Report No. 47725-PA INTERNATIONAL BANK FOR ... of The World Bank FOR OFFICIAL USE ONLY Report No....

35

Document of The World Bank FOR OFFICIAL USE ONLY Report No. 47725-PA INTERNATIONAL BANK FOR RECONSTRUCTION AND DEVELOPMENT COUNTRY PARTNERSHIP STRATEGY PROGRESS REPORT FOR THE REPUBLIC OF PANAMA March 16,2009 Central America Country Management Unit Latin America and Caribbean Region InternationalBank for Reconstructionand Development This document has a restricted distribution and may be used by recipients only in the performance of their official duties. Its content may not otherwise be disclosed without World Bank authorization. Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized

Transcript of Report No. 47725-PA INTERNATIONAL BANK FOR ... of The World Bank FOR OFFICIAL USE ONLY Report No....

Document of The World Bank

FOR OFFICIAL USE ONLY

Report No. 47725-PA

INTERNATIONAL BANK FOR RECONSTRUCTION

AND DEVELOPMENT

COUNTRY PARTNERSHIP STRATEGY PROGRESS REPORT

FOR THE

REPUBLIC OF PANAMA

March 16,2009

Central America Country Management Unit Latin America and Caribbean Region International Bank for Reconstruction and Development

This document has a restricted distribution and may be used by recipients only in the performance o f their official duties. I t s content may not otherwise be disclosed without World Bank authorization.

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

AAA CCT CFAPAR CGR CFAA CPAR CPPR DPL ESW FSL FTA GNI ICA ICR LSMS MDG PER PIU

CURRENCY EQUIVALENTS Currency Unit = Balboa 1 US Dollar = 1 Balboa

FISCAL YEAR: January 1 - December 31

ACRONYMS AND ABBREVIATIONS

Analytical and Advisory Activities Conditional Cash Transfer Program Country Financial Accountability and Procurement Assessment Report Controller GeneraVContraZoria General Country Financial Accountability Assessment Country Procurement Assessment Report Country Portfolio Performance Review Development Policy Lending Economic and Sector Work Fixed-spread Loan Free Trade Agreement Gross National Income Investment Climate Assessment Implementation Completion Report Living Standards Measurement Survey Millennium Development Goals Public Expenditure Review Project Implementation Unit

FOR OFFICIAL USE ONLY

TABLE OF CONTENTS

PANAMA COUNTRY PARTNERSHIP STRATEGY - PROGRESS REPORT

A. Introduction B. Economic and Policy Developments C. Performance During the CPS Period D. Progress in Implementation and Adjustments to the CPS E. Risks

1 1 4 8 10

ANNEXES

Annex A1 Panama at a Glance ...................................................................................... 12 Annex B1 CPS Results Framework ............................................................................... 15 Annex B2 Selected Indicators of Portfolio Performance and Management ................. 22 Annex B3- 1 IBRD Program Summary ............................................ ................................ 23 Annex B3-2 IFC Program Summary ............................................................................... 23 Annex B 4 Summary o f Non-Lending Services ........................................................... 24 Annex B6 Key Economic Indicators ..... , , , .... . , .... , , , .. . , . , , .... . . ... , , , . .. , , , .. . , , , , ... , , .. . . . .. . ... . . .... ... 25 Annex B7 Key Exposure Indicators ..... . . . . ... . . . . .. . . . ... . . . . . .... . . ... . , , ... . . . ... . , , . ... . . .. . . .. . . .. . . ... . . .. .27 Annex B8-1 IBRD Operations Portfolio .......................................................................... 28 Annex B8-2 IFC Operations Portfolio ............................................................................. 29

MAP IBRD No. 33462R ....................................................................................... 30

Vice-president Pamela Cox Country Director Laura Frigenti

Task Manager Frederic de Dinechin

This document has a restricted distribution and may be used by recipients only in the performance o f their official duties. I t s contents may not be otherwise disclosed without World Bank authorization.

PANAMA COUNTRY PARTNERSHIP STRATEGY FYOS-10: PROGRESS REPORT

A. INTRODUCTION 1. This report assesses the implementation progress of the Panama-Bank FY08-10 Country Partnership Strategy (CPS) at mid-term The FY08-10 CPS, discussed at the Board in October 2007, represents a significant strengthening o f the relationship between Panama and the Bank, following a hiatus in new lending in the early years o f the new millennium. Cooperation between the Bank and Panama strengthened under the current administration (which came into office in 2005) in the context o f the joint interim strategy note (ISN) for the period 2005-2007. Successful implementation o f the ISN, in turn, paved the way for the present, full, CPS, which i s closely aligned with the strategic vision and program priorities laid out in the government’s national development plan.

2. The Panama CPS was built around four pillars aimed at addressing Panama’s development challenges: (i) reducing poverty and inequality; (io promoting economic growth; (iii) strengthening public financial management; and (iv) investing in human capital. Bank support with respect to each o f the pillars was focused on areas in which the Bank has a strong comparative advantage by virtue o f prior successful experience in Panama or relevant regional and global experience. The demand-driven partnership program included in the CPS was, from the outset, intended to be flexible and responsive to changes in client needs. The lending program included up to three Development Policy Loans including a programmatic series aimed at supporting fiscal consolidation and strengthened public financial management, as well as eight investment operations targeted mainly to poverty reduction, human development and infrastructure. Total lending was foreseen within a range o f US$390 to US$465 million for the three-year CPS period, taking into account Panama’s relatively strong economic performance, and solid and relatively small portfolio. AAA was planned in a few focused areas - poverty, urban development, environment and rural finance - to complement the extensive analytical work on economic growth and macro management and public sector finance and expenditures undertaken under the preceding ISN.

3. While the four CPSpillars outlined above were, and continue to be, relevant to Panama’s socio-economic context, some changes were made to the originally-proposed lending program to respond to the changing global economic .context and consequent changes in the government’s priorities. This Progress Report lays out these changes and assesses the performance and impact o f the CPS through mid FY09 in relation to Panama’s core development objectives (a revised Results Matrix i s provided in Annex Bl). The Progress Report also continues to advocate for a flexible and demand-driven approach in light o f the uncertainties related to the upcoming Presidential election in May 2009 and the economic uncertainty associated with the current global crisis.

B. ECONOMIC AND POLICY DEVELOPMENTS 4. Macroeconomic performance over the CPS period has been strong, particularly on the fiscal front as revenues surged and spending was kept under control. The nonfinancial public sector balance, excluding the Panama Canal Authority (PCA), turned from a deficit o f about 5 percent o f GDP in 2004 into surpluses o f 3.5 percent o f GDP in

1

2007 and 0.4 percent o f GDP in 2008. This outcome i s the result o f a number o f factors including: (i) government efforts on the tax front as evidenced by the tax reform package adopted by the Torrijos Administration in 2005; (ii) higher fiscal transfers from the PCA; (iii) more effective tax collection efforts; and (iv) some one-time events. The mirror image of the strong fiscal performance has been a marked reduction in public debt from a peak o f 62.2 percent of GDP in 2004 to 38 percent o f GDP in 2008. In 2008, the improved fiscal position contributed to a Standard & Poor’s upgrade o f Panama’s long- term foreign and local currency issuer default ratings from BB to BB+, while Fitch affirmed Panama’s rating at BB+ and revised the rating outlook to Positive.

