Region effects in the internationalization–performance relationship in Chinese firms

8

Region effects in the internationalization–performance relationship in Chinese firms Stephen Chen a, *, Hao Tan b,1 a Department of Business, Macquarie University, North Ryde, NSW 2109, Australia b School of Management, University of Western Sydney, Parramatta, NSW 2150, Australia 1. Introduction The internationalization–performance relationship is a key question in international business and significant research has been conducted over the last 30 or so years on this question. Despite the extensive research and attempts to develop a general model of the relationship between internationalization and performance (e.g. Contractor, Kundu, & Hsu, 2003; Lu & Beamish, 2004), findings are often conflicting and often vary depending on the home country of the firm (Elango & Sethi, 2007). Some scholars (e.g. Child & Rodriguez, 2005) have argued that Chinese firms operate in unusual economic, political and social conditions which affect their internationalization strategies. There are, therefore, good grounds to question the generalizability of existing models to the Chinese context. The question has taken on particular significance as China has now overtaken Germany to be the world’s largest exporter according to the latest statistics by the World Trade Organisation. 2 However, little research has been conducted on the internationalization–performance relationship of Chinese firms. One major contribution of this paper is, therefore, to test the generalizability of existing models of internationalization with a sample of Chinese firms. Despite recent efforts in extending the research to firms from emerging or newly industrialized econo- mies such as India (Contractor, Kumar, & Kundu, 2007) and Taiwan (Chiao & Li, 2009), empirical study focusing on firms from Mainland China with reliable financial data, to our best knowledge, is still rare. The lack of empirical evidence from China on implications of internationalization on firm performance may be due to the difficulty of access to reliable data, a common challenge facing studies on emerging economies such as China (Wright, Filatotchev, Hoskisson, & Peng, 2005). Secondly, al- though exports from China are now substantial, it was not that long ago that this was not the case. In 1979, the share of exports in the Chinese economy was well below the world average, even for low and middle income countries, and has only increased substantially following China’s accession to the WTO in 2001 (Naude ´& Rossouw, 2010). 3 Most previous studies on interna- tionalization performance of Chinese firms have employed perceptual measures of performance gathered from surveys (see e.g. Brouthers, O’Donnell, & Hadjimarcou, 2005). However, given the rapid development and increasing sophistication of the Chinese stock market, despite its relative newness, other studies have shown that stock market reports provide reliable informa- tion content to investors (Chen, Chen, & Su, 2001; Chen, Firth, & Gao, 2002), so we believe that using data derived from financial reports of listed companies from 2000 when companies started to provide information about their foreign sales gives a more reliable, and accurate measure of internationalization and firm performance. Journal of World Business 47 (2012) 73–80 A R T I C L E I N F O Keywords: Foreign sales Interregional sales Intraregional sales Tobin’s Q Dynamic panel model A B S T R A C T This paper examines the relationship between internationalization and performance in Chinese MNEs using panel data on 887 publicly listed Chinese firms over the nine-year period. A second aim of this paper was to test for the effects of the geographic regions where Chinese firms internationalize on their performance. The results show that the internationalization–performance relationship varies significantly depending on whether internationalization takes place within the Greater China region, within Asia or outside Asia. Internationalization within the Greater China region had the greatest benefit, the effect remaining positive and significant even after taking into account reverse causality effects. ß 2010 Elsevier Inc. All rights reserved. * Corresponding author. Tel.: +61 2 9850 8459; fax: +61 2 9850 8065. E-mail addresses: [email protected] (S. Chen), [email protected], [email protected] (H. Tan). 1 Tel.: +61 2 9685 9480. 2 See WTO Press Release: ‘Trade to expand by 9.5% in 2010 after a dismal 2009’, 26 March 2010. 3 According to the World Bank’s Investment Climate Private Enterprise Survey conducted in 2002–2003 with the participation of 3948 Chinese firms, 62% of the exporting firms start export operations within 3 years (Naude ´& Rossouw, 2010). Contents lists available at ScienceDirect Journal of World Business jo u r nal h o mep age: w ww.els evier .co m/lo c ate/jwb 1090-9516/$ – see front matter ß 2010 Elsevier Inc. All rights reserved. doi:10.1016/j.jwb.2010.10.022

-

Upload

stephen-chen -

Category

Documents

-

view

212 -

download

0

Transcript of Region effects in the internationalization–performance relationship in Chinese firms

Journal of World Business 47 (2012) 73–80

Region effects in the internationalization–performance relationshipin Chinese firms

Stephen Chen a,*, Hao Tan b,1

a Department of Business, Macquarie University, North Ryde, NSW 2109, Australiab School of Management, University of Western Sydney, Parramatta, NSW 2150, Australia

A R T I C L E I N F O

Keywords:

Foreign sales

Interregional sales

Intraregional sales

Tobin’s Q

Dynamic panel model

A B S T R A C T

This paper examines the relationship between internationalization and performance in Chinese MNEs

using panel data on 887 publicly listed Chinese firms over the nine-year period. A second aim of this

paper was to test for the effects of the geographic regions where Chinese firms internationalize on their

performance. The results show that the internationalization–performance relationship varies

significantly depending on whether internationalization takes place within the Greater China region,

within Asia or outside Asia. Internationalization within the Greater China region had the greatest benefit,

the effect remaining positive and significant even after taking into account reverse causality effects.

� 2010 Elsevier Inc. All rights reserved.

Contents lists available at ScienceDirect

Journal of World Business

jo u r nal h o mep age: w ww.els evier . co m/lo c ate / jwb

1. Introduction

The internationalization–performance relationship is a keyquestion in international business and significant research hasbeen conducted over the last 30 or so years on this question.Despite the extensive research and attempts to develop a generalmodel of the relationship between internationalization andperformance (e.g. Contractor, Kundu, & Hsu, 2003; Lu & Beamish,2004), findings are often conflicting and often vary depending onthe home country of the firm (Elango & Sethi, 2007). Some scholars(e.g. Child & Rodriguez, 2005) have argued that Chinese firmsoperate in unusual economic, political and social conditions whichaffect their internationalization strategies. There are, therefore,good grounds to question the generalizability of existing models tothe Chinese context. The question has taken on particularsignificance as China has now overtaken Germany to be theworld’s largest exporter according to the latest statistics by theWorld Trade Organisation.2 However, little research has beenconducted on the internationalization–performance relationshipof Chinese firms.

One major contribution of this paper is, therefore, to test thegeneralizability of existing models of internationalization with asample of Chinese firms. Despite recent efforts in extending theresearch to firms from emerging or newly industrialized econo-

* Corresponding author. Tel.: +61 2 9850 8459; fax: +61 2 9850 8065.

E-mail addresses: [email protected] (S. Chen),

[email protected], [email protected] (H. Tan).1 Tel.: +61 2 9685 9480.2 See WTO Press Release: ‘Trade to expand by 9.5% in 2010 after a dismal 2009’,

26 March 2010.

1090-9516/$ – see front matter � 2010 Elsevier Inc. All rights reserved.

doi:10.1016/j.jwb.2010.10.022

mies such as India (Contractor, Kumar, & Kundu, 2007) andTaiwan (Chiao & Li, 2009), empirical study focusing on firms fromMainland China with reliable financial data, to our bestknowledge, is still rare. The lack of empirical evidence fromChina on implications of internationalization on firm performancemay be due to the difficulty of access to reliable data, a commonchallenge facing studies on emerging economies such as China(Wright, Filatotchev, Hoskisson, & Peng, 2005). Secondly, al-though exports from China are now substantial, it was not thatlong ago that this was not the case. In 1979, the share of exports inthe Chinese economy was well below the world average, even forlow and middle income countries, and has only increasedsubstantially following China’s accession to the WTO in 2001(Naude & Rossouw, 2010). 3 Most previous studies on interna-tionalization performance of Chinese firms have employedperceptual measures of performance gathered from surveys(see e.g. Brouthers, O’Donnell, & Hadjimarcou, 2005). However,given the rapid development and increasing sophistication of theChinese stock market, despite its relative newness, other studieshave shown that stock market reports provide reliable informa-tion content to investors (Chen, Chen, & Su, 2001; Chen, Firth, &Gao, 2002), so we believe that using data derived from financialreports of listed companies from 2000 when companies started toprovide information about their foreign sales gives a morereliable, and accurate measure of internationalization and firmperformance.

