regi.tankonyvtar.hu · Web viewAgricultural Economics II. Agricultural Economics II. Agricultural...

203

Agricultural Economics II. Popp, József Created by XMLmind XSL-FO Converter.

Transcript of regi.tankonyvtar.hu · Web viewAgricultural Economics II. Agricultural Economics II. Agricultural...

Agricultural Economics II.Popp, József

Created by XMLmind XSL-FO Converter.

Agricultural Economics II.Popp, József

TÁMOP-4.1.2.A/1-11/1-2011-0009

University of Debrecen, Service Sciences Methodology Centre

Debrecen, 2013.

Created by XMLmind XSL-FO Converter.

TartalomTárgymutató ......................................................................................................................................... 11. 1. THE GLOBAL AGRICULTURAL ECONOMY, HUNGER, AND POVERTY ........................ 2

1. 1.1. Sustainable future ............................................................................................................ 21.1. 1.1.1. Economic and financial crisis (2006-2008) ..................................................... 31.2. 1.1.2. Food-security strategy ...................................................................................... 41.3. 1.1.3. External shocks in addition to demand and supply fundamentals .................. 41.4. 1.1.4. A way forward .................................................................................................. 61.5. 1.1.5. World market volatility challenges facing poor net food-importing countries 71.6. 1.1.6. Characteristics of food insecurity in net food importing countries ................. 71.7. 1.1.7. What can LDCs and NFIDCs do for themselves? ........................................... 81.8. 1.1.8. Avoiding export prohibitions and restrictions ................................................. 81.9. 1.1.9. Stockholding and domestic food assistance .................................................... 81.10. 1.1.10. Reducing the high transaction costs for intra-regional trade ...................... 81.11. 1.1.11. Using AoA flexibility to invest in food production and resilience ............... 81.12. 1.1.12. How can the international community help? ............................................... 8

2. 1.2. Limiting the role of food aid to emergency responses .................................................... 83. 1.3. Targeting export credits ................................................................................................... 94. 1.4. Strengthening food financing facilities ........................................................................... 95. 1.5. Increasing technical and financial assistance to boost productivity ................................ 96. Questions ................................................................................................................................ 97. References ............................................................................................................................ 10

2. 2. FOOD SECURITY AND SOCIAL PROTECTION .................................................................. 111. 2.1. Risks to food security .................................................................................................... 112. 2.2. Competition for land and water .................................................................................... 133. 2.3. Growth of agricultural output ........................................................................................ 134. Questions .............................................................................................................................. 145. References ............................................................................................................................ 15

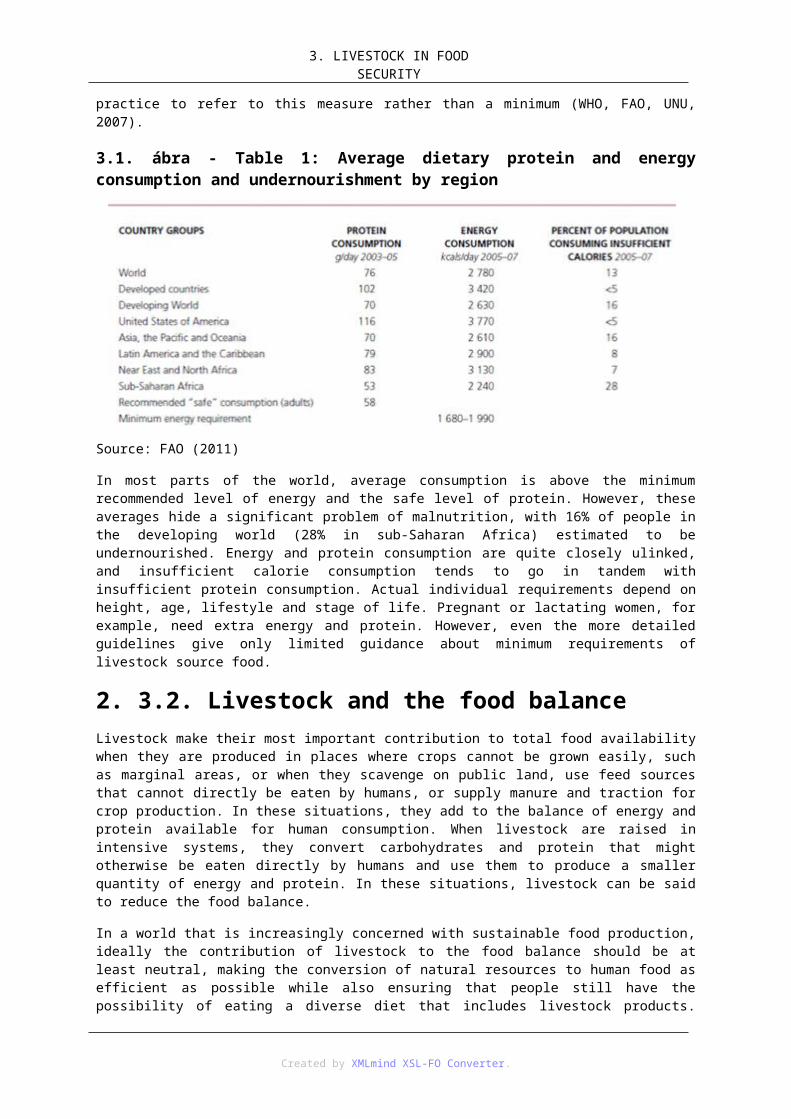

3. 3. LIVESTOCK IN FOOD SECURITY ........................................................................................ 161. 3.1. Livestock food in the diet .............................................................................................. 162. 3.2. Livestock and the food balance ..................................................................................... 173. 3.3. Livestock contributing to crop production .................................................................... 184. 3.4. Stability of food supplies ............................................................................................... 195. 3.5. Economic factors affecting choice of livestock source foods ....................................... 196. Questions .............................................................................................................................. 227. References ............................................................................................................................ 22

4. 4. TENSION BETWEEN FOOD, ENERGYAND ENVIRONMENTAL SECURITY ................ 251. 4.1. Food security ................................................................................................................. 262. 4.2. Energy security .............................................................................................................. 26

2.1. 4.2.1. Bioenergy potential ....................................................................................... 273. 4.3. Environmental impact: land use change and greenhouse gas emission ........................ 27

3.1. 4.3.1. Sustainability criteria for bioenergy ............................................................. 294. Questions .............................................................................................................................. 305. References ............................................................................................................................ 31

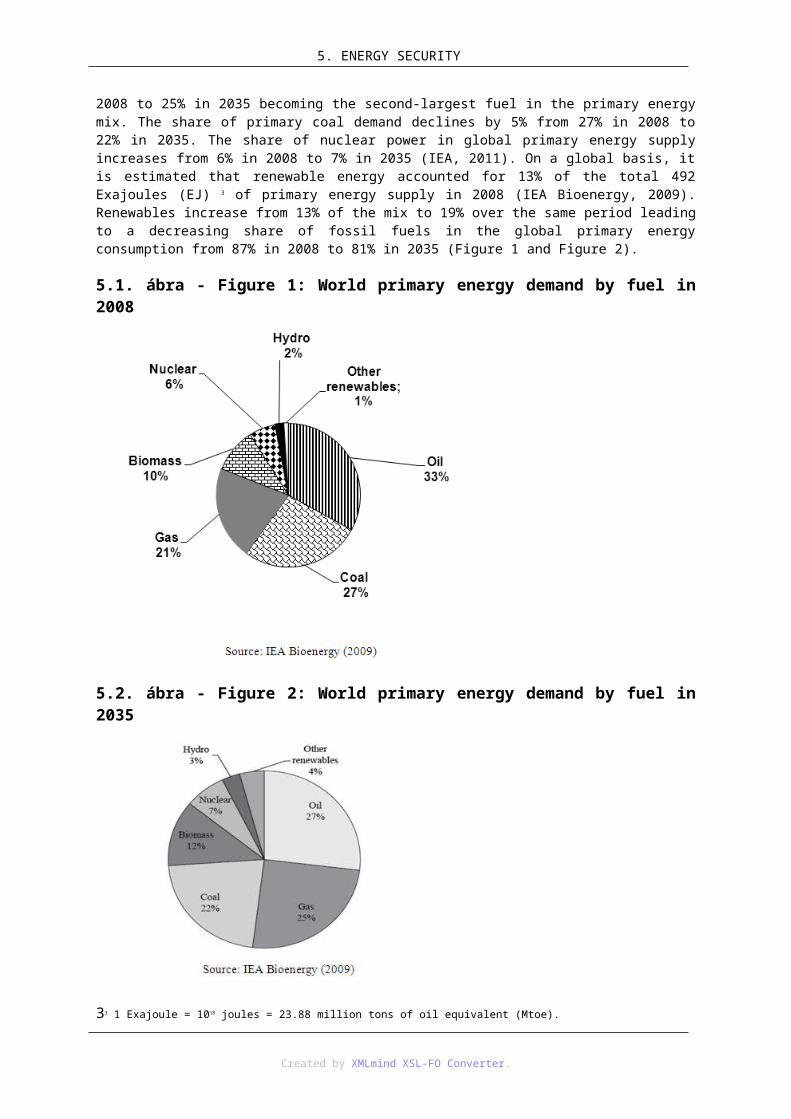

5. 5. ENERGY SECURITY ............................................................................................................... 321. 5.1. Global energy demand .................................................................................................. 322. 5.2. Rising transport demand reconfirms the end of cheap oil ............................................. 343. 5.3. Prospects for natural gas ............................................................................................... 34

Created by XMLmind XSL-FO Converter.

Agricultural Economics II.

4. 5.4. Coal in global energy demand ....................................................................................... 355. 5.5. Nuclear energy .............................................................................................................. 356. 5.6. Achieving energy for all ................................................................................................ 367. 5.7. Transport policies .......................................................................................................... 368. 5.8. Environmental impact ................................................................................................... 379. Questions .............................................................................................................................. 3810. References .......................................................................................................................... 38

