Reform. Perform. · PDF fileAdjustment of brought forward losses not to be denied to companies...

31

Highlights of Union Budget 2018 Reform. Perform. Transform. www.skpgroup.com/budget2018

Transcript of Reform. Perform. · PDF fileAdjustment of brought forward losses not to be denied to companies...

Highlights of Union Budget 2018

Reform. Perform. Transform.

www.skpgroup.com/budget2018

© 2

018

SKP

Bu

sin

ess

Co

nsu

ltin

g LL

P. A

ll ri

ghts

res

erve

d.

Winner of India Tax Firm of the Year 2016 at the Asia Tax Awards

Direct Tax Proposals

Indirect Tax Proposals

Coverage

203-02-2018

© 2

018

SKP

Bu

sin

ess

Co

nsu

ltin

g LL

P. A

ll ri

ghts

res

erve

d.

Direct Tax Proposals

303-02-2018

© 2

018

SKP

Bu

sin

ess

Co

nsu

ltin

g LL

P. A

ll ri

ghts

res

erve

d.

Winner of India Tax Firm of the Year 2016 at the Asia Tax Awards

Individuals No change in income-tax slabs and rates

No change in rate of surcharge

Standard Deduction of INR 40,000 introduced for salaried taxpayer in lieu of certain exemptions / allowances

Increased deductions for payment of medical insurance and expenditure on specified diseases for senior citizens

Interest earned by senior citizen on bank deposits to be exempt up to INR 50,000 (no deduction of INR 10,000 for interest

on savings account)

Corporates

No change in headline corporate tax rate of 30%

No change in rate of surcharge

Corporate tax rate of 25% to now also apply for companies with turnover or gross receipts of Financial Year

(FY) 2016-17 not exceeding INR 250 crores (approx USD 38.5mn)

Dividend Distribution Tax (DDT) of 30% on ‘deemed dividend’ in nature of advancing loan to shareholder or

associated enterprise

Education cess on tax and surcharge amount increased from 3% to 4% for all taxpayers and re-designated as

“Health and Education cess”

Tax Rates

403-02-2018

© 2

018

SKP

Bu

sin

ess

Co

nsu

ltin

g LL

P. A

ll ri

ghts

res

erve

d.

Winner of India Tax Firm of the Year 2016 at the Asia Tax Awards

Exemption for long-term capital gains (LTCG) on equity shares and equity mutual fund units withdrawn

Effective on gains earned on or after 1 April 2018

LTCG exceeding INR 1 lakh to be taxed @10%

Cost indexation benefit not available

Gains up to 31 January 2018 grandfathered

Applicable to all taxpayers (including Foreign Portfolio Investors [FPIs] / Foreign Institutional Investors [FIIs])

Equity-oriented mutual fund to pay dividend distribution tax (DDT) at 10%

Definition of ‘deemed dividend’ amended

Accumulated reserves of amalgamating company on date of amalgamation to be considered for computing DDT –effective from 1 April 2017 onwards

Compensation received by a business taxpayer on termination/modification in terms of contract to be taxable as business income

Compensation received on termination/modification in terms of employment to be taxable as income from other sources

Widening and Deepening of Tax Base

503-02-2018

© 2

018

SKP

Bu

sin

ess

Co

nsu

ltin

g LL

P. A

ll ri

ghts

res

erve

d.

Winner of India Tax Firm of the Year 2016 at the Asia Tax Awards

Definition of ‘Business Connection’ (similar to concept of Dependent Agent PE under tax treaties) widened:

Amendments in line with BEPS Multilateral Instrument to which Indian is a signatory

Added condition of agent in India habitually playing principal role leading to conclusion of contracts

Concept of ‘Significant Economic Presence’ introduced in Business Connection:

Focus is on taxing non-resident business which do not have any physical presence in India but use digital means to earn income from India such as:

Provision of download of data or software for specified amounts

Systematic and continuous soliciting of business or engaging in interaction with specified number of users

Rules and conditions to be prescribed by the Government after consultation with stakeholders

Clarified that in absence of amendment in definition of PE under tax treaties, the taxation of profits will continue to be governed by definition of PE under the tax treaties

Concept of Business Connection Widened

603-02-2018

© 2

018

SKP

Bu

sin

ess

Co

nsu

ltin

g LL

P. A

ll ri

ghts

res

erve

d.

