Rebels too old for a cause - · PDF fileRebels too old for a cause The dying motorcycle market...

22

Page 1 INTELLIGENCE, INDEPENDENCE, INTEGRITY www.analogica.jp Rebels too old for a cause The dying motorcycle market in Japan :; Mike Newman President & CEO Analogica K.K. May 23 rd , 2017

Transcript of Rebels too old for a cause - · PDF fileRebels too old for a cause The dying motorcycle market...

Page 1 INTELLIGENCE INDEPENDENCE INTEGRITY wwwanalogicajp

Rebels too old for a cause

The dying motorcycle market in Japan

Mike Newman President amp CEO Analogica KK

May 23rd 2017

Page 2 INTELLIGENCE INDEPENDENCE INTEGRITY wwwanalogicajp

1700000 gave up

motorcycle licenses in last 6 years

Who owns What

Executive Summary

The average age of motorcyclists in Japan is 53 years old and continuing to climb as younger riders

looking to obtain new licenses continues to drift Between 2010 and 2016 the Japanese National

Police Agency (JNPA) noted that large capacity motorcycle license holders (ogata ndash classified as

400cc+) have fallen by nearly 1500000 While mid-size (chugata ndash classified as below 400cc) have

risen around 715000 Female riders have shown a similar pattern of 178000 fall in ogata licenses

and 147000 increase in chugata respectively While there are still 9175mn men and 625000

women willing to get out on the highway with large capacity bikes the trend is alarming More

frighteningly new graduates arenrsquot lining up either 30000 fewer students lined up to get a mid or

large size bike license between 2014 and 2016 representing a 123 dip denoted by the red line in

Fig1

Source JNPA

Ownership

The Japanese motorcycle market is dominated by lt50cc scooters (referred to as gentsuki) Gentsuki

are popular because they can be ridden even with a standard Japanese car driverrsquos license The

gentsukirsquos low cost ($1000-1500) makes it practical to do short trips to the supermarket or

commutes especially considering the congested roads in Japan Fig2 Larger bore bikes are only

13 of the 12 million bikes on the road in Japan Motorcycles below 250cc do not require shaken

(compulsory inspection) unlike their bigger brothers

99

-2

7

-31

-4

0

-54

-5

5

-57

-6

0

-62

-6

6

-75

-7

6

-76

-8

0

-83

-8

5

-86

-8

9

-10

3-1

04

-10

7-1

10

-11

4-1

14

-11

7-1

17

-12

7-1

27

-13

2-1

33

-13

6-1

43

-14

5-1

45

-14

9-1

53

-15

8-1

60

-16

4-1

68

-17

2-1

73

-17

6-1

83

-19

3-2

01

-22

0

-350

-300

-250

-200

-150

-100

-50

00

50

100

150

Yam

agat

aFu

kui

Miy

azak

iK

agaw

aW

akay

ama

Saga

Ho

kkai

do

Shim

ane

Toky

oC

hib

aG

ifu

Niig

ata

Mie

Ku

mam

oto

Ehim

eSa

itam

aO

saka

Nar

aG

un

ma

Yam

anas

hi

Ibar

aki

Toch

igi

Yam

agu

chi

Nag

ano

Kyo

toIw

ate

Hir

osh

ima

Ko

chi

Nag

asak

iK

anag

awa

Ish

ikaw

aO

ita

Aic

hi

Fuku

oka

Ao

mo

riSh

iga

Oki

naw

aM

iyag

iH

yogo

Fuku

shim

aA

kita

Shiz

uo

kaTo

yam

aK

ago

shim

aTo

kush

ima

Oka

yam

aTo

tto

ri

Fig1 - Total New Motorcycle Graduates change (2016 vs 2014)

Page 3 INTELLIGENCE INDEPENDENCE INTEGRITY wwwanalogicajp

Gentsuki

Large bore only 13 of

total

Source JAMA

However ownership levels for gentsuki have been sliding for over a decade from around 980000

units per annum to just under 700000 Motorcycles over 50cc have shown the opposite although

at a very slow pace nudging over 500000 units before drifting back to 450000

Source JAMA

Larger bore motorcycle trends are slowly grinding higher In the 250cc+ market BMW holds an

effective 58 market share Harley Davidsonrsquos share is approximately 13 Yamaha made good

progress with the MT-0709 series which gave consumers a reasonably priced (yen700000-900000)

naked bike with ample performance The initial sales target of 1500 units annually was quickly raised

to 4000 after its release Simply put good product sells

Annual motorcycle sales in Japan hit a peak of 328 million in 1982 but decreased to 450000 by

2014 according to JAMA

6889459 58

1582925 13

1959845 16

1542856 13

Fig 2 Japan Motorcycle Ownership - Units (2012)

Scooter (lt50cc) 50cc-125cc) 125cc-250cc 250cc+

0

200000

400000

600000

800000

1000000

1200000

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Fig3 Trend of Japanese Motorcycle Purchase (2001-2012)

Gentsuki Motorcycle

Page 4 INTELLIGENCE INDEPENDENCE INTEGRITY wwwanalogicajp

Return riders

Emissions laws

Product offerings are clearly important One of the most significant trends is the popularity of

motorcycle sales to middle-aged and older people wanting larger capacity bikes than the common

250cc These people are often return riders The average age of motorcycle riders is now 53 up 93

years on 2005 Multi bike ownership is on the rise after the Global Financial Crisis in 2008

Source JAMA

Japanrsquos large bore domestic market has been hindered by restrictive emissions laws and power

limiters Some Japanese motorcycle purchasers prefer overseas specification motorcycles known

as reverse imports to dispense with the restrictions of the domestic offerings

A good example of this is the Yamaha XJR1300 The domestic version has not changed for the last

six years but there is no plan to introduce the 2017 European model in the Japanese market The

EuropeanUS version of the bike is offered under the branding of lsquoborn customisedrsquo Fig6

Fig 6 Domestic (left) and Overseas (right) versions of Yamaharsquos XJR1300

Source Company Data

So what drives the Japanese motorcycle buyer What are the main concerns and what are the

trends we should pay attention to

lt50cc 51-125cc 126-250cc 250cc+

2012 246095 90291 45306 60715

2013 238786 100947 55441 65289

2014 228918 96249 54303 70151

2015 236000 97000 56000 68000

0

50000

100000

150000

200000

250000

300000

Fig 4 Japan - New Motorcycle Sales by Engine Size

2012 2013 2014 2015

1 Bike 2 Bikes 3 Bikes 4+ Bikes Average

2005 68 19 5 4 14

2007 64 21 6 5 15

2009 50 13 4 2 14

2011 69 21 5 5 15

2013 58 26 8 8 16

01020304050607080

Fig 5 Motorcycle Ownership by individual household (units)

2005 2007 2009 2011 2013

Page 5 INTELLIGENCE INDEPENDENCE INTEGRITY wwwanalogicajp

JAMA study

Age

Replacement

Parking

Desire

Women

No real change in 2013

survey

Average ownership up

Foreign brands more

popular in large bore market

The Japan Automotive Manufacturers Association (JAMA) conducted a survey of 5150 people on

trends in motorcycling in Japan in 2011 Their findings were

A) Ownership declined among users in their 30s or younger but increased among users in

their 50s or older underscoring the continued rise in the average age of motorcycle users

B) Replacement demand accounted for 59 of all new-model purchases up from 57 in the

2009 survey First-time purchases accounted for 15 of the total not significantly different from

the previous surveyrsquos figure but underscoring a sustained decline in first-time motorcycle

purchases

C) Over 76 of owners in Tokyo (ie its main 23 wards) reported experiencing difficulties in

finding a parking space for their motorcycles

D) Respondents expressing the desire to continue riding motorcycles in the future totaled

87 down from the 92 peak recorded in 2009

E) A large percentage of women respondents viewed motorcycles as a ldquoMeans of transportrdquo and

ldquoLifestyle commodityrdquo while a significant percentage of male respondents considered them

a ldquoHobby itemrdquo

In 2013 the results from JAMArsquos survey was largely unchanged

F) Ownership has continued to decline steadily among young men in their teens 20s and

30s Ownership by women has levelled off since fiscal 2009 although among women

respondents in their 50s or older the ownership rate surpassed 60 Meanwhile ownership of

scooters and business-use lightweight motorcycles under 50cc in engine capacity among users

in their 50s or older has grown more pronounced

G) The average period of motorcycle ownership prior to its replacement with a new purchase

was 66 years up from the previous surveyrsquos 61 years This confirms the trend towards longer

ownership which was particularly marked for scooters 50cc and under in engine capacity Large

capacity motorcycles have an average turnover of 41 years up from 39 years 250cc-400cc

motorcycle ownership periods remained flat at 34 years

H) Respondents expressing the desire to continue riding motorcycles in the future totaled

88 up slightly from the 87 indicated in the previous survey but still down from the peak of

