Redefining Convenience: Retail, Leisure and Real Estate ...

62

Redefining Convenience: Retail, Leisure and Real Estate Perspectives 28 th September 2015 Savills, Margaret Street, London

Transcript of Redefining Convenience: Retail, Leisure and Real Estate ...

Redefining Convenience: Retail, Leisure and Real Estate PerspectivesLeisure and Real Estate Perspectives

28th September 2015Savills, Margaret Street, London

Redefining convenience1. Welcome & introduction to the event

Redefining convenience: global insightsJonathan Reynolds, Oxford Institute of Retail Management

2. Tom Whittington, Director of Retail Research, 2. Tom Whittington, Director of Retail Research, Savills

3. Alex McCulloch, Associate Partner, CACI4. Award of undergraduate certificates – Luke

Burns, University of Leeds5. Network drinks

SLA forward programme

• Sponsorship: past & future• Three events for 2016

– Spatial analysis and the omnichannel– Format innovation– Format innovation– Location analysis: international perspectives

• February, June and October• At least one outside London• Surveys, job advertising, website, student

awardsYour name here!

• An opportunity to invite a Masters student to undertake a research project for you

• Research will be conducted May – August 2016• Students are also supported by their university supervisors

• To apply:• Fill in a short project proposal form from cdrc.ac.uk/retail-

masters – Website launches next week!• Deadline: Friday 4th December 2015

• Students are also supported by their university supervisors• See our leaflet for more information

Property Research Course 1-2 December 2015Open for BookingsOpen for Bookings

For further information please visit:www.sprweb.com/spr-course/course

*Terms & conditions apply

Redefining convenience1. Welcome & introduction to the event

Redefining convenience: global insightsJonathan Reynolds, Oxford Institute of Retail Management

2. Tom Whittington, Director of Retail Research, 2. Tom Whittington, Director of Retail Research, Savills

3. Alex McCulloch, Associate Partner, CACI4. Award of undergraduate certificates – Luke

Burns, University of Leeds5. Network drinks

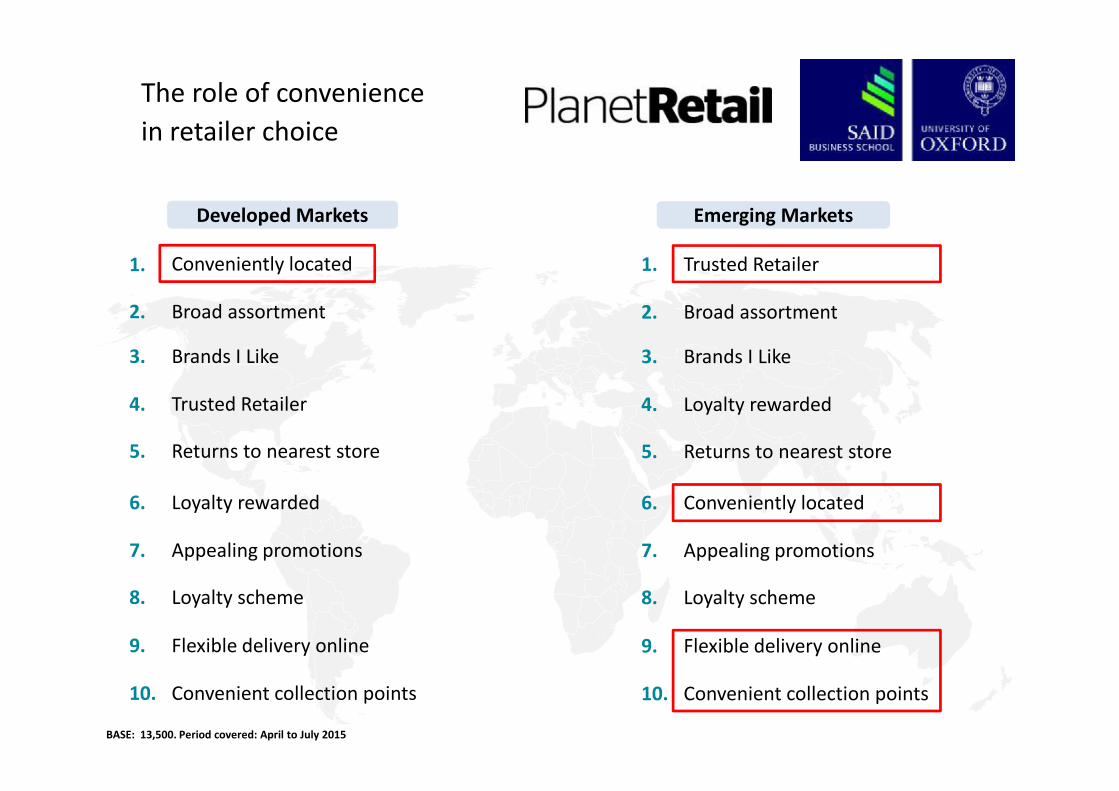

The role of convenience in retailer choice

1.

2.

3.

4.

Conveniently located

Broad assortment

Brands I Like

Trusted Retailer

Developed Markets

1.

2.

3.

4.

Trusted Retailer

Broad assortment

Brands I Like

Loyalty rewarded

Emerging Markets

10.

4.

5.

6.

7.

8.

9.

Trusted Retailer

Returns to nearest store

Loyalty rewarded

Appealing promotions

Loyalty scheme

Flexible delivery online

Convenient collection points

BASE: 13,500. Period covered: April to July 2015

10.

4.

5.

6.

7.

8.

9.

Loyalty rewarded

Returns to nearest store

Conveniently located

Appealing promotions

Loyalty scheme

Flexible delivery online

Convenient collection points

Shoppers’ choice of retailer in influenced by…

Redefining convenience

Convenient collection points to pick up online purchases

50%

67%

34%

Convenient location of stores

63%

75%

61%

BASE: 13,500. Period covered: April to July 2015

ability to return unwanted items bought online to their nearest store

58%

66% 66%

Redefining convenience

1. Welcome; the SLA forward programme –Jonathan Reynolds, Oxford Institute of Retail Management

2. Tom Whittington, Director of Retail Research, 2. Tom Whittington, Director of Retail Research, Savills

3. Alex McCulloch, Associate Partner, CACI4. Award of undergraduate certificates – Luke

Burns, University of Leeds5. Network drinks

The Convenience TripSLA/SPR

savills.com

SLA/SPRTom WhittingtonDirector Retail Research, Savills

28th September 2015

The catalyst of change

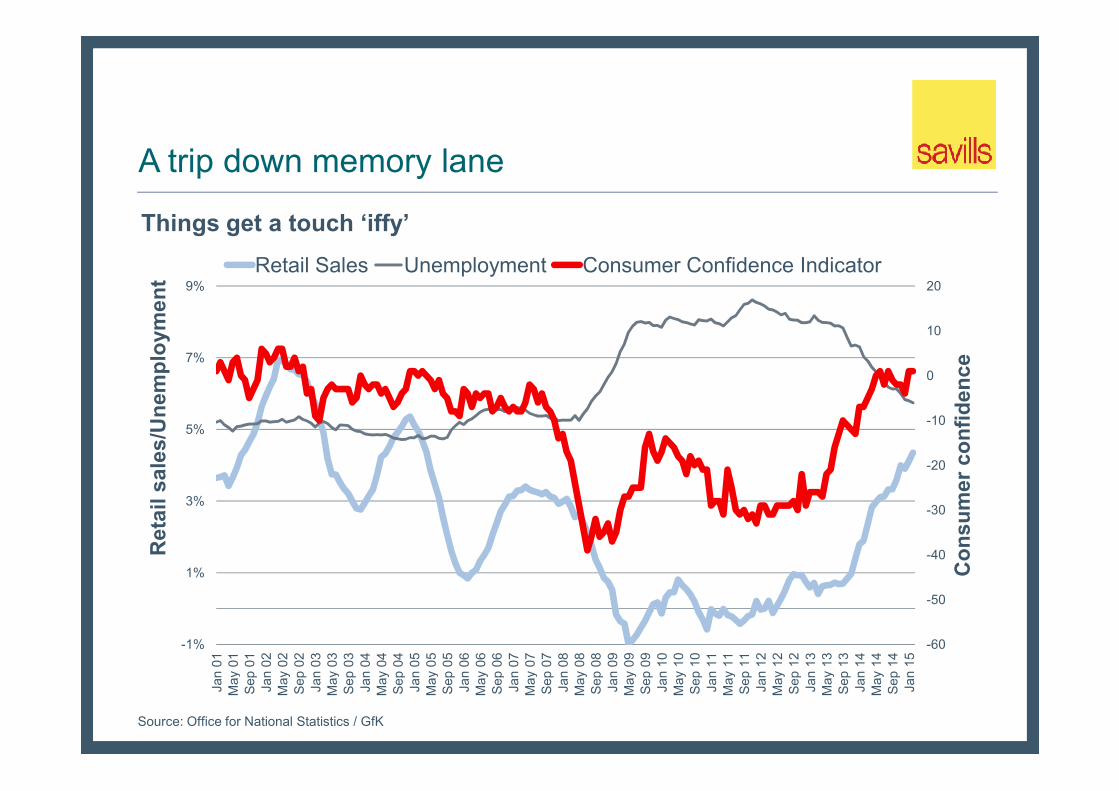

A trip down memory lane

0

10

20

7%

9%

Con

sum

er c

onfid

ence

Ret

ail s

ales

/Une

mpl

oym

ent Retail Sales Unemployment Consumer Confidence Indicator

Things get a touch ‘iffy’

Source: Office for National Statistics / GfK

-60

-50

-40

-30

-20

-10

-1%

1%

3%

5%

Jan

01M

ay 0

1Se

p 01

Jan

02M

ay 0

2Se

p 02

Jan

03M

ay 0

3Se

p 03

Jan

04M

ay 0

4Se

p 04

Jan

05M

ay 0

5Se

p 05

Jan

06M

ay 0

6Se

p 06

Jan

07M

ay 0

7Se

p 07

Jan

08M

ay 0

8Se

p 08

Jan

09M

ay 0

9Se

p 09

Jan

10M

ay 1

0Se

p 10

Jan

11M

ay 1

1Se

p 11

Jan

12M

ay 1

2Se

p 12

Jan

13M

ay 1

3Se

p 13

Jan

14M

ay 1

4Se

p 14

Jan

15

Con

sum

er c

onfid

ence

Ret

ail s

ales

/Une

mpl

oym

ent

Consumers

ConfidenceHangover from boom leaves consumer desire undiminished, but consumer confidence dashed.

PrudenceBargain hunting.

The aftermath

Bargain hunting.Smaller baskets.Many purchases put on hold.

OnlineInternet capitalises on demand for cheaper goods and apathy from consumers to go to the high street.

FrivolousYet people will gladly part with £100s for the latest smart phone.

