Reinvigorating Growth with a Dynamic Banking Sector AND ACRONYMS ABC African Banking Corporation...

82

Reinvigorang Growth with a Dynamic Banking Sector December 2013 | Edion No. 9 $104 $865 1963 Net Loans and Advances by banks KSh Billion 0 200 2005 337.5 1,491.8 400 800 1,000 1,200 1,400 1,600 2013 GDP per capita CREDIT SAVINGS LOANS CREDIT SAVINGS OVERDRAFT CREDIT SAVINGS LOANS CREDIT SAVINGS OVERDRAFT 2013 Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized

Transcript of Reinvigorating Growth with a Dynamic Banking Sector AND ACRONYMS ABC African Banking Corporation...

Reinvigorating Growth with a Dynamic Banking Sector

December 2013 | Edition No. 9

$104

$865

1963

Net

Loa

ns a

nd A

dvan

ces b

y ba

nks K

Sh B

illio

n

0

200

2005

337.5

1,491.8

400

800

1,000

1,200

1,400

1,600

2013

GDP per capitaCREDITSAVINGSLOANS CREDITSAVINGS

OVERDRAFT

CRED

ITSAVINGS

LOANS CREDITSAVINGS

OVERDRAFT

2013

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

wb456288

Typewritten Text

wb456288

Typewritten Text

wb456288

Typewritten Text

83267

wb456288

Typewritten Text

wb456288

Typewritten Text

Reinvigorating Growth with a Dynamic Banking Sector

TABLE OF CONTENTS

ABBREVIATIONS AND ACRONYMS i

FOREWORD ii

ACKNOWLEDGEMENTS iii

MAIN MESSAGES AND KEY RECOMMENDATIONS iv

EXECUTIVE SUMMARY v

THE STATE OF KENYA’S ECONOMY 11. Economic Performance in 2013 22. Growth Outlook: 2014 and Beyond 24

Special Focus: Increasing Access to Credit 31

REFERENCES 44

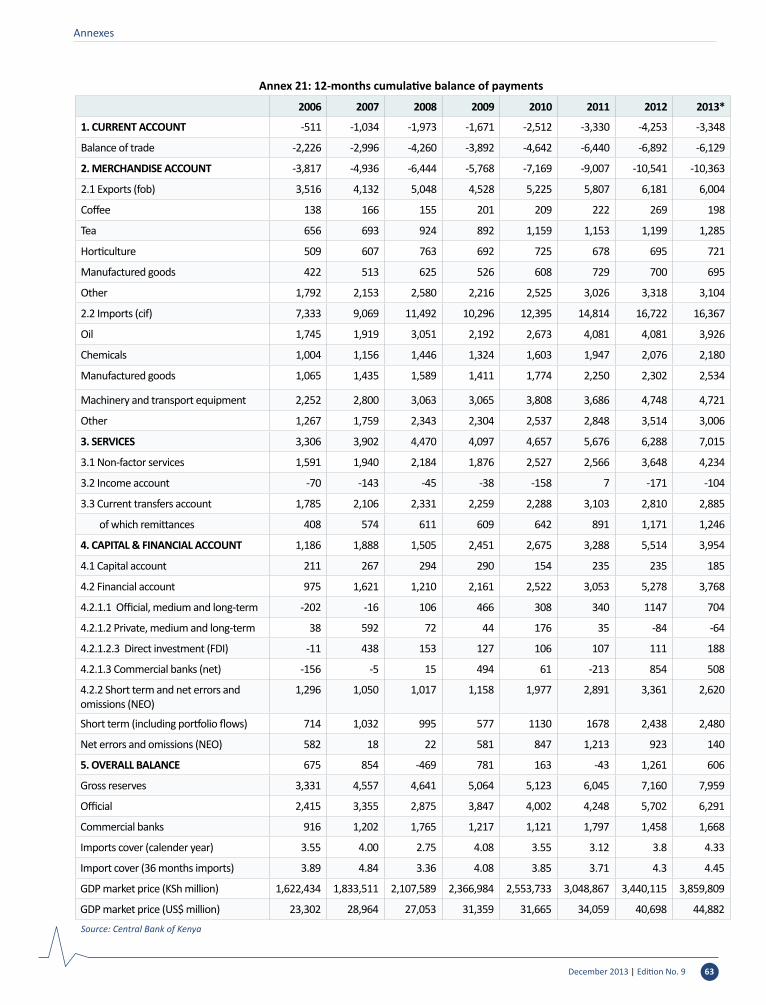

ANNEXESAnnex 1: Macroeconomic environment 44Annex 2: GDP growth rates for Kenya SSA and EAC (2008-2013) 44Annex 3: Kenya annual GDP 45Annex 4.a: Broad sectors growth (half year, percent) 45Annex 4.b: Quarterly growth rates (percent) 46Annex 5: Inflation 47Annex 6: Tea production and exports 48Annex 7: Coffee production and exports 49Annex 8: Horticulture exports 50Annex 9: Local electricity generation by source 51Annex 10: Soft drinks and sugar production 52Annex 11: Tourism arrivals 53Annex 12: New vehicles registration 54Annex 13: Exchange rates 55Annex 14: Interest rates 56Annex 15: Credit to private sector 57Annex 16: Money aggregate 58Annex 17: Mobile payments 59Annex 18: Nairobi stock exchange (20 share index) and the Dow Jones (New York) 60Annex 19: Nominal and real exchange rate 61Annex 20: Fiscal position 62Annex 21: 12-months cumulative balance of payments 63Annex 22: Growth Outlook 64

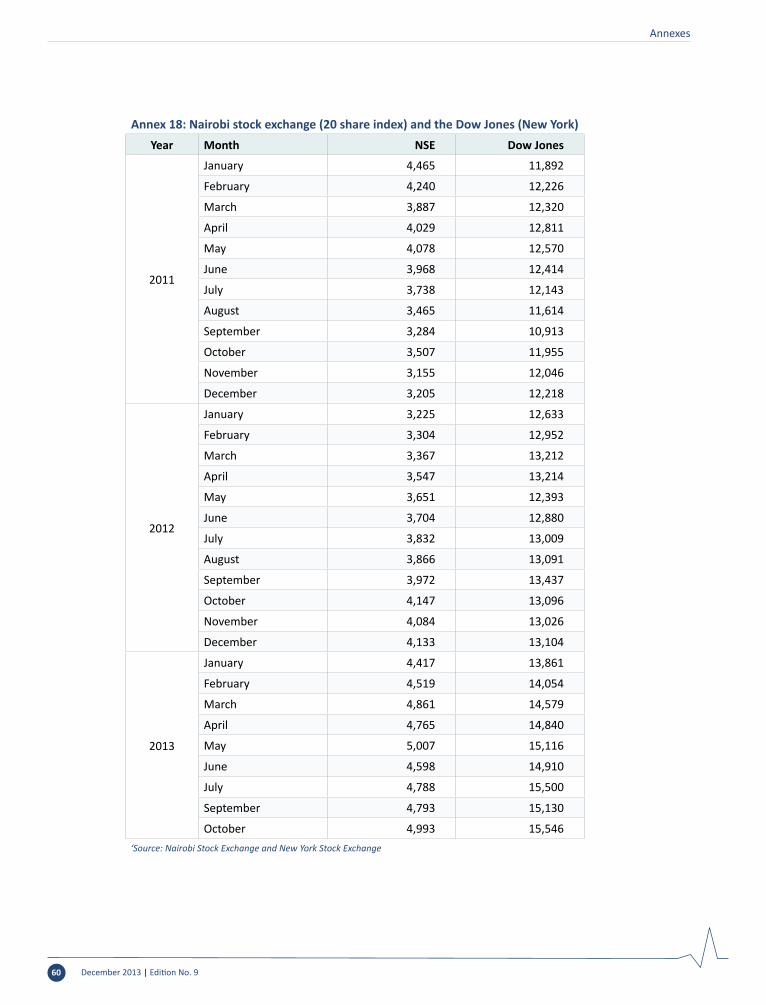

LIST OF FIGURESFigure 1: Kenya’s macroeconomic environment is strong vFigure 2: Budget execution remains a challenge viiFigure 3: Kenya has made tremendous progress in financial inclusion viiFigure 4: Kenyan banks lend more to small and medium-size enterprises than banks in some viii other countries in the regionFigure 5: Overheads and profits account for the bulk of interest rate spreads in Kenya viiiFigure 1.1: Modest growth in the first half of 2013 represented Kenya’s best first-half 2 performance since 2008Figure 1.2: Average growth was lower in Kenya than in most of its neighbors and 3 Sub-Saharan Africa as whole between 2009 and 2013Figure 1.3: For decades, Kenya has been more globally integrated than its neighbors 3Figure 1.4: All sectors except services showed strong growth in the first half of 2013 3Figure 1.5: Performance in the services sector was mixed in 2013 4Figure 1.6: Kenyans continue to embrace information and communications technology products 5Figure 1.7: The mobile money (M-Pesa) transfer boom continued 5Figure 1.8: Tourism contracted—partly as a result of security concerns 5Figure 1.9: A good harvest led to lower food prices 7Figure 1.10: Food inflation rose after June 2013, driving overall inflation 7Figure 1.11: The contribution of food to overall inflation rose in 2013 8Figure 1.12: Inflationary trends in the regions are roughly similar 8Figure 1.13: Rwanda has much stronger Doing Business indicators than Kenya 8Figure 1.14: Implementation of the new constitution triggered expansionary spending 9Figure 1.15: After years of narrowing, the gap between recurrent and development expenditure 10 widenedFigure 1.16: Low execution rates reduced development expenditure 11Figure 1.17: Income tax revenues rose and VAT and excise duties fell between 1999 and 2012 12Figure 1.18: Total and domestic public debt as a percent of GDP increased, and external debt fell 12Figure 1.19: The upward movement in the yield curve reflects market concerns about 12 budget implementationFigure 1.20: To support economic activity, Kenya’s Central Bank increased the money supply 13Figure 1.21: Liquidity shortages in the banking system dampened the effect of monetary policy 13 on interest ratesFigure 1.22: Lending rates declined marginally, but interest spreads remained wide 14Figure 1.23: Banking sector credit expanded, but the level remains below historical levels 14Figure 1.24: Credit to the private sector has not grown as rapidly as GDP since 2011 15Figure 1.25: Credit flowed to private households, trade, and business services—but 15 not to productive sectorsFigure 1.26: Households, trade, and real estate received the lion’s share of loans from 16 the banking systemFigure 1.27: Asset quality deteriorated in most sectors 16

Figure 1.28: The Nairobi Stock Exchange outperformed the Dow Jones Industrial average 17Figure 1.29: Short-term capital inflows are financing the current account deficit 18Figure 1.30: The trade balance improved significantly, as oil imports declined 18Figure 1.31: Slower global activity and weak local conditions reduced Kenya’s exports and imports 18Figure 1.32: Remittances continued to rise 20Figure 1.33: Kenya is attracting more short-term than long-term flows 20Figure 1.34: The Kenya shilling stabilized 21Figure 1.35: Kenya’s trade-weighted exchange rates are starting to depreciate as the 22 global economy recoversFigure 2.1: Growth will pick up in 2014, driven by investment and public spending 25Figure 3.1: Ownership structure of Kenyan banks 31Figure 3.2: Deposits, loans, and credit to the private sector have grown steadily 32Figure 3.3: Kenyan banks lend more to SMEs than in banks in some other countries in the region 33Figure 3.4: Banks’ response to the monetary policy rate has been asymmetric 37Figure 3.5: Interest rate spreads in Kenya have fallen over time 38Figure 3.6: Spreads are made up largely of overheads and profits 38Figure 3.7: Large banks account for most deposits and loans in Kenya 38Figure 3.8: Large banks in Kenya have higher spreads than smaller banks 39Figure 3.9: Large banks in Kenya offer lower rates on deposits than small banks 39Figure 3.10: Average lending rates are higher and less volatile than Treasury-bill rates 39

