Relationship Marketing and Its Impact in Nigeria: Study of … … · · 2018-05-01Relationship...

35

152 International Journal of Management Sciences Vol. 3, No. 3, 2014, 152-186 Relationship Marketing and Its Impact in Nigeria: Study of the Money Deposit Banking Sector A. E. Ndu Oko 1 , S. E. Kalu 2 Abstract Employees of the money deposit banking sector of Nigeria express dis-satisfaction based on employer- employee relationships thus grievances rate is high as well as rate of labour turnover. These impact negatively on the ability of these firms at customer satisfaction, thus profit reported periodically rather than base on consumer satisfaction is based on high service charges and cost of capital in exchange relationship. This work therefore studied for challenges to the adoption of relationship marketing principles in the banking sector of Nigeria, based on the adoption of the questionnaire method of data collection, hypotheses, spearman’s rank correlation co-efficient, and Pearson’s correlation co-efficient among others as date analysis tools. Findings among others include that management of these firms operate base on the task performance philosophy as against a balance between task and maintenance philosophies; operations are not internal marketing oriented and relationship marketing principles are not internalized in the employees as they are compelled to behave relationship marketing. It is believed that activities aimed to spurring intra industrial competition in this industry will spur up the adoption of relationship marketing principles Keywords: Management philosophies, internal marketing, customer exploitation, ICT, Interactive marketing, bank density and money deposit banks. 1. Introduction Relationship marketing practice in the de0veloped economies is challenged by the growth and development in information communication technology, with its attendant results as mass customization and reduction in the number of one-on-one relationships firms seek to maintain with customers-Berkowitz, Kerin, Hartley and Rudelius (2000) and Keith (1960), hence the role of marketing intermediaries is greatly relegated to the background. Hither-to, personal and tender-loving-care connections that existed between the vendors and (customers) consumer are obviously absent. Statistics on Nigeria as a developing nation show that more than 50% of the citizens live below the poverty line-BBC News (2007), World Development Report (2010) and National Bureau of Statistics; 70% of the country’s population dwell in the rural areas-Nkanga (2007) and 85% of the 60 million adults in the country under the age of 35 can neither read nor write –Onah (2007). Based on these reports, the questions is “Are Nigerians ready to embrace information communication technology for marketing dis-intermediation? If not, how are Nigerian firms especially in the Money Deposit Banking Sector adapting to and or adopting the relationship marketing principles. Theoretical Frame Work Developed societies, inspite of the high rate of growth and development in information communication and technology still depend on relationship marketing as a key goal of marketing with its ability at developing deep and enduring relationships with people and organizations, for direct and indirect impacts on corporate goals and marketing objectives actualization –Kotler and Keller (2009). Relationship marketing 1 Department of Marketing, Abia State University, Uturu-Nigeria 2 Faculty of Management Sciences, University of Port Harcourt, Rivers State-Nigeria

Transcript of Relationship Marketing and Its Impact in Nigeria: Study of … … · · 2018-05-01Relationship...

152

International Journal of Management Sciences

Vol. 3, No. 3, 2014, 152-186

Relationship Marketing and Its Impact in Nigeria: Study of the

Money Deposit Banking Sector

A. E. Ndu Oko1, S. E. Kalu

2

Abstract

Employees of the money deposit banking sector of Nigeria express dis-satisfaction based on employer-

employee relationships thus grievances rate is high as well as rate of labour turnover. These impact

negatively on the ability of these firms at customer satisfaction, thus profit reported periodically rather than

base on consumer satisfaction is based on high service charges and cost of capital in exchange relationship.

This work therefore studied for challenges to the adoption of relationship marketing principles in the banking

sector of Nigeria, based on the adoption of the questionnaire method of data collection, hypotheses,

spearman’s rank correlation co-efficient, and Pearson’s correlation co-efficient among others as date analysis

tools. Findings among others include that management of these firms operate base on the task performance

philosophy as against a balance between task and maintenance philosophies; operations are not internal

marketing oriented and relationship marketing principles are not internalized in the employees as they are

compelled to behave relationship marketing. It is believed that activities aimed to spurring intra industrial

competition in this industry will spur up the adoption of relationship marketing principles

Keywords: Management philosophies, internal marketing, customer exploitation, ICT, Interactive

marketing, bank density and money deposit banks.

1. Introduction

Relationship marketing practice in the de0veloped economies is challenged by the growth and

development in information communication technology, with its attendant results as mass customization and

reduction in the number of one-on-one relationships firms seek to maintain with customers-Berkowitz, Kerin,

Hartley and Rudelius (2000) and Keith (1960), hence the role of marketing intermediaries is greatly relegated

to the background. Hither-to, personal and tender-loving-care connections that existed between the vendors

and (customers) consumer are obviously absent.

Statistics on Nigeria as a developing nation show that more than 50% of the citizens live below the

poverty line-BBC News (2007), World Development Report (2010) and National Bureau of Statistics; 70%

of the country’s population dwell in the rural areas-Nkanga (2007) and 85% of the 60 million adults in the

country under the age of 35 can neither read nor write –Onah (2007). Based on these reports, the questions is

“Are Nigerians ready to embrace information communication technology for marketing dis-intermediation?

If not, how are Nigerian firms especially in the Money Deposit Banking Sector adapting to and or adopting

the relationship marketing principles.

Theoretical Frame Work

Developed societies, inspite of the high rate of growth and development in information communication

and technology still depend on relationship marketing as a key goal of marketing with its ability at

developing deep and enduring relationships with people and organizations, for direct and indirect impacts on

corporate goals and marketing objectives actualization –Kotler and Keller (2009). Relationship marketing

1Department of Marketing, Abia State University, Uturu-Nigeria

2Faculty of Management Sciences, University of Port Harcourt, Rivers State-Nigeria

A. E. N. Oko & S. E. Kalu

153

aims at building mutually satisfying long term relationships with key constituents of an organization in order

to earn and retain their businesses-Gummesson (1999), Mckenna (1991) and Christopher, Payne &

Ballentyne (1991).

Unlike these advanced nations, Nigeria is characterized thus:

Research results show that Nigeria consumers are up and coming and believe in technology for

carrier advancement thus are techno-strivers-Kotler and Armstrong (2006) but over 90% of these

consumers are rural dwellers and are traditionalists who are suspicious about technology –

Oko(2013).

Common features of Nigeria marketing systems are supermarkets, departmental stores, mobile shops

and automatic vending machine based. This is however dominated by open market stalls, street

trading and hawking oriented businesses –Ibe (1993) and Oko (2013).

Traditional marketing system in Nigeria, based on its intermediating philosophies ensures as well as

enhances loyalty and creates value in exchange relationship –Kotler and Armstrong (2006), thus is

considered a virtue for relationship marketing.

Nigeria is under banked by virtue of the low density of bank branches –Ike (1985), especially as

bank density is recorded at 1:30,432-www.eco/bacons.it.com/component/simple download

The question thus is; given the characteristics of Nigeria markets compared to developed economies,

and the relative good quality for the practice of relationship marketing, why are Nigerian business outfits

especially in the money deposit banking sector averse to the principles of relationship marketing?

Objectives of the Study

This work has the objective of re-positioning firms in the money deposit banking sector of Nigeria for

efficiency based on the adoption of relationship marketing principles.

This is based on the achievement of subsidiary objectives of:

Determining the level of adoption (acceptance for application) of the practice of relationship

marketing in the banking sector;

Ascertaining the challenges to the adoption of the principles of relationship marketing;

Ascertaining the ability of firms at measuring the benefits (advantages) associated with the adoption

of relationship marketing principles;

Ascertaining the extent to which the availability of the technology of information communication or

otherwise aids the practice of relationship marketing; and

To determine the degree of relevance of internal marketing in relationship marketing as practiced in

the money deposit sector of Nigeria.

Significance of the Study

Relationship marketing is in vogue in most developed and some developing economies of the globe

with managers of businesses involved in task –oriented activities and behaviours of planning, scheduling, co-

ordinating, provision of resources and setting performance goals-Likert (1967), based on relationship

oriented behaviour that demonstrate trust and confidence, acts of friendliness and considerate kindness and

care, showing appreciation, keeping people informed among others-Bateman & Snell (1999). These

performance and maintenance leadership styles and tasks that have their anchor on relationship marketing

generate satisfied employees, fewer grievances and less labour turnover in work units –Fleishonan & Harris

(1962), hence external customer satisfaction rate is high.

Preliminary survey work on the management of firms in the money deposit banking sector of Nigeria

shows that managers are more task performance oriented in behavior, thus employees grievance rate is high

as well as the rate of labour turnover, consequently external customers’ satisfaction rate is considered low.

This work thus is significant as it is focused at guiding managers of firms in the Nigeria banking sector

towards a combination of performance-oriented behaviour (concern for production) and maintenance –

International Journal of Management Sciences

154

oriented behaviour (concern for people) based on the principles of relationship marketing; for enhanced

external customer satisfaction and corporate profitability.

Hypotheses

Analyses of this study are predicted on the following null hypotheses

H1: The rate of adoption of relationship marketing principles is insignificantly low in the banking sector

of Nigeria

H2: Improper combination of performance and maintenance behaviour in the management of money

deposit banks in Nigeria does not significantly challenge the adoption of relationship marketing

principles

H3: Benefits of relationship marketing practices are not significantly maximized by firms involved

compared to non-adoption of the principles

H4: Inability to maximized the role of technology of information communication does not significantly

affect the adoption of the practice of relationship marketing

H5: Efficiency in internal marketing management does not contribute significantly to relationship

marketing efficiency.