Retailers

AdministrationsBut several ‘big ones’ are due to underlying financial or business practices rather than demandOr from ‘over exposed’ sectors.

Opportunists

The aftermath

OpportunistsSeveral retailers ‘cleaned’ up on taking the best units.Around ½ units available from administration of Woolworths, Clintons and Blockbuster were rescued/snapped up.Pureplays like Asos, Amazon and Ebay are booming.

ConsolidationThe threat to slash stores never happened.Some still underway but from large brands that still have and intend to keep hundreds of stores.

VoidsA problem yes, but not always the best barometer for retail vitality.

A trip down memory lane

250

300

7%

9%

Ret

ail s

ales

/Une

mpl

oym

ent

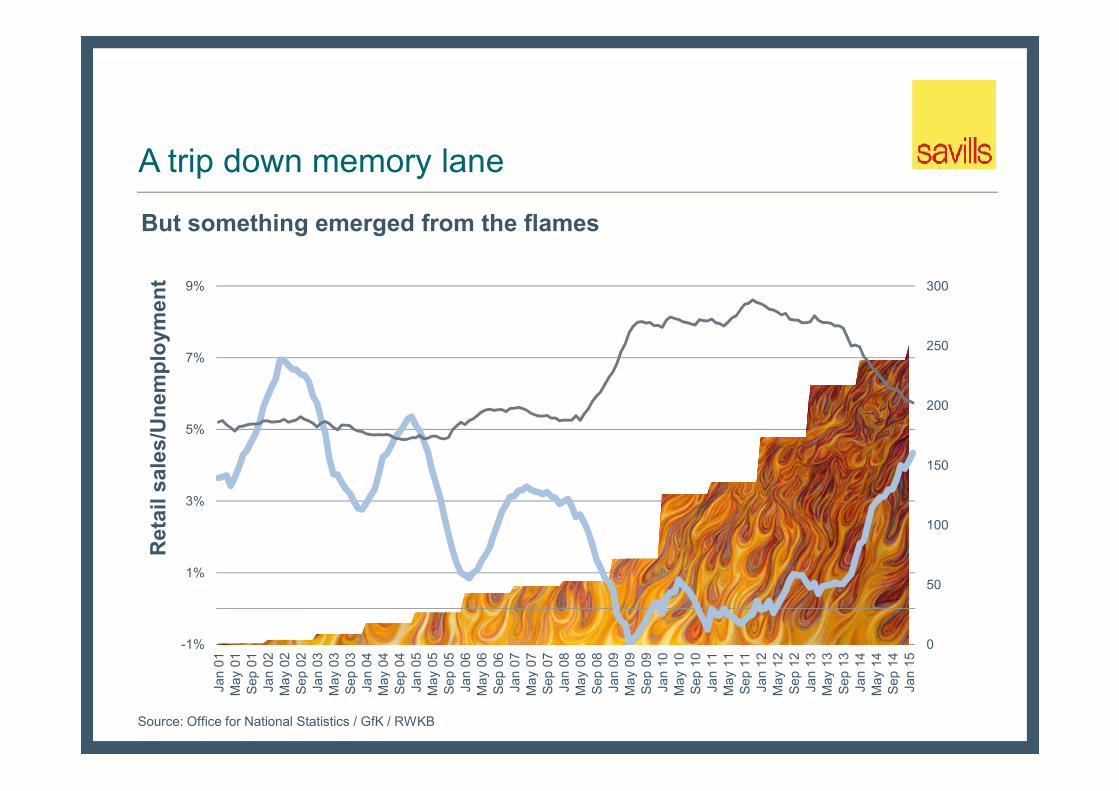

But something emerged from the flames

Source: Office for National Statistics / GfK / RWKB

0

50

100

150

200

-1%

1%

3%

5%

Jan

01M

ay 0

1Se

p 01

Jan

02M

ay 0

2Se

p 02

Jan

03M

ay 0

3Se

p 03

Jan

04M

ay 0

4Se

p 04

Jan

05M

ay 0

5Se

p 05

Jan

06M

ay 0

6Se

p 06

Jan

07M

ay 0

7Se

p 07

Jan

08M

ay 0

8Se

p 08

Jan

09M

ay 0

9Se

p 09

Jan

10M

ay 1

0Se

p 10

Jan

11M

ay 1

1Se

p 11

Jan

12M

ay 1

2Se

p 12

Jan

13M

ay 1

3Se

p 13

Jan

14M

ay 1

4Se

p 14

Jan

15

Ret

ail s

ales

/Une

mpl

oym

ent

The store portfolio dilemmaIt was said during the recession that retailers needed just 80 stores to have It was said during the recession that retailers needed just 80 stores to have national representation.

In reality there are few retailers that have culled their portfolios so dramatically.

In fact, most sectors have grown

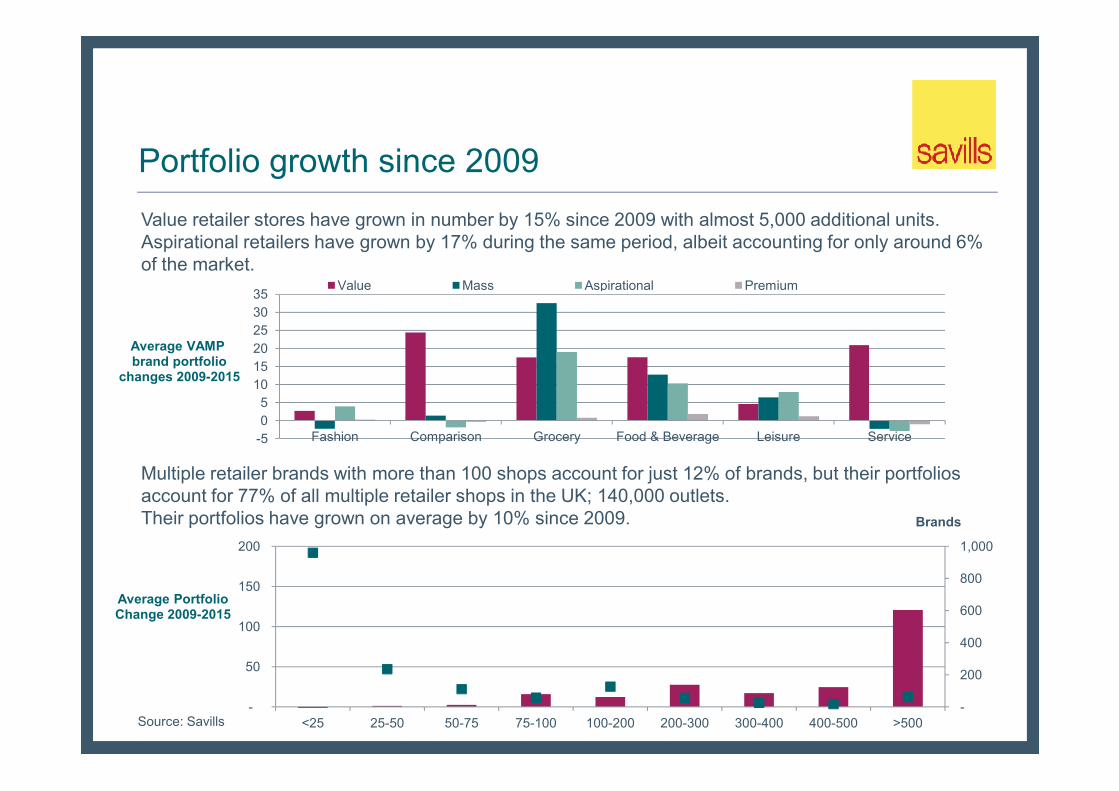

Value retailer stores have grown in number by 15% since 2009 with almost 5,000 additional units.Aspirational retailers have grown by 17% during the same period, albeit accounting for only around 6% of the market.

101520253035

Average VAMPbrand portfolio

changes 2009-2015

Value Mass Aspirational Premium

Portfolio growth since 2009

-

200

400

600

800

1,000

-

50

100

150

200

<25 25-50 50-75 75-100 100-200 200-300 300-400 400-500 >500

Average PortfolioChange 2009-2015

Brands

Multiple retailer brands with more than 100 shops account for just 12% of brands, but their portfolios account for 77% of all multiple retailer shops in the UK; 140,000 outlets. Their portfolios have grown on average by 10% since 2009.

-505

Fashion Comparison Grocery Food & Beverage Leisure Service

Source: Savills

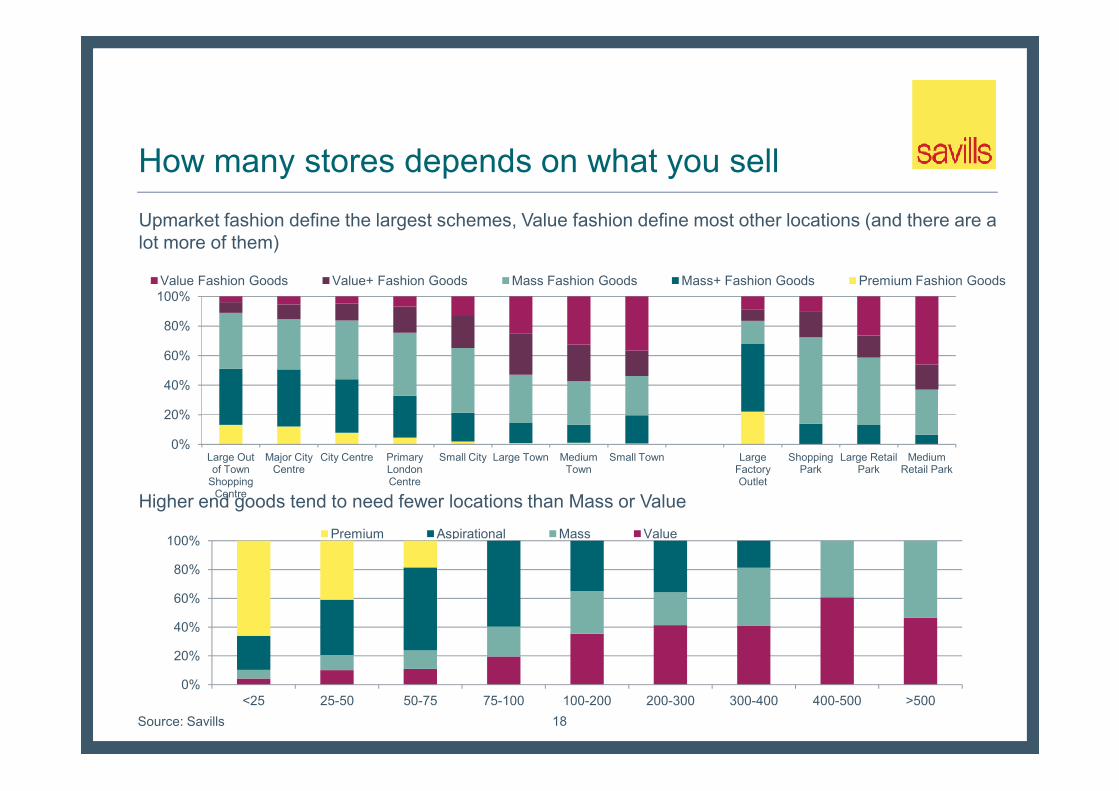

Upmarket fashion define the largest schemes, Value fashion define most other locations (and there are a lot more of them)

