Quarterly Q1, 2017 Content Review - Ultra...

6

Content Review · The last quarter of the old year leſt nothing to desire… Outlook/Equities · As already outlined, a look at the US mood barometer… Currencies · The active and successful management of curren- cies should again… Interest Rates/Bonds · From the vantage point of the present the trend towards rising… Commodities · We anticipate that oil and industrial metals will first move… Quarterly Q1, 2017 g 1 Review The last quarter of the old year leſt nothing to desire. The unexpected confidence following the election of Donald Trump as the new and 45 th President of the Unites States, resulted in a strong upward move of equity markets. Since the financial crisis 2008 all central banks have, with enormous monetary funds, tried everything to increase the growth rates of the respective economies, while simultaneously fighting deflationary forces. Many financial assets (equities, bonds, real estate, etc.) profited from this policy, whilst mainly lower income workers, but also, at an increasing level, midd- le-class citizens fell by the wayside and where not able to profit from this development. Statements by the President-elect that large infrastructure projects and tax reductions whe- re planned to stimulate the economy where enough to trigger a turnaround in interest rates, currencies and equity markets. A move from monetary measures alone to a direct intervention based on the ideas mentioned above, was already being discussed by experts long before Trumps election, however they were never implemented. Investors have over the past few weeks clearly indicated their optimism and are showing great hope for a stronger world economy. If we also share this optimism will be outlined on the following pages. (Fig. 1) Source: UBS Technical Research Quelle: Thomson Reuters Datastream As already outlined, a look at the US mood ba- rometer (Fig.1) clearly indicates that investors have started the New Year with a large portion of optimism. Outlook/Equities Low percentage of neutral investors suggests the market is very convinced about its 2017 outlook

Transcript of Quarterly Q1, 2017 Content Review - Ultra...

Content

Review· The last quarter of the

old year left nothing to desire…

Outlook/Equities· As already outlined,

a look at the US mood barometer…

Currencies· The active and successful

management of curren-cies should again…

Interest Rates/Bonds· From the vantage point

of the present the trend towards rising…

Commodities · We anticipate that oil

and industrial metals will first move…

Quarterly Q1, 2017

g1

ReviewThe last quarter of the old year left nothing to desire. The unexpected confidence following the election of Donald Trump as the new and 45th President of the Unites States, resulted in a strong upward move of equity markets.

Since the financial crisis 2008 all central banks have, with enormous monetary funds, tried everything to increase the growth rates of the respective economies, while simultaneously fighting deflationary forces. Many financial assets (equities, bonds, real estate, etc.) profited from this policy, whilst mainly lower income workers, but also, at an increasing level, midd-le-class citizens fell by the wayside and where not able to profit from this development.

Statements by the President-elect that large infrastructure projects and tax reductions whe-re planned to stimulate the economy where enough to trigger a turnaround in interest rates, currencies and equity markets. A move from monetary measures alone to a direct intervention based on the ideas mentioned above, was already being discussed by experts long before Trumps election, however they were never implemented.

Investors have over the past few weeks clearly indicated their optimism and are showing great hope for a stronger world economy. If we also share this optimism will be outlined on the following pages.

(Fig. 1)