2. Methodology

The scope of this research is the money deposit banking sector of Nigeria; made up of 25 money deposit

banks that trade on the floor of the Nigeria stock exchange market – The Guardian (January 14, 2014), drawn

from the six geo-political zones of Nigeria, selected employees both on regular and contract bases and

selected artificial and natural persons as external customers. The entire 25 banks are considered both the

population and sample because on the smallness of the (number of firms in) size of firms in the industry.

Sets of questionnaires which were administered on top members of staff (managers as representatives)

of the banks yielded 68% return and 62% validity rate, while those administered on the regular and contract

personnel, artificial persons and natural person customers yielded 70%, 66% and 64% return rates and 65%,

63% and 61% validity rates respectively.

Mode of employment, employee emoluments, promotion, discipline and cessation programmes as

personnel related issues were compared to the contents of employee job description and specification.

Performance standard setting procedures were also evaluated in line with the provisions of the principles of

management by objectives, total quality management and open-book management system respectively. The

work also evaluated for relevance, the role of and management attitude to quality circle activities.

Activities at the different customer touch points in banking were evaluated and adopted as basis for

evaluating customers’ satisfaction with banks services rendition with respect to the quality of services, price

paid for services, employees treatment to customers, after sales services, range of services, handling of

complaints and enquiries, bank employees knowledge and extra extended service components of bank

services in terms of employees’ friendliness, ability and willingness to show understanding and empathy to

customers, fairness to customers; degree of control customers impact on the way things turn out in the banks,

availability of options and alternatives as solution to customers problems and willingness and ability to

provide customers with educative information on available bank (products) services, policies and procedures

in their dealings with the banks.

The Likert rank order scale measurement was introduced to aid the analyses of the set of questionnaires

as it aided respondents assign value to their ratings of variables that influence, especially the customers’

assessment of bank service-efficiency and bank personnel disposition as extra-extended service components

and bank personnel assessment of management.

A. E. N. Oko & S. E. Kalu

155

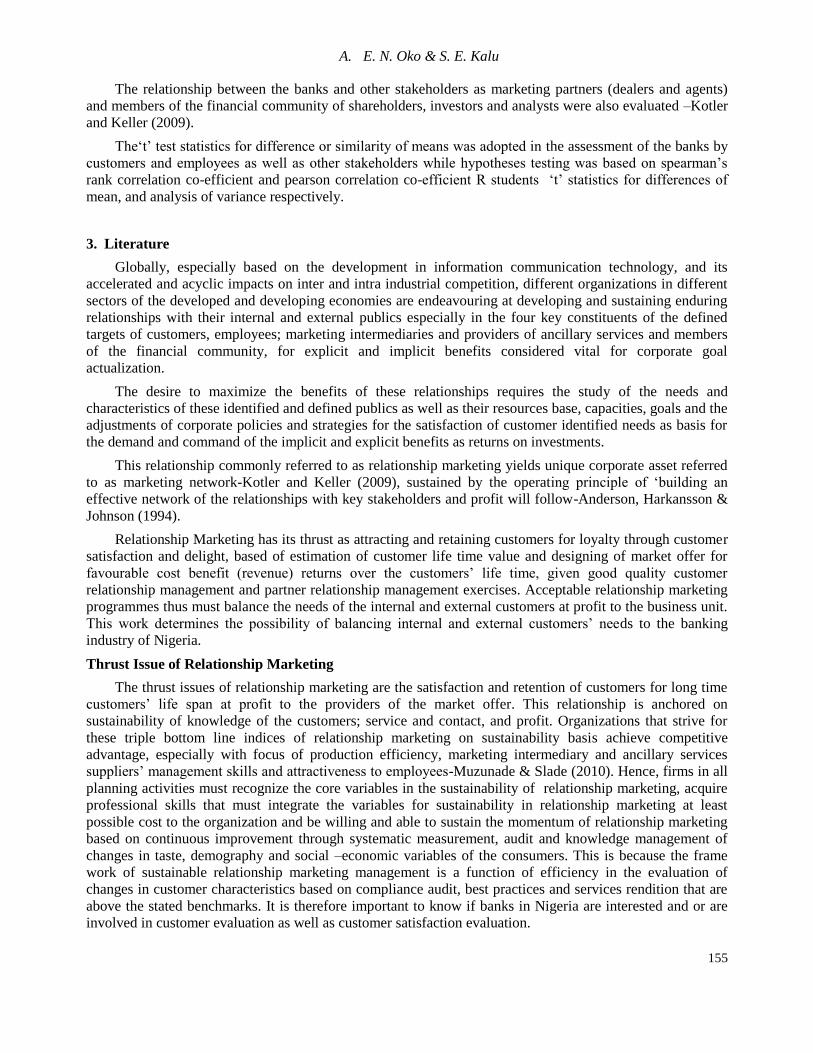

The relationship between the banks and other stakeholders as marketing partners (dealers and agents)

and members of the financial community of shareholders, investors and analysts were also evaluated –Kotler

and Keller (2009).

The‘t’ test statistics for difference or similarity of means was adopted in the assessment of the banks by

customers and employees as well as other stakeholders while hypotheses testing was based on spearman’s

rank correlation co-efficient and pearson correlation co-efficient R students ‘t’ statistics for differences of

mean, and analysis of variance respectively.

3. Literature

Globally, especially based on the development in information communication technology, and its

accelerated and acyclic impacts on inter and intra industrial competition, different organizations in different

sectors of the developed and developing economies are endeavouring at developing and sustaining enduring

relationships with their internal and external publics especially in the four key constituents of the defined

targets of customers, employees; marketing intermediaries and providers of ancillary services and members

of the financial community, for explicit and implicit benefits considered vital for corporate goal

actualization.

The desire to maximize the benefits of these relationships requires the study of the needs and

characteristics of these identified and defined publics as well as their resources base, capacities, goals and the

adjustments of corporate policies and strategies for the satisfaction of customer identified needs as basis for

the demand and command of the implicit and explicit benefits as returns on investments.

This relationship commonly referred to as relationship marketing yields unique corporate asset referred

to as marketing network-Kotler and Keller (2009), sustained by the operating principle of ‘building an

effective network of the relationships with key stakeholders and profit will follow-Anderson, Harkansson &

Johnson (1994).

Relationship Marketing has its thrust as attracting and retaining customers for loyalty through customer

satisfaction and delight, based of estimation of customer life time value and designing of market offer for

favourable cost benefit (revenue) returns over the customers’ life time, given good quality customer

relationship management and partner relationship management exercises. Acceptable relationship marketing

programmes thus must balance the needs of the internal and external customers at profit to the business unit.

This work determines the possibility of balancing internal and external customers’ needs to the banking

industry of Nigeria.

Thrust Issue of Relationship Marketing

The thrust issues of relationship marketing are the satisfaction and retention of customers for long time

customers’ life span at profit to the providers of the market offer. This relationship is anchored on

sustainability of knowledge of the customers; service and contact, and profit. Organizations that strive for

these triple bottom line indices of relationship marketing on sustainability basis achieve competitive

advantage, especially with focus of production efficiency, marketing intermediary and ancillary services

suppliers’ management skills and attractiveness to employees-Muzunade & Slade (2010). Hence, firms in all

planning activities must recognize the core variables in the sustainability of relationship marketing, acquire

professional skills that must integrate the variables for sustainability in relationship marketing at least

possible cost to the organization and be willing and able to sustain the momentum of relationship marketing

based on continuous improvement through systematic measurement, audit and knowledge management of

changes in taste, demography and social –economic variables of the consumers. This is because the frame

work of sustainable relationship marketing management is a function of efficiency in the evaluation of

changes in customer characteristics based on compliance audit, best practices and services rendition that are

above the stated benchmarks. It is therefore important to know if banks in Nigeria are interested and or are

involved in customer evaluation as well as customer satisfaction evaluation.

International Journal of Management Sciences

156

Customer Satisfaction

Providing customer satisfaction as the goal of marketing yields profitability as objective; hence

marketers must produce satisfied customers to be successful in the long run. Given this, organizations gain

competitive advantages as they strive to create committed (loyal) customers through customer delight, as a

step beyond satisfaction. Customer relationship management is based on customer value and customer

satisfaction as building blocks, thus profitable customer relationships are aimed at delivering superior

customer value and satisfaction –Kotler & Keller (2010). Customer satisfaction is a function of the product’s

(service’s) perceived performance relative to the customers’ expectations. Relationship marketing thus relies

upon the communication and acquisition of consumer requirements from existing customers in a mutually

beneficial exchange relationship permitted by the customer through an “option” system-Gala & Chapaman

(1994), thus it is integrated into the buyer’s decision process for need recognition, information search,

evaluation of alternatives, decision to or not to buy, and post purchase behaviour management. Based on the

above, marketers in relationship marketing offer customers service that excess their expectations for the

generation in the customers, a sense of satisfaction and or the creation of feelings of goodwill towards the

service providers. This created delight encourages customers to develop positive perceptions and to return

(creating customer loyalty),-businesscasestudy.co.uk/…customer-service/the-customer-service.conce, for

enhanced loyalty.

