Reading 1: Introduction and Structural Overviewblsa.uchicago.edu/2009.2010.outlines/Income Tax...

153

Themes and Big Questions 1) What should we tax? Some general considerations: a) Is this regressive/progressive? b) What does a tax on X incentivize? c) Bigger base lower rates; narrower base higher rates d) Obvious tax easier to avoid (consumption tax only) e) Hidden tax people don’t worry about it as much (VAT) f) Horizontal v vertical equity 2) The tax code affects basically everything a) Big economic pictures and questions b) American suburban life is driven by the tax code – subsidies for gasoline and owning your own home make suburb living possible c) Structure of corporate deals is driven by this (think tax-shelters) d) State and local funding issues (municipal bonds) 3) Distinguishing between: a) Gain or loss, realization, recognition, capital gains? Introduction 4) History: a) First income tax created during Civil War, but repealed after the war, and tariffs were used instead. b) Another income tax was passed in 1894 (Cleveland’s second term) after much struggle. Tax was on only those people with a certain level of income, so it basically amounted on a tax of the rich. c) Pollock v. Farmers’ Loan & Trust Co. (SCOTUS, 1895) – declared the tax invalid, in part because it was in essence a tax on property, and as such was not levied on states in proportion to population, hence it violated the prohibition on unapportioned direct taxes in Art I § 9 cl 4 of the constitution. d) 16 th amendment, 1913: “The Congress shall have the power to lay and collect taxes on incomes, from whatever source derived, without apportionment among the several States, and without regard to any census or enumeration.”

Transcript of Reading 1: Introduction and Structural Overviewblsa.uchicago.edu/2009.2010.outlines/Income Tax...

Themes and Big Questions1) What should we tax? Some general considerations:

a) Is this regressive/progressive?b) What does a tax on X incentivize?c) Bigger base lower rates; narrower base higher ratesd) Obvious tax easier to avoid (consumption tax only)e) Hidden tax people don’t worry about it as much (VAT)f) Horizontal v vertical equity

2) The tax code affects basically everythinga) Big economic pictures and questionsb) American suburban life is driven by the tax code – subsidies for gasoline and

owning your own home make suburb living possiblec) Structure of corporate deals is driven by this (think tax-shelters)d) State and local funding issues (municipal bonds)

3) Distinguishing between:a) Gain or loss, realization, recognition, capital gains?

Introduction4) History:

a) First income tax created during Civil War, but repealed after the war, and tariffs were used instead.

b) Another income tax was passed in 1894 (Cleveland’s second term) after much struggle. Tax was on only those people with a certain level of income, so it basically amounted on a tax of the rich.

c) Pollock v. Farmers’ Loan & Trust Co. (SCOTUS, 1895) – declared the tax invalid, in part because it was in essence a tax on property, and as such was not levied on states in proportion to population, hence it violated the prohibition on unapportioned direct taxes in Art I § 9 cl 4 of the constitution.

d) 16th amendment, 1913: “The Congress shall have the power to lay and collect taxes on incomes, from whatever source derived, without apportionment among the several States, and without regard to any census or enumeration.”

e) Tax Reform Act of 1986 reduced the maximum marginal rate to 28%, but there are ways of getting around this by certain “penalties.”

5) Percentage of federal revenue as taxes:a) 1913: 2%b) WWI: 20%c) New Deal: 5%d) WWII: 40%e) After WWII: 18-19%

i) Essentially no changes since here. Clinton pushed it above 20% a bit. Bush brought it back down to historic level of 18-19%.

ii) Unless we can somehow decrease Medicare and Medicaid expenses, however, we need to get more money from somewhere.

6) How do you figure out how much tax you owe?a) Basic definitions:

i) Gross income

ii) Exclusions – things that theoretically could be in gross income, but are not. iii) Deductions – subtractions from gross income. Our tax code breaks these up

into two pieces because we want to treat the below-the-line ones differently. This different treatment is done in two ways. First, you can get a standard deduction (this year $10,700 for married jointly). Second, as your income goes up, itemized deductions are phased out. Where something fits in (above or below), matters. For instance, charitable donations are below the line. This matters, because you can’t get a deduction for them unless you itemize, which mostly only rich people do. So non-rich people who give to charity don’t get a deduction for it.(1) Above-the-line: mostly production-related expenses, like moving expenses

incurred for a job(2) Below-the-line:

(a) Standard (b) Itemized

(3) Note: exclusions and deductions are effectively the same thing.b) General Process:

i) Calculate your gross income (§ 61). Things that don’t go into your gross income are called exclusions. They never even make it into the calculation of gross income.

ii) Subtract the amount of above-the-line deductions (§ 62). The result is adjusted gross income. Note that above-the-line deductions are functionally the same as exclusions. Exclusions are never included, atl deductions are included, then subtracted.

iii) Next, do one of the following:(1) Subtract standard deductions (§ 63(c)), or(2) Subtract the below-the-line (itemized) deductions (§ 63)

(a) Calculate gross amount of allowable itemized deductions(b) Subtract from that calculation the lesser of the following two:

(i) 2% of the amount by which the income exceeds and inflation-adjusted threshold of $100k

(ii) 80% of the gross amountiv) Subtract personal exemptions (§ 151). The result at this point is taxable

income. Calculating personal exemptions is a two-step process.(1) Multiply personal exemption amount by the appropriate number of people.(2) Reduce that amount by 2% for each $2500 by which AGI exceeds an

inflation adjusted threshold of $100k.v) Apply the appropriate tax rate schedule to TI. If this TI includes capital gains

(§ 1222(11)), then apply the proper rate to them. At this point, you have amount of tax owed.

vi) Subtract any credits from the previous step, to get total liability.7) After Tax Income: The after tax income tells us something about what the tax system

is doing, but for that matter, even the pretax amount in a sense is affected by the tax system, because if you know how the tax system will affect your income, it might change how much work you do, or what type you do.

8) Average and marginal tax rates

a) What does average tell us about? Average tells us who’s paying what. These show us about progressivity.

b) What does marginal tell us about? Marginal rates are important because they tell us about behavior. Marginal tax rate is the rate that applies to the next dollar of income earned. They are not in general equal to average rates. What are my incentives to earn the next dollar? Marginal rates have nothing to do with progressivity. Deduction phase-outs are used (ex in § 151) to increase (effective) marginal rates beyond the maximum 28%. Disallowing deductions increases the taxpayer’s taxable income, and hence, tax liability.

c) Was a time when marginal rate was 90%. People sometimes looked to this as really socking the rich, but that wasn’t true. There were ways the rich could avoid this. The marginal rate is now much, much lower, but the progressivity of the tax is much stronger, because now the base is much broader—that is, the rich can’t avoid the tax as easily. So even though marginal rates are lower, the progressivity is higher.

9) Sources of authoritya) Constitution – 16th amendment as a response to Pollock, allows income tax based

not on number of people b) Congress responded within months to pass IRC. IRC divided into sections. Courts

can’t overturn these laws unless they’re unconstitutional, but that’s never really an issue.i) Who interprets the code?

(1) Primary interpreter is the agency delegated to do so—treasury department. IRS is part of treasury. Treasury issues regulations. Under Chevron, these regs generally have the force of law.

(2) Lots of courts can interpret the code, which makes being a tax litigator complicated, because it involves choice of forum.

c) Revenue Rulings. These are essentially baby fact patterns with a holding and an explanation. These have no authority . . . if you don’t like it. If you like it, you can rely on it. The IRS won’t go against its own ruling. But if you don’t like it, you can challenge it and win . . . you’ll be stuck on audit, though. We won’t deal with these much.

d) Private Letter rulings. No binding authority. Can go to IRS and get the results from a fact pattern. They’ll sometimes give you a document with results. They’re bound by it, but no one else is, and no one else can cite it for anything, even if their fact-pattern is exactly the same.

10) Some basic theory:a) “Ability to pay” – term used to describe the attribute that might justify requiring

some people to pay more tax than othersi) What does this term even mean?

(1) Narrow view – convenience in paying, such as holding liquid assets(a) Problem: this incentivizes unliquidating your assets.

(2) Broad view – look to economic well-being(a) Problem: what does this encompass? It’s hard to measure.

(3) Broader view – look at person’s underlying wage rate, the rate at which you could earn money

(a) Problem: What in the world does that mean?!ii) Assuming an agreed-upon definition of ability to pay, how do you implement

it?(1) Income

(a) What is the definition of income?(i) Receipts less allowances for the costs of producing those receipts(ii) Sum of taxpayer’s consumption plus change in net worth, each

defined in terms of market value (Haig-Simons)(b) The statutory concept of “taxable income” is influenced heavily by the

notion of ability to pay and its implementation via the notion of “income.”

