Renewable Electricity Markets & Policies...European balancing markets are often technology-neutral....

18

© OECD/IEA 2018 Renewable Electricity Markets & Policies An IEA Perspective Dr. Paolo Frankl, Head Renewable Energy Division, IEA METI Sub-Committee, Tokyo, 10 June 2019 IEA 資料2-1

Transcript of Renewable Electricity Markets & Policies...European balancing markets are often technology-neutral....

© OECD/IEA 2018

Renewable Electricity Markets & Policies An IEA Perspective

Dr. Paolo Frankl, Head Renewable Energy Division, IEA

METI Sub-Committee, Tokyo, 10 June 2019

IEA

資料2-1

2© OECD/IEA 2018

Distributed generation capacity growth makes the difference in solar PV’s leadership

Cumulative PV capacity could reach 1.1 TW and wind over 0.9 TW by 2023 under the accelerated case

Renewable electricity capacity growth by technology

Solar PV and wind expanding very fast in the next five years

0

100

200

300

400

500

600

700

800

2006-2011 2012-2017 2018-2023

GW

Wind Utility-scale PV Distributed PV HydropowerBioenergy Other renewables Accelerated case

Notes: Utility-Scale PV: more than 1MW, Distributed PV: less than 1MW but the data also takes into account country definitions due to availability of information and may include projects

larger than 1 MW under the distributed PV category. For instance, China’s definition of distributed PV may include projects up to 5 MW but these are connected to the distribution grid.

3© OECD/IEA 2018

Japan is #6 worldwide in terms of cumulative installed renewable power capacity; #3 for solar PV

Renewable electricity status and forecast

Cumulative installed renewable power capacity in selected countries, 2017 & forecast 2023

4© OECD/IEA 2018

Both country-specific conditions and policy design influence the cost of wind and solar PV

Renewable investment costs are relatively high in Japan

Investment cost of onshore wind and solar PV by technology

Source: IRENA

0

1 000

2 000

3 000

4 000

5 000

6 000

7 000

8 000

2010 2012 2014 2016 2018

USD

/kW

China Germany India Japan United States Korea Italy

Solar PV

0

500

1 000

1 500

2 000

2 500

3 000

3 500

4 000

2010 2012 2014 2016 2018

Onshore wind

5© OECD/IEA 2018

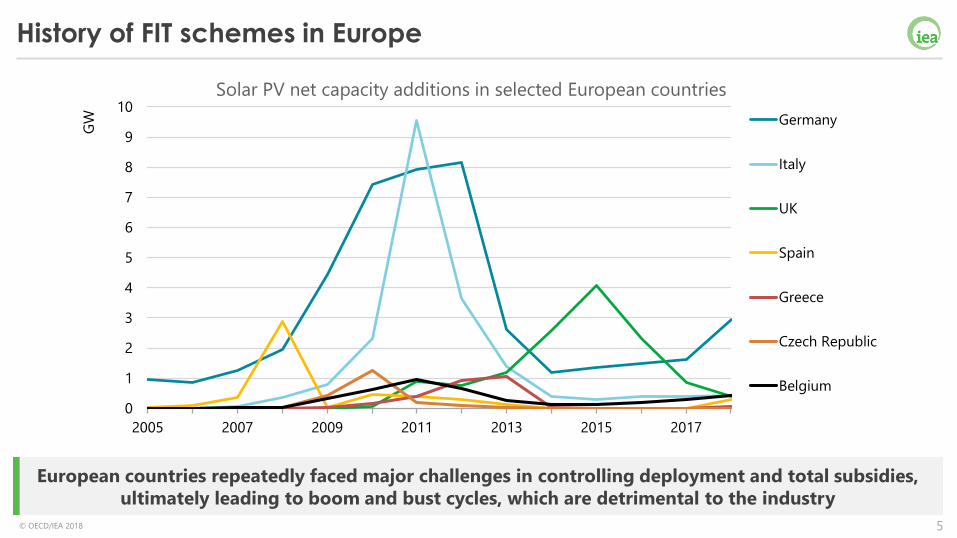

European countries repeatedly faced major challenges in controlling deployment and total subsidies,

ultimately leading to boom and bust cycles, which are detrimental to the industry