Winner of India Tax Firm of the Year 2016 at the Asia Tax Awards

Conditions for availing tax holiday by start-ups relaxed

Gains/loss of non-resident from transfer of bonds/GDR/derivative in IFSC to be exempt from capital gains tax if consideration paid in foreign currency

Alternate Minimum Tax (AMT) on non-corporate units in IFSC reduced from 18.5% to 9%

Conditions for obtaining additional deduction of 30% on emoluments paid to new employees relaxed

Trading in agricultural commodity derivatives not to be treated as ‘speculative business’

5 year 100% tax holiday introduced for Farm Producer Companies with turnover less than INR 100 crore

Incentives

703-02-2018

© 2

018

SKP

Bu

sin

ess

Co

nsu

ltin

g LL

P. A

ll ri

ghts

res

erve

d.

Winner of India Tax Firm of the Year 2016 at the Asia Tax Awards

MAT provisions rationalized for companies under insolvency proceedings process

Aggregate of unabsorbed depreciation and loss brought forward to be allowed to be reduced from book profit

Adjustment of brought forward losses not to be denied to companies under insolvency proceedings process due to change in 51% shareholding

An opportunity of hearing to however be provided to the tax authorities

Tax return of companies under insolvency proceedings process to be signed by appointed insolvency professional

Facilitating Insolvency Resolution

803-02-2018

© 2

018

SKP

Bu

sin

ess

Co

nsu

ltin

g LL

P. A

ll ri

ghts

res

erve

d.

Winner of India Tax Firm of the Year 2016 at the Asia Tax Awards

MAT not to apply to foreign companies offering following income on presumptive basis:

Shipping

Exploration of mineral oils and natural gas

Aircrafts

Turnkey power projects

Amendment made retrospectively applicable from 1 April 2000

Tax holidays under various sections to be denied if tax return not filed on time

Sale value of immovable property to be accepted if variation from stamp duty value not more than 5%

No adjustment to returned income on account of difference in tax credit statements

Transfer of capital assets between holding company and wholly owned subsidiary to be tax exempt even under gift tax provisions

Foundation laid for prescribing extensive procedure for e-assessment proceedings

Rationalisation Measures

903-02-2018

© 2

018

SKP

Bu

sin

ess

Co

nsu

ltin

g LL

P. A

ll ri

ghts

res

erve

d.

Winner of India Tax Firm of the Year 2016 at the Asia Tax Awards

ICDS, introduced with effect from 1 April 2016, provided for making certain adjustments to taxable income irrespective of accounting treatment provided in books

Constitutional validity of ICDS was upheld by Delhi High Court but various provisions were struck down as outside the scope of the law as laid down by several Supreme Court rulings

Various provisions struck down by the Delhi High Court are now incorporated in the law

ICDS kept applicable from 1 April 2017 itself - compliance to be undertaken if not done already

Income Computation and Disclosure Standards (ICDS)

1003-02-2018

© 2

018

SKP

Bu

sin

ess

Co

nsu

ltin

g LL

P. A

ll ri

ghts

res

erve

d.

Winner of India Tax Firm of the Year 2016 at the Asia Tax Awards

Country-by-Country Report (CbCR) provisions rationalised

Timeline for furnishing CbCR for FY 2017-18 extended from 9 months to 12 months i.e. 31 March 2019

No change in due date for furnishing Master File

Additional obligation on Indian entity

No CbCR rules in country of parent entity still Indian entity will have to prepare and furnish CbCR in India

Transfer Pricing

1103-02-2018

© 2

018

SKP

Bu

sin

ess

Co

nsu

ltin

g LL

P. A

ll ri

ghts

res

erve

d.