Customers develop trust and confidence in the product based on the quality of the core, augments and

extended product characteristics. Hence in addition to core issue of product function, marketers in

relationship marketing management emphasis the quality of the products (goods and services); the price;

employees treatment of customers; after sales services; range of products, customer complaints/enquire

management and knowledgeablity of personnel-as characteristics of the augment, and ability of employees at

satisfying the implicit customers needs in the offer, as friendliness (associated with being accepted politely

and courteously), understanding and empathy (that involves customers’ need to feel that the service provider

understand and appreciates their circumstances and feelings without criticisms or judgement); fairness (the

need to be treated fairly in all transactions); control (represented by customers’ need to feel really or

apparently, that they have control in the service providers’ decisions concerning their welfare), options and

alternatives (showing customers’ need to feel and be assured of the existence of other avenues or solutions to

the situations at hand) and information (desire to be educated and be informed on and about the product

characteristics, management policies as well as corporate procedures to be adopted in dealings with the

service providers)-businesscasestudy.co.uk…customer-service/the-customer-service-conce. Corporate ability

and efficiency in the satisfaction of customers in the core, augmental and extended features of the market

offer generates customer loyalty and retention as well enhances profitability-Andrson, Fornell & Lehmann

(1994).

Customer Relation

Relationship marketing management principles and strategies achieve greater than customer

satisfaction. They in addition create customer delight, causing customers to remain loyal and favourably

disposed to be involved in word of mouth communication concerning the organization and its offer-Johnson,

Zinkham &Ayala (1998). Loyal customers are committed to the product (service) and to the firm, resulting

mostly from the manner in which the firm responds to customers’ complaints or problems.

Research results show that loyal and committed customers do not require additional product promotion

as information for decision to buy, they are resistant to competitors’ marketing efforts and are more receptive

to line extensions and other new products offered by the same firm and are more likely to forgive occasional

product or service failures by the firm. –Deighton Henderson & Neslin (1994) and Bejou & Palmer (1998).

Given this discourse, authorities in marketing consider relationship marketing a key to customer loyalty

and retention, based on various practices that ensure repeated trade from pre-exiting customers by satisfying

requirements above those of competing firms through mutually beneficial relationship-Gale & Chapman

(1994) and Gord on (1999). For maximization of profit and counteracting the “Leaky bucket theory of

business” where gained new customers in older direct marketing oriented businesses are at the trade off or

A. E. N. Oko & S. E. Kalu

157

coincide with the loss of older customers, relationship marketing as a technique is adopted as means of

counter balancing these new customers and opportunities with current and existing ones-Kotler & Armstrong

(2010) and Saunders & Wong (1999).

Relationship marketing principles and strategies are favourably deployed in corporate churn

management, especially as churn rate reduction has significant impact on profitability, even where the

retained customers are primarily repeat purchasers. Reducing the number of customers who leave a firm per

period increases the average “life” of the firm’s customer base-Hawkins, Best &Coney (2001) and Li (1995).

Customers’ retention is profitable because the longer the customers are retained by a firm, the more

profits the firm derives from the customers, hence a stable customer base yields higher profitability per

customer. Thus reducing the number of customer who leaves the firm based on relationship marketing

techniques each year by 5% (ie increasing customer retention) has the ability of increasing corporate

profitability for between 25 and 85 percent depending on the characteristics of the industry-Rerchheld &

Sasser (1990). This increase is however in terms of net present value-

http://en.wikipedie.org/wiki/relationship-marketing .retrieved 25/5/2013.

The claim of Rerchheld & Sasser (1990), on profitability of retained customers is validated by Flaming

& Asplund (1991), whose research result shows that engaged customers generate 1.7 times more revenue

than normal customers, while combined engaged employees and customers yield revenue returns of 3.4.

These claims of Relchheld & Sasser (1990) and Fleming &Asplund (1991), on the potency of retained

customers is challenged by Carrol & Reichheld (1992), who dispute the accuracy of these calculations,

claiming they result from faulty cross sectional analyses.

It is worthy of note that the claimed potency of retained customers on profitability enhancement is given

a boost by Buchanan & Gilles (1990) as reported in http://en.wikipedia.org/wiki/relationship-marketing.

Buchanan & Gilles (1990) record that the increase in profitability associated with customer retention efforts

occurs given the adoption of relationship marketing and its impacts on exchange and transaction

relationships over the life span of the customers are as a result of the following:

The cost of acquisition of customers occurs only at the beginning of a relationship, so the longer the

relationship, the lower the amortized cost

Account maintenance cost in favour of customers’ decline as a percentage of total cost (or as a

percentage of revenue)

Longer term customers tend to be less inclined to switch, and also tend to be less prices sensitive.

This can result in stable unit sales volume and increase in dollar-sales volume

Long-term customers may initiate free word of mouth promotions and referrals

Long –term customers are more likely to purchase ancillary products and high margin supplemental

products.

Customers that stay with you tend to be satisfied with the relationship and are less likely to switch to

competitors, making it difficult for competitors to enter the market or gain market share

Regular customers tend to be less expensive to service because they are familiar with the process,

require less ‘education’ and are consistent in their order placement

Increased customer retention and loyalty makes the employees’ job easier and more satisfying. In

turn, happy employees feed back into better customer’s satisfaction in a virtuous circle.

Relationship marketing is centered on understanding customers’ needs at the individual customer’s

level-Bendapudi & Berry (1997), thus the customers are encouraged to use more of the brand or related

products and services offered by the firm-Wansink & Ray (1992), as substantial relationship marketing

efforts are expended on pricing, in a manner to encourage loyalty by encouraging repeat purchases –Vaura

(1993). Care should however be taken to ensure that the relationship marketing programmes are designed to

generate committed customers rather than repeat purchases –Levin (1993), Miller (1994), Fulkerson (1996)

and Passignham (1998), as committed customers have reasonable strong emotional attachment to the product

and firm based on the believe that the firm is treating them fairly and is to some extent at least, concerned

about their well being - Hawkins, Best & Coney (2001). Integrated relationship marketing programmes, for

International Journal of Management Sciences

158

generating committed customers require a customer focused attitude in the firm that is translated into actions

that meet customers’ needs-Rice (1993) and Conred, Brain & Haramon (1997). Given this discourse

http://en.wikipedia.org/wiki/relationship-marketing, advocates that customer retention efforts of

organizations should be based on the following considerations:

Customer valuation

Gardon (1999), describes how to value customers and categorize them according to their financial and

strategic values so that companies can decide where to invest for deeper relationships and on which

relationships need to be served differently or even terminated.

Customer retention measurement

Dawkins & Reichheld (1990), calculate a company’s customer retention rate. This is simply the

percentage of customers at the beginning of the year that are still customers by the end of the year. In

accordance with this statistic, an increase in retention rate from 80% to 90% is associated with a doubling of

the average life of a customer relationship from 5 to 10 years. This ratio can be used to make comparisons

between products, between market segments and over time.

Determine reasons for defection

Look for the root causes, not mere symptoms. This involves probing for details when talking to former

customers. Other techniques include the analysis of customers’ complaints and competitive bench marking.

Develop and Implement a corrective plan

This could involve actions to improve employee practices, using bench marking to determine best

corrective practices, visible endorsement of top management, adjustments to the company’s record and

recognition systems and the use of ‘recovery terms’ to eliminate the cause of defections.

Keys to Relationship Marketing

Efficiency in relationship marketing management anchores of some key elements inclusive of:-Berry

(1995)

Developing a core service or product around which to build a customer relationship;

Customizing the relationship to the individual customer;

Augmenting the core service or product with extra benefits;

Pricing in a manner to encourage loyalty, and

Marketing to employees (internal customer marketing) so that they will perform well for (external

customers) customers.

Efficiency in the integration of these keys to relationship marketing generates ‘relationship ladder of

customer loyalty” that groups types of customers according to their level of loyalty, made up of prospects;

customers; clients; supporters; advocates, and partners-htt://en.wikipedia.org/wiki/Relationship.marketing;

hence the objective of converting prospects and customers to advocates and partners through clients and

supporters based on the provision of more personalized services that are quality oriented for delight to be

achieved.

Strategies for Customer Retention

Developing committed customers for different institutions inclusive of those in the banking sector of

Nigeria requires a good understanding of customers’ desires at the point of commencement of exchange and

transaction relationships. At all the stages in this relationship, the vendor is required to create satisfaction,

delight and affection in the customers-Taher, Leigh & French (1996); through service rendition.

These customer retention strategies embody activities that build barriers to customer switching based on

product bundling, cross selling, cross promotions, loyalty programmes, increasing switching cost and

integrating computer systems of multiple organizations. Kotler & Keller (2010), O’Brien (2003), Ostenon

(2002) and Grant & Schlesinger (1995), advocate the use of activities aimed at reducing the rate of customer

defection; increasing the longevity of the customer relationship; enhancing the growth potential of each

customer through “share of wallet”, cross selling and up-selling; making low profit customers more

profitable or terminating them and focusing dis-proportionate efforts on high value customers; as strategies

A. E. N. Oko & S. E. Kalu

159

for customer retention management. This work thus ascertains the impact of the practice of relationship

marketing on customer retention ability of firms in the money deposit banking sector of Nigeria.

