files.constantcontact.com file · Web viewfiles.constantcontact.com

Regional Workshops

Hot Topics for Successful Projects: Lease-Leaseback Options, Cost Escalation and Financial Markets, and Sacramento Policy Updates

COAST CCD

Friday, May 18, 2018 9:00 am to 2:00 pm District Board Room 1370 Adams Avenue

Costa Mesa, CA 92626

AGENDA

9:00 am Welcome and Opening Remarks Jerry Marchbank, CCFC Board of Directors, Coast CCD 9:15 am Cost Escalation and the Current Construction Climate: Understanding and

Navigating the Market Geoffrey Bachanas, Kitchell CEM Wendy Cohen, Kitchell CEM Tom Macias, MiraCosta College 10:15 am 2018 Financial Issues and the Bond Market Robert Barna, Stifel, Nicolaus & Company, Inc. 10:45 am Break 11:00 am Lease-Leaseback: Best Practices for a Competitive Selection Process Carri Matsumoto, Rancho Santiago CCD Philip J. Henderson, Orbach Huff Suarez & Henderson LLP 12:15 pm Lunch 1:15 pm CCFC Policy Update: Proposition 51 Implementation and Capital Outlay

Legislation Rebekah Cearley, Community College Facility Coalition 2:00 pm Evaluations & Adjourn

CCFC Regional Workshop

Hot Topics for Successful Projects: Lease-Leaseback Options, Cost Escalation and Financial Markets, and Sacramento Policy Updates

Friday, May 18, 2018 9:00 a.m. – 2:00 p.m.

Coast CCD

COMMUNITY COLLEGE FACILITY COALITION 1303 J Street, Suite 520 ♦ Sacramento, CA 95814 ♦ Phone (916) 446-3042 ♦ Fax (916) 441-3893 ♦ www.caccfc.org

Cost Escalation and the Current Construction Climate: Understanding and Navigating the Market

Geoffrey Bachanas Kitchell CEM

Wendy Cohen Kitchell CEM

Tom Macias

MiraCosta College

May 18, 2018

CCFC Workshop 1

May 18, 2018

CCFC Workshop 2

May 18, 2018

CCFC Workshop 3

TBD – Rob McGregor’s slides

May 18, 2018

CCFC Workshop 4

May 18, 2018

CCFC Workshop 5

May 18, 2018

CCFC Workshop 6

May 18, 2018

CCFC Workshop 7

CCFC Regional Workshop

Hot Topics for Successful Projects: Lease-Leaseback Options, Cost Escalation and Financial Markets, and Sacramento Policy Updates

Friday, May 18, 2018 9:00 a.m. – 2:00 p.m.

Coast CCD

COMMUNITY COLLEGE FACILITY COALITION 1303 J Street, Suite 520 ♦ Sacramento, CA 95814 ♦ Phone (916) 446-3042 ♦ Fax (916) 441-3893 ♦ www.caccfc.org

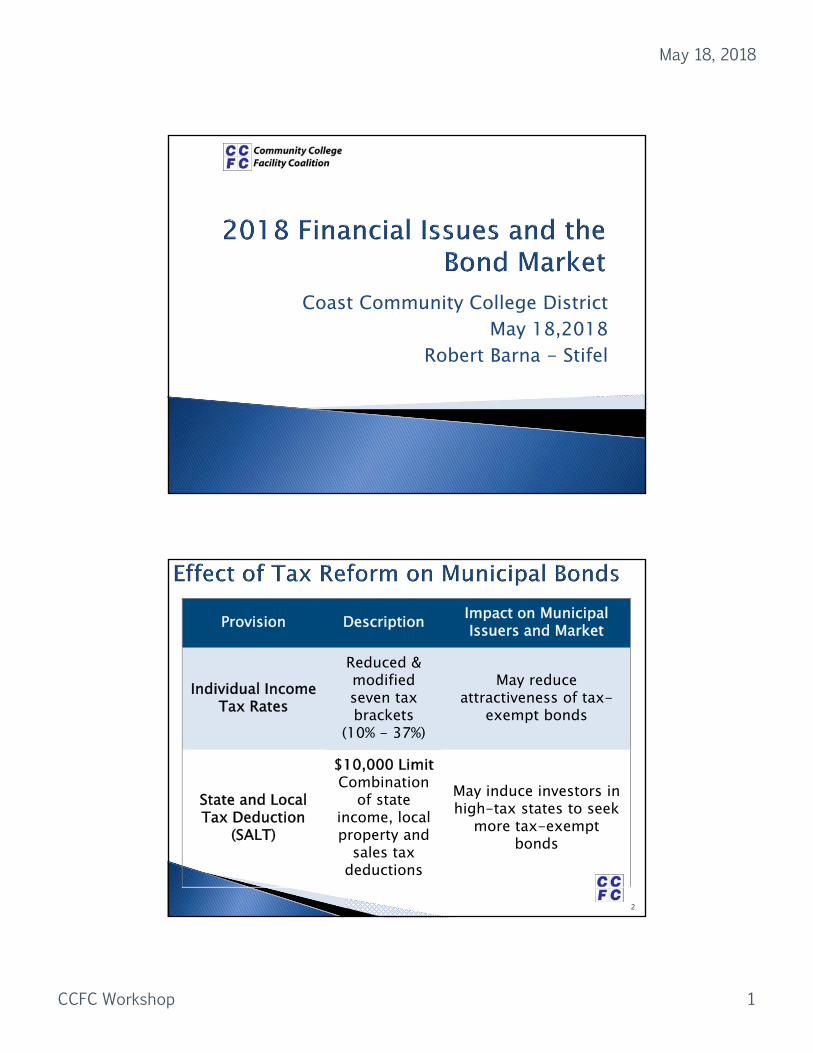

2018 Financial Issues and the Bond Market

Robert Barna Stifel, Nicolaus & Company, Inc.

