REPORT - mtc.gov

66

REPORT Subject: Finnigan Briefing Book Provided to Phil Skinner, Idaho Prepared by: MTC Legal Staff Date: June 8, 2018 INTRODUCTION This briefing book addresses a public comment received at the Uniformity Committee’s April, 2018 meeting asking the Committee to consider adding a “Finnigan” option in the Commission’s Model Statute for Combined Reporting, which currently uses the “Joyce” approach. 1 It provides an executive summary of the Joyce/Finnigan debate and related issues and also includes appendices that provide additional background information. In addition to the Model Statute for Combined Reporting, 2 adopting a Finnigan approach would directly affect two other MTC uniformity recommendations which follow the Joyce approach, at least to an extent: the Statement of Information Concerning Practices of Multistate Tax Commission and Signatory States Under Public Law 86-272; 3 and the Model Factor Presence Nexus Standard for Business Activity Taxes. 4 In addition, it may affect a provision in our model General Allocation and Apportionment Regulations. 5 State positions have shifted since these models were adopted. The most significant reason the Commission had for adopting the Joyce approach was to avoid litigation. The risks that litigation may have posed have not materialized, however. 1 The Joyce/Finnigan issues is so-named because of two administrative decisions from California: In re the Appeal of Joyce, Inc., California Board of Equalization (1966); and In re the Appeal of Finnigan Corporation, No. 85-623-LB, California Board of Equalization (1990)(Finnigan II, on rehearing). 2 Appendix A. 3 Appendix B (Subsection E). 4 Appendix C, but only with respect to the application of P.L. 86-272. (Subsection E.) 5 See Reg. IV.3.(b).Taxable in Another State: When a Corporation Is "Subject to" a Tax under Article IV.3.(1).

Transcript of REPORT - mtc.gov

R E P O R T

Subject: Finnigan Briefing Book

Provided to Phil Skinner, Idaho

Prepared by: MTC Legal Staff

Date: June 8, 2018

INTRODUCTION

This briefing book addresses a public comment received at the Uniformity Committee’s April,

2018 meeting asking the Committee to consider adding a “Finnigan” option in the

Commission’s Model Statute for Combined Reporting, which currently uses the “Joyce”

approach.1 It provides an executive summary of the Joyce/Finnigan debate and related issues

and also includes appendices that provide additional background information.

In addition to the Model Statute for Combined Reporting,2 adopting a Finnigan approach

would directly affect two other MTC uniformity recommendations which follow the Joyce

approach, at least to an extent: the Statement of Information Concerning Practices of

Multistate Tax Commission and Signatory States Under Public Law 86-272;3 and the Model

Factor Presence Nexus Standard for Business Activity Taxes.4 In addition, it may affect a

provision in our model General Allocation and Apportionment Regulations.5

State positions have shifted since these models were adopted. The most significant reason the

Commission had for adopting the Joyce approach was to avoid litigation. The risks that

litigation may have posed have not materialized, however.

1 The Joyce/Finnigan issues is so-named because of two administrative decisions from California: In re the Appeal of Joyce, Inc., California Board of Equalization (1966); and In re the Appeal of Finnigan Corporation, No. 85-623-LB, California Board of Equalization (1990)(Finnigan II, on rehearing). 2 Appendix A. 3 Appendix B (Subsection E). 4 Appendix C, but only with respect to the application of P.L. 86-272. (Subsection E.) 5 See Reg. IV.3.(b).Taxable in Another State: When a Corporation Is "Subject to" a Tax under Article IV.3.(1).

2

EXECUTIVE SUMMARY – THE JOYCE/FINNIGAN DEBATE

THE ISSUE

The question at the center of the Joyce/Finnigan debate is:

Are states limited in their ability to tax an apportioned share of the income of

a unitary business conducted by multiple legal entities if some portion of that

income might be attributed to an entity over which the state lacks taxing

jurisdiction?

The primary authorities implicated by this question are the unitary business principle, the

substantial nexus standard, and P.L. 86-272 (Appendix D).

Simply put, advocates of the Joyce theory argue states cannot tax unitary business income

that may be attributed to a legal entity over which the state does not have taxing

jurisdiction—whether under substantial nexus theories or P.L. 86-272. Advocates of the

Finnigan theory disagree.

Adoption of the Joyce or Finnigan theory will directly affect:

How a state apportions unitary business income earned by multiple entities and how

it assigns a portion of the total tax to those entities.

How the state applies throw-out or throw-back rules to entities in a unitary group

(assuming those rules are conditioned on whether sales sourced to another

jurisdiction are subject to tax).

Adoption of the Joyce or Finnigan theory may also indirectly affect:

How a state treats tax attributes (e.g. NOLs or state tax credits and carryovers, etc.)—

assigning them either to each entity or to the group as a whole.

The positions of the states on the Joyce/Finnigan debate have fluctuated.6 The U.S. Supreme

Court has never weighed in despite opportunities to do so.7

6 See a summary of current positions in Appendix E. 7 See Deluxe Corp. v. Franchise Tax Bd., No. 991237 (Cal. Super. Ct. - San Francisco May 28, 1999)(not citable); Deluxe Corp. v. California Franchise Tax Board, U.S., No. 01-603, cert. denied,1/7/02; Citicorp North America, Inc. v. Franchise Tax Bd., 83 Cal.App.4th 1403, 100 Cal.Rptr.2d 509 (App. 1st Dist. 2000)(cert. denied, No. 00-1537, 6/29/01).

3

CRITICAL DISTINCTION – JOYCE IS NOT A THEORY OF JURISDICTION

Both Joyce and Finnigan are, essentially, theories about how jurisdictional principles are

applied. Joyce is thought of as an entity-by-entity approach to determining state corporate

income tax jurisdiction—whether the determination is made under the substantial nexus

standard or under P.L. 86-272. Finnigan, in contrast, is thought of as a group approach,

looking to the jurisdiction over the unitary business as a whole.

But neither Joyce nor Finnigan are, themselves, theories of jurisdiction. In particular, Joyce

does not posit that actions of third parties or affiliates cannot create nexus for a particular

entity. Nor does Joyce dictate that the activities of an entity’s affiliates, which may benefit that

entity, must be ignored in reaching an entity-specific determination of jurisdiction. Assume,

for example, that the employees of one entity solicit sales in a state for an affiliate. Also

assume that, in doing so, those employees take actions that exceed the protections of P.L. 86-

272. This would clearly give the state jurisdiction over the affiliate, even under the Joyce

theory. Likewise, Finnigan does not posit that the jurisdictional standards are, themselves,

lower. Rather, it posits that the standards can be met, for each entity in the unitary business,

if the activities of the unitary business itself meet the standards.

A SIMPLE ILLUSTRATION – COMBINED FILING

Under Joyce, a state will not tax a portion of the income of a unitary business that may be

attributed to entities over which it lacks jurisdiction. That does not mean, however, that the

state effectively uses separate entity filing. Instead, the state starts with the total income for

the unitary business, including income attributed to entities over which it lacks jurisdiction.

But only entities over which it has jurisdiction are required to apportion their share of that

income (whether that is done on a separate or combined report). The denominator of the

apportionment factor used by each reporting entity includes the everywhere amounts for the

entire unitary business, again, including factor amounts attributed to entities over which the

state lacks jurisdiction. The apportionment factor numerator for each reporting entity

includes the state-sourced amounts for that reporting entity. In this way, the factors used to

apportion income will exclude state-sourced amounts (typically receipts) attributed to

entities over which the state lacks jurisdiction.

The following illustration demonstrates that the tax result will differ under separate filing,

Joyce, and Finnigan apportionment methods.

4

Assume:

State A uses a single sales factor and imposes a 10% tax.

Corporations X, Y, and Z are unitary but Z is protected by P.L. 86-272.

Separate apportionable income and factors for X, Y, and Z in State A (prior to

consolidating eliminations) are:

X $2 million $1 million/$2 million

Y $2 million $1 million/$2 million

Z $6 million $3 million/$6 million

Consolidating eliminations: Z has $2 million of intercompany sales to X and Y, all of

which are sourced to state Z. Z’s post-elimination receipts factor, therefore, would be:

Z $1 million/$4 million8

Total combined apportionable income is $10 million.

Separate Basis Tax:

For X and Y each = $2 million X ($1 million/$2 million) X 10% = $100,000

For Z = $0 (since State A lacks jurisdiction to tax Z under P.L. 86-272)

Total = $200,000

Joyce Basis Tax:

For X and Y each = $10 million X ($1 million/$8 million) X 10% = $125,000

For Z = $0 (since State A would exclude its receipts from the factor numerator)

Total = $250,000

Finnigan Basis Tax:

For group = $10 million X ($3 million/$8 million) X 10% = $375,000.

