Really Managing Corporate Credit Risk You Can’t Afford to Wait

49

Really Managing Corporate Credit Risk – You Can’t Afford to Wait Phil Burch, CTP Vice President and CFO Nichols Brothers, Inc. 918.398.2715 [email protected] George Garner President CreditPoint Software 918.639.4205 [email protected]

Transcript of Really Managing Corporate Credit Risk You Can’t Afford to Wait

Really Managing Corporate Credit Risk – You Can’t Afford to Wait

Phil Burch, CTP

Vice President and CFO

Nichols Brothers, Inc.

918.398.2715

George Garner

President

CreditPoint Software

918.639.4205

Industry Statistics on Write-offs

• How Big is the Problem?

• # of Fortune 1000 Companies with

DSO>90 Days

• Bad Debt Expense

• Largest Uninsured loss is from Trade

Receivables

Lower Perceived Financial

Rating

Deteriorates Key

Financial Ratios

Management Time

Income

Interest Expense

Borrowing

Financial Effect of Credit Losses

Uses Cash

Increase in

Working Capital

Negative impact on Stock and Shareholder Value

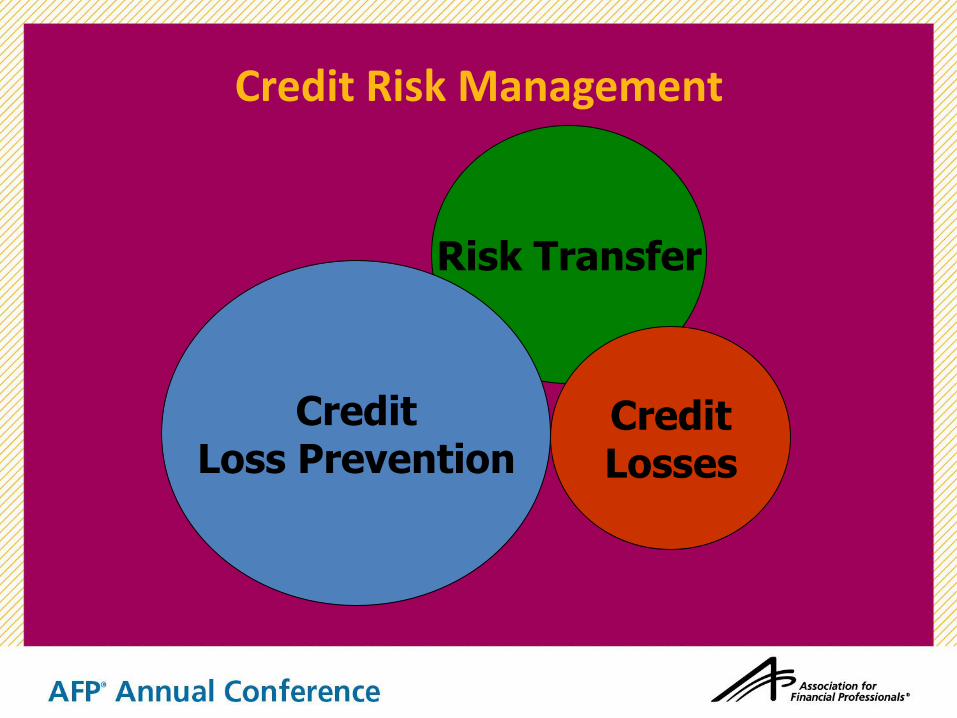

Risk Management Concepts

Risk Transfer

Loss Management

Loss Prevention

Unmanaged Credit Risk

Risk Transfer

Credit Losses Credit Loss

Prevention

Credit Risk Management

Risk Transfer

Credit Losses

Credit Loss Prevention

Credit Policy

Credit Loss Prevention

Credit Scoring

Invoice Process

Measuring

Reporting

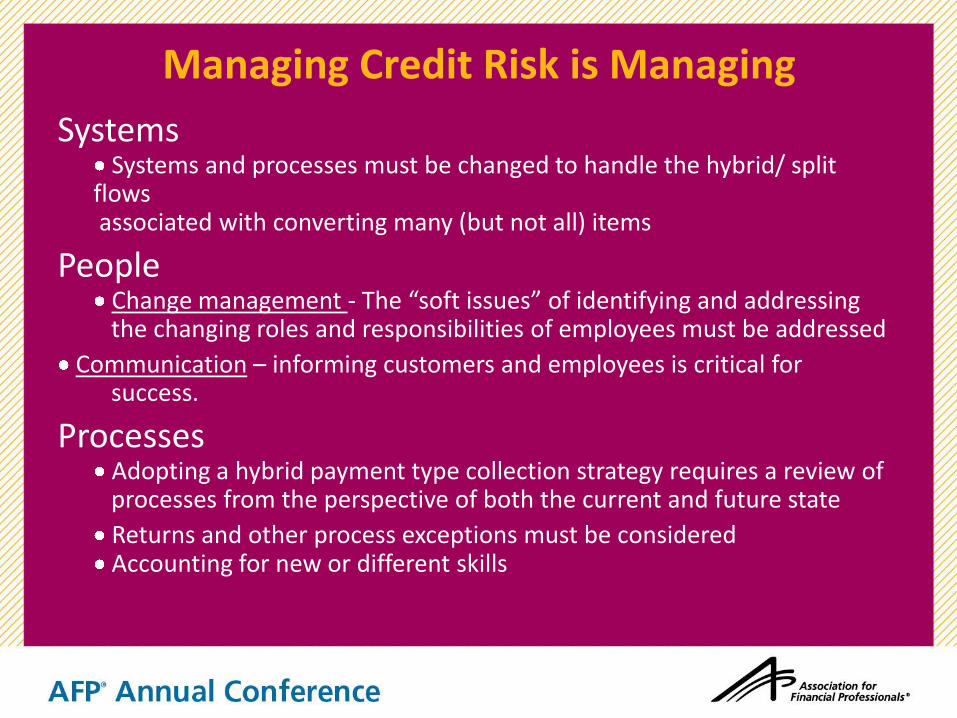

Managing Credit Risk is Managing

Systems Systems and processes must be changed to handle the hybrid/ split

flows associated with converting many (but not all) items

People Change management - The “soft issues” of identifying and addressing

the changing roles and responsibilities of employees must be addressed

Communication – informing customers and employees is critical for success.

Processes Adopting a hybrid payment type collection strategy requires a review of

processes from the perspective of both the current and future state

Returns and other process exceptions must be considered Accounting for new or different skills

HIGH OIL OR GAS PRICES HIGH CUSTOMER CASH FLOW AGGRESSIVE SPENDING $1,000,000 CREDIT LOSS = $3,000,000 REPLACEMENT REVENUE

$20 MM

$3 MM

$30

$20

$10

MARGIN 5 % 33 %

TIGHT POLICY FLEXIBLE POLICY

LOW OIL OR GAS PRICES LOW CUSTOMER CASH FLOW UNCERTANITY $1,000,000 CREDIT LOSS = $20,000,000 REPLACEMENT REVENUE

Term and Conditions

Credit Risk Transfer

Collateral

Credit Insurance

Collection Policy

Credit Loss Management

Collection Process

Measuring

Reporting

Proactive and Systematic

Mitigated Risk

Data Aggregation, Accessibility

Workflow Automation, Productivity

Standardized, Streamlined

Process

CASE STUDY #1

The Reason We’re Here…

To Standardize the Collections Process

Reduce working capital allocation charge Improve cash flow Improve DSO

Current Challenge Business Impact

Inconsistency in collectors’ follow ups: tracking short/slow pays, promises, & disputes

Year-over-year, DSO is slow to improve

Account resolution moves slowly (some accounts are over one year old)

Lack of accountability and visibility into collectors’ activities

Repeat offender accounts disproportionately affecting bad debt reserves

Inconsistency in approach between collectors, managers & regions

No formalized process to maximize efforts in collecting dollars (especially during quarter-end and year-end)

