![SEARCH ENGINE PP - clib.dauniv.ac.in ENGINE PP.pdf · Zapmeta ( ) According scope the Search engine SE ... Microsoft PowerPoint - SEARCH ENGINE PP [Compatibility Mode] Author: Nandkishor](https://static.fdocuments.in/doc/165x107/5ad9f25f7f8b9afc0f8bd1ac/search-engine-pp-clib-engine-pppdfzapmeta-according-scope-the-search-engine.jpg)

Registration u/s Sec. 80G & 12 A Registration & Rejection CA Nandkishor Malpani NVM & Associates...

22

Registration u/s Sec. 80G & Registration u/s Sec. 80G & 12 A 12 A Registration & Rejection CA Nandkishor Malpani NVM & Associates Chartered Accountant, Ramkunj, Railway Station Road, New Osmanpura, Aurangabad -431005 Ph: 0240-2326106 M: 9823388620

-

Upload

rudolf-richardson -

Category

Documents

-

view

224 -

download

0

Transcript of Registration u/s Sec. 80G & 12 A Registration & Rejection CA Nandkishor Malpani NVM & Associates...

Registration u/s Sec. 80G & Registration u/s Sec. 80G & 12 A 12 A

Registration & Rejection

CA Nandkishor Malpani NVM & AssociatesChartered Accountant, Ramkunj, Railway Station Road, New Osmanpura, Aurangabad -431005Ph: 0240-2326106 M: 9823388620

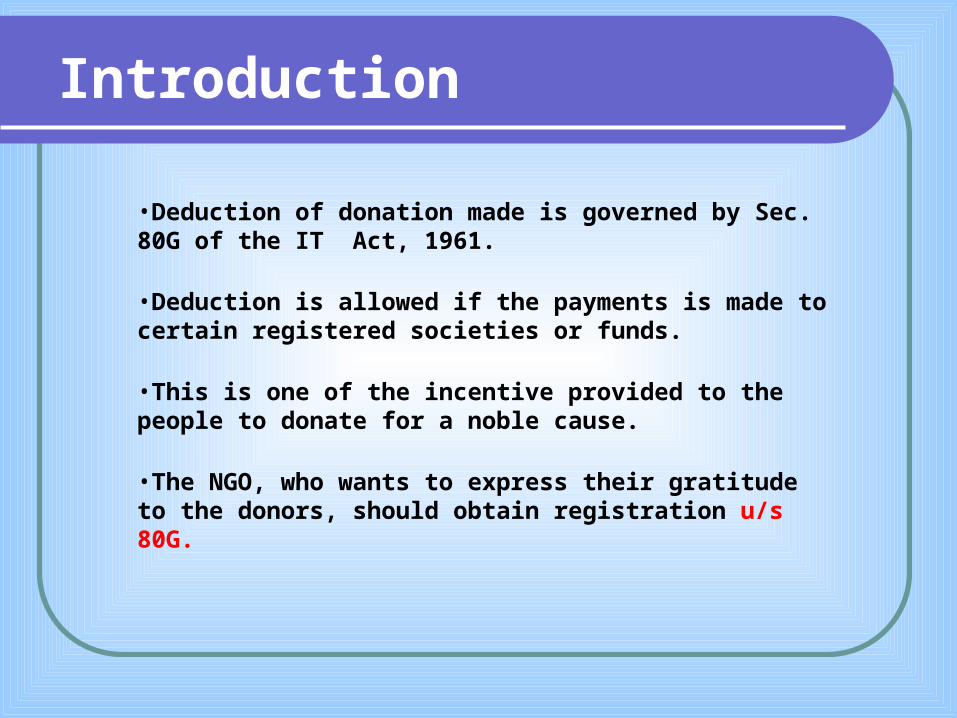

Introduction

•Deduction of donation made is governed by Sec. 80G of the IT Act, 1961.

•Deduction is allowed if the payments is made to certain registered societies or funds.

•This is one of the incentive provided to the people to donate for a noble cause.

•The NGO, who wants to express their gratitude to the donors, should obtain registration u/s 80G.

What is Sec 80 G?

•Section 80G of the I.T. Act, 1961 enables an assessee to claim deduction for donation made by him to certain organizations. This deduction is subject to certain conditions.

• a. The organization receiving the donation should be registered or noted u/s 80G.

