APPENDICES ....................................................................................................................................... 65

NON-CONFIDENTIAL APPENDIX 1 - VARIABLE FACTORS ESTABLISHED IN REVIEW 499 ............................................ 66

PUBLIC RECORD

Continuation Inquiry 505 — HRS from Japan, Korea, Taiwan and Thailand

iii

ABBREVIATIONS

the 2016 Steel and Aluminium Report

Analysis of Steel and Aluminium Markets Report to the Commissioner of the Anti-Dumping Commission

the 2017 Steel Manufacturing and Fabricating Markets report

Analysis of Australia’s Steel Manufacturing and Fabricating Markets Report to the Commissioner of the Anti-Dumping Commission November 2017

ABF Australian Border Force

ACCC Australian Competition and Consumer Commission

the Act the Customs Act 1901

ADN Anti-Dumping Notice

Ai Group Australian Industry Group

the applicant OneSteel Manufacturing Pty Ltd trading as Liberty Steel

ASEAN Association of Southeast Asian Nations

BOS basic oxygen steelmaking

China the People’s Republic of China

the Commission the Anti-Dumping Commission

the Commissioner the Commissioner of the Anti-Dumping Commission

CTMS cost to make and sell

Dragon Steel Dragon Steel Corporation

the Dumping Duty Act the Customs Tariff (Anti-Dumping) Act 1975

EAF electric arc furnace

EPR electronic public record

Feng Hsin Feng Hsin Steel Co Ltd

FOB free on board

FIS free in store

FY financial year, being the period from 1 July to 30 June

the goods the goods the subject of the application

GUC goods under consideration

IPP import parity pricing

Hyundai Hyundai Steel Co., Ltd

HRS hot rolled structural steel sections

IDD interim dumping duty

Korea the Republic of Korea

Liberty Steel OneSteel Manufacturing Pty Ltd trading as Liberty Steel

the Minister the Minister for Industry, Science and Technology

MPa Megapascals

NIP non-injurious price

OECD Organisation for Economic Co-operation and Development

OneSteel OneSteel Manufacturing Pty Ltd

PUBLIC RECORD

Continuation Inquiry 505 — HRS from Japan, Korea, Taiwan and Thailand

iv

OneSteel Trading OneSteel Trading Pty Ltd

the then Parliamentary Secretary

the then Parliamentary Secretary to the Minister for Industry

REP 223 Anti-Dumping Commission Report No. 223

REP 499 Final report for Review of Measures 499

ROI return on investment

SEF 505 statement of essential facts for Continuation Inquiry 505

Steelforce Steelforce Holdings Pty Ltd

SYS Siam Yamato Steel Co Ltd

Thailand the Kingdom of Thailand

TS Steel TS Steel Co Ltd

Tung Ho Tung Ho Steel Enterprise Corporation

USA United States of America

USP unsuppressed selling price

WTO World Trade Organization

PUBLIC RECORD

Continuation Inquiry 505 — HRS from Japan, Korea, Taiwan and Thailand

1

1 SUMMARY

1.1 Introduction

This report sets out the facts on which the Commissioner of the Anti-Dumping Commission (the Commissioner and the Commission respectively) bases recommendations to the Minister for Industry, Science and Technology (the Minister) on whether the continuation of anti-dumping measures, in the form of a dumping duty notice, that apply to exports of hot rolled structural steel sections (HRS or ‘the goods’) from Japan, the Republic of Korea (Korea), Taiwan (except for exports by Feng Hsin Steel Co Ltd (Feng Hsin)) and the Kingdom of Thailand (Thailand) to Australia is justified.

The anti-dumping measures are due to expire on 20 November 2019 (the specified expiry day). This inquiry considers whether the continuation of the anti-dumping measures, as amended by Review 499, beyond the specified expiry day, is justified.

This inquiry is being conducted in response to an application lodged by OneSteel Manufacturing Pty Ltd trading as Liberty Steel (Liberty Steel).1

1.2 Legislative framework

Division 6A of Part XVB of the Customs Act 1901 (the Act) 2 sets out, among other things, the procedures to be followed by the Commissioner in dealing with an application for the continuation of anti-dumping measures.

Section 269ZHE(1) requires that the Commissioner must, within 110 days after the publication of the notice or such longer period as allowed, place on the public record a statement of the essential facts (SEF) which the Commissioner proposes to base his recommendations to the Minister concerning the continuation of the measures. Section 269ZHE(2) requires that in doing so, the Commissioner must have regard to the application and any submissions received within 37 days of the initiation of the inquiry, and may have regard to any other matters that he considers relevant.

Under subsection 269ZHE(3), the Commissioner is not obliged to have regard to any submissions relating generally to the inquiry that are received by the Commissioner after the end of the 37 day period referred to in subsection 269ZHE(2) if to do so would, in the Commissioner’s opinion, prevent the timely placement of the SEF on the public record.3

Under subsection 269ZHF(4), the Commissioner is not obliged to have regard to any submissions made in response to the SEF that are received by the Commissioner after the end of the 20 day period after publication of the SEF and referred to in subsection

1 On 29 July 2019, Liberty Steel was re-named. Since that date it is known as OneSteel Manufacturing Pty Ltd trading as Infrabuild Steel. In this report, it is referred to as Liberty Steel, the trading name recorded by the company on its application. 2 All legislative references are to the Customs Act 1901, unless otherwise specified. 3 Under 269ZHE(3), the Commissioner did not have regard to two submissions that were received by the Commissioner after the end of the 37 day period referred to in subsection 269ZHE(2) because to do so would, in the Commissioner’s opinion, prevent the timely placement of the SEF on the public record. These submissions were: a submission from Staughtons Trade Advisory Group Pty Ltd on behalf of Siam Yamato Steel received on 7 August 2019; and a submission from J. Bracic and Associates on behalf of Dragon Steel Corporation received on 9 August 2019. The Commissioner has had regard to these submissions in preparing this report. These submissions are on the public record.

PUBLIC RECORD

Continuation Inquiry 505 — HRS from Japan, Korea, Taiwan and Thailand

2

269ZHF(3) if to do so would, in the Commissioner’s opinion, prevent the timely preparation of the report to the Minister.

Subsection 269ZHF(1) requires that the Commissioner must, after the conduct of this inquiry, give the Minister a report which recommends that the relevant notice:

remain unaltered;

cease to apply to a particular exporter or to a particular kind of goods;

have effect in relation to a particular exporter or to exporters generally as if different variable factors had been ascertained; or

expire on the specified expiry day.

Under subsection 269ZHF(2), the Commissioner must not recommend that the Minister take steps to secure the continuation of the anti-dumping measures unless the Commissioner is satisfied that the expiration of the anti-dumping measures would lead, or would be likely to lead, to a continuation of, or a recurrence of, the dumping and the material injury that the anti-dumping measures are intended to prevent.

1.3 The statement of essential facts

The Commissioner published Statement of Essential Facts No. 505 (SEF 505) on 12 August 2019. The SEF set out the essential facts on which the Commissioner proposed to base his final recommendations to the Minister based on the information before him at that time. Interested parties were invited to lodge written submissions in response to SEF 505 by no later than 2 September 2019.4

1.4 The public record

The public record contains non-confidential submissions from interested parties, non-confidential versions of the Commission’s verification reports and other publicly available documents.