LIST OF TABLESTable 1.1: Kenya’s Doing Business environment has deteriorated since 2008 10 Table 1.2: Government expenditure rose between 2008/09 and 2012/13 11Table 1.3: Shares of imports by broad economic category, 2009–2013 19Table 2.1: GDP is projected to grow by a little more than 5 percent through 2016 25 (annual percentage increase)Table 3.1: Large banks dominate both the share of deposits and net yield 35Table 3.2: Selected donor partnerships with Kenyan banks 36Table 3.3: Donors have partnered with Kenyan banks to increase lending to small and 42 medium-size enterprises

LIST OF BOXESBox 1.1: Tourism: A pillar for economic growth and job creation 6Box 1.2: Is Kenya’s real exchange rate over- or undervalued? 23Box 2.1: Lack of efficiency in education and health: Results from the World Bank’s 29 Service Delivery Indicators

ABBREVIATIONS AND ACRONYMS

ABC African Banking CorporationAML/CFT Anti-money Laundering - Combating the Financing of TerrorismCBA Commercial Bank of AfricaCBK Central Bank of KenyaCBR Central Bank RateCIF Cost Insurance FreightCOMESA Common Market for Eastern and Southern AfricaCoop Bank Cooperative BankCRB Credit Reference BureauDB Doing BusinessDEG Deutsche Investitions- und Entwicklungsgesellschaft (Germany Investment Corporation)DSA Debt Sustainability AnalysisEAC East African CommunityFDI Foreign Direct InvestmentFMO Financierings-Maatschappij voor Ontwikkelingslanden (Netherlands Development Finance Company)FSAP Financial Sector Assessment ProgramG2P Government to PersonGDP Gross Domestic ProductGEMS Growth Enterprise Market SegmentI&M Investments and MortgagesICT Information Communication and TechnologyIFMIS Integrated Financial Management Information SystemIMF International Monetary FundKCB Kenya Commercial BankKfW Kreditanstalt für Wiederaufbau (Reconstruction Credit Institute)MTPII Second Medium Term Plan NEO Net Errors and OmissionsNFS Non-factor ServicesNorfund Norwegian Investment FundNSE Nairobi Stock ExchangePFM Public Financial ManagementPROPARCO Promotion et Participation pour la Coopération EconomiqueREER Real Effective Exchange RateSACCOs Savings and Credit CooperativesSIDA Swedish International Development AgencySIM Subscriber Identity ModuleSMEs Small and Medium EnterprisesTTCI Travel and Tourism Competitiveness IndexUS United StatesUSAID United States Agency for International DevelopmentVAT Value Added Tax

December 2013 | Edition No. 9 i

It is my pleasure to present the ninth edition of the Kenya Economic Update, which coincides with Kenya’s 50th independence anniversary. There is much for Kenya to celebrate—economically, socially, and

institutionally. Kenya has a strong track record of macroeconomic management, with low inflation, low fiscal deficits, and sustainable debt levels. Economic growth has not been as high as in its peers, but Kenya’s market-oriented policies have paid dividends. Kenya’s private sector is more vibrant, its financial sector is now the third largest in terms of assets in Sub-Saharan Africa, and citizens have benefited enormously from the mobile revolution. In the social sectors, Kenya has made tremendous progress. Kenyans are living two decades longer than they did at independence, infant mortality has fallen by 50 percent, and primary school enrollment is now almost universal (and full gender parity almost achieved). What’s more, the new Constitution, passed in 2010, has created a strong foundation for better institutions. The jubilee year is a time for celebration. But it is also a time to reflect on the measures needed to transform the lives of the majority of Kenyans. Nearly 4 of every 10 Kenyans is poor; maternal mortality remains among the highest in Africa, with 488 deaths per 100,000 live births; secondary school enrollment is at a low 32 percent; and learning achievement levels, well below their potential for what is needed to fuel a modern market economy.

This report has three main messages. First, the economy is estimated to have grown at 5 percent in 2013, and Kenya will enter 2014 on a strong economic position. This is a major achievement, as Kenya’s growth usually collapses during election years. With a strong macroeconomic foundation and ongoing structural reforms, this growth momentum is expected to be maintained in 2014, when output is projected to grow by 5.1 percent. Second, an enabling framework for significant private sector–led growth is critical. Continued investment is needed in infrastructure, bottlenecks that increase the cost of doing business need to be addressed, and sound monetary and fiscal policies need to be maintained. Third, Kenyan banks are ahead of their counterparts in other African countries in many innovations, including lending to the SMEs but the cost of bank financing remains high,an issue the report discusses in some depth.

The World Bank remains a committed partner as Kenya celebrates its jubilee year and beyond. Its series of Economic Updates, published every six months, have become its main vehicle for analyzing development trends in Kenya. Through these reports and other knowledge products, the World Bank aims to support all those who want to improve economic management in Kenya. As in the past, we are proud to have worked with many Kenyan economic stakeholders during the preparation of this report. We hope that they will join us in debating the policy issues that are topical in Kenya and in contributing to helping Kenya grow, permanently reduce poverty, and bring shared prosperity to all Kenyans.

Diarietou GayeCountry Director for Kenya

World Bank

FOREWORD

December 2013 | Edition No. 9ii

ACKNOWLEDGEMENTS

This edition of the Kenya Economic Update was prepared by a team led by John Randa and Smita Wagh, supervised by Apurva Sanghi. The core team consisted of Angélique Umutesi, Kennedy Mukuna Opala,

Margaret Nyamumbo, Barbara Karni, and Sophie Rabuku. The team gratefully acknowledges contributions from Robert Waiharo.

The report benefitted from the insights of several peer reviewers, including Yira Mascaro, Ravi Ruparel, and Prof. Terry Ryan, as well as comments from Jane Kiringai, Gunhild Bergn, Maria Paulina Mogollon, and Evans Osano. The team also received guidance from Pablo Fajnzylber, Thomas O’Brien, and Diarietou Gaye.

Partnership with key Kenyan policy makers was instrumental in the production of this report. On December 3, 2013, a draft of the report was presented at the Quarterly Economic Roundtable. The meeting was attended by senior officials from the National Treasury, the Ministry of Devolution and Planning, the Central Bank of Kenya, the Kenya National Bureau of Statistics, the Kenya Revenue Authority, the Kenya Institute of Public Policy Research and Analysis, the International Monetary Fund, and the National Economic and Social Council.

December 2013 | Edition No. 9 iii

MAIN MESSAGES AND KEY RECOMMENDATIONS

Main Messages

• Macroeconomic conditions are favorable in Kenya, with the economy projected to grow 5.0 percent in 2013 and 5.1 percent in 2014. Inflation remains low, the fiscal deficit remains manageable, and the exchange rate remains stable.

• The government has maintained fiscal discipline, adopting domestic revenue-raising measures. However, execution of the budget, especially investment spending, leaves room for improvement. Higher execution rates would help promote the much sought after growth take-off.

• Small and medium-size enterprises (SMEs) cite the cost of credit as a barrier to bank financing. High lending rates can be traced to a range of factors, including the macroeconomic environment, high bank overheads and profits, information gaps, the structure of the banking sector, and the volatility of the risk-free return. A multipronged approach is needed to increase bank lending to this critical sector if growth and job creation are to take-off.

Key Recommendations for Reinvigorating the Economy

• Continue structural reforms to improve the ease of doing business environment and boost growth in the near term. Reductions in delays in the clearance of cargo at the Port of Mombasa and recent measures to address the challenges of transporting cargo along the northern corridor are steps in the right direction to promoting regional trade. The removal of all roadblocks along the routes of cargo destined to countries in the region as part of the wider initiative to curb trade bottlenecks is a major step. Scaling up Huduma centers, which provide one-stop-shop delivery of services, should enhance the business environment and reduce inefficiency, which encourages corruption.

• Improve budget absorption of development expenditures, which are key to growth. Execution of the budget, especially investment spending, needs improvement. Higher execution rates would help promote the much sought after growth take-off. As part of the transition to the new government, new procurement has been a challenge.

• Deepen reforms in public financial management (PFM) to increase savings and efficiency in the use of public resources. Adopting and operationalizing PFM regulations to entrench the PFM law would help ensure accountability, transparency, and the effective and efficient collection and utilization of public resources. Efforts should include making the Integrated Financial Management Information System (IFMIS) and the Treasury Single Account fully functional.

Key Recommendations for Increasing access to Credit to SMEs

• Study the factors that influence the way in which banks price loans, in order to develop a comprehensive policy agenda for reducing the cost of credit. The competitive structure of the banking sector in Kenya cannot be viewed in isolation. A host of other factors, such as the macroeconomic environment, government borrowing, bank overheads, risk premiums, and market maturity, all contribute to determining the interest structure, including the cost of credit, in an economy.

• Strengthen credit information systems and other parts of the financial infrastructure. Information asymmetries raise the pricing of loans to SMEs in Kenya. The high levels of informality within the sector and inadequate systems of collateral verification hinder lending. Banks, savings and credit cooperatives (SACCOs), payment service providers, and utility companies should be encouraged to share positive information about consumers. Effective collateral registries should be developed and creditor rights framework strengthened.

• Diversify funding sources and instruments for SMEs. It is important that at least some SMEs look beyond bank financing to meet their working capital needs if they are to fully realize their growth and job-creating potential. Efforts should be made to enable some SMEs to tap equity funding, either through private funds or through the Growth Enterprise Market Segment of the Nairobi Stock Exchange.

December 2013 | Edition No. 9iv

Growth has picked up, and prospects for 2014 are strong

After 50 years of independence, there is much for Kenya to celebrate. Kenyans are

living two decades longer; the fertility and infant mortality rates have been cut in half; and school enrollment, at both the primary and secondary level, has more than doubled. On the economic front, GDP per capita increased eightfold; the largest share of GDP is the services sector, not agriculture; and the financial sector is now the third largest in Sub-Saharan Africa (after South Africa and Nigeria). These accomplishments are extraordinary. But the country’s 50th anniversary is also the time to reflect on measures needed to transform the lives of the majority of Kenyans. Nearly 4 of every 10 Kenyans live in poverty; maternal mortality is among the highest in Africa, with 488 deaths per 100,000 live births, secondary school enrollment is at a low 32 percent; and learning achievement levels are well below their potential and what is needed to fuel a modern market economy. GDP growth, while solid, has yet to takeoff at the rapid, sustained rate needed to transform the lives of ordinary citizens.

Kenya’s overall macroeconomic conditions are favorable. Growth is picking up, inflation remains low, the fiscal deficit remains manageable, and the exchange rate remains stable. The economy is estimated to have grown by 5.0 percent in 2013, up from 4.6 percent in 2012—the highest level since 2010, when the economy grew by 5.8 percent. This performance, although weak for East Africa, is commendable given Kenya’s history of low growth during election years (during which output rose less than 3 percent on average). Growth was driven mainly by consumption and to some extent investment. There was little volatility in international oil prices, and rainfall was adequate, which helped stabilize both food and energy prices. Year-on-year inflation was 7.4 percent in November 2013, and average inflation was 5.6 percent, down from 9.6 percent in 2012. Netting out the impact of the recent VAT increases, the inflation rate is within the 2 percentage-point margin of the 5 percent medium-term target.

