Reform of Fiscal Federalism in Russia: Fiscal Behavior at the Subnational Level of Government...

37

Reform of Fiscal Federalism Reform of Fiscal Federalism in Russia: Fiscal Behavior in Russia: Fiscal Behavior at the Subnational Level of at the Subnational Level of Government Government Barcelona - December, 13 2004 Ilya Trunin Ilya Trunin Institute for the Institute for the Economy in Economy in Transition, Moscow Transition, Moscow www.iet.r www.iet.r u u

-

Upload

sophia-johnston -

Category

Documents

-

view

215 -

download

1

Transcript of Reform of Fiscal Federalism in Russia: Fiscal Behavior at the Subnational Level of Government...

Reform of Fiscal Federalism in Russia: Reform of Fiscal Federalism in Russia: Fiscal Behavior at the Subnational Fiscal Behavior at the Subnational

Level of GovernmentLevel of Government

Barcelona - December, 13 2004

Ilya TruninIlya Trunin

Institute for the Economy in Institute for the Economy in Transition, MoscowTransition, Moscow

www.iet.ruwww.iet.ru

General Overview of the IET Activities General Overview of the IET Activities in the Area of Fiscal Federalismin the Area of Fiscal Federalism

1. Consulting services and research provided to the 1. Consulting services and research provided to the government of Russia:government of Russia:

• Design of the budgetary systemDesign of the budgetary system• Assignment of expenditure responsibilitiesAssignment of expenditure responsibilities• Assignment of taxing powersAssignment of taxing powers• Design of the intergovernmental transfers system (incl. Design of the intergovernmental transfers system (incl.

fiscal capacity and expenditure needs estimation fiscal capacity and expenditure needs estimation models)models)

• Fiscal relations between the regional and municipal Fiscal relations between the regional and municipal levels of governmentlevels of government

• Program-oriented and performance-based budgetingProgram-oriented and performance-based budgetingwww.iet.ruwww.iet.ru22

General Overview of the IET Activities General Overview of the IET Activities in the Area of Fiscal Federalismin the Area of Fiscal Federalism

2. Research projects:2. Research projects:• Analysis of the fiscal behavior of the regional Analysis of the fiscal behavior of the regional

governments governments • Analysis of the redistribution and stabilization Analysis of the redistribution and stabilization

features of the system of intergovernmental features of the system of intergovernmental transfers and federal shared taxes transfers and federal shared taxes

• Modeling the budget constraints of the regional Modeling the budget constraints of the regional governments in Russiagovernments in Russia

• Analysis of the institutional aspects of the Analysis of the institutional aspects of the intergovernmental fiscal relations mechanismsintergovernmental fiscal relations mechanisms

www.iet.ruwww.iet.ru33

General Overview of the IET Activities General Overview of the IET Activities in the Area of Fiscal Federalismin the Area of Fiscal Federalism

3. Consulting services to the regional governments:3. Consulting services to the regional governments:• Intergovernmental fiscal relations with Intergovernmental fiscal relations with

municipalitiesmunicipalities• Drafting legislation for the municipal reform Drafting legislation for the municipal reform

starting in 2005-2006starting in 2005-2006• Elaboration of the regional development strategiesElaboration of the regional development strategies• Public finance management (public procurement, Public finance management (public procurement,

debt management, budget institutions reform, debt management, budget institutions reform, program-oriented budegting, medium-term program-oriented budegting, medium-term planning etc.)planning etc.)

www.iet.ruwww.iet.ru44

Intergovernmental Arrangements in the Intergovernmental Arrangements in the Early Transition PeriodEarly Transition Period

• Sharp decrease in public revenues during transition to a new tax system

• Decentralizing public expenditures instead of cutting them down (from about 60% GDP)

• Need for preventing the federation from decay• Emerging of the practices of unfunded mandates as an

alternative to decreasing consolidated public expenditures in accordance with revenue possibilities

• Using intergovernmental fiscal transfers and shared taxes in political processes

Results: unstable and inefficient system of Results: unstable and inefficient system of intergovernmental fiscal arrangementsintergovernmental fiscal arrangements www.iet.ruwww.iet.ru55

