Report & Accounts 2014 - Target Group

50

Report & Accounts 2014

Transcript of Report & Accounts 2014 - Target Group

Report & Accounts 2014

Contents5 CEO Statement

8 Our Board

10 Our Vision

12 Our Clients

14 Our Key Highlights

19 Directors’ Report

20 Strategic Report

23 Statement of directors’ responsibilities in respect of the Directors’ Report, Strategic Report and the financial statements

24 Independent auditor’s report to the members of Target Group Limited

28 Consolidated Profit and Loss Account

29 Consolidated Balance Sheet

30 Company Balance Sheet

31 Consolidated Cash Flow Statement

31 Reconciliation of net cash flow to movement in net debt

32 Notes

www.targetgroup.com

4

2014 has undoubtedly been a year of building momentum on our 2013 results as we continue to execute our strategic vision to be the software driven, service provider of choice for loans, investments and insurance.

During the year we achieved a number of significant milestones in the business including increasing the assets running on our systems to over £22 billion, bringing 4 million accounts under management and processing a record £5.5 billion worth of Direct Debits. Our workforce grew during the year to 543 in order to support this growth.

Ground-breaking year 2014 was a breakthrough year for us. We secured a number of major contracts covering a range of products and services and delivered on these successfully. This demonstrated our capability to deal with large scale projects and deliver new and innovative software and servicing solutions for our clients.

Highlights included: • Securing the contract to provide a hosted

payments processing solution with Concentrix, to support the DVLA with their introduction of Direct Debit payments for Vehicle Road Tax.

• Supporting a key client with a complex remediation programme for investment products. Within two weeks, we were able to mobilise a team of trained telephone staff to provide inbound call handling and outbound mailing activity for a significant number of customer accounts, in line with FCA requirements.

• Winning a number of new loan servicing contracts during the year. We succesfully migrated four portfolios onto our loan processing platform swiftly, efficiently and compliantly.

• Executing a major migration of structured products onto our platform.

• Delivering a new flexible accounting system to a leading bank to support its retail credit portfolio. Our new solution has transformed their finance team’s accounting processes providing much deeper levels of visibility into its portfolio and financial performance.

Our Growth StoryI am delighted to report that Target Group has had another year of strong growth which saw both our turnover and EBITDA improve significantly on last year with increases of 33% and 150% respectively.

Paddy Byrne Chief Exectutive Officer Target Group

5

www.targetgroup.com

Positioned well for the futureWe offer our clients a highly cost efficient and well governed servicing model. This is built on the economies of scale we are able to harness, underpinned by our own proprietary software, a wealth of experience across the workforce and regulatory permissions. These capabilities, combined with operational excellence and strong control environment, provide new entrants and established providers with speed to market not available by using in house solutions. Our experience in executing new launches and migrations ensures a manageable, low risk on boarding process for our clients.

The introduction of new requirements from the Financial Conduct Authority (FCA) in April 2014 means that the UK mortgage market is more regulated than it has ever been. We achieved a smooth transition to the new MMR regulations for our clients, having been ‘MMR ready’ well in advance of the deadline. Our understanding of the regulatory landscape, given the changes our business has already managed this

year (the Mortgage Market Review, OFT to FCA, changes to CCA and MCOB) puts us in a strong position for the implementation of the forthcoming European Mortgage Credit Directive (EMCD). Our focus is on ensuring we support our clients to operate compliantly and efficiently, as well as enabling them to bring products to market swiftly.

During the year we maintained our unrelenting focus on arrears management and loss mitigation delivering outstanding performance for our clients. This was achieved through our highly skilled teams using our state of the art in-house arrears management system. These attributes were recognised in the award of our new Standard & Poor’s Special Servicer rating.

During 2014, we significantly increased our capabilities as an organisation with a number of new joiners in key roles. These include Ian Larkin who joined us as Chief Financial Officer, Terry Baxter who joined as Director of Risk and Compliance, Ian Ferguson who joined as Director of Servicing and Buddy Willard as Director of Change.

Our Growth Story (continued)

6

Target Annual Report & Accounts 2014

In 2015 we will be moving into new markets including the design and distribution of Structured Products (Plan Management) through Intermediary channels. This will position us as both a product manufacturer and a provider of third party administration in this market. Mike Newman has joined us from Investec as Director of Structured Products to lead our entry into Plan Management.

The wider outlook for the Group is generally also encouraging. We are operating in a more benign market with the backdrop of an improving UK economy that has moved into sustainable growth. We have seen confidence return to the lending market, both on the part of lenders and consumers, which presents opportunities with both existing lenders and new entrants into the marketplace. We expect to see continued activity in the loan trading markets at levels near to 2014 and expansion of opportunity in the ‘Peer to Peer’ and unsecured lending markets where returns on capital and customer demand appear attractive. Our experience in these markets means we are well positioned to take advantage of such opportunities.

I would like to thank our growing number of clients for their continued confidence in Target. Our mission is to help our clients achieve their business goals and we have been delighted to play a part in some notable successes in 2014. All this could not have been achieved without our dedicated staff. I would like to thank all our teams for their continued hard work, passion and focus which has undoubtedly underpinned our success. I would also like to mention our investors, Pollen Street Capital who bring deep market knowledge to the company and who have worked tirelessly with us to continue to develop and grow the business.

This is certainly shaping up to be an exciting year and one where Target is very well placed to flourish. Based on all the solid foundations established in 2014, I look forward to 2015 and continuing our successful growth story.

Our mission is to help our clients achieve their business goals and we have been delighted to play a part in some notable successes in 2014.

7

www.targetgroup.com

Richard Houghton ChairmanRichard Houghton is Chairman of Target having joined in May 2012. In 1999 he was a founding director of Xchanging plc, the business process and technology services provider and integrator. For over 10 years he held senior roles including Chief Operating Officer, and more recently Chief Financial Officer. He led the successful flotation of the business on the London Stock Exchange in 2007.

James Scott Non-Executive DirectorJames has been with the Pollen Street Capital investment team since 2004 and has been originating and managing investments across various sectors. Over the last five years James has focused on investing in credit opportunities and Financial Services. Prior to his current role James worked for RBS and as a Commercial Director for a software engineering firm, in a consulting role for EY and qualified as a Chartered Accountant with PwC.

Paddy Byrne Chief Executive OfficerPaddy has over 20 years’ experience in senior management roles working in Financial Services, Government and Telecommunications, Before joining Target, Paddy held several senior roles within Xchanging plc where he achieved significant growth running first the Technology business and then taking overall control of the UK business providing business critical services to Lloyds of London and the London Metal Exchange amongst others. Paddy joined Xchanging from HMRC where he was Business Solutions Director and a member of the Technology Board. Prior to this Paddy was CIO at a number of large financial Institutions.

Our Board Target’s Board of Directors provides strategic direction and governance across our business in the UK, Australia and New Zealand.