1.5 Submissions received from interested parties

The Commission received several submissions in response to SEF 505 which are available on the public record.

Under section 269ZHF(4), the Commissioner is not obliged to have regard to any submissions made in response to the SEF that were received after 2 September 2019 if to do so would, in the Commissioner’s opinion, prevent the timely preparation of the report to the Minister. The Commissioner has not had regard to a submission received on 8 October 2019 from Staughtons Trade Advisory Group Pty Ltd on behalf of ThyssenKrupp Materials Trading Australia and to a submission received on 9 October 2019 from Liberty Steel because to do so would, in the Commissioner’s opinion, prevent the timely preparation of this report to the Minister. These submissions are on the public record.5

4 The due date of 1 September 2019 fell on a Sunday. The effective date was Monday 2 September 2019. 5 Item 57 and item 58 respectively on the public record refer.

PUBLIC RECORD

Continuation Inquiry 505 — HRS from Japan, Korea, Taiwan and Thailand

3

1.6 Final report

The Commissioner’s final report and recommendations must be provided to the Minister within 155 days after the publication of a notice under section 269ZHD(4) or such longer period as the Minister allows.

Extensions of time for the provision of the Commissioner’s final report and recommendations to the Minister have been granted under subsection 269ZHI(3). The Commissioner’s recommendations are due to be made in a report to be provided to the Minister on or before 14 October 2019.

Refer to section 2.1 of this report for further details.

1.7 Findings

Based on the Commission’s analysis of the available evidence, the Commissioner is satisfied that if the anti-dumping measures expire, it is likely that:

dumping of HRS will continue by;

o all exporters from Japan;

o all exporters from Korea;

o Dragon Steel and uncooperative exporters from Taiwan; and

o all exporters from Thailand

and

dumping of HRS by TS Steel Co Ltd (TS Steel) of Taiwan will recur.

The Commissioner is not satisfied that if the anti-dumping measures expire, it is likely that dumping of HRS by Tung Ho Steel Enterprise Corporation (Tung Ho) of Taiwan will recur.

Based on the Commission’s analysis of the available evidence, the Commissioner is satisfied that the expiration of the anti-dumping measures on exports of HRS to Australia from Japan, Korea, Taiwan (except for Feng Hsin and Tung Ho) and Thailand would be likely to lead to a continuation of the material injury that the anti-dumping measures are intended to prevent.

1.8 The Commissioner’s recommendations 6

The Commissioner recommends to the Minister that:

in accordance with subsection 269ZHG(1)(b), DECLARE that the Minister has decided to secure the continuation of the anti-dumping measures relating to HRS exported to Australia from Japan, Korea, Taiwan (except for Feng Hsin and Tung Ho) and Thailand; and

in accordance with subsection 269ZHG(1)(a), DECLARE that the Minister has decided not to secure the continuation of the anti-dumping measures currently applying to HRS exported to Australia from Taiwan by Tung Ho.

6 For the purposes of this continuation inquiry, the Commissioner has had regard to other matters considered relevant to the inquiry, including the variable factors established in Review 499. In respect of Review 499, the Commissioner recommended to the Minister that the dumping duty notice be altered in respect of HRS exported to Australia from Japan, Korea, Taiwan (except for Feng Hsin) and Thailand. Refer to REP 499 which is on the public record.

PUBLIC RECORD

Continuation Inquiry 505 — HRS from Japan, Korea, Taiwan and Thailand

4

The Commissioner recommends that the Minister, in accordance with subsection 269ZHG(4)(a)(ii), DETERMINE that the dumping duty notice continues in force after 20 November 2019, but that after that day the notice ceases to apply to Tung Ho.

PUBLIC RECORD

Continuation Inquiry 505 — HRS from Japan, Korea, Taiwan and Thailand

5

2 BACKGROUND

2.1 Application and initiation

On 23 November 2018, and in accordance with subsection 269ZHB(1), the Commissioner published a notice 7 on the Commission’s website inviting the following persons to apply for the continuation of the anti-dumping measures:

the person whose application under section 269TB resulted in the anti-dumping measures (subsection 269ZHB(1)(b)(i)); or

persons representing the whole or a portion of the Australian industry producing like goods to the goods covered by the anti-dumping measures (subsection 269ZHB(1)(b)(ii)).

On 21 January 2019, an application for the continuation of the anti-dumping measures was received from Liberty Steel. A non-confidential version of the application is available on the Commission’s public record.

Following consideration of the application, the Commissioner decided not to reject the application and initiated Continuation Inquiry 505. Notification of the initiation of the inquiry was made in Anti-Dumping Notice (ADN) No. 2019/21 which was published on the Commission’s website on 11 February 2019. ADN No. 2019/21 indicated that the Commissioner will examine the period from 1 January 2018 to 31 December 2018 (the inquiry period) to determine whether the anti-dumping measures should:

i. remain unaltered; or ii. cease to apply to a particular exporter or to a particular kind of goods; or iii. have effect in relation to a particular exporter or to exporters generally, as if

different variable factors had been ascertained; or iv. expire on the specified expiry day.

The Commissioner indicated in ADN No. 2019/21 that a SEF will be placed on the public record by 23 April 2019 and that a recommendation to the Minister will be made in a report on or before 7 June 2019.

On 15 April 2019, the timeframe for publishing the SEF and final report was extended under subsection 269ZHI(3) to allow time to analyse submissions and matters in relation to injury effects and causation, as well as the likelihood that dumping will continue or recur. Notification of this extension was made in ADN No. 2019/55 8 which indicated that the SEF would be published no later than 11 July 2019 and that the Commissioner’s recommendations will be made in a final report due to be provided to the Minister on or before 30 August 2019.

On 8 July 2019, the timeframe for publishing the SEF and final report was extended under subsection 269ZHI(3) to allow time to consider submissions from interested parties in respect of material injury claims made by the applicant. Notification of this extension was made in ADN No. 2019/87 9 which indicated that the SEF would be published no later

7 ADN No. 2019/173 refers. 8 Item 7 on the public record refers. 9 Item 22 on the public record refers.

PUBLIC RECORD

Continuation Inquiry 505 — HRS from Japan, Korea, Taiwan and Thailand

6

than 12 August 2019 and that the Commissioner’s recommendations will be made in a report due to be provided to the Minister on or before 1 October 2019.

On 11 September 2019, the timeframe for providing the final report to the Minister was extended under subsection 269ZHI(3) to allow time to consider submissions made in response to the SEF from interested parties. Notification of this extension was made in ADN No. 2019/117 10 which indicated that the Commissioner’s recommendations will be made in a report due to be provided to the Minister on or before 14 October 2019.

Further details are available on the Commission’s website.

2.2 Submission received regarding the application

2.2.1 Siam Yamato Steel Co Ltd submission of 4 April 2019

On 4 April 2019, Siam Yamato Steel Co Ltd (SYS) submitted that the continuation of measures is not justified and that the application should have been rejected.11

The Commission’s assessment

The submission was received after the Commissioner published a notice under subsection 269ZHD(4) indicating that this inquiry had already been initiated. ADN No. 2019/21 provides the reasons why the Commissioner did not reject the application. For those reasons, the Commissioner remains of the view that the application should not have been rejected.

