Ralph E Lerner: Taxation I & II.ppt

20

Taxation by Ralph E. Lerner RalphELerner.com [email protected] 590 Madison Ave, New York, NY, 10022 (212) 521-4437 http://www.RalphELerne r.com/

-

Upload

ralph-lerner -

Category

Art & Photos

-

view

89 -

download

0

Transcript of Ralph E Lerner: Taxation I & II.ppt

Taxationby

Ralph E. LernerRalphELerner.com

[email protected] Madison Ave, New York, NY, 10022

(212) 521-4437

http://www.RalphELerner.com/

Casualty Loss – §165(h)

The lower of the fair market value or the cost per item lost less $100 per casualty.

http://www.RalphELerner.com/

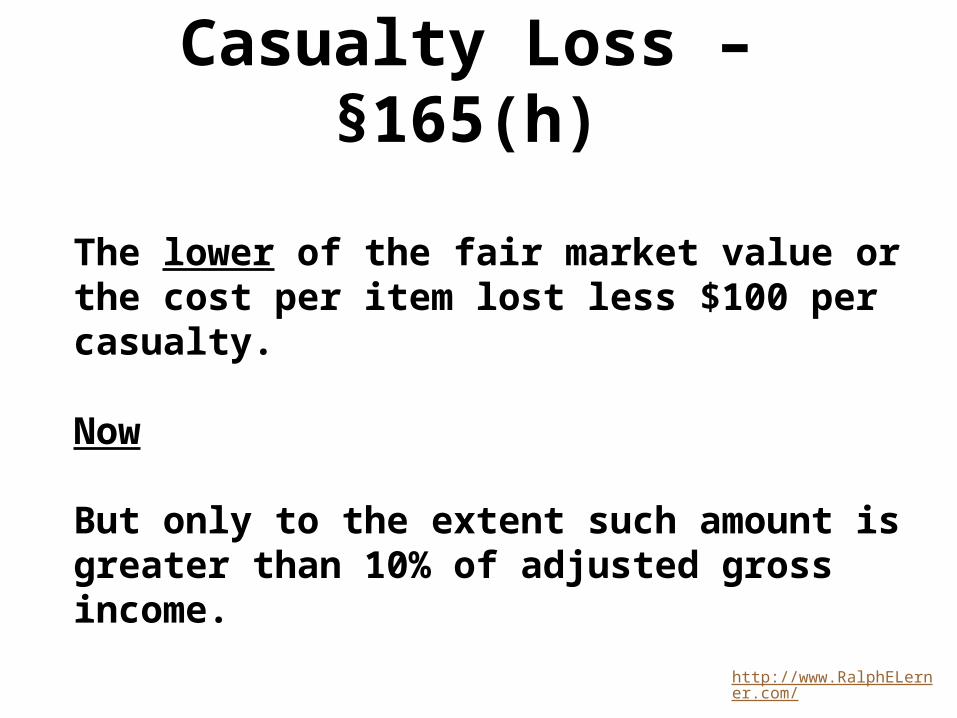

Casualty Loss – §165(h)

The lower of the fair market value or the cost per item lost less $100 per casualty.

Now

But only to the extent such amount is greater than 10% of adjusted gross income.