Specific Challenges

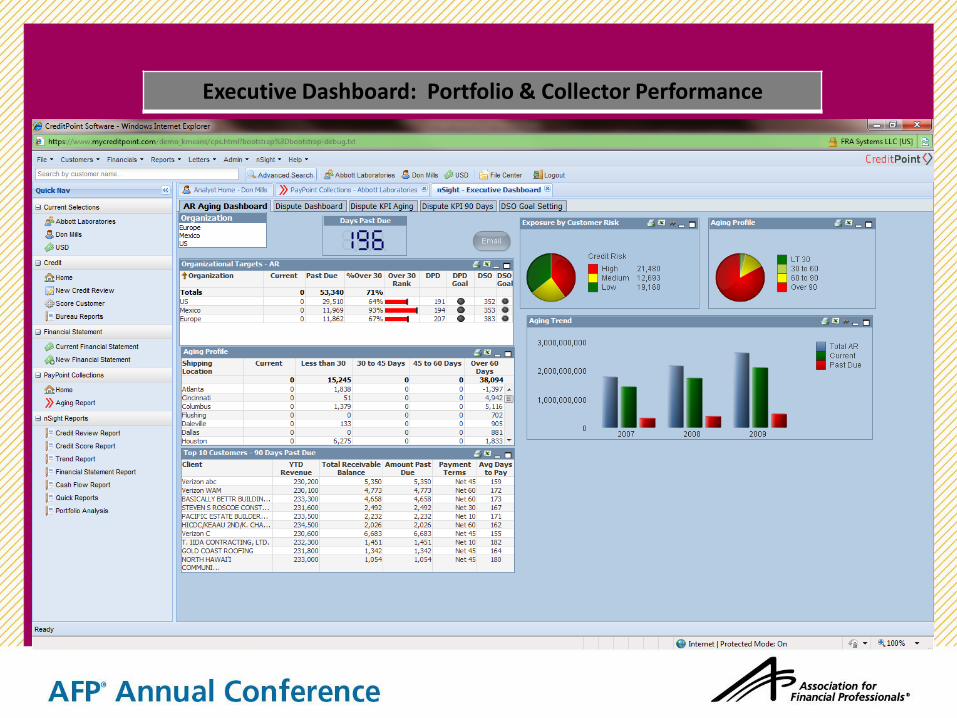

Executive Dashboard: Portfolio & Collector Performance

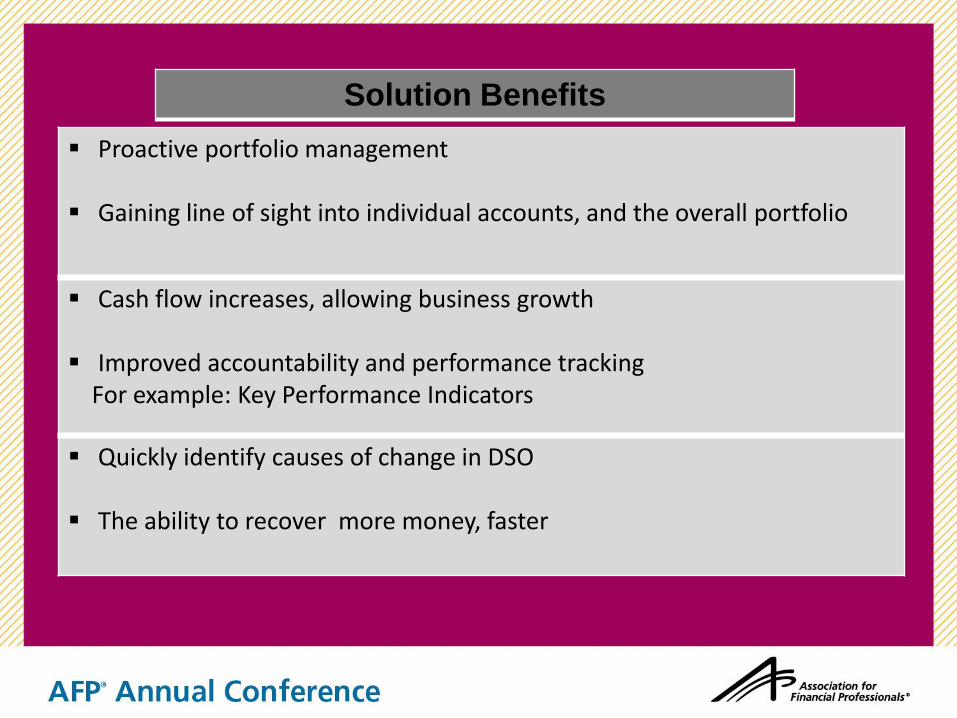

Proactive portfolio management

Gaining line of sight into individual accounts, and the overall portfolio

Cash flow increases, allowing business growth

Improved accountability and performance tracking For example: Key Performance Indicators

Quickly identify causes of change in DSO

The ability to recover more money, faster

Solution Benefits

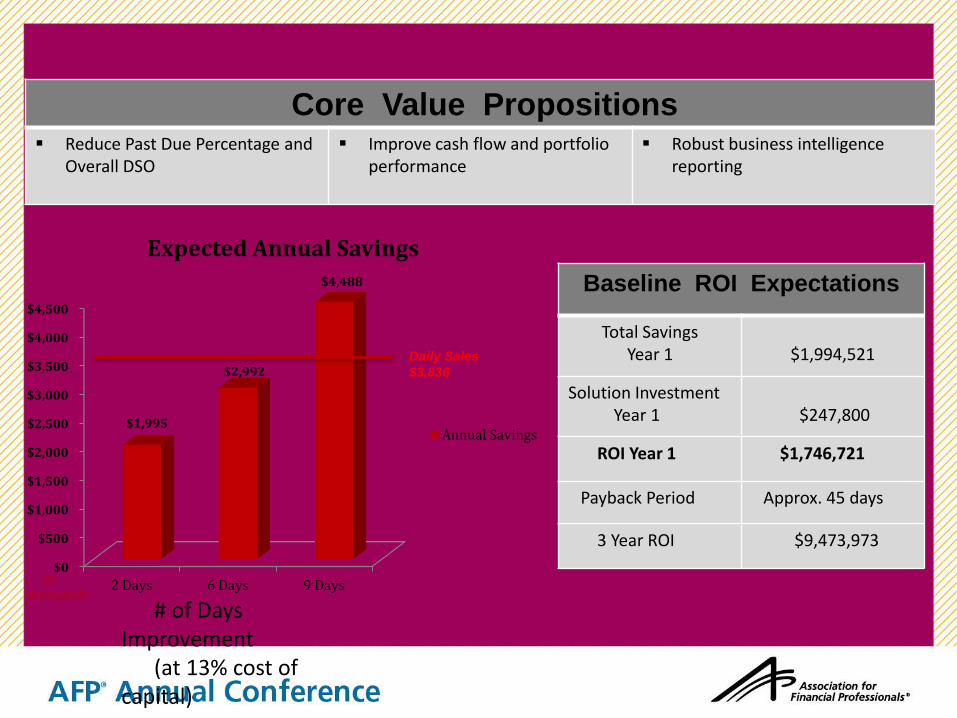

Core Value Propositions Reduce Past Due Percentage and

Overall DSO Improve cash flow and portfolio

performance

Robust business intelligence reporting

Baseline ROI Expectations

Total Savings Year 1

$1,994,521

Solution Investment Year 1

$247,800

ROI Year 1 $1,746,721

Payback Period Approx. 45 days

3 Year ROI $9,473,973

$0

$500

$1,000

$1,500

$2,000

$2,500

$3,000

$3,500

$4,000

$4,500

2 Days 6 Days 9 Days

$1,995

$2,992

$4,488

Expected Annual Savings

Annual Savings

in thousands

Daily Sales

$3,836

# of Days Improvement (at 13% cost of capital)

CASE STUDY #2

A Global Success Story Transforming Credit Risk

Management

The Situation:

•Sales growth from $17B to $31B in 2 years

•Global Manufacturing on 4 Continents

•Decentralized Credit Function

•12 Divisions & 100 ERP Systems

•Executive Directive to Improve Metrics

Major Benefits of Project:

•Establish Global Shared Services Center

•Reduce staffing costs by 85%

•Total Project Savings of $10 Million

•Annual Department Reduction of $2M

•50% Reduction in Credit Decision Time

•30% Gain in Customer Credit Tracking

•Ability to quantify/segment portfolio risk

•Ability to obtain total customer exposure

•Enhanced Risk Analysis Modeling

CASE STUDY #3

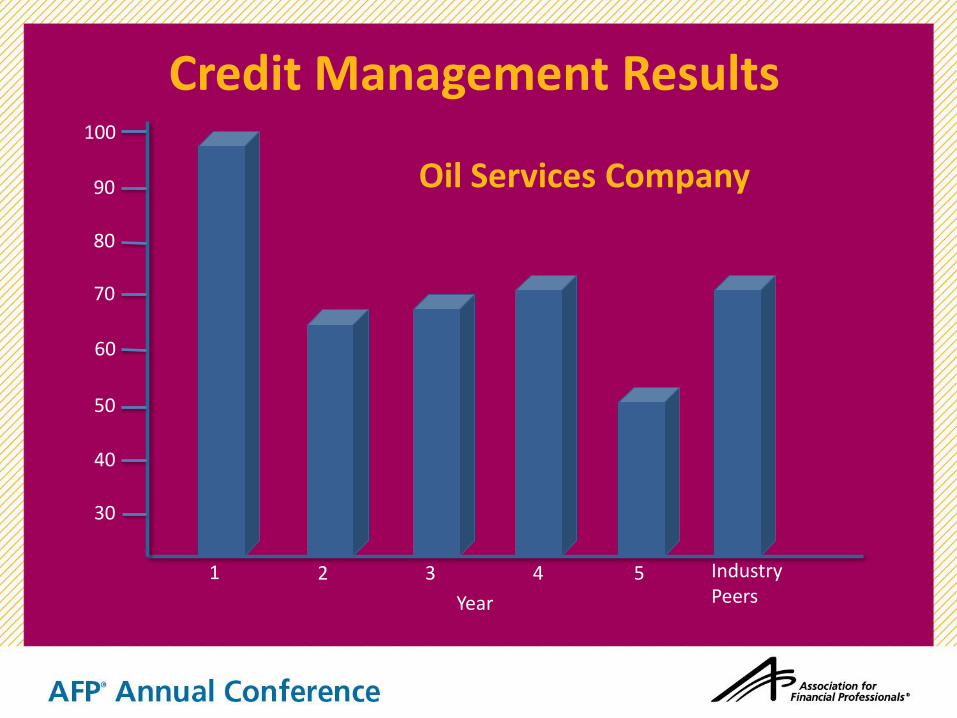

Credit Management Results

Year

80

2 3 5 Industry Peers

4

100

90

60

70

1

50

40

30

Oil Services Company

1

SAMPLE

Accounts Receivable Analysis

2

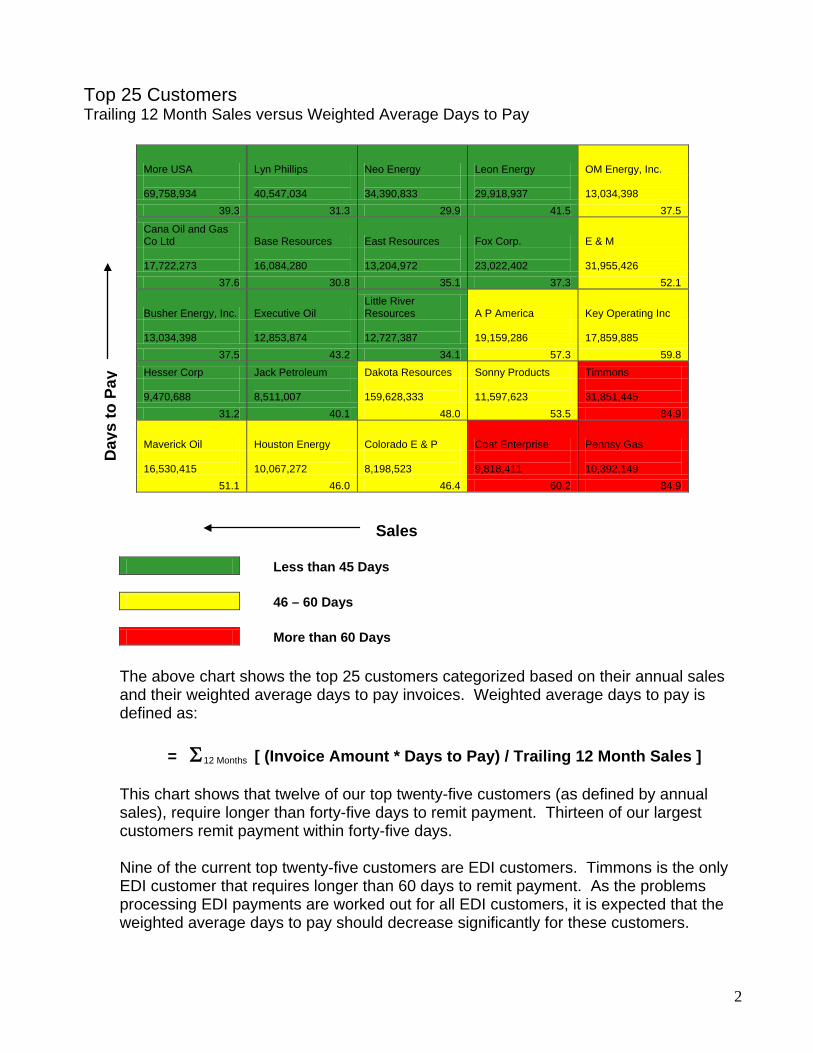

Top 25 Customers Trailing 12 Month Sales versus Weighted Average Days to Pay

More USA Lyn Phillips Neo Energy Leon Energy OM Energy, Inc. 69,758,934

40,547,034

34,390,833

29,918,937

13,034,398

39.3 31.3 29.9 41.5 37.5

Cana Oil and Gas Co Ltd Base Resources East Resources Fox Corp. E & M 17,722,273

16,084,280

13,204,972

23,022,402

31,955,426

37.6 30.8 35.1 37.3 52.1

Busher Energy, Inc. Executive Oil Little River Resources A P America Key Operating Inc

13,034,398

12,853,874

12,727,387

19,159,286

17,859,885

37.5 43.2 34.1 57.3 59.8 Hesser Corp Jack Petroleum Dakota Resources Sonny Products Timmons 9,470,688

8,511,007

159,628,333

11,597,623

31,851,445

31.2 40.1 48.0 53.5 84.9

Maverick Oil Houston Energy Colorado E & P Coat Enterprise Pennsy Gas 16,530,415

10,067,272

8,198,523

9,818,411

10,392,149

51.1 46.0 46.4 60.2 84.9

Less than 45 Days 46 – 60 Days More than 60 Days

The above chart shows the top 25 customers categorized based on their annual sales and their weighted average days to pay invoices. Weighted average days to pay is defined as: = Σ12 Months [ (Invoice Amount * Days to Pay) / Trailing 12 Month Sales ] This chart shows that twelve of our top twenty-five customers (as defined by annual sales), require longer than forty-five days to remit payment. Thirteen of our largest customers remit payment within forty-five days. Nine of the current top twenty-five customers are EDI customers. Timmons is the only EDI customer that requires longer than 60 days to remit payment. As the problems processing EDI payments are worked out for all EDI customers, it is expected that the weighted average days to pay should decrease significantly for these customers.

Sales

Day

s to

Pay

3

Accounts Receivable

0.00%10.00%20.00%30.00%40.00%50.00%60.00%70.00%

Feb-04Mar-04Apr-04May-04Jun-04Jul-04Aug-04Sep-04Oct-04Nov-04Dec-04

Current % Over 30 % Over 60 % Over 90

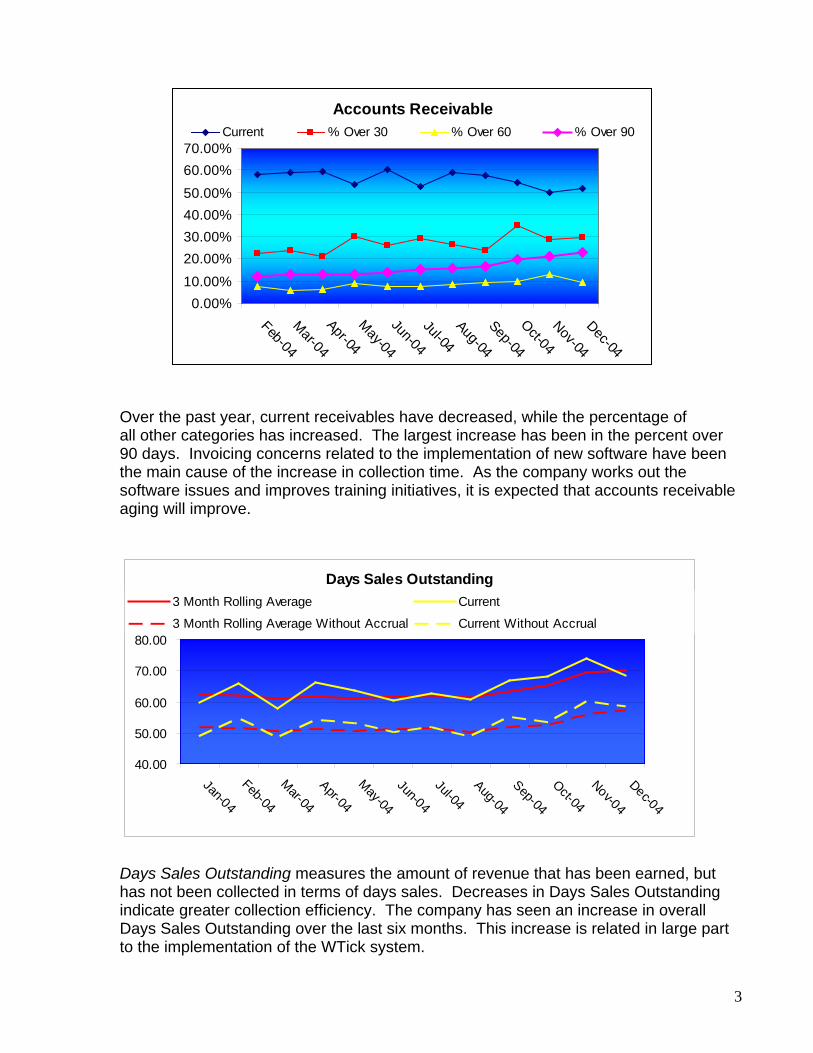

Over the past year, current receivables have decreased, while the percentage of

all other categories has increased. The largest increase has been in the percent over 90 days. Invoicing concerns related to the implementation of new software have been the main cause of the increase in collection time. As the company works out the software issues and improves training initiatives, it is expected that accounts receivable aging will improve.

Days Sales Outstanding

40.00

50.00

60.00

70.00

80.00

Jan-04

Feb-04

Mar-04

Apr-04

May-04

Jun-04

Jul-04Aug-04

Sep-04

Oct-04

Nov-04

Dec-04

3 Month Rolling Average Current

3 Month Rolling Average Without Accrual Current Without Accrual

Days Sales Outstanding measures the amount of revenue that has been earned, but has not been collected in terms of days sales. Decreases in Days Sales Outstanding indicate greater collection efficiency. The company has seen an increase in overall Days Sales Outstanding over the last six months. This increase is related in large part to the implementation of the WTick system.

