Ratemaking for Multi-Peril Crop Insurance

32

Ratemaking for Multi- Peril Crop Insurance CAS Seminar on Ratemaking Thomas Worth, Ph.D. Concurrent Session COM-7 Senior Actuary Philadelphia, PA Research and Development March 21-22, 2004 Risk Management Agency U.S. Dept. of Agriculture

-

Upload

dorian-morris -

Category

Documents

-

view

33 -

download

2

description

Ratemaking for Multi-Peril Crop Insurance. CAS Seminar on RatemakingThomas Worth, Ph.D. Concurrent Session COM-7Senior Actuary Philadelphia, PA Research and Development March 21-22, 2004 Risk Management Agency U.S. Dept. of Agriculture. - PowerPoint PPT Presentation

Transcript of Ratemaking for Multi-Peril Crop Insurance

Ratemaking for Multi-Peril Crop Insurance

CAS Seminar on Ratemaking Thomas Worth, Ph.D.

Concurrent Session COM-7 Senior Actuary

Philadelphia, PA Research and Development

March 21-22, 2004 Risk Management Agency U.S. Dept. of Agriculture

Mission of the Federal Crop Insurance Program

• “to promote the national welfare... through

a sound system of crop insurance”

• “provide the means for the research and experience helpful in devising and establishing such insurance.”

• FCIC Act, section 502(a), Feb. 16, 1938

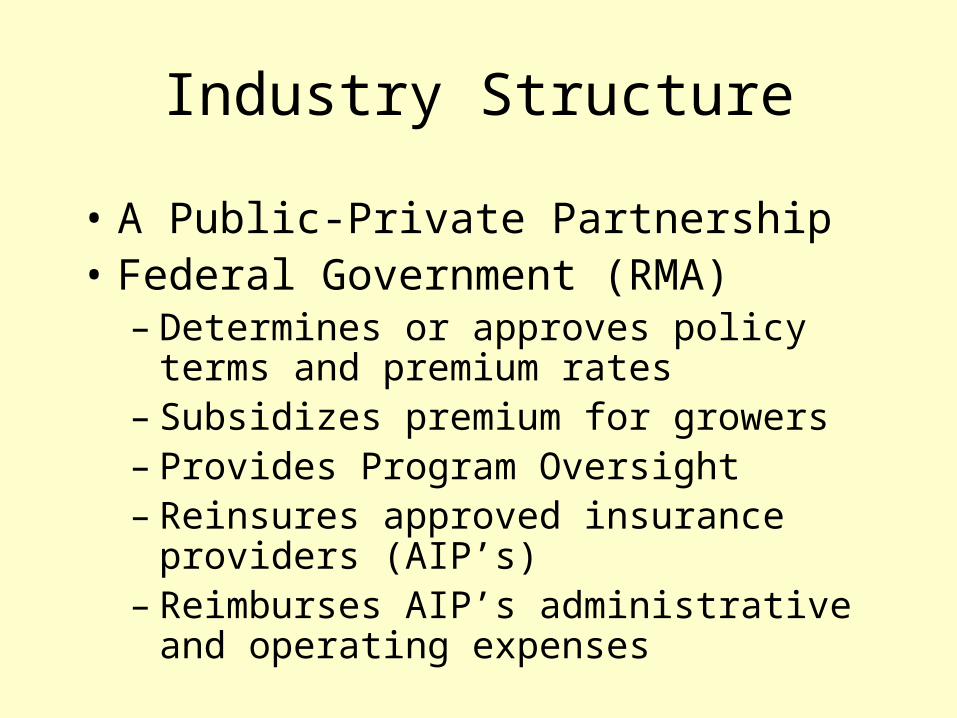

Industry Structure

• A Public-Private Partnership• Federal Government (RMA)

– Determines or approves policy terms and premium rates

– Subsidizes premium for growers– Provides Program Oversight– Reinsures approved insurance providers

(AIP’s)– Reimburses AIP’s administrative and operating

expenses

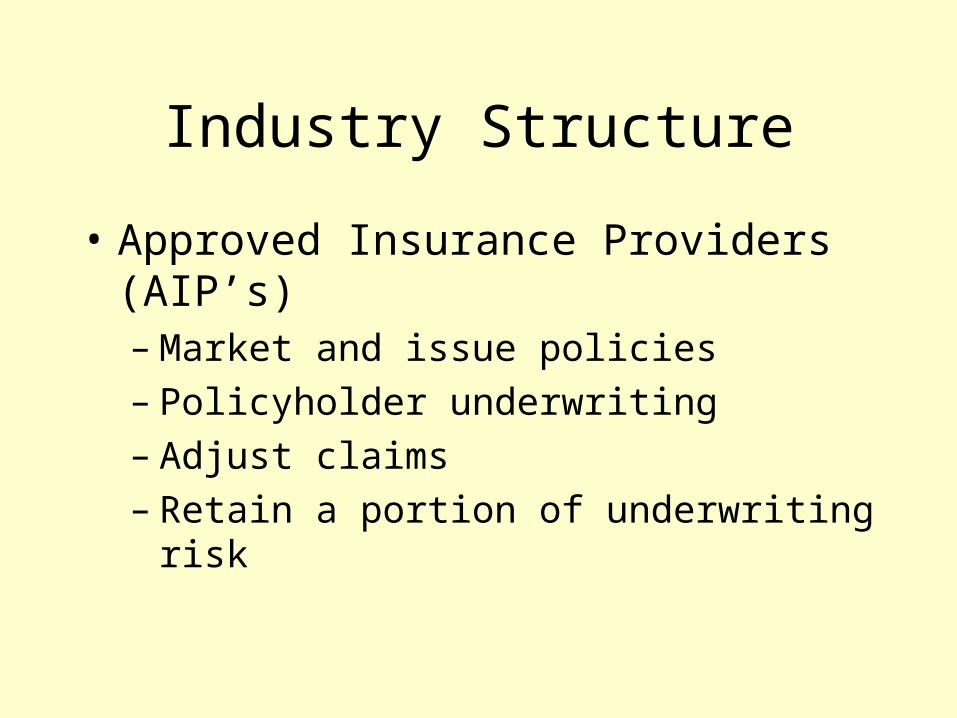

Industry Structure

• Approved Insurance Providers (AIP’s)– Market and issue policies– Policyholder underwriting– Adjust claims– Retain a portion of underwriting risk

