Quarterly Global Market Scan - Global Reporting … NFR...To avoid undue burden on smaller...

30

Quarterly Global Market Scan The EU Non-Financial Reporting Directive - what does it mean for my company? 22 April 2016

Transcript of Quarterly Global Market Scan - Global Reporting … NFR...To avoid undue burden on smaller...

Quarterly Global Market Scan

The EU Non-Financial Reporting Directive -what does it mean for my company?

22 April 2016

How to use Webex

Agenda

Time Description

15:00-15:05 Opening by Sabine Content, GRI Deputy Director Corporate &

Stakeholder Relations

15:05 – 15:25 Bernd Kasemir, Sustainserv Managing Partner –

Overview of the EU NFR Directive (Scope, main disclosures

timeline, EC consultation on non-binding guidelines)

15:25 – 15:40 Wim Bartels, KPMG Partner & Global Head of Sustainability

Reporting and Assurance –

Next steps for companies, overview of reporting practices

15:40 – 15:55 Q&A

15:55 – 16:00 Closing, Sabine Content

The EU Non-Financial Reporting Directive – what does it mean for

your company?

Key points on the EU NFR

Directive

Bernd Kasemir, Managing Partner Sustainserv

GRI GOLD Community webinar, April 22, 2016

Brief introduction

5

Managing partner at Sustainserv, an international sustainability management

consultancy with offices in Zurich and Boston

Support for our clients: strategy, KPI’s, communication, change management

15 years in business, GRI Training Partner, more than 200 CSR reports

GRI GOLD Community webinar, April 22, 2016

Table of contents

6

Goals of NFR Directive

Implementation in national law

Close link to financial reporting

Content of «non-financial statement»

Methods for reporting

Timeline

Key drivers for reporting

Questions for you to consider

GRI GOLD Community webinar, April 22, 2016

Goals of the NFR Directive

7

EU Directive 2014/95/EU on Non-Financial Reporting (aka CSR Directive)

Aims to “raise to a similar high level across all Member States the transparency of the

social and environmental information provided by undertakings in all sectors”

Amends earlier Directive (2013/34/EU) that regulates financial reporting and mainly

targets companies of more than 250 employees

To avoid undue burden on smaller companies, limited to stock-listed companies,

banks and insurances of more than 500 employees. But Member States can expand

scope.

GRI GOLD Community webinar, April 22, 2016

Implementation on national level

8

Implementation (transposition) to national law required until December 2016

Example Denmark

Law published

While early estimates of companies directly affected across the EU are at about 6,000 companies, more than 1,000 will be covered in Denmark alone

Key reason: lowering of threshold to 250 employees

Example Germany

Draft legislation in consultation process by Federal Ministry for Justice and Consumer Protection

Draft very close to EU Directive requirements

Possible extension of scope: GmbH & Co KG’s (limited liability companies) and cooperatives could be included

GRI GOLD Community webinar, April 22, 2016

9

Some examples for national implementation

GRI GOLD Community webinar, April 22, 2016

✓ (✓)(✓) - (1) - (2)

(1) 2012: Grenelle II

(2) 2013: UK Companies Act:

Mandatory Greenhouse Gas Reporting

Close link to financial report obligations

10

Management report specified as the default part of corporate reporting where non-financial statement should be included.

Member States may allow companies to issue the non-financial statement as a separate report, if

it is published together with the management report, and

covers the same financial year as the management report.

For example, the German draft legislation allows this option

Statutory audit firm will have to check whether non-financial statement has been provided

Not required by NFR Directive that content to checked as well, but

member states may require that the information is verified by an independent assurance provider.

Subsidiaries have to report unless they are covered in consolidated management report of parent company meeting the requirements

GRI GOLD Community webinar, April 22, 2016

Content of non-financial statement

11GRI GOLD Community webinar, April 22, 2016

Suggestions (should, may, could) and as appropriate/necessary

Environmental Employee/social H. rights/anti-corrupt.