8

Target Annual Report & Accounts 2014

Ian Larkin Chief Financial Officer Ian has over 20 years of Financial Services experience and has worked in leadership roles across Lloyds Banking Group, most recently as Managing Director of Lloyds Commercial Finance, the UK’s largest asset-based lender, and previously as Managing Director of Lloyds Consumer Banking. Before joining Lloyds Ian spent three years as Chief Financial Officer at Virgin Money and four years at McKinsey. Ian has a first class Degree in Chemical Engineering from University College Dublin, an INSEAD MBA and is a Fellow of the Chartered Institute of Management Accountants.

Bill Alley Group Chief Operating OfficerBill has over 25 years’ experience working within the Financial Services, Investment Banking and Insurance sectors. He has extensive C-level experience and has a strong strategic, operational and consulting background at major corporates delivering significant financial and service performance. He has a successful track record in leading technology driven organisations at Xchanging, Dun and Bradstreet, ING Barings and KPMG.

James Snow Group Sales DirectorJames’ experience spans over 23 years during which he has held a number of C level roles. Prior to joining Target, he ran the sales and marketing division of Rental Research and was National Sales Manager for Advanced Technologies International. Earlier in his career he held a systems and software finance sales consultancy role for ECS International, a subsidiary of Société Generale.

The Board 1. Richard Houghton 2. James Scott 3. Paddy Byrne 4. Ian Larkin 5. Bill Alley6. James Snow

1.

4.

2.

5.

3.

6.

9

www.targetgroup.com

Lending

Investments

Insurance

Our markets

Our VisionThe software driven service provider of choice for loans, investments and insurance.

Managed

Services

BPO

Software

Our services

Our ClientsOver 50 major financial institutions rely on us to manage their lending, investment and insurance business. Below are some of our clients we support across our offerings.

12

Target Annual Report & Accounts 2014

Sammy Talker Head of Change

13

www.targetgroup.com

33%

29%

150%EBITDA

£2.2m£5.5m

ASSETS SERVICED ON OUR SYSTEMS

£17bn£22bn

TURNOVER

£34.7m£46.1m

EMPLOYEES AT END OF THE YEAR

5085437%

2013

2014

Our Key HighlightsINCREASE

14

Target Annual Report & Accounts 2014

£5.5 bn

4million

£400

£1billionInvestments matured

Worth of Direct Debits processed on our systems in 2014

Accounts under management

million arrears collected

Jayde Davies Client Development Manager

15

www.targetgroup.com

New Special Servicer rating achievedIn 2014, we achieved a Standard & Poor’s Special Servicer rating of “Average” at our first attempt, whilst also maintaining our “Above Average” rating for primary servicing. Our overall rating reflects us as an innovative and well-established business with strong customer service and client engagement, alongside a robust, stable and flexible IT platform.

Shortlisted for an industry awardIn December we were shortlisted for the FS Tech award for “Best use of IT in Retail Banking and Insurance” for our work with Welcome Finance. Through implementing our account and arrears management system, we have enabled Welcome Finance to reduce its annual IT costs from £7.5million to £2.5million, significantly mitigate risk and reduce its IT headcount from 42 to 9, for a fee that was nearly 12% below the original budget.

Shawbrook extend contractWe began our relationship with what is now Shawbrook Bank in 2010, servicing their secured loan portfolio. Since then, as the Bank has grown, we have added the servicing of Commercial and Unsecured Consumer loans to the Secured portfolio, enhancing our business partnership and entered into a new 5 year contract in December 14.

We entered the payment processing market with the DVLA contractOn October 1st 2014 the Government introduced legislation to reduce tax administration costs through the removal of the paper tax disc and allowing payments by Direct Debit annually, bi-annually or monthly. We were delighted to work with Concentrix to support the DVLA initiative by supplying a solution to set up and manage ongoing Direct Debit payments.

Our Key Highlights (continued)

16

Target Annual Report & Accounts 2014

New key appointmentsDuring 2014, we made a number of additional appointments with a view to enhancing our business leadership and underpinning our ambitious growth plans. Key appointments include:

1. Ian Larkin, Chief Financial Officer. Brings over 20 years’ experience to the team including leadership roles at Lloyds and Virgin Money.

2. Terry Baxter Director of Risk and Compliance. Terry has spent over 20 years’ in senior compliance and regulatory roles at Grant Thornton and the FSA.

3. Buddy Willard, Director of Change has previously spearheaded change across businesses including GE Capital and JP Morgan.

4. Ian Ferguson, Director of Servicing brings over 30 years’ experience from companies including Zurich, Kensington Mortgages and more recently GE Money Home Lending.

5. Mike Newman, Director of Structured Products, Mike brings over 27 years of experience in investment banking including senior roles at Investec and BNP Paribas.

Launching our remediation servicesWe supported a number of our clients with the delivery of large scale remediation programmes in response to regulatory reviews or enforcement. We delivered these projects quickly whilst providing robust and compliant end to end solutions underpinned by our regulatory understanding and expertise.

Cultural Change2014 has seen the initiation of a company-wide Cultural Change Programme focusing on the values and behaviours which will make growth and success achievable as one team. We recognise our people are our greatest asset and this programme creates a strong platform for future growth. This journey will continue into 2015 as we further embed these values and behaviours into everything that we do.

Our PeopleWe are committed to providing high quality, innovative learning & development opportunities for all our staff and as a reflection of this, we have been awarded the Investors in People accreditation. We have invested significantly in the acquisition and development of key talent with the continuation of our management graduate scheme as well as recruiting new graduates into developmental roles. We are also developing our future senior leaders through a high potential leadership programme, equipping them with the skills they need to exhibit to drive Target’s ambitious growth trajectory.

Helping our communityEach year our team selects our annual charity via our employee opinion survey and in 2014 they chose Macmillan Cancer Care. Our people worked tirelessly to raise over £15,000. In the last ten years they have contributed to raising over £100,000 through fundraising activities such as The Three Peaks UK, Cardiff to Paris Bike ride and climbing Mount Kilimanjaro. We also operate a charitable payroll giving programme and regular blood donation drives.

Enhanced Data Analytics capabilityIn 2014, we further developed our data analytics capability with some key hires and investment in MI infrastructure to enhance our client support through improved internal process insight and control. This has also enabled us to offer clients improved portfolio value / risk mitigation through predictive analytics supporting portfolio strategy decisions.

DATA ANALYTICS

Driving business results through data

www.targetgroup.com

of the world’s top 20 banks rely on Target

17

www.targetgroup.com

Neil Andrews Operational Trainer

18

Target Annual Report & Accounts 2014

In accordance with Section 414C (11) of the Companies Act 2006, certain information around the trading activities of the group are contained within the Strategic Report.

Results and dividendsThe Group’s results are set out in the consolidated profit and loss account on page 28.

The directors do not recommend the payment of a dividend for the year (2013: £Nil).

Directors The directors who held office during the year were as follows:

P.Byrne J.Hunt, resigned 16 October 2014 R. Houghton J.R.B. Snow W.M.Alley, appointed 1 March 2014 I.D. Larkin, appointed 23 October 2014

DonationsNo political donations were made (2013: £Nil).

