CONNECTICUT RECOMMENDED REVISIONS TO THE FY 2019 BUDGET DANNEL P. MALLOY, GOVERNOR February 7, 2018...

38

CONNECTICUT RECOMMENDED REVISIONS TO THE FY 2019 BUDGET DANNEL P. MALLOY, GOVERNOR February 7, 2018

Transcript of CONNECTICUT RECOMMENDED REVISIONS TO THE FY 2019 BUDGET DANNEL P. MALLOY, GOVERNOR February 7, 2018...

CONNECTICUT

RECOMMENDED REVISIONSTO THE

FY 2019 BUDGET

DANNEL P. MALLOY, GOVERNOR

February 7, 2018

Introduction

The Governor’s budget proposal for the biennium:

Makes minor revisions to bipartisan budget to achieve balance

Recommends revenues to avoid project deferrals, fare hikes, and service cuts in transportation

Reduces out-year budget gaps by half

2

Budget Overview

3

FY 2019 General Fund Budget Challenge(in millions)

4

Adopted

Budget

Consensus

Adjustments

Revised

Total

Revenues 18,908.2$ (282.8)$ 18,625.4$

Appropriations 18,790.6 - 18,790.6

Balance 117.6$ (282.8)$ (165.2)$

Other Adopted Budget Challenges

Revenue - Unspecified elimination of tax expenditures (10.0)

Required technical budget adjustments

Annualize funding for FY 2018 deficiencies (10.4)

Fund programming for Juan F. compliance (16.3)

Revise funding due to cost and caseload adjustments (10.5)

Adjust for overly aggressive savings estimates (7.5)

All other adjustments (net) 4.9

Unachievable lapses (51.2)

Total (including consensus revisions) (266.3)

Distribution of Budgeted Lapses(in millions)

Adopted Budget Recommended FY 2019 FY 2019

LAPSES

Unallocated Lapse (51.8)$ (9.5)$

Unallocated Lapse - Legislative (1.0) -

Unallocated Lapse - Judicial (8.0) (5.0)

Targeted Savings (150.9) -

Statewide Hiring Reduction (7.0) -

Municipal Contribution to Renters Rebate (8.5) -

Achieve Labor Concessions (867.6) -

CHANGES TO AGENCY APPROPRIATIONS

Annualization of FY 2018 Holdbacks (175.9)

Reflect changes to TRS employee contributions (40.1)

Allocate General Fund SEBAC Savings (813.0)

TOTAL ADJUSTMENTS (1,094.7)$ (1,043.5)$

SEBAC Savings Attributable to Other Funds (54.6)

Other Adjustments 3.4

TOTAL (1,094.7)$

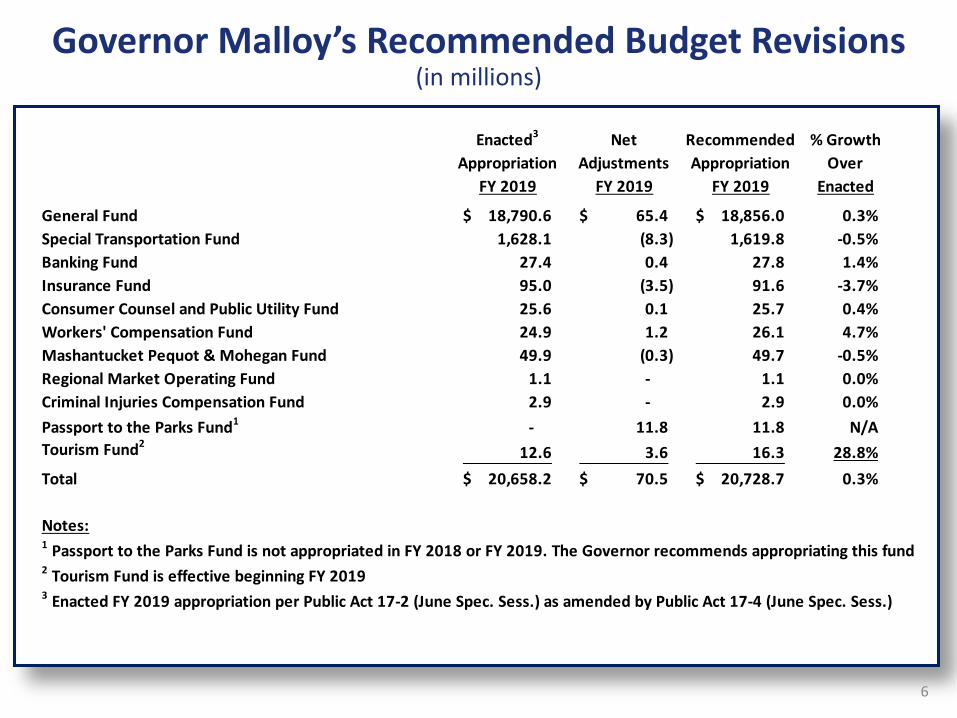

Governor Malloy’s Recommended Budget Revisions(in millions)