Note: If there were no intercompany receipts, the results under the three methods would still

be different. And, if State A had a traditional three-factor formula, the difference between

Joyce and Finnigan would be mitigated because the effect of the difference in the receipts

factor would be reduced through the averaging of that factor with the property and payroll

factors (which, for a protected entity, would likely be zeros). Also, as discussed further below,

if State A had a throw-out/back rule, this might affect the tax outcome in some cases,

potentially making the tax owed under Joyce greater in those cases.

8 This report assumes that these intercompany receipts would be eliminated although the Model Statute for Combine Reporting does not explicitly address this point.

5

THE EFFECT OF THROW-BACK AND THROW-OUT RULES

States that use throw-back or throw-out rules in computing the receipts factor typically

condition the application of the rules on whether the seller is subject to tax in the destination

state. This condition is met when the destination state lacks taxing jurisdiction over the seller.

A state’s decision to follow Joyce or Finnigan for determining the apportionment approach

will affect its application of throw-back or throw-out rules. So states that follow Joyce throw

back (or out) any receipts if the seller, as an entity, is not subject to tax in the destination

state. States that follow Finnigan will only throw back (or out) any receipts if the group, as a

whole, is not subject to tax in the destination state. The overall revenue impact of Joyce versus

Finnigan, therefore, is mitigated by throw-back or throw-out rules.

INTERACTION WITH CONSTITUTIONAL NEXUS AND P.L. 86-272

As noted above, while Joyce is not a theory of jurisdiction, its method of applying

jurisdictional principles (entity by entity) means that the precise jurisdictional principles, or

standards, that are applied may matter more. And, as those standards change, the results

under Joyce (unlike those under Finnigan) are likely to change.

Substantial nexus has certainly evolved beyond traditional jurisdictional principles. For one

thing, physical presence is no longer considered necessary for substantial nexus, outside the

sales tax area. Some states have explicitly adopted economic presence or similar factor

presence standards (applying market sourcing for the receipts portion of that standard). Also,

under representative nexus theories, an argument can be made that the activities of an

entity’s unitary affiliates create nexus for that entity, provided those activities substantially

contribute to that entity’s portion of the unitary business in the state. These and similar

developments make it far more likely that, if a state has substantial nexus with the unitary

business, it will also have substantial nexus with most or all of the constituent entities, even

on an entity-by-entity basis.

Similarly, the text of P.L. 86-272 clearly recognizes that activities that create jurisdiction

include those performed either “by” or “on behalf of” a “taxpayer.” And while there have been

various arguments suggesting that P.L. 86-272 implicitly intends that only solicitation

activities performed on behalf of a business can create nexus, there is no sound authority for

these arguments. So, as with substantial nexus, even a Joyce state may conclude that activities

performed by affiliates in the state, if unprotected, may cause any entity that benefits from

those activities to be outside of the federal statute’s preemptive scope.

6

NOL DEDUCTIONS AND STATE TAX CREDITS

States also consider the treatment of NOL deductions, state tax credits, and sometimes other

attributes when deciding whether to take a Joyce or Finnigan approach to combined filing.

There is a theoretical connection between how the state treats these items and whether it

follows the Joyce or Finnigan approach. It would appear to be more consistent with the Joyce

approach to limit NOL deductions and tax credits to the legal entity which gave rise to those

items. There may be, however, other reasons to limit the use of NOL deductions or state tax

credits to the entity that generated those items. Likewise, a state would not necessarily be

prohibited from allowing NOL or credit offsets among a group, even if it were to adopt the

Joyce approach to apportionment.

OBSERVED PLANNING WITH JOYCE

Experience shows that taxpayers may try to use Joyce to avoid having sales included in a

state’s sales factor for the unitary group by isolating activities into separate entities for that

purpose. In addition, Joyce complicates both combined filing and the determination of

substantial nexus, especially where special purpose entities are involved.

POSSIBLE ALTERNATIVE FINNIGAN APPROACHES

There are three possible approaches to implementing a Finnigan apportionment method:

Combined returns—The first is to simply impose a tax, filing, and payment obligation

on the group, jointly and severally, and to use a combined return that consolidates

income and factors (and also handles allocable income).

Post-apportionment attribution of tax —The second is to take the same

apportionment approach as under a combined return but then to attribute a specific

portion of the tax to each entity over which the state has jurisdiction.

Pre-apportionment attribution of state-sourced receipts—The third is to retain the

entity-by-entity reporting approach but require the reporting of state-sourced

receipts for any entities over which the state lacks jurisdiction, allocating those

amounts for inclusion in the factors of the reporting entities.

7

SUMMARY OF CONSIDERATIONS FOR THE UNIFORMITY COMMITTEE

The trend is now clearly away from Joyce and toward Finnigan, although the states

are still very much split. (See Appendix E.)9

Adoption of a Finnigan “option” may be a simple solution (although keeping the

entity-by-entity reporting approach will complicate matters) but having it as an

option to Joyce does little to advance the cause of uniformity and consistency.

State uniformity in this area would eliminate the results of the inconsistent treatment

of the same receipts. Assuming states have throw-back rules, the same receipts could

be included in the receipts factor for two states. In other cases, receipts may end up

being excluded from the factor in any state.

Finnigan may be implemented in a simplified fashion, reducing the complexity of

combined reporting.

States will also need to consider what Finnigan means in the international context

especially when market-sourcing of receipts is adopted.

While it seems unlikely at this point, the Finnigan approach could potentially still be

subject to challenge. Also, any challenge of Finnigan is more likely to come under P.L.

86-272 and the states might have the opportunity to raise other issues in the context

of that challenge.

Examination of this issue might cause a number of other issues with respect to the

model to be raised—so thought will need to be given to whether the scope of the

project should, or should not, be limited.

ADDITIONAL RESOURCES

The following are also provided in appendices to this report:

Appendix F – Past MTC Staff and Uniformity Committee Memos

Appendix G – Matter of Disney Enterprises, Inc. v. Tax Appeals Tribunal

9 But even states that adopt the latter approach may determine that they need to attribute a share of the tax owed under that approach to each nexus-entity in the group. This can complicate the reporting of tax, but can be done in a way that does not change the tax amount owed under the general Finnigan theory.

APPENDIX A Multistate Tax Commission

Proposed Model Statute for Combined Reporting

As approved by the Multistate Tax Commission August 17, 2006 As amended by the Multistate Tax Commission July 29, 2011

Section 1. Definitions.

A. “Person” means any individual, firm, partnership, general partner of a partnership, limited liability company, registered limited liability partnership, foreign limited liability partnership, association, corporation (whether or not the corporation is, or would be if doing business in this state, subject to [state income tax act]), company, syndicate, estate, trust, business trust, trustee, trustee in bankruptcy, receiver, executor, administrator, assignee or organization of any kind.

B. “Taxpayer” means any person subject to the tax imposed by [State Corporate income tax act].

C. “Corporation” means any corporation as defined by the laws of this state or organization of any kind treated as a corporation for tax purposes under the laws of this state, wherever located, which if it were doing business in this state would be a “taxpayer.” The business conducted by a partnership which is directly or indirectly held by a corporation shall be considered the business of the corporation to the extent of the corporation’s distributive share of the partnership income, inclusive of guaranteed payments to the extent prescribed by regulation.

D. "Partnership" means a general or limited partnership, or organization of any kind treated as a partnership for tax purposes under the laws of this state.

E. “Internal Revenue Code” means Title 26 of the United States Code of [date] [and amendments thereto] without regard to application of federal treaties unless expressly made applicable to states of the United States.

F. “Unitary business” means [a single economic enterprise that is made up either of separate parts of a single business entity or of a commonly controlled group of business entities that are sufficiently interdependent, integrated and interrelated through their activities so as to provide a synergy and mutual benefit that produces a sharing or exchange of value among them and a significant flow of value to the separate parts.] Drafter’s note: This portion of the definition is drafted to follow MTC Reg. IV(b), defining a “unitary business.” A state that does not wish to define unitary business in this manner should consider alternative language. In addition, this MTC Regulation defining unitary business includes a requirement of common ownership or control. A state which treats ownership or control requirements separately from the unitary business requirement will need to make additional amendments to the statutory language. Any business conducted by a partnership shall be treated as conducted by its partners, whether directly held or indirectly held through a series of partnerships, to the extent of the partner's distributive share of the partnership's income, regardless of the percentage of the partner's ownership interest or its distributive or any other share of partnership income. A business conducted directly or indirectly by one corporation is unitary with that portion of a business conducted by another

2

corporation through its direct or indirect interest in a partnership if the conditions of the first sentence of this section 1.F. are satisfied, to wit: there is a synergy, and exchange and flow of value between the two parts of the business and the two corporations are members of the same commonly controlled group.

G. “Combined group” means the group of all persons whose income and apportionment factors are required to be taken into account pursuant to Section 2.A. or 2.B. in determining the taxpayer’s share of the net business income or loss apportionable to this State.

H. “United States” means the 50 states of the United States, the District of Columbia, and United States’ territories and possessions.