Disclosure of information to auditorThe directors who held office at the date of approval of this directors’ report confirm that, so far as they are each aware, there is no relevant audit information of which the company’s auditor is unaware; and each director has taken all the steps that he ought to have taken as a director to make himself aware of any relevant audit information and to establish that the company’s auditor is aware of that information.

AuditorPursuant to Section 487 of the Companies Act 2006, the auditor will be deemed to be reappointed and KPMG LLP will therefore continue in office.

By order of the board

I.D. Larkin, Director 11 March 2015

Directors’ ReportThe directors present their annual report, the strategic report and the audited financial statements for the year ended 31 December 2014.

Target HouseCowbridge Road EastCardiff CF11 9AU

Registered number 1208137

19

www.targetgroup.com

Principal activities and financial reviewThe principal activity of the Group is the provision of software and servicing solutions to the financial services sector. Our solutions are provided as software licence and related services sales or as services under IT hosting and business process outsourcing contracts. We have 36 years of experience and work with over 50 major financial institutions including a number of the top 20 global banks.

Our platform now supports over £22bn of business on behalf of our clients, comprising some £7bn under Third Party Administration and £15bn of financial services running on our software platform.

Financial reviewTurnover increased by 33.1% (2013: 12.5%) from £34,655,000 in year ended 31 December 2013 to £46,125,000 in the year ended 31 December 2014.

The group earnings before interest, tax, depreciation and amortisation of goodwill (EBITDA) was £5,496,000 (2013: £2,224,000) as follows:

The increases in both EBITDA and turnover are attributable to a number of factors. Projects that were delivered in 2013 went live in 2014 generating excellent revenue streams and cash. In 2014, several new client wins throughout the year have contributed to our profit increase including the provision of a hosted payments processing solution for the DVLA in partnership with Concentrix supporting the phase out of the road tax disc.

Increased change control income was generated from existing clients in relation to remediation services and other value-add activities undertaken on their behalf. We supported a key software client with the implementation of a new accounting system; completed a large remediation exercise on behalf of one of our main Investment clients; and off boarded a substantial loan portfolio on behalf of a major bank to a third party within extremely challenging timescales.

Strategic Report

Year ended31 December

2014

Year ended31 December

2013

£000 £000

Operating Profit 3,513 387

Depreciation (note 10) 1,541 1,395

Amortisation (note 9) 442 442

EBITDA 5,496 2,224

20

Target Annual Report & Accounts 2014

The business was also able to lower its cost base as a percentage of revenue through greater efficiencies from resource utilisation and economies of scale in property and system costs as more clients were serviced.

2014 marked our first full year of portfolio ownership under our brand Elderbridge Limited, the beneficial interest of which sits in Target Financial Systems Limited. Turnover increased from £139,000 in 2013 to £1,906,000 in 2014.

Business PerformanceWe achieved a Special Servicer rating of “Average” from Standard and Poor’s at our first attempt. We also maintained its Above Average rating for Primary Servicing. The overall ranking reflects Standard and Poor’s view of the business as a well-established business with strong customer service and client engagement, alongside a robust, stable and flexible IT platform.

Contributing to a successful year was the appointment of key individuals into the senior leadership team including Ian Larkin as Chief Financial Officer, Terry Baxter as Risk & Compliance Director, David Tweedy as Market Relations Director, and Buddy Willard as Director of Change.

Risks and Uncertainties Most of our clients are blue chip investment, retail banking, finance and insurance companies, which represent a low credit risk.

There is a moderate interest rate risk to the Group arising from the revolving credit facility.

While the Group has exposure to exchange rate fluctuations due to its operations in Australia, New Zealand, and the Euro zone, this is limited due to a natural hedge, in that revenues are largely offset by expenditure in the local currencies.

21

www.targetgroup.com

Our marketsOur clients are predominantly providers of lending, investments and insurance products. We service these markets through three key offerings; Business Process Outsourcing (BPO), managed services (incorporating hosted services) and software. These services are supported by our professional services and consultancy across all our markets.

Corporate Social Responsibility In 2014 we continued to support our annual charity, raising over £15,000 for MacMillan Cancer Support. Our team also contributed via charitable payroll giving, to a number of food banks and through the blood donation drive. In our Cardiff headquarters we reduced our general waste and increased our recycling by 55%. The community and team spirit that we have built through our volunteering efforts has become an essential part of our DNA.

PeopleThe average number of colleagues fell marginally in the period from 529 to 528. Although we have seen a ramp up in recruitment during the latter part of 2014, the 2013 average headcount factored in a reduction in the number of colleagues at one of our sites part way through the year. The graduate management scheme continued and a further 3 graduates joined the team. In our recent annual employee opinion survey 80% of our team indicated they would recommend Target as a great place to work.

In the latter part of 2014 a culture change programme saw the launch of a new set of values and underpinning behaviours which Target believe will be a key enabler in the pursuit of achieving our vision as we continue to build on our successes of 2014.

Disabled employeesApplications for employment by disabled persons are always fully considered, bearing in mind the aptitude of the applicant concerned. In the event of members of staff becoming disabled, every effort will be made to ensure their employment with the company continues and that the training, career development and promotion of disabled persons should, as far as possible, be identical with that of other employees.

OutlookWe are in an excellent position to capitalise on opportunities arising in the coming year, both from existing clients as they look to add to and develop their serviced portfolios and software solutions, and to new client and market prospects opening up following key appointments to the senior management team and our continued aggressive growth plan.

By order of the board

I.D. Larkin, Director 11 March 2015

Strategic Report (continued)

22

Target Annual Report & Accounts 2014

Statement of directors’ responsibilities in respect of the Directors’ Report, Strategic Report and the financial statements

The directors are responsible for preparing the Directors’ Report, Strategic Report and the financial statements in accordance with applicable law and regulations.

Company law requires the directors to prepare financial statements for each financial period. Under that law they have elected to prepare the group and parent company financial statements in accordance with UK Accounting Standards and applicable law (UK Generally Accepted Accounting Practice).

Under company law the directors must not approve the financial statements unless they are satisfied that they give a true and fair view of the state of affairs of the group and parent company and of their profit or loss for that period. In preparing each of the group and parent company financial statements, the directors are required to:

• select suitable accounting policies and then apply them consistently;

• make judgments and estimates that are reasonable and prudent;

• state whether applicable UK Accounting Standards have been followed, subject to any material departures disclosed and explained in the financial statements;

• prepare the financial statements on the going concern basis unless it is inappropriate to presume that the group and the parent company will continue in business.

The directors are responsible for keeping adequate accounting records that are sufficient to show and explain the parent company’s transactions and disclose with reasonable accuracy at any time the financial position of the parent company and enable them to ensure that its financial statements comply with the Companies Act 2006. They have general responsibility for taking such steps as are reasonably open to them to safeguard the assets of the group and to prevent and detect fraud and other irregularities.

The directors are responsible for the maintenance and integrity of the corporate and financial information included on the company’s website. Legislation in the UK governing the preparation and dissemination of financial statements may differ from legislation in other jurisdictions.

