REGULATING COMPANY SECRETARIES

19

HKICS Members – Compliance with Hong Kong’s Regulation of Corporate Services Providers (CSPs) 19 September 2016 Mr Paul DS Moyes CPA FCIS FCS(PE) Council Member and Chairman of the Professional Services Panel, HKICS Executive Director, Tricor Services Limited All Rights Reserved. Not intended as legal advice and for reference only

Transcript of REGULATING COMPANY SECRETARIES

HKICS Members –

Compliance with Hong Kong’s Regulation

of Corporate Services Providers (CSPs)

19 September 2016

Mr Paul DS Moyes CPA FCIS FCS(PE)

Council Member and Chairman of the Professional

Services Panel, HKICS

Executive Director, Tricor Services Limited

All Rights Reserved. Not intended as legal advice and for reference only

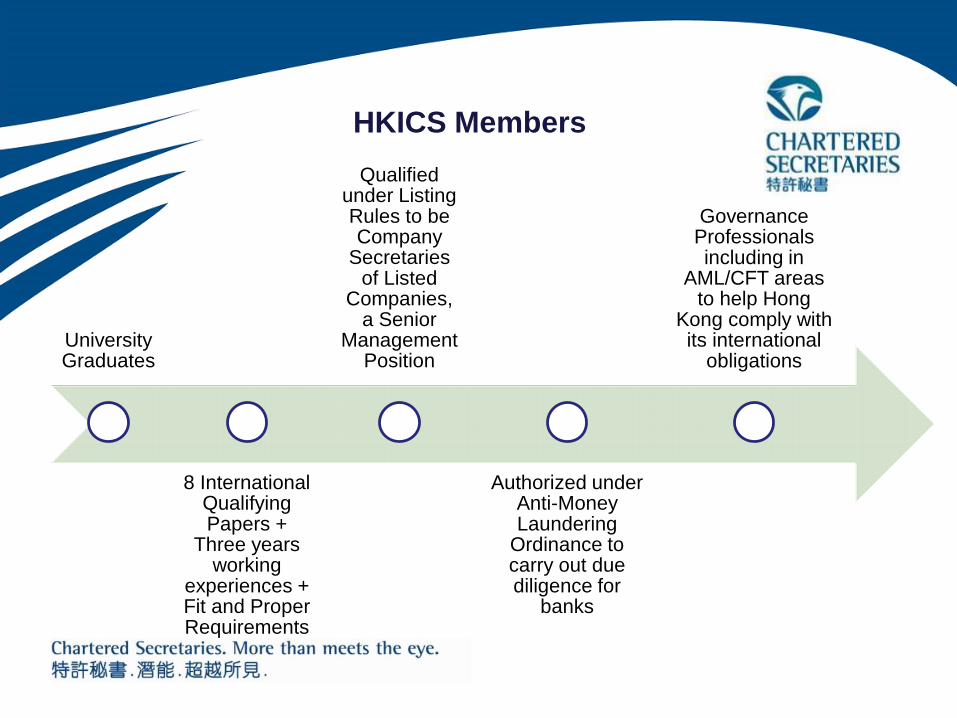

HKICS Members

University Graduates

8 International Qualifying Papers +

Three years working

experiences + Fit and Proper Requirements

Qualified under Listing Rules to be Company

Secretaries of Listed

Companies, a Senior

Management Position

Authorized under Anti-Money Laundering

Ordinance to carry out due diligence for

banks

Governance Professionals including in

AML/CFT areas to help Hong

Kong comply with its international

obligations

The Problem Area for HK - Financial Action Task Force (FATF)

Recommendation 22 – DNFBP Sector – HKICS Member – Please Help!