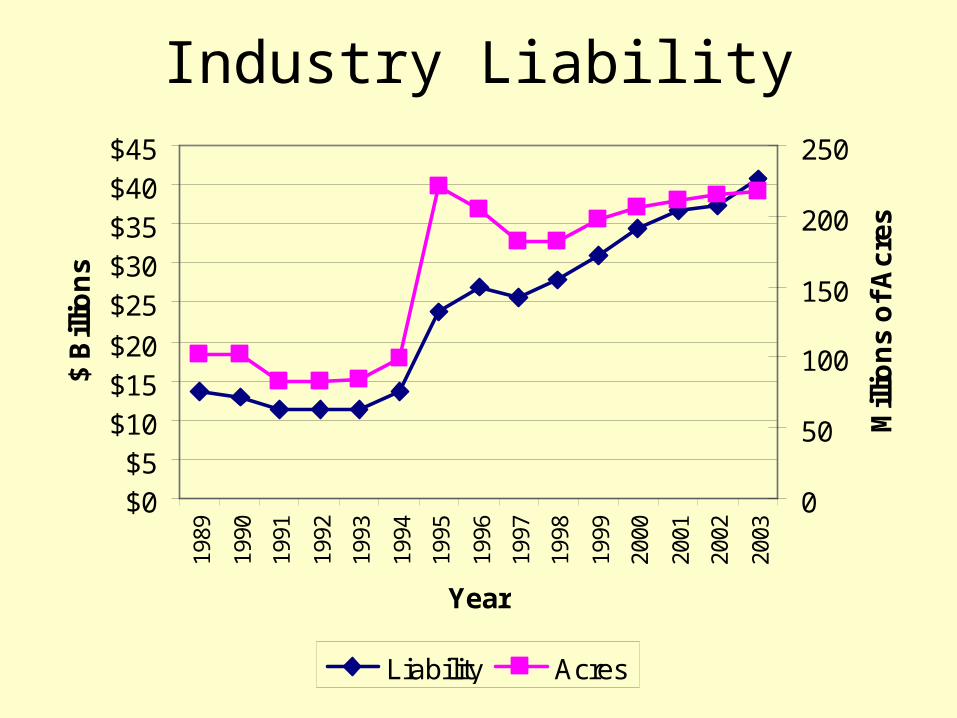

Industry Liability

$0$5

$10$15$20

$25$30$35$40$45

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

Year

$ B

illio

ns

0

50

100

150

200

250

Mill

ion

s o

f A

cre

s

Liability Acres

Industry Liability

Liabilityin Millions

0 to 1 (723)1 to 10 (973)

10 to 40 (850)40 to 100 (229)

100 to 451 (29)

2003 Total Liability All Crops

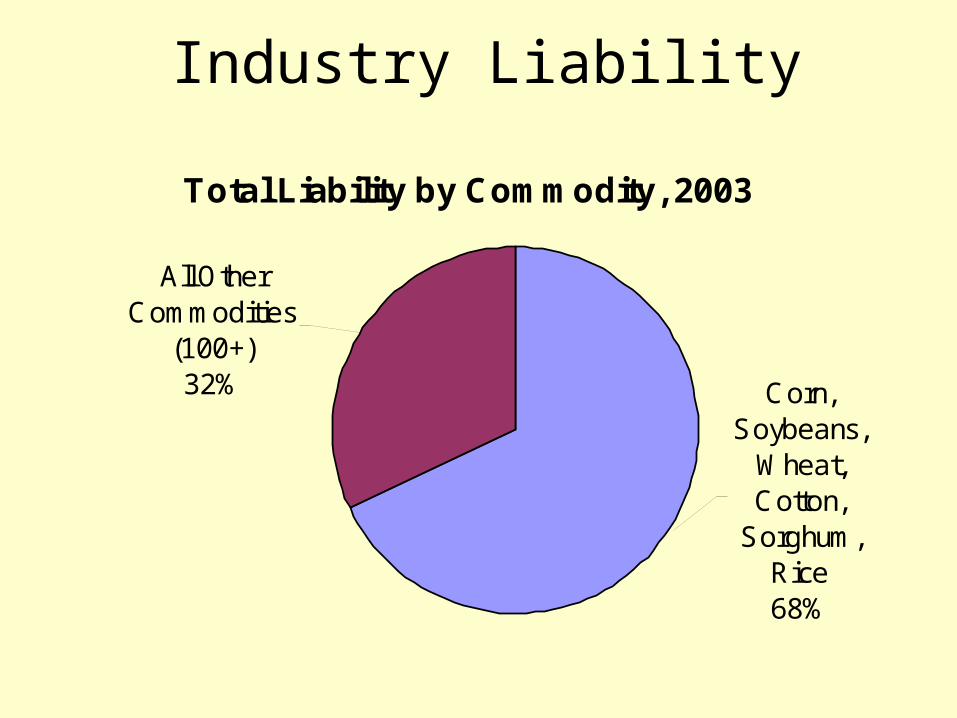

Industry Liability

Total Liability by Commodity, 2003

All Other Commodities

(100+)32% Corn,

Soybeans, Wheat, Cotton,

Sorghum, Rice68%

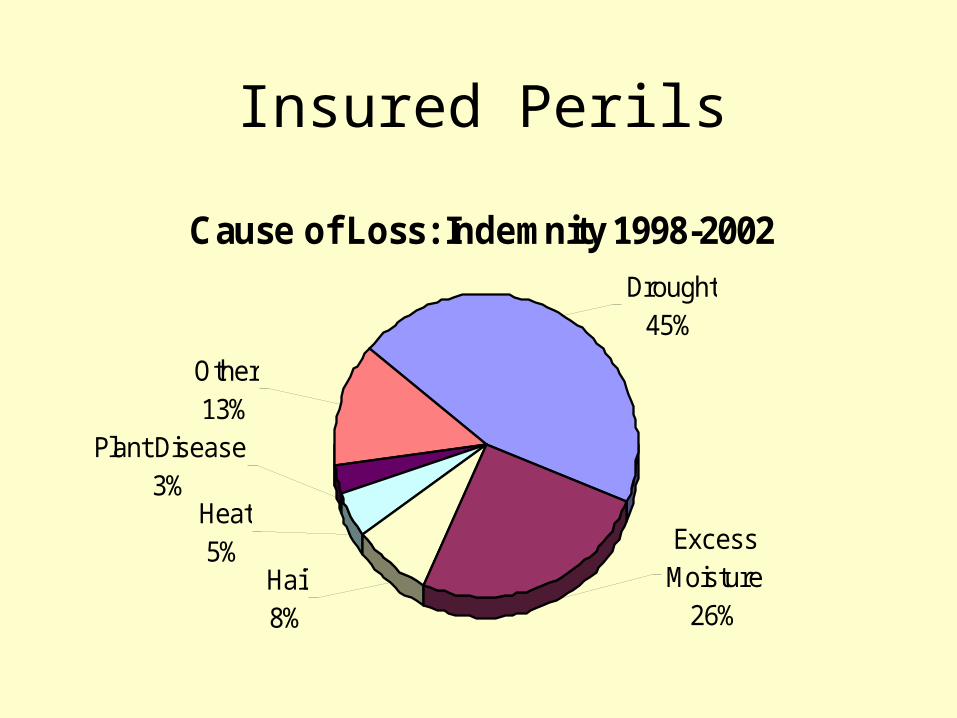

Insured Perils

Cause of Loss: Indemnity 1998-2002

Excess Moisture

26%

Plant Disease3%

Heat5%

Hail8%

Other13%

Drought45%

Crop Insurance Indemnity

Loss Ratios

0 to 0.5 (1310)0.5 to 1 (636)1 to 2 (559)2 to 4 (264)4 to 20.5 (49)