23

www.targetgroup.com

We have audited the financial statements of Target Group Limited for the year ended 31 December 2014 set out on pages 28 to 50. The financial reporting framework that has been applied in their preparation is applicable law and UK Accounting Standards (UK Generally Accepted Accounting Practice).

This report is made solely to the company’s members, as a body, in accordance with Chapter 3 of Part 16 of the Companies Act 2006. Our audit work has been undertaken so that we might state to the company’s members those matters we are required to state to them in an auditor’s report and for no other purpose. To the fullest extent permitted by law, we do not accept or assume responsibility to anyone other than the company and the company’s members, as a body, for our audit work, for this report, or for the opinions we have formed.

Respective responsibilities of directors and auditorsAs explained more fully in the Directors’ Responsibilities Statement set out on page 23, the directors are responsible for the preparation of the financial statements and for being satisfied that they give a true and fair view. Our responsibility is to audit the financial statements in accordance with applicable law and International Standards on Auditing (UK and Ireland). Those standards require us to comply with the Auditing Practices Board’s (APB’s) Ethical Standards for Auditors.

Independent auditor’s report to the members of Target Group Limited

KPMG LLP3 Assembly SquareBritannia QuayCardiff BayCF10 4AXUnited Kingdom

24

Target Annual Report & Accounts 2014

Scope of the audit of the financial statementsA description of the scope of an audit of financial statements is provided on the Financial Reporting Council’s web-site at www.frc.org.uk/auditscopeukprivate.

Opinion on financial statementsIn our opinion the financial statements:

• give a true and fair view of the state of the group’s and the parent company’s affairs as at 31 December 2014 and of the group’s profit for the year then ended;

• have been properly prepared in accordance with UK Generally Accepted Accounting Practice; and

• have been prepared in accordance with the requirements of the Companies Act 2006.

Opinion on other matter prescribed by the Companies Act 2006In our opinion the information given in the Directors’ Report and Strategic Report for the financial year for which the financial statements are prepared is consistent with the financial statements.

Matters on which we are required to report by exceptionWe have nothing to report in respect of the following matters where the Companies Act 2006 requires us to report to you if, in our opinion:

• adequate accounting records have not been kept by the parent company, or returns adequate for our audit have not been received from branches not visited by us; or

• the parent company financial statements are not in agreement with the accounting records and returns; or

• certain disclosures of directors’ remuneration specified by law are not made; or

• we have not received all the information and explanations we require for our audit.

By order of the board

Emma Holiday, (Senior Statutory Auditor)

18 March 2015

for and on behalf of KPMG LLP, Statutory Auditor Chartered Accountants

25

www.targetgroup.com

AccountsYear ended 31 December 2014

Note Year ended31 December 2014

Year ended31 December 2013

£000 £000

Turnover 2 46,125 34,655

Cost of Sales (31,962) (27,052)

Gross Profit 14,163 7,603

Administrative expenses (10,650) (7,216)

Operating profit 3,513 387

Interest payable and similar charges 3 (419) -

Interest receivable and similar income 3 - 430

Profit on ordinary activities before taxation 5 3,094 817

Tax (charge)/credit on profit on ordinary activities 8 (1,334) 1,033

Profit on ordinary activities after taxation 17 1,760 1,850

Consolidated Profit and Loss Accountfor the year ended 31 December 2014

Turnover and operating profit relate entirely to continuing operations.

The above results represent the total recognised gains and losses for both financial years.

28

Note Year ended31 December 2014

Year ended31 December 2013

£000 £000 £000 £000

Fixed assets

Goodwill 9 922 1,364

Tangible assets 10 4,331 2,666

5,253 4,030

Current assets

Debtors – due within one year 12 9,961 9,305

Debtors – due after one year 7,507 11,306

17,468 20,611

Cash at bank and in hand 4,626 3,703

22,094 24,314

Creditors: amounts falling due within one year 13 (13,753) (15,379)

Net current assets 8,341 8,935

Total assets less current liabilities 13,594 12,965

Creditors: amounts falling due after more than one year

14 (10,250) (11,381)

Net assets 3,344 1,584

Capital and reserves

Called up share capital 16, 17 810 810

Share premium account 17 501 501

Capital redemption reserve 17 68 68

Profit and loss account 17 1,965 205

Surplus on equity shareholders’ funds 17 3,344 1,584

Consolidated Balance Sheetat 31 December 2014

These financial statements were approved by the board of directors on 11 March 2015 and were signed on its behalf by:

I.D. Larkin, Director

29

Company Balance Sheetat 31 December 2014

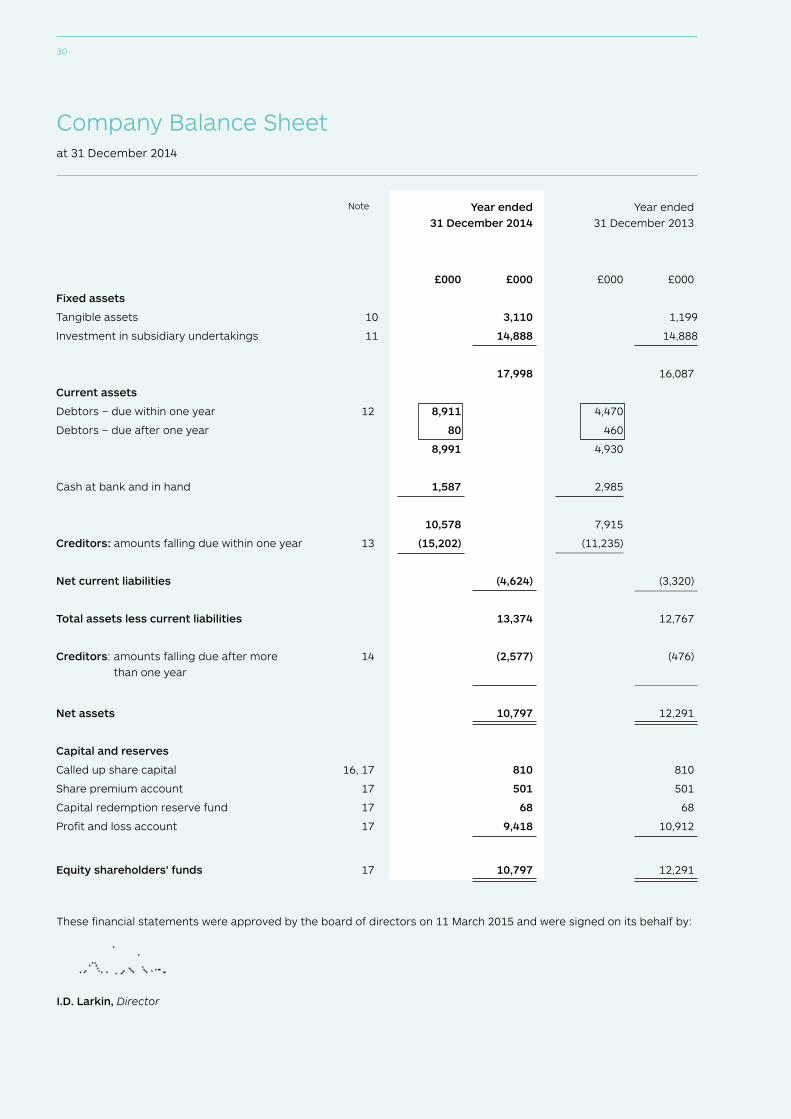

Note Year ended31 December 2014

Year ended31 December 2013

£000 £000 £000 £000

Fixed assets

Tangible assets 10 3,110 1,199

Investment in subsidiary undertakings 11 14,888 14,888

17,998 16,087

Current assets

Debtors – due within one year 12 8,911 4,470

Debtors – due after one year 80 460

8,991 4,930

Cash at bank and in hand 1,587 2,985

10,578 7,915

Creditors: amounts falling due within one year 13 (15,202) (11,235)

