Real Estate Update

16

Brought to you by: KW Research Commentary 2 The Numbers That Drive Real Estate 3 Recent Government Action 10 Topics for Home Buyers, Sellers, and Owners 13 Released: March 4, 2011

-

Upload

cquarantello -

Category

Business

-

view

206 -

download

0

Transcript of Real Estate Update

Brought to you by:

KW Research

Commentary 2

The Numbers That Drive Real Estate 3

Recent Government Action 10

Topics for Home Buyers, Sellers, and Owners 13

Released:

March 4, 2011

KW Research 2

Gradual progress in the housing market continues at a steady pace without government support. The market has shown remarkable improvement from the initial drop after the expiration of the home buyer tax credit this past July. Although higher-than-normal distressed sales skew the overall picture of home prices downward, inventory continues to shrink and sales continue to rise. The rock-bottom interest rates of 2010 are likely to trend upward. As economists anticipate rates at or above 6% by the end of 2012, buyers are moving off the sidelines and into the market.

A good sign for long-term market stability is that the median down payment on conventional mortgages has risen to 22%, up from 4% in 2006 and slightly above the 20% standard in the 1990s. This may keep buyers looking in slightly lower price ranges, but it is a good sign of future sustainability for homeowners and banks alike. There are still ample opportunities for those who would like down payments below 20%, including some conventional mortgages and those backed by the Federal Housing Administration, Veterans Affairs, and the Department of Agriculture’s Rural Development loans.

As the economy improves, stimulus efforts by the government and the Federal Reserve Board will gradually wind down, which typically means rising interest rates. Meanwhile, buyers continue to benefit from historically favorable buying conditions and sellers are encouraged by increased market stability.

Commentary

Brought to you by:

KW Research

Home Sales 4

Home Price 5

Inventory 6

Mortgage Rates 8

Affordability 9

The Numbers That Drive Real Estate

KW Research 4

Second Tax

Credit Expired

5.09

5.445.68

3.864.41

4.64

5.36

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Jan

Latest Data Release: February 23, 2011

Source: National Association of Realtors

Home SalesIn Millions

The increasing trend in existing home sales activity continued through January, and for the first time rose above year-ago levels when the home buyer tax credit was in effect. This marks the sixth monthly increase since July when the tax credit expired, and indicates a recovery that’s gaining a firmer footing without government support.

Extended and Expanded Home Buyer Tax CreditRenewed November 7, 2009

Must have had contract signed by April 30, 2010Must have close by June 30, 2010

Gradual Recovery WithoutTax Credit

January ’10-’11

January ’09-’10

KW Research 5

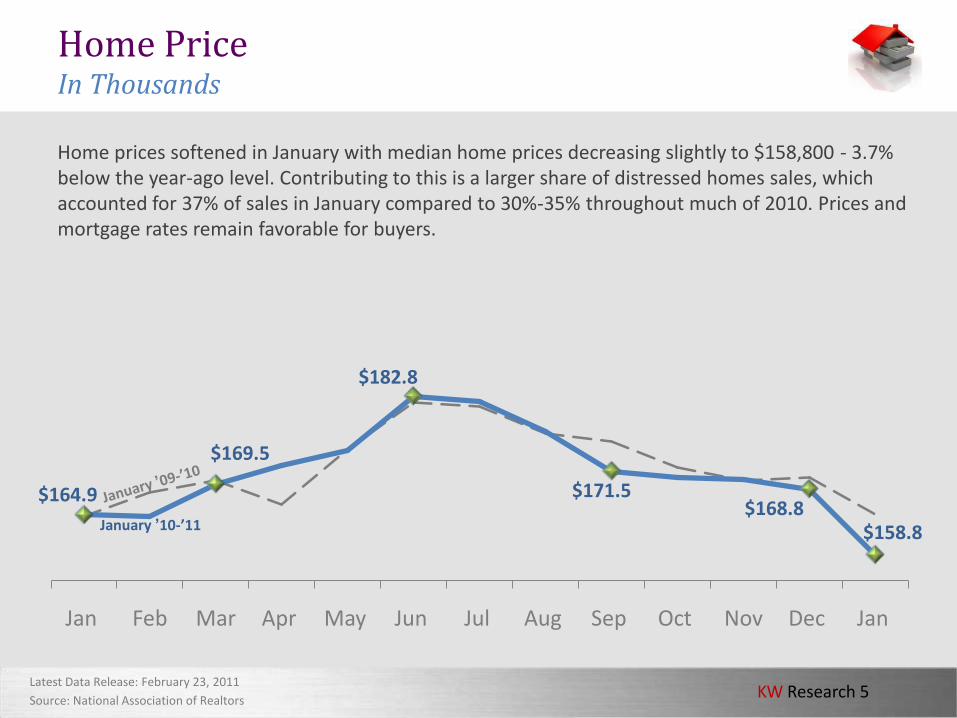

$164.9

$169.5

$182.8

$171.5 $168.8

$158.8

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Jan

Home PriceIn Thousands

Home prices softened in January with median home prices decreasing slightly to $158,800 - 3.7% below the year-ago level. Contributing to this is a larger share of distressed homes sales, which accounted for 37% of sales in January compared to 30%-35% throughout much of 2010. Prices and mortgage rates remain favorable for buyers.

January ’10-’11

Latest Data Release: February 23, 2011

Source: National Association of Realtors

KW Research 6

3.28 3.63

3.89 4.01

4.12

3.86

3.38

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Jan

Inventory -In Millions

Housing inventory continues to contract. There are now 3.38 million homes on the market, down 5.1% from December and only 3% above year-ago levels. More and more buyers are taking advantage of today’s exceptional affordability conditions. Expected improvements in lending standards and job growth will create great opportunities for buyers and investors.

