Rapid Revision on Service tax & VAT - My Thoughts on … Revision on Service tax & VAT For CA ... If...

49

Rapid Revision on Service tax & VAT For CA - Final 2nd Floor, MSN Business Centre, #46 Sir Madhavan Nair Road, Mahalingapuram, Chennai – 600034. Near Kodambakkam Railway Station / Aiyappan Temple Mobile: +91 99403 81858 / +91 98843 62828 Email: [email protected]

Transcript of Rapid Revision on Service tax & VAT - My Thoughts on … Revision on Service tax & VAT For CA ... If...

Rapid Revision on Service tax & VAT For CA - Final

2nd Floor, MSN Business Centre, #46 Sir Madhavan Nair Road,

Mahalingapuram, Chennai – 600034. Near Kodambakkam Railway Station / Aiyappan

Temple Mobile: +91 99403 81858 / +91 98843 62828

Email: [email protected]

For CA & CMA classes, call @ 9940381858 2

CHAPTER - 1 BASICS OF SERVICE TAX

Finance Act, 1994 Provisions relating to Service tax

Service tax Rules, 1994 Procedures to carry out the provisions of service tax

Point of taxation Rules, 2011 To determine the rate and date of payment of service tax i.e. point of payment of service tax

Service tax valuation Rules, 2006 To determine the value when consideration is nor ascertainable and value in special cases

Place of provision of Services, Rules 2012

To determine the taxable location for the purpose of levy of service tax

Service tax (Compounding of offences) Rules, 2012

Procedure for compounding of offence to get immunity from prosecution

Sec. 66B Levy of Service tax

Sec. 65B Definitions under the Act

Sec. 66C Meaning of taxable territory

Sec. 66D Negative list

Sec. 66E Declared Services

Sec. 66F Principles of interpretation

1.1 What is the meaning of “Service”?

SERVICE - Sec. 65B(44)

MEANS

- Any Service

- Carried out by a person for another

- for consideration

INCLUDES

Declared Services

EXCLUDES

M - Transfer of movable property

A - Actionable claims

I - Transfer of immovable property

L - Legal Fees

E - Employee-Employer relationship

D - Deemed Sales

Visit www.pinnacleacademy.co for CA & CMA classes 3

Levy Point of payment Collection

Sec. 66B – Date of provision of taxable service

Point of taxation Rules, 2011: Generally, the date of invoice or date of payment received, whichever is earlier

Rule 6 of Service tax Rules, 1994: In case of Individual or Firm NNoorrmmaall ppaayymmeenntt - 5

th of the month following every quarter EE PPaayymmeenntt - 6

th of the month following every quarter In case of others NNoorrmmaall PPaayymmeenntt - 5

th of the month following every month EE PPaayymmeenntt - 6

th of the month following every month

Note: For the month ending march and quarter ending march, the due date of payment is March 31st.

For the purpose of e-payment ,the above amount of ₹10 lakhs has been revised to ₹ 1 lakh vide

Notification No. 16/2013—ST

1.2 What are declared Services?

The following 9 services are covered under declared services

1. Renting of immovable property 2. Construction Services 3. IPR Services 4. IT Software Services 5. Doing an act, Not doing an act & Tolerating an act 6. Hiring & Leasing of goods 7. Hire-purchase or installment transactions 8. Works Contract 9. Restaurant or Catering Services 1.3 What are deemed sales?

The following transactions are deemed to be sales as per Article 366(29A) of the Constitution. 1. Transfer otherwise than in pursuance of contract 2. Works contract 3. Hire purchase or installment transactions 4. Transfer of right to use goods (i.e. Leasing) 5. Supply of goods by an unincorporated association or body to its members 6. Supply of goods as a part of service, being food, drink or any other article for human

consumption

1.4 What is the meaning of ACTIVITY for CONSIDERATION?

Consideration means ―quid pro quo‖ - i.e. something in return. Consideration can be monetary or non monetary Money value of non monetary consideration shall be included in value. There must be a direct link between activity and consideration Such link must be immediate but not remote Activity without consideration is not service Consideration without activity does not constitute service Consideration may be paid by a person other than the person receiving the benefit of

service

For CA & CMA classes, call @ 9940381858 4

1.5 What is the meaning of “Service provider” and “Service recipient”?

Service provider: Any person who provides taxable service is ―Service provider‖

Service Recipient:Any person who is receiving taxable service provided by a service

provider is ―Service recipient‖.

1.6 What is the Meaning of person?

[Sec. 65B(37)]: Individual, HUF, Firm, LLP, AOP or BOI whether incorporated or not,

Company, co-op society, Government (Central/State), a local authority, or every artificial

juridical person not falling within any of the preceding sub clauses.

1.7 Who is actual service recipient?

Normally, the person who is legally entitled to receive a service and, therefore, obliged to

make payment, is the receiver of a service, whether or not he actually makes the payment

or someone else makes the payment on his behalf.

1.8 What is the meaning of transaction in money or actionable claim?

The principal amount of deposits in or withdrawals from a bank account. Advancing or repayment of principal sum on loan to someone. Conversion of notes into coins to the extent of amount received.

2.1 DECLARED SERVICES VS. DEEMED SALES - HIRING & LEASING OF GOODS

Declared Services – Entry (f) of Sec. 66E: Transfer of goods by way of hiring, leasing,

licensing or in any such manner without transfer of right to use such goods

Deemed sales - Article 366(29A)(d): Transfer of the right to use any goods for any

purpose (Whether or not for a specified period)

2.2 When excluded from Service?

When there involves transfer of right to use goods

When covered under sales tax or VAT laws as ―Deemed sales‖

2.3 When taxable as service?

When there is no transfer of right to use goods

If not covered under sales tax or VAT laws, then covered under declared services and service tax payable.

2.4 What is the test to determine whether a transaction involves transfer of right to use goods?

BSNL V. UOI (2006) (Supreme Court)

There must be goods available for delivery;

There must be a consensus ad idem as to the identity of the goods;

The transferee should have legal right to use the goods consequently

all legal consequences of such use including any permissions or licenses required

Visit www.pinnacleacademy.co for CA & CMA classes 5

therefore should be available to the transferee;

For the period during which the transferee has such legal right , it has to be the

exclusion to the transferor viz., a ‗transfer of the right to use‘ and not merely a license

to use the goods;

Having transferred, the owner cannot again transfer the same right to others.

2.5 Whether service tax is leviable on the activity by way of erection of pandal or

shamiana?

CBEC vide its circular dated 168/3/2013 clarified that pandal/shamiana erection activities do

not amount to transfer of right to use goods because effective possession and control over

pandal or shaminana remains with the service provider, even after the erection is complete

and the specially made up space for temporary use handed over to customer. Hence the

said activity is declared service under sec. 66E

3.1 DECLARED SERVICES VS. DEEMED SALES - HIRE-PURCHASE OR

INSTALLMENT TRANSACTIONS

Declared Services – Entry (g) of Sec. 66E Activities in relation to delivery of goods on

hire purchase or any system of payment by installments

Deemed Sales - Article 366(29A)(c) - Delivery of goods on hire-purchase or any system

of payment by installments

3.2 When the said transaction is taxable as service?

The delivery of goods on hire purchase or any system of payment on installment is not

chargeable to service tax because as per Article 366(29A) of the Constitution such delivery

of goods is deemed to be a sale of goods. However activities or services provided in relation

to such delivery of goods are covered in this declared list entry.

3.3 What is the value of taxable service?

In equipment leasing/hire purchase agreements there are two different and distinct

transactions, viz., the financing transaction and the equipment leasing/hire-purchase

transaction and that the financing transaction, consideration for which was represented by

way of interest or other charges like lease management fee, processing fee, documentation

charges and administrative fees, which is chargeable to service tax. Therefore, such financial

services that accompany a hire purchase agreement fall in the ambit of this entry of

declared services.

3.4 Whether service tax is payable on the entire value?

In terms of the exemption notification relating to such activities, service tax is leviable only

on 10% of the amount representing interest plus other charges explicitly charged as

mentioned above. An unconditional abatement is available vide notification no. 26/2012 to

the extent of 90% of the value of taxable service.

For CA & CMA classes, call @ 9940381858 6

4.1 DECLARED SERVICES VS. DEEMED SALES - WORKS CONTRACT

Declared Services – Entry (h) of Sec. 66E Service portion in the execution of works

contract

Deemed Sales - Article 366(29A)(b) - Transfer of property in goods (whether as goods

or in some other form) involved in the execution of a works contract

4.2 What is the meaning of “Works contract”?

A contract wherein transfer of property in goods involved in the execution of such contract is leviable to tax as sale of goods and such contract is for the purpose of carrying out construction, erection, commissioning, installation, completion, fitting out, repair, maintenance, renovation, alteration of any moveable or immoveable property or for carrying out any other similar activity or a part thereof in relation to such property.

4.3 When the said activity is taxable as service?

There will be two elements in a transaction in the nature of works contract, SALE ELEMENT and SERVICE ELEMENT.

ON SALE ELEMENT:

If the transfer of property in goods takes place within the state then VAT shall be levied on

the sale element at the VAT rate applicable in that state. If the transfer of property in goods

takes place from one state to another state then CST shall be levied on the sale element at

the applicable CST rate.

ON SERVICE ELEMENT:

The service tax shall be payable on the value of works contract service.

4.4 How to determine the value of works contract service?

A works contract can be segregated into a contract of sale and contract of provision of

service – BSNL case (2006) (SC).

This declared list entry has been incorporated to capture this position of law in simple

terms.

The value of service portion shall be determined in terms of Rule 2A of valuation rules,

2006

4.5 What is the value of works contract service?

Value in case of Works Contract-Rule 2A

Normal Scheme - Deduction Method:

Gross amount charged for the works contract (-) Value of transfer of property in goods

involved in the execution of said works contract = Value of works contract service on which

service tax is payable.

Normal Scheme - Addition Method: Sum of all labour elements in the contract and appropriate profit margin. [No CENVAT credit on Inputs used in execution of works contract. But credit on Input services and capital goods available]

Composition Scheme: In case of composition scheme, a composite rate on ENTIRE amount is payable as service

tax and CENVAT credit is disallowed on inputs.

Visit www.pinnacleacademy.co for CA & CMA classes 7

Where works contract is for

Execution of original works

Maintenance or repair or reconditioning or restoration or servicing of any goods

Other works contracts

Value of the service portion shall be

40% of the total amount charged for the works contract

70% of the total amount charged for the works contract

60% of the total amount charged for the works contract

5.1 DECLARED SERVICES VS. DEEMED SALES - RESTAURANT SERVICE

Declared Services - Entry (i) of Sec. 66E Service portion in an activity wherein goods,

being food or any other article of human consumption or any drink (whether or not

intoxicating) is supplied in any manner as a part of the activity.

Deemed Sales - Article 366(29A)(f) - Supply, by way of or as part of any service in any

manner whatsoever, of goods, being food or any other article for human consumption or

any drink (whether or not intoxicating)

5.2 What are the activities covered under this entry?

The following activities are illustration of activities covered in this entry

a. Supply of food or drinks in a restaurant;

Supply of foods and drinks by an outdoor caterer.

5.3 How to determine the value of service portion?

A contract involving service along with supply of goods can be dissected into a

contract of sale of goods and contract of provision of service

This declared list entry has been incorporated to capture this position of law in

simple terms

The value of service portion shall be determined in terms of Rule 2C of Valuation

Rules, 2006.