Net current liabilities (4,624) (3,320)

Total assets less current liabilities 13,374 12,767

Creditors: amounts falling due after more than one year

14 (2,577) (476)

Net assets 10,797 12,291

Capital and reserves

Called up share capital 16, 17 810 810

Share premium account 17 501 501

Capital redemption reserve fund 17 68 68

Profit and loss account 17 9,418 10,912

Equity shareholders’ funds 17 10,797 12,291

These financial statements were approved by the board of directors on 11 March 2015 and were signed on its behalf by:

I.D. Larkin, Director

30

Consolidated Cash Flow Statementfor the year ended 31 December 2014

Reconciliation of net cash flow to movement in net debtfor the year ended 31 December 2014

Note Year ended31 December 2014

Year ended31 December 2013

£000 £000

Net cash inflow/(outflow) from operating activities 20 5,773 (5,611)

Returns on investments and servicing of finance 22 (203) (222)

Taxation (7) 25

Capital expenditure and financial investment 22 (799) (803)

Net cash inflow/(outflow) before use of liquid resources and financing

4,764 (6,611)

Financing 22 (3,841) 10,516

Increase in cash in the year 923 3,905

Note Year ended31 December 2014

Year ended31 December 2013

£000 £000

Increase in cash in the year 21 923 3,905

Cash outflow from repayment hire purchase and finance leases

21 659 949

Cash outflow from repayment of bank facility 21 3,182 -

New bank facility - (10,516)

Decrease/(increase) in net debt arising from cash flows

4,764 (5,662)

Non-cash changes - new hire purchase and finance lease obligations

(2,395) -

Net debt at beginning of the year 21 (10,816) (5,154)

Net debt at end of the year 21 (8,447) (10,816)

31

1. Accounting policies

The following accounting policies have been applied consistently in dealing with items which are considered material in relation to the financial statements of the company and the group.

Basis of preparation The financial statements have been prepared in accordance with applicable accounting standards and under the historical cost accounting rules, and with the requirements of the Companies Act 2006.

Going Concern The directors have presented the financial statements on the going concern basis.

This is predominantly because the directors expect the Group to sustain profitable trading and cash flows and trading to date in 2015 is showing the Group in a strong position in terms of both profits and cash flow.

The directors have prepared forecasts including cash flow information for the year ending 31 December 2016. On the basis of these forecasts and discussions with the group’s bankers, the directors consider that the group will continue to operate within the facility currently agreed.

Notwithstanding Company’s net current liabilities of £4,624,000, the directors have presented the financial statements on the going concern basis.

It is also their opinion that a subsidiary company will provide funding necessary if it is required to support the business to meets its obligations as they fall due for at least 12 months from the date of approval of the financial statements. This is based on a confirmation that support will be available if required for at least twelve months from the date of the approval of these financial statements.

Basis of consolidationThe consolidated financial statements incorporate the financial statements of the company and all its subsidiary undertakings made up to 31 December 2014. The acquisition method of accounting has been adopted. Under this method, the results of subsidiary undertakings acquired or disposed of in the year are included in the consolidated profit and loss account from the date of acquisition to the date of disposal.

The Company is a wholly owned subsidiary of Target Topco Limited, the Company has taken advantage of the exemption contained in FRS 8 and has therefore not disclosed transactions or balances with entities which form part of the group. The consolidated financial statements of Target Topco Limited, within which this Company is included, can be obtained from the address provided in Note 24.

Goodwill Purchased goodwill is capitalised at cost.

Goodwill on consolidation, arising on the acquisition of subsidiary undertakings, represents the excess of the fair value of the consideration given over the fair value of the separable net assets acquired, less any provision for impairment.

Both are capitalised within fixed assets and are amortised on a straight line basis over their estimated useful economic lives.

The directors consider each acquisition separately for the purpose of determining the amortisation period, being the period over which the directors estimate that economic benefit will continue to be derived from the purchase, as follows:

Notes(forming part of the financial statements)

32

Purchased goodwill 5 years

Goodwill on consolidation arising on acquisition of subsidiary undertakings 5 – 10 years

Investment in subsidiariesIn the Company’s financial statements, investments in subsidiary undertakings are stated at cost less any provision for impairment.

Turnover and revenue recognitionTurnover represents the amounts, excluding value added tax, derived from the provisions of solutions to third party customers. Solutions can be provided in three ways: as software licence and related service sales, under facilities management contracts and under business process outsourcing contracts.

Sales of proprietary software systems licences and enhancements to software systems Revenue from licence agreements for the delivery of software that does not require significant production or enhancement is recognised when, for this delivery, all the following are met:

• persuasive evidence of an arrangement exists;

• delivery of software has occurred;

• there are no significant remaining vendor obligations;

• the vendor’s fee is fixed or determinable; and

• collectability is probable.

Licence agreements and enhancements to software systems where production or enhancement is significant are treated as long term contracts and revenue is recognised in accordance with SSAP 9. Revenue is credited to turnover at cost appropriate to the stage of completion plus attributable profits, less amounts recognised in previous periods. Profit attributable to the stage of completion of a contract is only recognised when the outcome of the contract can be foreseen with reasonable certainty. Provision is made for any losses as soon as they are foreseen.

Amounts recoverable on contracts are included in debtors and represent revenue earned in excess of payments on account. Amounts invoiced in excess of revenue earned are included in creditors and represent deferred income.

MaintenanceRevenue received under maintenance contracts is credited to turnover on a straight-line basis over the period in which it is earned.

Facilities management contractsA facilities management contract typically contains a number of elements such as licence fees, enhancements, maintenance and facilities management services. The income arising from each of the elements of such a contract is treated in the same way as it would be were it made directly, as set out above. Licence fees and enhancements are accounted for in line with the methods described in the previous paragraphs, whereas the income from maintenance and facilities management services, which are delivered over the term of the contract, will be recognised equally over that term.