(2) Consumption(a) Andrews – consumption tax is just an income tax with a deduction for

savings; that is, what of your income you don’t consume (savings), isn’t taxed (deduction)

(3) Wealthb) Tax Expenditure Budget

i) Concept is that all is taxable, and the deductions the government allows are viewed as government expenses (since you are exempted from paying tax on X, the government loses that $, so it’s an expense to them), and hence the $ must be included in the budget.

ii) The tax expenditure budget depends on the notion that there is a natural, neutral, or normal income tax and that it is possible to identify departures without great difficulty or dissent.

iii) This is a valuable tool in exposing tax policy issues.c) Tax incidence – the ultimate burden; who really is burdened

i) Ex: tax incidence on production of refrigerators probably falls on the customers of refrigerators, not on the manufacture; higher prices to customer

d) Taxable unit – the individual or group that is being taxedi) Married people

(1) May file jointly or separately(a) Married single-earner couples are better off than they’d be under a

system with one schedule(b) Married couples with two incomes may face marriage penalty;

marginal rates for second earner are key hereii) Heads of householdsiii) Unmarried individuals

11) Compliance and Administrationa) No statutory limit on civil penalties; 6-year limit on criminal penaltiesb) Taxpayer must pay interest on all underpaymentsc) Taxpayer must pay penalty on any underpayment due to negligence; penalty may

be waived if taxpayer can show good faithd) Taxpayer is generally entitled to the benefit of the doubt in a close call; taxpayer

may further undercut government’s basis for asserting fraud by “red flagging” something on their return

e) Mistakes

i) Error becomes evident after report filed – correct in next year’s returnii) Plain error in time of reporting – file an amended return

f) Judicial reviewi) Tax court – available only if tax hasn’t been paid as of date of petition

(1) No jury trials(2) Reviewable by fed circuit court of appeals, and ultimately by SCOTUS (3) These are article III courts; judges have 15 year appointments

ii) Pay tax and sue for refund in fed district court, appeals to regular circuit courtiii) Pay tax and sue for refund in US Court of Federal Claims, appeals to federal

circuitiv) Note: if you don’t want to pay the tax before contesting, you have to go to the

tax court12) Related Code

a) § 1 – Tax rate schedulesi) § 1(a) – Married individuals filing joint returns and surviving spousesii) § 1(b) – Heads of householdiii) § 1(c) – Unmarried individuals (other than surviving spouses and heads of

household)iv) § 1(d) – Married individuals filing separate returnsv) § 1(e) – Estates and trustsvi) § 1(f) – phaseout of marriage penalty for 15-percent bracket; bracket

adjustments for inflation(1) § 1(f)(1)-(7) basically talk about how to adjust for inflation, how to use the

CPI, how to round, etc.(2) § 1(f)(8) – elimination of marriage penalty in 15-percent bracket; the way

it was before 2003, the 15% bracket for unmarried individuals was more than half of the 15% bracket for married couples, so the unmarried people got to include a higher proportion of income in the lowest bracket; this fixes that

vii)§ 1(h) – maximum capital gains rateb) § 11 – tax on corporations

i) § 11(a) – corporate incomes are taxableii) § 11(b) – four corporate tax brackets

c) § 62 – definition of adjusted gross incomei) § 62(a) – adjusted gross income is, for an individual, gross income minus

allowed deductions, which include:(1) § 62(a)(1) – trade and business deductions attributable to a trade or

business carried on by the taxpayer, if not consisting of the performance of services by the taxpayer as an employee (basically these are the costs of producing business income)

(2) § 62(a)(2) – certain trade and business deductions of employees(a) § 62(a)(2)(A) – reimbursements to employees(b) § 62(a)(2)(B) – expenses of performing artists(c) § 62(a)(2)(C) – expenses of officials(d) § 62(a)(2)(D) – expenses of elementary and secondary school teachers

for certain years

(e) § 62(a)(2)(E) – expenses of US armed forces reserve members(3) § 62(a)(3) – losses from sale or exchange of property(4) § 62(a)(4) – deductions attributable to rents and royalties(5) § 62(a)(5) – certain deductions of life tenants and income beneficiaries of

property(6) § 62(a)(6) – pension, profit-sharing, and annuity plans of self-employed

individuals(7) § 62(a)(7) – certain retirement savings(8) § 62(a)(9) – penalties forfeited because of premature withdrawal of funds

from time savings accounts or deposits(9) § 62(a)(10) – alimony (10) § 62(a)(11) – reforestation expenses(11) § 62(a)(12) – certain required payments of supplemental

unemployment compensation benefits(12) § 62(a)(13) – jury duty pay remitted to employer(13) § 62(a)(14) – deduction for clean-fuel vehicles and certain

refueling property(14) § 62(a)(15) – moving expenses(15) § 62(a)(16) – archer MSAs(16) § 62(a)(17) – interest on education loans(17) § 62(a)(18) – higher education expenses(18) § 62(a)(19) – health savings accounts(19) § 62(a)(20) – costs involving discrimination suits

ii) § 62(b) – specifics regarding qualified performing artistsiii) § 62(c) – exceptions not treated as reimbursement arrangementsiv) § 62(d) – definitions re: education stuff (educator, school)

d) § 63 – taxable income definedi) § 63(a) – generally, it means gross income minus deductions allowed by this

chapter, other than standard deductionii) § 63(b) – if you don’t itemize deductions, taxable income is adjusted gross

income minus the standard deductions and minus the deduction for personal exemptions provided in § 151

iii) § 63(c) – standard deduction(1) § 63(c)(1) – “standard deduction” is the sum of the basic standard

deduction and the additional standard deduction(2) § 63(c)(2) – “basic standard deduction” defined(3) § 63(c)(3) – additional standard deduction for aged and blind(4) § 63(c)(4) – inflation adjustments(5) § 63(c)(5) – limits on basic standard deduction for certain dependents, if

that dependent is claimed by another(6) § 63(c)(6) – people not eligible for standard deduction

iv) § 63(d) – “itemized deductions” definedv) § 63(e) – election to itemize

(1) § 63(e)(1) – must elect to itemize, or nothing gets itemized(2) § 63(e)(2) – must elect to itemize on the tax return(3) § 63(e)(3) – ways to change election after filing of the return

vi) § 63(f) – aged or blind additional amountsvii)§ 63(g) – marital status determined under § 7703

e) § 67 – 2% floor on misc itemized deductionsi) § 67(a) – misc itemized deductions allowed for individual only if they exceed

2% of adjusted gross incomeii) § 67(b) – “miscellaneous itemized deductions” defined (stuff relating to

interest, taxes, charitable contributions, medical expenses, impairment-related work expenses, etc.)

iii) § 67(c) – disallowance of indirect deduction through pass-thru entityiv) § 67(d) – definition of “impairment-related work expenses”

f) § 68 – overall limitation on itemized deductionsi) § 68(a) – if individual’s adjusted gross income exceeds applicable amount,

itemized deductions are reduced by the lesser of(1) § 68(a)(1) – 3% of excess of adjusted gross income over applicable

amount(2) § 68(a)(2) – 80% of amount of itemized deductions otherwise allowable

ii) § 68(b) – definition of “applicable amount”; adjusting for inflationiii) § 68(c) – exception for certain itemized deductionsiv) § 68(d) – this section shall be applied after the application of any other

limitation on the allowance of any itemized deductionv) § 68(e) – this section doesn’t apply to any estate or trustvi) § 68(f) – phaseout of limitation, certain yearsvii)§ 68(g) – this section doesn’t apply to years after 2009

g) § 151 – allowance of deductions for personal exemptionsi) § 151(a) – “In the case of an individual, the exemptions provided by this

section shall be allowed as deductions in computing taxable income.”ii) § 151(b) – exemption amount for taxpayer, and for spouse if a) no joint return

filed and b) if spouse has no gross income and is not the dependent of another taxpayer

iii) § 151(c) – exemption amount for each dependentiv) § 151(d) – exemption amount

(1) § 151(d)(1) – definition of “exemption amount”(2) § 151(d)(2) – when there’s a disallowance of the exemption amount for

certain dependents(3) § 151(d)(3) – phaseout stuff, involving percentage to reduce by, threshold

after which to reduce, etc.(4) § 151(d)(4) – inflation adjustments

v) § 151(e) – “No exemption shall be allowed under this section with respect to any individual unless the TIN (taxpayer identification number) of such individual is included on the return claiming the exemption.”

Fringe Benefits: Valuation Problems13) What constitutes income?

a) Old Colony Trust Co. v. Commissioner (1929, p. 41) – employer’s payment of federal income taxes on behalf of its employee constituted income to the employee; this case preceded income tax withholding

b) Benaglia v. Commissioner (1937, p. 42)i) Summary: free room and board that a hotel manager and his wife (who filed

taxes jointly) got from his employer were not considered as incomeii) Reasoning:

(1) “From the evidence, there remains no room for doubt that the petitioner’s residence at the hotel was not by way of compensation for his services, not for his personal convenience, comfort or pleasure, but solely because he could not otherwise perform the services required of him.”

