Ramirent results q3_2014_en_final

70

© 2014 Ramirent Q3 Interim Report January–September 2014 RESTRUCTURING MEASURES BEARING FRUIT, MIXED MARKET PICTURE REMAINS 6 November 2014 Magnus Rosén, President and CEO Jonas Söderkvist, CFO and EVP Corporate Functions

-

Upload

annika-berg -

Category

Investor Relations

-

view

29 -

download

0

Transcript of Ramirent results q3_2014_en_final

© 2014 Ramirent

Q3 Interim Report January–September 2014

RESTRUCTURING MEASURES BEARING FRUIT, MIXED MARKET PICTURE REMAINS 6 November 2014 Magnus Rosén, President and CEO Jonas Söderkvist, CFO and EVP Corporate Functions

© 2014 Ramirent © 2014 Ramirent

Agenda

2

Group performance

Segment review

Market outlook

Key figures

Financial position

Company overview

Appendix

© 2014 Ramirent 3

Restructuring measures bearing fruit, mixed market picture remains

Key figures Q3/2014

Business performance

Market situation

The market picture remained mixed and we saw no major changes in the market environment during the third quarter

Net sales down by 1.6%; adjusted for divested operations, net sales were

up by 1.9% at comparable exchange rates

EBITA MEUR 28.0 (25.9) or 17.1% (15.6%) of net sales

EBITA excl. non-recurring items and divested operations1) MEUR 29.9

(28.7) or 18.3% (17.5%) of net sales

Gross capex MEUR 23.8 (29.5)

Third-quarter net sales were supported by improving demand in the Swedish market as several projects started

A number of actions were carried out to adjust the cost base in low-performing segments

Interim Report January–September 2014 l 6 November 2014

1) Restructuring provision of EUR 1.9 million in Norway was booked in the third quarter of 2014. In the comparison period, non-recurring items included a EUR 1.5 million restructuring provision in Denmark, a EUR 1.9 million loss from disposal of Hungary and EUR 0.6 million EBITA result from Hungary.

© 2014 Ramirent 4

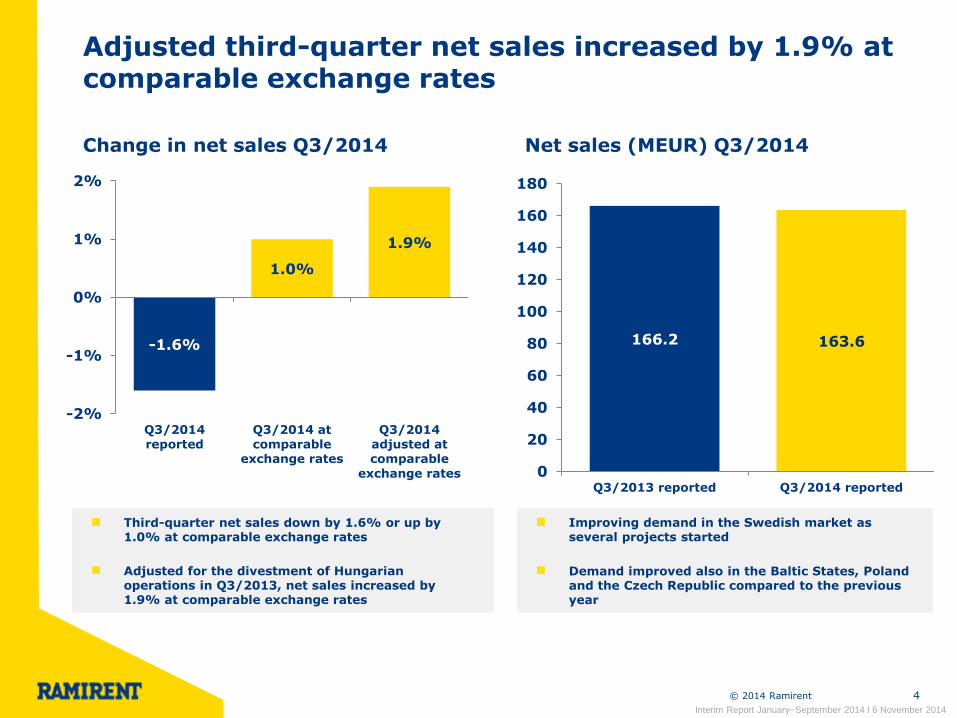

Adjusted third-quarter net sales increased by 1.9% at comparable exchange rates

Change in net sales Q3/2014

-1.6%

1.0%

1.9%

-2%

-1%

0%

1%

2%

Q3/2014reported

Q3/2014 atcomparable

exchange rates

Q3/2014adjusted atcomparable

exchange rates

Net sales (MEUR) Q3/2014

Third-quarter net sales down by 1.6% or up by 1.0% at comparable exchange rates

Adjusted for the divestment of Hungarian operations in Q3/2013, net sales increased by 1.9% at comparable exchange rates

166.2 163.6

0

20

40

60

80

100

120

140

160

180

Q3/2013 reported Q3/2014 reported

Improving demand in the Swedish market as several projects started

Demand improved also in the Baltic States, Poland and the Czech Republic compared to the previous year

Interim Report January–September 2014 l 6 November 2014

© 2014 Ramirent 5

Reported and adjusted EBITA margin improved compared to the previous year

15.6% 17.5% 17.1%

18.3%

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

Q3/2013reported

Q3/2013 excl.non-recurring

items

Q3/2014reported

Q3/2014 excl.non-recurring

items

Restructuring provision of EUR 1.9 million in

Norway was booked

Q3/2014 EBITA margin excl. non-recurring

items and divested operations 18.3% (17.5%1))

EBITA margin Q3/2014 EBITA (MEUR) Q3/2014

25.9 28.7 28.0

29.9

0

5

10

15

20

25

30

35

Q3/2013reported

Q3/2013 excl.non-recurring

items

Q3/2014reported

Q3/2014 excl.non-recurring

items

Q3/2014 reported EBITA MEUR 28.0 (25.9)

Q3/2014 EBITA excl. non-recurring items and

divested operations MEUR 29.9 (28.71))

Interim Report January–September 2014 l 6 November 2014

1) Non-recurring items in the third quarter of 2013 included the EUR 1.5 million restructuring provision in Denmark, the EUR 1.9 million loss from disposal of Hungary and the EUR 0.6 million EBITA result from Hungary.

© 2014 Ramirent 6

Third-quarter EPS increased slightly from the comparison period

Earnings Per Share (EPS)

-0.05

0.04

0.08

0.07

0.00

0.08

0.17

0.16

0.07

0.14

0.19

0.18

0.10

0.11

0.16

0.13

0.02

0.07

0.17

-0.06

-0.04

-0.02

0.00

0.02

0.04

0.06

0.08

0.10

0.12

0.14

0.16

0.18

0.20

0.22

Q12010

Q2 Q3 Q4 Q12011

Q2 Q3 Q4 Q12012

Q2 Q3 Q4 Q12013

Q2 Q3 Q4 Q12014

Q2 Q3

Interim Report January–September 2014 l 6 November 2014

0.50 0.59 0.41 0.10 0.26

(0.37)

© 2014 Ramirent 7

Ramirent has signed three cooperation agreements with large construction companies

Interim Report January–September 2014 l 6 November 2014

Skanska's internal machinery department, Skanska Maskin AB, signed a three-year equipment rental agreement with Ramirent in Sweden

The agreement covers the whole assortment of both companies, from light and heavy machinery to modules and cranes

Veidekke renewed its cooperating agreement and signed a nationwide three-year equipment rental agreement with Ramirent in Norway

The agreement covers the whole assortment of machines and services from Ramirent

Hartela Oy outsourced its fleet of tower cranes to Ramirent in Finland and signed a five-year co-operation agreement covering the whole assortment of machines and services from Ramirent

According to the agreement, three employees will

move to Ramirent

After the end of the review period

© 2014 Ramirent 8

Our efficiency programme is progressing according to plan

Sales and pricing

Other

Sourcing

Fleet management

• Developing logistics and maintenance & repair processes

• Optimisation of fleet life-cycle

• Developing support processes and systems

• Optimisation of sourcing terms and supplier portfolio

• Common system platform and performance management model

• Developing efficient back-office functions

Target at the end of 2016: The identified efficiency actions are planned to deliver a Group EBITA margin of 17%

Interim Report January–September 2014 l 6 November 2014

Main areas of improvement

• Developing the network and customer care model

• Revenue management • Promoting services and

integrated solutions

• New organisational model for Customer Centre Sales and Solutions Sales introduced in Sweden, Denmark, and Norway

Actions implemented in 1-9/2014

• Concentration of repair & maintenance operations to few locations in the Nordic countries

• Outsourced yard & storage operations in Finland

• Compliance increased in usage of approved suppliers in all countries

• Increase in number of Groupwide supplier agreements

• New rental system live in Sweden, Denmark and, Norway

• Integration of back-office functions in Sweden and Denmark

• Personnel reductions due to restructuring

© 2014 Ramirent © 2014 Ramirent 9

Group performance

Segment review

Market outlook

Key figures

Financial position

Company overview

Appendix

© 2014 Ramirent 10

Finland Q3/2014: Net sales increased due to acquisitions and active sales management

• Net debt to EBITDA 1.1x in Q4

• Long-term financial target: below 1.6x

(at the end of FY)