Source: UBS Technical ResearchQuelle: Thomson Reuters Datastream

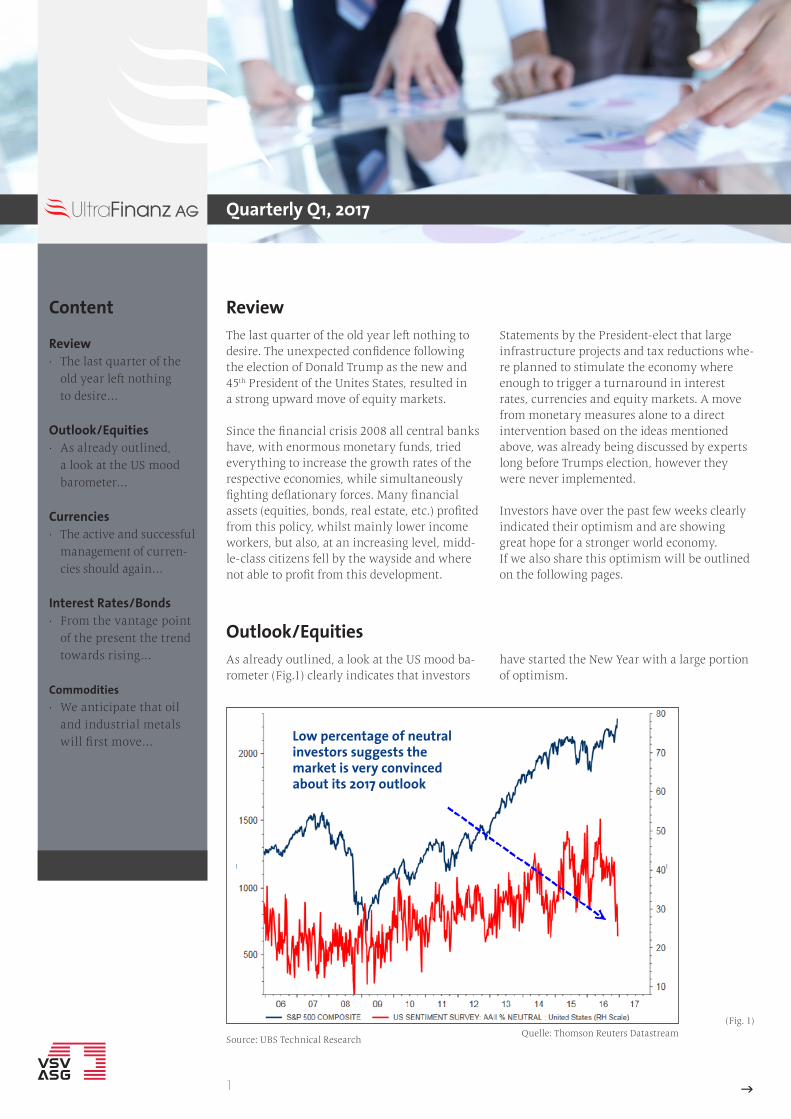

As already outlined, a look at the US mood ba-rometer (Fig.1) clearly indicates that investors

have started the New Year with a large portion of optimism.

Outlook/Equities

Low percentage of neutral investors suggests the market is very convinced about its 2017 outlook