I. “Tax haven” means a jurisdiction that, during the tax year in question has no or nominal effective tax on the relevant income and:

(i) has laws or practices that prevent effective exchange of information for tax purposes with other governments on taxpayers benefiting from the tax regime;

(ii) has tax regime which lacks transparency. A tax regime lacks transparency if the details of legislative, legal or administrative provisions are not open and apparent or are not consistently applied among similarly situated taxpayers, or if the information needed by tax authorities to determine a taxpayer’s correct tax liability, such as accounting records and underlying documentation, is not adequately available;

(iii) facilitates the establishment of foreign-owned entities without the need for a local substantive presence or prohibits these entities from having any commercial impact on the local economy;

(iv) explicitly or implicitly excludes the jurisdiction’s resident taxpayers from taking advantage of the tax regime’s benefits or prohibits enterprises that benefit from the regime from operating in the jurisdiction’s domestic market; or

(v) has created a tax regime which is favorable for tax avoidance, based upon an overall assessment of relevant factors, including whether the jurisdiction has a significant untaxed offshore financial/other services sector relative to its overall economy.

Section 2. Combined reporting required, when; discretionary under certain circumstances.

A. Combined reporting required, when. A taxpayer engaged in a unitary business with one or more other corporations shall file a combined report which includes the income, determined under Section 3.C. of this act, and apportionment factors, determined under [provisions on apportionment factors and Section 3.B. of this act], of all corporations that are members of the unitary business, and such other information as required by the Director.

B. Combined reporting at Director’s discretion, when. The Director may, by regulation, require the combined report include the income and associated apportionment factors of any persons that are not included pursuant to Section 2.A., but that are members of a unitary business, in order to reflect proper apportionment of income of entire unitary businesses. Authority to require combination by regulation under this Section 2.B. includes authority to require combination of persons that are not, or would not be if doing business in this state, subject to the [State income tax Act].

3

In addition, if the Director determines that the reported income or loss of a taxpayer engaged in a unitary business with any person not included pursuant to Section 2.A. represents an avoidance or evasion of tax by such taxpayer, the Director may, on a case by case basis, require all or any part of the income and associated apportionment factors of such person be included in the taxpayer’s combined report.

With respect to inclusion of associated apportionment factors pursuant to Section 2.B., the Director may require the exclusion of any one or more of the factors, the inclusion of one or more additional factors which will fairly represent the taxpayer's business activity in this State, or the employment of any other method to effectuate a proper reflection of the total amount of income subject to apportionment and an equitable allocation and apportionment of the taxpayer's income.

Section 3. Determination of taxable income or loss using combined report.

The use of a combined report does not disregard the separate identities of the taxpayer members of the combined group. Each taxpayer member is responsible for tax based on its taxable income or loss apportioned or allocated to this state, which shall include, in addition to other types of income, the taxpayer member’s apportioned share of business income of the combined group, where business income of the combined group is calculated as a summation of the individual net business incomes of all members of the combined group. A member’s net business income is determined by removing all but business income, expense and loss from that member’s total income, as provided in detail below.

A. Components of income subject to tax in this state; application of tax credits and post apportionment deductions.

i. Each taxpayer member is responsible for tax based on its taxable income or loss apportioned or allocated to this state, which shall include:

(a) its share of any business income apportionable to this State of each of the combined groups of which it is a member, determined under Section 3.B.,

(b) its share of any business income apportionable to this State of a distinct business activity conducted within and without the state wholly by the taxpayer member, determined under [provisions for apportionment of business income],

(c) its income from a business conducted wholly by the taxpayer member entirely within the state,

(d) its income sourced to this state from the sale or exchange of capital or assets, and from involuntary conversions, as determined under Section 3.C.ii.(g), below,

(e) its nonbusiness income or loss allocable to this State, determined under [provisions for allocation of non-business income],

(f) its income or loss allocated or apportioned in an earlier year, required to be taken into account as state source income during the income year, other than a net operating loss, and

(g) its net operating loss carryover or carryback.

If the taxable income computed pursuant to Section 3 results in a loss for a taxpayer member of the combined group, that taxpayer member has a [state] net operating loss (NOL), subject to the net operating loss limitations, carryforward and carryback provisions of [provisions on NOLs]. Such NOL is applied as a deduction in a prior or subsequent year only if that taxpayer has [State]

4

source positive net income, whether or not the taxpayer is or was a member of a combined reporting group in the prior or subsequent year.

ii. Except where otherwise provided, no tax credit or post-apportionment deduction earned by one member of the group, but not fully used by or allowed to that member, may be used in whole or in part by another member of the group or applied in whole or in part against the total income of the combined group; and a post-apportionment deduction carried over into a subsequent year as to the member that incurred it, and available as a deduction to that member in a subsequent year, will be considered in the computation of the income of that member in the subsequent year, regardless of the composition of that income as apportioned, allocated or wholly within this state.

B. Determination of taxpayer’s share of the business income of a combined group apportionable to this State.

The taxpayer’s share of the business income apportionable to this State of each combined group of which it is a member shall be the product of:

i. the business income of the combined group, determined under Section 3.C., and

ii. the taxpayer member’s apportionment percentage, determined under [provisions on apportionment factors], including in the [property, payroll and sales factor]numerators the taxpayer’s [property, payroll and sales, respectively,] associated with the combined group’s unitary business in this state, and including in the denominator the [property, payroll and sales] of all members of the combined group, including the taxpayer, which property, payroll and sales are associated with the combined group’s unitary business wherever located. The [property, payroll, and sales] of a partnership shall be included in the determination of the partner's apportionment percentage in proportion to a ratio the numerator of which is the amount of the partner's distributive share of partnership’s unitary income included in the income of the combined group in accordance with Section 3.C.ii.(c). and the denominator of which is the amount of the partnership’s total unitary income.

C. Determination of the business income of the combined group.

The business income of a combined group is determined as follows:

i. From the total income of the combined group, determined under Section 3.C.ii., subtract any income, and add any expense or loss, other than the business income, expense or loss of the combined group.

ii. Except as otherwise provided, the total income of the combined group is the sum of the income of each member of the combined group determined under federal income tax laws, as adjusted for state purposes, as if the member were not consolidated for federal purposes. The income of each member of the combined group shall be determined as follows:

(a) For any member incorporated in the United States, or included in a consolidated federal corporate income tax return, the income to be included in the total income of the combined group shall be the taxable income for the corporation after making appropriate adjustments under [state tax code provisions for adjustments to taxable income].

(b) (1) For any member not included in Section 3.C.ii.(a), the income to be included in the total income of the combined group shall be determined as follows:

5

(A) A profit and loss statement shall be prepared for each foreign branch or corporation in the currency in which the books of account of the branch or corporation are regularly maintained.

(B) Adjustments shall be made to the profit and loss statement to conform it to the accounting principles generally accepted in the United States for the preparation of such statements except as modified by this regulation.

(C) Adjustments shall be made to the profit and loss statement to conform it to the tax accounting standards required by the [state tax code]

(D) Except as otherwise provided by regulation, the profit and loss statement of each member of the combined group, and the apportionment factors related thereto, whether United States or foreign, shall be translated into the currency in which the parent company maintains its books and records.

(E) Income apportioned to this state shall be expressed in United States dollars.

(2) In lieu of the procedures set forth in Section 3.C.ii.(b)(1), above, and subject to the determination of the Director that it reasonably approximates income as determined under [the State tax code], any member not included in Section 3.C.ii.(a) may determine its income on the basis of the consolidated profit and loss statement which includes the member and which is prepared for filing with the Securities and Exchange Commission by related corporations. If the member is not required to file with the Securities and Exchange Commission, the Director may allow the use of the consolidated profit and loss statement prepared for reporting to shareholders and subject to review by an independent auditor. If above statements do not reasonably approximate income as determined under [the State tax code] the Director may accept those statements with appropriate adjustments to approximate that income.

(c) If a unitary business includes income from a partnership, the income to be included in the total income of the combined group shall be the member of the combined group's direct and indirect distributive share of the partnership's unitary business income.

(d) All dividends paid by one to another of the members of the combined group shall, to the extent those dividends are paid out of the earnings and profits of the unitary business included in the combined report, in the current or an earlier year, be eliminated from the income of the recipient. This provision shall not apply to dividends received from members of the unitary business which are not a part of the combined group.

(e) Except as otherwise provided by regulation, business income from an intercompany transaction between members of the same combined group shall be deferred in a manner similar to 26 CFR 1.1502-13. Upon the occurrence of any of the following events, deferred business income resulting from an intercompany transaction between members of a combined group shall be restored to the income of the seller, and shall be apportioned as business income earned immediately before the event:

(1) the object of a deferred intercompany transaction is

(A) re-sold by the buyer to an entity that is not a member of the combined group,

6

(B) re-sold by the buyer to an entity that is a member of the combined group for use outside the unitary business in which the buyer and seller are engaged, or

(C) converted by the buyer to a use outside the unitary business in which the buyer and seller are engaged, or

(2) the buyer and seller are no longer members of the same combined group, regardless of whether the members remain unitary.

