Quiz 3 solution sketches

21

Quiz 3 solution sketches 1:00 Lecture, Version A Note for multiple-choice questions: Choose the closest answer

description

Quiz 3 solution sketches. 1:00 Lecture, Version A Note for multiple-choice questions: Choose the closest answer. Finite PV. - PowerPoint PPT Presentation

Transcript of Quiz 3 solution sketches

Quiz 3 solution sketches

1:00 Lecture, Version A

Note for multiple-choice questions: Choose the closest

answer

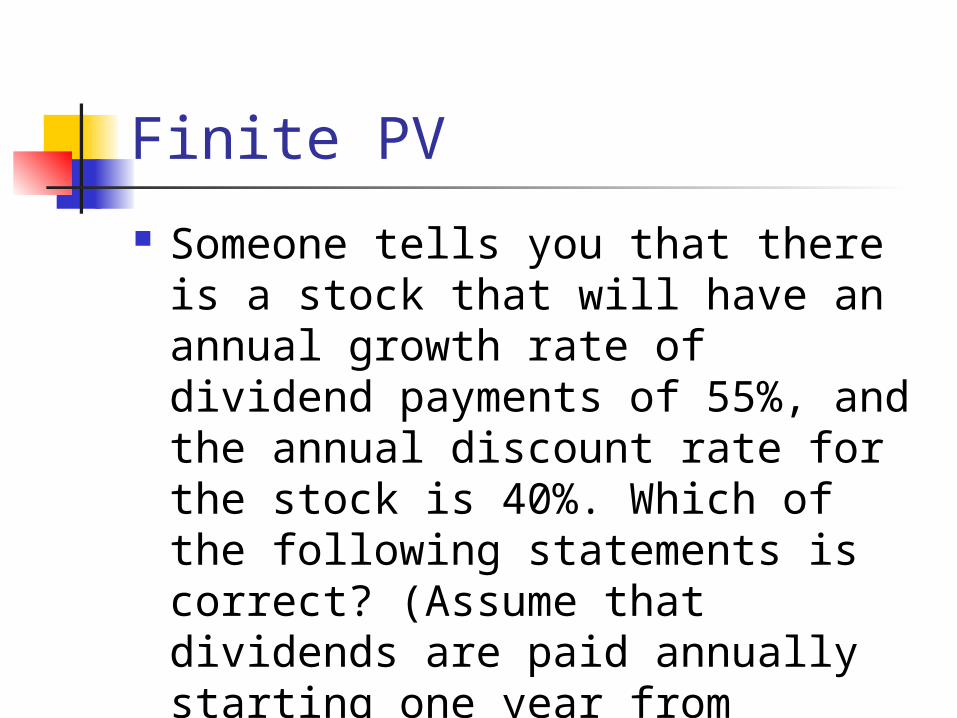

Finite PV Someone tells you that there is a

stock that will have an annual growth rate of dividend payments of 55%, and the annual discount rate for the stock is 40%. Which of the following statements is correct? (Assume that dividends are paid annually starting one year from today.)

Finite PV A: The stock is finitely valued if we

assume that dividends will be paid forever. No (g>r means infinite PV of

perpetuity) B: The stock is finitely valued if we

assume that dividends will be paid only for 100 years. Yes (each PV is finite)

Finite PV C: No stock can ever have dividend

growth of 55% from one year to the next. No, high growth rate is possible in any

year D: The PV of the stock is $0.

No, PV is positive since the dividend>0.

E: Both (A) and (B) No, because (A) is false.

Sample Standard Deviation A sample of 3 stocks has rates of

return of 8%, 5%, and 2%. What is the standard deviation of this sample? Avg = (8 + 5 + 2)/3 = 5% Variance