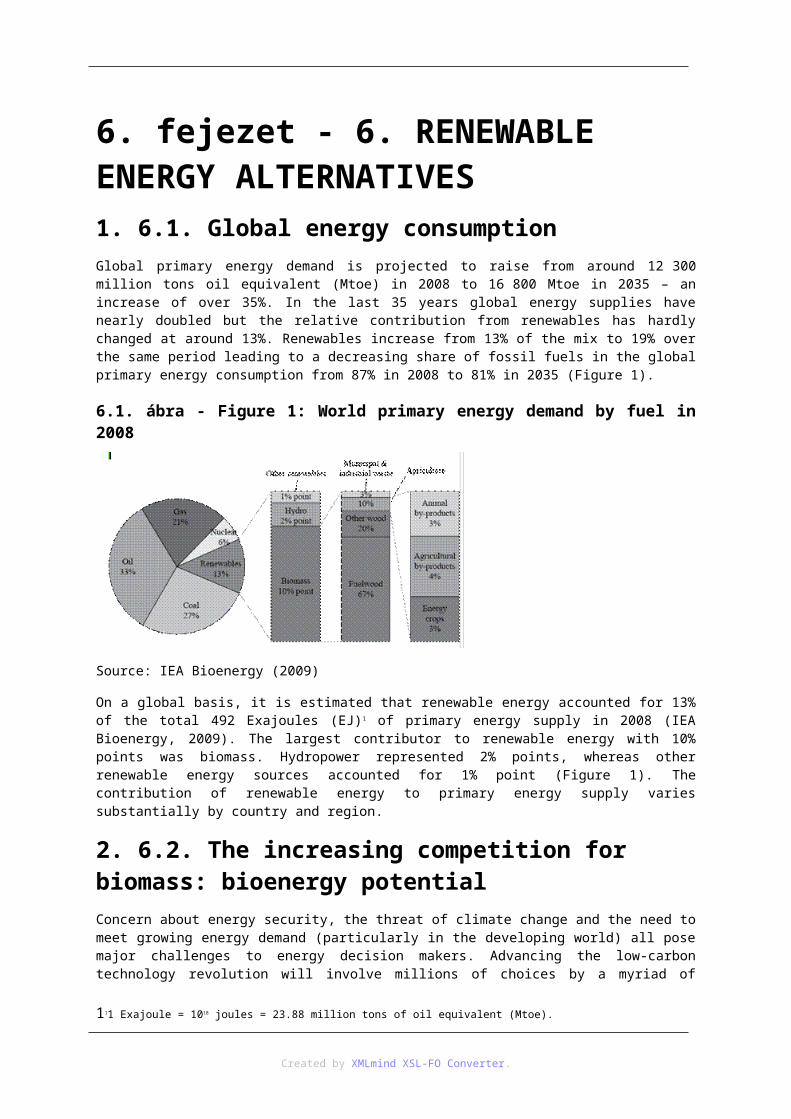

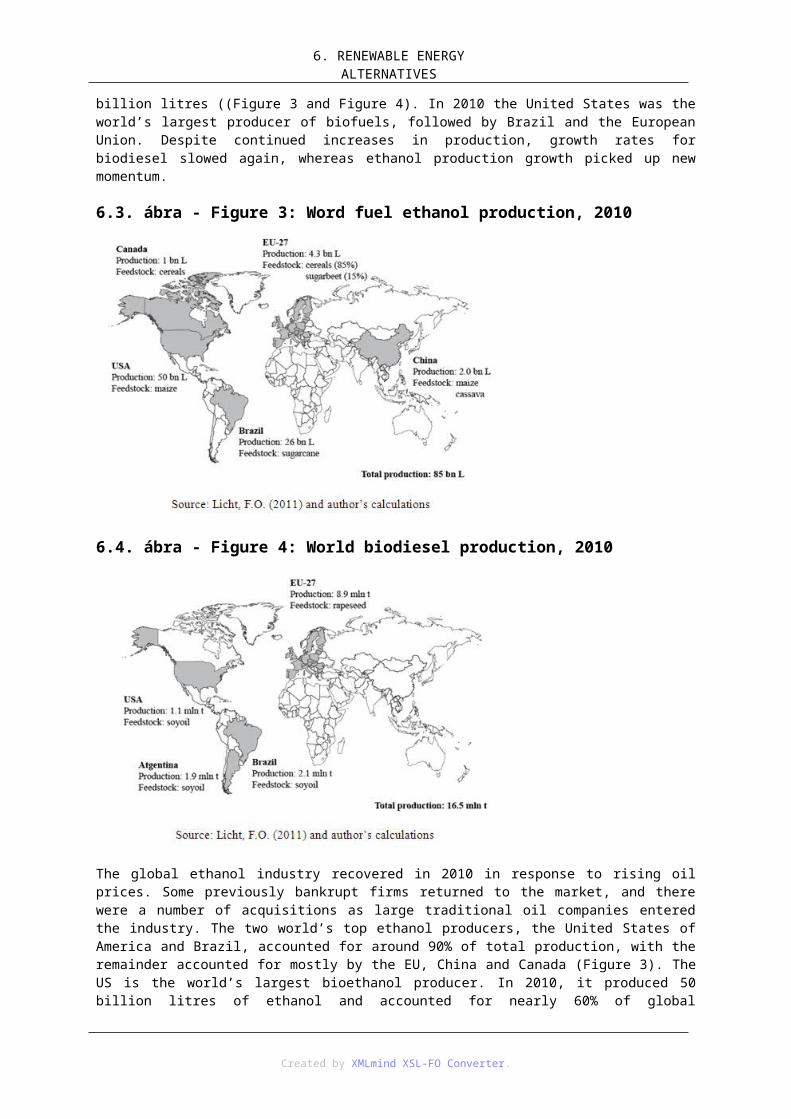

6. 6. RENEWABLE ENERGY ALTERNATIVES ............................................................................ 401. 6.1. Global energy consumption .......................................................................................... 402. 6.2. The increasing competition for biomass: bioenergy potential ..................................... 403. 6.3. Competition for financing between renewable energy alternatives ............................. 434. 6.4. Biofuels ......................................................................................................................... 435. 6.5. Land use for biofuels production .................................................................................. 466. 6.6. Environmental impact of biofuels ................................................................................. 477. Questions ............................................................................................................................. 488. References ............................................................................................................................ 48

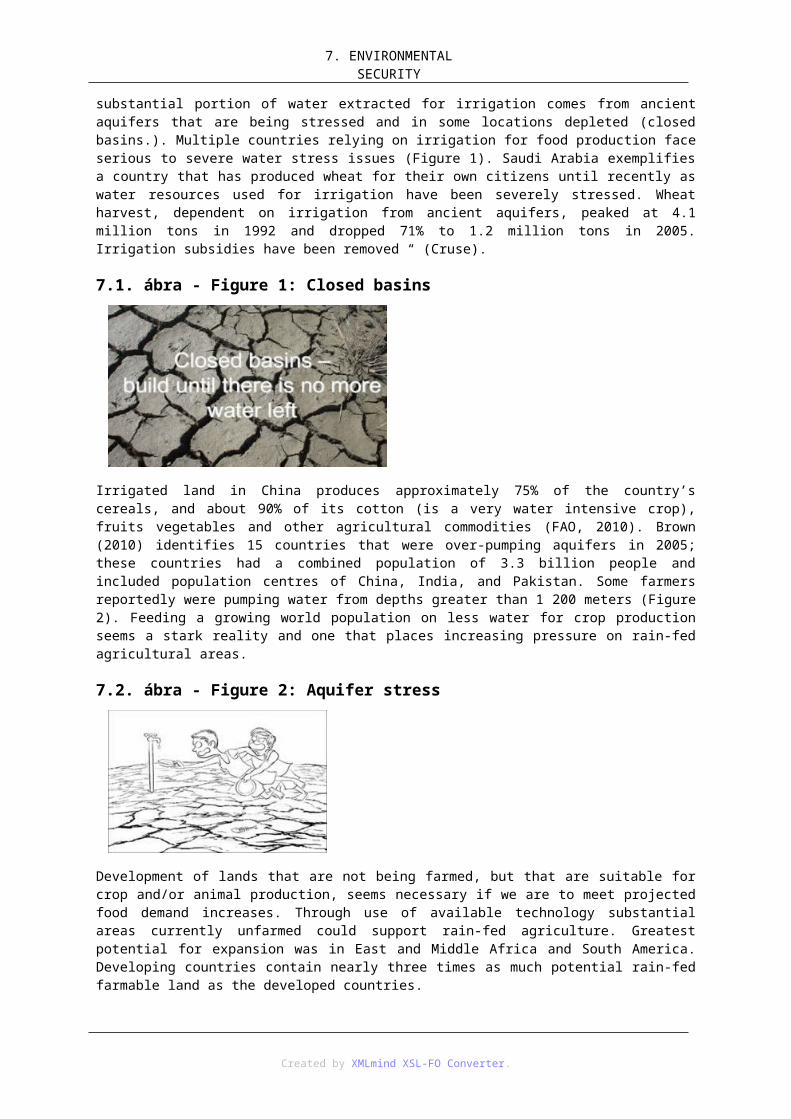

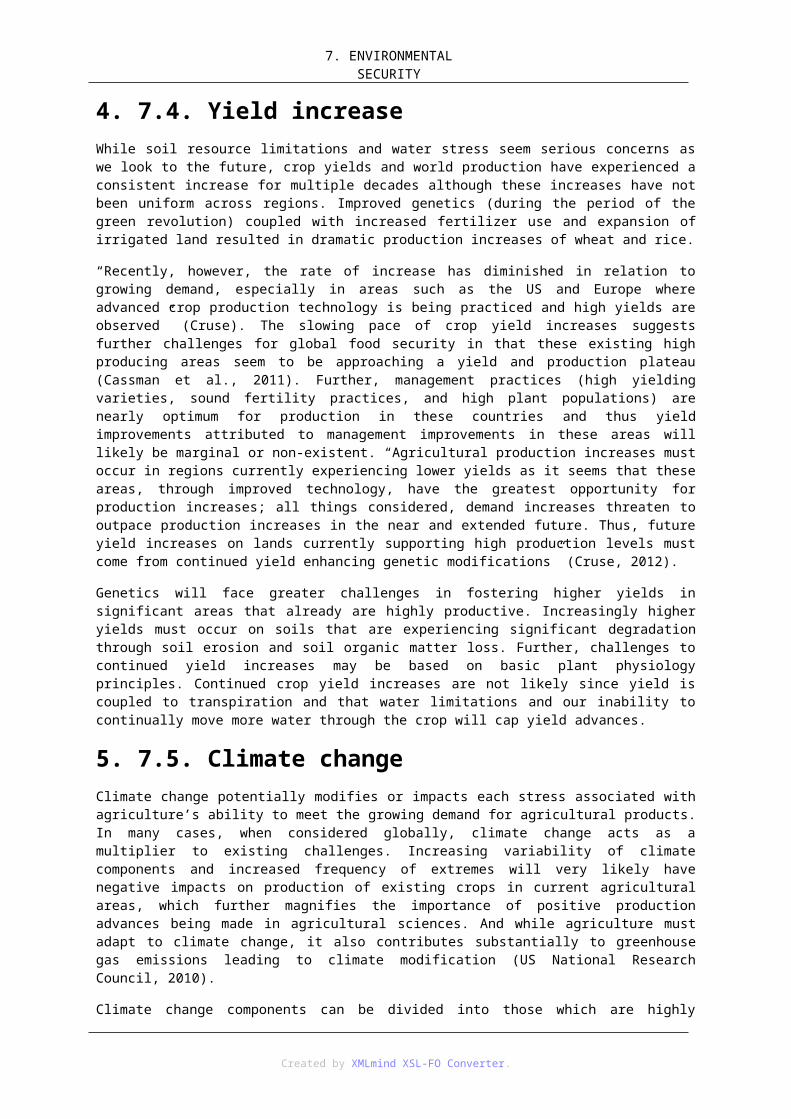

7. 7. ENVIRONMENTAL SECURITY ............................................................................................. 501. 7.1. Food cost ....................................................................................................................... 502. 7.2. Agricultural land depletion ............................................................................................ 503. 7.3. Irrigation and aquifer stress ........................................................................................... 514. 7.4. Yield increase ................................................................................................................ 525. 7.5. Climate change .............................................................................................................. 526. 7.6. Carbon dioxide concentration ....................................................................................... 537. 7.7. Temperature ................................................................................................................... 548. 7.8. Precipitation .................................................................................................................. 549. 7.9. Climate change, soil degradation and crop productivity interaction ............................ 5510. Questions ............................................................................................................................ 5511. References .......................................................................................................................... 56

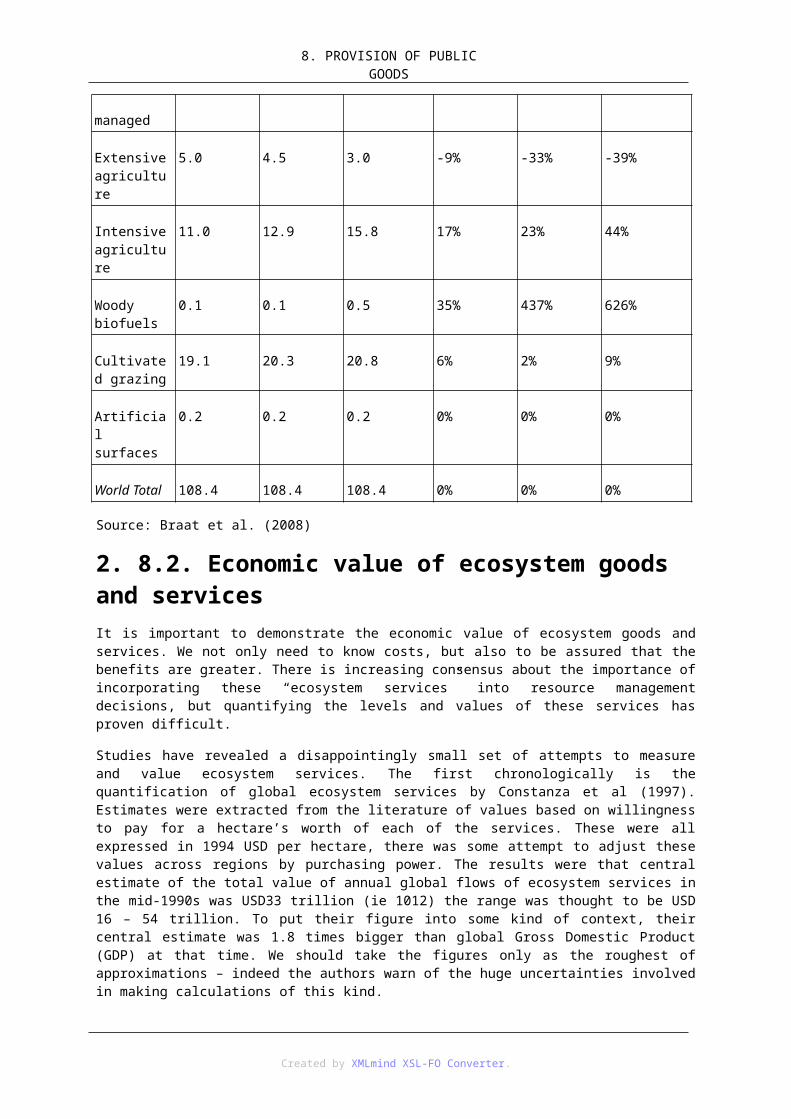

8. 8. PROVISION OF PUBLIC GOODS .......................................................................................... 581. 8.1. Loss of biodiversity ....................................................................................................... 582. 8.2. Economic value of ecosystem goods and services ........................................................ 593. 8.3. Markets for environmental services .............................................................................. 614. Questions .............................................................................................................................. 625. References ............................................................................................................................ 62

9. 9. CLIMATE CHANGE: IMPACT, ADAPTATION AND MITIGATION ................................... 641. 9.1. Definition of climate change ......................................................................................... 642. 9.2. Global greenhouse ......................................................................................................... 653. 9.3. Deeper cuts .................................................................................................................... 654. 9.4. The world needs to adapt to the impacts of climate change .......................................... 665. 9.5. Providing financing for adaptation ............................................................................... 666. 9.6. Timeline of climate change ........................................................................................... 667. Questions ............................................................................................................................. 698. References ............................................................................................................................ 69