Environmental impacts Ensure gender equality Prevention h.r. abuse

Health & safety impacts ILO conventions Instruments to fight

Energy use Working conditions - corruption

- Renewable energy Health & safety at work - bribery

- Non-renewable energy Social dialogue

GHG emissions Worker consultation

Water use Trade union rights

Air pollution Community dialogue

- For large undertakings also diversity policies for supervisory and

executive bodies (as part of corporate governance statement)

Methods for reporting

12

Materiality (as appropriate/to the extent necessary)

EU Commission consultation on their upcoming non-binding guidelines on

methodology for reporting closed last week

Included question of materiality approach vs. comprehensive list of KPI’s

Frameworks to use

No specific reporting framework mandatory

Directive suggests that companies may rely on ISO 26000 or the GRI guidelines

in addition to a number of EU, UN, ILO, OECD and national frameworks.

GRI GOLD Community webinar, April 22, 2016

Timeline

13

Timeline for implementation in national law

Required by December 6, 2016

Timeline for reporting by companies

Financial year starting January 1, 2017

Or financial year starting during calendar year 2017

GRI GOLD Community webinar, April 22, 2016

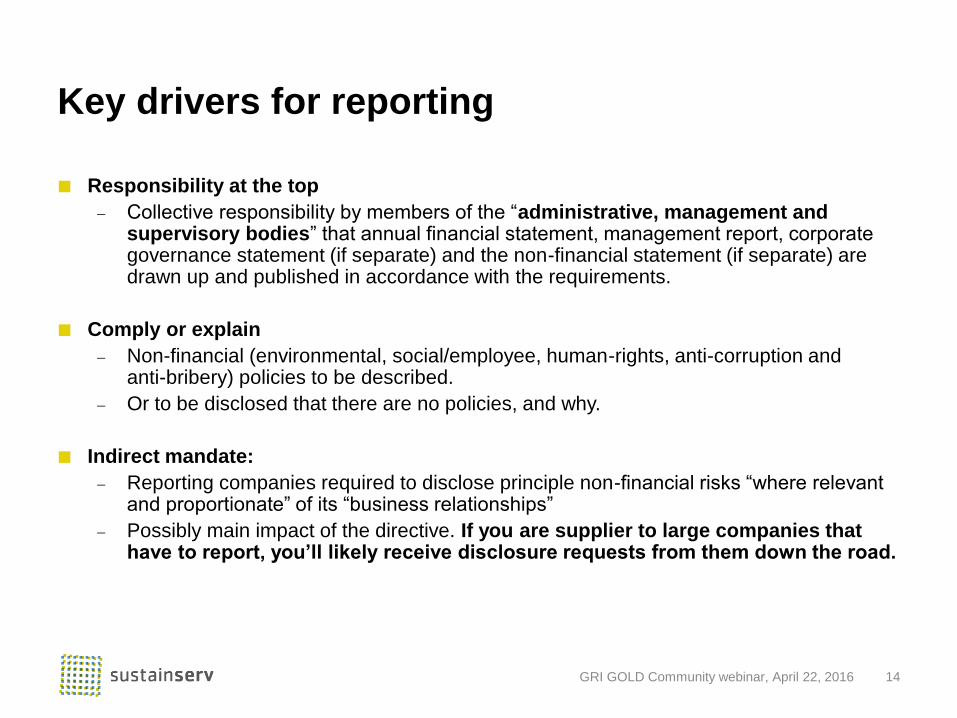

Key drivers for reporting

14

Responsibility at the top

Collective responsibility by members of the “administrative, management and supervisory bodies” that annual financial statement, management report, corporate governance statement (if separate) and the non-financial statement (if separate) are drawn up and published in accordance with the requirements.

Comply or explain

Non-financial (environmental, social/employee, human-rights, anti-corruption andanti-bribery) policies to be described.

Or to be disclosed that there are no policies, and why.

Indirect mandate:

Reporting companies required to disclose principle non-financial risks “where relevant and proportionate” of its “business relationships”

Possibly main impact of the directive. If you are supplier to large companies that have to report, you’ll likely receive disclosure requests from them down the road.

GRI GOLD Community webinar, April 22, 2016

Questions for you to considerAlso Q&A discussion at the end of this webinar

15

Are you covered directly?

