Ray O’Connor Regional Manager South-West Attracting investment to Regional Locations An IDA...

42

Ray O’Connor Regional Manager South-West Attracting investment to Regional Locations An IDA Perspective Association of Geography Teachers of Ireland Annual Conference Cork 3 rd October

-

Upload

anabel-bridges -

Category

Documents

-

view

215 -

download

1

Transcript of Ray O’Connor Regional Manager South-West Attracting investment to Regional Locations An IDA...

Ray O’ConnorRegional Manager

South-West

Attracting investment to Regional Locations

An IDA Perspective

Association of Geography Teachers of IrelandAnnual Conference

Cork 3rd October

Agenda

Overview of IDA Ireland - The Business of IDA

Regional Development

Challenges/Opportunities for Gateways & Hubs

The Business of IDA Ireland

IDA - overview

A state agency with its own board

Attracts FDI to develop economy

Supports existing clients to develop additional functions

Builds relationships with inward investors

Quantity & Quality of investments

• Regional spread• New business areas

Employs 295 people

FÁS National Training Agency

IDA Offices Worldwide

IrelandUK

Germany

JapanKorea

Australia

Taiwan

ChinaCalifornia

Chicago

Atlanta

FranceNew York

Paths to Winning Projects

Industry Groups

MarketResearch

Cold Calls Consultants

Call to IDA

Referrals

www.‘Business

Ireland’Conferences

LEADS

Presentations/Visits to Ireland /Win Project

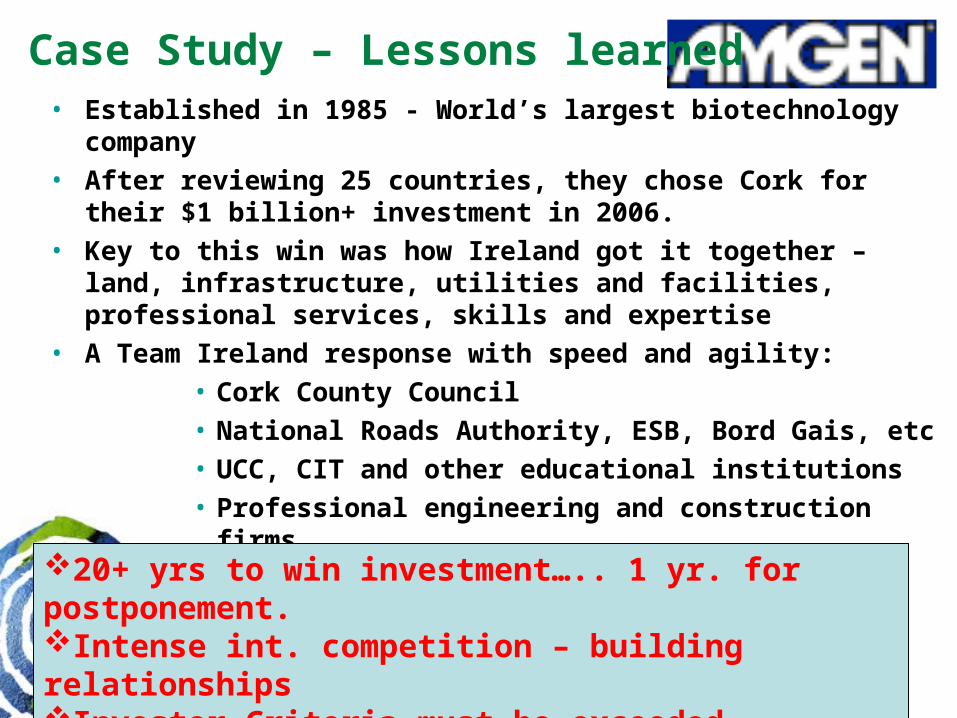

• Established in 1985 - World’s largest biotechnology company• After reviewing 25 countries, they chose Cork for their $1 billion+

investment in 2006.• Key to this win was how Ireland got it together – land,

infrastructure, utilities and facilities, professional services, skills and expertise

• A Team Ireland response with speed and agility:• Cork County Council• National Roads Authority, ESB, Bord Gais, etc• UCC, CIT and other educational institutions• Professional engineering and construction firms• Existing companies – their experience as reference

Case Study – Lessons learned

20+ yrs to win investment….. 1 yr. for postponement. Intense int. competition – building relationshipsInvestor Criteria must be exceededInvestor Decisions are made for commercial reasons

