Cholamandalam Investment and Finance - Initiating Coverage 12 June 12

Upload

vuongxuyenCategory

view

216download

0

REPCO Home Finance

1

November 29, 2013

Find Spark research on Bloomberg (SPAK <go>), Thomson First Call, Reuters Knowledge and Factset

REPCO Home Finance

Initiating Coverage

2

REPCO Home Finance CMP

Rs. 309

Target

Rs. 375

Rating

BUY

Find Spark research on Bloomberg (SPAK <go>), Thomson First Call, Reuters Knowledge and Factset

Stock performance (%)

1m 3m 12m

REPCO 7% 35% N/A

Sensex 0% 14% 9%

Bankex 1% 25% -7%

Date 29 Nov, 2013

Market Data

SENSEX 20535

Nifty 6092

Bloomberg REPCO IN

Shares o/s 62mn

Market Cap Rs. 19bn

52-wk High-Low Rs. 313-158

3m Avg. Daily Vol Rs. 5mn

Index member BSE 500

Latest shareholding (%)

Promoters 37.4

Institutions 18.6

Public 44.0

Initiating Coverage

Jyothi Kumar Varma

+91 44 4344 0033

Abhinesh Vijayaraj

+91 44 4344 0006

Navin Babu

+91 44 4344 0165

Catch them young, watch them grow

Financial summary

Year NII (Rs. mn) PAT(Rs. mn) ROE (%) ROA (%) ABV P/ABV(x)

FY13 1,401 800 17.1% 2.4% 96 3.2

FY14E 1,925 1,212 17.5% 2.9% 113 2.7

FY15E 2,493 1,579 19.2% 2.9% 134 2.3

We see REPCO Home Finance as a multi-year growth play on the theme of low-ticket size, more profitable self-

employed customer segment of housing finance in Southern & Western India. We believe the business has legs

to sustain >25% growth rate with an improving ROE profile (from ~17% to 21% by FY18E) translating into a

strong compounding story in 3-5 year horizon with potential to be a double bagger in a 3-year time frame. Holds

promise of further structural improvements in leverage, ROE and therefore multiples as company demonstrates

its performance overtime in line with peers and wins stake-holder confidence. Initiate coverage with BUY rating

and a TP of Rs. 375 valuing business at 2.7X FY15E ABV.

Key sector thoughts:

• Housing finance to self-employed segment and small ticket size loans remains under penetrated despite regulators

favouring lower ticket size loans by allowing lower risk weights, PSL status and refinancing options at low rates.

• Recently announced cap of 2% in Rural Housing Fund (RHF) refinance window of NHB makes lending sub-optimal

(Rs. 0.2mn to Rs.1.5mn) or not feasible for HFCs operating in the <Rs. 0.2mn segment and may be reversed.

• Under-ownership of houses is higher in Southern and Western India and has increased further in the last decade

Things that we like in REPCO

• In right geographies & preferred lower ticket size market: Presence of close to 90% by branches and 96% by loan

book in Southern and Western geographies. Ticket sizes of REPCO are almost 1/3rd lower than LICHF and close to

half of the ticket size of HDFC at Rs. 1mn.

• Volume driven growth: Loan book growth of 2.5X between FY10-13 has come with healthy 1.8X growth in customers

• Focus on Self- Employed Segment: minimal reliance on DSA channel: 50% of home loan book from self-

employed segment compared to 10-20% of other large players. Owns customers as it does not rely on DSA model.

• Margin buffers to cope with loss of RHF: Upgrade from rating agencies from A+ to AA-; potential liability

diversification to NCD/CP market; securitization (PSL benefit) and increase in proportion of LAP book to 18% by

FY16E from 14% in FY13 would help in absorbing some margin pressure without resorting to rate hike

• Similar ROAs as peers; leverage key difference: Has similar ROA profile as peers but inability to leverage without

impairing rating differentiates it from them. Winning stakeholder confidence and given that GOI ownership of parent

REPCO Bank should help in addressing this issue helping it in improving ROE’s structurally over time. Removal of cap

of 2% on RHF by NHB can add 1.5-2% to structural ROE’s .