2001 Loss Ratios2001 Loss Ratios

Loss Ratios

0 to 0.5 (835)0.5 to 1 (534)1 to 2 (633)2 to 4 (601)4 to 17.5 (208)

2002 Loss Ratios2002 Loss Ratios

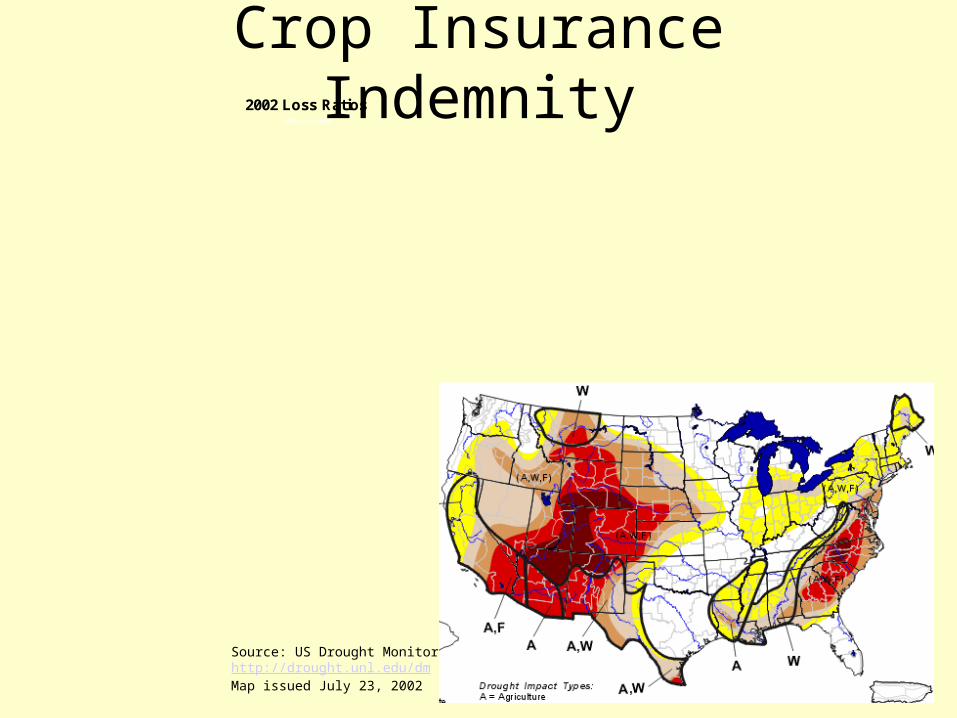

Crop Insurance Indemnity

Loss Ratios

0 to 0.5 (835)0.5 to 1 (534)1 to 2 (633)2 to 4 (601)4 to 17.5 (208)