4

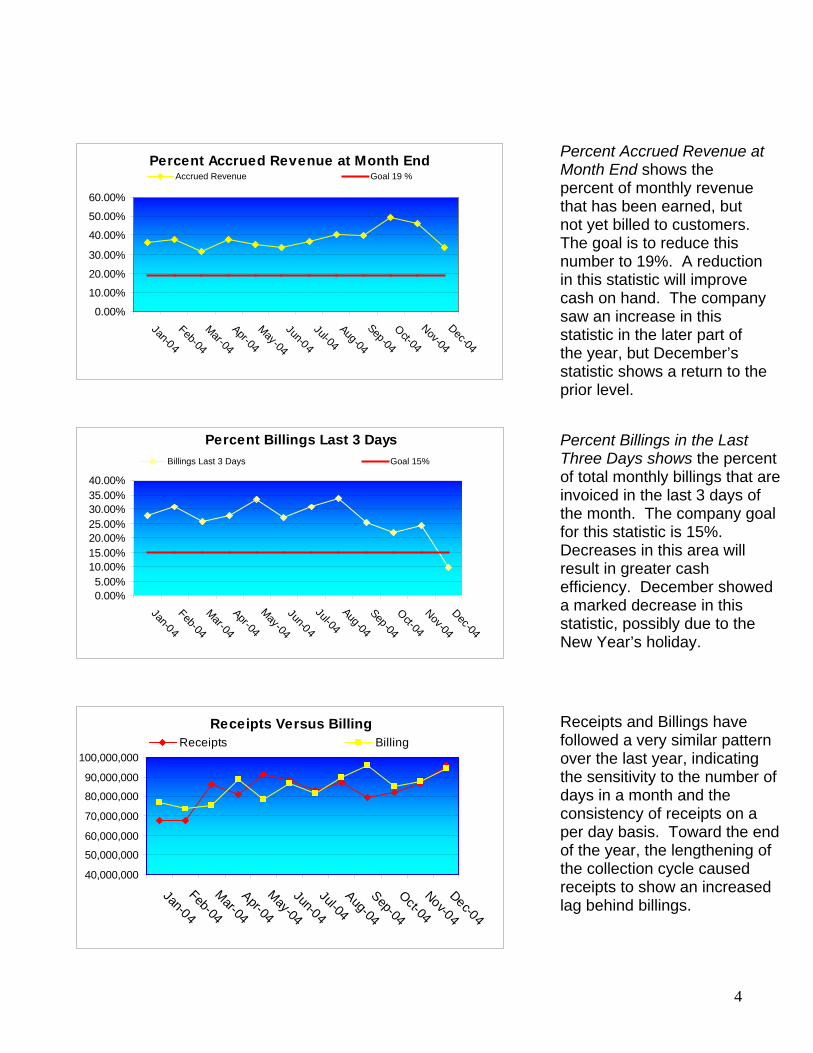

Percent Accrued Revenue at Month End

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

60.00%

Jan-04

Feb-04

Mar-04

Apr-04

May-04

Jun-04

Jul-04Aug-04

Sep-04

Oct-04

Nov-04

Dec-04

Accrued Revenue Goal 19 %

Percent Billings Last 3 Days

0.00%5.00%

10.00%15.00%20.00%25.00%30.00%35.00%40.00%

Jan-04Feb-04Mar-04Apr-04May-04Jun-04Jul-04Aug-04Sep-04Oct-04Nov-04Dec-04

Billings Last 3 Days Goal 15%

Receipts Versus Billing

40,000,000

50,000,000

60,000,000

70,000,000

80,000,000

90,000,000

100,000,000

Jan-04

Feb-04

Mar-04

Apr-04

May-04

Jun-04

Jul-04Aug-04

Sep-04

Oct-04

Nov-04

Dec-04

Receipts Billing

Percent Accrued Revenue at Month End shows the percent of monthly revenue that has been earned, but not yet billed to customers. The goal is to reduce this number to 19%. A reduction in this statistic will improve cash on hand. The company saw an increase in this statistic in the later part of the year, but December’s statistic shows a return to the prior level.

Percent Billings in the Last Three Days shows the percent of total monthly billings that are invoiced in the last 3 days of the month. The company goal for this statistic is 15%. Decreases in this area will result in greater cash efficiency. December showed a marked decrease in this statistic, possibly due to the New Year’s holiday.

Receipts and Billings have followed a very similar pattern over the last year, indicating the sensitivity to the number of days in a month and the consistency of receipts on a per day basis. Toward the end of the year, the lengthening of the collection cycle caused receipts to show an increased lag behind billings.

5

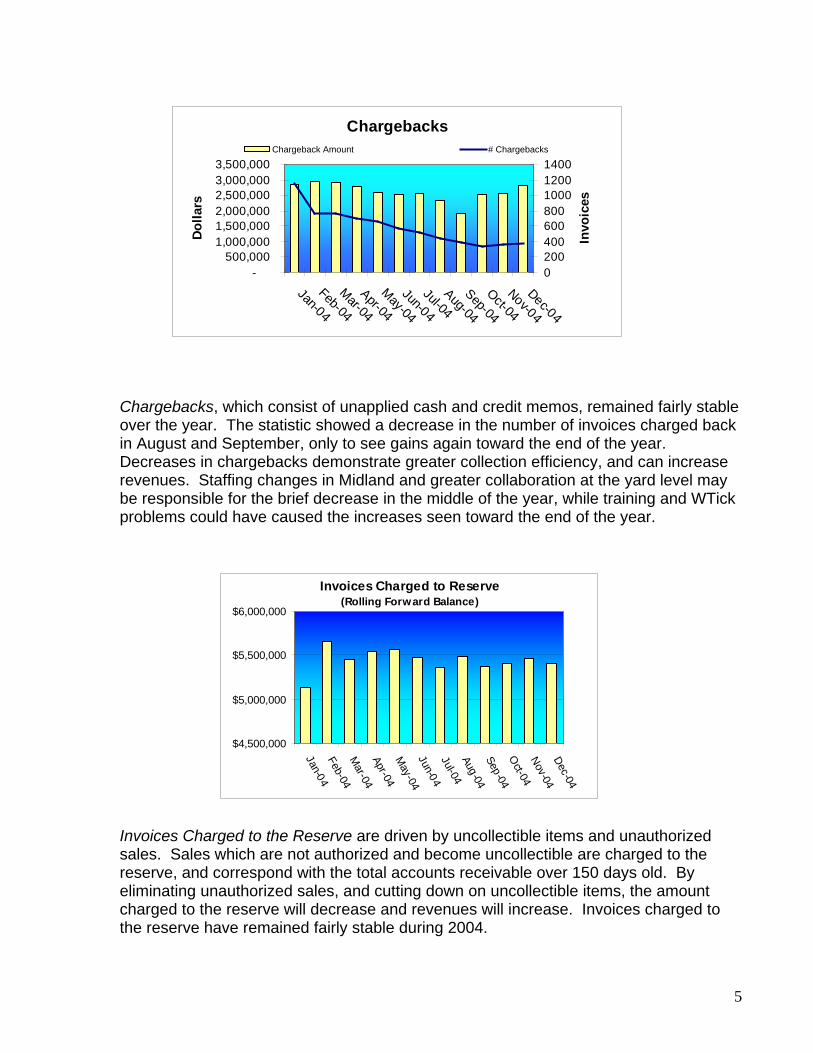

Chargebacks

-500,000

1,000,0001,500,0002,000,0002,500,0003,000,0003,500,000

Jan-04

Feb-04

Mar-04

Apr-04

May-04

Jun-04

Jul-04Aug-04

Sep-04

Oct-04

Nov-04

Dec-04

Dolla

rs

0200400600800100012001400

Invo

ices

Chargeback Amount # Chargebacks

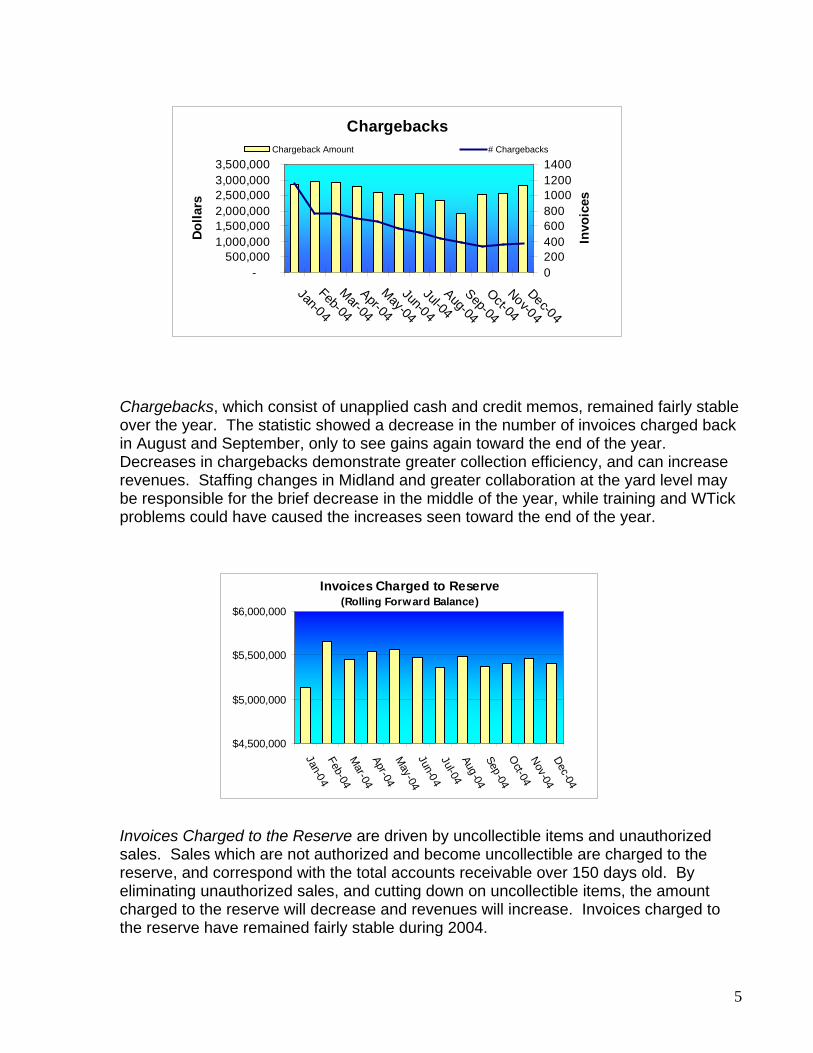

Chargebacks, which consist of unapplied cash and credit memos, remained fairly stable over the year. The statistic showed a decrease in the number of invoices charged back in August and September, only to see gains again toward the end of the year. Decreases in chargebacks demonstrate greater collection efficiency, and can increase revenues. Staffing changes in Midland and greater collaboration at the yard level may be responsible for the brief decrease in the middle of the year, while training and WTick problems could have caused the increases seen toward the end of the year.

Invoices Charged to Reserve(Rolling Forward Balance)

$4,500,000

$5,000,000

$5,500,000

$6,000,000

Jan-04Feb-04M

ar-04Apr-04M

ay-04Jun-04Jul-04Aug-04Sep-04O

ct-04Nov-04Dec-04

Invoices Charged to the Reserve are driven by uncollectible items and unauthorized sales. Sales which are not authorized and become uncollectible are charged to the reserve, and correspond with the total accounts receivable over 150 days old. By eliminating unauthorized sales, and cutting down on uncollectible items, the amount charged to the reserve will decrease and revenues will increase. Invoices charged to the reserve have remained fairly stable during 2004.