Winner of India Tax Firm of the Year 2016 at the Asia Tax Awards

Provisions clarified for taxation of stock-in-trade converted to capital asset

Penalties for non-compliance with reporting of financial transaction/reportable account (FATCA/CRS) increased

Orders levied against professionals for inaccurate reports/certificates can be appealed before the Income Tax Appellate Tribunal

Others

1203-02-2018

© 2

018

SKP

Bu

sin

ess

Co

nsu

ltin

g LL

P. A

ll ri

ghts

res

erve

d.

Indirect Tax Proposals

1303-02-2018

© 2

018

SKP

Bu

sin

ess

Co

nsu

ltin

g LL

P. A

ll ri

ghts

res

erve

d.

Winner of India Tax Firm of the Year 2016 at the Asia Tax Awards

First Budget post introduction of GST

Excise and Service tax already subsumed under GST

Proposals in the Union Budget 2018 limited to Customs duty as GST Council empowered with making changes in the GST legislation

Central Board of Excise and Customs (CBEC) to be renamed as Central Board of Indirect Taxes and Customs (CBIC)

Overview

1403-02-2018

© 2

018

SKP

Bu

sin

ess

Co

nsu

ltin

g LL

P. A

ll ri

ghts

res

erve

d.

1503-02-2018

Goods and Services Tax (GST) Implications of Proposed Union Budget 2018 and 25 GST Council Meet

© 2

018

SKP

Bu

sin

ess

Co

nsu

ltin

g LL

P. A

ll ri

ghts

res

erve

d.

Winner of India Tax Firm of the Year 2016 at the Asia Tax Awards

Legislative Updates | Tax Rate Changes

1603-02-2018

Rates reduced on number of goods and services – w.e.f. 25 Jan 2018

Rates increased on cigarette filter rods and rice bran

Royalty/IPR on which Customs duty is applicable exempted from GST

Goods Services

• Sale of old and used motor cars• Specified goods of agricultural sector• Household items such as LPG cylinders

• Construction of metro and monorail projects• Common effluent treatment plant services

© 2

018

SKP

Bu

sin

ess

Co

nsu

ltin

g LL

P. A

ll ri

ghts

res

erve

d.

Winner of India Tax Firm of the Year 2016 at the Asia Tax Awards

Legislative Updates | Other Changes

1703-02-2018

Changes effective 25 January 2018

Deferment of GST on Transferrable Development Rights (TDR) until possession or right in the property is transferred to the land owner

Exempt supplies to not include exempt interest or discount earned on value of deposits, loans or advances (except in case of banking company and financial institution including NBFCs)

Clarity on taxability of certain goods/services

Supplies to Indian Railways shall be at applicable GST rates of the products

Services by doctors/consultants/technicians hired by hospitals to be treated as not liable to tax (tribunal decision in case of Apollo Hospitals)

© 2

018

SKP

Bu

sin

ess

Co

nsu

ltin

g LL

P. A

ll ri

ghts

res

erve

d.

Winner of India Tax Firm of the Year 2016 at the Asia Tax Awards

Changes effective 23 Jan 2018

Relaxation in registration provisions – by removing 1 year time limit for cancellation

Penalties on delayed returns reduced

Extension of due date to file ISD returns

Clarity awaited on requirement to file mismatch returns

Procedural and Administrative Updates

1803-02-2018

© 2

018

SKP

Bu

sin

ess

Co

nsu

ltin

g LL

P. A

ll ri

ghts

res

erve

d.

