RECONCILIATION OF COST AND FINANCIAL … or over-absorption of ... reconciliation statement, ......

128

1 LESSON 1 RECONCILIATION OF COST AND FINANCIAL ACCOUNTS - I 1.0 Introduction 1.1 Objectives 1.2 Requirement for Reconciliation 1.3 Reasons for difference in Profit/Loss 1.4 System of Reconciliation 1.5 Memorandum Reconciliation Account 1.6 Summary of the chapter 1.7 Exercise 1.1 Objectives After studying this chapter, you would be able to: Understand the meaning and need of reconciliation of cost accounts and financial accounts Explain the reasons for difference in profit or loss as per cost and financial accounts Know the method of preparing a reconciliation statement or a memorandum reconciliation account When cost accounts and financial accounts are maintained separately in two different sets of books, two profit and loss accounts will be prepared-one for costing books and the other for financial books. The profit or loss shown by financial books may not agree with that shown by costing books. So, both sets of books are tallied to know the reasons for disagreement of the two profits. It is essential to know that the question of reconciliation of cost and financial accounts arises only under non-integral system. However, under the integral accounts, the problem of reconciliation does not arise since cost and financial accounts are integrated into one set of books and only one Profit and Loss Account is prepared. 1.2 Requirement for Reconciliation The necessity for reconciliation arises owing to the following reasons- 1. It discloses the causes for variance in profit or loss between cost and financial accounts. 2. Reconciliation aids in checking the arithmetic accuracy of both sets of books. In other words, it enables to test the reliability of cost accounts. 3. It promotes coordination between cost accounting and financial accounting departments.

Transcript of RECONCILIATION OF COST AND FINANCIAL … or over-absorption of ... reconciliation statement, ......

1

LESSON 1

RECONCILIATION OF COST AND FINANCIAL ACCOUNTS - I

1.0 Introduction

1.1 Objectives

1.2 Requirement for Reconciliation

1.3 Reasons for difference in Profit/Loss

1.4 System of Reconciliation

1.5 Memorandum Reconciliation Account

1.6 Summary of the chapter

1.7 Exercise

1.1 Objectives

After studying this chapter, you would be able to:

Understand the meaning and need of reconciliation of cost accounts and

financial accounts Explain the reasons for difference in profit or loss as per cost and financial accounts

Know the method of preparing a reconciliation statement or a memorandum

reconciliation account When cost accounts and financial accounts are maintained separately in two different sets of

books, two profit and loss accounts will be prepared-one for costing books and the other for

financial books. The profit or loss shown by financial books may not agree with that shown by

costing books. So, both sets of books are tallied to know the reasons for disagreement of the

two profits.

It is essential to know that the question of reconciliation of cost and financial accounts

arises only under non-integral system. However, under the integral accounts, the problem

of reconciliation does not arise since cost and financial accounts are integrated into one set

of books and only one Profit and Loss Account is prepared.

1.2 Requirement for Reconciliation The necessity for reconciliation arises owing to the following reasons-

1. It discloses the causes for variance in profit or loss between cost and

financial accounts.

2. Reconciliation aids in checking the arithmetic accuracy of both sets of

books. In other words, it enables to test the reliability of cost accounts.

3. It promotes coordination between cost accounting and financial accounting

departments.

2

1.3 Reasons for difference in Profit/Loss

Difference in profit or loss between cost and financial accounts may arise due to the

following reasons:

1. Items shown in cost accounts only- There are a few items which are included

in cost accounts and not in financial accounts. Examples:

• The notional cost of employing capital (Interest on capital employed but

not actually paid.)

• Notional rent (charge in lieu of rent when premises are owned and no

rent is payable), Notional salaries

• Notional depreciation (Depreciation on fully depreciated assets still in use)

2. Items shown only in financial accounts -there are a number of items which does

not appear in cost accounts but shown in financial accounts. At the time of reconciling,

any items under this category must be taken under consideration. Following are the

examples of such items.

(a) financial incomes

▪ Income tax refund

▪ Transfer fees received

▪ Dividend and interest received on investments

▪ Interest received on bank deposits

▪ Rent receivable

(b) financial expenses

• Loss on the sale of capital assets

• Amounts written off, goodwill, discount on debentures, preliminary expenses

• Provision for bad and doubtful debts

• Loss due to theft, pilferage, etc.

• Interest on bank loans and mortgages etc.

3. Under-absorption or over-absorption of overheads - overheads are recovered

at a predetermined rate in cost accounts while in financial accounts overheads are

recorded at actual cost. It causes difference in profit shown by cost accounts and

financial accounts.

4. Bases of stock valuation - stock valuation in financial accounts is based on the

principle of cost or market price whichever is less. Whereas stocks are valued

according to the method adopted in stores accounts, e.g. FIFO, LIFO, etc in cost

accounts. Different stock values result in some difference in profit or loss as shown

by the two sets of account books.

5. Different charges for depreciation- in financial accounts, depreciation may be

charged at straight line or diminishing balance method, etc., whereas machine hour

rate, production unit method, etc., may be adopted in cost accounts. This will also

cause a difference in the profit/ loss figures.

3

1.4 SYSTEM OF RECONCILIATION

The financial and cost accounts are reconciled by preparing a Reconciliation Statement or a

Memorandum Reconciliation Account. The following procedure is suggested for preparing

a Reconciliation Statement:

1. Start with the profit as per cost accounts.

2. Additions/ deductions regarding items

(a) expenses and losses:

Deduct: Items under-charged in cost accounts

Add: Items over-charged in cost accounts

For example, depreciation in cost accounts is Rs. 2,700 and that

in financial accounts is Rs. 2,900. There will be increase in costing

profit by Rs. 200 as compared to financial profit. Then in order to

reconcile, there will be deduction of Rs 200 from costing profit.

(b) Incomes and gains:

Deduct: Items over-recorded in cost accounts

Add: Items under-recorded or not recorded in cost accounts

For example, interest on investments received amounting to Rs.

2500 is not recorded in cost accounts. It will have negative effect in

profit as per cost books. So to reconcile, this amount of Rs. 2500 for

interest should be added in the costing profit.

(c) valuation of stock:

• Opening Stock-

Deduct: Amount of under-valuation in cost accounts

Add: Amount of over-valuation in cost accounts

• Closing Stock-

Deduct: Amount of over-valuation in cost accounts

Add: Amount of under-valuation in cost accounts

6. Closing stock of finished goods in cost accounts in calculated on the basis of cost

of production. Thus

Value of closing stock = Cost of production X Units Produced

Units of Closing Stock

Here

Units Produced =Units sold+ Units in closing stock - Units in opening stock

4. After making all the above additions and deductions in costing profit, the result will

be the profit as per financial books.

4

5. The above treatment of items will be reversed when the starting point in the

Reconciliation Statement is the profit as per financial accounts or loss as per cost

accounts.

Proforma of Reconciliation Statement Rs. Rs.

Profit as per cost accounts

Add:

• Financial incomes not recorded in cost books

• Items charged only in cost accounts

(Notional rent and interest on capital, etc.)

Over-absorption of overheads

• Over-valuation of opening stocks in cost books

• Under-valuation of closing stock in cost books

Less: . Under-absorption of overheads

• financial charges

• Under-valuation of opening stock in cost books

• Over-valuation of closing stock in cost books Profit as per financial accounts

Memorandum Reconciliation Account

It is a method of Reconciliation. The only difference is that the information is

shown in the form of an account. The procedure of its preparation is like that of

reconciliation statement, the only difference is that items shown under "+" column are

shown on the credit side and items shown under "-" column are shown on the debit side of

the memorandum reconciliation account. Proforma of Memorandum Reconciliation Account

Rs.

To (Item to be deducted) -

To (Item to be deducted) -

To (Item to be deducted) -

To (Item to be deducted) -

To (Item to be deducted) -

-(Balancing figure)

Rs.

To Profit as per financial

accounts

By (Item to be added) -

By (Item to be added) -

By (Item to be added) -

By (Item to be added) -

By (Item to be added) -

5

PROBLEMS AND SOLUTIONS

Illustration.1 From the following figures, prepare a reconciliation statement:

Rs.

Net profit as per financial books 31890

Net profit as per costing books 33380

Factory overheads under-recovered in costing 2850

Administration overheads recovered in excess 2125

Depreciation charged in financial books 1830

Depreciation recovered in costing 1975

Interest received but not included in costing 225

Income-tax provided in financial books 300

Bank interest credited in financial books 115

Stores adjustment (credited in financial books) 210

Depreciation of stock charged in financial accounts 430

Dividends appropriate in financial accounts 600

Loss due to theft and pilferage provided only in financial books 130

Solution

Reconciliation Statement

Rs. Rs.

Profit as per costing books 33380

Add: 1. Adm. overheads recovered in excess 2125

2. Depreciation overcharged in cost books (1975 - 1830) 145

3. Interest received but not included in costing 225

4. Bank interest credited in financial books only 115

5. Stores adjustment credited in financial books 210 2820

36200

Less: 1. Factory overheads under-recovered 2850

2. Income tax provided in financial books 300

3. Dividends appropriated 600

4. Depreciation of stock in financial books 430

5. Loss due to theft and pilferage not shown in cost books 130

4310

Profit as per financial books 31890

6

Illustration 2.

The profits as per cost accounts were Rs. 14,330, whereas the net profit as per

financial accounts of a company amounted to Rs. 9275. On reconciling the figure,

the following were noted:

Rs.

Director's fees not charged in cost accounts 525

A provision for bad and doubtful debts 485

Bank interest credited 15

Provision for income-tax 4150

Over-recovery of overhead in cost accounts 90

Prepare reconciliation statement. Also prepare memorandum

reconciliation account.

Solution

Reconciliation Statement

Particulars Rs. (+) Rs. (-)

Profit as per Cost Accounts 14,330

Less: Directors Fees not charged in Cost Account 525

Less: Provision for bad debts. not shown in Cost Accounts 485

Add: Bank interest credited in Profit & Loss Account 15

Less: Provision for income tax not shown in Cost Accounts 4150

Add: Over-recovery of overhead in Cost Accounts 90

14435 5160

Profit as per Financial Accounts 9275

14,435 14,435

Memorandum Reconciliation Account

Particulars Rs. Particulars Rs.

To Director's fees not By Profit as per Cost A/cs 14,435

charged in Cost A/c 525 By Bank Interest credited

15

To Provision for Bad Debts 485 in Profit and Loss A/c

To Provision for Income Tax 4150 By Over Recovery of

90

To Profit as per Financial A/cs 9275 Overhead in Cost A/c

14,330 14,330

7

Illustration 3.

From the following figures prepare a reconciliation statement:

Rs.