2002 Loss Ratios2002 Loss Ratios

Source: US Drought Monitorhttp://drought.unl.edu/dmMap issued July 23, 2002

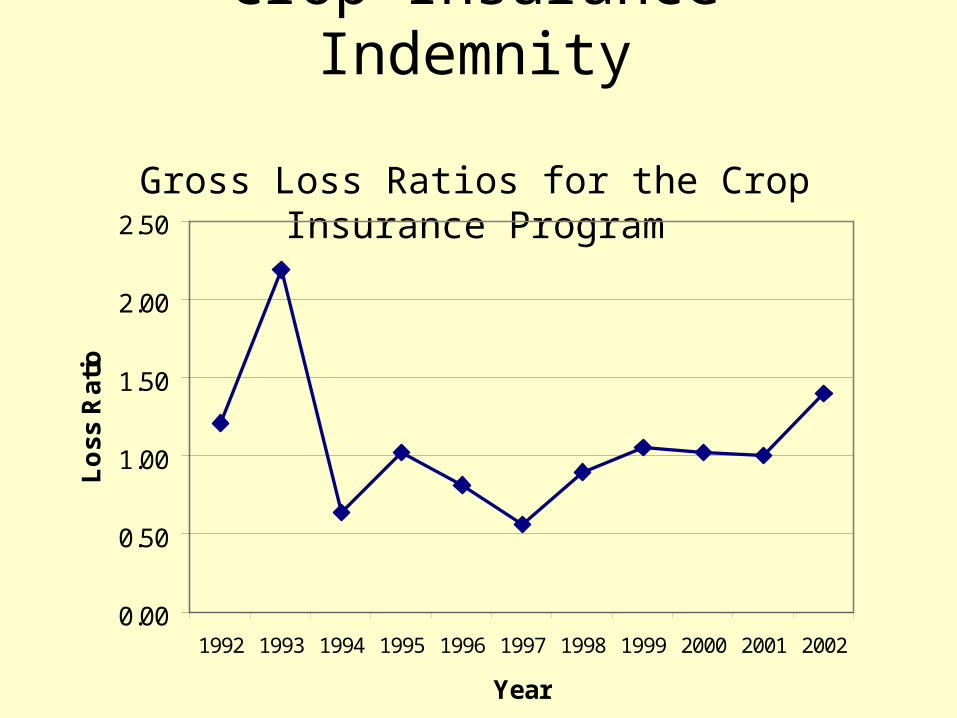

Crop Insurance Indemnity

Gross Loss Ratios for the Crop Insurance Program

0.00

0.50

1.00

1.50

2.00

2.50

1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002

Year

Lo

ss

Ra

tio

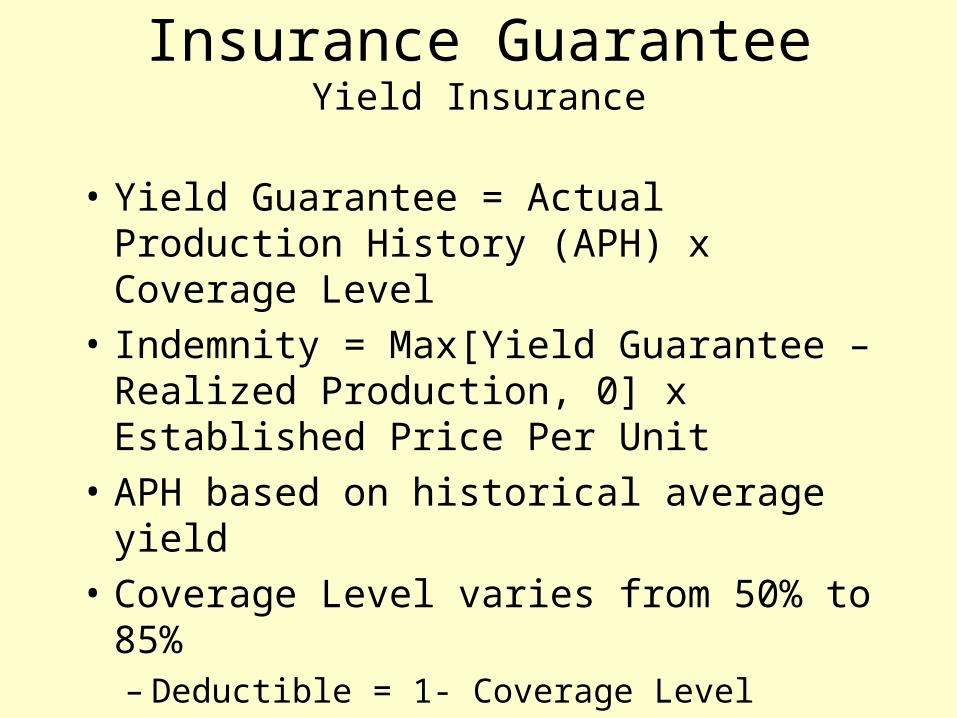

Insurance GuaranteeYield Insurance

• Yield Guarantee = Actual Production History (APH) x Coverage Level

• Indemnity = Max[Yield Guarantee – Realized Production, 0] x Established Price Per Unit

• APH based on historical average yield

• Coverage Level varies from 50% to 85%– Deductible = 1- Coverage Level

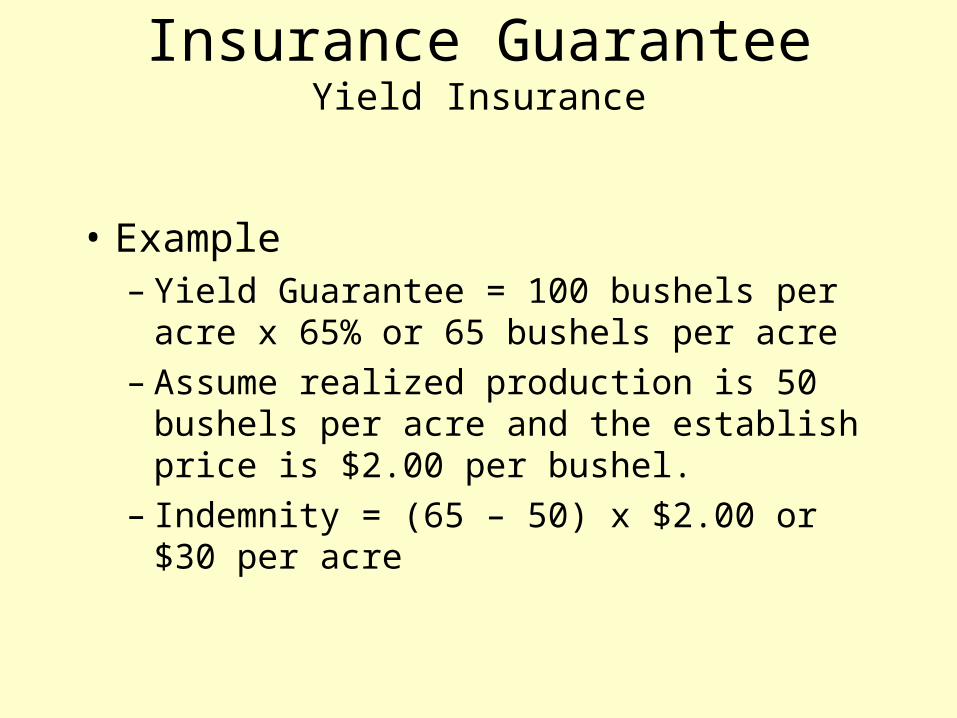

Insurance GuaranteeYield Insurance

• Example– Yield Guarantee = 100 bushels per acre x 65%

or 65 bushels per acre– Assume realized production is 50 bushels per

acre and the establish price is $2.00 per bushel.– Indemnity = (65 – 50) x $2.00 or $30 per acre