6

Enacted3 Net Recommended % Growth

Appropriation Adjustments Appropriation Over

FY 2019 FY 2019 FY 2019 Enacted

General Fund 18,790.6$ 65.4$ 18,856.0$ 0.3%

Special Transportation Fund 1,628.1 (8.3) 1,619.8 -0.5%

Banking Fund 27.4 0.4 27.8 1.4%

Insurance Fund 95.0 (3.5) 91.6 -3.7%

Consumer Counsel and Public Utility Fund 25.6 0.1 25.7 0.4%

Workers' Compensation Fund 24.9 1.2 26.1 4.7%

Mashantucket Pequot & Mohegan Fund 49.9 (0.3) 49.7 -0.5%

Regional Market Operating Fund 1.1 - 1.1 0.0%

Criminal Injuries Compensation Fund 2.9 - 2.9 0.0%

Passport to the Parks Fund1 - 11.8 11.8 N/A

Tourism Fund212.6 3.6 16.3 28.8%

Total 20,658.2$ 70.5$ 20,728.7$ 0.3%

Notes:1 Passport to the Parks Fund is not appropriated in FY 2018 or FY 2019. The Governor recommends appropriating this fund.2 Tourism Fund is effective beginning FY 20193 Enacted FY 2019 appropriation per Public Act 17-2 (June Spec. Sess.) as amended by Public Act 17-4 (June Spec. Sess.)

7

Expenditure GrowthLowest Average General Fund Growth in Decades

5.5%

5.1%

5.6%

7.3%

3.5%

9.3%

-2.4%

4.2%

5.7%

6.7%6.2% 6.4%

5.4%

2.1%

3.6%4.0%

4.8%

1.2%

2.3%2.6%

3.0%

-0.9%

5.4%

0.7%

-4%

-2%

0%

2%

4%

6%

8%

10%

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

*

20

15

20

16

20

17

20

18

Est

.

20

19

Re

c.

Ex

pe

nd

itu

re G

row

th R

ate

Fiscal Year

Average = 2.3%Average = 4.3%Average = 5.0%

Average represents the compound annual growth rate of each shaded section*2013 to 2014 growth has been adjusted to reflect the net budgeting of Medicaid

Without the increase in hospital funding, growth

would have been 2.1%

Out-year Budget Gaps Reduced($ in millions)

8

FY 2020 FY 2021 FY 2022

Bipartisan Budget (PA 17-2, JSS)

Revenue (January 2018 consensus) 17,510.1 17,612.9 17,753.5

Appropriations (per OFA fiscal note) 19,708.5 20,548.0 21,187.9

Projected Deficit (2,198.4) (2,935.1) (3,434.4)

Governor's Recommended Revisions

Revenue 18,708.6 18,870.3 19,045.4

Appropriations 19,552.7 20,375.2 20,988.7

Projected Deficit (844.1) (1,504.9) (1,943.3)

Out-year Balance Improvement 1,354.3 1,430.2 1,491.1

Rebuilding the Budget Reserve Fund

• Public Act 17-2, June Special Session, requires payments from the estimated and final portion of the personal income tax in excess of $3.15 billion be deposited to the Budget Reserve Fund

• If the legislature acts to close the projected FY 2018 deficit, the Rainy Day Fund will grow to $894.9 million, or an estimated 4.6 percent, by the end of FY 2019 based on current consensus revenue forecasts

$93.5

$270.7

$519.2

$235.6 $212.9

$877.8 $894.9

0.0%

0.5%

1.6%

3.0%

1.3%1.1%

4.7% 4.6%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

$0.0

$200.0

$400.0

$600.0

$800.0

$1,000.0

$1,200.0

$1,400.0

2011 2012 2013 2014 2016 2017 2018(EST.)

2019(EST.)