3

REPCO Home Finance CMP

Rs. 309

Target

Rs. 375

Rating

BUY

Find Spark research on Bloomberg (SPAK <go>), Thomson First Call, Reuters Knowledge and Factset

Table of Contents

Section Page

Introduction

•Factsheet 4 Click

Industry section

•Housing loans to Self-employed class 6 Click

•Low ticket size loans 7 Click

•Ownership trends in key geographies 8 Click

•Urban Housing ownership 9 Click

•NHB refinance schemes 10 Click

•Lending cap on RHF scheme 11 Click

Company section

•Key valuation drivers 13 Click

•Markets & segments 14 Click

•Margin Sustenance 15-16 Click

•Financial Leverage 17 Click

•Valuation 18 Click

•Crystal gazing 19 Click

•Risks 20 Click

•Financial Summary 21 Click

4

REPCO Home Finance CMP

Rs. 309

Target

Rs. 375

Rating

BUY

Find Spark research on Bloomberg (SPAK <go>), Thomson First Call, Reuters Knowledge and Factset

Factsheet

Corporate Factsheet

Background REPCO is a housing finance company headquartered in Chennai, Tamil Nadu. It was incorporated in April 2000 as a wholly owned

subsidiary of the REPCO Bank Limited, a Government of India enterprise. REPCO BANK was registered in 1969 as a Cooperative Society

with Jurisdiction over the State of Tamil Nadu, Andhra Pradesh, Karnataka, Kerala and Union Territory of Pondicherry for the purpose of

promoting the rehabilitation activities for repatriates from neighbouring countries mainly from Sri Lanka and Burma. It is 80% held by GOI

and other state governments.

Presence REPCO is operating through 82 branches and 20 satellite centres in Tamil Nadu, Andhra Pradesh, Kerala, Karnataka, Maharashtra,

Gujarat, Odisha, West Bengal and Pondicherry.

Management depth Mr. R Varadarajan (Managing Director)

Mr. R Varadarajan began his career with Syndicate Bank and worked in various capacities for around 23 years, and thereafter joined

Repco Bank as General Manager in the year 2000. He became Executive Director during 2006 and took charge as MD in 2010.

Mr. P Natarajan (Executive Director)

Mr. P Natarajan has nearly 30 years of experience in banking services, and previously he was a general manager at REPCO bank.

Mr. V Raghu (Executive Director)

Mr. V Raghu has an MBA & a masters degree in economics, and has prior work experience with NHB & RBI.

Management tenure Mr. R Varadarajan has been with the HFC for 13 years, and played a key role in the initial public offering of REPCO .

Business REPCO derives majority of its business from the four southern states.

Corporate Structure REPCO was incorporated as a wholly owned subsidiary of Repatriates Co-operative Finance and Development Bank Limited. REPCO

bank currently holds 37% stake in the company.

Loan book mix Home loans to Individuals – 84%

Loan against property (Mortgage) – 16%

Key Success Factors Owned Customer base, Operating in relatively niche market and sound underwriting

Capital History IPO in March 2013 raised Rs. 2.3bn

Auditors R Subramanian & Co., Chartered Accountants.

REPCO Home Finance

5

Industry Section

REPCO Home Finance

6

...and number of other challenges

Source: Spark Capital Research

Salary class Non-Salaried Class

Templatization of Lending process

Pooling of customers

Intensity of KYC checks

NPA volatility

Post Disbursement follow-up

Difference in originating fee structures also reflect the same*

Source: Spark Capital Research, * Industry interaction

SE form 50% of work force but only 10-15% of home loans

Source: NSSO, Spark Capital Research

SE segment typically has higher GNPA to salary segment...

Source: Company, Spark Capital Research

# 1. Competition lesser in self employed space (SE); Pricing is better

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

Dec-11 Mar-12 Jun-12 Sep-12 Dec-12 Mar-13 Jun-13 Sep-13

Salaried segment GNPA Non Salaried segment GNPA

Salaried, 16%

Self employed, 51%

Casual labour, 34%

0

20

40

60

80

100

Sa

lari

ed

Se

lf-e

mp

.

Sa

lari

ed

Se

lf-e

mp

.

Sa

lari

ed

Se

lf-e

mp

.

Sa

lari

ed

Se

lf-e

mp

.

HFC1 HFC2 Bank1 Bank2

Fee

pai

d (

Rs.

tho

usa

nd

s)

Loan amount (Rs.mn) 0.5 1 2 5 10

Favourable Unfavourable

REPCO Home Finance

7

...despite various incentives extended by regulators

Source: Spark Capital Research

Ticket SizeLowe NHB

Refinance ratesPSL status

Lower risk

weight

Upto Rs. 0.2 mn

Between Rs. 0.2 mn to Rs. 0.5 mn

Between Rs. 0.5 mn to Rs. 1.5 mn

Between Rs. 1.5-Rs. 2.5 mn

Upto Rs. 0.75 mn

> Rs. 7.5 mn

...pushing participants to chase higher value loans*...

Source: NHB, Spark Capital Research,* FY12 disbursement data for HFCs

GNPAs in lower ticket size 3-4x of larger size loans....

Source: NHB, Spark Capital Research

...bringing down proportion of lower ticket size loans....

