Rail, Truck, and Terminal Activity and Outlook – Getting ... · Rail, Truck, and Terminal...

18

Rail, Truck, and Terminal Activity and Outlook – Getting Crude Out April 16, 2013 Brian Freed [email protected] Direct – 214.621.9021

Transcript of Rail, Truck, and Terminal Activity and Outlook – Getting ... · Rail, Truck, and Terminal...

Rail, Truck, and Terminal Activity and Outlook – Getting Crude Out

April 16, 2013

Brian Freed [email protected] Direct – 214.621.9021

2

Forward Looking Statements

This presentation contains forward-looking statements, which are statements that are not historical in nature. Forward-looking statements are subject to certain risks, uncertainties, and assumptions. Should one or more of these risks or uncertainties materialize or any underlying assumption proves incorrect, actual results may vary materially from those anticipated, estimated, or projected. Among the key factors that could cause actual results to differ materially from those referred to in the forward-looking statements are: weather conditions that vary significantly from historically normal conditions; the general level of petroleum product demand and the availability of supply; the demand for high deliverability natural gas storage capacity in the Northeast and Texas; our ability to successfully implement our business plan; the outcome of rate decisions levied by the Federal Energy Regulatory Commission; our ability to generate available cash for distribution to unitholders; and the costs and effects of legal, regulatory, and administrative proceedings against us or which may be brought against us. These and other risks and assumptions are described in NRGY’s and NRGM’s annual reports on Form 10-K and other reports that are available from the United States Securities and Exchange Commission. Readers are cautioned not to place undue reliance on forward-looking statements, which reflect management’s view only as of the date made. We undertake no obligation to update any forward-looking statement, except as otherwise required by law.

NYSE: NRGY, NRGM

Agenda

• Inergy Introduction

• Overview of Bakken Production

• COLT Hub Overview

• Market Dynamics – ND Terminal – rail, pipeline, truck ins /outs – Rail – Where is the volume going? – Impact on Pipeline projects

3

4

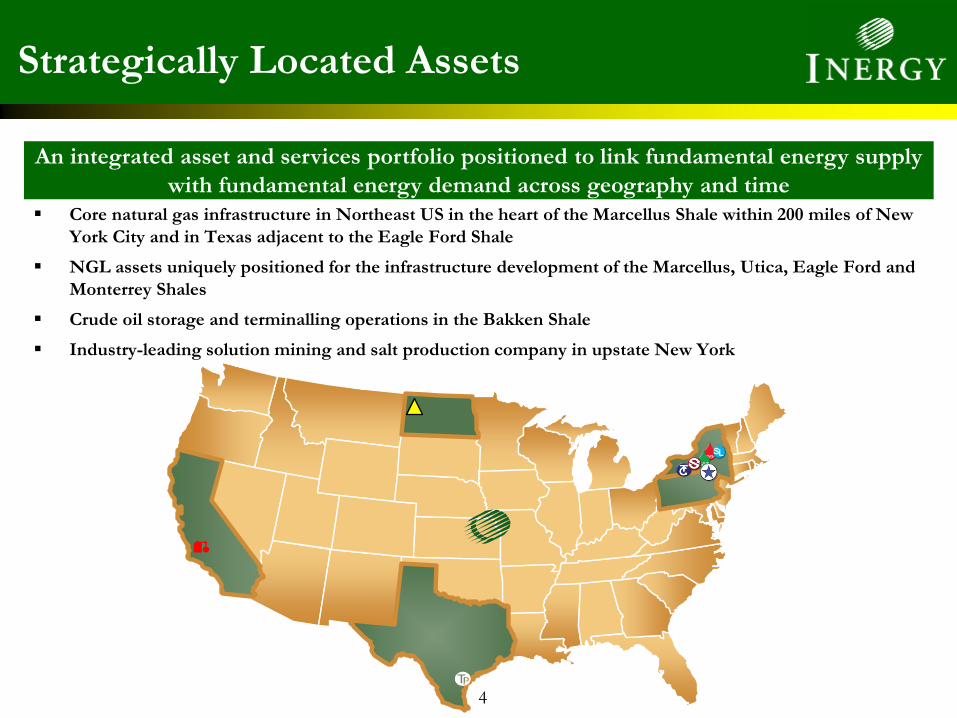

Strategically Located Assets

An integrated asset and services portfolio positioned to link fundamental energy supply with fundamental energy demand across geography and time