3 According to the World Bank’s Investment Climate Private Enterprise Survey

conducted in 2002–2003 with the participation of 3948 Chinese firms, 62% of the

exporting firms start export operations within 3 years (Naude & Rossouw, 2010).

S. Chen, H. Tan / Journal of World Business 47 (2012) 73–8074

Another reason which has been suggested for the conflictingfindings in previous studies of internationalization and perform-ance is that the performance benefits vary according to the hostregion where the firm internationalizes. Rugman and colleagues(Collinson & Rugman, 2008; Oh & Rugman, 2006; Rugman, 2007;Rugman & Collinson, 2004; Rugman & Verbeke, 2004) haveextensively documented how the world’s leading MNEs havestrong regional preferences in their internationalization strategies.Other studies (e.g. Chen, 2007; Li, 2005; Qian, Li, Li, & Qian, 2008;Rugman & Oh, 2007) have shown how regional strategies mayaffect the performance benefits firms obtain from internationali-zation. In this paper, we show how internationalization in theGreater China region (comprising Taiwan, Hong Kong and Macau),which has cultural similarity and historical links to Mainland Chinahas a particularly significant effect on the performance ofinternationalizing Chinese firms.

Third, we introduce a dynamic panel model for testing theinternationalization–performance relationship. This model en-abled us identify the direction of causality in the relationship, acriticism that has been leveled at previous studies (Chen, 2007).The results confirm that internationalization does have a signifi-cant, positive effect on performance of Chinese firms.

The remainder of the paper is organized as follows. First, weprovide a review of the theoretical background and literature onthe internationalization–performance relationship. Second, wedescribe the data collection, analysis and results of the study.Third, we discuss the implications of the results, limitations of thestudy and possible future directions for research.

2. Theoretical background

2.1. The internationalization–performance relationship

The relationship between internationalization and firm per-formance has long been a topic of interest to international businessresearchers (e.g. Hymer, 1976; Rugman, 1979; Caves, 1982).Despite many years of research, there is no clear consensus aboutthe relationship between internationalization and performance.Early researchers found a positive internationalization–perform-ance relationship (Buhner, 1987; Geringer, Beamish, & Costa, 1989;Grant, 1987; Rugman, Lecraw, & Booth, 1985) but later studiesfound a negative relationship (Michel & Shaked, 1986; Collins,1990; Shaked, 1986; Kumar, 1984). Addressing these contradictoryfindings, researchers from the 1990s onwards have elaboratedboth the benefits and costs. They suggested a curvilinearrelationship (e.g. Capar and Kotabe, 2003; Geringer et al., 1989;Gomes & Ramaswamy, 1999; Hitt, Hoskisson, & Kim, 1997; Mauri& Sambharya, 2001). Reasons given for an inverted-U shapedrelationship are that geographic expansion leads to enhancedcorporate performance up to a second threshold, beyond which theorganizational costs and complexity associated with managingwidely scattered operations begin to outweigh the advantages ofeven further international expansion.

Ruigrok and Wagner (2003) have found a standard U-shaperelationship between internationalization and firm performance.Building on Johanson and Vahlne’s (1977) classic work, they haveargued that the form of the internationalization–performancerelationship is likely to be determined by organizational learningprocesses. In the course of international expansion firms encounteran increasing imbalance between external environments andinternal competencies, which leads to a decrease in performancebut firms that successfully pass through the readjustment phasethen experience a reversal of fortunes, and restore positiveperformance development.

Contractor et al. (2003) and Lu and Beamish (2004) haveindependently suggested that all these contradictory findings

might be reconciled in a new three-stage theory of internationalexpansion in which positive, negative and U-shaped relationshipscan be found at different stages. In stage 1, the relationship isnegative slope as costs and barriers to initial internationalexpansion outweigh the benefits. In stage 2, the relationshipbecomes positive as geographical expansion makes possibleefficiencies that improve resource utilization, better scanning formarket opportunities, the ability of some companies to exerciseglobal market power and to extend the product cycle. In stage 3,the relationship becomes negative again as some firms expandbeyond an optimal threshold. In this stage, having expanded intothe most lucrative markets, the firm is left with minor or peripheralcountries with a lower profit potential. Secondly, beyond theoptimum point, the growth of coordination and governance costsmay exceed the benefits of further expansion. This is especiallytrue where the firm has to deal with different legal, cultural andlinguistic environments.

2.2. Home-country and -region factors

There are also good reasons to believe that the internationaliza-tion–performance relationship may vary depending on the home-country or geographic region. For instance, unlike the cubicrelationship found in their study of US firms (Contractor et al.,2003), Contractor et al. (2007) found a U-shaped relationshipbetween internationalization and firm performance in Indian firms.They attributed this finding to the late internationalization of Indianfirms compared to firms from developed countries. It is, therefore, ofinterest to see what the relationship is in Chinese firms.

Many researchers have identified significant differences betweenfirms in developed and less-developed countries, which might affecttheir internationalization strategies and the performance benefitsthey obtain. First, LDCs typically have lower labor costs, less efficientproduction and less internationally competitive knowledge-baseindustries (Amsden & Hikino, 1994; Guillen, 2000; Leff, 1978, 1979).Second, less-developed countries often suffer from weak or non-existent institutions (Khanna & Palepu, 2000a, 2000b; Khanna &Rivkin, 2001). Third, LDCs are generally less economically andpolitically stable compared with developed countries. Internation-alization has an added value in high-risk economies by enablingfirms to alleviate these factors and spread market risk (Rugman,1979). Fourth, the home markets for developing country firms maybe too small to provide significant scale advantages. The ability toreap the benefits of scale is vital when competing on the basis of lowcost, which is often the case of developing country firms.

Studies of earlier internationalization by firms from East Asiasuch as Taiwan, South Korea and Singapore suggest the possibilitythat some firms develop international links in order to seek assetsbecause they are entering international business to address arelative disadvantage rather than exploit a competitive advantage(Mathews, 2002). Firms in these countries had to ‘catch up’ withdeveloped country firms in terms of technology and know-how,and so internationalized in order to catch up with foreign rivals.Luo and Tung (2007) have argued that emerging market MNEs inother countries use international expansion as a springboard toacquire critical resources needed to compete more effectivelyagainst their competitors at home and abroad, and to overcomeinstitutional and market constraints in the domestic market. Theinternationalization of Chinese firms seems to be following asimilar pattern (Tseng, 1994; Cui, 1998; Warner, Ng, & Xu, 2004;Yang, Lim, Sakurai, & Seo, 2009). For instance, Boisot and Meyer(2008) have argued that, in contrast to the assumptions ofconventional international business theory, many Chinese firmsinternationalize in order to avoid a number of competitivedisadvantages incurred by operating exclusively in the domesticmarket.