92

While overall motorcycle license holders continue to increase in aggregate what is the rate of new

license holders Is it rising falling

Financing trends have remained pretty consistent at 12 of overall sales according to JAMA with

many preferring to pay cash

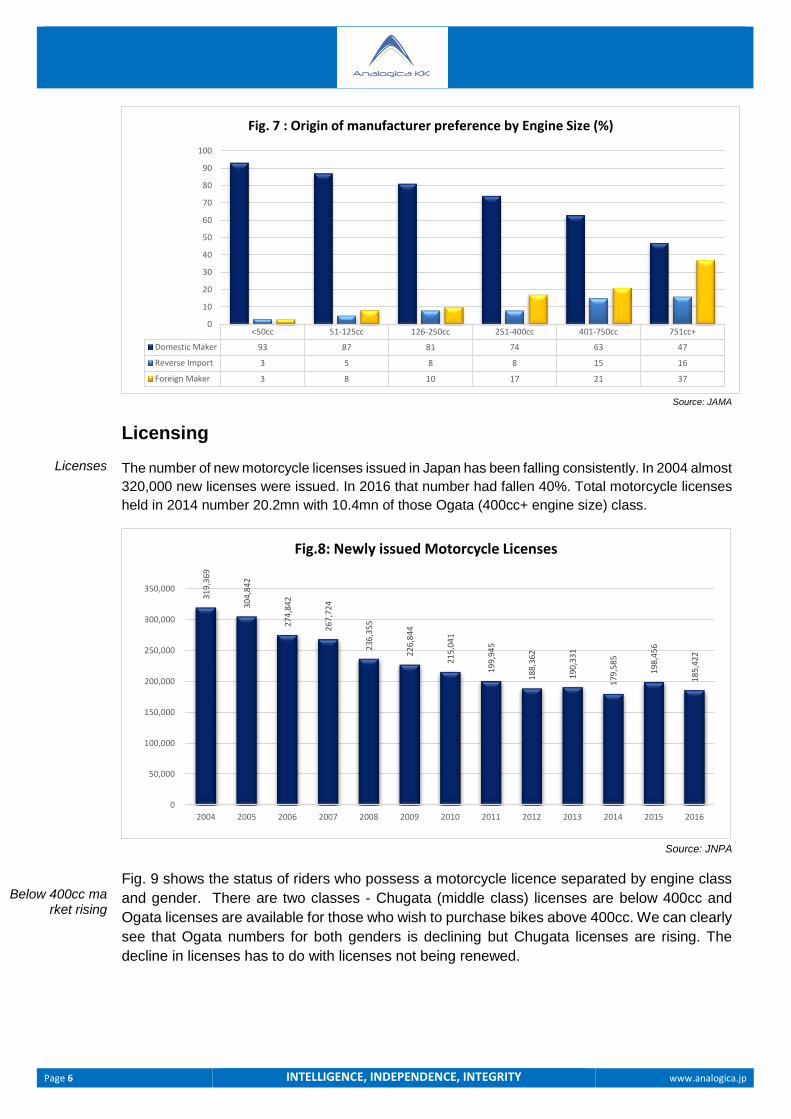

There is an inverse correlation between domestic brands and engine size Fig7 Foreign brand

popularity is driven in part due to the higher average engine capacity

Page 6 INTELLIGENCE INDEPENDENCE INTEGRITY wwwanalogicajp

Licenses

Below 400cc market rising

Source JAMA

Licensing

The number of new motorcycle licenses issued in Japan has been falling consistently In 2004 almost

320000 new licenses were issued In 2016 that number had fallen 40 Total motorcycle licenses

held in 2014 number 202mn with 104mn of those Ogata (400cc+ engine size) class

Source JNPA

Fig 9 shows the status of riders who possess a motorcycle licence separated by engine class

and gender There are two classes - Chugata (middle class) licenses are below 400cc and

Ogata licenses are available for those who wish to purchase bikes above 400cc We can clearly

see that Ogata numbers for both genders is declining but Chugata licenses are rising The

decline in licenses has to do with licenses not being renewed

lt50cc 51-125cc 126-250cc 251-400cc 401-750cc 751cc+

Domestic Maker 93 87 81 74 63 47

Reverse Import 3 5 8 8 15 16

Foreign Maker 3 8 10 17 21 37

0

10

20

30

40

50

60

70

80

90

100

Fig 7 Origin of manufacturer preference by Engine Size ()

319

369

304

842

274

842

267

724

236

355

226

844

215

041

199

945

188

362

190

331

179

585

198

456

185

422

0

50000

100000

150000

200000

250000

300000

350000

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Fig8 Newly issued Motorcycle Licenses

Page 7 INTELLIGENCE INDEPENDENCE INTEGRITY wwwanalogicajp

Driving schools

expensive

Source JNPA

Let us consider the cost to get a Japanese motorcycle license One cannot get an Ogata license

without getting Chugata first Fig 10 highlights the high cost of getting a license The dots represent

standard (blue) double time (red) and fast (green) So to get a full bore Ogata license from no license

at all could set one back over $3000 One could try to avoid the cost and try at the official test

centres but the tests are designed to test memory rather than skill to force schooling The schools

are authorised to give passing grades for licenses at the end of tuition and well over 95 of students

that go to these schools pass

Fig 10 Hinomaru Driving School costs to get a motorcycle license - $3000+ investment

Source Hinomaru Driving School

Ogata (400cc+)- Men Chugata (lt400cc)- Men Ogata (400cc+)- Women Chugata (lt400cc) - Women

2010 10670417 7842426 802520 1172508

2011 10427177 7956291 770726 1198582

2012 10193671 8086072 745259 1224714

2013 9997273 8220635 726418 1252057

2014 9732861 8343178 697214 1276514

2015 9454801 8453963 657783 1298578

2016 9175340 8557534 624476 1320082

0

2000000

4000000

6000000

8000000

10000000

12000000

Fig 9 Motorcycle Licence Holders in Japan by Type

2010 2011 2012 2013 2014 2015 2016

Motorcycle

Chugata

Ogata

Category License Class License Status

No

License

Car

License

Chugata

Plan Time Tuition Enrollment Fee

Page 8 INTELLIGENCE INDEPENDENCE INTEGRITY wwwanalogicajp

Young go small

Fig 11 denotes the number of chugataogata graduates from motorcycle license schools in 2016 The

yellow bars denote a GDPcapita ratio at 5 below the national average or above

Source JNPA

Fig12 shows at what age groups people move to take up their motorcycle licenses Chugata

licenses are the main target of the 20s-40s with Ogata picking up after 50s as the common

motorcycle license type It would be fair to assume that affordability is a likely factor in choosing a

license both schooling and motorcycle cost

Source JAMA Note some double counting due to multiple licenses taken out (eg Ogata amp car)

0

5000

10000

15000

20000

25000

Kan

agaw

a

Toky

o

Osa

ka

Kyo

to

Sait

ama

Aic

hi

Hyo

go

Ch

iba

Fuku

oka

Shiz

uo

ka

Hir

osh

ima

Toch

igi

Ho

kkai

do

Oki

naw

a

Ibar

aki

Miy

agi

Ku

mam

oto

Niig

ata

Oka

yam

a

Gif

u

Fuku

shim

a

Gu

nm

a

Mie

Kag

osh

ima

Shig

a

Ehim

e

Nag

ano

Yam

agat

a

Wak

ayam

a

Miy

azak

i

Nag

asak

i

Nar

a

Kag

awa

Oit

a

Saga

Yam

agu

chi

Yam

anas

hi

Ish

ikaw

a

Ao

mo

ri

Iwat

e

Shim

ane

Ko

chi

Toya

ma

Toku

shim

a

Fuku

i

Aki

ta

Tott

ori

Fig 11 - ChugataOgata Licence Graduates by prefecture (2016)

10s 20s 30s 40s 50s 60s 70+

Gentsuki Only 26 10 2 2 2 3 22

Car License incl Gentsuki 47 22 13 16 21 31 14

Bike license lt250cc 4 2 3 5 7 8 12

Chugata 22 57 61 61 37 11 7

Ogata 2 17 30 29 32 46 41

0

10

20

30

40

50

60

70

Fig 12 Age when Motorcyclists take up a license ()

Gentsuki Only Car License incl Gentsuki Bike license lt250cc Chugata Ogata

Page 9 INTELLIGENCE INDEPENDENCE INTEGRITY wwwanalogicajp

Female age rising

Sourcing information

Source JAMA

The average age of female and male riders has risen from 43-44yo range in 2005 to 53yo range in

2015 Thinking of it another way these 43-44yo group just grew 8 years old along with the survey

by JAMA Figs 15-16

Source JAMA

JAMArsquos 2013 motorcycle survey revealed that dealerships are a key source of information on

motorcycles followed by websites Fig 17

10s 20s 30s 40s 50+

2005 10 32 29 18 11

2007 3 27 29 22 19

2009 4 22 23 30 20

2011 3 23 21 29 24

2013 4 16 19 29 19

05

1015

20

2530

35

Fig 13 251cc-400cc Bike Ownership by Age ()

2005 2007 2009 2011 2013

10s 20s 30s 40s 50+

2005 1 22 23 35 18

2007 1 13 32 38 17

2009 0 12 30 33 23

2011 0 12 19 36 32

2013 0 6 15 33 42

05

1015202530354045

Fig 14 400cc+ Bike Ownership by Age ()

2005 2007 2009 2011 2013

10s 20s 30s 40s 50sAverage

Age

2005 7 14 21 23 34 429

2007 5 10 19 22 43 460

2009 4 8 18 25 45 470

2011 3 7 15 25 49 484

2013 3 5 10 24 58 510

0

10

20

30

40

50

60

70

Fig 15 Average Age of Motorcycle Riders Male ()

2005 2007 2009 2011 2013

10s 20s 30s 40s 50sAverage

Age

2005 11 19 16 13 42 442

2007 7 20 12 15 46 452

2009 6 8 11 16 59 489

2011 6 8 11 17 58 510

2013 8 6 9 17 61 520

0

10

20

30

40

50

60

70

Fig 16 Average Age of Motorcycle Riders - Female ()