Kenya will enter 2014 from a strong economic position. With inflationary pressure subdued—underpinned by stable energy prices and

December 2013 | Edition No. 9 v

EXECUTIVE SUMMARY

Figure 1: Kenya’s macroeconomic environment is strong

Source: World Bank, based on data from the Kenya National Bureau of Statistics

-6

-4

-2

0

2

4

6

8

10

4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2

2006 2007 2008 2009 2010 2011 2012 2013

GDP growth is picking up

Total GDP Agriculture GDP Non-agriculture GDP

0

5

10

15

20

25

30

Feb

Mar

Apr

May Jun Jul

Aug

Sept

Oct

Nov De

cJa

nFe

bM

arAp

rM

ay Jun Jul

Aug

Sept

Oct

Nov De

cJa

nFe

bM

arAp

rM

ay Jun Jul

Aug

Sept

Oct

Nov De

cJa

nFe

bM

arAp

rM

ay Jun Jul

Aug

Sept

Oct

Nov

2010 2011 2012 2013

Perc

ent

Perc

ent

Inflation has remained within the target range

Food inflation Core inflation Overall inflation

Executive Summary

December 2013 | Edition No. 9vi

moderation in food inflation, a stable exchange rate, and supportive monetary policy—Kenya has the potential for a growth spurt in 2014 (Figure 1). The government has set a bold agenda of reform outlined in the second Medium Term Plan (MTP II). However, it is the structural reforms currently being implemented that will boost growth in the near term. Reductions in delays in the clearance of cargo at the Port of Mombasa and recent measures to address the challenges of transporting cargo along the northern corridor are steps in the right direction to promoting regional trade. The removal of all roadblocks along the routes of cargo destined to countries in the region as part of the wider initiative to curb trade bottlenecks is a major step. “Huduma” centers, which provide one-stop-shop delivery of services, should curb the inefficiency that encouraged corruption and enhance the business environment.

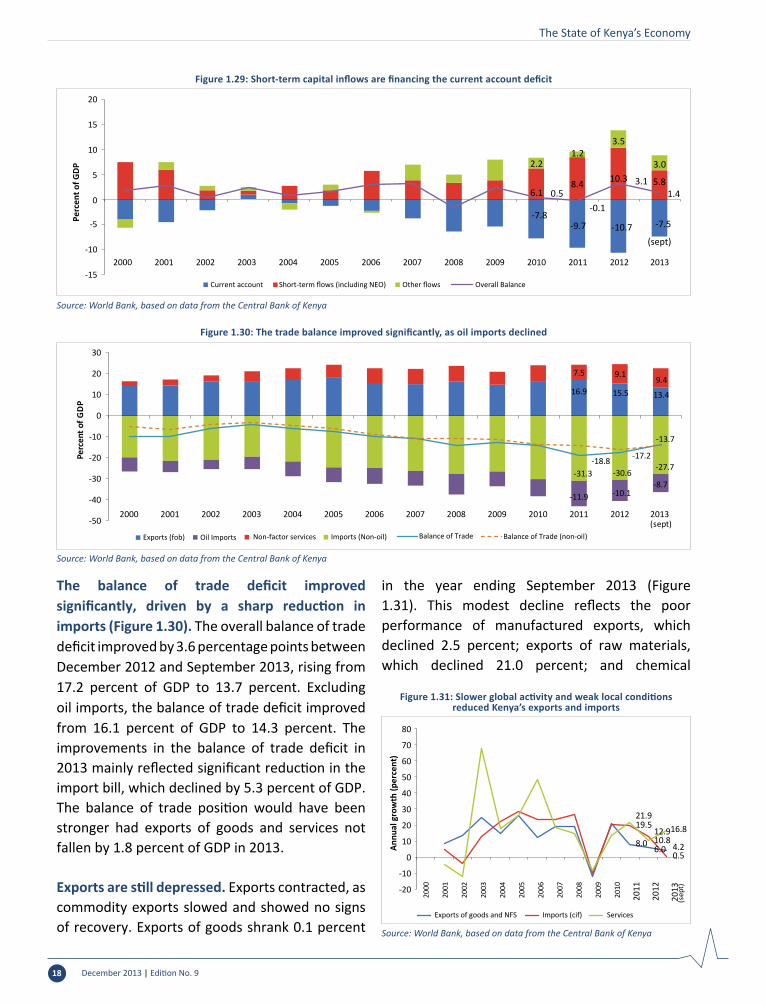

Kenya strengthened its external position substantially in recent years, accumulating international reserves to meet program targets under the successfully completed IMF program. At the same time, the financing of current account deficit presents challenges and risks. The current account deficit, which averaged more than 10 percent of GDP in 2011 and 2012, narrowed in 2013 to 7.5 percent of GDP by September 2013. The improvement reflected lower import demand and higher exports of services. However, there are risks that the current account will deteriorate when imports pick up as the economy regains strength. The current account deficit is expected to remain high partly because of the need for imports of capital goods to support the construction of large-scale infrastructural projects and exploration for gas and oil. Financing of the current account deficit is primarily through short-term flows, as

foreign investors look for higher yields on their portfolios. Such inflows help to build reserves at the Central Bank and to finance the current account deficit, but they also increase Kenya’s vulnerability, because they are prone to investor risk aversion and can change abruptly in response to political and economic events.

The government maintained fiscal discipline, adopting domestic revenue-raising measures. However, execution of the budget, especially investment spending, leaves room for improvement. Higher execution rates would help promote the much sought after growth take-off. As part of the transition to the new government,

new procurement was suspended in the first quarter of 2013, and spending by the government slowed dramatically. The result was two-fold. First, low spending meant that government deposits built up at both the Central Bank (draining the banking system of liquidity) and at commercial banks where government holds deposits

(skewing liquidity to few banks). As a result, liquidity was tight in the banking system, with some banks with excess cash and others short of liquidity causing interbank rates to sour and muting the impact of supportive monetary policy actions. Second, the freeze in spending before the election and the changes in administration after it, brought development spending almost to a halt. Concerns about governance during the electioneering period limited government procurement and payments and reduced capital spending in the second half of fiscal 2012/13. The effect on infrastructure projects slowed economic growth. Moreover, the new administration reduced the number of ministries from 44 to 18. This consolidation though commendable had the undesirable effect as new procedures delayed the disbursement of funds (Figure 2).

The government’s policy of avoiding nonconcessional

borrowing has been a key factor in sustainable

debt management

A more dynamic banking sector could accelerate growth

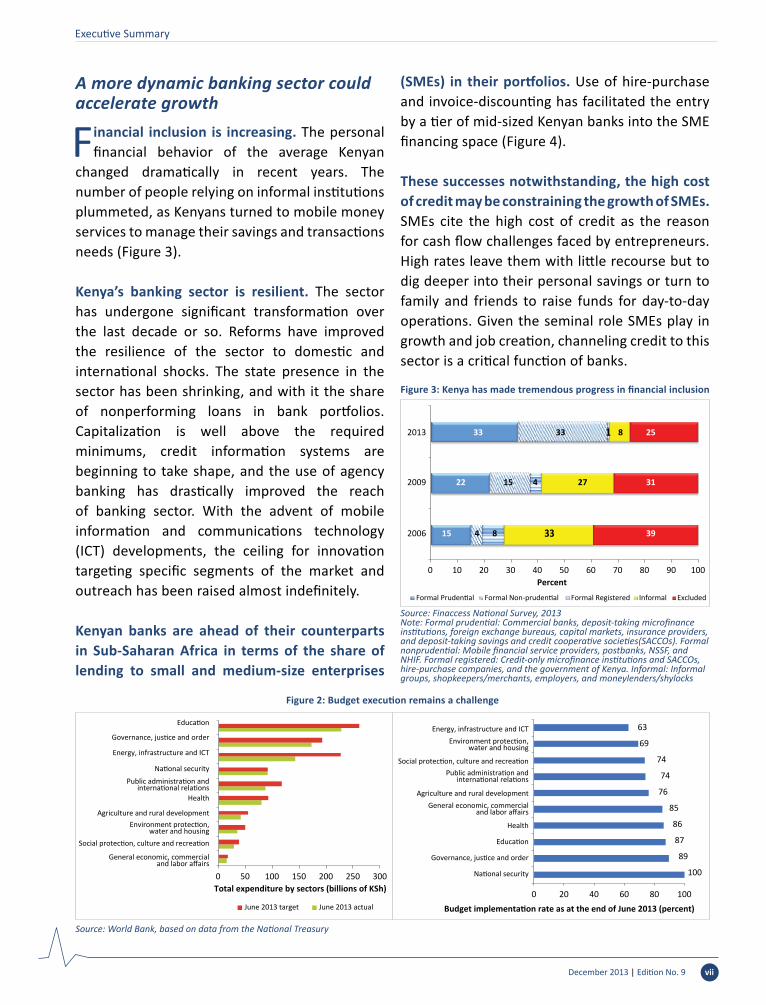

Financial inclusion is increasing. The personal financial behavior of the average Kenyan

changed dramatically in recent years. The number of people relying on informal institutions plummeted, as Kenyans turned to mobile money services to manage their savings and transactions needs (Figure 3).

Kenya’s banking sector is resilient. The sector has undergone significant transformation over the last decade or so. Reforms have improved the resilience of the sector to domestic and international shocks. The state presence in the sector has been shrinking, and with it the share of nonperforming loans in bank portfolios. Capitalization is well above the required minimums, credit information systems are beginning to take shape, and the use of agency banking has drastically improved the reach of banking sector. With the advent of mobile information and communications technology (ICT) developments, the ceiling for innovation targeting specific segments of the market and outreach has been raised almost indefinitely.

Kenyan banks are ahead of their counterparts in Sub-Saharan Africa in terms of the share of lending to small and medium-size enterprises

(SMEs) in their portfolios. Use of hire-purchase and invoice-discounting has facilitated the entry by a tier of mid-sized Kenyan banks into the SME financing space (Figure 4).

These successes notwithstanding, the high cost of credit may be constraining the growth of SMEs. SMEs cite the high cost of credit as the reason for cash flow challenges faced by entrepreneurs. High rates leave them with little recourse but to dig deeper into their personal savings or turn to family and friends to raise funds for day-to-day operations. Given the seminal role SMEs play in growth and job creation, channeling credit to this sector is a critical function of banks.

December 2013 | Edition No. 9 vii

Executive Summary

Figure 3: Kenya has made tremendous progress in financial inclusion

Source: Finaccess National Survey, 2013Note: Formal prudential: Commercial banks, deposit-taking microfinance institutions, foreign exchange bureaus, capital markets, insurance providers, and deposit-taking savings and credit cooperative societies(SACCOs). Formal nonprudential: Mobile financial service providers, postbanks, NSSF, and NHIF. Formal registered: Credit-only microfinance institutions and SACCOs, hire-purchase companies, and the government of Kenya. Informal: Informal groups, shopkeepers/merchants, employers, and moneylenders/shylocks

15

22

33

4

15

33

8

4

1

33

27

8

39

31

25

0 10 20 30 40 50 60 70 80 90 100

2006

2009

2013

Percent

Formal Prudential Formal Non-prudential Formal Registered Informal Excluded

Figure 2: Budget execution remains a challenge

Source: World Bank, based on data from the National Treasury

0 50 100 150 200 250 300Total expenditure by sectors (billions of KSh)

June 2013 target June 2013 actual

100

89

87

86

85

76

74

74

69

63

0 20 40 60 80 100

National security

National security

Governance, justice and order

Governance, justice and order

Education

Education

Health

HealthGeneral economic, commercial

and labor affairs

General economic, commercialand labor affairs

Agriculture and rural development

Agriculture and rural development

Public administration andinternational relationsPublic administration and

international relations

Social protection, culture and recreation

Social protection, culture and recreation

Environment protection,water and housing

Environment protection,water and housing

Energy, infrastructure and ICT

Energy, infrastructure and ICT

Budget implementation rate as at the end of June 2013 (percent)