May 18, 2018

CCFC Workshop 1

Coast Community College DistrictMay 18,2018

Robert Barna - Stifel

2

Provision Description Impact on Municipal Issuers and Market

Individual Income Tax Rates

Reduced & modified seven tax brackets

(10% - 37%)

May reduce attractiveness of tax-

exempt bonds

State and Local Tax Deduction

(SALT)

$10,000 Limit Combination

of state income, local property and

sales tax deductions

May induce investors in high-tax states to seek

more tax-exempt bonds

May 18, 2018

CCFC Workshop 2

3

Provision Description Impact on Municipal Issuers and Market

Corporate Tax Rate

Reduced to 21%

May lower attractiveness of tax-

exempt bonds for corporations and

insurance companies

Tax Credit Bonds

Eliminated ability to issue QZABs, CREBs, QSCBs, BABs, and other tax credit bonds

No changes to subsidy payments for bonds

issued before December 31, 2017; may reduce

incentive to fund energy efficiency projects

4

Provision Description Impact on Municipal Issuers and Market

Advance Refundings

Eliminated tax-exempt advanced

refundings

Limits issuers to current refundings; may reduce

feasibility of refundings and encourage use of taxable bonds or forward delivery

structures

Fiscal Impact

Estimated to generate $1.5 trillion deficit over the next

decade

Deficit of more than $150 billion in any year may

trigger additional sequestration of federal subsidies for BABs and similar products; may

increase Treasury borrowing needs which may increase

bond interest rates

May 18, 2018

CCFC Workshop 3

34%

50%41%

38%

27%

25%

8%7%

15%

16% 12% 14%

4% 4% 5%

0%

20%

40%

60%

80%

100%

1997 2007 2017 2018+

Individuals* Mutual Funds (1) Banking Institutions (2) Insurance Companies (3) Other (4)

$1.3 Trillion $3.5 Trillion $3.9 Trillion

5

Did not limit or repeal the tax deductibility of interest from municipal bonds

The reduction of corporate tax rate to 21% will likely reduce the appetite of bank portfolios and property/casualty insurance companies for tax-exempt municipals

Source: SIFMA and the Federal Reserve System(1) Includes mutual funds, money market funds, closed‐end funds and exchange traded funds.(2) Includes U.S. chartered depository institutions, foreign banking offices in the U.S., banks in U.S. affiliated areas, credit unions, and broker dealers.(3) Includes property‐casualty and life insurance companies.(4) Includes nonfinancial corporate business, nonfinancial non‐corporate business, state and local governments and retirement funds, government‐sponsored enterprises and foreign holders.* Household holdings is revised up by about $840 billion, on average, from 2004 forward.

Changing Landscape of Municipal Bond Investors

?

6

Limiting State and Local Government Tax Deduction to $10,000 and the mortgage interest deduction cap to a $750,000 mortgage could affect the willingness of California voters to approve additional taxes and impact CCDs’ ability to pass local bond measures

Eliminating tax credit bonds increases the cost of borrowing for California educational facilities (QZABs and CREBs have financed solar & energy efficiency projects in recent years)

Eliminating tax-exempt advanced refundings reduces the ability to restructure or refinance existing bonds

Source: Thomson Reuters.

May 18, 2018

CCFC Workshop 4

7

Assembly Bill 195 (Obernolte) 75-Word Ballot Statement :—Must include the amount of money to be raised annually

and the rate and duration of the tax to be levied for the bonds

—Must be a true and impartial synopsis of the purpose of the proposed measure

—Must be in language that is neither argumentative nor likely to create prejudice for or against the measure

8

Unintended Consequences of AB 195 Confusion instead of transparency

Requirement consumes 15-20 of the 75-word limit for the ballot question

“To ______________________, shall this measure of the _______ Community College District issuing $___ in bonds at legal rates be adopted, levy on average 2.5 cents per $100 assessed value, $___ annually for ______ [e.g. job training facilities], while bonds are outstanding, with annual audits, etc.?”

Sample Ballot Statement

May 18, 2018

CCFC Workshop 5

9

Senate Bill 450 (Hertzberg) Prior to authorization of the issuance of bonds the governing

body shall obtain and disclose all of the following information in a meeting open to the public:— The true interest cost of the bonds— The finance charges of the bonds (essentially costs of issuance)— The amount of proceeds received by the issuer less finance charges,

reserves and capitalized interest— The total payment amount of the bonds (debt service + finance charges

not paid with proceeds of the bonds), calculated to the final maturity date

Good faith estimates can be provided by the underwriter, financial adviser or private lender

10

Senate Bill 1029 (Hertzberg) Establishes local debt policies and reporting requirements

for California local government agencies— Types of debt and purposes for debt proceeds— Relationship of the debt to the issuer’s capital improvement

program or budget— Policy goals related to the issuer’s planning goals and objectives

Effective for all debt sold on or after January 21, 2017

A report must be provided to California Debt and Investment Advisory Commission (CDIAC) no later than 30 days prior to issuance that the issuer has adopted a debt policy and that the bond issue complies with those debt policies