(2) Residence at the hotel was necessary(3) Not income just because it relieves employer of an expense he’d otherwise

bear(4) Key language: “The advantage to him was merely an incident of the

performance of his duty, but its character for tax purposes was controlled by the dominant fact that the occupation of the premises was imposed upon him for the convenience of the employer.”

iii) Dissent:(1) First of all, there’s evidence that this manager could do his job without

having to live there, so there’s something wrong.(2) Second, contractual language indicates this was bargained for, understood,

and intended as compensation for employment(3) Solely for employer’s convenience does not imply that employee wasn’t

benefited to the extend that it’s income . . . “I do not think the question here is one of convenience or of benefit to the employer. What the tax law is concerned with is whether or not petitioner was financially benefited by having living quarters furnished to himself and wife.”

(4) This was a mutual beneficial arrangement.iv) Class Discussion:

(1) Is this result here right?(a) What facts point to the convenience of the employer?

(i) This is a 24-hour a day job.(ii) Condition of employment – wouldn’t take job if couldn’t live

there.(iii) Forced

consumption. Rather than giving employee extra cash, the employer forces Benaglia to consume a certain residence.

(b) What can dissent use?(i) Not really necessary to live there(ii) Doesn’t need a suite(iii) It’s bargained for(iv)Sure, it’s convenience to employer, but it’s a big benefit to

employee, too.(v) Reg says nothing about spouse, so at minimum half of the income

should be taxable . . . though this in 1937, so maybe different perceptions of wives at the time wouldn’t make this a winner.

(2) Notice that § 61 makes no distinction between cash and in-kind. So the problem here has nothing to do with the fact that this is in-kind.

(3) Notice if the IRS is going to tax this stuff, it has to do so right away. There’s not a “second chance” to tax this, as there might be for something like an annuity given to an employee. (Tax when given v. tax when $ withdrawn.)

(4) The test here is convenience of employer.(a) Isn’t salary convenient? Doesn’t the employer pay the employee

because it’s convenient to have someone come and do stuff for him?(b) How helpful is that language? What does that mean? Possible tests:

(i) Business necessity (ex: Navy must provide food and housing, b/c you can’t get it otherwise in the middle of the ocean)1. What goes against this here is that Benaglia is away for some

times . . . so is it really necessity?(ii) Forced consumption. Did the employee have a choice?

“Convenience of the employer” gets to this idea, a bit. It indicates the method of payment might not be the employee’s first choice, and so we take account for that a bit.1. How much should someone be taxed for forced consumption?

a. The law – 0b. IRS – fair market value; probably overestimates valuec. Another option – subjective value; this is completely

accurate, but this is impossible to administer, and people will just underestimate . . . “oh, I really hate gorgeous, luxurious hotels . . . staying there was worth about $1/day to me”

(5) See § 119 (“Meals or lodging furnished for the convenience of the employer) for modern-day handling. Exclude meals/lodging from GI in given to him, spouse, or any dependents by or on behalf of the employer “for the convenience of the employer,” but only if:(a) § 119(a)(1): “meals are furnished on the business premises,” or(b) § 119(a)(2): lodging . . . “employee is required to accept such lodging

on the business premises of his employer as a condition of his employment”

(6) § 119, though, doesn’t fix everything. It contains many ambiguous terms that subsequent decisions disagree over. See pp. 47-48: (a) What is a “meal”? Groceries? No – Tougher v. Commissioner. Yes –

Jacob v. United States. (b) What does it mean to “furnish”? Is giving cash for meals furnishing a

meal? No – Commissioner v. Kowalski (cash for cops to buy food). But yes, for a fireman to deduct $ paid to participate in an obligatory organized mess at the station house – Sibla v. Commissioner.

(c) What is “convenience of the employer”? Often established by proof that the employee is on call outside of business hours.

(d) What are the “business premises”? Roads and highways are included for state police – US v. Barrett. House across the street from beachfront hotel included – Lindeman v. Commissioner.

(e) Examples from class:

(i) NJ state trooper gets $20/day meal allowance. Maybe on business premises, but the meal isn’t furnished by the employer, they just give you cash. SCOTUS held this not furnished, but didn’t decide what premises were. But later, something decided premises were basically everything.

(ii) Waiter at a restaurant. Give you breakfast when you have an early shift. It’s on premise, furnished. What about convenience of employer? Does it matter if there’s a Starbucks next door? Breakfast is harder to order convenience. Just get up a half an hour earlier. Lunch is easier, especially if you have a restricted time in which to eat . . . regs actually talk about this.

(iii) Lunch provided by law firm. On premises and furnished are easy. What about convenience? Make an emergency argument . . . if something comes up, you’re there. Might be convenient to have law firm cafeteria because you can talk about client info in a secure place. No confidentiality worries.

(iv)Happy hours at work? Probably not a meal, so not excludable.(v) Hospital provides bed for doctors in hospital? Yes. What if the

room provided is at a hotel right across the street? Convenience is there, required to accept is there. But it’s not on the business premises. Need to argue that the hotel is your premises. Maybe if you have a standing agreement with the hotel, you can do this.

(7) If you make something tax free, you’ll incentivize people to do more of it than they normally would. (Free parking example on p. 57. If you give people free parking, then maybe more people will drive to work than really want to do so.)

(8) Source of authority is Regulation 1.119-1. This reg requires two inquiries:(a) Furnished on premises? Factual determination. (b) Furnished for convenience?

(i) Substantial non-compensatory business reason convenience.(ii) Furnished so employee is available for emergency convenience.(iii) Mostly as

additional compensation no convenience.(iv)Meal before or after work, or non workday no convenience.(v) Restricted meal time convenience.(vi)Insufficient eating places nearby convenience.

(9) See handout 5 for some specific numbers that show how different rules (FMV, subjective, excluded) allocate $ differently.

c) Arguments for deciding how much to taxi) Efficiency argument

(1) Free parking example on p. 57(a) Cost to employer of parking is $50; employee values it at $40(b) No tax – employee wants $50 cash; in fact, can make a deal with

employer, because any amount of cash between $40 and $50 makes both better off than providing the free parking

(c) Both cash and parking are taxed (at 40%) – if we value the parking at $50, benefit to employee is $40 minus 40% of $50, which is $20; if we value the parking at the subjective value of $40, then the benefit to employee is $40 minus 40% of $40, which is $24 . . . either way, these are lower than $50 cash minus tax of $20, which yields $30.

(d) Only cash is taxed – here value of parking is $40, and value of taxed cash is $30, so employee chooses parking

(e) Schoup article on p. 58 notes that tax system can create too much of something people didn’t really want to begin with. Here, we might end up with more people driving into cities than would normally occur, because parking is tax free. Relating this to Benaglia, if we favor him by not requiring tax on the room/food he gets, then what we might get is too many people going to work for fancy hotels, then maybe too many fancy hotels open up, and then this trickles through the economy and skews it. We see this in health insurance. (p. 56)

(2) Fairness argument(a) Horizontal equity/fairness

(i) Take two people, A and B. Assume a 40% tax rate.1. A gets $15k per year. Pays $6k in tax.2. B gets $10k per year, plus $5 for housing. If housing isn’t

taxed, pays $4k in tax. (ii) Fairness argument says: why should B get off with lower taxes

than A? (b) Vertical equity/fairness

(i) Unfair to let fringes be tax-free, because this benefits those people who are more highly compensated. This manager is benefited, whereas the maid who doesn’t get fringe benefits such as free housing doesn’t enjoy any tax benefit. This may end up imposing a level of regressivity.

(ii) Another way to conceive this is that tax free stuff is more valuable to the wealthy, because their marginal tax rate is (most likely) higher.

(3) Administrability(a) Fairness and efficiency arguments argue for taxing. This one does not. (b) Classic example in book by Henry Simons (UofC law prof in 20s) is

an attendant to a prince. What does the attendant have to do? Go with the prince and take care of him. Goes to the opera, horseback riding, vacationing, etc. Does all the luxurious things. But in Simons example, he would really just prefer a burger and a football game. But it’s his job to be fancy. Should he be taxed on these benefits? If yes, how do we value it? Obvious analogies in the current world: rock star, sports hero.

(c) Things like satisfaction from job are super-hard to tax. What about more mundane stuff . . . what about President of the United States . . . tax the fact that he has free housing? What about an associate who gets

a three-martini lunch? What about the navy guy who gets a cot on a destroyer? What about a foxhole while in army?