6

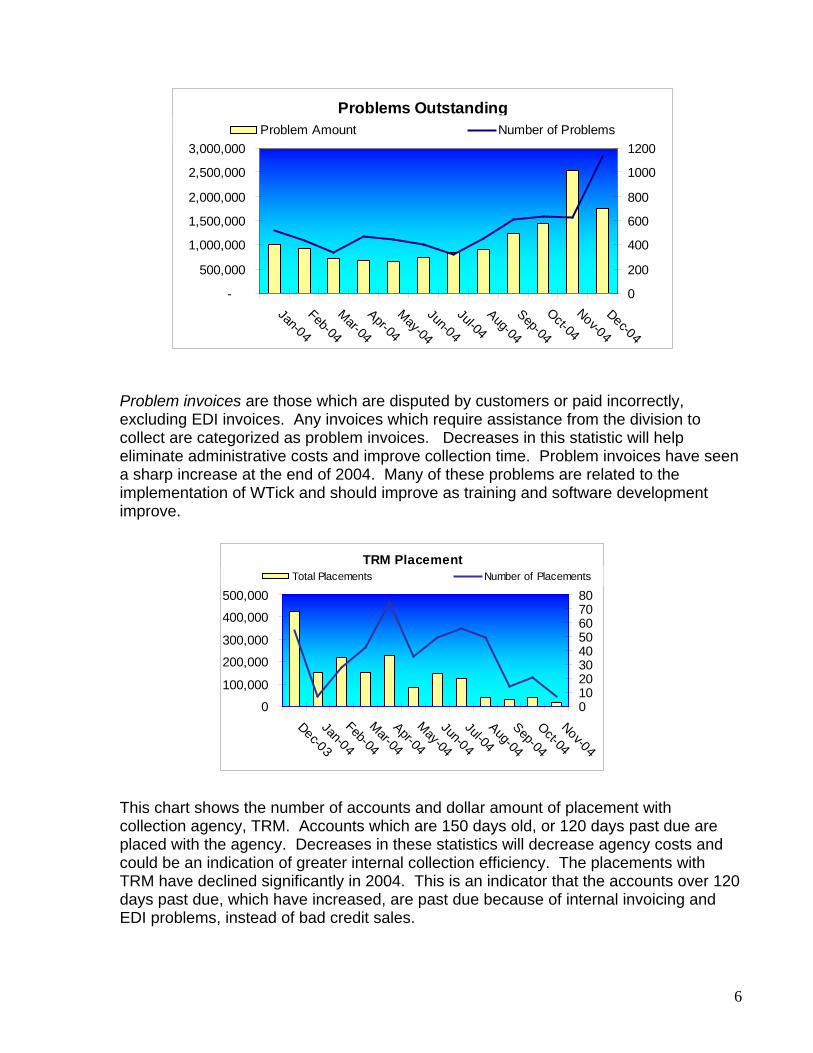

Problems Outstanding

-

500,000

1,000,000

1,500,000

2,000,000

2,500,000

3,000,000

Jan-04

Feb-04

Mar-04

Apr-04

May-04

Jun-04

Jul-04Aug-04

Sep-04

Oct-04

Nov-04

Dec-04

0

200

400

600

800

1000

1200Problem Amount Number of Problems

Problem invoices are those which are disputed by customers or paid incorrectly, excluding EDI invoices. Any invoices which require assistance from the division to collect are categorized as problem invoices. Decreases in this statistic will help eliminate administrative costs and improve collection time. Problem invoices have seen a sharp increase at the end of 2004. Many of these problems are related to the implementation of WTick and should improve as training and software development improve.

TRM Placement

0

100,000

200,000

300,000

400,000

500,000

Dec-03

Jan-04

Feb-04

Mar-04

Apr-04

May-04

Jun-04

Jul-04Aug-04

Sep-04

Oct-04

Nov-04

01020304050607080

Total Placements Number of Placements

This chart shows the number of accounts and dollar amount of placement with collection agency, TRM. Accounts which are 150 days old, or 120 days past due are placed with the agency. Decreases in these statistics will decrease agency costs and could be an indication of greater internal collection efficiency. The placements with TRM have declined significantly in 2004. This is an indicator that the accounts over 120 days past due, which have increased, are past due because of internal invoicing and EDI problems, instead of bad credit sales.

7

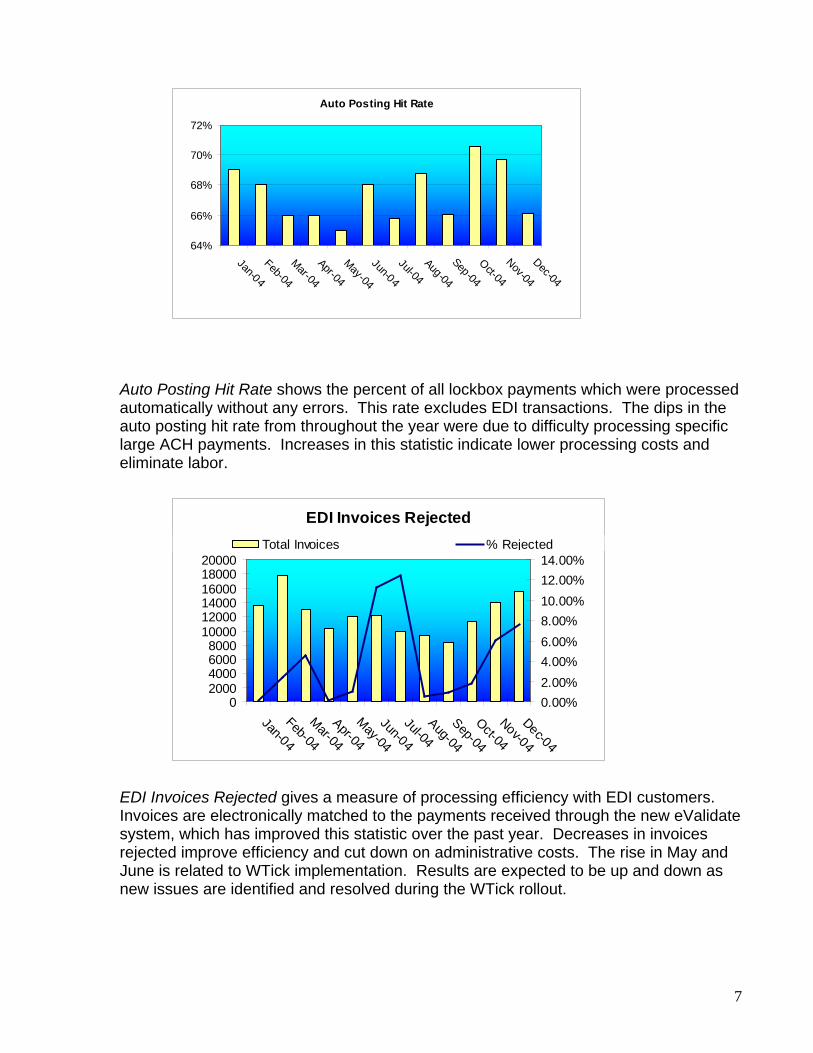

Auto Posting Hit Rate

64%

66%

68%

70%

72%

Jan-04

Feb-04

Mar-04

Apr-04

May-04

Jun-04

Jul-04Aug-04

Sep-04

Oct-04

Nov-04

Dec-04

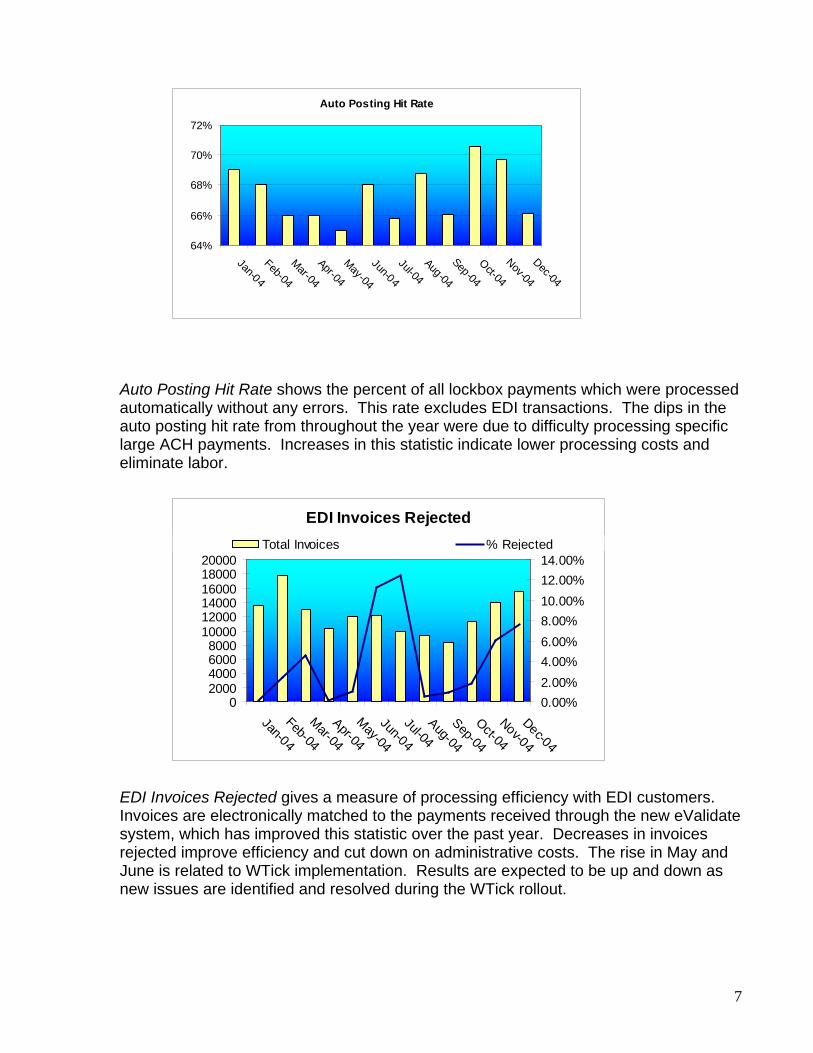

Auto Posting Hit Rate shows the percent of all lockbox payments which were processed automatically without any errors. This rate excludes EDI transactions. The dips in the auto posting hit rate from throughout the year were due to difficulty processing specific large ACH payments. Increases in this statistic indicate lower processing costs and eliminate labor.