5.4 What is the value of service portion?

Value in case of restaurant or outdoor catering - Rule 2C

The value of service portion is as follows:

Goods being food or any other article for human consumption Supplied in a restaurant —> Value = 40% of total amount charged

Goods being food or any other article for human consumption supplied as a part of outdoor catering —> Value = 60% of total amount charged

CENVAT Credit Implications for above: No CENVAT credit on goods falling under chapter 1 to 22 of CETA (i.e food, edibles or

beverages incl. live animals) CENVAT credit available on other inputs, input services and capital goods subject to the

provision of CENVAT credit rules

For CA & CMA classes, call @ 9940381858 8

Bundled service of Catering with Renting: - Notification No. 26/2012) Taxable Value = 70% of total amount, without taking CENVAT credit on any goods used for providing service Computation of total amount charged for the purpose of Rule 2C as well as

Notification no. 26/2012.:

Gross amount charged XXX

AddAdd: FMV of all goods and services supplied by the service receiver in or in relation to the supply of food or any other article of human consumption or any drink (whether or not intoxicating), under the same contract or any other contract

XXX

Less: Amount charged for the goods or services provided by the service receiver

(XX)

Less: VAT or Sales tax levied to the extent they form part of the gross amount or the total amount, as the case may be.

(XX)

Total amount charged for the purpose of Rule 2C or Notification no. 26/2012

XXX

6. CASE DIGEST:

Dewan Chand Ram Saran Case (SC)

In case of reverse charge, the liability is on service recipient. But out of a contract, the said

liability can be shifted to service provider. There is nothing in law to prevent them from

entering into agreement regarding burden of tax arising under the contract between them

Cherthala Muncipality Case (HC) Service tax burden can be passed on to the service recipient, even though in the contract or

agreement there is no provision for payment of service tax by service recipient. It is the

statutory right of the service provider to pass service tax liability to service recipient.

TTD Case (HC) Service tax is payable when there is an activity for consideration, unless such activity is

specified in negative list or is exempted. Its does not matter whether such activity is

performed with a profit motive or not. Even though accommodation service is for charitable

purpose, but service tax is payable as there is consideration involved in the transaction.

Mayo College General Council Case (HC) When service provider permitted other schools to use their name, logo as motto, it clearly

tantamounted to provider franchise service. The asseessee cannot take a stand that it

received collaboration fees as consideration and not franchise fees. For levy of service tax

consideration must be present and the name of consideration is not relevant.

TCS Case (SC) - Land mark Judgment A software, whether customized or non customised , would become goods provided it has

the attributes thereof having regard to (a) Utility (b) Capable og being bought and sold (c)

Visit www.pinnacleacademy.co for CA & CMA classes 9

Capable of transmitted, transferred, delivered, stored and possessed.

Infotech software dealers association (ISODA) Case (HC) When right to use software has been transferred to the subscribers of software for a

consideration, even though the software is goods, the said transaction may not amount to

sale in all cases and hence service tax shall be levied.

Nahar Industrial Enterprises Ltd. Case (HC) As per the principle of mutuality, there must be two parties for the levy of service tax and

one cannot provide service to himself. There is no service involved when a service provider

stored the goods, in a warehouse owned by him. The position will be same even though

service provider received subsidy from government, as such subsidy received is on account

of loss of interest, cost of insurance etc., incurred for compliance of the directions of

government.

Lincoln Helios (india) Ltd. Case (HC) In a transaction, which involves manufacture and provision of service, excise duty must be

payable on the aspect of manufacture and service tax must be payable on the aspect of

service. It does not amount to payment of tax twice

For CA & CMA classes, call @ 9940381858 10

7. POINT OF TAXATION RULES, 2011

Explanation to the above table:

For point no. 4 –As amount is received prior to starting the work, the point of

taxation shall be the date when payment is received [In such cases the invoice given

shall be known as ―Proforma Invoice‖ or ―Quotation‖]. But Rule 4A of ST Rules, 1994

requires that invoice in case of advance received should be issued within 30 days

from the date of advance received. (This is a procedural requirement but do not

have any bearing on the point of taxation)

For point no. 5 – As amount is received prior to completion of work, the point of

taxation shall be the date when payment is received [In such case, the invoice is not

necessarily the invoice as per Rule 4A of Service tax Rules, 1994]. But Rule 4A of ST

Rules, 1994 requires that invoice in case of advance received should be issued within

30 days from the date of advance received.

For point no. 7 – There is a mandatory requirement as per Rule 4A of ST Rules, 1994

that an invoice must be issued within 30 days from the date of completion of service

and if the invoice is issued within the stipulated time, then point of taxation shall be

the date of invoice and if not, then the point of taxation shall be the date of

completion of service.

In effect, always remember, point of taxation shall be the date of invoice or date

of payment received, whichever is earlier.

Visit www.pinnacleacademy.co for CA & CMA classes 11

Different situations and the point of taxation in each situation.

Date of Completion of service (note 1)

Date of Invoice

Date of payment received

Rule 3 THE RATE OF DUTY IS SAME ON ALL THE DATES – Normal Service

(i) If payment is received before issuing invoice. (i.e. Advance) [See note 4 below]

POT

(ii) If Invoice is issued within 30 or 45 days from the date of completion of service

POT shall be earlier of these two dates

(iii) If Invoice is not issued within 30 or 45 days from the date of completion of service

POT

Rule 3CONTINUOUS SUPPLY OF SERVICE [See note 2 for meaning]

Same as situation (i) except that deeming fiction regarding the COMPLETION OF SERVICE [See note 3 below]

Rule 4(a) SERVICE PROVIDED BEFORE CHANGE IN RATE

POT shall be EARLIER of these 2 dates

[See note 5 below]

Rule 4(b) SERVICE PROVIDED AFTER CHANGE IN RATE [See note 6 below]

(i) If both invoice and payment are received before change in rate (or) If both invoice and payment are received after change in rate

POT shall be EARLIER of these 2 dates

(ii) In a case other than (i) above POT shall be LATER of these 2 dates

Rule 5 WHEN A SERVICE BECOMES TAXABLE FOR THE FIRST TIME

(i) If invoice is issued and payment is received before the new service becomes taxable

NO TAX PAYABLE to that extent

(ii) If invoice is issued within 14 days after the new service becomes taxable but payment is received before

NO TAX PAYABLE [Provided, invoice is issued to the extent of

payment received]

(iii) Scenario (i) - If invoice is issued before, but payment is received after. (Or) Scenario (ii) - If invoice not issued within 14 days after the new service becomes taxable but payment is received before.

POT

(iv) If both invoice and payment date falls after the new service becomes taxable.

POT shall be EARLIER of these 2 dates

Rule 7 REVERSE CHARGE [See note 8]

POT (If payment is not made to SP within 6 months

from invoice date)

POT (If payment is made to SP

within 6 months from Invoice

date)

Rule 7 TRANSACTIONS WITH ASSOCIATED ENTERPRISES (Where person providing service is outside India)[Remember: The liability to pay duty is on the service recipient]

Date of debit in the books of service recipient or date of making

payment, whichever is earlier

Rule 8 Payments pertaining to copyrights and trademarks [See Note 7 below]

POT shall be EARLIER of these 2 dates

For CA & CMA classes, call @ 9940381858 12

Notes to above table:

1. Meaning of completion of Service Not only completion of physical part of

providing service but also the completion of all other auxiliary activities that enable

the service provider to be in a position to issue the invoice [This is the Acid

Test]. Such auxiliary activities could include activities like measurement, quality

testing etc which may be essential pre-requisites for identification of completion of

service. However such activities DO NOT INCLUDE flimsy or irrelevant grounds for

delay in issuance of invoice. – Circular No. 144/13/2011.

2. Meaning of “Continuous supply of Service” MEANS any service which is to be

provided or to be provided continuously or on recurrent basis, under a contract, for a

period exceeding 3 months with the obligation for payment periodically from time to

time. (or) Services notified by central government as continuous supply of service,

irrespective of the period.

Following services are notified by central government for this purpose

Telecommunication service

Works contract service.

3. Date of completion of provision of service in case of continuous supply of

service in case of continuous supply of service, where the provision of whole or

part of the service is determined periodically on the completion of an event in terms

of a contract, which requires the receiver of service to make any payment to service

provider, the date of completion of each such event specified in the contract shall be

deemed to be the date of completion of provision of service.

4. POT in case where payment upto 1,000 received in excess of the invoiced

amount when a service provider receives a payment upto 1,000 in excess of

amount indicated in invoice, the POT to the extent of such excess amount, shall be

a) Date of invoice or date of completion, whichever is earlier.(Or)

b) Date of receipt of payment.

The service provider can choose either (a) or (b) above as POT. [This is a facilitation

provided to service providers in telecommunications, credit card business who

regularly receive minor excess payments from their customers]

5. As the service is provided before the change in rate, the intention of the department

is to collect old rate. Due to this reason, the POT shall be earlier of Invoice date or

payment received date.

6. In this case, as services are provided after the change in rate, the intention of the

department is to collect new rate. Due to this reason, the POT shall be later of

Invoice date or payment received date. But, in case where all the events fall before

the change in rate, the tax shall be payable as per the old rate (Earlier of two dates

or later of two dates is not relevant, as on both the dates the prevailing rate is old

rate!!!)

7. In case of royalties and payments pertaining to copyrights, trademarks, designs or

patents, the whole amount of the consideration for the provision of service is not

ascertainable at the time when service was performed, and subsequently the use or

benefit of these services by a person other than the provider gives raise to any

payment of consideration.

Visit www.pinnacleacademy.co for CA & CMA classes 13

8. In case where payment is not made by service recipient within 6 months from the

date of Invoice, then Rule 7 will not be applicable and POT shall be determined as

per Rule 3 i.e. Where invoice is issued by the service provider within 30 days from

the date of completion, then POT shall be the date of Invoice or else POT shall be

the date of completion of service

8. PLACE OF PROVISION OF SERVICES RULES, 2012

Explanation to the above chart:

Case (i) – When both service provider and service recipient are in taxable territory, the

service shall be a taxable service and liability to pay service tax is on the service provider.

Case (ii) – When both service provider and service recipient are in non-taxable territory,

the service shall not be a taxable service and there is no liability to pay service tax on

either party.

Case (iii) – When service provider is in taxable territory and service recipient is in non-

taxable territory, the service shall not be a taxable service as the service is CONSUMED in

non-taxable territory. There is no tax liability on either party.