(d) The common thread through these things is that they are mixed-use. They have a business purpose, even things like three-martini lunches, but they also have independent consumption value.

d) Valuation of fringe benefitsi) Basic valuation rule is “fair market value” (Regs § 1.61-21(b)

(1) “In general—An employee must include in gross income the amount by which the fair market value of the fringe benefits exceeds the sum of . . . [t]he amount, if any, paid for the benefit by or on behalf o f the recipient, and . . . [t]he amount, if any, specifically excluded from gross income by some other section of subtitle A of the IRC of 1986.”

ii) Optional safe-harbor rates applyiii) Cafeteria plans – allow employee to choose an excludable benefit (maybe

parking benefit) or opt out for a taxable amount of cash; (1) These are expressly authorized by § 125(2) § 125(d)(2)(A) is the use it or lose it rule – the book says this, thought I

don’t totally see it from the language; the idea is that if you take $5X worth of some benefit at the beginning of the year, and don’t use it all, you don’t get the difference back; think of pre-tax withholding of money for healthcare

e) § 132 – Certain fringe benefitsi) Historical background: for years, tax rates were very low, and the IRS just

didn’t bother enforcing a lot of these small items. So lots of fringes were historically excluded, and this continued to be the case after WWII even after taxes went up a bit. Coming into the 70s and 80s, there’s a long history of things’ being excluded from people’s earnings. They were a pattern of American life, and so the IRS/Congress couldn’t just go back and include these things. So they just tried to codified it, and put some clear boundaries on things. So many of these exclusions aren’t there for some efficiency/policy reason, but based only on history and tradition.

14) Related Codea) § 61 – gross income defined

i) § 61(a) – “Except as otherwise provided in this subtitle, gross income means all income from whatever source derived, including (but not limited to) the following items:”(1) Notice that this defines gross income as basically everything, and then

stuff is excepted. So the default is inclusion. (2) § 61(a)(1) through § 61(a)(15) includes things like compensation, fringe

benefits, gross income derived from business, gains from dealings in property, interest, rents, royalties, dividends, alimony, annuities, life insurance, endowments, pensions, income from discharge of indebtedness, distributive share of partnership income, income in respect of a decedent, and income from an interest in an estate or trust

b) § 119 – meals or lodging furnished for the convenience of the employer

i) § 119(a) – gross income doesn’t include food or lodging given to employee by employer if its one of the following(1) § 119(a)(1) – “meals are furnished on the business premises of the

employer” (Note: no requirement that you eat it)(2) § 119(a)(2) – “employee is required to accept such lodging on the business

premises of his employer as a condition of his employment”ii) § 119(b) – special rules

(1) § 119(b)(1) – K terms aren’t determinative of whether meals or lodging are intended as compensation; that is, you can’t just say in a K, “this has been bargained for” and that’s that, or vice versa

(2) § 119(b)(2) – in deciding what’s deductible, don’t take into account whether a charge was made for the meals or whether the employee may decline the meals

(3) § 119(b)(3) – if employee is required to pay on periodic basis a fixed charge for meals, and they are furnished for employer convenience, they aren’t included

(4) § 119(b)(4) – served on business premises are treated as furnished for employer convenience if more than half of employees who get the meals are given the meals for the employer’s convenience

iii) § 119(c) – stuff about living in campsiv) § 119(d) – stuff about food and lodging provided by educational institutions

c) § 132 – certain fringe benefitsi) § 132(a) – those excluded from gross income

(1) § 132(a)(1) – no-additional-cost services (offered to customers in ordinary course and line of business, no substantial additional cost)(a) What’s the purpose of taxing something that’s costless? It just

incentivizes waste. Why not use that empty airline seat?(2) § 132(a)(2) – qualified employee discounts

(a) Has to be stuff employer regularly sells; employer can’t lose $ on it(3) § 132(a)(3) – working condition fringe (if you could deduct it yourself,

and employer gives it to you for free, it’s excluded)(4) § 132(a)(4) – de minimis fringe (so small accounting for it is silly)(5) § 132(a)(5) – qualified transportation fringe(6) § 132(a)(6) – qualified moving expense reimbursement(7) § 132(a)(7) – qualified retirement planning services(8) § 132(8) – qualified military base realignment and closure fringe

ii) § 132(h) – certain individuals are treated the same as employees for purposes of subsections (a)(1) and (2): people retired from the co, spouses of deceased employees, spouses and dependent children of company workers, and a special rule for parents with the airline industry

iii) § 132(i) – ok to have reciprocal agreements with other employersiv) § 132(j)(1) – can’t make special exceptions only for highly-compensated

employees; must be available in general to all

Gifts and Disguised Compensation15) Basics of gifts

a) § 102(a) exempts from incomeb) Probable that transferor is in higher bracketc) Gifts from employer to employee become profitable over salary when the

employee’s marginal rate exceeds the employer’s marginal rate. For some numbers, see handout 6.

16) Commissioner v. Glenshaw Glass (1955, p. 70)a) Summary: punitive damages from antitrust suits count as income under then § 22

(now § 61)b) Reasoning:

i) § 22 (current § 61) uses extremely broad language (“gains or profits and income derived from any source whatever”) to exert “the full measure of its taxing power”.

ii) Court has given a liberal construction to this phrasing, and has applied no limitations except to those specifically exempted.

iii) Why exclude punitive, when not compensatory damages? No logical reason.iv) Court distinguishes Eisner v. Macomber, because in that case (considering

whether dividend was a realized gain to stockholder or changed only the form, not the essence, of the stockholder’s holdings) the court was distinguishing gain from capital. Note that there was a little bit of a difference of income definition in Eisner, where the language used was “the gain derived from capital, from labor, or from both combined.”

v) “Here we have instances of undeniable accessions to wealth, clearly realized, and over which the taxpayers have complete dominion.”

c) Class discussion:i) How would you define income after this case? “undeniable accession to

wealth” is a good place, probablyii) How can we apply this rule to some other examples, like those we went over

in fringe benefits?(1) Quiz show prizes.

(a) What if you win 1,000,000 Snickers bars? Under Glenshaw this is income. How might you argue based on our fringe benefits case that it’s not. The contestant probably didn’t really want this. This is forced consumption. There are also valuation problems. You can’t possibly consume all these before they go bad, can you? Are they liquid assets?

(b) What if you win a car with insane options that you never would pay for yourself? Same arguments as above.

(2) Oscars.(a) If you win an Oscar, you get a goody bag that can be worth many

thousand dollars. One of the things you get is invitations on cruises. And as a celebrity, you can’t really go on these cruises. The IRS actually sent out a memo specifically warning Oscar winners that their prizes are taxable, and they’d be prosecute. What can the celebrity do? Might be able to donate it to charity. But otherwise, probably stuck. Also, probably can’t just deny this, because that’d be bad for publicity.

(3) Home Run Ball.(a) IRS said, if you do anything but get cash for it, it’s not taxed.

(b) If you sell it, and get the $1mill, then it’s taxable.(c) It seems here that the IRS just made an exception because of things

like traditions of baseball.(4) Oprah’s cars.

(a) After she gave cars, the IRS told her she had to send tax forms to all the people, because the cars are taxable. Later she sent money to all the people to cover the tax.

17) Gifts are clearly going to be an exception to Glenshaw glass. But what is a gift? § 102 doesn’t really define it. We just have a little idea. Is it only within the family? Probably not. Can be generous to other people, too. But how do we tell? Don’t want to count salary as a gift. But where to draw the line?a) Commissioner v. Duberstein (1960, p. 75, SCOTUS)

i) Summary: this decisions combines two cases, Duberstein and Stanton(1) Duberstein – Duberstein gave Berman some very helpful information that

got Berman lots of business from some customers; Berman thanked Duberstein with a Cadillac; Duberstein didn’t include it as income, calling it a gift; Duberstein was basically forced to take the car; Duberstein admitted Berman wouldn’t have given it without the info Berman got re: the customers; Berman deducted the car as a business expense

(2) Stanton – upon resigning, Stanton got a gratuity from his company that was to release any pension, etc. obligations the company might have to him, and it was also given “in appreciation of the services rendered by Mr. Stanton”; “we were all unanimous in wishing to make Mr. Stanton a gift”; there’s dispute as to whether this is gift or some sort of severance pay

ii) Issue: Are these things gifts, and hence not included as income by their recipients?

iii) Holdings:(1) Duberstein – SCOTUS reverses the appeals court, and reinstates the trial

court’s decision that this was not a gift, it is income to Duberstein; SCOTUS didn’t see anything clearly erroneous with trial court’s facts(a) Note: trial was in tax court(b) Good general rule: treat things symmetrically. If you allow it tax free

on one side, you can’t allow a deduction on the other side. So we can’t both allow Duberstein to take tax free as a gift, and for Berman to deduct as a business expense.

(2) Stanton – trial court found this to be a gift, appeals court reversed, SCOTUS remanded because weren’t enough factual findings done by trial court(a) Note: trial was in federal district court; tax lawyers generally think that

the district court judges are easily duped(b) Weisbach finds this completely bogus. This is money given for past

services, so it’s got to be income. (c) If this were decided today, § 102(c) says that it’s definitely taxable,

because you can’t “exclude from gross income any amount transferred by or for an employer to, or for the benefit of, an employee.”

iv) Reasoning (Brennan):

(1) Go case-by-case and look at donor’s intent.(2) When considering whether something is a gift, you have to look to the

transferor’s intent, not the transferee’s intent.(3) Government wanted to promulgate a new test to help determine whether

something is a gift. SCOTUS rejects this invitation. These cases are basic examples of when payments are made in a context with business overtones, and so we can just review similar cases that are on point to this pretty common situation.