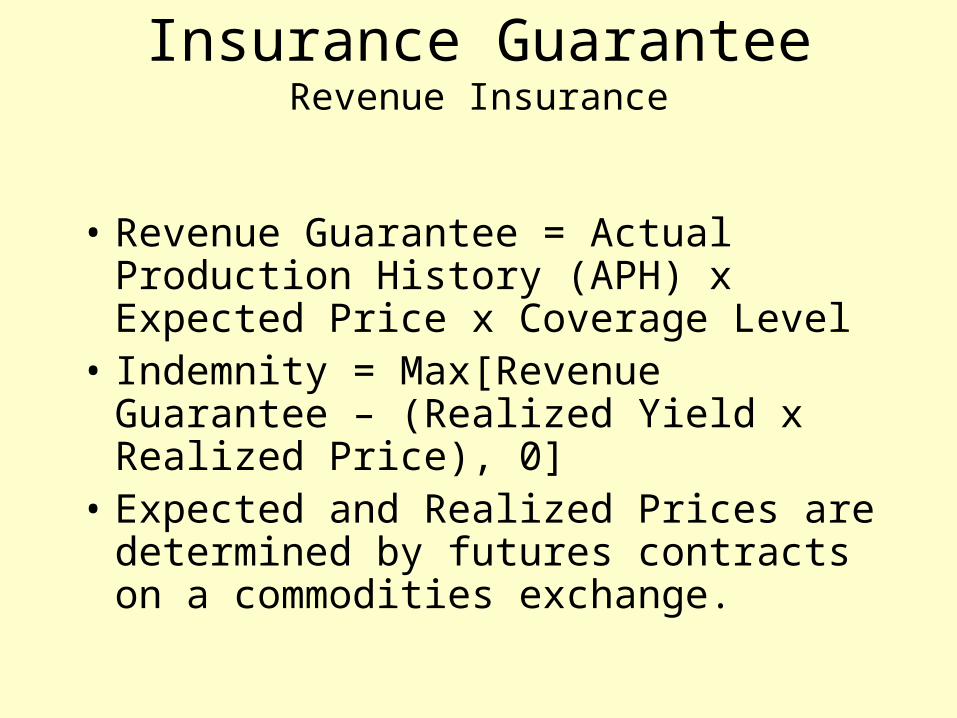

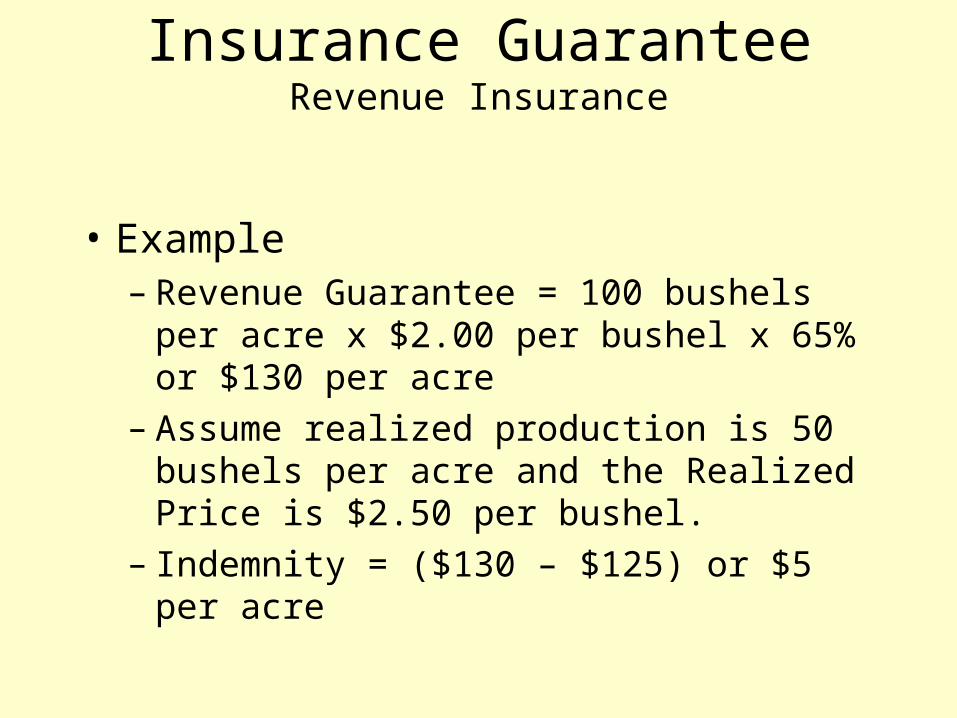

Insurance GuaranteeRevenue Insurance

• Revenue Guarantee = Actual Production History (APH) x Expected Price x Coverage Level

• Indemnity = Max[Revenue Guarantee – (Realized Yield x Realized Price), 0]

• Expected and Realized Prices are determined by futures contracts on a commodities exchange.

Insurance GuaranteeRevenue Insurance

• Example– Revenue Guarantee = 100 bushels per acre x

$2.00 per bushel x 65% or $130 per acre– Assume realized production is 50 bushels per

acre and the Realized Price is $2.50 per bushel.– Indemnity = ($130 – $125) or $5 per acre

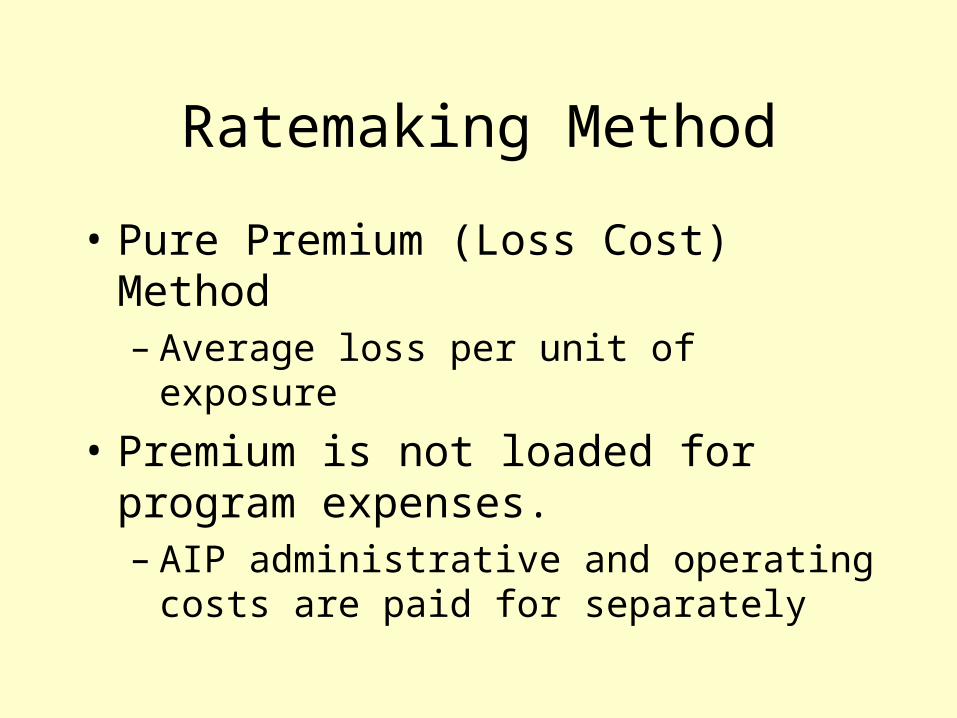

Ratemaking Method

• Pure Premium (Loss Cost) Method– Average loss per unit of exposure

• Premium is not loaded for program expenses.– AIP administrative and operating costs are paid

for separately

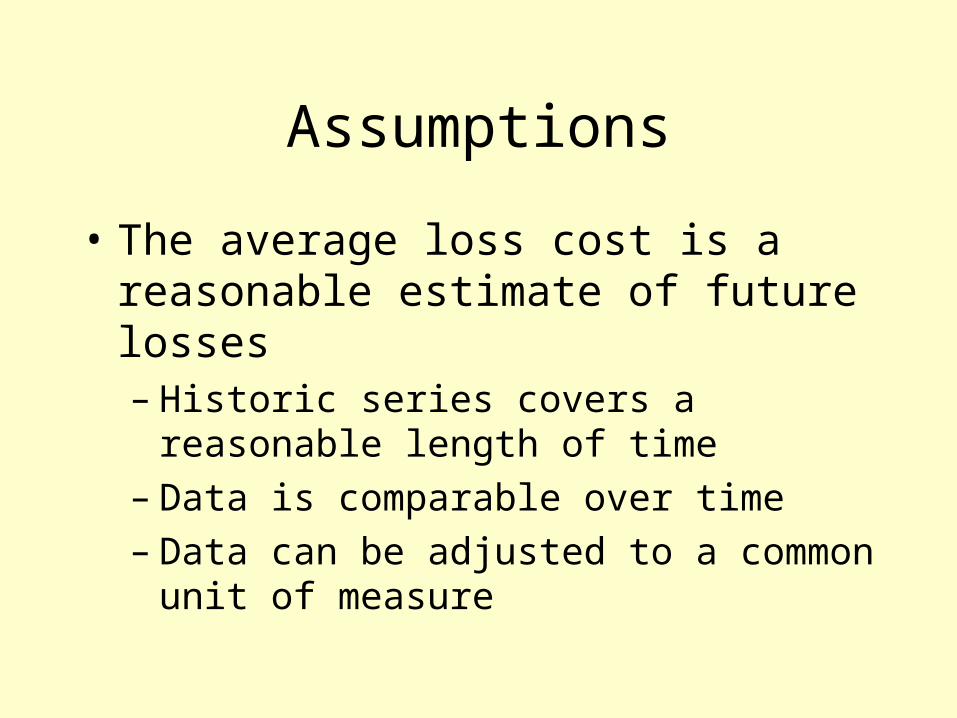

Assumptions

• The average loss cost is a reasonable estimate of future losses– Historic series covers a reasonable length of