40%

60%

80%

100%Value Fashion Goods Value+ Fashion Goods Mass Fashion Goods Mass+ Fashion Goods Premium Fashion Goods

How many stores depends on what you sell

0%

20%

40%

60%

80%

100%

<25 25-50 50-75 75-100 100-200 200-300 300-400 400-500 >500

Premium Aspirational Mass Value

18Source: Savills

Higher end goods tend to need fewer locations than Mass or Value

0%

20%

Large Out of Town

Shopping Centre

Major City Centre

City Centre Primary London Centre

Small City Large Town Medium Town

Small Town Large Factory Outlet

Shopping Park

Large Retail Park

Medium Retail Park

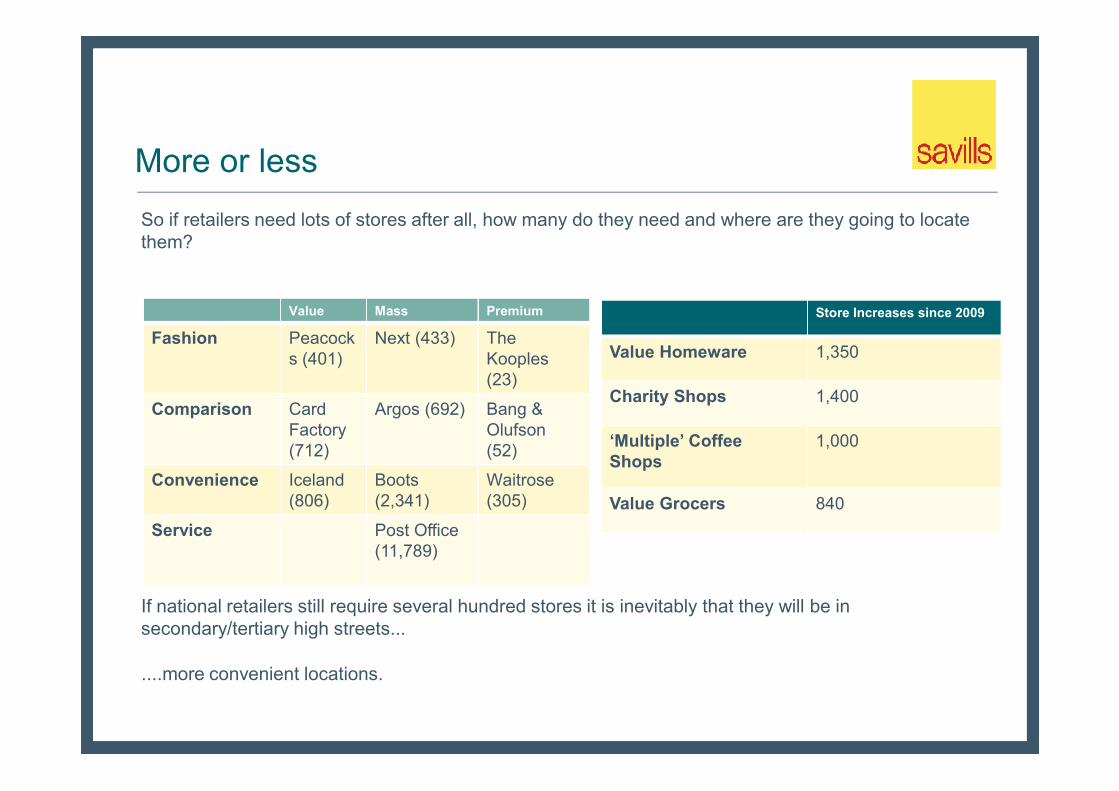

More or lessSo if retailers need lots of stores after all, how many do they need and where are they going to locate them?

Value Mass Premium

Fashion Peacocks (401)

Next (433) The Kooples(23)

Store Increases since 2009

Value Homeware 1,350

Charity Shops 1,400Comparison Card

Factory (712)

Argos (692) Bang & Olufson(52)

Convenience Iceland (806)

Boots(2,341)

Waitrose (305)

Service Post Office (11,789)

Charity Shops 1,400

‘Multiple’ Coffee Shops

1,000

Value Grocers 840

If national retailers still require several hundred stores it is inevitably that they will be in secondary/tertiary high streets...

....more convenient locations.

Redefining ‘C’onvenienceIf consumers wouldn’t come to the shops then retailers would have to come to

them

Fashion accounts for 50% of units in regional malls, but <5% of suburban tertiary high streets.

Convenience and service retail accounts for 15% of regional malls, but over 50% of tertiary high streets.

Where do we shop and for what?

Source: Savills / GeoLytix

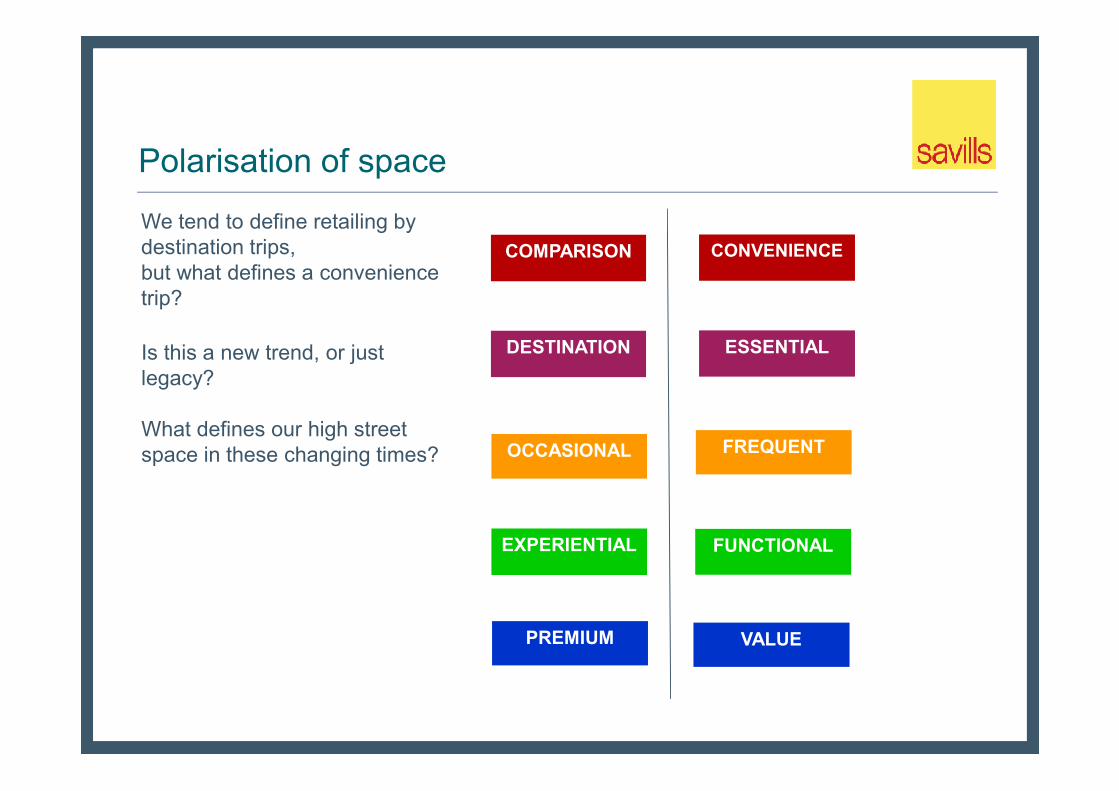

ESSENTIALDESTINATION

COMPARISON CONVENIENCE

Polarisation of space

We tend to define retailing by destination trips, but what defines a convenience trip?

Is this a new trend, or just legacy?

OCCASIONAL

EXPERIENTIAL

PREMIUM

FREQUENT

VALUE

FUNCTIONAL

What defines our high street space in these changing times?

The convenience trip

GrocerySmaller baskets seen as more economical – buy what you need, more locally‘Top up shopping’ becomes more prevalent.Grocery retailers have led the way, but convenience no longer refers to just food.

Every day ‘comparison’ goods?Or are these retailers actually selling us convenience?

The convenience trip

Source: Savills / GeoLytix

Discount goodsLocated in the largest centres, but with a significant presence in the Secondary and Tertiary high street.

The convenience trip

Source: Savills / GeoLytix

The lost mid-market

Many retailers lack distinction

Is Value the new Mass?

A shift to from the middle ground

Several retailers have altered their pitches, or have a polarised offer

Next fashion versus Next HomeM&S fashion versus M&S Simply Food

So what about clothing?Functional fashionTights and undies are (sadly) not always exciting and few of us go commando

The convenience trip

Source: Savills / GeoLytix

So what is convenience really?

Coming to a high street near you...

Affordable Homeware

GroceryRetail ServiceConvenience Food and Beverage

Affordable HomewareAffordable Fashion

...anything that is disposable, consumerable or replaceable...

The changing face of the high streethigh street

Apparently the high street is dead, grocery is all out of town and the internet is killing everything else off.