(4) To figure out what gift means, we need to consider it in a colloquial sense.(5) Old Colony Trust v. Commissioner – mere absence of a legal or moral

obligation to make a payment doesn’t mean it’s a gift (employer paid employee’s tax burdens; this was included in employee’s income)

(6) Bogardus v. Commissioner – if the payment proceeds primarily from the constraining force of any moral or legal duty, or from the incentive of anticipated benefit of an economic nature, it’s not a gift; the most critical consideration is the transferor’s intention(a) Doesn’t moral duty encompass a lot? Couldn’t you say that giving

Christmas presents to your kids comes from a moral duty? Is that taxable, then?

(7) What the parties hope the tax treatment will be has nothing to do with it.(8) The conclusion whether a transfer amounts to a gift is one that must be

reached on a consideration of all the factors. Because of this, we have to give major deference to the trial courts. We won’t make a more precise and tidy definition here. Congress can do that if it so desires. But now, we must go case-by-case, and as such, appellate review should be quite restricted.

v) Frankfurter’s Dissent:(1) “business implications are so forceful that I would apply a presumptive

rule placing the burden upon the beneficiary to prove the payment wholly unrelated to his services to the enterprise”

vi) Class discussion:(1) Are these gifts?

(a) Tip you give to a server in a restaurant, and you know you’ll never be in the restaurant again. Not a gift, because it’s given for past services due. But can make a clever argument that it’s a gift. Recall, it’s the donor’s intent. What if they feel as though they’re just being nice, and they don’t have to give it. Does that mean not taxable?

(b) Strike benefits. Seems like it is income. May have a bit of an issue with where this money comes from. If it’s from union dues, and you already paid some union dues in. You’ll likely be taxed on whatever you get back that exceeds the amount you paid in.

18) Related Codea) § 102 – gifts and inheritances

i) § 102(a) – General rule is that gifts aren’t income: “Gross income does not include the value of property acquired by gift, bequest, devise, or inheritance.”

ii) § 102(b) – gifts that are included in income include:

(1) § 102(b)(1) – income from any property referred to in (a) – if you give me land, and I rent it out, I have to include that rental income as income

(2) § 102(b)(2) – if the gift comes from income of property – I can’t give you $ from profits I make on land, and allow you to exclude it from income

iii) § 102(c) – gifts from/on behalf of employers aren’t excluded; there is a de minimis exception(1) Stanton would be different under this. It would come out the other way.(2) Example from book. If a surgeon saves your life, and you want to give her

a lavish gift—a ski trip—is the trip taxable?(a) Is the surgeon your employee? No. So § 102(c) doesn’t apply.(b) Weisbach says this language is extremely problematic, because it

draws the line between employer/employee, not just in relation to service providers in general. This case came up with Clinton’s first attorney general nominee. Was her nanny an employee? (i) What if your boss comes to your kid’s wedding, and gives your kid

a wedding gift. We don’t expect this to be taxed, but § 102(c) seems as though it can cover it. Weisbach says a strict reading of the language must cover it.

b) § 274 – disallowance of certain entertainment, etc., expensesi) § 274(b) – gifts

(1) § 274(b)(1) – if you give a gift of more than $25 to someone, you can’t deduct it; gift is defined as any item excludable from gross income of the recipient under § 102 non excludable any other provisions

(2) § 274(b)(2) – this limitation in part (b)(1) applies to partnerships and each member of the partnership; married people count as one taxpayer for these purposes

(3) Enacted in the 50s and the #s have never been changedii) § 274(j) – employee achievement awards

(1) § 274(j)(1) – “No deduction shall be allowed under § 162 or § 212 for the cost of an employee achievement award except to the extent that such cost does not exceed the deduction limitations of paragraph (2).”

(2) § 274(j)(2) – deduction limitations for employer who gives gift to employee

iii) § 274(n) – 50 percent of meal and entertainment expenses allowed as deduction. Example:(1) Employer

(a) Pays employee $90. Can deduct this as a salary expense.(b) Gets $100 for the widget made by employee.(c) Makes $10 profit.

(2) Employee(a) Gets $90.

(3) Total benefit here is $100 ($90 to employee, $10 to employer). So what we want to make sure happens is that $100 worth of stuff is taxed. How?(a) Employee got $90 benefit, so tax them on $90. Employer got $10

benefit, so tax them on $10.

(b) What if it’s really hard to tax the $90 given to employee? Maybe because that figure includes three-martini lunches, etc. Then just tax the $100 all at once when the $100 sale takes place. And so long as the tax rates are the same, the government gets the same. This is known as substitute taxation. This happens all over the tax code. § 274(n) does this (sort of) for three-martini lunches.

(c) Why the 50% only here? Recall this business meal is a split-use thing. There’s consumption value, and business value. So since access to the actual subjective values in each of these categories is basically impossible, Congress just drew a bright line and said half will be attributed to consumption value, so that’s the half that’s taxed. Used to be 20% or something.

(d) This section was highly influenced by restaurant lobby. Tons of $ is spent here each year.

The Concept of Gain and its Relation to Basis19) Introductory Comments:

a) Buying and Selling Stock Examplesi) Example #1

(1) 1/15/08 – you buy 10 shares of stock for $1,000(2) 2/15/09 – sell all 10 shares of stock for $1,250(3) What gets taxed and when? You’re taxed on the $250 gain at the time of

the sale.ii) Example #2

(1) 1/15/08 – you buy 10 shares of stock for $1,000(2) 2/15/09 – you sell 8 shares or $1,000(3) 2/15/12 – you sell 2 shares for $250(4) What gets taxed and when?

(a) Possibility 1 (no gain till basis is covered)(i) At 2/15/09, you get taxed nothing, because the amount realized is

the same as the basis ($1,000), so you haven’t “gained” anything yet.

(ii) At 2/15/12, you get $250 more, but have $0 left in the basis, so you gain $250 at this point, and are taxed on it at this point.

(iii) Note: this is good for seller, because taxes are delayed 3 years.

(b) Possibility 2 (no basis deduction till all is gone)(i) At 2/15/09, you get $1,000 gain (taxed then)(ii) At 2/15/12, you get -$750 gain (taxed [deduction] then)(iii) Total gain again of $250, but taxed differently(iv)Note: This is not as good for the seller, because the tax comes

earlier(v) Note: Something like this also allows for manipulation like that in

Gavit. How? If all of the basis is attached to a couple of stocks, you can then sell these stocks early and generate a huge loss

immediately that can cover future tax obligations. This is discussed more under Gavit.

(c) Possibility 3 (pro rata)(i) At 2/15/09, you receive $1000 for 80% of the original, so 80% of

basis is $800, so gain here is $200(ii) Similarly, at 2/15/12, your gain is $50(iii) Total gain is again $250(iv)Note: this is economically the most accurate, but things can get

harder to calculate when it’s not shares of stock, but instead is land or something like that (Inaja)

iii) Government prefers the third possibility above, taxing the gains as they are realized. They don’t prefer 2, because it allows for manipulation. People can create trusts (like in Gavit), then allow the people sell the remainder, and then realize a loss, and then essentially end up not paying taxes, because they have losses to distribute to their actual realized gains.

b) How is basis assigned in gifts?i) Gross income includes “gains from dealings in property” (§ 61(a)(3))

(1) How do you calculate the gain? The amount of the gain is the “excess of the amount realized . . . over the adjusted basis” (§ 1001).

(2) What is the adjusted basis? The adjusted basis is the basis, defined under § 1012 as “cost” (with certain exceptions), “adjusted as provided in section 1016.” (a) There is an exception in § 1015 for property acquired by gift.

ii) Donee’s basis (this phrase is used in § 1015, and it means the adjusted basis) is the same as the donor’s basis. So if A gives B a gift, B gets A’s basis. The donee takes a “transferred basis” from the donor (§ 7701(a)(43))(1) Exception: if at the time of the gift the donor’s basis is greater than the fair

market value of the property (so the donor would have a loss if he or she sold the property), then for purposes of computing the donee’s loss (but not gain) on any subsequent sale, the donee’s basis is the fair market value at the time of the gift.