Internal and Interactive Marketing in Relationship Marketing

Relationship marketing prospers most, based on the harmony in relationship between internal marketing

and interactive marketing. Internal marketing recognizes the place for the internal customers and provides

that the firm should hire good quality personnel, train and motivate its customer-contract employees and

support service people for team relationships in the provision of external customer satisfaction-Kotler &

Armstrong (2010) Kotler & Keller (2009) and Brian Jones & Shaw (2002), at both marketing functions level

of sales force management, advertising, customer service management, product management, marketing

research and marketing departments’ relationship with other departments-Homburg, Workman & Krohmen

(1999), for interactive relationship that pulls all functions and departments together for the deliverance of

greater marketing accountability and engaging in marketing programmes-Wood (2003) and Hamburg &

Furst (2003).

Good quality internal marketing programmes based on proper integration of the principles of

management by objectives and total quality management, blended with acceptable internal customer

relationship management skills and techniques anchored on the principles of quality circle, guarantee

efficiency in interactive marketing, as employees’ skill in serving the external clients is brought to bear on

the technical and functional qualities of service rendition-Gronoroos (1984), Hartline, Maxham & Mekee

(2000), de Jong; de Ruyter &Lemmink (2004) and Hartline &Ferrell (1996), as team work built on delegated

authority especially among frontline employees generates work flexibility and adaptability in service

delivery through better problem solving, close employee cooperation and more efficient knowledge transfer.

These attributes influence the quality of (product)-service rendered, as customers compare the perceived

service with the expected service-Voss, Parasureman & Grewel (1998), for delight, as perceived value

surpass expected value of service based on added benefits to the offering attributed to relationship marketing

–Rust & Oliver (2002).

Given this discourse, the research establishes the impact of management philosophy and leadership

behaviour on the practice of relationship marketing based on the integration of the principles of internal

customer management, internal marketing and interactive marketing.

Relationship Marketing and Information Communication Technology

Interactive marketing and its electronic base has improved relationship between the vendors (producers)

and the customers with greater promises in the future; sales volume is enhanced –Kranta (1998), as it allows

for greater flexibility in the management of elements of the marketing mix-Woolley (1998). Added to these

benefits is its wide-customer reach based on limitless geographical boundaries –Berkowitz, Kerin, Hartley &

Rudelius (2000). Despite the associated benefits in interactive marketing and its elements base, firms in the

money deposit banking sector of Nigeria like some other firms globally are yet to tap into this for

relationship marketing efficiency-Pepper, Roger & Dorf (1999) and Downes & Mlli (1998).

The practice of relationship marketing as facilitated by ability at generating customer relationship

management soft wares, allows for the linking and analyzing of individual customers preferences, activities,

tastes, likes, dislikes and complaints for the purpose of developing customized market offers and associated

benefits.

Firms push out corporate and marketing web site information to online consumers rather than wait for

consumers to find the sites themselves. This as customized information in news, entertainment, company

product and service information are tailored around the customers’ preferences-Charleston (1999) and

www.pointcasr.com. Based on reverse action in web applications, consumers shopping profiles are

developed as the customers shop on web sites. Information there-to serves as basis for computing customer’s

likely preferences in other categories. These predicted offerings are shown to customers through cross-sell e-

mail recommendations and other channels-http://en:Wikipedia.org/wiki/Relationship-marketing.

International Journal of Management Sciences

160

It is important to note that the period of pre-information communication technology as firms, based on

digital technology produced unique and personalized pieces for each customer containing their data base

with essential highlights of name, addresses, demographics, purchases history and other variables as well as a

reflection of customers’ needs, and preferences. Based on relationship marketing practice, these data on

customer have increasing relevance as customers response rate increase.

Based in this analysis, the questions is, is it possible for customer patronage of firms in the money

deposit banking sector of Nigeria to increase for increased corporate profitability given efficiency in the

adoption of relationship marketing principles based on proper integration of the potentials of the information

communication technology.

Exchange and Transaction in Relationship Marketing

Marketing ordinarily is exchange and transaction focused for customer satisfaction and (vendor)

producer’s profit goal and objective actualization, hence is reward and deal oriented, with emphasis on

acquisition of new customers, sales incentives and product /service unique characteristics. Studies show that

although vendors in general marketing practice promise value and capitalize on thrust as concepts, the

interactive marketing functions that elongate customers’-vendors’ relationship beyond the point of exchange

is often absent –Baker (1996), Kotler & keller (2010), Keller & Armstrong (2010) and Agbonifoh, Ogwo,

Nnolim & Nkamnebe (2007).

Relationship Marketing is built on both managerial orientation and business function philosophies that

integrate corporate, business and functional strategies based on the management of the distrust dimensions of

marketing culture, strategies and tactics for the purpose of building long-term relationships with customers

and other parties as marketing partners and members of the financial community-Kotler & Keller (2010).

Relationship marketing thus depends on inputs from marketing specialists and non-specialists in different

departments across the organization and beyond for the creation of relationship that ensures the actualization

of the desires of parties and elimination of the challenges incumbent in transaction focused exchange.

Based on this discourse, after sale supports and services as extended (extra) service characteristics of

offer are seen as investment for the sustenance of relationship rather than cost and closure of sales is

considered the genesis of relationship marketing-Okpara (2002). Given this, this work establishes the

position of firms in the money deposit banking sector in the practice of relationship marketing with regards

to relationship with marketing partners and members of the financial communities.

4. Analysis

Data as bases of the analysis are ranked based Likert ranking order scale principles and test for

significancy of correlationship or otherwise is based use various test statistics.

Hence the general decision rule is:

If the value calculated is greater than 50 (fifty) percent (acceptable mean), accept the projected

statement, if otherwise reject.

The issues of analyses are built around the hypotheses of this study as well as relevant questions built

into the literature; hence analyses are as flows:

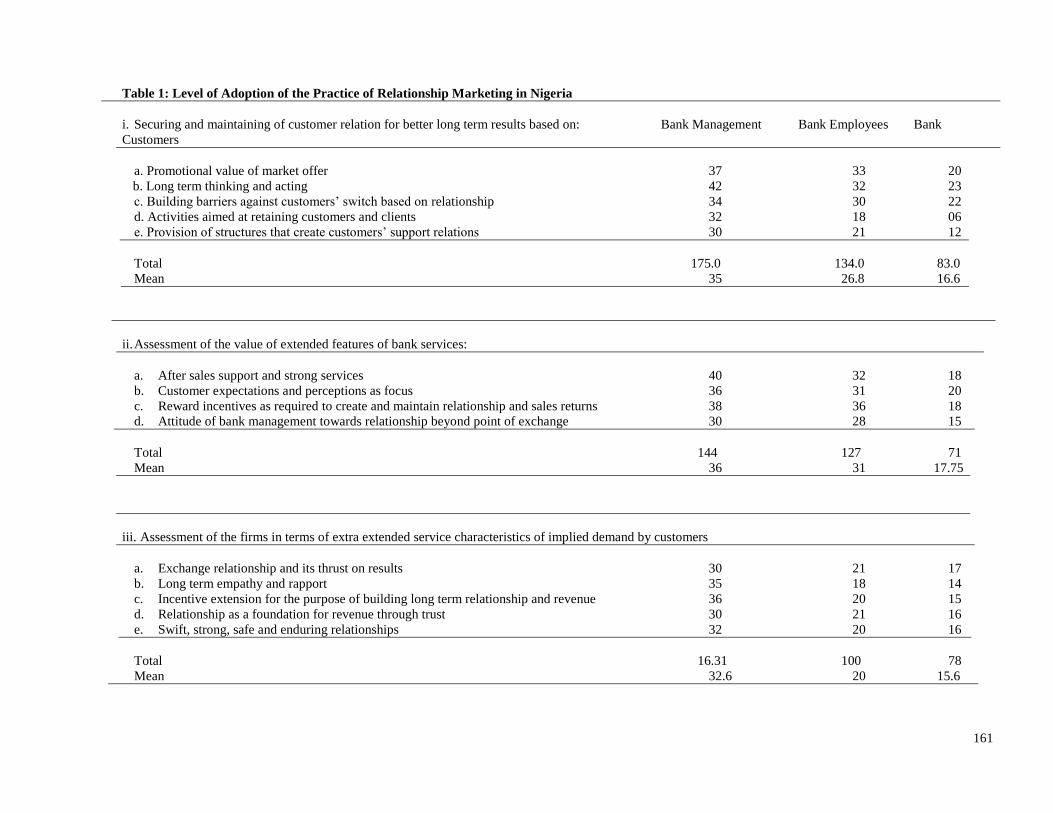

Table 1

1. Testing for the level of adoption of the practice of Relationship Marketing in the money deposit

banking sector of Nigeria:

The sets questionnaires as administered on top management, employees and customers on relevant

issues of the adoption of the practice relationship marketing in Nigeria yielded the following as presented in

table 1

161

Table 1: Level of Adoption of the Practice of Relationship Marketing in Nigeria

i. Securing and maintaining of customer relation for better long term results based on: Bank Management Bank Employees Bank

Customers

a. Promotional value of market offer 37 33 20

b. Long term thinking and acting 42 32 23

c. Building barriers against customers’ switch based on relationship 34 30 22

d. Activities aimed at retaining customers and clients 32 18 06

e. Provision of structures that create customers’ support relations 30 21 12

Total 175.0 134.0 83.0

Mean 35 26.8 16.6

ii. Assessment of the value of extended features of bank services:

a. After sales support and strong services 40 32 18

b. Customer expectations and perceptions as focus 36 31 20

c. Reward incentives as required to create and maintain relationship and sales returns 38 36 18

d. Attitude of bank management towards relationship beyond point of exchange 30 28 15