24.9% 24.5%

19.0%

0%

5%

10%

15%

20%

25%

30%

Q12012

Q2 Q3 Q4 Q12013

Q2 Q3 Q4 Q12014

Q2 Q3

Net sales (MEUR) Highlights Q3/2014

45.0 41.8 43.5

05

101520253035404550

Q12012

Q2 Q3 Q4 Q12013

Q2 Q3 Q4 Q12014

Q2 Q3

EBITA margin Key figures

Demand remained at a good level in region South and Central

EBITA was burdened by the challenging pricing environment

Finland Q3

2014 Q3

2013 Change 2013

Net sales, MEUR 43.5 41.8 4.0% 151.9

EBITA, MEUR 8.3 10.2 −19.3% 25.7

% of net sales 19.0% 24.5% 16.9%

Capital expenditure, MEUR

4.9 7.4 −33.5% 28.8

Personnel (FTE) 538 531 1.4% 547

Customer centres 67 74 −9.5% 74

Net sales up by 4.0%

Interim Report January–September 2014 l 6 November 2014

© 2014 Ramirent 11

Sweden Q3/2014: Improving demand in the Swedish market as several projects started

• Net debt to EBITDA 1.1x in Q4

• Long-term financial target: below 1.6x

(at the end of FY)

18.0%

16.8% 17.2%

0%

5%

10%

15%

20%

25%

Q12012

Q2 Q3 Q4 Q12013

Q2 Q3 Q4 Q12014

Q2 Q3

Net sales (MEUR) Highlights Q3/2014

53.0 51.1 52.0

0

10

20

30

40

50

60

70

Q12012

Q2 Q3 Q4 Q12013

Q2 Q3 Q4 Q12014

Q2 Q3

EBITA margin Key figures

The demand for equipment rental in large construction projects started to improve and increased ancillary income

Ramirent carried out actions to reduce its fixed cost base during the quarter

Net sales up by 1.7% or by 7.7% at

comparable exchange rates

Sweden Q3

2014 Q3

2013 Change 2013

Net sales, MEUR 52.0 51.1 1.7% 207.3

EBITA, MEUR 8.9 8.6 4.1% 36.6

% of net sales 17.2% 16.8% 17.6%

Capital expenditure, MEUR

10.3 7.6 34.1% 35.8

Personnel (FTE) 771 644 19.8% 656

Customer centres 75 75 − 74

Interim Report January–September 2014 l 6 November 2014

© 2014 Ramirent 12

Norway Q3/2014: Focus on cost reductions to adjust to prevailing market conditions

• Net debt to EBITDA 1.1x in Q4

• Long-term financial target: below 1.6x

(at the end of FY)

17.0% 17.6%

11.8%

0%

5%

10%

15%

20%

25%

Q12012

Q2 Q3 Q4 Q12013

Q2 Q3 Q4 Q12014

Q2 Q3

Net sales (MEUR) Highlights Q3/2014

41.1 35.9 34.0

0

10

20

30

40

50

60

Q12012

Q2 Q3 Q4 Q12013

Q2 Q3 Q4 Q12014

Q2 Q3

EBITA margin Key figures

Net sales were affected by lower demand from residential construction especially in the capial city area

Actions to adjust the cost base continued and a restructuring provision of EUR 1.9 million was booked in the quarter

Net sales down by 5.3% or by 1.6% at

comparable exchange rates

Norway Q3

2014 Q3

2013 Change 2013

Net sales, MEUR 34.0 35.9 −5.3% 153.6

EBITA, MEUR 4.01) 6.3 −36.2% 22.0

% of net sales 11.8%1) 17.6% 14.3%

Capital expenditure, MEUR

3.8 8.4 −55.3% 34.5

Personnel (FTE) 410 470 −12.8% 460

Customer centres 43 43 - 43

Interim Report January–September 2014 l 6 November 2014

1) EBITA excluding non–recurring items was EUR 5.9 million, representing 17.3% of net sales. Non–recurring items included the EUR 1.9 million restructuring provision booked in the third quarter of 2014.

© 2014 Ramirent

Denmark Q3

2014 Q3

2013 Change 2013

Net sales, MEUR 10.1 11.9 −15.0% 44.0

EBITA, MEUR −0.1 −2.01) 94.0% −4.31)

% of net sales −1.2% −17.3%1) −9.7%1)

Capital expenditure, MEUR

1.5 1.3 17.6% 6.6

Personnel (FTE) 151 192 −21.3% 175

Customer centres 16 16 − 16

13

Denmark Q3/2014: Performance is improving

• Net debt to EBITDA 1.1x in Q4

• Long-term financial target: below 1.6x

(at the end of FY)

7.3%

-17.3%

-1.2%

-25%

-20%

-15%

-10%

-5%

0%

5%

10%

Q12012

Q2 Q3 Q4 Q12013

Q2 Q3 Q4 Q12014

Q2 Q3

Net sales (MEUR) Highlights Q3/2014

11.4 11.9

10.1

0

2

4

6

8

10

12

14

Q12012

Q2 Q3 Q4 Q12013

Q2 Q3 Q4 Q12014

Q2 Q3

EBITA margin Key figures

Net sales were disrupted due to restructuring measures being implemented to restore profitability

Performance is improving but was still burdened by low rental income

Integration of back-office functions to realise synergies with Sweden continued

Net sales down by 15.0% or by 15.1% at comparable exchange

rates

1) EBITA excluding non–recurring items was EUR –0.6 million or –4.7% of net sales in July–September 2013 and EUR –2.8 million or –6.3% of net sales in January–December 2013. Non–recurring items included the EUR 1.5 million restructuring provision in the third quarter of 2013. Interim Report January–September 2014 l 6 November 2014

© 2014 Ramirent 14

Europe East Q3/2014: Growth driven by demand from construction and energy sectors

• Net debt to EBITDA 1.1x in Q4

• Long-term financial target: below 1.6x

(at the end of FY)

Net sales (MEUR) Highlights Q3/2014

18.8

9.8 10.3

02468

101214161820

Q12012

Q2 Q3 Q4 Q12013

Q2 Q3 Q4 Q12014

Q2 Q3

EBITA margin Key figures

Net sales up by 4.9%

1) EBITA excluding non–recurring items and EBITA from Russia and Ukraine was EUR 6.0 million, representing 19.3% of net sales. Non–recurring items included the non–taxable capital gain of EUR 10.1 million from the formation of Fortrent Group, recorded in the first quarter of 2013 and EBITA from Russia and Ukraine. 2) EBITA margin excluding Fortrent transaction was 9.1% in the first quarter of 2013.

113.5%2)

Europe East Q3

2014 Q3

2013 Change 2013

Net sales, MEUR 10.3 9.8 4.9% 35.5

EBITA, MEUR 3.7 3.5 5.4% 17.31)

% of net sales 35.8% 35.6% 48.8%1)

Capital expenditure, MEUR

1.3 2.5 −47.9% 9.6

Personnel (FTE) 241 240 0.4% 235

Customer centres 42 41 2.4% 41

The Baltic States

23.5%

35.6% 35.8%

30.4% 31.3%

-5%

0%

5%

10%

15%

20%

25%

30%

35%

40%

Q12012

Q2 Q3 Q4 Q12013

Q2 Q3 Q4 Q12014

Q2 Q3

Interim Report January–September 2014 l 6 November 2014

Net sales increased in all Baltic countries compared to the last year

Profitability strengthened as a result of increased rental income and higher fleet utilisation

High uncertainty continued in Fortrent's markets

© 2014 Ramirent 15

Europe Central Q3/2014: Stable demand in Poland, the Czech Republic recovering

• Net debt to EBITDA 1.1x in Q4

• Long-term financial target: below 1.6x

(at the end of FY)

3.2%

7.0% 11.3%

-25%

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

Q12012

Q2 Q3 Q4 Q12013

Q2 Q3 Q4 Q12014

Q2 Q3

Net sales (MEUR) Highlights Q3/2014

17.9 16.9

14.2

02468

101214161820

Q12012

Q2 Q3 Q4 Q12013

Q2 Q3 Q4 Q12014

Q2 Q3

EBITA margin Key figures

Net sales decreased by 15.6% at comparable

exchange rates; adjusted for divested operations net sales decreased by 7.0%

1) Adjusted for the divestment of the Hungarian operations in the third quarter 2013 the decrease in net sales was 7.0%. 2) EBITA excluding non–recurring items was EUR 2.5 million or 16.2% of net sales July–September 2013 and EUR 0.7 million or 1.2% of net sales in January–December 2013. The non-recurring items included the EUR 1.9 million loss from disposal of operations in Hungary, recorded in the third quarter 2013 and EBITA from Hungary.