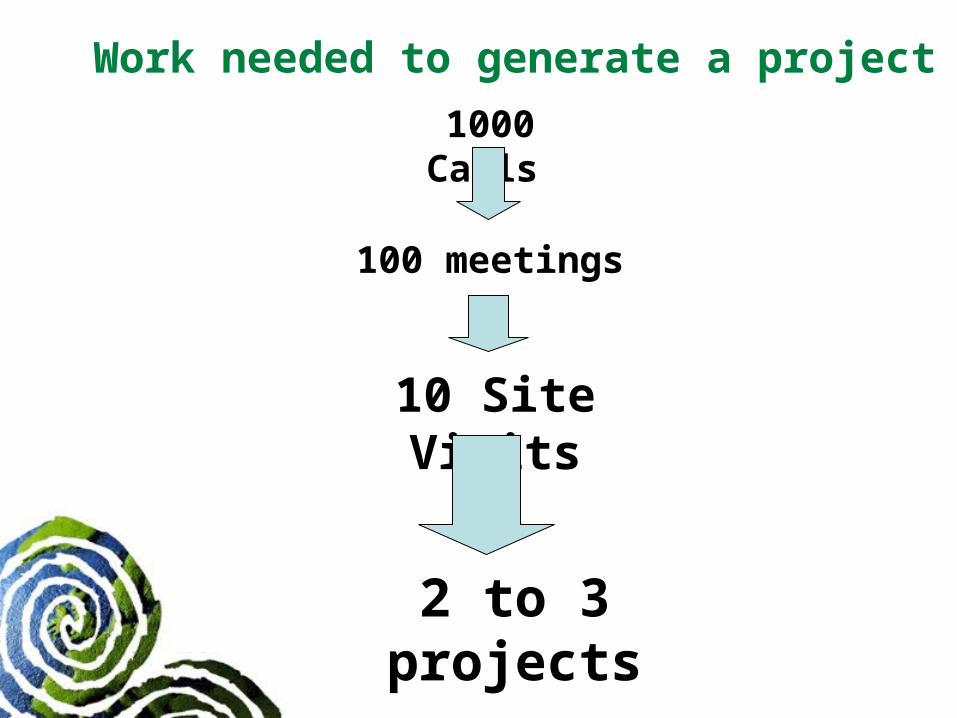

Work needed to generate a project

1000 Calls

100 meetings

10 Site Visits

2 to 3 projects

National IDA Job Gains and Losses 1997 - 2006

-20000

-15000

-10000

-5000

0

5000

10000

15000

20000

25000

Gains

Losses

Net

Source: Forfas Annual Employment Surveys

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006

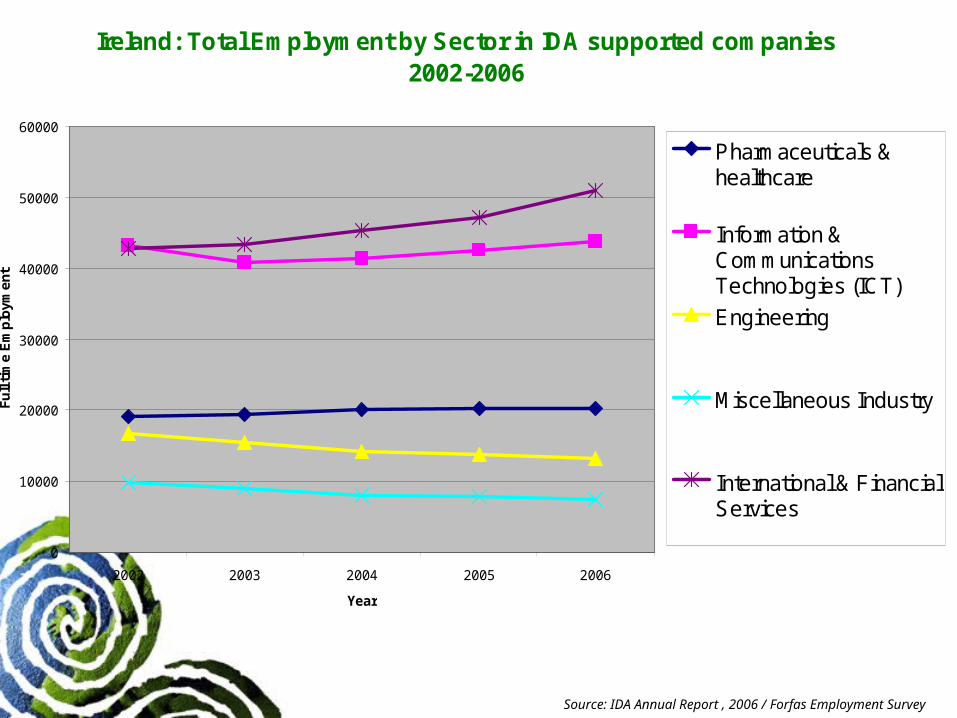

Source: IDA Annual Report , 2006 / Forfas Employment Survey

Ireland: Total Employment by Sector in IDA supported companies 2002-2006

0

10000

20000

30000

40000

50000

60000

2002 2003 2004 2005 2006

Year

Fu

ll ti

me

Em

plo

ym

en

t

Pharmaceuticals &healthcare

Information &CommunicationsTechnologies (ICT)

