RC&C FINANCE COMPANY 31 July 2008 Mike Purnell. RC&C FINANCE Who is RC&C Finance? Business Model...

22

RC&C FINANCE COMPANY 31 July 2008 Mike Purnell

-

Upload

jessica-payne -

Category

Documents

-

view

215 -

download

2

Transcript of RC&C FINANCE COMPANY 31 July 2008 Mike Purnell. RC&C FINANCE Who is RC&C Finance? Business Model...

RC&C FINANCE COMPANY31 July 2008

Mike Purnell

RC&C FINANCEWho is RC&C Finance?Business ModelRisk ManagementFundingBase AnalysisRelevant StatisticsThe Future

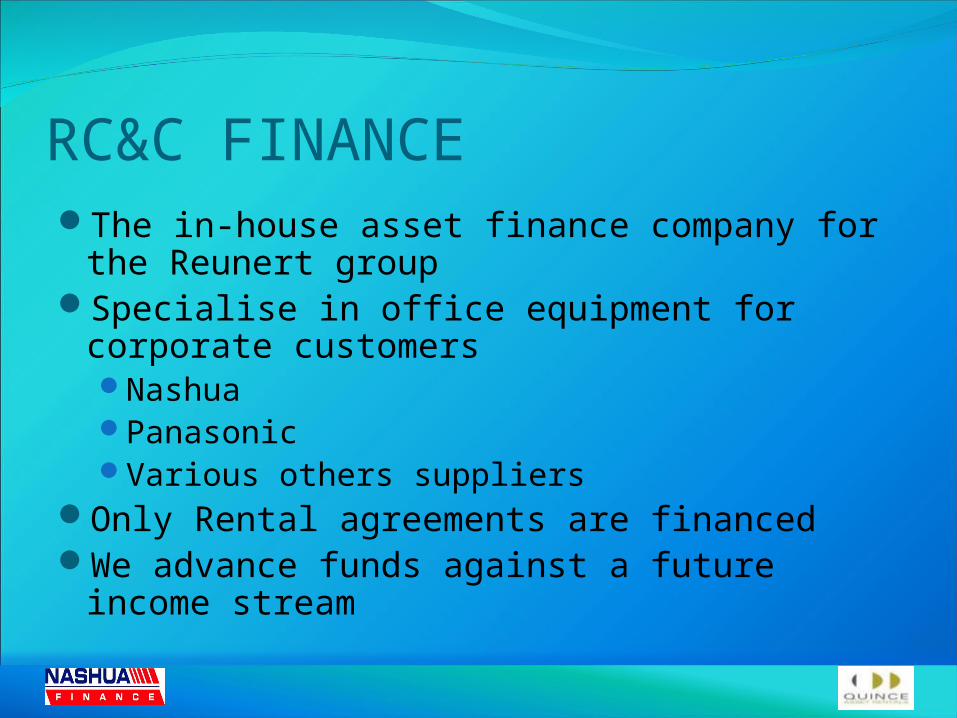

RC&C FINANCEThe in-house asset finance company for the

Reunert groupSpecialise in office equipment for corporate

customersNashuaPanasonicVarious others suppliers

Only Rental agreements are financedWe advance funds against a future income

stream

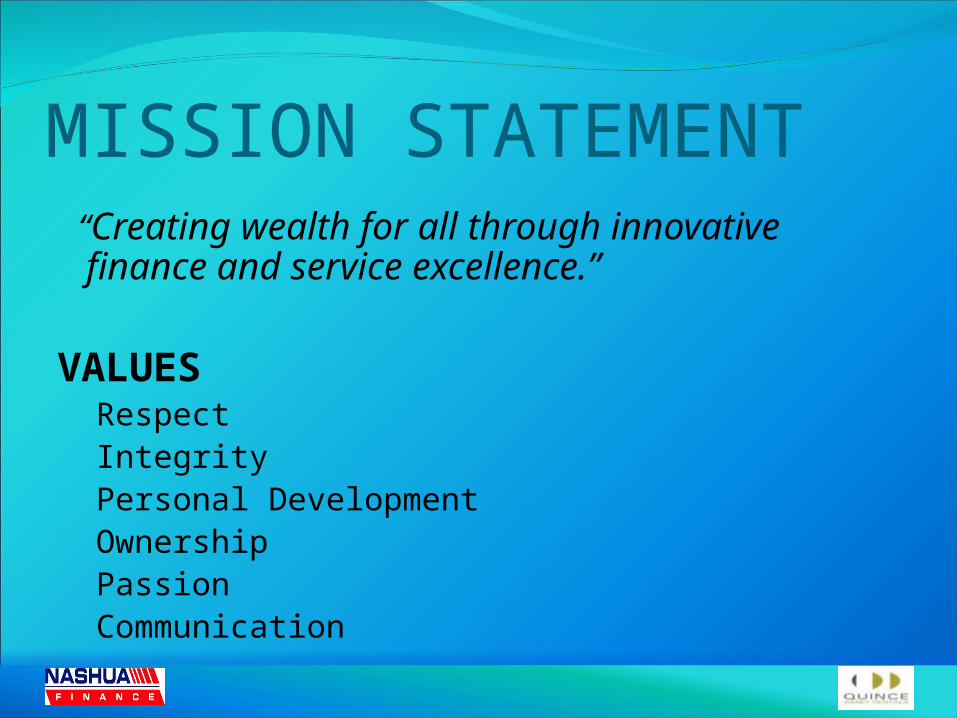

MISSION STATEMENT “Creating wealth for all through

innovative finance and service excellence.”