2.3 History of the existing anti-dumping measures

2.3.1 Original investigation

On 24 October 2013, a dumping investigation into HRS exported to Australia from Japan, Korea, Taiwan and Thailand was initiated following an application lodged by OneSteel,12 a manufacturer of HRS in Australia. The investigation period was 1 October 2012 to 30 September 2013.

In that investigation, as outlined in Anti-Dumping Commission Report No. 223 (REP 223),13 it was found that:

the goods exported to Australia from Japan, Korea, Taiwan and Thailand were dumped, with margins ranging from 2.20 per cent to 19.48 per cent;

10 Item 47 on the public record refers. 11 Item 6 on the public record refers. 12 At that time, Liberty Steel was trading as OneSteel. In 2018, OneSteel began referring to itself as OneSteel Manufacturing Pty Ltd trading as Liberty Steel. As stated in Footnote 1 of this report, on 29 July 2019 Liberty Steel was re-named but in this report it is referred to as Liberty Steel, the trading name recorded by the company in its application.

In 2017, OneSteel was acquired by the Liberty House Steel Group and became part of its Liberty Steel Division. The Liberty House Steel Group is an international metals and industrial group, specialising in commodities, metals recycling, and the manufacture of steel, aluminium and engineering products which has its headquarters in London. It is part of the GFG Alliance is an international grouping of businesses, founded by the British Gupta family. 13 Item 96 on the public record for Investigation 223 refers.

PUBLIC RECORD

Continuation Inquiry 505 — HRS from Japan, Korea, Taiwan and Thailand

7

the dumped exports caused material injury to the Australian industry producing like goods; and

continued dumping may cause further material injury to the Australian industry.

The findings and recommendations in REP 223 were provided to the then Parliamentary Secretary to the Minister for Industry (the then Parliamentary Secretary), recommending the publication of a dumping duty notice in respect of the goods. Notice of the then Parliamentary Secretary’s decision to accept the recommendations in REP 223 was published in The Australian newspaper and the Commonwealth of Australia Gazette. Interested parties were also advised of this outcome in ADN No. 2014/127 on 20 November 2014.14

During the conduct of Investigation 223 and after becoming satisfied that during the investigation period Feng Hsin did not dump HRS, the Commissioner terminated the investigation insofar as it related to that exporter on 31 October 2014. As such, Feng Hsin is exempt from anti-dumping measures. Termination of Investigation No. 223 sets out the reasons for this termination and is available on the public record for Investigation 223.

On 7 August 2015, following a review by the Anti-Dumping Review Panel of the decision to impose dumping duties, the dumping duty notice was varied so that the effective rate of duty for HRS exported to Australia by SYS was altered from 18.28 per cent to 18.00 per cent with effect from 20 November 2014.

2.3.2 Previous reviews of measures

Review 345 - exports of the goods from Taiwan by Tung Ho

On 21 March 2016, Tung Ho lodged an application for a review of the dumping duty notice applying to HRS exported to Australia from Taiwan claiming that the variable factors relevant to the taking of the anti-dumping measures had changed.

The review period was 1 January 2015 to 31 December 2015.

In Anti-Dumping Commission Report No. 345, the Commissioner found that Tung Ho was not dumping and recommended that the dumping duty notice have effect in relation to Tung Ho as if different variable factors relevant to the determination of duty had been ascertained.

The then Parliamentary Secretary’s decision to alter the notice as it applied to Tung Ho was published on the Commission’s website on 19 October 2016. The effect of the review was that the measures applying to exports from Tung Ho were altered from a dumping margin of 2.2 per cent (ad valorem duty method) to a floor price.

Review 346 - exports of the goods from Thailand by SYS

On 23 March 2016, SYS lodged an application for a review of the dumping duty notice applying to HRS exported to Australia from Thailand insofar as it affected SYS. The review period was 1 January 2015 to 31 December 2015.

In Anti-Dumping Commission Report No. 346, the Commissioner found that SYS was not dumping and recommended that the dumping duty notice have effect in relation to SYS as if different variable factors relevant to the determination of duty had been ascertained.

14 Item 98 on the public record for Investigation 223 refers.

PUBLIC RECORD

Continuation Inquiry 505 — HRS from Japan, Korea, Taiwan and Thailand

8

The then Parliamentary Secretary’s decision to alter the notice as it applied to SYS was published on the Commission’s website on 19 October 2016. The effect of the review was that the measures applying to exports from SYS were altered from a dumping margin of 18.0 per cent (ad valorem duty method) to a floor price.

Accelerated review 359 - exports from Taiwan by Dragon Steel Corporation

On 9 June 2016, Dragon Steel Corporation (Dragon Steel) lodged an application for an accelerated review of the dumping duty notice applying to certain HRS exported to Australia from Taiwan insofar as it affected Dragon Steel. The review period was 1 April 2015 to 31 March 2016.

Anti-Dumping Commission Report No. 359 recommended that the dumping duty notice have effect in relation to Dragon Steel as if the then Parliamentary Secretary had fixed specific different variable factors relevant to the determination of duty.

The then Parliamentary Secretary’s decision to alter the notice as it applied to Dragon Steel was published on the Commission’s website on 18 October 2016. The effect of the accelerated review was that measures applying to exports from Dragon Steel were altered from a dumping margin of 7.9 per cent (ad valorem duty method) to a floor price.

Review 465 - exports of the goods from Korea

On 27 February 2018, Liberty Steel 15 lodged an application requesting a review of the anti-dumping measures as they apply to all exporters of HRS to Australia from Korea. The review period for Review 465 was 1 January 2017 to 31 December 2017.

Anti-Dumping Commission Report No. 465 recommended that the dumping duty notice have effect in relation to:

Hyundai Steel Co., Ltd (Hyundai); and

uncooperative and all other exporters from Korea

as if different variable factors relevant to the determination of duty had been ascertained.

The Minister’s decision to alter the notice was published on the Commission’s web site on 18 December 2018. The effect of the review was that:

measures applying to exports from Hyundai were altered from 2.52 per cent (ad valorem duty method) to 9.9 per cent (combination fixed and variable duty method); and

measures applying to uncooperative exporters from Korea were altered from 3.24 per cent (ad valorem duty method) to 13.9 per cent (combination fixed and variable duty method) .

2.4 Review 499

On 21 November 2018, an application was lodged by Liberty Steel requesting a review of the anti-dumping measures as they apply to all exporters of HRS to Australia from Japan, Korea, Taiwan (except for exports by Feng Hsin) and Thailand.

The Commissioner decided not to reject the application. Notification of Review 499 was made in ADN No. 2019/02 which was published on the Commission’s website on 3 January 2019.

15 In that application, OneSteel Manufacturing Pty Ltd indicated that it was trading as Liberty OneSteel.

PUBLIC RECORD

Continuation Inquiry 505 — HRS from Japan, Korea, Taiwan and Thailand

9

2.5 Notification and participation in the inquiry

On 11 February 2019, ADN No.2019/21 advised of the initiation of this continuation inquiry. The Commissioner established an inquiry period of 1 January 2018 to 31 December 2018.