5 . Inflation, which had accelerated rapidly in 2007 and 2008, is now on a downward path. Year-on-year CPI inflation peaked at 10.0 percent in September 2008 driven by food and commodity prices, and strong domestic and foreign demand. Food prices (accounting for a third o f the consumer basket) rose by 15.4 percent in the same month compared to 2.4 percent in January 2007. However, in line with global trends inflation rates have been declining over the second half o f 2008, falling to 4.3 percent in February 2009 on a year to year basis.

6. On the external front, Panama’s current account balance is estimated to have reached a deficit of 12.1 percent of GDP in 2008 up from 4.9percent in 2005. This was the result o f two main factors: the high oi l prices during 2008 and imports (particularly o f capital goods) associated with the canal expansion. The current account deficit has been financed by foreign direct investment-mainly in the financial, commerce and housing sectors-averaging more than 9 percent o f GDP annually since 2004.

7. Sound macroeconomic management together with a positive external environment resulted in remarkably strong growth. Growth rates accelerated rapidly in 2007 and 2008 to 11.5 percent and 9.2 percent respectively driven by strong external and domestic demand, with transportation, communications, and construction leading GDP growth over this period.

8. However, Panama’s economy is being affected by the global crisis in the form o f a contraction in credit growth, reduced trade financing and a halt in new construction lending. Moreover, the global economic recession, particularly in the United States, i s leading to reduced demand for Panamanian trade-based economic services, real estate, goods and tourism. The planned investment arising from the Panama Canal expansion project currently underway i s expected to provide a substantial fiscal stimulus that will partially offset the negative impact, but overall economic uncertainty has increased substantially.

9. Credit growth is contracting with important effects on medium-term growth. The direct effects o f the global financial crisis have been modest to date owing to a limited direct asset exposure by the banking sector. According to the Banking Superintendency, less than 0.1 percent o f total banking sector assets in Panama were linked to US subprime mortgages and troubled financial institutions. As a result Panamanian banks have so far experienced limited capital losses. Yet, credit growth slowed substantially in the last quarter o f 2008 and local businesses began to report difficulties in accessing credit and the cancellation o f previously agreed credit l ines as

2

banks are currently hoarding liquidity and exhibit strong caution in extending credit. A contraction o f consumer credit i s also expected to slow domestic demand.

10. The real estate sector is expected to experience a slowdown during 2009 owing to financing constraints and reduced foreign demand. The Panamanian housing market has experienced a construction and price boom in recent years fueled by growth in the economy, access to credit, tax incentives, and strong foreign demand. Construction activity was growing by at very high rates prior to the onset o f the US financial crisis. Owing to uncertainty in the strength o f future demand, most large banks have decided not to finance new high-end projects, although they continue to finance ongoing projects. The growth rate in the value o f construction and maintenance fel l from 33.9 percent in 2007 to 18.7 percent in 2008, according to the General Controller’s office, including a 14 percent decline for the fourth quarter. This trend i s expected to continue throughout 2009. Nonetheless, the real estate sector i s unlikely to pose a systemic risk for the financial sector in Panama (about 9 percent o f bank assets are in housing loans and another 3 percent are in construction loans).

1 1. The liquidity position of the banking system remains comfortable. The liquidity position o f the International Banking Sector (CBI) and the National Banking System (SBN) banks has remained fairly stable over time, and has even increased in the fourth quarter o f 2008. Private Panamanian banks (which hold 45.8 percent o f the national banking system assets), however, are less liquid than foreign and public banks. The liquidity ratio (liquid assets plus investments over total deposits) o f this group fe l l from 50.5 percent in 2006 to 40.6 percent in 2008 (4th quarter figures) - including a slight increase relative to the third quarter o f 2008. Foreign banks and the two public banks (Banco Nacional de Panama and Caja de Ahorros) are the most liquid banking groups, with 55.8 and 61.9 percent respectively, and they also registered noticeable improvements in the final quarter o f 2008.

12. The government has already taken a number of actions to mitigate risks in the financial sector. In October 2008 the President formed a crisis committee which includes the Minister o f Finance, the Superintendent o f Banks, and the President o f the Bank o f Panama (BNP); in November 2008, BNP created a collateralized line o f credit o f US$400 million for the banking sector; and in January 2009, the government announced a stimulus package for US$l .l billion. This total reflects the US$400 million line o f credit from the BNP and new funds from the Inter-American Development Bank and the Corporacion Andina de Fomento.

13. Against this background the growth outlook for 2009 and 2010 has been revised downwards. GDP growth projections for 2009 and 2010, which until recently were in the 7-8 percent range, have been reduced to 3 percent in 2009 and 4 percent in 2010 before

1

There are currently about 200 high-rise buildings with approximately 19,000 new apartments under construction in Panama with a total project value o f about US$4,300 mi l l ion-only 62 percent o f which i s being financed. Ha l f o f the apartments under construction have already been pre-sold to Panamanian and foreign buyers. * Note that these are end-of-quarter liquidity figures. The legal requirement for al l banks i s based on weekly data and includes liabilities and assets up to 186 days. For the banking system as a whole, the weekly liquidity ratio has remained above 60 percent since the week of November 21, 2008, and was about 61 percent as o f the week of March 17,2009. The weekly legal required liquidity ratio i s 30 percent.

1

3

returning to 7 percent in 201 1. These growth rates, which are driven in part by the canal expansion works, are s t i l l relatively high by regional standards and subject to significant uncertainty. As o f March 2009, market analysts had 2009 growth projections ranging from -1.3 percent to 5.2 percent.

14. Despite global economic conditions, Panama is expected to continue having a sound medium term macroeconomic framework. On the fiscal front, despite expected lower revenues, the overall fiscal deficit i s projected to remain below 1 percent o f GDP over the medium term as expenditures are expected to be kept in check in adherence to the recently approved Social and Fiscal Responsibility Law (SFRL).3

15. Inflation is expected to further moderate in 2009 as the high prices that food and commodities, particularly oil, reached in 2008 are reverted in the coming years. Current projections for the 2009 consumer price index inflation rate are about 4 percent which i s close to i t s historical low average. On the external front, the current account deficit i s projected to peak at about 14 percent o f GDP in 2010. This relatively high deficit i s primarily driven by capital and other imports related to the canal expansion, which are to a large extent already pre-financed. The current account deficit i s expected to contract again once the project nears i t s end in 2014.

C. PERFORMANCE DURING THE CPS PERIOD

16. Since the CPS was approved, Panama has made significant progress towards the development goals laid out by government. In fact CPS outcomes have, in many instances, already been achieved or exceeded targets. A detailed description o f progress towards CPS milestones in each o f the four pillars i s presented in the revised CPS Results Framework in Annex B 1.

17. The program of lending and AAA activities included in the CPS has been an important contributor to Panama’s performance. For example, through solid analytic work (Country Economic Memorandum/Investment Climate Assessment, Report on Observance of Standards and Codes (Accounting and Auditing) and up coming Policy Notes), lending (Competitiveness and Public Finance Management DPLs), and IFC’s role in the Canal Expansion Project, the Bank has been a key partner in supporting the government’s growth and public finance objectives. Similarly, the Social Protection (FY08), Health (FY09) and Education (FY09) operations have been critical in helping to design and establish systems to effectively target and monitor the government’s flagship CCT program, Red the Oportunidades. In addition, ongoing support has been provided in a range o f other areas such as water, urban transport, sustainable tourism, land administration and human development, each o f which i s linked to the CPS objectives.