PER

CEN

T FU

ND

ED

RA

INY

DA

Y F

UN

D V

ALU

E (I

N M

ILLI

ON

S)

FISCAL YEAR

RAINY DAY FUND BALANCES

9

Staffing At Lowest Levels Since 1950s(Executive Branch excluding Higher Education)

7.00

7.50

8.00

8.50

9.00

9.50

10.00

10.50

16,000

18,000

20,000

22,000

24,000

26,000

28,000

30,000

32,000

34,000

Jun-60 Mar-74 Nov-87 Jul-01 Apr-15

Number of Employees

Number of Employees per 1,000 Residents

10

Transportation

11

Special Transportation Fund

• Insufficient revenue collections in the STF will trigger service

cuts, fare increases, and deferral of important infrastructure

projects

• The Governor recommends adding revenue to the STF in

order to:

Restore capital spending to adequately address the

state’s infrastructure needs

Avoid service reductions, rail and bus fare increases and

cuts to transit district subsidies

12

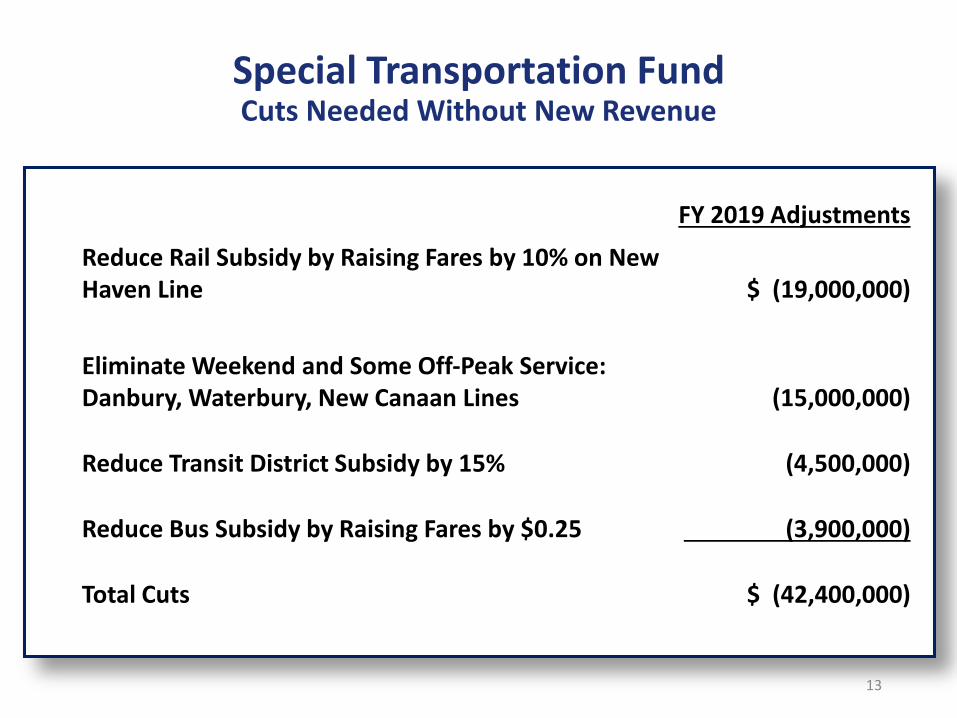

Special Transportation FundCuts Needed Without New Revenue

13

FY 2019 Adjustments

Reduce Rail Subsidy by Raising Fares by 10% on New Haven Line $ (19,000,000)

Eliminate Weekend and Some Off-Peak Service: Danbury, Waterbury, New Canaan Lines (15,000,000)

Reduce Transit District Subsidy by 15% (4,500,000)

Reduce Bus Subsidy by Raising Fares by $0.25 (3,900,000)

Total Cuts $ (42,400,000)

Special Transportation FundRecommended Restorations Supported by Proposed

Revenue

14

FY 2019 Adjustments

Fully Fund Bus Operations Without fare increases $ 23,266,111

Fully Fund Rail Operations Without fare increases 13,447,293

Comply with General Permit for the Discharge of Stormwater 3,105,136

Annualize ADA Para-Transit Expenditures 2,756,775

Other Adjustments: Delayed Hiring, Reduction to PAYGO Program, Non-Service Metro North Reductions, UConn CTfastrak Annualization (9,642,306)

Total Restorations $ 32,933,009

Special Transportation FundRevenue Proposals

• Statewide Tolling – Will provide the funding necessary to address some of the

state’s largest infrastructure projects and provide essential traffic mitigation

• Gasoline Tax – Add 7 cents to the gasoline tax by FY 2022, raising gasoline taxes

from 25 cents to 32 cents to sustain the fund until tolls are implemented

• Accelerate transfer of sales tax on cars by two years

Special Transportation Fund Revenue Proposals(in millions)