Number of homes available for sale

January ’09-’10

January ’10-’11

Latest Data Release: February 23, 2011

Source: National Association of Realtors

KW Research 7

7.7 8.0 8.2

12.5

10.6

7.6

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Jan

Supply of InventoryIn Months

The uptick in home sales and a shrinking inventory pared down the month’s supply to 7.6 months, a decrease of 7.3% from December and 1% from year-ago levels. This is the lowest level in more than a year and marks the first time since July that the month’s supply is below where it was the previous year. Months of inventory has declined steadily (64%) from its peak of 12.5 months in July and is now back to pre-tax credit expiration levels. The supply of inventory is not far from a seller’s market, which is less than 6 month’s supply.

January ’09-’10

January ’ 10-’11

Latest Data Release: February 23, 2011

Source: National Association of Realtors

KW Research 8

Mortgage rates jumped above 5% for the first time since April 2009 in January. While rates dipped back to just below 5%, they are expected to continue an upward trend throughout the year. As overall economic recovery remains on track, rates will likely rise to keep inflation in check. Buyers wanting to capture the savings in monthly payments that a historically low interest rate affords are expected to take advantage of excellent buying conditions.

Mortgage Rates30-Year Fixed

Source: Freddie Mac

4-Feb5.01%

8-Apr5.21% 13-May

4.93%

26-Aug4.36%

11-Nov4.17%

16-Dec4.83%

3-Feb4.81%

1-Year Average – 4.67%

Historical Average – 8.9%

KW Research 9

Affordability -Percentage of Income

Housing affordability hit a new record in January. The relationship between mortgage rates, home prices, and family income is the most favorable on record for buying. The home price-to-income ratio continues to remain well below the historical standard. Stabilizing home prices and rising interest rates are expected to reverse the recent affordability trend.

Affordability as of January every year. Calculations assume a 20% down payment.

Source: National Association of Realtors

The percentage of a median family’s income required to make mortgage payments on a median-priced home

19.8% 18.6% 19.4% 18.4% 18.6% 19.9% 22.8% 21.5% 19.0% 13.6% 13.9% 13.1%

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Brought to you by:

KW Research

Recent Government Action

FHA to Increase Insurance Premiums 11

KW Research 11

FHA to Increase Insurance Premiums

The Federal Housing Administration (FHA) will be increasing mortgage insurance

premiums that its borrowers pay each year by 0.25% starting April 18, 2011.

Loans backed by the FHA currently account for more than one-third of all new

loans, up from only 2% in 2006. The FHA has taken several steps to strengthen its

financial standing since September 2009, when it indicated that reserves would fall

below the 2% minimum. Measures taken in January 2010 include raising the upfront

insurance fees by 0.5%, capping seller contributions to buyers closing costs at

3%, down from 6%, and requiring a higher down payment for those with poor credit.

As the FHA remains a great option among first time home buyers, those with smaller

down payments, and those with spotty credit, its strength and continued viability of

FHA is key to the housing market. Upcoming changes to FHA insurance premiums also

mean that buyers who are out looking and who intend to use FHA financing will want

to finalize their deal and close before April 18.

Sources: The Wall Street Journal, Bloomberg, Forbes

Brought to you by:

KW Research

Topics for Home Buyers, Sellers, and

Owners

Preparing to Sell 13

KW Research 13

Preparing to Sell

Preparing your home for sale in a buyer’s market can seem daunting, but these five tips will help you get the best price in the least amount of time.

1. Organizing and cleaning is crucial when prepping a home for sale. Potential home buyers have a more positive reaction to homes that are clutter-free and give them the feeling that the home is “move-in ready.”

2. Presale home inspection can inform you of any trouble areas within your home that can stand out to potential buyers. An inspection can also help you make any repairs necessary before future open houses.

3. Determine replacement estimates before listing your home, even if you are not planning on making the replacements yourself. This information can help buyers to make informed decisions.

4. Have your warranties ready – especially for all those home appliances that will stay within the home after the sale.

5. Curb appeal is a crucial factor because it determines first impressions. A negative first impression can cloud their entire opinion about the home.

KW Research 14

Although it is important to stay informed about what is going on in the national economy and housing market, many different factors impact the real estate market in your own area.

Talk to your KW associate for assistance interpreting the conditions in your local market.

KW associates are equipped with the knowledge and information to help you navigate the home-buying or selling process in this challenging market.

Your Local Market

KW Research 15

About Keller Williams Realty

Founded in 1983, Keller Williams Realty, Inc., is an international real estate company with more than 80,000 associates and 686 offices across the United States and Canada. The company began franchising in 1991 and, after years of phenomenal growth and success, became the third-largest U.S. residential real estate firm in 2009.

The company has succeeded by treating its associates as partners and sharing its knowledge, policy control, and company profits on a systemwide basis.

By focusing on helping associates realize their fullest potential, Keller Williams Realty is known as an industry leader for its family culture, unmatched education, profit-sharing business model, phenomenal coaching programs, and technology offerings.

www.kw.com

KW Research 16

The opinions expressed in This Month in Real Estate are intended to supplement opinions on real estate expressed by local and national media, local real estate agents, and other expert sources. You should not treat any opinion expressed in This Month in Real Estate as a specific inducement to make a particular investment or follow a particular strategy, but only as an expression of opinion. Keller Williams Realty, Inc., does not guarantee and is not responsible for the accuracy or completeness of information, and provides said information without warranties of any kind. All information presented herein is intended and should be used for educational purposes only. Nothing herein should be construed as investment advice. You should always conduct your own research and due diligence and obtain professional advice before making any investment decision. All investments involve somedegree of risk. Keller Williams Realty, Inc., will not be liable for any loss or damage caused by your reliance on information contained in This Month in Real Estate.