Table 1Distribution of firms in sample by primary industry sector.

Industry Frequency

1. Agriculture 9

2. Natural resources 54

3. Manufacturing 174

4. Distribution and transport 504

5. Retail 31

6. Business Services 108

7. Utilities 7

Total 887

4 Results of the tests using ROA are available from the authors upon request.

S. Chen, H. Tan / Journal of World Business 47 (2012) 73–80 75

These arguments suggest that Chinese firms gain a competitiveadvantage from internationalizing both as a result of resourceacquisition, and from overcoming domestic constraints so wehypothesize that:

Hypothesis 1. In general the performance of Chinese firms shouldvary positively with the degree of internationalization.

2.3. Host-country and -region factors

There are also good reasons to believe that the nature of theinternationalization–performance relationship may also vary withthe host markets that the firm enters (Pangarkar, 2008). As shownby Rugman (2000), even among the world’s most internationalizedcompanies, most still derive the bulk of their sales in the homeregion. By definition, home regional markets are geographicallycloser. This reduces transportation costs. As they are in the sametime zone, it is also easier to coordinate activities. Markets in thesame region are also likely to be part of the same trade blocs and sobenefit from reduced market entry barriers.

Institutional theorists also point to significant differencesbetween business systems internationally that may affect thecompetitive advantage of firms in particular markets (Griffiths &Zammuto, 2005). For example, there are many differences in theinstitutional systems, such as differences in legal and politicalinstitutions (Whitley, 1999), which increase the costs of businesstransactions in other business systems. Since business systems canto a large extent be divided regionally, this too would tend to favora focus on the home region. An initial study by Fortanier and vanTulder (2009) of some leading Chinese firms found that they tooexhibit this preference to internationalize into the home region.These arguments and findings would suggest that:

Hypothesis 2. Internationalization by Chinese firms within Asiashould lead to greater performance compared with internationali-zation outside the region.

In addition to the economic and institutional factors above, akey factor which has been examined in the internationalizationliterature is psychic distance. The Uppsala model of international-ization (Johanson & Vahlne, 1977) proposed that firms interna-tionalize incrementally from ‘‘psychically close’’ countries to‘‘psychically distant’’ countries. This would predict a pattern ofinternationalization in which one would find internationalizationin familiar countries in the first stage, and internationalization inless familiar countries in the latter stages of the three-stage model.China’s distinctive cultural and institutional legacy, including thetendency to rely on close personal relationships in businesstransactions (Chen & Chen, 2004), may be expected to increase theimportance of psychic distance faced by its firms as they seek tointernationalize. Boisot and Child (1996) have argued that theChinese have a cultural preference for transacting in less codifiedregimes typified by fiefs, and clan networks rather than by thecodified formality and impersonality of bureaucracies or markets.Previous research on overseas Chinese firms (Sim & Pandian, 2003)has shown the preference to rely ethnically based social networks,a feature of Mainland Chinese firms. Earlier studies have shownhow Mainland Chinese firms showed a preference to go tocountries where Chinese social networks are present (Cai, 1999;Deng, 2004). Other studies have shown that such transnationalsocial networks have a performance benefit (Zhou, Wu, & Luo,2007). Therefore, we hypothesize:

Hypothesis 3. Internationalization of Chinese firms within theGreater China region should lead to greater performance comparedwith internationalization outside the region.

3. Methods

3.1. Sample and data collection

The hypotheses were tested with a sample of publicly listedChinese companies drawn from the database provided by WIND, aleading financial data vendor in China. This database providesdetails of all publicly listed companies in China so we are confidentthat we have a complete sample of Chinese firms for whichfinancial data is available from public sources. Data on interna-tional operations (foreign sales, foreign assets, etc) was obtainedfor each company since 2000 when sales from geographicsegments were first reported. The final sample of firms that hadgeographic segment data amounted to 887 firms listed in Shanghaiand Shenzhen, the only two stock exchanges in the Mainland Chinawith a total of 4129 firm-year observations. Table 1 shows thecharacteristics of firms in the sample. (It should be noted that thenumber of firms in each regression may vary as the firms in thesample varied in the amount of geographic segment informationdisclosed. Some firms only provided figures of total foreign sales,others provided a more detailed breakdown by geographic regionwhile others provided detailed breakdown by country).

3.2. Variables and measures

3.2.1. Dependent variable

Performance was measured by Tobin’s Q, calculated as follows:Tobin’s Q = (equity market value + liabilities book value)/(equitybook value + liabilities book value). Tobin’s Q has been usedextensively to measure performance of firms from severalcountries, including USA, India and Japan(see e.g. Khanna &Palepu, 2000a, 2000b; Lu & Beamish, 2004; McGahan, 1999;Wernerfelt & Montgomery, 1988). It has previously been employedas a performance measure in the context of Chinese listed firms byMa, Yao, & Xi (2006). The advantage of using Tobin’s Q over otheraccounting-based performance measures, such as ROA and ROS, isthat it includes a market-based measure of expected futureearnings as well as current earnings (Christophe & Lee, 2005). Forfirms in a fast developing market such as China, this may well be aparticularly important motivation for internationalization. Maet al. (2006) further remark that financial indicators such as ROA orROE are more likely to be manipulated by listed companies inChina, which makes Tobin’s Q a favorable measure for performanceof publicly listed firms. (Nevertheless, as a precaution, we did alsotest the models using ROA. These generated similar results,although with a lower model fit. This analysis has not beenincluded in this paper.4)

3.2.2. Independent variables

Degree of internationalization (DOI) was measured using threemeasures:

Table 2Descriptive statistics.

Variable Description Observations Mean Std. Dev.

Tobin’s Q Dependent variable for firm performance 4121 1.93 1.62

FSTS (%) Percentage of total sales from foreign sales 4129 26.04 25.79

ISTS (%) Percentage of total sales from within Asia excluding China 472 21.56 21.60

IGC (%) Percentage of total sales from the Greater China region (comprising Hong Kong, Macau and Taiwan) 234 12.21 16.94

SIZE Natural logarithm of total firm assets 4121 21.30 1.27

AGE Number of years since incorporation of the company 4128 12.60 4.76

INTANGIBLE Ratio of total intangible assets to total assets 4121 0.034 0.041

S. Chen, H. Tan / Journal of World Business 47 (2012) 73–8076

� Total Foreign Sales as a percentage of Total Sales (FSTS).� Intraregional sales/total sales (ISTS) calculated as the percentage

of total sales arising from within Asia.� Intragreater China sales/total sales (IGC), calculated as the

percentage of total sales from the Greater China region(comprising Hong Kong, Macau and Taiwan).

As Contractor et al. (2003, p.12) remark, ‘‘there is no standardapproach for measuring the degree of multinationality’’ inthe internationalization–performance literature. Frequentlyemployed measures include the ratios of foreign to total sales,or the ratios of foreign to total assets which involves foreign directinvestment (FDI), or ratio of overseas employees to totalemployees, or number of plants/offices in foreign locations(Contractor et al., 2003). In the current study, we focus on foreignsales or exports, as an indicator of internationalization for threemain reasons. First, compared with the amount of foreign salesmade by Chinese companies, the amount of the outward FDI fromChina is still relatively low (less than 4% of the value of exports).5

Second, due to the lack of resources and experience, firms fromemerging markets such as China usually rely on direct exportingas the first and primary channel, to expose to the internationalmarket (Brouthers et al., 2005; Chiao & Li, 2009). Third, manyprevious studies of the internationalization–performance rela-tionship of firms from different countries e.g. the US (Contractoret al., 2003), Japan (Lu & Beamish, 2004), India (Elango & Pattnaik,2007), Taiwan (Chiao & Li, 2009) and China (Jeong, 2003), haveused the foreign sales/total sales ratio as a measure ofinternationalization. We likewise measure the degree of interna-tionalization within Asia, and the degree of internationalizationwithin the Greater China region by the percentage of sales withinthat region. This provides the most direct measure of the salescontribution of that region to performance and is consistent withprevious studies, which have examined the effect of internation-alization within regions on firm performance (Chen, 2007; Li,2005; Rugman & Oh, 2007).