Pillar I. Reducing; Poverty and Inequality

18. Poverty -both overall and extreme- has declined in recent years. While final assessment o f changes in poverty will need to await full analysis o f the recent living standards measurement survey (LSMS), preliminary figures suggest that overall poverty

~ ~~

The Social and Fiscal Responsibility Law established a ceiling for the fiscal deficit o f the non financial public sector of 1 percent of GDP, unless growth falls to 1 percent of less, in which case the deficit i s allowed to expand to 3 percent o f GDP and 2 percent the subsequent year. Current growth projections (paragraph 5 ) do not indicate a need to break the 1 percent o f GDP ceiling.

3

4

has fallen by about 4.5 percent from 36.8 percent in 2003 to 32.4 percent in 2008. There i s also a small but significant decline in extreme poverty, which according to the same preliminary figures fell from 16.6 percent to 14.2 percent over the same period. Despite this progress, the poverty declines appear smaller than might have been expected given the country’s stellar economic growth rates for the same period. Moreover, extreme poverty remains endemic in indigenous areas.

19. To address Panama’s poverty challenges the current Administration introduced a Flagship Poverty Program, Red de Oportunidades. The 2007 Poverty Assessment noted that the relatively high levels of poverty in Panama are not due to lack o f social spending but rather to inadequate targeting, efficiency, and effectiveness o f the different programs. Thus Red de Oportunidades i s an important step in this respect. Launched in 2006 i t provides conditional cash transfers to the poorest households in exchange for better utilization o f health, nutrition and education services by children in the household. Today, more than 70,000 families benefit from the monetary transfer, and an efficient targeting mechanism i s in place. Red de Oportunidades was also a key instrument to mitigate the impact o f the 2008 food crisis on the poorest households o f the country; the monthly transfer was increased from US$35 to US$50 to offset the higher prices o f food.

20. Bank support for poverty reduction has focused on improving the targeting and effectiveness of Red de Oportunidades and increasing rural productivity. The Bank, together with the IDB, has helped the government to develop Red de Oportunidades and i s helping i t s implementation particularly in the areas o f program management, and monitoring and evaluation. The Bank i s also supporting efforts to increase economic opportunities in rural areas. The Land Administration Project and the Rural Productivity Project and GEF Grant have already achieved significant results, issuing more than 10,000 land tit les and promoting more than 100 productive sub-projects.

21. The Bank will continue its support for this pillar during the rest of the CPS period through additional analytical work and new lending operations. A planned Poverty Assessment for F Y 10, based on three LSMS (1 997, 2003 and 2008), wi l l be key to monitor the impact o f existing social programs. The Poverty Assessment i s expected to provide valuable information to further refine the five year National Development Strategy to be prepared by the new administration after it takes over in July 2009. On the lending side, the planned FY 10 Second Land Project and Rural Microfinance Project are designed to support sustainability o f outcomes in the ongoing land and rural productivity programs. Finally, the proposed Protecting the Poor under Global Uncertainty DPL - being considered in parallel to this CPS Progress Report- supports country efforts to mitigate the impact o f economic shocks on the poor through improved targeting and coverage o f social sector programs.

Pillar 11. Promoting Economic Growth

22. Panama has experienced high growth rates over the CPSperiod as a result of both a positive external environment, and prudent macroeconomic policies (see Section B.) as well as government efforts to improve the country’s competitiveness. Indeed during the CPS period: (i) the investment climate improved through more streamlined regulation processes (according to the Doing Business Report the time needed to start a new business had been reduced from 19 days to about 13 between 2007 and 2008, and

5

the time for exporting from 16 days to 10 over the same period); (ii) business transaction costs were reduced through the simplification o f government procedures (for example the internet portal PanamaTramita offers 90 online business related transactions from 75 in June 2007, and legal and regulatory reforms to govern the use o f electronic signatories were approved); and (iii) progress was made on the innovation front by strengthening the National Secretariat for Science, Technology and Innovation and the National Training Institute.

23. The Bank has supported government through a combination of analytical work and lending operations. On the analytical front, a Country Economic Memorandum was prepared in conjunction with an Investment Climate Assessment to assess the challenges and opportunities for achieving sustained high growth. These helped inform government policies such as the ambitious modernization program promoted by the Governmental Innovation Presidential Secretariat. O n the lending front, the Competitiveness and PFM DPL series, and the Public Policy Reform Technical Assistance Loan have contributed to the enhancement o f private sector competitiveness and the consolidation o f fiscal sustainability, and transparency and efficiency o f the state. At the Government’s request the second D P L in the series was topped up from US$75 mi l l ion to US$lOO mi l l ion in response to the worsening global financial environment.

24. The Bank will continue its support during the remainder of the CPS period through investment lending, budget support, and additional analytical work. For example, the planned FY 10 Sustainable Tourism and Urban Transport investment operations will aim at removing bottlenecks in two key economic sectors o f the Panamanian economy. Similarly the proposed Protecting the Poor under Global Uncertainty DPL will support government’s efforts to enhance growth prospects by reducing the risks o f a potential banking crisis through enhanced risk management and strengthened regulation and supervision. On the analytical front, a set o f Policy Notes will be used to contribute to the national dialogue on options to face the global crisis while continuing to pursue medium-term development challenges.

THE IFC PROGRAM

25. IFC’s activities over the CPS period have been fully aligned with the IBRD program with a special focus on the growth pillar of the government’s program. As anticipated, IFC has continued to focus its operations in the financial and infrastructure sectors with an emphasis on projects that would increase service to currently underserved areas. IFC is also actively looking for opportunities in the renewable energy sector, particularly in mini-hydros where it i s evaluating several opportunities and where IFC would bring value added in terms o f improved environmental and social practices. Selected operations for FY09 in Panama include: (i) a US$300 mi l l ion loan from the joint Bank-IFC Subnational Finance Department to the Panama Canal Authority to support the expansion o f the canal and thereby help strengthen global trade and expand government resources available for economic and social development4; (ii) a US$50 mi l l ion loan to

Bank-1~~ participation in the canal expansion was decided after the CPS was approved. The 4

project wil l contribute to the second pillar o f the government strategy, Le., promoting economic growth. The loan was approved in November 2008.

6

Digicel for the construction o f a greenfield mobile cellular telephone network to increase coverage to over 90 percent in Panama and expand accessibility to the lower income families, and (iii) a US$15.6 mi l l ion equity investment in Panama-based financial conglomerate Grupo Mundial to help expand i t s insurance and banking services to underserved markets in Central America and Colombia. Finally, IFC has maintained and will continue i t s overall interest in supporting institutions that have a regional focus rather than a country level focus, so that the small economies in Central America would benefit from economies o f scale in various aspects, including physical and financial infrastructure.