Case (iv) – When service provider is in non-taxable territory and service recipient is in

taxable territory, the service shall be a taxable service as the service is CONSUMED in

taxable territory. In such a case, the liability to pay tax is on the service recipient and it is

termed as reverse charge (a.k.a tax shift)

For CA & CMA classes, call @ 9940381858 14

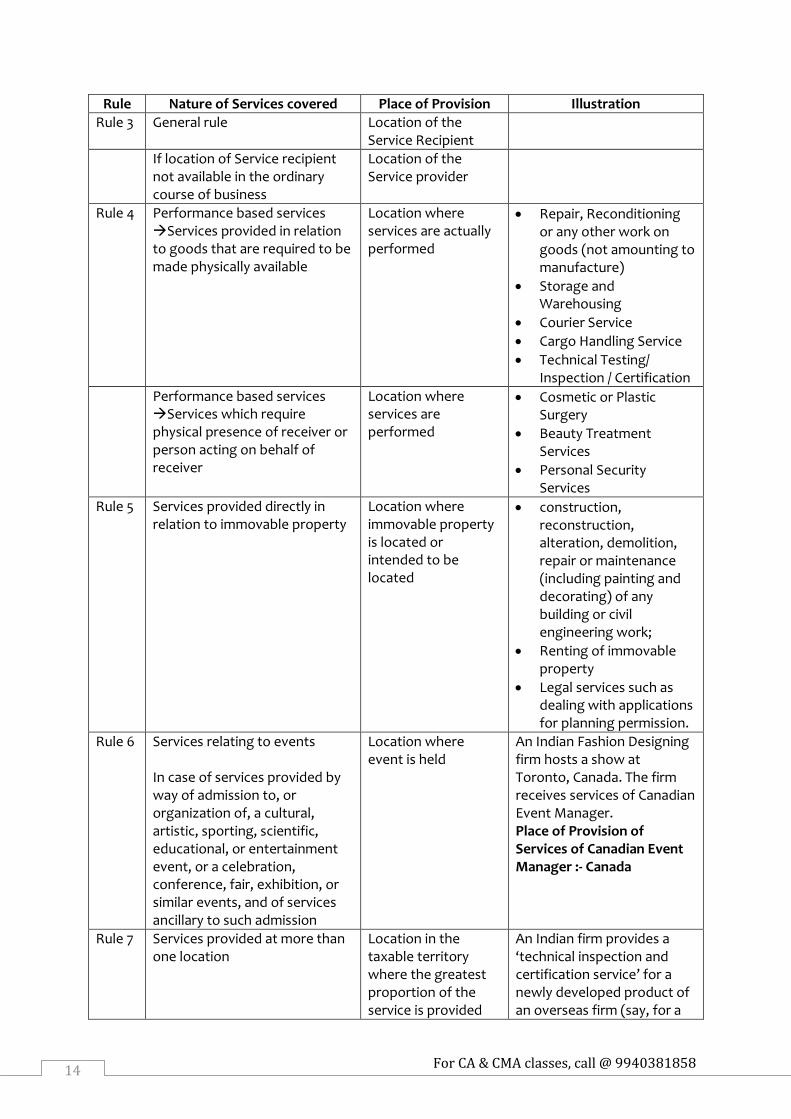

Rule Nature of Services covered Place of Provision Illustration

Rule 3 General rule Location of the Service Recipient

If location of Service recipient not available in the ordinary course of business

Location of the Service provider

Rule 4 Performance based services Services provided in relation to goods that are required to be made physically available

Location where services are actually performed

Repair, Reconditioning or any other work on goods (not amounting to manufacture)

Storage and Warehousing

Courier Service

Cargo Handling Service

Technical Testing/ Inspection / Certification

Performance based services Services which require physical presence of receiver or person acting on behalf of receiver

Location where services are performed

Cosmetic or Plastic Surgery

Beauty Treatment Services

Personal Security Services

Rule 5 Services provided directly in relation to immovable property

Location where immovable property is located or intended to be located

construction, reconstruction, alteration, demolition, repair or maintenance (including painting and decorating) of any building or civil engineering work;

Renting of immovable property

Legal services such as dealing with applications for planning permission.

Rule 6 Services relating to events In case of services provided by way of admission to, or organization of, a cultural, artistic, sporting, scientific, educational, or entertainment event, or a celebration, conference, fair, exhibition, or similar events, and of services ancillary to such admission

Location where event is held

An Indian Fashion Designing firm hosts a show at Toronto, Canada. The firm receives services of Canadian Event Manager. Place of Provision of Services of Canadian Event Manager :- Canada

Rule 7 Services provided at more than one location

Location in the taxable territory where the greatest proportion of the service is provided

An Indian firm provides a ‘technical inspection and certification service’ for a newly developed product of an overseas firm (say, for a

Visit www.pinnacleacademy.co for CA & CMA classes 15

newly launched motorbike which has to meet emission standards in different states or countries). Say, the testing is carried out in Maharashtra (20%), Kerala (25%), and an international location (say, Colombo 55%). Place of Provision: - Kerala notwithstanding the fact that the greatest proportion of a service rendered is outside the taxable territory.

Rule 8 Service provider and service receiver located in taxable territory In case where the place of provision of service provided in the taxable territory may be determinable to be outside taxable territory by applying one of the earlier rules but the service provider and service recipient are located in taxable territory

Location of the Service recipient

A helicopter of PawanHans Ltd (India based) develops a technical snag in Nepal. Say, engineers are deputed by Hindustan Aeronautics Ltd, Bangalore, to undertake repairs at the site in Nepal. Place of Provision: - Within the Taxable Territory. But for this Rule, Rule 4(1) would apply in this case and the place of provision would have been Nepal i.e. outside the taxable territory.

Rule 9 In case of following specified services (a) Services provided by a banking company, or a FI, or a NBFC, to account holders;

Location of the service provider

Services linked to or requiring opening and operation of bank accounts such as lending, deposits, safe deposit locker etc.

(b) Online information and database access or retrieval services;

Digitized content of books and other electronic publications, subscription of online newspapers and journals, online news, flight information and weather reports;

Web-based services providing access or download of digital content.

(c) Intermediary services; Travel Agent (any mode of travel)

Tour Operator

Commission agent for a service [an agent for

For CA & CMA classes, call @ 9940381858 16

buying or selling of goods is excluded]

(d) Service consisting of hiring of means of transport, upto a period of one month.

Vehicles designed specifically for the transport of sick or injured persons.

Mechanically or electronically propelled invalid carriages.

Rule 10

Goods transportation Services Services of transportation of goods, other than by way of mail or courier.

place of destination of the goods

If a consignment of crystal ware is consigned from Paris to New Delhi. Place of Provision:- New Delhi

Goods transportation services Services provided by goods transport agency (GTA)

Location of person liable to pay tax

Rule 11 Passenger transportation services

Place where the passenger embarks on the conveyance for a continuous journey

Rule 12 In case of services provided on board a conveyance during the course of a passenger transport operation, including services intended to be wholly or substantially consumed while on board

The first scheduled point of departure of that conveyance for the journey

A video game or a movie-on demand is provided on a Delhi-Kolkata-Bangkok-Jakarta flight during the Bangkok-Jakarta leg Place of Provision :- Delhi

Rule 13

In order to prevent double taxation or non-taxation of the provision of a service, orfor the uniform application of rules, the Central Government shall have the power to notify any description of service or circumstances in which the place of provision shall be the place of effective use and enjoyment of a service.

Rule 14

Notwithstanding anything stated in any rule, where the provision of a service is, prima facie, determinable in terms of more than one rule, it shall be determined in accordance with the rule that occurs later among the rules that merit equal consideration. Illustration: An architect based in Mumbai provides his service to an Indian Hotel Chain (which has business establishment in New Delhi) for its newly acquired property in Dubai. If Rule 5(Property Rule) were to be applied, the place of provision would be the location of the property i.e. Dubai (outside the taxable territory). With this result, the service would not be taxable in India. Whereas, by application of Rule 8, since both the provider and the receiver are located in taxable territory, the place of provision would be the location of the service receiver i.e. New Delhi. Consequently, service would be taxable in India. By application of Rule 14, the latter of the Rules i.e. Rule 8 would be applied to determine the place of provision.

Visit www.pinnacleacademy.co for CA & CMA classes 17

Whether filing of declaration of description, value etc. of input services used in providing IT enabled services (call centre/BPO services) exported outside India, after the date of export of services will disentitle an exporter from rebate of service tax paid on such input services?

Wipro Ltd. v. Union of India (2013) (Del.)

As per notification no. 39/2012 the provider of taxable service to be

exported has to file a declaration with jurisdictional AC/DC of excise

describing the taxable service intended to be exported with

description, value and the amount of service tax/excise duty and

cess payable on input services or inputs actually required to be used

in providing taxable service to be exported, PRIOR to the date of

export of such taxable service.

Facts of the case:

Wipro Ltd. rendered IT-enabled services such as technical support services, customer-care services, back-office services etc. to clients outside the country.

It involved attending to cross-border telephone calls relating to a variety of queries from existing or prospective customers in respect of the products or services of multinational corporations.

For rendering such services, the appellant used input services such as night transportation, recruitment, training, bank charges etc. The appellant claimed rebate of the service tax paid by it on such input services, used in providing the output services which were exported during a particular time period, under the said notification.

However, the declaration required under the notification was filed only after the export of the services i.e., after the particular time period during which the services were exported and for which the rebate claim was filed.

The rebate claims were rejected by the Department on the ground that the prescribed procedure, as laid down in Notification, for obtaining the rebate was not followed by the appellant.

Decision:

Continuous service: The High Court observed that Since the calls were received and attended to in the call centre on a continuous basis, it was impossible for the appellant to not only determine the date of export but also anticipate the call so that the declaration could be filed ―prior‖ to the date of export.

Incomplete information for declaration: The appellant was also required to describe, value and specify the amount of service tax payable on input services actually required to be used in providing taxable service to be exported. The High Court opined that except the description of the input services, the appellant could not provide the value and amount of service tax payable.

One to one correlation not possible: Further, the High Court also observed that one-to-one matching of input services with exported services was impossible since every phone call was export of taxable service but the invoices in respect of the input-services were received only at regular intervals, viz. monthly or fortnightly etc.

Thus, the High Court was of the view that in the very nature of things, and considering the peculiar features of the appellant's business, it was difficult to comply with the requirement ―prior‖ to the date of the export.

The High Court, therefore, allowed the rebate claims filed by the appellants.

For CA & CMA classes, call @ 9940381858 18

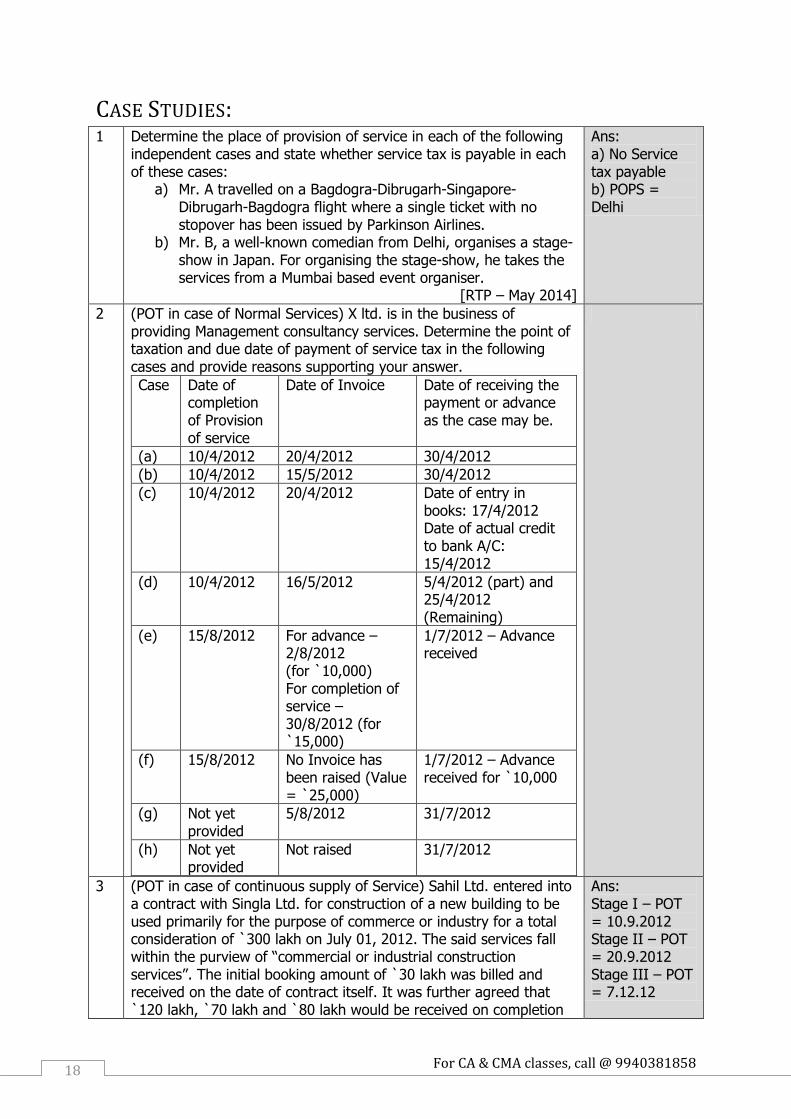

CASE STUDIES: 1 Determine the place of provision of service in each of the following

independent cases and state whether service tax is payable in each of these cases:

a) Mr. A travelled on a Bagdogra-Dibrugarh-Singapore-Dibrugarh-Bagdogra flight where a single ticket with no stopover has been issued by Parkinson Airlines.

b) Mr. B, a well-known comedian from Delhi, organises a stage-show in Japan. For organising the stage-show, he takes the services from a Mumbai based event organiser.