Quarterly Q1, 2017

2 g

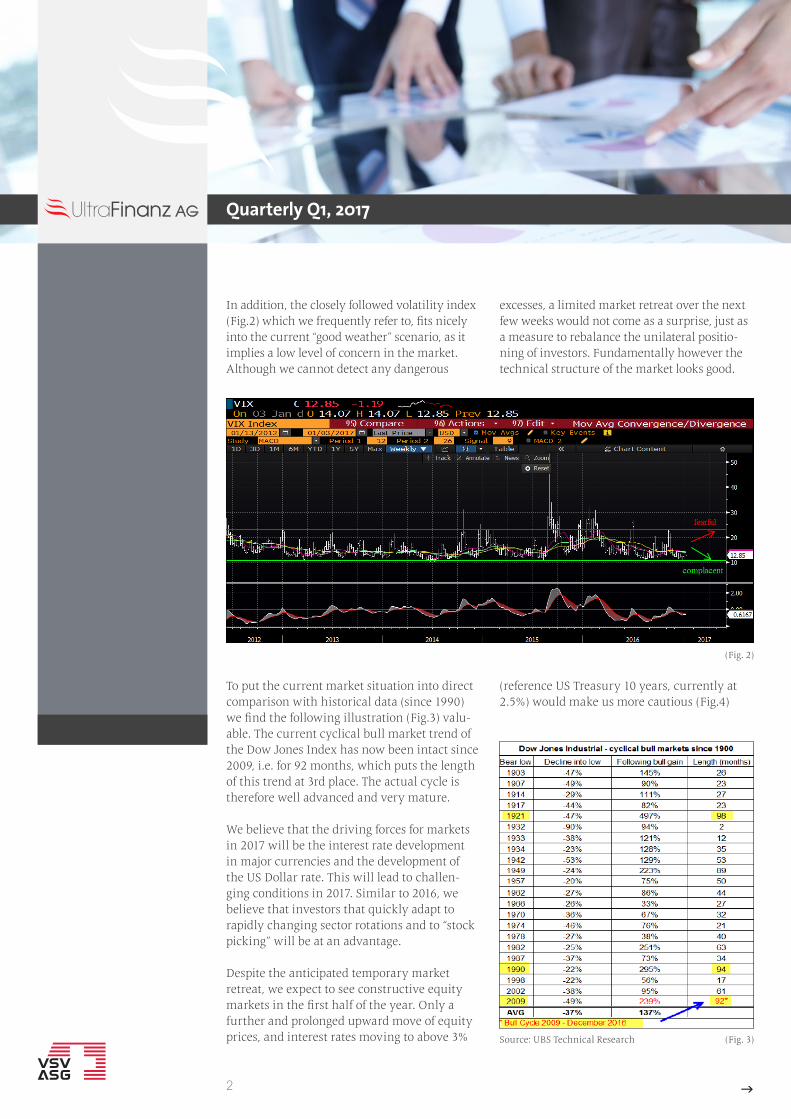

In addition, the closely followed volatility index (Fig.2) which we frequently refer to, fits nicely into the current “good weather” scenario, as it implies a low level of concern in the market. Although we cannot detect any dangerous

excesses, a limited market retreat over the next few weeks would not come as a surprise, just as a measure to rebalance the unilateral positio-ning of investors. Fundamentally however the technical structure of the market looks good.

(Fig. 2)

To put the current market situation into direct comparison with historical data (since 1990) we find the following illustration (Fig.3) valu-able. The current cyclical bull market trend of the Dow Jones Index has now been intact since 2009, i.e. for 92 months, which puts the length of this trend at 3rd place. The actual cycle is therefore well advanced and very mature.

We believe that the driving forces for markets in 2017 will be the interest rate development in major currencies and the development of the US Dollar rate. This will lead to challen-ging conditions in 2017. Similar to 2016, we believe that investors that quickly adapt to rapidly changing sector rotations and to “stock picking” will be at an advantage.

Despite the anticipated temporary market retreat, we expect to see constructive equity markets in the first half of the year. Only a further and prolonged upward move of equity prices, and interest rates moving to above 3% (Fig. 3)Source: UBS Technical Research

(reference US Treasury 10 years, currently at 2.5%) would make us more cautious (Fig.4)

Quarterly Q1, 2017

3 g

Based on a scenario of continued and impro-ving growth in the economic environment, led by the USA and together with higher com-modity prices, we expect inflation to increa-se, interest rates to rise and therefore the US Dollar to strengthen. The populist moves that are to be seen in many countries could have a further inflationary effect. Greater control of immigration, higher custom duties, increased infrastructure spending and tax reductions, coupled with a stronger influence of the work-force on prices (mainly in the USA) are just a few of the driving factors. Therefore, equities should fare better this year than bonds, as they offer a better protection against rising inflation.

Apart from our core holdings in Switzerland and Germany, we will choose a very opportu-nistic investment approach as we – as already

mentioned – expect short-term and strong price fluctuations in the markets. Inflexible asset allocations would prevent our flexibility and also lengthen our reaction times.

In an environment of rising interest rates, we are placing emphasis on financial assets that will profit from increased margins. American financial equities seem at first glance to look more attractive, but European shares have a greater catch-up potential even though not all law cases have yet been settled.

We are looking for companies that will profit from a widely diversified economic recovery. From a relative point of view, and because of the weaker EUR, we believe that European markets are in a good position for the first half of the year. We liquidated our investment in Japan for tactical reasons, as the recent

(Fig. 4)Source: UBS Technical Research

Make or break … a test of 3.00% in 2017 is very likely !!

Quarterly Q1, 2017

4 g

(Fig. 5)

strength of the Japanese equity market was based practically solely on the weakness of the Yen. A market that reacts so strongly to currency fluctuations require a high level of conviction and nerves. With this sale we have reduces the susceptibility to fluctuations in our portfolios.

For the emerging growth markets, which on the one hand are influenced by commodity prices and on the other hand by the develop-ment of the US Dollar, forecasts are conside-rably more difficult to make. Russia and Brazil may well remain favoured by higher commo-

dity prices and as a result from a stronger cur-rency, but many other Asian markets will be fighting against the strength of the US Dollar.