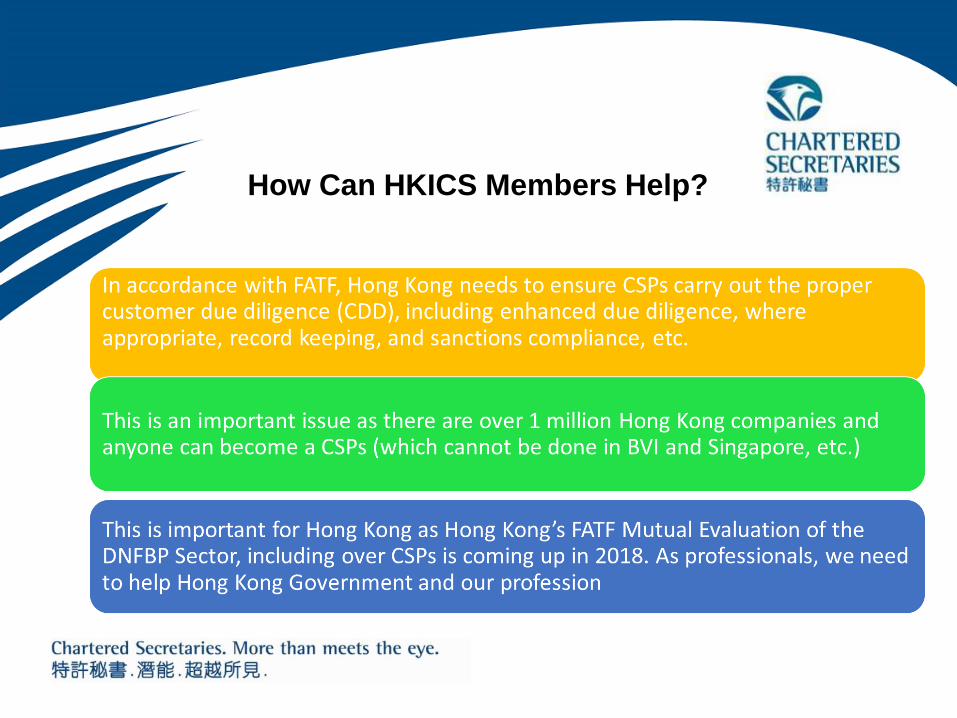

How Can HKICS Members Help?

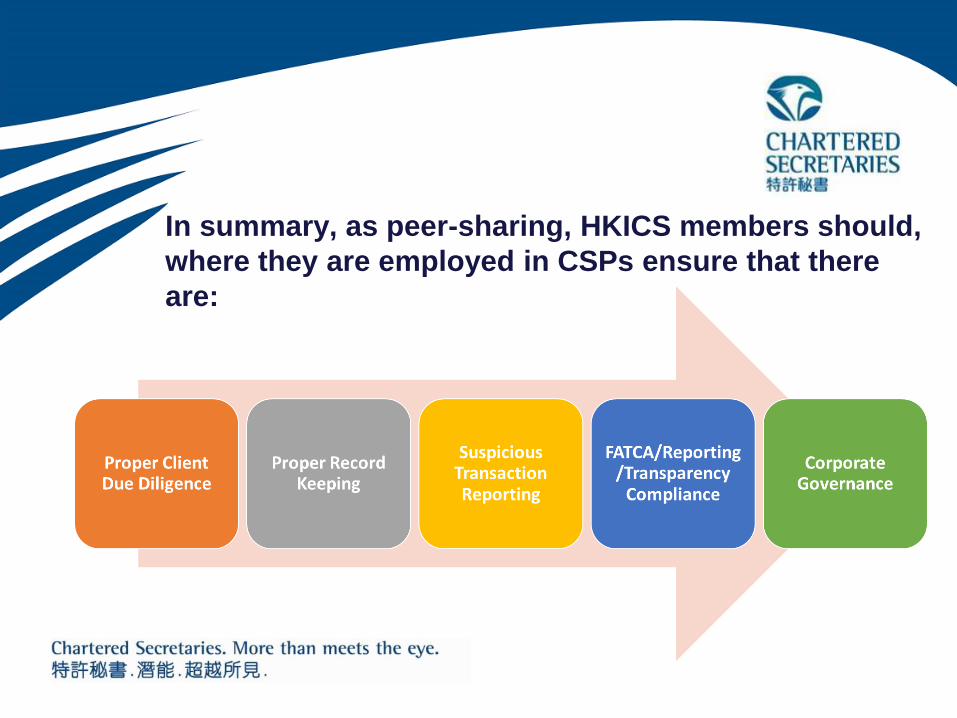

In summary, as peer-sharing, HKICS members should,

where they are employed in CSPs ensure that there

are:

Sanctions Compliance

• Please remember sanctions compliance as part of CDD and ongoing

compliance. See SFC and OFAC websites

• These apply to dealings with North Korea, Sudan, etc.