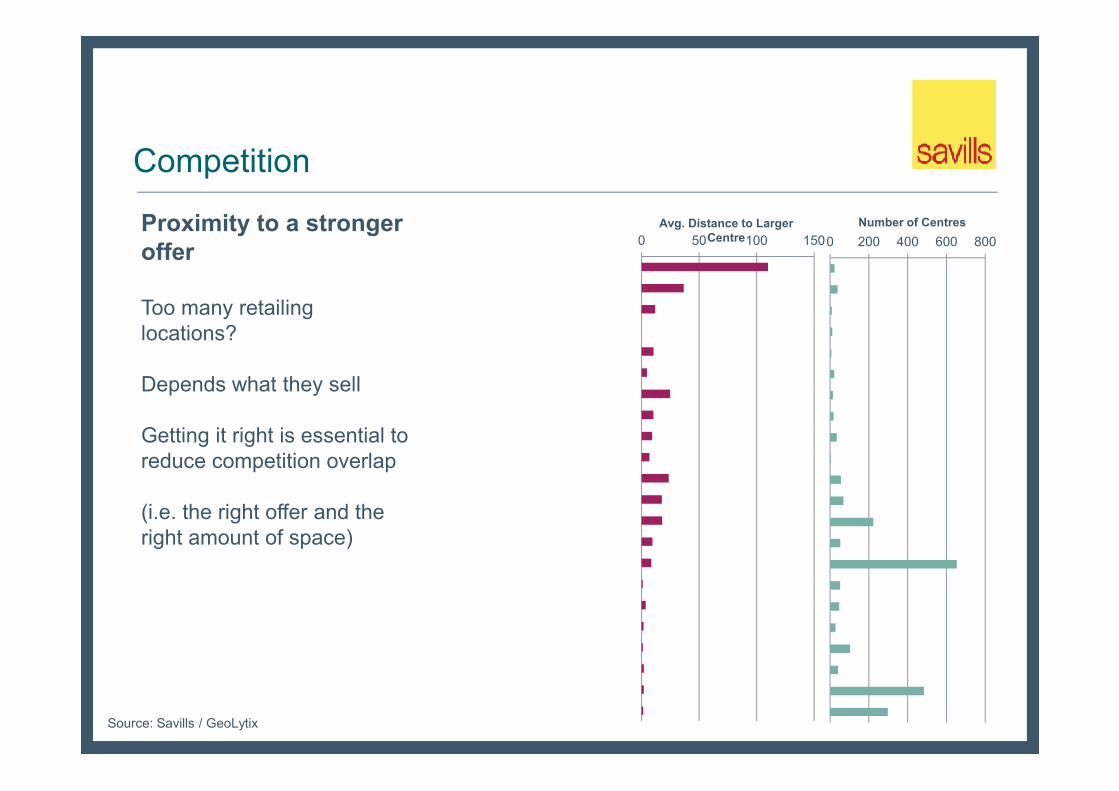

Proximity to a stronger offer

Too many retailing locations?

Depends what they sell

Competition

0 50 100 1500 200 400 600 800Avg. Distance to Larger

CentreNumber of Centres

Depends what they sell

Getting it right is essential to reduce competition overlap

(i.e. the right offer and the right amount of space)

Source: Savills / GeoLytix

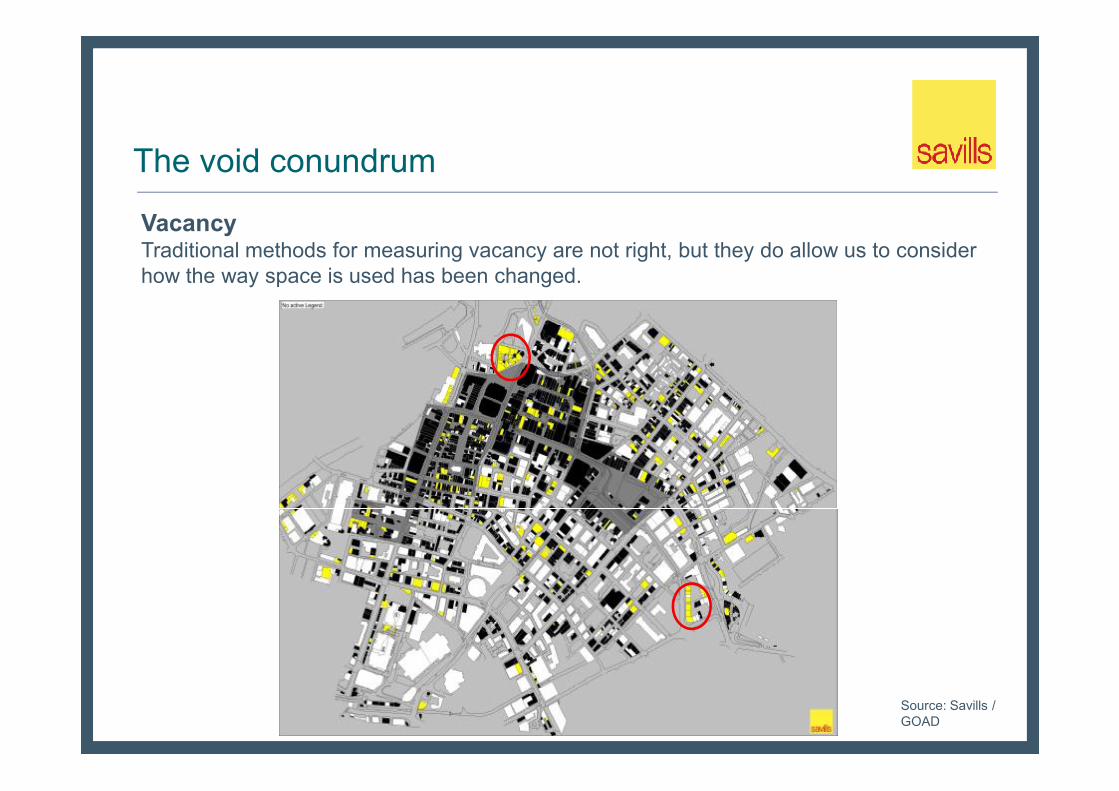

VacancyTraditional methods for measuring vacancy are not right, but they do allow us to consider how the way space is used has been changed.

The void conundrum

Source: Savills / GOAD

VacancyShort term (churn?)Medium term (a problem?)Long term (redundant stock)

The void conundrum

Source: Savills / GeoLytix / GOAD

Online / high street paradox

The elephant in the room?Internet.....C&C.....channel integration

Online to level out at 20-25%?C&C – 18% of online increasing to...?

C&C sees 25% uplift in store sales

Convenience driver?High street saviour?

What’s in store?

Smaller high street formatsDemand likely to increase for smaller units as retailers trial new formats and demand for space in convenience and high street locations.

More ‘hub and spoke’ models.

Change of useChange of usePitch shift and oversupply means that a lot of traditional retailing space is redundant stock.But that doesn’t mean that the place has no retail vitality.

Changing use, either to office, residential, or leisure space creates a new demand for retail........predominantly for convenience retail.

Consumers likely to remain both prudent and frivolousConsumer confidence is improving, but lessons learned in the last 7 years are likely to persevere.

Good times to continue for Value and Aspirational with challenges for the mid market.

What’s in store?

Right place, right offerGrocery and value retailers have led the way, but convenience no longer refers to just food.Its nothing new really, we’d just not really thought about it this way.

The main thing is giving consumers something locally things that they need regularly and allowing specialist trips to be serviced elsewhere.

Convenience is kingWhether locally, or in regional malls

Experience is everythingWhether locally, or in regional malls

The retail place will remainThey might just have to keep a hold on what drives their essential purpose

Consumers can increasingly be drawn by increased levels of personalisation and service. Lessons from Primary retail centres start to trickle down to the high street.

Thank you for listening

The small print:

*Over generalisation warning!

**Some high streets ARE in real threat!

***Little account has been made for OOT or independents

****Opinions and predictions valid until next week

CCI | Commercial in Confidence © CACI Ltd, 2015

September 2015

Alex McCulloch

Associate Partner

THE CONVENIENT SHOPPER

WHAT DO WE MEAN BY CONVENIENCE?

CCI | Commercial in Confidence © CACI Ltd, 2015

38

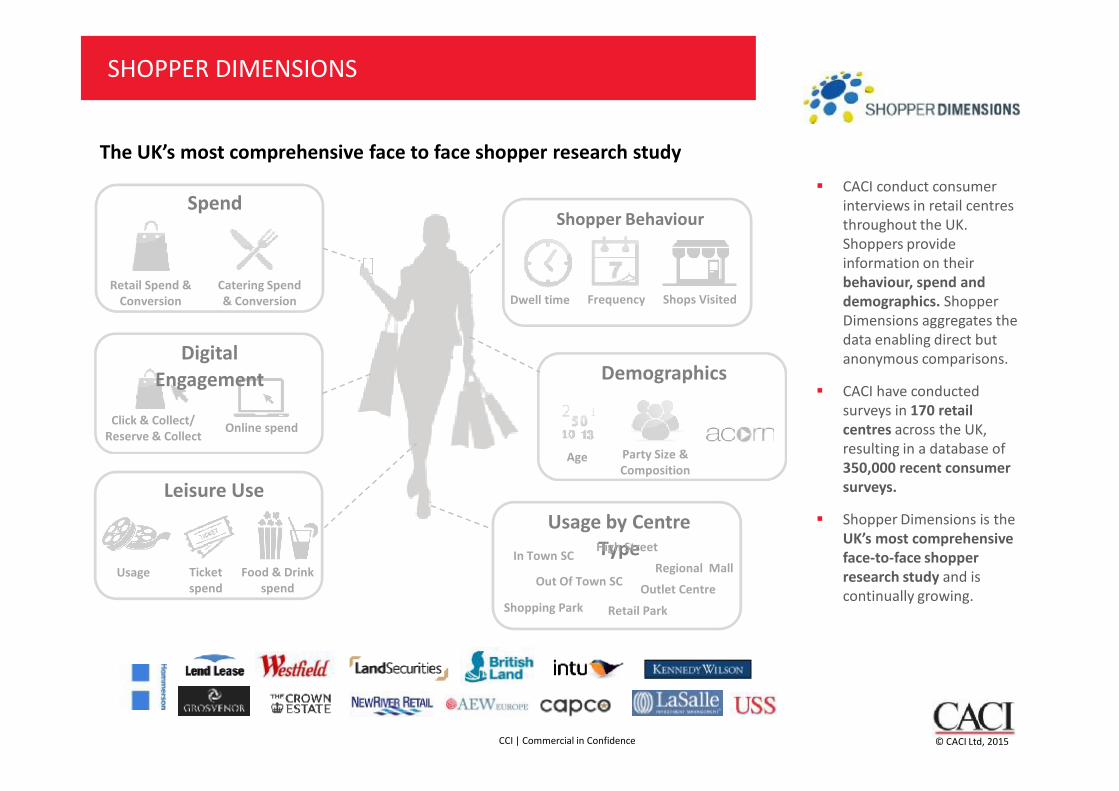

The UK’s most comprehensive face to face shopper research study

Shopper Behaviour

Dwell time Frequency Shops Visited

Demographics

Spend

Retail Spend & Conversion

Catering Spend & Conversion

Digital Engagement

§ CACI conduct consumer interviews in retail centres throughout the UK. Shoppers provide information on their behaviour, spend and demographics. Shopper Dimensions aggregates the data enabling direct but anonymous comparisons.

§ CACI have conducted

SHOPPER DIMENSIONS

CCI | Commercial in Confidence © CACI Ltd, 2015

39

Party Size & Composition

Age

Click & Collect/Reserve & Collect

Online spend

§ CACI have conducted surveys in 170 retail centres across the UK, resulting in a database of 350,000 recent consumer surveys.

§ Shopper Dimensions is the UK’s most comprehensive face-to-face shopper research study and is continually growing.