EDI Invoices Rejected

02000400060008000

100001200014000160001800020000

Jan-04

Feb-04

Mar-04

Apr-04

May-04

Jun-04

Jul-04Aug-04

Sep-04

Oct-04

Nov-04

Dec-04

0.00%2.00%4.00%6.00%8.00%10.00%12.00%14.00%

Total Invoices % Rejected

EDI Invoices Rejected gives a measure of processing efficiency with EDI customers. Invoices are electronically matched to the payments received through the new eValidate system, which has improved this statistic over the past year. Decreases in invoices rejected improve efficiency and cut down on administrative costs. The rise in May and June is related to WTick implementation. Results are expected to be up and down as new issues are identified and resolved during the WTick rollout.

8

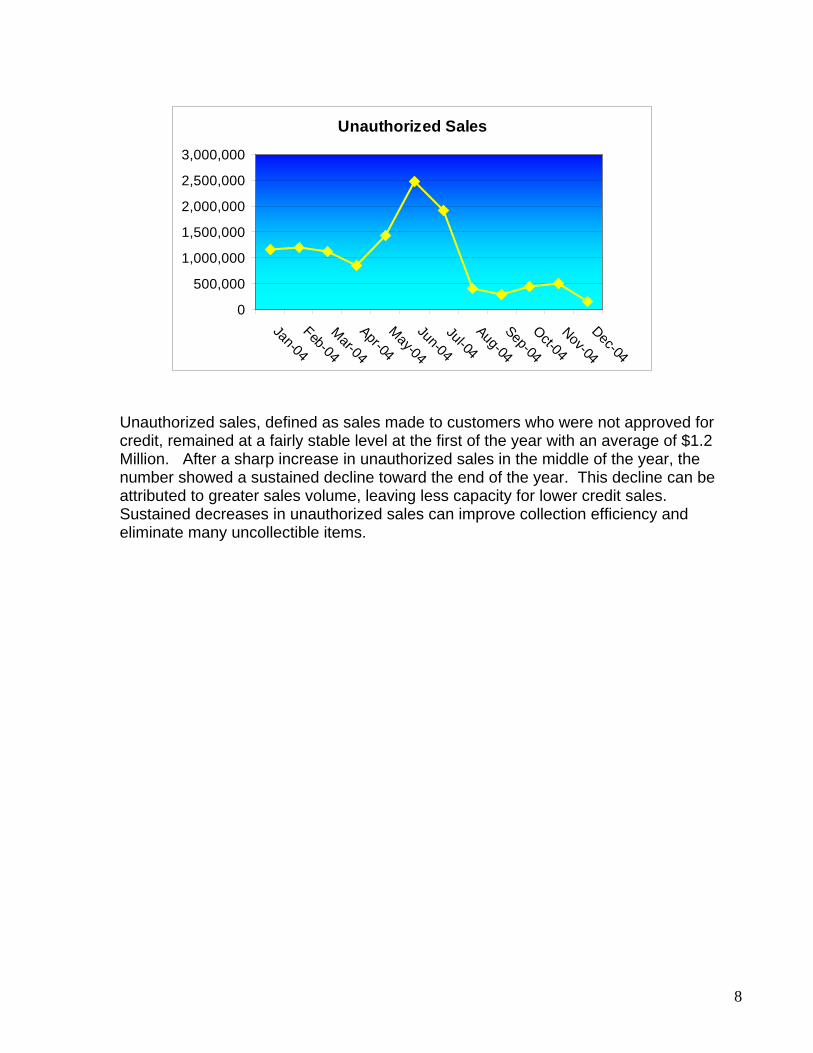

Unauthorized Sales

0

500,000

1,000,000

1,500,000

2,000,000

2,500,000

3,000,000

Jan-04

Feb-04

Mar-04

Apr-04

May-04

Jun-04

Jul-04Aug-04

Sep-04

Oct-04Nov-04

Dec-04

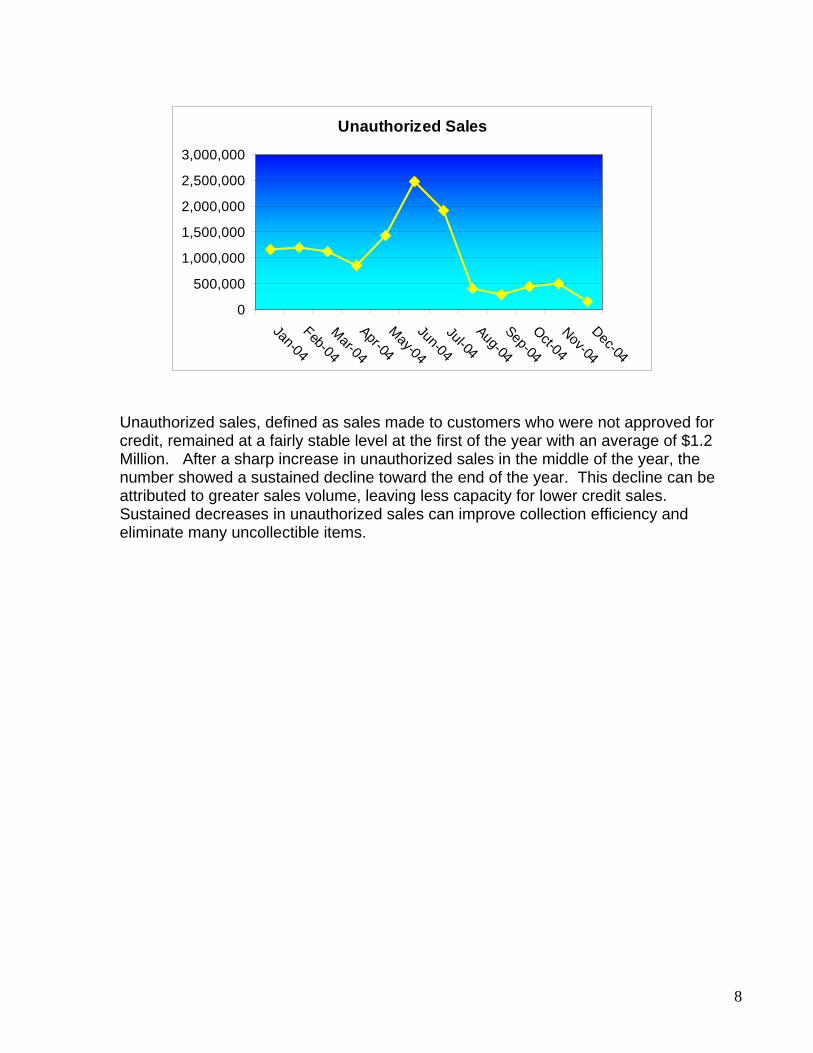

Unauthorized sales, defined as sales made to customers who were not approved for credit, remained at a fairly stable level at the first of the year with an average of $1.2 Million. After a sharp increase in unauthorized sales in the middle of the year, the number showed a sustained decline toward the end of the year. This decline can be attributed to greater sales volume, leaving less capacity for lower credit sales. Sustained decreases in unauthorized sales can improve collection efficiency and eliminate many uncollectible items.

KEY ENERGY SERVICES, INC.SAMPLE CREDIT POLICY

In order to serve our customers, both internally and externally, Key Energy ServicesCOMPANY, Inc. adopts the following Credit Policy.

CREDIT GRANTING AUTHORITY AND TERMS THEREOF All credit decisions will be made by the Credit Manager and/or the Assistant Credit Manager. Granting of credit will be made on the analysis of each customer’s ability to pay their invoices in full no later than THIRTY DAYS from invoice date. The credit decisions made by the credit department can only be overturned by the CEO/PRESIDENT, the Executive VP Operations, or the Executive VP/ CFO. Management realizes there may be customers that are vital to a division’s profitability who may pay their vendors in excess of thirty days and yet are creditworthy. In these instances a division manager shall submit a “Justification for Extension of Credit” (forms will be available through the credit department) which will require the division manager to substantiate why we should sell to this customer. Once completed resubmit this form back to the credit manager, who will take it to the proper officer for review and final disposition. You will be notified of the final decision made under these circumstances.

CHAIN OF COMMAND Each yard manager is responsible to verify that credit is approved for any work done by his respective yard. The yard manager or his designee will be responsible for having proper approval for each job, for each customer, being delivered from their yard. Should the yard manager not agree with the credit decision he receives, he will contact his division manager. If the division manager believes the decision should be reviewed, he will in turn contact the Group VP for that region. If the VP wishes to have the decision reviewed, the Executive VP Operations will be contacted. He will review the credit decision with the Credit or Assistant Credit Manager and either agree with the decision or override it and notify the Group VP of this decision. The Group VP will then pass this final decision back through the appropriate chain of command.

CREDIT APPROVALS

Credit Approvals may be obtained in one of the following manners: 1. Viewing the customer’s credit rating on line through our database. Each active customer will have a

credit designation code assigned to it. ACTIVE CUSTOMER is stressed because if the customer has not had any activity in the past ninety days, the code will be blank and the credit will need to be verified by the credit department to determine where they will be classified following the appropriate credit investigation.