Source: NHB, SCB data, Spark Capital Research

0%

20%

40%

60%

80%

100%

FY10 FY11 FY12

Housing credit outstanding (SCBs)

> 2.5 mn

1 - 2.5 mn

0.5 - 1 mn

0.2 - 0.5 mn

Upto 0.2 mn

1% 0.2 - 0.5 mn3%

0.5 - 1 mn14%

1 - 1.5 mn14%

1.5 - 2.5 mn25%

> 2.5 mn43%

# 2. Small ticket housing - It is simple but not easy; not growing despite regulatory push

0%

2%

4%

6%

8%

10%

12%

14%

FY10 FY11 FY12

<Rs. 0.2 mn Rs. 0.2mn- Rs. 0.5mn Rs. 0.5mn- Rs. 1.0mn

Rs. 1.0mn- Rs. 2.5mn >Rs. 2.5mn

REPCO Home Finance

8

# 3. Under ownership of houses higher in Southern & Western India; declined further in the last decade

On other social parameters like safe

drinking water, electrification and

sanitation southern and western

Indian states score betterSource: Census 2011, Spark Capital Research

REPCO Home Finance

9

Urban ownership of housing is going up in India...

Source: Census 2011, Spark Capital Research

..driven by higher housing credit penetration despite which...

Source: : NHB*, SCB data for FY11, Spark Capital Research

...households with >1 family is up in urban, down in rural

Source: Census 2011, Spark Capital Research

Rural, 7%

Semi urban, 16%

Urban, 28%

Metro, 49%

Urban and

metro housing

accounting for

77% of total

credit

63.1 66.8 69.2

94.6 94.4 94.786.3 86.7 86.6

40

60

80

100

1991 2001 2011 1991 2001 2011 1991 2001 2011

Urban Rural Total

Owned (%)

14.516.3

20.2 19.4 18.6 18.2

10

12

14

16

18

20

22

2001 2011 2001 2011 2001 2011

Urban Rural Total

Proportion of households with >1 married couples/house

# 4. Cohabitation & housing ownership increasing in urban; Rural India surprisingly going more nuclear

Implications

• More opportunity for housing finance in rural

areas compared to past as nuclearization picks

up

• Opportunity in urban areas especially in lower

ticket sizes can go up as next generations starts

seeking their own homes

REPCO Home Finance

10

Scheme Location Ticket Size Customer type Covenants

Liberalized Refinance Scheme

(LRS)Any Upto Rs. 1.5mn Any

Golden Jubilee Rural Housing

Refinance Scheme (GJRHRS)Rural Upto Rs. 1.5mn Any

Rural Housing Fund (RHF) Rural Upto Rs. 1.5mn Weaker Sections 2% above max refinance rate

Special Refinance for Urban Low

Income HousingUrban Upto Rs. 1.0mn

Annual HH Income of

< Rs. 0.2mn2.75% above max refinance rate;

Refinance Scheme for Women Urban Upto Rs. 2.5mnWomen ownership

(Sole/Joint ownership

Windows of NHB refinancing to HFCs

Source: NSSO, Spark Capital Research

# 5. HFCs are key takers of NHB refinance schemes; especially in Rural Housing Fund

40% NHB disbursements* is to rural o/w >50% is through RHF

Source: NHB Data, Spark Capital Research * FY12 data

Since inception ~80% of disbursements in RHF to HFCs

Source: NHB data, Company, Spark Capital Research

Interest rate Cap introduced

recently (Sep 05, 2013)

If interest rate cap reduces viability

of refinance in this scheme, it would

curtail disbursements through this

window

Urban, 61%

GJRHF, 18%

RHF, 21% Non-HFC institutions,

19%

Repco, 11%

Other HFCs, 70%

Other, 81%

REPCO Home Finance

11

Lending rate cap on RHF creates sub-optimal ROE; may push HFCs to look at other avenues