Eff. Fiscal Fiscal Fiscal Fiscal

Date 2019 2020 2021 2022

Increase Gasoline Tax by 7 Cents (2, 1, 2, 2) 7/1/2018 $ 30.0 $ 45.0 $ 75.0 $ 105.0

Accelerate Transfer of Car Sales Tax by 2 Years 7/1/2018 9.1 66.9 78.7 74.9

Impose a Tire Fee ($3 per tire) 7/1/2018 8.0 8.0 8.0 8.0

Retain Suspended License Restoration Fees in STF 7/1/2019 - 2.0 2.0 2.0

Institute Statewide Tolling (Begins in FY 2023) 7/1/2018 - - - -

$ 47.1 $ 121.9 $ 163.7 $ 189.9

15

Special Transportation Fund

• The November Consensus Revenue projection identified a drop-off in revenue due to continued low oil prices/slow growing revenue

• As a result, the fund would have gone into deficit and run out of money in FY 2020

• To address the revenue drop, the state identified actions to balance the fund with no new revenues:• 20% rail fare hike and a $0.25

bus fare hike• Major service cuts to Shore Line

East and Branch Lines• Deferral of over $4.3 billion in

infrastructure projects• All together, these actions will produce

a balanced Special Transportation Fund 16

$56.9

$22.2

$(11.9)

$9.9 $40.9

$154.6

$215.7

$(50.0)

$-

$50.0

$100.0

$150.0

$200.0

$250.0

FY 2018 FY 2019 FY 2020 FY 2021 FY 2022

(in

mill

ion

s)

Indefinitely Postpone Projects, Service Cuts and Fare Hikes

Operating Surplus/(Deficit) Cumulative Balance

$43.5

$(38.1)$(116.0)

$(159.0)$(216.1)

$141.1

$(388.1) $(500.0)

$(400.0)

$(300.0)

$(200.0)

$(100.0)

$-

$100.0

$200.0

FY 2018 FY 2019 FY 2020 FY 2021 FY 2022

iIn m

illio

ns)

Adopted Bipartisan Budgetwith November 13, 2017 Consensus Revenue

Operating Surplus/(Deficit) Cumulative Balance

Special Transportation FundGovernor’s Recommendation:

No Service Cuts, No Fare Hikes, and No Project Deferrals

• No service cuts, no fare hikes, and no project deferrals

• Annual gas tax increase of 2¢, 1¢, 2¢, 2¢ in FY 2019 through FY 2022

• Authorization of tolls to produce revenue in FY 2023

• Advance diversion of sales tax on motor vehicles into FY 2019

17

$56.9

$15.5 $16.0 $8.7 $4.8

$154.5

$199.5

$-

$50.0

$100.0

$150.0

$200.0

$250.0

FY 2018 FY 2019 FY 2020 FY 2021 FY 2022

(in

mill

ion

s)

Governor's Recommended Budget Projection

Operating Surplus/(Deficit) Cumulative Balance

Municipal Aid

18

Changes in Municipal Aid

After annualizing FY 2018 holdbacks, the FY 2019 budget reduces municipal aid by $32.0 million:

• Caps all appropriated non-education municipal aid payments at a maximum of their FY 2018 amounts

• Eliminates appropriated grants, including education, to municipalities with an Equalized Net Grand List Per Capita above $200,000, with the exception of Alliance Districts which are held harmless from this reduction

19

Education Cost Sharing

• Retains formula passed in bipartisan budget including increases to underfunded communities

• Two factors that affect the phase-in are adjusted:

Base grant amount is changed to reflect FY 2018 estimated grants rather than FY 2017 grants

Phase-in percentage for towns whose fully funded grant is greater than its base grant is changed to 8% in FY 2019 and 6.76% in FY 2020

• Eliminates grants to the wealthiest communities based on Equalized Net Grand List Per Capita (ENGLPC)

20

State Aid to or on Behalf of Local Governments(in millions)

$579.60 $576.70 $502.40

$3,311.0$3,011.5 $3,059.8

$1,146.4$1,425.8 $1,465.4

$0

$1,000

$2,000

$3,000

$4,000

$5,000

$6,000

FY 2017 FY 2018 FY 2019General Government Education Teachers' Retirement: Debt Service, Retiree Health and Retirement Contributions