Engineering

Miscellaneous Industry

International & FinancialServices

Business Mega-Trends Future Business in Ireland

• Globalisation, technology and digital media.• Growth of Asia and integration with West• Growth of Eastern Europe• Demographic constraints in Europe • Growth of services – now 50% of world trade• Higher value, more knowledge-intensive and capital-intensive • Business transformation & new business models - ‘virtual’• Increasing speed and shorter life cycles e.g. Dell• High value manufacturing still critically important • Investment will be more mobile than ever & ‘weightless’ – less

rooted and potentially footloose• More ‘open’ and overseas R&D by multinationals

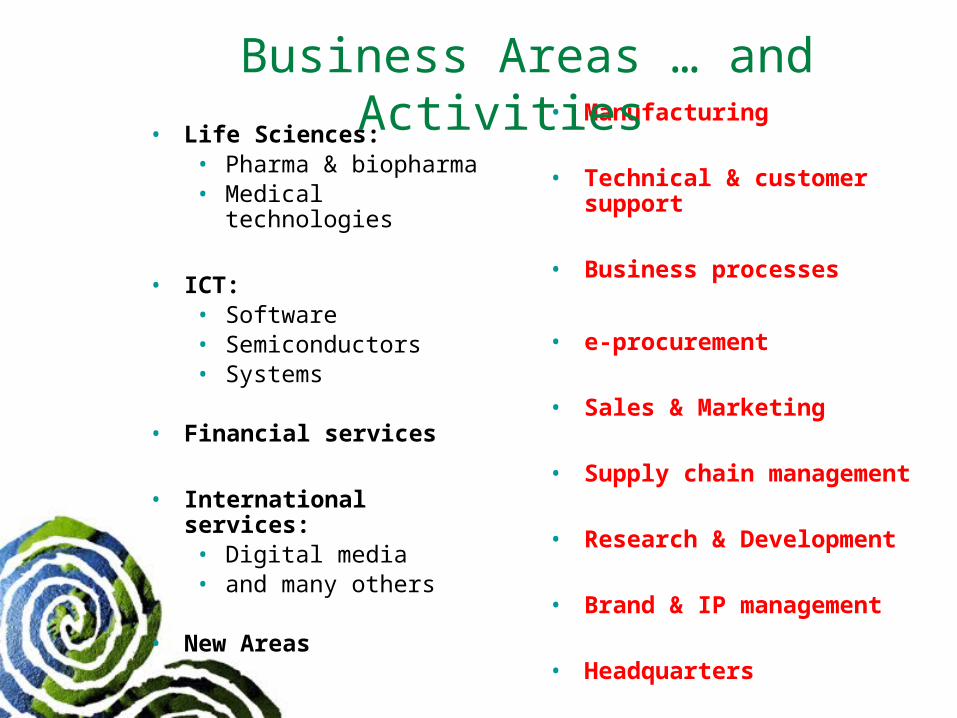

• Life Sciences:• Pharma & biopharma• Medical technologies

• ICT:• Software• Semiconductors• Systems

• Financial services

• International services:• Digital media • and many others

• New Areas

• Manufacturing

• Technical & customer support

• Business processes

• e-procurement

• Sales & Marketing

• Supply chain management

• Research & Development

• Brand & IP management

• Headquarters

Business Areas … and Activities

Ireland of the Future - the ‘Knowledge Economy’