Core natural gas infrastructure in Northeast US in the heart of the Marcellus Shale within 200 miles of New York City and in Texas adjacent to the Eagle Ford Shale

NGL assets uniquely positioned for the infrastructure development of the Marcellus, Utica, Eagle Ford and Monterrey Shales

Crude oil storage and terminalling operations in the Bakken Shale

Industry-leading solution mining and salt production company in upstate New York

5

Key Focus Areas

Continue to build out service offerings for customers focusing on long-term contracted, fee-based cash flows

Leverage existing relationships to expand into additional shale plays and serve premium markets

“Blocking and Tackling” – deliver consistent operational and financial performance

Identify and execute on-time, on-budget capital expansions around existing asset base

Execute on organic commercial opportunities

Pursue complementary midstream opportunities

Evaluate capital structure for ways to most efficiently finance growth

Deliver Operational Excellence Disciplined Growth Strategy

6

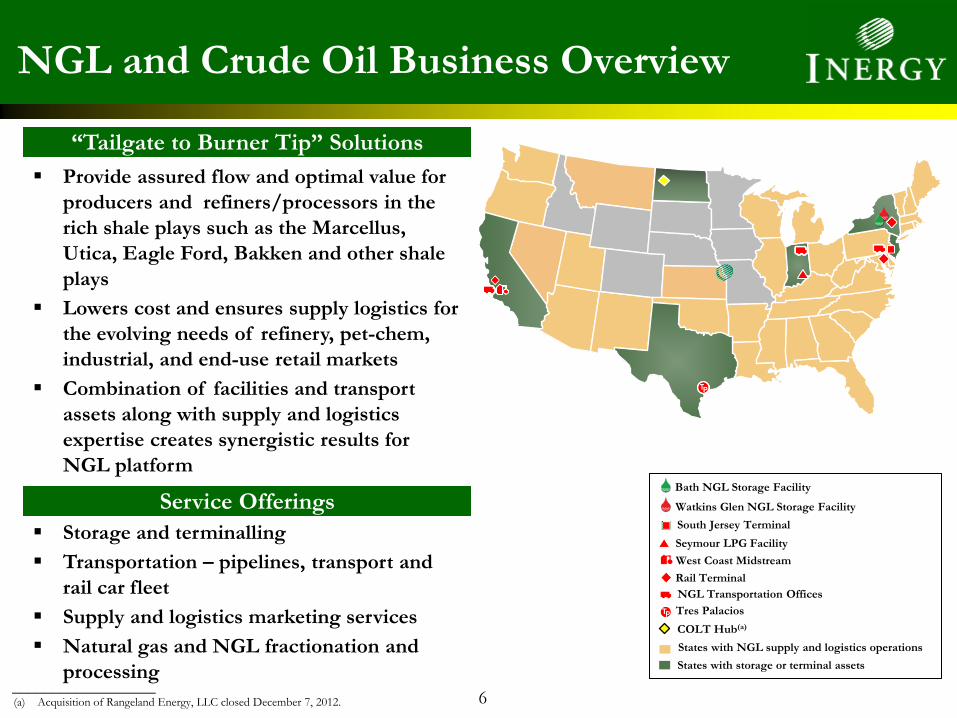

NGL and Crude Oil Business Overview

“Tailgate to Burner Tip” Solutions

Provide assured flow and optimal value for producers and refiners/processors in the rich shale plays such as the Marcellus, Utica, Eagle Ford, Bakken and other shale plays

