Raport Anual Banca Comerciala Ion Tiriac 2003

87

-

Upload

aurelian-buliga-stefanescu -

Category

Documents

-

view

34 -

download

2

Transcript of Raport Anual Banca Comerciala Ion Tiriac 2003

HIGHLIGHTS Income Statement

2003 Net interest income 40,055 Net fee and commission income 15,404 Other income 2,136 Operating income 57,595 Operating profit* 18,206 Profit after lax 11,188

Balance Sheet Total assets Risk weighted assets Liquid assets Loans, gross value: - individuals - companies

Due to banks Due to clients - individuals - companies

IFRS â '000 2002 2001

22,298 24,468 15,379 16,649 6,016 1,674

43,692 42,791 11,611 8,751 10,324 8,036

IFRS â '000 481,596 401,276 379,440 354,806 255,902 218,937 136,731 156,725 177,818 287,336 176,242 133,064 143,842 42,418 8,342 143,494 133,824 124,722

Shareholders' equity 75,089 55,606 45,538

Key Profitability Ratios Operating return on average equity 27.86% 22.96% 21.08% Operating return on average assets 4.12% 2.97% 2.36% Net return on average equity 17.12% 20.42% 19.36% Net return on average assets 2.53% 2.64% 2.1 7% Net return on average risk weighted assets 3.66% 4.35% 3.62% Cost I income ratio** 58.59% 76.40% 76.99%

Key Capital Ratios Tier 1 capital ratio 21.16% 21.73% 20.80% Total capital ratio 21.16% 21.73% 20.80% Equity 1 total assets 15.59% 13.86% 12.00%

Shares Outstanding shares 11,800,472 7,142,616 5,278,128 Operating profit per share â 2.00 €1. ? 1.66 Net profit per share â 1.23 €1. ? 1.52

Branch Network ATM Network POS Network Employees

Fitch Ratings Short term B B B Long term B B B-

* Profit before tax and impairment of property.

** Cost to income ratio: all non interest expenses, excluding ttie impairment of property and exceptional depreciation / net operating income.

Highlights

Foreword by the President 1

Corporate Governance 3Mission, Vision and ValuesShareholders Board of Directors Management Committee

Banca }iriac’s 2003 Achievements 7

Bank’s Profile 9Individual Banking Commercial BankingCardsBancassuranceTreasuryInternational ActivityRisk ManagementHuman Resources

Report of Independent Auditors and Financial Statements 19

Network and Contacts 75

Financial Calendar 2004 / 2005

CONTENTS

FOREWORD BY THE PRESIDENT

FOREWORDBY THE PRESIDENT

chapter 1

Dear shareholders, clients and colleaguesPromised and delivered, daring but rewarding, this was briefly 2003.On behalf of the Managing Board, I am proud to break this good newsto you. The commitments to reach the ambitious targets we undertooksome years ago, we fulfilled last year.

I address this message with a feeling of pride considering the bank’sremarkable achievements in 2003, which have positioned Banca }iriacamong the top financial institutions in Romania.

The bank’s performance came along with an improved macroeconomic framework and a better shapedand strengthened Romanian banking sector. Also the world economy had an upturn.

The year 2003 represented for Banca }iriac the confirmation of the success of the restructuring processassumed in 2000 at the level of all structural components of the bank: systems, concepts, business lines,organization and distribution networks.

Despite a banking sector characterised by an increased competition, Banca }iriac’s performance wasimpressive.

First, the financial performance of the bank in 2003 was one of the best in the banking system, Banca}iriac ranking third place with 6% of the banking system’s net profit while holding a 3.2% market share oftotal banking assets. A very important aspect is that this level of profitability was achieved while observingall prudential exposure limits imposed by the authorities.

The operating profit reached a record ¤ 18.2 million, 57% up from 2002, showing the outstandingperformance of the core business of the bank.

Second, with the capital base substantially consolidated in the last three years, both through retainedearnings and new cash contributions of the shareholders, the bank managed to significantly increase itsbalance sheet to ¤ 481.6 million at the end of 2003. This strong development was mainly led by a unique63% growth of the loan portfolio which reached ¤ 287.3 million at year end.

Following the increased focus the bank has placed in the past years on retail, lending to individuals rose to50% in total loans portfolio, being 2.4 times higher than the 2002 year’s end level. Banca }iriac qualified asone of the top players in this market segment, ranking as number 4 among peer banks.

The development of the loans portfolio was mainly sustained by increasing clients’ deposits which reached¤ 375.6 million at the end of 2003 and by the continuous increase in shareholders’ equity to ¤ 75 million.

The range of products and services provided was enlarged, while we strove for higher standards in termsof both quality and speed. Our distribution network has been expanded through new branches andagencies in locations with economic potential and through ATM’s and POS’s.

The client oriented approach contributed to a 68% increase in the number of clients, the clients’ portfolioreaching 583,890 at the end of the year.

George Toma MucibabiciPresident and CEO

page

1

FOREWORD BY THE PRESIDENT

page

2

George Toma MucibabiciPresident and CEO

FORE

WOR

D BY

THE

PRE

SIDE

NT

How do we see the future?

We believe that the Romanian economy will continue to perform well in 2004, confirming the positive trend of the previous years. The economic growth, the stability and improvement of the fiscal system are prerequisite for further development and consolidation of the banking system.

Banca Tiriac is clearly on an ascendant successful course. This is both rewarding and challenging. Rewarding - for all the hard work and dedication of our committed staff and for the confidence and support extended by our shareholders. Challenging - as success means even harder work to further develop the bank’s operations on an increasingly competitive market.

Our future plans and strategy envisage an ongoing development of the retail operations and an increased business volume on the corporate segment, while maintaining a balanced weight between our retail and corporate loans portfolio. In addition to profitable customer oriented services and cost control, risk management and adequate solvency remain our priorities. We will strive for higher profitability and market share.

The sound growth of last year is indicative of the focus and commitment to build our existing businesses. Increasing profitability, improving efficiency and enhanced brand awareness are key directions to pursue for delivering higher value to our shareholders.

CORPORATEGOVERNANCE

chapter 2

CORPORATE GOVERNANCE

page

3

CORPORATE GOVERNANCE

CORPORATE GOVERNANCEMission statementBanca }iriac aims to maximize the shareholder value, by achieving an optimum convergence between the interests of its clients,employees and shareholders.

Vision statementBanca }iriac wants to be a leading, innovative and customer-focused institution, that provides best quality and integrated financialservices to both individuals and companies, including small and medium-sized companies.

ShareholdersBanca }iriac is the result of the courage and the vision of its founding members – Mr. Ion }iriac and his group of companies.Some 5,500 individuals and companies joined this initiative as shareholders.

Since the beginning, the bank has benefited from an excellent reputation, which was further enhanced when European Bank forReconstruction and Development (EBRD) became a shareholder in the bank in April 1993. The investment in Banca }iriac wasEBRD’s first participation in an Eastern European bank.

The ownership structure as of December 31st, 2003:

Banca }iriac delivers under its brand:

Leading values and principles

PROFESSIONALISM INTEGRITY FLEXIBILITY

EXCELLENCE

• High quality services provided to clients;• Highly professional staff and open career

opportunities;• Increasing bank’s value for the benefit of the

shareholders.

CONFIDENCE INNOVATION

through

Mr. Ion }iriac and his group of companies EBRD Others73.61 % 5.43 % 20.96 %

Romanian Individuals

Foreign Individuals

ForeignCompanies

Romanian Companies

14.3%

34.6%

1.2%

49.9%

0

200

400

600

800

1000

1200

1999 2000 2001 2002 2003

207.0

490.9 490.9

664.3

1097.4

Ownership structure, end of 2003 Share capital (year end statutory figures)(ROL billion)

Over the years the bank’s shareholders have shown their strong support to the bank, sustaining both the restructuring processand the business development. The share capital increases, through both new cash subscription and reinvested dividends, havesecured an adequate level of the capital base.

• Recognition of the bank as a stable and solif institution;

• High moral and ethical standards, fair treatment and confidentiality.

• Promoter of competitive and innovative products, services, and concepts.

page

4

CORP

ORAT

E GO

VERN

ANCE

Board of DirectorsEXECUTIVE MEMBERS

• Chairman of the Board and CEO since August 2003.• Joined the Board in October 2001 as First Deputy Chairman.• Former General Director of Credit and Market Operations Department in National Bank of Romania.• Former Advisor to the Executive Director for the Constituency of Netherlands within IMF.• Alternate Member of the Investment Committee of the IMF Staff Retirement Plan.• Former President of ACI- Financial Market Association Romania, currently honorary member.• Executive Committee Member of ACI-FMA as Sub-Regional Executive for Central and Eastern Europe.

George Toma Mucibabici 44

• Vice chairman of the Board since April 1997.• Joined the bank in March 1991 and was entrusted with increased levels of responsibility from head of

department to vice chairman.• Responsible for Individual Banking, Work Out Unit, Cards Operations and Bancassurance.• President of the Romanian Cards Fraud Forum and member of the Board of Directors of Allianz-}iriac

Asigur`ri.