20) Taft v. Bowers (1929, p. 96)a) Summary: A buys stocks for $1000; value rises to $2000; A gives stocks to B; B

sells for $5000b) Issue: whether B should be taxed on the $3000 gain from $2000 to $5000 or the

$4000 gain from $1000 to $5000c) Holding: donee must pay tax on the whole $4000 differenced) Reasoning:

i) “the settled doctrine is that the Sixteenth Amendment confers no power upon Congress to define and tax as income without apportionment something which theretofore could not have been properly regarded as income”

ii) Case notes Eisner v Macomber – “gain derived from capital, from labor, or from both combined”; so if you work for it or if you have it through investment. It also cites Phellis to explain what a “gain derived from capital” is: it is “not a gain accruing to capital, nor a growth or increment of value in the investment, but a gain, a profit, something of exchangeable value

proceeding from the property, severed from the capital however invested, and coming in, that is, received or drawn by the claimant for his separate use, benefit and disposal.”

iii) If we don’t do it this way, there’s $1000 gain that isn’t taxed, and this creates a loophole to avoid taxes. A’s basis is $1000 . . . if B’s is $2000, the $1000 in between isn’t taxed. Oh, you think this is unfair to B, because B didn’t really “experience” this gain? Then B doesn’t have to take the gift. “She accepted the gift with knowledge . . .” It basically just makes the gift not as good, that’s all, because there’s more tax to pay on it.

e) Class Discussion:i) The holding of this case is codified in § 1015 – “basis shall be the same as it

would be in the hands of the donor or the last preceding owner by whom it was no acquired by gift”; exception if basis is higher than FMV, in which case donee’s basis becomes FMV

ii) Some options here:(1) First – general rule, outside of gifts

(a) A pays tax on $1000, since the stocks gained $1000 in his hands(b) B pays tax on $3000, since the stocks gained $3000 in his hands(c) Total taxed is $4000(d) This is the most accurate, but it presents valuation problems (how

much was it worth when A gave it as a gift?), and also presents a liquidity problem (maybe A doesn’t have any money to pay the tax)

(2) Second – Taft v. Bowers rule(a) A pays tax on $0(b) B pays tax on $4000(c) Total taxed is $4000(d) This is the rule in Taft v. Bowers. Easy to administer, because just

value and tax on the sale, and don’t have to follow it all through any gift-giving stuff. Also, it’s not really unfair to the recipient. It just means the gift is less valuable, perhaps.

(3) Fourth – anti-Taft v. Bowers(a) A pays tax on $4000(b) B pays tax on $0(c) Total taxed still $4000(d) Seems a bit unfair, but it does close a loophole for evading taxes by

shifting the value to someone in a lower tax bracket. For instance, if A is the father in a higher tax bracket, and B is his daughter, he can give it as a gift to B, so she has to pay less tax. But this disallows that.

iii) Notice that here, the question is not whether to tax this appreciation while the donor held the stocks, but whom to tax. It would be administratively ridiculous to tax donor, and treat this like a sale.

21) Questions on p. 102a) A buys stock for $1k, gives to B when FMV is $2.5k.

i) B sells for $3.5k B recognizes $2,500 gainii) B sells for $1.5k B recognizes $500 gain

b) C buys stock for $2k and gives to D when FMV is $1k.

i) D sells for $2.5k $500 gainii) D sells for $1k $500 loss – note here, that since it’s a loss (transferred basis

> amount realized), FMV of $1000 is usediii) D sells for $1.5k $0 gain or loss. No gain or loss. This is the case whenever

the following holds: Original basis > price sold for > FMV. 22) Irwin v. Gavit (1925, p. 103)

a) Summary: Remainder of trust given to daughter; father gets the interest payments from each of the 15 years the trust pays interest till the daughter turns 21; father has to pay tax on the interest payments, daughter doesn’t on the receipt of the principal, because the basis attaches to what the daughter has, not what the father has. The father’s argument amounted to arguing that taxpayers could arrange to exempt from tax the income from property through the simple expedient of making “split gifts,” whereby one person gets a term or life interest and another gets the remainder interest.

b) Arguments:i) Both sides agree that granddaughter isn’t taxed. ii) Father: argues that the annual interest payments are also included in the gift,

and as such, shouldn’t be taxed. He should’ve argued that taxing him on the interest was undoubtedly incorrect, because he had a basis of $49,975.

iii) Gov’t: each time you get an interest payment, you still have the $100,000 amount in the trust, so these are earnings, and as such, are taxed

c) Class discussion:i) See handout folded up in my book.ii) Present Values of Gifts

(1) How much is granddaughter’s interest worth on the day her grandfather dies? Discounted value of $100k, which turns out to be $50,025.

(2) How much is dad’s interest worth on the day the grandfather dies? Discounted value of the interest payments. On the handout, this is the discounted value of 9 payments of $8,000.

iii) Tax advice for Marcia in the world of the holding of the case: Sell immediately, and recognize a loss. She’s got a basis of $100k for something worth $50,025, so she gets a $49,975 loss now, which is good for her. This might not matter for stuff like a family trust, since they might not be sellable, but the issue of a possible tax shelter is there. Also, she probably doesn’t have any tax liabilities, but it might help if she can carry those through into future periods. This advice for Marcia is basically a tax shelter. You can create one of these on your own through bond-stripping. You buy a bond, and sell the interest to person A, and sell principal to person B. If person B has all the basis (as Marcia did) he can sell immediately and get a loss.

iv) Amount taxed under either theory (giving Marcia all the $100k basis, or giving Palmer and Marcia each about $50k . . . ) is the same. The difference is in timing. Also, presumably Marcia is in a lower tax bracket when she turns 21 than the bracket her father is in right now. (1) Way 1: all basis for Marcia. What’s taxed? Each year of the nine years, the

$8k of interest the father gets is taxed. So that’s $72k taxed total.(2) Way 2: (basically) split the basis.

(a) Dad is taxed on $72k minus his $50k basis = $22k(b) Marcia is taxed on $100k minus her $50k basis = $50k(c) Total here is $72k again

(3) Way 3: Another way, if we think it’s unfair to make Marcia pay tax each year even though she doesn’t get any actual money, she just gets closer to getting real money, is to make her pay, once she gets the $100,000, the present value of the taxes she would have paid along the way.

(4) Notice: really what’s going on is that, no matter who we say owns what, each year this thing (the trust) is generating $8000 more money, and that’s what’s getting taxed. So if we say that all the basis is Marcia’s, then Dad has to pay all that tax. Or otherwise. Whatever. No matter how we split it up, we’re taxing the same amount.

v) We could tax Marcia each year on the amount she “gains.” She gains 8% each year, because she gets a little closer to realizing the $100,000, so the present value rises. We could tax her on that little gain. We could tax Dad on all of it, instead.

23) Inaja Land Co. v. Commissioner (1947, p. 107)a) Summary: taxpayer bought 1,236 acres of land on the banks of a river in CA for

$61k (this is his basis, because it’s his cost) for fly fishing; LA began to divert foreign waters into the river that basically ruined part of his land and made his fishing suck; so he settles with LA for $50k, but incurred $1k of legal expenses; LA gets to keep polluting, and taxpayer relinquishes all rights to suit; taxpayer reports none of this $49k on his tax return; gov’t says he should report all $49k as income because it’s for lost profits,

b) Arguments:i) Gov’t says basis comes last, because you actually own the land still, and this

was a payment for lost profitsii) Landowner says basis comes first, as this was for payment of an easement and

for damage done to the land; also, it’s really hard in this case to apportion basis, and in such a case a taxpayer should not be charged with gain on pure conjecture unsupported by any foundation of ascertainable fact

c) Normal rule: allocate the basis sort of pro rata; this is easy with stocks, but here this is tricky; how much is portion X of the land worth?; how much is a set of limited rights to a portion of the land worth?

d) Holding: taxpayer wins; “Apportionment with reasonable accuracy of the amount received not being possible, and this amount being less than petitioner’s cost basis for the property, it can not be determined that petitioner has, in fact, realized gain in any amount. Applying the rule as above set out, no portion of the payment in question should be considered as income, but the full amount must be treated as a return of capital and applied in reduction of petitioner’s cost basis.”

e) Chirelstein: “the courts have permitted the taxpayer to offset the condemnation award by the full cost of the property and to report no gain unless the amount received exceeds his entire initial investment”

f) Class Discussion:i) This is an interesting result, because notice everyone agrees that if taxpayer

got rent money for the land, that’d be taxable income. Why? Because he still

owns the land. So what if he got pre-paid rent that ended up being $49k up front? He’d have to pay taxes on that, and couldn’t enjoy his basis. So what’s the deal here? Interesting. It’s a little taste where the form of the transaction seems to matter.

ii) Could treat this as . . . (1) Unit-sale approach. Purchase of a portion of the land. Then break the land

into pieces, allocated portions of the basis to each piece, and then deduct this $ against the proper proportion of basis. Chirelstein likes this one the most.

(2) Payment for a leasehold. Then these are rents. Then receipts should be immediately included in income.