(f) A charitable expense incurred by a member of a combined group shall, to the extent allowable as a deduction pursuant to Internal Revenue Code Section 170, be subtracted first from the business income of the combined group (subject to the income limitations of that section applied to the entire business income of the group), and any remaining amount shall then be treated as a nonbusiness expense allocable to the member that incurred the expense (subject to the income limitations of that section applied to the nonbusiness income of that specific member). Any charitable deduction disallowed under the foregoing rule, but allowed as a carryover deduction in a subsequent year, shall be treated as originally incurred in the subsequent year by the same member, and the rules of this section shall apply in the subsequent year in determining the allowable deduction in that year.

(g) Gain or loss from the sale or exchange of capital assets, property described by Internal Revenue Code Section 1231(a)(3), and property subject to an involuntary conversion, shall be removed from the total separate net income of each member of a combined group and shall be apportioned and allocated as follows.

(1) For each class of gain or loss (short term capital, long term capital, Internal Revenue Code Section 1231, and involuntary conversions) all members' business gain and loss for the class shall be combined (without netting between such classes), and each class of net business gain or loss separately apportioned to each member using the member's apportionment percentage determined under Section 3.B., above.

(2) Each taxpayer member shall then net its apportioned business gain or loss for all classes, including any such apportioned business gain and loss from other combined groups, against the taxpayer member's nonbusiness gain and loss for all classes allocated to this State, using the rules of Internal Revenue Code Sections 1231 and 1222, without regard to any of the taxpayer member's gains or losses from the sale or exchange of capital assets, Section 1231 property, and involuntary conversions which are nonbusiness items allocated to another state.

(3) Any resulting state source income (or loss, if the loss is not subject to the limitations of Internal Revenue Code Section 1211) of a taxpayer member produced by the application of the preceding subsections shall then be applied to all other state source income or loss of that member.

(4) Any resulting state source loss of a member that is subject to the limitations of Section 1211 shall be carried forward [or carried back] by that member, and shall be treated as state source short-term capital loss incurred by that member for the year for which the carryover [or carryback] applies.

7

(h) Any expense of one member of the unitary group which is directly or indirectly attributable to the nonbusiness or exempt income of another member of the unitary group shall be allocated to that other member as corresponding nonbusiness or exempt expense, as appropriate.

Section 4. Designation of surety.

As a filing convenience, and without changing the respective liability of the group members, members of a combined reporting group may annually elect to designate one taxpayer member of the combined group to file a single return in the form and manner prescribed by the department, in lieu of filing their own respective returns, provided that the taxpayer designated to file the single return consents to act as surety with respect to the tax liability of all other taxpayers properly included in the combined report, and agrees to act as agent on behalf of those taxpayers for the year of the election for tax matters relating to the combined report for that year. If for any reason the surety is unwilling or unable to perform its responsibilities, tax liability may be assessed against the taxpayer members.

Section 5. Water’s-edge election; initiation and withdrawal.

A. Water’s-edge election.

Taxpayer members of a unitary group that meet the requirements of Section 5.B. may elect to determine each of their apportioned shares of the net business income or loss of the combined group pursuant to a water’s-edge election. Under such election, taxpayer members shall take into account all or a portion of the income and apportionment factors of only the following members otherwise included in the combined group pursuant to Section 2, as described below:

i. the entire income and apportionment factors of any member incorporated in the United States or formed under the laws of any state, the District of Columbia, or any territory or possession of the United States;

ii. the entire income and apportionment factors of any member, regardless of the place incorporated or formed, if the average of its property, payroll, and sales factors within the United States is 20 percent or more;

iii. the entire income and apportionment factors of any member which is a domestic international sales corporations as described in Internal Revenue Code Sections 991 to 994, inclusive; a foreign sales corporation as described in Internal Revenue Code Sections 921 to 927, inclusive; or any member which is an export trade corporation, as described in Internal Revenue Code Sections 970 to 971, inclusive;

iv. any member not described in [Section 5.A.i.] to [Section 5.A.iii.], inclusive, shall include the portion of its income derived from or attributable to sources within the United States, as determined under the Internal Revenue Code without regard to federal treaties, and its apportionment factors related thereto;

v. any member that is a “controlled foreign corporation,” as defined in Internal Revenue Code Section 957, to the extent of the income of that member that is defined in Section 952 of Subpart F of the Internal Revenue Code (“Subpart F income”) not excluding lower-tier subsidiaries’ distributions of such income which were previously taxed, determined without regard to federal treaties, and the apportionment factors related to that income; any item of income received by a controlled foreign corporation shall be excluded if such income was subject to an effective rate of income tax imposed by a foreign country greater than 90 percent of the maximum rate of tax specified in Internal Revenue Code Section 11;

8

vi. any member that earns more than 20 percent of its income, directly or indirectly, from intangible property or service related activities that are deductible against the business income of other members of the combined group, to the extent of that income and the apportionment factors related thereto; and

vii. the entire income and apportionment factors of any member that is doing business in a tax haven, where “doing business in a tax haven” is defined as being engaged in activity sufficient for that tax haven jurisdiction to impose a tax under United States constitutional standards. If the member’s business activity within a tax haven is entirely outside the scope of the laws, provisions and practices that cause the jurisdiction to meet the criteria established in Section 1.I., the activity of the member shall be treated as not having been conducted in a tax haven.

B. Initiation and withdrawal of election

i. A water’s-edge election is effective only if made on a timely-filed, original return for a tax year by every member of the unitary business subject to tax under [state income tax code]. The Director shall develop rules and regulations governing the impact, if any, on the scope or application of a water’s-edge election, including termination or deemed election, resulting from a change in the composition of the unitary group, the combined group, the taxpayer members, and any other similar change.

ii. Such election shall constitute consent to the reasonable production of documents and taking of depositions in accordance with [state statute on discovery].

iii. In the discretion of the Director, a water’s-edge election may be disregarded in part or in whole, and the income and apportionment factors of any member of the taxpayer's unitary group may be included in the combined report without regard to the provisions of this section, if any member of the unitary group fails to comply with any provision of [this act] or if a person otherwise not included in the water's-edge combined group was availed of with a substantial objective of avoiding state income tax.

iv. A water’s-edge election is binding for and applicable to the tax year it is made and all tax years thereafter for a period of 10 years. It may be withdrawn or reinstituted after withdrawal, prior to the expiration of the 10 year period, only upon written request for reasonable cause based on extraordinary hardship due to unforeseen changes in state tax statutes, law, or policy, and only with the written permission of the Director. If the Director grants a withdrawal of election, he or she shall impose reasonable conditions as necessary to prevent the evasion of tax or to clearly reflect income for the election period prior to or after the withdrawal. Upon the expiration of the 10 year period, a taxpayer may withdraw from the water’s edge election. Such withdrawal must be made in writing within one year of the expiration of the election, and is binding for a period of 10 years, subject to the same conditions as applied to the original election. If no withdrawal is properly made, the water’s edge election shall be in place for an additional 10 year period, subject to the same conditions as applied to the original election.

86

sales

5.

6.

7.

8.

9.

10.

11.

12.

13.

14.

15.

16.

b.

d.

g.

h.

17.

18.

19.

20. ESERVED

21.

1.

2.

3.

4.

5.

6.

7.

8.

9.

10.

11.

12. Mediating direct customer complaints when the purpose thereof is solely

for ingratiating the sales personnel with the customer and facilitating requests for orders.

13. Owning, leasing, using or maintaining personal property for use in the

employee or representative's "in-home" office or automobile that is solely limited to the conducting of protected activities. Therefore, the use of personal property such as a cellular telephone, facsimile machine, duplicating equipment, personal computer and computer software that is limited to the carrying on of protected solicitation and activity entirely ancillary to such solicitation or permitted by this Statement under paragraph IV.B. shall not, by itself, remove the protection under this Statement.

v INDEPENDENT CONTRACTORS

P.L. 86-272 provides protection to certain in-state activities if conducted by an

independent contractor that would not be afforded if performed by the company cr its employees or other representatives. Independent contractors may engage in the following limited activities in the state without the company's loss of immunity:

1. Soliciting sales.

2. Making sales.

3. Maintaining an office.

Sales representatives who represent a single principal are not considered to be

independent contractors and are subject to the same limitations as those provided under P.L. 86-272 and this Statement.

Maintenance of a stock of goods in the state by the indepenlent contractor under

consignment or any other type of arrangement with the company, except for purposes of display and solicitation, shall remove the protection.

VI APPLICATION OF DESTINATION STATE LAW

IN CASE OF CONFLICT

When it appears that two or more signatory states have included or will include the same receipts from a sale in their respective sales factor numerators, at the written request of the company, said states will in good faith confer with one another to determine which state should be assigned said receipts. Such conference shall identify

PPLICATION OF .