May 18, 2018

CCFC Workshop 6

11

Equity Market Performance

1,000

1,200

1,400

1,600

1,800

2,000

2,200

2,400

2,600

2,800

3,000

11,500

13,500

15,500

17,500

19,500

21,500

23,500

25,500

27,500

Jan‐13 Jan‐14 Jan‐15 Jan‐16 Jan‐17 Jan‐18

S&P 500DJIA

DJIA

S&P 500

Source: US Treasury Department, Bloomberg, Thomson Reuters. As of 5/3/18

12Source: US Treasury Department, Bloomberg, Thomson Reuters. As of 5/3/18

Treasury Market Yields

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

Jan‐15 Jul‐15 Jan‐16 Jul‐16 Jan‐17 Jul‐17 Jan‐18

30‐Year UST

10‐Year UST

2‐Year UST

May 18, 2018

CCFC Workshop 7

Source: Thomson Reuters. As of 5/3/18 13

‘AAA’ Municipal Market Data Yields

• Sharp uptick in rates in 2018 YTD due to ongoing recovery of US economy and Federal Reserve rate hikes

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

Jan‐15 Apr‐15 Jul‐15 Oct‐15 Jan‐16 Apr‐16 Jul‐16 Oct‐16 Jan‐17 Apr‐17 Jul‐17 Oct‐17 Jan‐18 Apr‐18

30-Year MMD

10-Year MMD

2-Year MMD

Source: Thomson Reuters. As of 5/3/18 14

MMD Yield Curve

• Despite rising short-term interest rates, long-term rates have declined from 2017 highs

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

1 3 5 7 9 11 13 15 17 19 21 23 25 27 29

5/3/2018

2017 High (3/14/17)

2017 Low (12/6/17)

May 18, 2018

CCFC Workshop 8

15Source: Thomson Reuters. As of 5/3/18

30-Year AAA MMD Since January 1, 2015

1.75%

2.00%

2.25%

2.50%

2.75%

3.00%

3.25%

3.50%

Jan‐15 Mar‐15 May‐15 Jul‐15 Sep‐15 Nov‐15 Jan‐16 Mar‐16 May‐16 Jul‐16 Sep‐16 Nov‐16 Jan‐17 Mar‐17 May‐17 Jul‐17 Sep‐17 Nov‐17 Jan‐18 Mar‐18 May

‐33 bps

+52 bps

‐26 bps

+54 bps

‐14 bps

+33 bps

‐36 bps

+25 bps

‐23 bps

+17 bps

‐57 bps

+27 bps

‐14 bps

‐32 bps

‐29 bps

+41 bps

‐5 bps

+36 bps

US Election11/8/2016

+81 bps

Brexit6/24/2016

‐47 bpsAverage: 2.81%

Max: 3.36% (6/10/2015)Min: 1.93% (7/6/2016)

Current: 3.00% (5/3/2018)

‐30 bps

‐39 bps

+18 bps

‐24 bps

+25 bps

‐39 bps

+52 bps

Tax Reform 1/1/2018

‐13 bps

+19 bps

+19 bps

+9 bps

+19 bps

1Long term issues only. Weekly averages of estimated 30‐day visible supply.Sources: SDC, Thomson Reuters, Investment Company Institute. As of 5/7/18

16

Municipal Market Annual Volume

• Municipal supply in 2017: $410 billion1

• Municipal supply in 2018 YTD: $102 billion1

– Volume down over 22% compared to same period in 2017

‐

50

100

150

200

250

300

350

400

450

500

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

($ in Billions)New Money Refunding

$410$386

$407$430

$277

$367

$312 $315

$378$424 $410

May 18, 2018

CCFC Workshop 9

1Long term issues only. Weekly averages of estimated 30‐day visible supply.Sources: SDC, Thomson Reuters, Investment Company Institute. As of 5/7/18

17

Weekly Municipal Mutual Fund Flows

• Investor demand remaining strong– Strong overall inflows into municipal mutual funds 2018 YTD

‐4

‐3

‐2

‐1

0

1

2

3

4

($ in Billions)

$3.5 billion of net inflows 2018 YTD12 weeks of inflows in 2018

$16 billion in outflows (Nov. 2016 ‐ Jan. 2017)

$31 billion in inflows (Jan. 2016 ‐ Oct. 2016)

18Source: U.S. Treasury Department, Bloomberg. Market Consensus Projections as of 5/3/18

Market Consensus Yield Curve ProjectionsCurrent 3Q18 4Q18 1Q19 2Q19

Fed Funds 1.75% 2.20% 2.40% 2.60% 2.80%

2-Year UST 2.48% 2.56% 2.70% 2.84% 2.96%

10-year UST 2.94% 3.02% 3.11% 3.21% 3.32%

30-year UST 3.12% 3.32% 3.44% 3.52% 3.62%

• Market consensus for the Federal Reserve to have two additional rate hikes in 2018

• Federal Reserve expected to continue “gradual” pace of rate increases with economic recovery

May 18, 2018

CCFC Workshop 10

Q & A

Robert BarnaManaging DirectorStifel, Nicolaus & Company, IncorporatedLos Angeles, Californiatel: 213-443-5205e-mail: [email protected]

Robert Barna is a Managing Director in the Los Angeles public finance office ofStifel. Mr. Barna began his public finance career in 1993 and has experience in allfacets of the municipal finance business. He specializes in the management,structuring and sale of California K‐14 Education new money and refundinggeneral obligation bonds, certificates of participation, tax credit bonds, Mello‐Roosbonds and tax and revenue anticipation notes. Throughout his career, he hascompleted more than 200 financings totaling over $15.0 billion.

Mr. Barna graduated with a degree in Economics from University of California,Berkeley, and a Masters of Business Administration from Columbia University.

CCFC Regional Workshop

Hot Topics for Successful Projects: Lease-Leaseback Options, Cost Escalation and Financial Markets, and Sacramento Policy Updates

Friday, May 18, 2018 9:00 a.m. – 2:00 p.m.