ADN No. 2019/21 noted that the applicant, the countries from which the goods are under review, the respective importers and exporters of HRS and the period being examined in Review 499 are identical to those in this continuation inquiry.

For the purposes of this continuation inquiry, the Commissioner has had regard to other matters considered relevant to the inquiry, including the variable factors established in Review 499, to assess whether dumping has occurred during the inquiry period, and whether dumping is likely to continue or recur if the anti-dumping measures were to expire. Details of the variable factors established in Review 499 are at Non-Confidential Appendix 1.

2.5.1 Australian industry

Liberty Steel, the sole manufacturer of HRS in Australia, provided sales and cost to make and sell (CTMS) data to the Commission. The Commission visited Liberty Steel’s manufacturing plant on 19 to 21 March 2019 and its offices on 26 to 27 March 2019 to verify the information and data. The report in relation to these visits is available on the public record.16

2.5.2 Importers and exporters

The Commission performed a search of the Australian Border Force (ABF) import database and identified exporters and importers of HRS from Japan, Korea, Taiwan and Thailand during the inquiry period. All these exporters and importers were notified of the details of this inquiry and were invited to provide submissions.

As the Commissioner’s intention at the time of the initiation of this inquiry was to have regard to the variable factors established in Review 499 to assess whether dumping has occurred during the inquiry period, questionnaires were not required from exporters or importers.

Subsection 269T(1) provides that for an inquiry under Division 6A in relation to the publication of a dumping duty notice, an exporter is a ‘cooperative exporter’ where the exporter’s exports were examined as part of the inquiry and the exporter was not an ‘uncooperative’ exporter in relation to the inquiry.

The exporter and importer verification reports are available on the public records on Commission’s website for both this inquiry and for Review 499.

2.6 Dumping margins

The dumping margins that were found in the original investigation, or altered as the result of a subsequent review as described in section 2.3.2, and the respective forms of anti-dumping measures that applied at the time this continuation inquiry was initiated are provided in Table 1.

16 Item 8 of the public record refers.

PUBLIC RECORD

Continuation Inquiry 505 — HRS from Japan, Korea, Taiwan and Thailand

10

Country Manufacturer/ exporter Dumping margin

Duty Method

Method to establish

dumping margin

Japan

JFE Bars and Shapes Corporation

12.2% Ad valorem

Weighted average export prices were

compared with corresponding

normal values over the inquiiry period

in terms of s. 269TACB(2)(a) of the Customs Act

1901.

Uncooperative Exporters 12.2% Ad valorem

Korea

Hyundai Steel Company 9.9% Combination of fixed and variable duty method

Uncooperative Exporters 13.9% Combination of fixed and variable duty method

Taiwan

Dragon Steel Corporation N/A Floor price

TS Steel Co Ltd 4.7% Ad valorem

Tung Ho Steel Enterprise Corporation

N/A Floor price

Uncooperative Exporters 7.9% Ad valorem

Thailand Siam Yamato Steel Co Ltd N/A Floor price

Uncooperative Exporters 19.5% Ad valorem

Table 1 — HRS current dumping margins

PUBLIC RECORD

Continuation Inquiry 505 — HRS from Japan, Korea, Taiwan and Thailand

11

3 THE GOODS, LIKE GOODS AND THE AUSTRALIAN INDUSTRY

3.1 Legislative framework

The Commissioner must be satisfied that ‘like’ goods to the goods the subject of the anti-dumping measures are produced in Australia.

In making this assessment, the Commissioner must first determine that the goods produced by the Australian industry are ‘like’ to the imported goods. Subsection 269T(1) defines like goods as:

… goods that are identical in all respects to the goods under consideration or that, although not alike in all respects to the goods under consideration, have characteristics closely resembling those of the goods under consideration.

Subsection 269T(2) specifies that for goods to be regarded as being produced in Australia, they must be wholly or partly manufactured in Australia. In accordance with subsection 269T(3), at least one substantial process in the manufacture of those goods must be carried out in Australia for goods to be considered as partly manufactured in Australia.

3.2 The goods subject to the anti-dumping measures

The goods to which the current anti-dumping measures apply (the goods) are:

Hot rolled structural steel sections in the following shapes and sizes, whether or not containing alloys:

universal beams (I sections), of a height greater than 130 mm and less than 650 mm;

universal columns and universal bearing piles (H sections), of a height greater than 130 mm and less than 650 mm;

channels (U sections and C sections) of a height greater than 130 mm and less than 400 mm; and

equal and unequal angles (L sections), with a combined leg length of greater than 200 mm.

Sections and/or shapes in the dimensions described above, that have minimal processing, such as cutting, drilling or painting do not exclude the goods from coverage of the investigation.

The measures do not apply to the following goods:

hot rolled ‘T’ shaped sections, sheet pile sections and hot rolled merchant bar shaped sections, such as rounds, squares, flats, hexagons, sleepers and rails; and

sections manufactured from welded plate (e.g. welded beams and welded columns).

3.3 Tariff classification

Goods identified as hot rolled non-alloy steel sections (meeting the specified shapes and sizes set out above) are generally classified to the tariff subheading in Schedule 3 of the Customs Tariff Act 1995:

PUBLIC RECORD

Continuation Inquiry 505 — HRS from Japan, Korea, Taiwan and Thailand

12

7216.31.00 statistical code 30 (channels — U and C sections);

7216.32.00 statistical code 31(universal beams — I sections);

7216.33.00 statistical code 32 (universal column and universal bearing piles — H sections); and

7216.40.00 statistical code 33 (equal and unequal angles — L sections).

Goods identified as hot rolled alloy steel sections (meeting the specified shapes and sizes set out above) are generally classified to tariff subheading 7228.70.00 (statistical codes 11 and 12) in schedule 3 of the Customs Tariff Act 1995.

3.4 Other information – Australian steel standard

Imported HRS generally meets the requirements of Australian standard AS/NZA3679.1.

Liberty Steel’s standard HRS range is manufactured to 300 megapascals (MPa) yield strength as required by the Australian standard and is branded as 300PLUS. Liberty Steel confirmed that its entire range is manufactured to meet or exceed the Australian standard.

Liberty Steel also manufactures HRS product to ‘Grade 350’, which has a minimum yield strength of 350 MPa. Liberty Steel only manufactures ‘Grade 350’ on a custom order basis.

3.5 The Australian industry

Liberty Steel’s HRS manufacturing facilities are the fully integrated Whyalla Steelworks located in South Australia that includes the HRS rolling mill.

The Commission has visited Liberty Steel and has found that HRS is wholly produced in Australia at the Whyalla Steelworks. All HRS that is made by the Australian industry is produced at the Whyalla Steelworks.

HRS is manufactured at the Whyalla Steelworks by heating semi-finished steel in the form of blooms and rolling it to shape and size in a rolling mill. The Whyalla Steel works produces semi-finished steel that is used in Liberty Steel’s various rolling facilities, including in Whyalla.

The Whyalla Steelworks produces steel using a basic oxygen steelmaking (BOS) system in which liquid steel is cast into blooms, billets, or slabs. Billet is a semi-finished steel product that is used as feed for rod and bar products (not subject to this inquiry). Slab is a semi-finished steel product that is produced for export (not subject to this inquiry).