Executive Summary

December 2013 | Edition No. 9viii

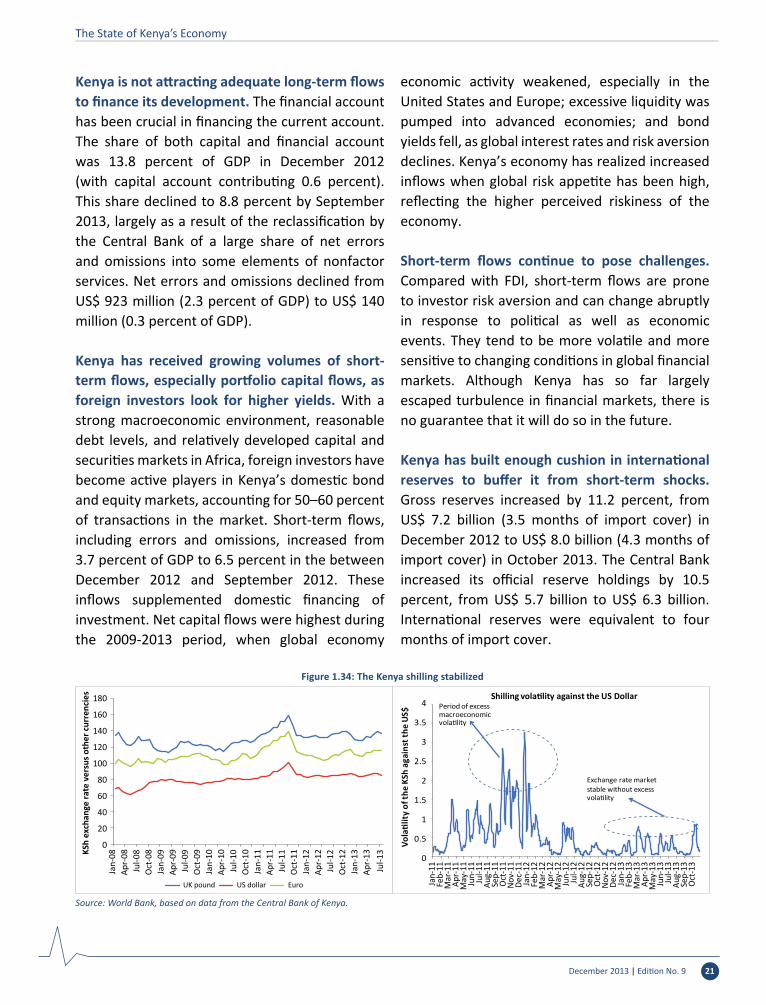

One criticism of the Kenyan banking sector is that the interest rate spread is high. The difference between the average rate of interest charged by banks on loans to customers and the average rate of interest banks pay on savings deposits remains persistently high, at the same time as banking sector profitability has grown (Figure 5). This perception of high spreads and growing profitability has left the industry open to repeated criticisms of collusive price-setting behavior. However, it is important to note that no hard rules prescribe the optimal interest spreads that correspond to specific market conditions; there is no definitive way to determine whether spreads are too high, too low, or just right, especially when information markets are incomplete.

Although it is difficult prima facie to determine whether spreads are “appropriate,” it is possible to dig deeper into the factors that affect the cost of credit in Kenya. Such factors include the overall macroeconomic and policy environment; market structure and price-setting behavior; the return on risk-free assets; the interest rate structure; and the risks (and perceived risks) associated with lending to SMEs, which are affected by information asymmetries, the level of informality, and the high costs of loan recovery in case of default.

Other challenges remain. The building blocks for the path forward are already falling into place, though some areas may need more effort than others. Recent improvements in the financial infrastructure through a better collateral registry system and a more effective creditor rights framework will plug some of the information gaps and enable banks to price risks at a lower level. A sound government debt management policy (essentially a regular issuance policy that lowers the volatility of the returns on the risk-free asset) that informs a stable interest rate structure will improve the transparency and predictability of the credit pricing models. Efforts to strengthen capital markets, pensions, and the insurance sector so that SMEs can access alternative sources and instruments for their financing needs will pay dividends. These developments will serve Kenya well in reaching its goal of attaining middle-income status. A mature banking sector—and more generally, a well-developed financial sector that supports a vibrant private sector—will be an important advantage to achieving the Vision 2030 goals.

The State of Kenya’s EconomyFigure 4: Kenyan banks lend more to small and medium-size enterprises than banks in some other countries in the region

Source: World Bank, 2013

0

2

4

6

8

10

12

14

16

18

20

Nigeria South Africa Tanzania Rwanda Kenya

Shar

e of

tota

l ban

k le

ndin

g th

at g

oes

to S

MEs

(per

cent

)Figure 5: Overheads and profits account for the bulk

of interest rate spreads in Kenya

Source: World Bank, based on data from the Central Bank of KenyaNote: Ex post spreads are calculated based on the actual balance sheets and profit and loss accounts (ex ante spreads are based on the difference between deposit and lending rates). The trends in the two measures are similar

0.6 0.6 0.7 0.9

4.5 4.0 4.34.7

0.80.9 0.4

0.5

4.2 5.0 5.75.6

0

2

4

6

8

10

12

2009 2010 2011 2012

Perc

ent

Reserves Overheads Provisions Profit

Executive Summary

The State of Kenya’s Economy

The State of Kenya’s Economy

December 2013 | Edition No. 92

The World Bank expects that Kenya’s GDP will grow 5.0 percent in 2013, marginally higher than the 4.6 percent growth achieved in 2012. Domestic factors played a role in the lower than expected

growth, reflecting a weakening investment climate, unsupportive fiscal environment at both the national and county level, and slow transmission of accommodative monetary policy stance into lower lending rates. There was good news in 2013, however: the current account deficit narrowed considerably, from more than 10 percent of GDP to 7.5 percent, reducing the economy’s vulnerability to external shock, and for the first time in years, the economy avoided the election-growth curse of lower growth in an election year.

1. Economic Performance in 2013

1.1 Growth Picked Up—Although It Remains below Potential

Growth accelerated in 2013. Macroeconomic conditions continued to improve, as

Kenya’s economy entered the third year of relative stability, with single-digit inflation and a stabilized exchange rate. GDP growth was lower than projected. However, despite the peaceful presidential election and smooth transfer of power in March 2013, the growth momentum generated in the last quarter of 2012 was lost in the second and third quarters of 2013, held down by lack of government spending and inadequate transmission of the monetary policy stance to the real economy.

The challenges facing government spending during the transition slowed growth, which is expected to reach 5.0 percent in 2013. Monetary policy efforts to stimulate the economy through accommodative monetary policy were thwarted by lack of liquidity in the banking system, which increased short-term rates, as government deposits accumulated at the Central Bank and the few commercial banks where the government had its deposits outside the Central Bank.

Monetary policy supported growth in 2013, as the Central Bank reduced its policy rate and provided liquidity support to the banking system. Intervention through repo operations prevented interbank rates from overshooting. Credit

activity remained subdued, as banks became more reluctant to lend during the transition and demand for credit waned in light of weaker business prospects.

GDP growth of 4.7 percent in the first half of 2013 was driven by the robust performance of agriculture and industry. Growth was higher than the 4.3 percent during the same period in 2012 and the highest growth in the first half of the year since 2008 (Figure 1.1). Abundant rain increased crop production and hydropower generation, which improved performance in both agriculture and industry. Low interest rates, low inflation, and a stable shilling created a better macroeconomic environment for industry and businesses in the first half of 2013.

Figure 1.1: Modest growth in the first half of 2013 represented Kenya’s best first-half performance since 2008

Source: World Bank calculations based on data from the Kenya National Bureau of Statistics.Note: Estimate for the second half of 2013 is based on revised annual growth projection of 5.0 percent.

1.7 1.4

4.0

1.6

3.7

7.8

4.24.5 4.3

4.8 4.75.3

0

1

2

3

4

5

6

7

8

9

H1 H2 H1 H2 H1 H2 H1 H2 H1 H2 H1 H2

Annu

al g

row

th (p

erce

nt)

2008 2009 2010 2011 2012 2013

December 2013 | Edition No. 9 3

The State of Kenya’s Economy

The economy is still underperforming compared to its neighbors. Average annual growth in Kenya was 4.4 percent in 2008-2013, much lower than in Uganda (5.6 percent), Tanzania (6.6 percent), Rwanda (7.3 percent), and Sub-Saharan Africa average as a whole (5.5 percent) (Figure 1.2).

Global volatility affected Kenya’s economic activity more than its neighbors’ because its economy is more integrated with the global economy (Figure 1.3). Average trade (exports plus imports) as a share of GDP stood at 66.6 percent during 2005-2011—a larger share than Tanzania (63.4 percent) or Uganda (51.5 percent).

The recent decline in global commodity prices constrained exports in the region as a whole; Kenya’s greater integration into the global economy leaves it particularly vulnerable to global oil price upsurges, exchange rate volatility, and global recession.

The first half of 2013 saw a rebound in agricultural output. Agriculture grew at an annual rate of 6.7 percent—three times the rate in the previous two years (Figure 1.4). Strong agricultural performance was the result of above-average rainfall, which boosted crop production. The uptick reflected much better climatic conditions than in 2012, when frost adversely affected tea production. Tea production rose from a low of 11 percent in the year ending July 2012 to a robust rate of growth of 38 percent during the same period in 2013, according to the Kenya National Bureau of Statistics. The production and export of tea increased despite civil unrest in Egypt, a major importer of Kenyan tea. Improved supply and continued low demand from Kenya’s trading partners caused commodity prices to fall. Despite the decline, exports from tea and horticulture exports increased, as a result of higher volume. The volume of tea production grew 42.6 percent in the first half of 2013, while the auction price dropped 7.6 percent. The volume of horticulture exports increased 12.2 percent,

Figure 1.2: Average growth was lower in Kenya than in most of its neighbors and Sub-Saharan Africa as a whole between 2008 and 2013

Source: World Bank, based on data from the Kenya National Bureau of Statistics and the World Bank.Note: 2013 projections are based on World Economic Prospects, except for Kenya, which was based on the revised projection of 5 percent.

4.04.4

5.5 5.6

6.67.3

0

1

2

3

4

5

6

7

8

Burundi Kenya Sub-Saharan Africa excluding

South Africa

Uganda Tanzania Rwanda

Annu

al g

row

th 2

009-

2013

(per

cent

)

Figure 1.3: For decades, Kenya has been more globallyintegrated than its neighbors

Source: World Development indicators database

0

10

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

20

30

40

50

60

70

80

Shar

e of

trad

e (e

xpor

ts +

impo

rts)

to G

DP (p

erce

nt)

Burundi Kenya Rwanda Uganda Tanzania

Figure 1.4: All sectors except services showed strong growth in the first half of 2013

Source: World Bank, based on data from the Kenya National Bureau of Statistics

2.0

3.5

4.3

5.2

2.11.8

4.9 4.8

6.7

4.2

8.8

4.0

0

1

2

3

4

5

6

7

8

9

Agriculture Manufacturing Other industries Services

Annu

al g

row

th ra

te (p

erce

nt)

2011 2012 2013

The State of Kenya’s Economy

December 2013 | Edition No. 94

and the value of exports grew 7.3 percent. Export volume expanded 38.5 percent for vegetables, 6.7 percent for fruits, and 2.6 percent for cut flowers. In contrast, the volume of coffee production decreased 8.8 percent and the value fell 32.1 percent, as both acreage under coffee and prices declined.

The industrial sector expanded. Manufacturing (which accounts for 9.8 percent of total GDP) grew by 4.2 percent, electricity and water by 7.9, construction by 9.8 percent, and mining and quarrying by 5.4 percent during the first half of 2013. Performance was attributed to above-average rainfall, a stable macroeconomic environment, improved access to credit, and lower energy costs. Significant hydropower generation increased the domestic electricity supply and reduced the cost associated with power losses. Hydropower generation increased 14.1 percent, and geothermal generation rose 10 percent. Thermal electricity generation contracted 10.8 percent, indicating the shift away from reliance on nonrenewable energy. Electricity consumption rose 3.2 percent. The construction subsector grew 9.8 percent, underpinned partly by growing domestic investment in buildings. The real value of buildings approved by the Nairobi City Council during the first half of 2013 rose to KSh 1.4 billion, up from KSh 1.3 billion during the same

period in 2012. Domestic cement production and consumption rose 3 percent. Recent data from the Kenya National Bureau of Statistics indicate that electricity generation grew 7.3 percent in the year ending August 2013, an increase over the 4.0 percent rise in 2012. Sugar production rose 0.6 percent in the year ending July 2013, up from 0.01 percent in 2012. For cement production, growth for the first seven months of 2013 stood at 3 percent, up from a 0.1 percent contraction in 2012, suggesting annual growth of 3.1 percent in 2013.