First Stage of the Intergovernmental First Stage of the Intergovernmental Fiscal Reform – a 1993 ConstitutionFiscal Reform – a 1993 Constitution

• New principles of federal-regional-municipal relations –similar to many of the modern federations

• Legislative allocation of tax revenues and taxing powers across levels of government – to a possible extent

• New system of intergovernmental transfers with its key element – formula-based equalization grants

• Growing amount of unfunded mandates and political reasons (the federal government kept being dependent on strong regions) hampered the fiscal reform process

Results: Excessive decentralization in case of reach Results: Excessive decentralization in case of reach regions and strong centralization concerning the regions and strong centralization concerning the

majority of the subjects of the Federationmajority of the subjects of the Federation www.iet.ruwww.iet.ru66

Second Stage of the Intergovernmental Second Stage of the Intergovernmental Fiscal Reform – a 1998 CrisisFiscal Reform – a 1998 Crisis

• The process of the federal grants allocation went out of control a sharp decline in tax revenue

• Introduction of new principles of equalization grants allocation

• Refraining from changing the results of formula-based calculations in the parliament as well as from providing large discretionary grants

• New proportions of the tax revenue allocation between the federal and regional budgets

• Drafting conceptual programs of the intergovernmental fiscal relations reformResults: A new framework for allocation of resources Results: A new framework for allocation of resources

across levels of governmentacross levels of government www.iet.ruwww.iet.ru77

Main Features of the Current Reforms in the Area of Main Features of the Current Reforms in the Area of Intergovernmental Fiscal RelationsIntergovernmental Fiscal Relations

• Elimination of unfunded mandates: normative Elimination of unfunded mandates: normative regulation, financing and administration powers regulation, financing and administration powers start to be clearly assigned to different levels of start to be clearly assigned to different levels of governmentgovernment

• This envisages increasing role of Compensation This envisages increasing role of Compensation Grants that will finance federal mandates imposed Grants that will finance federal mandates imposed on regionson regions

• Increasing fiscal autonomy of regional and Increasing fiscal autonomy of regional and municipal governments (more on expenditure that municipal governments (more on expenditure that on revenue side)on revenue side)

• Simplification of the transfers allocation formulaSimplification of the transfers allocation formulawww.iet.ruwww.iet.ru88

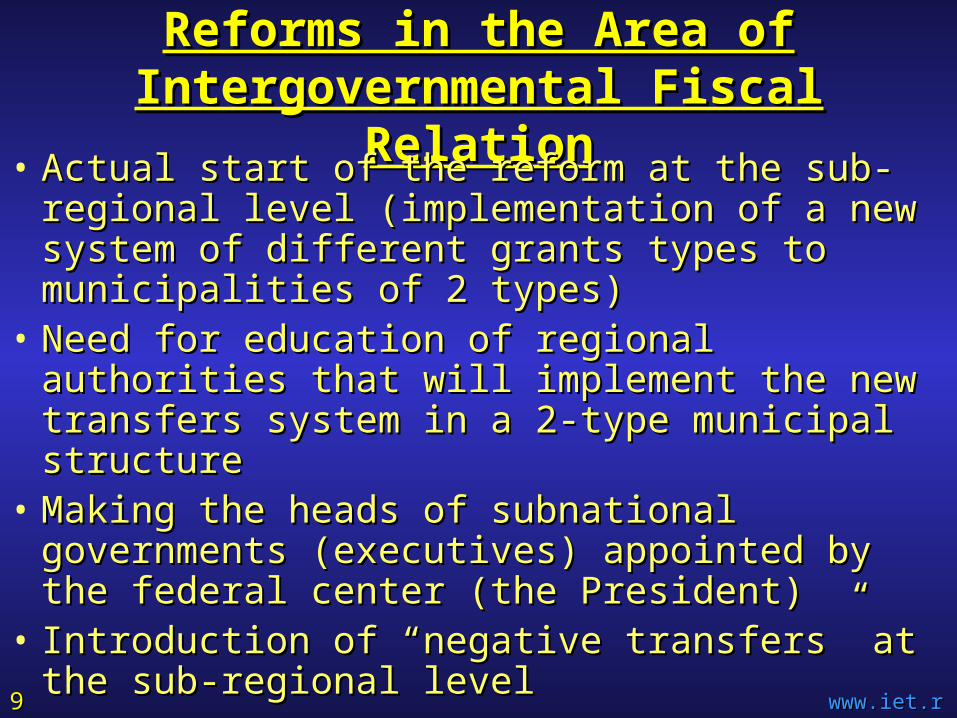

Main Features of the Current Reforms in the Main Features of the Current Reforms in the Area of Intergovernmental Fiscal RelationArea of Intergovernmental Fiscal Relation