Formatted: Justified

Formatted: Justified

Formatted: Justified

Formatted: Justified

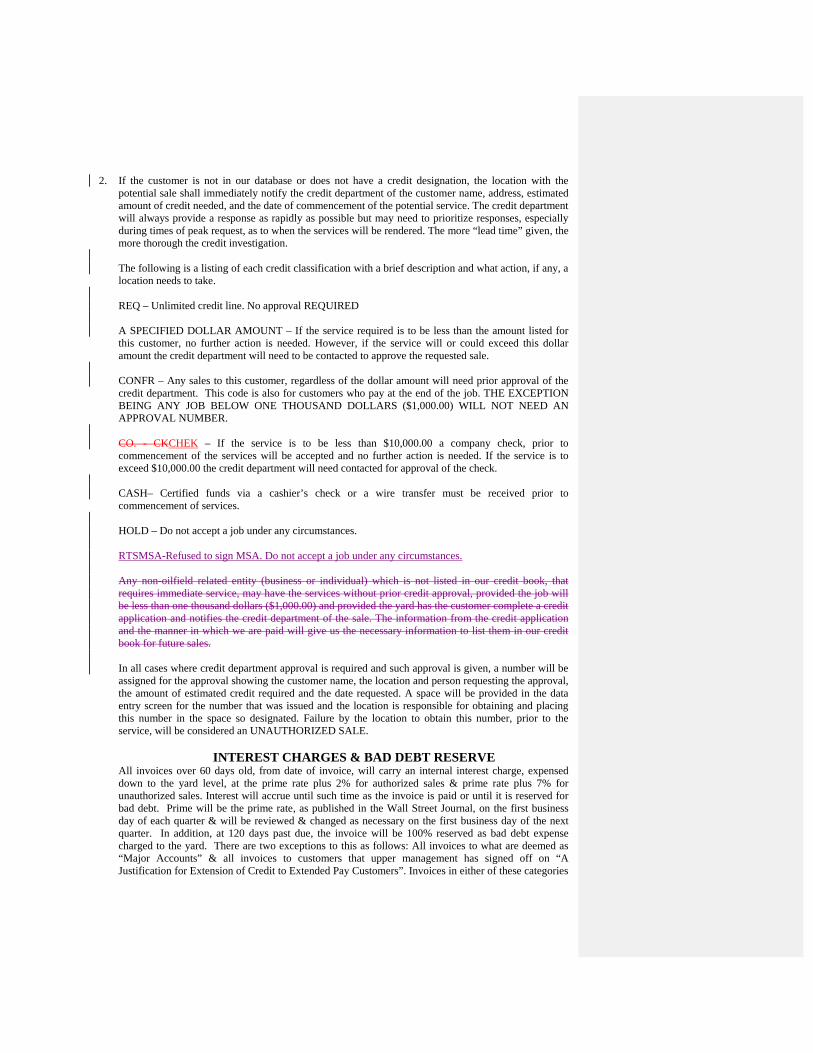

2. If the customer is not in our database or does not have a credit designation, the location with the potential sale shall immediately notify the credit department of the customer name, address, estimated amount of credit needed, and the date of commencement of the potential service. The credit department will always provide a response as rapidly as possible but may need to prioritize responses, especially during times of peak request, as to when the services will be rendered. The more “lead time” given, the more thorough the credit investigation.

The following is a listing of each credit classification with a brief description and what action, if any, a location needs to take. REQ – Unlimited credit line. No approval REQUIRED A SPECIFIED DOLLAR AMOUNT – If the service required is to be less than the amount listed for this customer, no further action is needed. However, if the service will or could exceed this dollar amount the credit department will need to be contacted to approve the requested sale. CONFR – Any sales to this customer, regardless of the dollar amount will need prior approval of the credit department. This code is also for customers who pay at the end of the job. THE EXCEPTION BEING ANY JOB BELOW ONE THOUSAND DOLLARS ($1,000.00) WILL NOT NEED AN APPROVAL NUMBER. CO. - CKCHEK – If the service is to be less than $10,000.00 a company check, prior to commencement of the services will be accepted and no further action is needed. If the service is to exceed $10,000.00 the credit department will need contacted for approval of the check. CASH– Certified funds via a cashier’s check or a wire transfer must be received prior to commencement of services. HOLD – Do not accept a job under any circumstances. RTSMSA-Refused to sign MSA. Do not accept a job under any circumstances. Any non-oilfield related entity (business or individual) which is not listed in our credit book, that requires immediate service, may have the services without prior credit approval, provided the job will be less than one thousand dollars ($1,000.00) and provided the yard has the customer complete a credit application and notifies the credit department of the sale. The information from the credit application and the manner in which we are paid will give us the necessary information to list them in our credit book for future sales. In all cases where credit department approval is required and such approval is given, a number will be assigned for the approval showing the customer name, the location and person requesting the approval, the amount of estimated credit required and the date requested. A space will be provided in the data entry screen for the number that was issued and the location is responsible for obtaining and placing this number in the space so designated. Failure by the location to obtain this number, prior to the service, will be considered an UNAUTHORIZED SALE.

INTEREST CHARGES & BAD DEBT RESERVE All invoices over 60 days old, from date of invoice, will carry an internal interest charge, expensed down to the yard level, at the prime rate plus 2% for authorized sales & prime rate plus 7% for unauthorized sales. Interest will accrue until such time as the invoice is paid or until it is reserved for bad debt. Prime will be the prime rate, as published in the Wall Street Journal, on the first business day of each quarter & will be reviewed & changed as necessary on the first business day of the next quarter. In addition, at 120 days past due, the invoice will be 100% reserved as bad debt expense charged to the yard. There are two exceptions to this as follows: All invoices to what are deemed as “Major Accounts” & all invoices to customers that upper management has signed off on “A Justification for Extension of Credit to Extended Pay Customers”. Invoices in either of these categories

will not be reserved for bad debt. Once an invoice is paid it will no longer be reserved as bad debt, but interest charged will never be reversed.

1

SAMPLE

Accounts Receivable Analysis

2

Top 25 Customers Trailing 12 Month Sales versus Weighted Average Days to Pay

More USA Lyn Phillips Neo Energy Leon Energy OM Energy, Inc. 69,758,934

40,547,034

34,390,833

29,918,937

13,034,398

39.3 31.3 29.9 41.5 37.5

Cana Oil and Gas Co Ltd Base Resources East Resources Fox Corp. E & M 17,722,273

16,084,280

13,204,972

23,022,402

31,955,426

37.6 30.8 35.1 37.3 52.1

Busher Energy, Inc. Executive Oil Little River Resources A P America Key Operating Inc

13,034,398

12,853,874

12,727,387

19,159,286

17,859,885

37.5 43.2 34.1 57.3 59.8 Hesser Corp Jack Petroleum Dakota Resources Sonny Products Timmons 9,470,688

8,511,007

159,628,333

11,597,623

31,851,445

31.2 40.1 48.0 53.5 84.9

Maverick Oil Houston Energy Colorado E & P Coat Enterprise Pennsy Gas 16,530,415

10,067,272

8,198,523

9,818,411

10,392,149

51.1 46.0 46.4 60.2 84.9

Less than 45 Days 46 – 60 Days More than 60 Days

The above chart shows the top 25 customers categorized based on their annual sales and their weighted average days to pay invoices. Weighted average days to pay is defined as: = Σ12 Months [ (Invoice Amount * Days to Pay) / Trailing 12 Month Sales ] This chart shows that twelve of our top twenty-five customers (as defined by annual sales), require longer than forty-five days to remit payment. Thirteen of our largest customers remit payment within forty-five days. Nine of the current top twenty-five customers are EDI customers. Timmons is the only EDI customer that requires longer than 60 days to remit payment. As the problems processing EDI payments are worked out for all EDI customers, it is expected that the weighted average days to pay should decrease significantly for these customers.

Sales

Day

s to

Pay

3

Accounts Receivable

0.00%10.00%20.00%30.00%40.00%50.00%60.00%70.00%

Feb-04Mar-04Apr-04May-04Jun-04Jul-04Aug-04Sep-04Oct-04Nov-04Dec-04

Current % Over 30 % Over 60 % Over 90

Over the past year, current receivables have decreased, while the percentage of

all other categories has increased. The largest increase has been in the percent over 90 days. Invoicing concerns related to the implementation of new software have been the main cause of the increase in collection time. As the company works out the software issues and improves training initiatives, it is expected that accounts receivable aging will improve.

Days Sales Outstanding

40.00

50.00

60.00

70.00

80.00

Jan-04

Feb-04

Mar-04

Apr-04

May-04

Jun-04

Jul-04Aug-04

Sep-04

Oct-04

Nov-04

Dec-04

3 Month Rolling Average Current

3 Month Rolling Average Without Accrual Current Without Accrual

Days Sales Outstanding measures the amount of revenue that has been earned, but has not been collected in terms of days sales. Decreases in Days Sales Outstanding indicate greater collection efficiency. The company has seen an increase in overall Days Sales Outstanding over the last six months. This increase is related in large part to the implementation of the WTick system.

4

Percent Accrued Revenue at Month End

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

60.00%

Jan-04

Feb-04

Mar-04

Apr-04

May-04

Jun-04

Jul-04Aug-04

Sep-04

Oct-04

Nov-04

Dec-04

Accrued Revenue Goal 19 %

Percent Billings Last 3 Days

0.00%5.00%

10.00%15.00%20.00%25.00%30.00%35.00%40.00%

Jan-04Feb-04Mar-04Apr-04May-04Jun-04Jul-04Aug-04Sep-04Oct-04Nov-04Dec-04

Billings Last 3 Days Goal 15%

Receipts Versus Billing

40,000,000

50,000,000

60,000,000

70,000,000

80,000,000

90,000,000

100,000,000

Jan-04

Feb-04

Mar-04

Apr-04

May-04

Jun-04

Jul-04Aug-04

Sep-04

Oct-04

Nov-04

Dec-04

Receipts Billing

Percent Accrued Revenue at Month End shows the percent of monthly revenue that has been earned, but not yet billed to customers. The goal is to reduce this number to 19%. A reduction in this statistic will improve cash on hand. The company saw an increase in this statistic in the later part of the year, but December’s statistic shows a return to the prior level.

Percent Billings in the Last Three Days shows the percent of total monthly billings that are invoiced in the last 3 days of the month. The company goal for this statistic is 15%. Decreases in this area will result in greater cash efficiency. December showed a marked decrease in this statistic, possibly due to the New Year’s holiday.

Receipts and Billings have followed a very similar pattern over the last year, indicating the sensitivity to the number of days in a month and the consistency of receipts on a per day basis. Toward the end of the year, the lengthening of the collection cycle caused receipts to show an increased lag behind billings.