VALUESRespectIntegrityPersonal DevelopmentOwnershipPassionCommunication

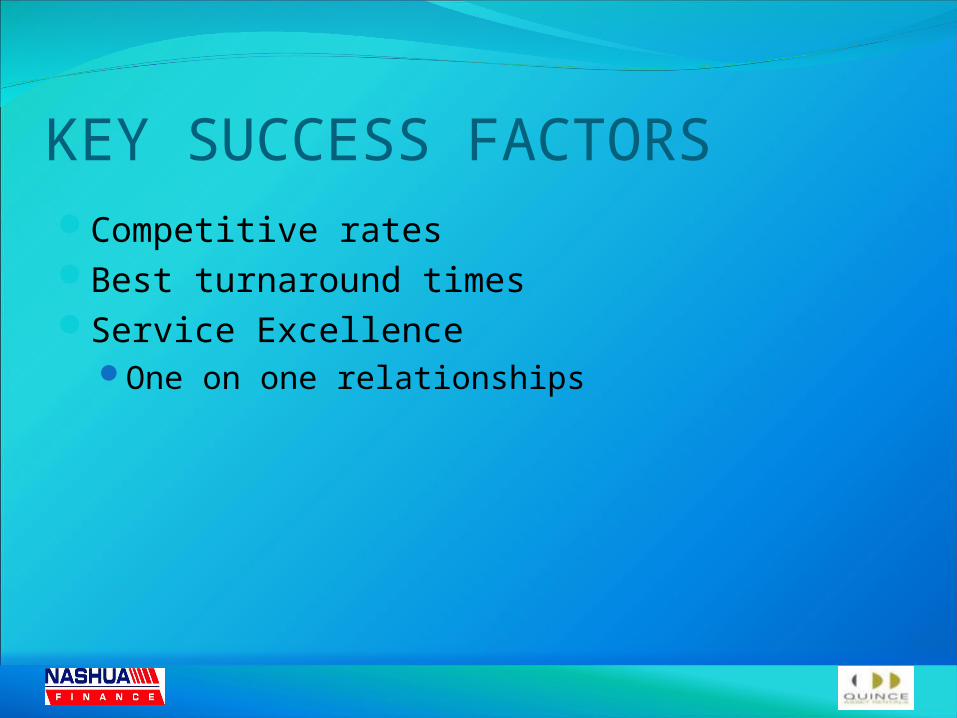

KEY SUCCESS FACTORSCompetitive ratesBest turnaround timesService Excellence

One on one relationships

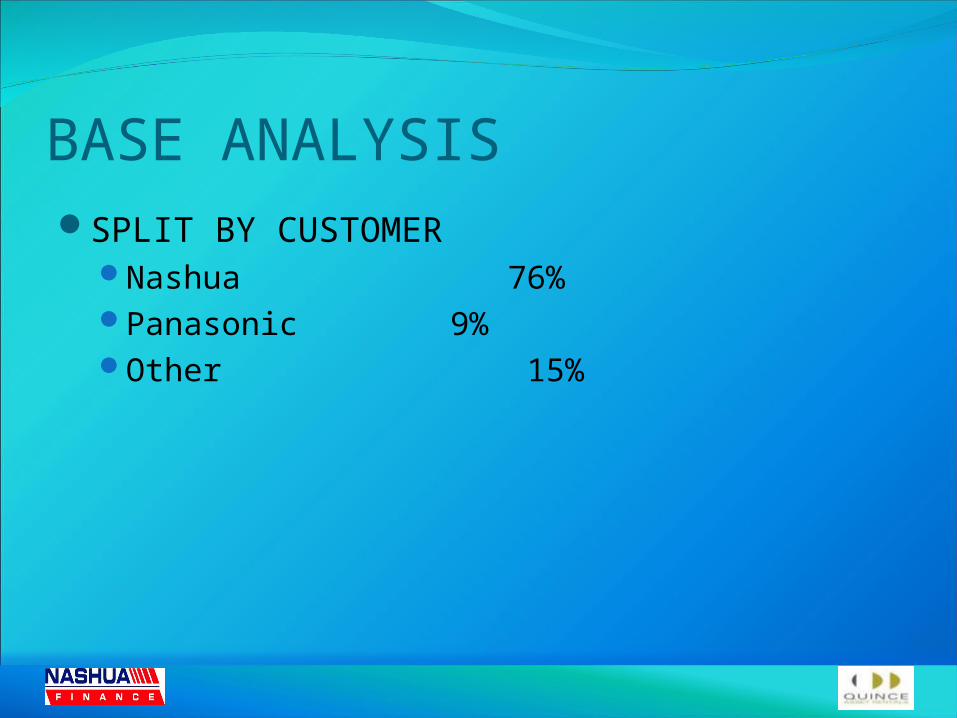

BASE ANALYSISSPLIT BY CUSTOMER

Nashua 76%Panasonic 9%Other 15%

BBBEE CERTIFICATION• Rating: “Non BEE-Limited Contribution”• Re-Rating in November 2008

• Investment in Staff Development• Development of “Black Management”• Investment in Corporate Social Investment

via Nashua Franchises

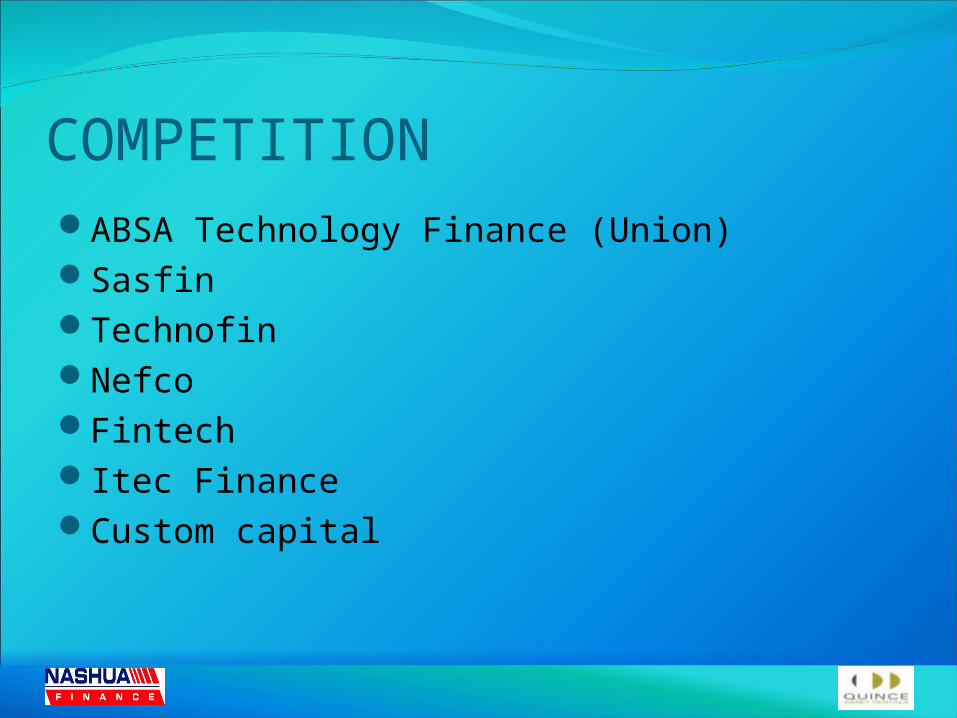

COMPETITIONABSA Technology Finance (Union)SasfinTechnofinNefcoFintechItec FinanceCustom capital