Europe Central Q3

2014 Q3

2013 Change 2013

Net sales, MEUR 14.2 16.9 −15.6%1) 57.3

EBITA, MEUR 1.6 1.22) 36.4% −0.72)

% of net sales 11.3% 7.0%2) −1.2%2)

Capital expenditure, MEUR

1.1 2.5 −55.9% 7.1

Personnel (FTE) 473 489 −3.3% 479

Customer centres 59 57 3.5% 56

Interim Report January–September 2014 l 6 November 2014

In Poland, net sales were affected by some large projects ending but overall there was stable demand both in the construction and industrial sectors

Demand for rental equipment started to recover in the Czech Republic

© 2014 Ramirent © 2014 Ramirent

Group performance

Segment review

Market outlook

Key figures

Financial position

Company overview

Appendix

16

© 2014 Ramirent 17

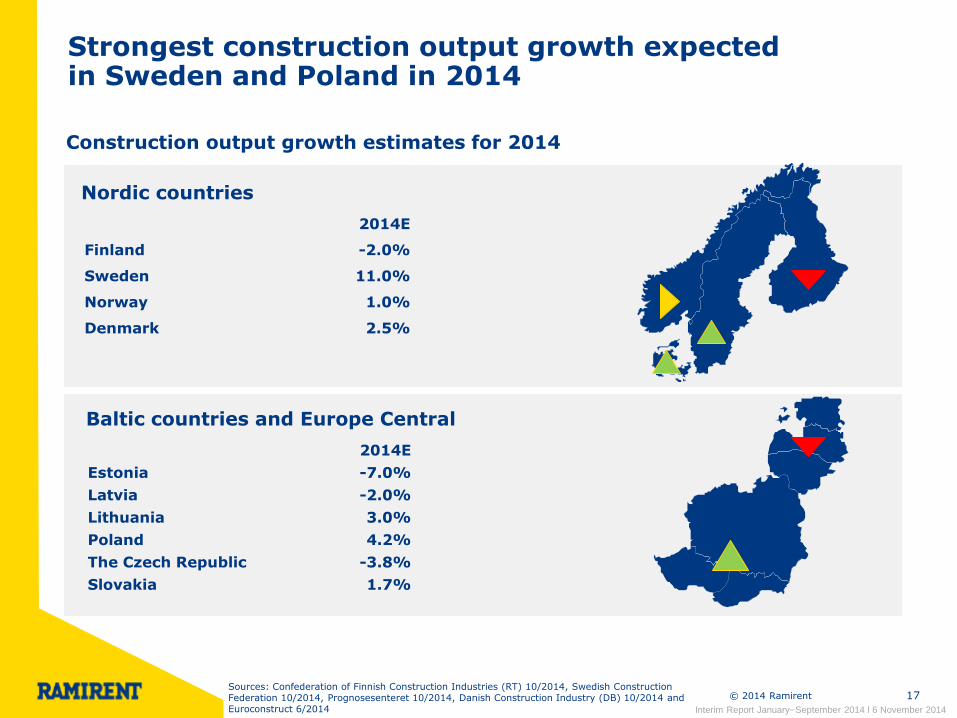

Strongest construction output growth expected in Sweden and Poland in 2014

Construction output growth estimates for 2014

Nordic countries

Baltic countries and Europe Central

2014E

Finland -2.0%

Sweden 11.0%

Norway 1.0%

Denmark 2.5%

2014E

Estonia -7.0%

Latvia -2.0%

Lithuania 3.0%

Poland 4.2%

The Czech Republic -3.8%

Slovakia 1.7%

Interim Report January–September 2014 l 6 November 2014

Sources: Confederation of Finnish Construction Industries (RT) 10/2014, Swedish Construction Federation 10/2014, Prognosesenteret 10/2014, Danish Construction Industry (DB) 10/2014 and Euroconstruct 6/2014

© 2014 Ramirent 18

Stable development in Ramirent's main equipment rental markets

Equipment rental market 2008-2015E (index)

Interim Report January–September 2014 l 6 November 2014

101

113

125

69

85

40

50

60

70

80

90

100

110

120

130

140

2008 2009 2010 2011 2012 2013 2014E 2015F

Finland Sweden Norway Denmark Poland

Source: ERA (European Rental Association) report 10/2014

© 2014 Ramirent 19

Equipment rental markets estimated to recover in 2015

Equipment rental market growth 2014-2015E (%)

Interim Report January–September 2014 l 6 November 2014

-1.6%

1.0%

2.0%

0.7%

1.5%

2.8%

2.1%

1.8%

1.1%

3.5%

5.3%

2.6%

-2.0%

-1.0%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

Finland Sweden Norway Denmark Poland Total Europe

2014E 2015E

Source: ERA (European Rental Association) report 10/2014

© 2014 Ramirent 20

Nordic construction order books increased by 5.2% compared to the previous year

Nordic construction companies order books (at comparable exchange rates)

billion

Nordic construction order books including NCC, YIT*, Lemminkäinen and SRV increased by 5.2% at comparable exchange rates compared to the previous year

Ramirent's rolling 12 months net sales declined by 8.0% (y-o-y)

*YIT's order book not fully comparable as it includes also order book from the Baltic States, Slovakia and the Czech Republic (change in reporting structure as of Q1/2014).

-40%

-20%

0%

20%

40%

60%

0

1

2

3

4

5

6

7

8

9

Q1

2007

Q2 Q3 Q4 Q1

2008

Q2 Q3 Q4 Q1

2009

Q2 Q3 Q4 Q1

2010

Q2 Q3 Q4 Q1

2011

Q2 Q3 Q4 Q1

2012

Q2 Q3 Q4 Q1

2013

Q2 Q3 Q4 Q1

2014

Q2 Q3

NCC YIT*

Lemminkäinen SRV

Change in Net sales (y-o-y), R12 Ramirent Change in order backlog (y-o-y), Nordic construction

Interim Report January–September 2014 l 6 November 2014

The economic growth in 2014 is

expected to be modest and construction

market demand remains mixed in our

core markets.

Ramirent will maintain strict cost

control and, for 2014, capital

expenditure is expected to be around

the same level as in 2013.

The strong financial position will enable

the Group to continue to address

profitable growth opportunities.

Ramirent outlook for 2014 unchanged

© 2014 Ramirent © 2014 Ramirent

Group performance

Segment review

Market outlook

Key figures

Financial position

Company overview

Appendix

23

Finland Sweden Norway Denmark Baltics Central

Net

Sale

s

(M

EU

R)

EB

IT

A m

arg

in

(%

)

R12 Q3/2013 R12 Q3/2014

Rolling 12 months EBITA margin improved in the Baltic States and Europe Central

17.6% 16.7% 16.0%

-6.1%2)

17.2%

-0.7%3)

15.2% 15.6%

9.5%

-9.1%

19.3%

2.3%

-20%

-10%

0%

10%

20%

Finland Sweden Norway Denmark The BalticStates

Europe Central

155.0

212.3

163.8

44.4 30.5

58.2

152.8

198.9

142.6

40.6 33.1 54.7

0.0

50.0

100.0

150.0

200.0

Finland Sweden Norway Denmark The BalticStates

Europe Central

1) Rolling 12 months EBITA excluding non–recurring items was EUR 15.5 million or 10.9% of net sales. Non-recurring items included restructuring provision of EUR 1.9 million in Norway, booked in the third quarter of 2014. 2) Rolling 12 months EBITA excluding non–recurring items was EUR −1.2 million or −2.7% of net sales. The non-recurring items included the EUR 1.5 restructuring provision for the third quarter of 2013. 3) Rolling 12 months EBITA excluding non–recurring items was EUR 1.5 million or 2.5% of net sales. The non-recurring items included the EUR 1.9 million loss from disposal of operation in Hungary, recorded in the third quarter 2013.

© 2014 Ramirent

1)

Interim Report January–September 2014 l 6 November 2014

© 2014 Ramirent 24

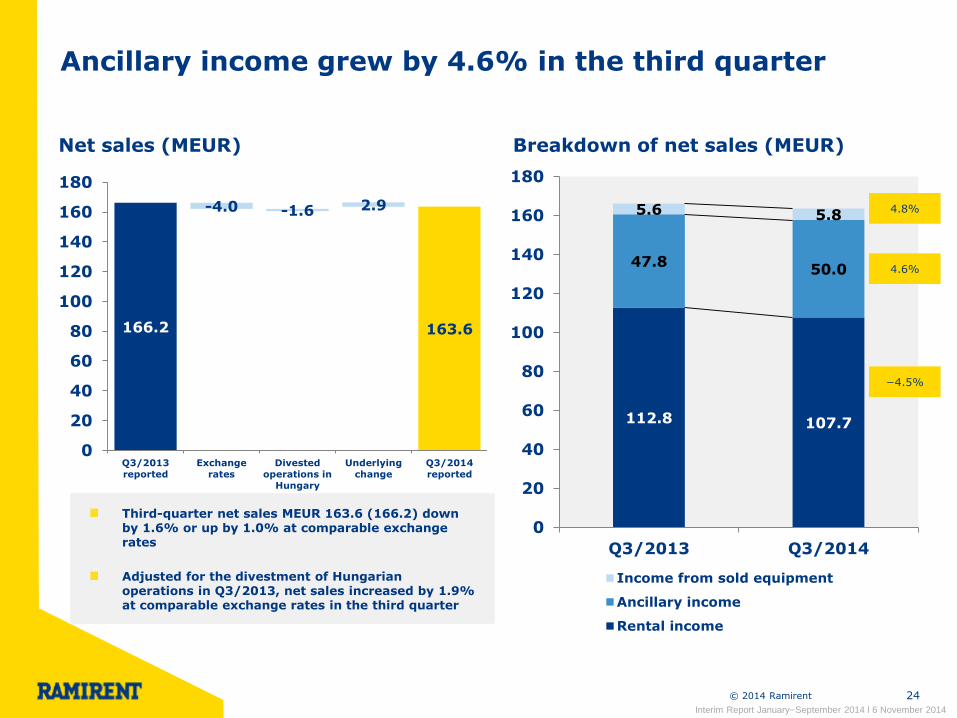

Ancillary income grew by 4.6% in the third quarter

Net sales (MEUR) Breakdown of net sales (MEUR)