• Actual start of the reform at the sub-regional level Actual start of the reform at the sub-regional level (implementation of a new system of different grants (implementation of a new system of different grants types to municipalities of 2 types)types to municipalities of 2 types)

• Need for education of regional authorities that will Need for education of regional authorities that will implement the new transfers system in a 2-type implement the new transfers system in a 2-type municipal structuremunicipal structure

• Making the heads of subnational governments Making the heads of subnational governments (executives) appointed by the federal center (the (executives) appointed by the federal center (the President)President)

• Introduction of “negative transfers” at the sub-Introduction of “negative transfers” at the sub-regional levelregional level

www.iet.ruwww.iet.ru99

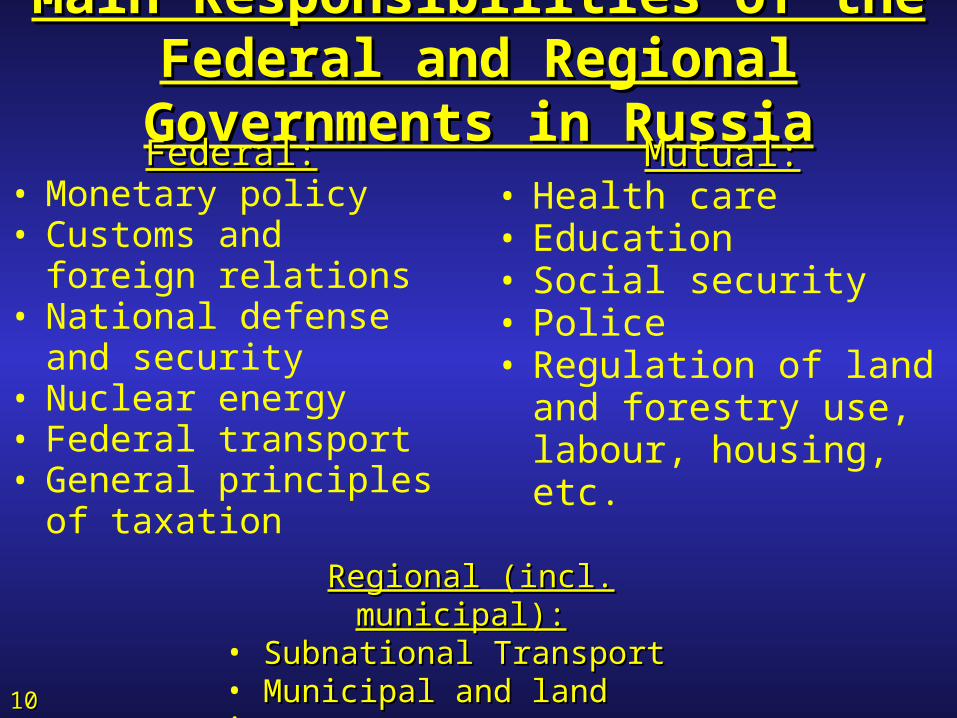

Main Responsibilities of the Federal and Main Responsibilities of the Federal and Regional Governments in RussiaRegional Governments in Russia

Federal:Federal:• Monetary policy• Customs and foreign

relations• National defense and

security• Nuclear energy• Federal transport• General principles of

taxation

Mutual:Mutual:• Health care• Education• Social security• Police• Regulation of land and

forestry use, labour, housing, etc.