Winner of India Tax Firm of the Year 2016 at the Asia Tax Awards

Mandatory implementation of E-way bills from 1 Feb 2018 for all inter-state transactions

States have time to implement e-way bill for intra-state transactions up to 31 May 2017

W.e.f. 1 June 2018 mandatory implementation of e-way bills for all intra-state transaction

Common e-way bill portal notified - www.ewaybill.gst.gov.in

E-way bills generated on common portal will be valid in all states for transportation

GSTN to capture data for returns from e-way bill portal

Provisions to carry out implementation and regulation of e-way bills in place

However, clarity on various practical aspects such as extension of validity of e-ways – still emerging

Update on E- Way Bills

1903-02-2018

© 2

018

SKP

Bu

sin

ess

Co

nsu

ltin

g LL

P. A

ll ri

ghts

res

erve

d.

Customs

2003-02-2018

© 2

018

SKP

Bu

sin

ess

Co

nsu

ltin

g LL

P. A

ll ri

ghts

res

erve

d.

Winner of India Tax Firm of the Year 2016 at the Asia Tax Awards

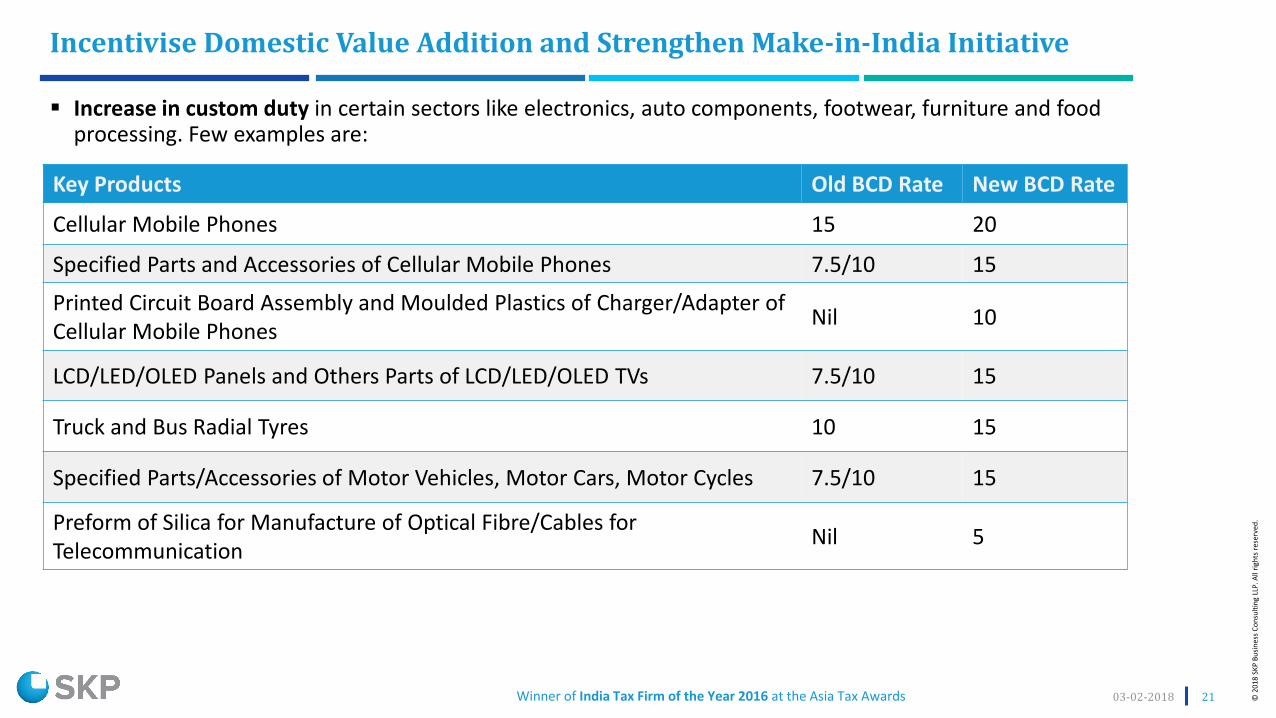

Key Products Old BCD Rate New BCD Rate

Cellular Mobile Phones 15 20

Specified Parts and Accessories of Cellular Mobile Phones 7.5/10 15

Printed Circuit Board Assembly and Moulded Plastics of Charger/Adapter of Cellular Mobile Phones