Profit as per costing records 10,000

Factory overheads under-recovered in costing 6,000

Selling and administration overheads over-recovered in costing 4,000

Bank interest credited in financial books 1000

Preliminary expenses written off in financial books 13000

Opening stock value:

in cost books 10000

in financial books 8000

Closing stock value:

in cost books 24000

in financial books 20,000

Solution (Do it yourself)

Reconciliation Statement

Particulars Rs. (+) Rs. (-)

Profit as per Cost A/cs 10,000

Add: Selling and administration overheads over-recovered _____

in Cost A/cs ____

Add: Bank Interest credited in Financial Books ______

Add: Opening Stock over valued in Costing Books

Less: Factory overheads under recovered in Cost A/cs _____

Less: Preliminary expenses written off in Financial Books ______

Less: Closing Stock overvalued in Costing Books _____

Loss as per Financial A/cs ______ _____

______

_______ _____

8

Illustration 4.

From the following figures,

prepare a reconciliation statement:

Cost Books Financial Books

Profit 25000 ?

Marketing overheads 4000 4,000

Provision for bad debts - 2500

Factory overheads 4250 3500

Director's fees - 1,000

Income Tax paid - 7500

Rent of owned Premises 3,000 -

Depreciation 5625 6,000

Share transfer fee (Cr.) - 500

Administrative overheads 2500 4,000

Solution

Reconciliation Statement

Particulars Rs - (+) Rs. (-)

Profit as per cost books 25000

Less: Provision for bad debts charged in financial books 2500

Add: Factory overheads over-absorbed in cost accounts 750

Less: Director's fees charged in financial books 1,000

Less: Income tax charged in financial books 7500

Add: Rent of owned premises charged in cost books 3,000

Less: Depreciation overcharged in financial books 375

Add: Share transfer fees credited in financial books 500

Less: Administrative overheads under absorbed in cost books 1500

29250

12875

Profit as per Financial Books 16375

29250 29250

9

Illustration 5 From the following information, reconcile the profit as per cost accounts with financial

accounts:

Cost A/c Financial A/c

Rs. Rs.

Profit 86,250

Opening Stock:

Material 10,000 10,300

Work-in-progress 8,500 8,000

Closing Stock:

Material 14,200 15,000

Work-In-Progress 6,000 5,600

Dividend and interest received Rs. 600. Loss on sale of investment Rs. 1,000. Interest

charged by the bank not considered in Financial Accounts and Cost Accounts Rs. 1,500.

Goodwill written off during the year Rs. 2,500. Preliminary expenses written off Rs. 3,000.

Overhead incurred Rs. 40,000. Overhead absorbed in Cost Accounts Rs. 38,500. Find out

profit as per financial accounts.

Solution (Do it yourself)

Reconciliation Statement

Particulars Rs. (+) Rs. (-)

Profit as per Cost Accounts 86,250

Add: Overvaluation of opening stock of material in

cost Accounts _____

Add: Overvaluation of opening stock of work-in-

progress in cost accounts _____

Add: Undervaluation of closing stock of material

in cost accounts _____

Less: Overvaluation of closing stock of work-in-progress

in cost accounts ______

Add: Dividend and interest credited in financial accounts ______

Less: Goodwill written off not recorded in cost accounts ______

Less: Preliminary expenses written off not recorded

in cost Accounts _______

Less: Loss on sale of investment not recorded in cost accounts ______

Less: Under-absorption of overheads in cost accounts _______

88,350 8,400

Profit as per Financial Accounts 79,950

88,350 88,350

Working Note: Interest charged by the bank not considered in Financial Accounts as

well as Cost Accounts will not be shown in Reconciliation Statement.

10

Illustration 6 (Do it yourself) A manufacturing company disclosed a net loss of Rs. 3,47,000 as per their cost accounts for the

year ended March 31, 2004. The financial accounts however disclosed a net loss of Rs.

5,10,000 for the same period. The following information was discovered as a result of

inspection of the figures of both the sets of accounts:

Rs.

Factory overheads under-absorbed 40,000

Administration overheads over-absorbed 60,000

Depreciation charged in Financial Accounts 3,25,000

Depreciation recovered in Cost Accounts 2,75,000

Interest on investments not included in Cost Accounts 96,000

Income-tax provided 54,000

Interest on loan funds in Financial Accounts 2,45,000

Transfer fee (credit in financial books) 24,000

Stores adjustment (credit in financial books) 14,000

Dividend received 32,000

Prepare a statement showing reconciliation between the figure of net loss as per

cost accounts and the figure of net loss shown in the financial books.

Solution (Do it yourself)

Memorandum Reconciliation Account

Particulars Rs. Particulars Rs.

To Net Loss as per Cost By Administration

Accounts 3,47,000 Overheads Over-absorbed ________

To Factory Overheads By Interest on Investments

Under-absorbed ______ not included in costs _______

To Income Tax not recorded By Transfer fees in

in Cost A/c _______ Financial Books ________

To Depreciation under By Stores Adjustment 14,000

absorbed in Cost A/c ________ By Dividend Received 32,000

To Interest on Loan funds in By Net Loss as per

Financial A/c 2,45,000 Financial Books

7,36,000 7,36,000

11

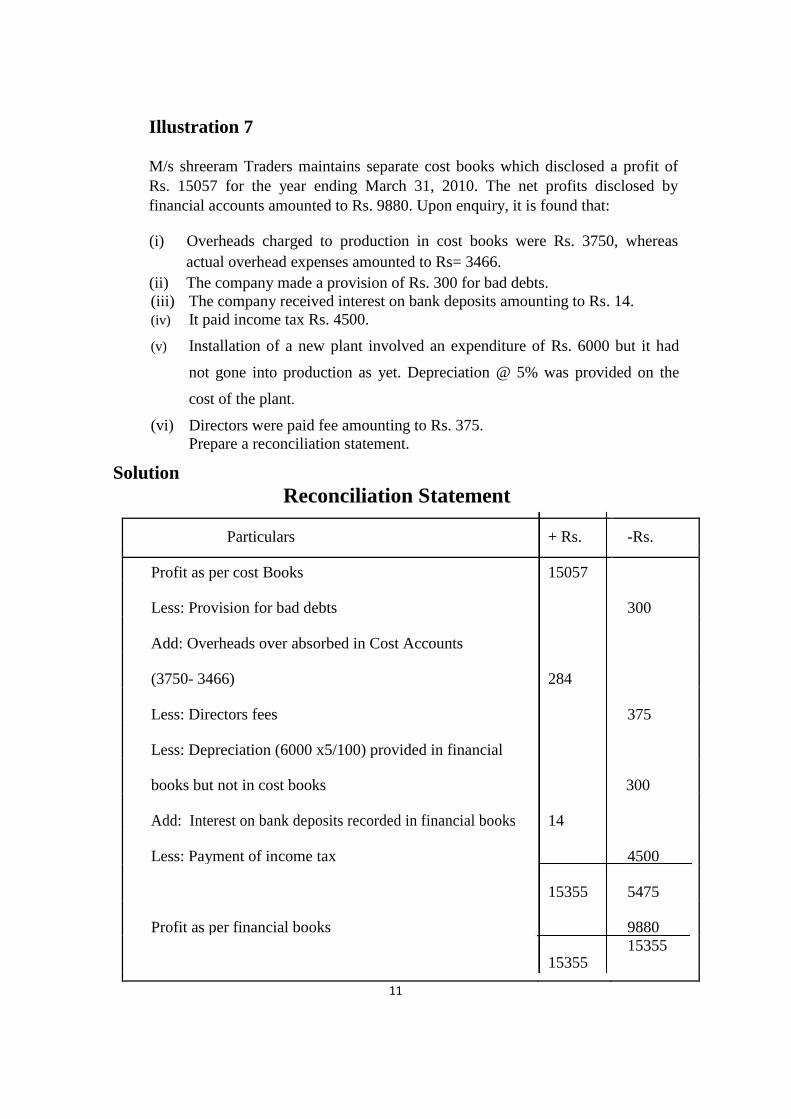

Illustration 7

M/s shreeram Traders maintains separate cost books which disclosed a profit of

Rs. 15057 for the year ending March 31, 2010. The net profits disclosed by

financial accounts amounted to Rs. 9880. Upon enquiry, it is found that:

(i) Overheads charged to production in cost books were Rs. 3750, whereas

actual overhead expenses amounted to Rs= 3466.

(ii) The company made a provision of Rs. 300 for bad debts.

(iii) The company received interest on bank deposits amounting to Rs. 14.

(iv) It paid income tax Rs. 4500.

(v) Installation of a new plant involved an expenditure of Rs. 6000 but it had

not gone into production as yet. Depreciation @ 5% was provided on the

cost of the plant.

(vi) Directors were paid fee amounting to Rs. 375.

Prepare a reconciliation statement.

Solution

Reconciliation Statement

Particulars + Rs. -Rs.

Profit as per cost Books 15057

Less: Provision for bad debts 300

Add: Overheads over absorbed in Cost Accounts

(3750- 3466) 284

Less: Directors fees 375

Less: Depreciation (6000 x5/100) provided in financial

books but not in cost books 300

Add: Interest on bank deposits recorded in financial books 14

Less: Payment of income tax 4500

15355 5475

Profit as per financial books 9880

15355 15355

12

Illustration 8

The following is the Trading and Profit & Loss Account of Sumit Industries Ltd.

for the year ended 31st December, 2016

Rs. Rs.

To Materials 45,000 By Sales (4,800 units) 96,000

To Wages 33,000 By Closing Stock

To Administrative Expenses 240,000 (1,200 units) 20,400

To Net Profit 8,400

1,16,400 1,16,400

The company's cost records show that:

(i) Works Overheads have been absorbed at Rs. 3 per unit produced; and

(ii) Administrative Overheads have been absorbed at Rs. 1.50 per unit produced.

Assuming there is nothing by way of work-in-progress either at the

beginning or at the end and there is no opening stock of finished goods.

Prepare:

(i) A statement of cost indicating the net profit; and

(ii) A statement reconciling the profit as disclosed by cost accounts and that

shown in financial accounts.

Solution:

Statement of Cost

Particulars Rs.

Materials 45,000

Wages 33,000

Prime Cost 78.000

Add: Works overhead (6,000 x 3) 18,000

Works Cost 96,000

Add: Administrative Overhead (6,000 x 1.50) 9,000

Cost of Production 1,05,000

Less: Closing Stock (1,05,000 x 1,200/6,000) 21,000

Cost of Goods sold 84,000

Profit 12,000

Sales 96,000

13

Working Note:

No. of units Produced = No. of units sold

+ No. of units in closing stock = 4.800 + 1.200 = 6,000

Reconciliation Statement

Particulars Rs. (+) Rs. (-)

Profits as per Cost Accounts 12,000

Less: Works overhead under absorbed in Cost

Accounts 6,000

Add: Administrative Overheads over absorbed in

Cost Accounts 3,000

Less: Closing Stock overvalued in Cost Accounts 600

15,000 6,600

Profits as per Profit and Loss A\c - 8,400

15,000 15,000

Illustration 9

The following Profit and Loss Account for the year ending 31st March, 2010 has

been extracted from the books of Awadesh Ltd.