Growth of the services sector was subdued. Services have accounted for 47 percent of Kenya’s GDP since 2005. The sector grew at an annual rate of just 4.0 percent during the first half of 2013, down from 4.8 percent during the same period in 2012. The transport and communication subsectors (which accounted for 25 percent of total services output) contracted. Growth in financial intermediation wholesale and retail trade, which usually grow much faster, was modest (Figure 1.5). Other services continued to experience very limited growth, following high lending rates. Wholesale and retail trade grew by 1.3 percent; financial intermediation by 0.6 percent; real estate, renting, and business services by 0.4 percent; and public administration by 0.2 percent.

Figure 1.5: Performance in the services sector was mixed in 2013

Source: Kenya National Bureau of Statistics, Leading Economic Indicators

0.2

0.3

0.4

0.5

0.6

1.3

1.3

-0.5 0 0.5 1.0 1.5 2.0

Hotels and restaurants

Financial intermediationindirectly measured

Public administration

Other services

Real estate, renting,business services

Education

Financial intermediation

Wholesale and retail trade

Transport and communication

Weighted growth (percent)First half of 2013 First half of 2012

-2

-1

0

1

2

3

4

5

6

7

8

2006 2007 2008 2009 2010 2011 2012 2013

Wei

ghte

d gr

owth

(per

cent

)

Wholesale and retail trade Transport and communicationFinancial intermediation Services

December 2013 | Edition No. 9 5

The State of Kenya’s Economy

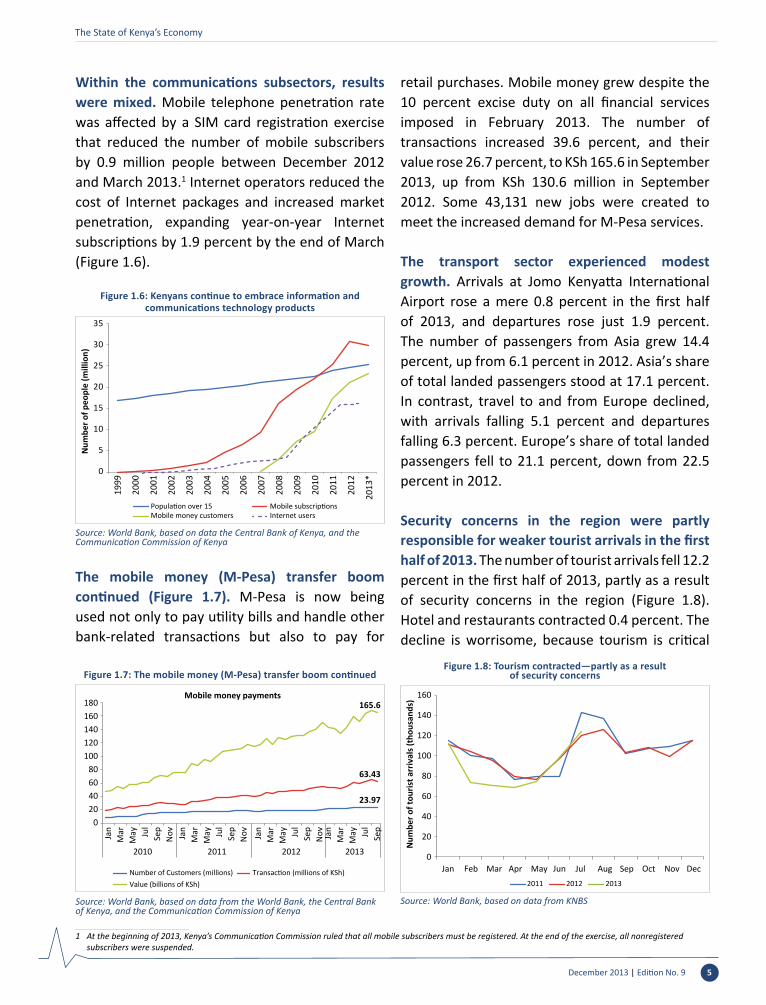

Within the communications subsectors, results were mixed. Mobile telephone penetration rate was affected by a SIM card registration exercise that reduced the number of mobile subscribers by 0.9 million people between December 2012 and March 2013.1 Internet operators reduced the cost of Internet packages and increased market penetration, expanding year-on-year Internet subscriptions by 1.9 percent by the end of March (Figure 1.6).

The mobile money (M-Pesa) transfer boom continued (Figure 1.7). M-Pesa is now being used not only to pay utility bills and handle other bank-related transactions but also to pay for

retail purchases. Mobile money grew despite the 10 percent excise duty on all financial services imposed in February 2013. The number of transactions increased 39.6 percent, and their value rose 26.7 percent, to KSh 165.6 in September 2013, up from KSh 130.6 million in September 2012. Some 43,131 new jobs were created to meet the increased demand for M-Pesa services.

The transport sector experienced modest growth. Arrivals at Jomo Kenyatta International Airport rose a mere 0.8 percent in the first half of 2013, and departures rose just 1.9 percent. The number of passengers from Asia grew 14.4 percent, up from 6.1 percent in 2012. Asia’s share of total landed passengers stood at 17.1 percent. In contrast, travel to and from Europe declined, with arrivals falling 5.1 percent and departures falling 6.3 percent. Europe’s share of total landed passengers fell to 21.1 percent, down from 22.5 percent in 2012.

Security concerns in the region were partly responsible for weaker tourist arrivals in the first half of 2013. The number of tourist arrivals fell 12.2 percent in the first half of 2013, partly as a result of security concerns in the region (Figure 1.8).Hotel and restaurants contracted 0.4 percent. The decline is worrisome, because tourism is critical

Figure 1.6: Kenyans continue to embrace information and communications technology products

Source: World Bank, based on data the Central Bank of Kenya, and the Communication Commission of Kenya

0

5

10

15

20

25

30

35

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

*

Num

ber o

f peo

ple

(mill

ion)

Population over 15 Mobile subscriptionsMobile money customers Internet users

Figure 1.7: The mobile money (M-Pesa) transfer boom continued

Source: World Bank, based on data from the World Bank, the Central Bank of Kenya, and the Communication Commission of Kenya

23.97

63.43

165.6

020406080

100120140160180

Jan

Mar

May Ju

lSe

pN

ov Jan

Mar

May Ju

lSe

pN

ov Jan

Mar

May Ju

lSe

pN

ov

2010 2011 2012

Jan

Mar

May Ju

lSe

p

2013

Mobile money payments

Number of Customers (millions) Transaction (millions of KSh)Value (billions of KSh)

1 At the beginning of 2013, Kenya’s Communication Commission ruled that all mobile subscribers must be registered. At the end of the exercise, all nonregistered subscribers were suspended.

Figure 1.8: Tourism contracted—partly as a result of security concerns

Source: World Bank, based on data from KNBS

0

20

Jan Feb Jul Aug Sep Oct Nov DecMar Apr May Jun

40

60

80

100

120

140

160

Num

ber o

f tou

rist a

rriv

als (

thou

sand

s)

2011 2012 2013

The State of Kenya’s Economy

December 2013 | Edition No. 96

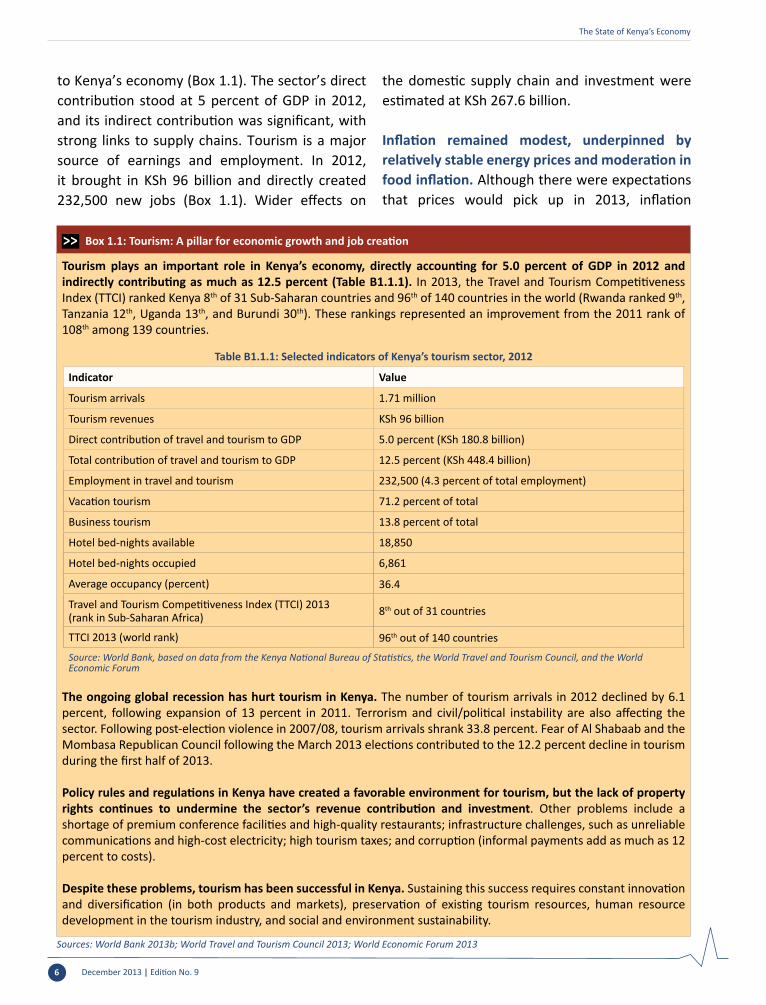

to Kenya’s economy (Box 1.1). The sector’s direct contribution stood at 5 percent of GDP in 2012, and its indirect contribution was significant, with strong links to supply chains. Tourism is a major source of earnings and employment. In 2012, it brought in KSh 96 billion and directly created 232,500 new jobs (Box 1.1). Wider effects on

the domestic supply chain and investment were estimated at KSh 267.6 billion.

Inflation remained modest, underpinned by relatively stable energy prices and moderation in food inflation. Although there were expectations that prices would pick up in 2013, inflation

Box 1.1: Tourism: A pillar for economic growth and job creation

Tourism plays an important role in Kenya’s economy, directly accounting for 5.0 percent of GDP in 2012 and indirectly contributing as much as 12.5 percent (Table B1.1.1). In 2013, the Travel and Tourism Competitiveness Index (TTCI) ranked Kenya 8th of 31 Sub-Saharan countries and 96th of 140 countries in the world (Rwanda ranked 9th, Tanzania 12th, Uganda 13th, and Burundi 30th). These rankings represented an improvement from the 2011 rank of 108th among 139 countries.

The ongoing global recession has hurt tourism in Kenya. The number of tourism arrivals in 2012 declined by 6.1 percent, following expansion of 13 percent in 2011. Terrorism and civil/political instability are also affecting the sector. Following post-election violence in 2007/08, tourism arrivals shrank 33.8 percent. Fear of Al Shabaab and the Mombasa Republican Council following the March 2013 elections contributed to the 12.2 percent decline in tourism during the first half of 2013.

Policy rules and regulations in Kenya have created a favorable environment for tourism, but the lack of property rights continues to undermine the sector’s revenue contribution and investment. Other problems include a shortage of premium conference facilities and high-quality restaurants; infrastructure challenges, such as unreliable communications and high-cost electricity; high tourism taxes; and corruption (informal payments add as much as 12 percent to costs).

Despite these problems, tourism has been successful in Kenya. Sustaining this success requires constant innovation and diversification (in both products and markets), preservation of existing tourism resources, human resource development in the tourism industry, and social and environment sustainability.