2005 2007 2009 2011 2013

Page 10 INTELLIGENCE INDEPENDENCE INTEGRITY wwwanalogicajp

Large bore attracts

hobbyists

Source JAMA

However JAMA also highlights (Fig18) that as engine size grows motorcycle magazines become a

very important source of new information Although there are dedicated BMW magazines (including

a dedicated version lsquoBMW Boxer Journalrsquo in Japan other broader magazines lsquoBike Brosrsquo lsquoBikejinrsquo

and the like are equally important to attract new customers Larger bore motorcycle riders clearly

view motorcycles as a hobby

Source JAMA

DealerMaker

WebsiteMotorcycleMagazine

CataloguePamphlet

Otherwebsite

Heard fromFriendExp

ert

Saw parkedon Street

Saw RidingPast

Pamphlet Newspaper Direct MailMotorsho

wTV Ad

MagazineAd

2005 40 7 13 11 2 6 6 4 2 1 0 0 2 1

2007 38 9 12 11 2 6 5 5 2 1 0 0 1 1

2009 41 12 11 9 3 5 3 3 1 0 0 0 1 0

2011 40 14 10 9 6 6 5 4 1 0 0 0 0 0

2013 43 14 9 7 6 6 4 3 1 1 0 0 0 0

0

5

10

15

20

25

30

35

40

45

50

Fig 17 How motorcycle riders source information on bikes () by year

2005 2007 2009 2011 2013

DealerMaker

WebsiteMotorcycleMagazine

CataloguePamphlet

Otherwebsite

Heard fromFriendExp

ert

Sawparked on

Street

Saw RidingPast

Pamphlet Newspaper Direct MailMotorsho

wTV Ad

MagazineAd

lt50cc 54 11 2 8 3 5 3 3 2 1 0 0 0 0

51-125cc 30 19 12 7 7 8 6 5 1 1 0 0 0 0

126-250cc 18 19 29 4 14 5 3 3 0 0 0 1 0 0

251-400cc 14 24 26 5 10 5 4 6 0 0 0 1 0 0

401-750cc 13 18 41 2 12 4 1 0 0 0 0 4 0 0

751cc+ 16 16 37 1 8 6 2 2 0 0 0 5 1 0

0

10

20

30

40

50

60

Fig 18 How motorcyclists gain information on bikes () by engine size

lt50cc 51-125cc 126-250cc 251-400cc 401-750cc 751cc+

Page 11 INTELLIGENCE INDEPENDENCE INTEGRITY wwwanalogicajp

Trend of the Japanese

Source JAMA

The plight of the Japanese makers globally

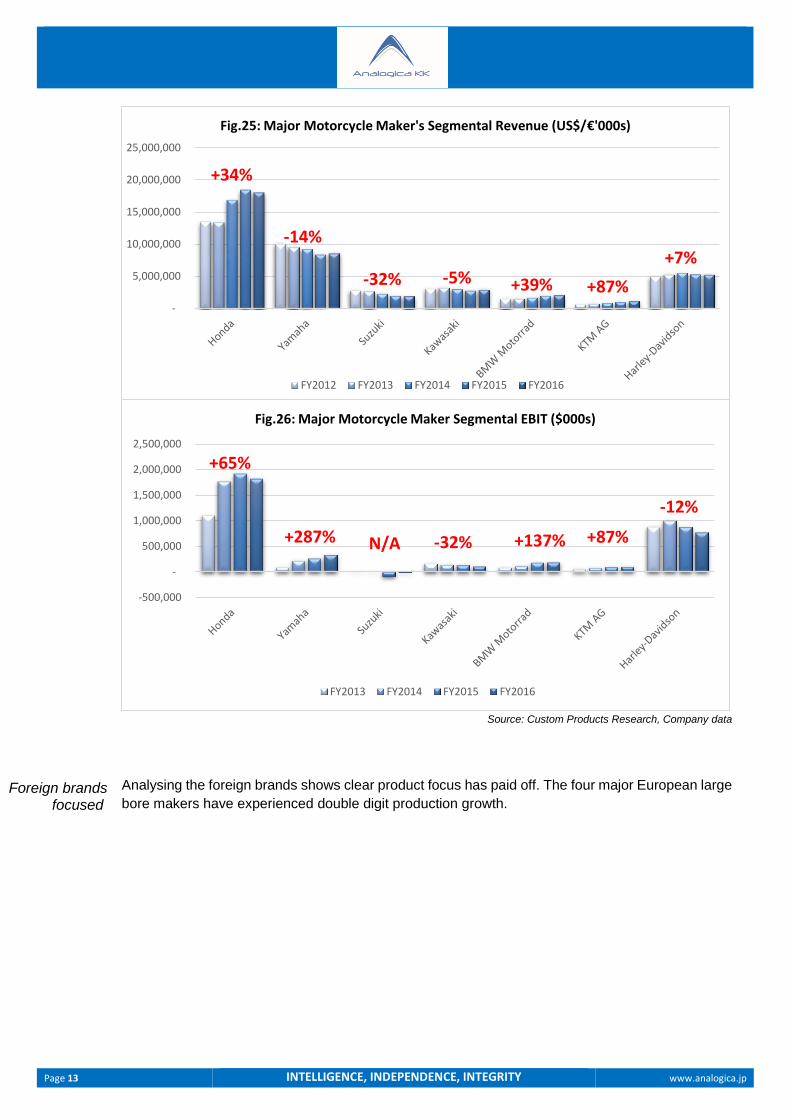

Looking over the last 5 years Japanese motorcycle manufacturers have been struggling Honda

remains at the top of the production tree at 177 million units but Yamaha has trended down while

Suzuki continues to suffer the steepest drop of all makers declining 8-19 per annum Kawasaki

Heavy has maintained a more focused strategy with larger bore motorcycles

Source Custom Products Research Company data

When analysing the contribution that motorcycle segments make to the Japanese makersrsquo group

revenue and EBIT we see the following

0

10

20

30

40

50

60

70

Want adifferent

type

Want to ridedifferentengine

capacity

Want toseparate use

Conveniencevs Hobby

Want to addto hobby

StyleDesign Current bikereliability

gettingworse

New modelrelease

Current bikeservicinggetting

expensive

Economicsituationimproved

Cheap price Touring withFamily

Members

Dealerpushed hard

Fig 19 Why owners choose a second bike ()

2011 2013

15494000

6090000

2574000

544000

17661000

5154000

1367000 540000

-

2000000

4000000

6000000

8000000

10000000

12000000

14000000

16000000

18000000

20000000

Honda Yamaha Suzuki Kawasaki

Fig20 Japanese makers Global Motorcycle Production (units)

FY2012 FY2013 FY2014 FY2015 FY2016

Page 12 INTELLIGENCE INDEPENDENCE INTEGRITY wwwanalogicajp

EBIT marhins

Source Custom Products Research Company data

Unsurprisingly Yamaha is the purest motorcycle play (Fig21) in Japan However its contribution

from motorcycles has been declining as a percentage of total revenue There are two factors at play

One is the growth in sales of boat engines (where it commands 40 a global share) and second is

a focus on more profitability per unit Fig22 EBIT margins for the global motorcycle majors can be

seen here Honda has seen its motorcycle segment grow as a percent of group EBIT due to weaker

performances in cars Suzuki is the worst performer

Source Custom Products Research Company Data

00

200

400

600

800

Honda Yamaha Suzuki Kawasaki

Fig21 Japanese motorcycle makers revenue as of group

FY2012 FY2013 FY2014 FY2015 FY2016

-200-100

00100200

300400

Honda Yamaha Suzuki Kawasaki

Fig 22 Japanese motorcycle makers EBIT as of group

FY2012 FY2013 FY2014 FY2015 FY2016

101

39

-05

38

90 90

147

-100-500050

100150200

Fig23 Major Motorcycle Makers segmented (not group) EBIT Margins ()

FY2012 FY2013 FY2014 FY2015 FY2016

3972 84

30

100 90

175

00

50

100

150

200

250

Fig 24 Group EBIT Margins ()

FY2012 FY2013 FY2014 FY2015 FY2016

Page 13 INTELLIGENCE INDEPENDENCE INTEGRITY wwwanalogicajp

Foreign brands focused

Source Custom Products Research Company data

Analysing the foreign brands shows clear product focus has paid off The four major European large

bore makers have experienced double digit production growth

-

5000000

10000000

15000000

20000000

25000000

Fig25 Major Motorcycle Makers Segmental Revenue (US$euro000s)

FY2012 FY2013 FY2014 FY2015 FY2016

+34

-14

-32 -5 +39 +87

+7

-500000

-

500000

1000000

1500000

2000000

2500000

Fig26 Major Motorcycle Maker Segmental EBIT ($000s)

FY2013 FY2014 FY2015 FY2016

+65

+87+137-32NA+287

-12

Page 14 INTELLIGENCE INDEPENDENCE INTEGRITY wwwanalogicajp

Efficiency

Severe pressure

Source Custom Products Research Company data

One thing Figs 20 amp 27 point out is that focused strategies appear to be paying off for the Europeans

and to some extent Kawasaki which has moved away from a me-too approach Efficiency and brand

seems to be paying off for BMWrsquos continued rise and a broad range of product unlike Harley which

seems to be stuck in a divine franchise scenario Profitable but struggling to break out of cruisers It

has had a stab at sports bikes through Buell (business was spun off and EBR has since closed) and

the Porsche designed V-Rod (now out of production) Now that Ducati is potentially being sold by

Audi does Harley look to use a proper sports brand with no clash in its line up to fuel (no pun

intended) its growth

Summary The Japanese motorcycle market is under severe pressure It is little wonder that the domestic

makers arenrsquot exerting too much effort into the market given the long-term decline in the market Half

of the decline is driven by apathy and poor product placement The lsquobuild it and they will comersquo dealer

model is a sure fire way to ensure the market dies The foreign luxury brands appear to be gaining

share They continue to target the heart not the head like the Japanese makers Yamaha Motor has

been the most proactive of the domestic makers in providing a product that attracts new riders Such

has the success been of the Yamaha Bolt that Harley-Davidson has had to respond with a

yen1000000 entry level model Sadly with 1800000 male and female motorcycle license holders

giving up the right to ride over the last 6 years there is not much time left to save the remaining 10

million that remain

The differences between the focused foreign brands and the everything for everyone Japanese is

clear While Honda can grunt with its huge economies of scale sadly Suzuki needs to resurrect its

former glories of the 1980s rather than produce more me-too Kawasaki would seem to have worked

that out

On top of that the employment situation in Japan doesnrsquot lend itself to allow for investment in such

hobbies as motorcycles We outline that plight in the appendix

-

50000

100000

150000

200000

250000

300000

BMW Motorrad KTM AG Harley-Davidson Ducati Triumph

Fig 27 Non-Japanese Motorcycle Maker Production (units)

FY2012 FY2013 FY2014 FY2015 FY2016

+28

+15+26

+6

+70

Page 15 INTELLIGENCE INDEPENDENCE INTEGRITY wwwanalogicajp

Income

Assets

Unemployment

Appendix - Income amp Demographics

Assessing the demographics of financial assets by age group there is no question that the 40s-50s

segments have more assets than the 20-30s cohort This means that a makers are unlikely to make

huge inroads with the set (backed up by the JAMA survey) in a declining market targeting an age

group that has proved less interested in riding than the peak of 2009

Fig 28 bears out the trend Remember that the 50s set are far more likely to buy gentsuki according

to JAMA For the target BMW KTM Harley or Triumph motorcycle buyer 30s to 50s should be the

addressable market comprising around 40 of assets by age

Source Japan Central Council for Financial Service Information

Here is where it gets tricky After the Global Financial Crisis of 2008 unemployment rates in Japan

have drifted downwards Fig 29 However this masks the new reality of the composition of

employment The quality of employment is deteriorating

Source Statistics Bureau

The days have passed when most department stores had their elevator girls and train stations had

their confetti bag laden ticket clippers waiting at the exits But Japan if anything is moving further