(3) Open-ended installment sale. This is the law. Offset the value received against the value of the property. Reduce basis appropriately, and realize gain or loss upon ultimate disposition of property.

iii) Case is probably still good law.iv) Rule of getting recovery of basis first against cash flows in known as the open

transaction doctrine.24) Hort v. Commissioner (1941, p. 695)

a) Summary: father gave petitioner property, a lot and ten-story office building; part of land was leased to Irving; lease became unprofitable to Irving, so the parties agreed to cancel the rest of the lease for $140k; petitioner didn’t include this in gross income, and rather counted as a loss the money he didn’t get from this cancellation

b) Issue: whether, in computing net gain or loss for income tax purposes, a taxpayer can offset the value of the lease canceled against the consideration received by him for the cancellation

c) Holding: no!d) Class Discussion:

i) Petitioner’s argument: amount received for cancellation was capital not ordinary income, hence it’s covered by capital gains and losses stuff; even if it’s ordinary gross income, there’s still a loss from § 165

ii) The loss calculated by Hort was the difference between the present value of the future lease payments minus the $140k and also minus $96k, which was the value of having the use of the building back.

iii) This is during the depression; probably why the lease was no longer beneficial for Irving Trust Co.

iv) Hort actually loses money here . . . the calculation mentioned above (and in footnote 12 on p. 698) shows this. He’s got a loss of essentially $21k. But the IRS says the $140 is income. So, for this all to balance out, the IRS must be acknowledging a $161k loss somewhere that Hort will eventually get (b/c $140-$161=-$21). So where does the IRS put/hide this loss? It’s in the property. Hort inherited the property with a lease on it. The property at first was worth $257k (includes lease value), but now it’s worth only $96k. So that’s the $161 loss. So why the different theories, if both essentially have the numbers the same. It’s just the loss is in a different place—Hort wants it earlier, but instead he won’t get it until he sells the property.

(1) IRS: whole $257 basis stays with the property.(2) Taxpayer: $160 basis goes with the rental, $96 (FMV) goes with the

property. v) The fundamental disagreement here is where the basis is allocated.vi) Is this consistent or inconsistent with Gavit? Yes, this is consistent, because

it’s the same basis. Here’s the analogy:(1) Gavit’s interest payment = Hort’s rental payments

(a) Gavit and Hort want all the basis to go here(2) Gavit’s remainder (to Marcia) = Hort’s FMV of property

(a) Holding puts basis here . . . just as Marcia could’ve sold her piece for a loss, Hort could’ve sold the property for a loss

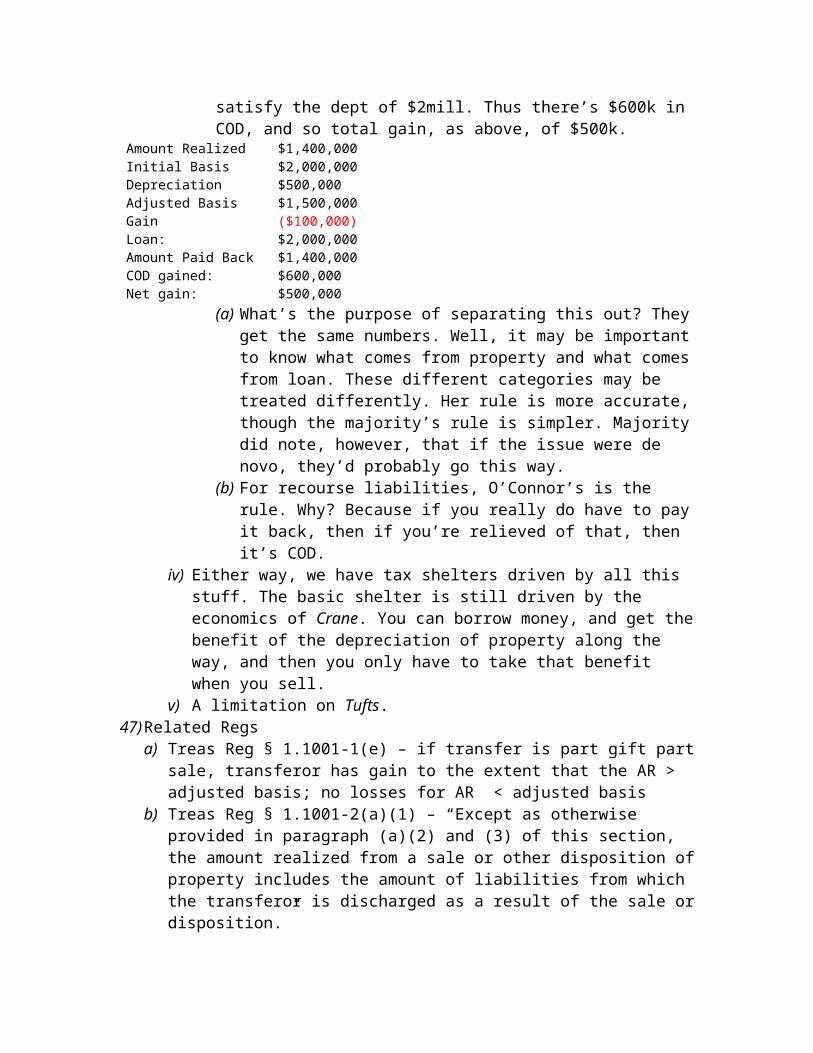

vii) Is Hort right? This is a simple rule, but can be abused. (1) A wants to sell B land for $100k. Normally, B would get basis of $100k,

A would have a net realization of $100k. (2) We can generate a tax loss by introducing a third party.(3) C steps in and buys from A for $100k, so A gets same. C rents to B for 99

years for PV of $100k. So C is same. (4) C still has $100k basis, if none of it goes to the property, you can have that

$100k basis tied to the remainder of the property. This remainder is essentially worth 1 cent, since the remainder after a really long lease is basically worthless. C can then sell the remainder for 1 cent, but the basis is $100k, so he gets a huge loss.

(5) Now, C still gets taxed on the rental payments, but again it’s a timing issue. C gets the loss today, and doesn’t have to pay the taxes on the rentals until they take place, some of which is way off in the future.

25) Related Codea) § 61(a)(3) – gross income includes “Gains derived from dealings in property”b) § 1001 – determination of amount of and recognition of gain or loss

i) § 1001(a) – gain is the excess gotten over adjusted basis (“the excess of the amount realized therefrom over the adjusted basis provided in section 1011”) and the loss is “the excess of the adjusted basis provided in such section for determining loss over the amount realized”

ii) § 1001(b) – how to calculate “amount realized”; $ + FMV of other property; there are some special rules on inclusion/exclusion of certain real property taxes under § 164(d)

iii) § 1001(c) – subject to exceptions, “the entire amount of the gain or loss, determined under this section, on the sale or exchange of property shall be recognized”

iv) § 1001(e) – certain term interests(1) § 1001(e)(1) – that portion of the adjusted basis of a term interest in

property that is determined under §§ 1014, 1015, or 1041 is disregarded(2) § 1001(e)(2) – definition of “term interest in property”:

(a) § 1001(e)(2)(A) – “a life interest in property”(b) § 1001(e)(2)(B) – “an interest in property for a term of years”(c) § 1001(e)(2)(C) – “an income interest in a trust”

(3) § 1001(e)(3) – exception; paragraph 1 doesn’t apply to a sale or other disposition that is part of a transaction where the entire interest is transferred to any person or persons

c) § 1011(a) – adjusted basis is basis in § 1012 adjusted according to § 1016d) § 1012 – basis is cost of property

i) Real property cost doesn’t include taxese) § 1014 – Basis of property acquired from a decedent

i) § 1014(a)(1) – basis is the fair market value of the property at the date of the decedent’s death (or 6 mos later, whichever is greater)

ii) This section is called stepped-up basis for death. Why stepped up? Because if you are going to realize a loss on death, you sell. This creates enormous potential to keep property. For example: Bill Gates has $50billion in stock of Microsoft. His basis? $0, because he put no money into the company, he just started working it. And on his death, his kids get FMV basis, which helps them enormously.

iii) Why treat bequests different than inter vivos? Not really a good answer.iv) This section ends at end of 2009. § 1022 comes in after.

f) § 1015 – basis of property acquired by gifts and transfers in trusti) § 1015(a) – for gifts after 12/31/1920, basis is same as in hands of donor, or

last preceding owner who didn’t get it by gift, unless that basis is greater than FMV of the property at the time of the gift, then for the purpose of determining loss the basis shall be such FMV; if can’t figure out basis, use FMV

ii) The different calculation for the loss makes it so that you can’t give away your losses to a person in a higher tax bracket.

g) § 1016(a) – adjustments you make to basis i) § 1016(a)(1) – for expenditures, receipts, losses or other items, properly

chargeable to capital accounts, but not for taxes of § 266 or expenditures of § 173 for which deductions have been taken in determining taxable income for the taxable year or any prior taxable year

ii) § 1016(a)(2) – (after 2/28/1913) for exhaustion, wear and tear, obsolescence, amortization, and depletion, to the extent of the amount allowed, and resulting in a reduction for any taxable year of the taxpayer’s taxes, or prior income, war-profits, or excess-profits tax laws . . .

h) Treasury Regs § 1.61-6 – gains derived from dealings in propertyi) “When a part of a larger property is sold, the cost or other basis of the entire

property shall be equitably apportioned among the several parts, and the gain realized or loss sustained on the part of the entire property sold is the difference between the selling price and the cost or other basis allocated to such part.”

ii) Sales of separate parts of something are treated as separate transactions.