Coast CCD

COMMUNITY COLLEGE FACILITY COALITION 1303 J Street, Suite 520 ♦ Sacramento, CA 95814 ♦ Phone (916) 446-3042 ♦ Fax (916) 441-3893 ♦ www.caccfc.org

Lease-Leaseback: Best Practices for a Competitive Selection Process

Carri Matsumoto

Rancho Santiago CCD

Philip J. Henderson Orbach Huff Suarez & Henderson LLP

May 18, 2018

CCFC Workshop 1

Lease-Leaseback in a Post-AB 2316 World—An Option for CCDs

Phil HendersonOrbach Huff

Suarez & [email protected]

Community College Facility Coalition May 2018

Carri MatsumotoRancho Santiago Community College [email protected]

District

Architect

Trade Contractor

LLB Contractor

Trade Contractor Trade Contractor

Lease-Leaseback Structure

May 18, 2018

CCFC Workshop 2

California Community College District Procurement Generally

Bid Limits. California Community College Districts must formally and publicly bid contracts for construction projects over $15,000, unless there is an exception. (Public Contract Code (“PCC”) § 20651.)Design-Bid-Build (DBB)

General Contractor (GC)Construction Manager / Multiple Prime (CM/MP)

Lease-Leaseback is an Exception to DBB. Lease-Leaseback (LLB): Education Code § 81335

Statutory AuthorityLLB was enacted at a time when there was a shortage of money for public construction (Education Code § 81335 (a)):

“… a community college district may let … real property which

belongs to the district if the [lease] requires the lessee … to

construct … a building or buildings for the use of the community

college district.”

For school districts (K-12), the language is different (prior

Education Code § 17406 (a)):“Notwithstanding Section 17417… a school district, without

advertising for bids, may let … real property that belongs to the

district if the [lease] requires the lessee … to construct … a

building or buildings for the use of the school district.”

May 18, 2018

CCFC Workshop 3

Statutory AuthorityA couple of years ago, multiple school district (K-12) LLB contracts were challenged, principally by one attorney.

Some of the LLB CasesDavis v. Fresno USD

McGee v. Torrance USD

CTAN v. Mt. Diablo USD (12 Cal.App.5th 115 (2017).)Follows McGee in rejecting the Davis holding that a lease‐leaseback must be a “genuine lease,” must include a financing component, and must provide for the use of the facilities “during the term of the lease” because those terms are not included in the authorizing statute.

Also follows McGee in holding that sufficient facts alleged to allow a conflict of interest cause of action under Government Code section 1090 for private contractors because CTAN alleged the contractor, Taber, performed the functions of a public employee.

May 18, 2018

CCFC Workshop 4

Some of the LLB Cases, cont’d.

California appellate courts are now divided on

whether financing and a lease term are required

in a Lease‐Leaseback.

This means that until the California Supreme

Court addresses the issue, all superior courts

are free to pick and choose whichever ruling

they wish to follow – or arrive at a result which

is entirely different.

Recent CasesConflict of Interest

Hub City / Sahlolbei: The California Supreme Court has ruled that Section 1090 applies (including the criminal penalties) to independent contractors or consultants, where the consultant influences a public entity’s contracting decisions or “otherwise acts in a capacity that demands the public trust.” (Hub City Solid Waste Services, Inc. v. City of Compton (2010), 186 Cal. App. 4th 1114, 1124-1125 (“Hub City”); see also, People v. Superior Court (Sahlolbei) (2017), 3 Cal. 5th 230, 237.).

May 18, 2018

CCFC Workshop 5

Recent CasesConflict of Interest, cont’d.

Critical factor is the extent to which the person influences an agency's contracting decisions or otherwise acts in a capacity that demands the public trust.

Resolves conflict between appellate districts on this issue.

Follows the Davis ruling as it pertains to lease‐leaseback contractors who are providing preconstruction services.

Districts should assure that they maintain control of contracting decisions and do not effectively outsource that responsibility to contractor consultants.

Rancho Santiago CCD: Decision to Follow Changes in K-12 Legislation

Legal risk reduced / Increased defensibility

Statutory process, even if for K-12, can bolster CCD process

Equal opportunity for contractors to participate in the prequalification process,

What is an adequate participation and response period and pool size?

May 18, 2018

CCFC Workshop 6

AB 2316 – New LLB Requirementsfor K-12 Districts

Became effective January 1, 2017.Was supported by trade unions, CASBO, CASH, others.LLBs must now be advertised in newspaper and in a trade paper.District can require a “lump sum” or a proposed fee for preconstruction and for the construction.

The LLB contract can include “preconstruction services” even if plans are not yet DSA-approved.

Best Value. Contract shall be awarded based on “competitive solicitation process” to contractor providing the best value based on RFQ & RFP. (Ed. Code § 17406 (a)(2).)

Board Action. District must adopt and publish the procedures and guidelines for evaluating the best value.

1-Step or 2-Step. District can either do one RFQ/P or separate RFQ and then an RFP.

Advertising for Subs. If it is not a lump sum (where the subcontractors are prequalified too), the contractor must select subcontractors, “in accordance with the publication requirements applicable to the competitive bidding process of the school district.” (Ed. Code § 17406 (a)(4)(B)(i).)

AB 2316 – New LLB Requirementsfor K-12 Districts

May 18, 2018

CCFC Workshop 7

Best Value DeterminationThe Board pre-approves the criteria, the scoring, etc. Similar to prequalification. These can be difficult to know ahead of time.

Pricing factors (GCs, mark-up, bonds/insurance, etc.)Past LLB experienceStaffingCurrent workloadEtc.

Reference checks? If so, when?

Interviews? If so, when?

AB 2316 – New LLB Requirementsfor K-12 Districts

Most Common StructureDistrict selects architect through competitive selection process. (Gov. Code § 4525, et seq.)