Pillar 111. Strenethenine Public Financial Management

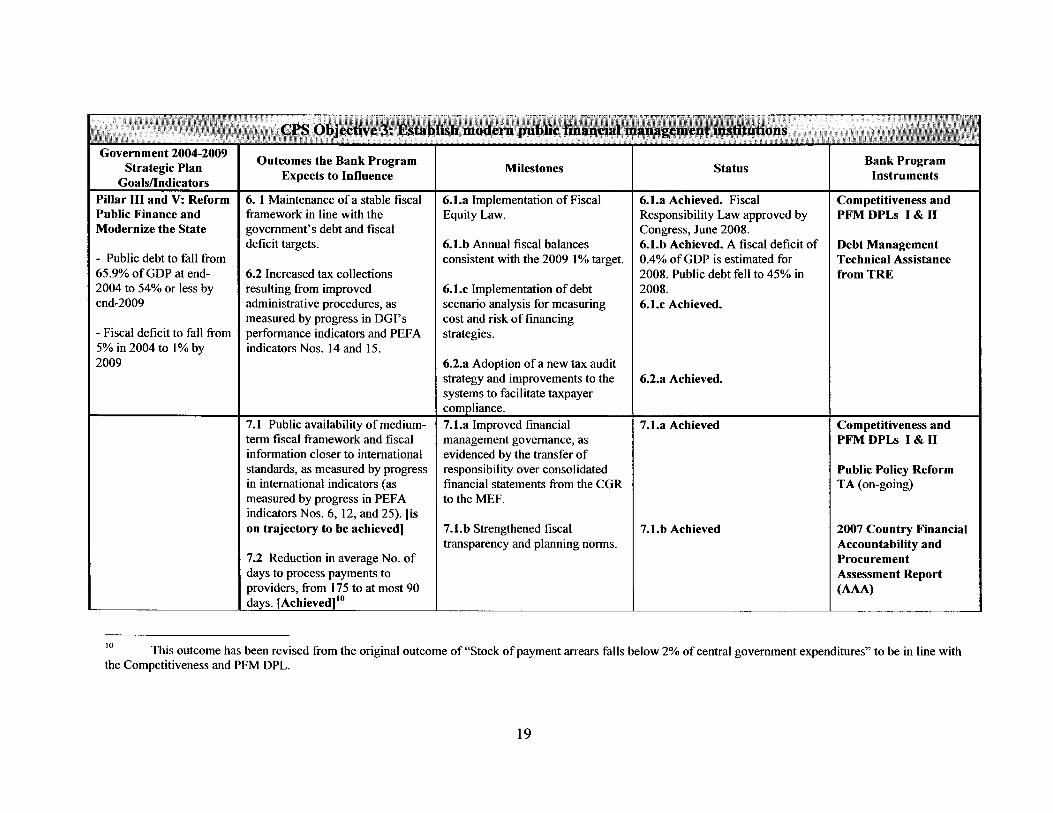

26. Over the CPS period Panama has made remarkable progress both in terms of fiscal performance and improved transparency and efficiency in public spending. Panama’s Social and Fiscal Responsibility Law was approved in mid 2008 and became effective on January 1, 2009. In addition to setting limits to the N o n Financial Public Sector fiscal balance, the law contains important provisions to help increase fiscal stability and transparency through the introduction o f clearer definitions to the components o f the fiscal accounts, periodic reports on compliance with the Law including a specific report on accounts payable, and increasing public access to the medium-term fiscal framework. Progress has also been made on the procurement front with the preparation o f a National Procurement Strategy including the full roll-out o f the e-procurement platform (PanamaCompra), and the introduction o f Framework Contracts.

27. The Bank program has contributed to these improvements through lending (Development Policy Loans series, Public Policy Reform Technical Assistance) and non lending (Debt Management, Country Financial Accountability Assessment and Country Procurement Assessment Report) activities. The Bank supported the elaboration o f the Social and Fiscal Responsibility L a w and associated Regulations in the Public Financial Management (PFM) D P L series, and contributed to improvements in the capacity o f the Ministry o f Economy and Finances to manage public debt. With respect to PFM, the Bank has been supporting the use o f the National Integrated Financial Management System (SIAFPA) for budget planning and execution. Bank financed projects are currently using PanamaCompra to publish bidding notices and results, and Panama’s “Framework Contracts” to replace shopping up to US$50,000. In view o f the significant advances in national procurement procedures and their implementation, Panama has been selected as one o f a l imited number o f pi lot countries for the use o f country procurement systems in Bank-financed projects.

28. For the remainder of the CPSperiod, Bank support will be channeled through the Public Policy Reform Technical Assistance Loan and the Non Lending Fiduciary Technical Assistance. These tasks will support the modernization o f PanamaCompra, the implementation o f a National Procurement Strategy and the strengthening o f the General Comptroller Office (CGR) control and audit models. In turn, this will help building capacity within CGR, the Ministry o f Economy and Finances and line ministries, and increasing the use o f country procedures over stand alone Project Implementation Units and financial agents.

7

Pillar IV. Investing in Human Capital

29. The CPS period has witnessed significant efforts by the government to strengthen the quality and coverage of social services to the extreme poor. For example, the government has included a comprehensive nutrition component in i t s package o f basic health services delivered to poor and isolated communities, as a part o f a new national plan to combat chi ld malnutrition. Similarly, the government has also expanded the geographical coverage o f the health service package delivered in isolated and poor areas through a more comprehensive inclusion o f previously underserved areas. As a result, in 2008 more than 50,000 families benefitted from the health package in rural areas. As for the education sector, the government’s strategy has focused on increasing the coverage and quality o f education at the preschool, primary and secondary education. In this regard, the CPS period witnessed the establishment o f additional preschools and home based programs as well as the establishment o f distance learning facilities.

30. I n parallel to its support for Red de Oportunidades, the Bank’s program has placed significant emphasis on helping the government to improve social service coverage in poor areas, through a number o f lending operations. For example the Health Equity Improvement Project is contributing to increase access o f targeted underserved rural communities to quality basic health services. Similarly, the recently approved Education Quality Improvement Project i s supporting both quality oriented interventions such as improvements in pedagogical methods, curricular relevancy and promotion o f IT literacy skills, and coverage oriented interventions such as increases in the number o f Telebasica (Le., distance education centers) in rural and indigenous communities, and the expansion o f Community and Family Centers. During the remaining CPS period, the Bank will continue to support government’s efforts to increase the quality and impact of social programs, particularly in extremely poor rural and indigenous areas with the FY 10 Poverty Assessment.

D. PROGRESS IN IMPLEMENTATION AND ADJUSTMENTS TO THE CPS

3 1. Porlfolio implementation is satisfactory, but disbursements have been slower than expected in some cases. All projects in the portfolio are rated MS or higher, but during the first eight months o f FY09 only US$lO.8 mi l l ion has been disbursed (Table 1). This slow pace o f disbursements can be attributed to two main factors: (i) the relative “youth” o f the portfolio, which affects disbursements as most operations tend to experience slower disbursement in their first 1-2 years o f implementation and many projects just became effective; and (ii) the decision to strengthen public institutional capacity for project implementation rather than use dedicated Project Implementation Units (PIUs), which requires time for Ministry staff to familiarize themselves with Bank procedures and requirements. These factors were foreseen in the CPS, and indeed the government and the Bank have been working to address them through special training in procurement and financial management requirements for ministry staff involved with project implementation. Since, as noted above, Panama has been selected as a pi lot country for the use o f country procurement systems, project implementation i s expected to speed up in the future and improve long term development impact. Portfolio implementation will continue to be a focus for discussion with both the current and new administration to avoid delays during the political transition.

