Recent trends in Private equity and Hybrid financing in Russia

15

1 NewRussiaGrowth Private Equity Advisors 2009 Alexander Abolmasov Recent trends in Private equity and Hybrid financing in Russia May I call you back? I am just in the middle of something.

-

Upload

alexander-abolmasov -

Category

Economy & Finance

-

view

1.396 -

download

1

Transcript of Recent trends in Private equity and Hybrid financing in Russia

1

NewRussiaGrowth Private Equity Advisors

2009

Alexander Abolmasov

Recent trends in Private equity and Hybrid financing in Russia

May I call you back? I am just in the middle of something.

2

- Liquidity crisis-We expect second wave of liquidity crisis in 3-5 months

- Private equity trends

- Hybrid financing trends

3

Credit crisis – problems with liquidity

- The amount of Russian corporate debt due in 2009 will be about $350bn out of $900bn outstanding:

- $200bn Russian bank loans

- $120bn external debt (syndicated loans and eurobonds)

- $27bn domestic bonds

-International debt capital (syndicated loans or Eurobonds) is accessible only to biggest Russian corporations

-24% of Russian Eurobonds are Gazprom, another 29% - VTB, Sberbank, TNK-BP, Gazprombank and Agricultural bank.)

- Mid-sized Russian companies have problems with access to their usual sources of debt :

- local bank loans

- domestic ruble bonds

Source: Central Bank of Russia

Source: Central Bank of Russia

Bank loans55061%

Ruble bonds455%

External debt 30034%

Bank loans

Ruble bonds

External debt

Russian outstanding corporate debt structure, $bn

up to 6 months

9%

6-12months27%

1-3 years29%

after 3 years35%

Bank loans term structure, %

44

Russian Banking System – liquidity problems for next 2-3 years

- New money is not available from the banks

- State banks (all TOP 5 banks) share increased from 42% to 47% of total loans since August 2008.

- Overwhelming share of government support goes to state banks

- State banks prioritize large state companies

- Private banks have problems with capital, because of losses and NPL, which could reach 10-30% by the end of 2009.

Source: Central Bank of Russia, Sberbank, RenCap

Source: Central Bank of Russia

-100

-50

0

50

100

150

200

3Q07 4Q07 1Q08 2Q08 3Q08 4Q08 1Q09 2Q09 E 3Q09 E 4Q09 E

Russian banking system capital and additional capital required to keep the current loan portfolio

Russian banking system capital

Additional capital required according to Renaissance forecast (real NLB rate 1Q09 -10%; 4Q09E -40%)

Additional capital required according to Sberbank forecast (real NLB rate 1Q09 -10%; 4Q09E -30%)

$bn

200

250

300

350

400

450

500

Dec

-06

Feb-

07

Apr

-07

Jun-

07

Aug

-07

Oct

-07

Dec

-07

Feb-

08

Apr

-08

Jun-

08

Aug

-08

Oct

-08

Dec

-08

Feb-

09

Apr

-09

Jun-

09

Aug

-09

Oct

-09

Dec

-09

Russian corporate loans outstanding $bn

5

Credit crisis – Corporate ruble bonds market will almost cease to exist

Source: cbonds.ru

- Banks were main buyers of bonds, but now the liquidity dried up

- No new corporate bond issues since August 2008 apart from Gazpromneft and Russian RailRoads (expected in April 2009)

- Average duration of domestic ruble bonds is just 0.86 years

- For third tier issues only 0.45 years

Source: Micex emission documents, evaluation of Bank of Moscow

0,0

1,0

2,0

3,0

4,0

5,0

6,0

Redemption Coupons Put option

The schedule of monthly payments of corporate sector*bn. $

0

10

20

30

40

50

60

70

80

Ap

r-00

Oct

-00

Ap

r-01

Oct

-01

Ap

r-02

Oct

-02

Ap

r-03

Oct

-03

Ap

r-04

Oct

-04

Ap

r-05

Oct

-05

Ap

r-06

Oct

-06

Ap

r-07

Oct

-07

Ap

r-08

Oct

-08

Ap

r-09

Oct

-09

Ruble corporate bonds outstanding$bn.