= 1/2*[(.08-.05)2 + (.05-.05)2 + (.02-.05)2]= 1/2*[.0018] = .0009

S.D. = (.0009)1/2 = .03 S.D. = 3%

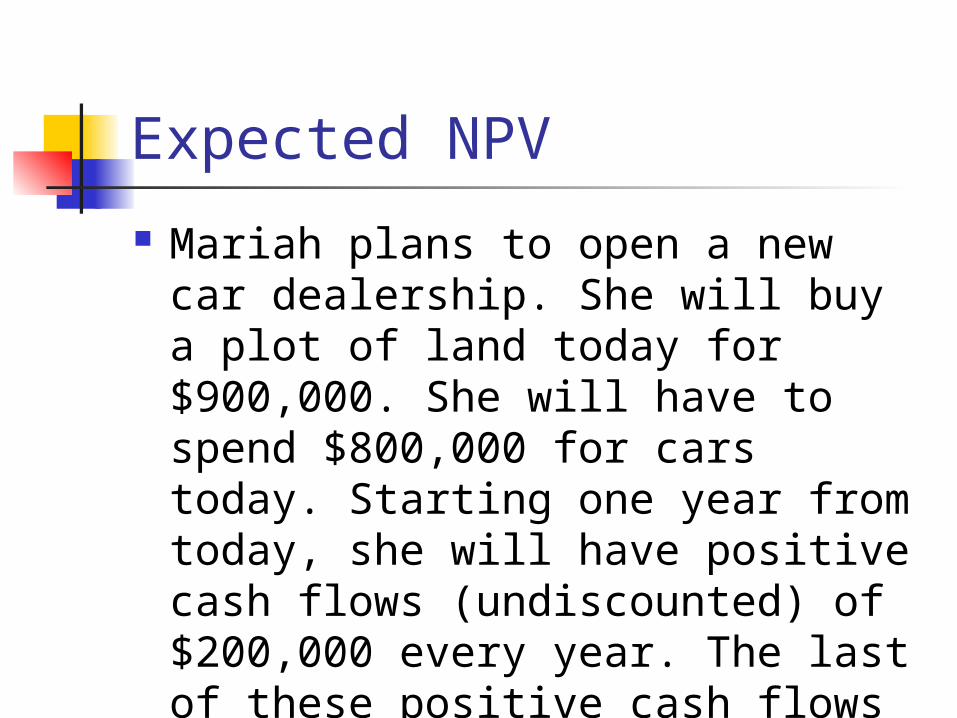

Expected NPV Mariah plans to open a new car

dealership. She will buy a plot of land today for $900,000. She will have to spend $800,000 for cars today. Starting one year from today, she will have positive cash flows (undiscounted) of $200,000 every year. The last of these positive cash flows will be 10 years from today.

Expected NPV There is a clause in the contract

that 10 years from today, the land must be sold to a university. If economic times are good, the plot will sell for $2 million. If not, the plot must be sold for $900,000. If the effective annual discount rate is 5% and you believe the probability of good economic times is 50%, what is the NPV of this investment?

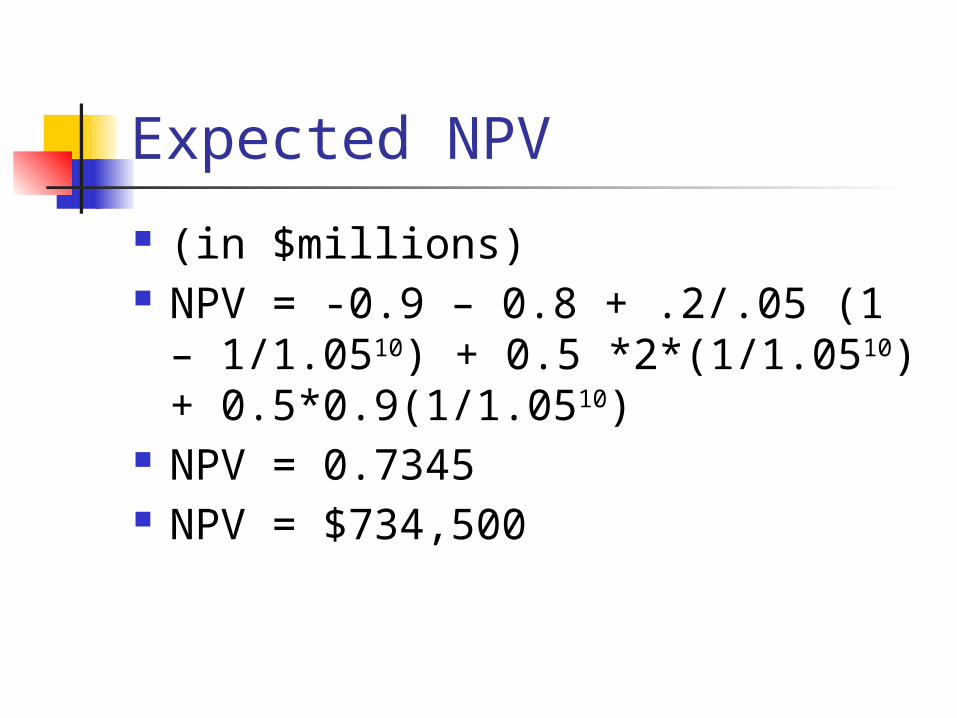

Expected NPV (in $millions) NPV = -0.9 – 0.8 + .2/.05 (1 –

1/1.0510) + 0.5 *2*(1/1.0510) + 0.5*0.9(1/1.0510)