The Commissioner is satisfied that there is an Australian industry producing like goods to the imported HRS and that this industry comprises that part of Liberty Steel that produces like goods at the Whyalla Steelworks.

3.6 Like goods

Subsection 269T(1) defines like goods as:

…goods that are identical in all respects to the goods under consideration or that, although not alike in all respects to the goods under consideration, have characteristics closely resembling those of the goods under consideration.

PUBLIC RECORD

Continuation Inquiry 505 — HRS from Japan, Korea, Taiwan and Thailand

13

The Commission has conducted a verification visit to Liberty Steel 17 and has found that the HRS manufactured in Australia are like goods on the following grounds:

Physical likeness: the primary physical characteristics of the goods and locally manufactured goods have similar shape, dimensions, appearance, weight and are produced to meet the same Australian standard;

Commercial likeness: the goods manufactured in Australia and the imported goods are commercially alike, directly competitive and are sold to common customers in the Australian market;

Functional likeness: both the goods manufactured in Australia and the imported goods are functionally alike as they have the same range of end uses; and

Production likeness: the goods manufactured in Australia are manufactured in a similar manner to the imported goods.

The findings on physical, commercial, functional and production likeness outlined above lead to the conclusion that the goods manufactured in Australia have characteristics closely resembling the goods the subject of the measures, and are therefore like goods. 18

17 Item 8 of the public record refers. 18 This is consistent with the Commission’s findings in Investigation 223. Item 96 on the public record for Investigation 223 refers.

PUBLIC RECORD

Continuation Inquiry 505 — HRS from Japan, Korea, Taiwan and Thailand

14

4 THE AUSTRALIAN MARKET

4.1 Supply of the Australian HRS market

At the industry verification visit, Liberty Steel indicated that the Australian HRS market is predominantly supplied by distributors and that one of these distributors is Liberty Metalcentre, which is a related entity of Liberty Steel.

The distributors source products from the Australian industry or from overseas suppliers. Liberty Steel generally competes at the level of trade supplying distributors. Sales of HRS by distributors are to end users.

4.2 Substitutable products

At the industry verification visit, Liberty Steel indicated that the main alternative products to HRS are reinforced concrete along with imported fabricated steel components which are substitutable in some construction and engineering applications such as in high rise buildings.

4.3 Importers

The Commission has analysed ABF data and has found the 10 largest importers of HRS accounted for the vast majority of HRS imports from Japan, Korea, Taiwan and Thailand during the inquiry period. The Commission has found that eight of the top 10 importers of HRS in 2018 have been in the group of top 10 importers of HRS since 2010. Further, in 2018, all of those importers sourced HRS from countries and exporters subject to measures.

The Commission notes that in the inquiry period, Liberty Steel, through a combination of imports of its own accord or through other parties, was one of the major importers of HRS. These imports were of one type of section and were from Korea and Taiwan. The volume of imports by Liberty Steel was substantially higher in the year prior to the inquiry period. From 2011 to 2016, Liberty Steel’s import volumes of HRS were non-material relative to the total volume of HRS imports in the same period.

The Commissioner does not consider that the importation of the goods by Liberty Steel precludes it from also being the Australian industry producing HRS, or affects the Commission’s finding that Liberty Steel is the Australian industry producing like goods.

The Commission has received a number of submissions in respect of Liberty Steel’s importations of HRS and the purported implications of these importations on the Commission’s assessment of the Australian industry and the material injury experienced by the Australian industry. These submissions are discussed in detail in section 9 of this report.

4.4 Exporters to Australia

The Commission has analysed ABF data and has found that the 10 largest exporters of HRS to Australia accounted for the vast majority of HRS exports from the countries subject to measures during the inquiry period. The Commission has found that in 2018, the three largest exporters of HRS to Australia, Hyundai, Tung Ho and SYS, accounted for the largest proportion of HRS exports to Australia. The analysis also indicates that they have been the three largest exporters of HRS to Australia since 2010.

PUBLIC RECORD

Continuation Inquiry 505 — HRS from Japan, Korea, Taiwan and Thailand

15

4.5 Market size

The Commission has collated verified information submitted by Liberty Steel, importers and exporters, as well as ABF import data to estimate the size of the Australian HRS market. The Commission notes that at its full capacity, the Australian industry is not able to fully supply the entire Australian HRS market.

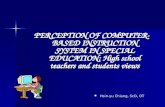

Figure 1 indicates the size of the entire Australian HRS market has fluctuated since 2010. In 2018, the HRS market was slightly larger than it was in 2010. The Commission also notes that since the implementation of the measures in 2014, there has been a general increase in the size of the whole Australian market.

Australian HRS Market (tonnes)

Figure 1 – Australian HRS Market Size

4.6 Demand in the Australian HRS market

The level of activity in the market segments in which end users operate drives demand in the Australian HRS market. The end users of HRS transform finished steel into fabricated products for a variety of end-uses.

In the Commission’s report, Analysis of Australia’s Steel Manufacturing and Fabricating Markets Report to the Commissioner of the Anti-Dumping Commission November 2017 (the 2017 Steel Manufacturing and Fabricating Markets Report), the Commission reported that the Australian steel fabrication industry is very diverse and primarily consists of small enterprises. It also reported that in 2013/14:

In Australia, about 88 per cent of steel fabricated products are purchased by three industries. These are:

• construction (50.3 per cent) • manufacturing (20.5 per cent)

PUBLIC RECORD

Continuation Inquiry 505 — HRS from Japan, Korea, Taiwan and Thailand

16

• mining (17.2 per cent).19

In the Commission’s Analysis of Steel and Aluminium Markets Report to the Commissioner of the Anti-Dumping Commission (the 2016 Steel and Aluminium Report),20 it was reported that most steel products are purchased by the construction, manufacturing and mining industries.

The Commission notes that the Australian Industry Group (Ai Group) in its November 2018 Construction Outlook 21 states that:

Turnover from all major construction work is forecast to further moderate in 2019-20 (+3.8%), mainly reflecting the negative influence of a sharp fall in multi-apartment building work (-17.6%).

However, engineering construction will lift to a higher level, with expected growth of 8.0%. The downturn in resources-related engineering construction is expected to have largely run its course in 2019-20 with the decline in construction on oil and gas processing projects to moderate markedly (-2.0%) over the year. In addition, a slight recovery in mining-related construction is forecast to emerge (+2.3%) as investment in new mine capacity lifts in response to improving commodity prices and a turnaround in exploration activity.

The expansion in non-mining infrastructure (+8.9%) is expected to ease somewhat over the year. This mainly reflects a slower growth contribution from other civil projects (+21.7%) while telecommunications is expected to decline by 13.7% as NBN spending winds down. Turnover derived from utilities construction is expected to hold at relatively unchanged levels on the back of support from investment in new pipeline infrastructure for gas supply, wind and solar projects, electrical sub-station upgrades and the construction of water treatment facilities.

Commercial construction is projected to continue to expand in 2019-20, albeit at a slower pace of 6.3%. Private sector building activity is expected to rise by 6.3% while investment in education and health building projects is set to underpin a 5.6% growth outlook for public sector building activity.