Total 144 127 71

Mean 36 31 17.75

iii. Assessment of the firms in terms of extra extended service characteristics of implied demand by customers

a. Exchange relationship and its thrust on results 30 21 17

b. Long term empathy and rapport 35 18 14

c. Incentive extension for the purpose of building long term relationship and revenue 36 20 15

d. Relationship as a foundation for revenue through trust 30 21 16

e. Swift, strong, safe and enduring relationships 32 20 16

Total 16.31 100 78

Mean 32.6 20 15.6

International Journal of Management Sciences

162

iv. Assessment of service, based on its core related issues of:

a. Quality of service 30 28 26

b. Price of service 35 24 21

c. Treatment of customers 30 22 16

d. Contents of after sale services 30 28 17

e. Range of services 30 29 22

f. Management of customers’ inquiries and complaints 27 25 15

g. Personnel personal knowledge of the different service situations 30 31 16

Total 212 187 133

Mean 30.28 26.71 19.00

v. Assessment of firms based on its ability to identify and satisfy unexpressed needs of the

target markets

a. Friendliness, (associated with customers’ need for friendliness, and other characteristics

of politeness and courteousness) 30 17 12

b. Understanding and sharing; associated with empathy for customers and appreciating

their circumstances and feelings) 30 27 15

c. Treating the customers fairly in business relationships 33 28 24

d. Giving the customers the impressions that they have control over the end product in

quality and otherwise 28 16 10

e. Giving the customers alternatives as solutions to their problems 25 17 12

f. Provision of information and education on services, policies and procedures of the banks 30 26 18

Total 476 131 91

Mean 29.3 21.8 15.16

163

The data on table 1. are re- structured in table 2 thus:

Table 2: Rating of Bank Services by Management Staff, Employees and Customers

Variable Management Employees Customers

[

Service for long term relationship 35.00 26.80 16.60

Extended features of banking services 36.00 31.00 17.75

Extra extended service characteristics 32.60 20.00 15.60

Value of bank core service s 30.28 26.71 19.00

Satisfaction of unexpressed customers’ needs 29.30 21.80 15.16

Total 163.18 126.31 84.11

Mean 32.66 25.26 16.82

Decision Rule

Based on Likert ranking order scale, if the value calculated is greater than 50(fifty) percent (acceptable

mean), accept the projection that the rate of adoption of relationship marketing principles is significantly

high in the banking sector of Nigeria.

If otherwise, reject.

The computation on table 2, shows that the mean value of assessment of bank management, employees

and customers are 32.66%, 25.26% and 16.82% respectively. These are below acceptable mean percent of

50. Following this, the H0 is rejected and H1 accepted, as the rate of adoption of relationship marketing

principles is significantly low in the banking sector of Nigeria.

To test for significance at the chosen level of confidence, the mean difference or otherwise between the

rating of bank management, employees and customers on the rate of adoption of the practice of relationship

marketing in the banking industry in Nigeria, the test hypothesis is re-structured as:

H0: (µ1 = µ2 ≠ µ3) There is no significant difference in the assessment of the bank management

employees and customers on the rate of adoption of relationship marketing practice in banks.

H1: (µ, ≠ µ2 ≠ µ3) Significant difference exist between the assessment of the bank management

employees and customers on the rate of adoption of relationship marketing practice in banks

Where µ1, µ2 and µ3 are means rating of the different classes of respondents

Given: F = Vb = between groups variance = S2b 1)

Vw within groups variance S2W

Where: VB = SSB and (2)

dfB

Vw = SSW (3)

dfw

International Journal of Management Sciences

164

For computation of f-ratio, table 3 is considered

Table 3: Assessment of Relationship Marketing Related Variables in Banks in Nigeria

Management Employees Customers

XA X2A XB X

2B XC X

2C

35.00 1225.00 26.80 718.24 16.60 275.56

36.00 1296.00 31.00 961.00 17.75 315.06

32.60 1062.76 20.00 400.00 15.60 243.36

30.28 916.88 26.71 713.42 19.00 361.00

29.30 858.49 21.80 475.24 15.16 229.83

∑XA =163.18 ∑X2A =5359.13 ∑XB = 126.31 ∑X

2B 3267.9 ∑XC=84.11 ∑X

2C=1424.11

A = 32.66 B = 25.26 c = 16.82

n = 5 n = 5 n = 5

Grand mean = 32.66 + 25. 26 + 16. 82

3

= 24.91

SSW = 33.58+77.05 + 9.90

= 120.53

SSY = SSB + SSW

= 24.91+ 120.53

= 145.44

Substituting values for variables

VB = SSB

dfB

VW = SSW

dfw

dfB = number of groups (k) minus 1

dfw = number of the cases within each sub group (n) minus 1

Where VB = Variance between group

Vw = Variance within group

dfB = Degree of freedom between group

dfw = Degree of freedom within group

Substituting for mathematical notations 2 and 3:

VB = SSB = 673.175

dfB 2

= 336.59

VW = SSW = 120.5

dfw 12

= 10.04

A. E. N. Oko & S. E. Kalu

165

Substituting the f-ratio mathematical notation 1

f = VB

VW

= 336.59

10.04

= 33.52

Summary of the ANOVA to capture the computation is shown in table 4

Table 4: Summary of ANOVA

Source of df Sum of Squares Mean of Squares f- cal Critical Significance Decision

Variance SS MS value of

f

Between groups 2 SSB = 673.67 VB = 336.59 Significant Reject

Within groups 12 SSW = 120.53 VW = 10.04 33.52 2.96 H0

Total 14 79420 346.63

5. Conclusion:

At 0.05 level of significance, the critical value of f = 1.70

Since F > F0.05 (2.96), the H0 is rejected, the accepted conclusion is that the mean values are not equal.

Hence significant differences exist between the assessment of the bank management, employees and

customers on the rate of adoption of relationship marketing practices in banks in Nigeria. The rating of

managers and employees of banks on the rate of adoption of relationship marketing principles are higher

compared with the rating of customers, although the level (rate) of adoption of this principle is relatively low.

Test 2:

Assessment of the appropriateness or otherwise of the management style and attitude of firms in the

money banking industry and its impact on the adoption of relationship marketing principles in Nigeria

banking sector

Data for this assessment as generated are thus in table 5

Table 5: Assessment of Money Deposit Banks Work Group Management Philosophies

Issues of Assessment: Management Employees

1. Assessment of management in terms attitude to

quality circle activities of:

a. Management and team members joint responsibility in goal

determination and planning of work 45 40

b. Management and team members in cross training 61 52

c. Management and team members in sharing of information

International Journal of Management Sciences

166

at all levels 43 42

d. Continuous learning based on interpersonal, administrative and

technical trainings 40 38

e. Management and team members’ attitude towards risk taking

and supportive activities 41 36

f. Permitting people to work together 56 42

g. Attitude to reward as based on individual’s performance and

contributions to corporate performance 48 40

h. Work on individual basis, for continuous improvement of

methods and processes 58 47

Total 392 337

Mean 49.0 42.13

2. Assessment of management and corporate activities based on the

following integrals of the principles of open book management

a. Attitude to involving subordinates on business decision issues 56 32

b. Sharing of financial and operational information with employees 51 26

c. Educating employees based on financial information 50 22

d. Sharing with employees the impact of their work (efforts)

on corporate financial results 45 20

e. Linking non-financial measures to financial results 60 21

f. Targeting priority areas and empowering employees to make

improvements 60 42

g. Reviewing of results together and keeping employees accountable 50 40

h. Post result events and celebration of success with employees 60 30

i. Distribution of bonus awards based on employees contribution to

financial outcome 50 16

j. Sharing of ownership of firm with employees 20 06

Total 502 255

Mean 50.2 25.5

[

3. Assessment of Management in terms of Task Performance Management Employees

leadership style (philosophy)

a. Strictness in observation of regulations 30 65

b. Level of issuance of instructions and orders 50 80

c. Strictness over volume of job done 40 72

d. Strictness over time schedules and job specifications 50 68

e. Achievement of maximum capacity 50 70

f. Reaction to situation of greater job inadequacy compared to job

adequacy 60 80

g. Level of precision about work plan and achievement within

defined time. 67 82

h. Strictness in demand for report on work done 60 80

Total 407 597

Mean 50.86 74.62

A. E. N. Oko & S. E. Kalu

167

4. Assessment of Management in terms of Maintenance Leadership

Style (Philosophy)

a. Liberty at superior –subordinate discussions 60 40

b. Level of support received from superiors 63 42

c. Superiors’ concern about subordinates personal problems 60 40

d. Level of trust superiors have for subordinates 60 30

e. Willingness and liberty at recognizing sub-ordinates for well

done job 50 18

f. Superiors’ attitude and opinion to solution to problems at work

place 60 25

g. Superiors’ concern about the future benefits of sub-ordinates 60 20

h. Fairness in treatment to sub-ordinates 50 15

Total 463 230

Mean 57.88 28.75

5. Assessment of Management in Terms of Attitude to factors that

enhance the quality of Work Life of Sub-ordinates (employees).