District advertises and selects contractor through Board-approved process, criteria and scoring.

District and contractor enter into a LLB contract.District leases real property to a builder for $1.

Contractor develops a price to construct the facility.This can happen at different points in the process.

The District determines what portion of that price it will finance from the contractor.

May 18, 2018

CCFC Workshop 8

Most Common Structure, cont’d.

Contractor constructs the facility, then leases the facility back to the District. This is the “leaseback” component.

The construction terms and conditions are part of the contract documents.

District pays for construction costs through tenant improvement payments during construction.District pays lease payments, plus interest, for a period oftime after construction.

This portion is the amount being financed.

Title to the new facility vests in the District as lease payments are made.

One Possible Process That Follows AB 2316 Changes

Board Action. District Board adopts the procedures and guidelines regarding criteria for best value evaluation.RFQ. District issues an RFQ to solicit contractors based on the Board-adopted criteria.Advertisement. District publishes notice of RFQ in newspaper and in trade paper.Prequalification. The RFQ includes a prequalification questionnaire, either the District’s existing form, a new specific firm, or a 3rd-party process (e.g., QualityBidders).Contract. RFQ includes the form of LLB contract.

May 18, 2018

CCFC Workshop 9

One Possible Process That Follows AB 2316 Changes, cont’d.

Evaluation of RFQ. The District evaluates the RFQ responses based on the evaluation criteria and form that was part of the RFQ. This will likely result in a shortlist of qualified contractors.RFP. The District issues an RFP that asks qualified contractors to price the project.Award. The District awards the contract to the contractor with the best value proposal.Important

The above process is only one option of many that are permitted under the new statute. A district can combine the RFQ and RFP steps, it can create a pool for multiple projects, it can award a contract on a lump sum price or on pricing factors, etc.A district should consider various options and confer with its consultants and legal counsel prior to initiating one process.

Rancho Santiago CCD Lessons Learned

Using LLB can enhance working relationships and collaboration.

Creating a short list of contractors can help keep interest high

Staff review can take a lot of time:Prequalification forms (general and subcontractors), RFQ response, RFP responses

May 18, 2018

CCFC Workshop 10

Rancho Santiago CCD Lessons Learned, cont’d.

Subcontractor selection can be confusing and misunderstood (including the need for the contractor to advertise).Financing the lease payments is sometimes misunderstood.Phasing of the RFQ, RFP, etc. and coordination of steps can be difficult.Ensure your process to prequalify subcontractors that want to prequalify for more than one license classification.Will you be actually evaluating the contractors’ financial records?

Some Questions to Ask Before Setting the Procurement Process

Are the Plans DSA approved?

Are preliminary services/preconstruction services desired?

Will there be some scopes (e.g., non-DSA scopes) that can be done in an earlier phase before pricing of the whole project?

One project? Multiple projects?

If only one project, can you select the contractor in one step (RFQ/P)?

Will there be a need for a “pool” of contractors for multiple projects?

Will you call references and do interviews and, if so, will you shortlist the respondents first?

May 18, 2018

CCFC Workshop 11

Some Questions to Ask Before Setting the Procurement Process,

cont’d.Is the project sufficiently described for a contractor to price its general conditions? Mark-up on subcontractor work? Mark-up on change order work? Fee? Bonds & Insurance? Other charges?When to prequalify the MEP subcontractors? In the RFQ? In the RFP? If a contractor is selected and is free to select subcontractors later, do you permit a best value determination or low bid? How do you ensure the contractor is incentivized to keep its price down at that time?If contractors are still competing at the RFP stage, is the answer the same?How much of the price to put into lease payments / financing? Many more…