3.2.3. Control variables

Previous studies identify a number of factors that may haveimpacts on firm performance, apart from the degree of interna-tionalization of firms. Therefore, we included a set of controlvariables in our models.

SIZE and AGE: Firm size and age are widely regarded as twofactors that moderate the relationship between internationaliza-tion, and firm performance (see e.g. Bausch & Krist, 2007; Chiao &Li, 2009; Contractor et al., 2007). Those two factors have also beenincluded as control variables in studies examining performance ofChinese listed firms (e.g. Chen, 2001). In our current study, firmsize (SIZE) was measured by the natural logarithm of total firmassets, and was used to control for the potential effect of scale

5 According to the data from the Ministry of Commerce, P.R.C. (http://

www.mofcom.gov.cn/tongjiziliao/tongjiziliao.html) (in Chinese), in 2008 the total

value of exports from China reached USD 1428 billion; while in the same year FDI

from China amounted to USD 56 billion, less than 4% of the value of the exports.

economy differences. Logarithmic transformation not only makesthe results easy to interpret, because the changes in the logarithmdomain represent relative (percentage) changes in the originalmetric and also, makes the distribution of data closer to normality.Firm age (AGE) is measured by the number of years sinceincorporation of the company.

INTANGIBLE: To reflect the competitive advantage of a firmderived from its resources and capabilities, some previous studieshave taken into account the impact of intangible assets possessedby a firm with measures such as R&D intensity, or advertisingintensity (Bausch & Krist, 2007; Chiao & Li, 2009; Lu & Beamish,2004). In the current study, we utilize the ratio of total intangibleassets to total assets (INTANGIBLE) as reported by the listed firms,as a control variable.

INDUSTRY: Firm performance may be significantly influencedby industry-specific factors (McGahan & Porter, 1999). Consistentwith similar studies (e.g. Contractor et al., 2007; Chiao & Li, 2009),we introduce an industry type dummy variable (INDUSTRY) basedon the one-digit classification code specified by the ChinaSecurities Regulatory Commission for firms listed in stockexchanges in Mainland China.

3.3. Descriptive statistics

Table 2 shows the means and standard deviations of variableswhile Table 3 shows the correlations between variables. Anexamination of Table 3 indicates no multicollinearity problemsbetween the independent variables in each model tested. This isconfirmed by the variance inflation factors (all well below thenormal cutoff figure of 10) and tolerance figures (all well above 0),shown in Table 4.

4. Analysis

Following similar studies of internationalization and perform-ance (Lu & Beamish, 2004; Contractor et al., 2003), the data wasanalyzed using a cross-sectional time series model, which makes itpossible to reveal individual explanatory variables as well as thedynamics over time. Following the advice of Beck and Katz (1995),as the number of time periods in our sample was relatively small(the mean was 5 years) compared with the number of companies(887), instead of using feasible generalized least-squares regres-sion (FGLS) as did the previously cited researchers, OLS regressionwith panel-corrected standard errors was used, implementedusing the xtpcse command in Stata. Unlike FGLS, disturbances areassumed to be heteroskedastic and contemporaneously correlatedacross panels (Stata, 2003). We tested the effect of internationali-zation using each of the three measures FSTS, ISTS and IGC in linear,quadratic and cubic models, as follows. Panel-specific autocorre-lation of the first order (AR1) was assumed in all modelstested.Model 1 (Linear):

Per formanceit ¼ a þ b1ðSIZEitÞ þ b2ðAGEitÞ þ b3ðINTANGIBLEitÞ

þ b4ðDOIitÞ þX

b4þmIm þ b4þmaxðmÞþ1C1 þ þeit

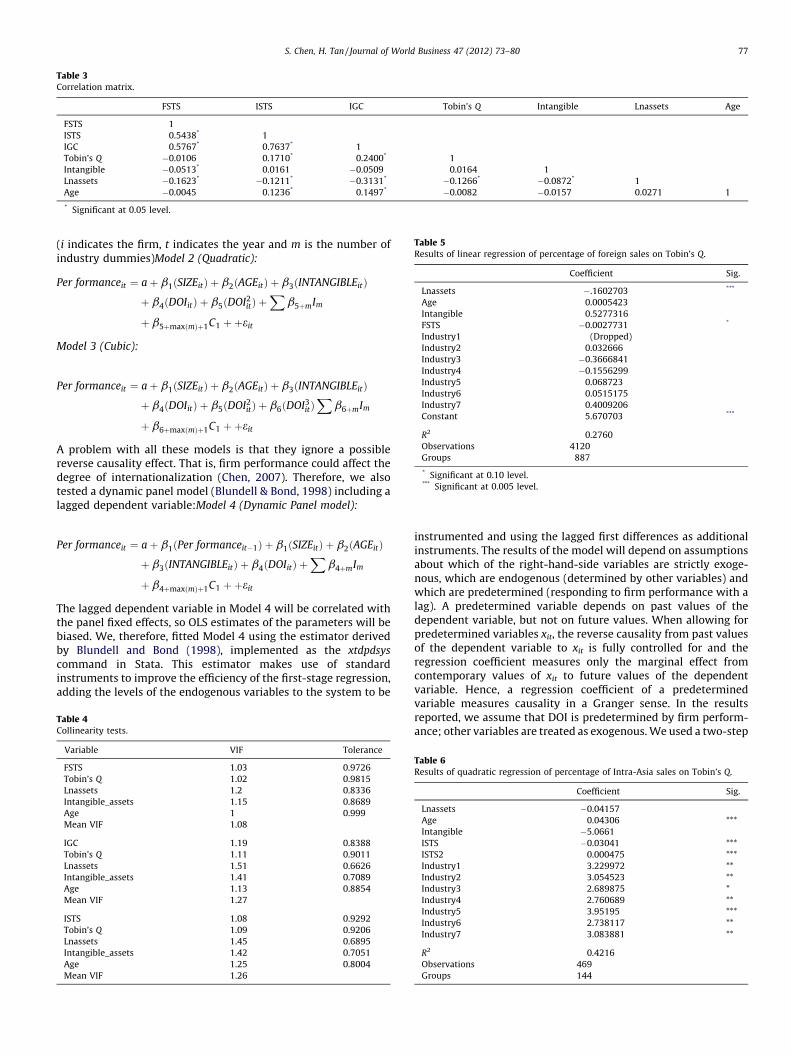

Table 5Results of linear regression of percentage of foreign sales on Tobin’s Q.

Coefficient Sig.

Lnassets �.1602703 ***

Age 0.0005423

Intangible 0.5277316

FSTS �0.0027731 *

Industry1 (Dropped)

Industry2 0.032666

Industry3 �0.3666841

Industry4 �0.1556299

Industry5 0.068723

Industry6 0.0515175

Industry7 0.4009206

Constant 5.670703 ***

R2 0.2760

Observations 4120

Groups 887

* Significant at 0.10 level.*** Significant at 0.005 level.

Table 3Correlation matrix.