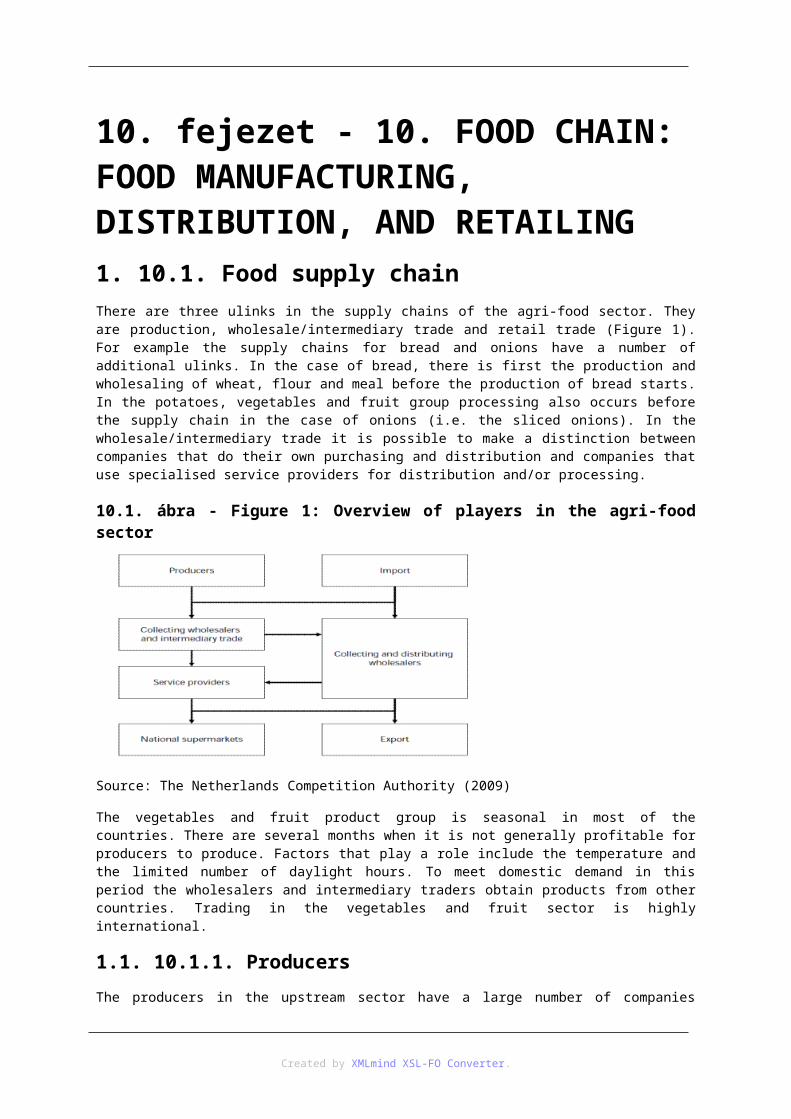

10. 10. FOOD CHAIN: FOOD MANUFACTURING, DISTRIBUTION, AND RETAILING ........ 711. 10.1. Food supply chain ....................................................................................................... 71

1.1. 10.1.1. Producers ..................................................................................................... 711.2. 10.1.2. Wholesalers ................................................................................................. 711.3. 10.1.3. Supermarkets ............................................................................................... 72

2. 10.2. Food retail trade .......................................................................................................... 722.1. 10.2.1. Negotiations ................................................................................................. 722.2. 10.2.2. Price, discounts, financial contributions and risks ...................................... 73

Created by XMLmind XSL-FO Converter.

Agricultural Economics II.

3. 10.3. Asymmetric price adjustment ..................................................................................... 744. Questions .............................................................................................................................. 755. References ............................................................................................................................ 75