33

1. Accounting policies (continued)

Facilities management contracts (continued)• Where these figures are not separately identified in the contract then estimated figures are calculated using the

following assumptions:

• facilities management income is based upon staff costs included at charge rate and an allocation of relevant overheads;

• enhancement income is based upon specific estimates to complete, valued at charge rate;

• maintenance income is based upon the same ratio of maintenance to licence revenue as when these are sold directly;

• licence fee income is calculated as the remaining income released over the term of the contract.

Business process outsourcing (servicing) contractsRevenue received under loan servicing and other business process outsourcing contracts is recognised as turnover in the period that the servicing is carried out. All existing servicing contracts provide for charging clients on a monthly basis, either by reference to the portfolio size or according to a fixed fee structure.

Costs incurred in advance of the commencement of live servicing (net of upfront implementation fees received) which are recoverable over the period of the initial contract are shown as debtors within “other amounts recoverable on contracts” and amortised over the initial contract life. Costs which are not recoverable are fully expensed in the period incurred.

Services incomeShort-term service revenues such as training, consultancy, and installation revenues are recognised once the service has been delivered.

Tangible fixed assets and depreciationDepreciation is provided to write off the cost less the estimated residual value of tangible fixed assets by equal instalments over their estimated useful economic lives from the point they are brought into use as follows:

Short leasehold property the term of the lease

Computer equipment 3-7 years

Fixtures and fittings 3-10 years

Motor vehicles 2-4 years

Owned Loan Portfolio Owned Loan portfolios acquired from third parties are recognised at fair value, being purchase consideration payable, plus transaction costs. Thereafter all loans are valued at amortised cost with the Effective Interest Rate (‘EIR’) method. The EIR method spreads the expected net income arising from a loan over its expected life. The EIR is that rate of interest which, at inception, exactly discounts the future cash payments and receipts arising from the loan to the initial carrying amount.

The loan balances are reviewed for impairment annually and written down using an impairment provision where required.

Notes (continued)

(forming part of the financial statements)

34

Leasing and hire purchase obligationsAssets held under finance leases, which are leases where substantially all the risks and rewards of ownership of the asset have passed to the company, and hire purchase contracts are capitalised in the balance sheet and depreciated over their estimated useful lives. The capital elements of future obligations under the leases and hire purchase contracts are included as liabilities in the balance sheet.

The interest elements of the rental obligations are charged in the profit and loss account over the periods of the leases and hire purchase contracts and represent a constant proportion of the balance of capital repayments outstanding.

Rentals payable under operating leases are charged in the profit and loss account on a straight line basis over the lease term.

Foreign currenciesTransactions in foreign currencies are translated at the exchange rate ruling at the date of the transaction. Monetary assets and liabilities in foreign currencies are translated at the rates of exchange ruling at the balance sheet date. All exchange differences are dealt with through the profit and loss account.

For consolidation purposes, the assets, liabilities and profit and loss accounts of overseas subsidiary undertakings are translated at the closing rate (for balance sheet items) and average rate (for profit and loss items). Exchange differences arising on these translations are taken directly to reserves.

Research and software developmentResearch and software development costs are written off against revenue as and when incurred other than as described above for system enhancement and development for a customer.

TaxationThe (charge)/credit for taxation is based on the result for the year and takes into account taxation deferred because of timing differences between the treatment of certain items for taxation and accounting purposes.

Deferred tax is recognised, without discounting, in respect of all timing differences between the treatment of certain items for taxation and accounting purposes which have arisen but not reversed by the balance sheet date, except as otherwise required by FRS 19. Deferred tax assets are recognised as recoverable to the extent that, on the basis of all available evidence, it can be regarded as more likely than not that there will be suitable taxable profits from which the future reversal of underlying timing differences can be deducted.

Financial instrumentsFollowing the adoption of FRS 25, financial instruments issued by the Group are treated as equity (i.e. forming part of shareholders’ funds) only to the extent that they meet the following two conditions:

a) they include no contractual obligations upon the Company (or Group as the case may be) to deliver cash or other financial assets or to exchange financial assets or financial liabilities with another party under conditions that are potentially unfavourable to the Company (or Group); and

b) where the instrument will or may be settled in the Company’s own equity instruments, it is either a non-derivative that includes no obligation to deliver a variable number of the Company’s own equity instruments or is a derivative that will be settled by the Company’s exchanging a fixed amount of cash or other financial assets for a fixed number of its own equity instruments.

PensionThe group makes pension contributions on behalf of employees to their individual pension plans. The amount charged against profit represents the contributions payable in respect of the accounting period.

35

2. Segmental information

Turnover by destination was UK £44,914,000 (2013: £31,068,000) and rest of the world £1,211,000 (2013: £3,587,000).

The table below sets out information for each of the group’s industry segments:

Amortisation of the goodwill arising from the acquisition of Harlosh is included in the Software segment.

3. Interest payable/(receivable) and similar charges

The other charges credit in 2013 included interest accrued in prior years which was waived by the immediate holding company.

Software Services Total

2014 2013 2014 2013 2014 2013

£000 £000 £000 £000 £000 £000

Turnover 14,483 12,735 31,642 21,920 46,125 34,655

Year ended31 December 2014

Year ended31 December 2013

£000 £000

Bank interest and charges 55 61

Hire purchase and finance interest 55 75

Loan interest 161 174

Other charges 148 (740)

419 (430)

Notes (continued)

(forming part of the financial statements

36

Number of employees

Year ended31 December 2014

Year ended31 December 2013

Technical and operational 459 444

Sales, marketing, management and administration 69 85

528 529

Year ended31 December 2014

Year ended31 December 2013

£000 £000

Profit on ordinary activities before taxation is stated after charging/(crediting):

Depreciation (note 10)

Owned 686 857

Leased 855 538

Profit on disposal of fixed assets (13) (9)

Amortisation of goodwill 442 442

Rentals under operating leases - property 870 887

Auditor’s remuneration:

Audit of these financial statements 18 30

Audit of financial statements of other group companies pursuant to legislation

30 36

Other services relating to taxation - 30

Year ended31 December 2014

Year ended31 December 2013

£000 £000

Wages and salaries 16,316 16,799

Social security costs 2,222 2,335

Pension costs 1,118 891

19,656 20,025

4. Staff numbers and costs

The average number of persons employed by the Group (including directors) during the year, analysed by category, was as follows:

5. Profit on ordinary activities before taxation

The aggregate payroll costs of these persons were as follows:

Auditor’s remuneration in respect of the company was £18,000 (2013: £30,000). Audit of other group companies relates to the audit fees for the subsidiaries Harlosh Limited, Target Servicing Limited, Target Financial Systems Limited, Target Financial Solutions Limited and Elderbridge Limited and the parent companies Robin TG Investments Limited and Target Topco Limited.

37

6. Profit and loss account of parent company

As permitted by Section 408 of the Companies Act 2006, the profit and loss account of the parent company is not presented as part of these financial statements. The parent company’s loss after taxation for the financial period was £1,494,000 (2013:£1,820,000).