C`t`lin Pårvu 47

• Vice chairman of the Board since August 2003.• Joined the bank in February 2000 as Chief Financial Controller.• Responsible for Internal Audit, Controller, Strategy & Research and General Secretariat.• Vice-president of the Romanian Credit Bureau.• Former CFO in Shell Romania Exploration BV, ING Bank and MOL Romania.

Florian Kubinschi 44

page

5

Ion Nestor 51

• Member of the Board since November 1999.• Director of Autorom, Mercedes Benz’s representative office in Romania.• Owner of the marketing company WSM, based in Munich, Germany.

Dan Petrescu 50

Victor Anagnoste 76

Christodoulakis Theodorou 52

NON-EXECUTIVE MEMBERS

Ion }iriac 65

• Member of the Board since 1991. • Founder of the bank and the major shareholder.• Coach and manager of famous tennis players, manager of some first class ATP and WTA tennis

tournaments.• Investor and businessman, holds import licenses for ten automotive brands: Mercedes Benz, Smart,

Chrysler, Jeep, Mitsubishi, Ford, Mazda, Jaguar, Land Rover and Hyundai.• Other strategic investments: Allianz-}iriac Asigur`ri, }iriac Leasing, Metro Cash and Carry, }iriac Air and

Casa Copilului Foundation.• Former member of the National Ice Hockey team, 9 times Romania’s Tennis National Champion, 150

participations as a tennis player in the Davis Cup, including 3 Cup Finals, over 40 international tennistitles.

• Chairman of the Romanian Olympic Committee, Honorary Chairman of the Romanian Tennis Federation.

CORPORATE GOVERNANCE

• Member of the Board since April 2001. • Lawyer in Bucharest and previously in Galati and Birlad.• Member of the Romanian Senate 1990-1991.• Former President of the Romanian Lawyers Union, former Director of the International Legal Assistance

Bureau, former Vice-president of the Bucharest Lawyers Association and President of the Galati LawyersAssociation.

• Member of the Board since August 2003.• Chief Financial Officer of }iriac Holdings Ltd. Cyprus.• Member of the Institute of Chartered Accountants in England and Wales. Member of the Cyprus Institute of

Certified Public Accountants.• Former Vice-president and President of the VAT Committee of the Cyprus Institute of Cer tified Public

Accountants.• Former Director of the VAT Department of PricewaterhouseCoopers Cyprus. Other previous positions in:

Tree&Son UK, Data Entry International Limited-Cyprus, Cyprus Cargo Airline.

• Member of the Board since November 1999. • Founding par tner of Nestor Nestor Diculescu Kingston Petersen (1990), a Romanian legal practice. • Member of the Bucharest Bar Association and Arbitrator with the International Court of Arbitration of

the Romanian Chamber of Commerce and Industry.• Former counsellor and chief legal advisor of the Romanian Consulting Institute Romconsult and a legal

expert with the Institute for Legal Research of the Romanian Academy.

page

6

CORP

ORAT

E GO

VERN

ANCE

COMMITTEES

Credit CommitteeAssets and Liabilities CommitteeRisk CommitteeWork Out Committee

EXTERNAL AUDITOR

PricewaterhouseCoopers (since 1991)

MANAGEMENT TEAM

Nicolae Surdu, Head of Commercial BankingC`t l̀in Pårvu, Vice-presidentGeorge Toma Mucibabici, PresidentFlorian Kubinschi, Vice-president and Chief Financial OfficerCarmen Popa, Head of NetworkGabriel Diamandopol, Chief Operating Officer

From left to right:

BANCA }IRIAC’s2003 ACHIEVEMENTS

chapter 3

BANCA }IRIAC’s2003 ACHIEVEM

ENTS

page

7

BANCA }IRIAC’s2003 ACHIEVEM

ENTS

Market position and market share in the Romanian banking system at the end of 2003:

BANCA }IRIAC's 2003 ACHIEVEMENTS

Shareholders' equity increased by 35%

Clients' funds rose by 17%

Total loans portfolio grew with 63%

Retail loans portfolio expanded by 239%

119,000 new cardsThe bank issued

The clients' portfolio enlarged with 235,800 new clients

Operating profit grew with 57%

of the total cards aquiring volume (the largest acquirer)

of the total banking system7.7%

of the total banking system6%

of the total banking system3.2%

of the total banking system2.7%

of the total banking system3.9%

of the total banking system4%

of the total banking system3.6%

of the FX cards7%

in the retail lending4th place

in total net profit3rd place

in total net banking assets10th place

in total share capital7th place

in total own funds4th place

in total loans7th place

in total deposits8th place

of the total issued cards4.3%

40%

BANK’s PROFILEchapter 4

BANK’s PROFILE

page

9

Individual Banking

BANK's PROFILE

BANK’s PROFILE

The year 2003 was definitely the year of retail.

As the macroeconomic framework improved, the consumption stirred and the banks seized the growth and profitability potential. Being ignored for a long time, the development of the retail lending recorded a real boom as the loans to individuals displayed an outstanding increase of almost 260%, up to 25% of the total non-government credit. It still stands, however at only 4% of the GDP.

Banca }iriac was amongst the pioneers and a market maker in the retail business development in Romania, ranking as number 4 in terms of market share at the end of 2003.

The bank’s retail development strategy in the last four years placed an important focus on products and services portfolio enlargement and quality as well as on clients’ satisfaction, loyalty and retention.

Defining itself as a customer focused institution, Banca }iriac pursued a gradual expansion of the number of its retail clients which reached 555,000 at the end of 2003, with a substantial y/y increase of 71%.

The volume of the retail loans granted in 2003 soared 2.4 times, reaching ROL 5,914.3 billion. The weight of the retail loans in total loans portfolio increased up to 50% at the end of 2003 compared to 24% in 2002 and to 6.3% in 2001. The partnerships concluded with large retailers for white goods financing were the driven force for this dynamic growth. Furthermore, the car loans, Central Account overdraft and other credit facilities (Personal Credit, MultiCredit) had an important contribution to the expansion of the retail loan portfolio.

Banca }iriac granted in 2003 an impressive number of new retail loans of around 210,000 out of which 170,000 consumer loans, 3,000 car loans, 14,500 personal loans and around 22,500 overdraft facilities.

The increase of the retail loans, based mainly on the expansion of the ROL denominated portfolio, significantly sustained the improvement of the bank’s profitability, considering that generally ROL lending secures higher margins.

Despite the high development of the retail portfolio, the non-performing loans remained at a low level due both to the standardized credit approval and proper risk management. The default rate defined as loans being overdue by more than 90 days in total loans granted stood at 1.2% at the end of the year 2003.

The individuals’ deposits recorded a 16.2% increase up to ROL 10,418 billion, remaining the core funding source of the bank. Significant growths have been recorded by the individuals’ funds denominated in local currency and in Euro.

The products and services provided by Banca }iriac cover an extensive range of individuals’ savings and lending needs: deposits, CDs, consumer loans, car loans, personal loans and overdrafts.

Also, Banca }iriac provides travellers’ cheques, cards, insurance policies and MoneyGram transfers.

In order to fulfil the clients’ demands, the bank launched in 2003 new and innovative products for individuals:• MultiCredit (a general purpose loan);• Junior Account (a product for parents who want to save money for their under age children);• USD denominated CDs (apart from the already existing ROL and EUR denominated CDs); • Discounted CDs (sold by Treasury Marketing Unit to high net worth individuals and corporates).

In order to sustain the retail business’ dynamic, the bank increased the sale force, developed the support systems and distribution channels, and also intensified its promoting and advertising actions.

page

10

2001 2002 2003

Evolution of individuals clients

Evolution of individuals’ loans(ROL billion)

0

100,000

200,000

300,000

400,000

500,000

600,000

0

2,000,000

4,000,000

6,000,000

8,000,000

10,000,000

12,000,000

0

1,000,000

2,000,000

3,000,000

4,000,000

5,000,000

6,000,000

2001 2002 2003

2001 2002 2003

Commercial Banking

Evolution of individuals’ deposits(ROL billion)

BANK

’s P

ROFI

LE

Banca }iriac was one of the first and most enthusiastic supporters of the Credit Bureau implementation, acknowledging the necessity of such an institution. One of the Bank’s vice-president holds a vice-president position in the Board of the Credit Bureau.

For 2004 Banca }iriac plans to increase the quality of the existing retail products, to include in its offer the housing loans, to develop new standard retail products and to start internet and mobile banking for individuals. Also the bank will further streamline processing, enlarge the distribution channels and improve its customer service by implementing a modern call centre.

Apart from the aggressive development of the retail business, Banca }iriac focused on enhancing its partnership built over the years with its corporate clients while targeting good performing companies.

Despite increased competition Banca }iriac achieved steady but sound growth of its corporate portfolio. The number of corporate clients consisting of middle and up-market companies – including SMEs, public sector and other financial institutions advanced to around 28,900 at the end of 2003.

Banca }iriac continued to provide quality products and services for its corporate clients. Beside the improvement of the existent offer, the bank launched new products (e.g. Medicredit).