$5,037.0 $5,014.0 $5,027.6

19

Other Program Changes

22

Significant General Fund Spending Reductions(in millions)

23

• Reduce Growth in Municipal Aid $(18.6)

• Eliminate Municipal Aid Grants to the Wealthiest Communities (14.2)

• DCF - Reflect Savings from Closure of CJTS (11.4)

• DSS - Eliminate Medicaid Subsidy for Graduate Medical Education (10.6)

• DSS – Reduce Enhanced Reimbursement for Primary Care Providers (3.5)

• DMHAS – Recognize Savings from Increased FFS Billings (3.0)

• DMHAS – Restructure State Operated Services (2.1)

• OPM - Fund Councils of Government at FY 2018 Level (2.3)

• DCF - Reduce Juvenile Justice Staffing (1.2)

Significant General Fund Spending Increases(in millions)

24

New Initiatives

• DDS – Add Funding for Emergency Placements $5.0 • DOC – Enhance Inmate Nutrition 1.5 • DOL – Maintain Funding for UI and other Federal Programs 0.5 • DOH – Provide Funding for Persons Displaced by Hurricane Maria 0.4

Technical and Caseload Adjustments

• Adjust Budget to Reflect GF Portion of 2017 Labor Agreement $54.6 • Fringe Benefits – Accounting Change for Higher Ed Alt. Retirement Plan 27.3 • DCF – Fund Juan F. Compliance Costs 16.3 • DOC – Annualize Funding for FY 2018 Deficiency 9.8 • DSS – Adjust Funding for TFA and State Supplement 8.2 • CSCU – Partially Restore Funding for Community Colleges 6.3 • DPH – Transfer Children's Health Initiatives from the Insurance Fund 2.9 • DCF – Re-estimate Caseload-Driven Expenditures 2.3 • DDS / DSS – Fund Money Follows the Person Placements 2.0

Other Budget Changes

• Reduces assessments on the insurance industry by almost 3.7% (approximately $3.5 million)

DPH - Children’s Health Initiatives account moved from the Insurance Fund to the General Fund

• This budget completes two agency reorganizations included in the bipartisan budget:

State Unit on Aging and Office of the Long Term Care Ombudsman are consolidated in the Department of Rehabilitation Services following federal model

Office of Health Strategy

• Office of Higher Education is consolidated into the State Department of Education as the Division of Post-Secondary Education, saving $300,000

• Budgeted agencies reduced from 81 in FY 2011 to 56 in FY 2019

• Establishes a .05% administrative assessment on the first $15,000 in wages paid to shore up the Department of Labor’s program operations. One-time funding of $500,000 is recommended for DOL until the assessment commences on January 1, 2019

25

Passport to the Parks and Tourism

• Passport to the Parks Fund The enacted budget included language making expenditures subject to

appropriations, but no appropriation was included in the adopted budget

The Governor proposes appropriating this fund

No other changes are proposed

• Tourism Fund Hotel Occupancy Tax increased from 15% to 17%

This raises $16.7 million, enabling the elimination of the $12.7 million transfer from the General Fund in the enacted budget

Spending adjustments include:

Increasing the investment in statewide tourism promotion and marketing by $3.8 million

Shifting support for the Connecticut Open from the General Fund to the Tourism Fund, and increasing support by $400,000

Providing DECD with resources for administering arts and tourism grants - $368,000

Arts and tourism grants maintained at the levels in the enacted budget26

Revenue

27

Restoring Balance to FY 2019

28

FY 2019

Amount

Eliminate the $200 property tax credit* 49.7$

Accounting change for Higher Ed Alt. Retirement 35.5

Repeal exemption for nonprescription drugs* 30.0

Limit $2.5 million cap on unitary to manufacturers 25.0

Increases to real estate conveyance tax rates* 22.9

Increase cigarette tax rate to $4.60/pack* 20.0

Corporate surcharge of 8% beginning in IY 2019 18.0

Expand bottle bill to wine & liquor at 25 cents* 13.0

Net impact of hotel occupancy tax changes* 12.7

Restore energy fund sweeps in FY 2019 (RGGI/Green Bank) (24.0)

All Other Changes - Net 31.8

234.6$ *Tax types modified or considered for adjustment in 2017

Major revenue changes in FY 2019 include:(in millions)