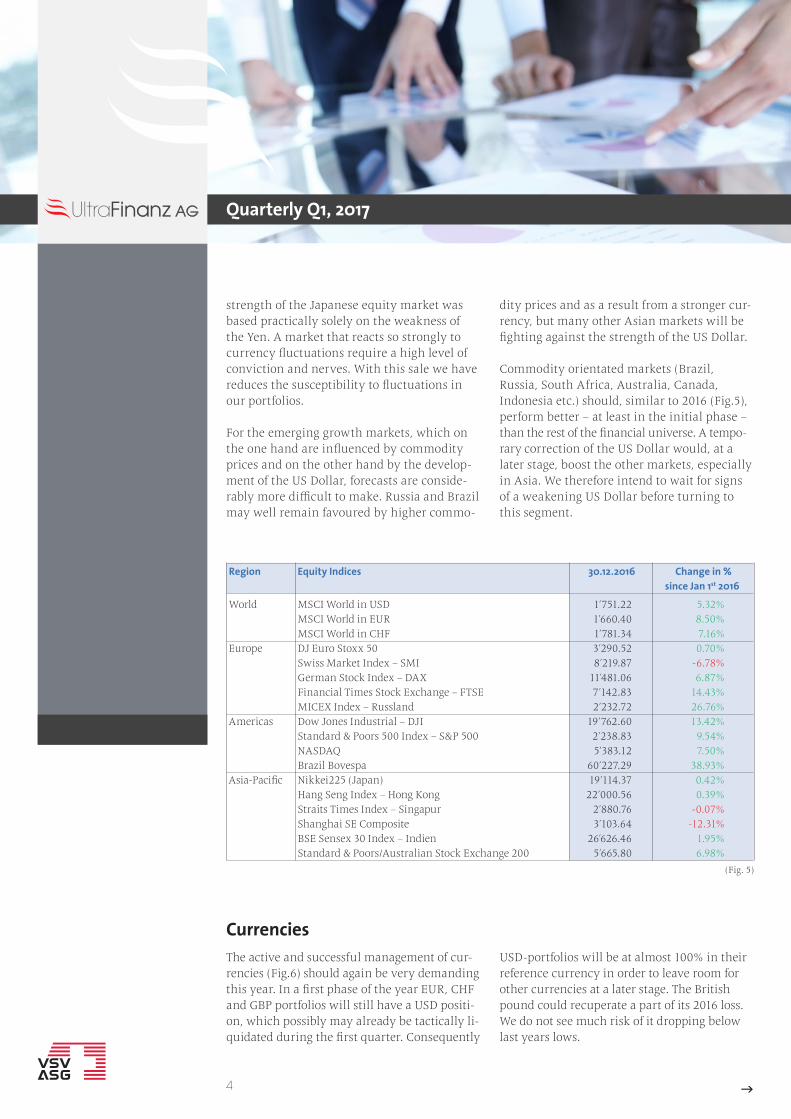

Commodity orientated markets (Brazil, Russia, South Africa, Australia, Canada, Indonesia etc.) should, similar to 2016 (Fig.5), perform better – at least in the initial phase – than the rest of the financial universe. A tempo-rary correction of the US Dollar would, at a later stage, boost the other markets, especially in Asia. We therefore intend to wait for signs of a weakening US Dollar before turning to this segment.

Region Equity Indices 30.12.2016 Change in % since Jan 1st 2016

World MSCI World in USD 1’751.22 5.32% MSCI World in EUR 1’660.40 8.50% MSCI World in CHF 1’781.34 7.16% Europe DJ Euro Stoxx 50 3’290.52 0.70% Swiss Market Index – SMI 8’219.87 -6.78% German Stock Index – DAX 11’481.06 6.87% Financial Times Stock Exchange – FTSE 7’142.83 14.43% MICEX Index – Russland 2’232.72 26.76% Americas Dow Jones Industrial – DJI 19’762.60 13.42% Standard & Poors 500 Index – S&P 500 2’238.83 9.54% NASDAQ 5’383.12 7.50% Brazil Bovespa 60’227.29 38.93% Asia-Pacific Nikkei225 (Japan) 19’114.37 0.42% Hang Seng Index – Hong Kong 22’000.56 0.39% Straits Times Index – Singapur 2’880.76 -0.07% Shanghai SE Composite 3’103.64 -12.31% BSE Sensex 30 Index – Indien 26’626.46 1.95% Standard & Poors/Australian Stock Exchange 200 5’665.80 6.98%

The active and successful management of cur-rencies (Fig.6) should again be very demanding this year. In a first phase of the year EUR, CHF and GBP portfolios will still have a USD positi-on, which possibly may already be tactically li-quidated during the first quarter. Consequently

USD-portfolios will be at almost 100% in their reference currency in order to leave room for other currencies at a later stage. The British pound could recuperate a part of its 2016 loss. We do not see much risk of it dropping below last years lows.