Do you expect supply chain pressure for disclosure?

Are you supplier to large companies likely to be covered?

Have your customers already asked you for environmental and social information

(RFP’s etc.)?

Would you have policies and metrics in place to respond if needed?

Have you done a materiality assessment to understand what to focus on?

If you would report due to legal requirements of supply chain pressure

Would it be best for you to “reduce to the max”?

Would it be best for you to use this as an opportunity for market differentiation?

GRI GOLD Community webinar, April 22, 2016

Thank you!

Sustainserv, Inc.

31 State Street, 10th Floor

Boston MA 02109

USA

T +1 617 330 5001

Sustainserv GmbH

Gartenstrasse 16

8002 Zurich

Switzerland

T +41 44 500 53 00

www.sustainserv.com

Implications of the NFI Directive for your company: a big opportunityWim Bartels, Global Head of Sustainability Assurance & Reporting at KPMG

—

22 April 2016

18

c o l o u r

© 2016 KPMG Staffing & Facility Services B.V., registered with the trade register in the Netherlands under number 33263682, is a member firm of the KPMG network of independent member firms

affiliated with KPMG International Cooperative (‘KPMG International’), a Swiss entity. All rights reserved.

The opportunities from the NFI Directive• Integrating your (CSR) reporting in mainstream reporting

• Connecting CSR issues to the business model

• Focusing on the financially material CSR issues that matter to strategy

• Redefining the value of CSR to the business

• Further strengthening systems and controls

19

c o l o u r

© 2016 KPMG Staffing & Facility Services B.V., registered with the trade register in the Netherlands under number 33263682, is a member firm of the KPMG network of independent member firms

affiliated with KPMG International Cooperative (‘KPMG International’), a Swiss entity. All rights reserved.

Base: N100 companies

Source: KPMG Survey of Corporate Responsibility Reporting 2015

4%

20%

51%

56%

2008 2011 2013 2015

Integrating CSR into mainstream reporting

20

c o l o u r

© 2016 KPMG Staffing & Facility Services B.V., registered with the trade register in the Netherlands under number 33263682, is a member firm of the KPMG network of independent member firms

affiliated with KPMG International Cooperative (‘KPMG International’), a Swiss entity. All rights reserved.

Connecting CSR to the business model

Business model

Source: KPN Annual Report, 2015

21

c o l o u r

© 2016 KPMG Staffing & Facility Services B.V., registered with the trade register in the Netherlands under number 33263682, is a member firm of the KPMG network of independent member firms

affiliated with KPMG International Cooperative (‘KPMG International’), a Swiss entity. All rights reserved.

Focusing on financially material issues that matter to strategy

Risks related to CSR matters

Source: AkzoNobel Annual Report 2015

22

c o l o u r

© 2016 KPMG Staffing & Facility Services B.V., registered with the trade register in the Netherlands under number 33263682, is a member firm of the KPMG network of independent member firms

affiliated with KPMG International Cooperative (‘KPMG International’), a Swiss entity. All rights reserved.

Redefining the value of CSR to the business

Policies & outcome of policies, including KPIs

Source: Unilever Annual Accounts 2015

23

c o l o u r

© 2016 KPMG Staffing & Facility Services B.V., registered with the trade register in the Netherlands under number 33263682, is a member firm of the KPMG network of independent member firms

affiliated with KPMG International Cooperative (‘KPMG International’), a Swiss entity. All rights reserved.