NPV = 0.7345 NPV = $734,500

Semiannual Bond Coupons A bond pays coupons of $60

annually, starting six months from today, until the bond matures (with the last coupon on the maturity date). The bond will mature 3½ years from today and pay a face value of $500. What is the PV of this bond if the appropriate effective annual interest rate for this bond is 8%?

Semiannual Bond Coupons PV = 60/(1.08)1/2 + 60/(1.08)3/2 +

60/(1.08)5/2 + 560/(1.08)7/2 PV = $588.46

Zero-Coupon Bond Value A zero-coupon bond will mature 5

years from today. The promised payment at maturity is $10,000. The current market rate (as an effective annual interest rate) is 12%. What is the current value of owning this bond? X * (1.12)5 = 10,000 X = 10,000/(1.12)5

X = $5674.27

Change in Bond Value You currently own a zero-coupon

bond with maturity date in 18 months. The bond will pay $3,000 on the maturity date. The effective annual rate of return for this bond at the beginning of today is 9%. At the end of the day the rate drops to 8%. How much does the value of the bond change today?

Change in Bond Value PV @ 9% = 3000/(1.09)3/2 =

$2,636.22 PV @ 8% = 3000/(1.08)3/2 =

$2,672.92 r decreases PV increases Change in PV = 2672.92 – 2636.22 Change in PV = $36.70

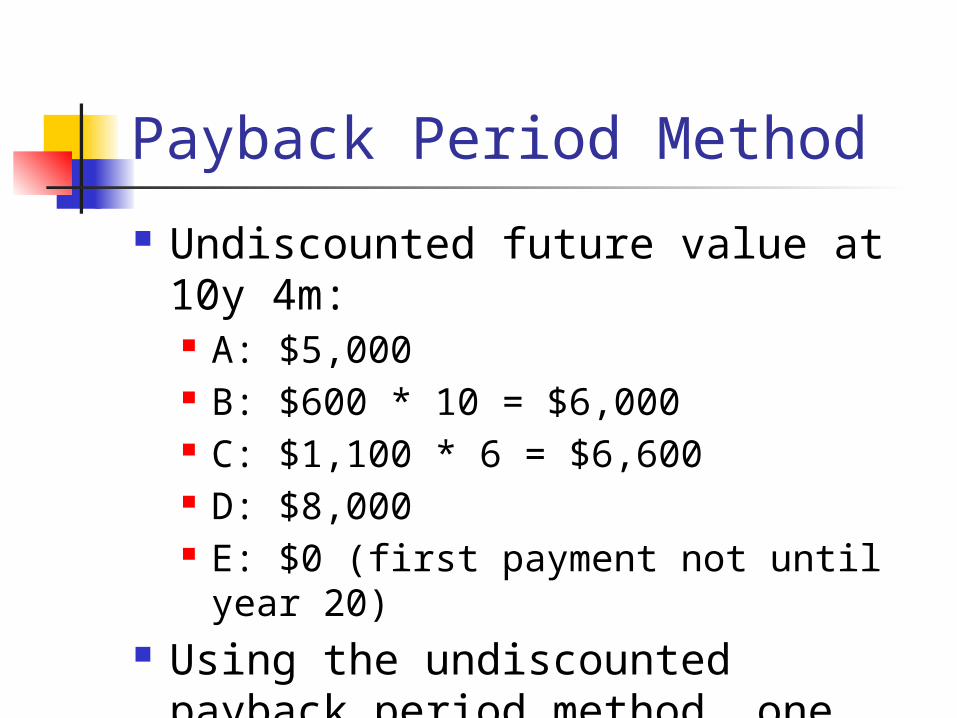

Payback Period Method Use the undiscounted payback

period method, with the cutoff date 10 years, 4 months from now. (In other words, the payback period is 10 years, 4 months.) The effective annual discount rate is 37.934%. Which of the following offers should be picked if someone uses this method?