Currencies

Quarterly Q1, 2017

5

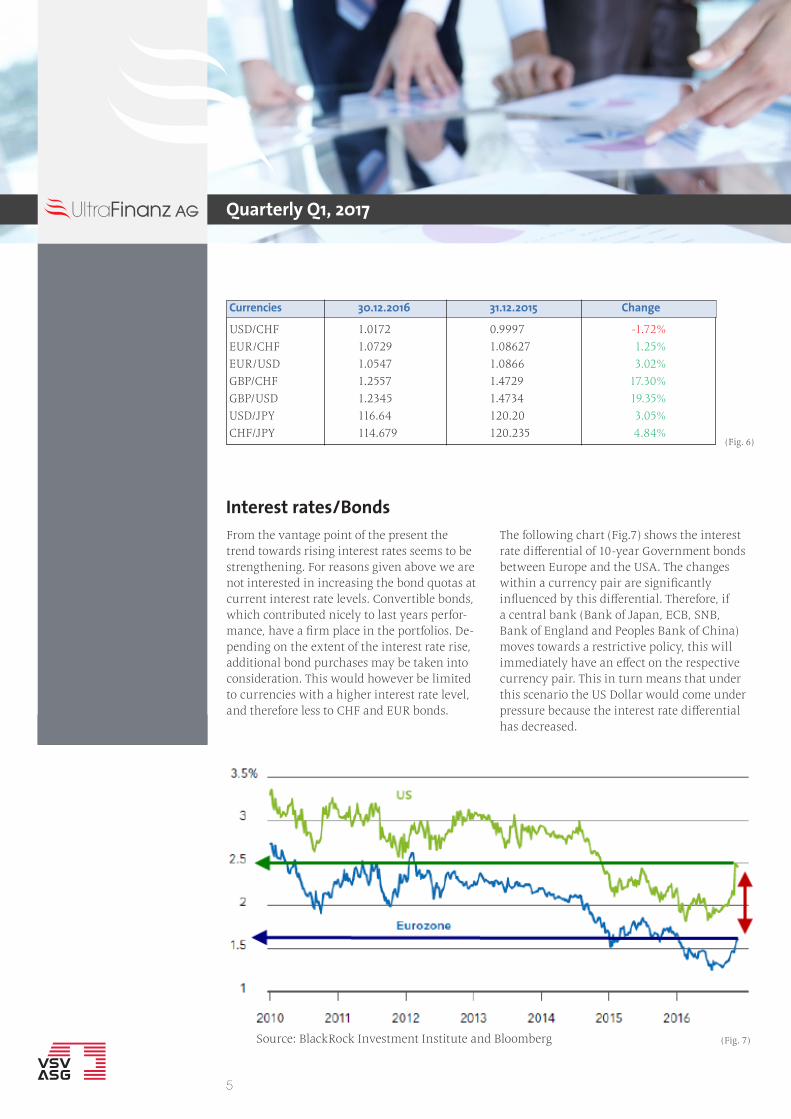

From the vantage point of the present the trend towards rising interest rates seems to be strengthening. For reasons given above we are not interested in increasing the bond quotas at current interest rate levels. Convertible bonds, which contributed nicely to last years perfor-mance, have a firm place in the portfolios. De-pending on the extent of the interest rate rise, additional bond purchases may be taken into consideration. This would however be limited to currencies with a higher interest rate level, and therefore less to CHF and EUR bonds.

The following chart (Fig.7) shows the interest rate differential of 10-year Government bonds between Europe and the USA. The changes within a currency pair are significantly influenced by this differential. Therefore, if a central bank (Bank of Japan, ECB, SNB, Bank of England and Peoples Bank of China) moves towards a restrictive policy, this will immediately have an effect on the respective currency pair. This in turn means that under this scenario the US Dollar would come under pressure because the interest rate differential has decreased.