History of FIT schemes in Europe

0

1

2

3

4

5

6

7

8

9

10

2005 2007 2009 2011 2013 2015 2017

GW Germany

Italy

UK

Spain

Greece

Czech Republic

Belgium

Solar PV net capacity additions in selected European countries

6© OECD/IEA 2018

Almost 60% of renewable capacity additions over 2018-23 remunerated by competitive auctions;

announced contract prices need to be verified as project delivery schedules and final costs may differ

Competition accelerating cost reductions

Average auction price by project commissioning date

0

50

100

150

200

250

300

2012 2014 2016 2018 2020 2022

USD/MWh

Onshore wind price Offshore wind price Solar PV price

Fixed remuneration type of utility-scale projects

0

100

200

300

400

500

600

700

800

900

2012-17 Renewables 2017,2017-22

Renewables 2018,2018-23

GW

Administratively set Competitively set

Notes: For countries all over the world

7© OECD/IEA 2018

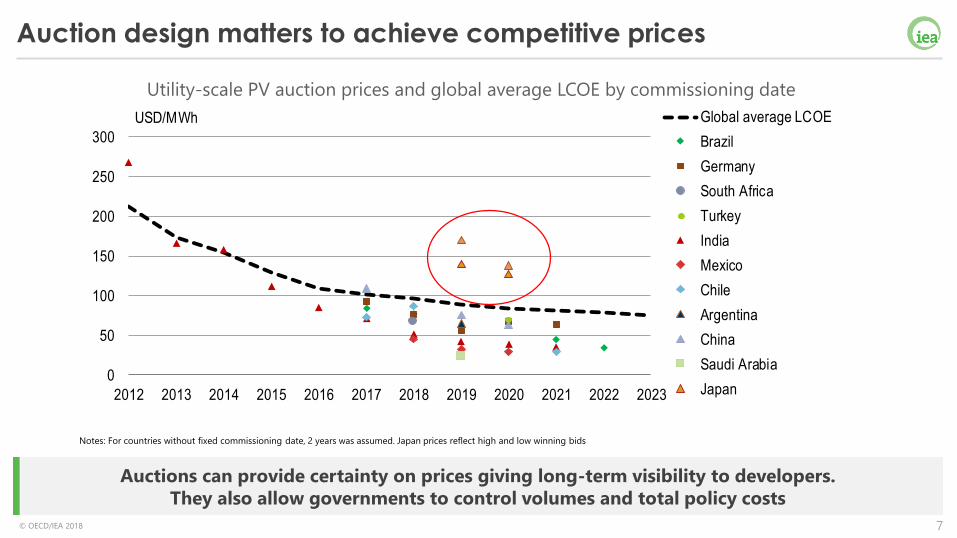

Auctions can provide certainty on prices giving long-term visibility to developers.

They also allow governments to control volumes and total policy costs

Auction design matters to achieve competitive prices

0

50

100

150

200

250

300

2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023

USD/MWh Global average LCOE

Brazil

Germany

South Africa

Turkey

India

Mexico

Chile

Argentina

China

Saudi Arabia

Japan

Utility-scale PV auction prices and global average LCOE by commissioning date

Notes: For countries without fixed commissioning date, 2 years was assumed. Japan prices reflect high and low winning bids

8© OECD/IEA 2018

Transferring risk

Demonstration

projects

• No risk for developers

Capital grants

• Few risks, in the installation phase

FiT• Technology and resource

risk (energy must be produced for some years)

Sliding FiP

• Some exposure to market prices

• Imbalance risk

Fixed FiP

• Larger exposure to market prices

Administratively set prices

Lack of project selection

Auction schemes

Project selection

9© OECD/IEA 2018

Specific power system regions can be at higher VRE integration phases due to limited interconnection

and VRE penetration. This can require market reforms to meet increased flexibility requirements

System integration: different phases

% V

RE o

f an

nu

al ele

ctri

city

gen

era

tio

n

0%

10%

20%

30%

40%

50%

60%

70%

VRE shares in total electricity generation by region in 2018

Phase 1 - No relevant impact on system Phase 2 - Minor to moderate impact on system operation

Phase 3 - VRE determines the operation pattern of the system Phase 4 - VRE makes up almost all generation in some periods

10© OECD/IEA 2018

The challenges faced by specific subsystems will vary according to the flexibility resources available.