Table B1.1.1: Selected indicators of Kenya’s tourism sector, 2012

Indicator Value

Tourism arrivals 1.71 million

Tourism revenues KSh 96 billion

Direct contribution of travel and tourism to GDP 5.0 percent (KSh 180.8 billion)

Total contribution of travel and tourism to GDP 12.5 percent (KSh 448.4 billion)

Employment in travel and tourism 232,500 (4.3 percent of total employment)

Vacation tourism 71.2 percent of total

Business tourism 13.8 percent of total

Hotel bed-nights available 18,850

Hotel bed-nights occupied 6,861

Average occupancy (percent) 36.4

Travel and Tourism Competitiveness Index (TTCI) 2013 (rank in Sub-Saharan Africa) 8th out of 31 countries

TTCI 2013 (world rank) 96th out of 140 countries

Source: World Bank, based on data from the Kenya National Bureau of Statistics, the World Travel and Tourism Council, and the World Economic Forum

Sources: World Bank 2013b; World Travel and Tourism Council 2013; World Economic Forum 2013

Figure 1.9: A good harvest led to lower food prices

Source: World Bank, based on data from the Kenya National Bureau of Statistics

33

35

37

39

41

43

45

47

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Aver

age

reta

il pr

ice

(KSh

per

kilo

)

Dry maize

2012 2013 2012 2013

68

70

72

74

76

78

80

82

84

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Aver

age

reta

il pr

ice

(KSh

per

kilo

)

Dry beans

December 2013 | Edition No. 9 7

The State of Kenya’s Economy

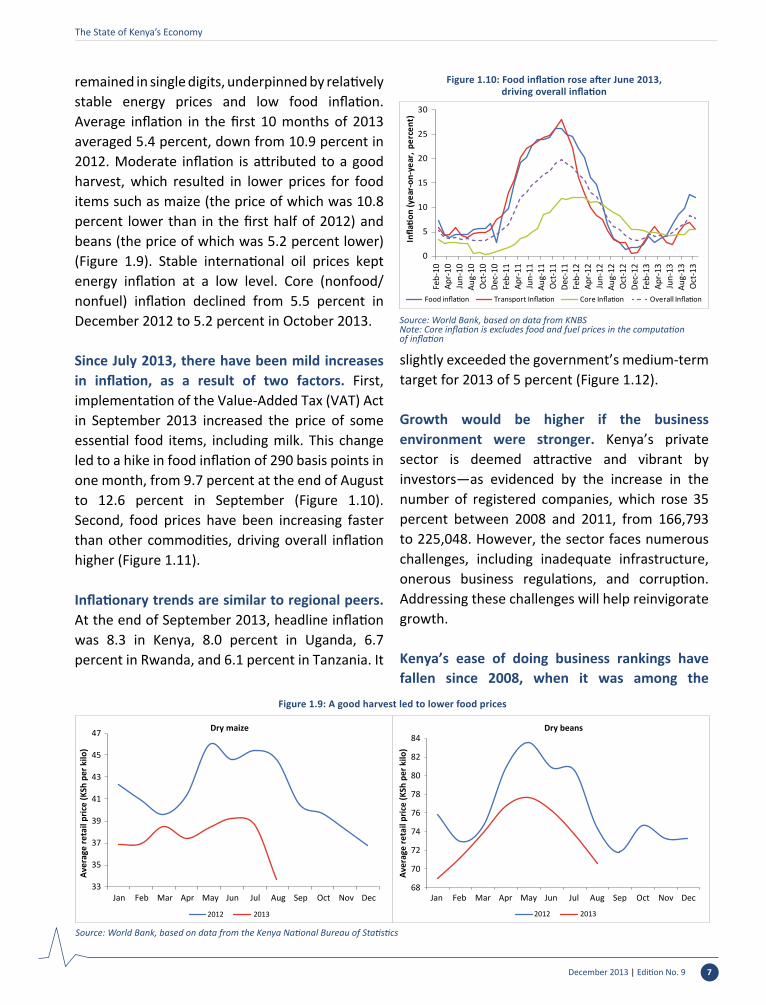

remained in single digits, underpinned by relatively stable energy prices and low food inflation. Average inflation in the first 10 months of 2013 averaged 5.4 percent, down from 10.9 percent in 2012. Moderate inflation is attributed to a good harvest, which resulted in lower prices for food items such as maize (the price of which was 10.8 percent lower than in the first half of 2012) and beans (the price of which was 5.2 percent lower)(Figure 1.9). Stable international oil prices kept energy inflation at a low level. Core (nonfood/nonfuel) inflation declined from 5.5 percent in December 2012 to 5.2 percent in October 2013.

Since July 2013, there have been mild increases in inflation, as a result of two factors. First, implementation of the Value-Added Tax (VAT) Act in September 2013 increased the price of some essential food items, including milk. This change led to a hike in food inflation of 290 basis points in one month, from 9.7 percent at the end of August to 12.6 percent in September (Figure 1.10).Second, food prices have been increasing faster than other commodities, driving overall inflation higher (Figure 1.11).

Inflationary trends are similar to regional peers. At the end of September 2013, headline inflation was 8.3 in Kenya, 8.0 percent in Uganda, 6.7 percent in Rwanda, and 6.1 percent in Tanzania. It

slightly exceeded the government’s medium-term target for 2013 of 5 percent (Figure 1.12).

Growth would be higher if the business environment were stronger. Kenya’s private sector is deemed attractive and vibrant by investors—as evidenced by the increase in the number of registered companies, which rose 35 percent between 2008 and 2011, from 166,793 to 225,048. However, the sector faces numerous challenges, including inadequate infrastructure, onerous business regulations, and corruption. Addressing these challenges will help reinvigorate growth.

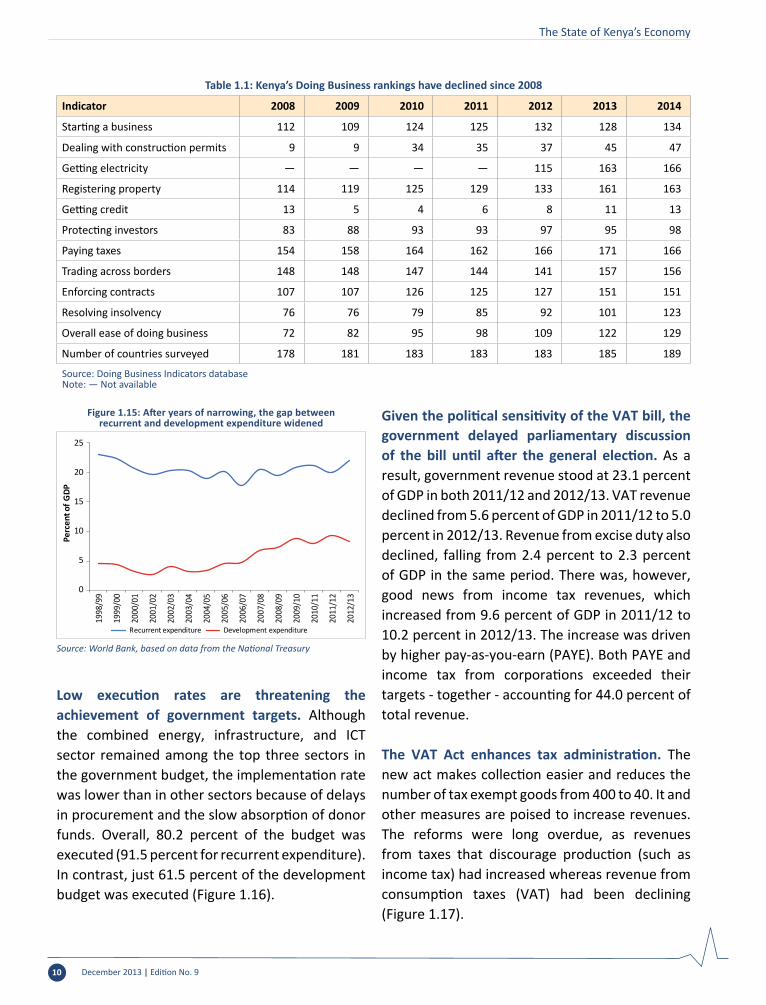

Kenya’s ease of doing business rankings have fallen since 2008, when it was among the

Figure 1.10: Food inflation rose after June 2013, driving overall inflation

Source: World Bank, based on data from KNBSNote: Core inflation is excludes food and fuel prices in the computation of inflation

0

5

10

15

20

25

30

Infla

tion

(yea

r-on

-yea

r, pe

rcen

t)

Food inflation Transport Inflation Core Inflation Overall Inflation

Feb-

10Ap

r-10

Jun-

10Au

g-10

Oct

-10

Dec-

10Fe

b-11

Apr-

11Ju

n-11

Aug-

11O

ct-1

1De

c-11

Feb-

12Ap

r-12

Jun-

12Au

g-12

Oct

-12

Dec-

12Fe

b-13

Apr-

13Ju

n-13

Aug-

13O

ct-1

3

The State of Kenya’s Economy

December 2013 | Edition No. 98

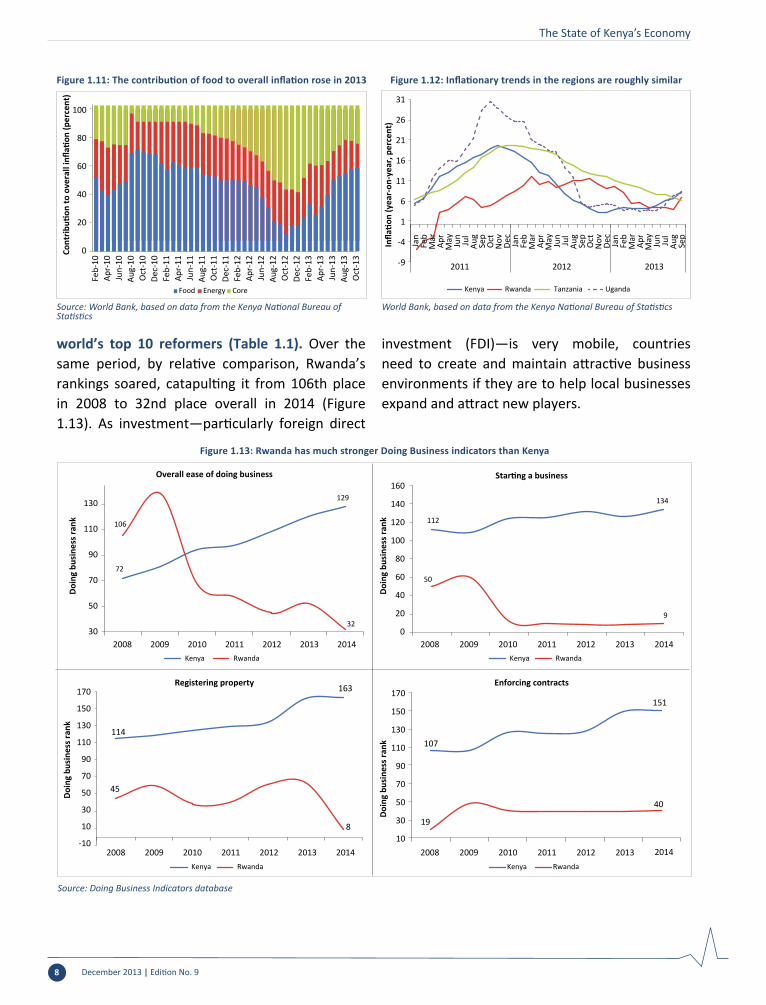

world’s top 10 reformers (Table 1.1). Over the same period, by relative comparison, Rwanda’s rankings soared, catapulting it from 106th place in 2008 to 32nd place overall in 2014 (Figure 1.13). As investment—particularly foreign direct

investment (FDI)—is very mobile, countries need to create and maintain attractive business environments if they are to help local businesses expand and attract new players.