Interest rates/Bonds

Source: BlackRock Investment Institute and Bloomberg

(Fig. 6)

Currencies 30.12.2016 31.12.2015 Change

USD/CHF 1.0172 0.9997 -1.72% EUR/CHF 1.0729 1.08627 1.25% EUR/USD 1.0547 1.0866 3.02% GBP/CHF 1.2557 1.4729 17.30% GBP/USD 1.2345 1.4734 19.35% USD/JPY 116.64 120.20 3.05% CHF/JPY 114.679 120.235 4.84%

(Fig. 7)

Quarterly Q1, 2017

6

Grossmünsterplatz 6P.O. BoxCH-8024 ZurichPhone +41 (0)44 266 60 00Fax +41 (0)44 266 60 01E-mail: [email protected]: www.ultrafinanz.ch

Bundesstrasse 9CH-6304 ZugPhone +41 (0)41 729 49 88Fax +41 (0)44 266 60 01

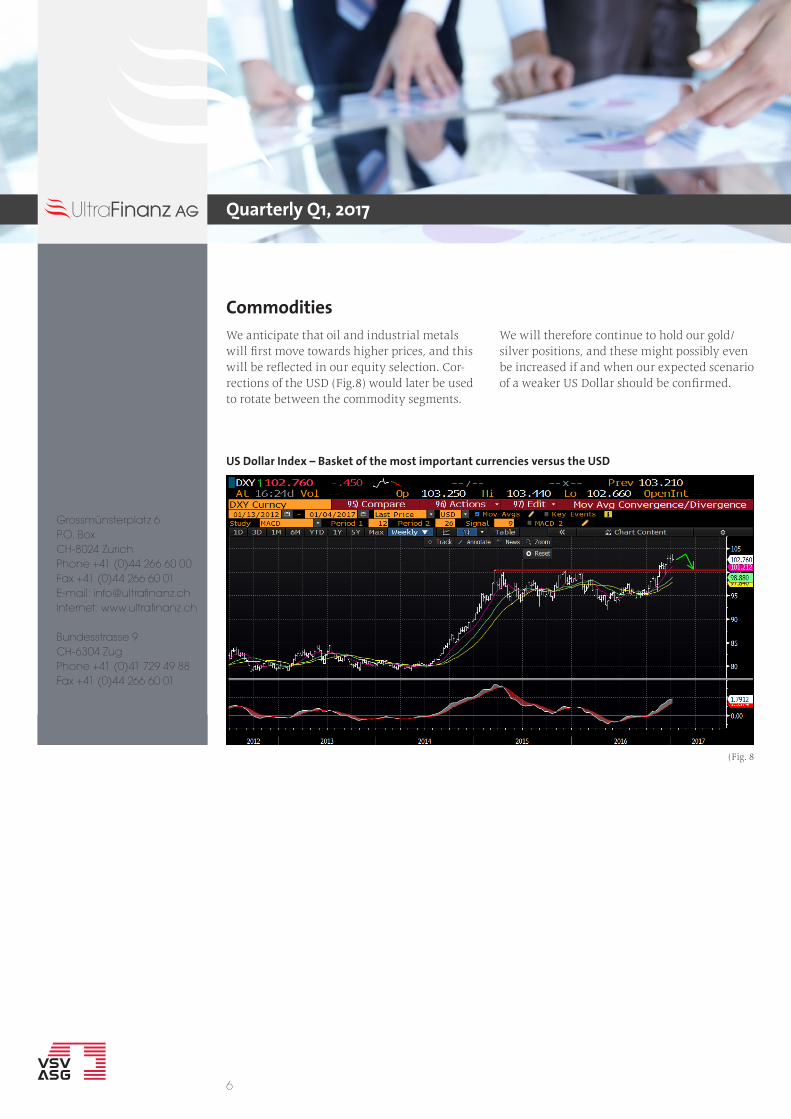

We anticipate that oil and industrial metals will first move towards higher prices, and this will be reflected in our equity selection. Cor-rections of the USD (Fig.8) would later be used to rotate between the commodity segments.

We will therefore continue to hold our gold/ silver positions, and these might possibly even be increased if and when our expected scenario of a weaker US Dollar should be confirmed.

Commodities

(Fig. 8

US Dollar Index – Basket of the most important currencies versus the USD