Regional (incl. municipal):Regional (incl. municipal): • Subnational TransportSubnational Transport• Municipal and land improvementMunicipal and land improvement• The rest of responsibilitiesThe rest of responsibilities1010

Tax Reform and Intergovernmental Tax Reform and Intergovernmental Fiscal RelationsFiscal Relations

Main Regional and Local Taxes Main Regional and Local Taxes Before the Tax Reform of 2000-04Before the Tax Reform of 2000-04

• Corporate Income Tax (in part)

• Road Tax (corporate tax on the turnover)

• Housing and Communal tax (tax on the corporate turnover)

• Corporate Tax on Assets (similar to the property tax)

• Sales Tax

• Land Tax (both on individuals and businesses)

• Individual Property Tax

• Other regional and local taxes and fees on businesses (on school maintenance, police etc.)

Main Regional and Local Main Regional and Local Taxes After the Tax ReformTaxes After the Tax Reform• Corporate income tax (?)• Corporate property tax (not effective at the moment)• Tax on Motor Vehicles• Individual Property Tax• Land Tax• Presumptive Tax for Small Businesses• “Self-taxation”

www.iet.ruwww.iet.ru1111

The Main Features of the Federal Grants to The Main Features of the Federal Grants to the Regions at Presentthe Regions at Present

1.1. Equalization GrantsEqualization Grants – a formula-based mechanism, equalization of – a formula-based mechanism, equalization of regional fiscal capacity adjusted for expenditure needs differentialsregional fiscal capacity adjusted for expenditure needs differentials

2.2. Compensation GrantsCompensation Grants – formula-based specific purpose grants – formula-based specific purpose grants aimed at funding certain federal mandatesaimed at funding certain federal mandates

3.3. Regional Finance Reform GrantsRegional Finance Reform Grants – conditional grants to regions – conditional grants to regions performing regional finance reform programperforming regional finance reform program

4.4. Social Expenditure GrantsSocial Expenditure Grants – matching grants aimed at funding – matching grants aimed at funding certain most important regional expenditurescertain most important regional expenditures

5.5. Regional Development GrantsRegional Development Grants – specific purpose grants to finance – specific purpose grants to finance regional public investment in infrastructureregional public investment in infrastructure

6.6. Other Grants and LoansOther Grants and Loans – numerous grants (road construction, – numerous grants (road construction, compensation for changes in federal legislation, etc) allocated mainly compensation for changes in federal legislation, etc) allocated mainly on discretionary basison discretionary basis www.iet.ruwww.iet.ru1212

Per Capita Tax Revenues and Expenditures Per Capita Tax Revenues and Expenditures of the Regional Budgets in 2003 (rbl.)of the Regional Budgets in 2003 (rbl.)

www.iet.ruwww.iet.ru1313

0

10000

20000

30000

40000

50000

60000

70000

80000

Tax Revenues (incl. shared taxes) Expenditures

Per Capita Tax Revenues and Expenditures of the Per Capita Tax Revenues and Expenditures of the Regional Budgets in 2003 (rbl., adjusted)Regional Budgets in 2003 (rbl., adjusted)

www.iet.ruwww.iet.ru1414

0

5000

10000

15000

20000

25000

30000

35000

40000

Adjusted Tax Revenues Adjusted Expenditures

Tax Revenues of the Different Levels of Tax Revenues of the Different Levels of Government in the Russian FederationGovernment in the Russian Federation (% (% GDP)GDP)

www.iet.ruwww.iet.ru

0%

5%

10%

15%

20%

25%

30%

35%

40%

Regional Budgets 12,4% 14,3% 13,06% 11,9% 11,6% 12,7% 11,5% 10,4% 10,2% 9,6% 10,0% 10,0%

Federal Budget 15,8% 10,3% 11,2% 10,7% 9,9% 9,4% 8,8% 10,7% 13,2% 16,2% 18,6% 18,0%

Off-budget social funds 9,7% 10,6% 9,4% 8,2% 8,2% 7,7% 9,6% 8,6% 9,5% 8,2% 5,6% 5,7%

1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003

Regional Budgets

Federal Budget

Off-budget Social Funds

1515

Adjusted Fiscal Capacity Equalization Adjusted Fiscal Capacity Equalization Principle in Russia (illustration)Principle in Russia (illustration)

www.iet.ruwww.iet.ru1616

Federal Grants to the Regions Since 1992 (% Federal Grants to the Regions Since 1992 (% of GDP)of GDP)