20-29 05 30-39 56

40-49 128

50-59 21860-69 366

70+ 227

Fig 28 Total Financial Assets by Age Group

20-29 30-39 40-49 50-59 60-69 70+

00

20

40

60

80

100

15~24 25~34 35~44 45~54 55~64 65+

Fig 29 Unemployment Rate by Age Group (2007-2015)

2007 2008 2009 2010 2011 2012 2013 2014 2015

Page 16 INTELLIGENCE INDEPENDENCE INTEGRITY wwwanalogicajp

Changes in labour laws

FT vs PT

towards a service economy Unfortunately the labour productivity gains over the last 20yrs have

come almost exclusively from the manufacturing sector with retail transport restaurants hotels and

business services falling well below their global peers for productivity At least the service is still

great

Significant revisions to the labour personnel dispatch laws in rsquo95 and rsquo99 made it much easier to

employ irregular and subcontract workers and hence began a dumbing-down of the workforce since

less time was spent on education and training in general (putting Japanese workers in more direct

competition with their Asian neighbours) Average monthly wages (including overtime bonus and

social welfare deductions) have generally been flat over the last 5 years though increased 03 in

2015 due to overtime and bonuses but management is reticent to add to fixed costs with wage

increases as it would rather maintain flexibility through higher bonuses Legally mandated social

welfare costs mainly paid by employers have risen at a compound rate of 139 pa over the last

20 years while nominal wages have only increased 027 pa such that social welfare costs have

risen from 104 to 148 of wages during this time

Fig 30 Wages by type of employment by age (yenhour)

Source Ministry of Health Labor amp Welfare (MHLW)

The long running trend of full-time work in a regular capacity has given way to a lot more part-time

(lower paying) jobs which involves less lsquoother costsrsquo like insurance retirement and so on This

change puts pressure on the household budget The instance of lower paid part-time work has grown

since then from 30 to 374 of the total For women this is now 56

Page 17 INTELLIGENCE INDEPENDENCE INTEGRITY wwwanalogicajp

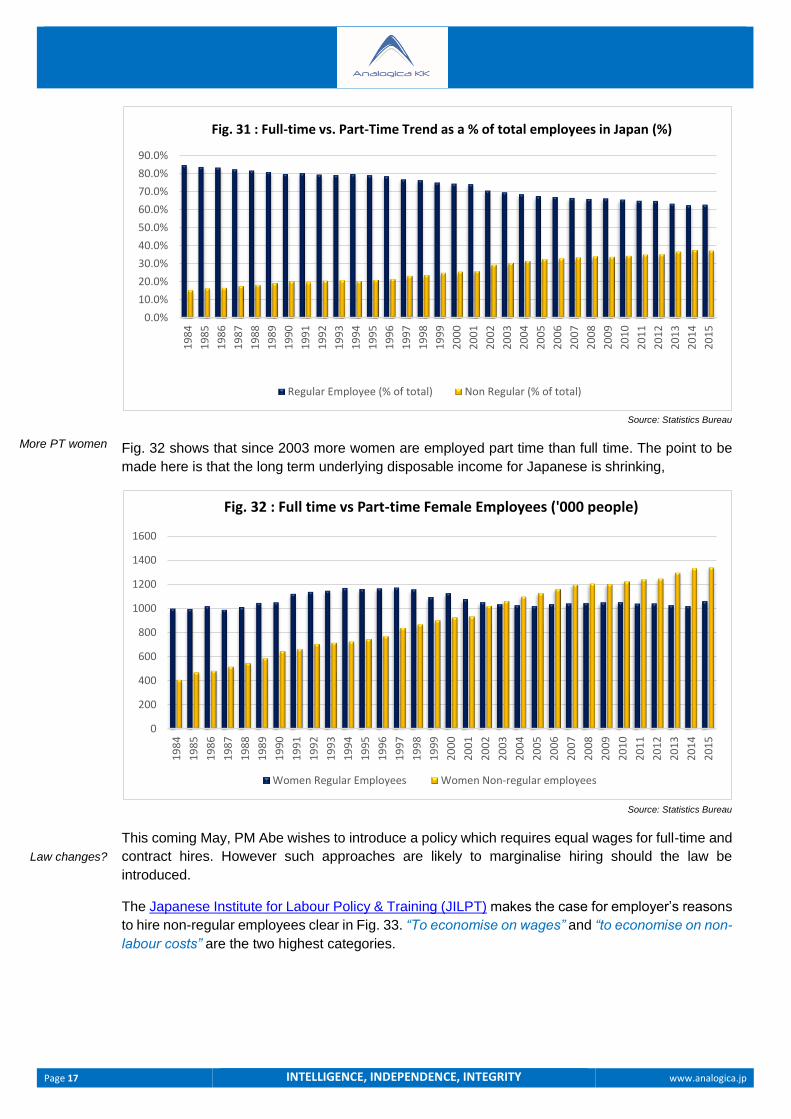

More PT women

Law changes

Source Statistics Bureau

Fig 32 shows that since 2003 more women are employed part time than full time The point to be

made here is that the long term underlying disposable income for Japanese is shrinking

Source Statistics Bureau

This coming May PM Abe wishes to introduce a policy which requires equal wages for full-time and

contract hires However such approaches are likely to marginalise hiring should the law be

introduced

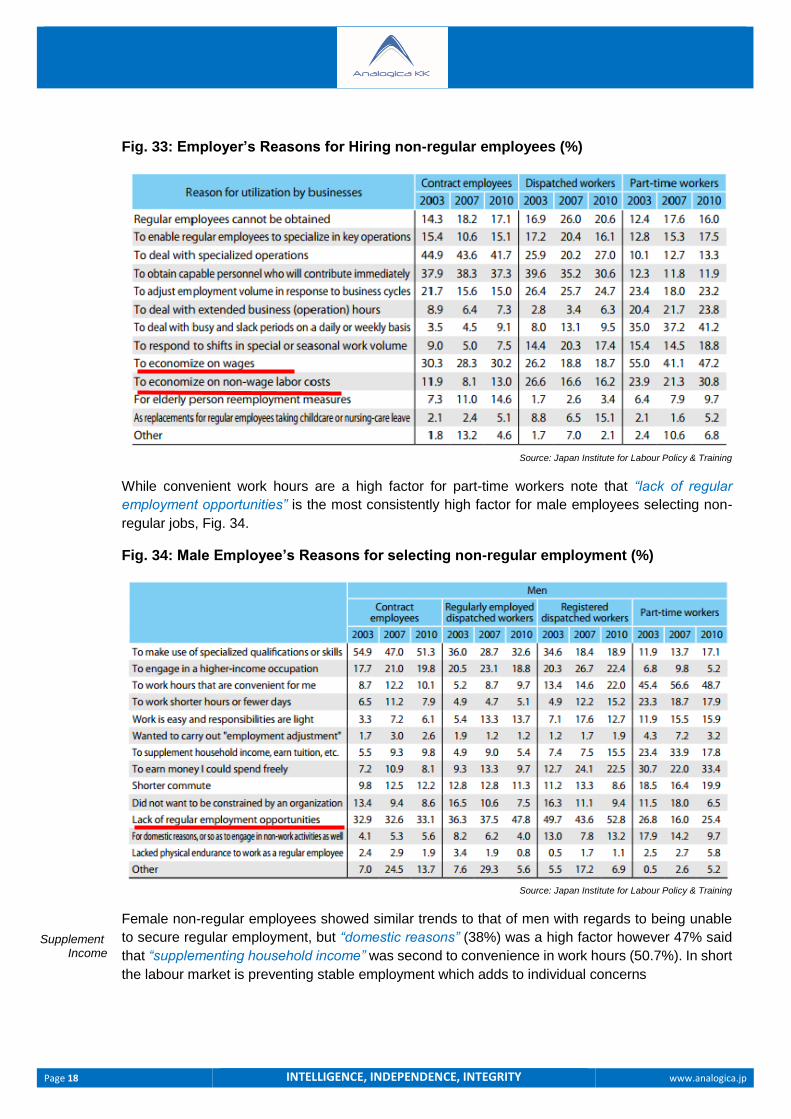

The Japanese Institute for Labour Policy amp Training (JILPT) makes the case for employerrsquos reasons

to hire non-regular employees clear in Fig 33 ldquoTo economise on wagesrdquo and ldquoto economise on non-

labour costsrdquo are the two highest categories

00

100

200

300

400

500

600

700

800

900

19

84

19

85

19

86

19

87

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

Fig 31 Full-time vs Part-Time Trend as a of total employees in Japan ()

Regular Employee ( of total) Non Regular ( of total)

0

200

400

600

800

1000

1200

1400

1600

19

84

19

85

19

86

19

87

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

Fig 32 Full time vs Part-time Female Employees (000 people)

Women Regular Employees Women Non-regular employees

Page 18 INTELLIGENCE INDEPENDENCE INTEGRITY wwwanalogicajp

Supplement Income

Fig 33 Employerrsquos Reasons for Hiring non-regular employees ()

Source Japan Institute for Labour Policy amp Training

While convenient work hours are a high factor for part-time workers note that ldquolack of regular

employment opportunitiesrdquo is the most consistently high factor for male employees selecting non-

regular jobs Fig 34

Fig 34 Male Employeersquos Reasons for selecting non-regular employment ()

Source Japan Institute for Labour Policy amp Training

Female non-regular employees showed similar trends to that of men with regards to being unable

to secure regular employment but ldquodomestic reasonsrdquo (38) was a high factor however 47 said

that ldquosupplementing household incomerdquo was second to convenience in work hours (507) In short

the labour market is preventing stable employment which adds to individual concerns