• b. The amount of donation is deductible 50% or 100%, max. to the extent of 10% of G.T.I. (except noted funds)

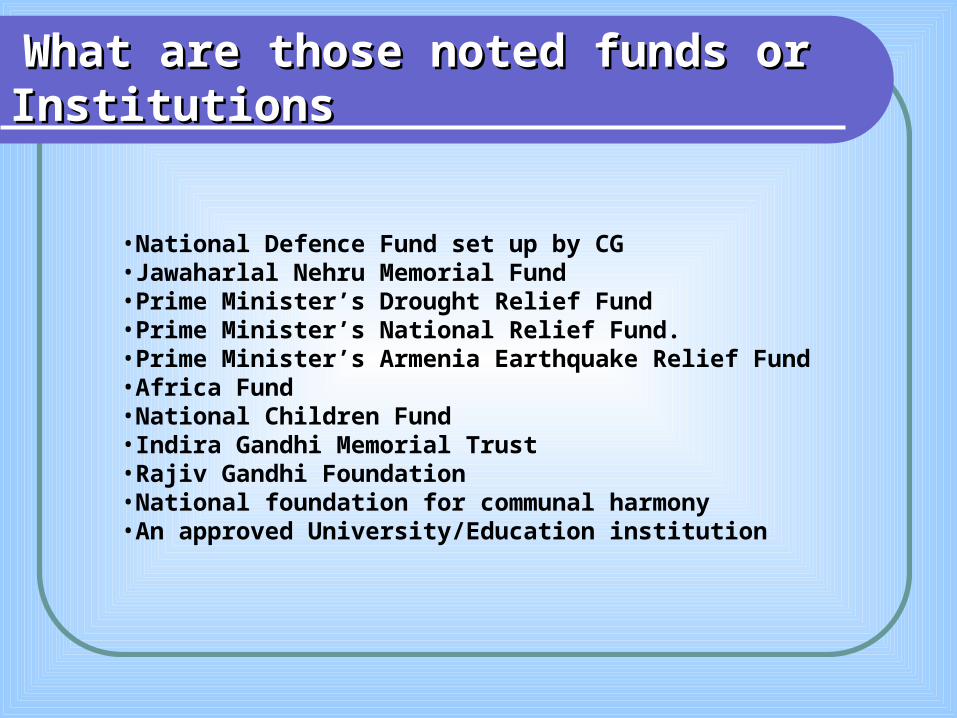

What are those noted funds or What are those noted funds or InstitutionsInstitutions

•National Defence Fund set up by CG•Jawaharlal Nehru Memorial Fund•Prime Minister’s Drought Relief Fund•Prime Minister’s National Relief Fund.•Prime Minister’s Armenia Earthquake Relief Fund•Africa Fund•National Children Fund•Indira Gandhi Memorial Trust•Rajiv Gandhi Foundation•National foundation for communal harmony•An approved University/Education institution