[RTP – May 2014]

Ans: a) No Service tax payable b) POPS = Delhi

2 (POT in case of Normal Services) X ltd. is in the business of providing Management consultancy services. Determine the point of taxation and due date of payment of service tax in the following cases and provide reasons supporting your answer.

Case Date of completion of Provision of service

Date of Invoice Date of receiving the payment or advance as the case may be.

(a) 10/4/2012 20/4/2012 30/4/2012

(b) 10/4/2012 15/5/2012 30/4/2012

(c) 10/4/2012 20/4/2012 Date of entry in books: 17/4/2012 Date of actual credit to bank A/C: 15/4/2012

(d) 10/4/2012 16/5/2012 5/4/2012 (part) and 25/4/2012 (Remaining)

(e) 15/8/2012 For advance – 2/8/2012 (for `10,000) For completion of service – 30/8/2012 (for `15,000)

1/7/2012 – Advance received

(f) 15/8/2012 No Invoice has been raised (Value = `25,000)

1/7/2012 – Advance received for `10,000

(g) Not yet provided

5/8/2012 31/7/2012

(h) Not yet provided

Not raised 31/7/2012

3 (POT in case of continuous supply of Service) Sahil Ltd. entered into a contract with Singla Ltd. for construction of a new building to be used primarily for the purpose of commerce or industry for a total consideration of `300 lakh on July 01, 2012. The said services fall within the purview of ―commercial or industrial construction services‖. The initial booking amount of `30 lakh was billed and received on the date of contract itself. It was further agreed that `120 lakh, `70 lakh and `80 lakh would be received on completion

Ans: Stage I – POT = 10.9.2012 Stage II – POT = 20.9.2012 Stage III – POT = 7.12.12

Visit www.pinnacleacademy.co for CA & CMA classes 19

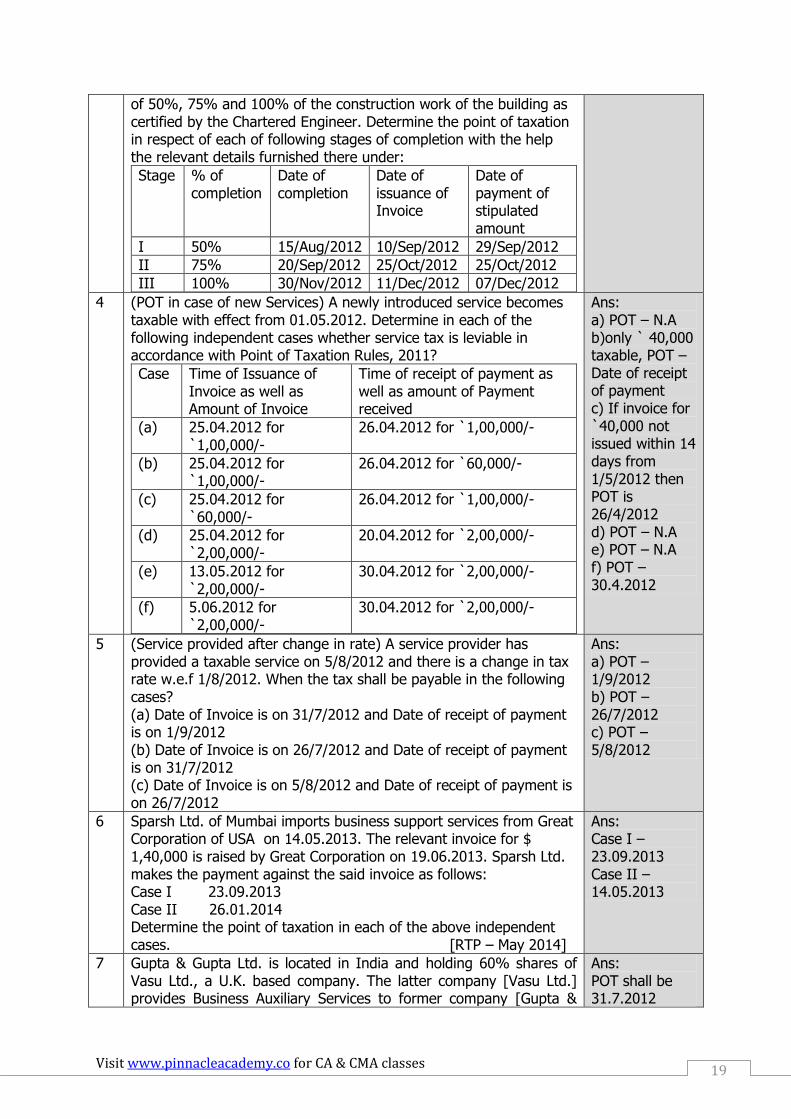

of 50%, 75% and 100% of the construction work of the building as certified by the Chartered Engineer. Determine the point of taxation in respect of each of following stages of completion with the help the relevant details furnished there under:

Stage % of completion

Date of completion

Date of issuance of Invoice

Date of payment of stipulated amount

I 50% 15/Aug/2012 10/Sep/2012 29/Sep/2012

II 75% 20/Sep/2012 25/Oct/2012 25/Oct/2012

III 100% 30/Nov/2012 11/Dec/2012 07/Dec/2012

4 (POT in case of new Services) A newly introduced service becomes taxable with effect from 01.05.2012. Determine in each of the following independent cases whether service tax is leviable in accordance with Point of Taxation Rules, 2011?

Case Time of Issuance of Invoice as well as Amount of Invoice

Time of receipt of payment as well as amount of Payment received

(a) 25.04.2012 for `1,00,000/-

26.04.2012 for `1,00,000/-

(b) 25.04.2012 for `1,00,000/-

26.04.2012 for `60,000/-

(c) 25.04.2012 for `60,000/-

26.04.2012 for `1,00,000/-

(d) 25.04.2012 for `2,00,000/-

20.04.2012 for `2,00,000/-

(e) 13.05.2012 for `2,00,000/-

30.04.2012 for `2,00,000/-

(f) 5.06.2012 for `2,00,000/-

30.04.2012 for `2,00,000/-

Ans: a) POT – N.A b)only ` 40,000 taxable, POT – Date of receipt of payment c) If invoice for `40,000 not issued within 14 days from 1/5/2012 then POT is 26/4/2012 d) POT – N.A e) POT – N.A f) POT – 30.4.2012

5 (Service provided after change in rate) A service provider has provided a taxable service on 5/8/2012 and there is a change in tax rate w.e.f 1/8/2012. When the tax shall be payable in the following cases? (a) Date of Invoice is on 31/7/2012 and Date of receipt of payment is on 1/9/2012 (b) Date of Invoice is on 26/7/2012 and Date of receipt of payment is on 31/7/2012 (c) Date of Invoice is on 5/8/2012 and Date of receipt of payment is on 26/7/2012

Ans: a) POT – 1/9/2012 b) POT – 26/7/2012 c) POT – 5/8/2012

6 Sparsh Ltd. of Mumbai imports business support services from Great Corporation of USA on 14.05.2013. The relevant invoice for $ 1,40,000 is raised by Great Corporation on 19.06.2013. Sparsh Ltd. makes the payment against the said invoice as follows: Case I 23.09.2013 Case II 26.01.2014 Determine the point of taxation in each of the above independent cases. [RTP – May 2014]

Ans: Case I – 23.09.2013 Case II – 14.05.2013

7 Gupta & Gupta Ltd. is located in India and holding 60% shares of Vasu Ltd., a U.K. based company. The latter company [Vasu Ltd.] provides Business Auxiliary Services to former company [Gupta &

Ans: POT shall be 31.7.2012

For CA & CMA classes, call @ 9940381858 20

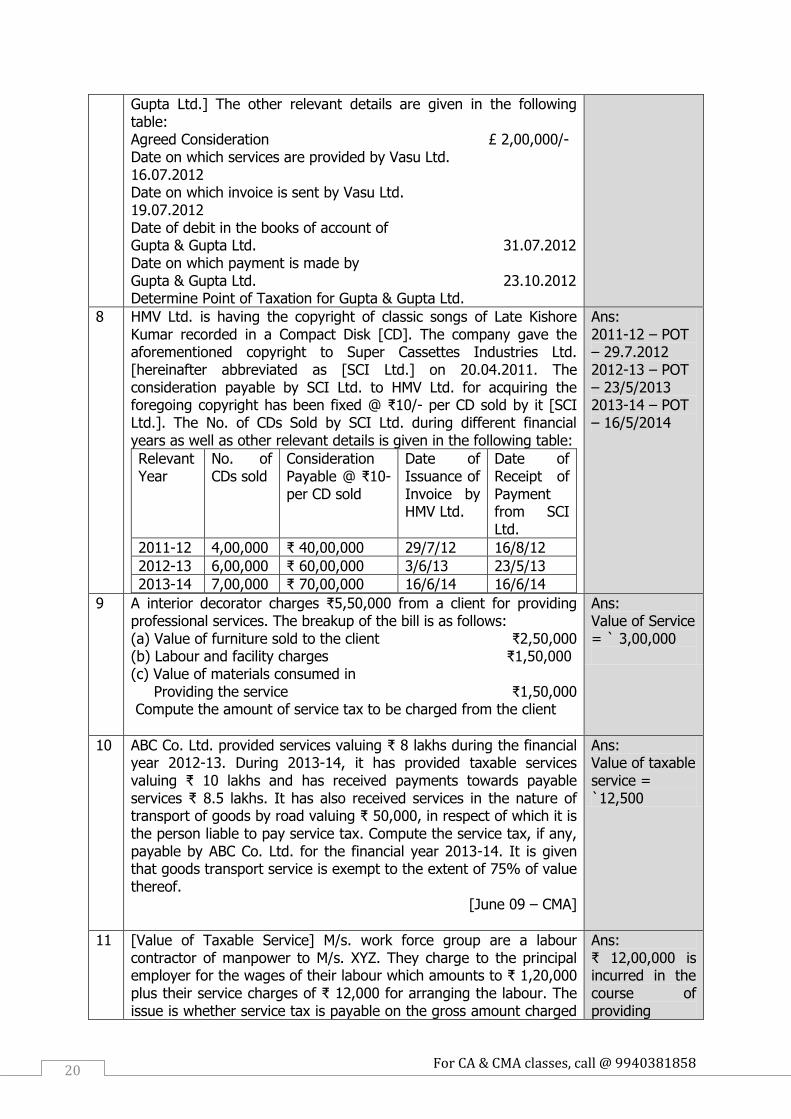

Gupta Ltd.] The other relevant details are given in the following table: Agreed Consideration £ 2,00,000/- Date on which services are provided by Vasu Ltd. 16.07.2012 Date on which invoice is sent by Vasu Ltd. 19.07.2012 Date of debit in the books of account of Gupta & Gupta Ltd. 31.07.2012 Date on which payment is made by Gupta & Gupta Ltd. 23.10.2012 Determine Point of Taxation for Gupta & Gupta Ltd.