Figure 1.11: The contribution of food to overall inflation rose in 2013

Source: World Bank, based on data from the Kenya National Bureau of Statistics

0

20

Feb-

10Ap

r-10

Jun-

10Au

g-10

Oct

-10

Dec-

10Fe

b-11

Apr-

11Ju

n-11

Aug-

11O

ct-1

1De

c-11

Feb-

12Ap

r-12

Jun-

12Au

g-12

Oct

-12

Feb-

13Ap

r-13

Jun-

13Au

g-13

Oct

-13

Dec-

12

40

60

80

100

Cont

ributi

on to

ove

rall

infla

tion

(per

cent

)

Food Energy Core

Figure 1.12: Inflationary trends in the regions are roughly similar

World Bank, based on data from the Kenya National Bureau of Statistics

-9

-4

1

6

11

16

21

26

31

Jan

Feb

Mar

Apr

May Jun

Jul

Aug

Sep

Oct

Nov De

cJa

nFe

bM

arAp

rM

ay Jun

Jul

Aug

Sep

Oct

Nov De

cJa

nFe

bM

arAp

rM

ay Jun

Jul

Aug

Sep

2011 2012 2013

Infla

tion

(yea

r-on

-yea

r, pe

rcen

t)

Kenya Rwanda Tanzania Uganda

Figure 1.13: Rwanda has much stronger Doing Business indicators than Kenya

Source: Doing Business Indicators database

72

129

106

3230

50

70

90

110

130

2008 2009 2010 2011 2012 2013 2014

Doin

g bu

sine

ss ra

nk

Overall ease of doing business

Kenya Rwanda

112

134

50

9

0

20

40

60

80

100

120

140

160

2008 2009 2010 2011 2012 2013 2014

Doin

g bu

sine

ss ra

nk

Starting a business

Kenya Rwanda

114

163

45

8

-10

10

30

50

70

90

110

130

150

170

2008 2009 2010 2011 2012 2013 2014

Doin

g bu

sine

ss ra

nk

Registering property

Kenya Rwanda

107

151

19

40

10

30

50

70

90

110

130

150

170

2008 2009 2010 2011 2012 2013 2014

Doin

g bu

sine

ss ra

nk

Enforcing contracts

Kenya Rwanda

December 2013 | Edition No. 9 9

The State of Kenya’s Economy

1.2 Fiscal Discipline Maintained Despite Emerging Pressures

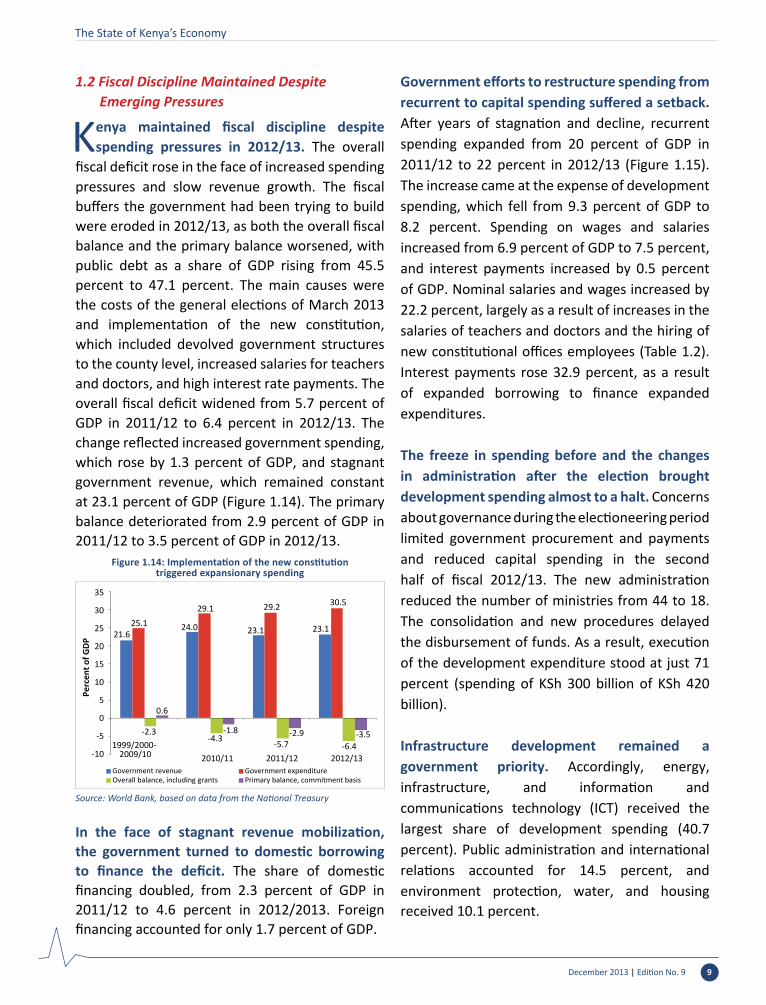

Kenya maintained fiscal discipline despite spending pressures in 2012/13. The overall

fiscal deficit rose in the face of increased spending pressures and slow revenue growth. The fiscal buffers the government had been trying to build were eroded in 2012/13, as both the overall fiscal balance and the primary balance worsened, with public debt as a share of GDP rising from 45.5 percent to 47.1 percent. The main causes were the costs of the general elections of March 2013 and implementation of the new constitution, which included devolved government structures to the county level, increased salaries for teachers and doctors, and high interest rate payments. The overall fiscal deficit widened from 5.7 percent of GDP in 2011/12 to 6.4 percent in 2012/13. The change reflected increased government spending, which rose by 1.3 percent of GDP, and stagnant government revenue, which remained constant at 23.1 percent of GDP (Figure 1.14). The primary balance deteriorated from 2.9 percent of GDP in 2011/12 to 3.5 percent of GDP in 2012/13.

In the face of stagnant revenue mobilization, the government turned to domestic borrowing to finance the deficit. The share of domestic financing doubled, from 2.3 percent of GDP in 2011/12 to 4.6 percent in 2012/2013. Foreign financing accounted for only 1.7 percent of GDP.

Government efforts to restructure spending from recurrent to capital spending suffered a setback. After years of stagnation and decline, recurrent spending expanded from 20 percent of GDP in 2011/12 to 22 percent in 2012/13 (Figure 1.15). The increase came at the expense of development spending, which fell from 9.3 percent of GDP to 8.2 percent. Spending on wages and salaries increased from 6.9 percent of GDP to 7.5 percent, and interest payments increased by 0.5 percent of GDP. Nominal salaries and wages increased by 22.2 percent, largely as a result of increases in the salaries of teachers and doctors and the hiring of new constitutional offices employees (Table 1.2). Interest payments rose 32.9 percent, as a result of expanded borrowing to finance expanded expenditures.

The freeze in spending before and the changes in administration after the election brought development spending almost to a halt. Concerns about governance during the electioneering period limited government procurement and payments and reduced capital spending in the second half of fiscal 2012/13. The new administration reduced the number of ministries from 44 to 18. The consolidation and new procedures delayed the disbursement of funds. As a result, execution of the development expenditure stood at just 71 percent (spending of KSh 300 billion of KSh 420 billion).

Infrastructure development remained a government priority. Accordingly, energy, infrastructure, and information and communications technology (ICT) received the largest share of development spending (40.7 percent). Public administration and international relations accounted for 14.5 percent, and environment protection, water, and housing received 10.1 percent.

Figure 1.14: Implementation of the new constitutiontriggered expansionary spending

Source: World Bank, based on data from the National Treasury

21.624.0 23.1 23.125.1

29.1 29.2 30.5

-2.3-4.3 -5.7 -6.4

0.6

-1.8 -2.9 -3.5

-10

-5

0

5

10

15

20

25

30

35

1999/2000-2009/10 2010/11 2011/12 2012/13

Perc

ent o

f GDP

Government revenue Government expenditureOverall balance, including grants Primary balance, commitment basis

The State of Kenya’s Economy

December 2013 | Edition No. 910

Low execution rates are threatening the achievement of government targets. Although the combined energy, infrastructure, and ICT sector remained among the top three sectors in the government budget, the implementation rate was lower than in other sectors because of delays in procurement and the slow absorption of donor funds. Overall, 80.2 percent of the budget was executed (91.5 percent for recurrent expenditure).In contrast, just 61.5 percent of the development budget was executed (Figure 1.16).

Given the political sensitivity of the VAT bill, the government delayed parliamentary discussion of the bill until after the general election. As a result, government revenue stood at 23.1 percent of GDP in both 2011/12 and 2012/13. VAT revenue declined from 5.6 percent of GDP in 2011/12 to 5.0 percent in 2012/13. Revenue from excise duty also declined, falling from 2.4 percent to 2.3 percent of GDP in the same period. There was, however, good news from income tax revenues, which increased from 9.6 percent of GDP in 2011/12 to 10.2 percent in 2012/13. The increase was driven by higher pay-as-you-earn (PAYE). Both PAYE and income tax from corporations exceeded their targets - together - accounting for 44.0 percent of total revenue.

The VAT Act enhances tax administration. The new act makes collection easier and reduces the number of tax exempt goods from 400 to 40. It and other measures are poised to increase revenues. The reforms were long overdue, as revenues from taxes that discourage production (such as income tax) had increased whereas revenue from consumption taxes (VAT) had been declining (Figure 1.17).

Table 1.1: Kenya’s Doing Business rankings have declined since 2008

Indicator 2008 2009 2010 2011 2012 2013 2014

Starting a business 112 109 124 125 132 128 134

Dealing with construction permits 9 9 34 35 37 45 47

Getting electricity — — — — 115 163 166

Registering property 114 119 125 129 133 161 163

Getting credit 13 5 4 6 8 11 13

Protecting investors 83 88 93 93 97 95 98

Paying taxes 154 158 164 162 166 171 166

Trading across borders 148 148 147 144 141 157 156

Enforcing contracts 107 107 126 125 127 151 151

Resolving insolvency 76 76 79 85 92 101 123

Overall ease of doing business 72 82 95 98 109 122 129

Number of countries surveyed 178 181 183 183 183 185 189

Source: Doing Business Indicators databaseNote: — Not available

Figure 1.15: After years of narrowing, the gap between recurrent and development expenditure widened

Source: World Bank, based on data from the National Treasury

0

5

10

1998

/99

1999

/00

2000

/01

2001

/02

2002

/03

2003

/04

2004

/05

2005

/06

2006

/07

2007

/08

2008

/09

2009

/10

2010

/11

2011

/12

2012

/13

15

20

25

Perc

ent o

f GDP

Recurrent expenditure Development expenditure

December 2013 | Edition No. 9 11

The State of Kenya’s Economy

More tax revenues streams have been identified to expand the base. The government targeted new revenue streams by imposing a 10 percent excise tax on mobile banking and other financial services and a 1.5 percent import levy on railway development. Both of these measures will significantly raise revenue and expand the tax base. These measures are a step in the right direction, as they rebalance tax composition away from taxation of sources of production toward taxation of consumption.

Public debt as a ratio of GDP increased, reducing the fiscal space Kenya had built up. The share of net public debt in GDP increased from 45.5

percent of GDP in 2011/12 to 47.1 percent in 2012/13. The increase was financed mainly from domestic resources, with domestic debt rising from 26.5 percent of GDP to 28.7 percent. External debt declined, falling from 23.9 of GDP to 23.0 percent (Figure 1.18). Kenya is set to tap into the international financial market by issuing a US$ 1.5 billion of Eurobonds in January 2014. Although the issuance will increase its external indebtedness, the overall debt sustainability outlook remains favorable: the 2013 joint Word Bank/IMF Debt Sustainability Analysis shows that Kenya’s debt distress rating remains low, thanks partly to the government’s policy of avoiding nonconcessional borrowing.