Nil 10

LCD/LED/OLED Panels and Others Parts of LCD/LED/OLED TVs 7.5/10 15

Truck and Bus Radial Tyres 10 15

Specified Parts/Accessories of Motor Vehicles, Motor Cars, Motor Cycles 7.5/10 15

Preform of Silica for Manufacture of Optical Fibre/Cables for Telecommunication

Nil 5

Incentivise Domestic Value Addition and Strengthen Make-in-India Initiative

2103-02-2018

Increase in custom duty in certain sectors like electronics, auto components, footwear, furniture and food processing. Few examples are:

© 2

018

SKP

Bu

sin

ess

Co

nsu

ltin

g LL

P. A

ll ri

ghts

res

erve

d.

Winner of India Tax Firm of the Year 2016 at the Asia Tax Awards

To be effective from 2 February 2018

Social Welfare Surcharge introduced to provide and finance education, health and social security

*exemption provided from levy of SWS on IGST and GST Compensation Cess

Introduction of Social Welfare Surcharge (SWS)

2203-02-2018

Tariff Heading Goods Rate

Any Chapter All imported goods (Except certain Exemptions)10% of aggregate

duties of customs*

2710, 7106, 7108

Motor Spirit, Sliver and Gold3% of aggregate

duties of customs

Any ChapterSpecified Goods which were exempted from Customs Education and Secondary and Higher Education Cess

Exempted

© 2

018

SKP

Bu

sin

ess

Co

nsu

ltin

g LL

P. A

ll ri

ghts

res

erve

d.

Winner of India Tax Firm of the Year 2016 at the Asia Tax Awards

Ease of Doing Business and Digitalisation

2303-02-2018

To be effective from enactment of Finance Bill, 2018

Advance Rulings

Scope to apply for Advance Ruling has been broadened by omitting definition for ‘activity’ and amending definition for ‘advance ruling’ to include the questions raised by the applicant in respect of any goods prior to its importation or exportation

Extended to all person either holding a Importer Exporter code Number or exporting any goods to India or with a justifiable cause to the satisfaction of the Authority

Time limit to pronounce the Advance Ruling in writing reduced to three months (from six months) from the receipt of application

Introducing the Electronic Credit Ledger to ease the payments for importer and exporters through the ledger instead of transaction wise payment as being done at present

Notices and Orders may be issued electronically for clearances and removal of goods for importation, exportation, deposit in warehouse, home consumption, etc.

© 2

018

SKP

Bu

sin

ess

Co

nsu

ltin

g LL

P. A

ll ri

ghts

res

erve

d.

Winner of India Tax Firm of the Year 2016 at the Asia Tax Awards

Ease of Doing Business and Digitalisation

2403-02-2018

To be effective from enactment of Finance Bill, 2018

Central Government empowered to exempt whole or any part of duty of customs leviable on

goods imported for repair, further processing or manufacture

reimported goods which were exported for the purposes of repair, further processing or manufacture

Scope of verification by officer broadened to include declarations made in bill of entry or shipping bill in addition to self-assessment. However, the selection of cases for verification to be primarily on risk evaluation.

© 2

018

SKP

Bu

sin

ess

Co

nsu

ltin

g LL

P. A

ll ri

ghts

res

erve

d.

Winner of India Tax Firm of the Year 2016 at the Asia Tax Awards

Anti-Evasion

2503-02-2018

To be effective from enactment of Finance Bill, 2018

Applicability of Customs Act extended also “to any offence or contravention thereunder committed outside India by any person”

Recovery of tax provisions streamlined

‘Pre- notice consultation’ to be conducted before issuance of SCN

Grant of facility to issue a supplementary notice which will be akin to SCN

Time-limit for determination of duty under recovery proceedings curtail to a fixed period of 6 months in normal cases and 1 year in case of fraud or willful suppression (extendable to further 6 months and 1 year)

Special provision of premise audit introduced

Power to Central Government to enter into a agreement with any country outside India for reciprocal exchange of information for facilitation of trade

© 2

018

SKP

Bu

sin

ess

Co

nsu

ltin

g LL

P. A

ll ri

ghts

res

erve

d.