FSTS ISTS IGC Tobin’s Q Intangible Lnassets Age

FSTS 1

ISTS 0.5438* 1

IGC 0.5767* 0.7637* 1

Tobin’s Q �0.0106 0.1710* 0.2400* 1

Intangible �0.0513* 0.0161 �0.0509 0.0164 1

Lnassets �0.1623* �0.1211* �0.3131* �0.1266* �0.0872* 1

Age �0.0045 0.1236* 0.1497* �0.0082 �0.0157 0.0271 1

* Significant at 0.05 level.

S. Chen, H. Tan / Journal of World Business 47 (2012) 73–80 77

(i indicates the firm, t indicates the year and m is the number ofindustry dummies)Model 2 (Quadratic):

Per formanceit ¼ a þ b1ðSIZEitÞ þ b2ðAGEitÞ þ b3ðINTANGIBLEitÞ

þ b4ðDOIitÞ þ b5ðDOI2itÞ þ

Xb5þmIm

þ b5þmaxðmÞþ1C1 þ þeit

Model 3 (Cubic):

Per formanceit ¼ a þ b1ðSIZEitÞ þ b2ðAGEitÞ þ b3ðINTANGIBLEitÞ

þ b4ðDOIitÞ þ b5ðDOI2itÞ þ b6ðDOI3

itÞX

b6þmIm

þ b6þmaxðmÞþ1C1 þ þeit

A problem with all these models is that they ignore a possiblereverse causality effect. That is, firm performance could affect thedegree of internationalization (Chen, 2007). Therefore, we alsotested a dynamic panel model (Blundell & Bond, 1998) including alagged dependent variable:Model 4 (Dynamic Panel model):

Per formanceit ¼ a þ b1ðPer formanceit�1Þ þ b1ðSIZEitÞ þ b2ðAGEitÞ

þ b3ðINTANGIBLEitÞ þ b4ðDOIitÞ þX

b4þmIm

þ b4þmaxðmÞþ1C1 þ þeit

The lagged dependent variable in Model 4 will be correlated withthe panel fixed effects, so OLS estimates of the parameters will bebiased. We, therefore, fitted Model 4 using the estimator derivedby Blundell and Bond (1998), implemented as the xtdpdsys

command in Stata. This estimator makes use of standardinstruments to improve the efficiency of the first-stage regression,adding the levels of the endogenous variables to the system to be

Table 4Collinearity tests.

Variable VIF Tolerance

FSTS 1.03 0.9726

Tobin’s Q 1.02 0.9815

Lnassets 1.2 0.8336

Intangible_assets 1.15 0.8689

Age 1 0.999

Mean VIF 1.08

IGC 1.19 0.8388

Tobin’s Q 1.11 0.9011

Lnassets 1.51 0.6626

Intangible_assets 1.41 0.7089

Age 1.13 0.8854

Mean VIF 1.27

ISTS 1.08 0.9292

Tobin’s Q 1.09 0.9206

Lnassets 1.45 0.6895

Intangible_assets 1.42 0.7051

Age 1.25 0.8004

Mean VIF 1.26

instrumented and using the lagged first differences as additionalinstruments. The results of the model will depend on assumptionsabout which of the right-hand-side variables are strictly exoge-nous, which are endogenous (determined by other variables) andwhich are predetermined (responding to firm performance with alag). A predetermined variable depends on past values of thedependent variable, but not on future values. When allowing forpredetermined variables xit, the reverse causality from past valuesof the dependent variable to xit is fully controlled for and theregression coefficient measures only the marginal effect fromcontemporary values of xit to future values of the dependentvariable. Hence, a regression coefficient of a predeterminedvariable measures causality in a Granger sense. In the resultsreported, we assume that DOI is predetermined by firm perform-ance; other variables are treated as exogenous. We used a two-step

Table 6Results of quadratic regression of percentage of Intra-Asia sales on Tobin’s Q.

Coefficient Sig.

Lnassets �0.04157

Age 0.04306 ***

Intangible �5.0661

ISTS �0.03041 ***

ISTS2 0.000475 ***

Industry1 3.229972 **

Industry2 3.054523 **

Industry3 2.689875 *

Industry4 2.760689 **

Industry5 3.95195 ***

Industry6 2.738117 **

Industry7 3.083881 **

R2 0.4216

Observations 469

Groups 144

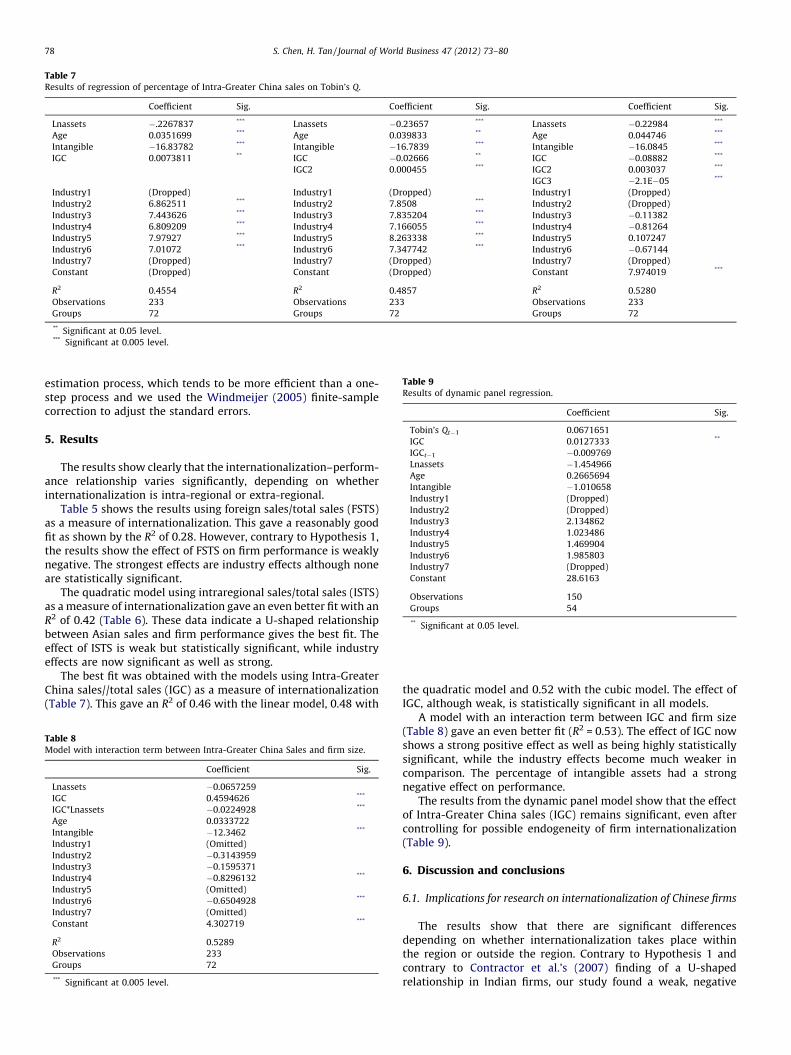

Table 7Results of regression of percentage of Intra-Greater China sales on Tobin’s Q.

Coefficient Sig. Coefficient Sig. Coefficient Sig.