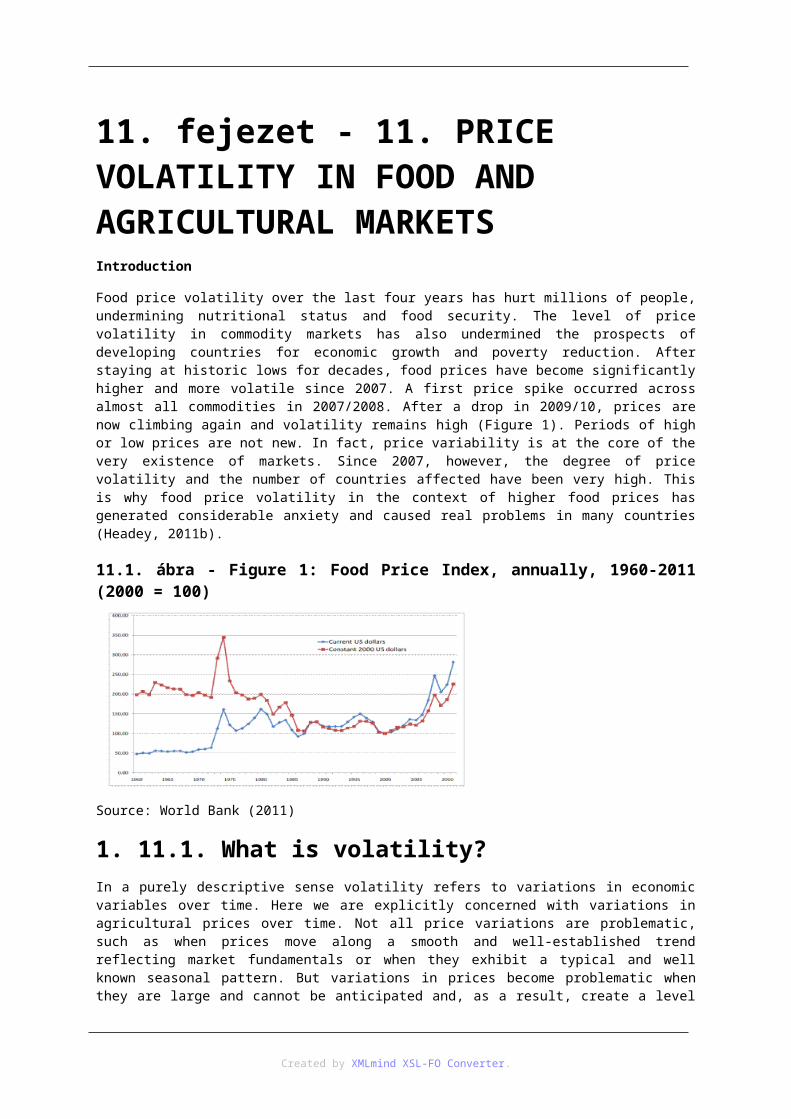

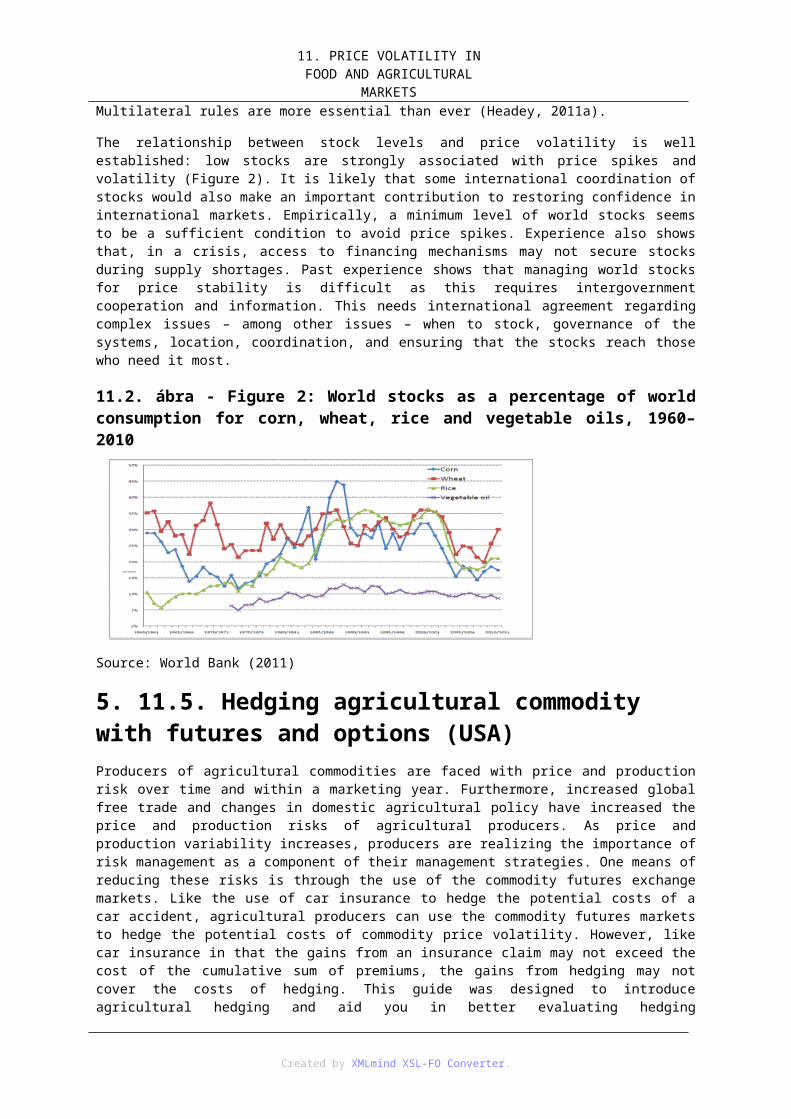

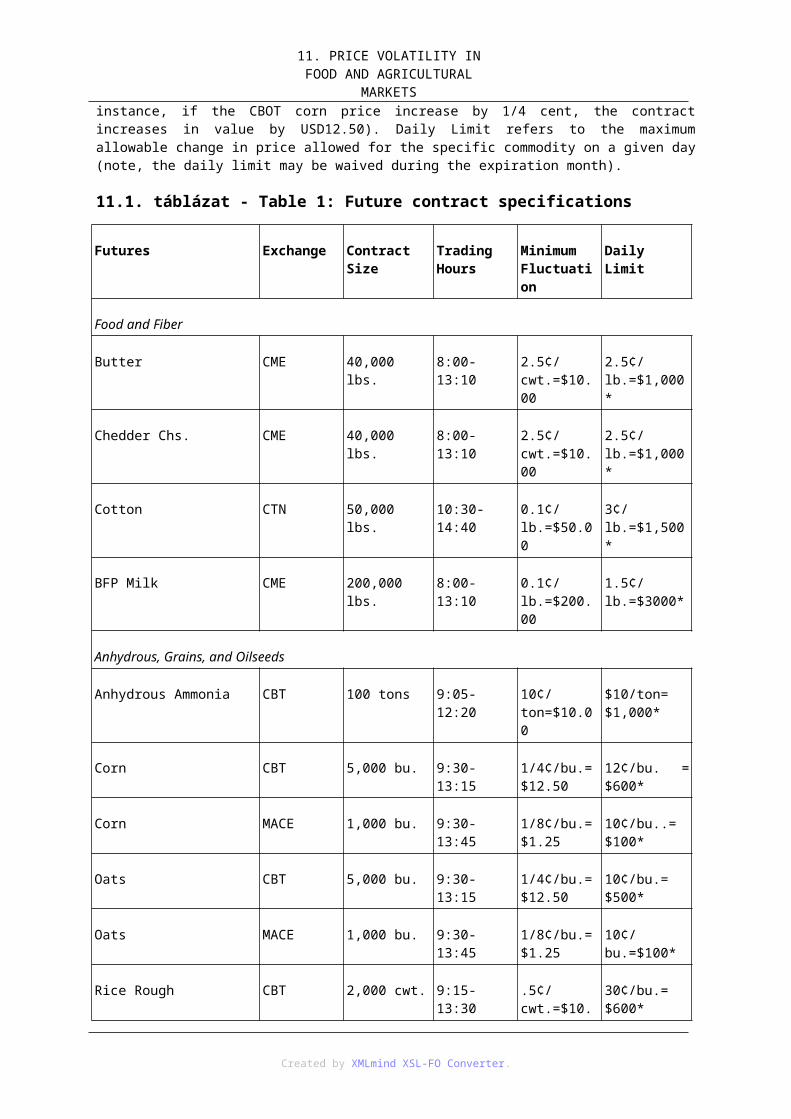

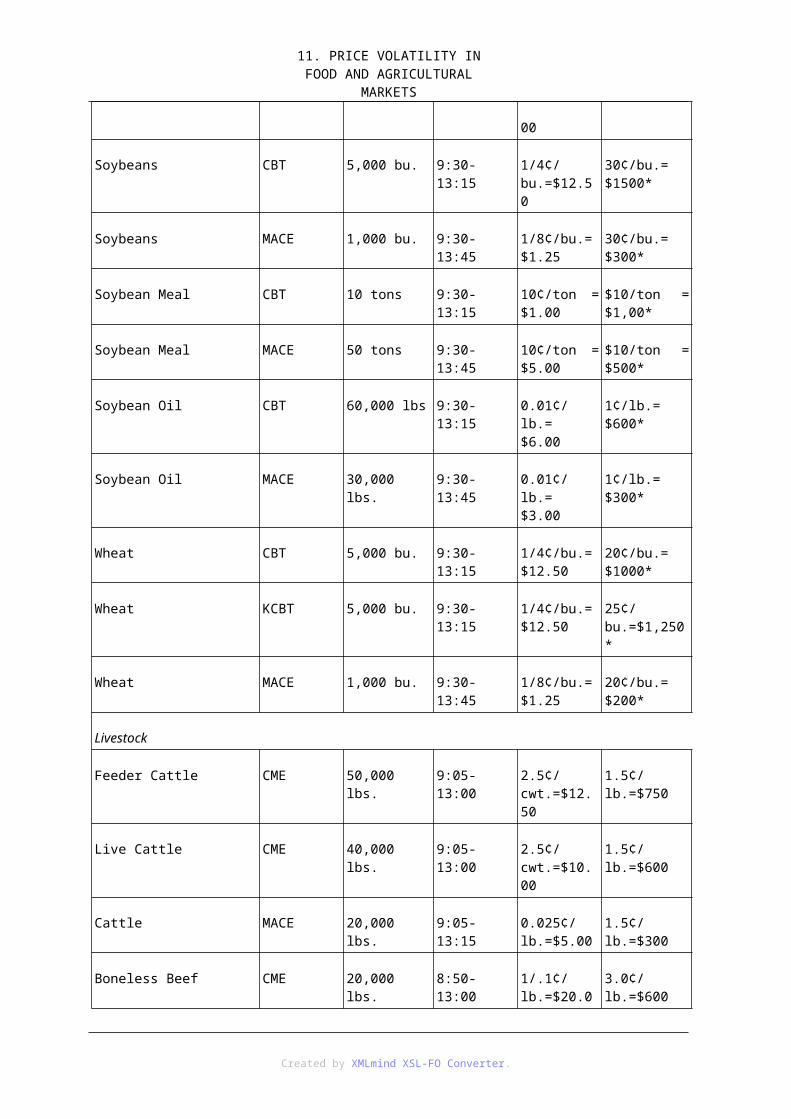

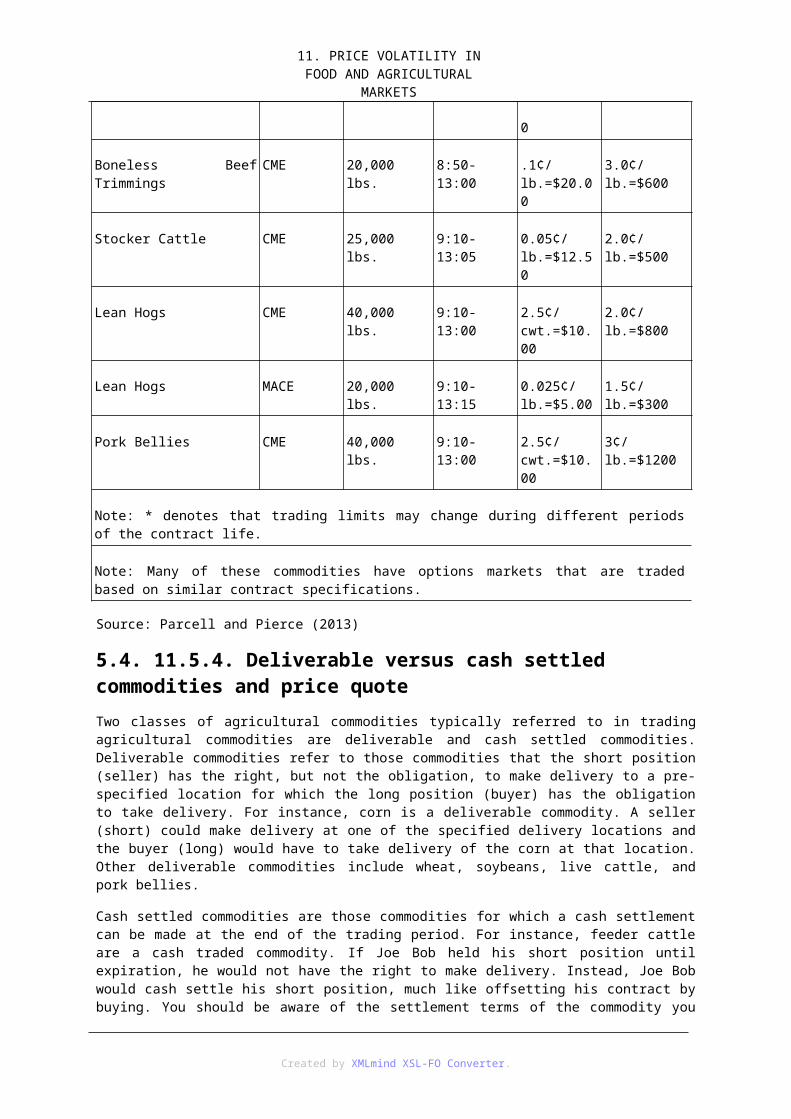

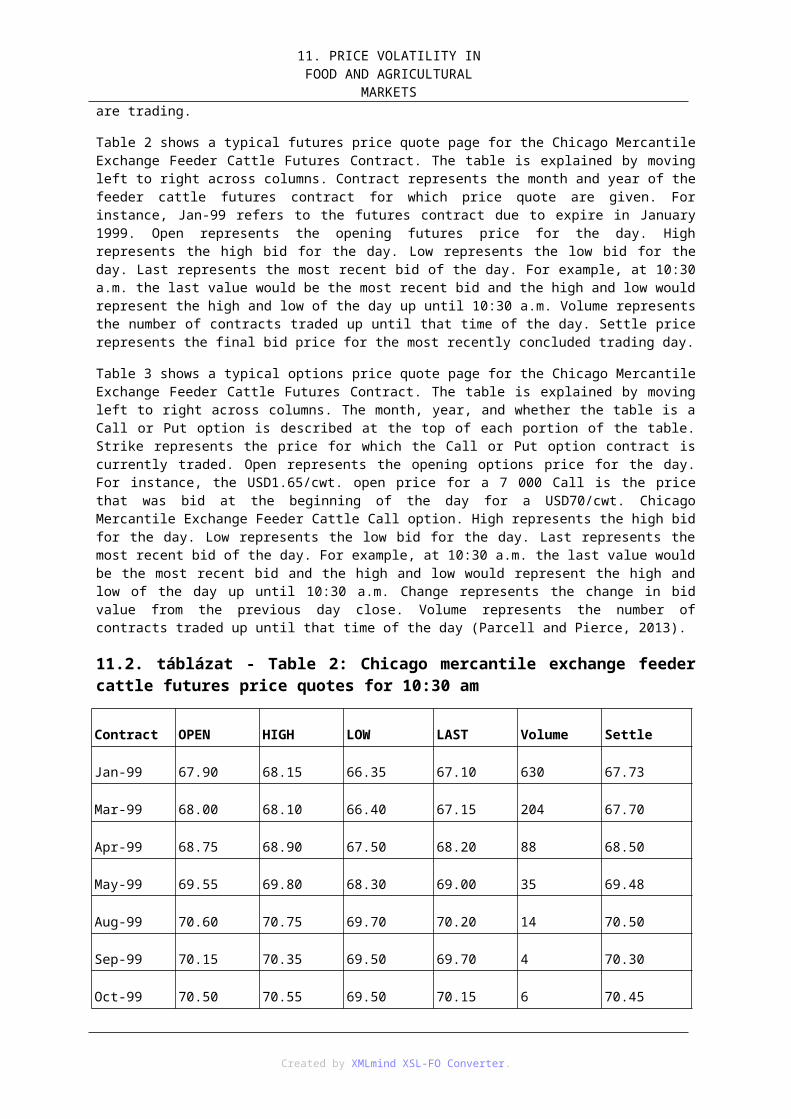

11. 11. PRICE VOLATILITY IN FOOD AND AGRICULTURAL MARKETS .............................. 761. 11.1. What is volatility? ....................................................................................................... 762. 11.2. Price levels and food security ...................................................................................... 763. 11.3. Drivers of food price volatility .................................................................................... 77

3.1. 11.3.1. Demand elasticity ........................................................................................ 774. 11.4. Trade policies ............................................................................................................. 785. 11.5. Hedging agricultural commodity with futures and options (USA) ............................. 79

5.1. 11.5.1. Commodity arbitrage and the operations of a commodity exchange ......... 795.1.1. 11.5.1.1. If the future price goes higher, lower or does not change ............ 81

5.2. 11.5.2. Options ......................................................................................................... 825.3. 11.5.3. Future contract specifications for selected agricultural commodities ........ 835.4. 11.5.4. Deliverable versus cash settled commodities and price quote ..................... 855.5. 11.5.5. What is commodity basis? .......................................................................... 875.6. 11.5.6. Speculation on the futures market ............................................................... 88

6. 11.6. Demand for food products in the future ..................................................................... 886.1. 11.6.1. Investing in agriculture ................................................................................ 896.2. 11.6.2. Food waste ................................................................................................... 896.3. 11.6.3. Biofuels ........................................................................................................ 906.4. 11.6.4. GHG-emission ............................................................................................. 906.5. 11.6.5. Promoting food security strategy programmes ............................................ 90

7. Questions .............................................................................................................................. 908. References ........................................................................................................................... 91

12. 12. Plant biotechnology ............................................................................................................... 921. 12.1. History ......................................................................................................................... 92

1.1. 12.1.1. Thousands of years ago ............................................................................... 922. 12.2. How biotechnology works? ......................................................................................... 943. 12.3. Why biotechnology matters? ....................................................................................... 944. 12.4. Why do we need biotechnology? ................................................................................ 955. 12.5. What is genetic modification? ..................................................................................... 956. 12.6. What sort of changes can be brought about by genetic modification? ........................ 957. 12.7. How can we assure that these new developments are safe? ........................................ 968. 12.8. How do we know that genetically modified crops are safe to eat? ............................. 969. 12.9. What about the impact of genetically modified crops on the environment? ............... 9610. 12.10. Could the new genes in these crops to be passed on the other plants? .................. 9611. 12.11. What about consumer information? ........................................................................ 9612. 12.13. Substantial equivalence of genetically engineered crops and products with their conventional counterparts ........................................................................................................ 9613. Questions ............................................................................................................................ 9814. References .......................................................................................................................... 98

13. 13. ECONOMICS OF GM CROP CULTIVATION .................................................................... 991. Introduction .......................................................................................................................... 992. 13.1. Global status of commercialised GM crops in 2011 ................................................... 993. 13.2. Global maize trade .................................................................................................... 1024. 13.3. Global soybean and soymeal trade ............................................................................ 1035. 13.4. The authorisation process in practice ........................................................................ 1046. 13.5. The GM debate in Europe ........................................................................................ 1087. Questions ............................................................................................................................ 1108. References .......................................................................................................................... 110

14. 14. ECONOMICS OF CROP PROTECTION MEASURES .................................................... 111

Created by XMLmind XSL-FO Converter.

Agricultural Economics II.

1. 14.1. Challenges facing scientists and pest management experts ...................................... 1112. 14.2. Estimates of crop losses due to pests ........................................................................ 1113. 14.3. Cost and benefit of pesticides ................................................................................... 1124. 14.4. Global pesticide market ............................................................................................ 1155. Questions ........................................................................................................................... 1166. References .......................................................................................................................... 116

15. 15. INTERNATIONAL AGRICULTURAL TRADE: WORLD TRADE ORGANIZATION (WTO) .......................................................................................................................................................... 118

1. 15.1. The WTO Agreements .............................................................................................. 1181.1. 15.1.1. Objectives of the WTO: ............................................................................ 1181.2. 15.1.2. Functions of the WTO: .............................................................................. 1181.3. 15.1.3. The Ministerial Conference ....................................................................... 1191.4. 15.1.4. The General Council .................................................................................. 1191.5. 15.1.5. The Trade Negotiations Committee .......................................................... 1191.6. 15.1.6. The Councils & Subsidiary Bodies ........................................................... 1191.7. 15.1.7. Decision- making in the WTO .................................................................. 119

2. 15.2. Principles ................................................................................................................... 1203. 15.3. Rules on unfair trade ................................................................................................. 120

3.1. 15.3.1. Anti-dumping measures ............................................................................. 1203.2. 15.3.2. Subsidies & countervailing duties ............................................................. 120

4. 15.4. Non-discrimination ................................................................................................... 1214.1. 15.4.1. MFN under GATT ..................................................................................... 1214.2. 15.4.2. National treatment under GATT ................................................................ 121

5. 15.5. Tariffs ........................................................................................................................ 1215.1. 15.5.1. Negotiations on tariff reduction ................................................................. 1215.2. 15.5.2. National tariffs ........................................................................................... 1225.3. 15.5.3. Other duties and charges ........................................................................... 122

6. 15.6. Non-tariff barriers ..................................................................................................... 1226.1. 15.6.1. Quantitative restrictions ............................................................................ 1226.2. 15.6.2. Specific exceptions .................................................................................... 1236.3. 15.6.3. Other non-tariff barriers ............................................................................ 123

7. 15.7. Technical regulations and standards .......................................................................... 1247.1. 15.7.1. Sanitary and phytosanitary measures ........................................................ 124

8. 15.8. General safeguards .................................................................................................... 1259. 15.9. Waivers ...................................................................................................................... 12510. 15.10. Dispute settlement ................................................................................................. 12511. 15.11. Agreement on Agriculture .................................................................................... 125

11.1. 15.11.1. Tarification ............................................................................................. 12611.2. 15.11.2. Bindings and reductions ........................................................................ 12611.3. 15.11.3. Tariff-rate quotas .................................................................................... 12611.4. 15.11.4. The boxes ............................................................................................... 12711.5. 15.11.5. Green box ............................................................................................... 12711.6. 15.11.6. Amber box ............................................................................................. 12711.7. 15.11.7. Blue box ................................................................................................. 12711.8. 15.11.8. De minimis ............................................................................................. 12811.9. 15.11.9. Export competition ................................................................................ 12911.10. 15.11.10. Anti-circumvention ........................................................................... 130

12. 15.12. WTO negotiations after 2000 ................................................................................ 13113. Questions .......................................................................................................................... 13214. References ........................................................................................................................ 132

Created by XMLmind XSL-FO Converter.