0,0%

0,5%

1,0%

1,5%

2,0%

2,5%

3,0%

3,5%

1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003

% G

DP

Other Federal Grants and Loans

Equalization Transfers

Compensation Grants

Other Formula-Based Grants

www.iet.ruwww.iet.ru1717

Positive Impacts of the ReformsPositive Impacts of the Reforms• The new system has been established that has got many features The new system has been established that has got many features of an efficient system of intergovernmental fiscal equalizationof an efficient system of intergovernmental fiscal equalization

• Federal government started to base its calculations on the fiscal Federal government started to base its calculations on the fiscal capacity and expenditure needs indicators rather than on the actual capacity and expenditure needs indicators rather than on the actual revenues and expenditures in the previous periodsrevenues and expenditures in the previous periods

• The procedures of formula-based calculations has been elaborated The procedures of formula-based calculations has been elaborated and introduced to the budget planning practicesand introduced to the budget planning practices

• Compensation of unfunded mandates has been launchedCompensation of unfunded mandates has been launched

• Regional (and federal) governments started to get used to the new Regional (and federal) governments started to get used to the new philosophy of equalization – unified approach on the basis of the philosophy of equalization – unified approach on the basis of the independent statistics instead of the case by case ad hoc agreementsindependent statistics instead of the case by case ad hoc agreements

www.iet.ruwww.iet.ru1818

Current Deficiencies of the IGFR SystemCurrent Deficiencies of the IGFR System

www.iet.ruwww.iet.ru

• Limited fiscal autonomy of the regional and local governments

• Low taxing powers at the subnational level of government:Limits the fiscal autonomy of regional and local governmentsCaused by objective reasons (expenditure obligations set by

federal mandates, quality of tax legislation)

• Lack of development at the level of municipal governments• Growing resources allocated among regions at discretionary

basis causes soft budget constraints and strengthens political influence of the federal center

• Uncertainty of tax and transfers allocation mechanisms undermines the efficiency of regional and local decision-making1919

• Large amount of unfunded federal mandates that enable regions to apply for additional grants and federation – to influence regional fiscal decisions

• Unwillingness of the federal center to lose political control over regional governments

• Many reforms in different sectors (taxation, natural monopolies etc.) at the same time lead to seeking compromise in less important areas (like IGFR)

• A real IGFR reform should follow a general federal reform that will effectively start in 2005-06 only

Reasons for DeficienciesReasons for Deficiencies

www.iet.ruwww.iet.ru2020

1. Traditional models that describe impact of the transfer allocation mechanisms on the fiscal decisions of the recipients (Gramlich (1977), Thurow (1966), Bradford and Oates (1971), King (1982), etc.).

Main hypothesis: the decision-making process of subnational governments depends on the preferences of a representative of the voters' community (median voter)

2. Models that describe behavior of subnational governments taking into account the existence of the own preferences of the bureaucrats that form the government (Niskanen (1968), Niskanen (1971), Romer and Rosenthal (1980), Oates (1979), Break (1980), King (1984))

Main hypotheses:

• the preferences of the bureaucrats don't match the preferences of the regional voters

• own preferences of the government could explain the flypaper effect - phenomena, when empirical results of the impact of fiscal transfers don't match the hypotheses following from the traditional models

Models of Subnational Fiscal BehaviorModels of Subnational Fiscal Behavior

www.iet.ruwww.iet.ru2121

Definition of the fiscal equalizationDefinition of the fiscal equalization:: When tax revenues of a subnational budget are equal to a standard value (fiscal capacity), this budget is entitled to receive a grant, that is sufficient to finance provision of the public goods in this jurisdiction taking into account the regional expenditure needs (King (1980), Aronson (1977), Musgrave (1961))

Approaches to Fiscal EqualizationApproaches to Fiscal Equalization::

1. Equalization of the actual subnational expenditures of the regional budgets (USSR, Italy)

2. Equalization of the subnational expenditures taking into account regional fiscal capacity (eastern Länder in Germany, annual block grants in the UK).