8

Table 1. Panama Portfolio Performance (as of March 2.2009)

32. I n line with the flexible, demand-driven nature of the CPS, some adjustments were made to the lending program to better support Panama's response to global economic shocks. In particular, the lending program was adjusted to increase the amount o f the DPL operations in the program in order to allow the government increased financial liquidity to address actual and potential spending needs. In th i s context, DPL I1 was increased b y US$25 mill ion to US$lOO mill ion and i t was agreed that a third US$80 mill ion Development Policy Loan - which had originally been seen as optional - would be processed in FY09. This Protecting the Poor under Global Uncertainty Development Policy Loan, which i s being presented at the same time as the Progress Report, i s designed to support the efforts of the government to protect vulnerable groups in the context of the global economic crisis by mitigating the impact o f economic shocks on the poor and by reducing the risks of a potential banking crisis. The preparation o f investment operations originally foreseen for FY09 (Sustainable Tourism, Rural Microfinance, Second Land Access), has been delayed and these operations are programmed in F Y l O following presidential elections and consultations with the new government. Two follow-up operations planned for F Y l O (Social Protection 11, and Public Policy Reform TA 11) are expected to slip from this CPS period (Table 2).

Table 2. CPS versus CPS Pros CPS FYO8 Competitiveness and PFM DPL 1 (US$75 million) Education I1 (US$30 million) Health (US$30 million)

FY09 Competitiveness and PFM DPL 2 (US$75 million) Land Access (US$45 million) Rural Microfinance (US$25 million) Sustainable Tourism (US$30 million)

F Y 10 Optional DPL (US$75 million) Urban Transport (US$50 million) Social Protection I1 (US$20 million) Public Policy Reform TA 2 (US$lO million) 'ote: Projects in bold have been delivered.

ess Report Lending Program CPSPR

FY08 US$75 million FY09 US$35 million FY09 US$40 million

FY09 US$lOO million Slip to F Y l O (US$45 million) Slip to F Y l O (US$25 million) Slip to F Y l O (US$30 million)

FY09 Protecting the Poor DPL (US$80 million) Slip to F Y l O (US$50 million) Expected to slip from CPS period Expected to slip from CPS period

9

33. The objectives laid out in the CPS remain fully relevant to Panama’s development challenges but there is a need for continuedjlexibility in the partnership program to accommodate uncertainty going forward. The combined uncertainty o f the external environment and the upcoming elections in May 2009 make i t difficult to predict the exact nature o f adjustments for the remainder o f the CPS period (see also risk section below). Indeed, the new administration may decide to move forward with the projects as designed or with modifications that may be accommodated within the current CPS. In the event o f a broad shift in government priorities, the preparation o f a new CPS could be advanced to respond better to government’s needs.

E. R I S K S 34. The CPS identified risks in three areas: economic, political and portfolio performance. These areas remain valid, but the nature of the economic risk has changed.

35. The main economic risk at present derives from the ongoing global crisis and more specifically from the possibility of a deeper and/or more prolonged global deceleration than has been anticipated thus far. Although Panama is relatively wel l positioned to weather the current global crisis and i s not expected to fal l into recession during the remaining CPS period, growth i s expected to be adversely affected as credit tightens, the real estate sector slows down, and Canal traffic and exports decline. Should the global slowdown be more protracted than anticipated the government may find the need to adjust i t s current priorities including the operations planned for the remainder o f the CPS period. The Bank and the IMF are maintaining a close dialogue with authorities on macroeconomic policy issues to support the government’s efforts to mitigate these risks.

36. The main political risk relates to the upcomin elections in May 2009 and subsequent change in administration on July 1, 2009. Government transitions can slow the implementation o f the country’s development program including those components supported by current Bank operations and those under preparation. There may also be some shifts in policy or programmatic emphasis. The Bank i s providing support through the preparation o f a set o f pol icy notes to provide presidential candidates with an additional source o f information about development challenges and on-going policies and programs (the Policy Notes are currently being finalized). I t i s expected that the CPS will be flexible enough to accommodate some adjustments in response to shifts in government priorities fol lowing the elections; however if necessary the preparation o f the next CPS could be accelerated.

37. Portfolio performance also remains a risk in that the relatively young portfolio and the government’s need to build experience in project execution could contribute towards a slowing down in the rate of project implementation. Furthermore the pace o f implementation also typically slows down at times o f political transition. Mit igation efforts identified at the time o f the CPS are being implemented. For example, the Bank i s working with the government on intensive capacity building efforts and regular Country Portfolio Performance Reviews. These efforts will continue during the remainder o f the

f

Under Panama’s Constitution, the president may not be elected to a consecutive term. 5

10

CPS period, including with the new administration to build on progress achieved to date. The risks o f a short-term slow down in implementation remain acceptable in light o f the substantial up-side potential o f building more efficient public management institutions and capacity in l ine ministries responsible for delivering improved social assistance and services to the poor.

11

CPS Annex A1 - PANAMA AT A GLANCE, 1/29/09

Key Development Indicators

(2007)

Population, mi&year (millions) Surface area (housand sq. km) Population gowth (YO) Urnan population (% of toki population)

GNI (Adas method, US$ billions) GNI percapita (Atlas method, US$) GNI percapita (PPP, internatonal$)

GDP growth (%) GDP per capita growth (%)

(most recent estimate, 2000-2007)

Povertvheadcwnt ratioat$1.25adav(PPP.%) Poverty headcount ratio at $2.00 a day (PPP, %) Life eqmtancyat birh (years) Infant mortality (per 1 ,000 live birhs) Child malnubilion (% of children under 5)

Adult literacy, male (% of ages 15 and older) Adult literacy, female (YO of ages 15 and older) Oms pcimary enrollment, male (% ofage grwp) Gross primary enrollment, female ( O h of age group)

Access to an improved vater source (% of population) Access to improved sanitation facilities (% of population)

Panama

3.3 76 1.7 71

18.4 5,500

10,830

11.5 9.7

75 19

93 91

114 11 1

90 73

Latin America 8 Carib.