112.8 107.7

47.8 50.0

5.6 5.8

0

20

40

60

80

100

120

140

160

180

Q3/2013 Q3/2014

Income from sold equipment

Ancillary income

Rental income

−4.5%

4.6%

4.8%

166.2

-4.0 -1.6 2.9

163.6

0

20

40

60

80

100

120

140

160

180

Q3/2013

reported

Exchange

rates

Divested

operations in

Hungary

Underlying

change

Q3/2014

reported

Third-quarter net sales MEUR 163.6 (166.2) down by 1.6% or up by 1.0% at comparable exchange rates

Adjusted for the divestment of Hungarian operations in Q3/2013, net sales increased by 1.9% at comparable exchange rates in the third quarter

Interim Report January–September 2014 l 6 November 2014

© 2014 Ramirent 25

Ramirent carried out actions to reduce its fixed cost base during the third quarter

Customer centres Personnel (FTE)

334 325 306 304 302 301 302

Q12013

Q2 Q3 Q4 Q12014

Q2 Q3

Finland Sweden Norway Denmark Europe East -Baltics Europe Central

Number of customer centres has been adjusted

to prevailing market conditions during 2014

Improving efficiency of repair & maintenance

operations on-going

Third-quarter employee benefit expenses

decreased to MEUR 37.7 (39.6)

Ramirent carried out actions to reduce its

fixed cost base in the third quarter

Group: 2,621 (2,597)

Interim Report January–September 2014 l 6 November 2014

Finland

538

Sweden

771 Norway

410

Denmark

151

Europe East -

Baltics 241

Europe

Central 473

© 2014 Ramirent 26

Ramirent’s third-quarter fixed costs 5.6 MEUR lower compared to last year

Fixed costs (MEUR) and % of Group net sales

68.0 63.7

58.1 36.6%

38.3%

35.5%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

0

10

20

30

40

50

60

70

80

Q12012

Q2 Q3 Q4 Q12013

Q2 Q3 Q4 Q12014

Q2 Q3

Group fixed costs MEUR 58.1 (63.7) in the third quarter

Third-quarter fixed costs of net sales 35.5% (38.3%)

Q3/14 fixed costs:

• Employee benefit expenses MEUR 37.7 (39.6)

• Other operating expenses MEUR 20.4 (24.1)

Fixed costs rolling 12 months MEUR 239.0 or 38.5% of net sales

Interim Report January–September 2014 l 6 November 2014

© 2014 Ramirent 27

Third-quarter reported and adjusted EBITDA margin improved from the previous year

EBITDA margin

31.3% 33.3% 33.0% 34.1%

0%

5%

10%

15%

20%

25%

30%

35%

40%

Q3/2013reported

Q3/2013 excl.non-recurring

items

Q3/2014reported

Q3/2014 excl.non-recurring

items

EBITDA margin quarterly

30.0%

32.7% 32.5% 31.3%

33.0%

0%

5%

10%

15%

20%

25%

30%

35%

Q1

2010

Q2 Q3 Q4 Q1

2011

Q2 Q3 Q4 Q1

2012

Q2 Q3 Q4 Q1

2013

Q2 Q3 Q4 Q1

2014

Q2 Q3

Restructuring provision of EUR 1.9 million in

Norway was booked

Q3/2014 EBITDA margin excl. non-recurring

items and divested operations 34.1% (33.3%1))

Year-to-date EBITDA MEUR 127.8 (148.8) or

28.2% (31.0%) of net sales

Year-to-date EBITDA excluding non-recurring

items and adjusted for transferred or divested

operations was MEUR 129.7 (139.6) or 28.6%

(29.7%)

Interim Report January–September 2014 l 6 November 2014

1) Non-recurring items in the third quarter of 2013 included the EUR 1.5 million restructuring provision in Denmark, the EUR 1.9 million loss from disposal of Hungary and the EUR 0.6 million EBITDA result from Hungary.

© 2014 Ramirent 28

Third-quarter reported EBITA was 28.0 MEUR, 17.1% of net sales

12.4%

17.9% 17.1%

15.6%

17.1%

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

Q1

2010

Q2 Q3 Q4 Q1

2011

Q2 Q3 Q4 Q1

2012

Q2 Q3 Q4 Q1

2013

Q2 Q3 Q4 Q1

2014

Q2 Q3

15.6% 17.5% 17.1%

18.3%

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

Q3/2013reported

Q3/2013 excl.non-recurring

items

Q3/2014reported

Q3/2014 excl.non-recurring

items

Restructuring provision of EUR 1.9 million in

Norway was booked

Q3/2014 EBITA margin excl. non-recurring

items and divested operations 18.3% (17.5%1))

Year-to-date EBITA MEUR 51.3 (71.2) or 11.3%

(14.8%) of net sales

Year-to-date EBITA excl. non-recurring items and

adjusted for transferred or divested operations

was MEUR 53.2 (62.7) or 11.7% (13.3%)

EBITA margin EBITA margin quarterly

Interim Report January–September 2014 l 6 November 2014

1) Non-recurring items in the third quarter of 2013 included the EUR 1.5 million restructuring provision in Denmark, the EUR 1.9 million loss from disposal of Hungary and the EUR 0.6 million EBITA result from Hungary.

© 2014 Ramirent 29

EBITA excl. non-recurring items was 11.7% in January-September 2014

71.2

62.7

51.3

1.93)

6.81)

64.4

1.72)

53.2

0.0

10.0

20.0

30.0

40.0

50.0

60.0

70.0

80.0

1-9/2013 reported 1-9/2013 excl. non-

recurring items

1-9/2013 adjusted 1-9/2014 reported 1-9/2014 excl. non-

recurring items

EBITA (MEUR) 1-9/13 vs 1-9/14

1) Non-recurring items in 2013: -the loss from disposal Hungary MEUR 1.9 -the non-taxable capital gain from Fortrent transation MEUR 10.1 -the restructuring provision in Denmark MEUR 1.5

2) EBITA result from Russia, Ukraine and Hungary

3) Restructuring provision of EUR 1.9 million in Norway

14.8% 13.3% 11.3% EBITA margin 13.4%

Interim Report January–September 2014 l 6 November 2014

11.7%

© 2014 Ramirent 30

Group R12 EBITA margin was 11.6%

Q3/2014 R12 EBITA margin by segment (%)

15.2 15.6

9.5

-9.1

19.3

2.3

11.6

-5

0

5

10

15

20

Finland Sweden Norway Denmark Baltics Europe Central Group

Group EBITA targeted to reach 17% by

the end of 2016…

…by delivering at least 18% EBITA

margin on segment level

18%

10%

Interim Report January–September 2014 l 6 November 2014

© 2014 Ramirent 31

Investments in machinery and equipment adjusted to prevailing market conditions

Gross capital expenditure (MEUR) and % of net sales

9.7

119.9

28.0 29.5 23.8

0%

10%

20%

30%

40%

50%

60%

70%

80%

0

20

40

60

80

100

120

140

Q12010

Q2 Q3 Q4 Q12011

Q2 Q3 Q4 Q12012

Q2 Q3 Q4 Q12013

Q2 Q3 Q4 Q12014

Q2 Q3

Gross Capex Share of net sales-%

Third-quarter gross capex MEUR 23.8 (29.5) of which 0.1 (0.0) related to acquisitions

Investments in machinery and equipment MEUR 20.4 (28.0) in the third quarter

Gross capex in 1-9/2014 was MEUR 125.6 (91.9)

Interim Report January–September 2014 l 6 November 2014

© 2014 Ramirent 32

Capital expenditure focused on Finland and Sweden

• Net debt to EBITDA 1.1x in Q4

• Long-term financial target: below 1.6x

(at the end of FY)

Capital expenditure by segment (MEUR)

Investments

21.9

26.8

25.4

4.7

6.9

4.9

31.4

56.0

13.5

3.3

8.7

6.7

0.0 20.0 40.0 60.0

Finland

Sweden

Norway

Denmark

East

Central1-9/14

1-9/13 In January-September 2014, investments in

machinery and equipment MEUR 92.5 (85.3)

Interim Report January–September 2014 l 6 November 2014

© 2014 Ramirent 33

Cash flow after investments and cash conversion positive

-60%

-40%

-20%

0%

20%

40%

60%

80%

-60

-40

-20

20

40

60

80

EBITDA (MEUR)

Cashflow after investments (MEUR)

Cash Conversion

Cash flow after investments (MEUR) Cash conversion (MEUR and %)