Lowers cost and ensures supply logistics for the evolving needs of refinery, pet-chem, industrial, and end-use retail markets

Combination of facilities and transport assets along with supply and logistics expertise creates synergistic results for NGL platform

Service Offerings

Storage and terminalling Transportation – pipelines, transport and

rail car fleet Supply and logistics marketing services Natural gas and NGL fractionation and

processing

Watkins Glen NGL Storage Facility

Bath NGL Storage Facility

South Jersey Terminal Seymour LPG Facility West Coast Midstream

NGL Transportation Offices Rail Terminal

Tres Palacios COLT Hub(a)

States with NGL supply and logistics operations States with storage or terminal assets

__________________ (a) Acquisition of Rangeland Energy, LLC closed December 7, 2012.

Bakken Crude Oil Production – 2 Million?

7

Bentek projects Bakken production to surpass 1.7 MMBD in 2017 and 2.1 MMBD in 2025 in their base case forecast (2.1 and 2.7 respectively in the high case)

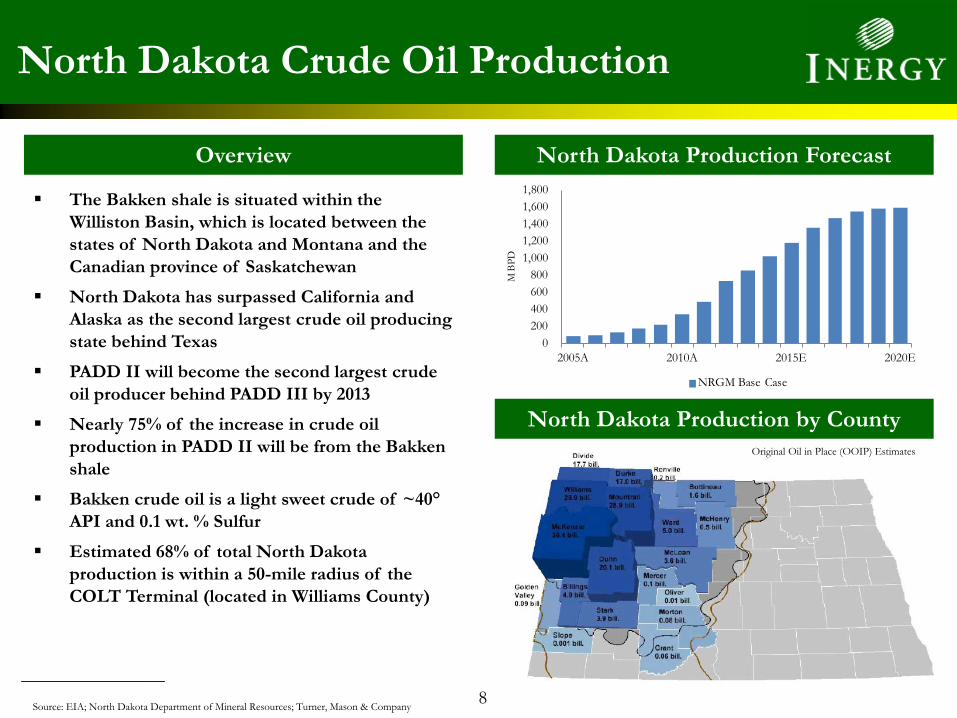

The Bakken shale is situated within the Williston Basin, which is located between the states of North Dakota and Montana and the Canadian province of Saskatchewan

North Dakota has surpassed California and Alaska as the second largest crude oil producing state behind Texas

PADD II will become the second largest crude oil producer behind PADD III by 2013

Nearly 75% of the increase in crude oil production in PADD II will be from the Bakken shale

Bakken crude oil is a light sweet crude of ~40° API and 0.1 wt. % Sulfur

Estimated 68% of total North Dakota production is within a 50-mile radius of the COLT Terminal (located in Williams County)