Source: Spark Capital Research

Favourable refinance rates but constrained by ticket size

Source: NHB, Spark Capital Research * rates as of FY12

S. No Particulars MMFS GRUH REPCO SUHF

1 Eligible Refinance rate 6.5% 7.5% 7.5% 7.5%

2 Int cost as % of assets ( assuming 85% of B/S is debt ) 5.5% 6.4% 6.4% 6.4%

3 Opex to Assets (Only 33% of opex taken except for MMFS) 7.0% 0.3% 0.3% 0.3%

4 Credit costs 0.3% 0.3% 0.3% 0.3%

5 Min rate to cover opex, cc and COF (2+3+4) 12.8% 7.0% 7.0% 7.0%

6 Max lending rate possible (Eligible refinance rate + 2.0%) 9.5% 9.5% 9.5% 9.5%

7 Int income as % of assets (assuming 97% of B/S is loans) 9.3% 9.3% 9.3% 9.3%

8 Pre-Tax ROA(7-5) -3.5% 2.3% 2.3% 2.3%

9 Post Tax ROA ( Tax rate of 25%) -3.5% 1.8% 1.8% 1.8%

10 Assets/ Equity (15% equity) 6.7 6.7 6.7 6.7

11 ROE (9*10) -23.4% 11.7% 11.7% 11.7%

Ticket Size Rate of Refinance through RHF*

Upto Rs. 0.2mn 6.5%

Between Rs. 0.2mn to Rs. 0.5 mn 7.0%

Between Rs. 0.5mn to Rs. 1.5 mn 7.5%

# 6. With a lending cap of 2% RHF scheme unviable/sub-optimal for most HFCs; may push NHB to rethink

GRUH, REPCO and SUHF ticket sizes match RHF requirement

Source: Spark Capital Research

0.0

0.5

1.0

1.5

2.0

2.5

FY

10

FY

11

FY

12

FY

13

FY

10

FY

11

FY

12

FY

13

FY

10

FY

11

FY

12

FY

13

FY

10

FY

11

FY

12

FY

13

FY

10

FY

11

FY

12

FY

13

GRUH REPCO SUF LICHF HDFC

Incre

me

nta

l Le

nd

ing

in R

s.

mn

With 2% cap on RHF funding,

lending is unviable or suboptimal.

If off-take in RHF decreases NHB

may rethink on the lending rate

cap

12

REPCO Home Finance CMP

Rs. 309

Target

Rs. 375

Rating

BUY

Find Spark research on Bloomberg (SPAK <go>), Thomson First Call, Reuters Knowledge and Factset

Company Section

13

REPCO Home Finance CMP

Rs. 309

Target

Rs. 375

Rating

BUY

Find Spark research on Bloomberg (SPAK <go>), Thomson First Call, Reuters Knowledge and Factset

Margin sustenance through

Liability diversification

+

increase in proportion of LAP

Presence in segments

with pricing power

(LAP+ Self Employed)

Presence in under-owned

regions of Southern and Western India

Structural increase in

financial leverage pushing up ROE

Key valuation drivers

Valuation rerating

14

REPCO Home Finance CMP

Rs. 309

Target

Rs. 375

Rating

BUY

Find Spark research on Bloomberg (SPAK <go>), Thomson First Call, Reuters Knowledge and Factset

No reliance on DSA imply “Owned Customers”; Better pricing

Source: Spark Capital Research, Company

0%

15%

20%

0%

5%

10%

15%

20%

25%

30%

35%

40%

REPCO HDFC LICHF

Sale through DSA Channel

# 1. Right markets, profitable segments & “Owned customers” base

2.5X growth in loan book; 1.8X increase in customers

Source: Company,NHB, Spark Capital Research, *HFC & SCB date not available for FY13

91% of branches and 96% of loan book in under-owned states

Source: Spark Capital Research

Housing loan book with pricing power >50% of the book*

Source: Spark Capital Research, * Indicative range only, excluded developer book from

ambit

51%66%

16%

12%15%

13%

0%

20%

40%

60%

80%

100%

Branches Loan Book

TN Karnataka AP Maharashtra Guj Kerala WB Odisha

58%

18%

42%

82%

0%

20%

40%

60%

80%

100%

REPCO Other large HFCs

LAP+ Self-Employed Housing loans Housing Loan to Salaried class

2.0

1.5

2.5

1.4

1.1

1.8

1.0

1.2

1.4

1.6

1.8

2.0

2.2

2.4

2.6

SCB Large HFC REPCO

Loan Book growth Growth in customers

15

REPCO Home Finance CMP

Rs. 309

Target

Rs. 375

Rating

BUY

Find Spark research on Bloomberg (SPAK <go>), Thomson First Call, Reuters Knowledge and Factset

Rating improvement from A+ to AA -to push down borrowing

costs...

Source: Spark Capital Research

# 2. Liability diversification, rating benefit and increase in LAP book….

...and help in market related borrowings at lower rates

Source: Spark Capital Research

Higher yield LAP book to increase from 14% to 18% by FY15

Source: Spark Capital Research

Securitization window yet to be explored

As sizable portion of the loans originated by

REPCO qualify for PSL, securitization window

can give funding at lower than bank base rates

10.30%

10.10%

9.9%

10.0%

10.1%

10.2%

10.3%

10.4%

0

1

2

3

4

5

A rating AA rating

Capital Consumed for loan of Rs. 100

Differential in indicative lending rates

13% 12%20%

24%18%

10%

63%68% 65%

0%

20%

40%

60%

80%

100%

FY13 FY14E FY15E

NHB-non RHF Refinance RHF Refinance Banks CPs & NCD

14%

16%

18%

10%

12%

14%

16%

18%

20%

FY13 FY14E FY15E

16

REPCO Home Finance CMP

Rs. 309

Target

Rs. 375

Rating

BUY

Find Spark research on Bloomberg (SPAK <go>), Thomson First Call, Reuters Knowledge and Factset