3. Equalization of subnational fiscal capacity (Canada)

4. Combined schemes, including theoretical (Cripps-Godley scheme, Mathews scheme, Korea)

Models of Allocation of the Equalization Models of Allocation of the Equalization GrantsGrants

www.iet.ruwww.iet.ru2222

Fiscal Behavior of Subnational Governments Fiscal Behavior of Subnational Governments in Russia: the Modelin Russia: the Model

www.iet.ruwww.iet.ru2323

ЕЕ – – expenditures of the regional budgetexpenditures of the regional budget;;ТТ – – tax revenues of the regional budgettax revenues of the regional budget..

TrTr – fiscal transfers from the federal budget – fiscal transfers from the federal budget

TTEETr

11

T

E

– – estimation of the regional fiscal capacity made by the estimation of the regional fiscal capacity made by the federal governmentfederal government;;– – estimation of the regional expenditure needs made by the estimation of the regional expenditure needs made by the federal governmentfederal government;;

TE

TEU,

)()( max, Regional government utility function:Regional government utility function:

The budget constraintThe budget constraint: : Е Е Т+Tr Т+Tr

Formula of the federal transfers allocation across regions:Formula of the federal transfers allocation across regions:

, , , , – – parameters of the modelparameters of the model

Analysis of the ModelAnalysis of the Model1. 1. Analysis of the impact of the extent to which the "fiscal gap" Analysis of the impact of the extent to which the "fiscal gap"

between expenditure and revenue indicators is financed from the between expenditure and revenue indicators is financed from the federal budget federal budget (() ) on the regional fiscal decisionson the regional fiscal decisions

2. Analysis of the impact of the extent to which the transfers 2. Analysis of the impact of the extent to which the transfers allocation formula depends on the actual public expenditures of allocation formula depends on the actual public expenditures of the regions in the previous periods the regions in the previous periods (() ) on the regional fiscal on the regional fiscal decisionsdecisions

3. 3. Analysis of the impact of the extent to which the transfers Analysis of the impact of the extent to which the transfers allocation formula depends on the actual public revenues of the allocation formula depends on the actual public revenues of the regions in the previous periods regions in the previous periods (() ) on the regional fiscal on the regional fiscal decisionsdecisions

4. Analysis of the impact of changes in the other factors on the 4. Analysis of the impact of changes in the other factors on the fiscal decisions of the regional governmentsfiscal decisions of the regional governments

www.iet.ruwww.iet.ru2424

Main Conclusions from the Theoretical Main Conclusions from the Theoretical AnalysisAnalysis

Signs of the partial derivatives of the optimal values of tax revenues Signs of the partial derivatives of the optimal values of tax revenues ((T*T*)) and and expenditures (expenditures (E*E*) chosen by the regional governments with respect to the ) chosen by the regional governments with respect to the parameters of the model (for the recipient regions):parameters of the model (for the recipient regions):

• By changing the model parameters the federal government could create By changing the model parameters the federal government could create different kinds of fiscal incentives for the regional governments different kinds of fiscal incentives for the regional governments depending of the objectives of the federal budget policydepending of the objectives of the federal budget policy

• When the approach towards equalization is symmetrical (When the approach towards equalization is symmetrical (α α = = ββ)) - - growth growth in the transfer amount should cause growth in the recipient's expenditures in the transfer amount should cause growth in the recipient's expenditures by the amount that is less than the amount received. At the same time the by the amount that is less than the amount received. At the same time the tax revenues should decline. tax revenues should decline.

• When the approach is not symmetricalWhen the approach is not symmetrical ((α <>α <> ββ))– – effects of the growth in effects of the growth in fiscal transfers are not evident fiscal transfers are not evident a prioria priori

Y Derivative of E* + + – + – ?#

Derivative of T* + – + + – ?##

E

T

www.iet.ruwww.iet.ru2525

Main Conclusions from the Theoretical Main Conclusions from the Theoretical AnalysisAnalysis

Transfers allocation formula after regrouping:Transfers allocation formula after regrouping:

• If the federal government uses actual If the federal government uses actual expenditures while allocating grants (expenditures while allocating grants ( >0>0) it ) it creates incentives for public expenditure growthcreates incentives for public expenditure growth

• If the federal government uses actual revenues If the federal government uses actual revenues while allocating grants (while allocating grants ( >0>0) it creates incentives ) it creates incentives for tax collection decreasefor tax collection decrease