a. Adequacy and fairness of compensation 60 22

b. Provision of safe and healthy environment 50 21

c. Availability of job that develop human capacity 60 40

d. Provision of opportunities for personal growth and security 50 38

e. Social environments that foster personal identity, freedom from

prejudice, sense of community and upward mobility 60 41

f. Constitutionalism as right to privacy, decency and due process 58 42

g. Work role that minimizes infringements on personel leisure

and family needs 56 30

h. Socially responsible organizational actions 60 28

Total 454 262

Mean 56.75 32.75

For the adoption of the spearman’s rank correlation co-efficient to describe the relationship or otherwise

that exist between the assessment of these two groups of respondents (management and employees) on the

attitude of management to the enhancement of the work life of subordinates without making any assumption

about the frequency distribution of the variables-htt://en.wiki.pedia.org/wiki/spearman’s ranking; this work

adopts the correlation-co-efficient statistical tool represented by the mathematical notation 4

rs = 1 – 6 ∑d2

(4)

N(N2-1)

Where: d = the difference between each rank of corresponding values of x and y

N = the number of pairs of values

Table 6 is the restructured data in table 5

International Journal of Management Sciences

168

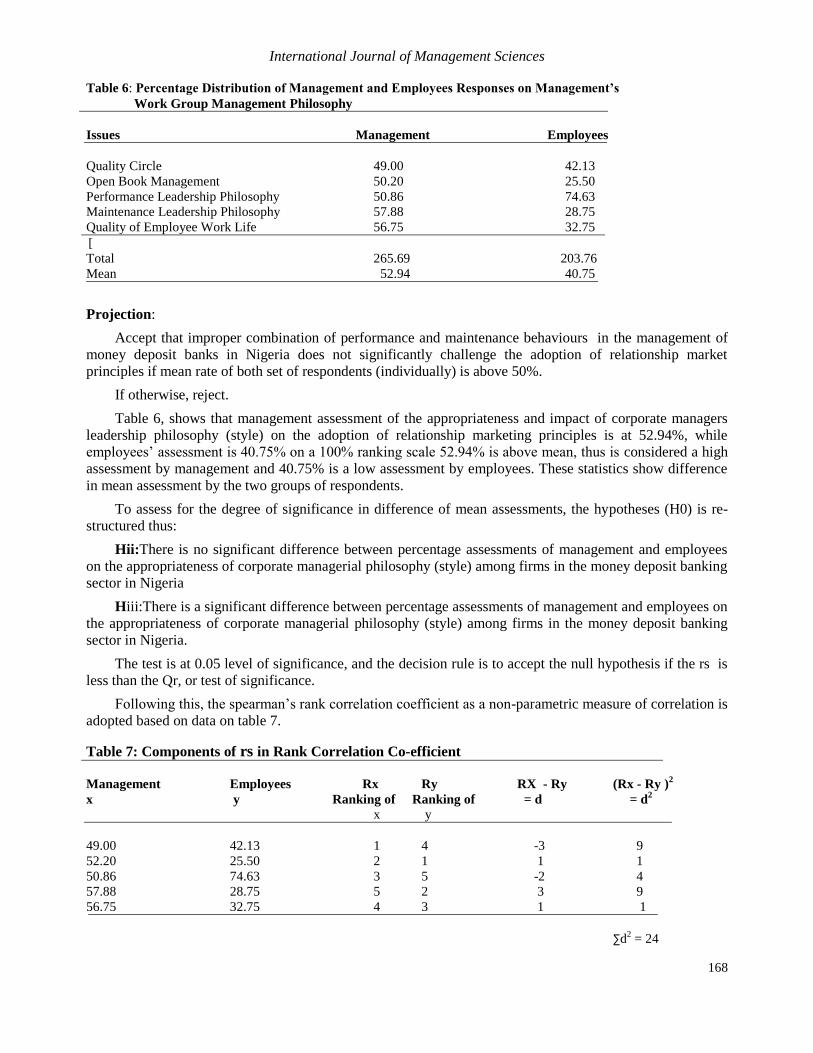

Table 6: Percentage Distribution of Management and Employees Responses on Management’s

Work Group Management Philosophy

Issues Management Employees

Quality Circle 49.00 42.13

Open Book Management 50.20 25.50

Performance Leadership Philosophy 50.86 74.63

Maintenance Leadership Philosophy 57.88 28.75

Quality of Employee Work Life 56.75 32.75

[

Total 265.69 203.76

Mean 52.94 40.75

Projection:

Accept that improper combination of performance and maintenance behaviours in the management of

money deposit banks in Nigeria does not significantly challenge the adoption of relationship market

principles if mean rate of both set of respondents (individually) is above 50%.

If otherwise, reject.

Table 6, shows that management assessment of the appropriateness and impact of corporate managers

leadership philosophy (style) on the adoption of relationship marketing principles is at 52.94%, while

employees’ assessment is 40.75% on a 100% ranking scale 52.94% is above mean, thus is considered a high

assessment by management and 40.75% is a low assessment by employees. These statistics show difference

in mean assessment by the two groups of respondents.

To assess for the degree of significance in difference of mean assessments, the hypotheses (H0) is re-

structured thus:

Hii:There is no significant difference between percentage assessments of management and employees

on the appropriateness of corporate managerial philosophy (style) among firms in the money deposit banking

sector in Nigeria

Hiii:There is a significant difference between percentage assessments of management and employees on

the appropriateness of corporate managerial philosophy (style) among firms in the money deposit banking

sector in Nigeria.

The test is at 0.05 level of significance, and the decision rule is to accept the null hypothesis if the rs is

less than the Qr, or test of significance.

Following this, the spearman’s rank correlation coefficient as a non-parametric measure of correlation is

adopted based on data on table 7.

Table 7: Components of rs in Rank Correlation Co-efficient

Management Employees Rx Ry RX - Ry (Rx - Ry )2

x y Ranking of Ranking of = d = d2

x y

49.00 42.13 1 4 -3 9

52.20 25.50 2 1 1 1

50.86 74.63 3 5 -2 4

57.88 28.75 5 2 3 9

56.75 32.75 4 3 1 1

∑d2 = 24

A. E. N. Oko & S. E. Kalu

169

Substituting the mathematical notation 4

r2 = 1 - 6∑d2 (4)

N (N2 – 1)

= 1 – 6 (24)

5 (25-1)

= 0.200

The test of significance Qrs; for this test, the statistic is conducted using mathematical notation 5,

represented thus:

Qrs = Z -1 (5)

n- 1

= 1.96 (1)

15-1

= 0.98

Where z is standard normal deviation and which at 0.05 level of significance is given as 1.96

Following the results of the computations, the decision is to accept the alternative hypothesis since rs is

less than the Qrs . It is therefore concluded that the test is insignificant at 0.05 level of confidence; hence the

position of this work is to reject the alternative hypothesis. Thus there is no significant difference between

percentage assessment of management and employees on the appropriateness of corporate managerial

philosophy (style) among firms in the money deposit banking sector in Nigeria.

The assessment of employees is accepted as they (consumers) are the direct target of the managerial

philosophy. The work therefore concludes that the corporate managerial philosophy of firms in the money

deposit banking sector of Nigeria shows improper combination of the performance and maintenance

behaviours. Thus the internal marketing activities based on employees’ and departmental relationship is poor,

hence relationship marketing with its thrust as external customers is poor in the banking sector in Nigeria.

Test 3:

Assessment of the level of maximization of the benefits of relationship marketing by management of

money deposit banks in Nigeria.

Data for this assessment and analysis are based on table 8

Projection:

Accept that the benefits of relationship marketing practice are significantly maximized by firms if mean

assessments are above 50%, that is the acceptable mean score.

If otherwise Reject

International Journal of Management Sciences

170

Table 8: Maximization of the Benefits of Relationship Marketing:

Issues of Assessment Management Customers

a. Long term relationship built on promises, trust and

interactive marketing and its impact on turnover 40 32

b. Profitability following reduction in cost of serving

customers and absence of switching costs 48 28

c. Confidence in internal marketing activities following

the development of marketing network 40 32

d. Customer retention and loyalty based on customization of offer 40 40

e. Adaptivity and responsiveness resulting to reduction of customer

stress 40 32

f. Publicity gained based on word of mouth of communication 40 25

g. Cost reduction in marketing activities 43 31

h. Pre-payment by customers based on customer confidence creation 28 08

Total 319 22.8

Mean 39.88 28.5

Data based on table 8 show clearly that firms in the money deposit banking sector in Nigeria do not

maximize the benefits associated with the practice of relationship marketing. Both the management and

employees of different banks scored the firms’ benefits maximization ability at a mean value of 39.88% and

28.5% respectively. These scores are below the acceptable mean value of 50% on a 100% ranking scale, thus

the projected statement is rejected. Accepted is that the benefits of relationship marketing practice are not

significantly maximized by firms in the money deposit banking sector of Nigeria.

To test for the degree of significance in mean variation between the scores of corporate management

and employees (personnel) of these institutions, the students’ t-test statistics for difference of mean is

adopted. This is represented by mathematical notation 6

t = - 12 (6)

S21 + S

22

n1 n2

n1 = sample size of the first category

n2 = sample size of the second category

S21 = variance (S

21) or standard deviation (s) of the first category

S22 = variance (S

22) or standard deviation (S2) of the second category

Data on table 8 are re-structured for table 9 thus:

Table 9: Benefits Maximization Based on the Practice of Relationship Marketing

Variable Management (X1) Employees (X2)

a 40 32

b 48 28

c 40 32

d 40 40

e 40 32

f 40 25

g 43 31

h 26 08

A. E. N. Oko & S. E. Kalu

171

The hypotheses are re-structured thus:

H01:There is no significance difference between the assessment of corporate management and

employees on the ability of firms in the money deposit banking sector of Nigeria to maximize the

benefits of relationship marketing.

