Reading of Ledger Account

18

READING OF LEDGER ACCOUNTS PREPARED BY- PARMINDER NEERAJA JASPREET JASMEET

-

Upload

neeru792000 -

Category

Documents

-

view

568 -

download

0

description

its a presentation on reading of ledger accounts..

Transcript of Reading of Ledger Account

READING OF LEDGER ACCOUNTS

PREPARED BY-

PARMINDER NEERAJA JASPREET JASMEET

INTRODUCTION

THINGS TO BE CHECKED

WHILE READING THE LEDGER ACCOUNT

Opening Balance

Books of Accounts

Amount of Transactions

Period

Accounting Principle

Amount of Closing Balance

Treatment to the Closing Balance

How to Interpretate the

Ledger Accounts..??

Debtor’s Account

Creditor’s Account

(1) Reading of Debtors and Creditors Account:

To Balance b/d xxx

By Balance b/d xxx

Debtor’s Account

Creditor’s Account

By Sales-Return xxx

To Sales A/c xxx

By Purchases A/c xxx

To Purchase-Return xxx

Debtor’s Account

To Bills-Receivable A/c xxx (Dishonoured)

By Bills-Receivable A/c xxx

To Interest A/c xxx

Creditor’s Account

To Bills-Payable A/c xxxBy Bills-Payable A/c xxx (Dishonoured)

By Interest A/c xxx

Debtor’s Account

Creditor’s Account

By Cash A/c xxBy Discount -Allowed A/c xx

To Cash A/c xx

To Discount -Received A/c xx

Debtor’s Account

Creditor’s Account

By Cash A/c xx

To Cash A/c xx

Debtor’s Account

Creditor’s Account

By Balance c/d xxx

To Balance c/d xxx

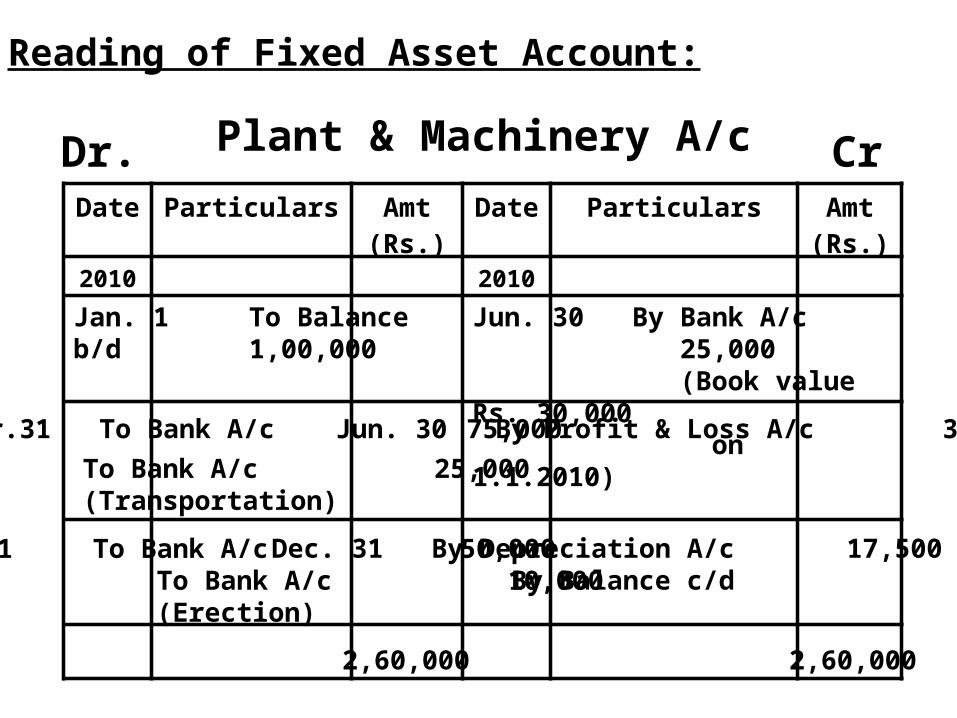

(2) Reading of Fixed Asset Account:

Plant & Machinery A/cDr. Cr.Dat

eParticulars Amt

(Rs.)Date

Particulars Amt(Rs.)

2010 2010Jan. 1 To Balance b/d 1,00,000

Jun. 30 By Bank A/c 25,000 (Book value Rs. 30,000 on 1.1.2010)

Mar.31 To Bank A/c 75,000

To Bank A/c 25,000(Transportation)

Jun. 30 By Profit & Loss A/c 3,500

Oct. 1 To Bank A/c 50,000 To Bank A/c 10,000 (Erection)

Dec. 31 By Depreciation A/c 17,500 By Balance c/d 2,14,000

2,60,000 2,60,000

(3) Reading of Deferred Revenue Expenditure Account:

Advertisement Expenses A/c

Date

Particulars

Amt(Rs.)

Date Particulars Amt(Rs.)

2009

2009

2010

2010

Jan. 1To Bank A/c36,000Dec. 31By Profit & Loss A/cBy Balance c/d

18,00018,000

Jan. 1To Bank A/c18,000Dec. 31 18,000

18,000 18,000

Dr. Cr.

By Profit & Loss A/c

36,000 36,000

(4) Reading of Advance Account:

Date

Particulars Amount

(Rs.)

Date Particulars Amount

(Rs.)

2010

2010May. 5

To Cash A/c (Ajay)

1,000

May. 15

To Cash A/c (Vijay)

2,500

May. 25

To Cash A/c (Sanjay)

750

May .12

By Travelling expenses (Ajay)

1,000

May . 20

By Travelling expenses (Vijay)By Cash (Vijay)

2,000

500

May . 31

By Balance c/d (Sanjay)

750

4,250

4,250

Advance Account

Dr.

Cr.

(5) Reading of Capital Account:

Date Particulars Amt(Rs.)

Date Particulars Amt(Rs.

)

2010 2010Mar . 5

To Bank Drawings A/c

5,000

Mar . 15

To Drawings (Goods)

3,000

Mar . 31

To Balance c/d

67,000

Mar . 1

By Balance b/d

49,000

May. 20

By Interest

2,000

Mar. 31

By Profit & Loss A/c

24,000

75,000

75,000

Capital Account

Dr.

Cr.

CONCLUSION

THANK YOU