.

.

ART OF .

JOYCE ULE.

1 Updated September 2003

APPENDIX C

Factor Presence Nexus Standard for Business Activity Taxes

Approved by the Multistate Tax Commission

October 17, 2002

The Commisison adopted the following uniformity proposal as part of an amendment to MTC Policy Statement 02-02, Ensuring the Equity, Integrity and Viability of State Income Tax Systems, approved on October 17, 2002. A working group of states formulated the proposal over several months through public teleconferences and the Commission held four public hearings covering the technical, policy and constitutional aspects of the proposed provision. This factor presence nexus standard is intended to represent a simple, certain and equitable standard for the collection of state business activity taxes. Professor Charles McLure, Senior Fellow with the Hoover Institution at Stanford University, originated the idea of factor presence nexus and set forth an explanation of the concept in his December 2000 National Tax Journal article entitled, "Implementing State Corporate Income Taxes in the Digital Age." Professor McLure reiterated his concept during the Commission's July 2001 Federalism at Risk seminar.

A. (1) Individuals who are residents or domiciliaries of this State and business entities that are organized or commercially domiciled in this State have substantial nexus with this State.

(2) Nonresident individuals and business entities organized outside the State that are

doing business in this State have substantial nexus and are subject to [list appropriate business activity taxes for the state, with statutory citations] when in any tax period the property, payroll or sales of the individual or business in the State, as they are defined below in Subsection C, exceeds the thresholds set forth in Subsection B.

B. (1) Substantial nexus is established if any of the following thresholds is exceeded

during the tax period:

(a) a dollar amount of $50,000 of property; or

(b) a dollar amount of $50,000 of payroll; or

(c) a dollar amount of $500,000 of sales; or

(d) twenty-five percent of total property, total payroll or total sales.

(2) At the end of each year, the [tax administrator] shall review the cumulative percentage change in the consumer price index. The [tax administrator] shall adjust the thresholds set forth in paragraph (1) if the consumer price index has changed by

2 Regulations, Statutes, and Guidelines

Multistate Tax Commission

5% or more since January 1, 2003, or since the date that the thresholds were last adjusted under this subsection. The thresholds shall be adjusted to reflect that cumulative percentage change in the consumer price index. The adjusted thresholds shall be rounded to the nearest $1,000. As used in this subsection, “consumer price index” means the Consumer Price Index for All Urban Consumers (CPI-U) available from the Bureau of Labor Statistics of the United States Department of Labor. Any adjustment shall apply to tax periods that begin after the adjustment is made.

C. Property, payroll and sales are defined as follows:

(1) Property counting toward the threshold is the average value of the taxpayer's real property and tangible personal property owned or rented and used in this State during the tax period. Property owned by the taxpayer is valued at its original cost basis. Property rented by the taxpayer is valued at eight times the net annual rental rate. Net annual rental rate is the annual rental rate paid by the taxpayer less any annual rental rate received by the taxpayer from sub-rentals. The average value of property shall be determined by averaging the values at the beginning and ending of the tax period; but the tax administrator may require the averaging of monthly values during the tax period if reasonably required to reflect properly the average value of the taxpayer's property.

(2) Payroll counting toward the threshold is the total amount paid by the taxpayer for compensation in this State during the tax period. Compensation means wages, salaries, commissions and any other form of remuneration paid to employees and defined as gross income under Internal Revenue Code § 61. Compensation is paid in this State if (a) the individual's service is performed entirely within the State; (b) the individual's service is performed both within and without the State, but the service performed without the State is incidental to the individual's service within the State; or (c) some of the service is performed in the State and (1) the base of operations or, if there is no base of operations, the place from which the service is directed or controlled is in the State, or (2) the base of operations or the place from which the service is directed or controlled is not in any State in which some part of the service is performed, but the individual's residence is in this State.

(3) Sales counting toward the threshold include the total dollar value of the taxpayer’s

gross receipts, including receipts from entities that are part of a commonly owned enterprise as defined in D(2) of which the taxpayer is a member, from

(a) the sale, lease or license of real property located in this State;

(b) the lease or license of tangible personal property located in this State;

(c) the sale of tangible personal property received in this State as indicated by

receipt at a business location of the seller in this State or by instructions, known to the seller, for delivery or shipment to a purchaser (or to another at the direction of the purchaser) in this State; and

3 Updated September 2003

Factor Presence Nexus

(d) The sale, lease or license of services, intangibles, and digital products for primary use by a purchaser known to the seller to be in this State. If the seller knows that a service, intangible, or digital product will be used in multiple States because of separate charges levied for, or measured by, the use at different locations, because of other contractual provisions measuring use, or because of other information provided to the seller, the seller shall apportion the receipts according to usage in each State.

(e) If the seller does not know where a service, intangible, or digital product will

be used or where a tangible will be received, the receipts shall count toward the threshold of the State indicated by an address for the purchaser that is available from the business records of the seller maintained in the ordinary course of business when such use does not constitute bad faith. If that is not known, then the receipts shall count toward the threshold of the State indicated by an address for the purchaser that is obtained during the consummation of the sale, including the address of the purchaser’s payment instrument, if no other address is available, when the use of this address does not constitute bad faith.

(4) Notwithstanding the other provisions of this Subsection C, for a taxpayer subject to the special apportionment methods under [Multistate Tax Commission Regulations IV.18.(d) through (j)], the property, payroll and sales for measuring against the nexus thresholds shall be defined as they are for apportionment purposes under those regulations. Financial institutions subject to an apportioned income or franchise tax shall determine property, payroll and sales for nexus threshold purposes the same as for apportionment purposes under the [MTC Recommended Formula for the Apportionment and Allocation of Net Income of Financial Institutions]. Pass-through entities, including, but not limited to, partnerships, limited liability companies, S corporations, and trusts, shall determine threshold amounts at the entity level. If property, payroll or sales of an entity in this State exceeds the nexus threshold, members, partners, owners, shareholders or beneficiaries of that pass-through entity are subject to tax on the portion of income earned in this State and passed through to them.

D. (1) Entities that are part of a commonly owned enterprise shall determine whether

they meet the threshold for nexus as follows:

(a) Commonly owned enterprises shall first aggregate the property, payroll and sales of their entities that have a minimum presence in this State of $5000 of combined property, payroll and sales, including those entities that independently exceed a threshold and separately have nexus. The aggregate number shall be reduced based on detailed disclosure of any intercompany transactions where inclusion would result in one State’s double counting assets or revenue. If that aggregation of property, payroll and sales meets any threshold in Subsection B,

Multistate Tax Commission

4 Regulations, Statutes, and Guidelines

the enterprise shall file a joint information return as specified by the [tax agency] separately listing the property, payroll and sales in this State of each entity.

(b) Those entities of the commonly owned enterprise that are listed in the joint information return and that are also part of a unitary business grouping conducting business in this State shall then aggregate the property, payroll and sales of each such unitary business grouping on the joint information return. The aggregate number shall be reduced based on detailed disclosure of any intercompany transactions where inclusion would result in one State’s double counting assets or revenue. The entities shall base the unitary business groupings on the unitary combined report filed in this State. If no unitary combined report is required in this State, then the taxpayer shall use the unitary business groupings the taxpayer most commonly reports in States that require combined returns.

(c) If the aggregate property, payroll or sales in this State of the entities of any unitary business of the enterprise meets a threshold in Subsection B, then each entity that is part of that unitary business is deemed to have nexus and shall file and pay income or franchise tax as required by law.

(2) “Commonly owned enterprise” means a group of entities under common control either through a common parent that owns, or constructively owns, more than 50 percent of the voting power of the outstanding stock or ownership interests or through five or fewer individuals (individuals, estates or trusts) that own, or constructively own, more than 50 percent of the voting power of the outstanding stock or ownership interests taking into account the ownership interest of each such person only to the extent such ownership is identical with respect to each such entity.

E. A State without jurisdiction to impose tax on or measured by net income on a

particular taxpayer because that taxpayer comes within the protection of Public Law 86-272 (15 U.S.C. § 381) does not gain jurisdiction to impose such a tax even if the taxpayer’s property, payroll or sales in the State exceeds a threshold in Subsection B. Public Law 86-272 preempts the state’s authority to tax and will therefore cause sales of each protected taxpayer to customers in the State to be thrown back to those sending States that require throwback. If Congress repeals the application of Public Law 86-272 to this State, an out-of-state business shall not have substantial nexus in this State unless its property, payroll or sales exceeds a threshold in this provision.

APPENDIX D – P.L. 86-272

5 U.S. Code § 381 - Imposition of net income tax

(a)Minimum standards. No State, or political subdivision thereof, shall have power to impose, for any taxable year ending after September 14, 1959, a net income tax on the income derived within such State by any person from interstate commerce if the only business activities within such State by or on behalf of such person during such taxable year are either, or both, of the following:

(1)the solicitation of orders by such person, or his representative, in such State for sales of tangible personal property, which orders are sent outside the State for approval or rejection, and, if approved, are filled by shipment or delivery from a point outside the State; and

(2)the solicitation of orders by such person, or his representative, in such State in the name of or for the benefit of a prospective customer of such person, if orders by such customer to such person to enable such customer to fill orders resulting from such solicitation are orders described in paragraph (1).