http://www.RalphELerner.com/

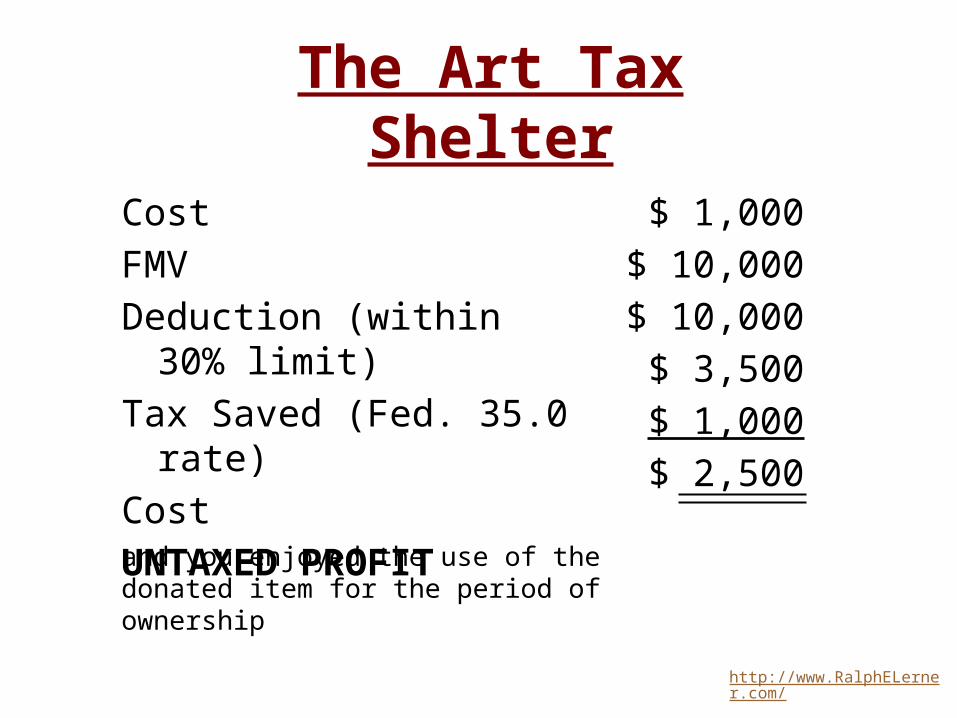

Cost

FMV

Deduction (within 30% limit)

Tax Saved (Fed. 35.0 rate)

Cost

UNTAXED PROFIT

$ 1,000

$ 10,000

$ 10,000

$ 3,500

$ 1,000

$ 2,500

and you enjoyed the use of the donated item for the period of ownership

The Art Tax Shelter

http://www.RalphELerner.com/

The Four Questions

1. What type of donee organization - public charity or private foundation?

http://www.RalphELerner.com/

The Four Questions

1. What type of donee organization - public charity or private foundation?

2. What type of property - ordinary income type property or long-term capital gain type property?

http://www.RalphELerner.com/

1. What type of donee organization - public charity or private foundation?

2. What type of property - ordinary income type property or long-term capital gain type property?

3. Have you satisfied the related-use rule?

The Four Questions

http://www.RalphELerner.com/

The Four Questions

1. What type of donee organization - public charity or private foundation?

2. What type of property - ordinary income type property or long-term capital gain type property?

3. Have you satisfied the related-use rule?

4. Have you obtained a qualified appraisal by a qualified appraiser?

http://www.RalphELerner.com/

FUTURE INTEREST RULE

Section 170(a)(3) - There is no charitable deduction for a gift of a future interest in tangible personal property until there is no intervening interest in, right of possession of, or enjoyment of the property held by the donor, spouse or certain related individuals. http://www.RalphELerner.com/

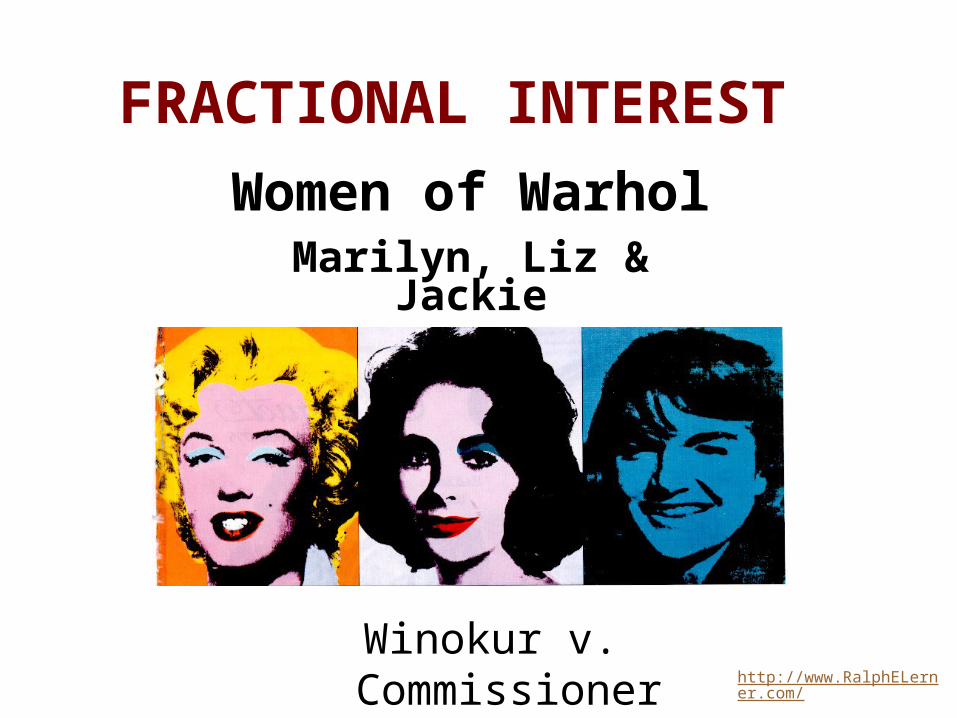

FRACTIONAL INTEREST

Winokur v. Commissioner

Women of WarholMarilyn, Liz & Jackie

http://www.RalphELerner.com/

CHARITABLE REMAINDER TRUST

However, an income tax deduction would be allowed under section 170(a)(3) when the trustee sells the musical instrument.