Payback Period Method A: A one-time payment of $5,000

today B: $600 every year forever,

starting 1 year from now C: $1,100 every 2 years, starting

today D: $8,000 every 10 years, starting

8 years from now E: $20,000 every 20 years, starting

11 years from now

Payback Period Method Undiscounted future value at 10y

4m: A: $5,000 B: $600 * 10 = $6,000 C: $1,100 * 6 = $6,600 D: $8,000 E: $0 (first payment not until year 20)

Using the undiscounted payback period method, one should choose option D

Price-to-Earnings Ratio Stocks A and B have the same

annual discount rate, and would each pay the same dividend if they acted as cash cows. Stock A has no growth opportunities with positive NPV. Stock B has many growth opportunities with positive NPV. Which of the following statements is true if both companies maximize the value of their stock?

Price-to-Earnings Ratio A: Stock A will have a lower price-to-

earnings ratio than Stock B B: Stock A will have a higher price-to-

earnings ratio than Stock B C: Both stocks will have the same price-

to-earnings ratio D: Stock A will have a higher price-to-

earnings ratio than Stock B if the growth opportunities are small enough

E: None of the above

Price-to-Earnings Ratio Price per share / Earnings per share

= 1/R + NPVGO/EPS 1/R is positive and the same for

both NPVGO is positive for B and zero

for A A’s P-E ratio < B’s P-E ratio, so the

correct response is A

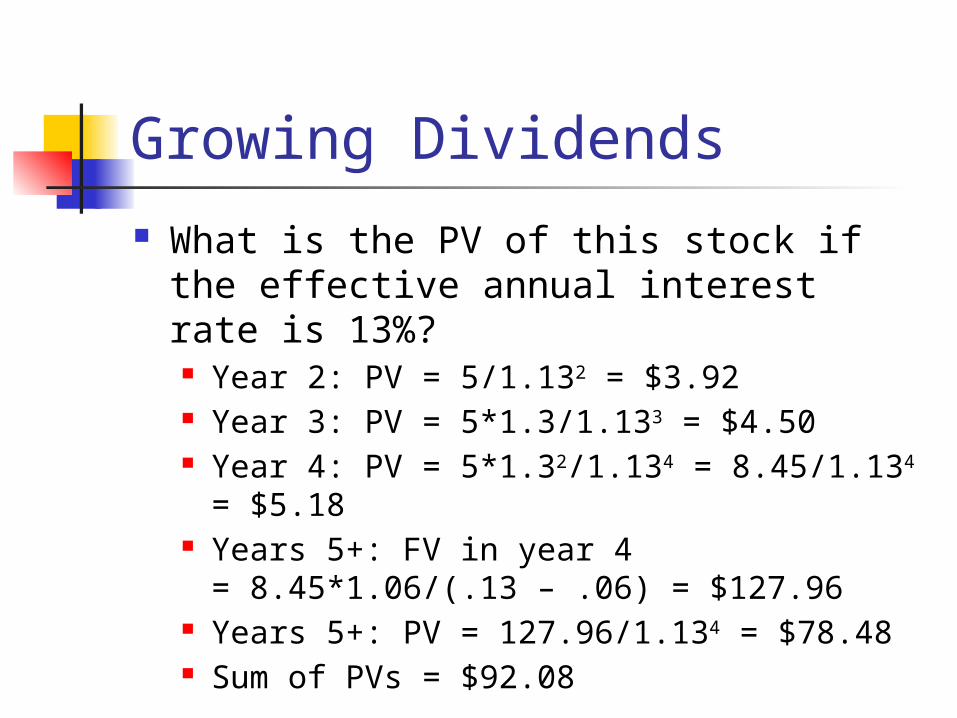

Growing Dividends Goliath Galloping Ghost, Inc. will

pay its first dividend two years from today, and will pay annually thereafter forever. The first dividend payment (in 2 years) is $5 per share. Each of the next two dividend payments will be 30% higher than the previous payment. After that, dividend payments will grow at 6% per year forever.

Growing Dividends What is the PV of this stock if the

effective annual interest rate is 13%? Year 2: PV = 5/1.132 = $3.92 Year 3: PV = 5*1.3/1.133 = $4.50 Year 4: PV = 5*1.32/1.134 = 8.45/1.134 =

$5.18 Years 5+: FV in year 4

= 8.45*1.06/(.13 – .06) = $127.96 Years 5+: PV = 127.96/1.134 = $78.48 Sum of PVs = $92.08