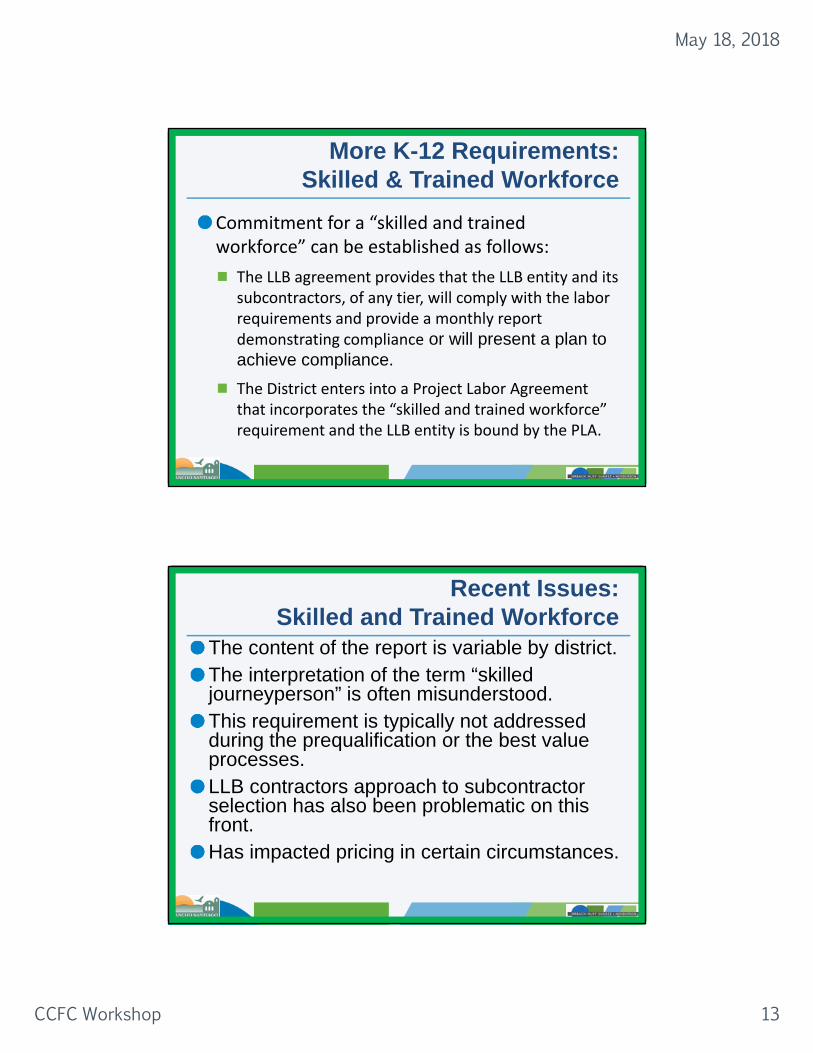

Contractor to provide an “enforceable commitment” to use “skilled and trained workforce” to perform all work falling within an “apprenticeable occupation” in the building trades. (Educ. Code § 17407.5.)The project’s “skilled and trained workforce” must be comprised of journeymen who have graduated from a state‐approved program or have enough on‐the‐job hours to have graduated, and apprentices that are enrolled in a state‐approved program.

The District is the enforcing agency.

More K-12 Requirements: Skilled & Trained Workforce

May 18, 2018

CCFC Workshop 12

January 1, 2019 50%

January 1, 2020 60%

As of January 1, 2018, at least 40% of the workers employed by the entity and each of its subcontractors at every tier must be graduates of an approved apprenticeship program for the applicable occupation (certain subcontractors capped at 30%).

Percentage only applies to each “apprenticeable” trade and not the entire labor force.

Percentage increases over next two years:

More K-12 Requirements: Skilled & Trained Workforce

Teamsters are no longer included.

Skilled Journeypersons must be at 40% starting January2018, except the following categories will remain at 30%:

“acoustical installer, bricklayer, carpenter, cement mason, drywall installer or lather, marble mason, finisher, or setter, modular furniture or systems installer, operating engineer, pile driver, plasterer, roofer or waterproofer, stone mason, surveyor, teamster, terrazzo worker or finisher, and tile layer, setter, or finisher.”

SB 418 (Hernandez)Changes to Skilled and Trained

Workforce

May 18, 2018

CCFC Workshop 13

Commitment for a “skilled and trained workforce” can be established as follows:

The LLB agreement provides that the LLB entity and its subcontractors, of any tier, will comply with the labor requirements and provide a monthly report demonstrating compliance or will present a plan to achieve compliance.The District enters into a Project Labor Agreement that incorporates the “skilled and trained workforce” requirement and the LLB entity is bound by the PLA.

More K-12 Requirements: Skilled & Trained Workforce

Recent Issues:Skilled and Trained Workforce

The content of the report is variable by district.The interpretation of the term “skilled journeyperson” is often misunderstood.This requirement is typically not addressed during the prequalification or the best value processes.LLB contractors approach to subcontractor selection has also been problematic on this front.Has impacted pricing in certain circumstances.

May 18, 2018

CCFC Workshop 14

Lease-Leaseback in a Post-AB 2316 World—An Option for CCDs

Phil HendersonOrbach Huff

Suarez & [email protected]

Community College Facility Coalition May 2018

Carri MatsumotoRancho Santiago Community College [email protected]

CCFC Regional Workshop

Hot Topics for Successful Projects: Lease-Leaseback Options, Cost Escalation and Financial Markets, and Sacramento Policy Updates

Friday, May 18, 2018 9:00 a.m. – 2:00 p.m.

Coast CCD

COMMUNITY COLLEGE FACILITY COALITION 1303 J Street, Suite 520 ♦ Sacramento, CA 95814 ♦ Phone (916) 446-3042 ♦ Fax (916) 441-3893 ♦ www.caccfc.org

CCFC Policy Update: Proposition 51 Implementation and Capital Outlay

Rebekah Cearley Community College Facility Coalition

May 18, 2018

CCFC Workshop 1

Rebekah CearleyCCFC Legislative Advocate

Spring 2018 Regional Workshop

Paul Holmes Facilities Leadership Achievement Award Nominations

Political Landscape Community College Capital Outlay and

Budget 2018 Legislation

May 18, 2018

CCFC Workshop 2

Nominees should demonstrate a commitment and dedication to the Mission and Values of CCFC:

Mission: Provide leadership in legislative advocacy and deliver critical information, education, and training on facilities issues for community college districts and their business partners to enhance student learning.

Vision: Be the voice of and provide resources and education for professionals engaged in California’s community college facilities.

Nominations due to Jessica Contreras at CCFC by Friday, May 25, 2018.

Second year of legislative session began Jan. 3, 2018◦ May 25 – Appropriations deadline in first house

Climate and culture in the Legislature◦ Sexual harassment◦ Federal issues

2018 election◦ Governor’s race – Brown is a lame duck◦ Legislative supermajority in jeopardy?