8 HMV Ltd. is having the copyright of classic songs of Late Kishore Kumar recorded in a Compact Disk [CD]. The company gave the aforementioned copyright to Super Cassettes Industries Ltd. [hereinafter abbreviated as [SCI Ltd.] on 20.04.2011. The consideration payable by SCI Ltd. to HMV Ltd. for acquiring the foregoing copyright has been fixed @ ₹10/- per CD sold by it [SCI Ltd.]. The No. of CDs Sold by SCI Ltd. during different financial years as well as other relevant details is given in the following table:

Relevant Year

No. of CDs sold

Consideration Payable @ ₹10- per CD sold

Date of Issuance of Invoice by HMV Ltd.

Date of Receipt of Payment from SCI Ltd.

2011-12 4,00,000 ₹ 40,00,000 29/7/12 16/8/12

2012-13 6,00,000 ₹ 60,00,000 3/6/13 23/5/13

2013-14 7,00,000 ₹ 70,00,000 16/6/14 16/6/14

Ans: 2011-12 – POT – 29.7.2012 2012-13 – POT – 23/5/2013 2013-14 – POT – 16/5/2014

9 A interior decorator charges ₹5,50,000 from a client for providing professional services. The breakup of the bill is as follows: (a) Value of furniture sold to the client ₹2,50,000 (b) Labour and facility charges ₹1,50,000 (c) Value of materials consumed in Providing the service ₹1,50,000 Compute the amount of service tax to be charged from the client

Ans: Value of Service = ` 3,00,000

10 ABC Co. Ltd. provided services valuing ₹ 8 lakhs during the financial year 2012-13. During 2013-14, it has provided taxable services valuing ₹ 10 lakhs and has received payments towards payable services ₹ 8.5 lakhs. It has also received services in the nature of transport of goods by road valuing ₹ 50,000, in respect of which it is the person liable to pay service tax. Compute the service tax, if any, payable by ABC Co. Ltd. for the financial year 2013-14. It is given that goods transport service is exempt to the extent of 75% of value thereof.

[June 09 – CMA]

Ans: Value of taxable service = `12,500

11 [Value of Taxable Service] M/s. work force group are a labour contractor of manpower to M/s. XYZ. They charge to the principal employer for the wages of their labour which amounts to ₹ 1,20,000 plus their service charges of ₹ 12,000 for arranging the labour. The issue is whether service tax is payable on the gross amount charged

Ans: ₹ 12,00,000 is incurred in the course of providing

Visit www.pinnacleacademy.co for CA & CMA classes 21

by them or only their charges for labour. Advice? [May 2006]

service and hence includible in value.

12 IOC has awarded a contract in August, 2012 for ₹140 lakh to M/s Jagjit Construction Ltd. in respect of alterations to one of its buildings. The said building was abandoned by IOC five years ago. The materials required for carrying out alterations will be supplied by Jagjit constructions Ltd. itself. The purpose of awarding the foregoing contract is to make the said building workable. Whether the aforesaid services of Jagjit constructions Ltd. are subject to service tax and if so, determine the amount of service tax payable?

Ans: Amount of service tax payable ₹ 6,92,160/-

13 A&Co. of Srinagar rendered taxable services both within and outside the state of Jammu and Kashmir. It received ₹26,12,000 for the services rendered inside the state of Jammu & Kashmir and ₹18,00,000 for the services rendered outside the state of Jammu & Kashmir. Compute its taxable service value and service tax liability. Answer with reference to the provisions of place of provision of service Rules, 2012. In case, A&Co. was situated in Mumbai what would be the value of taxable service and service tax liability?

Answer as follows

14 State briefly, Whether service tax will be levied in each of the following independent cases: (i) Services provided in the state of Rajasthan by a person having place of business in the state of Jammu and Kashmir. (ii) Agency services provided by Raj Ltd. [located in taxable territory] in October, 2012 for ₹1,00,000 to Preethi Ltd. [Which is also located in taxable territory] (iii) Service provided to an Export oriented unit located in India (iv) Kirti Ltd. [Service Provider] is a German Company. It renders a service to a subsidiary of Tata Ltd. [an Indian company] located abroad. However, payment to Kirti Ltd. has been made by holding Indian company. (v) Nitin Ltd. provided services to Indian Oil Corporation from vessels located in the continental shelf of India for the purposes of prospecting natural gas for ₹50 lakh in September, 2012. [Practice manual]

Answer as follows

15 Determine the place of provision of services as well as their taxability in each of the following independent cases: (i) Mr. A, the owner of an immovable property located in New Delhi gives on rent the said property to Mr. B of UP for commercial purposes. (ii) Mr. Rahul, a Delhi based interior decorator provides his professional services in respect of property which is intended to be located in Punjab. (iii) A USA based company possessing specialization in mineral exploration has been awarded a contract for mineral exploration in respect of specific sites in Canada by Mumbai based Mr. Ram kapoor. (iv) ABC Ltd. agrees to provide [by virtue of single agreement for consolidated consideration] services connected with oil exploration to XYZ Ltd. in respect of specific sites located in Assam, Gujarat and Maharashtra. The proportion of services provided by ABC Ltd. in relation to above states worked out to be

Answer as follows

For CA & CMA classes, call @ 9940381858 22

25%, 60% and 15% (v) Rohit, a consulting engineer provides his professional consultancy services to a U.K based company in respect of its three properties located in UK, USA and Dubai. (vi) Yokesh, Chennai based professional valuer provides his professional services of valuation of immovable properties [vide a single contract for consolidated consideration] to Mumbai based Reliance Industries Ltd. in respect of its four properties located in Delhi, Kashmir, Kolkata and London. It is assumed that Yogesh performed 20%, 30%, 15% and 35% of his total services in foregoing four cities respectively. (vii) A Delhi based builder provides construction services to Punjab based company in respect of construction of its new building in Bangladesh.

Answer to Question No. 13:

Reference: Rule 3 of Place of provision of services Rules, 2012

Provision: In ordinary cases, the place of provision of service shall be the location of

service receiver. If service receiver is located in taxable territory, then such service is

taxable. If service recipient is located in non taxable territory, then such service is non

taxable service

Facts & Discussion:

Applicability of Service tax if A&Co. is located in Srinagar:

Service provided within the state of Jammu and Kashmir is not subject to service tax as the

location of service recipient is relevant and service recipient is located in nontaxable

territory. Hence, ₹ 26,12,000 for services rendered in the state of jammu and Kashmir is not

chargeable to service tax. Services rendered outside Jammu & Kashmir are ₹ 18,00,000,

which will be subject to service tax.

Value of taxable Service = ₹ 18,00,000

Service tax payable = Rs. 18,00,000 X 12.36% = ₹ 2,22,480

Applicability of Service tax if A&Co. is located in Mumbai:

The liability would be same even if A&Co. were located in Mumbai, as service provided by

them in J&K will not be taxable. However, in that case, reverse charge will not apply.

Conclusion: Service tax payable by A&Co. in both the cases is ₹ 2,22,480

Answer to Question No. 14:

i. As per Section 64(1) of Finance Act 1994, Service Tax provisions do not extend to

the State of jammu & Kashmir. But in the present case Service Tax is provided in

the state of Rajasthan but not in the state of jammu & Kashmir. As per the point of

taxation rules, 2012 the location of the service recipient is relevant for taxability.

Accordingly Service tax is payable in the present case as services are provided in

taxable territory i.e. Rajasthan.

ii. When both Service provider and Service recipient are located in taxable territory,

the said service shall be taxable service and the value of taxable service shall be

Visit www.pinnacleacademy.co for CA & CMA classes 23

the gross amount charged for service as per Section 67 of Finance Act, 1994. In the

present case service tax shallbe payable at the prevailing rate of 12.36% on

₹1,00,000/-

iii. Services provided to EOU located in India is liable to Service Tax as Service provider

and service recipient are located in taxable territory i.e. India

iv. As per the general rule of place of provision of services rules, 2012 the location of

service recipient is relevant in determining the taxability of service. In the present

case as the actual service recipients is located outside the taxable territory, the said

services provided by Kirti Ltd is not taxable.

v. India includes the installations, structures and vessels located in the continental

shelf of India and exclusive economic zone of India. Since in the present case Nitin

Ltd provided services to IOC from vessels located in the continental shelf of India

for the purposes of prospecting natural gas , it implies that services have been

provided in taxable territory by one person to another for consideration. Therefore,

service tax is leviable in the present case.

Answer to Question No. 15:

i. In this case, since the immovable property in question is located in New Delhi,

place of provision of services will be New Delhi which falls within the ambit of

‗Taxable Territory‘ and resultantly these services will be taxable.

ii. In this case, place of provision of services will be Punjab as the concerned property

is intended to be located in Punjab which also falls within the ambit of ‗Taxable

Territory‘ and resultantly these services will be taxable.

iii. In this case, since specific sites in respect of which mineral exploration is to be

carried out are located in Canada, the place of Provision of service will be Canada

which does not fall within the ambit of ‗Taxable Territory‘ and resultantly these

services will not be taxable. The fact that service providing Company is located in

U.S.A and service recipient is located in U.S.A. and service recipient is located in

Mumbai (India) is wholly insignificant.

iv. In this case, place of provision of service shall be Gujarat because greatest

proportion of taxable service (60%) is provided there. The students may tempt to

draw conclusion here as all the locations given in this example fall within the

taxable territory, place of provision of services rules have no applicability. However,

students must keep in mind that POPS, rules, 2012 are useful for those service

providers who operate from multiple locations within India without having

centralized registration for the purpose of determining the precise taxable

jurisdiction applicable to their operations. Therefore, in the present case if it is

assumed that ABC Ltd has decentralized registration, it will pay applicable service

tax in respect of services provided to XYZ Ltd. In Gujarat.

v. Since in this case, consulting engineer‘s services provided by Rohit are in respect of

locations which fall within non-taxable territory, place of provision of the services

provided is U.K., USA and Dubai for the respective services and hence, no service

tax is chargeable by Mr. Rohit [Rule 5 of the PoPS Rules].