Usage by Centre TypeIn Town SC

Out Of Town SC

Shopping Park Retail Park

High StreetRegional Mall

Outlet Centre

Leisure Use

Usage Ticketspend

Food & Drinkspend

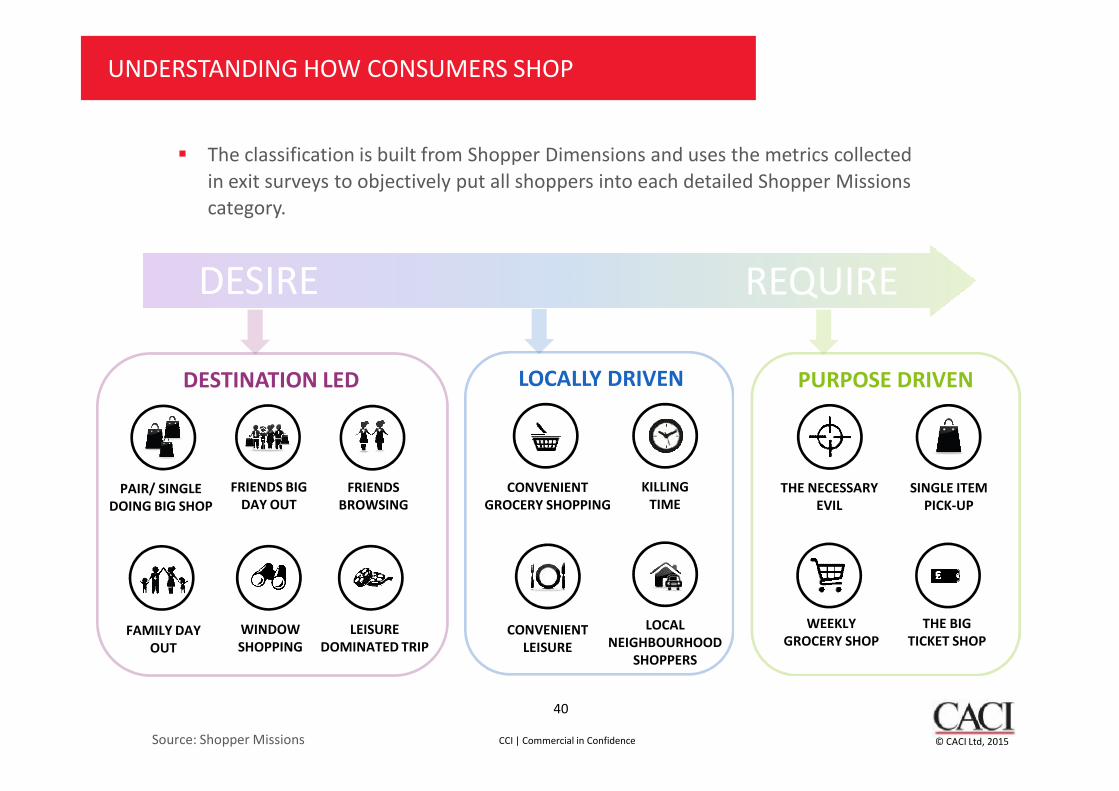

UNDERSTANDING HOW CONSUMERS SHOP

DESIRE REQUIRE

§ The classification is built from Shopper Dimensions and uses the metrics collected in exit surveys to objectively put all shoppers into each detailed Shopper Missions category.

DESTINATION LED LOCALLY DRIVEN PURPOSE DRIVEN

CCI | Commercial in Confidence © CACI Ltd, 2015

40

Source: Shopper Missions

LEISURE DOMINATED TRIP

FAMILY DAY OUT

FRIENDS BROWSING

PAIR/ SINGLE DOING BIG SHOP

FRIENDS BIG DAY OUT

WINDOW SHOPPING

CONVENIENT GROCERY SHOPPING

CONVENIENT LEISURE

LOCAL NEIGHBOURHOOD

SHOPPERS

KILLING TIME

WEEKLY GROCERY SHOP

THE NECESSARY EVIL

THE BIG TICKET SHOP

SINGLE ITEM PICK-UP

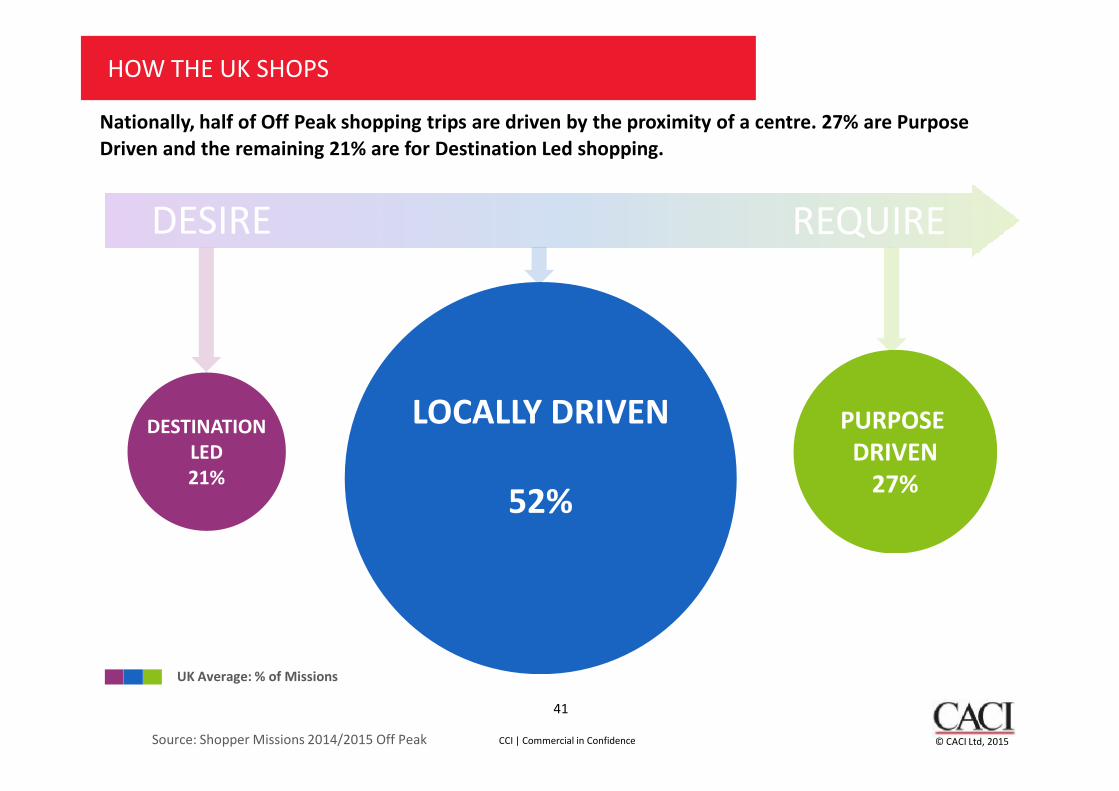

HOW THE UK SHOPS

LOCALLY DRIVEN

Nationally, half of Off Peak shopping trips are driven by the proximity of a centre. 27% are Purpose Driven and the remaining 21% are for Destination Led shopping.

DESIRE REQUIRE

CCI | Commercial in Confidence © CACI Ltd, 2015

41

PURPOSE DRIVEN

27%

DESTINATIONLED21%

LOCALLY DRIVEN

52%

Source: Shopper Missions 2014/2015 Off Peak

UK Average: % of Missions

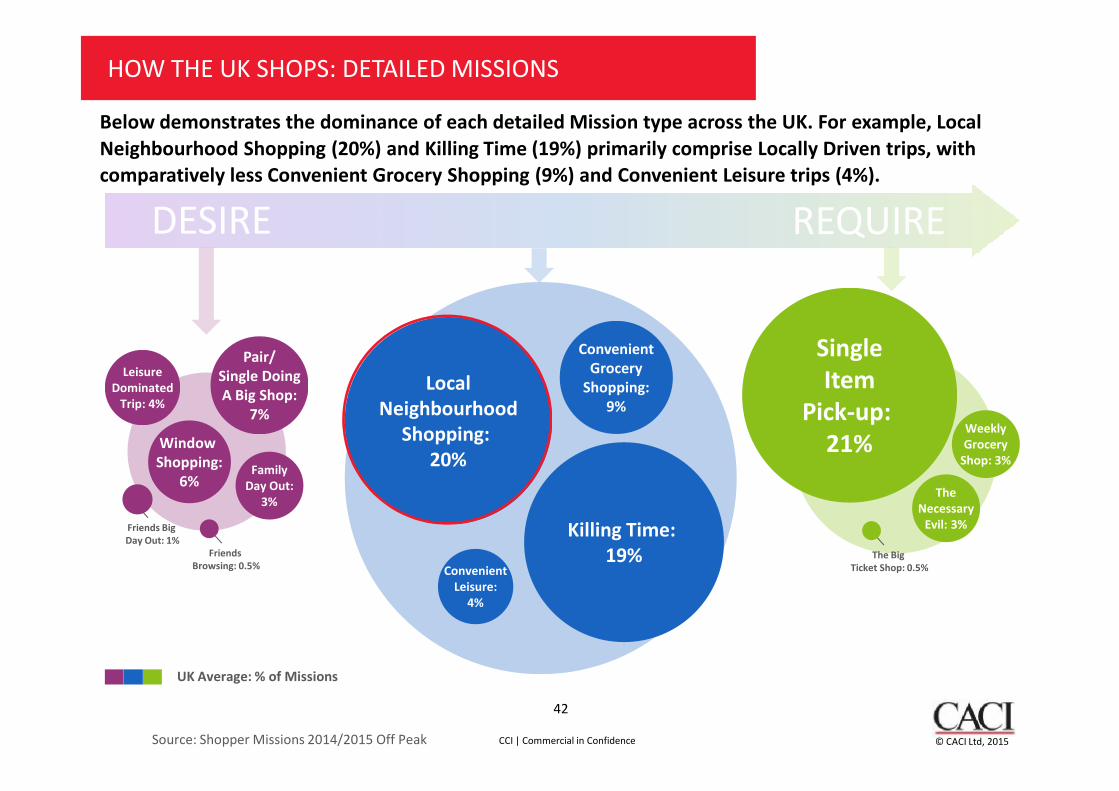

HOW THE UK SHOPS: DETAILED MISSIONS

SingleItem

Pick-up: Local

Neighbourhood

Below demonstrates the dominance of each detailed Mission type across the UK. For example, Local Neighbourhood Shopping (20%) and Killing Time (19%) primarily comprise Locally Driven trips, with comparatively less Convenient Grocery Shopping (9%) and Convenient Leisure trips (4%).

DESIRE REQUIRE

ConvenientGrocery

Shopping:

Pair/Single DoingA Big Shop:

LeisureDominated

CCI | Commercial in Confidence © CACI Ltd, 2015

42

ItemPick-up:

21%

LocalNeighbourhood

Shopping: 20%

Source: Shopper Missions 2014/2015 Off Peak

UK Average: % of Missions

Killing Time: 19%

Shopping:9%

ConvenientLeisure:

4%

WeeklyGrocery

Shop: 3%

TheNecessary

Evil: 3%

The BigTicket Shop: 0.5%

A Big Shop:7%

Friends Browsing: 0.5%

Friends Big Day Out: 1%

FamilyDay Out:

3%

Window Shopping:

6%

DominatedTrip: 4%

LOCAL NEIGHBOURHOOD SHOPPERS

They typically visit 2 or 3 stores but tend to have low

CCI | Commercial in Confidence © CACI Ltd, 2015

43

They typically visit 2 or 3 stores but tend to have low total spend. They tend to visit alone or with another shopper and have a below average drivetime.