Page 19 INTELLIGENCE INDEPENDENCE INTEGRITY wwwanalogicajp

Zero growth

Economic revival Scenario

City mergers

Fig 35 is an outline of the government projections of employment growth by industry according to

the JILPT Under a zero growth scenario they expect to see most job categories decline 20-30 by

2030 (based on 2012) One of the key assumptions is that JILPT expects that under zero growth

there is unchanged labour force participation while economic revival calls for progressive labour

participation

Source Japan Institute for Labour Policy amp Training

Fig36 looks at jobs growth by industry under the governmentrsquos bullish lsquoeconomic revivalrsquo scenario

This assumes workforce participation gradually recovers None-the-less a lot of jobs will go through

retirement and restructuring Once again this poses issues for the set-up of new dealerships with

this economic backdrop

Source Japan Institute for Labour Policy amp Training

It should be noted that since the 1990s the Japanese national government has run an aggressive

campaign to merge towns and cities known as lsquoshichison gappeirsquo in an attempt to streamline public

services to account for rapidly aging and shrinking populations in the regional areas Fig 36 shows

the large scale migration towards the cities as evidenced by population growth since 1920 There

could be no rational argument for a dealership in Shimane Prefecture based on zero population

-600

-500

-400

-300

-200

-100

00

100

200

300Fig 35 Jobs growth by industry in a Zero Growth outlook

Zero growth (2020) Zero growth (2030)

-400

-300

-200

-100

00

100

200

300Fig 36 Jobs growth by industry in Economic Revival outlook

Economic Revival (2020) Economic Revival (2030)

Page 20 INTELLIGENCE INDEPENDENCE INTEGRITY wwwanalogicajp

Divorce

Birth rates

growth since in the last 90 years Any children born in these areas will quickly realise that job

prospects will be highly limited much like the eastern areas of Germany immediately post

reunification

Source Statistics Bureau

Divorce rates have been surging since 2000 Since 2007 women are now entitled to 50 of their

ex-husbandrsquos pension

Source Statistics Bureau

Japanese births rates among females in their 20s continues to fall as women choose career and feel

a lack of suitable partners In 1990 557 of men and 433 of women were not married at 50 but

this has now reached 201 and 106 respectively Fig 31 highlights those women who married

583

9

445

1

365

3

255

7

254

6

242

5

148

0

144

1

143

5

142

9

142

7

133

4

131

8

128

8

120

0

116

7

104

8

945

920

907

855

816

743

735

597

572

566

510

489

480

474

469

394

392

377

367

346

337

336

295

261

256

208

206

205

172

139

03

00

1000

2000

3000

4000

5000

6000

7000

Kan

agaw

a

Sait

ama

Ch

iba

Toky

o

Aic

hi

Osa

ka

Nar

a

Miy

agi

Oki

naw

a

Shiz

uo

ka

Hyo

go

Ho

kkai

do

Fuku

oka

Jap

an

Ibar

aki

Shig

a

Kyo

to

Gif

u

Toch

igi

Gu

mm

a

Hir

osh

ima

Ao

mo

ri

Miy

azak

i

Mie

Oka

yam

a

Iwat

e

Ish

ikaw

a

Toya

ma

Fuku

shim

a

Yam

anas

hi

Ku

mam

oto

Kag

awa

Yam

agu

chi

Oit

a

Nag

ano

Ehim

e

Fuku

i

Niig

ata

Wak

ayam

a

Tott

ori

Saga

Nag

asak

i

Aki

ta

Yam

agat

a

Kag

osh

ima

Toku

shim

a

Ko

chi

Shim

ane

Fig 37 Population Growth by prefecture (2010 vs 1920)

15-19 20-24 25-29 30-34 35-39 40-44 45-49 50-54 55-59 60-64 65-69 70-74 75+

1990 00 04 16 29 42 52 53 48 43 42 39 31 21

1995 00 05 18 34 44 56 64 60 51 43 40 37 23

2000 00 07 24 42 56 63 70 74 65 53 43 39 28

2005 01 09 26 50 70 81 82 82 81 68 53 42 32

2010 00 08 25 45 68 86 95 92 88 84 68 52 35

00

10

20

30

40

50

60

70

80

90

100

Fig 38 Divorce Rates of females by age group ( of married population)

1990 1995 2000 2005 2010

Page 21 INTELLIGENCE INDEPENDENCE INTEGRITY wwwanalogicajp

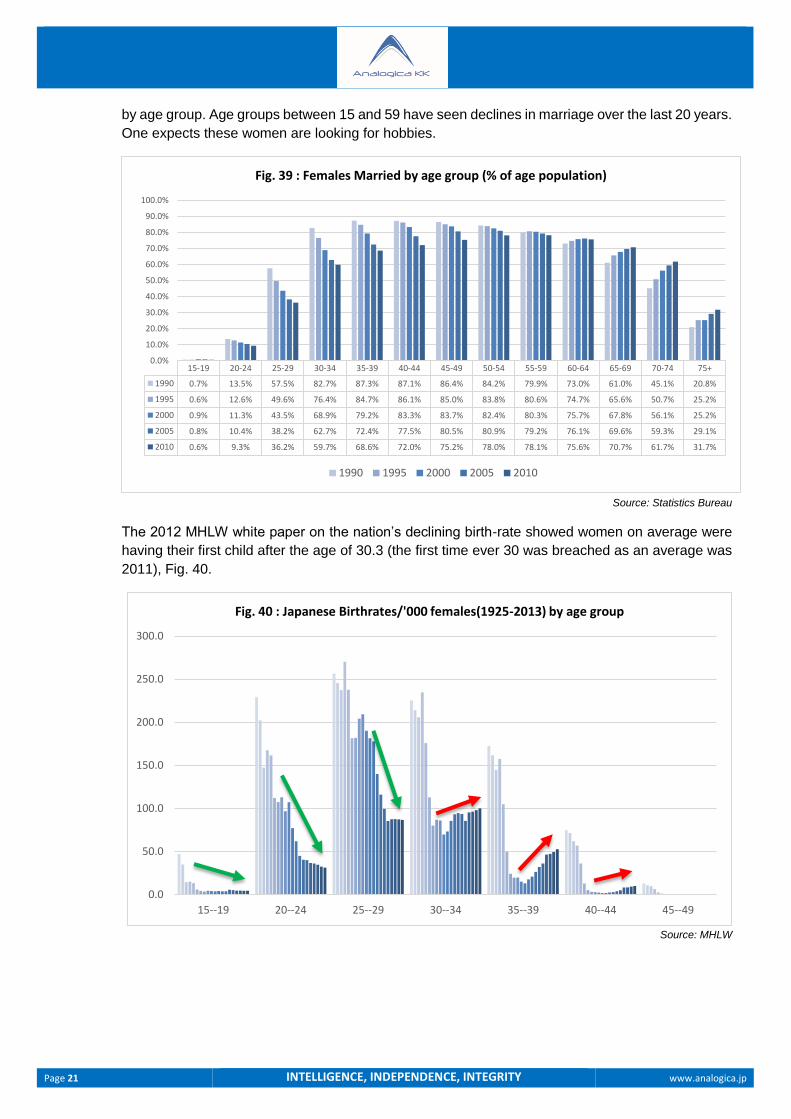

by age group Age groups between 15 and 59 have seen declines in marriage over the last 20 years

One expects these women are looking for hobbies

Source Statistics Bureau

The 2012 MHLW white paper on the nationrsquos declining birth-rate showed women on average were

having their first child after the age of 303 (the first time ever 30 was breached as an average was

2011) Fig 40

Source MHLW

15-19 20-24 25-29 30-34 35-39 40-44 45-49 50-54 55-59 60-64 65-69 70-74 75+

1990 07 135 575 827 873 871 864 842 799 730 610 451 208

1995 06 126 496 764 847 861 850 838 806 747 656 507 252

2000 09 113 435 689 792 833 837 824 803 757 678 561 252

2005 08 104 382 627 724 775 805 809 792 761 696 593 291

2010 06 93 362 597 686 720 752 780 781 756 707 617 317

00

100

200

300

400

500

600

700

800

900

1000

Fig 39 Females Married by age group ( of age population)

1990 1995 2000 2005 2010

00

500

1000

1500

2000

2500

3000

15--19 20--24 25--29 30--34 35--39 40--44 45--49

Fig 40 Japanese Birthrates000 females(1925-2013) by age group

Page 22 INTELLIGENCE INDEPENDENCE INTEGRITY wwwanalogicajp

Important Disclosures

This material was prepared for you and is for your information and use only This material should only be distributed to other members of that organization on a need to know basis and should not be distributed or disseminated to any other person or entity

This material is for information purposes only and it should not be regarded as an offer to sell or as a solicitation of an offer to buy the securities or other instruments mentioned in it This material is based on current public information that Analogica KK (Analogica) considers reliable but we make no representation that it is accurate or complete and it should not be relied on as such No investment opinion or advice is provided intended or solicited Analogica offers no warranty either expressed or implied regarding the veracity of data or interpretations of data included in this report This material is provided with the understanding that Analogica is not acting in a fiduciary capacity Opinions expressed herein reflect the opinion of Analogica and are subject to change without notice

The products mentioned in this document may not be eligible for sale in some states or countries and they may not be suitable for all types of investors The value of and the income produced by products may fluctuate so that an investor may get back less than they invested Value and income may be adversely affected by exchange rates interest rates or other factors Past performance is not necessarily indicative of future results If a product is income producing part of the capital invested may be used to pay that income copy 2015 Analogica KK All rights reserved

Tokyo 17F Roppongi Hills North Tower 6-2-31 Roppongi Minato-ku Tokyo Japan 106-0032

Office Locations

Tokyo Michael Newman President amp CEO Analogica KK

+81-80-4446-8200 mcnanalogicajp

Contact

Headquarters 942 Win Aoyama 2-2-15 Minamiaoyama Minato-ku Tokyo Japan 107-0062

Page 2 INTELLIGENCE INDEPENDENCE INTEGRITY wwwanalogicajp

1700000 gave up

motorcycle licenses in last 6 years

Who owns What

Executive Summary

The average age of motorcyclists in Japan is 53 years old and continuing to climb as younger riders

looking to obtain new licenses continues to drift Between 2010 and 2016 the Japanese National