The lending facilities cover a wide range of companies’ needs: credit lines (overdrafts), receivables financing, overall limit for receivables financing, non-cash limit, inventory financing, import financing, export pre/post financing, project financing, equity financing, lease financing, financing for medical equipment and medical offices’ refurbishment.

The loans granted with PHARE funding to SMEs for financing the direct investments reached about ¤ 5 million by the year end, while loans granted for SAPARD projects for agriculture development and improvement of rural infrastructure stood at ¤ 650,000.

page

11

Evolution of companies' loans(ROL billion)

0

1,000

2,000

3,000

4,000

5,000

6,000

2001 2002 2003

Evolution of companies clients

0

5,000

10,000

15,000

20,000

25,000

30,000

2001 2002 2003

Evolution of companies' funds(ROL billion)

0

1,000

2,000

3,000

4,000

5,000

6,000

2001 2002 2003

BANK’s PROFILE

Also based on agreements concluded with The Rural Credit Guarantee Fund and The Romanian Credit Guarantee Fund the bank undertook sector risk secured with letters of guarantee issued by these funds.

Companies’ loans reached ROL 5,900 billion at the end of 2003, with an increase of 7.2% from 2002. The weight in total loans portfolio decreased from 76% at the end of the previous year, to 50% at the end of 2003, due to the increased focus placed on retail. The non-performing loans, defined as class “E” loans according to the NBR’s definition, stood at 0.4% of total companies’ loans at the end of 2003.

In order to secure a good lending process the bank uses a multilevel lending competences system, the decision chain includes branches, regions, Head Office Commercial Banking Department, Central Credit Committee, Management Committee and for exposures higher than 10% of own funds, the Board of Directors.

Based on a large range of savings and investment options offered by the bank, the companies’ funds increased by 20% and reached ROL 5,025.8 billion at the end of 2003.

The bank strived to provide in a professional manner through the Relationship Management Department a wide range of products and services, structured and shaped according to the clients’ business needs.The clients have also access to cash management services, trade finance services, cash settlements and other operations.

The number of clients using Banca }iriac’s e-banking service, Office2Office, increased by 40% in 2003, due to the clients’ increased awareness of the benefits of this efficient tool.

Banca }iriac plans to develop in 2004 its already comprehensive offer for the corporate and SMEs clients with medium term project financing, factoring, internet banking, mobile banking and also to provide co-financing under different programs.

page

12

Cards by brand

0

50,000

100,000

150,000

200,000

2001 2002 2003

- Visa - MasterCardEvolution of cards number

0

50,000

100,000

150,000

200,000

250,000

300,000

2001 2002 20030

10

20

30

40

50

60

70

80

Merchants acquiring volume(USD million)

2001 2002 2003

Cards

BANK

’s P

ROFI

LE

One of the most successful business line of the bank is represented by cards, Banca }iriac being one of the leading banks on this market segment.

Banca }iriac is issuing 14 different types of cards under the brands of Visa, MasterCard and American Express. The cards issued are: debit cards, charge cards, debit cards with financing facilities attached (overdraft up to one month’s salary and/or revolving credit up to 6 net months’ salaries).

The number of cards issued reached 255,718 with a year on year increase of 86.6%. The Visa cards recorded a 59% growth, while the number of cards issued under MasterCard brand almost doubled.

Banca }iriac is the sole Romanian bank offering acquiring services for American Express, Dinners Club and JCB, being also the only bank that covers all international brands.

The acknowledgement of the bank’s position on the market was emphasized by the award for “The Bank with the largest acquiring volume” (USD 69.2 million in 2003) received for the third consecutive year at No-Cash Gala Awards. Banca }iriac is still holding a 40% share of the acquiring market.

At the end of 2003, Banca }iriac in co-operation with other two acquiring banks launched through Romcard a new system, called 3-D Secure e-commerce. The service allows merchants to sell their products through a secure channel via Internet. Soon, the 3-D Secure system will be available for all cards issued by Banca }iriac.

In order to meet the clients’ demands, the customer service for cardholders was extended in 2003 and now is available 24 hours.

Banca }iriac has enlarged the usage area of the Visa Electron card. Now, the new Visa Electron is a debit card designed for individuals that travel abroad. Usage of Visa Electron card in Euro region has increased due to Euro settlement of transactions.

During 8 years of experience the structure of acquiring customers by category remained almost unchanged: main hotels in Romania, representative travel agencies, direct marketing companies, restaurants, car rental companies, health care centers, international airlines, duty free stores, sport clubs and supermarkets.

In 2003, Banca }iriac further expanded its ATM and POS network, covering all important areas of the country. Thus, the number of ATMs increased with 56 units, to 200 at the end of 2003, while the POS network increased with 385 units, to 882.

Banca }iriac started in 2003 an upgrade process of the cards system to EMV standard (Eurocard-Mastercard-Visa compliance). In this respect, all the equipment acquired by Banca }iriac in 2003 is EMV compliant.

At the beginning of 2004, Banca }iriac will conclude new agreements with utilities companies for collecting bills issued by them through ATMs. In 2004, Banca }iriac will also launch its first credit card.

page

13

0

50,000

100,000

150,000

200,000

250,000

300,000

350,000

0

1,000

2,000

3,000

4,000

5,000

6,000

Jan 03 Feb 03 Mar 03 Apr 03 May 03 Jun 03 Jul 03 Aug 03 Sep 03 Oct 03 Nov 03 Dec 03

Earned premiums and number of policies- Earned premiums - Number of policies

Number ofpoliciesEuro

Bancassurance

Treasury

BANK’s PROFILE

The financial services sector is continuously developing, the integrated services concept being the trend of the past years. The banks and insurance companies have found common ground and teamed in order to launch complex offers, providing insurance and banking products and services while sharing the distribution channels and the clients’ base.

At the end of 2002, Banca }iriac entered into a strategic partnership with one of the most important players on the Romanian insurance market, Allianz-}iriac Asigurari, for bancassurance products. The contract concluded could be considered as the best structured agreement in the Romanian market. Presently, in the bank’s branches and agencies, the clients have access to any type of insurance policies, both life and non-life, covering the needs of individuals and companies clients.

About 18,000 insurance policies were concluded in 2003 while the gross written premiums volume at the end of December 2003 was around EUR 3 million (2.2% of the total gross written premiums of Allianz-}iriac Asigur`ri), exceeding by far the whole year estimations.

The Bancassurance offer of Banca }iriac contains:

• Non-life insurance: household insurance, private property insurance, motor hull insurance, accident insurance, travel health insurance, green card insurance, MTPL insurance, carriers liability insurance, third party liability insurance, equipment insurance, inventories insurance;• Life insurance: unit linked life insurance, endowment insurance, dowry study plan insurance, term life insurance and group life insurance.

Banca }iriac and Allianz-}iriac Asigur`ri will continue to improve their offer in order to support the development of the integrated services on the market.

Banca }iriac strived to consolidate its position as an active player on the market, able to provide products and solutions in line with the clients’ continuously increasing business needs and developing financial markets.

The Treasury department activity was conducted in order to provide the highest return for proprietary trading and for the customers in the financial markets within the framework of a prudent and professional trading.

Banca }iriac strengthened its interbank trading position reaching an average of 4% market share in the money market activity and a 2.6% market share in FX trading.

page

14

International Activity

FX interbank market share(%)

MM new deals market share(%)

0.0

0.5

1.0

1.5

2.0

2.5

3.0

2001 2002 20030

2.0

4.0

6.0

8.0

10.0

2001 2002 2003

BANK

’s P

ROFI

LE

Starting February 2003, Banca }iriac received the primary dealer status in the government securities market, which allowed the bank to operate in the primary market for its clients and its own account, to trade on the secondary market and to open and manage custody accounts for its customers-individuals, companies, banks and other financial institutions. Banca }iriac has bought in 2003 1.2% of the government securities issued by the Ministry of Finance on the primary market.

Also, in 2003 within Treasury Department it was established a separate unit - Treasury Market Unit - for a better service of the bank’s large corporate clients and high net worth individuals. As a result, throughout 2003, the volume of deposits managed by Treasury Market Unit increased extensively: 88% in EUR, 292% in ROL and 55% in USD and there were over 100 new clients added to the clients’ portfolio.

The Treasury department is also in charge with the preparation of the documentation for ALCO meetings.

Banca }iriac will further strengthen its position on the Romanian market by increasing the quality and volume of the transactions and by developing a whole range of treasury operations addressed to its clients such as credit and FX derivatives and fixed income investments in international and local bonds.

Internationally, the bank has earned the trust of an extensive number of domestic and international banks proved by more than 50 commercial and treasury lines granted to Banca }iriac.

Banca }iriac enjoyed the security and confidence of doing business with large banking organizations worldwide, covering the major financial centres, such as: Frankfurt, New York, London, Tokyo etc.

The bank has built SWIFT ties with over 600 banks over the world and correspondent banking relationships with a selective sample of 250 top financial institutions.

The bank provides a broad range of international settlement services from documentary credits, export and import collection, bills discounting, export and import bills purchase, to letters of guarantees, structured trade finance, cheques and international payment transactions.