8

North Dakota Crude Oil Production

Overview North Dakota Production Forecast

North Dakota Production by County

Source: EIA; North Dakota Department of Mineral Resources; Turner, Mason & Company

Original Oil in Place (OOIP) Estimates

__________________

0 200 400 600 800

1,000 1,200 1,400 1,600 1,800

2005A 2010A 2015E 2020E

M B

PD

NRGM Base Case

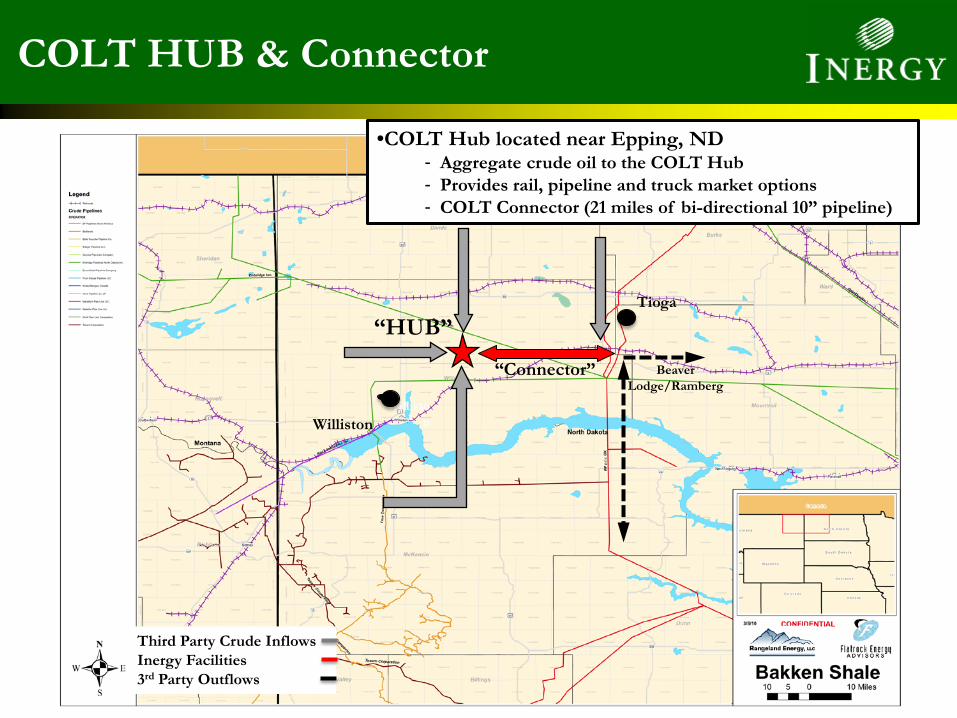

COLT HUB & Connector

“HUB”

•COLT Hub located near Epping, ND - Aggregate crude oil to the COLT Hub - Provides rail, pipeline and truck market options - COLT Connector (21 miles of bi-directional 10” pipeline)

Tioga

“Connector”