• Higher value activities & higher skills

• More sophisticated and complex jobs

• New patterns of investment

• More continuous learning and re-learning

• Technology and science more pervasive

• Premium on flexibility and responsiveness

Niche Markets•

Low Labour Content

CustomisedKnowledge Intensive

Specialised SkillsEmerging/Growth After sales

service Intensive

High Margin

High Skills

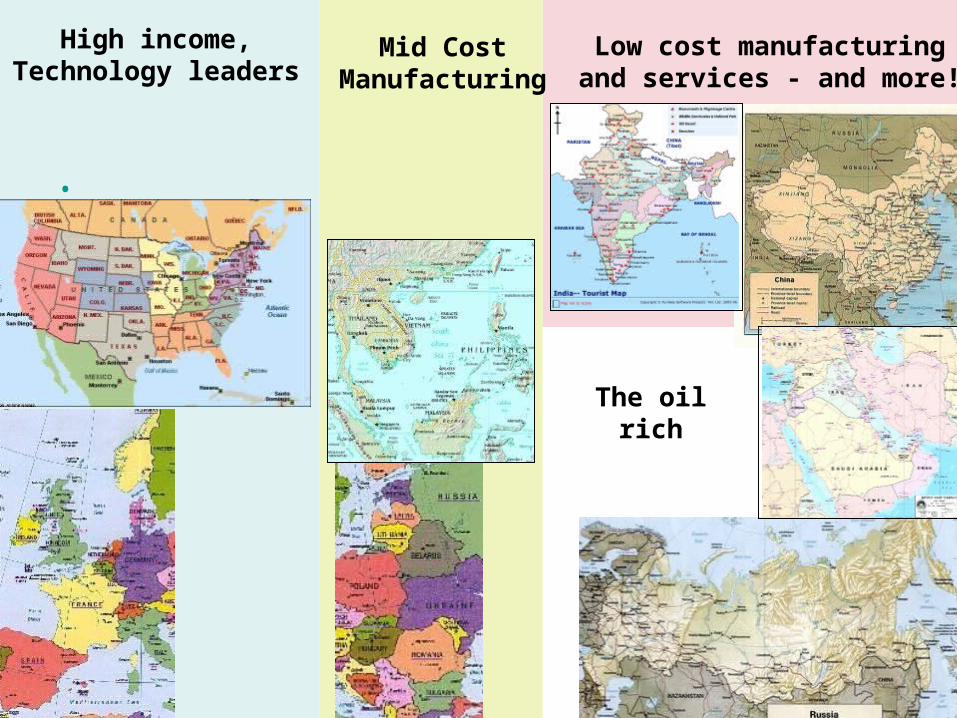

Regional DevelopmentAttracting FDI to Ireland’s Regions

Regional Development Growing recognition in Europe that major city-regions play a

central role in developing modern knowledge based economies

Knowledge based sectors are heavily concentrated in or near the centres of major cities

We compete with city-regions elsewhere with populations of 1 million or more

Ireland’s regions are small in comparison

We must think and act regionally, not locally

Critical mass is essential and gateways are key

IDA Ireland is aligned to the NSS with an embedded regional Structure

•

High income,Technology leaders

Mid CostManufacturing

Low cost manufacturingand services - and more!

The oilrich

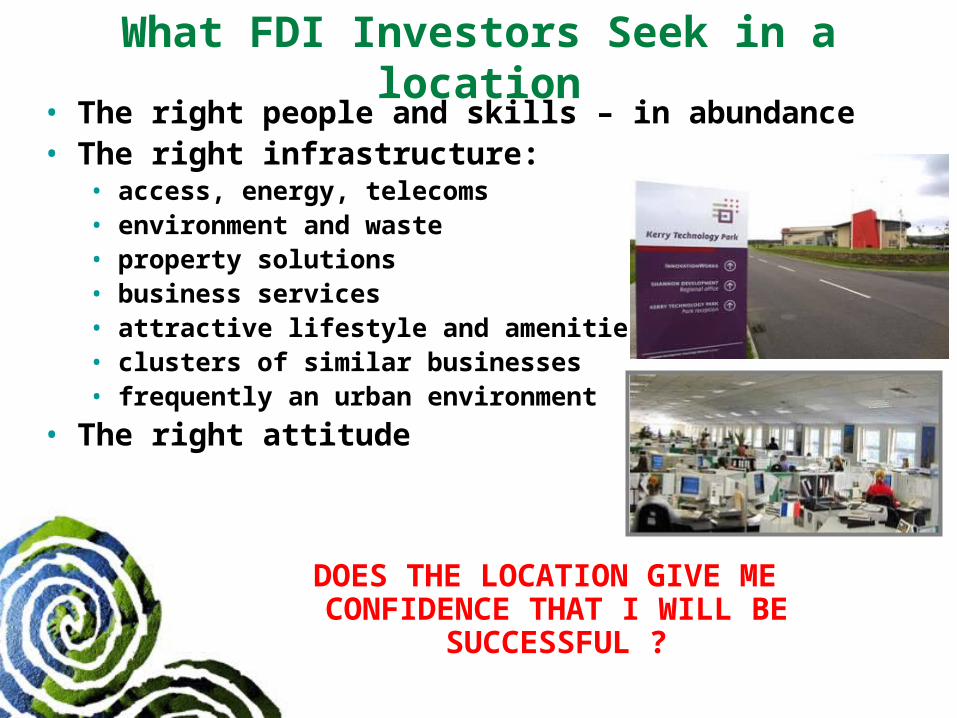

What FDI Investors Seek in a location• The right people and skills – in abundance• The right infrastructure:

• access, energy, telecoms• environment and waste• property solutions• business services• attractive lifestyle and amenities• clusters of similar businesses• frequently an urban environment

• The right attitude

DOES THE LOCATION GIVE ME CONFIDENCE THAT I WILL BE

SUCCESSFUL ?