In 2003 strong emphasize has been put again on the prevention of money laundering and terrorist financing. Besides compliance with the country regulations, the bank had set new and more powerful internal rules to prevent the involvement of the bank in facilitating such activities.

In the last quarter of 2003 the bank took a strategic decision to access international long-term financing to leverage the customers’ needs for long term financing on the domestic market.

page

15

BANK’s PROFILE

Risk Management

Miscellaneous3.6%

Transport & Communications3.2%

Manufacturing21.3%

Retail Customers50.1% Agriculture

4.1%

Trade & Finance 17.7%

Banca }iriac initiated discussion with the IFC and EBRD and started cooperation with FMO, DEG/ KFW in order to raise additional long term funding.

In 2004 the bank will focus on the development of new internal guidelines for corporate governance and environmental and social procedures.

Banca }iriac will also make greater efforts to sustain the trade finance business of its customers and to develop its international banking products and services while preserving high-quality standards.

Furthermore the bank will act so as to maintain the excellent relationships abroad, to increase the correspondent banking network on a selective basis and to approach new markets for the international businesses of its customers.

Banca }iriac recognises a wide variety of risk types, and ensures that the control framework adequately covers all of these, including those that do not readily lead themselves to measurement, such as operational, legal, regulatory, reputation and human resources risks.

In this respect, an independent Risk Management function was set up, which has the mission to identify, monitor, manage and report the risks the bank is exposed to.

The main objective of Risk Management is to further develop risk policies and proper instruments. Generally, the risk management objectives and policies are real key drivers of the overall business strategy, being implemented through the specific supporting operational procedures.

The Risk Management Department is in charge with organizing the Risk Committee which has an advisory function and which analyzes the risk profile of the bank and issues recommendations in order to mitigate risks.

In addition to the traditional risk administration bodies (i.e. Assets and Liabilities Management Committee, Credit Committee, Risk Committee), support and control functions, such as the middle and back offices, legal, internal audit, IT and human resources, are integral parts of the overall risk management framework.

CREDIT RISK

In order to mitigate credit risk, Risk Management is involved in the following activities:

• set up, update, review, advise of credit risk policies and procedures, including rating systems;• analysis on the credit portfolio in order to highlight the risk profile of the bank.

Banca }iriac uses an internal credit rating system based on 10 risk classes, with an early warning system for the 7 and 8 classes which are monitored by the Supervision Unit from Commercial Banking Department. The loans included in classes 9 and 10 are managed by the Workout Department.

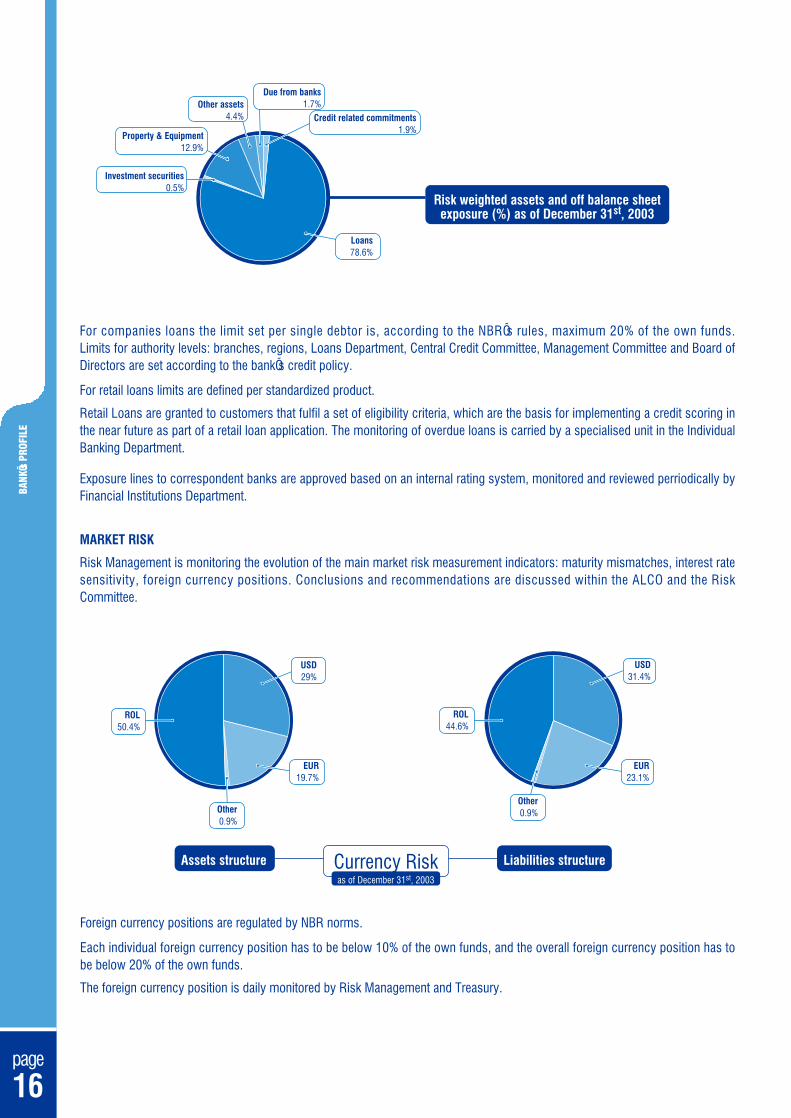

Loan concentration by economic sector (%)as of December 31st, 2003

page

16

BANK

’s P

ROFI

LE

Risk weighted assets and off balance sheetexposure (%) as of December 31st, 2003

Due from banks1.7%Other assets

4.4%

Property & Equipment 12.9%

Investment securities 0.5%

ROL50.4%

USD29%

EUR19.7%

Other 0.9%

ROL 44.6%

USD31.4%

EUR23.1%

Other0.9%

Assets structure Currency Risk Liabilities structureas of December 31st, 2003

Credit related commitments1.9%

Loans78.6%

For companies loans the limit set per single debtor is, according to the NBR’s rules, maximum 20% of the own funds. Limits for authority levels: branches, regions, Loans Department, Central Credit Committee, Management Committee and Board of Directors are set according to the bank’s credit policy.

For retail loans limits are defined per standardized product.

Retail Loans are granted to customers that fulfil a set of eligibility criteria, which are the basis for implementing a credit scoring in the near future as part of a retail loan application. The monitoring of overdue loans is carried by a specialised unit in the Individual Banking Department.

Exposure lines to correspondent banks are approved based on an internal rating system, monitored and reviewed perriodically by Financial Institutions Department.

MARKET RISK

Risk Management is monitoring the evolution of the main market risk measurement indicators: maturity mismatches, interest rate sensitivity, foreign currency positions. Conclusions and recommendations are discussed within the ALCO and the Risk Committee.

Foreign currency positions are regulated by NBR norms.

Each individual foreign currency position has to be below 10% of the own funds, and the overall foreign currency position has to be below 20% of the own funds.

The foreign currency position is daily monitored by Risk Management and Treasury.

page

17

1-3 month6.2%

3 months - 1 year21.9%

1-5 years23.3%

> 5 years13.4%

Assets structure Liquidity Risk Liabilities structure

< 1 month65.3%

1-3 month12.6%

3 months - 1 year17.5%

1-5 years4.6%

> 5 years0.1%

Human Resources

as of December 31st, 2003

BANK’s PROFILE

LIQUIDITY RISK

Liquidity risks defined as funding risk and market liquidity risk are mitigated by the following actions:

• monitoring of evolution of liquidity indicators – quick liquidity tier I and tier II and monthly liquidity per maturity bands, calculated according to the Central Bank’s rules;

• following the liquidity strategy which includes the contingency plan.

OPERATIONAL RISK

The operational risk defined as the risk of direct and indirect losses resulting from inadequate or failed internal processes, people, systems or from external events, it is properly monitored and addressed through specific risk procedures or operational procedures which include concrete risk management measures and/or keys and/or models.

Additionally, the newly implemented IT system offers real advantages for operational risk management (Enhancement Security System, including authorisation levels / limits, access, limits set up, control of limit excesses, etc.).

It features on-line controls performed by the system which stops any transaction that would break the limits. The middle and back offices are responsible for ensuring that trades are recorded in a prompt, accurate and complete manner whilst minimizing the scope for error and fraud. To enable them to fulfil these obligations, the management has reporting lines to the trading function.