time– Data is comparable over time– Data can be adjusted to a common unit of

measure

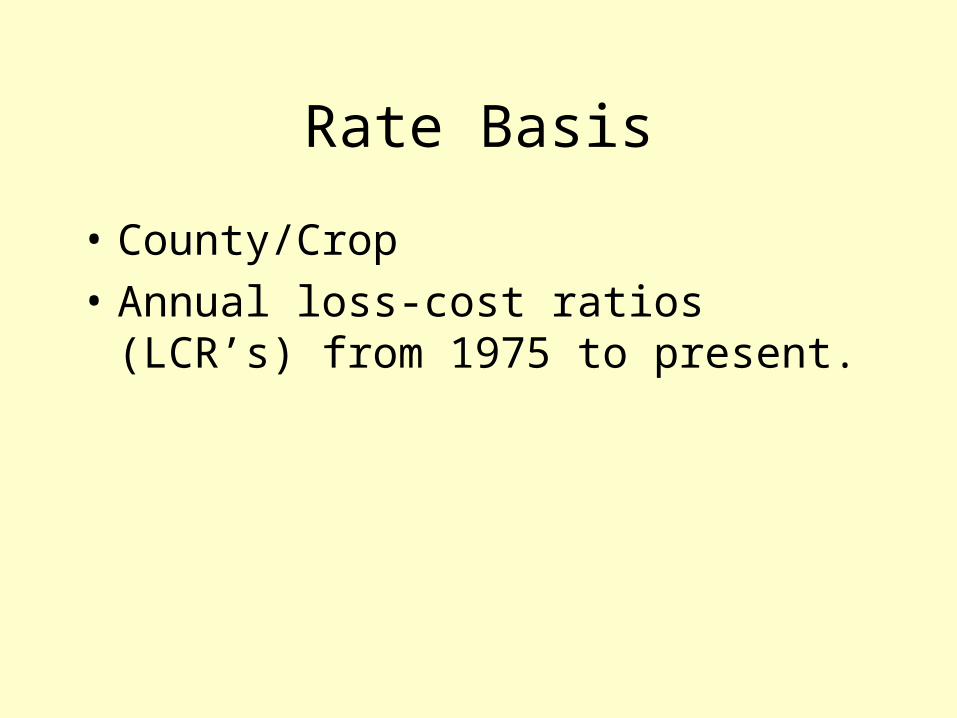

Rate Basis

• County/Crop

• Annual loss-cost ratios (LCR’s) from 1975 to present.

Rating ProcessAdjusting Loss and Exposure to a Common Unit

• Historic data is adjusted to a common coverage level -- 65%.– Most business is around this coverage level.

• The liability and indemnity of all growers in a county are adjusted to reflect the values that would have been reported had the coverage been purchased at the 65% level.

• Adjusting lower coverage levels up to 65% requires estimation.

Rating ProcessDevelop Unloaded County Base Rates

• Adjusted data is used to derive historic annual LCR’s for each crop and county.

• Each county’s LCR is capped at the 80th percentile.– Losses above the cap are pooled at the state

level

• Each county’s capped LCR is averaged with those of surrounding counties.– The amount of weight given to surrounding

county LCR’s is determined by a credibility measure

Rating ProcessDevelop Loaded County Base Rate

• Several loads are applied to the unloaded county base rate.– Disaster Reserve Factor– State Excess Load– Prevented Planting Load– Unit Division Factor

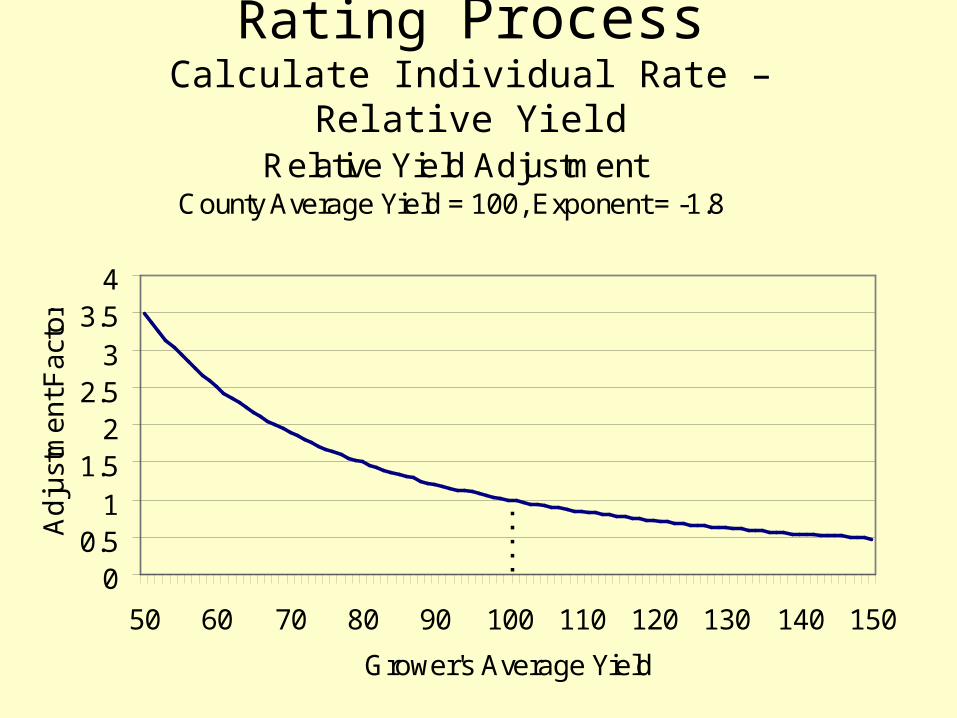

Rating ProcessCalculate Individual Rate – Relative Yield

• The county rate reflects rates for growers whose average yield is at the county average yield.

• Probability of loss is correlated with grower’s average yield relative to the county average yield.– The probability of loss is lower for growers

with an average yield that is above the county average.

– Vice-versa.