Lnassets �.2267837 *** Lnassets �0.23657 *** Lnassets �0.22984 ***

Age 0.0351699 *** Age 0.039833 ** Age 0.044746 ***

Intangible �16.83782 *** Intangible �16.7839 *** Intangible �16.0845 ***

IGC 0.0073811 ** IGC �0.02666 ** IGC �0.08882 ***

IGC2 0.000455 *** IGC2 0.003037 ***

IGC3 �2.1E�05 ***

Industry1 (Dropped) Industry1 (Dropped) Industry1 (Dropped)

Industry2 6.862511 *** Industry2 7.8508 *** Industry2 (Dropped)

Industry3 7.443626 *** Industry3 7.835204 *** Industry3 �0.11382

Industry4 6.809209 *** Industry4 7.166055 *** Industry4 �0.81264

Industry5 7.97927 *** Industry5 8.263338 *** Industry5 0.107247

Industry6 7.01072 *** Industry6 7.347742 *** Industry6 �0.67144

Industry7 (Dropped) Industry7 (Dropped) Industry7 (Dropped)

Constant (Dropped) Constant (Dropped) Constant 7.974019 ***

R2 0.4554 R2 0.4857 R2 0.5280

Observations 233 Observations 233 Observations 233

Groups 72 Groups 72 Groups 72

** Significant at 0.05 level.*** Significant at 0.005 level.

Table 9Results of dynamic panel regression.

Coefficient Sig.

Tobin’s Qt�1 0.0671651

IGC 0.0127333 **

IGCt�1 �0.009769

Lnassets �1.454966

Age 0.2665694

Intangible �1.010658

Industry1 (Dropped)

Industry2 (Dropped)

Industry3 2.134862

Industry4 1.023486

Industry5 1.469904

Industry6 1.985803

Industry7 (Dropped)

Constant 28.6163

Observations 150

Groups 54

** Significant at 0.05 level.

S. Chen, H. Tan / Journal of World Business 47 (2012) 73–8078

estimation process, which tends to be more efficient than a one-step process and we used the Windmeijer (2005) finite-samplecorrection to adjust the standard errors.

5. Results

The results show clearly that the internationalization–perform-ance relationship varies significantly, depending on whetherinternationalization is intra-regional or extra-regional.

Table 5 shows the results using foreign sales/total sales (FSTS)as a measure of internationalization. This gave a reasonably goodfit as shown by the R2 of 0.28. However, contrary to Hypothesis 1,the results show the effect of FSTS on firm performance is weaklynegative. The strongest effects are industry effects although noneare statistically significant.

The quadratic model using intraregional sales/total sales (ISTS)as a measure of internationalization gave an even better fit with anR2 of 0.42 (Table 6). These data indicate a U-shaped relationshipbetween Asian sales and firm performance gives the best fit. Theeffect of ISTS is weak but statistically significant, while industryeffects are now significant as well as strong.

The best fit was obtained with the models using Intra-GreaterChina sales//total sales (IGC) as a measure of internationalization(Table 7). This gave an R2 of 0.46 with the linear model, 0.48 with

Table 8Model with interaction term between Intra-Greater China Sales and firm size.

Coefficient Sig.

Lnassets �0.0657259

IGC 0.4594626 ***

IGC*Lnassets �0.0224928 ***

Age 0.0333722

Intangible �12.3462 ***

Industry1 (Omitted)

Industry2 �0.3143959

Industry3 �0.1595371

Industry4 �0.8296132 ***

Industry5 (Omitted)

Industry6 �0.6504928 ***

Industry7 (Omitted)

Constant 4.302719 ***

R2 0.5289

Observations 233

Groups 72

*** Significant at 0.005 level.

the quadratic model and 0.52 with the cubic model. The effect ofIGC, although weak, is statistically significant in all models.

A model with an interaction term between IGC and firm size(Table 8) gave an even better fit (R2 = 0.53). The effect of IGC nowshows a strong positive effect as well as being highly statisticallysignificant, while the industry effects become much weaker incomparison. The percentage of intangible assets had a strongnegative effect on performance.

The results from the dynamic panel model show that the effectof Intra-Greater China sales (IGC) remains significant, even aftercontrolling for possible endogeneity of firm internationalization(Table 9).

6. Discussion and conclusions

6.1. Implications for research on internationalization of Chinese firms

The results show that there are significant differencesdepending on whether internationalization takes place withinthe region or outside the region. Contrary to Hypothesis 1 andcontrary to Contractor et al.’s (2007) finding of a U-shapedrelationship in Indian firms, our study found a weak, negative

S. Chen, H. Tan / Journal of World Business 47 (2012) 73–80 79

relationship between internationalization and performance inChinese firms. However, in accordance with Hypotheses 2 and 3, anexcellent fit was obtained with models where only Intra-Asia andIntra-Greater China sales were considered. The best fit wasobtained with a cubic model and Intra-Greater China sales. Thisconfirms the validity of the three-stage model of internationaliza-tion for Chinese firms but shows that in the case of Chinese firms, itis foreign sales within the Greater China region that is mostsignificant.

Our findings have a number of implications for research oninternationalization of Chinese firms and more generally, researchon the relationship between internationalization and firm perform-ance. First, the results show that it is not just foreign sales that matterbut more importantly, where foreign sales are generated. This isconsistent with the arguments made in other studies, which haveargued for the importance of considering host country/region effectsin internationalization strategies (Chen, 2007; Li, 2005; Rugman &Oh, 2007). Second, the fact that the nature of the relationshipbetween internationalization and performance we found in Chinesefirms differs from the relationship found by Contractor et al. (2007)in their study of Indian firms, suggests that it is also necessary toconsider home-country specific factors in such studies. Third, theresults highlight how a region is defined in internationalizationstudies can make a significant difference to the results, a point whichhas also been made by other researchers (Asmussen, 2009;Osegowitsch & Sammartino, 2008). In this case, it appears that forChinese firms the ‘‘home region’’ is best defined as Greater China.This is consistent with the many studies, which have highlighted theimportance of psychic or cultural distance in internationalization offirms (Johanson & Vahlne, 1977).

Furthermore, the results with the dynamic panel model confirmthe positive impact of internationalization within the GreaterChina region on performance of Chinese firms, even after takingaccount a possible reverse causality effect in which past firmperformance affects firm internationalization. We can, therefore,exclude a common criticism leveled at past studies of internation-alization and performance that they only measured a correlation,but not temporal links between the two. We recommend the use ofthis method in testing for reverse causality in future studies.

The finding of no significant effect of sales within Asia, althougha significant effect of sales within Greater China in the dynamicpanel model is puzzling, but it suggests an ordering of countrieswith respect to their effect on firm performance. Internationaliza-tion into countries having a close cultural and historical link havethe greatest positive effect on firm performance, which decreasesand may even become negative with internationalization intocountries into more culturally distant countries. This is consistentwith the findings of Rugman and others (Oh & Rugman, 2006;Rugman, 2007; Rugman & Collinson, 2004; Rugman & Verbeke,2004; Qian et al., 2008), which have found a strong preference forthe home region in internationalization of MNEs from othercountries but shows that, in the case of Chinese firms, thepreference may be even stronger for certain countries or a sub-region within the home geographic region. It is also consistent withmacro-level data on outwards FDI from China (Cheng & Ma, 2010;Buckley et al., 2007; Morck, Yeung, & Zhao, 2008), which suggeststhat cultural proximity may be a significant factor in the selectionof some host countries.

6.2. Managerial relevance

First and most importantly, our study shows that there aresignificant differences in the internationalization–performancerelationship in Chinese firms depending on whether internationali-zation takes place within the region or outside the region. Linear,quadratic and cubic relationships can be found depending on where

internationalization takes place or is measured. The results confirmthe importance of considering how the region is defined by Chinesefirms in framing their internationalization strategy. Rather thannarrowly defining a firm’s home region according to the geographiccontinent where it is located, it may be more useful to considerdifferent regions depending on the context of the internationaliza-tion. In the case of Chinese firms we have shown that the GreaterChina region appears to be the most significant for firm performance.We speculate that this may be due to cultural factors.