19

-5

34

25

-5

-22

14

-30

-20

-10

0

10

20

30

40

Q1

2013

Q2 Q3 Q4 Q1

2014

Q2 Q3

Cash flow after investments MEUR 13.7 (34.4) in

the third quarter

Cash flow after investments MEUR -10.7 (48.2) in

January-September 2014

Interim Report January–September 2014 l 6 November 2014

© 2014 Ramirent 34

Return on investment at 12.3% at the end of the third quarter

Return on investment % ROI % and Invested capital MEUR

17.5%

12.3%

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

Q3/2013 Q3/2014

509.2

588.3 605.0 604.1 605.2

5.4%

13.2%

18.6%

17.5%

12.3%

0%

5%

10%

15%

20%

25%

0

100

200

300

400

500

600

700

Q1

2010

Q2 Q3 Q4 Q1

2011

Q2 Q3 Q4 Q1

2012

Q2 Q3 Q4 Q1

2013

Q2 Q3 Q4 Q1

2014

Q2 Q3

Rolling 12 months ROI at the end of Q3 was

12.3% (17.5%)

Return on investment decreased compared year-

on-year mainly due to lower profit generation

The Group's invested capital was close to last

year's level and amounted to 605.2 (604.1) at the

end of Q3/14

Interim Report January–September 2014 l 6 November 2014

© 2014 Ramirent 35

Return on equity at 12.0% at the end of the third quarter

Return on equity % ROE % and Total equity (MEUR)

16.9%

12.0%

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

Q3/2013 Q3/2014

307.5 305.3

346.8 360.7

342.1

-0.6%

11.4%

18.7%

16.9%

12.0%

-5%

0%

5%

10%

15%

20%

25%

0

50

100

150

200

250

300

350

400

Q1

2010

Q2 Q3 Q4 Q1

2011

Q2 Q3 Q4 Q1

2012

Q2 Q3 Q4 Q1

2013

Q2 Q3 Q4 Q1

2014

Q2 Q3

Rolling 12 months ROE at the end of Q3 was

12.0% (16.9%)

Long-term financial target: ROE of 18% over a

business cycle

The Group's total equity amounted to MEUR 342.1

(360.7) at the end of Q3/14

Equity per share was 3.17 (3.35) at the of the

quarter

Interim Report January–September 2014 l 6 November 2014

Target 18%

© 2014 Ramirent © 2014 Ramirent 36

Group performance

Segment review

Market outlook

Key figures

Financial position

Company overview

Appendix

© 2014 Ramirent 37

Net debt to EBITDA ratio below long-term financial target

Net debt (MEUR) Net debt to EBITDA ratio

230

260

0

50

100

150

200

250

300

Q1

2013

Q2 Q3 Q4 Q1

2014

Q2 Q3

1.7x 1.7x

1.2x

1.1x

1.5x

0.0

0.5

1.0

1.5

2.0

2.5

Q12010

Q2 Q3 Q4 Q12011

Q2 Q3 Q4 Q12012

Q2 Q3 Q4 Q12013

Q2 Q3 Q4 Q12014

Q2 Q3

Net debt MEUR 259.7 (230.3) at the end of

Q3/14

Net debt increased by 12.7% (y-o-y)

Net debt to EBITDA 1.5x (1.1x) at the end of

September, which was below Ramirent's long-

term financial target of maximum 1.6x at the end

of each fiscal year

Interim Report January–September 2014 l 6 November 2014

© 2014 Ramirent 38

Equity ratio and gearing weakened slightly year-on-year

Equity ratio (%) Gearing (%)

45.2% 42.8%

0%

10%

20%

30%

40%

50%

60%

Q1

2013

Q2 Q3 Q4 Q1

2014

Q2 Q3

63.9%

75.9%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

Q1

2013

Q2 Q3 Q4 Q1

2014

Q2 Q3

Third-quarter equity ratio decreased to 42.8%

(45.2%)

Total equity amounted to MEUR 342.1 (360.7) at the

end of the quarter

Third-quarter gearing increased to 75.9% (63.9%)

Net debt MEUR 259.7 (230.3) at the end of the

quarter

Interim Report January–September 2014 l 6 November 2014

© 2014 Ramirent 39

An ordinary dividend of EUR 0.37 per share was paid and the

AGM authorised the Board to decide on a potential additional

dividend of up to EUR 0.63 per share

Earnings Per Share and Dividend Per Share

0.04

0.13

0.41

0.59

0.50

0.15

0.25 0.28

0.34

0.00

0.10

0.20

0.30

0.40

0.50

0.60

0.70

0.80

0.90

1.00

2009 2010 2011 2012 2013

EPS DPS

Ordinary dividend of EUR 0.37 per share paid in April 2014 representing a payout ratio of 73.7% (57.6%) for fiscal year 2013

Potential for an additional dividend of up to EUR 0.63 per share for fiscal year 2013, which would represent a total payout ratio of up to 199% for fiscal year 2013

Long-term financial target: Dividend payout ratio at least 40% of net profit

1.00

0.37

0.63

Interim Report January–September 2014 l 6 November 2014

© 2014 Ramirent 40

Working capital at 6.4% of net sales

Working capital (MEUR) Working capital / Rolling 12 months net sales

5.3% 5.6% 5.5% 5.6%

6.4%

-6.0%

-4.0%

-2.0%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

Q1

2010

Q2 Q3 Q4 Q1

2011

Q2 Q3 Q4 Q1

2012

Q2 Q3 Q4 Q1

2013

Q2 Q3 Q4 Q1

2014

Q2 Q3

14.4 12.0

125.3 121.1

-102.0 -93.3

-200

-150

-100

-50

0

50

100

150

200

Q12013

Q2 Q3 Q4 Q12014

Q2 Q3

Trade payables and other liabilities

Trade and other receivables

Inventories

Credit losses and change in the allowance for bad

debt:

7-9/2014: MEUR -1.0 (-0.3)

1-9/2014: MEUR -2.5 (-3.2)

Working capital of rolling 12 months net sales

6.4% (5.6%) at the end of September

Dividend of MEUR 39.8 (36.6) paid in April 2014

Interim Report January–September 2014 l 6 November 2014

© 2014 Ramirent 41

At the end of September 2014, Ramirent had unused committed back–up loan facilities of MEUR 156.4

Repayment schedule of interest-bearing liabilities (MEUR) Ramirent had unused committed back-up loan facilities of MEUR 156.4 available at the end of the third quarter

The average interest rate of the loan portfolio including interest rate hedges was 2.8% (3.9%) at the end of the third quarter

In addition to bank facilities, Ramirent is utilising a domestic commercial paper program of up to EUR 150 million

Net debt EUR 259.7 million

EUR 415.0 million in committed credit facilities

Interim Report January–September 2014 l 6 November 2014

Senior unsecured bond

75

95

100

145

2014 2015 2016 2017 2018 2019 2020

© 2014 Ramirent 42

Two of our long-term financial targets were met in Q3/2014

Leverage and risk

Profit generation

Dividend

Element Target level

ROE

Net Debt / EBITDA

ratio

Dividend pay-out

ratio

18% p.a. over a business cycle

Below 1.6x at the end of each fiscal year

At least 40% of Net profit

Measure Q3/2014

12.0%

1.5x

73.7% of 2013 net profit

STATED OBJECTIVES

Interim Report January–September 2014 l 6 November 2014

For further information:

Magnus Rosén, President and CEO, tel. +358 20 750 2845 Jonas Söderkvist, CFO, tel. +358 20 750 3248 Franciska Janzon, IR, tel. +358 20 750 2859

www.ramirent.com

© 2014 Ramirent © 2014 Ramirent 44

Group performance

Segment review

Market outlook

Key figures

Financial position

Company overview

Appendix

© 2014 Ramirent

Ramirent is a generalist equipment rental and service company

45

Where

Geographic presence

Home market Europe with focus on the Baltic Rim

How

Concept Ramirent is a generalist rental company, with an extensive customer centre network enabling customer proximity while managing through decentralised operations

What

Offering Ramirent’s business offering stretches from single products to managing the entire fleet capacity at a customer site

Who

Customers Ramirent’s diverse customer base includes construction, industry, services, the public sector and private households

302 customer centres in 10

countries

2,621 employees serving 200,000 customers with

200,000 rental items

MEUR 647 of sales (2013)

Definition of Ramirent's business and strategic choices

Interim Report January–September 2014 l 6 November 2014

© 2014 Ramirent 46

Vision

To be the leading and most progressive equipment rental solutions company in Europe, setting the benchmark for industry performance and customer service

Values Open

Engaged

Progressive

Mission

We simplify business by delivering Dynamic Rental SolutionsTM

Brand promise

More than Machines

Our strategic choices

Interim Report January–September 2014 l 6 November 2014

© 2014 Ramirent 47

We increased geographical focus on core Baltic Rim markets and widened the customer base

Europe Central

(PL+CZ+SL)

# 1 59 customer

centres

Finland # 1

67 customer centres

Sweden # 2

75 customer centres

Norway # 1

43 customer centres

Denmark # 1

16 customer centres

Europe East –Baltics

# 1 42 customer

centres

Finland 25%

Sweden 32%

Norway 22%

Denmark 6%

Europe East -Baltics

5%

Europe Central 9%

Sales per customers 1-9/2014

Construction 63% Industrial

18%

Services & Retail 13%

Public 4%

Private 2%

Current state close to target of 40% non-construction dependent sales

Russia and Ukraine presence through JV Fortrent

Sales per segment 1-9/2014

Interim Report January–September 2014 l 6 November 2014

© 2014 Ramirent Event / Name of presentor 48

0 200 400 600 800 1000

Loxam

Cramo

Ramirent

Algeco

Scotsman

Kiloutou

Sarens

Speedy Hire

Liebherr-

Mietpartner

Mediaco Levage

Zeppelin Rental

Net sales 2013 (MEUR) Net sales 2013 (MEUR)