LOCAL NEIGHBOURHOOD SHOPPERS

£34 Below average

100% Above average

69 min Average

CCI | Commercial in Confidence © CACI Ltd, 2015

44

69 min Average

£6 Below average

32% Average

LOCAL NEIGHBOURHOOD SHOPPERS’ TOP BRANDS

CCI | Commercial in Confidence © CACI Ltd, 2015

45

LOCAL NEIGHBOURHOOD SHOPPERS

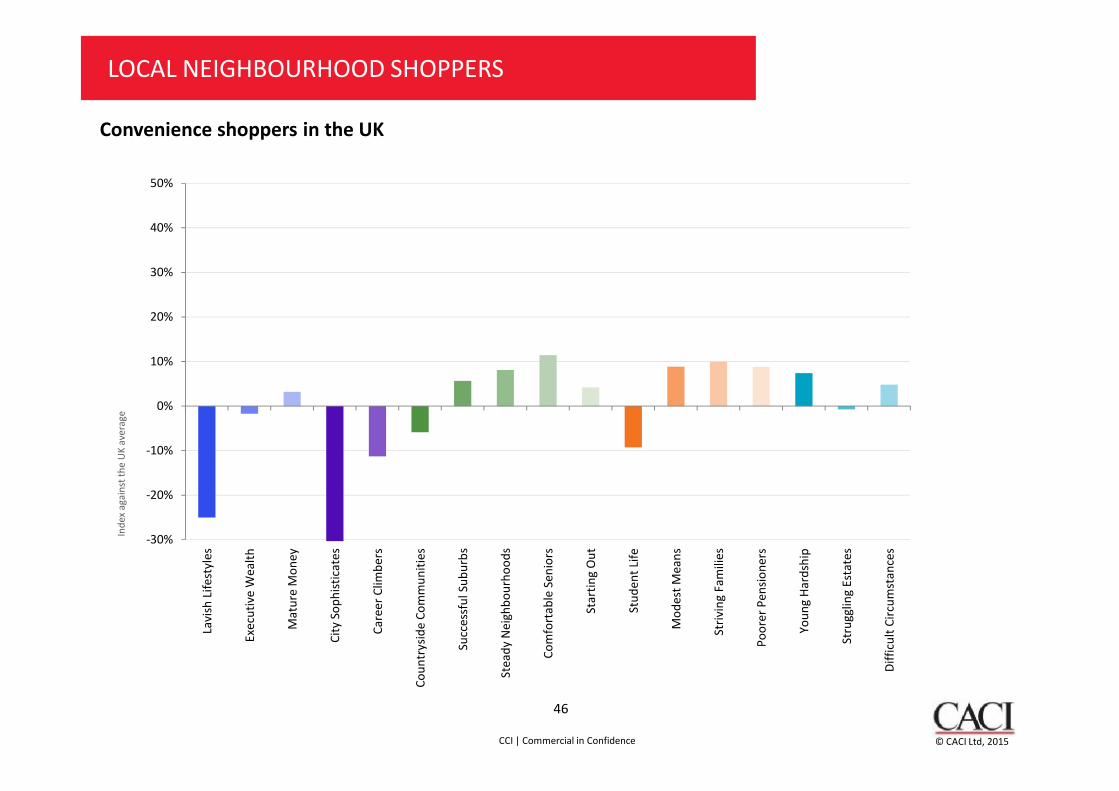

Convenience shoppers in the UK

10%

20%

30%

40%

50%

CCI | Commercial in Confidence © CACI Ltd, 2015

46

-30%

-20%

-10%

0%

Lavi

sh L

ifest

yles

Exec

utiv

e W

ealth

Mat

ure

Mon

ey

City

Sop

hist

icat

es

Care

er C

limbe

rs

Coun

trys

ide

Com

mun

ities

Succ

essf

ul S

ubur

bs

Stea

dy N

eigh

bour

hood

s

Com

fort

able

Sen

iors

Star

ting

Out

Stud

ent L

ife

Mod

est M

eans

Striv

ing

Fam

ilies

Poor

er P

ensio

ners

Youn

g Ha

rdsh

ip

Stru

gglin

g Es

tate

s

Diffi

cult

Circ

umst

ance

s

Inde

x ag

ains

t the

UK

aver

age

9centres visited

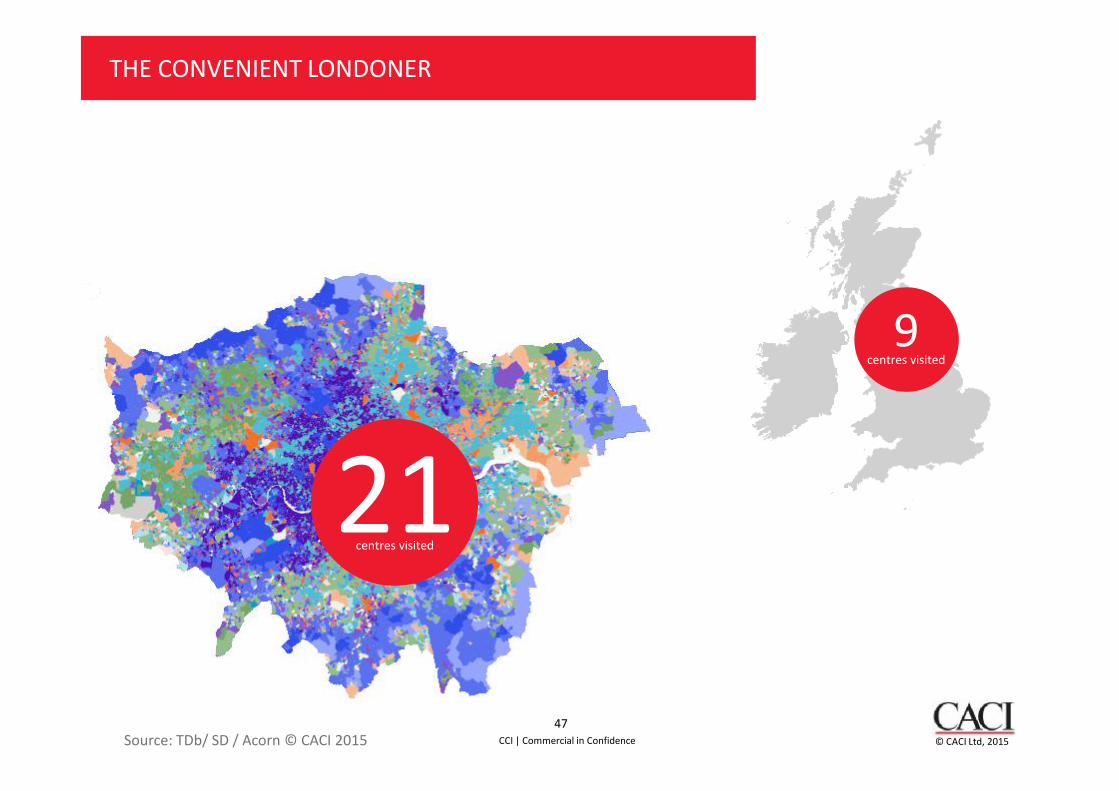

THE CONVENIENT LONDONER

CCI | Commercial in Confidence © CACI Ltd, 2015

47

centres visited

Source: TDb/ SD / Acorn © CACI 2015

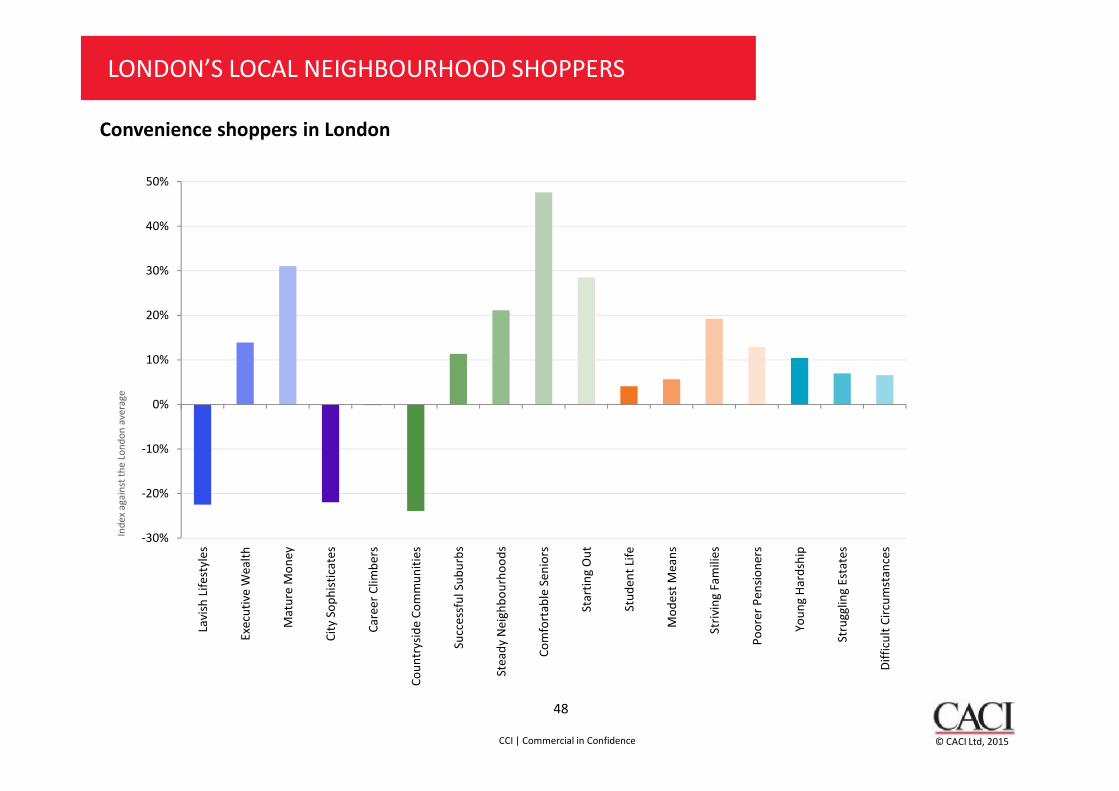

LONDON’S LOCAL NEIGHBOURHOOD SHOPPERS

Convenience shoppers in London

10%

20%

30%

40%

50%

Inde

x ag

ains

t the

Lon

don

aver

age

CCI | Commercial in Confidence © CACI Ltd, 2015

48

-30%

-20%

-10%

0%

Lavi

sh L

ifest

yles

Exec

utiv

e W

ealth

Mat

ure

Mon

ey

City

Sop

hist

icat

es

Care

er C

limbe

rs

Coun

trys

ide

Com

mun

ities

Succ

essf

ul S

ubur

bs

Stea

dy N

eigh

bour

hood

s

Com

fort

able

Sen

iors

Star

ting

Out

Stud

ent L

ife

Mod

est M

eans

Striv