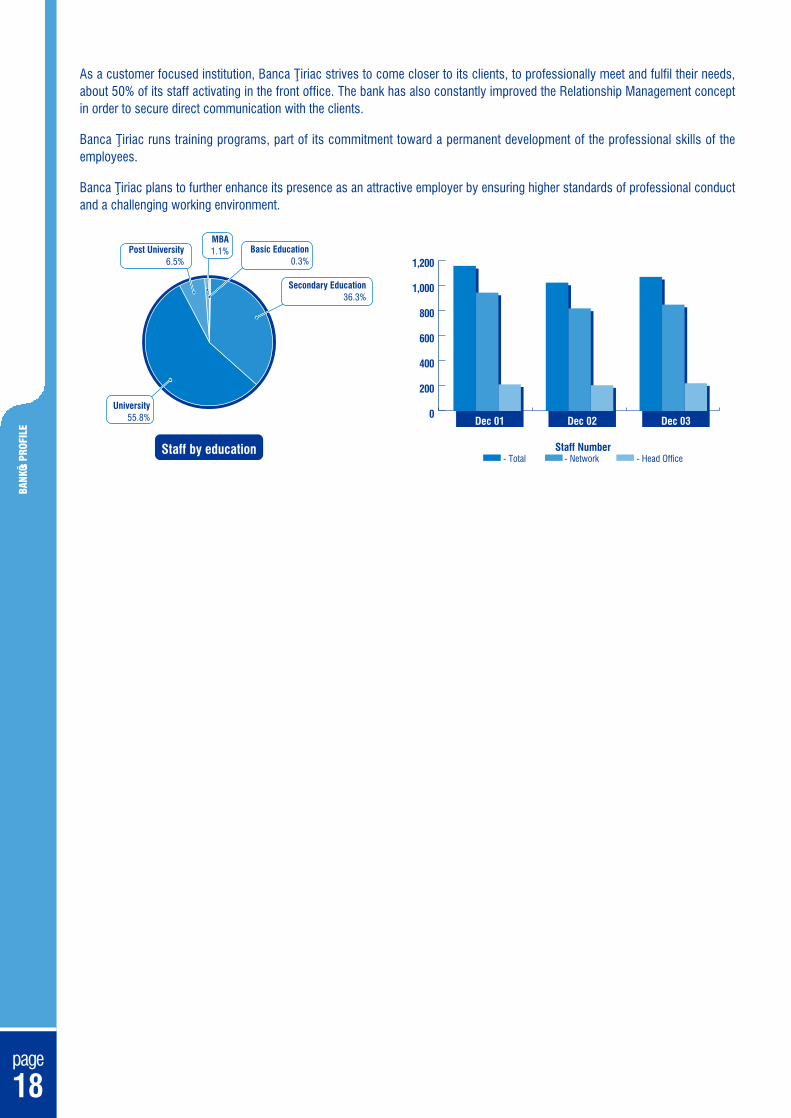

Recognizing the high importance of the human capital to the business development, the related policies have focused on attracting and maintaining quality, talented and professionally re-known staff at each level of the organization.

Banca }iriac benefits from a flat and efficient organization structure with clear hierarchical and functional lines, allowing a faster decision-making process and enhancing competitiveness.

The team comprises relatively young but experienced staff, the number of employees aged below 40 years counting for 64% of the total staff.

Following the expansion of the branch network, part of the continuous development of the bank, the staff number slightly increased by 46 employees in 2003, while the profitability per employee had an upswing. The operating profit per employee increased by over 60%, from 10,700 euro/employee in 2002 to 17,500 euro/employee in 2003.

< 1 month35.2%

page

18

BANK

’s P

ROFI

LE

Staff by education

University55.8%

Secondary Education36.3%

Basic Education0.3%

Post University6.5%

MBA1.1%

0

200

400

600

800

1,000

1,200

Dec 01 Dec 02 Dec 03

Staff Number- Total - Network - Head Office

As a customer focused institution, Banca }iriac strives to come closer to its clients, to professionally meet and fulfil their needs, about 50% of its staff activating in the front office. The bank has also constantly improved the Relationship Management concept in order to secure direct communication with the clients.

Banca }iriac runs training programs, part of its commitment toward a permanent development of the professional skills of the employees.

Banca }iriac plans to further enhance its presence as an attractive employer by ensuring higher standards of professional conduct and a challenging working environment.

REPORT OF INDEPENDENT AUDITORS AND FINANCIAL STATEMENTS

chapter 5

REPORT OF INDEPENDENTAUDITORS AND FINANCIALSTATEM

ENTS

REPORT OF INDEPENDENT AUDITORS AND FINANCIAL STATEMENTS

CONTENTS

General information

Report of the independent auditors

Income statement

Balance sheet

Statement of changes in shareholders' equity

Cash flow statement

Notes to the financial statements

PAGE

NATURE OF THE ENTERPRISE

Commercial Bank "Ion Tiriac" SA (the "Bank") has been incorporated in Romania since 1991 and is licensed by the National Bank of Romania to conduct banking activities. The Bank is principally engaged in wholesale and retail banking operations in Romania. The Bank operates through its head office located in Bucharest and its network consisting of the following:

Branches Agencies Working points ATM's POS's

Bucharest Rest of the country Total -

The address of its registered office is as follows: City Business Center, 3 Nerva Traian Street, Complex M 101 Bucharest, Romania.

The Bank's number of employees as at 31 December 2003 was of 1,067 (31 December 2002: 1,021).

DIRECTORS

The Bank is managed by a Board of Directors made up of 8 members elected for 4 years by the ordinary shareholders' meeting, lead by a president which also holds the position of Chief Executive Officer. The Composition of the Board of Directors as at 31 December 2003 is as follows:

Position

President Vice-president Vice-president Member Member Member Member Member

Mr. George Toma Mucibabici Mr. CStalin Parvu Mr. Florian Kubinschi Mr. Ion Tiriac Mr. Dan Petrescu Mr. Ion Nestor Mr. Victor Anagnoste Mr. Christodoulakis Theodorou

DIRECTORS (CONTINUED)

a) On 15 May 2003 Mr. Constantin Barbu, Vice-president of the Banks' Board of Directors resigned for health reasons. I b) On 11 August 2003 the Board of Directors named Mr. Florian Kubinschi as Vice-president of the Board of Directors

and Mr. Christodoulakis Theodorou as member of the Board of Directors. I c) On 18 August 2003 Mr. Anthony van der Heijden, President of the Bank's Board of Directors and Chief Executive

Officer, resigned and, in his place, the Board of Directors named Mr. George Toma Mucibabici as President of the Board of Directors and Chief Executive Officer.

I CAPITAL ADEQUACY

The Bank calculates the adequacy of its capital using ratios established by the Bank for International Settlements (BIS), based upon its financial statements prepared in accordance with International Financial Reporting Standards (IFRS). Based upon financial information prepared in accordance with IFRS the Tier 1 and Tier 2 capital adequacy ratios of the Bank at 31 December 2003 were both 21.16% (31 December 2002: 21.73% both). The minimum required capital adequacy ratio is 8%.

Under BIS guidelines assets are weighted according to broad categories of notional credit risk, being assigned a risk weighting according to the amount of capital deemed to be necessary to support them. Four categories of risk weights (0%, 20%, 50%, 100%) are applied; for example cash and money market instruments have a zero risk weighting which means that no capital is required to support the holding of these assets. Property and equipment carries a 100% risk weighting, meaning that it must be supported by capital equal to 8% of the carrying amount. Other asset categories have intermediate weightings.

Off-balance sheet credit related commitments and forwards and options based derivative instruments are taken into account by applying different categories of credit conversion factors, designed to convert these items into balance sheet equivalents. The resulting credit equivalent amounts are then weighted for credit risk using the same percentages as for balance sheet assets.

CAPITAL ADEQUACY (CONTINUED)

Tier 1 capital consists of shareholders' equity. Tier 2 capital includes the Bank's eligible long-term debt and general provisions.

Balance sheet1 Nominal amount

31 December 31 December 31 December 2003 2002 700a

(ROL million) (ROL million) (ROL million)

Balance sheet assets (net of provisions)

Due from other banks 1,237,467 Loans and advances to customers ll,585,9l 5 Investment securities - available

for sale 75,217 Property and equipment 1,874,696 Other assets 643,989

Off balance sheet positions

Credit related commitments

Total risk weighted assets

BIS Capital ratios

Tier 1 capital Tier 1 + Tier 2 capital

Capital 31 December 31 December 31 December

2003 2002 2003 (ROL million) (ROL million) ( M L million)

Risk weighted amount

31 December 2002

(ROL million)

BIS % 31 December

2002 (ROL million)

PricewaterhouseCoopers Audit SRL 1-5 Costache Negri Street Bucharest 5, Romania Telephone +40 (21) 202 8500 Facsimile +40 (21) 202 8600

INDEPENDENT AUDITORS' REPORT TO THE BOARD OF DIRECTORS OF BANCA COMERCIALA 'ION TIRIAC" SA

We have audited the accompanying balance sheet of Commercial BankHIon Tiriac" SA (the "Bank") as at 31 December 2003 and the related statements of income and cash flows for the year then ended, expressed in the current purchasing power of the Romanian Lei ("ROL") as at 31 December 2003. These financial statements are the responsibility of the Bank's management. Our responsibility is to express an opinion on these financial statements based on our audit.

We conducted our audit in accordance with International Standards on Auditing. Those Standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosure in the financial statements. An audit also includes assessing the accounting principles used and significant estimates made by management, as well as evaluating the overall financial statement presentation. We believe that our audit provides a reasonable basis for our opinion.