Profit and Loss Accounts for the year ending 31.3.2010

Rs.

To Direct Materials 10,000

To Direct Labour 20,000

To Factory Expenses 9,500

To Administration Expenses 5,200

To Selling and Distribution Expenses 3,800

To Interest on Capital 1,000

To Goodwill written off 1,500

14

To Net Profit 3,000

54,000

By Sales 50,000

By Work-in-Progress in hand:

Direct labour 600

Direct Material 400

Factory Expenses 300 1,300 2,700

By Finished Stock in hand 54,000

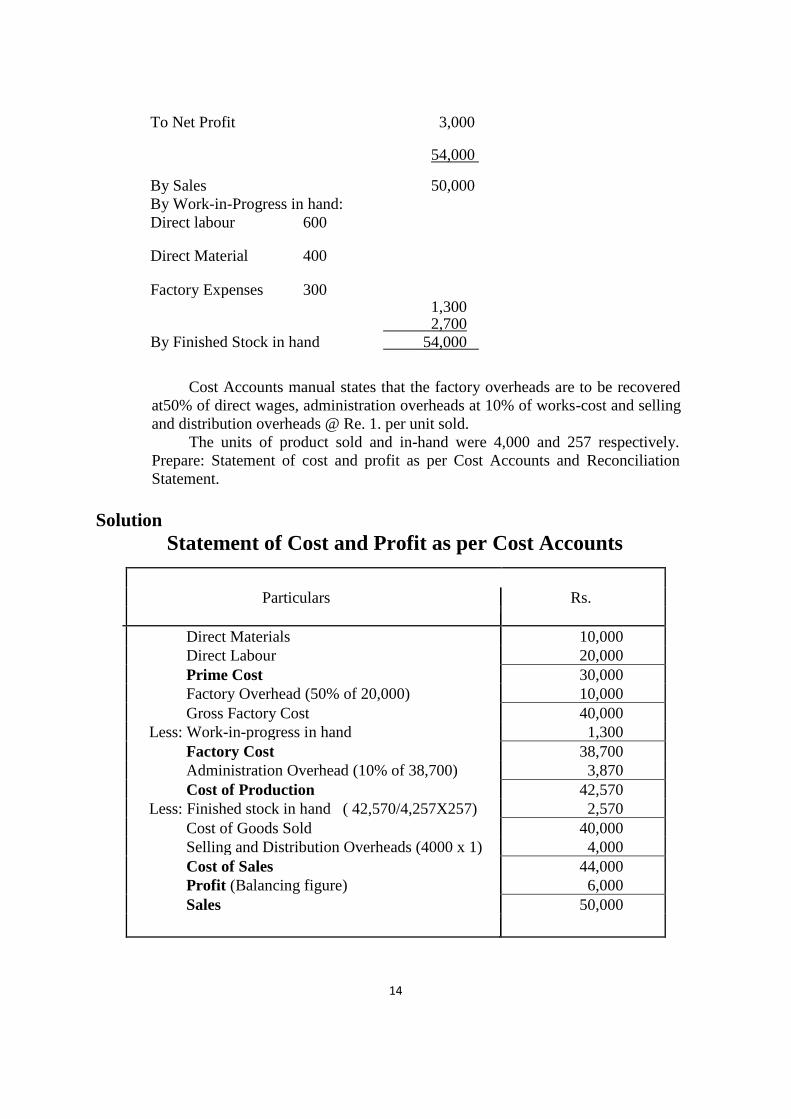

Cost Accounts manual states that the factory overheads are to be recovered

at50% of direct wages, administration overheads at 10% of works-cost and selling

and distribution overheads @ Re. 1. per unit sold.

The units of product sold and in-hand were 4,000 and 257 respectively.

Prepare: Statement of cost and profit as per Cost Accounts and Reconciliation

Statement.

Solution

Statement of Cost and Profit as per Cost Accounts

Particulars

Rs.

Direct Materials 10,000

Direct Labour 20,000

Prime Cost 30,000

Factory Overhead (50% of 20,000) 10,000

Gross Factory Cost 40,000

Less: Work-in-progress in hand 1,300

Factory Cost 38,700

Administration Overhead (10% of 38,700) 3,870

Cost of Production 42,570

Less: Finished stock in hand ( 42,570/4,257X257) 2,570

Cost of Goods Sold 40,000

Selling and Distribution Overheads (4000 x 1) 4,000

Cost of Sales 44,000

Profit (Balancing figure) 6,000

Sales 50,000

15

Reconciliation Statement

Particulars Rs. (+) Rs. (-)

Profit as per Cost Accounts 6,000 -

Add: Factory Expenses over-absorbed in Cost Accounts 500 -

Selling and Distribution Expenses over-absorbed in

Cost Accounts 200 -

Closing stock of finished goods under-valued in

Cost Accounts 130 -

Less: Interest on Capital not shown in Cost Accounts - 1,000

Goodwill written off not shown in Cost Accounts - 1,500

Administration Overhead under-absorbed in

Cost Accounts - 1,330

6,830 3,830

Profit as per Profit and Loss Account (6,830 - 3,830) 3,000

6,830 6,830

Illustration 10 From the following information, prepare:

(a) Profit and Loss Account

(b) Cost Sheet

(c) Reconciliation Statement.

Rs. Units

Sales 2,50,000 20,000

Materials 1,00,000

Wages 50,000

Factory Overheads 45,000

Office and Administration Overheads 26,000

Selling and Distribution Overheads 18,000

Closing Stock: Finished Goods

Work-in-Progress :

Material 3,000

Wages 2,000

Factory Overheads 2,000

7,000

Goodwill written off 20,000

Interest on Capital 2,000

In Costing Books, factory overhead is charged at 100% on wages,

administration overhead at 10% of factory cost and selling and distribution

overheads at the rate of Re. 1 per unit sold.

16

Solution (Do it yourself)

Profit and Loss Account

Particulars Rs. Particulars Rs.

To Materials 1,00,000 By Sales 2,50,000

To Wages 50,000 By Closing stock of finished

To Factory Overheads 45,000 Goods ?

To Office and Administration By Work-in-progress

Overheads 26,000 Materials

To Selling and Distribution Wages

Overheads 18,000 Factory overheads ?

To Goodwill written off 2,000

To Interest on Capital 2,000

To Net Profit 11,000

2,72,000 2,72,000

Cost Sheet

Particulars Rs.

Materials 1,00,000

Wages 50,000

Prime Cost 1,50,000

Factory Overhead ?

Gross Factory Cost 2,00,000

Less: Closing Work-in-Progress 7,000

Factory Cost 1,93,000

Office and Administrative Overheads

(10% of Factory Cost 19,300

Cost of Production 2,12,300

Less: Closing Stock of Finished Goods ?

Cost of Goods Sold 2,00,000

?

Cost of Sales 2,20,000

Profit (Balancing figure) 30,000

Sales 2,50,000

17

Working Notes:

(i) Work-in-progress has been adjusted to calculate factory cost.

(ii) Value of work-in-progress has been taken the same as is given for Profit and

Loss Account.

(iii) Value of closing stock of finished goods has been calculated on the basis of

cost of production.

(iv) Number of Units Produced = Number of Units Sold

+ Number of Units in Closing Stock =

20,000 + 1,230 = 21,230 Units

(v) Selling and distribution overhead is calculated for number of units sold.

Reconciliation Statement

Particulars Rs. (+) Rs. (-)

Profit as per Cost Accounts 30,000 -

Add: Over-absorption of factory overheads in

Cost Accounts ? -

Less: Under-absorption of office and administration

overheads in Cost Accounts - 6700

Add: Over-absorption of selling and distribution

overheads in Cost A/cs ? -

Less: Goodwill written off and interest on capital

not included in Cost Accounts - 2,200

Add: Under-valuation of closing stock in Cost A/cs ?

39,700 28,700

Profit as per Profit and Loss A/c (39,700 - 28,700) - 11,000

39,700 39,700

18

Illustration 11(Do it yourself) From the following information you are required to prepare:

(i) Cost Sheet for Articles A and B.

(ii) Profit and Loss Account as per financial hooks.

(iii) Reconciliation between profit as per cost books and as per financial books.

Works overhead (Actual) 1,42,000

Office expenses (Actual) 95,700

Number of Price per Price per

Articles sold Article Rs.

A 180 1,450

B 220 1,600

There was neither opening stock nor any closing stock. Works overhead are charged

100% on labour and office overhead are charged at 25% on works cost.

Solution:

Profit & Loss Account as per Financials’ Books

Particulars Rs. Particulars Rs.

To Material communed By Sales

? ?

To Labour ?

To Works Overheads 1,42,000

To Office Overheads 95,700

To Net Profit 1,44,300

6,13,000 6,13,000

Cost Sheet

Particulars A B Total

Rs. Rs. Rs.

Material communed 36,000 48,400 84,400

Labour Cost 63,000 83,600 1,46,600

Prime Cost 99,000 1,32,000 2,31,000

Add: Works overheads @ 100% on Labour Cost ? ? ?

Works Cost 1,62,000 2,15,600 3,77,600

Add: Office overhead @ 25% on works cost ? ? ?

Cost of Goods produced/Sold ? ? ?

Profit 58,500 82 500 1,41,000

Total Sales 2,61,000 3,52,000 6,13,000

19

Reconciliation Statement

Particulars Rs.

Profit as per Cost Accounts 1,41,000

Add: Over-absorption of Works Overheads ?

Less: Under-absorption of Office Overheads ?

Profit as per Financial Accounts -1,300

1,44,300

Illustration 12 M/s Mysore petro Ltd. Showed a net loss of Rs 2,08,000 as per their financial accounts for

the year ended 31st march, 1989. The cost accounts, however, disclosed a net loss of Rs

1,64,00 for the same period. The following information was revealed as a result of the

scrutiny of the figures of both the sets of books:

Factory overhead under-recovered 3000

Administration overhead over-recovered 2000

Depreciation charged in financial accounts 60,000

Interest on investment not included in costs 10000

Depreciation recovered in costs 65000

Income-tax provided 60000

Transfer fees (in financial books) 1000

Stores adjustment (credit in financial books) 1000

Prepare a memorandum reconciliation account Solution

Memorandum Reconciliation Account ================================================================ To Net Loss as per Costing Books 1,64,000 By administration overhead Over-recovered in costs 2,000 To Factory overhead Under-recovered in costs 3000 By Depreciation over-charged In costs 5,000 To Income-tax not provided in

Costs 60,000 By interest on investment not included in costs 10,000 By Transfer fees in financial Books 1,000 By Stores adjustments 1,000 By Net loss as per financial Books 2,08,000

2,27,000 2,27,000 =============================================================================== Illustration 13

In reconciliation between cost and financial accounts, one of the areas of differences is for

different methods of stock valuation. State, with reasons, in each of the following

circumstances whether costing profit will be higher or lower than the financial profit.