6

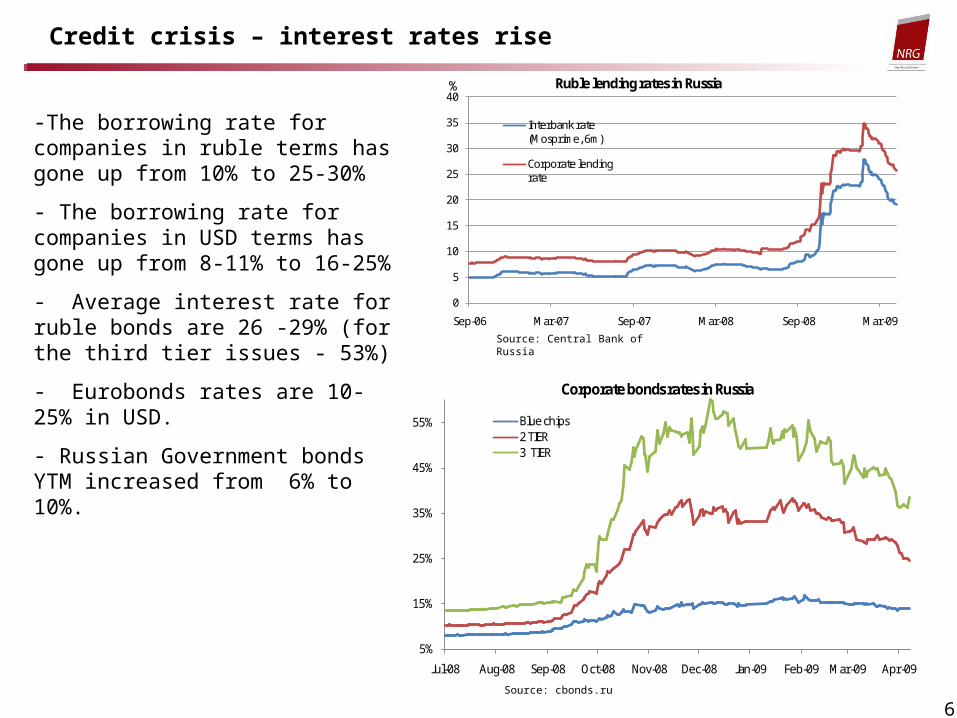

Credit crisis – interest rates rise

-The borrowing rate for companies in ruble terms has gone up from 10% to 25-30%

- The borrowing rate for companies in USD terms has gone up from 8-11% to 16-25%

- Average interest rate for ruble bonds are 26 -29% (for the third tier issues - 53%)

- Eurobonds rates are 10-25% in USD.

- Russian Government bonds YTM increased from 6% to 10%.

Source: cbonds.ru

Source: Central Bank of Russia

0

5

10

15

20

25

30

35

40

Sep-06 Mar-07 Sep-07 Mar-08 Sep-08 Mar-09

Ruble lending rates in Russia

Interbank rate (Mosprime, 6m)

Corporate lending rate

%

5%

15%

25%

35%

45%

55%

Jul-08 Aug-08 Sep-08 Oct-08 Nov-08 Dec-08 Jan-09 Feb-09 Mar-09 Apr-09

Blue chips2 TIER3 TIER

Corporate bonds rates in Russia

7

- Liquidity crisis-We expect second wave of liquidity crisis in 3-5 months

- Private equity trends -Private equity funds have problems with access to new money

- Hybrid financing trends

8

• Total AUM of the global PE industry has grown from $960bn in 2003 to just under $2.5trn in 2008

• Overhang of $250bn of private equity fund interests:

• Liquidity problem (28%)• Denominator effect (35%)

LPs want to reduce exposure to private equity

9

PE still out-perform other asset classes

Money weighted all PE average IRR’s

Source: Preqin, Volume 5, Issue 1

Med

ian

retu

rn (%

)

• PE returns will decline, especially the 2005-2007 vintages

• Median return from PE outperforms equities and real estate

Median return by asset classes of public pension plans, as of June 2008

10

Problems with distributions and valuations

• Distributions from PE funds reduced 3-5 times in 2008 compared with 2007

• Problems with valuation:

• Number of funds with no valuation change increased from 15% to 80%.