)()()( iiiiiii TETTEETr

www.iet.ruwww.iet.ru2626

Main Conclusions from the Theoretical Main Conclusions from the Theoretical AnalysisAnalysis

1. If 1. If = = then effects are similar to classic then effects are similar to classic approachapproach

2. If 2. If > > then there are incentives to increase then there are incentives to increase public expenditures with the increase in public public expenditures with the increase in public revenues (if revenues (if γγ < 1) < 1)

3. If 3. If < < then there are incentives for the regions then there are incentives for the regions to decrease public revenues in order to get more to decrease public revenues in order to get more grants from the federal budget (as compared to grants from the federal budget (as compared to the symmetrical case). The worst incentive is to the symmetrical case). The worst incentive is to cut expenditures after cutting tax revenues and cut expenditures after cutting tax revenues and receiving grantsreceiving grants

www.iet.ruwww.iet.ru2727

The Model of the Regional Fiscal Behavior: The Model of the Regional Fiscal Behavior: Empirical TestsEmpirical Tests

www.iet.ruwww.iet.ru

2,1,0,)()()( ,,3,2,10, sTEaTTaEEaaTr stistististiti The linear regression equation:The linear regression equation:

aa33==, , aa11==.., , aa22==..

Main hypotheses:Main hypotheses:

aa00=0=0, , i.e. there is no component in the federal grant that is calculated as i.e. there is no component in the federal grant that is calculated as

a lump-sum amount for all regionsa lump-sum amount for all regions;;

0 0 a a33 1 1, , that is similar tothat is similar to 0 0 1 1;;

0 0 a a11 a a33, , taking into account that taking into account that aa11== .. and the condition with and the condition with

respect torespect to aa33 this is similar tothis is similar to 0 0 1 1;;

0 0 -a -a22 a a33, , taking into account that taking into account that aa22== .. and the condition withand the condition with

respect to respect to aa33 this is similar tothis is similar to 0 0 1 1.. 2828

Main Results of the Empirical Tests1. 1. The federal governments while allocating fiscal transfers acts in The federal governments while allocating fiscal transfers acts in

order to fill the gap between estimates of the regional revenue order to fill the gap between estimates of the regional revenue and expenditure indicators and expenditure indicators ((γγ > 0)> 0)

2. 2. Four sub-periods have been specified for equalization transfersFour sub-periods have been specified for equalization transfers: : 1994, 1995–19971994, 1995–1997,, 1998–2 1998–2000 and 2000-2003.000 and 2000-2003.

3. 3. The extent to which the government used fiscal capacity while The extent to which the government used fiscal capacity while allocating fiscal transfers in general has been lower than for allocating fiscal transfers in general has been lower than for expenditure needs expenditure needs (( < < ))

4. 4. Allocation of the additional fiscal transfers (except for Allocation of the additional fiscal transfers (except for equalization) has been made in accordance with less objective equalization) has been made in accordance with less objective criteria criteria ((our estimates ofour estimates of и и are higher for the additional are higher for the additional transfers)transfers)

www.iet.ruwww.iet.ru2929

Main Results of the Empirical Tests

55. . For the group of regions that are highly dependent on the For the group of regions that are highly dependent on the federal fiscal transfers the federal government used actual federal fiscal transfers the federal government used actual revenues and expenditures to a greater extentrevenues and expenditures to a greater extent ( ( andand ), ), and and filled the larger share of the gapfilled the larger share of the gap ( (), ), than for the other than for the other regionsregions..