ing

Fam

ilies

Poor

er P

ensio

ners

Youn

g Ha

rdsh

ip

Stru

gglin

g Es

tate

s

Diffi

cult

Circ

umst

ance

s

Inde

x ag

ains

t the

Lon

don

aver

age

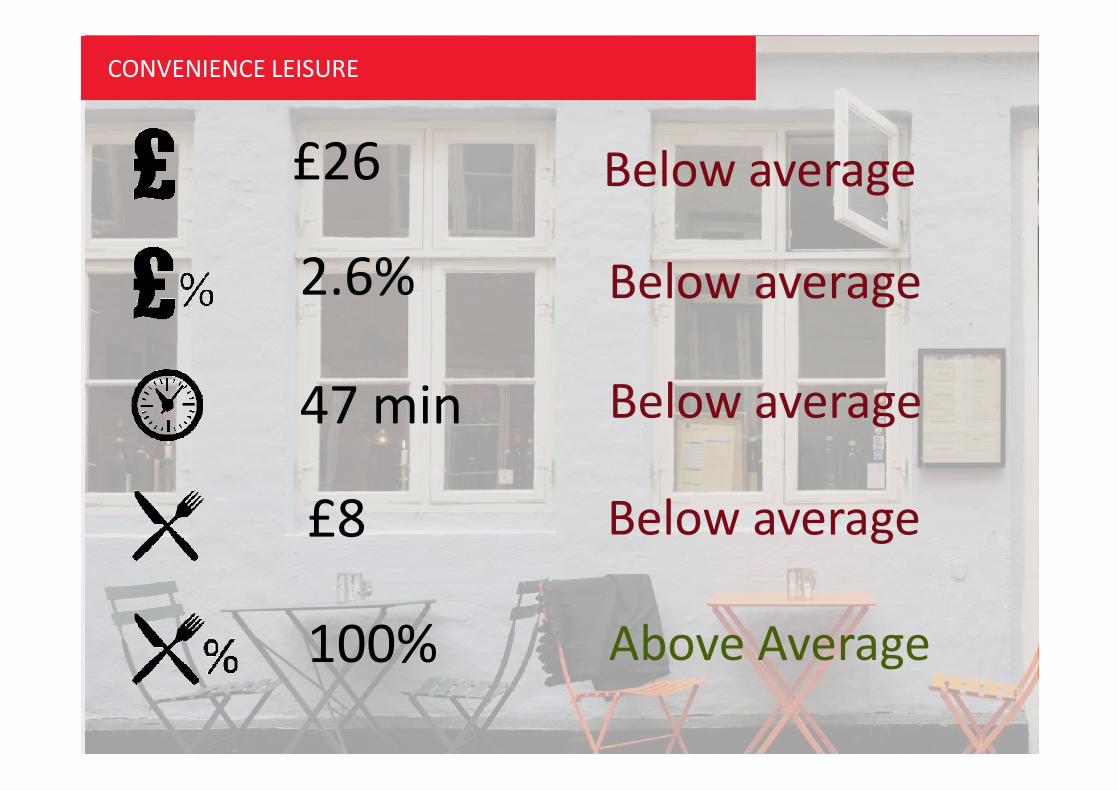

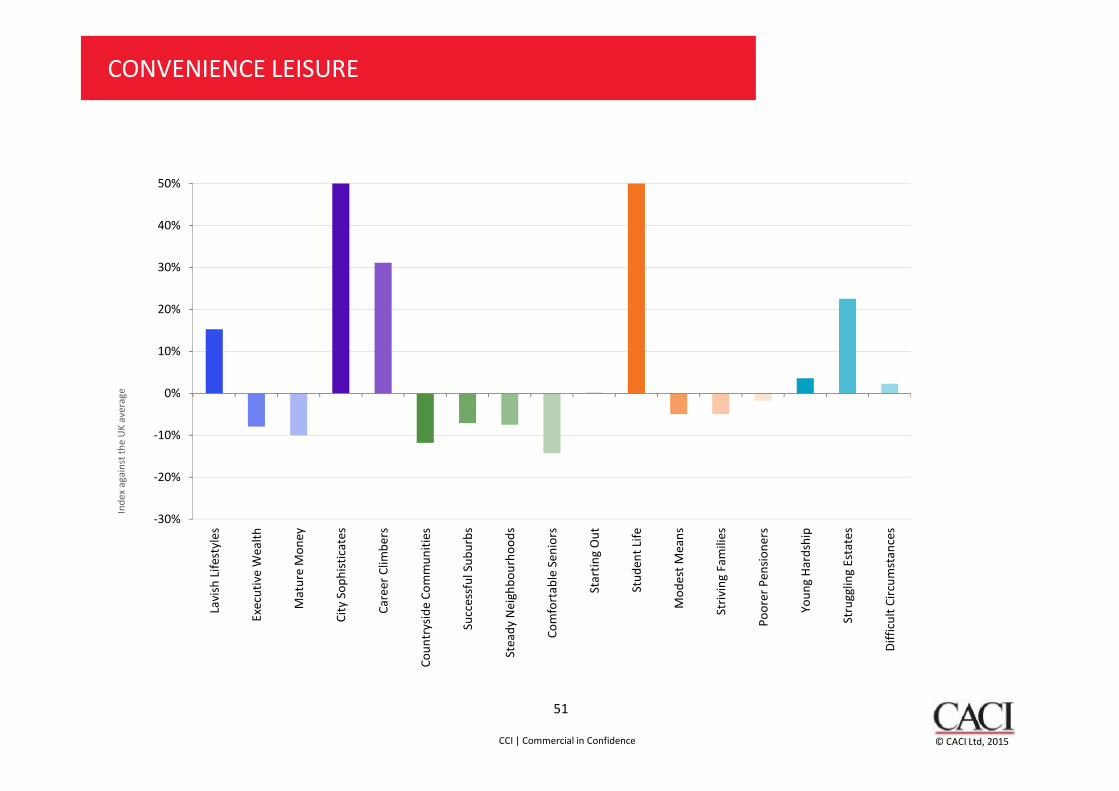

CONVENIENCE LEISURE

These trips are quick and are dominated by low

CCI | Commercial in Confidence © CACI Ltd, 2015

49

These trips are quick and are dominated by low value catering engagement – typically a café or takeaway. The trip is likely to include a visit to a retailer but spend is very unlikely.

CONVENIENCE LEISURE

£26 Below average

2.6% Below average

47 min Below average

CCI | Commercial in Confidence © CACI Ltd, 2015

50

47 min Below average

£8 Below average

100% Above Average

CONVENIENCE LEISURE

0%

10%

20%

30%

40%

50%

Inde

x ag

ains

t the

UK

aver

age

CCI | Commercial in Confidence © CACI Ltd, 2015

51

-30%

-20%

-10%

0%

Lavi

sh L

ifest

yles

Exec

utiv

e W

ealth

Mat

ure

Mon

ey

City

Sop

hist

icat

es

Care

er C

limbe

rs

Coun

trys

ide

Com

mun

ities

Succ

essf

ul S

ubur

bs

Stea

dy N

eigh

bour

hood

s

Com

fort

able

Sen

iors

Star

ting

Out

Stud

ent L

ife

Mod

est M

eans

Striv

ing

Fam

ilies

Poor

er P

ensio

ners

Youn

g Ha

rdsh

ip

Stru

gglin

g Es

tate

s

Diffi

cult

Circ

umst

ance

s

Inde

x ag

ains

t the

UK

aver

age

CCI | Commercial in Confidence © CACI Ltd, 2015

52

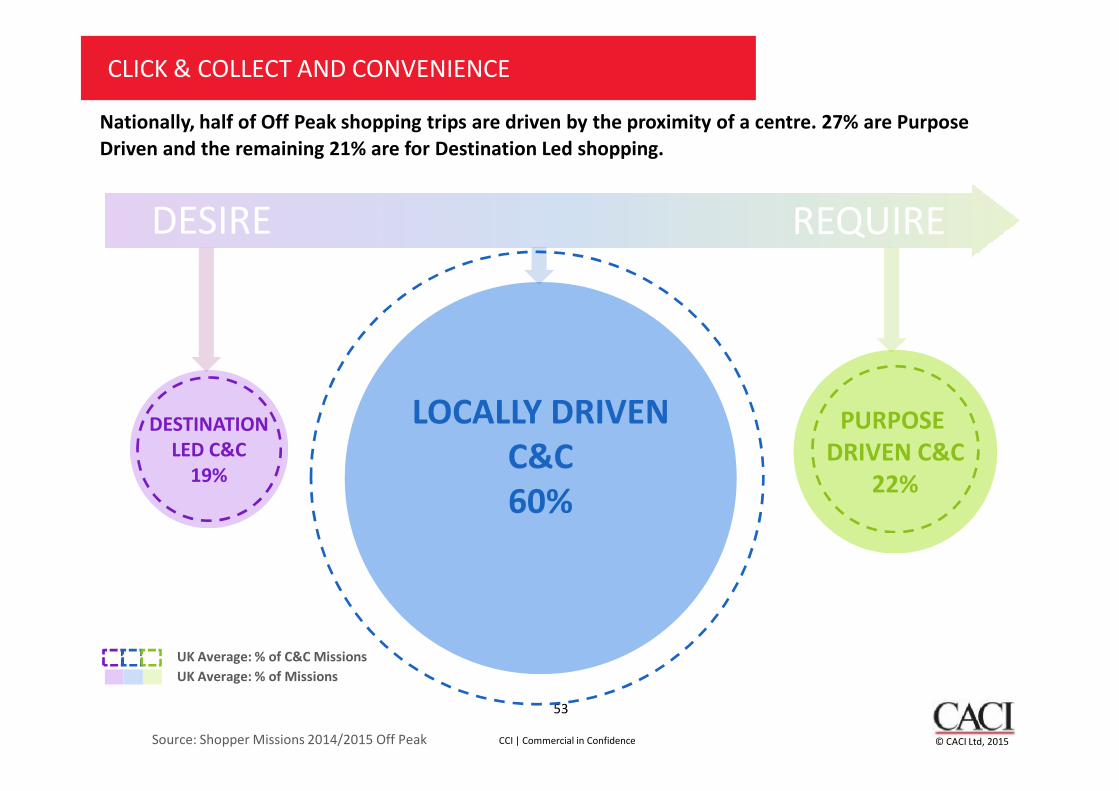

CLICK & COLLECT AND CONVENIENCE

LOCALLY DRIVEN

Nationally, half of Off Peak shopping trips are driven by the proximity of a centre. 27% are Purpose Driven and the remaining 21% are for Destination Led shopping.