20

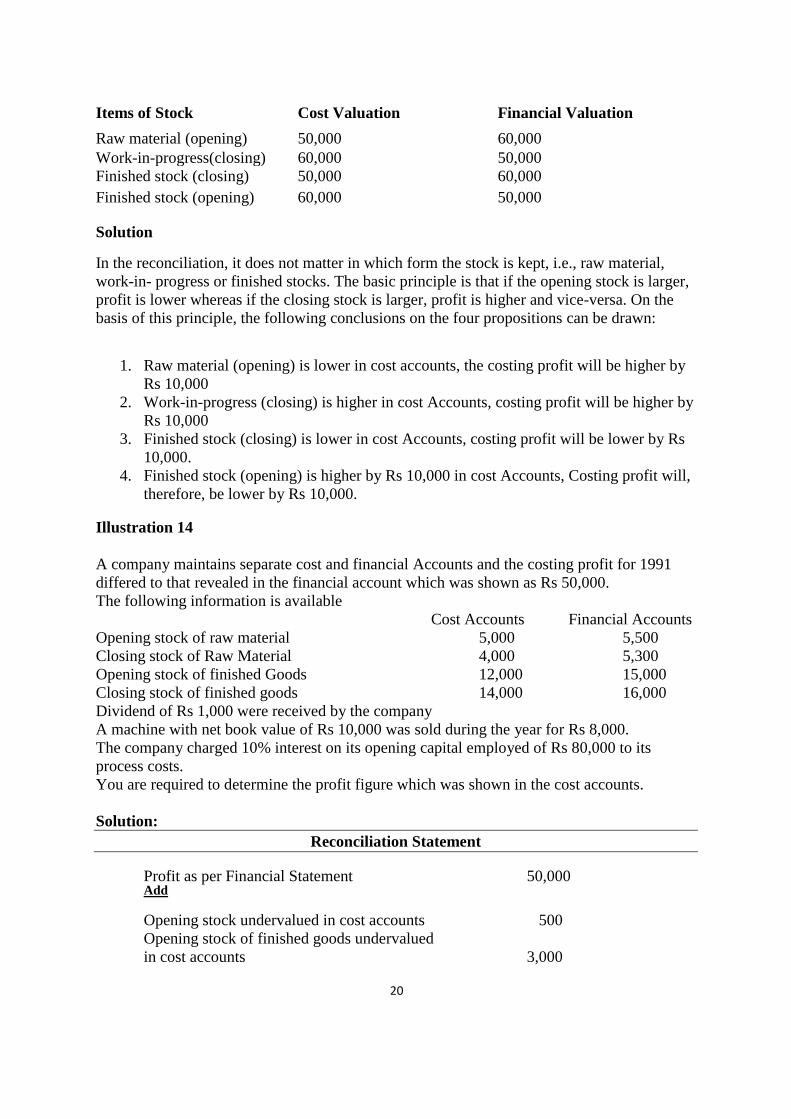

Items of Stock Cost Valuation Financial Valuation

Raw material (opening) 50,000 60,000

Work-in-progress(closing) 60,000 50,000

Finished stock (closing) 50,000 60,000

Finished stock (opening) 60,000 50,000

Solution

In the reconciliation, it does not matter in which form the stock is kept, i.e., raw material,

work-in- progress or finished stocks. The basic principle is that if the opening stock is larger,

profit is lower whereas if the closing stock is larger, profit is higher and vice-versa. On the

basis of this principle, the following conclusions on the four propositions can be drawn:

1. Raw material (opening) is lower in cost accounts, the costing profit will be higher by

Rs 10,000

2. Work-in-progress (closing) is higher in cost Accounts, costing profit will be higher by

Rs 10,000

3. Finished stock (closing) is lower in cost Accounts, costing profit will be lower by Rs

10,000.

4. Finished stock (opening) is higher by Rs 10,000 in cost Accounts, Costing profit will,

therefore, be lower by Rs 10,000.

Illustration 14

A company maintains separate cost and financial Accounts and the costing profit for 1991

differed to that revealed in the financial account which was shown as Rs 50,000.

The following information is available

Cost Accounts Financial Accounts

Opening stock of raw material 5,000 5,500

Closing stock of Raw Material 4,000 5,300

Opening stock of finished Goods 12,000 15,000

Closing stock of finished goods 14,000 16,000

Dividend of Rs 1,000 were received by the company

A machine with net book value of Rs 10,000 was sold during the year for Rs 8,000.

The company charged 10% interest on its opening capital employed of Rs 80,000 to its

process costs.

You are required to determine the profit figure which was shown in the cost accounts.

Solution:

Reconciliation Statement

Profit as per Financial Statement 50,000 Add Opening stock undervalued in cost accounts 500

Opening stock of finished goods undervalued

in cost accounts 3,000

21

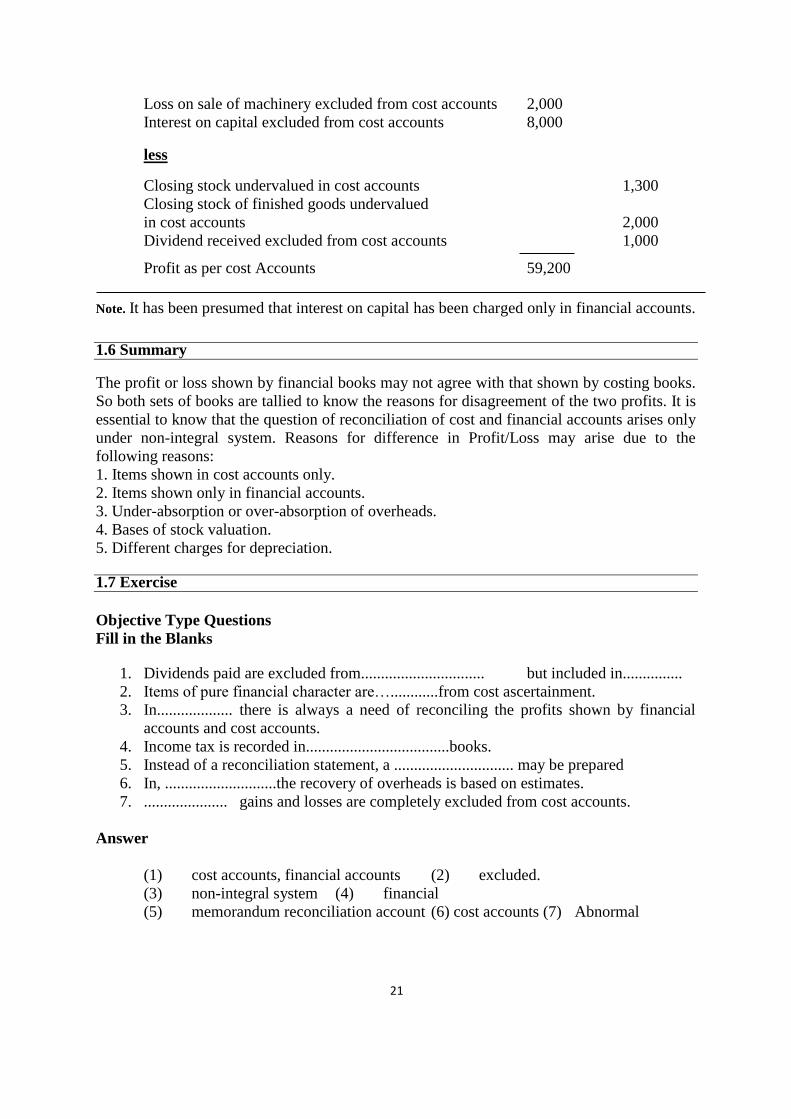

Loss on sale of machinery excluded from cost accounts 2,000

Interest on capital excluded from cost accounts 8,000

less Closing stock undervalued in cost accounts 1,300

Closing stock of finished goods undervalued

in cost accounts 2,000

Dividend received excluded from cost accounts 1,000 Profit as per cost Accounts 59,200

Note. It has been presumed that interest on capital has been charged only in financial accounts.

1.6 Summary The profit or loss shown by financial books may not agree with that shown by costing books.

So both sets of books are tallied to know the reasons for disagreement of the two profits. It is

essential to know that the question of reconciliation of cost and financial accounts arises only

under non-integral system. Reasons for difference in Profit/Loss may arise due to the

following reasons:

1. Items shown in cost accounts only.

2. Items shown only in financial accounts.

3. Under-absorption or over-absorption of overheads.

4. Bases of stock valuation.

5. Different charges for depreciation.

1.7 Exercise

Objective Type Questions

Fill in the Blanks

1. Dividends paid are excluded from............................... but included in...............

2. Items of pure financial character are…............from cost ascertainment.

3. In................... there is always a need of reconciling the profits shown by financial

accounts and cost accounts.

4. Income tax is recorded in....................................books.

5. Instead of a reconciliation statement, a .............................. may be prepared

6. In, ............................the recovery of overheads is based on estimates.

7. ..................... gains and losses are completely excluded from cost accounts.

Answer

(1) cost accounts, financial accounts (2) excluded.

(3) non-integral system (4) financial

(5) memorandum reconciliation account (6) cost accounts (7) Abnormal

22

True or False Statements

1. The requirement for reconciliation of costing profits and financial profits arises if cost accounts are maintained independent of financial accounts.

2. Income tax is provided only in financial accounts and not in cost accounts. 3. Different methods of charging depreciation are adopted in cost and financial books. 4. Rent on owned building is included in cost: accounts. 5. Purely financial incomes are included in Profit and Loss Account but are excluded

from the cost sheet. 6. Under-absorption of overheads decreases profit in costing books.

Answer

a) True

b) True. c) True d) True

e) True. f) False. Under-absorption of overheads results in more profits.

Descriptive Questions

1. What is meant by Reconciliation Statement? What is the need for Reconciliation

Statement?

2. Enumerate the items which are generally excluded from cost accounts.

3. Name any five items which are included in financial accounts but are excluded in cost

accounts.

4. Describe, in brief, the conditions which necessitate reconciliation of financial and cost

records.

5. State the steps involved in the preparation of reconciliation statement.

6. Write a note on "Memorandum Reconciliation Statement".

7. Explain the causes of difference between profit shown by Financial accounts and

profit shown by Cost Accounts.

8. Enumerate the causes of difference between profits shown by financial and cost

accounts.

9. Indicate the reasons why it is necessary for the cost and financial accounts of an

organisation to be reconciled.

10. Indicate the reasons why it is necessary for the cost and financial accounts of an

organisation to be reconciled and explain the main reasons of difference which would

enter in such accounts.

11. Write short note on items excluded from Cost Accounts.

12. Distinguish between Reconciliation Statement and Reconciliation Account.

13. Name any five items which are included in financial accounts but are not included in

cost accounts and also state the effect on the profits of cost accounts.