BUSINESS MODEL

Nashua Finance

Quince Asset Rentals

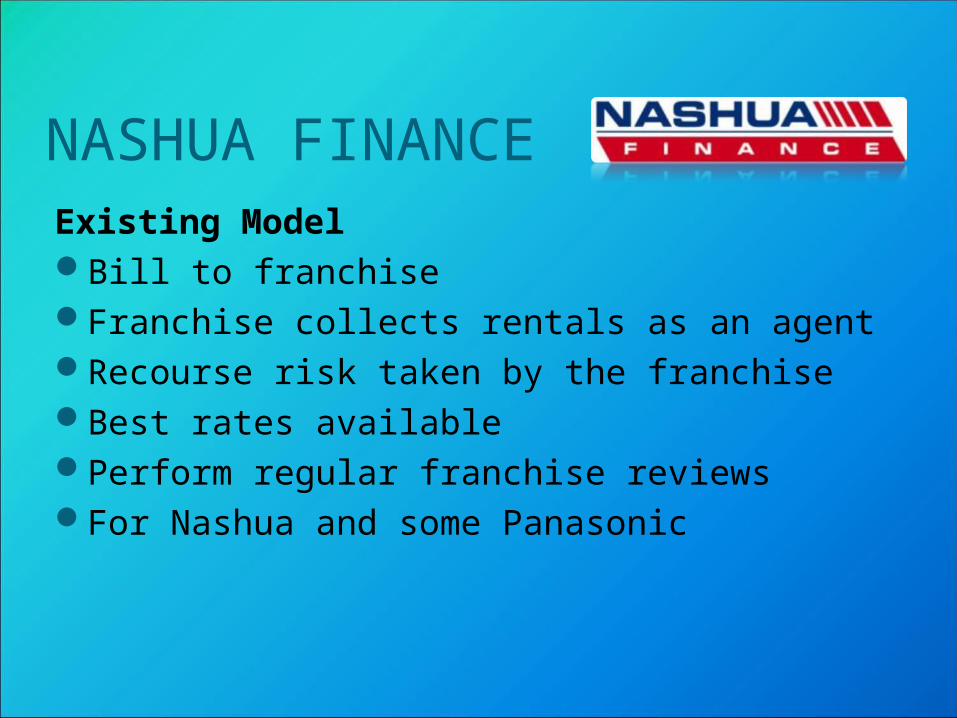

NASHUA FINANCEExisting ModelBill to franchiseFranchise collects rentals as an agentRecourse risk taken by the franchiseBest rates availablePerform regular franchise reviewsFor Nashua and some Panasonic

QUINCE ASSET RENTALSBill Direct to end userWe collect directlyFinance company takes the credit riskRates competitive with opposition productNo franchise review procedure necessaryPanasonic, Siemens, Brokers and other OA

Dealers

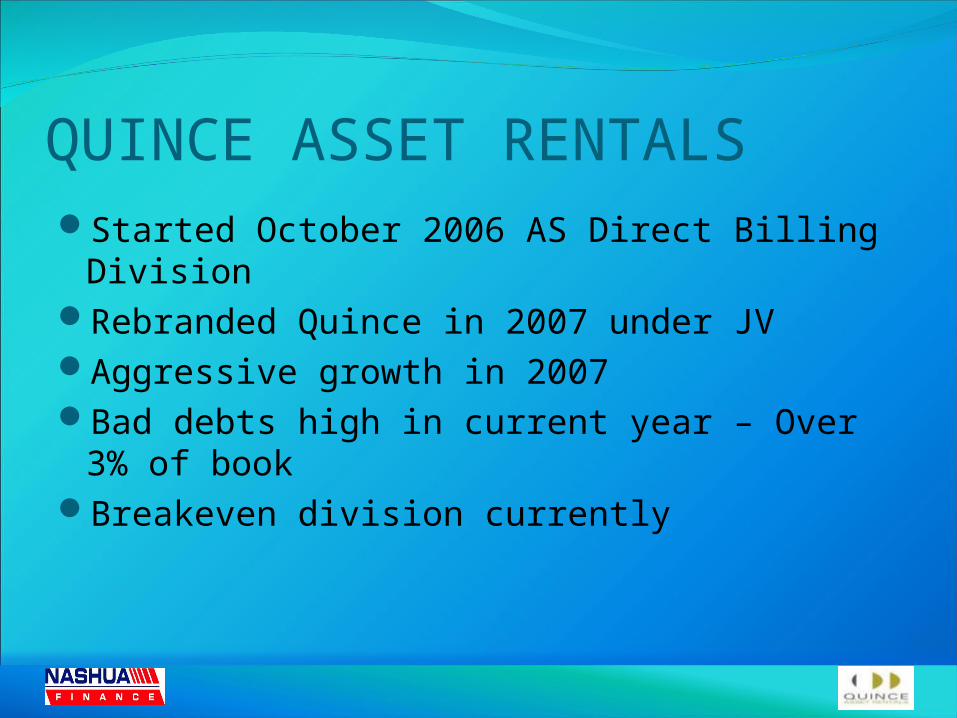

QUINCE ASSET RENTALSStarted October 2006 AS Direct Billing

DivisionRebranded Quince in 2007 under JVAggressive growth in 2007Bad debts high in current year – Over 3% of

bookBreakeven division currently

RISK MANAGEMENTNew computerised vetting systemSystem scores dealsExecutive review of overridesPricing verificationsVoice recording confirmationsQuality control prior to payoutEFT debit orders on each dealOngoing analysis of bad debts against baseMonthly credit committee reviews