Even at low VRE shares, integration can require policy and regulatory innovation.

Flexibility requirements depend on a combination of factors

Denmark Hokkaido Ireland Kyushu

VRE Share 63% 8% 29% 11%

Area (1000*km2) 42.9 83.4 84.4 36.7

Peak electricity

demand (GW)

5.8 5.3 4.9 15.9

Total electricity

demand (TWh)

31.7 30.6 28.2 87.8

Interconnector

capacity

8 GW combined

AC and HVDC

900 MW HVDC 420 MW 2.78 GW AC

Population

(million)

5.75 5.28 4.78 12.97

11© OECD/IEA 2018

Flexibility requirements depend on phase

A comprehensive approach to system flexibility covers not only technical aspects, but also policy,

market and regulatory frameworks, as well as institutional arrangements.

12© OECD/IEA 2018

System-friendly renewables policies

System services: wind and sun contribute to balance system24/7

Spain: wind activeon balancing market

Location: siting VRE closer to existing network capacity and/or load centers

Mexico: auctions reflect time-and location- value of electricity

Technology mix: balanced mix of VRE resources can foster lasting synergies

South Africa: Integrated Resource Plan

Local integration with other resources such as demand-side response, storage

Australia: incentives for self-consumption

Optimising generation time profile: design of wind and solar plants

California: incentive to produce at peak times

Integrated planning: wind and solar embedded in energy strategy

Denmark: integrated energy strategy

Action area Policy example

13© OECD/IEA 2018

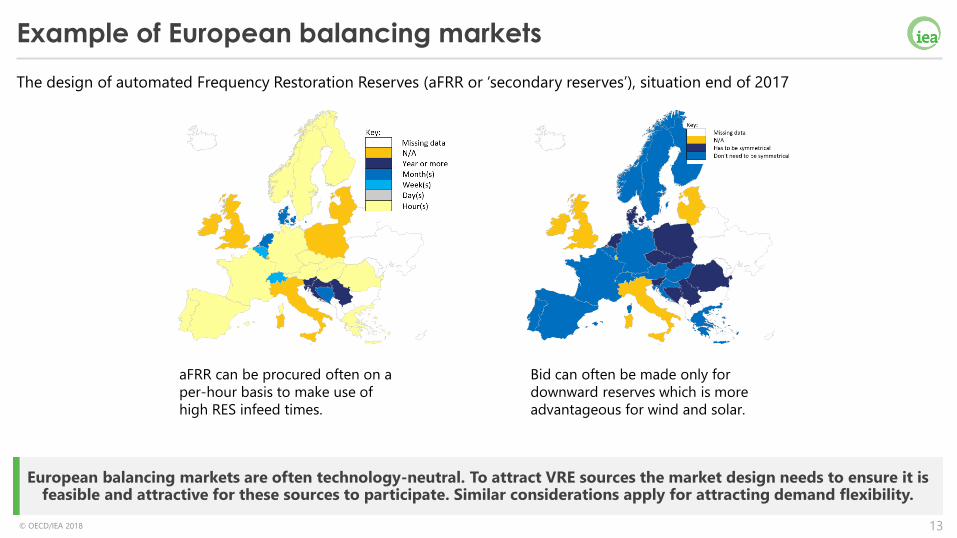

European balancing markets are often technology-neutral. To attract VRE sources the market design needs to ensure it is feasible and attractive for these sources to participate. Similar considerations apply for attracting demand flexibility.

Example of European balancing markets

The design of automated Frequency Restoration Reserves (aFRR or ‘secondary reserves’), situation end of 2017

aFRR can be procured often on a

per-hour basis to make use of

high RES infeed times.

Bid can often be made only for

downward reserves which is more

advantageous for wind and solar.

14© OECD/IEA 2018

Also in liberalized energy markets, there is value in having an integrated planning exercise to understand

system limits, guide investment plans and create incentives for VRE connection in suitable locations.