5

Chargebacks

-500,000

1,000,0001,500,0002,000,0002,500,0003,000,0003,500,000

Jan-04

Feb-04

Mar-04

Apr-04

May-04

Jun-04

Jul-04Aug-04

Sep-04

Oct-04

Nov-04

Dec-04

Dolla

rs

0200400600800100012001400

Invo

ices

Chargeback Amount # Chargebacks

Chargebacks, which consist of unapplied cash and credit memos, remained fairly stable over the year. The statistic showed a decrease in the number of invoices charged back in August and September, only to see gains again toward the end of the year. Decreases in chargebacks demonstrate greater collection efficiency, and can increase revenues. Staffing changes in Midland and greater collaboration at the yard level may be responsible for the brief decrease in the middle of the year, while training and WTick problems could have caused the increases seen toward the end of the year.

Invoices Charged to Reserve(Rolling Forward Balance)

$4,500,000

$5,000,000

$5,500,000

$6,000,000

Jan-04Feb-04M

ar-04Apr-04M

ay-04Jun-04Jul-04Aug-04Sep-04O

ct-04Nov-04Dec-04

Invoices Charged to the Reserve are driven by uncollectible items and unauthorized sales. Sales which are not authorized and become uncollectible are charged to the reserve, and correspond with the total accounts receivable over 150 days old. By eliminating unauthorized sales, and cutting down on uncollectible items, the amount charged to the reserve will decrease and revenues will increase. Invoices charged to the reserve have remained fairly stable during 2004.

6

Problems Outstanding

-

500,000

1,000,000

1,500,000

2,000,000

2,500,000

3,000,000

Jan-04

Feb-04

Mar-04

Apr-04

May-04

Jun-04

Jul-04Aug-04

Sep-04

Oct-04

Nov-04

Dec-04

0

200

400

600

800

1000

1200Problem Amount Number of Problems

Problem invoices are those which are disputed by customers or paid incorrectly, excluding EDI invoices. Any invoices which require assistance from the division to collect are categorized as problem invoices. Decreases in this statistic will help eliminate administrative costs and improve collection time. Problem invoices have seen a sharp increase at the end of 2004. Many of these problems are related to the implementation of WTick and should improve as training and software development improve.

TRM Placement

0

100,000

200,000

300,000

400,000

500,000

Dec-03

Jan-04

Feb-04

Mar-04

Apr-04

May-04

Jun-04

Jul-04Aug-04

Sep-04

Oct-04

Nov-04

01020304050607080

Total Placements Number of Placements

This chart shows the number of accounts and dollar amount of placement with collection agency, TRM. Accounts which are 150 days old, or 120 days past due are placed with the agency. Decreases in these statistics will decrease agency costs and could be an indication of greater internal collection efficiency. The placements with TRM have declined significantly in 2004. This is an indicator that the accounts over 120 days past due, which have increased, are past due because of internal invoicing and EDI problems, instead of bad credit sales.

7

Auto Posting Hit Rate

64%

66%

68%

70%

72%

Jan-04

Feb-04

Mar-04

Apr-04

May-04

Jun-04

Jul-04Aug-04

Sep-04

Oct-04

Nov-04

Dec-04

Auto Posting Hit Rate shows the percent of all lockbox payments which were processed automatically without any errors. This rate excludes EDI transactions. The dips in the auto posting hit rate from throughout the year were due to difficulty processing specific large ACH payments. Increases in this statistic indicate lower processing costs and eliminate labor.

EDI Invoices Rejected

02000400060008000

100001200014000160001800020000

Jan-04

Feb-04

Mar-04

Apr-04

May-04

Jun-04

Jul-04Aug-04

Sep-04

Oct-04

Nov-04

Dec-04

0.00%2.00%4.00%6.00%8.00%10.00%12.00%14.00%

Total Invoices % Rejected

EDI Invoices Rejected gives a measure of processing efficiency with EDI customers. Invoices are electronically matched to the payments received through the new eValidate system, which has improved this statistic over the past year. Decreases in invoices rejected improve efficiency and cut down on administrative costs. The rise in May and June is related to WTick implementation. Results are expected to be up and down as new issues are identified and resolved during the WTick rollout.

8

Unauthorized Sales

0

500,000

1,000,000

1,500,000

2,000,000

2,500,000

3,000,000

Jan-04

Feb-04

Mar-04

Apr-04

May-04

Jun-04

Jul-04Aug-04

Sep-04

Oct-04Nov-04

Dec-04

Unauthorized sales, defined as sales made to customers who were not approved for credit, remained at a fairly stable level at the first of the year with an average of $1.2 Million. After a sharp increase in unauthorized sales in the middle of the year, the number showed a sustained decline toward the end of the year. This decline can be attributed to greater sales volume, leaving less capacity for lower credit sales. Sustained decreases in unauthorized sales can improve collection efficiency and eliminate many uncollectible items.

KEY ENERGY SERVICES, INC.SAMPLE CREDIT POLICY

In order to serve our customers, both internally and externally, Key Energy ServicesCOMPANY, Inc. adopts the following Credit Policy.

CREDIT GRANTING AUTHORITY AND TERMS THEREOF All credit decisions will be made by the Credit Manager and/or the Assistant Credit Manager. Granting of credit will be made on the analysis of each customer’s ability to pay their invoices in full no later than THIRTY DAYS from invoice date. The credit decisions made by the credit department can only be overturned by the CEO/PRESIDENT, the Executive VP Operations, or the Executive VP/ CFO. Management realizes there may be customers that are vital to a division’s profitability who may pay their vendors in excess of thirty days and yet are creditworthy. In these instances a division manager shall submit a “Justification for Extension of Credit” (forms will be available through the credit department) which will require the division manager to substantiate why we should sell to this customer. Once completed resubmit this form back to the credit manager, who will take it to the proper officer for review and final disposition. You will be notified of the final decision made under these circumstances.

CHAIN OF COMMAND Each yard manager is responsible to verify that credit is approved for any work done by his respective yard. The yard manager or his designee will be responsible for having proper approval for each job, for each customer, being delivered from their yard. Should the yard manager not agree with the credit decision he receives, he will contact his division manager. If the division manager believes the decision should be reviewed, he will in turn contact the Group VP for that region. If the VP wishes to have the decision reviewed, the Executive VP Operations will be contacted. He will review the credit decision with the Credit or Assistant Credit Manager and either agree with the decision or override it and notify the Group VP of this decision. The Group VP will then pass this final decision back through the appropriate chain of command.

CREDIT APPROVALS

Credit Approvals may be obtained in one of the following manners: 1. Viewing the customer’s credit rating on line through our database. Each active customer will have a

credit designation code assigned to it. ACTIVE CUSTOMER is stressed because if the customer has not had any activity in the past ninety days, the code will be blank and the credit will need to be verified by the credit department to determine where they will be classified following the appropriate credit investigation.

Formatted: Justified

Formatted: Justified

Formatted: Justified

Formatted: Justified

2. If the customer is not in our database or does not have a credit designation, the location with the potential sale shall immediately notify the credit department of the customer name, address, estimated amount of credit needed, and the date of commencement of the potential service. The credit department will always provide a response as rapidly as possible but may need to prioritize responses, especially during times of peak request, as to when the services will be rendered. The more “lead time” given, the more thorough the credit investigation.

The following is a listing of each credit classification with a brief description and what action, if any, a location needs to take. REQ – Unlimited credit line. No approval REQUIRED A SPECIFIED DOLLAR AMOUNT – If the service required is to be less than the amount listed for this customer, no further action is needed. However, if the service will or could exceed this dollar amount the credit department will need to be contacted to approve the requested sale. CONFR – Any sales to this customer, regardless of the dollar amount will need prior approval of the credit department. This code is also for customers who pay at the end of the job. THE EXCEPTION BEING ANY JOB BELOW ONE THOUSAND DOLLARS ($1,000.00) WILL NOT NEED AN APPROVAL NUMBER. CO. - CKCHEK – If the service is to be less than $10,000.00 a company check, prior to commencement of the services will be accepted and no further action is needed. If the service is to exceed $10,000.00 the credit department will need contacted for approval of the check. CASH– Certified funds via a cashier’s check or a wire transfer must be received prior to commencement of services. HOLD – Do not accept a job under any circumstances. RTSMSA-Refused to sign MSA. Do not accept a job under any circumstances. Any non-oilfield related entity (business or individual) which is not listed in our credit book, that requires immediate service, may have the services without prior credit approval, provided the job will be less than one thousand dollars ($1,000.00) and provided the yard has the customer complete a credit application and notifies the credit department of the sale. The information from the credit application and the manner in which we are paid will give us the necessary information to list them in our credit book for future sales. In all cases where credit department approval is required and such approval is given, a number will be assigned for the approval showing the customer name, the location and person requesting the approval, the amount of estimated credit required and the date requested. A space will be provided in the data entry screen for the number that was issued and the location is responsible for obtaining and placing this number in the space so designated. Failure by the location to obtain this number, prior to the service, will be considered an UNAUTHORIZED SALE.

INTEREST CHARGES & BAD DEBT RESERVE All invoices over 60 days old, from date of invoice, will carry an internal interest charge, expensed down to the yard level, at the prime rate plus 2% for authorized sales & prime rate plus 7% for unauthorized sales. Interest will accrue until such time as the invoice is paid or until it is reserved for bad debt. Prime will be the prime rate, as published in the Wall Street Journal, on the first business day of each quarter & will be reviewed & changed as necessary on the first business day of the next quarter. In addition, at 120 days past due, the invoice will be 100% reserved as bad debt expense charged to the yard. There are two exceptions to this as follows: All invoices to what are deemed as “Major Accounts” & all invoices to customers that upper management has signed off on “A Justification for Extension of Credit to Extended Pay Customers”. Invoices in either of these categories

will not be reserved for bad debt. Once an invoice is paid it will no longer be reserved as bad debt, but interest charged will never be reversed.

![Cloud Can’t Wait [Infographic]](https://static.fdocuments.in/doc/165x107/54c384594a79593a698b458a/cloud-cant-wait-infographic.jpg)

![Social Media Facts You Can’t Afford to Snub [Infographic]](https://static.fdocuments.in/doc/165x107/58cf8d811a28ab65538b480d/social-media-facts-you-cant-afford-to-snub-infographic.jpg)