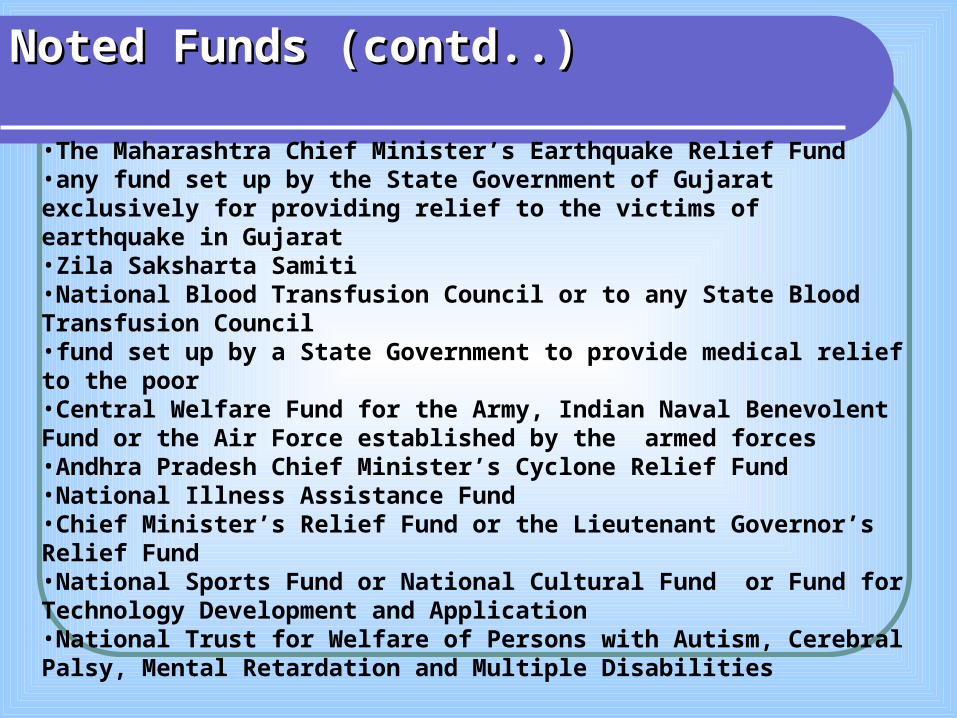

Noted Funds (contd..)Noted Funds (contd..)

•The Maharashtra Chief Minister’s Earthquake Relief Fund•any fund set up by the State Government of Gujarat exclusively for providing relief to the victims of earthquake in Gujarat•Zila Saksharta Samiti•National Blood Transfusion Council or to any State Blood Transfusion Council•fund set up by a State Government to provide medical relief to the poor•Central Welfare Fund for the Army, Indian Naval Benevolent Fund or the Air Force established by the armed forces•Andhra Pradesh Chief Minister’s Cyclone Relief Fund•National Illness Assistance Fund•Chief Minister’s Relief Fund or the Lieutenant Governor’s Relief Fund•National Sports Fund or National Cultural Fund or Fund for Technology Development and Application •National Trust for Welfare of Persons with Autism, Cerebral Palsy, Mental Retardation and Multiple Disabilities

Limit of 10% of G.T.I. is not applicable for the donations made all above funds

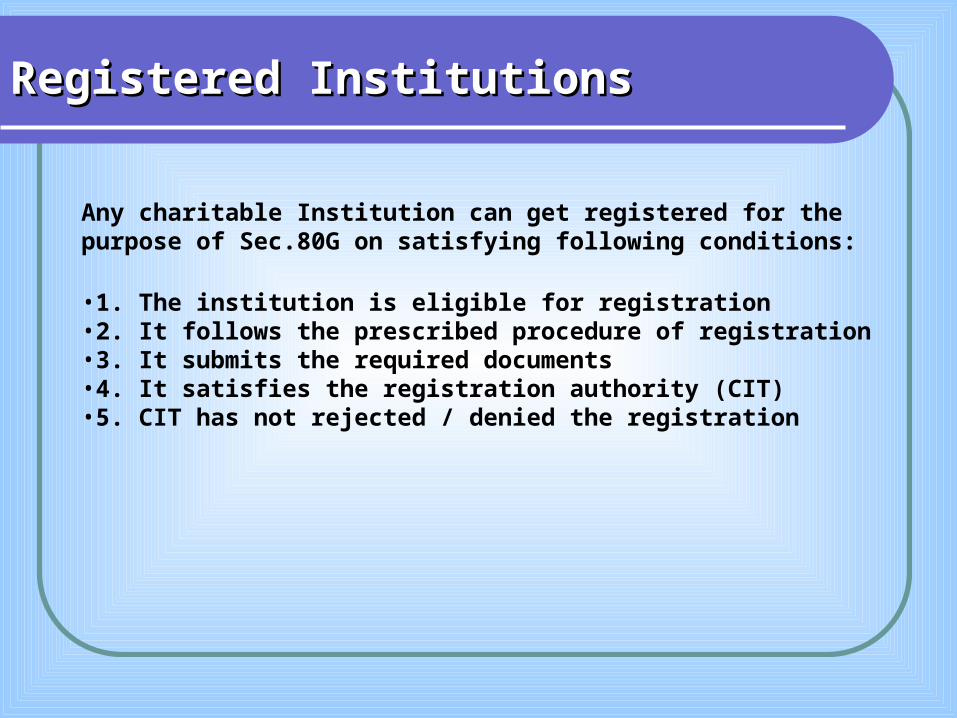

Registered InstitutionsRegistered Institutions

Any charitable Institution can get registered for the purpose of Sec.80G on satisfying following conditions:

•1. The institution is eligible for registration •2. It follows the prescribed procedure of registration •3. It submits the required documents•4. It satisfies the registration authority (CIT)•5. CIT has not rejected / denied the registration