As discussed in Note 3.1. - "Fee and commission income1' and in Note 6 - "Other operating expenses" to the financial statements, commissions and related expenses for loan origination are recognised on a cash basis and are not deferred with the related loans, this accounting treatment being not in accordance with IAS 18 - "Revenue". If these commissions and related costs were deferred with the loans, the fee and commission income for the year ended 31 December 2003 would have been ROL 660,221 million instead of ROL 776,222 million and operating expenses for the year ended would have been 1,446,726 million instead of ROL 1,518,917 million. Accordingly, by deferring both loan origination fees and loan origination costs in accordance with the requirements of IAS 18 "Revenues", the loans balance as at 31 December 2003 should be decreased by

Registration Number: J4011722311993 Fiscal Code: R4282940

ROL 43,809 million, the deferred tax at 31 December 2003 should be decreased by ROL 10,952 million and the shareholders' equity at 31 December 2003 should be decreased by ROL 32,857 million.

4. In our opinion, except for the failure to defer commission income as required by IAS 18 - "Revenue" as described in paragraph 3, the accompanying financial statements present fairly, in all material respects, the financial position of the Bank at 31 December 2003 and the results of its operations and its cash flows for the year then ended in accordance with International Financial Reporting Standards.

L. < 3 ~ t o p &.~JL PricewaterhouseCoopers Audit SRL Bucharest, 26 April 2004

AS AT 31 DECEMBER 2003 (all amounts expressed in ROL million, in terms of purchasing power of the Romanian Lei (ROL) at 31

December 2003, unless stated otherwise)

Year ended 31 December 2003

Year ended 31 December 2002

Interest income Interest expense Net interest income

Fee and commission income Fee and commission expense Net fee and commission income

Net foreign exchange gains Gains less losses from

investments securities Gains less losses from

dealing securities Other operating income Loss/(gain) on net monetary position

Operating income

Impairment losses on loans, advances and other assets

Other operating expenses

Profit from operations before tax and impairment of property

Impairment of property

Profit from operations and before tax

Income tax

Net profit for the period

The financial statements set out on pages 1 to 49, prepared in accordance with International Financial Reporting Standards on the basis of the statutory accounts, were approved by the Board of Directors on 26 April 2004 and signed on its behalf by:

Mr. George Toma Mucibabici President and Chief Executive Officer

Mr. Florian Kubinschi hief Financial Controller

The accounting policies and notes on pages 5 to 49 form an integral part of these financial statements. IFRS Financial Statements, page 1

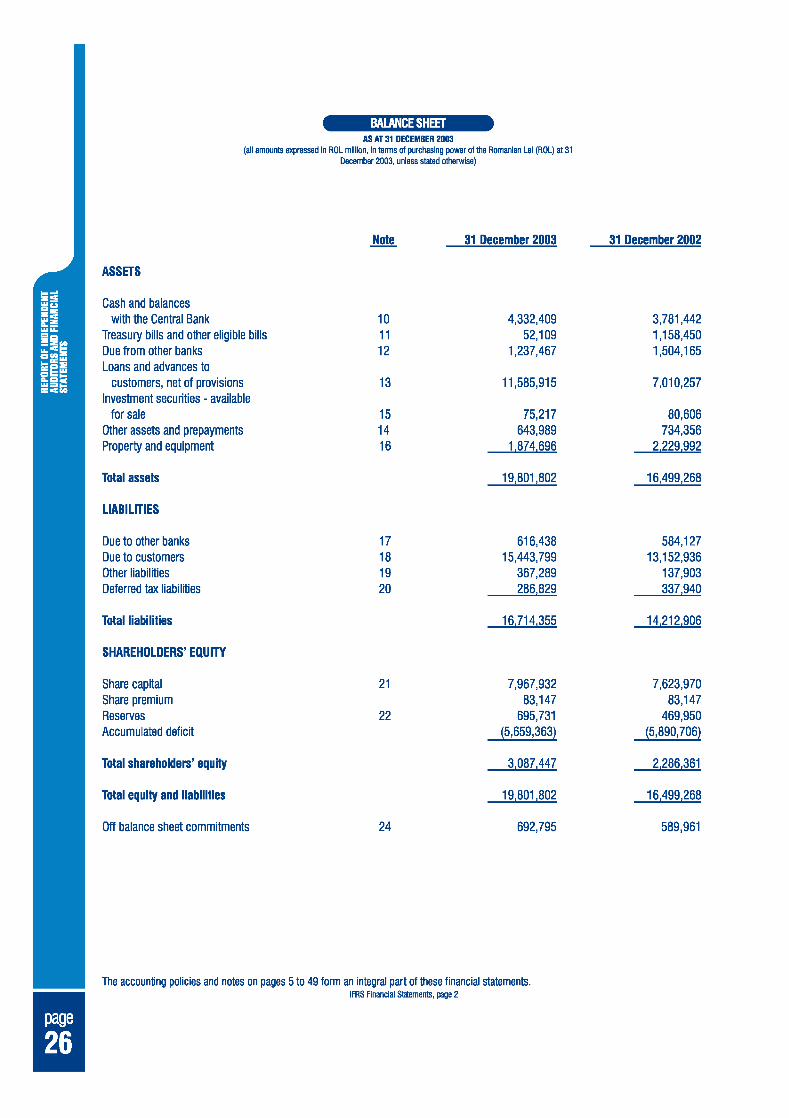

AS AT 31 DECEMBER 2003 (all amounts expressed in ROL million, in terms of purchasing power of the Romanian Lei (ROL) at 31

December 2003, unless stated otherwise)

Note - 31 December 2003 31 December 2002

ASSETS

Cash and balances with the Central Bank

Treasury bills and other eligible bills Due from other banks Loans and advances to

customers, net of provisions Investment securities - available

for sale Other assets and prepayments Property and equipment

Total assets

LIABILITIES

Due to other banks Due to customers Other liabilities Deferred tax liabilities

Total liabilities

SHAREHOLDERS' EQUITY

Share capital Share premium Reserves Accumulated deficit

Total shareholders' equity

Total equity and liabilities

Off balance sheet commitments

1 The accounting policies and notes on pages 5 to 49 form an integral part of these financial statements. IFRS Financial SHements, page 2

I

Balance at 1 January 2002

Net profit for 2002 Dividend for 2001 Distribution of 2001

statutory profit Issue of share capital for cash

FOR THE YEAR ENDED 31 DECEMBER 2003 (all amounts expressed in ROL million, in terms of purchasing power of trie Romanian Lei (ROL) at 31

December 2003, unless stated otherwise)

Balance at 31 December 2002

Balance at 1 January 2003

Net profit for the period Distribution of 2002

statutory profit Issue of share capital from

incorporation of reserves Issue of share capital

for cash

Balance at 31 December 2003

Share Share Notes cauital uremium Reserves

Accumulated deficit

(6,011,093)

424,508 (72,943)

(231,178)

Total Eauib

1,872,370

424,508 (72,943)

62,428

2.286.361

The accounting policies and notes on pages 5 to 49 form an integral part of these financial statements. IFRS Financial SHements, page 3

FOR THE YEAR ENDED 31 DECEMBER 2003 (all amounts expressed in ROL million, in terms of purchasing power of the Romanian Lei (ROL) at 31

December 2003, unless stated otherwise)

Year ended Year ended 31 December 2003 31 December 2002

Cash flows from operating activities Interest receipts Interest payments Commission receipts Commission paid Dividend receipts Cash payments to employees and suppliers Income tax paid Net cash flow before changes in operating

assets and liabilities

Changes in operating assets and liabilities Net increase in loans to customers Net increase in deposits to banks with

maturity over 90 days including mandatory reserve Net decrease 1 (increase) in treasury bills with

maturity over 90 days Net decrease in other assets Net increase in customers deposits Net (decrease) 1 increase in deposits from other banks Net (decrease) I increase in other liabilities Cash flow used in operating activities

Cash flows from investing activities Purchase of property and equipment Proceeds on sale of property and equipment Purchase of investment securities Sale of investment securities Net cash used in investing activities

Cash flows from financing activities Cash proceeds from issue of share capital Dividends paid Net cash from financing activities

Effect of inflation on cash and cash equivalents Effect of exchange rate changes

Net decrease in cash and cash equivalents

Cash and cash equivalents at beginning of period

Cash and cash equivalents at end of period

The accounting policies and notes on pages 5 to 49 form an integral part of these financial statements. IFRS Financial Statements, page 4

FOR THE YEAR ENDED 31 DECEMBER 2003 (all amounts expressed in ROL million, in terms of purchasing power of the Romanian Lei (ROL) at 31

December 2003, unless stated otherwise)

ACCOUNTING POLICIES

The principal accounting policies adopted in the preparation of these financial statements are set out below:

1.1 Basis of presentation

The financial statements are prepared in accordance with and comply with International Financial Reporting Standards (IFRS). I The financial statements are prepared under the historical cost convention as modified by the revaluation of available-for-sale investment securities, financial assets and financial liabilities held for trading. The financial statements have also been prepared in accordance with IAS 29 - "Reporting in hyperinflationary economies1', as described in Note 1.4 below.

1.2 Currency of Presentation

The accompanying financial statements are presented in terms of the purchasing power of the Romanian Lei (ROL) as at 31 December 2003. These financial statements are measured in ROL million unless stated otherwise.