For CA & CMA classes, call @ 9940381858 24

CHAPTER - 2 VALUATION UNDER SERVICE TAX

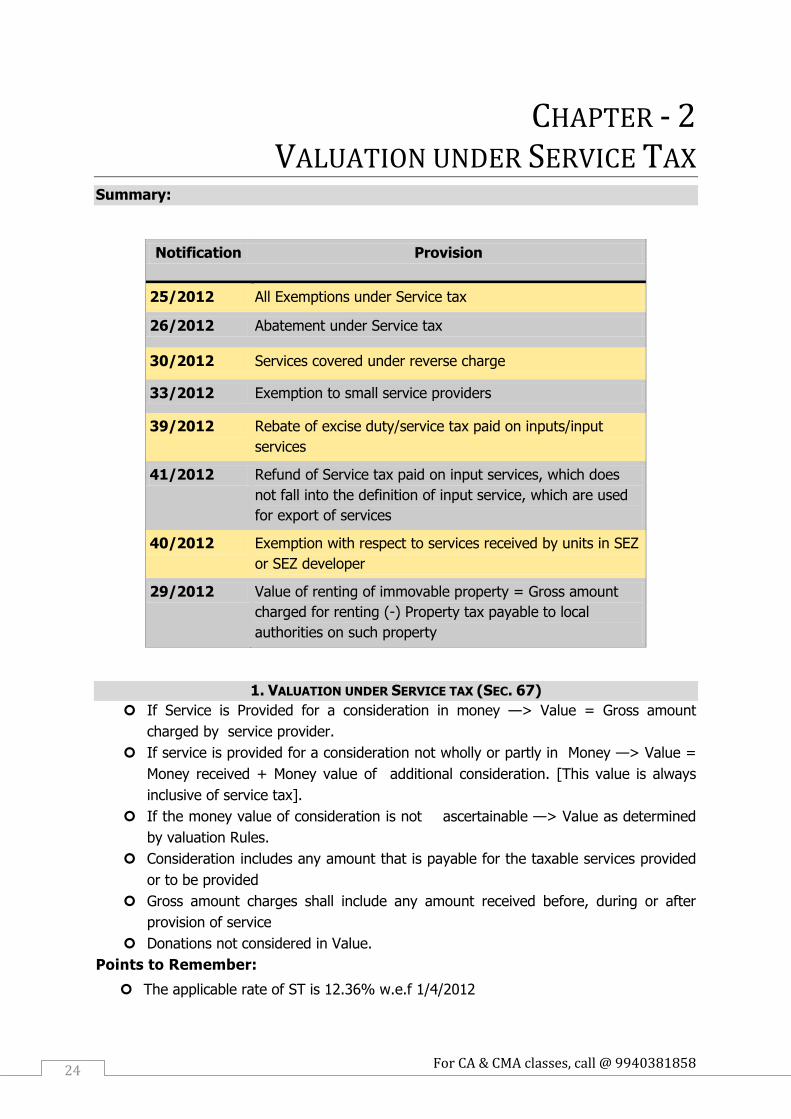

Summary:

Notification Provision

25/2012 All Exemptions under Service tax

26/2012 Abatement under Service tax

30/2012 Services covered under reverse charge

33/2012 Exemption to small service providers

39/2012 Rebate of excise duty/service tax paid on inputs/input

services

41/2012 Refund of Service tax paid on input services, which does

not fall into the definition of input service, which are used

for export of services

40/2012 Exemption with respect to services received by units in SEZ

or SEZ developer

29/2012 Value of renting of immovable property = Gross amount

charged for renting (-) Property tax payable to local

authorities on such property

1. VALUATION UNDER SERVICE TAX (SEC. 67)

If Service is Provided for a consideration in money —> Value = Gross amount

charged by service provider.

If service is provided for a consideration not wholly or partly in Money —> Value =

Money received + Money value of additional consideration. [This value is always

inclusive of service tax].

If the money value of consideration is not ascertainable —> Value as determined

by valuation Rules.

Consideration includes any amount that is payable for the taxable services provided

or to be provided

Gross amount charges shall include any amount received before, during or after

provision of service

Donations not considered in Value.

Points to Remember:

The applicable rate of ST is 12.36% w.e.f 1/4/2012

Visit www.pinnacleacademy.co for CA & CMA classes 25

If the POT is before 1/4/2012, apply ST as 10.3%

Unless otherwise specified, consider value as exclusive of tax. (Make a note in that regard)

Always comment on the availability of CENVAT credit.

2. Valuation Rules: (Service tax valuation rules, 2006)

Gross amount charged by service provider for providing SIMILAR service

Rule 3(a)

If above is not possible, EQUIVALENT money value, which should not be less then cost of provision of service.

Rule 3(b)

AO has power to deter- mine Value by issuing SCN Rule 4

Expenditure incurred in the course of providing service is INCLUDED in value.

Rule 5(1)

Expenditure incurred on behalf of SR as pure agent is EXCLUDED in value.

Rule 5(2)

3. VALUE OF FOREX TRANSACTIONS (INCL. MONEY CHANGING) - RULE 2B

The ―VALUE‖ as per Rule 2B is as follows:

1. When there is purchase or sale of INR and the RBI reference rate is available, Value = (Buying/Selling rate - RBI ref. rate) X Units of currency [Ignore +ve/-ve]

2. When there is purchase or sale of INR and the RBI reference rate is not available, Value = Gross amount of INR provided or received X 1%

3. When the currencies involved in the exchange transaction are foreign currencies, Value =

Note: On the value ascertained above , ST @ 12.36% is payable.

4. VALUE IN CASE OF RESTAURANT OR OUTDOOR CATERING - RULE 2C

The value of service portion is as follows:

Goods being food or any other article for human consumption Supplied in a restaurant —> Value = 40% of total amount charged

Goods being food or any other article for human consumption supplied as a part of outdoor catering —> Value = 60% of total amount charged

For CA & CMA classes, call @ 9940381858 26

CENVAT Credit Implications for above: No CENVAT credit on goods falling under chapter 1 to 22 of CETA (i.e food, edibles

or beverages incl. live animals) CENVAT credit available on other inputs, input services and capital goods subject to

the provision of CENVAT credit rules Bundled service of Catering with Renting: - Notification No. 26/2012) Taxable Value = 70% of total amount, without taking CENVAT credit on any goods used for providing service Computation of total amount charged for the purpose of Rule 2C as well as Notification no. 26/2012.:

Gross amount charged XXX

Add: FMV of all goods and services supplied by the service

receiver in or in relation to the supply of food or any

other article of human consumption or any drink

(whether or not intoxicating), under the same contract

or any other contract

XXX

Less: Amount charged for the goods or services provided by

the service receiver

(XX)

Less: VAT or Sales tax levied to the extent they form part of

the gross amount or the total amount, as the case may

be.

(XX)

Total amount charged for the purpose of Rule 2C or

Notification no. 26/2012

XXX

5. SERVICE TAX VS. TDS - IN CASE OF REVERSE CHARGE (MAINLY FOR NOV 2014 EXAMS)

In case of reverse charge the service recipient has to pay service tax and at the

same time has to deduct TDS on the payment made by him to service provider.

There was confusion till 2014 as to whether TDS should be calculated on the amount

including service tax as service tax is paid by the service recipient.

But CBDT vide its circular no. 1/2014 dated 6.1.2014 has clarified that while

computing TDS, service tax element should be excluded as service tax is not the

income part but is a statutory liability.

Service provider under reverse charge will raise invoice only on the service portion

excluding service tax and service recipient has to calculate service tax as well as

TDS on the same amount and pay to the respective authorities accordingly.

Even if service provider charges in his invoice only his part of service tax (in case of

partial reverse charge), TDS should be computed only that service value excluding

the part amount of service tax.

Service tax Vs. TDS

CBDT vide Cir. 1/2014 clarified that no TDS is required to be made on service tax

Visit www.pinnacleacademy.co for CA & CMA classes 27

component, if service tax is shown separately in invoice.

TVS Motor Co. Ltd. V CCE (2012) (CESTAT)

Service tax is payable on amount inclusive of income tax TDS

Example:

Professional services by Mr. A to Mr. B is ₹1,00,000.

Service tax payable @ 12.36% is ₹12,360

Invoice by Mr. A to Mr. B = ₹1,12,360

TDS @ 10% should be calculated on ₹1,00,000 but not ₹1,12,360

Payment made by Mr. B to Mr. A = ₹1,02,360

Service tax payable to Govt. is ₹ 12,360 but not on ₹ 1,02,360 (Reverse working should not be done)

6. VALUE OF TELECOMMUNICATION SERVICE

Amendment vide Notification No. 24/2012:

The value of telecommunication service shall be the gross amount paid by the person to whom telecommunication service is actually provided. Exemption vide Notification No. 25/2012: Services by a selling agent or a distributor of SIM cards or recharge coupon vouchers are exempted from service tax. Example: MRP of SIM card = ₹200 Payment by Dealer = ₹150 Value in the hands of telecom company = ₹200

7. VALUE IN CASE OF DIRECTORS’ SERVICES TO COMPANY:

Services of director to company is covered under the provisions of reverse charge by

amending noti. 30/2012 w.e.f 7/8/2012 and remuneration to directors is as follows:

Service Provider - Director (Service Tax liability= 0%)

Service Recipient - Company (Service Tax liability = 100%)

Director INCLUDES Non-executive, Nominee, Public interest and Independent

directors

Director DOES NOT INCLUDE Managing Director, Whole time director and Executive

director, who are in full time employment of the company (Therefore no service tax

as it is contract of service).

Remuneration INCLUDES sitting fees, travelling expenses and incidental expenses for

attending the meetings of Board and their committees and commission or other

remuneration paid.

Remuneration DOES NOT INCLUDE travelling expenses other than for board

meetings and committee meetings.

Service tax should be paid @12.36% on gross value of services and not by back

calculations.

Service tax should be computed on the amount of remuneration and TDS should be

calculated on the same amount but not after including service tax.

For CA & CMA classes, call @ 9940381858 28

8. PRINCIPLE OF MUTUALITY - MEANING, EXCEPTIONS & EXEMPTIONS:

Meaning:

As per this principle, there must be two parties for levy of service tax i.e. service must be provided by one person to another person. Exceptions [Explanation 3 to Sec. 65B(44)]:

1. An establishment of a person located in taxable territory and another establishment of such person located in non-taxable territory are treated as establishments of distinct persons.

2. An unincorporated association or body of persons and members thereof are also treated as distinct persons.

Exemptions [Notification no. 25/2012]: Service by an registered, unincorporated body or a non- profit entity, to its own members by way of reimbursement of charges or share of contribution–

1. As a trade union; 2. For the provision of carrying out any activity which is exempt from the levy of service

tax; or 3. Up to an amount of ₹5,000 per month per member for sourcing of goods or services

from a third person for the common use of its members in a housing society or a residential complex [i.e. Resident Welfare Association (RWA)]

Circular No. 175/1/2014 (dated: 10/1/14) If per month, per member contribution exceeds ₹ 5,000, the entire contribution

would be ineligible for contribution and service tax would be leviable. Small Service Provider exemption under Notification no. 33/2012 is applicable to

RWA. RWA incurring expenses viz. electricity bill, telephone bill on behalf of members is

excluded as per rule 5(1) of valuation Rules, 2006 for determining the value of taxable services of RWA

RWA can avail CENVAT credit in terms of CENVAT credit rules, 2004

9. COMPOSITION SCHEME:

Air Travel agent - Rule 6(7):

@ 0.6% of the basic fare in the case of domestic bookings, and @ 1.2% of the basic fare in the case of international bookings, during any calendar month or quarter, as the case may be. Life Insurance - Rule 6(7A): Insurer has option to pay service tax on life insurance business on following basis:

If the amount allocated for investment to savings, is intimated to policy holder, at the time of providing service Gross premium charged (-) Amount allocated for investment

Other cases For the first year of the policy —> Service tax @ 3% of the gross amount of premium charged. For the subsequent year of the policy —> Service tax @ 1.5% of the gross amount of premium charged.