11

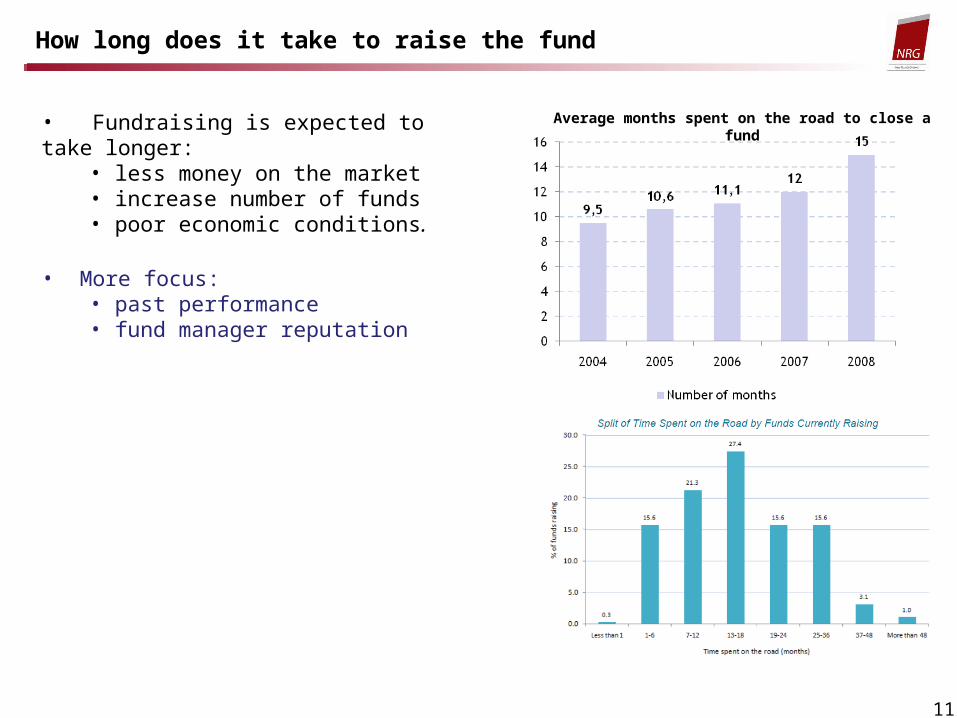

How long does it take to raise the fund

Source: Preqin

Average months spent on the road to close a fund• Fundraising is expected to take longer: • less money on the market • increase number of funds • poor economic conditions.

• More focus: • past performance• fund manager reputation

12

- Liquidity crisis-We expect second wave of liquidity crisis in 3-5 months

- Private equity trends -Private equity funds have problems with access to new money

- Hybrid financing trends -Hybrid financing funds is a temporary solution

13

Russian specific:

• Distressed funds will have very risky investment profile.

• Mezzanine funds will replace banks, which stopped to provide new money.

Corporate Restructuring:

• Acquire defaulted assets at deep discounts to intrinsic value;• Swap debt for equity.

Distressed Portfolios: Acquiring “Bad Bank” Assets • Seek deeply discounted portfolio;• Acquire and restructure portfolios into tranches and opportunistically sell off portions of

portfolios; and • Manage “bad bank” assets sourced from western funds, banks and other investors.

14

Example: Distressed debt strategy

15

Volga River Credit Opportunity Fund

Senior Debt with Equity Kickers

Strategy•18-24 month senior loans in USD•Low volatility businesses•No distressed companies•Collateralized•$10-50m ticket size•15%+ current return•Equity kickers – 30%+ gross return

Target industies•Non-cyclical (food and beverages, telecoms)•Counter-cyclical industries (discounters, fast food)•Import-substitution (agriculture, pharmaceuticals) •Exporters (petrochemicals)

Deal terms to include•Strong security•Control over use of funds•Board participation and strong shareholder-type negative covenants•Amortization after 15-18 months