14. write short notes on

(a) Why we need reconciliation statement

(b) Items excluded from financial Account

(c) Items added in reconciliation statement

(d) Items less in reconciliation Statement

23

LESSON 2

RECONCILIATION OF COST AND FINANCIAL ACCOUNTS

2.0 Introduction

2.1 Objectives

2.2 Reconciliation

2.3 Profit and Loss Account as per financial books

2.4 Summary of the chapter

2.5 Exercise

2.1 Objectives

After Studying this chapter, you would be able to : Explain the reasons for difference in profit or loss as per cost and financial accounts

Know the method of preparing a reconciliation statement or a memorandum

reconciliation account.

Illustration 1.The net profit of a Manufacturing Co. Ltd. appeared at Rs. 64,377

as per financial records for the year ended 31st December, 1990. The cost books,

however, showed a net profit of Rs. 86,200 for the same period. A scrutiny of the

figures from both the sets of accounts revealed the following facts:

Rs.

Works overhead under-recovered in costs 1,560

Administration overhead over-recovered in costs 850

Depreciation charged in financial accounts 5,600

Depreciation recovered in costs 6,250

Interest on investments not included in costs 4,000

Loss due to obsolescence charged in financial accounts 2,850

Income tax provided in financial accounts 20,150

Bank interest and transfer fees in financial books 375

Stores adjustments (credit in financial books) 237

Loss due to depreciation in stock values (charged in financial 3,375

Prepare a statement showing the reconciliation between the figures of net profit

as per cost accounts and the figure of net profit shown in the financial books.

2.1 RECONCILIATION STATEMENT

RECONCILIATION STATEMENT

=============================================================

Net profit as per cost accounts 86,200

Add

Administration overhead over-recovered in costs 850

Excess depreciation charged in costs(6250-5600) 650

Interest on investment not included in costs 4,000

24

Bank interest and transfer fees 375

Stores adjustments 237

Less

Work overhead under-recovered in costs loss

Due to obsolescence not charged income-

Tax not provided 1,560

Depreciation in stock 20,150

Net profit as per Financial Records 64,377

=============================================================

RECONCILIATION WHEN COST AND/OR FINANCIAL PROFIT IS NOT GIVEN

Illustration 2

A transistor manufacturer, who commenced his business on 1st January, 1999

supplies you with the following information and asks you to prepare a statement

showing the profit per transistor sold. Wages and materials are to be charged at

actual cost, works overhead at 75% of wages and office overhead at 30% of works

cost. Number of transistors manufactured and sold during the year was 540.Other

particulars are:

Materials per set Rs. 240 Wages per set Rs. 80

Selling price per set Rs. 600

If the actual works expenses were Rs. 32,160 and office expenses were Rs. 61,800 .

Prepare a Reconciliation Statement.

Solution :

STATEMENT OF PROFIT AS PER COST ACCOUNTS

=============================================================

Materials (Rs 240x540) Rs 1,29,600

Wages (Rs 80*540) 43,200

Prime cost 1,72,800

Works overhead (75% of wages) 32,400

Works cost 2,05,200

Office overhead (30% of works cost) 61,560

Total cost 2,66,760

Profit 57,240

Sales 3,24,000

=============================================================

2.3 PROFIT AND LOSS ACCOUNT (AS PER FINANCIAL BOOKS)

Profit and Loss Account ( As per Financial Books)

=============================================================

To materials 129600 By Sales 3,24,000

To wages 43,200

To works expenses 32,160

To office expenses 61,800

To Net Profit 57,240

3,24000 3,24000

25

=============================================================

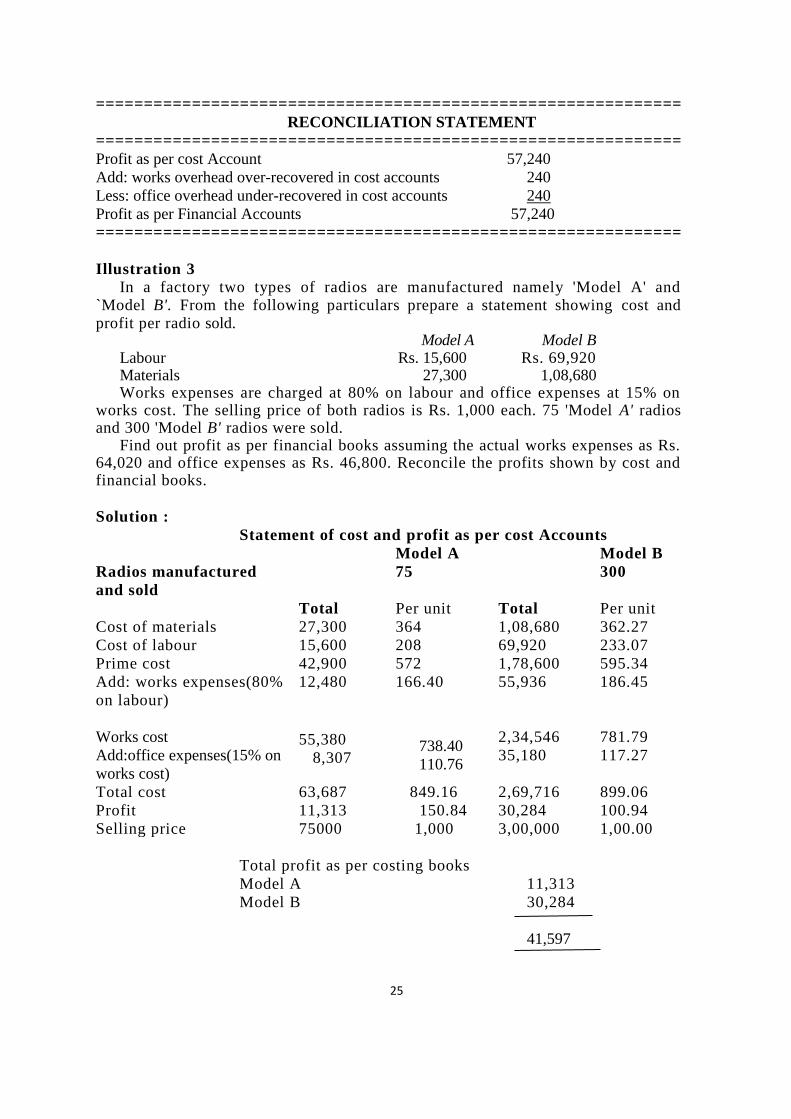

RECONCILIATION STATEMENT

=============================================================

Profit as per cost Account 57,240

Add: works overhead over-recovered in cost accounts 240

Less: office overhead under-recovered in cost accounts 240

Profit as per Financial Accounts 57,240

=============================================================

Illustration 3

In a factory two types of radios are manufactured namely 'Model A' and `Model B'. From the following particulars prepare a statement showing cost and profit per radio sold.

Model A Model B Labour Rs. 15,600 Rs. 69,920 Materials 27,300 1,08,680 Works expenses are charged at 80% on labour and office expenses at 15% on

works cost. The selling price of both radios is Rs. 1,000 each. 75 'Model A' radios and 300 'Model B' radios were sold.

Find out profit as per financial books assuming the actual works expenses as Rs. 64,020 and office expenses as Rs. 46,800. Reconcile the profits shown by cost and financial books.

Solution :

Statement of cost and profit as per cost Accounts

Model A Model B

Radios manufactured

and sold

75 300

Total Per unit Total Per unit

Cost of materials 27,300 364 1,08,680 362.27

Cost of labour 15,600 208 69,920 233.07

Prime cost

Add: works expenses(80%

on labour)

42,900

12,480

572

166.40

1,78,600

55,936

595.34

186.45

Works cost

Add:office expenses(15% on

works cost)

55,380

8,307

738.40

110.76

2,34,546

35,180

781.79

117.27

Total cost 63,687 849.16 2,69,716 899.06

Profit 11,313 150.84 30,284 100.94

Selling price 75000 1,000 3,00,000 1,00.00

Total profit as per costing books

Model A 11,313

Model B 30,284

41,597

26

Profit and Loss Account (As per financial Books)

=============================================================

To materials By sales

Model A 27,300 Model A 75,000

Model B 1,08,680 Model B 3,00,000

To Labour

Model A 15,600

Model 69,920

To work expenses 64,020

To office expenses 46,800

To Net Profit 42,680

3,75,000 3,75,000

=============================================================

RECONCILIATION STATEMENT

(+)

Profit as per Financial Accounts Rs. 42,680

Less :Works Expenses over-recovered in Costs Rs. 4,396

Add: Office Expenses under-recovered in Costs 3,313

43,993 4,396

Profit as per Cost Accounts 41,597

Working Notes :

1. Work Expenses charged in Cost

Accounts

Model A 12,480

Model B 55,936 68,416

Works Expenses charged in Financial Accounts 64,020

Works Expenses Over-recovered in Costs

4,396

2. Office Expenses charged in Financial

Accounts

46,800

Office Expenses charged in Cost Accounts

Model A 8,307

Model B 35,180 43,487

Works Expenses under-recovered in Costs.

3,313

27

Illustration 4

Mrs Piano co. which commenced business on 1 st January,1990, puts before you the

following information, and asks you to prepare a statement showing the profit per

piano sold (charge labour and material at actual cost, works overhead at 100% on

labour, and office overheads at 25% on works cost), and a statement showing a

reconciliation between the profits, as shown by the cost accounts and the profit as

shown by the profit and loss account for the year ended 31 st December, 1990.

Two grades of pianos are manufactured and are known as ‘Finis’ and ‘omega’.

There were no pianos in stock or in course of manufacture on 31 stDecember, 1990.

Average cost of materials per piano ‘Finis’ 8.000

Average cost of materials per piano ‘Omega’ 6.625

Average cost of Labour per Piano ‘Finis’ 14.625

Average cost of Labour per Piano ‘Omega’ 12.000

Finished Piano sold ‘finis’ 95

Finished Piano sold ‘Omega’ 160

Sale price per piano ‘Finis’ 60.000

Sale price per piano ‘Omega’ 45.000

Work expenses 4,200.00

Office expenses 1,555.00

You are required to prepare the necessary reconciliation statement

Solution: statement showing profit per piano sold

Particulars Finis Omega

Materials per piano 8.000 6.625

Labour per piano 14.625 12.000

Prime cost 22.625 18.625

Add: works overhead 100% on labour 14.625 12.00

Works cost 37.250 30.625

Add: office overhead 25% on

works cost 9.3125 7.65625

Total Cost 46.5625 38.28125

Profit 13.4375 6.71875

Selling price 60.0000 45.00000

=============================================================

PROFIT AND LOSS ACCOUNT FOR THE YEAR ENDED DEC. 31, 1990

=============================================================

To Material: Rs Rs By Sales Rs Rs.