Pro-active communication on system hosting capacities

(Example: Vito, Belgian voluntary study on hosting

capacity for PV on substation level)

(Example: PG&E Distribution Resource

Plan in line with CPUC code)

15© OECD/IEA 2018

Potential of self-consumption critically depends on the match between PV supply and load demand,

which can strongly vary across countries, type of end-uses and remuneration schemes

High retail prices are a driver for self-consumption

Residential electricity prices compared with average residential PV LCOE, 2017

0

150

300

450

0 0.5 1 1.5 2 2.5

Average variable retail electricity price (USD/MWh)

Average variable retail electricity price / Average residential PV LCOE

Italy

Australia

Spain

Germany

Japan

France

Korea

UK

India

China

Mexico

California

PV profitable for self-consumptionPV not profitable for self-consumption

Notes: Residential PV: less than 10kW

16© OECD/IEA 2018

A new Clean Energy Ministerial horizontal accelerator focused on sector coupling will be considered in

2019 to broaden understanding and share experiences of this trend.

Sector Coupling addresses wider energy system decarbonisation

• Sector coupling efforts have the potential to enroll new flexible loads at scale to enhance power system flexibility.

• As all energy sectors are impacted there is a need for coordination of economic policies beyond the power system.

• Interlinkage of taxes and tariffs between various sectors of electricity, fuels, gas and bioenergy should not become barriers for wider system decarbonization

17© OECD/IEA 2018

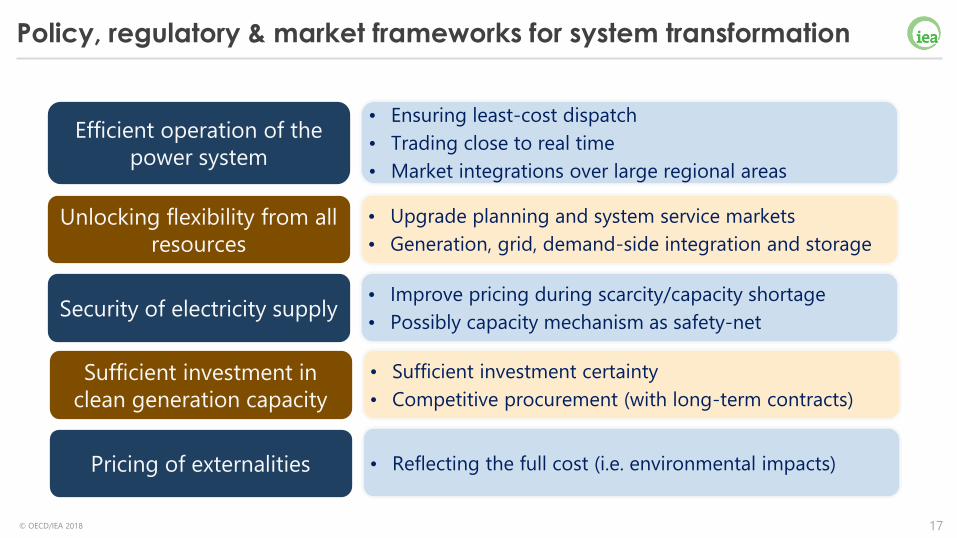

Policy, regulatory & market frameworks for system transformation

• Ensuring least-cost dispatch

• Trading close to real time

• Market integrations over large regional areas

Efficient operation of the

power system

• Upgrade planning and system service markets

• Generation, grid, demand-side integration and storage

Unlocking flexibility from all

resources

• Improve pricing during scarcity/capacity shortage

• Possibly capacity mechanism as safety-netSecurity of electricity supply

• Sufficient investment certainty

• Competitive procurement (with long-term contracts)

Sufficient investment in

clean generation capacity

• Reflecting the full cost (i.e. environmental impacts)Pricing of externalities

18© OECD/IEA 2018

Recommendations for Japan

• Increase competition and complete transition from FITs to auctions (except for small-

scale installations)

• Aim at deploying a larger portfolio of renewables, including wind off-shore, bioenergy,

geothermal

• Make renewables responsible for balancing and allow them to participate in ancillary

service markets

• Implement integrated planning and provide information on system-readiness to

integrate renewables

• Foster distributed energy resources, self-consumption and distributed flexibility

• Plan in advance coherent sector-coupling, including looking at tariffs and taxation