Az ábrák listája1.1. Figure 1: Poor people spend much of their income on food ......................................................... 31.2. Figure 2: Countries requiring external assistance for food (34 countries) .................................... 92.1. Figure 1: World population growth ............................................................................................. 112.2. Figure 2: Losses along the food chain ........................................................................................ 123.1. Table 1: Average dietary protein and energy consumption and undernourishment by region .... 163.2. Table 2: Changes in global livestock production total and per person 1967 to 200 ................... 185.1. Figure 1: World primary energy demand by fuel in 2008 ........................................................... 335.2. Figure 2: World primary energy demand by fuel in 2035 ........................................................... 336.1. Figure 1: World primary energy demand by fuel in 2008 ........................................................... 406.2. Figure 2: Global bioenergy sources ............................................................................................ 416.3. Figure 3: Word fuel ethanol production, 2010 ............................................................................ 446.4. Figure 4: World biodiesel production, 2010 ............................................................................... 457.1. Figure 1: Closed basins ............................................................................................................... 517.2. Figure 2: Aquifer stress ............................................................................................................... 517.3. Figure 3: Climate change ............................................................................................................ 5210.1. Figure 1: Overview of players in the agri-food sector .............................................................. 7111.1. Figure 1: Food Price Index, annually, 1960-2011 (2000 = 100) ............................................... 7611.2. Figure 2: World stocks as a percentage of world consumption for corn, wheat, rice and vegetable oils, 1960–2010 .................................................................................................................................. 7912.1. Figure 1: Bt Cotton lifecycle .................................................................................................... 9513.1. Figure 1: GM crop plantings 2011 by crop ............................................................................ 10013.2. Figure 2: Share of GM crops in global plantings of key crops in 2011* ................................ 10013.3. Figure 3: GM Product submissions and authorisations. Status of 1 February 2012 .............. 10814.1. Figure 1: Development of crop losses from 1996-98 to 2001-03 ........................................... 11214.2. Figure 2: Development of efficacy of actual crop protection practices from 1996-98 to 2001-03 11215.1. Figure 1: Tariff-Quota ............................................................................................................. 12315.2. Figure 2: TBT and SPS measures relating to the international trade of oranges .................... 12415.3. Figure 1: Amber Box and de minimis: Current Total Aggregate Measurement of Support ... 12815.4. Table 3: Reduction formula for ad valorem tariffs ................................................................. 131

Created by XMLmind XSL-FO Converter.

A táblázatok listája8.1. Table 1: Scenario of the future: 2050 .......................................................................................... 5911.1. Table 1: Future contract specifications ..................................................................................... 8311.2. Table 2: Chicago mercantile exchange feeder cattle futures price quotes for 10:30 am ........... 8611.3. Table 3: Chicago mercantile exchange feeder cattle options price quotes for 10:30 am .......... 8611.4. Table 4: How a grain producer should use basis in marketing strategies ................................. 8813.1. Table 1: Area of GM crops by country (2011) Million hectares ............................................... 9913.2. Table 2: Adoption rate of GM crops in the leading exporting countries of maize and soybean (2011) .......................................................................................................................................................... 10113.3. Table 3: Global maize trade (Million tonnes) ......................................................................... 10213.4. Table 4: Global soybean trade (Million tonnes) ..................................................................... 10313.5. Table 5: Global soybean meal trade (Million tonnes) ............................................................ 10413.6. Table 6: Events in commercial GM crops and in pipelines worldwide, by crop .................... 10613.7. Table 7: Events in commercial GM crops and in pipelines worldwide by region of origin ... 10613.8. Table 8: Asynchronous and isolated foreign approvals as potential sources for low-level presence .......................................................................................................................................................... 10714.1. Table 1: Value of herbicides, insecticides and fungicides in U.S. crop production ................ 11314.2. Table 2: Total estimated environmental and social costs from pesticides in the USA ........... 11414.3. Table 3: Annual estimated pesticide use in the world ............................................................. 11515.1. Table 1: The reductions in agricultural subsidies and protection agreed in the Uruguay Round 12515.2. Table 2: Domestic support structure ....................................................................................... 128

Created by XMLmind XSL-FO Converter.

Tárgymutató

Created by XMLmind XSL-FO Converter.

1. fejezet - 1. THE GLOBAL AGRICULTURAL ECONOMY, HUNGER, AND POVERTYIntroduction

As stated in the 1972 United Nations Conference on the Human Environment and the 1992 Earth Summit, human beings are at the centre of sustainable development. However, even today, over 900 million people still suffer from hunger. Poor populations worldwide, especially in rural areas, are among those most vulnerable to the food, climate, financial, economic, social and energy crises and threats the world faces today We cannot call development sustainable while this situation persists, while nearly one out of every seven men, women and children are victims of undernourishment (FAO, 2012a).

The quest for food security can be the common thread that ulinks the different challenges we face and helps build a sustainable future. To feed a growing population that is expected to top the nine billion mark in 2050, the Food and Agriculture Organization of the United Nations (FAO) projects the need to increase agricultural output by at least 60% in the next decades. But even then the pressure on our natural resources will be extreme. So we must also change the way we eat and find ways to feed the world without the need to produce as much. We can do this by changing to healthier diets in the richer segments of our population and by diminishing the food loss and waste that exist in industrialized and developing countries, and that make us throw away 1.3 billion tonnes of food every year, between production and consumption (FAO, 2012a).

However, even if we do increase agricultural output by 60%, the world would still have 300 million people hungry in 2050 because, like the hundreds of millions today, they would still lack the means to access the food they need. For them, food security is not an issue of insufficient production; it is an issue of inadequate access. The only way to ensure their food security is by creating decent jobs, paying better wages, giving them access to productive assets and distributing income in a more equitable way. We must bring them into society, complementing support to smallholders and income generation opportunities with the strengthening of safety nets, cash for work and cash transfer programmes that contribute to strengthening of local production and consumption circuits, in an effort that must contribute to our sustainable development goals.

The transition to a sustainable future also requires fundamental changes in the governance of food and agriculture and an equitable sharing of the transition costs and benefits. In the past, the poorer have paid a greater share of transition costs and received a smaller share of benefits. This is an unacceptable balance and one that needs to change. The speed of change should also be a concern, so that the vulnerable population can adapt and be part of the changes instead of widening the gaps that exist today.

1. 1.1. Sustainable futureImproving agricultural and food systems is essential for a world with healthier people and healthier ecosystems. Healthy and productive lives cannot be achieved unless “all people at all times have physical, social and economic access to sufficient, safe and nutritious food which meets their dietary needs and food preferences for an active and healthy life” (FAO, 1996). Healthy ecosystems must be resilient and productive, and provide the goods and services needed to meet current societal needs and desires without jeopardizing the options for future generations to benefit from the full range of goods and services provided by terrestrial, aquatic and marine ecosystems. There are very strong ulinkages between the conditions to achieve universal food security and nutrition, responsible environmental stewardship and greater fairness in food management. They intersect in agricultural and food systems at the global, national and local levels. The transition to a sustainable future requires fundamental changes in the governance of food and agriculture and an equitable distribution of the transition costs and benefits.

The sustainable management of agriculture and food systems is key to a sustainable future. Sound policies are needed to create the incentives and capacities for sustainable consumption and production and to enable consumers and producers to make sustainable choices.

Created by XMLmind XSL-FO Converter.

1. THE GLOBAL AGRICULTURAL ECONOMY,

HUNGER, AND POVERTYNational governments and other stakeholders need to:

• Establish and protect rights to resources, especially for the most vulnerable;

• Incorporate incentives for sustainable consumption and production into food systems;

• Promote fair and well-functioning agricultural and food markets;

• Reduce risk and increase the resilience of the most vulnerable; and

• Invest public resources in essential public goods, including innovation and infrastructure.

1.1. 1.1.1. Economic and financial crisis (2006-2008)Small import-dependent countries, especially in Africa, were deeply affected by the food and economic crises. Some large countries were able to insulate themselves from the crisis through restrictive trade policies and functioning safety nets, but trade insulation increased prices and volatility on international markets. High and volatile food prices are likely to continue. Demand from consumers in rapidly growing economies will increase, population continues to grow, and any further growth in biofuels will place additional demands on the food system. On the supply side, there are challenges due to increasingly scarce natural resources in some regions, as well as declining rates of yield growth for some commodities. Food price volatility may increase due to stronger ulinkages between agricultural and energy markets, as well as an increased frequency of weather shocks (FAO, 2011a).

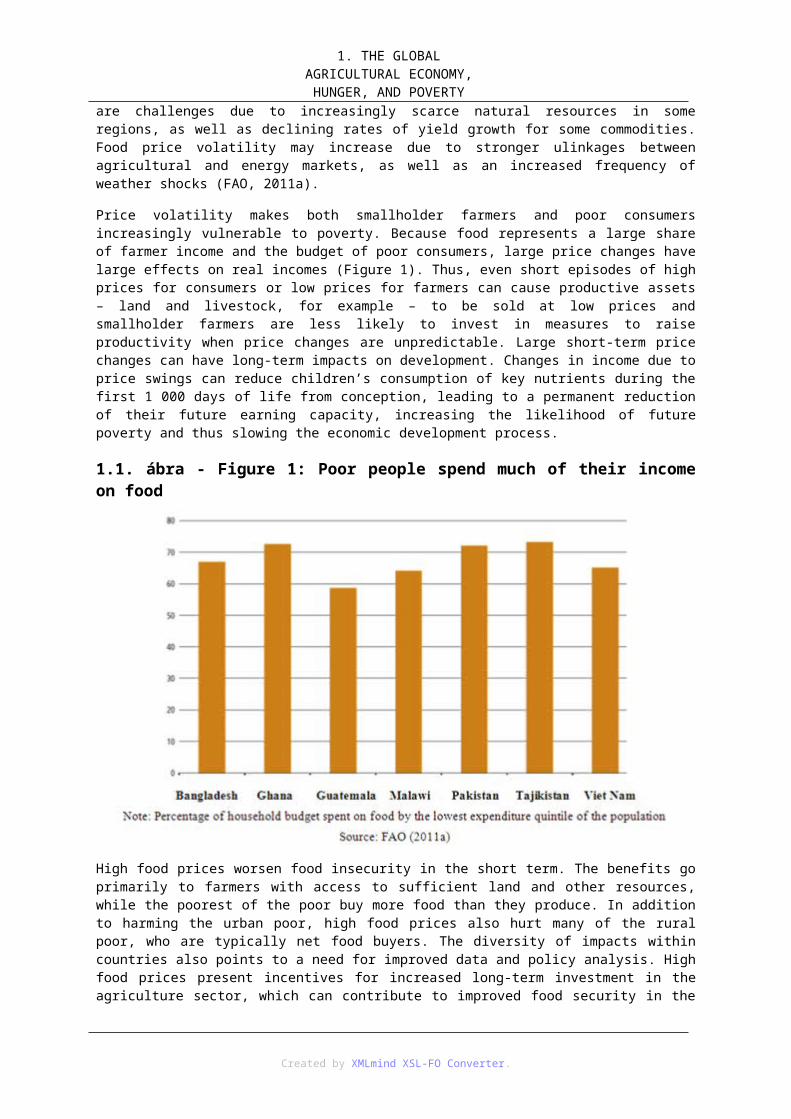

Price volatility makes both smallholder farmers and poor consumers increasingly vulnerable to poverty. Because food represents a large share of farmer income and the budget of poor consumers, large price changes have large effects on real incomes (Figure 1). Thus, even short episodes of high prices for consumers or low prices for farmers can cause productive assets – land and livestock, for example – to be sold at low prices and smallholder farmers are less likely to invest in measures to raise productivity when price changes are unpredictable. Large short-term price changes can have long-term impacts on development. Changes in income due to price swings can reduce children’s consumption of key nutrients during the first 1 000 days of life from conception, leading to a permanent reduction of their future earning capacity, increasing the likelihood of future poverty and thus slowing the economic development process.