DESIRE REQUIRE

CCI | Commercial in Confidence © CACI Ltd, 2015

53

PURPOSE DRIVEN C&C

22%

DESTINATIONLED C&C

19%

LOCALLY DRIVEN C&C60%

Source: Shopper Missions 2014/2015 Off Peak

UK Average: % of MissionsUK Average: % of C&C Missions

CCI | Commercial in Confidence © CACI Ltd, 2015

54

Alex McCulloch

020 7605 6223

@AlexMcRetail / @Caci_LocStrat

Undergraduate Awards 2015

Presentation to winners

28th September 2015

Background

• Inaugural SLA Undergraduate Awards• Designed to recognise outstanding

achievements in the field of location analysis• Dissertations and extended projects• Dissertations and extended projects• Applications received from a range of sectors• Judging panel independently selected winners• Same again for 2016 – please help us to

promote this…!

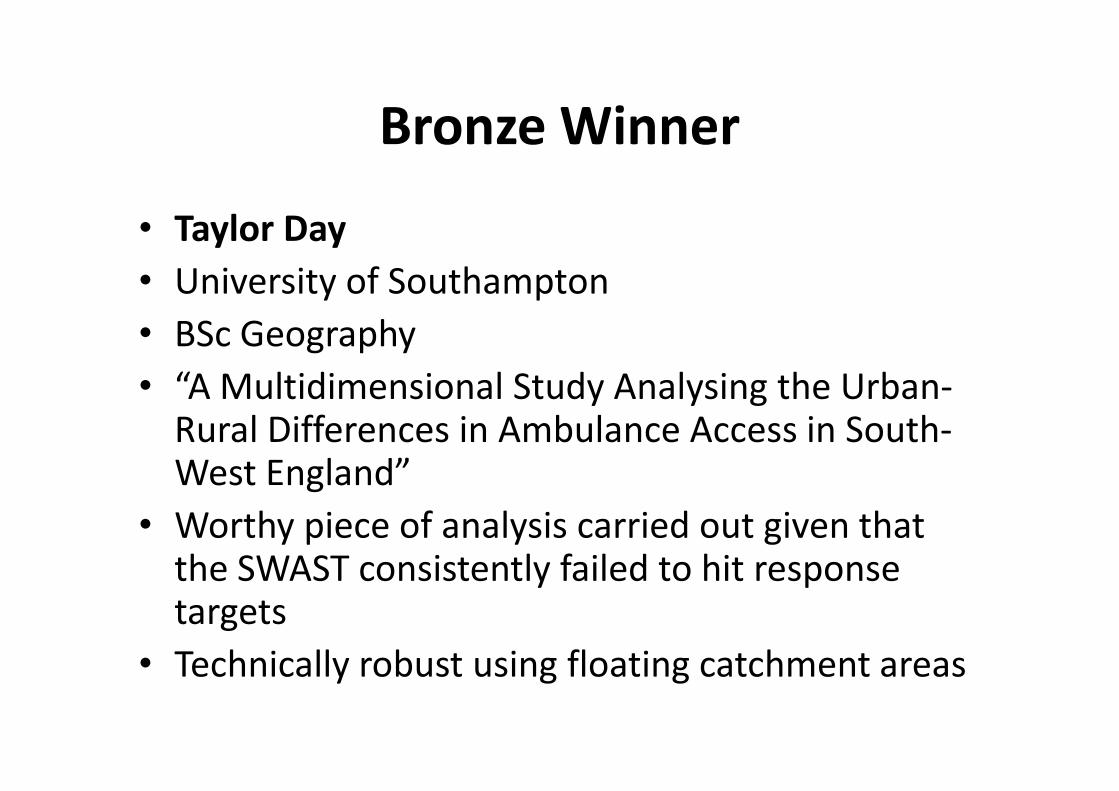

Bronze Winner

• Taylor Day• University of Southampton• BSc Geography• “A Multidimensional Study Analysing the Urban-• “A Multidimensional Study Analysing the Urban-

Rural Differences in Ambulance Access in South-West England”

• Worthy piece of analysis carried out given that the SWAST consistently failed to hit response targets

• Technically robust using floating catchment areas

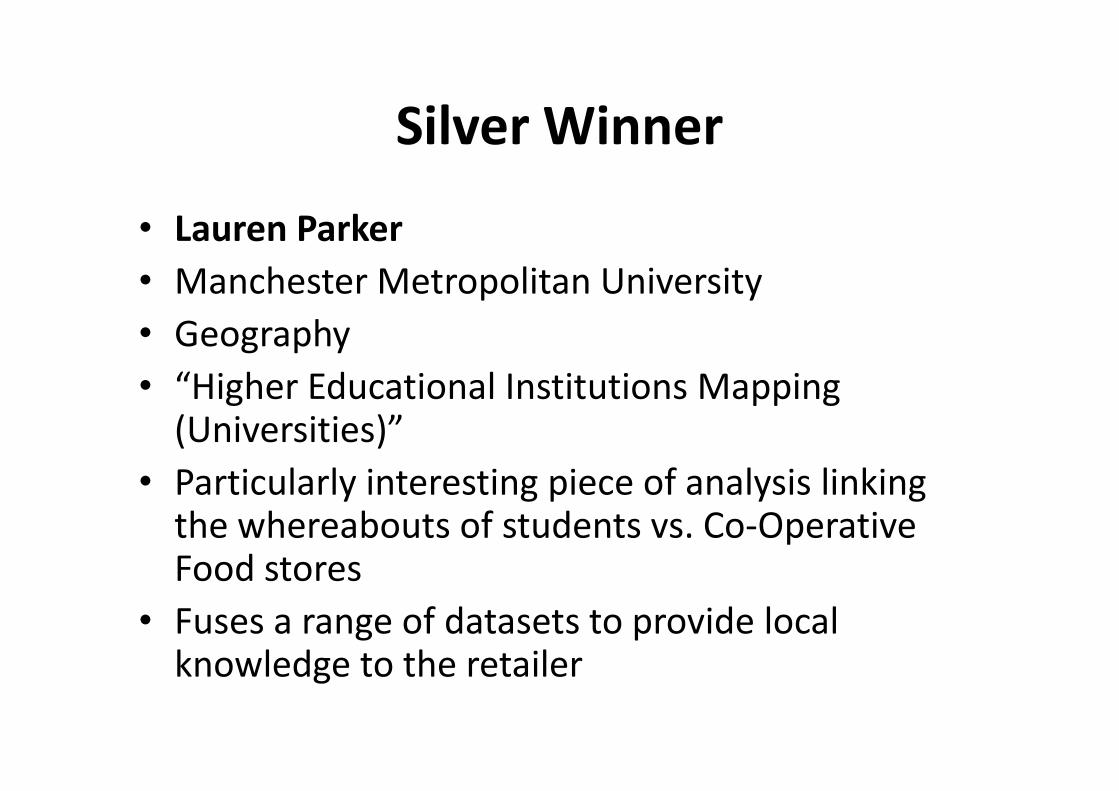

Silver Winner

• Lauren Parker• Manchester Metropolitan University• Geography• “Higher Educational Institutions Mapping • “Higher Educational Institutions Mapping

(Universities)”• Particularly interesting piece of analysis linking

the whereabouts of students vs. Co-Operative Food stores

• Fuses a range of datasets to provide local knowledge to the retailer

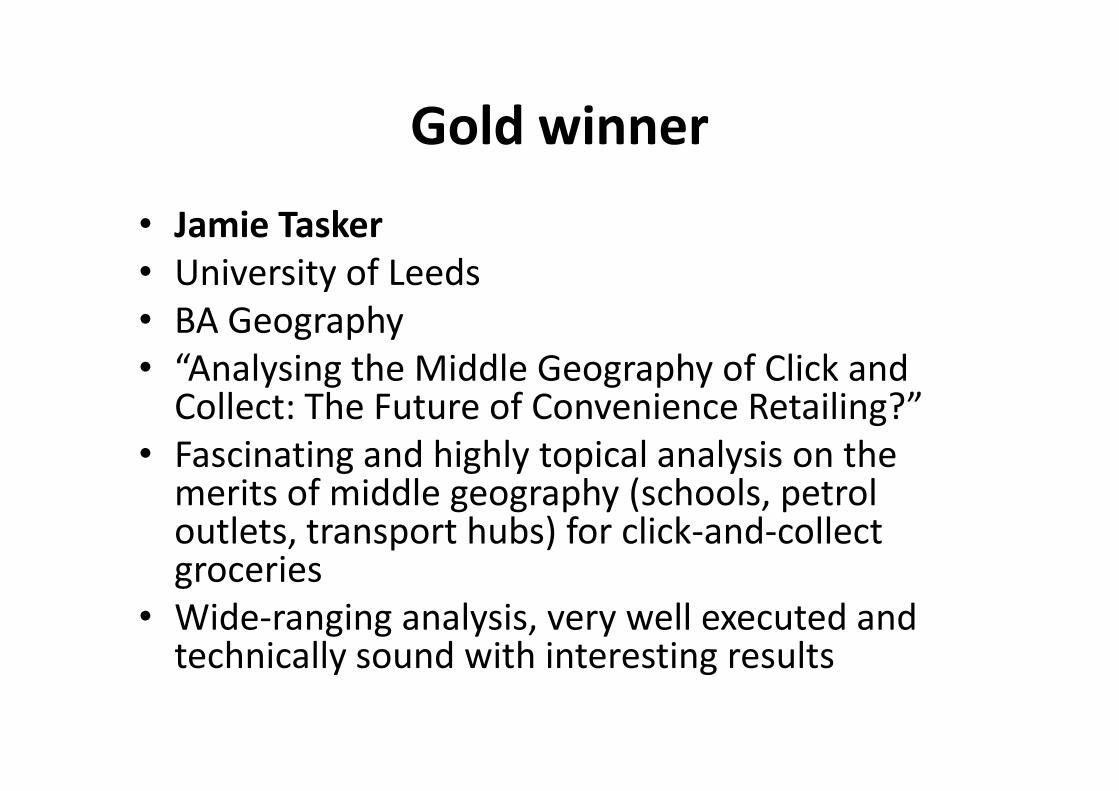

Gold winner• Jamie Tasker• University of Leeds• BA Geography• “Analysing the Middle Geography of Click and

Collect: The Future of Convenience Retailing?”Collect: The Future of Convenience Retailing?”• Fascinating and highly topical analysis on the

merits of middle geography (schools, petrol outlets, transport hubs) for click-and-collect groceries

• Wide-ranging analysis, very well executed and technically sound with interesting results