‘Finis’ 760 ‘Finis’ 5,700

‘Omega’ 1,060 1,820.000 ‘Omega’ 7,200 12,900.00

To Labour:

‘Finis’ 1,389.375

‘Omega’ 1,920.000 3,309.375

To work expenses 4,200.000

To office expenses 1,555.000

To Net profit 2,015.625

------------- -------------

12,900.000 12,900.000

28

=============================================================

STATEMENT OF RECONCILIATION

=============================================================

(+) (-)

Profit as per profit and loss Account 2,015.625

Add: works overhead undercharged in cost accounts:

Works expenses 4200

Works overhead 3,309.375 890.625

Less: office overhead overcharged in cost accounts

Office overheads 2,109.688

Office expenses 1,565.000 554.688

2,906.250 554.688

Profit as per cost Accounts 2,351.562

‘finis’ Rs 13.4375 per piano on 95 pianos 1,276.562

‘Omega’ Rs 6.71875 per piano on 160 pianos 1,075.000

2,351.562

Illustration 5

The financial records by Modern Manufactures Ltd.

Reveal the following data for the year ended March 31, 1993 :

Sales (20,000 units) 4,000

Materials 1,600

Wages 800

Factory Overheads 720

Office and Administrative Overheads 416

Selling and Distribution Overheads 288

Closing Stock of Finished Goods (1,230 units) 240

Work-in-progress (Closing) Rs.

Materials 48

Labour 32

Overheads (Factory) 32 112

Goodwill written off 320

Interest on Capital 32

In the costing records, factory overhead is charged at 100% of wages,

administration overhead at 10% of works cost and selling and distribution

overhead at Rs. 16 per unit sold.

Prepare a statement reconciling the profit as per cost records with the profit as

per financial records of the company.

All workings should form part of your answer.

29

Solution :

=============================================================

STATEMENT OF PROFIT AS PER COST ACCOUNTS

=============================================================

Materials Rs. 16,00,000 Wages 8,00,000

Prime Cost 24,00,000

Factory Overheads (100% of Wages) 8,00,000

32,00,000

Less :Closing Stock of Work-in-progress 1,12,000

Works Cost 30,88,000

Add: Administration overheads(10% on works cost) 3,08,800

Cost of production(21,230 units) 33,96,800

Less: closing stock (1,230 units) 1,96,800

Cost of production of goods sold 32,00,000

Add: selling and distribution over heads @Rs 16per unit sold 3,20,000

Cost of sales 35,20,000

Profit 4,80,000

Sales 40,00,000

=============================================================

Profit and loss Account (financial Books) =============================================================

To Materials 16,00,000 By Sales 40,00,000

To Wages 8,00,000 By Closing Stock:

To Factory Overheads 7,20,000 work-in-progress 1,12,000

To Office & admin.overheads 4,16,000 finished Goods 2,40,000

To selling &dist. Overheads 2,88,000

To Goodwill written off 3,20,000

To interest on capital 32,000

To Net profit 1,76,000

43,52,000 43,52,000

=============================================================

Reconciliation Statement

=============================================================

(+) (-)

Profit as per cost Accounts 4,80,000

Add: over-absorption of factory overheads in cost account 80,000

Over-absorption of selling & dist. Ov.hds. in cost Accounts 32,000

Over-valuation of finished goods in financial Accounts 43,200

Less: un-absorption of admin. Overheads in cost Accounts 1,07,200

Goodwill written off in Financial Accounts 3,20,000

Interest on capital charged in Financial Accounts 32,000

6,35,200 4,59,200

Profit as per Financial Accounts 1,76,000

=============================================================

30

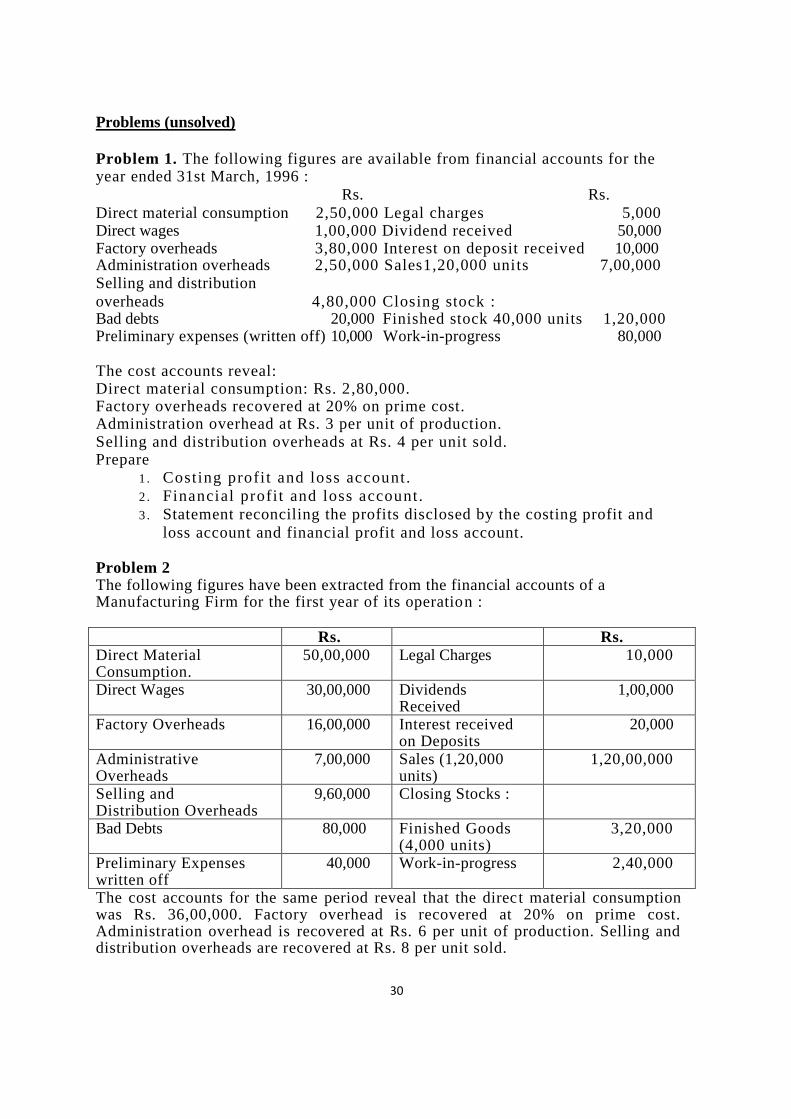

Problems (unsolved)

Problem 1. The following figures are available from financial accounts for the year ended 31st March, 1996 :

Rs. Rs.

Direct material consumption 2,50,000 Legal charges 5,000 Direct wages 1,00,000 Dividend received 50,000 Factory overheads 3,80,000 Interest on deposit received 10,000 Administration overheads 2,50,000 Sales1,20,000 units 7,00,000 Selling and distribution

overheads 4,80,000 Closing stock : Bad debts 20,000 Finished stock 40,000 units 1,20,000 Preliminary expenses (written off) 10,000 Work-in-progress 80,000 The cost accounts reveal: Direct material consumption: Rs. 2,80,000. Factory overheads recovered at 20% on prime cost. Administration overhead at Rs. 3 per unit of production. Selling and distribution overheads at Rs. 4 per unit sold. Prepare

1 . Costing profit and loss account.

2 . Financial profit and loss account.

3 . Statement reconciling the profits disclosed by the costing profit and

loss account and financial profit and loss account. Problem 2 The following figures have been extracted from the financial accounts of a Manufacturing Firm for the first year of its operation :

Rs. Rs.

Direct Material Consumption.

50,00,000 Legal Charges 10,000

Direct Wages 30,00,000 Dividends Received

1,00,000

Factory Overheads 16,00,000 Interest received on Deposits

20,000

Administrative Overheads

7,00,000 Sales (1,20,000 units)

1,20,00,000

Selling and Distribution Overheads

9,60,000 Closing Stocks :

Bad Debts 80,000 Finished Goods (4,000 units)

3,20,000

Preliminary Expenses written off

40,000 Work-in-progress 2,40,000

The cost accounts for the same period reveal that the direct material consumption was Rs. 36,00,000. Factory overhead is recovered at 20% on prime cost. Administration overhead is recovered at Rs. 6 per unit of production. Selling and distribution overheads are recovered at Rs. 8 per unit sold.

31

Prepare the Profit and Loss Accounts both as per Financial Records and as per

Cost Records. Reconcile the profits as per the two records.

Problem 3 The net profit of a company amounted to Rs. 60,412 for the year ending 31st

December, 1996, as per its financial records. The cost records, however, revealed a different figure. A scrutiny of the two sets of accounts disclosed the following facts:

(a) Works overhead recovered in Cost Accounts during the period amounted to Rs. 28,450 while the actual amount of these expenses was Rs. 21,390 only.

(b) Actual office expenses for the period were Rs. 19,850, whereas the office overhead recovered in Cost Accounts amounted to Rs. 14,500.

(c) The annual rental value of premises owned by the company, amounting to Rs: 10,800 was charged in Cost Accounts but not in Financial Accounts.

(d) Selling and Distribution expenses for the period amounting to Rs. 16,490 were excluded from costing records.

(e) Excess depreciation charged in Cost Accounts-Rs. 2,400. (f) Expenses not included in Cost Accounts and shown in Financial Accounts :

Interest of Bank Loan Rs. 1,600 Bank charges 160 Director's fees 750 Penalty due to late completion on contract 2,500

(g) Gains during the year not included in Cost Accounts Transfer fees Rs. 45 Profit on sale of investment 4,250

Interest on investments 9,450 (h) The following appropriation had been made before arriving at the profit

figure of Rs. 60,412, shown above : Transfer to Dividend Equalization Fund Rs. 10,500

Transfer to Income Tax Reserve 6,400 Transfer to Debenture Redemption Fund 9,000

(i) A sum of Rs. 10,000 given as donation to the Prime Minister's Relief Fund had been charged to-Profit and Loss Account as business expense.

Problem 4

The following information is available from the financial books of a company

having a normal production capacity of 60,000 units for the year ended 31st

March 1995 :

(i) Sales Rs. 10,00,000 (50,000 units).

(ii) There was no opening and closing stocks of finished units.

(iii) Direct material and direct wages cost were Rs.5,00,000 and Rs.2,50,000

respectively.

(iv) Actual factory expenses were Rs. 1,50,000 of which 60% are fixed.

(v) Actual administrative expenses were Rs. 45,000 which are completely

fixed.

(vi) Actual selling and distribution expenses were Rs. 30,000 of which 40% are

fixed.

(vii) Interest and dividends received Rs. 15,000.

32

You are required to :

(a) Find out profit as per financial books for the year ended 31st March, 1995;

(b) Prepare the cost sheet and ascertain the profit as per cost account for the year

ended 31st March, 1995 assuming that the indirect expenses are absorbed on the

basis of normal production capacity; and Prepare a statement reconciling

profits shown by financial and cost books.

Problem 5

The following transactions have been extracted from the financial books of

M/s Maheshwari Bros:

Rs. Units

Sales 2,50,000 20,000

Materials ' 1,00,000

Wages 50,000

Factory overheads 45,000

Office and administration overheads 26,000

Selling and distribution overheads 18,000

Closing Stock :

Finished goods 15,000 1,230

Work-in-progress:

Materials Rs. 3,000

Wages 2,000

Factory overheads 2,000 7,000

Goodwill written off 20,000

Interest on capital 2,000

In costing books factory overhead is charged at 100% on wages,

administration overhead at 10% of factory cost and selling and distribution at

the rate of Re 1 per unit sold. Prepare a statement reconciling the profit as per

cost and financial accounts.