1.1. ábra - Figure 1: Poor people spend much of their income on food

High food prices worsen food insecurity in the short term. The benefits go primarily to farmers with access to sufficient land and other resources, while the poorest of the poor buy more food than they produce. In addition

Created by XMLmind XSL-FO Converter.

1. THE GLOBAL AGRICULTURAL ECONOMY,

HUNGER, AND POVERTYto harming the urban poor, high food prices also hurt many of the rural poor, who are typically net food buyers. The diversity of impacts within countries also points to a need for improved data and policy analysis. High food prices present incentives for increased long-term investment in the agriculture sector, which can contribute to improved food security in the longer term.

Domestic food prices increased substantially in most countries during the 2006-08 world food crisis at both retail and farm gate levels. Despite higher fertilizer prices, this led to a strong supply response in many countries. It is essential to build upon this short-term supply response with increased investment in agriculture, including initiatives that target smallholder farmers and help them to access markets, such as Purchase for Progress (P4P). Safety nets are crucial for alleviating food insecurity in the short term, as well as for providing a foundation for long-term development. In order to be effective at reducing the negative consequences of price volatility, targeted safety-net mechanisms must be designed in advance and in consultation with the most vulnerable people (FAO, 2011a).

1.2. 1.1.2. Food-security strategyA food-security strategy that relies on a combination of increased productivity in agriculture, greater policy predictability and general openness to trade will be more effective than other strategies. Restrictive trade policies can protect domestic prices from world market volatility, but these policies can also result in increased domestic price volatility as a result of domestic supply shocks, especially if government policies are unpredictable and erratic. Government policies that are more predictable and that promote participation by the private sector in trade will generally decrease price volatility.

Investment in agriculture remains critical to sustainable long-term food security. Such investment will improve the competitiveness of domestic production, increase farmers’ profits and make food more affordable for the poor. For example, cost-effective irrigation and improved practices and seeds developed through agricultural research can reduce the production risks facing farmers, especially smallholders, and reduce price volatility. Private investment will form the bulk of the needed investment, but public investment has a catalytic role to play in supplying public goods that the private sector will not provide. These investments should consider the rights of existing users of land and related natural resources, benefit local communities, promote food security and not cause undue harm to the environment

The world is again experiencing a bout of heightened and prolonged price volatility in global food markets. Historically, occurrences are rare and each time they transpire, the world’s attention is temporarily galvanized, but concerted follow-up action has always fallen short of momentary expectations. The failure to prevent history from repeating itself is troubling, particularly when contrasted against other global systems that come under threat. When, for instance, financial crises take hold, the depth, breadth and rapidity of a coordinated response by the world’s leaders in marshalling resources to remedy imbalances demonstrates that global action is possible. When the world food order falters and millions forego food security, however, the resolve of global leadership fails. The impasse on inaction must be broken. Shielding food security against the threat of more frequent bouts of turmoil in global food markets must now be put at the top of the political and economic agenda (FAO, 2011b).

Much rests on the concept of “global governance” – building consensus on optimal policy choice and enhancing policy coordination. Global governance has important implications for shaping a more stable market environment; for instilling greater confidence, predictability and assurance in the international arena; for guaranteeing access to food for low-income countries and for better equipping governments to deal with the challenges ahead. But governance has a role within geographical boundaries. There are a host of initiatives that countries at risk can promote. These are principally directed towards building resilience and lowering vulnerability through investing in productivity for a diversified set of crops supported by incentive frameworks, instilling greater efficiency in domestic food systems and protecting those most at risk through safety nets. Enacting such measures will not only address the root cause of vulnerability, namely poverty, but would constitute a major step towards tackling the problem of hunger and malnutrition that still afflicts almost one billion people in the world today (FAO, 2011b).

1.3. 1.1.3. External shocks in addition to demand and supply fundamentalsThe seeds of crisis sown in past events change little, for instance the 1974 crisis and the 2006 – 08 turmoil, but time and again, policy-makers and the multilateral agencies have failed to prevent history from repeating itself.

Created by XMLmind XSL-FO Converter.

1. THE GLOBAL AGRICULTURAL ECONOMY,

HUNGER, AND POVERTYBy assuming world prices as a reference for measuring economic efficiency, trade liberalization would enhance resource allocation through exploiting comparative advantage. This increased reliance on markets was also concomitant to a progressive withdrawal of the state and intervention schemes from the food and agriculture sector, on the grounds that the private sector was more efficient from an economic point of view. Against these trends, public and private sectors in both developed and developing countries saw a limited need to invest in agricultural production and infrastructure, as food imports appeared an efficient way of achieving food security. Such perceptions, though, were radically changed when in 2006 prices of most internationally traded foodstuffs began to soar.

Episodes of extreme volatility are a major threat to food security in developing countries. Typically, low-income food-importing countries that are dependent on foreign aid and are characterized by high levels of foreign debt are the most vulnerable to positive food price shocks. The detrimental impact of rising volatility on these economies rests on their structural disposition: poor infrastructure, poor supply response, incomplete markets, weak capacity to import, sovereign risk, dependence on a single dominant staple, and susceptibility to climatic disturbances. Rising volatility can, in countries falling under this typology, increase the incidence of poverty, as well as putting a strain on government expenditure and borrowing, thus worsening debt sustainability. The deterioration of the terms-of-trade may destabilize the economy, thus impeding economic growth.

Beyond the uncertainty driven by environmental factors, including a changing climate and land degradation, the trajectory of the global food system is no longer determined by the resolution of demand and supply fundamentals. External shocks are emerging from a complexity of sources and are having a profound influence in shaping the agricultural landscape. Many of these shocks transcend international borders, spilling over from other sectors, and have the potential to amplify and perpetuate volatility. Their complexity compounds uncertainty, and is driving vulnerability in food systems. In this vein, there is a strong case that volatility is both a cause and consequence of vulnerability. The argument is framed in the context of both the resilience and response of food systems to shocks.

The growing exposure of vulnerable countries to bouts of market volatility is a challenge to all, and beckons the question of what policies governments should pursue to cope with an increasingly unpredictable environment, especially in the longer term. Authorities, including marketing boards in vulnerable food deficit nations, have attempted to intervene, but in most instances, budgetary constraints and the sheer scale of price increases have precluded any meaningful success at stabilization. Accordingly, interventions have been short-term, limited to the micro-level such as targeted consumer subsidies and safety nets and also to policies at the border, such as lowering tariffs and restraining exports. However, such policy cannot control the actions of myriads of private agents that are a feature of all food markets. Moreover, speculators can normally counteract the actions of all but the most well financed intervention activities.

An important “new reality” of the global food system that has sparked considerable controversy and debate, often polarized, concerns the influence of commodity speculation on food prices. On one side, it is recognized that speculation is crucial to the proper functioning of markets, there is strong conviction that unlimited speculation is not. The central argument here is that once speculation becomes “excessive” – to the point that the marginal benefit of the liquidity that speculators provide exceeds the marginal cost of the damage that they do to the price discovery function – there is need for intervention. As the prices broadcast from the major commodity exchanges reverberate around the world and affect billions of lives, a serious and more directed inquiry into the trading on the international commodity futures markets should commence.

World Trade Organization rules and disciplines are much less effective in situations of high world market price than they are in cases of depressed prices. This asymmetry is largely a consequence of the original objective of this system that aimed at disciplining situations leading to depressed prices in world markets adversely affecting exports. Thus, domestic and export subsidies, as well as import barriers, have been the target for reform, while policies that have the opposite effect (such as export taxes and prohibitions) have been largely tolerated. But the extent to which the fundamentals of world food markets have changed, the multilateral rules must adjust accordingly to be able to address trade issues that arise when food is no longer cheap. This would also add to the credibility of the system and foster an environment conducive to more trade openness on the part of importing countries, to the extent the latter are assured that the world market is a reliable source of supply, both in periods of plenty and in periods of relative scarcity.

In addition, under the present aggregate minimum commitment of the Food Aid Convention, diverting food aid resources away from their prioritized use may seriously compromise the timely availability of resources for meeting pressing emergency needs as well as the needs of chronically food-insecure populations. The present Convention offers little room for providing any relief to countries facing difficulties from high food prices.

Created by XMLmind XSL-FO Converter.

1. THE GLOBAL AGRICULTURAL ECONOMY,

HUNGER, AND POVERTYMultilateral agencies have responded to past turmoil in both food and financial markets by establishing global safety-net schemes with the objective of assisting countries in financing food imports. These schemes have been valuable, but they were set up as crisis response measures and for a limited duration. As high and volatile prices look likely to continue, what is now required is a longer-term response, with emphasis on established market mechanisms.

One approach, reliant on the purchase of call options, provides a promising way forward. This approach would enable vulnerable food importing countries to limit the impact of volatility in world food prices on their domestic markets and could be integrated with national food security structures. It would constitute a natural extension of trade-based policies recently advocated by multilateral donors. A structure through which multilateral agencies would intermediate optionality, such that costs and ownership remained with the countries themselves, would be appropriate. Taken together with an agreement to limit the use of restrictions on food exports, the market-based approach can re-establish food security on a trade basis and obviate the need for costly national food stockpiles.

The complexity of the new marketplace has placed exceptional demands on accurate and timely information on commodity developments and on the external drivers which influence market outcomes. It is argued that among the root causes of recent price volatility was the lack of reliable and up-to-date information on crop supply and demand and export availability. The problem is widespread. Despite the increase in the volume of raw data and the greater speed of transmitting information over recent years, the capacity to analyse the mass of often conflicting and variable-quality data and to disseminate the resulting analyses has not kept pace, particularly in the public, free-access sector. Furthermore, at the national level, the capacity of many countries to collect and process basic agricultural data has often deteriorated, and public statistical services have difficulties undertaking such forward-looking exercises as crop forecasts, let alone comprehensive supply/demand analyses and trade forecasts.

Another issue that requires urgent addressing concerns biofuels, especially those derived from food staple crops. Expansion of biofuels that is unpredicted, or so rapid that it outpaces the ability of the economy to accommodate it, reduces carryover stocks of grains and oilseeds, raises food price levels and increases the threat of further price spikes in response to any unforeseen short-run disturbance. If, as is likely, these policies are maintained and even expanded, their worst effects might be mitigated by food security call option agreements. If designed carefully and implemented before a new, possibly much more serious, food price spike occurs, such contracts could facilitate a diversion of commodities away from energy use to maintain the consumption of vulnerable populations during times of scarcity. They might also help to reduce pressure on global prices when undertaken by wealthier countries with significant food or feed-based biofuels industries and thus mitigate price hikes. Prudent humanitarian food policy would seek to mitigate the effects of such spikes to the well-being of poor grain consumers in affected developing countries, whether exporters or importers. “Diversion option contracts”, triggered at a certain price level for grains used as biofuel feed stocks could be part of such a policy.

1.4. 1.1.4. A way forwardWhen global systems fail, it is improbable that the actions of individuals alone will provide the necessary resolve. A coherent and effective system of governance of food security at both national and international levels is warranted. Global governance is concerned with reaching consensus in optimal policy choices and policy coordination. Global governance has important implications for shaping a more stable market environment; for instilling greater confidence, predictability and assurance in markets; for guaranteeing access to food by low-income food-deficit countries and for better equipping governments to the challenges that lie in the wake.

Market signals have to be strengthened for global price discovery: Commodity investment in organized exchanges has emerged as an integral part of the global food system. As an asset class, commodities that are key to food security, may be vulnerable to the behavioural dimensions of investors, whom on average as reflected by market outcomes, do not always fulfil rationality. Trading that pays little regard to market “fundamentals” can distort signals arising from these exchanges. Therefore, a challenge is how to enhance the price discovery function of international commodity exchanges. Clearly, trading behaviour that gives rise to excessive volatility does not contribute to this function.

An improved public global surveillance system on export availabilities and import demands would help temper uncertainty in organized markets that play a role in global price discovery. It would also enable countries to equip themselves better before the full impacts of crises transpire.

At the national level, there is no single catchall solution for framing optimal policy design, for there exists

Created by XMLmind XSL-FO Converter.

1. THE GLOBAL AGRICULTURAL ECONOMY,

HUNGER, AND POVERTYsubstantial heterogeneity among countries in terms of their stage of economic development, dietary patterns, in agri-climatology, in geography (e.g. proximity to seaports) and net-trade statuses. Even within countries, the proportion of the population who are landless, the urban-rural composition of the population and expected changes to the ratio over time will also have an important influence on policy design.

1.5. 1.1.5. World market volatility challenges facing poor net food-importing countriesAround 75% of the poor live in rural areas and many depend on agriculture for their livelihoods. They eke out a living on farms of often less than two hectares, work as small entrepreneurs or earn low wages in the agriculture-related processing, storage, seed or feedstuffs sectors. They are poor because they rely on too few and too unproductive assets. A profound and prolonged lack of investment in agriculture has restrained the overall productivity of the sector, sometimes to the extent that it no longer stands as a viable base for poverty reduction. A lack of investment has also reduced the ability of farmers to cope with price volatility. Moreover, the cyclical tendency of investment flows appears to have pronounced price peaks and troughs.