The Commission considers that this indicates that high levels of demand in the Australian HRS market will continue to be present from 2019 to 2020. The Commission also considers it is likely that some of this demand will continue to be met by importers.

4.7 Import parity pricing

In the original investigation (223), the Commission found that OneSteel sets its prices by applying an import parity pricing (IPP) process in which it negotiates prices with reference to offers made in the HRS market for imported goods.

In its application for the continuation of measures, Liberty Steel stated that it continues to apply the IPP process and that pricing in the Australian market is driven by prices of HRS exported from Japan, Korea, Taiwan and Thailand. Liberty Steel also stated that known import offers in the market are used as a tool by customers to negotiate lower prices from Liberty Steel.

19 This report is available on the Commission’s web site. 20 This report is available on the Commission’s web site. 21 This report is available at https://aib.org.au/wp-content/uploads/2018/12/Construction-Outlook-ACA.pdf.

PUBLIC RECORD

Continuation Inquiry 505 — HRS from Japan, Korea, Taiwan and Thailand

17

At the industry verification visit, the Commission was presented with evidence that indicated Liberty Steel continues to apply the IPP process and that the processes of price setting and negotiation as described in REP 223 and in Liberty Steel’s application remain in place. This evidence included the provision of Liberty Steel’s IPP model which is used to negotiate and set prices and that incorporates prices of imported HRS, copies of correspondence with customers as well as discussions with relevant sales personnel at Liberty Steel.

PUBLIC RECORD

Continuation Inquiry 505 — HRS from Japan, Korea, Taiwan and Thailand

18

5 ECONOMIC CONDITION OF THE AUSTRALIAN INDUSTRY

5.1 Approach to analysis

This chapter considers the economic condition of the Australian industry from 1 January 2010 to 31 December 2018. This period has been examined to analyse trends before and after the imposition of the anti-dumping measures.

The analysis detailed in this chapter is based on verified information submitted by Liberty Steel, importers, exporters, import data from the ABF and submissions by interested parties. This analysis has also been conducted with regard to qualitative information related to market structure, practices and trends that has been provided by interested parties or obtained by the Commission.

As explained at section 4.3 of this report, Liberty Steel has imported HRS either directly or via intermediaries. The Commission has focussed its analysis on data pertaining to Liberty Steel’s production of HRS and excluded data on its importations of HRS, such that an assessment of the economic conditions is made in respect of the Australian industry as a producer of HRS.

5.2 Findings in the original investigation

The investigation period for the original investigation was 1 October 2012 to 30 September 2013.

In the original investigation, the Commission found that dumping of HRS exported to Australia from Japan, Korea, Taiwan and Thailand had caused material injury to the Australian industry in the forms of:

price depression;

price suppression;

reduced profits and profitability; and

reduced revenues.

In the original investigation, the Commission did not accept the proposition that price pressures arising from price undercutting and the IPP process will necessarily result in a loss of sales volume. The Commission stated that there may be a range of market-based factors other than price which result in market share being maintained. For example, in section 9.9.5 of REP 223, the Commission highlighted exclusivity arrangements as a factor which limited Liberty Steel’s ability to increase its volume.

In the original investigation, the Commission had insufficient information to conclude that reduced capacity utilisation and reduced employment suffered by Liberty Steel had contributed to injury caused by dumping. The Commission also considered that it was inconclusive whether the other injury factors claimed by Liberty Steel in Appendix A7 to its application were caused by dumping, or caused by other factors.

5.3 The Commission’s analysis – Continuation Inquiry 505

5.3.1 Price depression and price suppression

Price depression occurs when a company, for some reason, lowers its prices. Price suppression occurs when price increases, which otherwise would have occurred, have

PUBLIC RECORD

Continuation Inquiry 505 — HRS from Japan, Korea, Taiwan and Thailand

19

been prevented. An indicator of price suppression may be the margin between revenues and costs.

Figure 2 shows Liberty Steel’s unit revenue and unit CTMS for HRS.

Unit Revenue and Unit Cost to Make and Sell (AUD)

Figure 2 – Liberty Steel HRS Unit Revenue and CTMS

After anti-dumping measures were imposed, Liberty Steel’s HRS prices fell but recovered to new high levels by 2018. As such, it is not possible to definitively conclude that Liberty Steel has experienced price depression in that time. However, Liberty Steel has been unable to achieve prices sufficiently high to cover the increasing CTMS of HRS. The Commission considers that Liberty Steel has experienced injury in the form of price suppression in the period since 2010.

5.3.2 Sales volume

Figure 3 shows Liberty Steel’s total sales volumes for HRS in the Australian market.

Sales Volume (tonnes)

Figure 3 – Liberty Steel HRS Sales Volume

Liberty Steel’s sales volumes of HRS has fluctuated over the analysis period. From 2010 to 2014, volumes were relatively consistent with a noticeable decline in the period leading

PUBLIC RECORD

Continuation Inquiry 505 — HRS from Japan, Korea, Taiwan and Thailand

20

to the imposition of measures. From 2015 to 2016, sales volumes recovered temporarily, but not to the levels achieved from 2010 to 2014, with variability observed thereafter.

The Commission considers that Liberty Steel has experienced injury in the form of reduced sales volume since 2010.

5.3.3 Sales revenue

Figure 4 shows Liberty Steel’s net sales revenue for HRS in the Australian market.

Net Sales Revenue (A$)

Figure 4 – Liberty Steel HRS Net Sales Revenue

When anti-dumping measures were imposed in November 2014, net sales revenue was in decline. Since 2015, sales revenue recovered somewhat, but not to levels achieved from 2011 to 2014. The Commission considers that Liberty Steel has experienced injury in the form of reduced sales revenue in the period since 2011.

5.3.4 Profit and profitability

Figure 5 indicates that Liberty Steel’s total profit from sales of HRS has been negative since 2010.

Total Profit (A$)

Figure 5 – Liberty Steel HRS Profit

PUBLIC RECORD

Continuation Inquiry 505 — HRS from Japan, Korea, Taiwan and Thailand

21

Figure 6 shows Liberty Steel’s unit profit and unit profitability for HRS has been negative since 2010.

Unit Profit (A$) and Unit Profitability

Figure 6 – Liberty Steel Unit profit and profitability (Unit Gain or Loss/Price)

Since 2014, the year when anti-dumping measures were imposed, Liberty Steel’s unit profit and profitability of HRS sold in Australia declined. In 2018, profit and profitability recovered somewhat, but only to similar levels of losses incurred before anti-dumping measures were imposed. Liberty Steel has not achieved positive results on profit and profitability in the entire period since 2010. The Commission considers that Liberty Steel has experienced injury in the forms of reduced profits and profitability in the period since 2014.

5.3.5 Market share

Figure 7 has been derived from verified data received from Liberty Steel and unverified data from the ABF import database. It indicates that Liberty Steel’s market share by volume increased from 2010 to 2013 and then decreased each year until 2017. It achieved a small recovery in 2018, but not to the levels achieved before 2017.