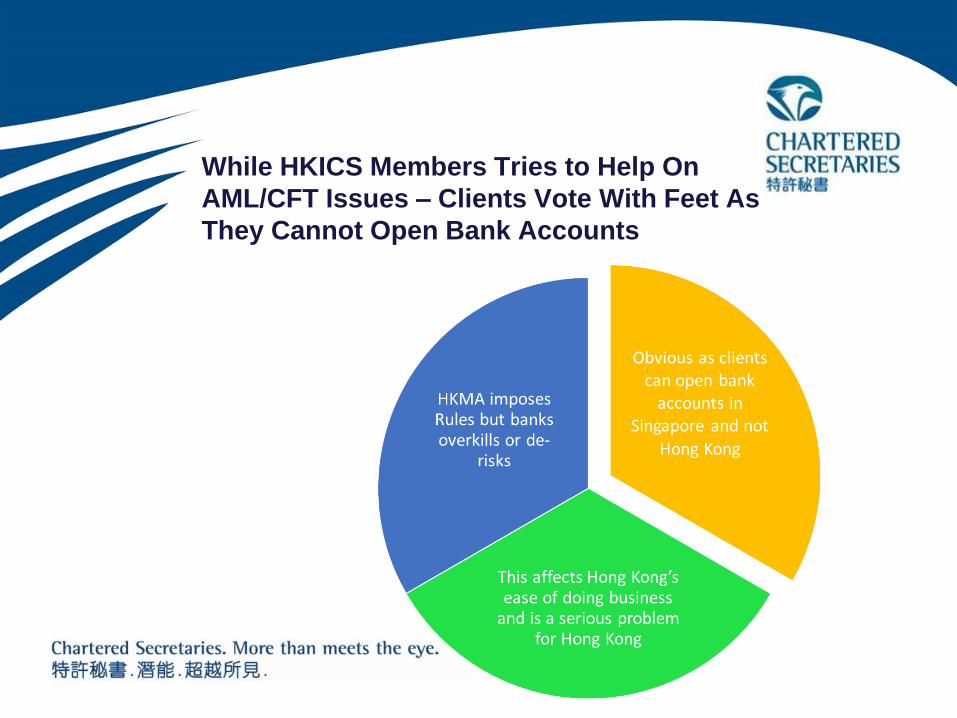

While HKICS Members Tries to Help On

AML/CFT Issues – Clients Vote With Feet As

They Cannot Open Bank Accounts

HKICS - 8 September 2016Bank Account Opening Survey Report

• 98% of the respondents thought that companies were having

difficulties opening bank accounts in Hong Kong.

• 79% of respondents thought there was a serious or somewhat

serious problem.

• 49% of respondents thought the stringent anti-money laundering

and counter-financing of terrorism (AML/CFT) requirements were

being used to keep away less revenue generating customers.

• Global, local and Chinese banks were cited indicating that the

problem is prevalent and not isolated to a few banks. The top

eight banks mentioned were HSBC, Standard Chartered Bank,

Hang Seng Bank, Bank of China, DBS, Bank of East Asia,

Citibank, and ICBC.

• 72 or 17% of those surveyed pointed out that while they could

not open the bank account in Hong Kong, they were able to do

so in another jurisdiction with the same bank.

https://www.hkics.org.hk/media/news/attachment/NEWS_A_310497_HKICS%20Ba

nk%20Account%20Opening%20Survey%20report%20-

%20Press%20Release%20(Eng).pdf

HKMA – 8 September 2016Circular on De-risking and Financial Inclusion

‘While it is important to ensure that AML/CFT controls are

sufficiently robust and comply with all the relevant regulatory

requirements, the HKMA expects AIs to adopt a risk-based

approach (RBA) and refrain from adopting practices that would

result in financial exclusion, particularly in respect of the need for

bona fide businesses to have access to basic banking services.’

http://www.hkma.gov.hk/media/eng/doc/key-information/guidelines-and-

circular/2016/20160908e1.pdf

• Risk differentiation – The risk assessment processes should be

able to differentiate the risks of individual customers within a

particular segment or grouping through the application of a range

of factors, including country risk, business risk, product/service

risk and delivery/distribution channel risk. It is inappropriate for

AIs to adopt a one-size-fits-all approach.

• Proportionality – Based on the likely risk level of a customer, AIs

should apply proportionate risk mitigating and CDD measures. It

is inappropriate for AIs to impose requirements disproportionate

to the risk level of the customer, as this would result in undue

burden on the customer and the AI concerned.