Since the late 1990s the world has entered a period of tight food supplies, higher prices and increased price volatility. These trends adversely affect the capacity of food import-dependent countries to access supplies. Poor households in these countries which already spend much of their income on food and have limited coping mechanisms at their disposal, suffer in the process. These developments are related, in part, to the implementation of reforms agreed under the Uruguay Round that came into effect in 1995, which resulted in a reduction of structural surpluses and a strengthening of world agricultural and food prices. Also as anticipated, other forms of food assistance made available in the past, such as subsidized exports and food aid, declined drastically in recent years. At the same time the world food market has been dramatically affected by factors external to agriculture, including energy prices and speculative activity from the financial sector, as well as unilateral export restrictions put in place by some countries.

1.6. 1.1.6. Characteristics of food insecurity in net food importing countriesThe average supply of calories and protein in the Least Developed Countries (LDCs) and Net-Food Importing Developing Countries (NFIDCs) is well below and much more variable than the aggregate for developing countries. Gains in the past half century have been modest. Considering also the often very unequal distribution of available supplies within countries, these trends are indicative of their food security vulnerability. A manifestation of the precariousness of the food security situation in these countries is the frequency of being in need of external assistance in response to food emergencies, with some of them permanently in that state. Their growing demand for basic foodstuffs continues to be met by domestic supplies and growing import volumes. In the case of cereals, self-sufficiency ratios are hovering around 90% and 70%, for LDCs and NFIDCs respectively (Konandreas, 2012).

While NFIDCs have generally kept the pace of other developing countries in increasing productivity, LDCs achieved only modest gains. Cereal yields in LDCs are only half of those attained by developing countries and one-third of those achieved by developed countries. Much of the increase in output has come from area expansion. Cereals comprise the largest item in the food import basket accounting for some 42% and 40% of the value of food imports of LDCs and NFIDCs, respectively, followed by oils and fats and sugar. Together these three commodity groups account for over three-quarters of the value of food items imported by LDCs and over two-thirds for the NFIDCs. The share of food aid in their total cereal imports has declined sharply, from close to 30% in the beginning of the 1990s for the LDCs (8% for the NFIDCs), to about 8 percent in the last 3 years (less than 0.5% for the NFIDCs).

The increase in the cost of cereal imports has been much more affected by price increases rather than volumes imported in recent years. Thus, for LDCs while the aggregate volume of commercial cereal imports increased by less than three times during 1990-2010, their cereal import bill increased by over six times during the same period. Similar sharp increases in the cereal import bill have been experienced by the NFIDCs, with a volume increase by about 70% and a cereal import bill nearly quadrupling (therefore rising by some 300%). For both LDCs and NFIDCs, there is considerable variation between countries, and for some, all the increase in their cereal import bill was due to price. The escalating burden of food imports, necessary to meet immediate consumption, represents a serious threat for the economies of most LDCs and NFIDCs. The share of food imports to total merchandize exports is very high even under normal years, especially for the LDCs, and

Created by XMLmind XSL-FO Converter.

1. THE GLOBAL AGRICULTURAL ECONOMY,

HUNGER, AND POVERTYskyrockets for some countries during price spikes. The imperative of importing food often comes at the expense of other imports including capital goods necessary for long-term development (Konandreas, 2012).

1.7. 1.1.7. What can LDCs and NFIDCs do for themselves?Lowering or eliminating import tariffs is the most common measure that governments take to cushion the impact on domestic prices of imported goods when world market prices rise. However, this option is severely limited when applied tariffs are already low as is generally the case in many poor countries and even their elimination is a small relief when import prices shoot up by several multiples of prevailing tariff levels.

1.8. 1.1.8. Avoiding export prohibitions and restrictionsWhile export restraints are seemingly politically attractive in the short term, they are a blunt instrument. By aggravating further world market prices they shift the burden of an even greater adjustment to other countries. There are always much more attractive approaches to address the needs of vulnerable domestic consumers than imposing export prohibitions/restrictions, which are also less costly in the longer term. Also, to the extent that the country is a regular exporter of food commodities, it risks losing markets if it turns on and off exports unilaterally. Net food importing countries should be enthusiastic proponents of approaches in strengthening WTO rules on export prohibitions and restrictions.

1.9. 1.1.9. Stockholding and domestic food assistanceBuilding modest stocks has been a very common response to market instability and, although often an expensive undertaking, their appeal is clear from the point of view of vulnerable countries to offer some degree of protection against domestic and external shocks. In general, there are no effective limitations from the WTO Agreement on Agriculture (AoA) for public stockholding for food security purposes as long as these form an integral part of a food security programme identified in national legislation. The same applies to domestic food aid under clearly-defined eligibility criteria related to nutritional objectives. The limitations arise from cost considerations and clear rules for accumulation and release of such stocks are essential.

1.10. 1.1.10. Reducing the high transaction costs for intra-regional tradeWeak market integration in regions where the majority of net food-importing countries are located tends to result in higher food prices, adding to their vulnerability. Some relief can be obtained by reducing transaction costs, which is an important mitigating factor in containing price increases and price volatility. Transactions costs can be curbed through improvements to physical infrastructure (e.g. roads) but also through a facilitation of regional transport and transit formalities, simplification of cross-border regulations and cracking down on petty corruption, which is highly detrimental to food security.

1.11. 1.1.11. Using AoA flexibility to invest in food production and resilienceIn general the AoA disciplines are not constraining poor countries in investing in agriculture, even with production and trade distorting policies. The policy mix that individual countries may use would depend on their specific circumstances but one policy that has proven very effective in achieving rapid increases in output is targeted investment assistance to farmers and “smart” input subsidies to resource poor farmers.

1.12. 1.1.12. How can the international community help?Among the measures to assist net food-importing countries to deal with escalating food import bills. These include: food aid; export credits; compensatory financing; and assistance to increase agricultural productivity and infrastructure.

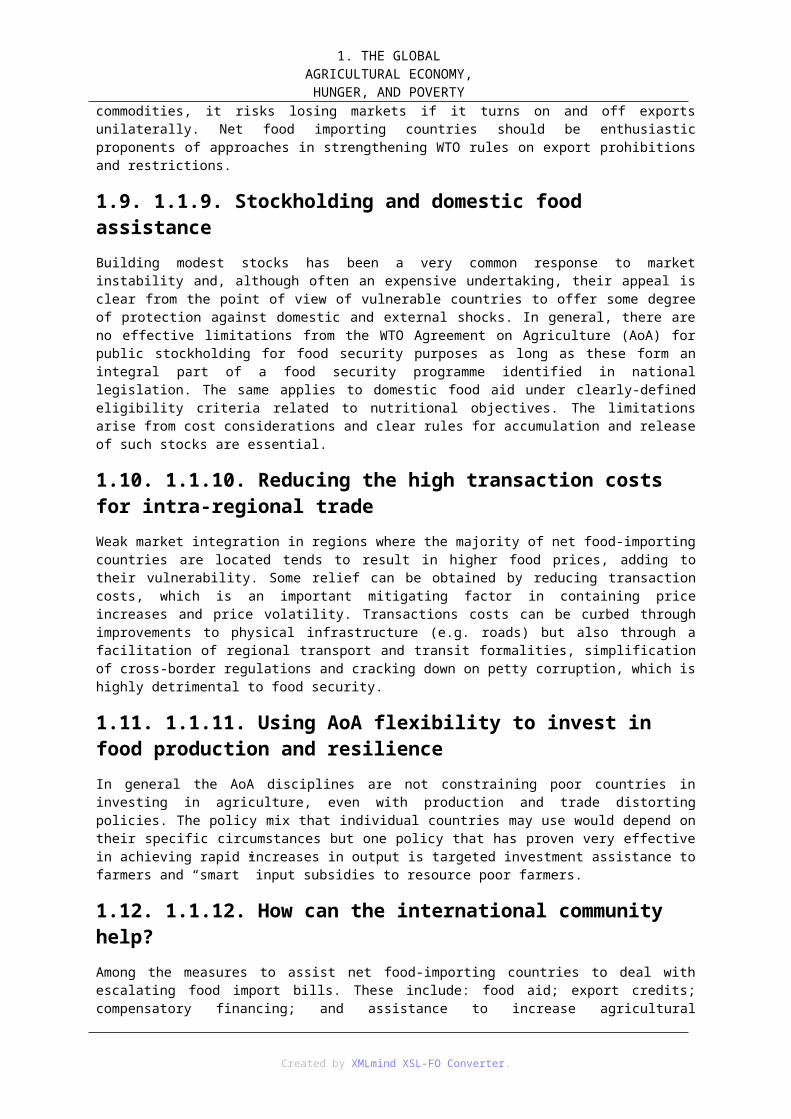

2. 1.2. Limiting the role of food aid to emergency responses

Created by XMLmind XSL-FO Converter.

1. THE GLOBAL AGRICULTURAL ECONOMY,

HUNGER, AND POVERTYWhile food aid has been an important resource in the past to help countries with structural deficits, it now barely meets the requirements of growing emergency situations (Figure 2). Also the provision of food aid for budgetary support has been increasingly under scrutiny. Considering also the nutritional needs of poor households, especially in periods of scarcity, it would be prudent to limit the use of food aid to emergencies and nutritional support and, perhaps, broaden its scope by including essential agricultural inputs as part of the donors’ contributions under the Food Aid Convention (FAC).

1.2. ábra - Figure 2: Countries requiring external assistance for food (34 countries)

Source: FAO (2012b)

3. 1.3. Targeting export creditsThe record of officially supported export credits in providing assistance to liquidity-constrained countries to import food has not been very good. Only a very small share of such credits was given to poor net food importing countries and the concessionality element was minimal.

4. 1.4. Strengthening food financing facilitiesThe need for assistance in financing imports of basic foodstuffs is evident from the already heavy burden net food-importing countries endure even when import prices are normal. IMF and the World Bank facilities had been identified as most relevant in the context of the Marrakesh Decision, although their utility has been questioned by beneficiary countries for a number of reasons. A battery of new instruments has now been created by these institutions with improved conditions of access and necessary resources, reflecting the need to address increased vulnerabilities in poor countries in recent years.

5. 1.5. Increasing technical and financial assistance to boost productivityTargeting agricultural productivity reflects a genuine recognition of the fundamental causes of

vulnerability. The types of technical and financial assistance would have to be holistic by addressing constraints along the supply chain, including appropriate technologies, processing, storage and marketing of agricultural commodities. Reversing the past declining trends in Official Development Assistance (ODA) investment to agriculture can be instrumental in reducing vulnerability in poor net food importing countries.

6. Questions1. Sustainable future?

2. Food expenditure shares in percentage of per capita income?

3. Food crisis and financial crisis?

Created by XMLmind XSL-FO Converter.

1. THE GLOBAL AGRICULTURAL ECONOMY,

HUNGER, AND POVERTY4. Hunger and malnourishment?

5. Increase of agricultural output?

6. Characteristics of food insecurity in net food importing countries?

7. ReferencesFAO (1996): World Food Summit. 13-17 November 1996. Food and Agriculture Organization of the United Nations. Rome, 1996. http://www.fao.org/docrep/003/w3548e/w3548e00.htm

FAO (2011a): The State of Food Insecurity in the World. How does international price volatility affect domestic economies and food security? Food and Agriculture Organization of the United Nations. Rome, 2011. p. 50.

FAO (2011b): Safeguarding food security in volatile global markets. Edited by Adam Prakash. Food and Agriculture Organization of the United Nations, Rome, 2011. p. 594.

FAO (2012a): Towards the future we want. End hunger and make the transition to sustainable agricultural and food systems. Food and Agriculture Organization of the United Nations. Rome, 2012. p. 28.

FAO (2012b): Crop Prospects and Food Situation. Food and Agriculture Organization of the United Nations. No.1. March 2012. http://www.fao.org/giews/english/cpfs/index.htm

Konandreas, P. (2012): Trade policy responses to food price volatility in poor net food-importing countries. Issue Paper No. 42, 2012. Published by International Centre for Trade and Sustainable Development (ICTSD). p. 65, Geneva, Switzerland. http://ictsd.org/downloads/2012/06/trade-policy-responses-to-food-price-volatility-in-poor-net-food-importing-countries. pdf

Created by XMLmind XSL-FO Converter.