H1:There is significant difference between the assessments of corporate management and employees on

the ability of firms in the money deposit banking sector of Nigeria to maximize the benefits of

relationship.

Substituting t – test for mathematical notation (formula) 6

t = - 2

S21 + S

22

n1 n2

t = 39.875 – 28.5

(5.566)2 + (9.319)

2

8 8

t = 2.96

At 0.05 level of significance and 14 degrees of freedom, the critical value is given 1.761. Since 2.96 is

greater than 1.761, the decision is to reject the null hypothesis. Hence there is significance difference

between the assessment of corporate management and employees on the ability of firms in the money deposit

banking sector of Nigeria to maximize the benefits of relationship marketing; although the assessments of

both management and employees in this sector are below the acceptable mean of 50%, thus are low.

Test 4 :

Assessment of the ability of money deposit banks at the maximization of the role of information

communication technology in the practice of relationship marketing.

Projection:

Accept that inability to maximize the role ICT does not have significant effect on the adoption of

relationship marketing practice in Nigeria, if calculated mean is greater than 50%

If otherwise; reject

Table 10: Assessment of the rate of and challenges to the adoption of information communication

technology

Issues of Assessment Management Customers

a. Impact of cost on access to ICT services given

the low level of per capita income in Nigeria 30 26

b. Impact of the unfavourable rural/urban population density

on access to ICT 20 12

c. Perception of ICT as luxury rather than necessity 28 26

d. Impact of the high level of illiteracy in Nigeria on the use of

ICT facilities 26 20

e. Impact of the low level of communication between ICT service

subscribers and service providers on service consumption 21 19

f. Lack of access to bank customers and to the needed customers data base 19 16

g. Ability of information communication technology to create customer

value 20 18

Total 164 137

Mean 23.43 19.57

International Journal of Management Sciences

172

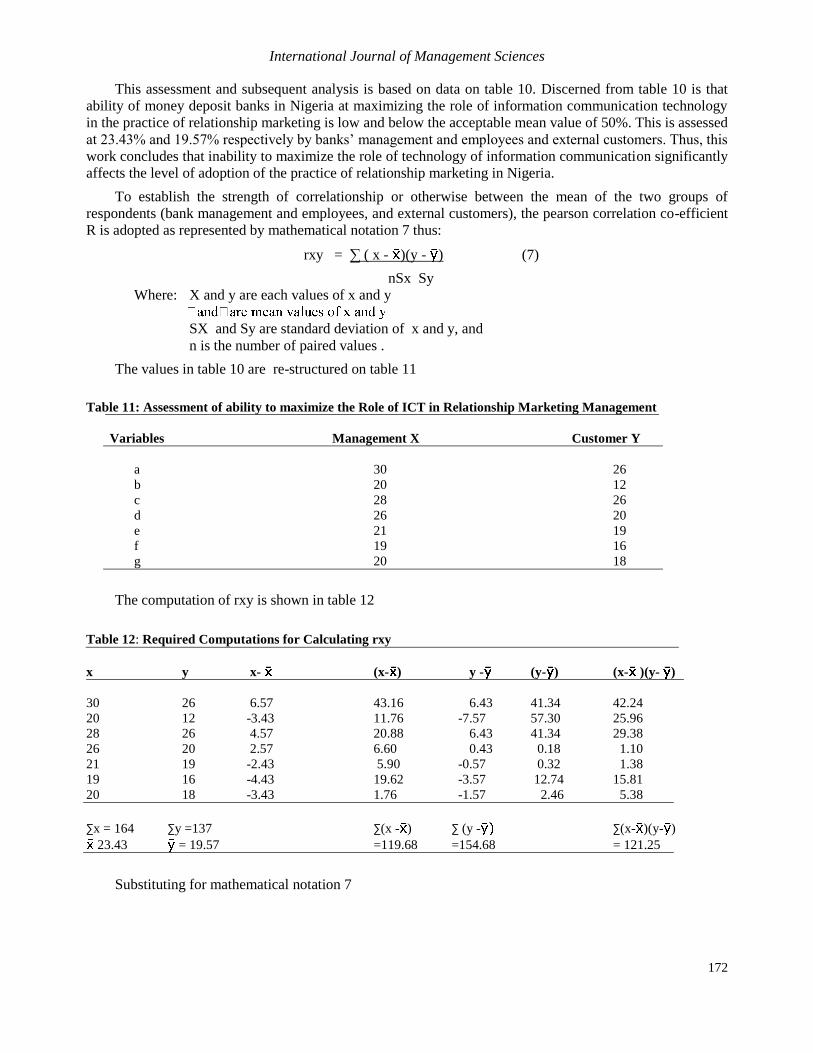

This assessment and subsequent analysis is based on data on table 10. Discerned from table 10 is that

ability of money deposit banks in Nigeria at maximizing the role of information communication technology

in the practice of relationship marketing is low and below the acceptable mean value of 50%. This is assessed

at 23.43% and 19.57% respectively by banks’ management and employees and external customers. Thus, this

work concludes that inability to maximize the role of technology of information communication significantly

affects the level of adoption of the practice of relationship marketing in Nigeria.

To establish the strength of correlationship or otherwise between the mean of the two groups of

respondents (bank management and employees, and external customers), the pearson correlation co-efficient

R is adopted as represented by mathematical notation 7 thus:

rxy = ∑ ( x - )(y - ) (7)

nSx Sy

Where: X and y are each values of x and y

SX and Sy are standard deviation of x and y, and

n is the number of paired values .

The values in table 10 are re-structured on table 11

Table 11: Assessment of ability to maximize the Role of ICT in Relationship Marketing Management

Variables Management X Customer Y

a 30 26

b 20 12

c 28 26

d 26 20

e 21 19

f 19 16

g 20 18

The computation of rxy is shown in table 12

Table 12: Required Computations for Calculating rxy

x y x- (x- ) y - (y- ) (x- )(y- )

30 26 6.57 43.16 6.43 41.34 42.24

20 12 -3.43 11.76 -7.57 57.30 25.96

28 26 4.57 20.88 6.43 41.34 29.38

26 20 2.57 6.60 0.43 0.18 1.10

21 19 -2.43 5.90 -0.57 0.32 1.38

19 16 -4.43 19.62 -3.57 12.74 15.81

20 18 -3.43 1.76 -1.57 2.46 5.38

∑x = 164 ∑y =137 ∑(x - ) ∑ (y - ∑(x- )(y- )

23.43 = 19.57 =119.68 =154.68 = 121.25

Substituting for mathematical notation 7

A. E. N. Oko & S. E. Kalu

173

rxy = ∑ ( x - )( y - )

nSx Sy

= 121.25

7(1.82)(2.08)

= 4.57

Based on the computation, a correlation of 4.57 is established, showing positivity in correlationship

between the assessments of banks management and employees as x variable and employees as y variable.

For the test of significant of the correlation, this work adopts the students’‘t’ test statistic with

mathematical equation represented as 8 thus:

t = r n – 2 (8)

1-r2

= 4.57 7-2

1 – 4.572

= 0.51

Where: r is the value of the pearson correlation

n is the number of paired observations.

To conduct this test, these re-structured hypothesis are considered

H0: µ = 0 (there is a linear relationship between x and y

H0: µ ≠ 0 (there is no linear relationship between x and y

The value of the t computed is 0.56, at 0.05 level of significance and 5 degree of freedom (7-2), the

critical value of the ‘t’ statistics is given as 2.015, This test is significant, thus the null hypothesis is rejected.

Accepted is that there is a linear relationship between the assessment of corporate management and

employees (x) and external customers (y) hence it is inferred that inability to maximize the role of

information communication technology in the banking industry in Nigeria significantly affects the rate and

level of adoption of the practice of relationship marketing.

Test 5

Assessment of the level of efficiency in internal marketing management and its contribution to

efficiency in the adoption of relationship marketing.

Projection:

Accept that inefficiency in internal marketing management does not contribute to inefficiency in the

adoption of relationship marketing in Nigeria, if calculated mean is above 50%

If otherwise reject

This assessment and analysis is based on data generated based on table 13

International Journal of Management Sciences

174

Table 13: Assessment of Variables Considered vital in Internal Marketing Management for Relationship

Marketing

Issues of Assessment Management Employees

a. Policies of employee development of:

i. Recruitment 60 25

ii. Training 55 30

iii. Communication of customers’ value 45 25

iv. Reward system 55 28

v. Administration, internal force in choice of policies

and provision of direction 60 40

b. Internal marketing orientation to relationship marketing goals

and concepts 60 28

c. Building of creative marketing organization based on:

i. Development of company wide passion for internal customers 65 28

ii. Organizational policies built around natural customers segments

rather than service 60 25

iii. Understanding internal customers based on qualitative and

quantitative research 50 18

d. Design and execution of internal customer chain relation 52 21

Total 562 265

Mean 56.2 26.5

It is discerned from table 13, that the mean value for corporate management and employees’ assessment

of the level of efficiency on the adoption of internal marketing as pre-requisite for marketing network based

on interactive marketing and for external marketing –Kotler & Armstrong (2010), Kotler & Keller (2009)

and Berkowitz, Kerin, Hartley & Rudelius (2000), vary; corporate management assessed this at 56.2% while

employees have it as 26.5%. Based on the 50% acceptable mean value, corporate management’s assessment

is high while employees’ assessment is low. This work is inclined to accepting as correct, the assessment of

employees as the internal customer target of internal marketing and the basis of test of efficiency based on

perceived and actual satisfaction.