7. Directors’ remuneration

Emoluments of the directors were as follows:

The aggregate of emoluments of the highest paid director were £274,000 (2013:£236,000) and company pension contributions of £14,000 (2013: £14,000) were made to a money purchase pension plan on his behalf. Retirement benefits are paid for 5 directors (2013: 4 directors) under their individual money purchase pension plans.

8. Taxation

The tax (charge)/credit for the year comprises:

Year ended31 December 2014

Year ended31 December 2013

£000 £000

Directors’ emoluments 1,088 718

Company contributions to money purchase pension scheme 36 128

1,124 846

Year ended31 December 2014

Year ended31 December 2013

£000 £000

Current tax:

Tax in foreign subsidiary - (4)

Prior year tax adjustment 80 -

Total current tax credit/(charge) 80 (4)

Deferred tax:

Origination and reversal of timing differences (note 15) (1,414) 1,037

Tax (charge)/credit on profit on ordinary activities (1,334) 1,033

Notes (continued)

(forming part of the financial statements)

38

8. Taxation (continued)

The current tax credit is lower (2013: lower) than the standard rate of corporation tax in the UK of 21.5% (2013: 23.25%) as explained below:

A reduction in the rate from 24% to 23% (effective 1 April 2013) was substantively enacted on 3 July 2012. Further reductions to 21% (effective from 1 April 2014) and 20% (effective from 1 April 2015) were substantively enacted 2 July 2013. This will reduce the company’s future current tax charge accordingly.

Year ended31 December 2014

Year ended31 December 2013

£000 £000

Profit on ordinary activities before tax 3,094 817

Profit at 21.5% (2013:23.25%) 665 188

Expenses not deductible for tax purposes 92 3

Difference between depreciation and capital allowances (114) 222

Losses arising in current period carried forward 528 -

Losses utilised (1,141) (413)

Other (30) 8

Overseas taxation - (4)

Prior year movement (80) -

Current period (credit)/charge as above (80) 4

9. Goodwill

£000

Group

Cost

At 1 January 2014 and 31 December 2014 5,141

Amortisation

At 1 January 2014 3,777

Charge for the year 442

At 31 December 2014 4,219

Net book value

At 31 December 2014 922

At 31 December 2013 1,364

39

Group

Shortleaseholdproperty

Computerequipment

Fixtures and fittings

Motorvehicles

Total

£000 £000 £000 £000

Cost

At 1 January 2014 100 10,701 612 110 11,523

Additions 153 3,000 53 - 3,206

Disposals - - - (66) (66)

At 31 December 2014 253 13,701 665 44 14,663

Depreciation

At 1 January 2014 100 8,074 590 93 8,857

Charge for the year 8 1,513 12 8 1,541

Disposals - - - (66) (66)

At 31 December 2014 108 9,587 602 35 10,332

Net book value

At 31 December 2014 145 4,114 63 9 4,331

At 31 December 2013 - 2,627 22 17 2,666

10. Tangible fixed assets

Included in tangible fixed assets of the group are assets held under hire purchase and finance lease agreements with a cost and net book value at 31 December 2014 of £4,953,000 and £2,790,000 respectively (2013: £2,558,000 and £1,249,000 respectively). The associated depreciation for the year on those assets was £855,000 (2013: £737,000).

Notes (continued)

(forming part of the financial statements)

40

Company Shortleaseholdproperty

Computerequipment

Fixtures and fittings

Motorvehicles

Total

£000 £000 £000 £000

Cost

At 1 January 2014 100 6,097 552 95 6,844

Additions 153 2,425 55 - 2,633

Disposals - - - (51) (51)

At 31 December 2014 253 8,522 607 44 9,426

Depreciation

At 1 January 2014 100 4,923 544 78 5,645

Charge for the year 8 690 16 8 722

Disposals - - - (51) (51)

At 31 December 2014 108 5,613 560 35 6,316

Net book value

At 31 December 2014 145 2,909 47 9 3,110

At 31 December 2013 - 1,174 8 17 1,199

10. Tangible fixed assets (continued)

Included in tangible fixed assets of the company are assets held under hire purchase and finance lease agreements with a cost and net book value at 31 December 2014 of £1,924,000 and £629,000 respectively (2013: £877,000 and £352,000 respectively). The associated depreciation for the period on those assets was £512,000 (2013: £241,000).

41

11. Investment in subsidiary undertakings

The company’s wholly owned subsidiaries at 31 December 2014 were:

Company £000

Cost

At 1 January 2014 and 31 December 2014 17,976

Provisions

At 1 January 2014 and 31 December 2014 3,088

Net book value

At 31 December 2014 and 31 December 2013 14,888

Country ofincorporation

Principalactivity

Subsidiary undertakings

Target Servicing Limited United Kingdom Provision of business process outsourced services

100%

Harlosh Limited United Kingdom Provision of computer applications software and related services

100%

Harlosh NewZealand Limited New Zealand Provision of computer applications software and related services

100%

Target Financial Systems Limited United Kingdom Management of owned loan portfolios

100%

Target Financial Solutions Limited United Kingdom Consultancy Services 100%

Target Computer Group Limited United Kingdom Dormant 100%

Target Group Trustee Company Limited United Kingdom Dormant 100%

Elderbridge Limited United Kingdom Lender of record for loan portfolios 100%

Notes (continued)

(forming part of the financial statements)

42

12. Debtors

Group Company

2014 2013 2014 2013

£000 £000 £000 £000

Trade debtors 1,969 1,682 1,019 818

Owned Loan Portfolio ** 10,069 12,284 - -

Services delivered payable by instalments ** 398 200 398 200

Other amounts recoverable on contracts ** 1,411 2,486 304 190

Other debtors 118 496 2 71

Prepayments and accrued income 3,001 1,730 978 598

Deferred tax asset (note 15) ** 319 1,733 - 517

Amounts due to parent undertakings 183 - 183 -

Amounts due from subsidiary undertakings - - 6,107 2,536

17,468 20,611 8,991 4,930

Group Company

2014 2013 2014 2013

£000 £000 £000 £000

Services delivered payable by instalments 80 42 80 42

Owned Loan Portfolio 6,715 9,571 - -

Other amounts recoverable on contracts 502 973 - -

Deferred tax (note 15) 210 720 - 418

7,507 11,306 80 460

** Included in the above figures are the following amounts due after more than one year:

43

13. Creditors: amounts falling due within one year

14. Creditors: amounts falling due after more than one year

Group Company

2014 2013 2014 2013

£000 £000 £000 £000

Obligations under finance leases 991 507 980 466

Revolving credit facility - HSBC 3,000 3,000 3,000 3,000

Trade creditors 1,086 2,614 423 1,309

Corporation tax 1 88 - 8

Other taxes and social security costs 1,345 1,435 513 773

Other creditors 161 134 161 132

Accruals and deferred income 5,050 5,606 2,241 2,035

Amounts due to subsidiary undertakings - - 5,765 1,517

Amounts due to parent undertaking 2,119 1,995 2,119 1,995

13,753 15,379 15,202 11,235

Group Company

2014 2013 2014 2013

£000 £000 £000 £000

Obligations under finance leases (amounts payable in the second to fifth years inclusive)

1,748 496 1,748 476

Accruals and deferred income 1,168 369 829 -

Bank loan (payable in second to fifth years inclusive) 7,334 10,516 - -

10,250 11,381 2,577 476

The revolving credit facility with HSBC of £3m was renewed on 31 December 2014 for another year. Of the total available, £3.0m was drawn down by the year end and each drawdown within the amount drawn is repayable in accordance with the period established for that drawdown.