Second, we have shown that, through our use of the dynamicpanel method in testing for reverse causality, the performancebenefits of internationalization persist even after controlling for apossible reverse causal effect of firm performance on internation-alization. We trust this finding is encouraging for Chinese firms topursue a more active internationalization strategy in order toimprove their financial performance.

6.3. Limitations and directions for future research

Clearly this study has limitations and there are severalopportunities for further research. First, the sample may be biasedas we were only able to include firms, which provided the requiredfinancial data. Results may be different for non-publicly listedfirms that were excluded, because they did not provide thenecessary data. Second, as noted previously, the Chinese economyhas undergone significant changes in the last ten years, a processwhich is still continuing, so the findings may change as Chinesefirms develop new competitive strategies. Third, although we didfind a statistically significant effect of internationalization on firmperformance in our models, the effect appears to vary with firmsize and the effect of intangible assets was much stronger. Thissuggests that future researchers may wish to restrict samples to aparticular range of firm size or intangible asset percentage in ordermore clearly distinguish effects of internationalization on per-formance. Lastly, while the findings strongly suggest thatinternationalization within Greater China does have a significantimpact on firm performance, we do not have data on what actuallymotivated these firms to internationalize in the first place, andwhat factors contributed to their choice of location.

It is outside the scope of this study, but our findings also raise aquestion about which country factors are most significant indetermining performance benefits from internationalization –cultural distance, institutional distance or geographic distance –and when. In the case of FDI, a significant factor appears to be taxadvantages (Morck et al., 2008) but in the case of exporting,cultural and linguistic similarity may be more important. Furtherresearch might attempt to answer those questions.

References

Amsden, A., & Hikino, T. (1994). Project execution capability, organisational know-howand conglomerate corporate growth in late industrialization. Industrial and Corpo-rate Change, 3: 111–147.

Asmussen, C. G. (2009). Local, regional, or global? Quantifying MNE geographic scope.Journal of International Business Studies, 40: 1192–1205.

Bausch, A, & Krist, M. (2007). The effect of context-related moderators on the interna-tionalization–performance relationship: Evidence from meta-analysis. Manage-ment International Review, 47(3): 319–347.

Beck, N., & Katz, J. N. (1995). What to do (and not to do) with time-series cross-sectiondata. American Political Science Review, 89: 634–647.

Blundell, R., & Bond, S. (1998). Initial conditions and moment restrictions in dynamicpanel data models. Journal of Econometrics, 87(1): 115–143.

Boisot, M., & Child, J. (1996). From fiefs to clans and network capitalism: ExplainingChina’s emerging economic order. Administrative Science Quarterly, 41: 600–628.

Boisot, M., & Meyer, M. N. (2008). Which way through the open door? Reflections onthe internationalization of Chinese firms. Management and Organization Review,4(3): 349–365.

Brouthers, L. E., O’Donnell, E., & Hadjimarcou, J. (2005). Generic product strategies foremerging market exports into Triad nation markets: A mimetic isomorphismapproach. Journal of Management Studies, 42(1): 225–245.

S. Chen, H. Tan / Journal of World Business 47 (2012) 73–8080

Buckley, P. J., Clegg, L. J., Cross, A. R., Liu, X., Voss, H., & Zheng, P. (2007). Thedeterminants of Chinese outward foreign direct investment. Journal of InternationalBusiness Studies, 38: 499–518.

Buhner, R. (1987). Assessing international diversification of West German corpora-tions. Strategic Management Journal, 8: 25–37.

Cai, K. G. (1999). Outward foreign direct investment: A novel dimension of China’sintegration into the regional and global economy. China Quarterly, 160: 856–880.

Caves, R. E. (1982). Multinational Enterprise and Economic Analysis. Cambridge, UK:Cambridge University Press.

Chen, C. J. P., Chen, S., & Su, X. (2001). Is accounting information value-relevant in theemerging Chinese stock market? Journal of International Accounting, Auditing &Taxation, 10: 1–22.

Chen, G., Firth, M., & Gao, N. (2002). The information content of concurrently an-nounced earnings, cash dividends, and stock dividends: An investigation of theChinese stock market. Journal of International Financial Management and Account-ing, 13(2): 101–112.

Chen, J. (2001). Ownership structure as corporate governance mechanism: Evidencefrom Chinese listed companies. Economics of Planning, 34: 53–72.

Chen, S. (2007). Testing the internationalization–performance relationship in Asianservice firms. In A. Rugman (Ed.), Research on Global Strategic Management: RegionalAspects of Multinationality and Performance (pp. 337–358). Amsterdam: Elsevier.

Chen, X.-P., & Chen, C. C. (2004). On the intricacies of the Chinese guanxi: A processmodel of guanxi development. Asia Pacific Journal of Management, 21: 305–324.

Cheng, L. K., & Ma, Z. (2010). China’s outward foreign direct investment. In R. C. FeenstraS.-J. Wei (Eds.), China’s Growing Role in World Trade. Chicago: The University ofChicago Press. pp. 545–578.

Chiao, Y.-C., & Li, P.-Y. (2009). Are more exports better for a firm’s performance? Themoderating effect of FDI. European Journal of International Management, 3(3): 286–301.

Child, J., & Rodriguez, S. (2005). The internationalization of Chinese firms: A case fortheoretical extension? Management and Organization Review, 1(3): 381–410.

Christophe, S. E., & Lee, H. (2005). What matters about internationalization: A market-based assessment. Journal of Business Research, 58(5): 636–643.

Collins, J. M. (1990). A market performance comparison of U.S. firms active in domestic,developed and developing countries. Journal of International Business Studies, 21:271–287.

Collinson, S., & Rugman, A. M. (2008). The regional nature of Japanese multinationalbusiness. Journal of International Business Studies, 39: 215–230.

Contractor, F. J., Kumar, V., & Kundu, S. K. (2007). Nature of the relationship betweeninternational expansion and performance: The case of emerging market firms.Journal of World Business, 42: 401–417.

Contractor, F. J., Kundu, S. K., & Hsu, C. C. (2003). A three-stage theory of expansion ofinternational expansion: The link between multinationality and performance inthe service sector. Journal of International Business Studies, 34(1): 5–18.

Cui, G. (1998). The evolutionary process of global market expansion: Experiences ofMNCs in China. Journal of World Business, 33(1): 87–110.

Deng, P. (2004). Outward investment by Chinese MNCs: Motivations and implications.Business Horizons, 47: 8–16.

Elango, B., & Pattnaik, C. (2007). Building capabilities for international operationsthrough networks: A study of Indian firms. Journal of International Business Studies,38(4): 541–555.

Elango, B., & Sethi, S. P. (2007). An exploration of the relationship between country oforigin (COE) and the internationalization–performance paradigm. ManagementInternational Review, 47: 369–392.

Fortanier, F., & van Tulder, R. (2009). Internationalization trajectories—A cross-countrycomparison: Are large Chinese and Indian companies different? Industrial andCorporate Change, 18(2): 223–247.

Geringer, J. M., Beamish, P. W., & Costa, R. C. (1989). Diversification strategy andinternationalization: Implications for MNE performance. Strategic ManagementJournal, 10: 109–119.

Gomes, L., & Ramaswamy, K. (1999). An empirical examination of the form of therelationship between internationalization and performance. Journal of Internation-al Business Studies, 30: 173–188.