PUBLIC RECORD

Continuation Inquiry 505 — HRS from Japan, Korea, Taiwan and Thailand

22

Australian HRS Market Shares by Volume (tonnes) 22

Figure 7 – Australian HRS Market Shares by Volume

Figure 7 also indicates that the market share of exports from:

Japan has been relatively low for the whole of the analysis period;

Korea has increased since 2010;

Taiwan has increased since 2010 with steady growth since measures were imposed;

Thailand has fallen since 2010, with significant falls in 2014 and 2015 when measures were put in place, but started to recover in 2018; and

countries or exporters not subject to measures has not fluctuated greatly since 2010.

Further, Korea’s increase in export volumes coincided with decreases in the Australian industry’s market share until 2018 and Korea represents the largest market share of the countries subject to measures.

The Commission considers that Liberty Steel has experienced injury in the form of reduced market share in the period since 2013.

22 In Figure 7, Liberty Steel’s market share includes its sales of HRS that it had imported directly or through other parties. Its imports are not included in the market share of exports from Taiwan and Korea. In respect of those two countries, exports to Liberty Steel in the inquiry period were of material volumes, but Liberty Steel was not the largest customer of exporters from these countries. From 2011 to 2016, Liberty Steel’s imports of HRS were of non-material volumes relative to the total volume of HRS imports in the same period

PUBLIC RECORD

Continuation Inquiry 505 — HRS from Japan, Korea, Taiwan and Thailand

23

5.3.6 Other economic factors

In Appendix A7 to its application, Liberty Steel provided information in relation to other injury factors on a financial year (FY) basis (which captures the period from 1 July to 30 June) for the period from 1 July 2009 to 30 June 2018.

Capacity utilisation

Figure 8 indicates that Liberty Steel’s capacity utilisation, based on its highest HRS production level which was in FY14, has trended downwards since FY10.

The Commission considers that Liberty Steel has experienced injury in the form of reduced capacity utilisation in the period since FY 2014.

Capacity Utilisation

Figure 8 – Liberty Steel HRS Production Capacity Utilisation

Capital investment

Figure 9 indicates that Liberty Steel’s level of capital investment in the production of HRS has remained relatively constant from FY10 to FY16, apart from FY11 when the blast furnace was upgraded.

The Commission notes that various public announcements have been made in respect of planned investment in the Whyalla Steelworks. These announcements relate to investment that will take place in coming years.

The Commission’s analysis has not identified any capital investment that was made in the inquiry period and that related to these announcements. The announcements relate to a range of activities and not only to HRS production.

The Commission considers that Liberty Steel has not experienced injury in the form of reduced capital investment.

PUBLIC RECORD

Continuation Inquiry 505 — HRS from Japan, Korea, Taiwan and Thailand

24

Capital Investment (A$)

Figure 9– Liberty Steel Capital Investment in HRS Production (A$)

Return on investment

Figure 10 shows Liberty Steel’s return on investment (ROI) in the production of HRS.

Return on Investment (%)

Figure 10 – Liberty Steel Return on Investment in HRS Production

Liberty Steel’s ROI in the production of HRS declined from FY10 to FY16. From FY16 to FY18, ROI recovered to FY10 levels. ROI has been negative for the entire period since FY10, except for FY13 when a marginal positive result was achieved.

The Commission considers that Liberty Steel has experienced injury in the form of negative ROI in the period since FY 2013.

Employment

Figure 11 shows Liberty Steel’s staff levels related to the production of HRS.

PUBLIC RECORD

Continuation Inquiry 505 — HRS from Japan, Korea, Taiwan and Thailand

25

Employment

Figure 11 – Liberty Steel employee numbers in HRS Production

Liberty Steel’s staff levels have declined since FY10. Liberty Steel has indicated to the Commission that the period of voluntary administration of OneSteel led to the retrenchment of experienced staff. New staff were recruited as part of the company restructure. The Commission considers that Liberty Steel has experienced injury in the form of reduced employment in the period since FY 2011.

Wages

Figure 12 shows Liberty Steel’s average wage to employees producing HRS has increased overall since FY10, but has fallen since FY14. It also indicates that the wages of HRS employees have remained below the wages of employees who are involved in other production.

Average Wages

Figure 12– Liberty Steel Employees Average Wages (A$ per hour)

The Commission considers that Liberty Steel has experienced injury in the form of reduced wages for employees in the period since FY 2015.

PUBLIC RECORD

Continuation Inquiry 505 — HRS from Japan, Korea, Taiwan and Thailand

26

Productivity

Figure 13 shows Liberty Steel’s productivity, measured as tonnes of like goods produced per person hour, increased from FY10 to FY14, but has since declined to a level similar to that in FY10.

Productivity

Figure 13 – Liberty Steel HRS Productivity (tonnes per hour)

The Commission considers that Liberty Steel has experienced injury in the form of reduced productivity in period since FY 2014.

5.4 Conclusion

The Commission has found that in the inquiry period Liberty Steel has experienced injury in the forms of price suppression and reduced:

sales volume;

sales revenue;

profit and profitability;

market share;

capacity utilisation;

return on investment;

employment levels;

wages for employees; and

productivity.

PUBLIC RECORD

Continuation Inquiry 505 — HRS from Japan, Korea, Taiwan and Thailand

27

6 VARIABLE FACTORS

For the purposes of this continuation inquiry, the Commissioner has had regard to other matters considered relevant to the inquiry, including the variable factors established in Review 499, to assess whether dumping has occurred during the inquiry period, and whether dumping is likely to continue or recur if the anti-dumping measures were to expire.

Review 499 found that certain exports of HRS to Australia were at dumped prices in the review period, 1 January 2018 to 31 December 2018, which is the same as the inquiry period for this inquiry. The dumping margins determined in Review 499 are provided in Table 2.

Country Manufacturer/ exporter Dumping margin Duty Method

Method to establish

dumping margin

Japan All Exporters 12.2%

Combination fixed and variable duty method

Weighted average export prices were

compared with corresponding normal values

over the inquiry period in terms of s. 269TACB(2)(a)

of the Customs Act 1901.

Korea

Hyundai Steel Company 4.7%

Combination fixed and variable duty method

Uncooperative Exporters 7.9%

Combination fixed and variable duty method

Taiwan

Dragon Steel Corporation 9.0% Combination fixed and variable duty method

TS Steel Co Ltd -1.6% Floor price

Tung Ho Steel Enterprise Corporation

-1.6% Floor price

Uncooperative Exporters 12.3%

Combination fixed and variable duty method

Thailand

Siam Yamato Steel Co Ltd 5.0%

Combination fixed and variable duty method

Uncooperative Exporters 7.7%

Combination fixed and variable duty method

Table 2 — Review 499 HRS dumping margins

Details in respect of the Commission’s determination of variable factors as a result of Review 499 are at Non-Confidential Appendix 1 to this report.

Review 499 also states that the non-injurious price (NIP) should continue to be set equal to the normal value. As such, the NIP for each exporter has changed but is not operative, and therefore does not affect the effective rates of duty set out in Table 2.