(b)Domestic corporations; persons domiciled in or residents of a State. The provisions of subsection (a) shall not apply to the imposition of a net income tax by any State, or political subdivision thereof, with respect to—

(1)any corporation which is incorporated under the laws of such State; or

(2)any individual who, under the laws of such State, is domiciled in, or a resident of, such State.

(c)Sales or solicitation of orders for sales by independent contractors.

For purposes of subsection (a), a person shall not be considered to have engaged in business activities within a State during any taxable year merely by reason of sales in such State, or the solicitation of orders for sales in such State, of tangible personal property on behalf of such person by one or more independent contractors, or by reason of the maintenance, of an office in such State by one or more independent contractors whose activities on behalf of such person in such State consist solely of making sales, or soliciting orders for sales, or tangible personal property.

2

(d)Definitions. For purposes of this section—

(1)the term “independent contractor” means a commission agent, broker, or other independent contractor who is engaged in selling, or soliciting orders for the sale of, tangible personal property for more than one principal and who holds himself out as such in the regular course of his business activities; and

(2)the term “representative” does not include an independent contractor.

(Pub. L. 86–272, title I, § 101, Sept. 14, 1959, 73 Stat. 555.)

APPENDIX E

Topic Allocation and ApportionmentThe Sales FactorThrowback and Throwout RulesJoyce and Finnigan Rules for CombinedReporting

Group TaxationCombined ReturnsComputation of Combined Taxable IncomeApportionment and AllocationJoyce vs. Finnigan

Alabama No combined reporting.Alabama does not permit taxpayers to filecombined returns. [ Ala. Code § 40 1839(i); Ala. Admin. Code r. 810 27 1 .09. ]BNA CITN AL 6.4.4.3.

Not permitted.Alabama does not permit taxpayers to filecombined returns. Ala. Code § 40 18 39(i).BNA CITN AL 8.3.3.4.6.

Alaska Neither.Alaska does not follow either the Joyce orFinnigan rules.]BNA CITN AK 6.4.4.3.

Joyce.Alaska follows the Joyce rule.[ Bloomberg BNASurvey of State Tax Departments. ]BNA CITN AK 8.3.3.4.6.

Arizona Finnigan rule.Arizona follows the Finnigan rule. Ariz.Admin. Code 15 2D 404.B.BNA CITN AZ 6.4.4.3.

Finnigan.Arizona follows the Finnigan rule. Ariz. Admin.Code R15 2D 404(B).BNA CITN AZ 8.3.3.4.6.

Arkansas No combined reporting.Arkansas does not permit taxpayers to filecombined returns. [ Ark. Code Ann. § 26 51804. ]BNA CITN AR 6.4.4.3.

Not permitted.Arkansas does not permit taxpayers to filecombined returns. Ark. Regs. 3.26 51 701.BNA CITN AR 8.3.3.4.6.

California Finnigan.California follows the Finnigan rule. [ Cal.Rev. & Tax. Code § 25135; Cal. Code Regs.tit. 18, § 25106.5(c)(7)(A)(iii).]BNA CITN CA 6.4.4.3.

Finnigan.California follows the Finnigan rule. [ Cal. Rev.&Tax. Code § 25135(b); Cal. Code Regs. tit. 18,§ 25106.5(c)(7)(A)(1)(b)(iii).]BNA CITN CA 8.3.3.4.6.

Colorado Joyce.Colorado follows the Joyce rule. Colo. Rev.Stat. § 39 22 303(11)(c)(II).BNA CITN CO 6.4.4.3.

Joyce.Colorado follows the Joyce rule. Colo. Rev. Stat.§ 39 22 303(11)(c)(II); 39 Colo. Code Regs. § 22303.5.4(a)(3).

Connecticut Finnigan.Connecticut follows the Finnigan rule.[Conn. Gen. Stat. §§ 12 213(a)(29).]BNA CITN CT 6.4.4.3.

Finnigan.Connecticut follows the Finnigan rule.[ Conn. Gen.Stat. §§ 12 213(a)(29), 12 213(a)(35), 12213(a)(36), and 12 218e(b).]

Delaware No combined reporting.Delaware does not permit taxpayers to filecombined returns. [ Delaware Form 1100,Corporation Income Tax Return,Instructions. ]BNA CITN DE 6.4.4.3.

Not permitted.Delaware does not permit taxpayers to filecombined returns. Del. Div. of Rev., Instructions toForm 1100, Corporation Income Tax Return.BNA CITN DE 8.3.3.4.6.

District ofColumbia

Joyce.The District of Columbia follows the Joycerule.[ D.C. Mun. Regs. tit. 9, § 169.1. ]BNA CITN DC 6.4.4.3.

Joyce.The District of Columbia follows the Joyce rule.[D.C. Mun. Regs. tit. 9, § 169.1. ]BNA CITN DC 8.3.3.4.6.

Topic Allocation and ApportionmentThe Sales FactorThrowback and Throwout RulesJoyce and Finnigan Rules for CombinedReporting

Group TaxationCombined ReturnsComputation of Combined Taxable IncomeApportionment and AllocationJoyce vs. Finnigan

Florida No combined reporting.Florida does not permit taxpayers to filecombined returns. [ Fla. Admin. Code Ann.r. 12C 1.015(7). ]BNA CITN FL 6.4.4.3.

Not permitted.Florida does not permit taxpayers to file combinedreturns.BNA CITN FL 8.3.3.4.6.

Georgia No combined reporting.Georgia does not permit taxpayers to filecombined returns. [ Ga. Code Ann. § 48 721(b)(7)(A). ]BNA CITN GA 6.4.4.3.

Not permitted.Georgia does not permit taxpayers to filecombined returns.BNA CITN GA 8.3.3.4.6.

Hawaii Joyce.Hawaii follows the Joyce rule.[ Haw. Regs.§ 18 235 22 03; Tax Information Release95 3 appendix, para. VII.E. ]BNA CITN HI 6.4.4.3.

Joyce.Hawaii follows the Joyce rule. Haw. Regs. § 18 23522 03.BNA CITN HI 8.3.3.4.6.

Idaho Joyce.Idaho follows the Joyce rule.[ Idaho Regs.§ 35.01.01.365.05.]BNA CITN ID 6.4.4.3.

Joyce.Idaho follows the Joyce rule.[ Idaho Regs.§ 35.01.01.365.05. ]BNA CITN ID 8.3.3.4.6.

Illinois Joyce.Illinois follows the Joyce rule.[ Ill. Admin.Code tit. 86, § 100.9720(f). ]BNA CITN IL 6.4.4.3.

Joyce.Illinois follows the Joyce rule.[ Ill. Admin. Code tit.86, §§ 100.9720(f), 100.5270(b)(1).]BNA CITN IL 8.3.3.4.6.

Indiana Finnigan.Indiana follows the Finnigan rule. Ind.Dept. of Rev., Indiana Tax Policy Directive 6(June 1992).BNA CITN IN 6.4.4.3.

Finnigan.Indiana follows the Finnigan rule. Ind. Dept. ofRev., Tax Policy Directive 6 (June 1992).BNA CITN IN 8.3.3.4.6.

Iowa No combined reporting.Iowa does not permit taxpayers to filecombined returns. [ Iowa Code Ann.§ 422.37. ]BNA CITN IA 6.4.4.3.

Not permitted.Iowa does not permit taxpayers to file combinedreturns.BNA CITN IA 8.3.3.4.6.

Kansas Finnigan.Kansas follows the Finnigan rule. [ Kan.Admin. Regs. 92 12 112(a). ]BNA CITN KS 6.4.4.3.

Finnigan.Kansas follows the Finnigan rule. Kan. Admin.Regs. 92 12 112(a); Kan. Dept. of Rev., RevenueRuling 12 91 1 (Jan. 1, 1991).

Topic Allocation and ApportionmentThe Sales FactorThrowback and Throwout RulesJoyce and Finnigan Rules for CombinedReporting

Group TaxationCombined ReturnsComputation of Combined Taxable IncomeApportionment and AllocationJoyce vs. Finnigan

Kentucky No combined reporting.Kentucky does not permit taxpayers to filecombined returns. [ Ky. Rev. Stat. Ann.§ 141.200(15). ]BNA CITN KY 6.4.4.3.

Yes.For taxable years beginning on or after Jan. 1,2019, Kentucky will require taxpayers engaged in aunitary business to file a combined report. 2018Ky. H.B. 487, § 120, effective for taxable yearsbeginning on or after Jan. 1, 2019.