563 20,421

1.2 78

3,118 5,540 9,320

5.7 4.5

6 16 73 22

5

91 89

120 116

91 78

Upper middle

income

6 23 41,497

0.6 75

5,750 6,9 87

11,668

5.8 5.1

70 22

94 92

112 109

95 83

Net Aid Flows

(US$ millions) Net ODA and official aid Top 3 donors (in 2006):

United States European Commission Spain

Aid (%of GNI) Aid per capita (US$)

Long-Term Economic Trends

Consumer piiaes(annua1 %change) GDP implicit deflator (annud % change)

Exchange rate (annual average, local per US$) T e n s of trade index (2000 = 100)

Population, mi& year (millions) GDP (US$ millions)

AgriCUltJ re Industry

Services

Hwsehold final consumpton ependture General gov'tfinal consumplion eqmnditure Gross capital foimaton

Exports of goods and services Imports of goods and services Ooss savings

Manufacturing

1980

45

15 0

1.3 23

13.8 33.7

1 .o 90

1 .9 3,810

8.9 19.5 11.0 71.5

44.9 17.6 26.1

98.2 88.8 27.6

1990 2000

99 16

97 -9 0 . 3 6 13

2.0 0.1 41 5

-5.1 1.5 0.6 -1.2

1.0 1.0 94 100

2.4 2.9 5,313 11,621

(% of GDP) 9.8 7.2

15.1 19.1 9,7 10.1

75.1 73.6

56.9 59.9 18.1 13.2 16.8 24.1

86.6 72.6 78.6 69.6 24.2 23.1

2007 a

30

19 13 6

0.2 9

4.2 3.3

1.0 105

3.3 19,740

6.7 16.5 7.1

76.6

60.1 11.5 23.3

80.0 75.0 17.8

Age dirttibution, 2007

Male Female

75.79

S O 6 4

05dB

30-34

15-19

0.1

15 10 5 0 5 10 15

percent

Jnder-5 mortality rate (per 1,000)

1990 1985 2000 2006

OPanama OLal in America (L the Caribbean

2rowth dGDPandGDPpercaplta ( O h )

C '-w 0 2

BO 95 00 05

-GDP - GDP percapita

198&90 1990-2WO 200047 (average annual p w t h %)

2.1 2 .o 1.8 0.5 4.7 6.0

2.5 3.1 4.1 -1 .3 6 .O 4.0 0.4 2.7 0.6 0.7 4.5 6.3

3.8 6.4 6. 7 1 .2 1 .7 4.0

-9.2 10.4 5.9

0.4 -0.4 5.8 1 .o 1.2 6.2

Note: Figures in italics are foryears other than those specified. 2007 data are preliminary. .. indicates data are not available. a. Aiddataarefor2006. Development Economics, Development Data Group (DECDG).

12

Panama

Balance of Payments and Trade

(US$ millions) Total merchandise exports (fob) Total merchandise imports (df) Net trade in goods and services

Workers' remittances and compensation of employees (receipts)

Current account balance as a % of GDP

Reserves, including gold

Central Government Finance

(X of GDP) Current revenue (including grants)

Current expenditure

Overall surplus/deficit

Highest marginal tax rate (%)

Tax revenue

Individual Corporate

External Debt and Resource Flows

(US$ millions) Total debt outstanding and disbursed Total debt service Debt relief (HIPC, MDRI)

Total debt (36 of GDP) Total debt service (% of exports)

Foreign direct investment (net inflows) Portfolio equity (net inflows)

2000

5,838 7,655 -279

16

-715 -6.2

707

18.2 9.8

16.9

-1.1

30 30

7,038 917

-

60.6 9.7

624 0

2007

9,241 13,293

-212

173

-1,079 -5.5

1,628

17.5 10.2 15.4

0.5

27 30

9,989 3,459 -

58.4 24 6

2,574 0

Composition of total external debt, 2006

Other muiu. Shon-term 505

Privata 8 I t 7 US$ millions

Private Sector Development

Time required to start a business (days) Cost to start a business (% of GNI per capita) Time required to register property (days)

Ranked as a major constraint to business (% of managers surveyed who agreed)

Electricity Tax rates

Stock market capitalization (% of GDP) Bank capital to asset ratio (56)

2000

2000

24.0 9.6

2008

13 19 6

44

2007

30 6 14 6

31.5 11 3

jovernance Indicators, 2000 and 2007

Voice and accountability

Political stability

Regulatory quality

Rule of law I I

Control of corruption

0 25 50 75 100

0 2007 02000 higher WIY~S tm@y betlerrdmpls

Country's penentile rank (0-100)

ource Kaufmann-Kraay-Mastwui, World Bank

Technology and Infrastructure 2000

Paved roads (% of total) Fixed line and mobile phone

High technology exports subscribers (per 1,000 people)

(56 of manufactured exports)

34.6

28

0.1

Environment

Agricultural land (% of land area)

Nationally protected areas (96 of land area)

Freshwater resources per capita (w. meters) Freshwater withdrawal (% of internal resources)

C02 emissions per capita (mt)

GDP per unit of energy use

29 57.9 Forest area (% of land area)

0.6

1.9

(2005 PPP S per kg of oil equivalent)

Energy use per capita (kg of oil equivalent)

7.3

875

0

(US$ milons)

IBRD Total debt outstanding and disbursed 283 Disbursements 22 Pnnwpal repayments 24 Interest payments 21

IDA Total debt outstanding and disbursed Disbursements Total debt service

0 0 0

iFC (fiscal year) Total disbursed and outstanding portfolio 226

117 84

2

of which IFC own account Disbursements for IFC own account

repayments for IFC own account Portfolio sales, prepayments and

MlGA Gross emosure 0 New guarantees 0

2007

86

0 3

30 57 7 17 6

45,613

1 8

9 0

804

2W7

216 74 43 13

0 0 0

175 157

0

54

0 0

Note: Figures in italics are for years other than those specified. 2007 data are preliminary .. indicates data are not available. - indicates observation is not applicable.

9/24/08

Development Economics, Development Data Group (DECDG).

13

Millennium Development Goals Panama

W/th selected targets to achieve between 1990 and 2015 (esbrnale dosesf fo date shown. +/- 2 yean)

Goal 1: halve the rates for extreme poverty and malnutrition 1990 1995 2000 2007 Poverty headcount ratio at 81.25 a day (PPP, % of population)

Share of income or consumption lo the poorest qunitiie (36) 2.1 2.3 2.4 2.5 Prevalence of malnutrition (% of children under 5)

Poverty headcount ratio at national poverty line (% of population) 37.3

6.3

Goal 2: ensure that children are able to complete primary schooling Primarv school enrollment (net. %) 92 98 98 Primah completion rate (%of relevant age group) Secondaly school enrollment (gross, %) Youth literacy rate (% of people ages 15-24)

66 94 94 62 67 70 95 96

Goal 3: ellmlnate gender dlsparlty In education and empower women Ratio of girls to boys in primary and secondary education (%) 100 101 Women employed in the nonagricultural sector (% of nonagricultural employment) 43 43 43 43 Proportion of seats heid by women in national parliament (%) 8 10 10 17

Goal 4: reduce under-5 mortality bylwo-thirds Under-5 mortality rate (per 1,000) 34 30 26 23 Infant mortality rate (per 1,000 live births) 27 23 20 18 Measles immunization (proportion of one-year olds immunized, %) 73 84 97 94

Goal 5: reduce maternal mottallty by three-fourths Maternal mortality ratio (modeled estimate, per 100,000 live births) 130 Births anended by skilled health staff (% of total) 86 90 91 Contraceptive prevalence (% of women ages 15-49)

Goal 6: halt and be@ to reverse the spread of HlVlAlDS and other major diseases Prevalence of HIV (% of population ages 15-49) 1.0 1 .o Incidence of tuberculosis (per 100,000 people) 69 60 53 45 Tuberculosis cases detected under DOTS (%) 35 134

Goal 7: halve the proportion of people without sustainable access to bask needs Access to an improved water source (% of population) 92 92 92 Access to improved sanitation facilities (% of population) Forest area (Oh of total land area) Nationally protected areas (% of total land area) C02 emissions (metric tons per capita) GDP per unit of energy use (constant 2005 PPP $ per kg of oil equivalent)

63 69 74 56.8 57.9 57.7

17.6 1.3 1.3 1.9 1.6 7.6 7.6 7.3 9.0

Telephone mainlines (per 100 people) Mobile phone subscribers (per 100 people) Internet users (per 100 people) Personal computers (per 100 people)

9.0 11.4 14.5 14.7 0.0 0.0 13.9 71.6 0.0 0.1 6.6 15.7

3.6 4 6

iducation indicators (K)

25 W E 2wO 2002 2004 20ffi

-0- Primary net enrollment ratio

+Ratio of girls to boys in pnmary 8 secondary education

Weasles immunization (X of I-year olds)

1990 1995 20W 2008

0 Panama 0 Latin Amnca 8 the Caribbean

CT indicators (per 1,000 people)

2 w 0 2W2 2W4 2wB

OFlxed + m b l l e subscnbrr Blnternei users

Note: Figures in italics are for years other than those specified. .. indicates data are not available.