Police Agency (JNPA) noted that large capacity motorcycle license holders (ogata ndash classified as

400cc+) have fallen by nearly 1500000 While mid-size (chugata ndash classified as below 400cc) have

risen around 715000 Female riders have shown a similar pattern of 178000 fall in ogata licenses

and 147000 increase in chugata respectively While there are still 9175mn men and 625000

women willing to get out on the highway with large capacity bikes the trend is alarming More

frighteningly new graduates arenrsquot lining up either 30000 fewer students lined up to get a mid or

large size bike license between 2014 and 2016 representing a 123 dip denoted by the red line in

Fig1

Source JNPA

Ownership

The Japanese motorcycle market is dominated by lt50cc scooters (referred to as gentsuki) Gentsuki

are popular because they can be ridden even with a standard Japanese car driverrsquos license The

gentsukirsquos low cost ($1000-1500) makes it practical to do short trips to the supermarket or

commutes especially considering the congested roads in Japan Fig2 Larger bore bikes are only

13 of the 12 million bikes on the road in Japan Motorcycles below 250cc do not require shaken

(compulsory inspection) unlike their bigger brothers

99

-2

7

-31

-4

0

-54

-5

5

-57

-6

0

-62

-6

6

-75

-7

6

-76

-8

0

-83

-8

5

-86

-8

9

-10

3-1

04

-10

7-1

10

-11

4-1

14

-11

7-1

17

-12

7-1

27

-13

2-1

33

-13

6-1

43

-14

5-1

45

-14

9-1

53

-15

8-1

60

-16

4-1

68

-17

2-1

73

-17

6-1

83

-19

3-2

01

-22

0

-350

-300

-250

-200

-150

-100

-50

00

50

100

150

Yam

agat

aFu

kui

Miy

azak

iK

agaw

aW

akay

ama

Saga

Ho

kkai

do

Shim

ane

Toky

oC

hib

aG

ifu

Niig

ata

Mie

Ku

mam

oto

Ehim

eSa

itam

aO

saka

Nar

aG

un

ma

Yam

anas

hi

Ibar

aki

Toch

igi

Yam

agu

chi

Nag

ano

Kyo

toIw

ate

Hir

osh

ima

Ko

chi

Nag

asak

iK

anag

awa

Ish

ikaw

aO

ita

Aic

hi

Fuku

oka

Ao

mo

riSh

iga

Oki

naw

aM

iyag

iH

yogo

Fuku

shim

aA

kita

Shiz

uo

kaTo

yam

aK

ago

shim

aTo

kush

ima

Oka

yam

aTo

tto

ri

Fig1 - Total New Motorcycle Graduates change (2016 vs 2014)

Page 3 INTELLIGENCE INDEPENDENCE INTEGRITY wwwanalogicajp

Gentsuki

Large bore only 13 of

total

Source JAMA

However ownership levels for gentsuki have been sliding for over a decade from around 980000

units per annum to just under 700000 Motorcycles over 50cc have shown the opposite although

at a very slow pace nudging over 500000 units before drifting back to 450000

Source JAMA

Larger bore motorcycle trends are slowly grinding higher In the 250cc+ market BMW holds an

effective 58 market share Harley Davidsonrsquos share is approximately 13 Yamaha made good

progress with the MT-0709 series which gave consumers a reasonably priced (yen700000-900000)

naked bike with ample performance The initial sales target of 1500 units annually was quickly raised

to 4000 after its release Simply put good product sells

Annual motorcycle sales in Japan hit a peak of 328 million in 1982 but decreased to 450000 by

2014 according to JAMA

6889459 58

1582925 13

1959845 16

1542856 13

Fig 2 Japan Motorcycle Ownership - Units (2012)

Scooter (lt50cc) 50cc-125cc) 125cc-250cc 250cc+

0

200000

400000

600000

800000

1000000

1200000

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Fig3 Trend of Japanese Motorcycle Purchase (2001-2012)

Gentsuki Motorcycle

Page 4 INTELLIGENCE INDEPENDENCE INTEGRITY wwwanalogicajp

Return riders

Emissions laws

Product offerings are clearly important One of the most significant trends is the popularity of

motorcycle sales to middle-aged and older people wanting larger capacity bikes than the common

250cc These people are often return riders The average age of motorcycle riders is now 53 up 93

years on 2005 Multi bike ownership is on the rise after the Global Financial Crisis in 2008

Source JAMA

Japanrsquos large bore domestic market has been hindered by restrictive emissions laws and power

limiters Some Japanese motorcycle purchasers prefer overseas specification motorcycles known

as reverse imports to dispense with the restrictions of the domestic offerings

A good example of this is the Yamaha XJR1300 The domestic version has not changed for the last

six years but there is no plan to introduce the 2017 European model in the Japanese market The

EuropeanUS version of the bike is offered under the branding of lsquoborn customisedrsquo Fig6

Fig 6 Domestic (left) and Overseas (right) versions of Yamaharsquos XJR1300

Source Company Data

So what drives the Japanese motorcycle buyer What are the main concerns and what are the

trends we should pay attention to

lt50cc 51-125cc 126-250cc 250cc+

2012 246095 90291 45306 60715

2013 238786 100947 55441 65289

2014 228918 96249 54303 70151

2015 236000 97000 56000 68000

0

50000

100000

150000

200000

250000

300000

Fig 4 Japan - New Motorcycle Sales by Engine Size

2012 2013 2014 2015

1 Bike 2 Bikes 3 Bikes 4+ Bikes Average

2005 68 19 5 4 14

2007 64 21 6 5 15

2009 50 13 4 2 14

2011 69 21 5 5 15

2013 58 26 8 8 16

01020304050607080

Fig 5 Motorcycle Ownership by individual household (units)

2005 2007 2009 2011 2013

Page 5 INTELLIGENCE INDEPENDENCE INTEGRITY wwwanalogicajp

JAMA study

Age

Replacement

Parking

Desire

Women

No real change in 2013

survey

Average ownership up

Foreign brands more

popular in large bore market

The Japan Automotive Manufacturers Association (JAMA) conducted a survey of 5150 people on

trends in motorcycling in Japan in 2011 Their findings were

A) Ownership declined among users in their 30s or younger but increased among users in

their 50s or older underscoring the continued rise in the average age of motorcycle users

B) Replacement demand accounted for 59 of all new-model purchases up from 57 in the

2009 survey First-time purchases accounted for 15 of the total not significantly different from

the previous surveyrsquos figure but underscoring a sustained decline in first-time motorcycle

purchases

C) Over 76 of owners in Tokyo (ie its main 23 wards) reported experiencing difficulties in

finding a parking space for their motorcycles

D) Respondents expressing the desire to continue riding motorcycles in the future totaled

87 down from the 92 peak recorded in 2009

E) A large percentage of women respondents viewed motorcycles as a ldquoMeans of transportrdquo and

ldquoLifestyle commodityrdquo while a significant percentage of male respondents considered them

a ldquoHobby itemrdquo

In 2013 the results from JAMArsquos survey was largely unchanged

F) Ownership has continued to decline steadily among young men in their teens 20s and

30s Ownership by women has levelled off since fiscal 2009 although among women

respondents in their 50s or older the ownership rate surpassed 60 Meanwhile ownership of

scooters and business-use lightweight motorcycles under 50cc in engine capacity among users

in their 50s or older has grown more pronounced

G) The average period of motorcycle ownership prior to its replacement with a new purchase

was 66 years up from the previous surveyrsquos 61 years This confirms the trend towards longer

ownership which was particularly marked for scooters 50cc and under in engine capacity Large

capacity motorcycles have an average turnover of 41 years up from 39 years 250cc-400cc

motorcycle ownership periods remained flat at 34 years

H) Respondents expressing the desire to continue riding motorcycles in the future totaled

88 up slightly from the 87 indicated in the previous survey but still down from the peak of

92

While overall motorcycle license holders continue to increase in aggregate what is the rate of new

license holders Is it rising falling

Financing trends have remained pretty consistent at 12 of overall sales according to JAMA with

many preferring to pay cash

There is an inverse correlation between domestic brands and engine size Fig7 Foreign brand

popularity is driven in part due to the higher average engine capacity

Page 6 INTELLIGENCE INDEPENDENCE INTEGRITY wwwanalogicajp

Licenses

Below 400cc market rising

Source JAMA

Licensing

The number of new motorcycle licenses issued in Japan has been falling consistently In 2004 almost

320000 new licenses were issued In 2016 that number had fallen 40 Total motorcycle licenses

held in 2014 number 202mn with 104mn of those Ogata (400cc+ engine size) class

Source JNPA

Fig 9 shows the status of riders who possess a motorcycle licence separated by engine class

and gender There are two classes - Chugata (middle class) licenses are below 400cc and

Ogata licenses are available for those who wish to purchase bikes above 400cc We can clearly

see that Ogata numbers for both genders is declining but Chugata licenses are rising The

decline in licenses has to do with licenses not being renewed

lt50cc 51-125cc 126-250cc 251-400cc 401-750cc 751cc+

Domestic Maker 93 87 81 74 63 47

Reverse Import 3 5 8 8 15 16

Foreign Maker 3 8 10 17 21 37

0

10

20

30

40

50

60

70

80

90

100

Fig 7 Origin of manufacturer preference by Engine Size ()

319

369

304

842

274

842

267

724

236

355

226

844

215

041

199

945

188

362

190

331

179

585

198

456

185

422

0

50000

100000

150000

200000

250000

300000

350000

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Fig8 Newly issued Motorcycle Licenses

Page 7 INTELLIGENCE INDEPENDENCE INTEGRITY wwwanalogicajp

Driving schools

expensive

Source JNPA

Let us consider the cost to get a Japanese motorcycle license One cannot get an Ogata license

without getting Chugata first Fig 10 highlights the high cost of getting a license The dots represent

standard (blue) double time (red) and fast (green) So to get a full bore Ogata license from no license

at all could set one back over $3000 One could try to avoid the cost and try at the official test

centres but the tests are designed to test memory rather than skill to force schooling The schools

are authorised to give passing grades for licenses at the end of tuition and well over 95 of students

that go to these schools pass

Fig 10 Hinomaru Driving School costs to get a motorcycle license - $3000+ investment