The loan bears interest at 3.5% per annum over LIBOR.

The bank loan is a 5 year loan bearing interest at 7.5% over LIBOR and is repayable on 23rd December 2018 although monthly repayments are made in line with the terms of the facility agreement based on portfolio collection activity.

Notes (continued)

(forming part of the financial statements)

44

15. Deferred taxation

Group Company

2014 2013 2014 2013

£000 £000 £000 £000

At 1 January - asset 1,733 696 517 454

(Charge)/Credit for the year in the P&L account (1,414) 1,037 (517) 63

At 31 December – asset (note 12) 319 1,733 - 517

2014 2013 2014 2013

£000 £000 £000 £000

The deferred tax asset comprises

Difference between depreciation and capital allowances - 240 - 313

Tax losses carried forward 319 1,458 - 189

Other timing differences - 35 - 15

319 1,733 - 517

Group Company

2014 2013 2014 2013

£000 £000 £000 £000

The unprovided deferred tax asset comprises

Difference between depreciation and capital allowances 309 - 249 -

Tax losses carried forward 2,071 1,011 1,692 646

Other timing differences 102 - 96 -

2,482 1,011 2,037 646

A further deferred tax asset of £2,482,000 for the group and £2,037,000 for the company has not been recognised due to uncertainty over its future utilisation. It is made up as follows:

45

16. Share capital

Ordinary

shares of 5p each

‘A’ shares of 5p each

‘B’ shares of 5p each

Total

Number Number Number Number

Allotted, called up and fully

At 31 December 2013 and 2014 11,557,417 1,476,287 3,161,200 16,194,904

Ordinary shares of 5p

each

‘A’ shares of 5p each

‘B’ shares of 5p each

Total

£000 £000 £000 £000

Allotted, called up and fully

At 31 December 2013 and 2014 579 73 158 810

Both the ‘A’ and ‘B’ shares carry no right to vote at, attend or receive notice of general meetings of the company. They have rights to income or capital only on a sale of the business for a value above specific defined thresholds.

Notes (continued)

(forming part of the financial statements)

46

17. Reconciliation of the movements on shareholders’ funds

Group Sharecapital

Sharepremiumaccount

Capitalredemption

reserve

Profit andloss

account

Total

£000 £000 £000 £000

At 1 January 2014 810 501 68 205 1,584

Profit for the year - - - 1,760 1,760

At 31 December 2014 810 501 68 1,965 3,344

CompanyShare

capitalShare

premiumaccount

Capitalredemption

reserve

Profit andloss

account

Total

£000 £000 £000 £000

At 1 January 2014 810 501 68 10,912 12,291

Loss for the year - - - (1,494) (1,494)

At 31 December 2014 810 501 68 9,418 10,797

2014Total

2013Total

£000 £000

Operating leases which expire:

In the first year - 229

In the second to the fifth years inclusive 68 68

Over five years 799 665

867 962

18. Commitments

Group capital commitments authorised and contracted at 31 December 2014 were £Nil (2013: £Nil).

Group annual commitments under non-cancellable operating leases are as follows:

Annual commitments at 31 December 2014 relate solely to property leases. The majority of leases of land and buildings are subject to rent reviews.

The company had no capital commitments or annual commitments at the year end (2013: £Nil).

47

19. Pensions

The assets of the pension schemes to which the group contributes on behalf of its employees are held within independently administered funds. The schemes are all defined contribution schemes thus the group’s obligation is solely to make contributions based on a percentage of salary. Employer contributions to the schemes for the year amounted to £1,118,000 (2013: £891,000).

20. Reconciliation of operating profit to net cash inflow/(outflow) from operating activities

21. Analysis of net debt

2014 2013

£000 £000

Operating profit 3,513 387

Depreciation of tangible fixed assets 1,541 1,395

Amortisation of goodwill 442 442

Profit on sale of tangible fixed assets (13) (9)

Decrease/(increase) in debtors 1,729 (11,619)

(Decrease)/increase in creditors (1,439) 3,793

Net cash inflow/(outflow) from operating activities 5,773 (5,611)

31

December 2013

Cash flows

Other non-cashchanges

31December

2014

£000 £000 £000 £000

Cash at bank and in hand 3,703 923 - 4,626

Bank loan due within one year (3,000) - - (3,000)

Hire purchase and finance lease (1,003) 659 (2,395) (2,739)

Bank loan due after more than one (10,516) 3,182 - (7,334)

(10,816) 4,764 (2,395) (8,447)

Notes (continued)

(forming part of the financial statements)

48

22. Analysis of cash flow for headings netted in the cash flow statements

2014 2013

£000 £000

Returns on investments and servicing of finance

Interest paid (203) (222)

(203) (222)

Capital expenditure and financial investments

Purchase of tangible fixed assets (812) (812)

Receipts from sale of tangible fixed assets 13 9

(799) (803)

Financing

Bank loan (3,182) 10,516

Repayment of hire purchase and finance lease (659) -

(3,841) 10,516

49

Notes (continued)

(forming part of the financial statements)

23. Contingent liability

The company is a guarantor to the loan notes held in Target TopCo Limited. At 31 December 2014, the amount outstanding was £16,291,000 (2013: £12,699,000).

24. Ultimate controlling party

100% of the issued share capital of Target Group Limited is owned by Robin TG Investments Limited. Target Topco Limited owns 100% of the issued share capital of Robin TG Investments Limited.

Robin SARL, a company registered in Luxembourg owns 75% of the voting rights in Target Topco Limited.

The largest group in which the results of the company are consolidated is Target Topco Limited. The consolidated financial statements of Target Topco Limited are available to the public and may be obtained from Target House, Cowbridge Road East, Cardiff.

25. Related Party Transactions

On 23rd December 2013, Shawbrook Bank Limited (an investment of Pollen Street Capital, formerly RBS Special Opportunities Fund, which owns 75% of Robin SARL) advanced £10.5m by way of a 5 year loan to Target Financial Systems Limited a wholly owned subsidiary of Target Group Limited. The loan was on normal commercial terms and Shawbrook Bank Limited were paid customary arrangement fees for the advancement of the facility. At 31st December 2014, £7,334,000 of this loan was outstanding.

Target Servicing Limited, a wholly owned subsidiary of Target Group Limited, services various portfolios, under customary commercial arrangements, on behalf of Shawbrook Bank Limited. Amounts charged to Shawbrook Bank Limited during 2014 was £4,638,000 (2013: £1,765,000) and £2,000 due from Shawbrook Bank Limited at 31st December 2014 (2013: nil).

50