• [Grower Yield/County Avg Yield]Exponent

Rating ProcessCalculate Individual Rate – Relative Yield

Relative Yield AdjustmentCounty Average Yield = 100, Exponent = -1.8

00.5

11.5

22.5

33.5

4

50 60 70 80 90 100 110 120 130 140 150

Grower's Average Yield

Ad

just

me

nt F

act

or

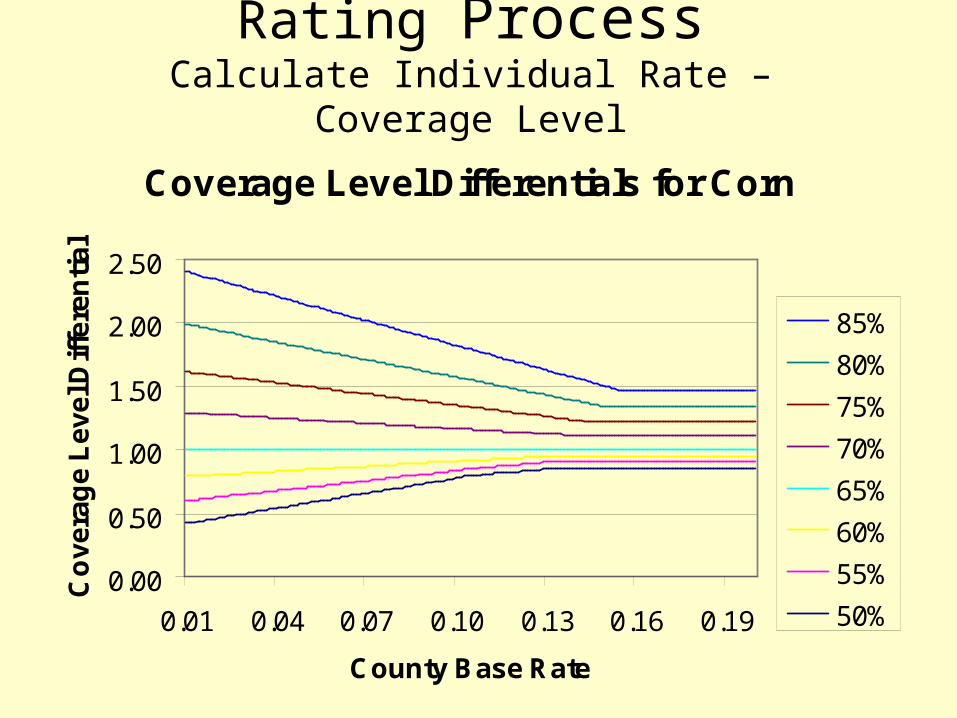

Rating ProcessCalculate Individual Rate – Coverage Level

• County base rate is for the 65% coverage level.

• Rate is adjusted by a coverage level differential (factor) to derive a rate for other coverage levels.

• The differential varies by county base rate.

Rating ProcessCalculate Individual Rate – Coverage Level

Coverage Level Differentials for Corn

0.00

0.50

1.00

1.50

2.00

2.50

0.01 0.04 0.07 0.10 0.13 0.16 0.19

County Base Rate

Co

ve

rag

e L

ev

el D

iffe

ren

tia

l

85%

80%

75%

70%

65%

60%

55%

50%

Rating ProcessSummary

• The final rate is the county base rate with cumulative adjustments.– Relative Yield– Coverage Level– Unit Division Factor– Type Practice Factors

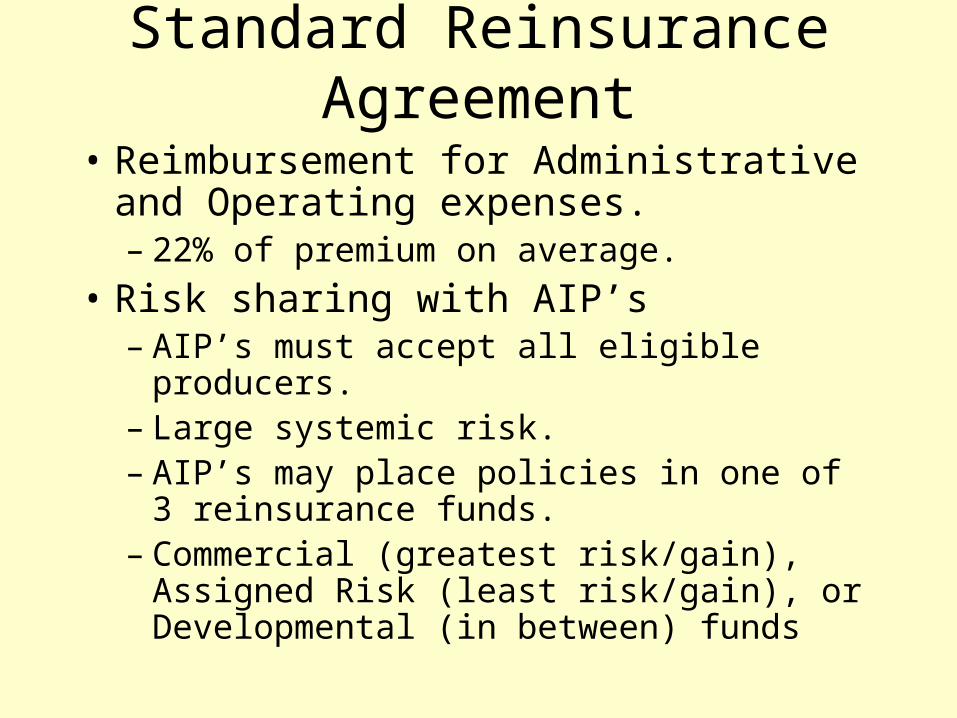

Standard Reinsurance Agreement

• Reimbursement for Administrative and Operating expenses.– 22% of premium on average.

• Risk sharing with AIP’s– AIP’s must accept all eligible producers.– Large systemic risk.– AIP’s may place policies in one of 3