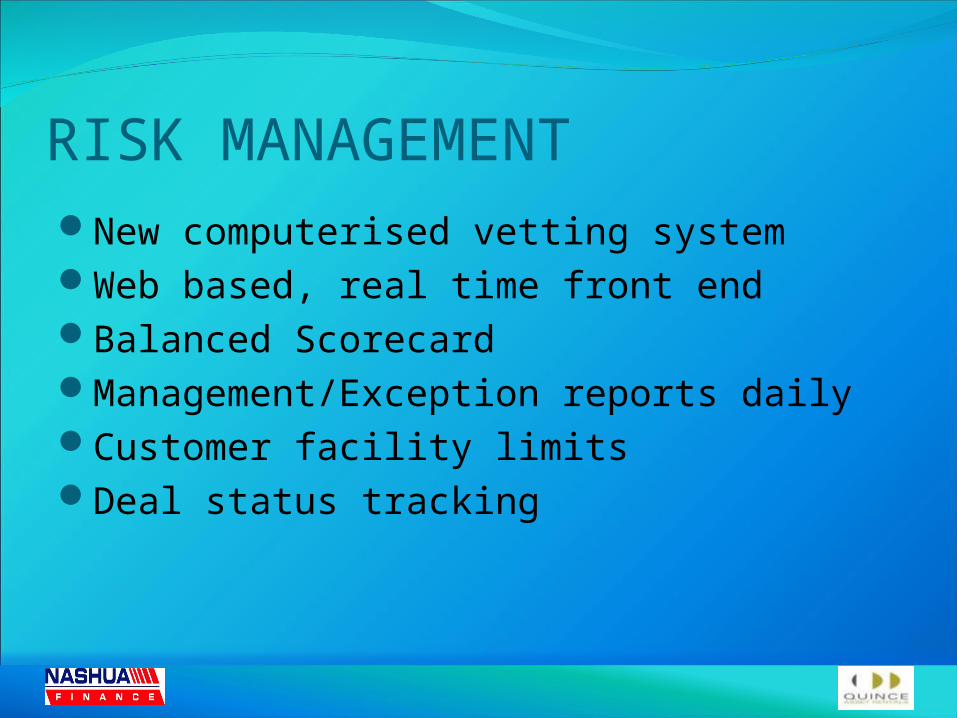

RISK MANAGEMENTNew computerised vetting systemWeb based, real time front endBalanced ScorecardManagement/Exception reports dailyCustomer facility limitsDeal status tracking