PUBLIC RECORD

Continuation Inquiry 505 — HRS from Japan, Korea, Taiwan and Thailand

28

7 LIKELIHOOD THAT DUMPING WILL CONTINUE OR RECUR

7.1 Australian industry’s claims

In its application, Liberty Steel claims that dumping will continue or recur because exporters from Japan, Korea, Taiwan and Thailand have:

been affected by global overcapacity and trade distortions from several steel trade defence actions abroad;

maintained their distribution channels to Australia and have continued to export the goods under consideration to Australia; and

continued to export the goods to Australia at dumped prices.

7.1.1 Overcapacity in the global steel industry 23

In its application, Liberty Steel referred to the Commission’s 2016 Steel and Aluminium Report which found that ongoing excess capacity, particularly in Asia, is a significant challenge for the global steel industry.

The Commission notes that the Organisation for Economic Co-operation and Development (OECD) has reported that global steelmaking capacity was expected to increase in 2018 for the first time since 2015.24

The OECD has also reported that global steelmaking capacity could increase by 2.3 per cent (52 million tonnes) between 2018 and 2020.25 In the same report, the OECD states that there are 39 million tonnes of capacity additions in the planning stages for possible start-up in the same period. Much of this additional, or proposed, production capacity is expected to be developed in the Middle East and in India.

The U.S. Department of Commerce has reported in its September 2018 Global Steel Report that global steelmaking capacity utilisation has declined in most years between 2005 and 2015, but began increasing thereafter and reached 75 per cent in 2017.26

Japan

The OECD has reported that there are no capacity investments underway in Japan.27 The OECD states in the same report that closures of some steelmaking facilities may result in higher capacity utilisation at other plants.

23 Note that general discussion here, and in material referred to on production capacity in steel markets, may be in reference to the production of crude steel in general. That is, it may also include discussion on the production of steel such as flat products that are not the subject of this inquiry. However, the Commission understands that long products, a major part of which is HRS, are a significant proportion of all steel that is made and, as such, considers that any verifiable or reliable discussion of steelmaking capacity in general is relevant to this inquiry. 24 See Recent Developments in Steelmaking Capacity (Reference DSTI/SC(2018)2/FINAL), OECD. This report is available on the OECD web site. 25 Office of the Chief Economist, Department of Industry, Innovation and Science, 2017, page 19. 26 See Global Steel Report, September 2018, U.S. Department of Commerce – International Trade Administration. 27 See Recent Developments in Steelmaking Capacity (Reference DSTI/SC(2018)2/FINAL), OECD. This report is available on the OECD web site.

PUBLIC RECORD

Continuation Inquiry 505 — HRS from Japan, Korea, Taiwan and Thailand

29

The Commission is not aware of plans to increase capacity of HRS production in Japan.

Korea

The OECD has reported that there are no capacity investments underway in Korea.28

The Commission has found at the verification visit that Hyundai has the capacity to increase its production of HRS. The Commission understands that 100 per cent capacity utilisation is based on a hypothetical name plate capacity of existing plant and on assumptions such as non-stop operation without closures to conduct maintenance. However, the Commission considers it noteworthy that the reserve capacity of Hyundai is nevertheless large relative to the production capacity of Liberty Steel and relative to the entire Australian HRS market.

The Commission is not aware of plans to increase capacity of HRS production in Korea.

Taiwan

The Commission has found that Tung Ho has limited capacity to increase HRS production. The Commission is not aware of plans to increase capacity of HRS production in Taiwan.

Thailand

The Commission understands that the Iron and Steel Institute of Thailand has stated that production and consumption of long steel products in Thailand fell in 2017.29 In that year, Thai steel producers experienced low levels of steel capacity utilisation.

The Commission has found that SYS has limited capacity to increase HRS production. The Commission is not aware of plans to increase capacity of HRS production in Thailand.

China

Exporters of HRS from the People’s Republic of China (China) are not the subject of this inquiry. However, as China is the world’s largest steel exporter and producer (producing approximately half of the world’s crude steel in 2018), excess capacity in China is a major factor in the analysis of world steel markets.30 The Commission considers that excess capacity in China encourages Chinese manufacturers to seek export markets for their products.

In respect of manufacturers that are under consideration in this inquiry, the Commission considers that they will continue to face competition in several markets from Chinese manufacturers and that it is in their interests to continue to export HRS to Australia. This is consistent with the Commission’s 2017 Steel Manufacturing and Fabricating Markets report where it was stated:

The adverse impacts of continuing global steel excess capacity included the potential, identified by the OECD, that ‘excess capacity in one region can displace

28 See Recent Developments in Steelmaking Capacity (Reference DSTI/SC(2018)2/FINAL), OECD. This report is available on the OECD web site. 29 See Thailand Steel Industry 2017 and Outlook 2018, Iron and Steel Institute of Thailand. This report was presented at the South East Asia Iron and Steel Institute 2018 Conference and Exhibition. 30 For example, see Steel Market Developments – Q4 2018 (Reference DSTI/SC(2018)8/FINAL), OECD. On page 29, the OECD indicates that in 2017, world crude steel production was 1,687,277 million tonnes, of which China produced 846,947 million tonnes. This report is available on the OECD web site.

PUBLIC RECORD

Continuation Inquiry 505 — HRS from Japan, Korea, Taiwan and Thailand

30

production in other regions, thus harming producers in those markets’, including through ‘unfair trade practices such as dumping’.

The Commission understands that while there has been Government of China mandated closures of illegal induction furnaces and outdated factories, there is other activity that has limited the intended reductions in capacity. For example, production in remaining mills increased up to 5.6 per cent in the year to October 2017. Steel mills in southern China are also expected to offset the reduced production in northern mills between November 2017 and March 2018.31 This indicates that any reductions in excess capacity may be less effective due to increased capacity at more efficient mills and in alternate geographic locations.

Conclusions on overcapacity

The Commission has found that, apart from Hyundai, there is little excess capacity for exporters of HRS that were verified in this continuation inquiry. However, the Commission has found that exports of HRS to Australia have been at dumped prices from exporters from all the countries subject to this continuation inquiry. However, in respect of Hyundai, its size is large relative to the Australian industry. The Commission considers that this size differential is of such a magnitude that a small increase in Hyundai’s HRS production would be sufficient to generate volumes that, if exported to Australia at dumped prices, could potentially have a major impact on market conditions in Australia. The Commission considers that this would be so even if Liberty Steel succeeded in its efforts to increase its HRS production capacity utilisation.

Excess steelmaking capacity in China is apparent. Diversion of HRS trade to any of the countries subject to this inquiry would likely result in the need for HRS producers in those countries to expand their export trade to other countries, including Australia. The Commission notes that exports of HRS to Australia from China have been at relatively low levels since 2010.

The Commission considers that the potential excess capacity in Korea is likely to result in increased export volumes should the measures expire. (This is discussed further in section 9.3.4 of this report.) The Commission does not consider the excess capacity in other countries subject to measures to be significant.

7.1.2 Distortions in steel markets 32

In its application, Liberty Steel stated:

Overcapacity in world steel markets has triggered an unprecedented number of global trade defence mechanisms including the United States’ (US) Section 232 tariffs, the European Union’s (EU) steel safeguard and Turkey’s steel safeguard actions. These actions are affecting export markets for all countries including those the subject of this application. It is expected that displaced export volumes will increasingly focus on open markets, making Australia an attractive destination for