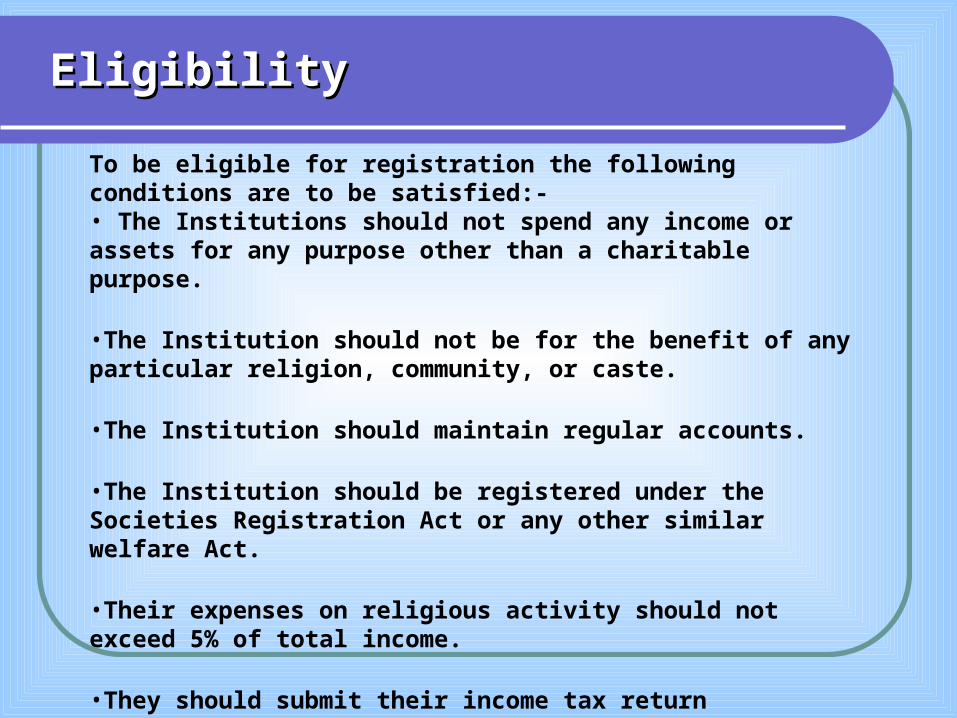

Eligibility Eligibility

To be eligible for registration the following conditions are to be satisfied:-• The Institutions should not spend any income or assets for any purpose other than a charitable purpose.

•The Institution should not be for the benefit of any particular religion, community, or caste.

•The Institution should maintain regular accounts.

•The Institution should be registered under the Societies Registration Act or any other similar welfare Act.

•Their expenses on religious activity should not exceed 5% of total income.

•They should submit their income tax return regularly.