Development Economics, Development Data Group (DECDG).

9/24/08

14

h

c

c

‘z?

cl- 0

s .E

? J?

F 2

m

.s '0

8 8

B .- & Y c

3

0

C'J

M

z e C

o

a

# m c? I

L

a,

Jz 2

CAS Annex B2 - Panama Selected Indicators* of Bank Portfolio Performance and Management

As of 02/12/2009

Indicator 2006 2007 2008 2009 Portfolio Assessment Number of Projects Under Implementationa 3 4 7 10 Average Implementation Period (years) 5.4 5.1 3.9 3.3 Percent of Problem Projects by Number 33.3 0.0 0.0 0.0 Percent of Problem Projects by Amount a* 47.7 0.0 0.0 0.0 Percent of Projects at Risk by Number 33.3 0.0 0.0 0.0 Percent of Projects at Risk by Amount 47.7 0.0 0.0 0.0 Disbursement Ratio (%) e 14.8 31.2 24.6 8.4 Portfolio Management CPPR during the year (yes/no) Yes Yes Yes Yes Supervision Resources (total US$) 322.4 300.4 768.6 909 Average Supervision (US$/project) 80.6 100.2 85.4 91

Memorandum Item Since FY 80 Last Five FYs

Proj Eva1 by OED by Amt (US$ millions) 864.8 64.0 % of OED Projects Rated U or HU by Number 38.2 33.3 % of OED Projects Rated U or HU by Amt 23.2 6.2

Proj Eva1 by OED by Number 36 3

a. As shown in the Annual Report on Portfolio Performance (except for current FY). b. Average age of projects in the Bank's country portfolio. c. Percent of projects rated U or HU on development objectives (DO) and/or implementation progress

d. As defined under the Portfolio Improvement Program. e. Ratio of disbursements during the year to the undisbursed balance of the Bank's portfolio at the

beginning of the year: Investment projects only. * All indicators are for projects active in the Portfolio, with the exception of Disbursement Ratio,

which includes all active projects as well as projects which exited during the fiscal year.

(IP). .

22

CAS Annex B3 - IBRDIIDA Program Summary Panama As Of Date 02/12/2009

Proposed IBRDllDA Base-Case Lending Program a

Strategic lmplementa tion US$(M) Rewards b b Risks

(H/M/L) (H/M/L) Fiscal proj ID year

2008

2009

Competitiveness and PFM DPL 1 Total Competitiveness and PFM DPL 2 Education II Health Protecting the Poor DPL Total

PA Access to Finance PA Sustainable Tourism PA Urban Transport Total

2010 PA (AF) Land Administration

Overall Total

75.0 75.0 100.0 35.0 40.0 80.0 255.0 45.0 25.0 30.0 50.0 150.0 480.0

M

H H M H

H M H H

L

M M L M

M M H H

Panama: IFC Investment Operations Program

2006 2007 2008 2009*

Commitments (US$m) Gross Net**

Net Commitments bv Sector 1%) EQUITY LOAN RISK PRODUCT Total

1.10 26.00 71.59 364.00 1.10 26.00 71.59 364.00

44.13 3.85 96.15 55.87 96.15

100 3.85 100 100 100 100

Net Commitments bv Investment Instrument (%) Equity Loan Risk product Total

44.13 3.85 96.15 55.87 96.15

100 3.85 100 100 100 100

As of March 31, 2009 ** IFC's Own Account only

23

CAS Annex B4 - Summary of Nonlending Services - Panama As Of 02/12/2009

Product Completion FY Cost (US$OOO) Audiencea Objectiveb

Recent completions Country Economic Memorandumhvestment Climate Assessment FY08 Country Environmental Analysis FY08

Underway Policy Notes FYO9 Poverty Assessment FY 09 Report on Observance of Standards and Codes FYO9

Planned Urban Development Study FYI0

150 G,B,PD KG , PD, PS

165 G,B,PD PD,PS

100 G,B,PD PD 191 GI D, B, P D KG, PD, PS

G,B KG,PS

335 G,B,PD KG,PD,PS

a. Government, donor, Bank, public dissemination. b. Knowledge generation, public debate, problem-solving.

24

CAS Annex B6 - Key Economic Indicators - Panama Actual Estimate Projected

Indicator 2005 2006 2007 2008 2009 2010 2011 2012 National accounts (as % of GDP) Gross domestic producta

Agriculture Industry Services

100 100 7 7

17 16 76 76

Total Consumption 75 73 Gross domestic fixed investment 17 18

Government investment 3 4 Private investment 14 14

Exports (GNFS), including CFZb 75 77 Imports (GNFS), including CFZ 69 69

Gross domestic savings Gross national savings‘

25 27 19 21

Memorandum items Gross domestic product 15465 17137 (US$ million at current prices) GNI per capita (US, Atlas method) 4650 4950

Real annual growth rates (%, calculated from 82 prices) Gross domestic product at market prices 7.2 8.5 Gross Domestic Income 9.8 6.8

100 100 7 6

17 16 77 77

77 79 23 24

6 8 17 16

80 70 75 75

23 21 19 16

19485 23518

5500 6150

11.5 9.0 11.8 0.2

100 100 100 100 6 6 6 6

15 16 16 16 79 78 78 78

81 81 80 80 24 27 25 23

8 9 9 9 16 18 16 14

66 66 66 66 72 74 73 70

19 19 20 20 15 15 16 16

25363 27177 29818 33022

6630 7250 7890 8660

3.0 4.0 6.0 7.0 1.5 0.3 4.1 6.5

Real annual per capita growth rates (“76, calculated from 82 prices) Gross domestic product at market prices 5.3 6.8 9.7 7.3 1.4 2.4 4.3 5.3 Total consumption 6.2 2.5 7.9 3.5 3.6 0.4 1.3 4.5 Private consumption 6.9 2.7 8.6 7.1 4.7 0.2 0.9 4.0

Exports (GNFS), including CFZb 10489 12416 14263 16471 16843 17947 19747 21662 Imports (GNFS), including CFZb 10688 11918 14627 17541 18342 20194 21706 23138

Ne t current transfers 245 253 253 250 220 140 80 0 Current account balance -1078 -527 -1423 -2296 -2650 -3420 -3159 -2637