Problem 6

From the following information

(i) determine the profit as it would be shown by cost accounts, and

(ii) prepare a statement reconciling it with profit shown by financial accounts

======================================================================

TRADING AND PROFIT AND LOSS ACCOUNT

(for the year ended 31st December, 1990)

======================================================================

Materials consumed Rs. 2,00,000 Sales (1,00,000 units) Rs. 4,00,000

Direct wages 1,00,000

Indirect expenses (works) 60,000

Office expenses 18,000

Selling and distribution

expenses 12,000

Net profit 10,000

Total 4,00,000

4,00,000

33

The normal output of the factory is 1,50,000 units. Works expenses of a fixed nature are Rs. 36,000. Office expenses are for all practical purposes constant. Selling and distribution expenses are constant to the extent of Rs. 6,000, and the balance varies directly with sales.

Problem 7: A firm of Sports Equipments commenced business on 1.4.93 for

manufacturing 2 varieties of bat, 'Senior' and `Sub-Junior'. The following information

has been extracted from the account records for the half-year period ended 30.9.1993:

Rs.

(i) Average material cost per piece of 'Senior' bat 80

(ii)Average material cost per piece of 'Sub-Junior' bat 60

(iii) Average cost of labour per piece of 'Senior' bat 140

(iv) Average cost of labour per piece of `Sub-Junior' bat 110

(v) Finished goods sold :

Senior 300 pieces

Sub-Junior 700 pieces

(vi) Sale price :

—per piece of 'Senior' bat 500

---per piece of `Sub-Junior' bat 390

(vi) Work expenses incurred during the period 1,20,000

(viii) Office expenses 68,000

You are required to prepare a statement showing

(1) The profit per each brand-piece of bat charge labour and material at

actual average cost, works on-cost at 100% on labour cost and office

cost at 25% of works cost. .

(2) Financial profit for the half-year ending 30.9.1993.

Reconciliation between profit as shown by cost accounts and financial accounts

Problem 8

A transistor manufacturer who commenced his business on 1st January, 1999

supplies you with the following information and asks you to prepare a statement

showing the profit per transistor sold. Wages and materials are to be charged at

actual cost, works overhead at 75% of wages and office overhead at 30% of works

cost. Number of transistors manufactured and sold during the year was 540.

Other particulars are:

Materials per set Rs.240

Wages per set Rs. 80

Selling price per set Rs. 600

If the actual works expenses were Rs. 32,160 and office expenses were Rs. 61,800,

prepare a Reconciliation Statement.

Problem 9

The following information is available from the financial books of a company

having a normal production capacity of 60,000 units for the year ended 31st

March 1995 :

(i) Sales Rs. 10,00,000 (50,000 units).

(it) There was no opening and closing stocks of finished units.

34

(iii) Direct material and direct wages cost were Rs. 5,00,000 and Rs.

2,50,000 respectively.

(iv) Actual factory expenses were Rs. 1,50,000 of which 60% are fixed.

(v) Actual administrative expenses were Rs. 45,000 which are completely

fixed. (vt) Actual selling and distribution expenses were Rs. 30,000 of which

40% are fixed. (vii) Interest and dividends received Rs. 15,000.

You are required to :

(a) Find out profit as per financial books for the year ended 31st March,

1995;

(b) Prepare the cost sheet and ascertain the profit as per cost account for the

year ended 31st March, 1995 assuming that the indirect expenses are

absorbed on the basis of normal production capacity; and

Prepare a statement reconciling profits shown by financial and cost books .

Problem 10

M/s Alpha Ltd. made a profit of Rs. 23,000 during the year 1990 as

per costing records, whereas their financial accounts disclosed a profit of Rs.

15,000. From the following profit and 16"ss account for the year ended 31.12.1990,

as per the financial books you are required to prepare a reconciliation statement :

RECONCILIATION OF COST AND FINANCIAL ACCOUNTS

PROFIT & LOSS ACCOUNT

Rs. Rs.

To Opening Stock 1,00,000 By Sales 1,75,000

To Purchases 80,000 By Closing Stock 80,000

To Direct Wages 20,000

To Factory Expenses 15,000

To Administration Expenses 10,000

To Selling Expenses 15,000

To Net Profit 15,000

2,55,000 2,55,000

The Costing records show the following :

(a) Stock Ledger Closing balance Rs. 89,000.

(b) Factory Overheads Rs. 13,000.

(c) Administrative overheads calculated @ 8% of the selling price.

(d) Selling expenses calculated @ 8% of the selling price.

Problem 11 During the year a company's profits have been estimated from the costing system to be Rs. 46,126, whereas the financial accounts audited by the auditors disclose a profit of Rs. 33,248. Given the following information, you are requi red to prepare a reconciliation statement showing clearly the reasons for the difference:

35

To Opening StockRs. 4,94,358 By Sales Rs. 6,93,000

To Purchases 1,64,308

6,58,666

Less :Closing Stock1,50,242 5,08,424

To Direct Wages 46,266 To Factory Overhea,d 41,652 To Gross Profit c/d 96,658

6,93,000 6,93,000

To Administration Expenses 19,690 By Gross Profit b/d 96,658

To Selling Expenses 44,352 By Sundry Income 632 To Net Profit 33,248

97,290 97,290

(a) Stock ledger closing balance is Rs. 1,56,394;

(b) Credit balance in wages control account is Rs. 49,734;

(c) Credit balance in factory overhead control account is Rs. 39,428;

(d) Administration expenses are charged to sales at 3% of selling price in cost

accounts, Selling price includes 5% (on sales) provision for selling

expenses. Sundry income is not considered in cost accounts.

Problem 12

From the following information (i) determine the profit as it would be shown by cost

accounts, and (a) prepare a statement reconciling it with profit shown by financial accounts

TRADING AND PROFIT AND LOSS ACCOUNT

(for the year ended 31st December, 1990)

Materials consumed Rs.

2,00,000

Sales (1,00,000

units) Rs. 4,00,000

Direct wages 1,00,000

Indirect expenses (works) 60,000

Office expenses 18,000

Selling and distribution

expenses 12,000

Net profit 10,000

Total 4,00,000

4,00,000

The normal output of the factory is 1,50,000 units. Works expenses of a fixed nature are Rs. 36,000. Office expenses are for all practical purposes constant. Selling and distribution expenses are constant to the extent of Rs. 6,000, and the balance varies directly with sales.

Problem 13

M/s B.K Piano Co., which commenced business on 1st January, 1990, puts

before you the following information, and asks you to prepare a statement showing

the profit per piano sold (charge labour and material at actual cost, works

overhead at 100% on labour, and office overheads at 25% on works cost), and a

statement showing a reconciliation between the profits, as shown by the cost

36

accounts and the profit as shown by the profit and loss account for the year

ended 31st December, 1990.

Two grades of pianos are manufactured and are known as 'Finis' and 'Omega'.

There were no pianos in stock or in course of manufacture on 31st December,

1990.

Average cost of materials per piano 'Finis' Rs. 8.000

Average cost of materials per piano 'Omega' 6.625

Average cost of labour per piano 'Finis' 14.625

Average cost of labour per piano `Omega' 12.000

Finished piano sold `Finis' 95

Finished piano sold 'Omega' 160

Sale price per piano 'Finis' 60.000

Sale price per piano 'Omega' 45.000

Works expenses 4,200.000

Office expenses 1,555.000

You are required to prepare the necessary reconciliation statement.

Problem 14 The net profit of a company amounted to Rs. 60,412 for the year ending 31st

December, 1996, as per its financial records. The cost records, however, revealed a different figure. A scrutiny of the two sets of accounts disclosed the following facts:

(a) Works overhead recovered in Cost Accounts during the period amounted to

Rs. 28,450 while the actual amount of these expenses was Rs. 21,390 only. (b) Actual office expenses for the period were Rs. 19,850, whereas the office

overhead recovered in Cost Accounts amounted to Rs. 14,500. (c) The annual rental value of premises owned by the company, amounting to

Rs: 10,800 was charged in Cost Accounts but not in Financial Accounts. (d) Selling and Distribution expenses for the period amounting to Rs. 16,490 were

excluded from costing records. (e) Excess depreciation charged in Cost Accounts-Rs. 2,400. (f) Expenses not included in Cost Accounts and shown in Financial Accounts :

Interest of Bank Loan Rs. 1,600 Bank charges 160 Director's fees 750 Penalty due to late completion on contract 2,500

(g)Gains during the year not included in Cost Accounts Transfer fees Rs. 45 Profit on sale of investment 4,250

Interest on investments 9,450 (h)The following appropriation had been made before arriving at the profit

figure of Rs. 60,412, shown above : Transfer to Dividend Equalization Fund Rs. 10,500

Transfer to Income Tax Reserve 6,400 Transfer to Debenture Redemption Fund 9,000

(i) A sum of Rs. 10,000 given as donation to the Prime Minister's Relief Fund had been charged to-Profit and Loss Account as business expense.

37

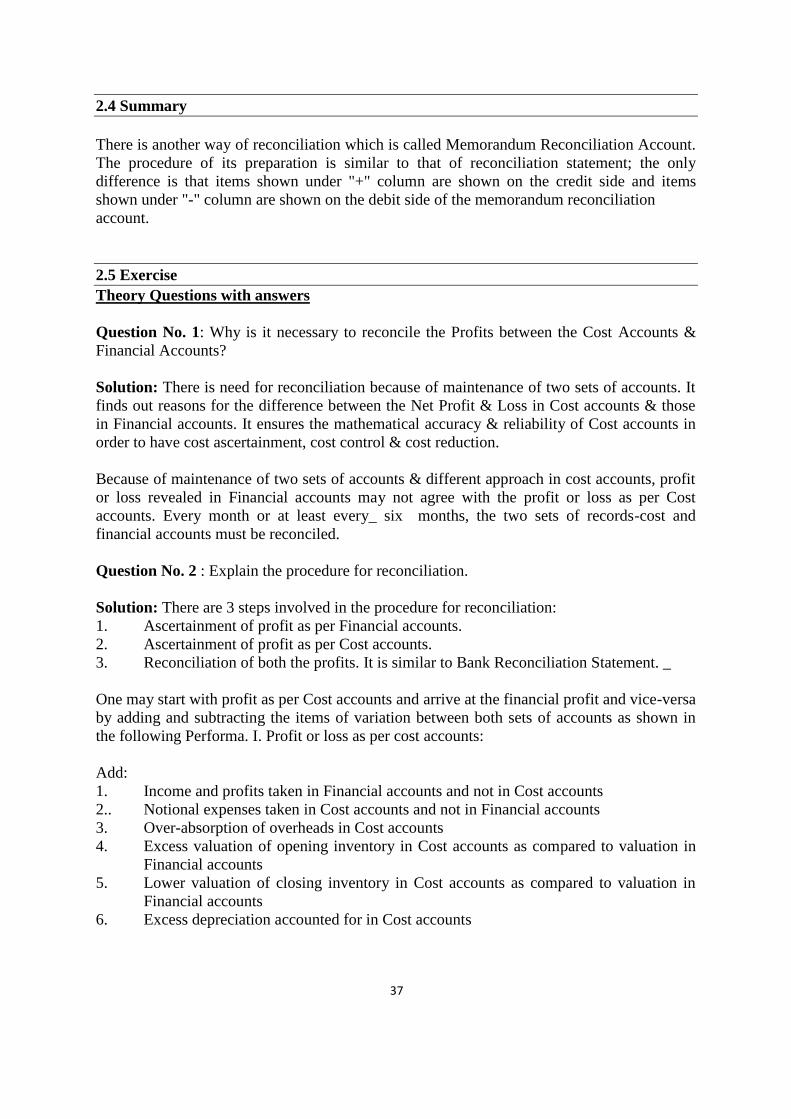

2.4 Summary

There is another way of reconciliation which is called Memorandum Reconciliation Account.