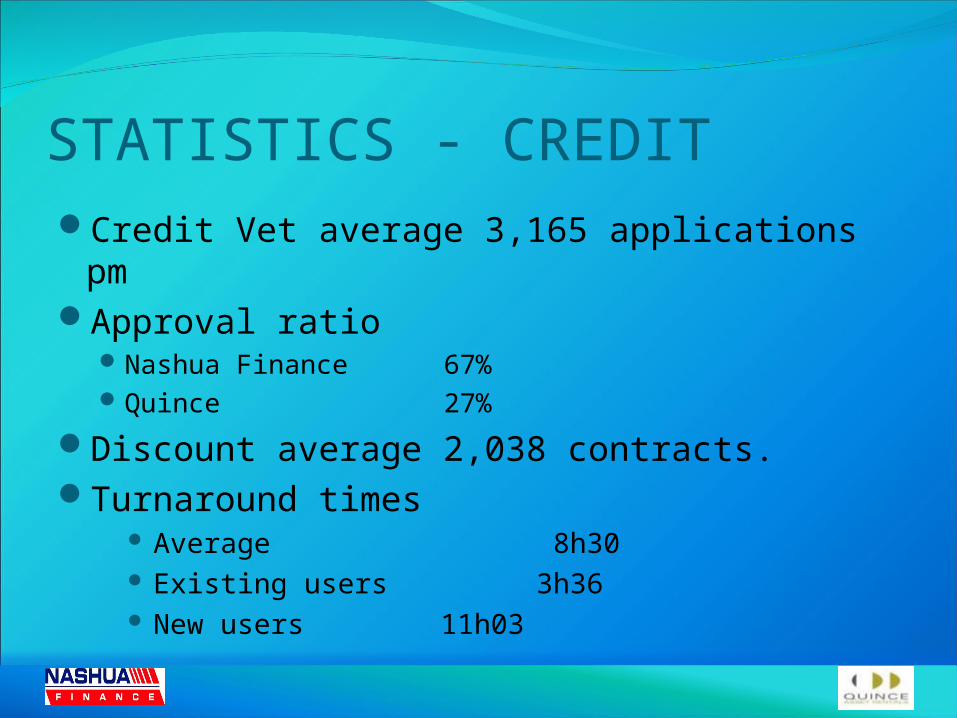

STATISTICS - CREDITCredit Vet average 3,165 applications pmApproval ratio

Nashua Finance 67%Quince 27%

Discount average 2,038 contracts.Turnaround times

Average 8h30 Existing users 3h36 New users 11h03

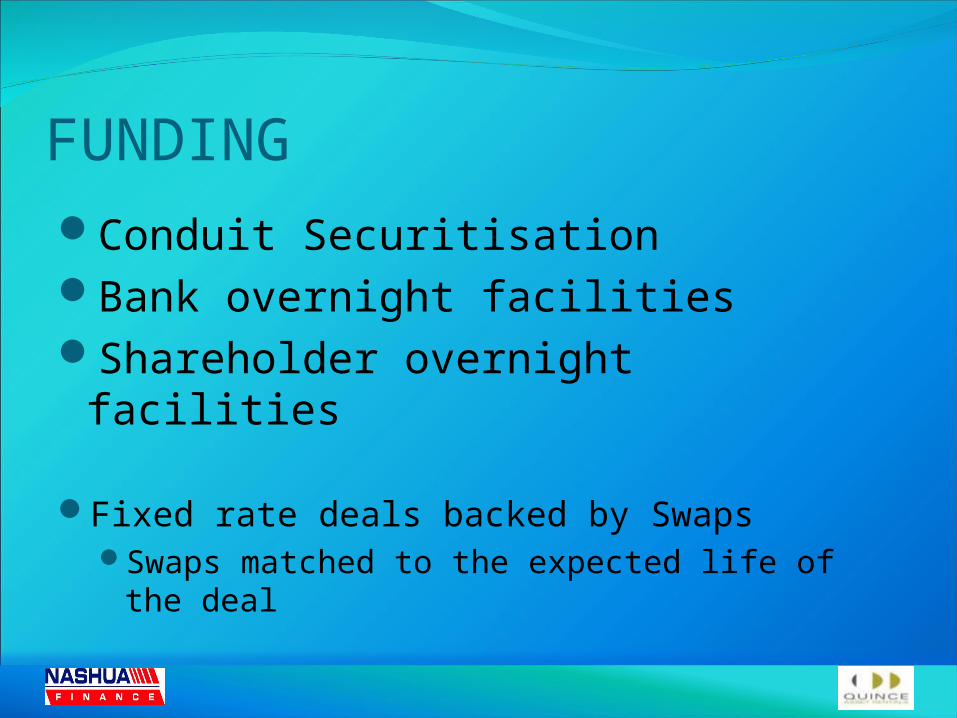

FUNDINGConduit SecuritisationBank overnight facilitiesShareholder overnight facilities

Fixed rate deals backed by SwapsSwaps matched to the expected life of the deal

INTEREST RATESMargins are managed

General Cut backs expected in volumesRand Devaluation – Increased values per deal

?