reinsurance funds.– Commercial (greatest risk/gain), Assigned Risk

(least risk/gain), or Developmental (in between) funds

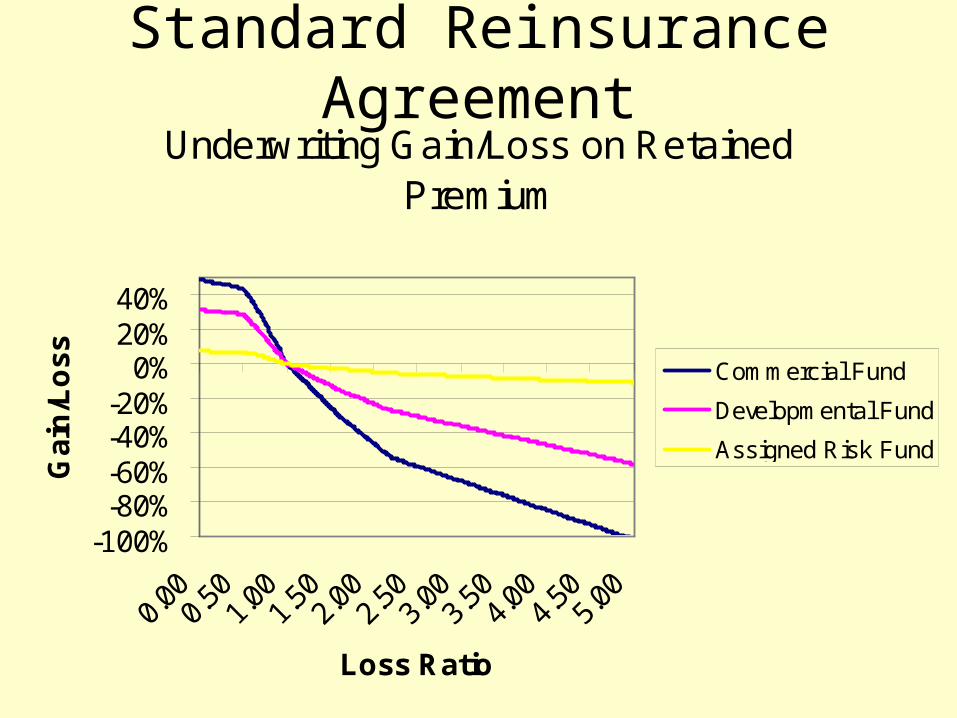

Standard Reinsurance AgreementUnderwriting Gain/Loss on Retained

Premium

-100%-80%-60%-40%-20%

0%20%40%

0.00

0.50

1.00

1.50

2.00

2.50

3.00

3.50

4.00

4.50

5.00

Loss Ratio

Ga

in/L

os

s

Commercial Fund

Developmental Fund

Assigned Risk Fund

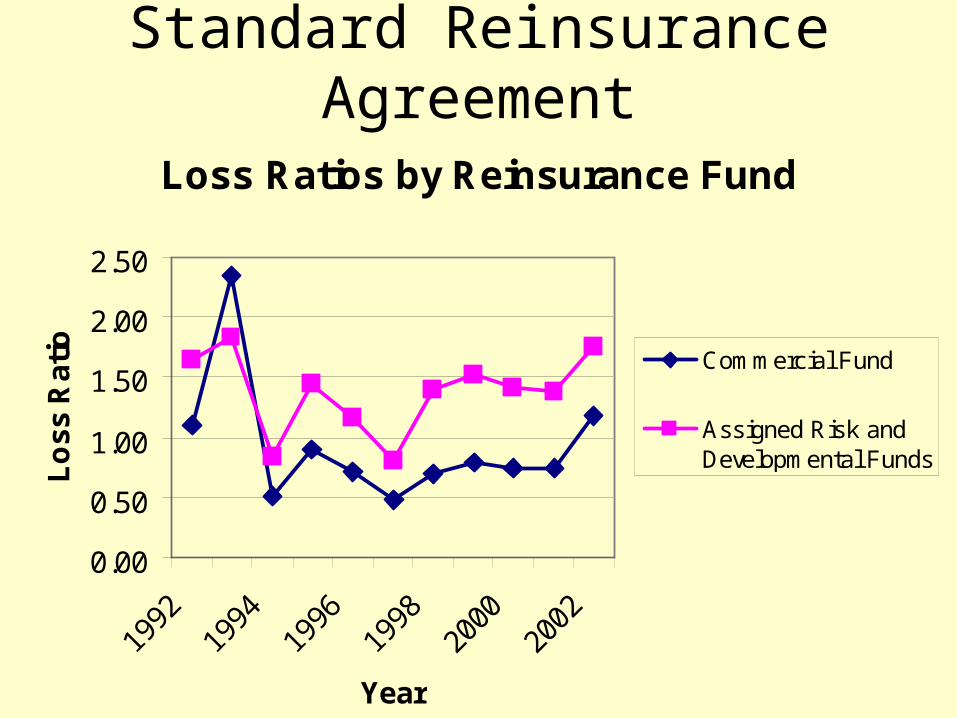

Standard Reinsurance Agreement

Loss Ratios by Reinsurance Fund

0.00

0.50

1.00

1.50

2.00

2.50

1992

1994

1996

1998

2000

2002

Year

Lo

ss

Ra

tio

Commercial Fund

Assigned Risk andDevelopmental Funds

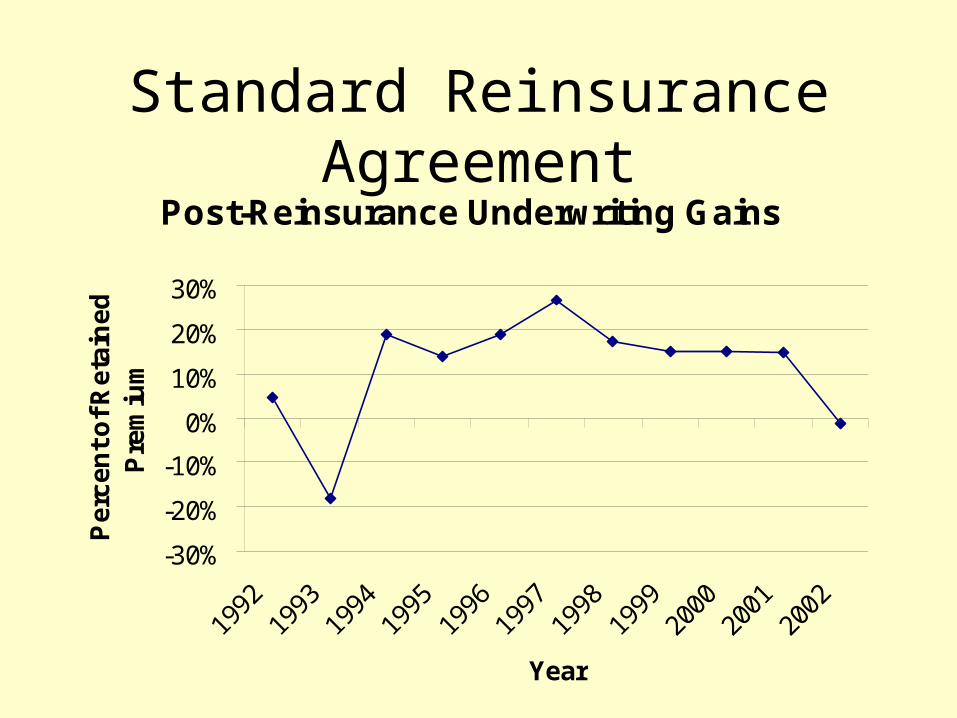

Standard Reinsurance AgreementPost-Reinsurance Underwriting Gains

-30%

-20%

-10%

0%

10%

20%

30%

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

Year

Pe

rce

nt

of

Re

tain

ed

P

rem

ium

Standard Reinsurance Agreement

• Agricultural Risk Protection Act of 2000:– Government “may renegotiate the Standard

Reinsurance Agreement once during the 2001 through 2005 reinsurance years.”

– Negotiations are under way.– An initial draft of the new SRA is available on

RMA’s website.

Thank You

Visit the RMA website for more information:

www.rma.usda.gov