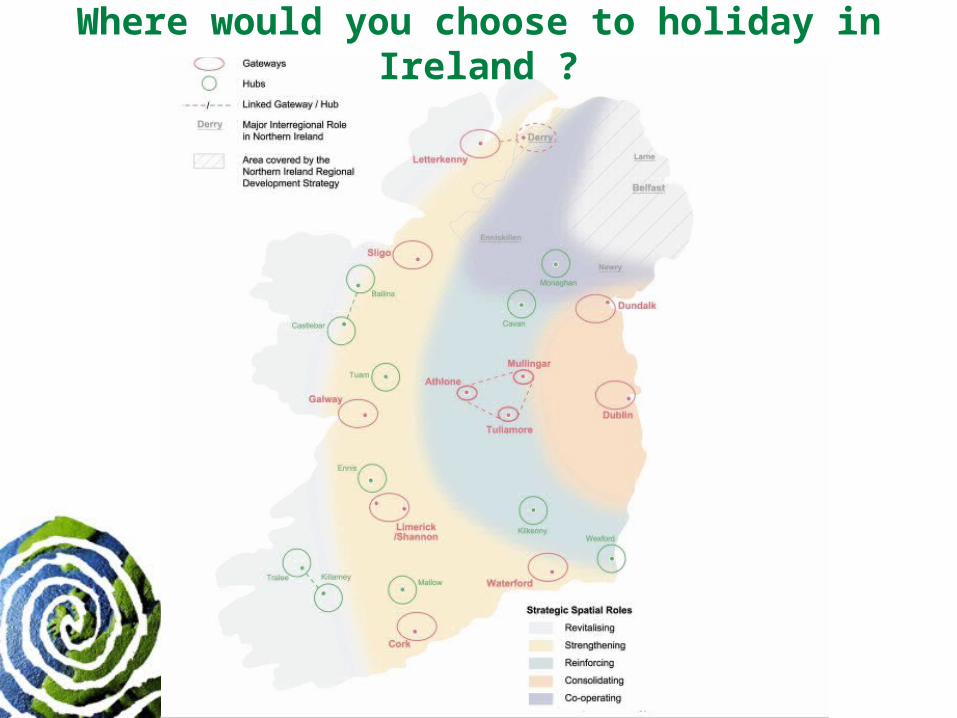

Where would you choose to holiday in Ireland ?

VISITOR ATTRACTIONS

FESTIVALS & EVENTS

EVENING ENTERTAINMENT

ACCOMMODATION

RESTAURANTS & PUBS

VISITOR SERVICES

INFRASTRUCTURE

Where would you choose to holiday in Ireland ?Components of a strong tourism centreComponents of a strong tourism centre

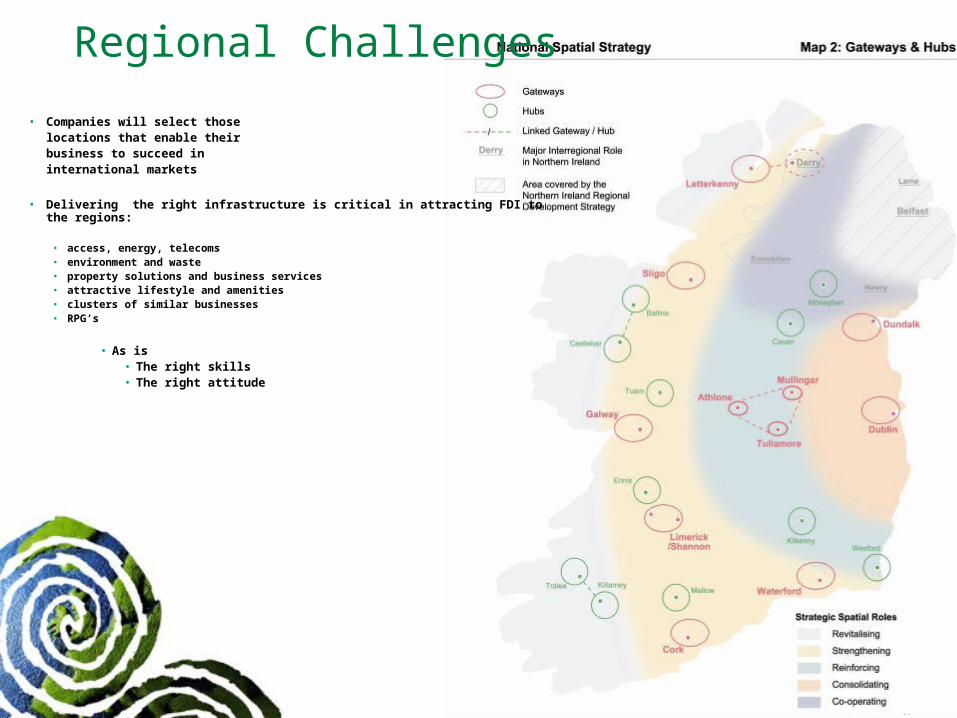

Regional Challenges

• Companies will select those locations that enable their business to succeed in international markets

• Delivering the right infrastructure is critical in attracting FDI to the regions:

• access, energy, telecoms• environment and waste• property solutions and business services• attractive lifestyle and amenities• clusters of similar businesses• RPG’s