http://www.RalphELerner.com/

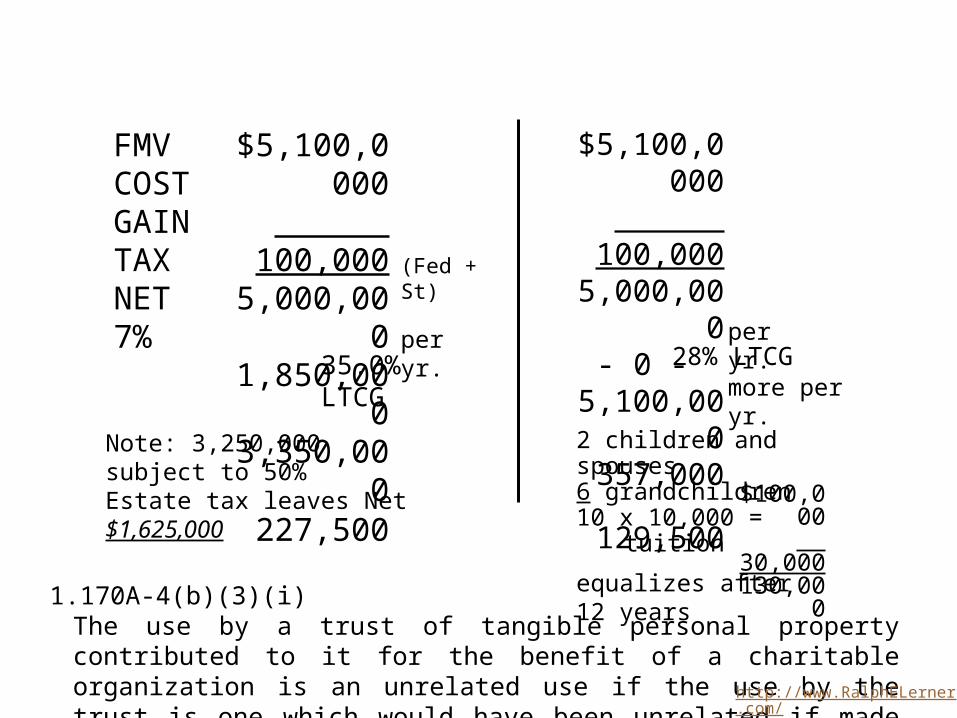

FMVCOSTGAINTAXNET7%

$5,100,0000 100,000

5,000,0001,850,0003,350,000

227,500

$5,100,0000 100,000

5,000,000- 0 -

5,100,000357,000

129,500

per yr.28% LTCG

more per yr.

Note: 3,250,000 subject to 50%Estate tax leaves Net $1,625,000

(Fed + St)

per yr.35.0% LTCG

2 children and spouses6 grandchildren10 x 10,000 =

tuition

equalizes after 12 years

$100,000 30,000130,000

1.170A-4(b)(3)(i)The use by a trust of tangible personal property contributed to it for the benefit of a charitable organization is an unrelated use if the use by the trust is one which would have been unrelated if made by the charitable organization.http://www.RalphELerner.com/

I WANT MY OWN MUSEUM

Private Operating Foundation - Reg. 53.4942(b)-2(a)(6) Ex. 4

http://www.RalphELerner.com/

FAIR MARKET VALUEHypothetical Willing Buyer/

Hypothetical Willing Seller

http://www.RalphELerner.com/

Quedlinburg Treasures

Fair Market Value is determined in the retail market in which the item is most commonly sold to the public.