Winner of India Tax Firm of the Year 2016 at the Asia Tax Awards

Other Proposals

2603-02-2018

To be effective from enactment of Finance Bill, 2018, unless otherwise

Levy of IGST/GST Compensation Cess on Warehoused Goods

Valuation prescribed in for levy of IGST and GST Compensation Cess for warehoused goods sold before clearance for home consumptions

Extension of Limit for Indian Customs Water

Limit of ‘Indian Customs Water’ into the sea from the existing ‘Contiguous zone of India’ to ‘Exclusive Economic Zone’

Introduction of Road and Infrastructure Cess (RIC) (to be effective from 2 February 2018)

Introduced as an Additional Duty of Customs on imported motor spirits

To be computed at a rate of INR 8 per litre

Other amendments in lieu of RIC

Imported motor spirits have been exempted from the Additional Duty of Customs (CVD)

Additional Duty of Customs (Road Cess) applicable at a rate of INR 6 per litre abolished

© 2

018

SKP

Bu

sin

ess

Co

nsu

ltin

g LL

P. A

ll ri

ghts

res

erve

d.

2703-02-2018

Erstwhile Legislation

© 2

018

SKP

Bu

sin

ess

Co

nsu

ltin

g LL

P. A

ll ri

ghts

res

erve

d.

Winner of India Tax Firm of the Year 2016 at the Asia Tax Awards

Retrospective exemptions under Service tax legislation provided to following

Services provided by GSTN to Government (from 28 March 2013 to 30 June 2017)

Life insurance services to coast guards by Naval Group Insurance Fund (from 10 September 2004 to 30 June 2017)

Government’s share of profit petroleum for services by the Government by way of grant of license/ lease to explore or mine petroleum crude or natural gas or both (from 1 April 2016 to 30 June 2017)

Refund for such excess service tax can be claimed within 6 months from date of finance bill receiving assent

Clarity awaited on powers to issue notices and audit under erstwhile legislation (Guwahati High Court in case of Mascot Entrade Pvt. Ltd)

Overview

2803-02-2018

© 2

018

SKP

Bu

sin

ess

Co

nsu

ltin

g LL

P. A

ll ri

ghts

res

erve

d.

Our Story

2903-02-2018

© 2

018

SKP

Bu

sin

ess

Co

nsu

ltin

g LL

P. A

ll ri

ghts

res

erve

d.

Winner of India Tax Firm of the Year 2016 at the Asia Tax Awards

SKP Today

3003-02-2018

India - Mumbai

Urmi Axis, 7th FloorFamous Studio Lane, Dr. E. Moses Road Mahalaxmi, Mumbai 400 011India

T: +91 22 6730 9000E: [email protected]

USA - Chicago

2917 Oak Brook Hills Road Oak Brook, IL 60523USA

T: +1 630 818 1830E: [email protected]

UAE - Dubai

Emirates Financial Towers503-C South Tower, DIFCPO Box 507260, DubaiUAE

T: +971 4 2866677E: [email protected]

Canada - Toronto

269 The East MallToronto, ON M9B 3Z1Canada

T: +1 647 707 5066E: [email protected]

The contents of this presentation are intended for general marketing and informative purposes only and should not be construed to be complete. This presentation may contain information other than our services and credentials.Such information should neither be considered as an opinion or advice nor be relied upon as being comprehensive and accurate. We accept no liability or responsibility to any person for any loss or damage incurred by relying on suchinformation. This presentation may contain proprietary, confidential or legally privileged information and any unauthorised reproduction, misuse or disclosure of its contents is strictly prohibited and will be unlawful.

Disclaimer

Connect with us

www.skpgroup.com