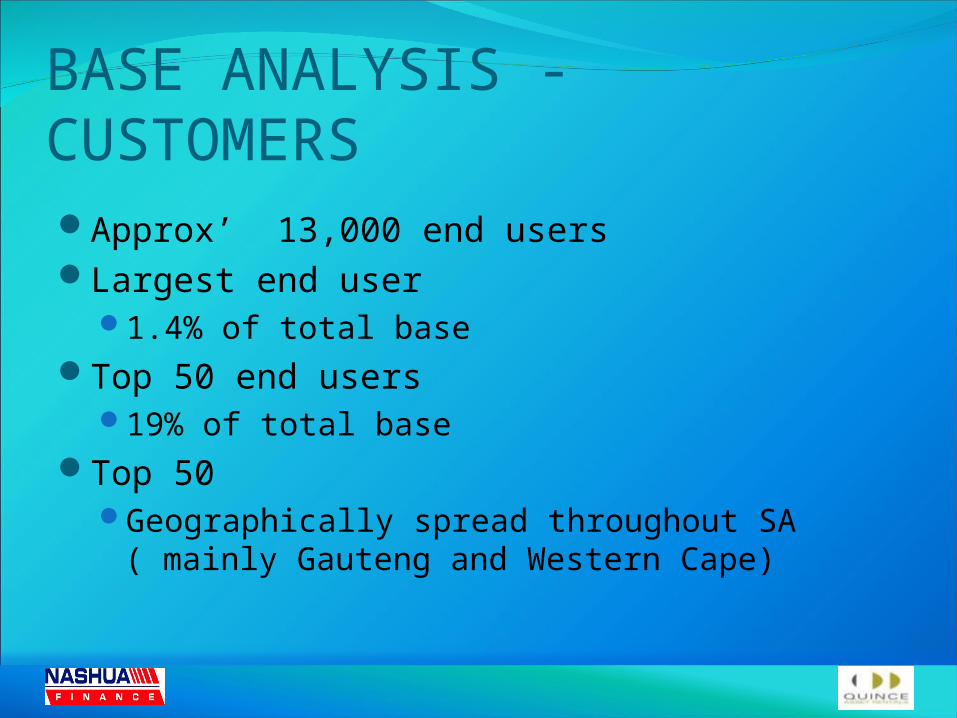

BASE ANALYSIS - CUSTOMERSApprox’ 13,000 end usersLargest end user

1.4% of total baseTop 50 end users

19% of total baseTop 50

Geographically spread throughout SA ( mainly Gauteng and Western Cape)