….alleviating some pain from lower borrowing from RHF refinance window

Despite 50bps loss in pre-tax ROA due to loss of RHF refinance* owing to 2% cap , we see Sufficient levers like increase in LAP,

utilizing securitization window which can reduce the impact to 20bps without resorting to any hike in rates

Source: Spark Capital Research, *Assuming it is replaced by bank borrowing

Given that almost 100% of the customers are “owned customers” pricing power would be better which can help in absorbing the loss; In case NHB

revokes the 2% cap on RHF, the above changes in liability and loan book composition can push up pretax ROA’s by almost 30bps.

50 3

18

9

20

0

10

20

30

40

50

Impact of loss of RHFfunding

Change to NCD/CP Securitization Increase in LAP portion Effective loss

Imp

act

on

Pre

-Tax R

OA

in

bp

s

17

REPCO Home Finance CMP

Rs. 309

Target

Rs. 375

Rating

BUY

Find Spark research on Bloomberg (SPAK <go>), Thomson First Call, Reuters Knowledge and Factset

S. No Particulars FY14E FY15E FY16E FY17E FY18E FY19E

1 Loan Growth 29.5% 29.3% 28.0% 28.0% 27.0% 27.0%

2 ROA 2.9% 2.9% 2.7% 2.6% 2.6% 2.5%

3 Equity 15.9% 14.8% 13.7% 12.8% 12.0% 11.3%

4 Leverage 6.14 6.55 7.05 7.58 8.11 8.61

5 ROE 17.6% 19.2% 19.0% 19.3% 20.7% 21.3%

6 Capital Adequacy 23.7% 22.1% 20.5% 19.1% 17.9% 16.9%

7 ABV 113 134 158 187 222 265

Improving leverage to result in ROE improvement from 18% to 21% by FY18E

Removing cap on RHF refinance window can push up ROA structurally by 1.4-2%*

Souce: Spark Capital, *1.4% assuming 15% of liabilities are funded through Rural Housing Finance scheme

S. No Particulars FY14E FY15E FY16E FY17E FY18E FY19E

1 Loan Growth 29.5% 29.3% 28.0% 28.0% 27.0% 27.0%

2 ROA 2.9% 2.9% 2.7% 2.8% 2.8% 2.7%

3 Equity 15.9% 14.8% 13.7% 13.0% 12.3% 11.7%

4 Leverage 6.14 6.55 7.05 7.52 7.94 8.34

5 ROE 17.6% 19.2% 19.0% 20.9% 22.0% 22.5%

6 Capital Adequacy 23.7% 22.1% 20.5% 19.3% 18.4% 17.5%

7 ABV 113 134 158 190 229 276

# 3. Financial Leverage to push up ROE; Regulatory capital consumption low

ROE to steadily increase to ~21% by

FY18

Notably regulatory capital ( Tier-1) would

still be ~17% well above the mandatory

requirement

Stock to get rerated in case NHB removes

the lending Cap

18

REPCO Home Finance CMP

Rs. 309

Target

Rs. 375

Rating

BUY

Find Spark research on Bloomberg (SPAK <go>), Thomson First Call, Reuters Knowledge and Factset