http://www.RalphELerner.com/

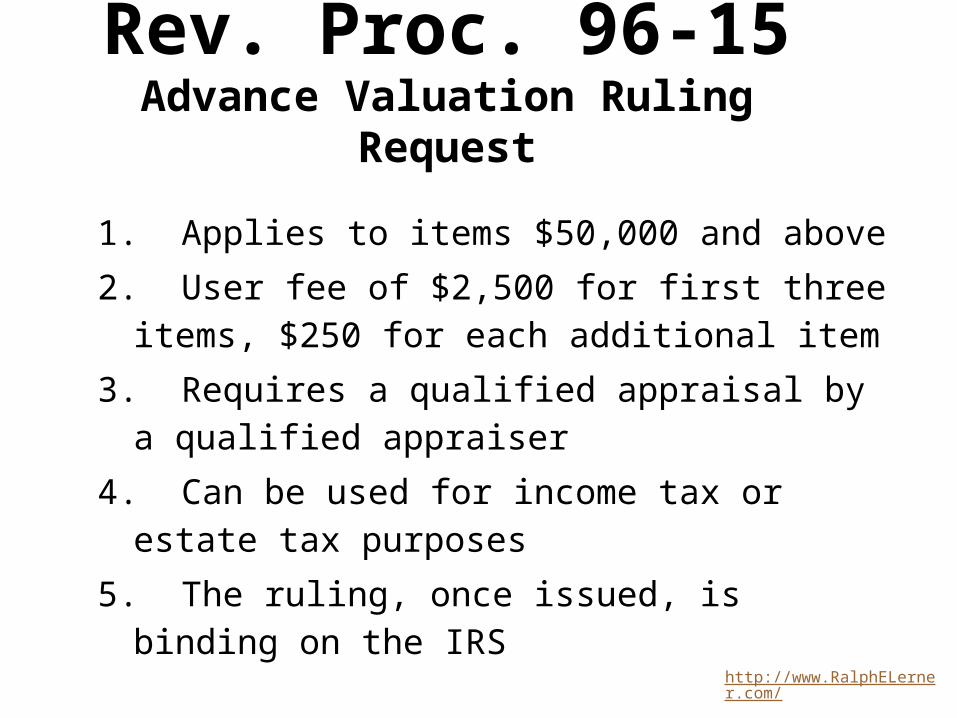

Rev. Proc. 96-15Advance Valuation Ruling Request

1. Applies to items $50,000 and above

2. User fee of $2,500 for first three items, $250 for each additional item

3. Requires a qualified appraisal by a qualified appraiser

4. Can be used for income tax or estate tax purposes

5. The ruling, once issued, is binding on the IRS

http://www.RalphELerner.com/

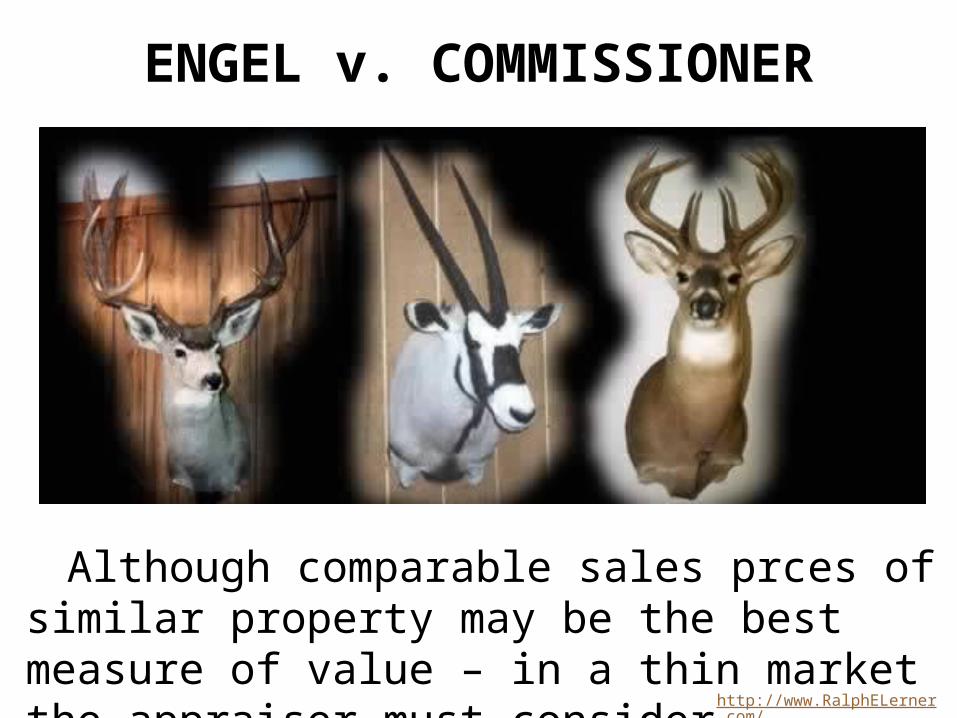

ENGEL v. COMMISSIONER

Although comparable sales prces of similar property may be the best measure of value – in a thin market the appraiser must consider replacement cost.

http://www.RalphELerner.com/

THE FIRST, THEY SAID, SHOULD BE SWEET LIKE LOVE; THE SECOND BITTER, LIKE LIFE; AND THE THIRD SOFT, LIKE DEATH.http://www.RalphELerner.com/

ROTHKO

Avoid Conflicts of Interest

Duty of Loyalty

An executor must care and manage the assets and affairs of the estate as would prudent persons of discretion and intelligence accented by “not honesty alone” but by the punctilio of an honor the most sensitive.

http://www.RalphELerner.com/