Source Hinomaru Driving School

Ogata (400cc+)- Men Chugata (lt400cc)- Men Ogata (400cc+)- Women Chugata (lt400cc) - Women

2010 10670417 7842426 802520 1172508

2011 10427177 7956291 770726 1198582

2012 10193671 8086072 745259 1224714

2013 9997273 8220635 726418 1252057

2014 9732861 8343178 697214 1276514

2015 9454801 8453963 657783 1298578

2016 9175340 8557534 624476 1320082

0

2000000

4000000

6000000

8000000

10000000

12000000

Fig 9 Motorcycle Licence Holders in Japan by Type

2010 2011 2012 2013 2014 2015 2016

Motorcycle

Chugata

Ogata

Category License Class License Status

No

License

Car

License

Chugata

Plan Time Tuition Enrollment Fee

Page 8 INTELLIGENCE INDEPENDENCE INTEGRITY wwwanalogicajp

Young go small

Fig 11 denotes the number of chugataogata graduates from motorcycle license schools in 2016 The

yellow bars denote a GDPcapita ratio at 5 below the national average or above

Source JNPA

Fig12 shows at what age groups people move to take up their motorcycle licenses Chugata

licenses are the main target of the 20s-40s with Ogata picking up after 50s as the common

motorcycle license type It would be fair to assume that affordability is a likely factor in choosing a

license both schooling and motorcycle cost

Source JAMA Note some double counting due to multiple licenses taken out (eg Ogata amp car)

0

5000

10000

15000

20000

25000

Kan

agaw

a

Toky

o

Osa

ka

Kyo

to

Sait

ama

Aic

hi

Hyo

go

Ch

iba

Fuku

oka

Shiz

uo

ka

Hir

osh

ima

Toch

igi

Ho

kkai

do

Oki

naw

a

Ibar

aki

Miy

agi

Ku

mam

oto

Niig

ata

Oka

yam

a

Gif

u

Fuku

shim

a

Gu

nm

a

Mie

Kag

osh

ima

Shig

a

Ehim

e

Nag

ano

Yam

agat

a

Wak

ayam

a

Miy

azak

i

Nag

asak

i

Nar

a

Kag

awa

Oit

a

Saga

Yam

agu

chi

Yam

anas

hi

Ish

ikaw

a

Ao

mo

ri

Iwat

e

Shim

ane

Ko

chi

Toya

ma

Toku

shim

a

Fuku

i

Aki

ta

Tott

ori

Fig 11 - ChugataOgata Licence Graduates by prefecture (2016)

10s 20s 30s 40s 50s 60s 70+

Gentsuki Only 26 10 2 2 2 3 22

Car License incl Gentsuki 47 22 13 16 21 31 14

Bike license lt250cc 4 2 3 5 7 8 12

Chugata 22 57 61 61 37 11 7

Ogata 2 17 30 29 32 46 41

0

10

20

30

40

50

60

70

Fig 12 Age when Motorcyclists take up a license ()

Gentsuki Only Car License incl Gentsuki Bike license lt250cc Chugata Ogata

Page 9 INTELLIGENCE INDEPENDENCE INTEGRITY wwwanalogicajp

Female age rising

Sourcing information

Source JAMA

The average age of female and male riders has risen from 43-44yo range in 2005 to 53yo range in

2015 Thinking of it another way these 43-44yo group just grew 8 years old along with the survey

by JAMA Figs 15-16

Source JAMA

JAMArsquos 2013 motorcycle survey revealed that dealerships are a key source of information on

motorcycles followed by websites Fig 17

10s 20s 30s 40s 50+

2005 10 32 29 18 11

2007 3 27 29 22 19

2009 4 22 23 30 20

2011 3 23 21 29 24

2013 4 16 19 29 19

05

1015

20

2530

35

Fig 13 251cc-400cc Bike Ownership by Age ()

2005 2007 2009 2011 2013

10s 20s 30s 40s 50+

2005 1 22 23 35 18

2007 1 13 32 38 17

2009 0 12 30 33 23

2011 0 12 19 36 32

2013 0 6 15 33 42

05

1015202530354045

Fig 14 400cc+ Bike Ownership by Age ()

2005 2007 2009 2011 2013

10s 20s 30s 40s 50sAverage

Age

2005 7 14 21 23 34 429

2007 5 10 19 22 43 460

2009 4 8 18 25 45 470

2011 3 7 15 25 49 484

2013 3 5 10 24 58 510

0

10

20

30

40

50

60

70

Fig 15 Average Age of Motorcycle Riders Male ()

2005 2007 2009 2011 2013

10s 20s 30s 40s 50sAverage

Age

2005 11 19 16 13 42 442

2007 7 20 12 15 46 452

2009 6 8 11 16 59 489

2011 6 8 11 17 58 510

2013 8 6 9 17 61 520

0

10

20

30

40

50

60

70

Fig 16 Average Age of Motorcycle Riders - Female ()

2005 2007 2009 2011 2013

Page 10 INTELLIGENCE INDEPENDENCE INTEGRITY wwwanalogicajp

Large bore attracts

hobbyists

Source JAMA

However JAMA also highlights (Fig18) that as engine size grows motorcycle magazines become a

very important source of new information Although there are dedicated BMW magazines (including

a dedicated version lsquoBMW Boxer Journalrsquo in Japan other broader magazines lsquoBike Brosrsquo lsquoBikejinrsquo

and the like are equally important to attract new customers Larger bore motorcycle riders clearly

view motorcycles as a hobby

Source JAMA

DealerMaker

WebsiteMotorcycleMagazine

CataloguePamphlet

Otherwebsite

Heard fromFriendExp

ert

Saw parkedon Street

Saw RidingPast

Pamphlet Newspaper Direct MailMotorsho

wTV Ad

MagazineAd

2005 40 7 13 11 2 6 6 4 2 1 0 0 2 1

2007 38 9 12 11 2 6 5 5 2 1 0 0 1 1

2009 41 12 11 9 3 5 3 3 1 0 0 0 1 0

2011 40 14 10 9 6 6 5 4 1 0 0 0 0 0

2013 43 14 9 7 6 6 4 3 1 1 0 0 0 0

0

5

10

15

20

25

30

35

40

45

50

Fig 17 How motorcycle riders source information on bikes () by year

2005 2007 2009 2011 2013

DealerMaker

WebsiteMotorcycleMagazine

CataloguePamphlet

Otherwebsite

Heard fromFriendExp

ert

Sawparked on

Street

Saw RidingPast

Pamphlet Newspaper Direct MailMotorsho

wTV Ad

MagazineAd

lt50cc 54 11 2 8 3 5 3 3 2 1 0 0 0 0

51-125cc 30 19 12 7 7 8 6 5 1 1 0 0 0 0

126-250cc 18 19 29 4 14 5 3 3 0 0 0 1 0 0

251-400cc 14 24 26 5 10 5 4 6 0 0 0 1 0 0

401-750cc 13 18 41 2 12 4 1 0 0 0 0 4 0 0

751cc+ 16 16 37 1 8 6 2 2 0 0 0 5 1 0

0

10

20

30

40

50

60

Fig 18 How motorcyclists gain information on bikes () by engine size

lt50cc 51-125cc 126-250cc 251-400cc 401-750cc 751cc+

Page 11 INTELLIGENCE INDEPENDENCE INTEGRITY wwwanalogicajp

Trend of the Japanese

Source JAMA

The plight of the Japanese makers globally

Looking over the last 5 years Japanese motorcycle manufacturers have been struggling Honda

remains at the top of the production tree at 177 million units but Yamaha has trended down while

Suzuki continues to suffer the steepest drop of all makers declining 8-19 per annum Kawasaki

Heavy has maintained a more focused strategy with larger bore motorcycles

Source Custom Products Research Company data

When analysing the contribution that motorcycle segments make to the Japanese makersrsquo group

revenue and EBIT we see the following

0

10

20

30

40

50

60

70

Want adifferent

type

Want to ridedifferentengine

capacity

Want toseparate use

Conveniencevs Hobby

Want to addto hobby

StyleDesign Current bikereliability

gettingworse

New modelrelease

Current bikeservicinggetting

expensive

Economicsituationimproved

Cheap price Touring withFamily

Members

Dealerpushed hard

Fig 19 Why owners choose a second bike ()

2011 2013

15494000

6090000

2574000

544000

17661000

5154000

1367000 540000

-

2000000

4000000

6000000

8000000

10000000

12000000

14000000

16000000

18000000

20000000

Honda Yamaha Suzuki Kawasaki

Fig20 Japanese makers Global Motorcycle Production (units)

FY2012 FY2013 FY2014 FY2015 FY2016

Page 12 INTELLIGENCE INDEPENDENCE INTEGRITY wwwanalogicajp

EBIT marhins

Source Custom Products Research Company data

Unsurprisingly Yamaha is the purest motorcycle play (Fig21) in Japan However its contribution

from motorcycles has been declining as a percentage of total revenue There are two factors at play

One is the growth in sales of boat engines (where it commands 40 a global share) and second is

a focus on more profitability per unit Fig22 EBIT margins for the global motorcycle majors can be

seen here Honda has seen its motorcycle segment grow as a percent of group EBIT due to weaker

performances in cars Suzuki is the worst performer

Source Custom Products Research Company Data

00

200

400

600

800

Honda Yamaha Suzuki Kawasaki

Fig21 Japanese motorcycle makers revenue as of group

FY2012 FY2013 FY2014 FY2015 FY2016

-200-100

00100200

300400

Honda Yamaha Suzuki Kawasaki

Fig 22 Japanese motorcycle makers EBIT as of group

FY2012 FY2013 FY2014 FY2015 FY2016

101

39

-05

38

90 90

147

-100-500050

100150200

Fig23 Major Motorcycle Makers segmented (not group) EBIT Margins ()