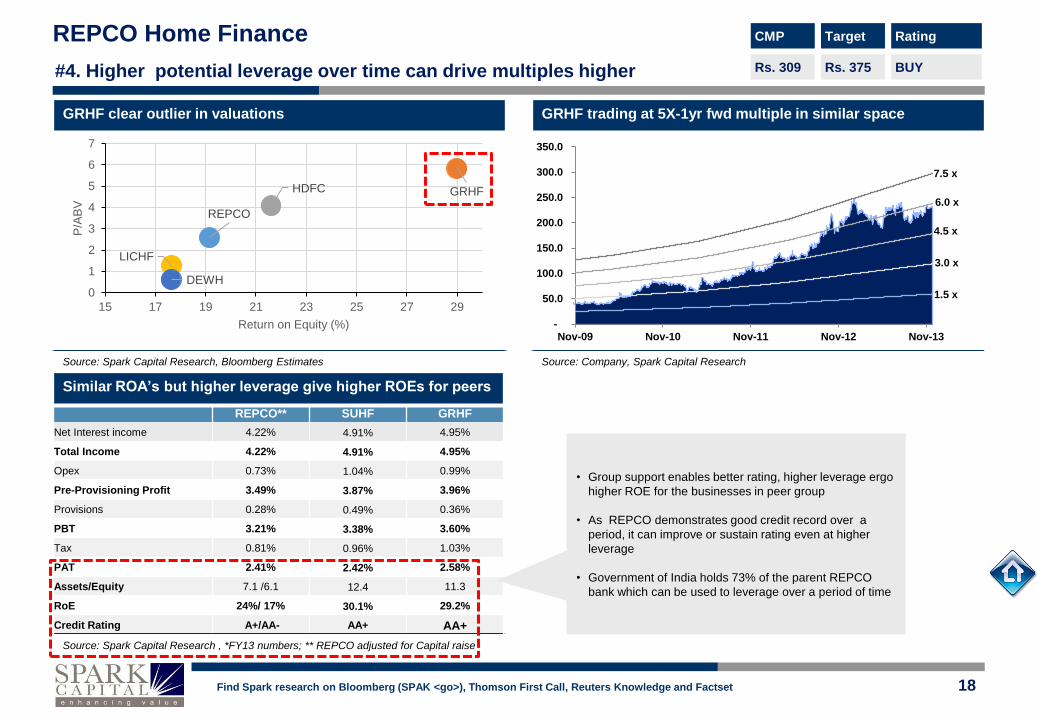

REPCO** SUHF GRHF

Net Interest income 4.22% 4.91% 4.95%

Total Income 4.22% 4.91% 4.95%

Opex 0.73% 1.04% 0.99%

Pre-Provisioning Profit 3.49% 3.87% 3.96%

Provisions 0.28% 0.49% 0.36%

PBT 3.21% 3.38% 3.60%

Tax 0.81% 0.96% 1.03%

PAT 2.41% 2.42% 2.58%

Assets/Equity 7.1 /6.1 12.4 11.3

RoE 24%/ 17% 30.1% 29.2%

Credit Rating A+/AA- AA+ AA+

Similar ROA’s but higher leverage give higher ROEs for peers

Source: Spark Capital Research , *FY13 numbers; ** REPCO adjusted for Capital raise

#4. Higher potential leverage over time can drive multiples higher

GRHF clear outlier in valuations

Source: Spark Capital Research, Bloomberg Estimates

GRHF trading at 5X-1yr fwd multiple in similar space

Source: Company, Spark Capital Research

REPCO

GRHFHDFC

LICHF

DEWH0

1

2

3

4

5

6

7

15 17 19 21 23 25 27 29

P/A

BV

Return on Equity (%)

1.5 x

-

50.0

100.0

150.0

200.0

250.0

300.0

350.0

Nov-09 Nov-10 Nov-11 Nov-12 Nov-13

7.5 x

6.0 x

4.5 x

3.0 x

• Group support enables better rating, higher leverage ergo

higher ROE for the businesses in peer group

• As REPCO demonstrates good credit record over a

period, it can improve or sustain rating even at higher

leverage

• Government of India holds 73% of the parent REPCO

bank which can be used to leverage over a period of time

19

REPCO Home Finance CMP

Rs. 309

Target

Rs. 375

Rating

BUY

Find Spark research on Bloomberg (SPAK <go>), Thomson First Call, Reuters Knowledge and Factset

Crystal gazing returns

An out-performer

with possible returns of 2x.

In 3 years, we see

REPCO to demonstrate

its capability of growing

>25% comfortably in the

more profitable self-

employed segment of the

market with further

improvement in branch

strength

A probable

rerating

Steady

compounding effect

of ROEs

Consistent

RoAs of 2.5%, with

RoEs of 18-21%

NIMs of 4%

with stable

asset quality

Accretion to

book value

As stake

holders gain

confidence

FY15E FY16E FY17E FY18E

PAT (Rs. mn) 1,579 1,865 2,253 2,872

ROA 2.9% 2.7% 2.6% 2.6%

ROE 19.2% 19.0% 19.3% 20.7%

FY15E FY16E FY17E FY18E

Book Value per

share (Rs.)144 170 203 242

Adj Book Value

per share (Rs.)134 158 187 222

P/B multiple FY18E ABV Price target

3.0x 222 666

2.0x 222 444

20

REPCO Home Finance CMP

Rs. 309

Target

Rs. 375

Rating

BUY

Find Spark research on Bloomberg (SPAK <go>), Thomson First Call, Reuters Knowledge and Factset

Risks & Other Issues

ESOP given below market price; Shared MD with REPCO

bank

REPCO has given ~0.93mn (~1.3% of capital base) ESOPs at a fixed

price of Rs. 78 per share to all the employees of REPCO. Although these

stocks were to be awarded in Aug-2012, SEBI required these to be

awarded only after 6 months of IPO.