Leadership transitions◦ New Senate President Pro Tem: Toni Atkins

May 18, 2018

CCFC Workshop 3

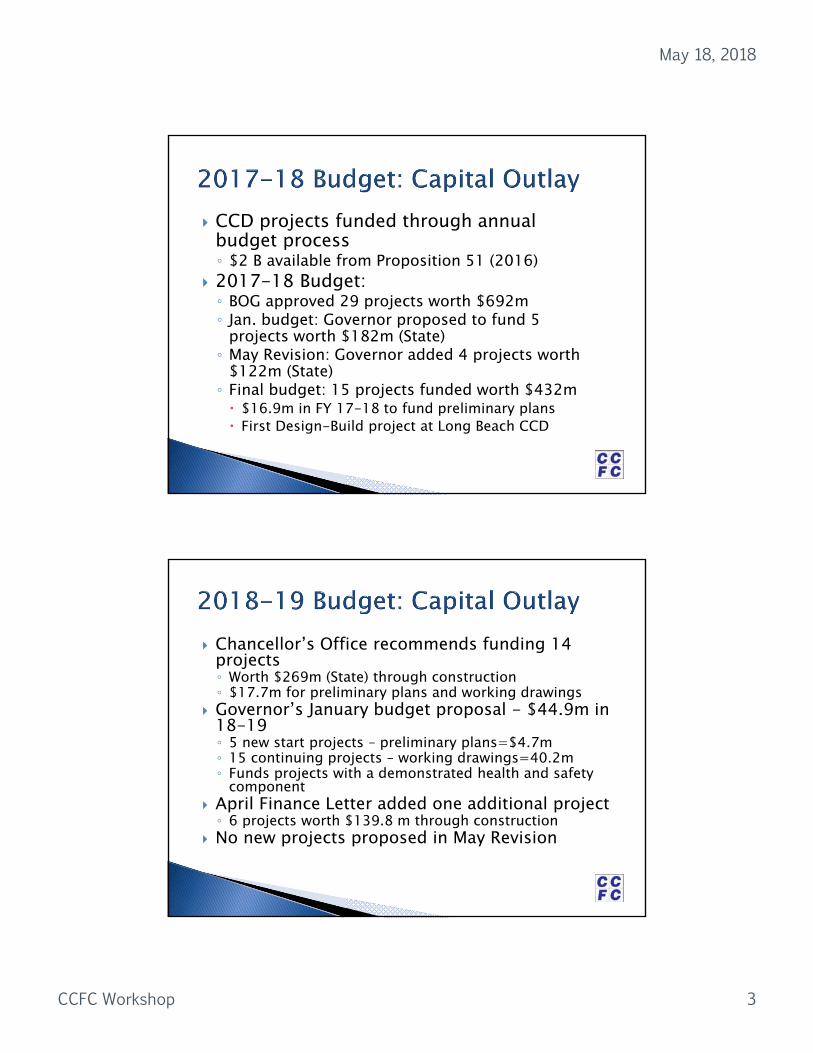

CCD projects funded through annual budget process◦ $2 B available from Proposition 51 (2016)

2017-18 Budget:◦ BOG approved 29 projects worth $692m◦ Jan. budget: Governor proposed to fund 5

projects worth $182m (State)◦ May Revision: Governor added 4 projects worth

$122m (State)◦ Final budget: 15 projects funded worth $432m $16.9m in FY 17-18 to fund preliminary plans First Design-Build project at Long Beach CCD

Chancellor’s Office recommends funding 14 projects◦ Worth $269m (State) through construction◦ $17.7m for preliminary plans and working drawings

Governor’s January budget proposal - $44.9m in 18-19◦ 5 new start projects – preliminary plans=$4.7m◦ 15 continuing projects – working drawings=40.2m ◦ Funds projects with a demonstrated health and safety

component April Finance Letter added one additional project◦ 6 projects worth $139.8 m through construction

No new projects proposed in May Revision

May 18, 2018

CCFC Workshop 4

Redwoods Community College District - College of the Redwoods: Arts Building Replacement [Category A]

Coast Community College District, Golden West College: Language Arts Complex [Category B]

Mt. San Antonio Community College District, Mt. San Antonio College: New Physical Education Complex [Category D]

Peralta Community College District, Laney College: Learning Resource Center [Category B]

Peralta Community College District, Merritt College: Child Development Center [Category D]

Imperial Valley CCD, Imperial Valley College: Academic Buildings Modernization [Category C] –April DOF Letter

CCFC is asking to fund all 14 new projects◦ Delay reduces purchasing power of $2 B◦ Chancellor’s Office is in best position to assess system-

wide priorities LAO: Recommends the Legislature consider

authorizing additional projects, develop a multi-year expenditure plan for remaining Prop 51 funds

Budget education subcommittees:◦ Assembly Member McCarty: “We respectfully disagree with

the Governor”◦ Senator Portantino: How do we get to all 14?

Chancellor’s Office plans $750m in FY 19-20, $500m in 20-21

May 18, 2018

CCFC Workshop 5

Online College - $120m◦ To serve working adults not currently accessing higher

education◦ Chancellor’s Office supports

New student funding formula for apportionments◦ Base grant (60%)◦ Supplemental grant – low income students (20% )◦ Student success incentive grant – number of degrees and

certificates (20%) Deferred Maintenance & Instructional Equipment◦ $275.2m in January ◦ $143.5 m in May Revision ◦ No district match required

Chancellor’s Office State Operations - $2m to fill 15 vacant positions

Sponsored by State Controller Increases CUPCCAA informal bid limits in statute CA Uniform Construction Cost Accounting

Commission recommends:◦ Increase the no-bid cap from $45k to $60k◦ Increase the informal bid level for projects between $45k

and $175k to projects between $60k and $200k◦ Increase the formal bid level to any project over $200k