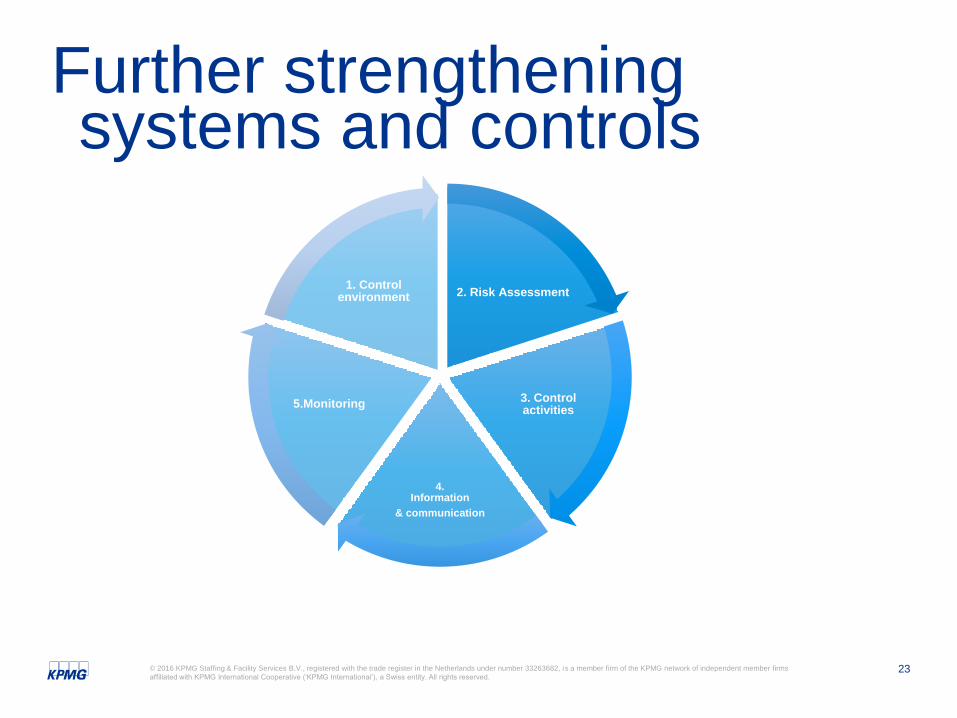

Further strengtheningsystems and controls

2. Risk Assessment

3. Control activities

4. Information

& communication

5.Monitoring

1. Control environment

24

c o l o u r

© 2016 KPMG Staffing & Facility Services B.V., registered with the trade register in the Netherlands under number 33263682, is a member firm of the KPMG network of independent member firms

affiliated with KPMG International Cooperative (‘KPMG International’), a Swiss entity. All rights reserved.

• Have we considered to include the material CSR information in the annual report and decided about its

placement?

• Is our business model sufficiently explained in the annual report – and how could a visualization of our

business model assist in better understanding the relevance of CSR for our business?

• How could we further strengthen the integration of CSR risks into our risk management processes to better

inform and connect to strategy?

• To what extent do the CSR aspects defined inspire to redefine the value of CSR to our business and the

purpose of our company?

• Are we sufficiently comfortable that the relevant KPIs for our CSR issues are properly embedded in internal

control and reporting processes to deliver reliable outputs?

Questions for you toconsider

KPMG on social media KPMG app

© 2016 KPMG Staffing & Facility Services B.V., registered with the trade register in the Netherlands under number 33263682, is a member firm of the KPMG network of

independent member firms affiliated with KPMG International Cooperative (‘KPMG International’), a Swiss entity. All rights reserved.

The KPMG name and logo are registered trademarks of KPMG International.

Thank you

Q&A

Linkage document

https://www.globalreporting.or

g/resourcelibrary/GRI_G4_EU

%20Directive_Linkage.pdf

5th GRI Global Conference

Join us at the 5th GRI Global Conference 2016Empowering Sustainable Decisions

18-20 May, Amsterdam, #GRI2016

Register here: http://bit.ly/1QLfR0j

Upcoming webinars

Date Topic

28 April Insights and experiences from the Corporate Leadership Group

on Reporting 2025

3 May G4 Forefront technical series: Session 2 - Materiality and

Boundaries

4 May A la Vanguardia con G4 Spanish technical series: Sesión 2 -

Materialidad y Cobertura

11 May SDG UN Update

26 May Update: National legislation roll out and what the 2015 reports

show us

Thank you

www.globalreporting.org

GRI

Barbara Strozzilaan 336

1083 HN Amsterdam

The Netherlands

Amsterdam | New York | Beijing | Sydney | New Delhi | Johannesburg | Bogota | São Paulo