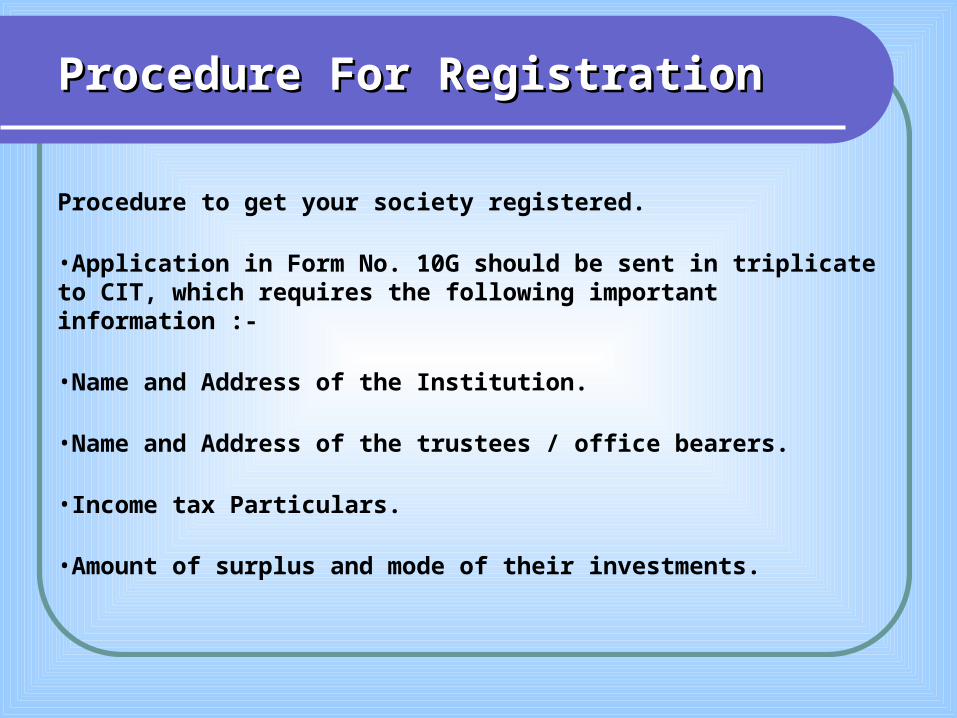

Procedure For Registration Procedure For Registration

Procedure to get your society registered.

•Application in Form No. 10G should be sent in triplicate to CIT, which requires the following important information :-

•Name and Address of the Institution.

•Name and Address of the trustees / office bearers.

•Income tax Particulars.

•Amount of surplus and mode of their investments.

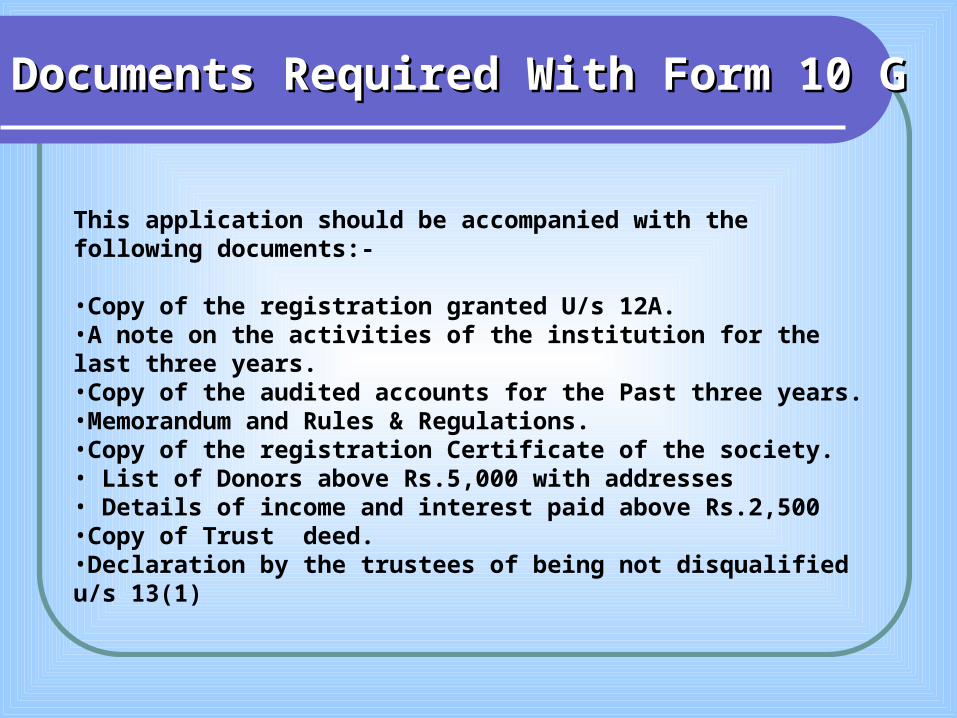

Documents Required With Form 10 Documents Required With Form 10 GG

This application should be accompanied with the following documents:-

•Copy of the registration granted U/s 12A.•A note on the activities of the institution for the last three years.•Copy of the audited accounts for the Past three years. •Memorandum and Rules & Regulations. •Copy of the registration Certificate of the society.• List of Donors above Rs.5,000 with addresses• Details of income and interest paid above Rs.2,500•Copy of Trust deed.•Declaration by the trustees of being not disqualified u/s 13(1)

Procedure followed by IT Department

•CIT may call for further information or cause such inquiries /inspection as he deems necessary to satisfy himself.

•If CIT satisfied that all conditions are fulfilled, he shall grant approval.

•CIT will grant registration within six months of submission of application, if he fails to grant/reject it shall be presumed that the registration is granted.