FY 2022

Amount

Maintain hospital tax at FY18/FY19 levels 516.0$

Eliminate restoration of the MRSA account 356.0

Eliminate the $200 property tax credit 105.0

Eliminate new exemption for pension income 57.5

Repeal 7/7 brownfield tax credit program 40.0

Eliminate new exemption for social security income 18.4

Eliminate $500 credit for STEM graduates 11.8

Eliminate restoration of the RPIA account 11.5

Eliminate transfer to the early childhood ed. program 10.0

Maintain teachers' pension exemption at 25% 8.0

Eliminate transfer to Tobacco & Health Trust Fund 6.0

All Other Changes - Net 151.7

1,291.9$

Reducing Out-year Budget Gaps

Changes which will significantly reduce out-year budget deficits include:

(in millions)

29

Protecting Connecticut From Federal Tax Changes

The Governor’s proposed budget introduces changes to ensure Connecticut remains competitive under the new federal tax regime:

• A revenue neutral tax on pass-through entities offset by a personal income tax credit will provide Connecticut’s small business owners with favorable federal tax treatment

• Allowing municipalities to create charitable organizations supporting town services, in conjunction with a local property tax credit, will allow our cities and towns to continue to provide services while reducing individuals’ federal taxes

In addition, to avoid a General Fund revenue loss:

• Connecticut will not adopt federal tax changes related to accelerated depreciation and asset expensing

• Federal estate tax exemption levels phase in by 2023

30

Proposed Capital Budget

31

Capital Budget Revisions

• $141 million in additional general obligation (GO) bond authorizations in FY 2019:

$100 million - continue rehabilitation of the XL Center in Hartford $25 million - continue information technology improvements in state

agencies $16 million - construct parking to support Bushnell area redevelopment

• These are in addition to previous authorizations by the General Assembly, which include:

$1.295 billion - various projects and programs $200 million - Next Generation Connecticut/UConn 2000 program $95 million - CSCU 2020 program $12.525 million - Bioscience Collaboration Program $15 million - Bioscience Innovation Fund

• These authorizations are offset by the cancellation of $40 million in existing GO bond authorizations

32

Addressing Long-Term Liabilities

33

State Employees’ Retirement SystemRecent benefit changes have reduced pension costs

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

5,0002

01

8

20

19

20

20

20

21

20

22

20

23

20

24

20

25

20

26

20

27

20

28

20

29

20

30

20

31

20

32

20

33

20

34

20

35

20

36

20

37

20

38

20

39

20

40

20

41

20

42

20

43

20

44

20

45

20

46

20

47

$ in

mill

ion

s

SERS (Before Recent SEBAC Agreements)

12/2016 Agreement

5/2017 Agreement

Note: The December 2016 agreement made changes to actuarial methods and assumptions, including a reduction in the assumed rate of investment return and revisions to the amortization period for portions of unfunded liability. The May 2017 agreement restructured wages and pension and healthcare benefits.

34

$21.7

$26.6

$31.2

$17.9 $16.2

$19.5 $18.9 $20.4

$17.4

$0.0

$5.0

$10.0

$15.0

$20.0

$25.0

$30.0

$35.0

2006 2008 2011withoutreforms

2011 withreforms

2012 2013 2015 2017withoutreforms

2017 withreforms

in b

illio

ns

35

• The Net OPEB Liability has decreased for the second valuation in a row. It would have increased if not for the reforms negotiated in the 2017 SEBAC agreement which include:

The implementation of a Medicare Advantage plan for existing Medicare-eligible retirees

Premium cost sharing and health care design changes for new retirees after October 1, 2017

Additional premium cost sharing for new retirees after June 30, 2022

• In addition, SEBAC 2011 required all employees to contribute 3% of salary to the OPEB Trust Fund for 10 years. SEBAC 2017 increased that to 15 years for new employees.

Other Post Employment BenefitsNet Liability

Teachers’ Retirement System

• The current funding methodology results in increasingly volatile changes in required contributions as we approach end of the fixed amortization period in 2032

• Covenants included in the pension obligation bonds issued in 2008 require full funding of the state contribution

• Mirroring the funding approach utilized for SERS last year will help minimize risk in future years

• As in 2017, proposed changes include: Reduced rate of return assumption Extended amortization period Transitioning to level dollar amortization Laddered amortization of future gains or losses

TRS Viability Commission report expected during 2018 session

36

Conclusion

37

Conclusion

The Governor’s budget proposal:

• Builds on framework of bipartisan budget

• Preserves structural changes

• Recommends revenues to avoid project deferrals, fare hikes, and service cuts to transportation

• Reduces out-year budget gaps by half

38