FY2012 FY2013 FY2014 FY2015 FY2016

3972 84

30

100 90

175

00

50

100

150

200

250

Fig 24 Group EBIT Margins ()

FY2012 FY2013 FY2014 FY2015 FY2016

Page 13 INTELLIGENCE INDEPENDENCE INTEGRITY wwwanalogicajp

Foreign brands focused

Source Custom Products Research Company data

Analysing the foreign brands shows clear product focus has paid off The four major European large

bore makers have experienced double digit production growth

-

5000000

10000000

15000000

20000000

25000000

Fig25 Major Motorcycle Makers Segmental Revenue (US$euro000s)

FY2012 FY2013 FY2014 FY2015 FY2016

+34

-14

-32 -5 +39 +87

+7

-500000

-

500000

1000000

1500000

2000000

2500000

Fig26 Major Motorcycle Maker Segmental EBIT ($000s)

FY2013 FY2014 FY2015 FY2016

+65

+87+137-32NA+287

-12

Page 14 INTELLIGENCE INDEPENDENCE INTEGRITY wwwanalogicajp

Efficiency

Severe pressure

Source Custom Products Research Company data

One thing Figs 20 amp 27 point out is that focused strategies appear to be paying off for the Europeans

and to some extent Kawasaki which has moved away from a me-too approach Efficiency and brand

seems to be paying off for BMWrsquos continued rise and a broad range of product unlike Harley which

seems to be stuck in a divine franchise scenario Profitable but struggling to break out of cruisers It

has had a stab at sports bikes through Buell (business was spun off and EBR has since closed) and

the Porsche designed V-Rod (now out of production) Now that Ducati is potentially being sold by

Audi does Harley look to use a proper sports brand with no clash in its line up to fuel (no pun

intended) its growth

Summary The Japanese motorcycle market is under severe pressure It is little wonder that the domestic

makers arenrsquot exerting too much effort into the market given the long-term decline in the market Half

of the decline is driven by apathy and poor product placement The lsquobuild it and they will comersquo dealer

model is a sure fire way to ensure the market dies The foreign luxury brands appear to be gaining

share They continue to target the heart not the head like the Japanese makers Yamaha Motor has

been the most proactive of the domestic makers in providing a product that attracts new riders Such

has the success been of the Yamaha Bolt that Harley-Davidson has had to respond with a

yen1000000 entry level model Sadly with 1800000 male and female motorcycle license holders

giving up the right to ride over the last 6 years there is not much time left to save the remaining 10

million that remain

The differences between the focused foreign brands and the everything for everyone Japanese is

clear While Honda can grunt with its huge economies of scale sadly Suzuki needs to resurrect its

former glories of the 1980s rather than produce more me-too Kawasaki would seem to have worked

that out

On top of that the employment situation in Japan doesnrsquot lend itself to allow for investment in such

hobbies as motorcycles We outline that plight in the appendix

-

50000

100000

150000

200000

250000

300000

BMW Motorrad KTM AG Harley-Davidson Ducati Triumph

Fig 27 Non-Japanese Motorcycle Maker Production (units)

FY2012 FY2013 FY2014 FY2015 FY2016

+28

+15+26

+6

+70

Page 15 INTELLIGENCE INDEPENDENCE INTEGRITY wwwanalogicajp

Income

Assets

Unemployment

Appendix - Income amp Demographics

Assessing the demographics of financial assets by age group there is no question that the 40s-50s

segments have more assets than the 20-30s cohort This means that a makers are unlikely to make

huge inroads with the set (backed up by the JAMA survey) in a declining market targeting an age

group that has proved less interested in riding than the peak of 2009

Fig 28 bears out the trend Remember that the 50s set are far more likely to buy gentsuki according

to JAMA For the target BMW KTM Harley or Triumph motorcycle buyer 30s to 50s should be the

addressable market comprising around 40 of assets by age

Source Japan Central Council for Financial Service Information

Here is where it gets tricky After the Global Financial Crisis of 2008 unemployment rates in Japan

have drifted downwards Fig 29 However this masks the new reality of the composition of

employment The quality of employment is deteriorating

Source Statistics Bureau

The days have passed when most department stores had their elevator girls and train stations had

their confetti bag laden ticket clippers waiting at the exits But Japan if anything is moving further

20-29 05 30-39 56

40-49 128

50-59 21860-69 366

70+ 227

Fig 28 Total Financial Assets by Age Group

20-29 30-39 40-49 50-59 60-69 70+

00

20

40

60

80

100

15~24 25~34 35~44 45~54 55~64 65+

Fig 29 Unemployment Rate by Age Group (2007-2015)

2007 2008 2009 2010 2011 2012 2013 2014 2015

Page 16 INTELLIGENCE INDEPENDENCE INTEGRITY wwwanalogicajp

Changes in labour laws

FT vs PT

towards a service economy Unfortunately the labour productivity gains over the last 20yrs have

come almost exclusively from the manufacturing sector with retail transport restaurants hotels and

business services falling well below their global peers for productivity At least the service is still

great

Significant revisions to the labour personnel dispatch laws in rsquo95 and rsquo99 made it much easier to

employ irregular and subcontract workers and hence began a dumbing-down of the workforce since

less time was spent on education and training in general (putting Japanese workers in more direct

competition with their Asian neighbours) Average monthly wages (including overtime bonus and

social welfare deductions) have generally been flat over the last 5 years though increased 03 in

2015 due to overtime and bonuses but management is reticent to add to fixed costs with wage

increases as it would rather maintain flexibility through higher bonuses Legally mandated social

welfare costs mainly paid by employers have risen at a compound rate of 139 pa over the last

20 years while nominal wages have only increased 027 pa such that social welfare costs have

risen from 104 to 148 of wages during this time

Fig 30 Wages by type of employment by age (yenhour)

Source Ministry of Health Labor amp Welfare (MHLW)

The long running trend of full-time work in a regular capacity has given way to a lot more part-time

(lower paying) jobs which involves less lsquoother costsrsquo like insurance retirement and so on This

change puts pressure on the household budget The instance of lower paid part-time work has grown

since then from 30 to 374 of the total For women this is now 56

Page 17 INTELLIGENCE INDEPENDENCE INTEGRITY wwwanalogicajp

More PT women

Law changes

Source Statistics Bureau

Fig 32 shows that since 2003 more women are employed part time than full time The point to be

made here is that the long term underlying disposable income for Japanese is shrinking

Source Statistics Bureau

This coming May PM Abe wishes to introduce a policy which requires equal wages for full-time and

contract hires However such approaches are likely to marginalise hiring should the law be

introduced

The Japanese Institute for Labour Policy amp Training (JILPT) makes the case for employerrsquos reasons

to hire non-regular employees clear in Fig 33 ldquoTo economise on wagesrdquo and ldquoto economise on non-

labour costsrdquo are the two highest categories

00

100

200

300

400

500

600

700

800

900

19

84

19

85

19

86

19

87

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

Fig 31 Full-time vs Part-Time Trend as a of total employees in Japan ()

Regular Employee ( of total) Non Regular ( of total)

0

200

400

600

800

1000

1200

1400

1600

19

84

19

85

19

86

19

87

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

Fig 32 Full time vs Part-time Female Employees (000 people)

Women Regular Employees Women Non-regular employees

Page 18 INTELLIGENCE INDEPENDENCE INTEGRITY wwwanalogicajp

Supplement Income

Fig 33 Employerrsquos Reasons for Hiring non-regular employees ()

Source Japan Institute for Labour Policy amp Training

While convenient work hours are a high factor for part-time workers note that ldquolack of regular

employment opportunitiesrdquo is the most consistently high factor for male employees selecting non-

regular jobs Fig 34

Fig 34 Male Employeersquos Reasons for selecting non-regular employment ()

Source Japan Institute for Labour Policy amp Training

Female non-regular employees showed similar trends to that of men with regards to being unable

to secure regular employment but ldquodomestic reasonsrdquo (38) was a high factor however 47 said

that ldquosupplementing household incomerdquo was second to convenience in work hours (507) In short

the labour market is preventing stable employment which adds to individual concerns

Page 19 INTELLIGENCE INDEPENDENCE INTEGRITY wwwanalogicajp

Zero growth

Economic revival Scenario

City mergers

Fig 35 is an outline of the government projections of employment growth by industry according to

the JILPT Under a zero growth scenario they expect to see most job categories decline 20-30 by

2030 (based on 2012) One of the key assumptions is that JILPT expects that under zero growth

there is unchanged labour force participation while economic revival calls for progressive labour

participation

Source Japan Institute for Labour Policy amp Training

Fig36 looks at jobs growth by industry under the governmentrsquos bullish lsquoeconomic revivalrsquo scenario

This assumes workforce participation gradually recovers None-the-less a lot of jobs will go through

retirement and restructuring Once again this poses issues for the set-up of new dealerships with

this economic backdrop

Source Japan Institute for Labour Policy amp Training

It should be noted that since the 1990s the Japanese national government has run an aggressive

campaign to merge towns and cities known as lsquoshichison gappeirsquo in an attempt to streamline public

services to account for rapidly aging and shrinking populations in the regional areas Fig 36 shows

the large scale migration towards the cities as evidenced by population growth since 1920 There

could be no rational argument for a dealership in Shimane Prefecture based on zero population

-600

-500

-400

-300

-200

-100

00

100

200

300Fig 35 Jobs growth by industry in a Zero Growth outlook

Zero growth (2020) Zero growth (2030)

-400

-300

-200

-100

00

100

200

300Fig 36 Jobs growth by industry in Economic Revival outlook

Economic Revival (2020) Economic Revival (2030)

Page 20 INTELLIGENCE INDEPENDENCE INTEGRITY wwwanalogicajp

Divorce

Birth rates

growth since in the last 90 years Any children born in these areas will quickly realise that job

prospects will be highly limited much like the eastern areas of Germany immediately post

reunification

Source Statistics Bureau

Divorce rates have been surging since 2000 Since 2007 women are now entitled to 50 of their

ex-husbandrsquos pension

Source Statistics Bureau

Japanese births rates among females in their 20s continues to fall as women choose career and feel

a lack of suitable partners In 1990 557 of men and 433 of women were not married at 50 but