Williston

Beaver Lodge/Ramberg

Third Party Crude Inflows Inergy Facilities 3rd Party Outflows

Williston

10

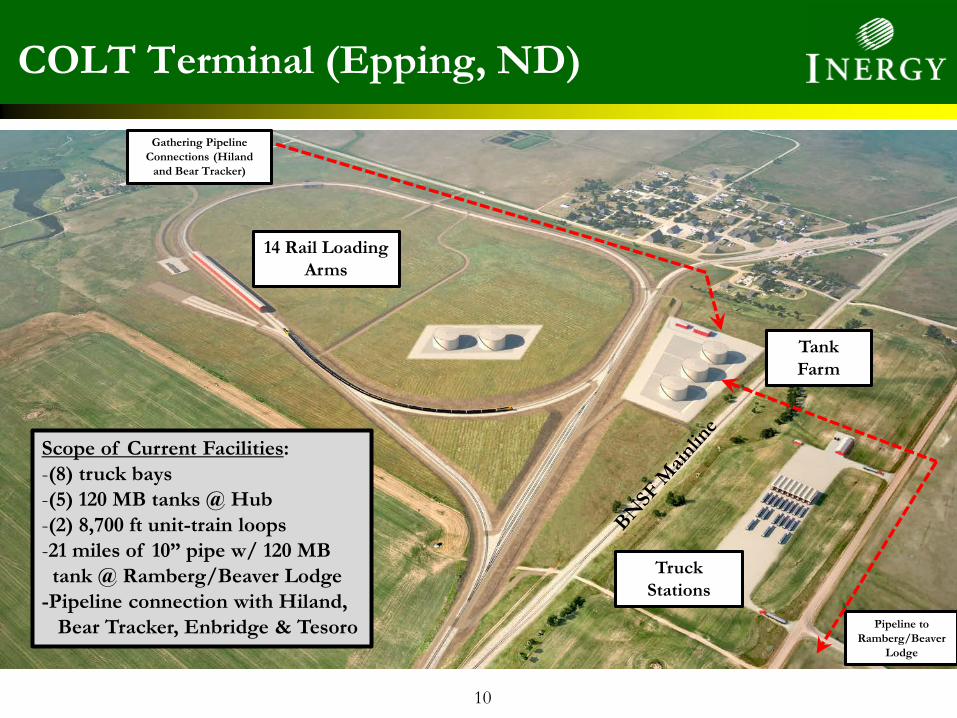

COLT Terminal (Epping, ND)

BNSF RAILWAY

Truck Stations

Tank Farm

14 Rail Loading Arms

Pipeline to Ramberg/Beaver

Lodge

Scope of Current Facilities: -(8) truck bays -(5) 120 MB tanks @ Hub -(2) 8,700 ft unit-train loops -21 miles of 10” pipe w/ 120 MB tank @ Ramberg/Beaver Lodge -Pipeline connection with Hiland, Bear Tracker, Enbridge & Tesoro

Gathering Pipeline Connections (Hiland

and Bear Tracker)

11

COLT Hub Asset Overview

Located in Epping, ND Commenced commercial operation in May 2012 120,000 BPD rail loading capacity

− Double rail loop − Connected to the Burlington Northern Santa Fe rail system

Truck unloading facility with capacity of 64,000 BPD

600,000 Bbl of dedicated customer storage capacity

21-mile, 10” bi-directional pipeline (COLT Connector) connects COLT Terminal to Dry Fork Terminal

Interconnected with Hiland gathering system Interconnect with Bear Tracker gathering system

Dry Fork Terminal Overview

Located at the intersection of four major pipelines at the Beaver Lodge/Ramberg pipeline hub

Crude oil metering and pipeline interconnection facilities allow transfer to: − Tesoro High Plains pipeline − Enbridge North Dakota pipeline

120,000 Bbl of working storage capacity Potential interconnections with Hess, Hiland

Crude and other pipelines

COLT Terminal Overview

Strictly Confidential 12

COLT Sourcing/Takeaway

Maximum Sourcing Capacity Maximum Takeaway Capacity

Sourcing Description COLT Connector 75,000 BPD capacity 21 mile,

10” bi-directional pipeline

Truck Bays 64,000 BPD current capacity, addition of 4 racks to 96,000 BPD

Hiland Interconnect (formerly Banner)

35,000 BPD current capacity, adding 1 mile of 8” pipe for additional 25,000 BPD

Meadowlark (formerly Bear Tracker)

40,000 BPD expected capacity, 10” pipeline

Takeaway Description Rail 120,000 BPD current capacity,

upgrading to 160,000 BPD

Hiland Pipeline 35,000 BPD capacity; bi-directional

COLT Connector 75,000 BPD capacity pipeline with interconnects at Dry Fork to:

Tesoro Pipeline 60,000 BPD capacity; bi-directional

Enbridge Pipeline 15,000 BPD capacity

Growth project capacity increases shown in yellow

Point of Liquidity

Largest Bakken

Merchant Crude Hub

Integrated network of railcar, pipeline and storage creates optimal source of liquidity and export optionality to optimal crude markets for customers – Railcar transportation provides only means of accessing PADD I and PADD V markets – COLT connector pipeline promotes access to central corridor and intra-region flexibility

Largest storage capacity in the Bakken with room for significant additional tankage Pipeline interconnections with major export lines and intra-regional lines provide sourcing and takeaway flexibility Creates a point of liquidity for Bakken crude oil production by bringing together multiple buyers and sellers

Hub and Spoke

Inergy has built a true “Hub” with multiple ingress and egress “Spokes,” centered around a large battery of tanks – Pipeline provides interconnection with two primary systems (Enbridge and Tesoro) – Interconnection agreements completed – Banner, Tesoro , Enbridge and Bear Tracker – Future connections with other pipelines

Working storage capacity of 720,000 Bbl currently enables the movement of up to 120,000 Bbl/d via rail, 75,000 Bbl/d via COLT Connector pipeline and 64,000 Bbl/d via tanker trucks

Size and scale of COLT will attract crude in a state where 75% of crude gathering still occurs via tanker truck

Via COLT, the COLT connector and its connections, customers have access to Guernsey, Clearbrook, Cushing, the Gulf Coast and PADD I & V refineries

Inergy’s integrated network will be a permanent fixture as the premiere Bakken hub, providing a point of liquidity by bringing together multiple buyers and sellers.

• Current Inbound to COLT – 60% Pipeline, 40% Truck – Truck Unloading – 8 truck racks – COLT Connector – 10” bi-directional with flows mostly into COLT

from Dry Fork (Ramberg/Beaver Lodge) – Hiland – Currently only receipts into COLT – Meadowlark (Bear Tracker) not yet in-service – Pipeline percentages are expected to continue to grow

• Current Outbound from COLT – 99.x% Rail – Rail loading – Enbridge (Beaver Lodge) – Tesoro High Plains (Ramberg) – bi-directional flow – Hiland deliveries awaiting market demand – Truck Loading

14

Terminal - rail, pipeline, truck ins/outs

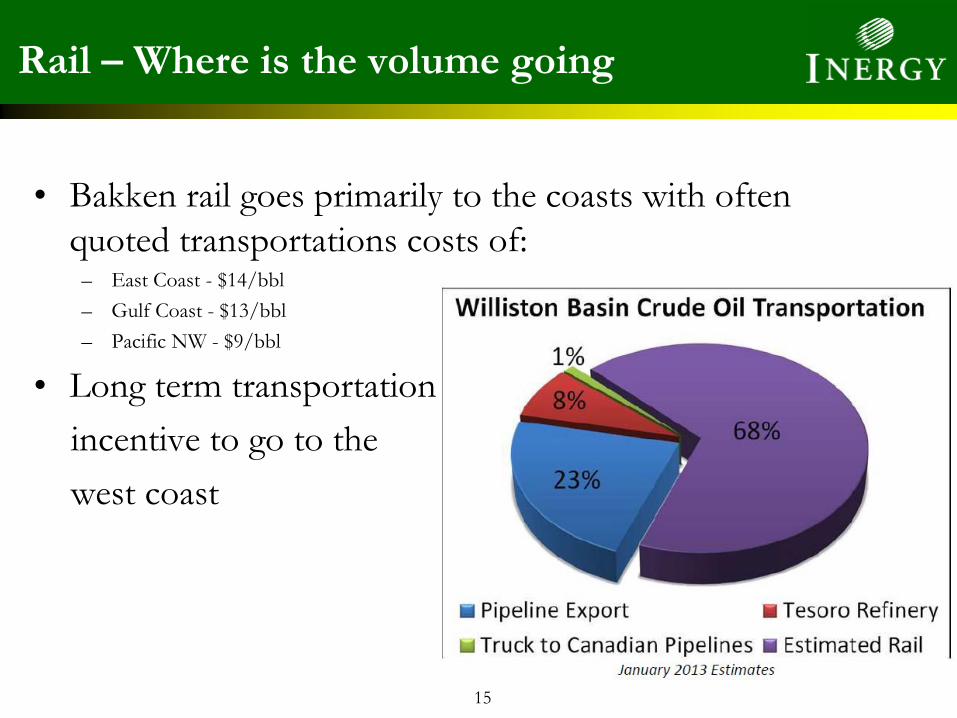

• Bakken rail goes primarily to the coasts with often quoted transportations costs of:

– East Coast - $14/bbl – Gulf Coast - $13/bbl – Pacific NW - $9/bbl

• Long term transportation incentive to go to the west coast

15

Rail – Where is the volume going

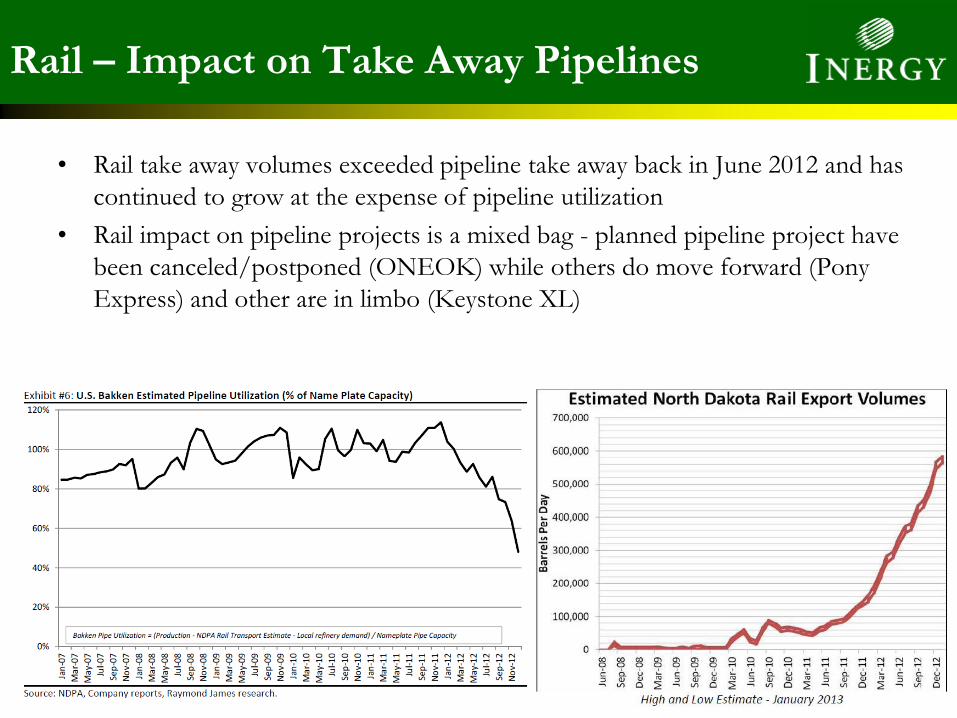

• Rail take away volumes exceeded pipeline take away back in June 2012 and has continued to grow at the expense of pipeline utilization

• Rail impact on pipeline projects is a mixed bag - planned pipeline project have been canceled/postponed (ONEOK) while others do move forward (Pony Express) and other are in limbo (Keystone XL)

16

Rail – Impact on Take Away Pipelines

17

Questions?

18

North American Crude Oil Pipelines

No existing or planned pipeline access to PADD V from Bakken

No significant existing or planned pipeline access to PADD I

Constraint Points

Petroleum Administration for Defense Districts (U.S) Major U.S. Crude Oil Pipelines Major Canadian Crude Oil Pipelines

Proposed Keystone XL

Source: Canadian Association of Petroleum Producers, June 2011

74% of PADD V refinery inputs are imported (a)

96% of PADD I refinery inputs are imported

__________________ (a) Alaska is included with imported totals for PADD V.