• As is • The right skills• The right attitude

Gateway

Hub

Int Fin Services

ICT

Pharma

Med Tech

Globally Traded Business

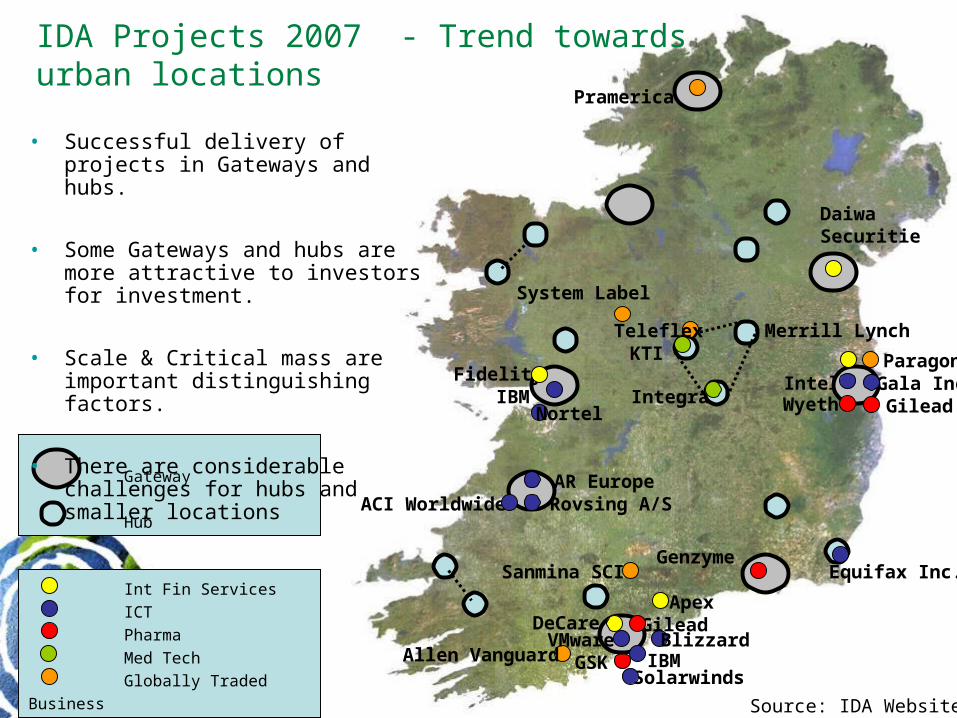

IDA Projects 2007 - Trend towards urban locations

Daiwa Securities

Intel

System Label

IBM

Equifax Inc.

IBMGSK

Integra

Gilead

Paragon

DeCare

ACI Worldwide Rovsing A/SAR Europe

Wyeth

Pramerica

Sanmina SCI

BlizzardAllen Vanguard

Solarwinds

Genzyme

Apex

Gala Inc.Gilead

VMware

KTIFidelity

• Successful delivery of projects in Gateways and hubs.

• Some Gateways and hubs are more attractive to investors for investment.

• Scale & Critical mass are important distinguishing factors.

• There are considerable challenges for hubs and smaller locations

Teleflex Merrill Lynch

Nortel

Source: IDA Website

Marketing Gateways & Hubs

Cork’s Development – reaching critical mass

• 27 Airlines• 850 flights weekly• 50+ international destinations

Professional Business Services (accountants, engineers, lawyers and others)

and .… Quality of Life

Clusters of similar and supporting businesses

Sell the region – not the town

• Population : 10,241

• Workforce: 4,624

• 3rd level colleges: 0

• Airports: 0

• Reference Companies: Kostal; ITW Hi-Cone; TR Southern Fastners, etc..

• Population: 689,012 within 60km.

• Workforce: 307,426 within 60km.

• 3rd level colleges: 5 colleges with access to 49,000 students.

• Airports: 3 international airports Reference Companies: approx 200 including Dell, Apple, EMC, Pfizer, GSK; Bank of New York, Kostal, McAfee, Kerry Group, Fexco, etc..

Innovative Property SolutionsKerry Technology Park, Tralee

• Vision for Seamless Integration of Education and Enterprise

• Shares 113 acre campus with ITT (Park area 52 acres)

• Joint KTP/ITT Physical Masterplan and Development Guidelines

• 26,000 sq ft InnovationWorks Building • 24,000 InnovationWorks 2 building• 16 companies on-site• Over 300 people employed• Active local Management• Shannon Development Investment to date:

€10m • Kerry Innovation Centre/ Campus Enterprise

Determination !West Cork Technology Park, Clonakilty

300,000 sq. ft. facility

Custom built office space from 2000 sq. ft. to 80,000 sq. ft.