1.3 Basis of Accounting

The Bank maintains its accounting records in Romanian Lei (ROL) and prepares its statutory financial statements in accordance with banking regulations issued by the National Bank of Romania. The accompanying financial statements are based on the statutory financial statements of the Bank, which are prepared on a going concern basis under the historical cost convention and subsequently have been adjusted to present financial statements that are in accordance and comply in all material respects with IFRS except for IAS 18 as describe in Note 3.1 "Fee and commission income" and in Note 6 "Other operating expenses".

1.4 Hyperinflation accounting

The Bank complies with IFRS requirements that financial statements prepared on a historical cost basis should be adjusted to take account of the effects of hyperinflation. International Accounting Standard No. 29 - "Reporting in Hyperinflationary Economies" ("IAS 29") provides guidance on how financial information should be prepared in such circumstances.

IFRS Financial Stternents, page 5

FOR THE YEAR ENDED 31 DECEMBER 2003 (all amounts expressed in ROL million, in terms of purchasing power of the Romanian Lei (ROL) at 31

December 2003, unless stated otherwise)

ACCOUNTING POLICIES (CONTINUED)

IFRS require that financial statements prepared on a historical cost basis should be adjusted to take account of the effects of inflation, if this has been significant. IAS 29 provides guidance on how financial information should be prepared in such circumstances. In summary it requires that financial statements should be restated in terms of measuring unit current at the balance sheet date and that any gain or loss on the net monetary position should be included in the income statement and disclosed separately. The restatement of financial statements in accordance with IAS 29 requires the use of a general price index that reflects changes in general purchasing power.

Hyperinflation is indicated by characteristics of the economic environment of a country, which include, but are not limited to, the following:

the general population prefers to keep its wealth in non-monetary assets or in a relatively stable foreign currency. Amounts of local currency held are immediately invested to maintain purchasing power;

the general population regards monetary amounts not in terms of the local currency but in terms of a relatively stable foreign currency. Prices may be quoted in that currency;

sales and purchases on credit take place at prices that compensate for the expected loss of purchasing power during the credit period, even if the period is short;

interest rates, wages and prices are linked to a price index; and

the cumulative inflation rate over three years is approaching, or exceeds, 100%. For information purposes only, the annual increase in the general price index as issued by the National Statistical Bureau over the three year period is calculated as follows:

Cumulative . . Inflation at

Cumulative Inflation at end of vear

IFRS Financial Statements, page 6

FOR THE YEAR ENDED 31 DECEMBER 2003 (all amounts expressed in ROL million, in terms of purchasing power of Die Romanian Lei (ROL) at 31

December 2003, unless stated otherwise)

ACCOUNTING POLICIES (CONTINUED)

The application of IAS 29 to specific categories of transactions and balances within the financial statements is set out as follows:

Monetary assets and liabilities

Cash, amounts due from banks, loans, accruals, receivables, payables (including taxes), borrowed funds, both long and short term, have not been restated as they are considered monetary assets and liabilities and therefore stated in ROL current at the balance sheet date.

I Non monetary assets and liabilities

Non monetary assets and liabilities (i.e. those balance sheet items that are not already expressed in terms of ROL current at the balance sheet date such as property and equipment) and components of shareholders' equity are restated from their historical cost by applying the general price index from either the date of acquisition, valuation or contribution to the balance sheet date.

Property and equipment

All tangible fixed assets are restated from the date of their purchase using the general price index. 1 Income statement

All income statement items are restated by applying the change in the general price index from the dates when the items of income and expenses were initially recorded in the accounting records to the balance sheet date. In practice this restatement has been calculated by using the monthly inflation indices.

Shareholders' equity

All components of shareholders' equity are restated by applying a general price index from the date of contribution or recording in the accounting records. The statutory increase of share capital by bonus issue from revaluation reserves is not taken in consideration. I

IFRS Financial Statements, page 7

FOR THE YEAR ENDED 31 DECEMBER 2003 (all amounts expressed in ROL million, in terms of purchasing power of the Romanian Lei (ROL) at 31

December 2003, unless stated otherwise)

ACCOUNTING POLICIES (CONTINUED)

Gain or loss on the net monetary position

In a period of hyperinflation, an entity holding an excess of monetary assets over monetary liabilities in a hyperinflationary currency loses purchasing power, while an entity holding an excess of monetary liabilities over monetary assets gains purchasing power. The net gain or loss on the net monetary position comprises the effects of changes in the general price indices on the net monetary asset/liability position. The net gain or loss is derived after having restated the balance sheet and the income statement in accordance with the procedures described above.

Cash flow statement

All items included in the cash flow statement are expressed in terms of ROL current at the balance sheet date.

Corresponding figures

Corresponding figures for the previous reporting period are restated by applying the change in the general price index so that the comparative figures are presented in terms of ROL current at the end of the reporting period. Information that is disclosed in respect of earlier periods is also expressed in terms of the measuring unit current as at 31 December 2003.

1.5 Principal accounting policies prior to hyperinflation adjustments

Set out below are the principal accounting policies adopted by the Bank in the preparation of the IFRS financial statements prior to the hyperinflation adjustments. This financial information is then adjusted for the effects of hyperinflation in accordance with the procedures described above in Note 1.4.

Foreign currency translation

Foreign currency transactions in the Bank are accounted for at the exchange rates prevailing at the date of the transactions. Gains and losses resulting from the settlement of such transactions and from the translation of monetary assets and liabilities denominated in foreign currencies, are recognised in the income statement. Such balances are translated at period-end exchange rates into ROL at the official rate of the National Bank of Romania existing at the balance sheet date.

IFRS Financial SHements, page 8

FOR THE YEAR ENDED 31 DECEMBER 2003 (all amounts expressed in ROL million, in terms of purchasing power of the Romanian Lei (ROL) at 31

December 2003, unless stated otherwise)

ACCOUNTING POLICIES (CONTINUED)

At 31 December 2003 the principal rates of exchange used for translating foreign balances were USD 1 = ROL 32,595 (31 December 2002: USD 1 =ROL 33,500) and EURO 1 = ROL 41,117 (31 December 2002: EURO 1 =ROL 34,919).

Offsetting financial instruments

Financial assets and liabilities are offset and the net amount reported in the balance sheet when there is a legally enforceable right to set off the recognised amounts and there is an intention to settle on a net basis, or realise the asset and settle the liability simultaneously. I Interest income and expense

Interest income and expense are recognised in the income statement for all interest bearing instruments on an accruals basis, using the effective yield method based on the actual purchase price. Interest income includes coupons earned on fixed income investment and trading securities and accrued discount and premium on treasury bills and other discounted instruments. When loans become doubtful of collection, they are impaired and interest income is thereafter recognised based on the rate of interest that was used to discount future cash flows for the purpose of measuring the impairment.

Fee and commission income

Fees and commissions consist mainly of fees received for foreign currency transactions and granting of loans. Fees arising from guarantees given, opening of letters of credit and commissions from managed funds on behalf of legal entities and citizens are also included.

Fees and commissions are generally recognised on an accrual basis when the service has been provided. Loan origination fees for loans which are probable of being drawn down, however, are recognised when received and are not deferred (together with related direct costs) and are not recognised as an adjustment to the effective yield on the loan in accordance with IAS 18 "Revenues". Commissions on foreign currency transactions are credited to income on receipt. Income on the endorsement of bills of exchange is recognised on an accruals basis.

IFRS Financial Statements, page 9

FOR THE YEAR ENDED 31 DECEMBER 2003 (all amounts expressed in ROL million, in terms of purchasing power of the Romanian Lei (ROL) at 31

December 2003, unless stated otherwise)

ACCOUNTING POLICIES (CONTINUED)

Investment securities

The Bank classified its investment securities as available-for-sale assets. Investment securities intended to be held for an indefinite period of time, which may be sold in response to needs for liquidity or changes in interest rates, exchange rates or equity prices are classified as available-for-sale. Management determines the appropriate classification of its investment at the time of the purchase.

Investment securities are initially recognised at cost (which includes transaction costs). Available-for-sale financial assets are subsequently re-measured at fair value through income statement unless fair value cannot be reliably measured for which they are carried at cost less impairement.

All regular way purchases and sales of investment securities are recognised at trade date, which is the date that the Bank commits to purchase or sell the asset.

Sale and repurchase agreements and lending of securities

Securities sold subject to a linked repurchase agreements ("repos") are retained in the financial statements as trading or investments securities and the counter-party liability is included in amounts due to other banks or deposits from banks, as appropriate. Securities purchased under agreements to resell ("reverse repos") are recorded as loans and advances to other banks. The difference between sale and repurchase price is treated as interest and accrued over the life of rep0 agreements using the effective yield method.

Securities borrowed are not recognised in the financial statements, unless these are sold to third parties, in which case the purchase and sale are recorded with the gain or loss included in trading income. The obligation to return them is recorded at fair value as a trading liability.