Transferred and Imaginary BasisThis reading is not on the updated syllabus, so probably isn’t that important.26) Examples under § 101

a) Life insurance covering plane crash; pay $5 for $50k if you die

i) $49,995 gain upon death is excluded under § 101(a)ii) If no death, $5 paid for insurance isn’t deductible iii) In the aggregate, if insurance companies do a good job setting their rates, then

the amount lost (sum of $5 payments, not deductible) will equal the amount gained (sum of $49,995 payments, excluded), so tax effects balance. This is not so in the individual cases, however. Some people gain big and aren’t taxed ($49,995 excluded), and others lose a little, and can’t deduct.

27) Clark v. Commissioner (1939, p. 121)a) Summary: Taxpayer’s tax man made a mistake which caused him to have to pay

$19k more in taxes; tax man paid taxpayer the $19k, but included this in the taxpayer’s income the next taxable year. Is this $19k taxable income? No.

b) Arguments:i) Respondent tax guy: this payment is income because it constituted taxes paid

for by a third party (like Old Colony)ii) Petitioner taxpayer: this payment is not taxable as it constituted compensation

for damages or loss caused by the error of t he tax counselc) Reasoning:

i) This $19k was paid to petition not qua taxes, but as compensation to petitioner for his loss. “The fact that such obligation was for taxes is of no moment here.” It mattered instead that it was “compensation for a loss which impaired petitioner’s capital.”

ii) The theory of the cases that back this up “is that recoupment on account of such losses is not income since it is not ‘derived from capital, from labor or from both combined.’ . . . And the fact that the payment of the compensation for such loss was voluntary, as here, does not change its exempt status.”

d) Class Discussion:i) Glenshaw Glass the ultimate reason for the holding is no good, as it was

based on the “derived from capital definition.” But the holding itself is fine. It has been limited to cases where the taxpayer has to pay more than the actual amount that should have been required, not to cases where the taxpayer has to pay more than the tax preparer originally said.

ii) Clark is really a choice between two types of errors. Do we overtax the taxpayer (require him to pay tax on the $19k) or undertax him (no tax on the $19k, which puts him in a situation better off than someone who doesn’t get the $19k payment from his tax preparer who made the same mistake). See ex. on p. 124.

iii) Note that you aren’t taxed on an income tax refund.28) Related Code

a) § 72 – annuities; certain proceeds of endowment and life insurance contractsi) § 72(a) – “gross income includes any amount received as an annuity . . . under

an annuity, endowment, or life insurance contract”ii) § 72(b) – exclusion ratio

(1) § 72(b)(1) – you can exclude a certain amount of the gross income from annuity, endowment, etc. . . . how much? The exclusion ratio is determined by dividing the investment in the contract by the expected

return, which is the aggregate fixed annuity (or whatever) payments you can expect to receive under the contract.

(2) § 72(b)(2) – the amount excluded can’t be more than the unrecovered investment in the K immediately before the receipt of such amount

(3) § 72(b)(3) – deduction where annuity payments stop before entire investment is recovered(a) § 72(b)(3)(A) – if payments stop because of death and there is still

unrecovered investment, the amount of unrecovered investment can be deducted for annuitant’s last taxable year

(b) § 72(b)(3)(B) – if annuity pays another person as under § 72(c)(2)(B) and (C), then that person can deduct from taxes in year were supposed to have received payments

(c) § 72(b)(3)(C) – deduction under this section is treated as if attributable to a trade or business of the taxpayer (references § 172)

(4) § 72(b)(4) – how to calculate unrecovered investment at a certain date: investment in the contract minus aggregate amount received under K after K’s starting date and before calculation date, so long as that amount was excludable from gross income under this subtitle

iii) § 72(c) – definitions(1) § 72(c)(1) – “investment in the contract” as of the start date is the

aggregate amount of premiums or other consideration paid for the K minus the aggregate amount received under the K before the start date, “to the extent that such amount was excludable from gross income under this subtitle or prior income tax laws”

(2) § 72(c)(2) – “adjustment in investment where there is refund feature”; deals with situation when return depends on life expectancy, etc.

(3) § 72(c)(3) – “expected return” (a) § 72(c)(3)(A) – if depends on life expectancy, use actuarial tables(b) § 72(c)(3)(B) – otherwise, it’s the aggregate of the amounts receivable

under the K as an annuity(4) § 72(c)(4) – “annuity starting date” is the first day of the first period for

which an amount is received as an annuity under the K, unless that was before 1/1/1954, in which case just use 1/1/1954

b) § 101 – certain death benefitsi) § 101(a) – proceeds of life insurance contracts payable by reason of death

(1) § 101(a)(1) – gross income doesn’t include amounts received under a life insurance K, if they are paid by reason of the death of the insured (there are exceptions to this)

(2) § 101(a)(2) – if a life insurance K or any interest in it is transferred for valuable consideration, the amount excluded from gross income by the previous section 1 shall not exceed the sum of the value of the consideration plus the premiums and other amounts subsequently paid by the transferee, but there are exceptions:(a) § 101(a)(2)(A) – if the K has a basis for determining gain or loss in the

hands of a transferee

(b) § 101(a)(2)(B) – if transfer is the insured, to a partner of insured, ro a partnership in which insured is a partner, or to a corp in which insured is a shareholder or officer

c) § 104 – compensation for injuries or sicknessi) § 104(a) – except in the case of amounts attributable to (and not exceeding)

deduction under § 231 (medical expenses, etc.) for any prior taxable year, gross income doesn’t include:(1) § 104(a)(1) – workmen’s comp(2) § 104(a)(2) – damages (save punitive) for personal physical

injuries/sickness(3) § 104(a)(3) - $ from accident or health insurance (except $ from an

employer to the extent that the # is attributable to contributions by the employer which were not included in gross income or were aid by the employer)

(4) § 104(a)(4) – pension, annuity, or similar allowances for persona injuries or sickness from active service in armed forces, etc.

(5) § 104(a)(5) – disability income attributable to injuries incurred as a direct result of a violent attack that the Sec of State determines to be a terrorist attack that occurred while the individual as a US employee and was working at time of injuries

d) § 165 – lossesi) § 165(a) – generally, can deduct any loss not covered by insuranceii) § 165(b) – basis for deduction is the adjusted basis from § 1011iii) § 165(c) – for an individual, deductions under (a) are limited to:

(1) § 165(c)(1) – losses from trade or business(2) § 165(c)(2) – losses from any transaction entered into for profit, though

not connected with trade or business(3) § 165(c)(3) – exceptions in (h), losses of property not connected with trade

or business or a transaction entered into for profit, if losses arise from fir, storm, shipwreck, or other casualty, or from theft

iv) § 165(d) – “losses from wagering transactions shall be allowed only to the extent of the gains from such transactions”

v) § 165(e) – theft losses are counted during taxable year when discoveredvi) § 165(f) – capital losses are limited by §§ 1211-1212vii)§ 165(g) – worthless securities

(1) § 165(g)(1) – “If any security which is a capital asset becomes worthless during the taxable year, the loss resulting therefrom shall, for the purposes of this subtitle, be treated as a loss from the sale or exchange, on the last day of the taxable year, of a capital asset.”

(2) § 165(g)(2) – definition of security (share, right, bond, etc.)viii) § 165(h) – treatment of casualty gains and losses

(1) § 165(h)(1) – (c)(3) stuff allowed only to the extent that it exceeds $100(2) § 165(h)(2) – net casualty loss allowed only to the extent it exceeds 10%

of adjusted gross income(a) § 165(h)(2)(A) – “If the personal casualty losses for any taxable year

exceed the personal casualty gains for such taxable year, such losses

shall be allowed for the taxable year only to the extent of the sum of” the amount of the gains plus the excess over 10% of the adjusted gross income of the individual

(b) § 165(h)(2)(B) – when personal casualty gains > personal casualty losses, all those gains are treated as gains from sales/exchanges of capital assets, and all the losses are treated as losses from sales/exchanges of capital assets

(3) § 165(h)(3) – definitions(a) § 165(h)(3)(A) – “Personal casualty gain” is the recognized gain from

any involuntary conversion of property described in (c)(3)(b) § 165(h)(3)(B) – “Personal casualty loss” is any loss described in (c)

(3)ix) § 165(i) – disaster losses

(1) § 165(i)(1) – any loss from a disaster in an area later determined by Pres to get Fed aid under Stafford Disaster Relief Act may be taken into account for taxable year immediately preceding the taxable year in which the disaster occurred

(2) § 165(i)(2) – casualty is treated as having occurred in year for which loss is taken

(3) § 165(i)(3) – amount of loss taken into account in preceding taxable year can’t exceed uncompensated amount determined on the basis of the facts existing at the date the taxpayer claims the loss

(4) § 165(i)(4) – this § doesn’t affect prescription of regs or other guidance for federal funds, etc.

Annual Accounting29) Introduction