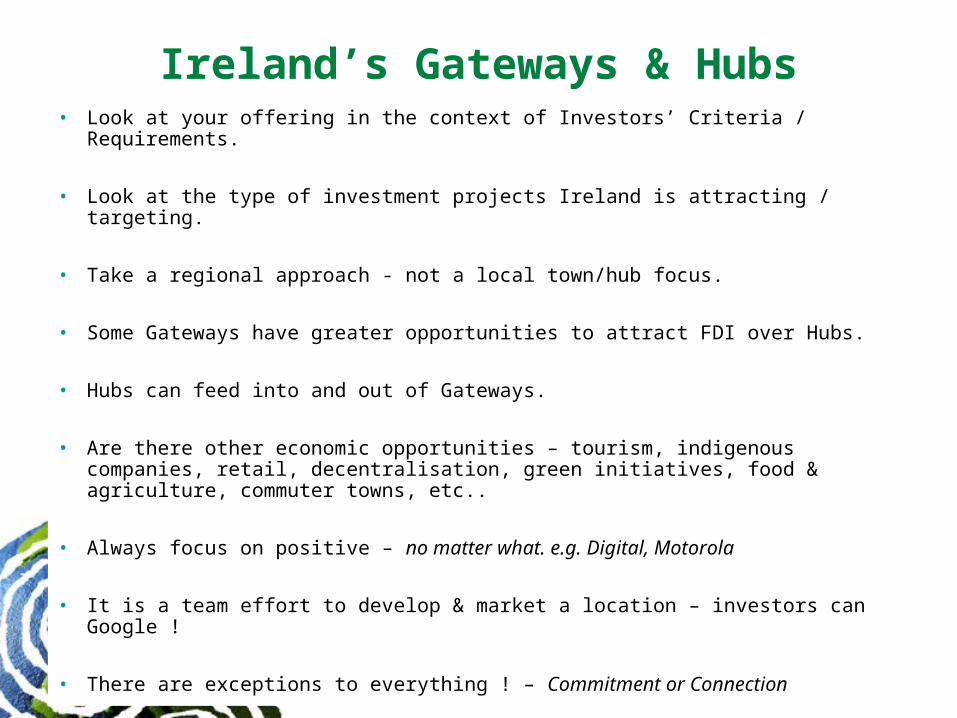

Ireland’s Gateways & Hubs• Look at your offering in the context of Investors’ Criteria / Requirements.

• Look at the type of investment projects Ireland is attracting / targeting.

• Take a regional approach - not a local town/hub focus.

• Some Gateways have greater opportunities to attract FDI over Hubs.

• Hubs can feed into and out of Gateways.

• Are there other economic opportunities – tourism, indigenous companies, retail, decentralisation, green initiatives, food & agriculture, commuter towns, etc..

• Always focus on positive – no matter what. e.g. Digital, Motorola

• It is a team effort to develop & market a location – investors can Google !

• There are exceptions to everything ! – Commitment or Connection

Ireland continues to win investment in 2008

Thank You

Ray O’ConnorRegional Manager

South-WestIDA Ireland

Support slides

Challenges/Opportunities for Mallow

• Companies will select those locations that enable their business to succeed in international markets

• How does Mallow link into the successful Gateway of Cork?

• Creating the distinctive pull factor for Mallow• ….what does it offer over other locations. • ….what does it offer to different sectors, sub sectors

• Regional Aid Guidelines phasing out for South Area

• Branding and identity

N

Mallow

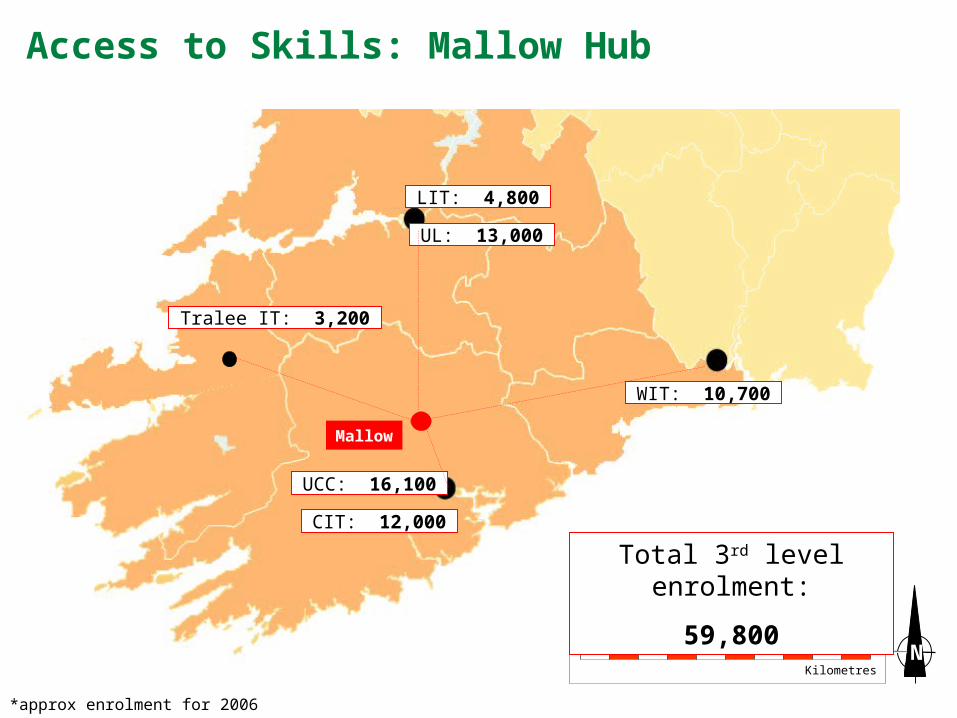

Tralee IT: 3,200

0 20 40 60 80 100

Kilometres

UL: 13,000

LIT: 4,800

UCC: 16,100

CIT: 12,000

WIT: 10,700

Total 3rd level enrolment:

59,800

*approx enrolment for 2006

Access to Skills: Mallow Hub

Mallow Key Selling Points: Infrastructure and Connectivity

Local Commitment to Business:-Mallow Chamber / Mallow Town Council

Hub location linking two Gateway towns of Limerick and Cork with access to People, Graduates and reference companies

Road & Rail Infrastructure Investment:Located on Atlantic Corridor - access to the primary route between Cork and Limerick/Shannon Continued Investment in Road & Rail

Broadband Connectivity:-fibre duct on rail line adjacent to town

Broadband capability provides the necessary connectivity for potential investors in Mallow

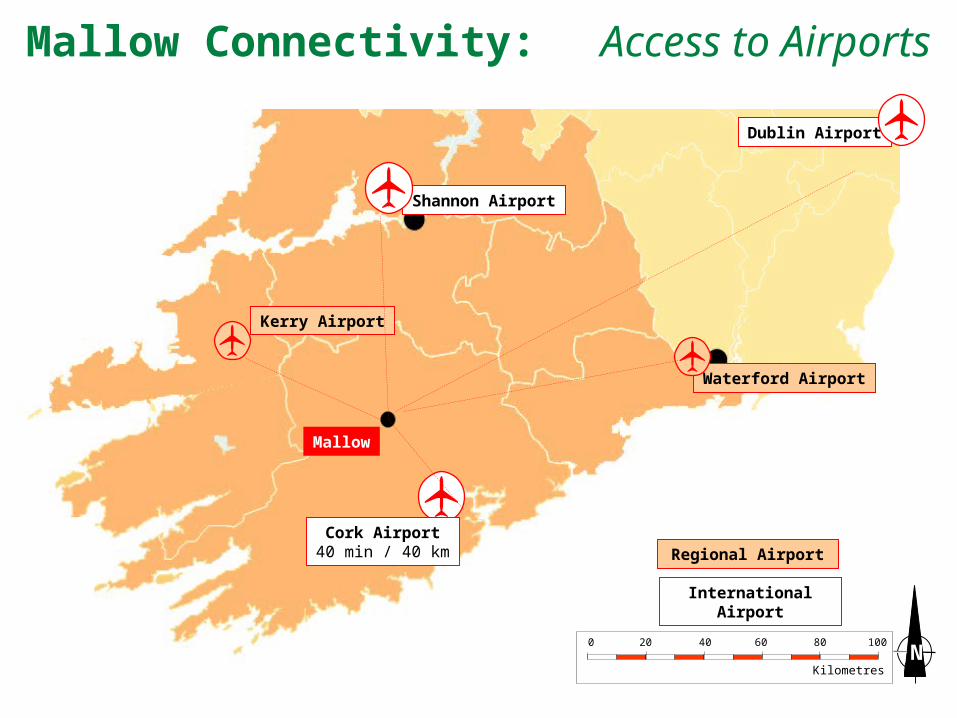

Air Access:-Three airports within 1hr 40 min of Mallow-Cork International Airport only 40 min from Mallow, servicing 850 weekly flights to 50 destinations by 27 airlines

Property Solutions

Mallow West - €500m worth of development on the 400-acre site.

N0 20 40 60 80 100

Kilometres

Mallow Connectivity: Access to Airports

Regional Airport

Kerry Airport

Waterford Airport

Shannon Airport

Dublin Airport

Cork Airport40 min / 40 km

International Airport

Mallow

Mallow: The need to create and communicate Mallow’s offering as an

investment location with the best of both worlds:

Skills Availability(,UCC,CIT, ITT, LIT. UL.. etc)

Access (40 min from Cork Int. Airport)

Infrastructure (Road Network, Rail connection, Broadband Connectivity)

Experience of Existing Companies

(Regional focus)

PLUS

More Cost Competitive (lower property costs, lower cost of living: house prices, childcare)

Less Traffic Congestion

Arguably Better Quality of Life (better work life balance)

Greater Staff Retention Rates

The Opportunity to be one of the Employers of Choice in a locality

Well-located business area,has access to the critical mass of:

The advantages of NOT being a city location:

![Flannery O’Connor[1]](https://static.fdocuments.in/doc/165x107/577d26321a28ab4e1ea080c5/flannery-oconnor1.jpg)