Procedure followed by IT Department

•Verification of Genuineness of the trust is not restricted to Sec. 12A

•Deep scrutiny of the proposal by I.T. Dept. is must as now the 80G is issued perpetually. And even International funds are procured by the trust.

•Scrutiny of financial documents such as Receipt Books, Cash Books, etc. plays important role to decide the genuineness of the trust.In case of rejection, notice shall be sent indicating the specific reason for the same, after giving an opportunity of being heard to the assessee.

Whether non attendance is equivalent to not being heard.

Reasons for rejection of application for registration u/s 80G can not be beyond non compliance of clauses (i) to (vi) of sec. 80G(5) & sec. 2(15) of I.T Act.

Clause u/s 80G(5) Of IT Act

Following shall result in rejection of application.

•Institution does not maintain separate books of account where it derives any income being profits & gains of business.

•The Institution does not maintain regular accounts

•The bylaws or objectives of the Institution are not specific about spending its income or assets for purposes other than charitable.

• Institution does not issue certificate to person making donation that it maintains separate books of account & that it will not use such donations for the purpose of such business.

• Institution uses the income derived for purpose other than charitable purpose

Cont…….

•The Institution is for the benefit of any particular religion, community, or caste.

•The Institution is not registered under the Societies Registration Act or any other similar welfare Act.

•The donations received by institution are used directly or indirectly for the purpose of such business.

SEC 2 (15) of I.T ACT

Section 2(15) of the Income Tax Act, 1961 (‘Act’) defines “charitable purpose” to include the following:-

(i) Relief of the poor(ii) Education.(iii) Medical relief.(iv) Preservation of environment.(v) Preservation of monuments or

places or objects of artistic or historic nature.

(vi) the advancement of any other object of general public utility.

Denial Of Registration

•Registration u/s 80G(5)(vi) cannot be denied to charitable trust even if it is running some activity that yields profit.

CASE LAW DETAILS: -

Decided by: ITAT, BANGALORE BENCH `B’,

In The case of: Prasanna Trust v. DIT (Exemption)

Appeal No: ITA No. 1391/Bang./2008

Decided on: June 12, 2009

Denial Of Registration

Can the Registration u/s 80G be denied to charitable trust in following conditions :

•Non-submission of list of donors above Rs.5,000

•Spending of trust is not more than 85% of receipts; And application for accumulation is not submitted in Form 10.

•Return of Income is not filed

•Resolution of accumulation is not submitted

•PAN of trustees are not submitted

Denial Of Registration

Can the Registration u/s 80G be denied to charitable trust in following conditions :

•ITRs of Trustees are not submitted.

•Trust money is advanced to a firm in which trustee(s) is interested.

•During inspection at sight the inspector could not find any administrative set-up at given address.

•Employee(s) of the trust is relative of trustees. {40A(2)(b)}

Denial Of Registration

Can the Registration u/s 80G be denied to charitable trust in following conditions :

•Shot term receipts are used for long term expenses.

•Rate of Interest of unsecured loan taken from trustees are higher than bank rate

•In the opinion of CIT, if concessional charges are recovered from the service availers will not amount to charity

Denial Of Registration

Can the Registration u/s 80G be denied to charitable trust in following conditions :

•In the opinion of CIT, if the discrimination is made in charging to service availers will not amount to charity

•Religious expenses are more than 5% of total expenses.

•In the opinion of CIT, Substantial exp. incurred on renovation of the temple is religious exp.

Some Important Points

•Even if the CIT denies the registration u/s 80G, the rejection order is now appeal able.

•Deduction u/s 80G is not available to the donor of in kind offerings.

•If the trust is having business directly related with the object of the trust and turnover of the business is more than Rs.60 Lacs, whether tax audit will require?

•If application of the funds by the trust is less than 85% on its object, then what are the rate of tax and what is the exemption limit to the trust?

Renewal For Approval

•If the 80G approval is existing as on 01/10/2009 it need not be renewed.

•Approval is deemed to have been continued unless it is cancelled by the Income tax authority.

•This amendment is as a consequence to the omission of the proviso to clause (vi) of section 80G(5) by The Finance (no.2)Bill,2009.

22

Contact:CA Nandkishor Malpani,

NVM & Associates,Chartered Accountants,

“Ramkunj”, Railway Station Road,New Osmanpura, Aurangabad-431005

Mobile No.: 9823388620Office:0240-2326106

E-mail ID: [email protected]