However, for an unbias conclusion, the mean of the means of the various groups’ assessment is

determined as:

56.2 + 26.5

2

= 41.35%

This 41.35% as mean of means is below acceptable means value of 50%, hence this work concludes that

the level of efficiency in the adoption of internal marketing principles and practices in the money deposit

banking sector in Nigeria is low. This accounts for the poor rate of contribution of relationship marketing to

corporate profitability as external customers are not maximally satisfied based on corporate value creation,

given activities of poorly motivated work force.

For the determination of the degree of significance or otherwise of the variance of the assessment of

corporate management and employees on efficiency in the adoption of internal marketing principles; the

spearman’s rank correlation co-efficiency statistics is adopted as represented by mathematical notation 9

rs = 1 – 6 ∑d2 ( 9)

N(N2 – 1)

A. E. N. Oko & S. E. Kalu

175

Based on values in table 14, rs is computed Table 14: Components of the rs (Efficiency in Adoption of Internal Marketing Practices)

Corporate Employees Rx R1 RX - Ry = (Rx - Ry )2

Management ranking of ranking of d =d2

x y

60 25 6 3 3 9’

55 30 4 8 4 16’

45 25 1 3 -2 9’

55 28 4 7 -3 9’

60 40 6 10 -4 16’

60 25 6 3 3 9

65 28 10 7 3 9

60 25 6 3 3 9

50 18 2 1 1 1

52 21 3 2 1 1

∑d2=83

The hypotheses are presented thus:

H0: There is no significant difference between percentage assessment of corporate management and

employees on the contribution of efficiency in internal marketing practice to efficiency in

relationship marketing in the banking sector of Nigeria.

H1: There is significant different between percentage assessment of corporate management and

employees on the contribution of efficiency in internal marketing practice to efficiency in

relationship marketing in the banking sector of Nigeria.

This test is executed at 0.05 level of significance and the decision rule is to accept the null hypothesis as

the rs is less than the Qr.

Thus substituting for the mathematical notation 9,

rs = 1- 6 ∑d2

N (N2 – 1)

= 1 – 6 (.83)

10(100-1)

= 0.50

The test of significance Qrs for this test statistics is based on mathematical notation 10

Qrs = Z – 1 (10)

n – 1

= 1.96(1)

10.1

= 0.65

International Journal of Management Sciences

176

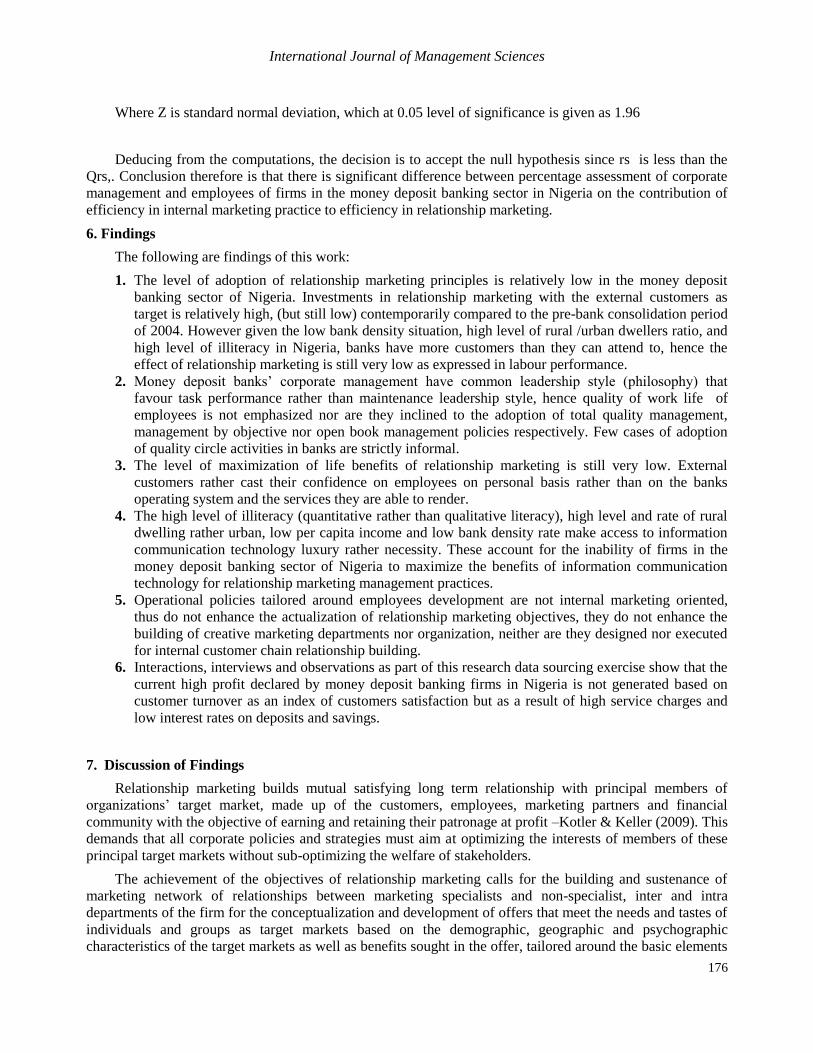

Where Z is standard normal deviation, which at 0.05 level of significance is given as 1.96

Deducing from the computations, the decision is to accept the null hypothesis since rs is less than the

Qrs,. Conclusion therefore is that there is significant difference between percentage assessment of corporate

management and employees of firms in the money deposit banking sector in Nigeria on the contribution of

efficiency in internal marketing practice to efficiency in relationship marketing.

6. Findings

The following are findings of this work:

1. The level of adoption of relationship marketing principles is relatively low in the money deposit

banking sector of Nigeria. Investments in relationship marketing with the external customers as

target is relatively high, (but still low) contemporarily compared to the pre-bank consolidation period

of 2004. However given the low bank density situation, high level of rural /urban dwellers ratio, and

high level of illiteracy in Nigeria, banks have more customers than they can attend to, hence the

effect of relationship marketing is still very low as expressed in labour performance.

2. Money deposit banks’ corporate management have common leadership style (philosophy) that

favour task performance rather than maintenance leadership style, hence quality of work life of

employees is not emphasized nor are they inclined to the adoption of total quality management,

management by objective nor open book management policies respectively. Few cases of adoption

of quality circle activities in banks are strictly informal.

3. The level of maximization of life benefits of relationship marketing is still very low. External

customers rather cast their confidence on employees on personal basis rather than on the banks

operating system and the services they are able to render.

4. The high level of illiteracy (quantitative rather than qualitative literacy), high level and rate of rural

dwelling rather urban, low per capita income and low bank density rate make access to information

communication technology luxury rather necessity. These account for the inability of firms in the

money deposit banking sector of Nigeria to maximize the benefits of information communication

technology for relationship marketing management practices.

5. Operational policies tailored around employees development are not internal marketing oriented,

thus do not enhance the actualization of relationship marketing objectives, they do not enhance the

building of creative marketing departments nor organization, neither are they designed nor executed

for internal customer chain relationship building.

6. Interactions, interviews and observations as part of this research data sourcing exercise show that the

current high profit declared by money deposit banking firms in Nigeria is not generated based on

customer turnover as an index of customers satisfaction but as a result of high service charges and

low interest rates on deposits and savings.

7. Discussion of Findings

Relationship marketing builds mutual satisfying long term relationship with principal members of

organizations’ target market, made up of the customers, employees, marketing partners and financial

community with the objective of earning and retaining their patronage at profit –Kotler & Keller (2009). This

demands that all corporate policies and strategies must aim at optimizing the interests of members of these

principal target markets without sub-optimizing the welfare of stakeholders.

The achievement of the objectives of relationship marketing calls for the building and sustenance of

marketing network of relationships between marketing specialists and non-specialist, inter and intra

departments of the firm for the conceptualization and development of offers that meet the needs and tastes of

individuals and groups as target markets based on the demographic, geographic and psychographic

characteristics of the target markets as well as benefits sought in the offer, tailored around the basic elements

A. E. N. Oko & S. E. Kalu

177

of (place, price promotion and product) marketing. Given this, the vendor is able to secure customer loyalty

as well as retain customers for profit over a long period of customer life span, following reduction in cost of

serving the customers.

The practice of relationship marketing in the money deposit banking sector in Nigeria does not show

these indices as they are cmmon with some advanced economics. These deficiencies are attributed to the

following:

Leadership of most firms in the money deposit banking sector of Nigeria are more performance task

oriented than maintenance task driven, thus employees’ grievances and turnover is high. The imbalance

created favours the welfare of the employers against those of employees, thus employees are always on the

heat of pressure and stress to meet schedules and expectations- Bateman & Snell (2000).

This work also established the fact that employees in the money deposit banking sector of Nigeria feel

they are poorly treated by the reward they receive (implicit and explicit) and the process of determining their