These options would be given out to employees over the next three years

(~0.24mn given in Q2FY14) with a vesting period of one year. Rewarding

employees with ESOPs below market price is an uncommon practice.

While we are not votaries of such a practice we take comfort from the fact

that the scheme is extended to all the employees of REPCO and

secondly, fixed pay of the top management is the lowest with ED pay

~Rs. 2.2mn for FY13. We add potential dilution and impact on operating

costs in our assumptions. Further, ~100,000 options has been set aside

in lieu of a civil suit which the ex-MD of REPCO is facing in Honourable

High Court of Madras.

REPCO bank and REPCO home finance share a MD .

Other Risks

TN and Chennai Concentration in loan book

High concentration risk as 2/3rd s of the book comes from Tamil Nadu and

1/4th of the book is from Chennai. Any sharp correction in these markets

can mean growth can take a hit. We do not expect NPA to be concern,

however growth can take a back seat

Management tenure

The current management tenure is for the next three years. In the event

of the current management not taking an extension, management change

is a key risk for investors looking beyond 3 years horizon.

21

REPCO Home Finance CMP

Rs. 309

Target

Rs. 375

Rating

BUY

Find Spark research on Bloomberg (SPAK <go>), Thomson First Call, Reuters Knowledge and Factset

Financial Summary

Abridged Financial Statements Key Metrics

Rs.mn FY12 FY13 FY14E FY15E FY12 FY13 FY14E FY15E

Profit & Loss Growth ratios

Net Interest Income 1,165 1,401 1,925 2,493 ABV per share 14% 62% 17% 19%

Other Income 1 3 194 219 Loan Assets 35% 26% 30% 29%

Total Income 1,166 1,403 2,119 2,712 Borrowings 37% 23% 24% 29%

Operating Expenses 194 243 332 438 NII 19% 20% 37% 29%

Pre-Provisioning Operating Profit 972 1,160 1,788 2,273 PAT 9% 30% 51% 30%

Provisions 155 92 163 168 EPS 9% -3% 51% 30%

PBT 816 1,068 1,625 2,105 Asset-Liability Profile

PAT 614 800 1,212 1,579 Leverage (x) 8.1 6.1 5.1 5.5

Balance Sheet Leverage (x) (Incl Off B/S) 8.1 6.1 5.1 5.5

Networth 3,033 6,345 7,470 8,964 Core Tier 1- CAR 16.4% 26.7% 24.3% 21.6%

Paid Up Capital 464 622 622 624 Profitability and Efficiency

Reserves 2,568 5,724 6,848 8,339 Net Interest Margin 4.8% 4.4% 4.7% 4.7%

Others Capital Instruments ROA 2.5% 2.4% 2.9% 2.9%

Borrowings 24,860 30,647 38,007 49,098 ROE 22.6% 17.1% 17.5% 19.2%

Total Liabilities & Networth 28,527 37,926 46,947 60,629 Cost/Income 17% 17% 17% 16%

Advances 28,041 35,448 45,917 59,348 Dupont Analysis

Fixed Assets 33 45 60 766 NII/Total Assets 4.7% 4.2% 4.5% 4.6%

Net Current Assets 293 2,101 721 8,853 TI/Total Assets 4.7% 4.2% 5.0% 5.0%

Total Assets 28,527 37,926 46,947 60,629 Opex/Total Assets 0.8% 0.7% 0.8% 0.8%

Off Balance Sheet Assets PPOP/Total Assets 3.9% 3.5% 4.2% 4.2%

Total AUM 28,527 37,926 46,947 60,629 Provisions/Total Assets 0.6% 0.3% 0.4% 0.3%

PAT/Total Assets 2.5% 2.4% 2.9% 2.9%

Shares outstanding (mn) 46 62 62 62 Valuation

Current market price (Rs.) 309 309 309 309 Book Value per share (Rs.) 65 102 120 144

Market capitalization (Rs. mn) 13,793 18,462 18,462 18,540 Adj Book Value per share (Rs.) 60 96 113 134

Earnings per share (Rs.) 13.2 12.9 19.5 25.3 P/ABV (x) 5.2 3.2 2.7 2.3

Dividend per share (Rs.) 1.10 1.10 1.20 1.20 P/E (x) 23.4 24.0 15.8 12.2

REPCO Home Finance

22

Spark Disclaimer

Spark Capital Advisors (India) Private Limited (Spark Capital) and its affiliates are engaged in investment banking, investment advisory and institutional equities. Spark Capital is registered with

SEBI as a Stock Broker and Category 1 Merchant Banker.

This document does not constitute or form part of any offer or solicitation for the purchase or sale of any financial instrument or as an official confirmation of any transaction. This document is

provided for assistance only and is not intended to be and must not alone be taken as the basis for an investment decision. Nothing in this document should be construed as investment or

financial advice, and nothing in this document should be construed as an advice to buy or sell or solicitation to buy or sell the securities of companies referred to in this document.