• Not a “Zero Failure” regime – RBA does not require or expect a

“zero failure” outcome. While AIs should take all reasonable

measures to identify ML/TF risks at the account opening stage

and, for existing customers, on an ongoing basis, it is unrealistic

to expect that no ML/TF activities would ever occur through the

banking system. AIs are not required to implement overly

stringent CDD processes with a view to eliminating, ex-ante, all

risks. Otherwise, such an approach would result in a large

number of bona fide businesses and individuals not being able to

open or maintain accounts.

• Transparency – Information and documentation requirements for

CDD purposes should be clearly set out and easily accessible to

new and existing customers. All retail banks are required to

enhance the transparency of account opening processes by

uploading basic information about the relevant procedures and

information and documentation requirements on their websites.

AIs should explain to customers the rationale for the information

requested and endeavor to assist customers in taking steps or

providing alternatives that can help satisfy the CDD processes

and introduce review mechanisms for unsuccessful applicants.

• Reasonableness – CDD processes and documentation requirements of

AIs should be relevant and pragmatic with respect to the customers’

background and circumstances. Furthermore, AIs should not use

AML/CFT as the ground for closing or rejecting an account when it is

actually for other considerations.

• Efficiency – AIs should have appropriate arrangements in place to

facilitate customers’ initiation of the account opening process. AIs are

encouraged to introduce online applications if practicable. AIs should

also maintain adequate communication with customers throughout the

account opening process by, for example, providing interim updates

about the progress of their applications (such as whether any

documents remain outstanding), timely feedback of the results of their

applications, and where an application is rejected, the reason for

rejection as appropriate.

Not Only are HKICS Members But

HKICS Also Helps on AML/CFT

In the Long Run

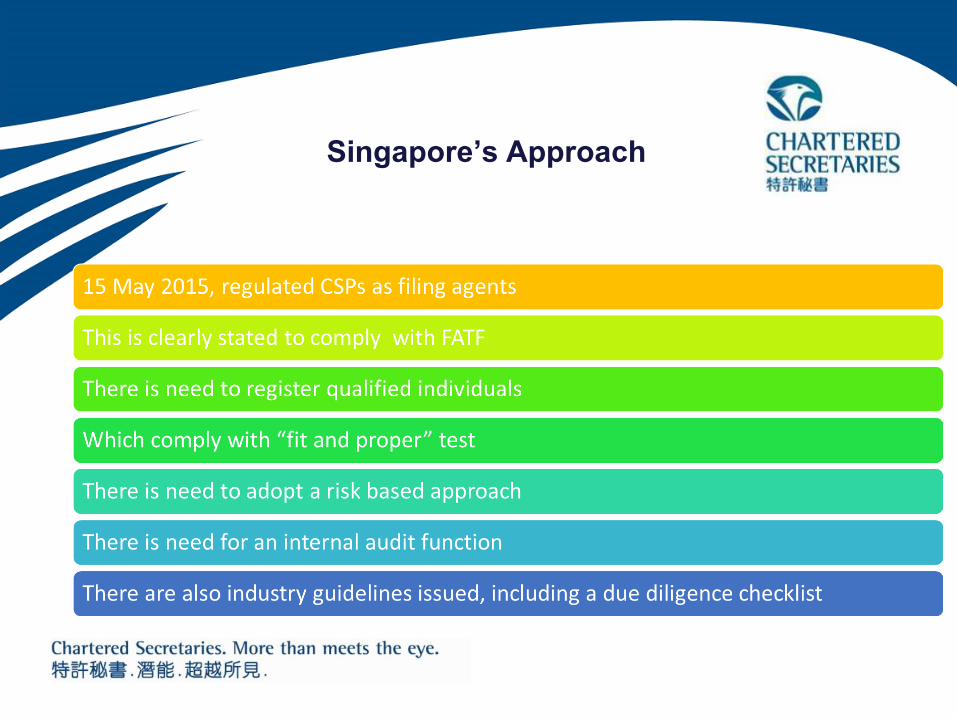

Singapore’s Approach

Conclusion

There is a need for Hong Kong to regulate CSPs in line with its international obligations

This affects not only CSPs but the ease of doing business in Hong Kong

Only professional and FATF compliant CSPs would be readily accepted by banks and financial institutions

As Hong Kong is coming up for its mutual evaluation by 2018, the Singapore and other models should be studied, to maintain the leadership position of Hong Kong