6. 6. While allocating fiscal transfers to the Northern regions the While allocating fiscal transfers to the Northern regions the federal government fills the gap federal government fills the gap (()) to a greater extent than to a greater extent than for the other regionsfor the other regions

7. 7. There has not been any evidence found that negative fiscal There has not been any evidence found that negative fiscal incentives exist in Russian (decreasing the tax revenues of incentives exist in Russian (decreasing the tax revenues of the regional budgets after increase in federal grants)the regional budgets after increase in federal grants)

www.iet.ruwww.iet.ru3030

Main Hypotheses for Estimation of the Main Hypotheses for Estimation of the Results of the Recent ReformsResults of the Recent Reforms

Implementation of the formula-based procedures

Allocation of additional federal revenues based on discretionary mechanisms

Centralization of tax revenues in the federal budget and compensation of regional losses caused by the tax reform

The equalization transfersThe equalization transfers allocation depends more on fiscal capacity and expenditure needs indicators than on actual revenues and expenditures

Less importance of fiscal capacity and expenditure needs indicators for the total transfersthe total transfers as compared to 1999-2001 period

Growth of the gap between the gap between revenue and expenditure revenue and expenditure indicatorsindicators while the total transfers allocation

www.iet.ruwww.iet.ru3131

A Soft Budget Constraint Problem – DefinitionsA Soft Budget Constraint Problem – Definitions• Economic agents could take decisions influenced by

the expectations of the additional financial resources from the principal (similar to a moral hazard problem)

• A multi-tier structure of government creates incentives for the soft budget constraints (SBC)

• Two main negative effects of the soft budget constraint:

Bad financial discipline (accumulation of debt, inefficient fiscal decisions)

Inefficient growth of public expenditures originating from the additional resources expectation

www.iet.ruwww.iet.ru3232

A Soft Budget Constraint Problem – ExperiencesA Soft Budget Constraint Problem – Experiences

• Two ways of preventing the SBC problem in a multi-tier government countries: InstitutionalInstitutional – creation of the market and public

institutions that prevent emerging the SBC HierarchicalHierarchical – mechanisms involving control by the

central government over the subnational governments

• Institutional mechanisms proved to be more effective (USA and Canada): Long-term anti-bailout policy Devolving responsibility for the borrowing and other

fiscal decisions Effective political mechanisms in a federation

www.iet.ruwww.iet.ru3333

A Soft Budget Constraint Problem – Experiences A Soft Budget Constraint Problem – Experiences (continued)(continued)

• Mechanisms of hierarchical control could be inefficient in large and multi-tier federations: Scale of problem: “too big to fail” reason (Germany) Political influence of subnational governments (Brazil)

• Efficient strategy in a multi-tier government structure should include decentralization of responsibilities (negative examples of China and Ukraine)

• Hierarchical control could be effective in small unitary countries (Norway, Hungary)

• SBC problem could be solved (Argentina)www.iet.ruwww.iet.ru3434

A Soft Budget Constraint Problem in RussiaA Soft Budget Constraint Problem in Russia

• The Russian Constitution does not contain clear division of responsibilities between levels of government

• Lack of market and public institutions aimed at the making subnational governments responsible for own fiscal decisions

• Unfunded mandates makes the federal government implicitly responsible for revenues and expenditures of subnational governments

• Political weakness of the federal center and compromise-seeking made the hierarchical control mechanisms ineffective throughout the 1990-s

www.iet.ruwww.iet.ru3535

A Soft Budget Constraint Problem in Russia - A Soft Budget Constraint Problem in Russia - MechanismsMechanisms

• Existence of various kinds of discretionary transfers with unclear mechanisms of allocation

• Nontransparent public finance system, the federal center is unable to control expenditures for the purposes of compensation grants when they are mandated to regions

• Possibility of borrowing from non-market sources: employees in the public sector service providers (electricity, heating, natural gas)

• Numerous and annual examples of bailouts of regions and municipalities

www.iet.ruwww.iet.ru3636

Further Reform AgendaFurther Reform Agenda

• Creating incentives for responsible behavior at the Creating incentives for responsible behavior at the regional and municipal levels of governmentregional and municipal levels of government

• Extensive usage of matching grants to pursuit Extensive usage of matching grants to pursuit federal objectives at the regional levelfederal objectives at the regional level

• Creating unified system of federal grants to regions Creating unified system of federal grants to regions including various kinds of present discretionary including various kinds of present discretionary transfers (road construction, investment programs, transfers (road construction, investment programs, ad hoc grants)ad hoc grants)

• Moving to real equalization of fiscal capacity from Moving to real equalization of fiscal capacity from grants allocation according to “normative” revenues grants allocation according to “normative” revenues and expendituresand expenditures

www.iet.ruwww.iet.ru3737