Each recipient of this document should make such investigations as it deems necessary to arrive at an independent evaluation of an investment in the securities of companies referred to in this

document (including the merits and risks involved), and should consult its own advisors to determine the merits and risks of such an investment. This document is being supplied to you solely

for your information and may not be reproduced, redistributed or passed on, directly or indirectly, to any other person or published, copied, in whole or in part, for any purpose. This report is not

directed or intended for distribution to or use by any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction, where such distribution,

publication, availability or use would be contrary to law, regulation or which would subject Spark Capital and/or its affiliates to any registration or licensing requirement within such jurisdiction.

The securities described herein may or may not be eligible for sale in all jurisdictions or to a certain category of investors. Persons in whose possession this document may come are required to

inform themselves of and to observe such applicable restrictions. This material should not be construed as an offer to sell or the solicitation of an offer to buy any security in any jurisdiction

where such an offer or solicitation would be illegal.

Spark Capital makes no representation or warranty, express or implied, as to the accuracy, completeness or fairness of the information and opinions contained in this document. Spark Capital ,

its affiliates, and the employees of Spark Capital and its affiliates may, from time to time, effect or have effected an own account transaction in, or deal as principal or agent in or for the

securities mentioned in this document. They may perform or seek to perform investment banking or other services for, or solicit investment banking or other business from, any company

referred to in this report.

This report has been prepared on the basis of information, which is already available in publicly accessible media or developed through an independent analysis by Spark Capital. While we

would endeavour to update the information herein on a reasonable basis, Spark Capital and its affiliates are under no obligation to update the information. Also, there may be regulatory,

compliance or other reasons that prevent Spark Capital and its affiliates from doing so. Neither Spark Capital nor its affiliates or their respective directors, employees, agents or representatives

shall be responsible or liable in any manner, directly or indirectly, for views or opinions expressed in this report or the contents or any errors or discrepancies herein or for any decisions or

actions taken in reliance on the report or the inability to use or access our service in this report or for any loss or damages whether direct or indirect, incidental, special or consequential

including without limitation loss of revenue or profits that may arise from or in connection with the use of or reliance on this report.

Spark Capital and/or its affiliates and/or employees may have interests/positions, financial or otherwise in the securities mentioned in this report. To enhance transparency, Spark Capital has

incorporated a disclosure of interest statement in this document. This should however not be treated as endorsement of views expressed in this report:

Absolute Rating Interpretation

Buy Stock expected to provide positive returns of >15% over a 1-year horizon

Add Stock expected to provide positive returns of >5% – <15% over a 1-year horizon

Reduce Stock expected to provide returns of <5% – -10% over a 1-year horizon

Sell Stock expected to fall >10% over a 1-year horizon

Recommendation History

Date CMP Target price Rating

REPCO Home Finance

23

Analyst Certification of Independence

The views expressed in this research report accurately reflect the analyst’s personal views about any and all of the subject securities or issuers; and no part of the research

analyst’s compensations was, is or will be, directly or indirectly, related to the specific recommendation or views expressed in the report.

Additional Disclaimer for US Institutional Investors

This research report prepared by Spark Capital Advisors (India) Private Limited is distributed in the United States to US Institutional Investors (as defined in Rule 15a-6 under the Securities

Exchange Act of 1934, as amended) only by Decker & Co, LLC, a broker-dealer registered in the US (registered under Section 15 of Securities Exchange Act of 1934, as amended). Decker &

Co accepts responsibility on the research reports and US Institutional Investors wishing to effect transaction in the securities discussed in the research material may do so through Decker & Co.

All responsibility for the distribution of this report by Decker & Co, LLC in the US shall be borne by Decker & Co, LLC. All resulting transactions by a US person or entity should be effected

through a registered broker-dealer in the US. This report is not directed at you if Spark Capital Advisors (India) Private Limited or Decker & Co, LLC is prohibited or restricted by any legislation

or regulation in any jurisdiction from making it available to you. You should satisfy yourself before reading it that Decker & Co, LLC and Spark Capital Advisors (India) Private Limited are

permitted to provide research material concerning investment to you under relevant legislation and regulations;

Disclosure of interest statement Yes/No

Analyst ownership of the stock No

Group/directors ownership of the stock No

Broking relationship with the company covered No

Investment banking relationship with the company covered No

![[JMFL] Repco Home Finance - Initiating Coverage 14 February 14](https://static.fdocuments.in/doc/165x107/58f172e61a28aba13f8b461f/jmfl-repco-home-finance-initiating-coverage-14-february-14.jpg)