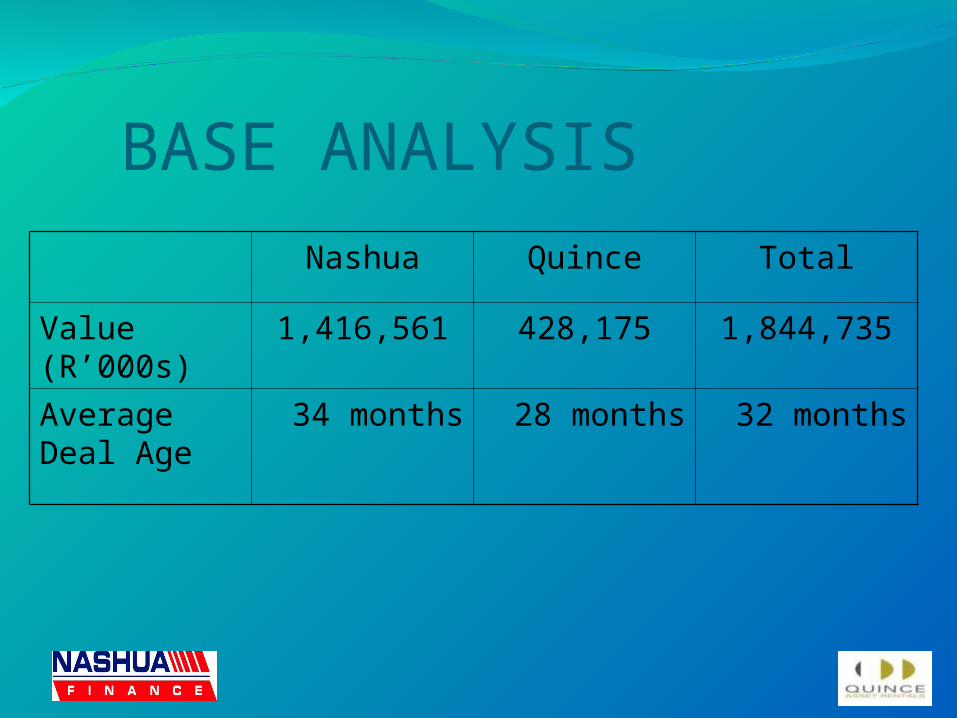

BASE ANALYSISNashua Quince Total

Value (R’000s) 1,416,561 428,175 1,844,735

Average Deal Age

34 months 28 months 32 months

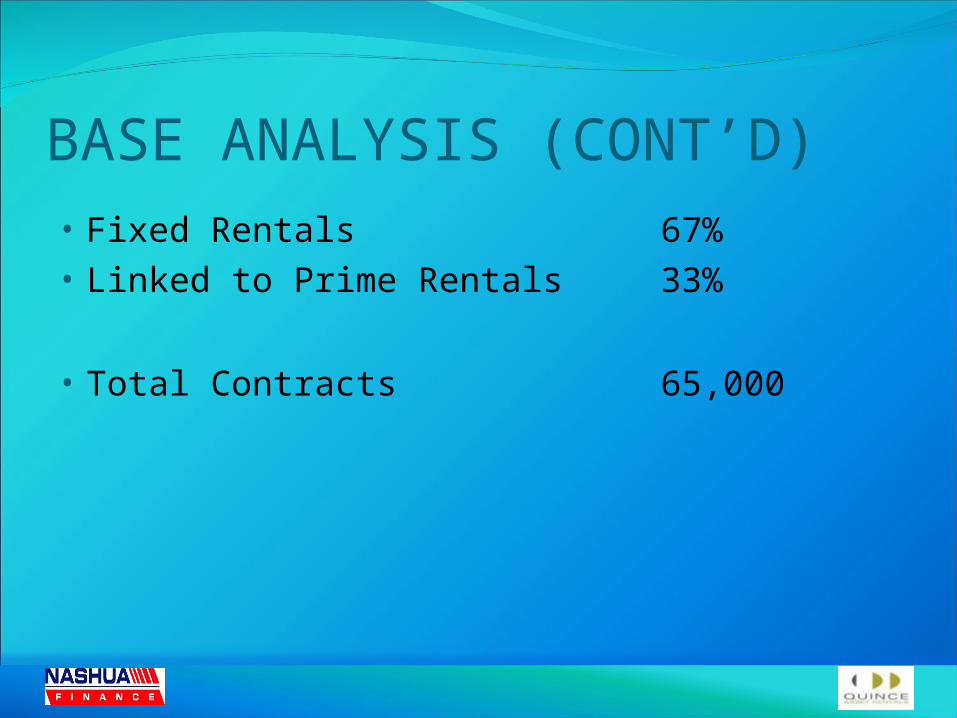

BASE ANALYSIS (CONT’D)• Fixed Rentals 67%• Linked to Prime Rentals 33%

• Total Contracts 65,000

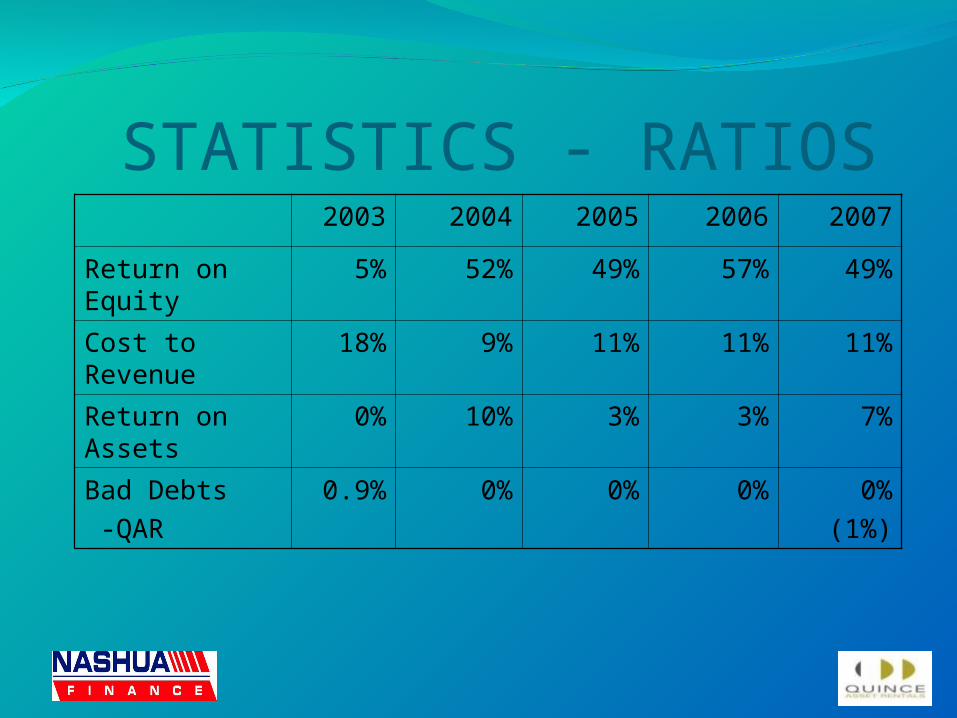

STATISTICS - RATIOS2003 2004 2005 2006 2007

Return on Equity 5% 52% 49% 57% 49%

Cost to Revenue 18% 9% 11% 11% 11%

Return on Assets 0% 10% 3% 3% 7%

Bad Debts

-QAR

0.9% 0% 0% 0% 0%

(1%)

THANK YOU

![FocusPRO Instructions 6000WRC Y Rc M29374 C YR Rc 5 G W C Y R Rc 6 G W C R Rc M29377 G C Y R M29378 Y2 W2 G W C Y R Rc M29379 Y2W2G W C Y R Rc M29380 ... 5 or 6 CPH] 12 Manual/Auto](https://static.fdocuments.in/doc/165x107/5e5d3877a6a3e20cd309c085/focuspro-instructions-6000-wrc-y-rc-m29374-c-yr-rc-5-g-w-c-y-r-rc-6-g-w-c-r-rc-m29377.jpg)