The procedure of its preparation is similar to that of reconciliation statement; the only

difference is that items shown under "+" column are shown on the credit side and items

shown under "-" column are shown on the debit side of the memorandum reconciliation

account.

2.5 Exercise

Theory Questions with answers

Question No. 1: Why is it necessary to reconcile the Profits between the Cost Accounts &

Financial Accounts?

Solution: There is need for reconciliation because of maintenance of two sets of accounts. It

finds out reasons for the difference between the Net Profit & Loss in Cost accounts & those

in Financial accounts. It ensures the mathematical accuracy & reliability of Cost accounts in

order to have cost ascertainment, cost control & cost reduction.

Because of maintenance of two sets of accounts & different approach in cost accounts, profit

or loss revealed in Financial accounts may not agree with the profit or loss as per Cost

accounts. Every month or at least every_ six months, the two sets of records-cost and

financial accounts must be reconciled.

Question No. 2 : Explain the procedure for reconciliation.

Solution: There are 3 steps involved in the procedure for reconciliation:

1. Ascertainment of profit as per Financial accounts.

2. Ascertainment of profit as per Cost accounts.

3. Reconciliation of both the profits. It is similar to Bank Reconciliation Statement. _

One may start with profit as per Cost accounts and arrive at the financial profit and vice-versa

by adding and subtracting the items of variation between both sets of accounts as shown in

the following Performa. I. Profit or loss as per cost accounts:

Add:

1. Income and profits taken in Financial accounts and not in Cost accounts

2.. Notional expenses taken in Cost accounts and not in Financial accounts

3. Over-absorption of overheads in Cost accounts

4. Excess valuation of opening inventory in Cost accounts as compared to valuation in

Financial accounts

5. Lower valuation of closing inventory in Cost accounts as compared to valuation in

Financial accounts

6. Excess depreciation accounted for in Cost accounts

38

Less:

7. Expenses and Losses accounted for in Financial accounts sand not in Cost accounts

8. Appropriations in Financial accounts only

9. Notional income taken in Cost accounts and not in Financial accounts

10. Under-absorption of overheads in Cost accounts

11. Lower valuation of opening inventory in Cost accounts as compared to valuation in

Financial accounts

12. Higher valuation of closing inventory in Cost accounts as compared to valuation in

Financial accounts

13. Lower depreciation accounted for in Cost accounts

Profit or loss as per Financial accounts

Note-Inventory includes raw materials, stores, spares, work-in-progress, stock of finished

goods etc. U. Profit as per Financial Accounts Add-Items 7 to 13 as mentioned above Less-

Items 1 to 6 as mentioned above Prof it or loss as per Cost accounts

Memorandum Reconciliation account: Alternatively, reconciliation may be affected by

Memorandum Reconciliation account also. The profit as per Cost accounts is credited to this

account. Items 1 to 6 which are to be added are entered on the credit side A items 7 to 13

which are to be deducted are debited to this account.

Question No. 3: What are the reasons for disagreement of Profits as per financial accounts &

cost Accounts? Discuss.

or

List the Financial expenses which are not included in cost

Solution: Reasons for difference between Profits shown in Cost accounts & those shown in

Financial accounts.

1. Items included in Financial Accounts-only

(a) Purely financial expenses:

(i) Interest on loans, bank mortgages.

(ii) Expenses & discounts on issue of shares, debentures etc.

(iii) Losses on sale of fixed assets & investments.

(iv) Other capital losses i.e., loss by fire not covered by insurance etc.

(v) Fines & penalties.

(vi) Stamp duty & expenses on transfer of shares.

(vii) Goodwill written off.

(viii) Preliminary expenses written off.

(ix) Donations & Subscriptions etc.

(x) Income Tax.

(xi) Underwriting commission written ff.

(xii) Cash Discount allowed to customers.

(b) Purely financial Income:

(i) Interest received on bank deposits, loans & investments.

(ii) Dividends received.

39

(iii) Profit on sale of fixed assets & investments.

(iv) Rents receivable.

(v) Fees received on issue & transfer of shares.

(vi) Profit on sale of shares.

(c) Appropriations of Profits:

(i) Dividends.

(ii) Transfer to reserves.

2. Items included in cost accounts only: These are notional charges called as imputed

costs/opportunity costs.

(a) Interest on capital at notional figure though not incurred. -

(b) Salary of owner manager at notional figure though not incurred.

(c) Notional rent of own building.

(d) Notional Depreciation on the asset fully depreciated for which book value is

nil.

3. Under or over-absorption of overheads, if transferred to next year's accounts: If the

under or over-absorption of overheads is transferred to next year's accounts. Profit or

losses in both sets of accounts may vary as

There will be difference between the overhead actually incurred in financial

accounts & overhead absorbed in cost accounts of a particular period. In other case

i.e., if it is transferred to same year's costing P&L A/c & if it is adjusted by

application of supplementary overhead rate, profit or losses of both sets of accounts

may not differ to this extent.

4. Different basis of stock valuation: In Financial accounts, stock may be valued at the

FIFO, Weighted Average or specific identification method whereas in Cost accounts,

the value of stock in hand may differ depending on the method followed for pricing of

material issues i.e., Simple Average, Specific identification, LIFO, HIFO, FIFO,

Weighted Average etc, resulting in different values of inventories in both these sets of

accounts:-

Valuation of work-in-progress (WTP) may be at prime cost or at prime cost + Factory

overhead & different basis may be used in valuing inventory of WIP in Cost &

Financial accounts. Similarly finished goods may be valued at prime cost ? Factory

overhead + Administration overhead i.e.. Cost of Production in Cost accounts and at

prime cost + Factory overhead in Financial accounts.

5. Different methods of charging depreciation: In Financial accounts, depreciation may

be calculated on the basis of straight line method (SLM) or written down value

(WDV) method etc whereas in Cost accounts, depreciation may be calculated on the

basis of machine hours or production units.

Question No. 4: "Is reconciliation of cost accounts and financial accounts necessary in case

of integrated accounting system?'

Solution: Integrated Accounting is the-name given to a system of accounting whereby cost

and financial accounts are kept in the same set of books. Such a system will have to afford

40

full information required for Costing as well as for Financial Accounts. In other words",

information and data Should be recorded in such a way so as to enable the firm to ascertain

the cost together with the necessary analysis of each product, job, process, operation or any

other identifiable activity.

The integrated accounts give full information in such a manner so that the profit and loss

account and the balance sheet can be prepared according to the requirements of law and the

management maintains full control over the liabilities, and assets of its business.

While non-integrated system of accounting necessitates reconciliation between financial and

cost accounts, no reconciliation between two sets of accounts is required under integrated

accounting.

Question No. 5 : "Reconciliation of cost & financial accounts in the modern computer age is

redundant."

Solution: In the modern computer age the use of computer knowledge and accounting

software has helped the field of Financial and Cost Accounting in a big way. In fact,

computers work at a very high speed and can process voluminous data for generating desired

output in no time. Output produced is precise and accurate. Computers can work for hours

without any fatigue. They can bring out different Financial Accounting Statements A reports

accurately in a presentable form. Financial accounts and Cost accounts show their results

accurately and precisely, when maintained on a computer system, but the profit shown by one

set of books may not agree with that of the other set.

Hence, the above statement is not correct & still reconciliation of financial & cost records is

impatient as both of records may differ.

41

LESSON 3

BUDGETARY CONTROL

3.0 Introduction

3.1 Objectives

3.2 Budget

2.2.1 Meaning

2.2.2 Definition of Budget

2.2.3 Characteristics

3.3 Budgeting

3.3.1 Meaning

3.3.2 Definition of Budgeting

3.3.3 Characteristics

3.3.4 Necessities of Budgeting

3.4 Budgetary Control

3.4.1 Definitions

3.4.2 Steps in the process of Budgetary Control System

3.4.3 Features

3.4.4 Objectives of Budgetary control

3.4.5 Advantages of Budgetary Control

3.4.6 Limitations of Budgetary Control

3.5 Fixed Budget and Flexible budget

3.6 Limitations of Fixed Budget and Flexible budget

3.7 Flexible Budget

3.7.1 Steps in preparing a flexible budget

3.7.2 Features

3.7.3 Benefits

3.8 Distinction between Distinction between Fixed & flexible budget

3.9 Summary of the chapter

3.10 Exercise

3.1 Objectives

After studying this chapter, students would be able to:

• Understand Budgeting- Meaning, Definition of Budgeting, characteristics &

Necessities of Budgeting

• Understand Budgetary Control-Definitions

• Understand Steps in the process of Budgetary Control System

• Understand Features and Objectives of Budgetary control

• Understand Advantages of Budgetary Control and Limitations of Budgetary Control

• Understand fixed Budget and Flexible budget and Limitations

• Understand Flexible Budget

--Steps in preparing a flexible budget

--Features

--Benefits • Distinction between Fixed & flexible budget

42

3.2 Budgetary Control

Planning is the basic step for good management because it involves observing systematically at

the future. Monetary planning plays an important role in all the spheres of activities. Whether

it is household or business or government, planning is the first basic exercise to carry out

before venturing out for any activity. Financial budgets help managers in developing

financial plan to guide them in allocating their resources over a specific future period.

Budgeting is the most commonly management used tool of planning and controlling cost.

Control is the process of measuring and correcting actual performance to ensure that plans for

implementing the chosen course of action are carried out.

3.2.1 Meaning

The word ‘budget’ is derived from a French term “bougette” denoting a leather pouch in

which money is put in order to meet expected expenses.

Budget is a plan relating which is expressed in monetary and/ or quantitative terms for a

definite future period of time in relative to commercial aspect; a budget is a formal

expression of the expected incomes and expenditures for a definite future period.

3.2.2 Definition of Budget