Largest rental companies in Europe Largest rental companies globally

One of the leading equipment rental companies both in Europe (#3) and globally (#10)

0 1000 2000 3000 4000

United Rentals

Aggreko

Ashtead Group

Algeco

Scotsman

Herz Equipment

Rental

Aktio Corp

Loxam

Coates Hire

Cramo

Ramirent

Source: IRN June 2014

Interim Report January–September 2014 l 6 November 2014

49

Our offering

MODULE AND SITE EQUIPMENT

HEAVY MACHINERY ACCESS EQUIPMENT

PLANNING

LIGHT EQUIPMENT

LOGISTICS

ON-SITE SERVICES

RENTAL INSURANCE

TRAINING ACCESSORIES

Ramirent SpaceSolveTM

Ramirent SafeSolveTM

Ramirent EcoSolveTM

Ramirent PowerSolveTM

Ramirent ClimateSolveTM

Ramirent AccessSolveTM

Ramirent TotalSolveTM

MACHINERY AND EQUIPMENT SERVICES

SOLUTION AREAS

© 2014 Ramirent 50

Equipment Services

Rental Business and Sector Knowledge

Benefits Lighter balance sheets, less investments

Benefits More uptime in core operations due to less downtime in equipment, less maintenance costs, right choice of equipment improves efficiency, less product liability risk

Benefits Understanding customer requirements helps to customise product selection and further improve productivity

Heavy Equipment

Access Equipment Lifts, Hoists,

Scaffolding, Tower cranes

Modules and site equipment

Light Equipment Tools, power and heating

equipment

• Planning

• On-site services

• Logistics

• Merchandise sale

• Rental insurance

• Training

• Construction

• Mining

• Paper

• Power generation

• Oil & Gas

• Shipyards

• Retail & Service

• Public sector

• Households

Integrated Solutions

Benefits Easy to buy, reduced number of subcontractors, increased focus on the core business

Ramirent combines the best equipment, services and knowhow into integrated rental solutions

Interim Report January–September 2014 l 6 November 2014

6%

34%

23%

38%

Share of Group equipment rental income (1-9/2014)

© 2014 Ramirent

Customer First

Common Ramirent Platform

Sustainable profitable

growth

Balanced business portfolio

51

Ramirent's strategic priorities

Strong local customer orientation and tailored offerings

Increased synergies & operational excellence

Further widening the customer base

Interim Report January–June 2014 l 29 July 2014

© 2014 Ramirent 52

Increased market share

Growth within current business

Extended customer value

proposition

Increasing services and integrated solutions

Increased penetration

Outsourcing opportunities

Increased footprint

New customer segments

New geographies

M&A

Acquisitions, joint ventures

and other transactions

1 2 3 4 5

Interim Report January–September 2014 l 6 November 2014

The five components of Ramirent's growth strategy

© 2014 Ramirent 53

Room for rental penetration to further increase in the Nordic countries

Equipment rental penetration 2014E (%)

3.5%

2.0%

1.5% 1.7%

Rental penetration (%)*

Sweden Norway Finland Denmark

Source: European Rental Association 10/2014; Rental Turnover / Total construction output

HIG

H

ME

DIU

M

LO

W

Average penetration in Europe: 1.5%

Interim Report January–September 2014 l 6 November 2014

© 2014 Ramirent 54

Ramirent has seen significant growth through outsourcing and acquisitions

Outsourcing deal in Finland

Acquisition of Finnish weather protection

rental company

Aquisition of Czech rental

business Acquisition of Czech

rental business

Acquisition of Swedish rental

company Acquisition of Danish rental

business

Acquisition of module rental company in Norway

Outsourcing of Mt Hojgaard's Danish scaffolding division

Acquisition of Swedish rental company

Acquisition of Swedish rental

company

Outsourcing deal in Norway

Joint venture in Russia and Ukraine

with Cramo

2011 - 2012 2013

Outsourcing deal in Finland

Divestment of operations in

Hungary

Formworks partnership with Doka in Finland

Extending geography to “white spots”

Complimentary product ranges or related services

Strengthening links to new customer segments

Targets mid-size companies mainly

Outsourcing of customer’s in-house fleets

Criteria

Proven track record of accretive acquisitions made at attractive multiples tied to earn-outs

Outsourcing deal in Denmark

2014

Acquisition of safety solutions

specialist company in Sweden

Acquisition of telehandler

business in Finland

DCC (Dry Construction

Concept) business in Sweden,

Denmark and Finland

Outsourcing deal in Finland

Joint Venture* with Zeppelin Rental in Fehmarnbelt tunnel construction project

in Germany and Denmark

*Subject to relevant authorities approval Interim Report January–September 2014 l 6 November 2014

© 2014 Ramirent 55

Ramirent's Financial Business Model: Three complimentary drivers of value creation

• Volumes • Upselling

• Pricing • Fleet management • Sourcing • Cost structure • Quality of earnings

• Cash conversion • Capex • Working capital • Dividend • Capital Structure

Organic Growth Operating Leverage Financial Leverage

Cash Flow

Target EBITA margin of 17% by the end of 2016

Net debt/ EBITDA target of below 1.6x (at y/e)

Capital

Expenditure

ROE target of 18% over the cycle

Dividend pay-out ratio of at least 40% of

net profit

Interim Report January–September 2014 l 6 November 2014

© 2014 Ramirent 56

Customer

service level

Total costs

Non- available

fleet

Capital efficiency

Optimising fleet maintenance strategy

Resourcing and repair & maintenance locations

Optimising workshop processes

Balanced fleet age structure

Fleet management activities

Efficiency utilisation* (%) R3 months

Total Fleet Yield** (%) R3 months

∗) 𝐸𝑓𝑓𝑖𝑐𝑖𝑒𝑛𝑐𝑦 𝑢𝑡𝑖𝑙𝑖𝑠𝑎𝑡𝑖𝑜𝑛 =𝐴𝑐𝑞𝑢𝑖𝑠𝑖𝑡𝑖𝑜𝑛 𝑣𝑎𝑙𝑢𝑒 𝑜𝑓 𝑟𝑒𝑛𝑡𝑒𝑑 𝑓𝑙𝑒𝑒𝑡

𝐴𝑐𝑞𝑢𝑖𝑠𝑖𝑡𝑖𝑜𝑛 𝑣𝑎𝑙𝑢𝑒 𝑜𝑓 𝑡𝑜𝑡𝑎𝑙 𝑓𝑙𝑒𝑒𝑡∗ 100 %

∗∗) 𝑇𝑜𝑡𝑎𝑙 𝐹𝑙𝑒𝑒𝑡 𝑌𝑖𝑒𝑙𝑑 =𝑅𝑒𝑛𝑡𝑎𝑙 𝑖𝑛𝑐𝑜𝑚𝑒 ∗ 100 %

𝐴𝑐𝑞𝑢𝑖𝑠𝑖𝑡𝑖𝑜𝑛 𝑣𝑎𝑙𝑢𝑒 𝑜𝑓 𝑡𝑜𝑡𝑎𝑙 𝑓𝑙𝑒𝑒𝑡

Goals KPIs

Efficient logistics

Fleet management potential realised at different levels

Interim Report January–September 2014 l 6 November 2014

30%

35%

40%

45%

50%

55%

60%

65%

Dec 0

9

Mar

10

Jun 1

0

Sep 1

0

Dec 1

0

Mar

11

Jun 1

1

Sep 1

1

Dec 1

1

Mar

12

Jun 1

2

Sep 1

2

Dec 1

2

Mar

13

Jun 1

3

Sep 1

3

Dec 1

3

Mar

14

Jun 1

4

Sep 1

4

20%

25%

30%

35%

40%

45%

50%

Dec 0

9

Mar

10

Jun 1

0

Sep 1

0

Dec 1

0

Mar

11

Jun 1

1

Sep 1

1

Dec 1

1

Mar

12

Jun 1

2

Sep 1

2

Dec 1

2

Mar

13

Jun 1

3

Sep 1

3

Dec 1

3

Mar

14

Jun 1

4

Sep 1

4

© 2014 Ramirent 57

Market Cap EUR 677.2 million

Trading information Listing: NASDAX OMX Helsinki Date of listing: April 30, 1998

Segment: Mid Cap Sector: Industrials

Trading code: RMR1V

16%

28%

9% 11%

2%

34%

Private companies

Financial and insurance institutions

Public sector organizations

Households

Non-profit organizations

Foreigners

Shareholders September 30, 2014

Largest shareholders September 30, 2014

Number of shares

% of share

capital

1. Nordstjernan AB 31,303,716 28.80%

2. Oy Julius Tallberg Ab 12,207,229 11.23%

3. Nordea funds 5,043,904 4.64%

4. Varma Mutual Pension Insurance Company 4,113,799 3.78%

5. Ilmarinen Mutual Pension Insurance Company 3,945,154 3.63%

6. Odin funds 2,758,691 2.54%

8. Aktia funds 2,275,562 2.09%

9. Fondita funds 1,055,000 0.97%

10. Oslo Pensjonsforsikring As 800,000 0.74%

Ramirent Plc 973,957 0.90%

Other shareholders 44,220,316 40.68%

Total 108,697,328 100.00%

Largest shareholders at the end of September 2014

Interim Report January–September 2014 l 6 November 2014

© 2014 Ramirent 58

Share price development year-to-date

Ramirent Plc (RMR1V)

Index

Interim Report January–September 2014 l 6 November 2014

0

20

40

60

80

100

120

Jan-14 Feb-14 Mar-14 Apr-14 May-14 Jun-14 Jul-14 Aug-14 Sep-14 Oct-14 Nov-14

RMR1V

Nasdaq Helsinki

Nasdaq Helsinki Mid-Cap

(6.35 Nov. 4, 2014)

© 2014 Ramirent

Attractive market - structural growth drivers and cyclical recovery potential

Number 1 position - market leader in 7/10 countries

Strong platform - above industry average profitability, balanced risk level and increasing operational excellence

Growth potential - 5 point growth strategy to capitalise on strong position

Financial strength – industry leading cash generation and leverage potential to finance growth, drive ROE and increase dividends

Proven management track record – experienced management has reshaped the company since 2008

59

Return on equity of 18% over a business cycle

YE net debt to EBITDA of below 1.6x

Dividend pay-out ratio of at least 40% of net profit

EBITA margin of 17% by the end of 2016

How will we deliver on our financial targets and create shareholder value?