Grant, R. M. (1987). Internationalization and performance among British manufactur-ing companies. Journal of International Business Studies, 18: 79–89.

Griffiths, A., & Zammuto, R. F. (2005). Institutional governance systems and variationsin national competitive advantage: An integrative framework. Academy of Man-agement Review, 30(4): 823–842.

Guillen, M. F. (2000). Business groups in emerging economies: A resource-based view.Academy of Management Journal, 43(3): 362–380.

Hitt, M. A., Hoskisson, R. E., & Kim, H. (1997). International diversification: Effects oninnovation and firm performance in product diversified firms. Academy of Man-agement Journal, 40: 767–798.

Hymer, S. H. (1976). A Study of Direct Foreign Investment. Cambridge, MA: MIT Press.Jeong, I. (2003). A cross-national study of the relationship between international

diversification and new product performance. International Marketing Review,20(4): 353–376.

Johanson, J., & Vahlne, J. (1977). The internationalization process of the firm: A model ofknowledge development and increasing foreign commitments. Journal of Interna-tional Business Studies, 8: 23–32.

Khanna, T., & Palepu, K. (2000a). The future of business groups in emerging markets:Long-run evidence from Chile. Academy of Management Journal, 43(3): 268–285.

Khanna, T., & Palepu, K. (2000b). Is group affiliation profitable in emerging markets? Ananalysis of diversified Indian business groups. Journal of Finance, 55: 867–891.

Khanna, T., & Rivkin, J. W. (2001). Estimating the performance effects of businessgroups in emerging markets. Strategic Management Journal, 22(1): 45–74.

Kumar, M. S. (1984). Growth Acquisition and Investment: An Analysis of the Growth ofIndustrial Firms and their Overseas Activities. Cambridge, UK: Cambridge UniversityPress.

Leff, H. N. (1978). Industrial organisation and entrepreneurship in the developingcountries: The economic groups. Economic Development and Cultural Change, 4:661–675.

Leff, H. N. (1979). Entrepreneurship and economic development: The problem revis-ited. Journal of Economic Literature, 17(March): 46–64.

Li, L. (2005). Is regional strategy more effective than global strategy in the US serviceindustries? Management International Review, 37–57 (Special Issue 2005/1).

Lu, J. E., & Beamish, P. W. (2004). International diversification and firm performance:The S-curve hypothesis. Academy of Management Journal, 47(4): 598–609.

Luo, Y., & Tung, R. (2007). International expansion of emerging market enterprises: Aspringboard perspective. Journal of International Business Studies, 38: 481–498.

Ma, X., Yao, X., & Xi, Y. (2006). Business group affiliation and firm performance in atransition economy: A focus on ownership voids. Asia Pacific Journal of Manage-ment, 23: 467–483.

Mathews, J. A. (2002). Competitive advantages of the latecomer firm: A resource-basedaccount of industrial catch-up strategies. Asia Pacific Journal of Management, 19:467–488.

Mauri, A., & Sambharya, R. (2001). The impact of global integration on MNC perform-ance: Evidence from global industries. Management International Review, 10: 441–454.

McGahan, A. M. (1999). The performance of US corporations: 1981–1994. Journal ofIndustrial Economics, 47(4): 373–398.

McGahan, A. M., & Porter, M. E. (1999). How much industry matter, really. StrategicManagement Journal, 18: 15–30 (Summer Special Issue).

Michel, A., & Shaked, I. (1986). Domestic corporations: Financial performance andcharacteristics. Journal of International Business Studies, 18: 89–100.

Morck, R., Yeung, B., & Zhao, M. (2008). Perspectives on China’s outward foreign directinvestment. Journal of International Business Studies, 39: 337–350.

Naude, W., & Rossouw, S. (2010). Early international entrepreneurship in China: Extentand determinants. Journal of International Entrepreneurship, 8: 87–111.

Oh, C. H., & Rugman, A. M. (2006). Regional sales of multinationals in the worldcosmetics industry. European Management Journal, 24(2–3): 163–173.

Osegowitsch, T., & Sammartino, A. (2008). Reassessing (home-) regionalization. Journalof International Business Studies, 39: 184–196.

Pangarkar, N. (2008). Internationalization and performance of small- and medium-sized enterprises. Journal of World Business, 43: 475–485.

Qian, G., Li, L., Li, J., & Qian, Z. (2008). Regional diversification and firm performance.Journal of International Business Studies, 39: 197–214.

Rugman, A. M. (2000). The End of Globalization: Why Global Strategy is a Myth and How toProfit from the Realities of Regional Markets. New York: Amacom.

Rugman, A. M. (Ed.). (2007). Research on Global Strategic Management: Regional Aspectsof Multinationality and Performance. Amsterdam: Elsevier.

Rugman, A. M., & Collinson, S. (2004). The regional nature of the world’s automotivesector. European Management Journal, 22(5): 471–482.

Rugman, A. M., & Oh, C. (2007). In A. Rugman (Ed.), Multinationality and RegionalPerformance 2001–2005 in Research on Global Strategic Management: RegionalAspects of Multinationality and Performance (pp. 31–43). Amsterdam: Elsevier.

Rugman, A. M., & Verbeke, A. (2004). A perspective on regional and global strategiesof multinational enterprises. Journal of International Business Studies, 35(1): 3–18.

Rugman, A. M. (1979). International Diversification and the Multinational Enterprise.Lexington, MA: Heath.

Rugman, A. M., Lecraw, D. J., & Booth, L. D. (1985). International Business: Firm andEnvironment. New York: McGraw-Hill.

Ruigrok, W., & Wagner, H. (2003). Internationalization and performance: An organiza-tional learning perspective. Management International Review, 43(1): 61–84.

Shaked, I. (1986). Are multinational corporations safer? Journal of International BusinessStudies, 17: 75–80.

Sim, A. B., & Pandian, J. R. (2003). Emerging Asian MNEs and Their internationalizationstrategies—Case study evidence on Taiwanese and Singaporean firms. Asia PacificJournal of Management, 20: 27–50.

Stata. (2003). Stata Cross-sectional Time Series: Reference Manual Release 8. CollegeStation. Texas: Stata Press.

Tseng, C.-S. (1994). The process of internationalization of PRC multinationals. In H.Schutte (Ed.), The Global Competitiveness of the Asian Firm. Basingstoke, UK:Macmillan. pp. 121–128.

Warner, M., Ng, S.-H., & Xu, X. (2004). Late development experience and the evolutionof transactional firms in the People’s Republic of China. Asia Pacific Business Review,10: 324–345.

Wernerfelt, B., & Montgomery, C. (1988). Tobin’s q and the importance of focus in firmperformance. American Economic Review, 78(1): 246–250.

Whitley, R. (1999). Divergent capitalisms: The Social Structuring and Change of BusinessSystems. Oxford: Oxford University Press.

Windmeijer, F. (2005). A finite sample correction for the variance of linear efficienttwo-step GMM estimators. Journal of Econometrics, 126: 25–51.

Wright, M., Filatotchev, I., Hoskisson, R. E., & Peng, M. W. (2005). Strategy research inemerging economies: Challenging the conventional wisdom. Journal of Manage-ment Studies, 42: 1–33.

Yang, X., Lim, Y., Sakurai, Y., & Seo, S. (2009). Internationalization of Chinese and Koreanfirms. Thunderbird International Business Review, 51(1): 37–51.

Zhou, L., Wu, W. P., & Luo, X. (2007). Internationalization and the performance of born-global SMEs: The mediating role of social networks. Journal of International BusinessStudies, 38: 673–690.