Louisiana No combined reporting.Louisiana does not permit taxpayers to filecombined returns. [ La. Admin. Code tit. 61,§ 1175. ]BNA CITN LA 6.4.4.3.

Not permitted.Louisiana does not permit taxpayers to filecombined returns, unless specifically required bythe Secretary of Revenue. La. Rev. Stat. Ann.§ 47:287.480(3); La. Rev. Stat. Ann. § 47:287.733.

Maine Finnigan.Maine follows the Finnigan rule.[ MaineTax Alert, Vol. 20, No. 9 (Sept. 2010). ]BNA CITN ME 6.4.4.3.

Finnigan.Maine follows the Finnigan rule.[ Maine Tax Alert,Vol. 20, No. 9 (Sept. 2010). ]BNA CITN ME 8.3.3.4.6.

Maryland No combined reporting.Maryland does not permit taxpayers to filecombined returns. [ Md. Regs. Code§ 03.04.03.03.]BNA CITN MD 6.4.4.3.

Not permitted.Maryland does not permit taxpayers to filecombined returns. [ Md. Code Ann. Tax Gen. § 10811.]BNA CITN MD 8.3.3.4.6.

Massachusetts

Finnigan.Massachusetts follows the Finnigan rule.Mass. Dept. of Rev., MassachusettsTechnical Information Release TIR 08 11(Aug. 15, 2008).BNA CITN MA 6.4.4.3.

Finnigan.Massachusetts follows the Finnigan rule.Massachusetts Technical Information Release TIR08 11 (Aug. 15, 2008); Mass. Regs. Code tit. 830,§ 63.32B.2(7)(b).BNA CITN MA 8.3.3.4.6.

Michigan FinniganMichigan follows the Finnigan rule. [ Mich.Comp. Laws § 206.691; Mich. Comp. Laws§ 206.663(2); Mich. Comp. Laws§ 208.1511. ]

Finnigan.Michigan follows the Finnigan rule. [ Mich. Comp.Laws § 206.691; Mich. Comp. Laws § 206.663(2);Mich. Comp. Laws § 208.1511. ]BNA CITN MI 8.3.3.4.6.

Minnesota Finnigan.Minnesota follows the Finnigan rule.[Minn. Stat. § 290.17(4)(f). ]BNA CITN MN 6.4.4.3.

Finnigan.Minnesota follows the Finnigan rule.[ Minn. Stat.§ 290.17(4)(f). ]BNA CITN MN 8.3.3.4.6.

Mississippi Joyce.Mississippi follows the Joyce rule.BNA CITN MS 6.4.4.3.

Joyce.Mississippi follows the Joyce rule. [ Miss. Regs.§ 35.III.08.07.102.02. ]

Topic Allocation and ApportionmentThe Sales FactorThrowback and Throwout RulesJoyce and Finnigan Rules for CombinedReporting

Group TaxationCombined ReturnsComputation of Combined Taxable IncomeApportionment and AllocationJoyce vs. Finnigan

Missouri No combined reporting.Missouri does not permit taxpayers to filecombined returns. [ Mo. Code Regs. Ann.tit. 12, § 10 2.075(66). ]BNA CITN MO 6.4.4.3.

Not permitted.Missouri does not permit taxpayers to filecombined returns. Mo. Code Regs. Ann. tit. 12,§ 10 2.075(66).BNA CITN MO 8.3.3.4.6.

Montana Finnigan.Montana follows the Finnigan rule.[ Mont.Admin. R. 42.26.260. ]BNA CITN MT 6.4.4.3.

Joyce.Montana follows the Joyce rule. Mont. Admin. R.42.26.511(1).BNA CITN MT 8.3.3.4.6.

Nebraska Joyce.Nebraska follows the Joyce rule. [ Neb.Admin. R. &Regs. 316 24 053.03(C). ]BNA CITN NE 6.4.4.3.

Joyce.Nebraska follows the Joyce rule. Neb. Admin. R. &Regs. 316 24 053.03(C).BNA CITN NE 8.3.3.4.6.

Nevada No corporate income tax.Nevada does not impose a corporateincome tax.BNA CITN NV 6.4.4.3.

No corporate income tax.Nevada does not impose a corporate income tax.BNA CITN NV 8.3.3.4.6.

NewHampshire

Joyce.New Hampshire follows the Joyce rule. [N.H. Code Admin. R. Dept. Rev. Admin.304.01(h); N.H. Code Admin. R. Dept. Rev.Admin. 304.01(h); N.H. Rev. Stat. Ann. § 77A:3(III). ]BNA CITN NH 6.4.4.3.

Joyce.New Hampshire follows the Joyce rule. [ N.H. CodeAdmin. R. Dept. Rev. Admin. 304.01(g). ]BNA CITN NH 8.3.3.4.6.

New Jersey No combined reporting.New Jersey does not permit taxpayers tofile combined returns. [ N.J. Admin. Codetit. 18, § 7 5.1. ]BNA CITN NJ 6.4.4.3.

Not permitted.New Jersey does not permit taxpayers to filecombined returns.BNA CITN NJ 8.3.3.4.6.

NewMexico Joyce.New Mexico follows the Joyce rule. [ N.M.Stat. Ann. § 7 4 17(A). ]BNA CITN NM 6.4.4.3.

Joyce.New Mexico follows the Joyce rule. [ N.M. Stat.Ann. § 7 4 17(A). ]BNA CITN NM 8.3.3.4.6.

New York Finnigan.New York follows the Finnigan rule. Matterof Disney Enterprises, Inc. v. New York TaxApp. Trib., 10 N.Y.3d 392, 888 N.E.2d 1029(N.Y. 2008).BNA CITN NY 6.4.4.3.

Finnigan.New York follows the Finnigan rule. [ N.Y. Tax Law§ 210 C(5)(a); N.Y. Comp. Codes R. & Regs. tit. 20,§ 4 4.8. ]BNA CITN NY 8.3.3.4.6.

Topic Allocation and ApportionmentThe Sales FactorThrowback and Throwout RulesJoyce and Finnigan Rules for CombinedReporting

Group TaxationCombined ReturnsComputation of Combined Taxable IncomeApportionment and AllocationJoyce vs. Finnigan

NorthCarolina

Finnigan.North Carolina follows the Finnigan rule.N.C. Gen. Stat. § 105 130.14.BNA CITN NC 6.4.4.3.

Finnigan.North Carolina follows the Finnigan rule. N.C.Admin. Code tit. 17, r. 05F.0501(5).BNA CITN NC 8.3.3.4.6.

North Dakota Joyce.North Dakota follows the Joyce rule. [ N.D.Admin. Code § 81 03 09 28. ]BNA CITN ND 6.4.4.3.

Joyce.North Dakota follows the Joyce rule. [ N.D. Admin.Code § 81 03 09 28. ]BNA CITN ND 8.3.3.4.6.

Ohio No.Ohio does not use an apportionmentformula for Commercial Activity Taxpurposes. Ohio Rev. Code Ann. § 5751.01.BNA CITN OH 6.4.4.3.

Neither.Ohio does not follow the Joyce or Finnigan rules.BNA CITN OH 8.3.3.4.6.

Oklahoma No combined reporting.Oklahoma does not permit taxpayers to filecombined returns. [ Okla. Admin. Code§ 710:50 17 34.]BNA CITN OK 6.4.4.3.

Not permitted.Oklahoma does not permit taxpayers to filecombined returns. [ Okla. Admin. Code § 710:5017 31(b).]BNA CITN OK 8.3.3.4.6.

Oregon No combined reporting.Oregon does not permit taxpayers to filecombined returns. [ Or. Rev. Stat.§ 317.710.]

Not permitted.Oregon does not permit taxpayers to filecombined returns.BNA CITN OR 8.3.3.4.6.

Pennsylvania No combined reporting.Pennsylvania does not permit taxpayers tofile combined returns. [ 72 Pa. Stat.§ 7404.]

Not permitted.Pennsylvania does not permit taxpayers to filecombined returns. 72 Pa. Stat. § 7404.BNA CITN PA 8.3.3.4.6.

Rhode Island Finnigan.Rhode Island follows the Finnigan rule. R.I.Gen. Laws § 44 11 4.1(a); R.I. Regs. § CT 1502, Rule 8(b); R.I. Regs. § CT 15 04, Rule8(e). For tax years beginning before Jan. 1,2015 Rhode Island did not permitcombined reporting.BNA CITN RI 6.4.4.3.

Finnigan.Rhode Island follows the Finnigan rule. [ R.I. Gen.Laws § 44 11 4.1(a); R.I. Regs. § CT 16 17, Rule10(f). ]BNA CITN RI 8.3.3.4.6.

SouthCarolina

Finnigan.South Carolina follows the Finnigan rule.[South Carolina Revenue Ruling No. 15 5(June 12, 2015). ]BNA CITN SC 6.4.4.3.

Finnigan.South Carolina follows the Finnigan rule.[ SouthCarolina Revenue Ruling No. 15 5 (June 12, 2015).]BNA CITN SC 8.3.3.4.6.