Company highlights Stated objectives

Interim Report January–September 2014 l 6 November 2014

© 2014 Ramirent © 2014 Ramirent 60

Group performance

Segment review

Market outlook

Key figures

Financial position

Company overview

Appendix

© 2014 Ramirent 61

Consolidated statement of income

Interim Report January–September 2014 l 6 November 2014

CONSOLIDATED STATEMENT OF INCOME 7–9/14

7–9/13

1–9/14

1–9/13

1–12/13

(EUR 1,000)

Rental income 107,672 112,764 292,541 316,133 420,895

Ancillary income 50,041 47,830 143,219 146,186 198,040

Sales of equipment 5,839 5,574 17,115 17,471 28,317

NET SALES 163,551 166,168 452,875 479,791 647,252

Other operating income 958 827 2,111 12,524 12,732

Materials and services −52,955 −51,876 −149,375 −152,064 −213,169

Employee benefit expenses −37,690 −39,625 −112,287 −120,813 −156,791

Other operating expenses −20,407 −24,099 −65,378 −70,277 −95,660

Share of result in associates and joint ventures 476 572 −106 −353 688

Depreciation, amortisation and impairment charges −27,905 −27,638 −82,217 −85,501 −112,768

EBIT 26,028 24,330 45,623 63,307 82,284

Financial income 3,195 3,207 7,365 13,031 15,639

Financial expenses −5,546 −6,946 −16,945 −25,302 −34,055

Total financial income and expenses −2,351 −3,739 −9,580 −12,270 −18,415

EBT 23,677 20,590 36,044 51,037 63,869

Income taxes −5,402 −3,776 −8,207 −10,907 −9,839

PROFIT FOR THE PERIOD 18,276 16,814 27,837 40,130 54,030

Profit for the period attributable to:

Owners of the parent company 18,435 16,814 28,142 40,130 54,030

Non-controlling interest −160 − −304 − −

18,276 16,814 27,837 40,130 54,030

Earnings per share (EPS) on parent company shareholders’ share of profit

Basic, EUR 0.17 0.16 0.26 0.37 0.50

Diluted, EUR 0.17 0.16 0.26 0.37 0.50

© 2014 Ramirent 62

Interim Report January–September 2014 l 6 November 2014

CURRENT ASSETS

Inventories 12,015 14,434 11,494

Trade and other receivables 121,148 125,300 109,207

Current tax assets 4,042 3,351 1,495

Cash and cash equivalents 3,436 13,118 1,849

TOTAL CURRENT ASSETS 140,642 156,202 124,045

TOTAL ASSETS 799,143 797,687 759,477

CONSOLIDATED STATEMENT OF FINANCIAL POSITION 30/9/2014

30/9/2013

31/12/2013

(EUR 1,000)

ASSETS

NON–CURRENT ASSETS

Goodwill 142,460 126,590 124,825

Other intangible assets 46,613 37,894 38,427

Property, plant and equipment 434,694 436,012 432,232

Investments in associates and joint ventures 14,747 19,026 18,524

Non–current loan receivables 18,254 20,261 20,261

Available–for–sale investments 150 412 517

Deferred tax assets 1,582 1,291 647

TOTAL NON–CURRENT ASSETS 658,500 641,486 635,432

Consolidated statement of financial position

© 2014 Ramirent 63

CONSOLIDATED STATEMENT OF FINANCIAL POSITION 30/9/2014

30/9/2013

31/12/2013

Consolidated statement of financial position (continued)

Interim Report January–September 2014 l 6 November 2014

(EUR 1,000)

EQUITY AND LIABILITIES

EQUITY

Share capital 25,000 25,000 25,000

Revaluation fund −724 −3,376 −1,502

Invested unrestricted equity fund 113,767 113,568 113,568

Retained earnings from previous years 174,980 185,368 179,882

Profit for the period 28,142 40,130 54,030

Equity attributable to the parent company shareholders 341,165 360,690 370,978

Non-controlling interest 950 − −

TOTAL EQUITY 342,114 360,690 370,978

NON–CURRENT LIABILITIES

Deferred tax liabilities 54,731 57,417 54,286

Pension obligations 17,600 14,806 13,923

Non–current provisions 2,399 1,379 1,198

Non–current interest–bearing liabilities 207,256 243,405 174,981

Other non–current liabilities 19,963 5,546 −

TOTAL NON–CURRENT LIABILITIES 301,949 322,553 244,388

CURRENT LIABILITIES

Trade payables and other liabilities 93,271 101,973 104,369

Current provisions 1,219 1,128 664

Current tax liabilities 4,727 11,303 5,278

Current interest–bearing liabilities 55,863 40 33,800

TOTAL CURRENT LIABILITIES 155,079 114,444 144,111

TOTAL LIABILITIES 457,028 436,997 388,499

TOTAL EQUITY AND LIABILITIES 799,143 797,687 759,477

© 2014 Ramirent 64

Key financial figures

1) The figures are calculated on a rolling twelve month basis

2) As of first quarter 2014, reporting of number of personnel was changed to FTE (full-time equivalent) which indicates the number of employees calculated as full

time workload for each person employed and actually present in the company. Comparative information has been changed accordingly.

Interim Report January–September 2014 l 6 November 2014

KEY FINANCIAL FIGURES 7–9/14

7–9/13

1–9/14

1–9/13

1–12/13

(MEUR)

Net sales, EUR million 163.6 166.2 452.9 479.8 647.3

Change in net sales, % −1.6% −10.6% −5.6% −7.7% −9.4%

EBITDA, EUR million 53.9 52.0 127.8 148.8 195.1

% of net sales 33.0% 31.3% 28.2% 31.0% 30.1%

EBITA, EUR million 28.0 25.9 51.3 71.2 92.1

% net sales 17.1% 15.6% 11.3% 14.8% 14.2%

EBIT, EUR million 26.0 24.3 45.6 63.3 82.3

% of net sales 15.9% 14.6% 10.1% 13.2% 12.7%

EBT, EUR million 23.7 20.6 36.0 51.0 63.9

% of net sales 14.5% 12.4% 8.0% 10.6% 9.9%

Profit for the period attributable to the owners of the

parent company, EUR million 18.4 16.8 28.1 40.1 54.0

% of net sales 11.3% 10.1% 6.2% 8.4% 8.3%

Gross capital expenditure, EUR million 23.8 29.5 125.6 91.9 125.8

% of net sales 14.6% 17.8% 27.7% 19.2% 19.4%

Invested capital, EUR million, end of period 605.2 604.1 579.8

Return on invested capital (ROI), %1) 12.3% 17.5% 16.5%

Return on equity (ROE), %1) 12.0% 16.9% 14.7%

Interest–bearing debt, EUR million 263.1 243.4 208.8

Net debt, EUR million 259.7 230.3 206.9

Net debt to EBITDA ratio1) 1.5x 1.1x 1.1x

Gearing, % 75.9% 63.9% 55.8%

Equity ratio, % 42.8% 45.2% 48.9%

Personnel, average during reporting period2) 2,564 2,767 2,725

Personnel, at end of reporting period2) 2,621 2,597 2,589

© 2014 Ramirent 65

Consolidated cash flow statement

Interim Report January–September 2014 l 6 November 2014

CONSOLIDATED CASH FLOW STATEMENT 7–9/14

7–9/13

1–9/14

1–9/13

1–12/13

(EUR 1,000)

CASH FLOW FROM OPERATING ACTIVITIES

EBT 23,677 20,590 36,044 51,037 63,869

Adjustments

Depreciation, amortisation and impairment charges 27,905 27,638 82,217 85,501 112,768

Adjustment for proceeds from sale of used rental equipment 3,231 1,304 14,101 7,703 8,975

Financial income and expenses 2,351 3,739 9,580 12,270 18,415

Adjustment for proceeds from disposals of subsidiaries − −5,481 − −15,609 −15,609

Other adjustments −4,538 20,035 −3,520 18,195 4,735

Cash flow from operating activities before change in working capital 52,626 67,826 138,422 159,098 193,153