Visit www.pinnacleacademy.co for CA & CMA classes 29

Distributor/Agent of lotteries - Rule 6(7C):

Where the guaranteed lottery prize payout is > 80% —> ₹ 7000/- on every ₹ 10 Lakhs (or part of ₹ 10 Lakhs) of aggregate face value of lottery tickets printed by the organizing State for a draw.

Where the guaranteed lottery prize payout is < 80% —> ₹ 11000/- on every ₹ 10 Lakhs (or part of ₹ 10 Lakhs) of aggregate face value of lottery tickets printed by the organizing State for a draw.

Sale/Purchase of foreign currency including money changing - Rule 6(7B): Upto ₹ 100,000:

0.12 % of the gross amount of currency exchanged (or) ₹ 30 whichever is higher

Exceeding ₹ 1,00,000 and upto ₹ 10,00,000:

₹ 120 + 0.06 % of the gross amount of currency exchanged (Exceeding ₹ 1,00,000)

Exceeding ₹ 10,00,000:

₹ 660 + 0.012 % of the gross amount of currency exchanged (Exceeding ₹ 10,00,000) (or) ₹ 6,000 whichever is lower.

COMPOSITION SCHEME - SPECIAL POINTS

All the above are ser- vice tax payable but not ―value‖.

The above is excluding EC & SHEC.

It is an optional scheme. If SP want to pay ST as per normal provisions, he can do so

The option should be availed in the beginning of every financial year in writing to AC/DC.

The option once availed will be applicable for entire financial year in respect of all trans- actions. In case of lotteries, it can be availed within one month.

If this option is availed, the SP comes under the category of ―Exempted services‖ for CENVAT credit purpose and accordingly, credit not available.

―In Normal scheme, there involves computation of Value & ST but in Composition scheme, only computation of ST‖

For CA & CMA classes, call @ 9940381858 30

In terms of practice followed, life insurance companies’ issues remainder notices/letters to policy holders to pay renewal premiums. Such reminders notices only solicit furtherance of service which if accepted by policy holder by payment of premium results in a service. Whether service tax needs to be paid on the basis of such reminders? CBEC vide circular no. 166/1/2013 dated 1.1.2013 clarified as follows: Under the point of taxation rules, 2011 the point of taxation generally is the date of issue of invoice or date of receipt of payment whichever is earlier. The invoice mentioned refers to the invoices as issued under Rule 4A of Service tax Rules, 1994. No tax point arises on account of such reminders. Thus, it is clarified that reminder letters/notices for insurance policies not being invoices would not invite levy of service tax. In case of issuance of any invoice, point of taxation shall accordingly be determined. Comments: In my opinion this circular can be applied in many cases and thus tax can be saved to a larger extent. When it is uncertain that service recipient will not pay services charges, it is not advisable to raise invoice, as raising invoice attracts payment of service tax and if the service recipient does not pay service charges then a credit note should be issued and refund be claimed. There is no concession for bad debts as per the departments circular. Therefore, as per this circular, a service provider can either raise a proforma invoice or remainder in case of continuous supply of service and on receipt of payment the service tax shall be paid and an invoice as per Rule 4A shall be issued within 30 days or 45 days once the payment is received.

Visit www.pinnacleacademy.co for CA & CMA classes 31

CHAPTER - 3 SERVICE TAX – PROCEDURES Departments Forte:

OFFENCES WHICH ATTRACTS IMPRISONMENT – SEC. 89

Penal provisions

under Service tax

Interest

Penalty

Offences

Arrest

Offences punishable under sec. 89

Category – A offence

(a) Willful evasion of payment of service tax

(b) Availment and utilization of credit of service tax/excise duty without actual receipt of taxable

service/excisable goods

(c) Maintenance of false books of accounts/ failure to supply an information /Supplying false

information

Category – B offence

Non payment of amount collected as service tax

for a period of more than 6 months from the

due date of payment

For CA & CMA classes, call @ 9940381858 32

COGNIZANCE OF OFFENCES – SEC. 90

Offences punishable under sec. 89

Category – A Offence

First time

Amount involved in the offence ≤50

lakhs

Imprisonment upto 1 year

Amount involved in the offence >50

lakhs

Imprisonment for 6 months

– 3 years

Second & every subsequent offence

Term of imprisonment may extend to

3 years

Category – B Offence

First time

Amount involved in the offence ≤50

lakhs

Imprisonment upto 1 year

Amount involved in the offence >50

lakhs

Imprisonment for 6 months

– 7 years

Second & every subsequent offence

Amount involved in the offence ≤50 lakhs

Upto 3 years

Amount involved in the offence >50 lakhs

Upto 7 years

Offences

Cognizable offence

It is a criminal offence in which the police is empowered to register an FIR, investigate and

arrest an accused without a court issued warrant

These offences are usually serious in nature

Bailable Offence Non-bailable offence

Non-Cognizable offence

It is an offence in which police can neither register an FIR, investigate nor effect arrest without the express permission or directions

from the court

Not much serious as cognizable offence

Always bailableoffence

Visit www.pinnacleacademy.co for CA & CMA classes 33

Offences which attracts imprisonment – Sec. 89 vis-à-vis Cognizance of offence –

Sec. 90

Sec. 90 provides that offence involving collection of any amount as service tax but failure to

pay the amount so collected to the credit of the central government beyond a period of six

months would be cognizable offence if the amount exceeds ₹ 50 lakhs. Therefore arrest can

be made for such an offence without a warrant

All other offences would be non-cognizable and bailable

POWERS OF ARREST [SEC. 91]

(i) Who can arrest? - New section 91 provides that the Commissioner of Central

Excise by general or special order authorize any officer of Central Excise, not

below the rank of Superintendent of Central Excise to arrest a person.

(ii) Who can be arrested? - A person who has committed any of the offences

specified under section 89(1) and the amount involved in the offence exceeds

`50 lakh.

Offences punishable under sec. 89

Category – A Offence

First time

Amount involved in the offence ≤50

lakhs

Imprisonment upto 1 year

Amount involved in the offence >50

lakhs

Imprisonment for 6 months –

3 years

Second & every subsequent offence

Term of imprisonment may extend to

3 years

Category – B Offence

First time

Amount involved in the offence ≤50

lakhs

Imprisonment upto 1 year

Second & every subsequent offence

Amount involved in the offence ≤50 lakhs

Upto 3 years

Cognizable offence

For CA & CMA classes, call @ 9940381858 34

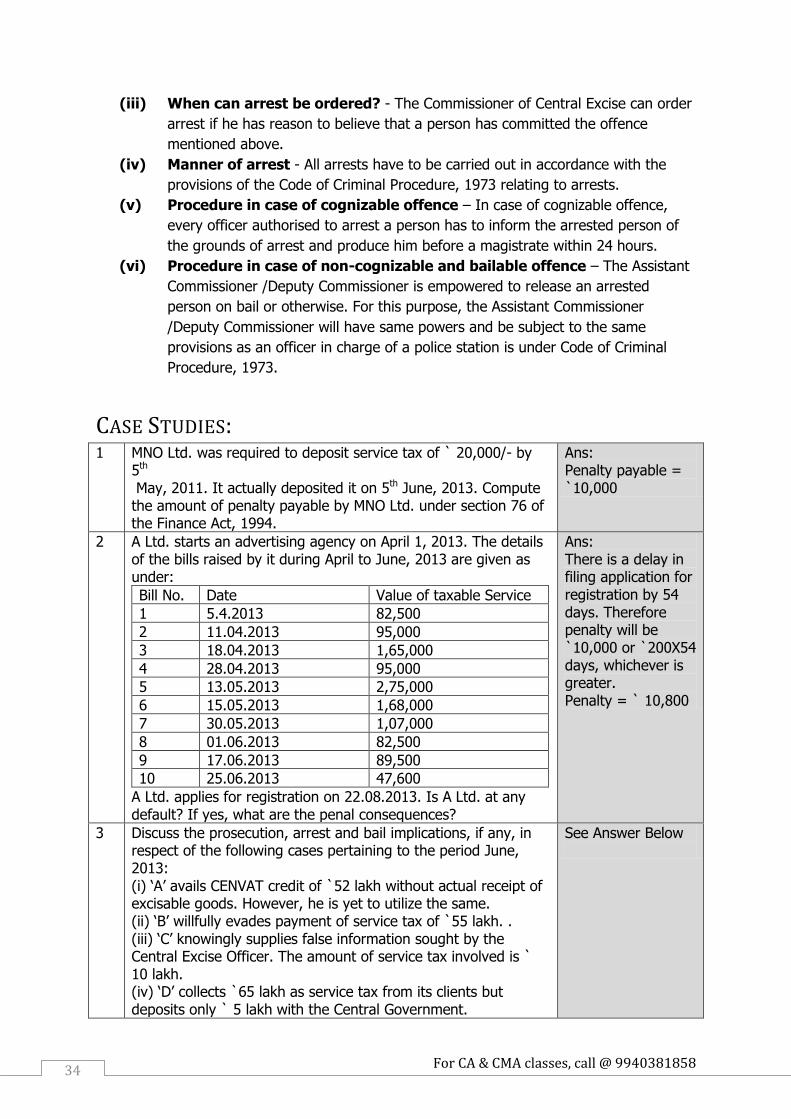

(iii) When can arrest be ordered? - The Commissioner of Central Excise can order

arrest if he has reason to believe that a person has committed the offence

mentioned above.

(iv) Manner of arrest - All arrests have to be carried out in accordance with the

provisions of the Code of Criminal Procedure, 1973 relating to arrests.

(v) Procedure in case of cognizable offence – In case of cognizable offence,

every officer authorised to arrest a person has to inform the arrested person of

the grounds of arrest and produce him before a magistrate within 24 hours.

(vi) Procedure in case of non-cognizable and bailable offence – The Assistant

Commissioner /Deputy Commissioner is empowered to release an arrested

person on bail or otherwise. For this purpose, the Assistant Commissioner

/Deputy Commissioner will have same powers and be subject to the same

provisions as an officer in charge of a police station is under Code of Criminal

Procedure, 1973.

CASE STUDIES: 1 MNO Ltd. was required to deposit service tax of ` 20,000/- by

5th May, 2011. It actually deposited it on 5th June, 2013. Compute the amount of penalty payable by MNO Ltd. under section 76 of the Finance Act, 1994.

Ans: Penalty payable = `10,000

2 A Ltd. starts an advertising agency on April 1, 2013. The details of the bills raised by it during April to June, 2013 are given as under:

Bill No. Date Value of taxable Service

1 5.4.2013 82,500

2 11.04.2013 95,000

3 18.04.2013 1,65,000

4 28.04.2013 95,000

5 13.05.2013 2,75,000

6 15.05.2013 1,68,000

7 30.05.2013 1,07,000

8 01.06.2013 82,500

9 17.06.2013 89,500

10 25.06.2013 47,600

A Ltd. applies for registration on 22.08.2013. Is A Ltd. at any default? If yes, what are the penal consequences?

Ans: There is a delay in filing application for registration by 54 days. Therefore penalty will be `10,000 or `200X54 days, whichever is greater. Penalty = ` 10,800

3 Discuss the prosecution, arrest and bail implications, if any, in respect of the following cases pertaining to the period June, 2013: (i) ‗A‘ avails CENVAT credit of `52 lakh without actual receipt of excisable goods. However, he is yet to utilize the same. (ii) ‗B‘ willfully evades payment of service tax of `55 lakh. . (iii) ‗C‘ knowingly supplies false information sought by the Central Excise Officer. The amount of service tax involved is ` 10 lakh. (iv) ‗D‘ collects `65 lakh as service tax from its clients but deposits only ` 5 lakh with the Central Government.