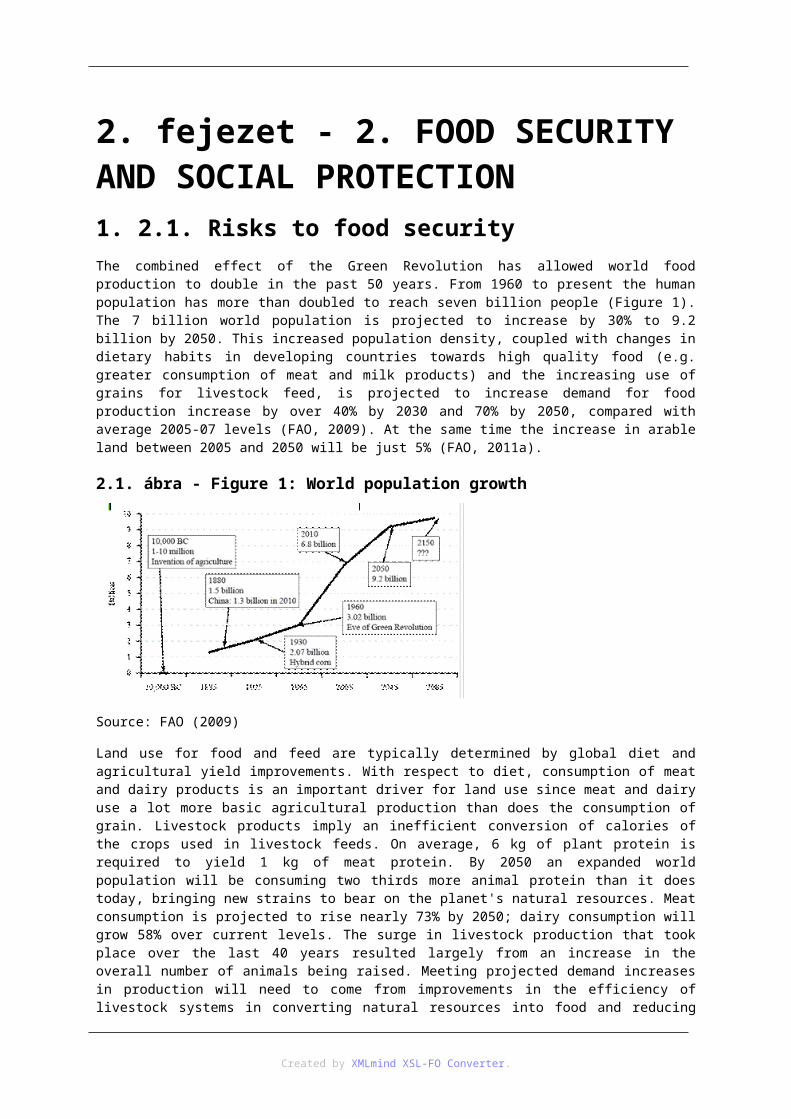

2. fejezet - 2. FOOD SECURITY AND SOCIAL PROTECTION1. 2.1. Risks to food securityThe combined effect of the Green Revolution has allowed world food production to double in the past 50 years. From 1960 to present the human population has more than doubled to reach seven billion people (Figure 1). The 7 billion world population is projected to increase by 30% to 9.2 billion by 2050. This increased population density, coupled with changes in dietary habits in developing countries towards high quality food (e.g. greater consumption of meat and milk products) and the increasing use of grains for livestock feed, is projected to increase demand for food production increase by over 40% by 2030 and 70% by 2050, compared with average 2005-07 levels (FAO, 2009). At the same time the increase in arable land between 2005 and 2050 will be just 5% (FAO, 2011a).

2.1. ábra - Figure 1: World population growth

Source: FAO (2009)

Land use for food and feed are typically determined by global diet and agricultural yield improvements. With respect to diet, consumption of meat and dairy products is an important driver for land use since meat and dairy use a lot more basic agricultural production than does the consumption of grain. Livestock products imply an inefficient conversion of calories of the crops used in livestock feeds. On average, 6 kg of plant protein is required to yield 1 kg of meat protein. By 2050 an expanded world population will be consuming two thirds more animal protein than it does today, bringing new strains to bear on the planet's natural resources. Meat consumption is projected to rise nearly 73% by 2050; dairy consumption will grow 58% over current levels. The surge in livestock production that took place over the last 40 years resulted largely from an increase in the overall number of animals being raised. Meeting projected demand increases in production will need to come from improvements in the efficiency of livestock systems in converting natural resources into food and reducing waste. This will require capital investment and a supporting policy and regulatory environment. Meat consumption in China alone increased from 27 to 60 kg per person per year between 1990 and 2010. Each additional kg of meat consumption increase in China results in a need for roughly 4-5 million tons of animal feed (FAO, 2011b).

Helping farmers lose less of their crops will be a key factor in promoting food security but even in the poorest countries those rural farmers aspire to more than self-sufficiency. The reduction of current yield losses caused by pests, pathogens and weeds are major challenges to agricultural production. Globally, an average of 35% of potential crop yield is lost to pre-harvest pests (Oerke, 2006). In addition to the pre-harvest losses transport, pre-processing, storage, processing, packaging, marketing and plate waste losses are relatively high. If there is going to be enough food at affordable prices for the global population, we may also have to change our food habits and decrease food waste.

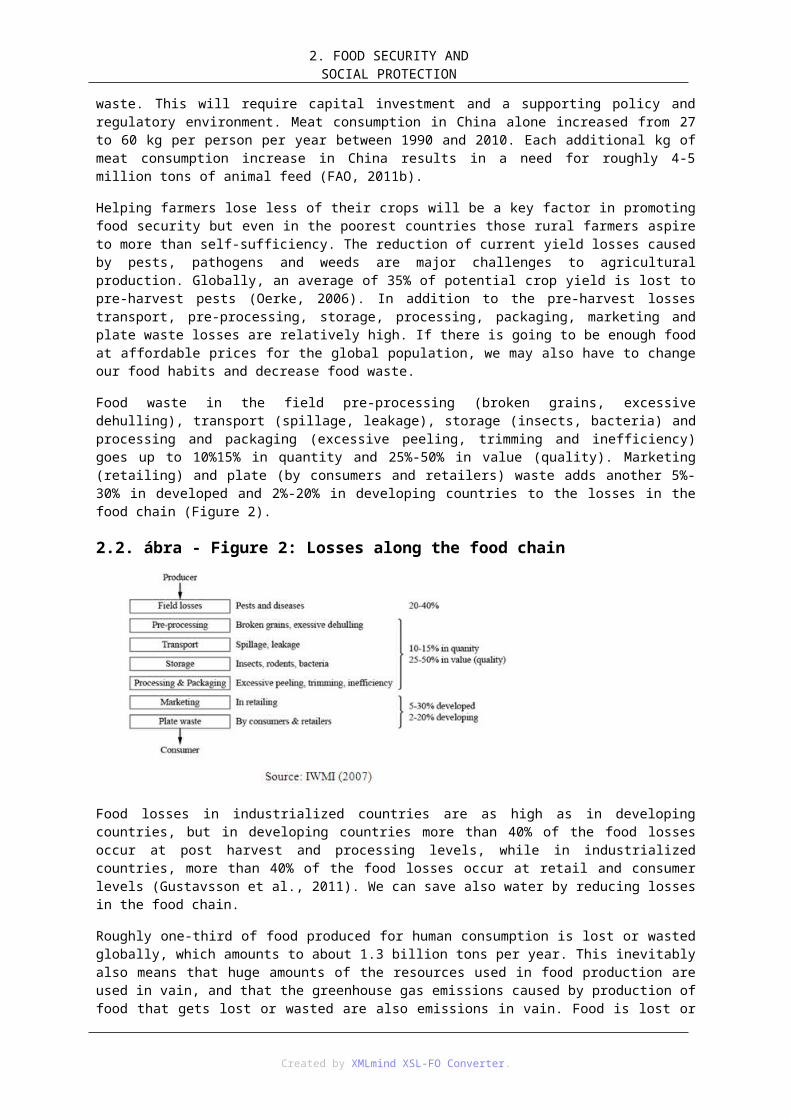

Food waste in the field pre-processing (broken grains, excessive dehulling), transport (spillage, leakage), storage (insects, bacteria) and processing and packaging (excessive peeling, trimming and inefficiency) goes up to

Created by XMLmind XSL-FO Converter.

2. FOOD SECURITY AND SOCIAL PROTECTION

10%15% in quantity and 25%-50% in value (quality). Marketing (retailing) and plate (by consumers and retailers) waste adds another 5%-30% in developed and 2%-20% in developing countries to the losses in the food chain (Figure 2).

2.2. ábra - Figure 2: Losses along the food chain

Food losses in industrialized countries are as high as in developing countries, but in developing countries more than 40% of the food losses occur at post harvest and processing levels, while in industrialized countries, more than 40% of the food losses occur at retail and consumer levels (Gustavsson et al., 2011). We can save also water by reducing losses in the food chain.

Roughly one-third of food produced for human consumption is lost or wasted globally, which amounts to about 1.3 billion tons per year. This inevitably also means that huge amounts of the resources used in food production are used in vain, and that the greenhouse gas emissions caused by production of food that gets lost or wasted are also emissions in vain. Food is lost or wasted throughout the supply chain, from initial agricultural production down to final household consumption. In medium- and high-income countries food is to a significant extent wasted at the consumption stage, meaning that it is discarded even if it is still suitable for human consumption (Gustavsson et al., 2011).

Significant losses also occur early in the food supply chains in the industrialized regions. In low-income countries food is lost mostly during the early and middle stages of the food supply chain; much less food is wasted at the consumer level. Overall, on a per-capita basis, much more food is wasted in the industrialized world than in developing countries. The per capita food waste by consumers in Europe and North-America is 95-115 kg/year, while this figure in Sub-Saharan Africa and South/Southeast Asia is only 6-11 kg/year (Gustavsson et al., 2011).

The causes of food losses and waste in low-income countries are mainly connected to financial, managerial and technical limitations in harvesting techniques, storage and cooling facilities in difficult climatic conditions, infrastructure, packaging and marketing systems. Given that many smallholder farmers in developing countries live on the margins of food insecurity, a reduction in food losses could have an immediate and significant impact on their livelihoods. The food supply chains in developing countries need to be strengthened by, inter alia, encouraging small farmers to organize and to diversify and upscale their production and marketing. Investments in infrastructure, transportation, food industries and packaging industries are also required. Both the public and private sectors have a role to play in achieving this.

The causes of food losses and waste in medium/high-income countries mainly relate to consumer behaviour as well as to a lack of coordination between different actors in the supply chain. Farmer-buyer sales agreements may contribute to quantities of farm crops being wasted. Food can be wasted due to quality standards, which reject food items not perfect in shape or appearance. At the consumer level, insufficient purchase planning and expiring “best-before-dates” also cause large amounts of waste, in combination with the careless attitude of those consumers who can afford to waste food. Food waste in industrialized countries can be reduced by raising awareness among food industries, retailers and consumers. There is a need to find good and beneficial use for safe food that is presently thrown away.

While increasing primary food production is paramount to meet the future increase in final demand, tensions

Created by XMLmind XSL-FO Converter.

2. FOOD SECURITY AND SOCIAL PROTECTION

between production and access to food can also be reduced by tapping into the potential to reduce food losses. Efficient solutions exist along the whole food chain, for reducing total amounts of food lost and wasted. Actions should not only be directed towards isolated parts of the chain, since what is done (or not done) in one part has effects in others. In low income countries, measures should foremost have a producer perspective, e.g. by improving harvest techniques, farmer education, storage facilities and cooling chains. In industrialized countries on the other hand, solutions at producer and industrial level would only be marginal if consumers continue to waste at current levels. Consumer households need to be informed and change the behaviour which causes the current high levels of food waste. Another point to be stressed is that the food supply chain of today is more and more globalized. Certain food items are produced, transformed and consumed in very different parts of the world. The impact of growing international trade on food losses still has to be better assessed.

2. 2.2. Competition for land and waterLand use change is not a new concept but is something that has been taking place since the beginning of civilization and continues to do so. In this context, agriculture has always been an important driver, so far mostly for food and feed production. A growing world population and a changing diet have led to continuously expanding areas of agricultural land, despite parallel increases in yields from existing cropland. In addition, cropland is lost due to erosion through chemical and physical degradation, which further increases the requirement for new agricultural land. On the other hand cultivated land is tightening due to population growth and accelerated urbanization and motorization1, changes in lifestyles, falling water tables and diversion of irrigated water towards the cities (Earth Institute, 2005).

The land surface of our planet is equal to 13.4 billion hectares of which 38% is given over to agriculture and 30% to forest (FAO, 2011a). The rest of the total is rounded out through a combination of man-made infrastructure, inland water systems, and land that is unsuited for agriculture and forestry (desert, rocks etc.). Of the 5 billion hectares of land used for agricultural purposes worldwide around one-third is suited to annual or permanent crops whereas just over two-thirds are allocated to permanent meadows or pasture. Just 1.6 billion hectares are used for crop production (arable land and land under permanent crops).

Over the last 50 years, land and water management has met rapidly rising demands for food and fibre. In particular, input-intensive, mechanized agriculture and irrigation have contributed to rapid increases in productivity. The world’s agricultural production has grown between 2.5 and 3 times over the period while the cultivated area has grown only by 12% as a result of two opposite trends: an increase of 227 million ha in developing countries, and a decline of 40 million ha in developed countries. More than 40% of the increase in food production came from irrigated areas, which have doubled in area over the same period, accounting for 15% of all arable land. In the same period, the cultivated area of land per person gradually declined from 0.45 to less than 0.23 ha indicating that the largest contribution to increases in agricultural output will most likely come from intensification of production on existing agricultural land (FAO, 2011c).