IFRS Financial Statements, page 10

FOR THE YEAR ENDED 31 DECEMBER 2003 (all amounts expressed in ROL million, in terms of purchasing power of the Romanian Lei (ROL) at 31

December 2003, unless stated otherwise)

ACCOUNTING POLICIES (CONTINUED)

Originated loans and provisions for loan impairment

Loans originated by the Bank by providing money directly to the borrower or to a sub-participation agent at draw down, other than those that are originated with the intent of being sold immediately or in the short-term which are recorded as trading assets, are categorised as loans originated by the Bank and are carried at amortised cost, which is defined as the fair value of cash consideration given to originate these loans as is determinable by reference to market prices at origination date. Third party expenses, such as legal fees, incurred in securing a loan are treated as part of the cost of the transaction.

All loans and advances are recognised when cash is advanced to borrowers.

An allowance for loan impairment is established if there is objective evidence that the Bank will not be able to collect all amounts due according to the original contractual terms of loans. The amount of the allowance for loan impairment is the difference between the carrying amount and the recoverable amount, being the present value of expected cash flows, including amounts recoverable from guarantees and collateral, discounted at the original effective interest rate of loans.

The allowance for loan impairment also covers losses where there is objective evidence that probable losses are present in components of the loan portfolio at the balance sheet date. These have been estimated based upon historical patterns of losses in each component, the credit ratings allocated to the borrowers and reflecting the current economic climate in which the borrowers operate. Statutory and other regulatory loan loss reserve requirements that exceed these amounts are dealt with in the general banking reserve as an appropriation of retained earnings.

If the amount of the impairment subsequently decreases due to an event occurring after the write- down, the release of the provision is credited to the bad and doubtful debt expense. I When a loan is un-collectable, it is written off against the related provision for impairments; subsequent 1 recoveries are credited to the bad and doubtful debt expense in the income statement.

IFRS Financial Statements, page 11

FOR THE YEAR ENDED 31 DECEMBER 2003 (all amounts expressed in ROL million, in terms of purchasing power of the Romanian Lei (ROL) at 31

December 2003, unless stated otherwise)

ACCOUNTING POLICIES (CONTINUED)

(h) Sundry debtors

A provision for sundry debtors is established on a case by case basis when there is objective evidence that the Bank will not be able to collect the amount due.

Provisions

Provisions are recognised when the Bank has a present legal or constructive obligation as a result of past events, it is probable that an outflow of resources embodying economic benefits will be required to settle the obligation, and a reliable estimate of the amount of the obligation can be made.

Specific provisions are made against identified risks related to off balance sheet commitments, in particular letters of guarantee.

Computer software development costs

Costs associated with maintaining computer software programmes are recognised as an expense as incurred. However, expenditure that enhances or extends the benefits of computer software programmes beyond their original specifications and lives is recognised as a capital improvement and added to the original cost of the software. Computer software development costs recognised as assets are amortised using the straight-line method over their useful lives but not exceeding a period of three years.

Property and equipment

Property and equipment are recorded at purchase or construction cost or valuation restated to the equivalent purchasing power of the ROL as at year end. At each reporting date the management assesses weather there is any indication of impairment of property, plant and equipment. If any such indication exists the management estimates the recoverable amount, which is determined as the higher of an asset's net selling price and its value in use. The carrying amount is reduced to the recoverable amount and the difference is recognised as an expense (impairment loss) in the income statement. An impairment loss recognised for an asset in prior years is reversed if there has been a change in the circumstances, which led to the impairment.

IFRS Financial Statements, page 12

AS AT 31 DECEMBER 2003 (all amounts expressed in ROL million, in terms of purchasing power of the Romanian Lei (ROL) at 31

December 2003, unless stated otherwise)

ACCOUNTING POLICIES (CONTINUED)

Gains and losses on disposal of property, plant and equipment, are determined by reference to their carrying amount and are taken into account in determining operating profit. Expenses for repairs and maintenance are charged to operating expenses as incurred. Interest expenses are not included in the cost of the cost of premises and equipment.

Assets for resale

Assets held for resale are initially recorded at fair value and subsequently measured at lower of cost or net realisable value.

Cash and cash equivalents

For the purposes of the cash flow statement, cash and cash equivalents comprise balances with less than 90 days maturity from the date of acquisition including: cash and balances with the Central Bank, treasury bills and other eligible bills and amounts due from other banks.

Treasury bills

Treasury bills are issued by the Romanian Ministry of Finance and other state corporations. Treasury bills are classified as held for trading and are carried at fair value. All interest income and any accrued gains/losses from trading in treasury bills are included in interest income. The changes in fair value are recognised in the statement of income.

Pension obligations and other post retirement benefits

In the normal course of business the Bank makes payments to the Romanian state funds on behalf of its employees for pension, health care and unemployment benefit. The cost of these payments is charged to the income statement in the same period as the related salary cost. All employees of the Bank are members of the State pension plan. The Bank does not operate any other pension scheme and, consequently, has no obligation in respect of pensions. The Bank does not operate any other defined benefit plan or post retirement benefit plan. The Bank has no obligation to provide further services to current or former employees.

IFRS Financial Statements, page 13

FOR THE YEAR ENDED 31 DECEMBER 2003 (all amounts expressed in ROL million, in terms of purchasing power of the Romanian Lei (ROL) at 31

December 2003, unless stated otherwise)

ACCOUNTING POLICIES (CONTINUED)

(p) Income taxes

The Bank records current profit tax based on the net income from the Bank's statutory financial statements, in accordance with Romanian profit tax legislation. Romanian profits tax legislation is based on a fiscal year ending on 31 December. In recording both the current and deferred income tax charge for the period, the Bank computes the income tax charge based on Romanian profit tax legislation enacted (or substantially enacted) at the balance sheet date.

Differences between financial reporting under International Financial Reporting Standards and Romanian fiscal regulations give rise to material differences between the carrying value of certain assets and liabilities and income and expenses for financial reporting and income tax purposes.

Deferred income tax is provided in full, using the balance sheet liability method, for all temporary differences arising between the tax bases of assets and liabilities and their carrying values for financial reporting purposes.

The principal temporary differences arise from the hyperinflation restatement of property and equipment, and provisions for impairment of loans and of other assets.

Deferred tax assets are recognised to the extent that it is probable that future taxable profit will be available against which the temporary differences can be utilised.

Deferred tax related to fair value re-measurement of available-for-sale investments which are charged or credited directly to equity, is also credited directly to equity and is subsequently recognised in the income statement together with the deferred gain or loss.

(q) Share capital

(i) Share issue costs

External costs directly attributable to the issue of new shares, other than on a business combination, are deducted from equity net of any related income taxes.

IFRS Financial Statements, page 14

FOR THE YEAR ENDED 31 DECEMBER 2003 (all amounts expressed in ROL million, in terms of purchasing power of the Romanian Lei (ROL) at 31

December 2003, unless stated otherwise)

ACCOUNTING POLICIES (CONTINUED)

(ii) Dividends on ordinary shares

Dividends on ordinary shares are recognised in equity in the period in which they are declared. Dividends for the year which are declared after the balance sheet date are dealt with in the subsequent events note. Dividends are declared on the basis of statutory financial statements prepared in accordance with banking regulations issued by the National Bank of Romania.

Acceptances

Acceptances comprise undertakings by the Bank to pay bills of exchange drawn by customers. The Bank expects most acceptances to be settled simultaneously with the reimbursement from the customers. Acceptances are accounted for as off-balance sheet transactions and are disclosed as contingent liabilities and commitments.

Fiduciary activities

Assets and income arising thereon together with related undertakings to return such assets to customers are excluded from these financial statements where the Bank acts in a fiduciary capacity such as nominee, trustee or agent.

Use of estimates

The preparation of financial statements in conformity with IFRS necessarily requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosures of contingent assets and liabilities at the date of the financial statements and reported expenses during the reported period.

Comparatives

Where necessary, comparative figures have been adjusted to conform with changes in presentation in the current year.

IFRS Financial Statements, page 15

FOR THE YEAR ENDED 31 DECEMBER 2003 (all amounts expressed in ROL million, in terms of purchasing power of the Romanian Lei (ROL) at 31

December 2003, unless stated otherwise)

NET INTEREST INCOME

Interest and discount income Interest income from banks Loans and advances Treasury bills

Year ended 31 December 2003

Year ended 31 December 2002

Interest expense Bank deposits Customer deposits Borrowings

FEE AND COMMISSION INCOME / EXPENSE

3.1 Fee and commission income

Year ended 31 December 2003

Year ended 31 December 2002

Commission income from money transfers

Commission income from loans and advances

Other fee and commission income

In the commission income from loans and advances there are commissions from loans origination which are recognized in the income statement when the loan is approved.

If these commissions were deferred and recognised as an adjustment to the effective yield of the loans, the commission income from loans and advances would be ROL 151,524 million, the amount of ROL 11 6,001 million being reclassified to loans and the deferred tax effect would result in a decrease of the deferred tax liability of ROL 29,000 million.

IFRS Financial Statements, page 16

FOR THE YEAR ENDED 31 DECEMBER 2003 (all amounts expressed in ROL million, in terms of purchasing power of the Romanian Lei (ROL) at 31

December 2003, unless stated otherwise)

FEE AND COMMISSION INCOME / EXPENSE (CONTINUED)

3.2 Fee and commission expense

Commission expense due to interbank operations

Other fee and commission expenses

NET FOREIGN EXCHANGE GAINS