Change in working capital

Change in trade and other receivables −9,242 7,022 −11,257 8,046 18,994

Change in inventories 1,057 1,196 −481 816 3,114

Change in non–interest–bearing liabilities −3,778 −13,829 −21,077 −17,868 −5,724

Cash flow from operating activities before interest and taxes 40,663 62,214 105,606 150,091 209,537

Interest paid −1,975 −2,972 −9,820 −8,022 −5,270

Interest received 256 549 959 1,857 1,047

Income tax paid −3,293 −2,566 −9,953 −17,153 −23,068

NET CASH FLOW FROM OPERATING ACTIVITIES 35,650 57,226 86,791 126,773 182,245

© 2014 Ramirent 66

Consolidated cash flow statement (continued)

CONSOLIDATED CASH FLOW STATEMENT 7–9/14

7–9/13

1–9/14

1–9/13

1–12/13

Interim Report January–September 2014 l 6 November 2014

CASH FLOW FROM INVESTING ACTIVITIES

Acquisition of businesses and subsidiaries, net of cash − − −27,272 − −2,832

Investment in tangible non–current asset (rental machinery) −19,809 −26,928 −72,576 −85,339 −110,115

Investment in other tangible non–current assets −239 −890 −817 −2,465 −2,825

Investment in intangible non–current assets −2,897 −588 −6,356 −4,121 −6,503

Proceeds from sale of tangible and intangible non–current assets

(excluding used rental equipment) − 138 7,482 262 360

Proceeds from sales of other investments − 5,481 − 14,681 14,681

Loan receivables, increase, decrease and other changes 1,006 − 2,006 −1,577 −1,577

NET CASH FLOW FROM INVESTING ACTIVITIES −21,939 −22,786 −97,534 −78,560 −108,812

CASH FLOW FROM FINANCING ACTIVITIES

Paid dividends − − −39,858 −36,618 −36,618

Borrowings and repayments of current debt (net) −22,621 −21,545 57,442 −49,719 −49,771

Borrowings of non–current debt − 37 − 99,113 99,031

Repayments of non–current debt −9 −2,906 −5,255 −49,210 −85,565

NET CASH FLOW FROM FINANCING ACTIVITIES −22,630 −24,414 12,330 −36,433 −72,923

NET CHANGE IN CASH AND CASH EQUIVALENTS

DURING THE FINANCIAL YEAR −8,919 10,026 1,588 11,780 511

Cash at the beginning of the period 12,356 3,093 1,849 1,338 1,338

Translation differences − − − − −

Change in cash −8,919 10,026 1,588 11,780 511

Cash at the end of the period 3,436 13,118 3,436 13,118 1,849

Presentation of the figures in the consolidated cash flow statement for January–June 2014 has been adjusted and consolidated cash flow statement for January–September

2014 has been adjusted accordingly. After adjustment the cash flows reflect better the impact of acquired businesses.

© 2014 Ramirent 67

Net sales

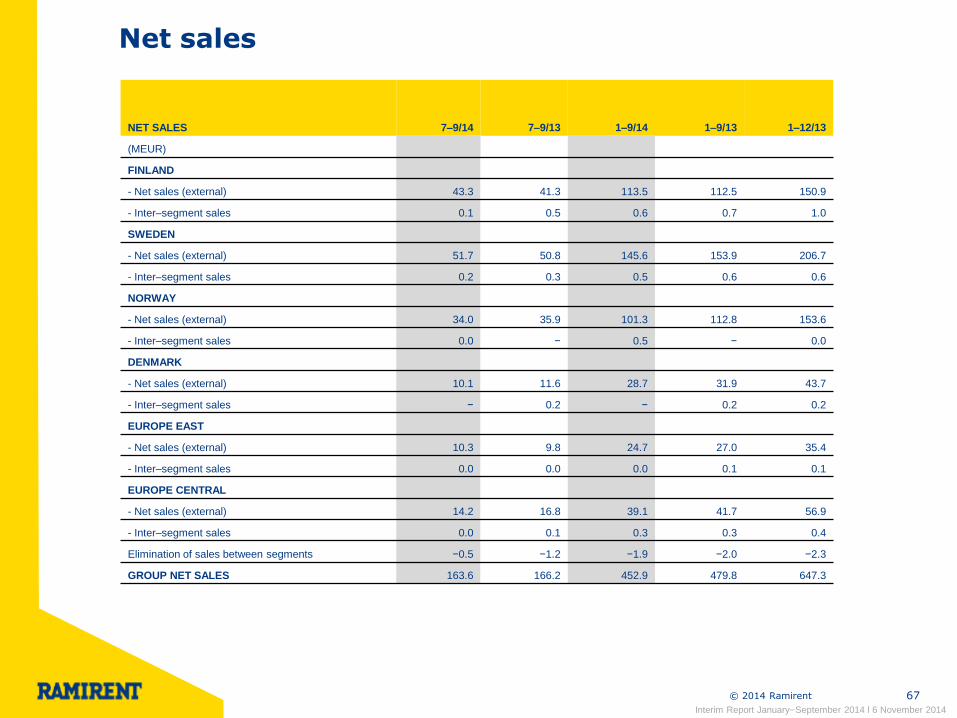

Interim Report January–September 2014 l 6 November 2014

NET SALES 7–9/14

7–9/13

1–9/14

1–9/13

1–12/13

(MEUR)

FINLAND

- Net sales (external) 43.3 41.3 113.5 112.5 150.9

- Inter–segment sales 0.1 0.5 0.6 0.7 1.0

SWEDEN

- Net sales (external) 51.7 50.8 145.6 153.9 206.7

- Inter–segment sales 0.2 0.3 0.5 0.6 0.6

NORWAY

- Net sales (external) 34.0 35.9 101.3 112.8 153.6

- Inter–segment sales 0.0 − 0.5 − 0.0

DENMARK

- Net sales (external) 10.1 11.6 28.7 31.9 43.7

- Inter–segment sales − 0.2 − 0.2 0.2

EUROPE EAST

- Net sales (external) 10.3 9.8 24.7 27.0 35.4

- Inter–segment sales 0.0 0.0 0.0 0.1 0.1

EUROPE CENTRAL

- Net sales (external) 14.2 16.8 39.1 41.7 56.9

- Inter–segment sales 0.0 0.1 0.3 0.3 0.4

Elimination of sales between segments −0.5 −1.2 −1.9 −2.0 −2.3

GROUP NET SALES 163.6 166.2 452.9 479.8 647.3

© 2014 Ramirent 68

EBITA

Interim Report January–September 2014 l 6 November 2014

EBITA 7–9/14

7–9/13

1–9/14

1–9/13

1–12/13

(MEUR)

FINLAND 8.3 10.2 17.2 19.7 25.7

% of net sales 19.0% 24.5% 15.1% 17.4% 16.9%

SWEDEN 8.9 8.6 19.9 25.5 36.6

% of net sales 17.2% 16.8% 13.6% 16.5% 17.6%

NORWAY 4.0 6.3 10.8 19.2 22.0

% of net sales 11.8% 17.6% 10.6% 17.0% 14.3%

DENMARK −0.1 −2.0 −3.0 −3.5 −4.3

% of net sales −1.2% −17.3% −10.4% −11.0% −9.7%

EUROPE EAST 3.7 3.5 4.6 14.6 17.3

% of net sales 35.8% 35.6% 18.5% 53.8% 48.8%

EUROPE CENTRAL 1.6 1.2 1.2 −0.8 −0.7

% of net sales 11.3% 7.0% 3.0% −1.9% −1.2%

Net items not allocated to segments 1.61) −1.8 0.7 −3.4 −4.6

GROUP EBITA 28.0 25.9 51.3 71.2 92.1

% of net sales 17.1% 15.6% 11.3% 14.8% 14.2%

1) Third-quarter net items not allocated to segments amounted to EUR 1.6 (-1.8) million due to reallocation of certain costs incurred in previous periods from

Ramirent Plc to the segments. The reallocated costs have been accrued as expenses in the respective segment for Q3 2014.

© 2014 Ramirent 69

Net sales in 1-9/2013 included business in Russia, Ukraine and Hungary

Net sales: Group, Russia & Ukraine, Hungary

EBITA: Group, Russia & Ukraine, Hungary

Net sales, MEUR Q1/2013 Q2/2013 Q3/2013 Q4/2013 Q1/2014 Q2/2014 Q3/2014

Group as reported 152.8 160.8 166.2 167.5 137.5 151.8 163.6

Russia & Ukraine 4.6

Hungary 1.5 1.7 1.6

Group (excl. Russia, Ukraine & Hungary) 146.7 159.1 164.6 167.5 137.5 151.8 163.6

EBITA, MEUR Q1/2013 Q2/2013 Q3/2013 Q4/2013 Q1/2014 Q2/2014 Q3/2014

Group as reported 22.6 22.7 25.9 20.9 7.1 16.2 28.0

Russia & Ukraine (incl. capital gain) 11.4

Hungary (incl. capital loss) -0.2 0.1 -1.3

Group (excl. Russia, Ukraine & Hungary) 11.4 22.6 27.3 20.9 7.1 16.2 28.0

Interim Report January–September 2014 l 6 November 2014

For further information:

Magnus Rosén, President and CEO, tel. +358 20 750 2845 Jonas Söderkvist, CFO, tel. +358 20 750 3248 Franciska Janzon, IR, tel. +358 20 750 2859

www.ramirent.com