Table 1.2: Government expenditure rose between 2008/09 and 2012/13

Item 2008/09 2009/10 2010/11 20011/12 2012/13

Recurrent spending 19.5 20.8 21.3 20.0 22.1

Wages and salaries 6.9 7.0 7.1 6.9 7.5

Interest payments 2.3 2.6 2.7 2.8 3.3

Domestic Interest 2.1 2.3 2.5 2.5 3.0

Foreign Interest 0.3 0.3 0.3 0.3 0.3

Pensions 1.2 1.2 0.9 0.8 0.7

Operations and maintenance 9.0 10.0 10.5 9.4 10.5

Transitional transfer to counties n.a. n.a. n.a. n.a. 0.3

Development expenditure and net lending 7.2 8.7 7.9 9.3 8.2

Total expenditure and net lending 26.6 29.5 29.1 29.2 30.5

Source: National Treasury, 2013Note: n.a. Not applicable

Figure 1.16: Low execution rates reduced development expenditure

Source: World Bank, based on data from the National Treasury

0 50 100 150 200 250 300

General economic, commercialand labor affairs

Social protection, cultureand recreation

Environment protection and water

Agriculture andrural development

Health

Public administrationand international

National security

Energy, infrastructure and ICT

Governance, justice and order

Education

Total expenditure by sectors (billions of KSh)

June 2013 target June 2013 actual

100

89

87

86

85

76

74

74

69

63

0 20 40 60 80 100

National security

Governance, justice and order

Education

Health

General economic, commercialand labor affairs

Agriculture and rural development

Public administration andinternational relations

Social protection, cultureand recreation

Environment protection, waterand housing

Energy, infrastructure and ICT

Budget implementation rate as at the end of June 2013 (percent)

December 2013 | Edition No. 912

The State of Kenya’s Economy

The upward movement of the yield curve reflects recent uncertainty over fiscal policy. The downward movement in the yields on government securities between December 2011 and December 2012 reflected the improved economic environment after the 2011 economic crisis, when inflation reached a peak of more than 19 percent a year and the exchange rate was volatile. The peaceful election, smooth transfer of power, and enthusiasm among investors that followed pushed the yield curve further down in June 2013 (Figure 1.19). However, challenges in implementing the budget combined with the slow absorption by ministries and the standoff between the national and county governments have disappointed the

market. Worries about fiscal risks and the strength of the economy pushed the yield curve upward, especially at short maturities.

1.3 Monetary Policy Remained Supportive

The Central Bank’s Monetary Policy Committee eased monetary conditions to boost economic

activity. To spur credit to the private sector, the Central Bank lowered its policy rate 250 basis points to 8.5 percent in September 2013, down from 11.0 percent in December 2012. As a result, interest rates at both the short and long ends of the market declined in 2013 from the high rates of December 2012.

The Central Bank operationalized its monetary policy stance by allowing monetary aggregates to expand. Between July 2012 and July 2013, M0 increased 12.2 percent to 15.2 percent, and M1 increased 16.2 percent to 18.7 percent (Figure 1.20). However, because of a build-up in liquidity at the Central Bank, M2 increased just 13.8 percent in July 2013, to the same level as in 2012.

Kenya’s monetary policy stance has kept inflation in check and spurred economic activity. Inflationary pressure eased in 2013, with core inflation declining from an average rate of 9.5 percent in 2012 to 4.7 percent in 2013. Economic

Figure 1.17: Income tax revenues rose and VAT and excise duties fell between 1999 and 2012

Source: World Bank, based on data from the National Treasury

7.0

9.3 9.610.2

5.46.2 5.7

5.0

2.01.7 1.6 1.6

3.2 2.92.4 2.3

0

2

4

6

8

10

12

Perc

ent o

f GDP

Income tax VAT Import duty Excise duty

2010/111999/2000-2009/10

2011/12 2012/13

Figure 1.18: Total and domestic public debt as a percent of GDP increased, and external debt fell

Source: World Bank, based on data from the National Treasury

35.822.6 24.2 23.2 25.9 23.9 23.0

24.2

21.9 23.3 26.9 27.4 26.5 28.7

55.5

39.5 42.2 44.948.3 45.5 47.1

0

10

20

30

40

50

60

70

Perc

ent o

f GDP

Kenya's public debt

External debt Domestic debt

2007/081999/2000-2006/07

2008/09 2009/10 2010/11 2011/12 2012/13

Figure 1.19: The upward movement in the yield curve reflects market concerns about budget implementation

Source: Africa Alliance Kenya Investment Bank

0

5

10

15

20

25

3 months

6 months

1 year

2 years

5 years

10 years

15 years

20 years

25 years

30 years

Inte

rest

rate

(per

cent

)

TenorDecember 2011 December 2012 June 2013 October 2013

The State of Kenya’s Economy

December 2013 | Edition No. 9 13

activity also increased. Growth also increased in the first half of the year, to 4.7 percent, up from 4.3 percent during the same period in 2012.

Several factors dampened the transmission of the Central Bank’s monetary stance to short-term rates. Although the Central Bank rate was reduced by 250 basis points, interbank rates rose 168 basis points and 91-day Treasury bill rates rose 128 basis points between December 2012 and the end of September 2013 (Figure 1.21). As part of the transition to the new government, new procurement was suspended in the first quarter of 2013, and spending by the government slowed dramatically. Low spending meant that government deposits built up at both the Central Bank and commercial banks where government

holds deposits. As a result, liquidity was tight in the banking system, with some banks with excess cash and others short of liquidity. As a result, interbank rates soared. Government deposits at the Central Bank also increased, draining the banking system of liquidity. Short-term rates were nevertheless lower than the peak in 2012, with interbank rates down by 1,650 basis points and 91-day Treasury bill rates down by 1,098 basis points by the end of September of 2013.

Long-term rates declined in 2013, as lending rates corrected for the overshooting in 2012. The decline reflects not the transmission mechanism from short-term rates but the reduction in commercial banks’ perceptions of risks following the general election and the smooth transfer of power. Average weighted lending rates declined by 119 basis points and overdraft lending rates by 90 basis points between December 2012 and the end of September 2013. Had liquidity concerns not hindered the transmission from the Central Bank rate to short-term rates, lending rates might have fallen further.

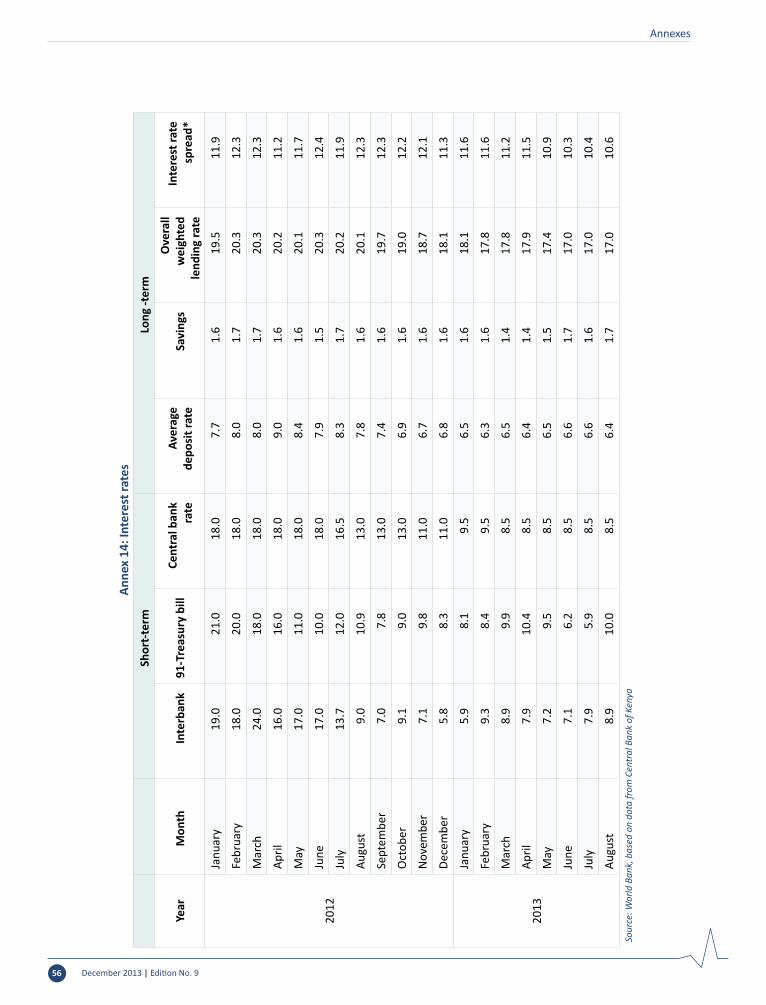

Interest rate spreads remained high, despite improved economic conditions. Spreads (lending minus deposit rates) remained in double digits in 2013, despite an improved economic environment and lower political risk. Measured as the difference

Figure 1.20: To support economic activity, Kenya’s Central Bank increased the money supply

Source: World Bank, based on data from the Central Bank of Kenya

-5

0

Mar

-07

May

-07

Jul-0

7

Sep-

07

Nov

-07

Mar

-08

May

-08

Jul-0

8

Sep-

08

Nov

-08

Jan-

08

Mar

-09

May

-09

Jul-0

9

Sep-

09

Nov

-09

Jan-

09

Mar

-10

May

-10

Jul-1

0

Sep-

10

Nov

-10

Jan-

10

Mar

-11

May

-11

Jul-1

1

Sep-

11

Nov

-11

Jan-

11

Mar

-12

May

-12

Jul-1

2

Sep-

12

Nov

-12

Jan-

12

Mar

-13

May

-13

Jul-1

3

Jan-

13

5

10

15

20

25

30

35

40Ch

ange

in m

oney

supp

ly (p

erce

nt)

Reserve money M0 M1

Figure 1.21: Liquidity shortages in the banking system dampened the effect of monetary policy on interest rates

Source: World Bank, based on data from the Central Bank of Kenya

0

5

10

15

20

25

30

Jan-

07M

ay-0

7Se

p-07

Jan-

08M

ay-0

8Se

p-08

Jan-

09M

ay-0

9Se

p-09

Jan-

10M

ay-1

0Se

p-10

Jan-

11M

ay-1

1Se

p-11

Jan-

12M

ay-1

2Se

p-12

Jan-

13M

ay-1

3Se

p-13

Inte

rest

rate

(per

cent

)

Interbank 91-day Tbill Central bank rate

December 2013 | Edition No. 914

The State of Kenya’s Economy

between lending and deposit rates, the spread averaged about 11 percent (Figure 1.22). Measured as the difference between the lending rate and the 91-day Treasury bill rate, the spread averaged 9 percent. Spreads capture perceived risk by lenders of borrowers’ ability to pay; they can also capture inefficiency in the banking system (as examined in the special topic section of this update).

Private sector credit is flowing again to finance economic activity, but the growth level of credit is still below recent historical levels. There was a significant increase in credit uptake in 2013, following the easing of monetary policy (Figure 1.23). Credit to the private sector grew 17.4 percent in 2013, up from 7.7 percent growth in 2012. Credit growth in 2013 was still well below normal, however. Private credit as a share of GDP increased from 23.0 percent in 2003 to 37.6 percent in 2013. Since 2011, the growth in private sector credit has not kept pace with GDP growth (Figure 1.24). Credit activity remains subdued, as banks have become more reluctant to lend given weaker economic activity during the government transition. At the same time, demand for credit has waned in light of weaker business prospects. Efforts to stimulate the economy through accommodative monetary policy were thwarted by lack of liquidity in the banking system,

which increased short-term rates. Under such circumstances, monetary easing had only limited impact on growth.

Credit to households and to trade and business services rose significantly. In contrast, the increase in credit to the more productive sectors—agriculture and manufacturing—was minimal (Figure 1.25). Between the end of December 2012 and the end of September 2013, commercial banks lent KSh 169 billion to the private sector. The other main beneficiaries were: households (32 percent of lending), trade (19 percent), business services (18 percent), and real estate (12 percent). A number of sectors made net repayments to the banking system. They included

Figure 1.22: Lending rates declined marginally, but interest spreads remained wide

Source: World Bank, based on data from the Central Bank of Kenya

0

2

4

6

8

10

12

14

16

18

Jan-

07Ap

r-07

Jul-0

7O

ct-0

7Ja

n-08

Apr-

08Ju

l-08

Oct

-08

Jan-

09Ap

r-09

Jul-0

9O

ct-0

9Ja

n-10

Apr-

10Ju

l-10

Oct

-10

Jan-

11Ap

r-11

Jul-1

1O

ct-1

1Ja

n-12

Apr-

12Ju

l-12

Oct

-12

Jan-

13Ap

r-13

Jul-1

3

Inte

rest

rate

spre

ads (

perc

ent)

Spread (lending rate-deposit Rate) Spread (lending rate-91 Treasury bill rate)

0

5

10

15

20

25

30

Jan-

07M