Topic Allocation and ApportionmentThe Sales FactorThrowback and Throwout RulesJoyce and Finnigan Rules for CombinedReporting

Group TaxationCombined ReturnsComputation of Combined Taxable IncomeApportionment and AllocationJoyce vs. Finnigan

South Dakota No corporate income tax.South Dakota does not impose a corporateincome tax.BNA CITN SD 6.4.4.3.

No corporate income tax.South Dakota does not impose a corporate incometax.BNA CITN SD 8.3.3.4.6.

Tennessee No combined reporting.Tennessee does not permit taxpayers tofile combined returns. [ Tenn. Code Ann.§ 67 4 2007(e). ]BNA CITN TN 6.4.4.3.

Neither.Tennessee does not follow the Joyce or Finniganrules.[ Tenn. Code Ann. § 67 4 2013(b)(2).BNA CITN TN 8.3.3.4.6.

Texas Joyce.Texas follows the Joyce rule. [ Tex. TaxCode Ann. § 171.103(b). ]BNA CITN TX 6.4.4.3.

Joyce.Texas follows the Joyce rule. Tex. Tax Code Ann.§ 171.103(b).BNA CITN TX 8.3.3.4.6.

Utah Finnigan.Utah follows the Finnigan rule. Utah CodeAnn. § 59 7 317; Utah Admin. Code § R8656F 24(B).BNA CITN UT 6.4.4.3.

Finnigan.Utah follows the Finnigan rule. Utah Code Ann.§ 59 7 317; Utah Admin. Code § R865 6F 24(B).BNA CITN UT 8.3.3.4.6.

Vermont Joyce.Vermont follows the Joyce rule. Vt. Code R.§ 1.5862(d) 8(a).BNA CITN VT 6.4.4.3.

Joyce.Vermont follows the Joyce rule.[ Vt. Code R.§ 1.5862(d) 8(a). ]BNA CITN VT 8.3.3.4.6.

Virginia Joyce.Virginia follows the Joyce rule. [ Va. Regs.§ 10 120 327.]BNA CITN VA 6.4.4.3.

Joyce.Virginia follows the Joyce rule. [ Va. Code Ann.§ 58.1 442(B)(2). ]BNA CITN VA 8.3.3.4.6.

Washington No corporate income tax.Washington does not impose a corporateincome tax.BNA CITN WA 6.4.4.3.

No corporate income tax.Washington does not impose a corporate incometax.BNA CITN WA 8.3.3.4.6.

West Virginia Joyce.West Virginia follows the Joyce rule. W.Va.Code R. tit. 110, § 110 24 7.7(d)(2).BNA CITN WV 6.4.4.3.

Joyce.West Virginia follows the Joyce rule. W.Va. Code R.tit. 110, § 110 24 7.7(d)(2).BNA CITN WV 8.3.3.4.6.

Wisconsin Finnigan.Wisconsin follows the Finnigan rule. [ Wis.Stat. § 71.255(5)(a). ]BNA CITN WI 6.4.4.3.

Finnigan.Wisconsin follows the Finnigan rule. [ Wis. Stat.§ 71.255(5)(a); Bloomberg BNA Survey of State TaxDepartments. ]

Topic Allocation and ApportionmentThe Sales FactorThrowback and Throwout RulesJoyce and Finnigan Rules for CombinedReporting

Group TaxationCombined ReturnsComputation of Combined Taxable IncomeApportionment and AllocationJoyce vs. Finnigan

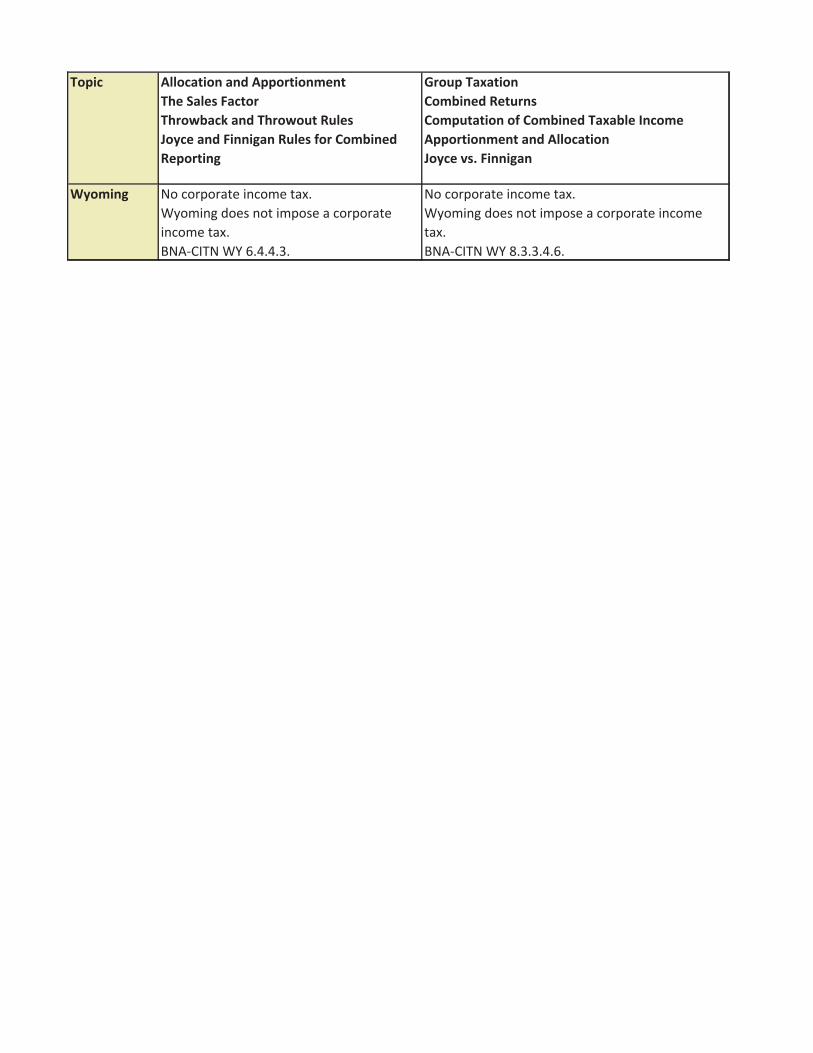

Wyoming No corporate income tax.Wyoming does not impose a corporateincome tax.BNA CITN WY 6.4.4.3.

No corporate income tax.Wyoming does not impose a corporate incometax.BNA CITN WY 8.3.3.4.6.

APPENDIX F

MTC Income & Franchise Tax Uniformity Subcommittee Work Group Recommendations Regarding Application of the Joyce Apportionment Formula

For the MTC Model Uniform Combined Reporting Statute

I. Introduction:

The MTC’s draft model uniform statute for combined reporting incorporates the Joyce method of apportionment. However, the Uniformity Committee has asked that consideration be given to substituting the Finnigan rule, as a means for counteracting tax planning activities that can take advantage of inadequacies in the nexus laws, even in a combined reporting context. For example, if an entity makes sales into Minnesota, and has activities in excess of solicitation in that state, Minnesota sales can be avoided by simply placing the nexus activity in a separate corporation, and asserting that the Minnesota sales are now protected by P.L. 86-272. If the state of origin does not have a "throw back" rule, the sale is not assigned to any taxing state. Because the sum of the apportionment percentages in all states the taxpayer does business does not add up to 100%, a substantial portion of a combined group's income is not subjected to tax in any taxing state. This problem would be vastly compounded under H.R. 3220.

II. Background:

A. Summary Description.

JoyceIn a nutshell, a state employing the Joyce rule does not consider the sales factor numerator of those members of the combined group that are not subject to taxation when they compute the sales factor percentage. So, for example, assume a California based unitary group has one corporation--Corporation A--that is subject to taxation in Minnesota. However, another member, Corporation B, is not subject to tax in Minnesota, but makes destination sales to customers in Minnesota. Under the Joyce rule, Minnesota would only use Corporation A’s sales to apportion income to Corporation A.

FinniganThe Finnigan rule uses all sales numerators of members of the combined group to apportion income to a state, regardless of whether each member is subject to taxation in that state. So, considering the example described above, both Corporation A's sales and Corporation B's sales made to customers in Minnesota would be used in determining the apportionment percentage for Corporation A, even though Corporation B is not subject to the Minnesota corporate franchise tax.

B. Case Law.

There are a number of cases governing the Finnigan and Joyce dichotomy. Finnigan/Joyce essentially involves the question on how to determine the California sales factor in context with combined income reporting in California.

In the Appeal of Joyce, Inc., 66 SBE 069 (November 23, 1966), the California State Board of Equalization ("BOE") ruled, inter alia, that Public Law 86-272 prohibited using sales to apportion income to California if the sales were made by a member of a unitary combined group that was exempt from taxation under Public Law 86-272.