Net private foreign direct investment 962 2498 1907 1950 1393 1836 2042 2256 Long-term loans (net) 543 928 362 541 2083 2933 2789 1167 Official -7 1 11 320 370 1211 1137 999 43 Private 614 917 42 172 872 1796 1790 1124

Other capital (net, incl. errors & ommissions) -948 -2727 -225 -36 -545 -1326 -1502 -633 Change in reservesd 521 -172 -622 -160 -281 -22 -170 -153

Balance o f Payments (US% millions)

Memorandum items Resource balance (% o f GDP) -1.3 2.9 -1.9 -4.5 -5.9 -8.3 -6.6 -4.5

(Continued)

25

CAS Annex B6 - Key Economic Indicators - Panama (continued)

Estimate Projected Indicator 2005 2006 2007 2008 2009 2010 2011 2012

Nonfinancial Public Sector Indicators (as % o f GDP at market prices)' Revenues, excluding PCA Expenditures, excluding PCA Overall Balance, excluding PCA Primary Balance, excluding PCA

Monetary indicators M2/GDP Growth o f A42 (%) Private sector credit growth / total credit growth (%)

Price indices( YRS2 =loo) Real exchange rate (US$/LCU)'

Real interest rates Consumer price index (% change)

22.3 24.9 -2.6 1.8

14.9 8.5

138.8

92.5

2.9

24.9 24.4

0.5 4.8

82.1 21.5

103.8

92.0

2.5

21.9 24.5

3.4 7.2

83.1 15.9

140.1

90.7

4.2

25.9 25.2

0.7 3.6

87.1 26.5 41.1

95.3

8.8

23.5 24.5 -1.0 1.6

87.7 7.8

89.0

100.3

4.7

24.0 24.9

1.5 -0.9

87.7 1.2

89.0

101.3

3.0

24.6 25.3

1.4 -0.7

87.7 9.7

89.0

102.8

3.5

25.0 25.5

1.3 -0.5

81.7 10.7 89.0

104.3

3.5 ~~~ ~~~ _ _ _ ~

a. GDP at factor cost b. "GNFS" denotes "goods and nonfactor services." c. Includes net unrequited transfers excluding official capital grants. d. Includes use o f IMF resources. e. NFPS f. "LCU" denotes "local currency units." An increase in US$/LCU denotes appreciation.

26

2 a

!?

go

R Y

rn

00

m

a

a

mm

d

a! ?

h

E

0 .- e n

wo

oo

oo

x 0

00

00

0

00

00

00

oo

om

oo

2

c! c?

wo

oo

oo

x 0

00

00

0

00

00

00

oo

om

ou

l

$2

BOCASBOCASDELDEL

TOROTORO

C H I R I Q U ÍC H I R I Q U Í

N G O B EN G O B EB U G L EB U G L E

V E R A G U A SV E R A G U A S

LOSLOSSANTOSSANTOS

D A R ID A R I É N

K U N A YA L A

EMB E R A

HE

RR

E R A

PA N A MPA N A M ÁC O LC O L Ó N

ChepoChepo

YavizaYaviza

YapeYape

CañitaCañita

Boca deBoca deLimónLimón

Santa FéSanta Fé

PiriáPiriá

CañazasCañazas

TocumenTocumen

La ChorreraLa Chorrera

El ValleEl ValleSoloySoloy

El CopéEl CopéSanta FéSanta Fé

DívisaDívisa

OcúOcúSonaSona

GuabaláGuabalá

PedregaPedrega

La ConcepciónLa Concepción

MacaracasMacaracas

TucutíTucutí

PenonomePenonome

SantiagoSantiago

DavidDavidChichicaChichica La PalmaLa PalmaCordi l lera Central

Cordi l lera de San Blas

Cerro PirreCerro Pirre(1445 m)(1445 m)

CerroCerroChucantiChucanti(1439 m)(1439 m)

CerroCerroPeña BlancaPeña Blanca(1314 m)(1314 m)

Cerro SantiagoCerro Santiago(2826 m)(2826 m)

Vulcán BarúVulcán Barú(3475 m)(3475 m) CerroCerro

ChorchaChorcha(2238 m)(2238 m)

Santa Maria

Chucunaque

Teribe

Panama

PanamaCanalCanal

LagoLagoGatúnGatún LagoLago

BayanoBayano

San

Pabl

o

Serranía del Darién

C O C LC O C L É

COSTACOSTARICARICA

COLOMBIACOLOMBIA

Salud

Portobelo

Chepo

Yaviza

Yape

Cañita

PuertoObaldía

Puerto Piña

GarachinéBoca de

Limón

Santa Fé

Piriá

UstupoYantupo

Cañazas

Chiman

Tocumen

La Chorrera

El Valle

Rio Hato

Coclédel Norte

SanCristóbal

Calovébora

Cusapin

ChiriquíGrande

Soloy

El CopéSanta Fé

Aguadulce

Dívisa

Ocú

PuertoMutis

El Tigre

Sona

Guabalá

Pedrega

La Concepción

Elena

Changuinola

Almirante

PuertoArmuelles

Macaracas

Los Asientos

Tonosí

Tucutí

Colón

Penonome

Santiago

DavidChichica

Chitre

Las Tablas

Bocas del Toro

El Porvenir

La Palma

PANAMÁ

BOCASDEL

TORO

C H I R I Q U Í

N G O B EB U G L E

V E R A G U A S

LOSSANTOS

KUNA DEMADUNGANDI

KUNA DEWARGANDI

EMBERA

D A R I É N

K U N A YA L A

EMB E R A

HE

RR

E R A

PA N A M ÁC O L Ó N

C O C L É

COSTARICA

COLOMBIA

Santa Maria

Chucunaque

Teribe

PanamaCanal

LagoGatún Lago

BayanoLago Chiriquí

San

Pabl

o

Car ibbean Sea

PACIFIC OCEAN

Golfo dePanamá

Bahía dePanamá

Golfo de losMosqui tos

To Corredor

To Uatsi

Cordi l lera Central

Cordi l lera de San Blas

Isla deCoiba

Isladel Rey

Serranía del Darién

CerroTacarcuna(1875 m)

Cerro Pirre(1445 m)

CerroChucanti(1439 m)

CerroPeña Blanca(1314 m)

CerroCambutal(1400 m)

Cerro Santiago(2826 m)

Vulcán Barú(3475 m) Cerro

Chorcha(2238 m)

83°W 82°W 81°W 80°W 79°W 78°W

77°W

83°W 82°W 81°W 80°W 79°W 78°W 77°W

8°N

9°N

10°N

7°N

8°N

9°N

10°N

PANAMA

This map was produced by the Map Design Unit of The World Bank. The boundaries, colors, denominations and any other informationshown on this map do not imply, on the part of The World BankGroup, any judgment on the legal status of any territory, or anyendorsement or acceptance of such boundaries.

0 80604020

0 20 40 60 Miles

100 Kilometers

IBRD 33462R

JUN

E 2007

PANAMASELECTED CITIES AND TOWNS

PROVINCE CAPITALS

NATIONAL CAPITAL

RIVERS

MAIN ROADS

RAILROADS

PROVINCE BOUNDARIES

INTERNATIONAL BOUNDARIES