Last increase was in 2011 CCFC Supports Status: Passed by Assembly, awaiting

consideration in Senate

May 18, 2018

CCFC Workshop 6

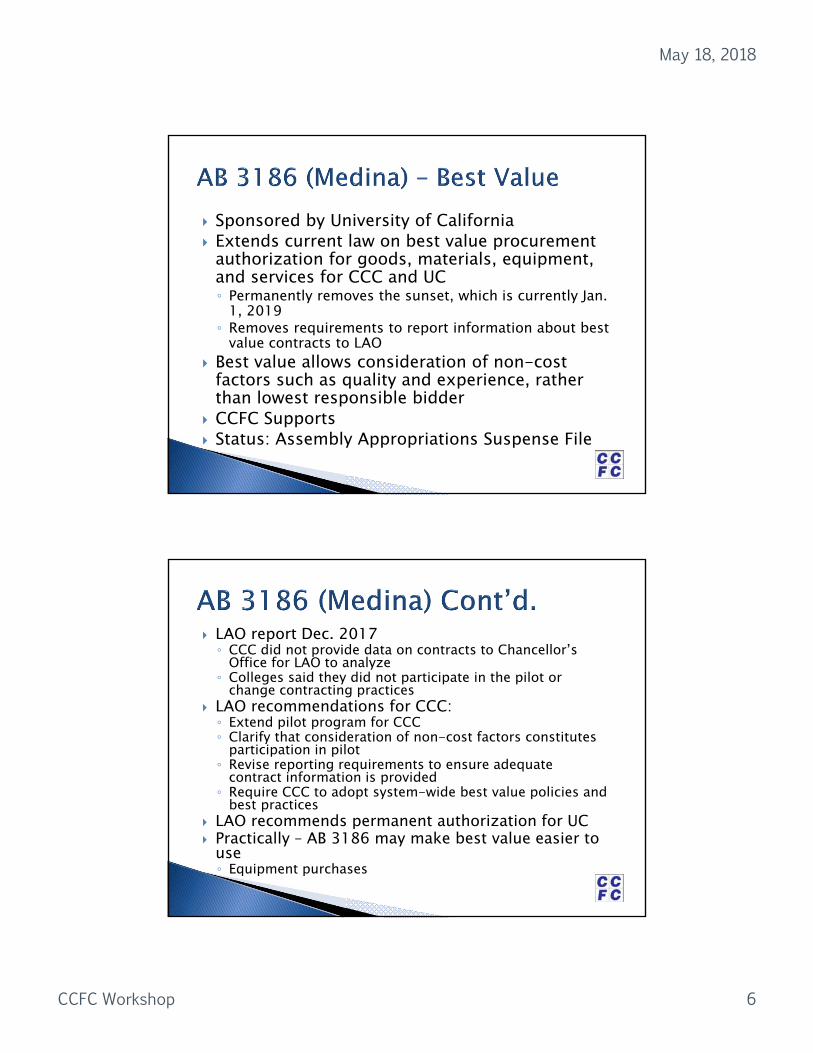

Sponsored by University of California Extends current law on best value procurement

authorization for goods, materials, equipment, and services for CCC and UC◦ Permanently removes the sunset, which is currently Jan.

1, 2019◦ Removes requirements to report information about best

value contracts to LAO Best value allows consideration of non-cost

factors such as quality and experience, rather than lowest responsible bidder

CCFC Supports Status: Assembly Appropriations Suspense File

LAO report Dec. 2017◦ CCC did not provide data on contracts to Chancellor’s

Office for LAO to analyze◦ Colleges said they did not participate in the pilot or

change contracting practices LAO recommendations for CCC:◦ Extend pilot program for CCC◦ Clarify that consideration of non-cost factors constitutes

participation in pilot◦ Revise reporting requirements to ensure adequate

contract information is provided◦ Require CCC to adopt system-wide best value policies and

best practices LAO recommends permanent authorization for UC Practically – AB 3186 may make best value easier to

use◦ Equipment purchases

May 18, 2018

CCFC Workshop 7

Sponsored by Women’s Policy Institute States that community colleges shall provide

reasonable accommodations for lactating students to express breast milk or breast feed a child

Requires a sink in the accommodation space for new campuses/buildings or renovation/replacement of existing building◦ Amendments in the works

CCFC has concerns with sink mandate, working with author and sponsors

Status: Assembly Appropriations Suspense File

Chaptered in 2017; applies to local bonds Requires local ballot measures that impose a tax

or raise the rate of a tax to include:◦ The rate of tax to be levied◦ The duration of tax to be levied◦ The amount of money to be raised annually

Polling shows 5 to 10% reduction in support with this language◦ Confused voters default to “NO” vote◦ Compliance with AB 195 uses ~33% of available 75

words on ballot label CCFC is asking for a fix in budget trailer bill

May 18, 2018

CCFC Workshop 8

Join us at the 2018 CCFC Annual Conference

September 10-12, 2018!

Sponsorships and Trade Show Booths available!

General registration opens in June.

Rebekah CearleyLegislative Advocate

Community College Facility [email protected]

(916) 446-3042

![-LINKS- [files.constantcontact.com]files.constantcontact.com/ffe891f7301/4dd8c62d-61aa-457f... · 2017. 3. 1. · MEMBER NEWSLETTER March 2017 4305 Brownsville Road ~ Pittsburgh,](https://static.fdocuments.in/doc/165x107/600fe800e60d2c76bf3b01d4/links-files-files-2017-3-1-member-newsletter-march-2017-4305-brownsville.jpg)

![Untitled-1 [files.constantcontact.com]files.constantcontact.com/3d72d0f4101/7874a19f-ab0c-4d08...New York City in the summer of 1922. Registered participants will be loaned a copy](https://static.fdocuments.in/doc/165x107/5f05f61e7e708231d4159833/untitled-1-files-files-new-york-city-in-the-summer-of-1922-registered-participants.jpg)

![WELCOME! [files.constantcontact.com]files.constantcontact.com/62a487b5001/421f1db5-fef5-43f4-bb56-63dd...I am delighted to welcome you to India Association of Greater Boston’s first-ever](https://static.fdocuments.in/doc/165x107/5ac05c827f8b9ad73f8ba44a/welcome-files-files-am-delighted-to-welcome-you-to-india-association-of-greater.jpg)