See Answer Below

Visit www.pinnacleacademy.co for CA & CMA classes 35

(v) ‗E‘ collects ` 55 lakh as service tax from its clients and deposits ` 51 lakh with the Central Government.

Answer to Question No. 3:

Person Offence Prosecution Arrest Bail

A No offence as both availment and utilization of credit without actual receipt of excisable goods constitutes an offence

N.A N.A N.A

B Non cognizable offence

6 months to 3 years

Arrest can be ordered by commissioner of central excise

Bailable offence

C Non cognizable offence

Upto 1 year No Arrest Bailable offence

D Cognizable offence 6 months to 7 years

Arrest can be ordered by commissioner of central excise without arrest warrant

Non bailable/ bailable offence

E Non cognizable offence

Upto 1 year No arrest Bailable offence

For CA & CMA classes, call @ 9940381858 36

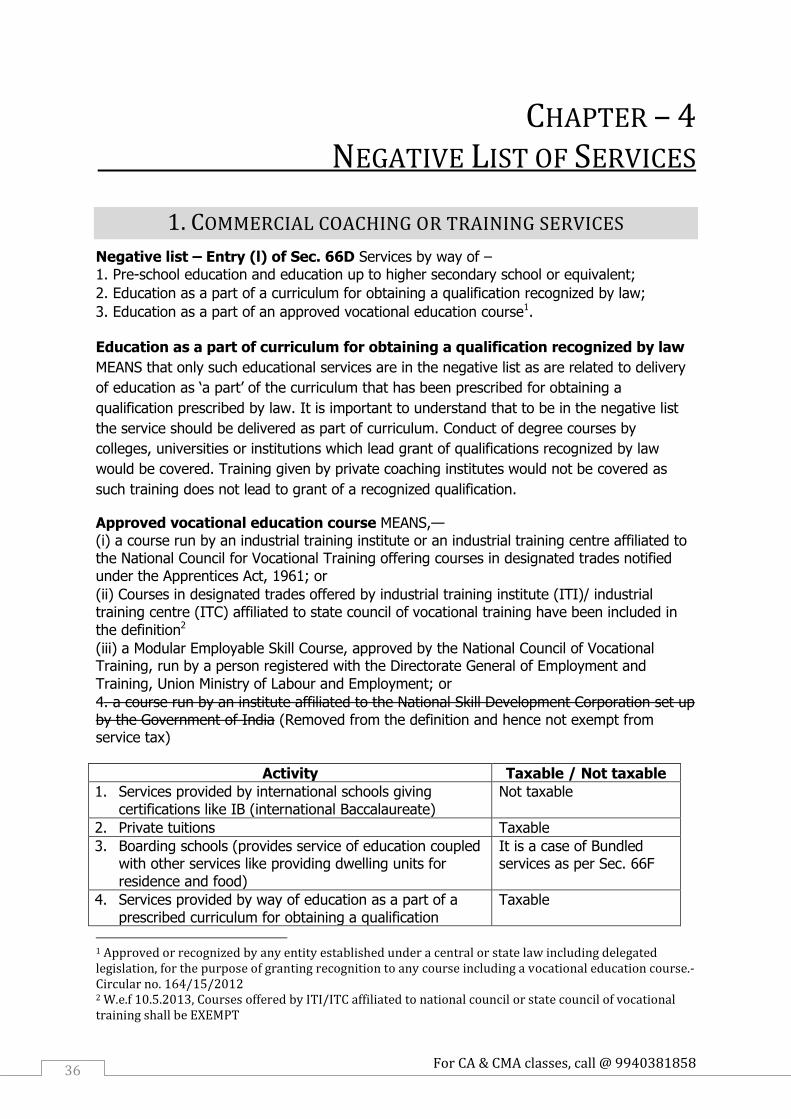

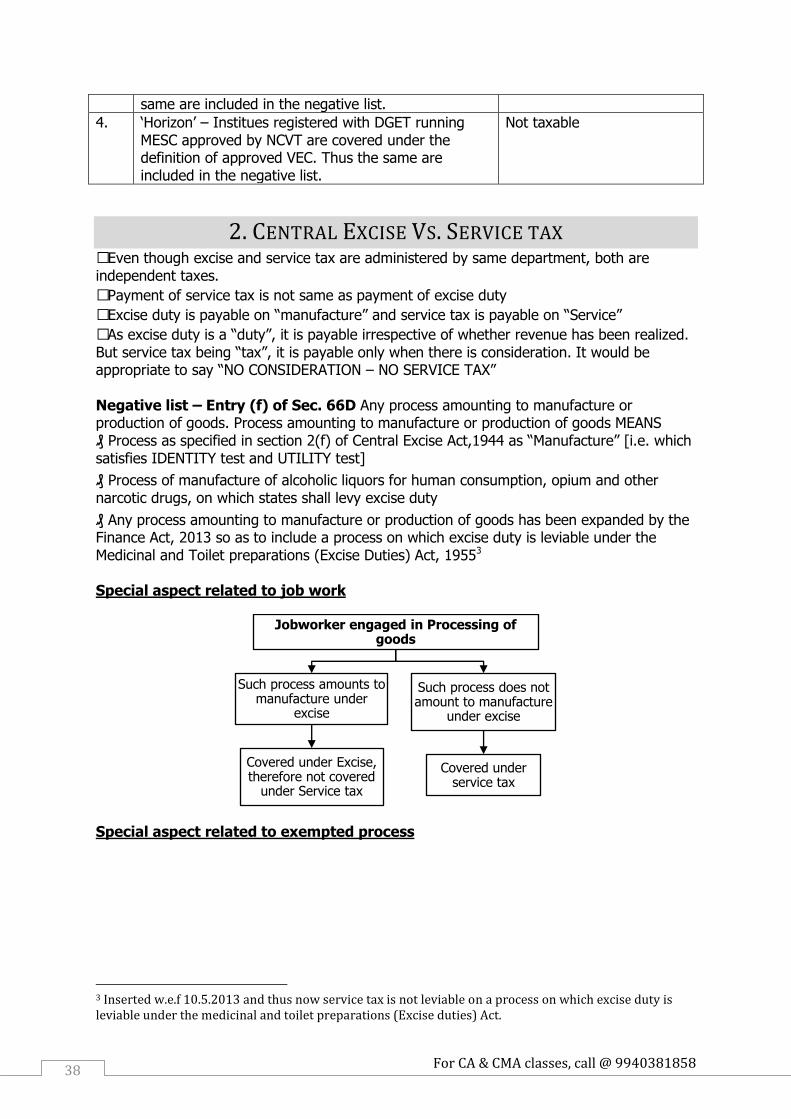

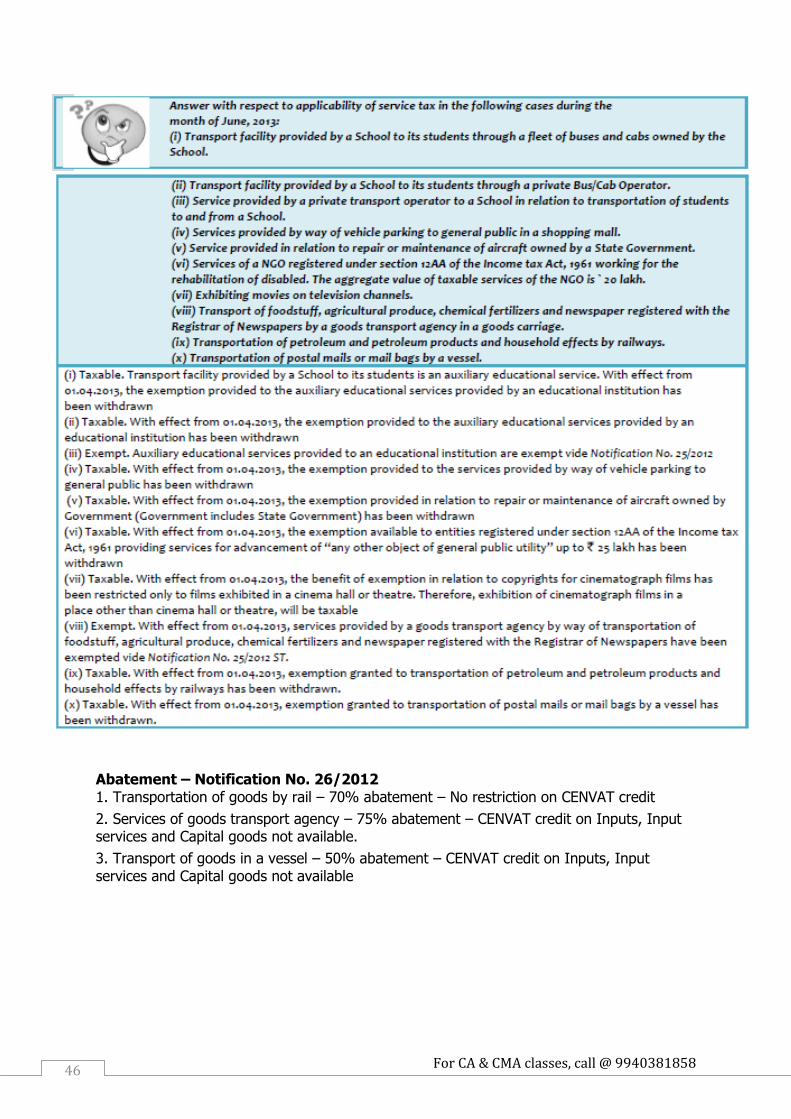

CHAPTER – 4 NEGATIVE LIST OF SERVICES

1. COMMERCIAL COACHING OR TRAINING SERVICES

Negative list – Entry (l) of Sec. 66D Services by way of – 1. Pre-school education and education up to higher secondary school or equivalent;

2. Education as a part of a curriculum for obtaining a qualification recognized by law;

3. Education as a part of an approved vocational education course1. Education as a part of curriculum for obtaining a qualification recognized by law

MEANS that only such educational services are in the negative list as are related to delivery

of education as ‗a part‘ of the curriculum that has been prescribed for obtaining a

qualification prescribed by law. It is important to understand that to be in the negative list

the service should be delivered as part of curriculum. Conduct of degree courses by

colleges, universities or institutions which lead grant of qualifications recognized by law

would be covered. Training given by private coaching institutes would not be covered as

such training does not lead to grant of a recognized qualification.

Approved vocational education course MEANS,— (i) a course run by an industrial training institute or an industrial training centre affiliated to the National Council for Vocational Training offering courses in designated trades notified under the Apprentices Act, 1961; or

(ii) Courses in designated trades offered by industrial training institute (ITI)/ industrial training centre (ITC) affiliated to state council of vocational training have been included in

the definition2

(iii) a Modular Employable Skill Course, approved by the National Council of Vocational Training, run by a person registered with the Directorate General of Employment and

Training, Union Ministry of Labour and Employment; or

4. a course run by an institute affiliated to the National Skill Development Corporation set up by the Government of India (Removed from the definition and hence not exempt from service tax)

Activity Taxable / Not taxable

1. Services provided by international schools giving certifications like IB (international Baccalaureate)

Not taxable

2. Private tuitions Taxable

3. Boarding schools (provides service of education coupled with other services like providing dwelling units for residence and food)

It is a case of Bundled services as per Sec. 66F

4. Services provided by way of education as a part of a prescribed curriculum for obtaining a qualification

Taxable