Quantifying Transfer Credits from a Revenue Perspective · ess Quantifying Transfer Credits from a...

34

Office of Institutional Effectiveness Quantifying Transfer Credits from a Revenue Perspective One Institutions Approach to Achieving Zen Presented by Michael Cogan & Sushant Khullar Office of Institutional Effectiveness October 27, 2011

Transcript of Quantifying Transfer Credits from a Revenue Perspective · ess Quantifying Transfer Credits from a...

O

ffic

e o

f In

stit

uti

on

al E

ffec

tive

nes

s

Quantifying Transfer Credits from a Revenue Perspective

One Institutions Approach to Achieving Zen

Presented by

Michael Cogan & Sushant Khullar

Office of Institutional Effectiveness

October 27, 2011

O

ffic

e o

f In

stit

uti

on

al E

ffec

tive

nes

s

Agenda

• Introduction to UST

• Definitions

• Freshman Student Outcomes

• Transfer Credit

– Pre-Matriculation

– Post-Matriculation

– Impact on Departments

• Implications

O

ffic

e o

f In

stit

uti

on

al E

ffec

tive

nes

s

University of St. Thomas

• Catholic…..Diocesan…..Doctoral/Research

• Teaching University

• Enrollment – 10,534

– Undergraduate – 6,176

– Incoming Freshman – 1,324

• Campuses in St. Paul, Minneapolis, Rome, and Owatonna

• Gender - ~50/50

• Minnesota Residence – 80%

O

ffic

e o

f In

stit

uti

on

al E

ffec

tive

nes

s

Definitions

• Freshman – First-time, First-Year students entering UST in fall of 2004-2007

• Pre-Matriculation Transfer Credit – All transfer credit earned by the student prior to matriculation and transferred to UST (e.g., PSEO, AP, and CLEP)

• Post-Matriculation Transfer Credit – All credits earned by a student outside of UST after initial enrollment at the institution (e.g., Two and Four-Year Colleges)

• Academic Departments – Institutional entities separated into fields of study using Classification of Instructional Program codes

O

ffic

e o

f In

stit

uti

on

al E

ffec

tive

nes

s

Data Development

• Transfer Credit

• Cohort assignment

• Descriptive analysis (chi-square & t-test)

• Isolate pre- and post matriculation credits

• Core and non-core curriculum

• Class recognition

O

ffic

e o

f In

stit

uti

on

al E

ffec

tive

nes

s

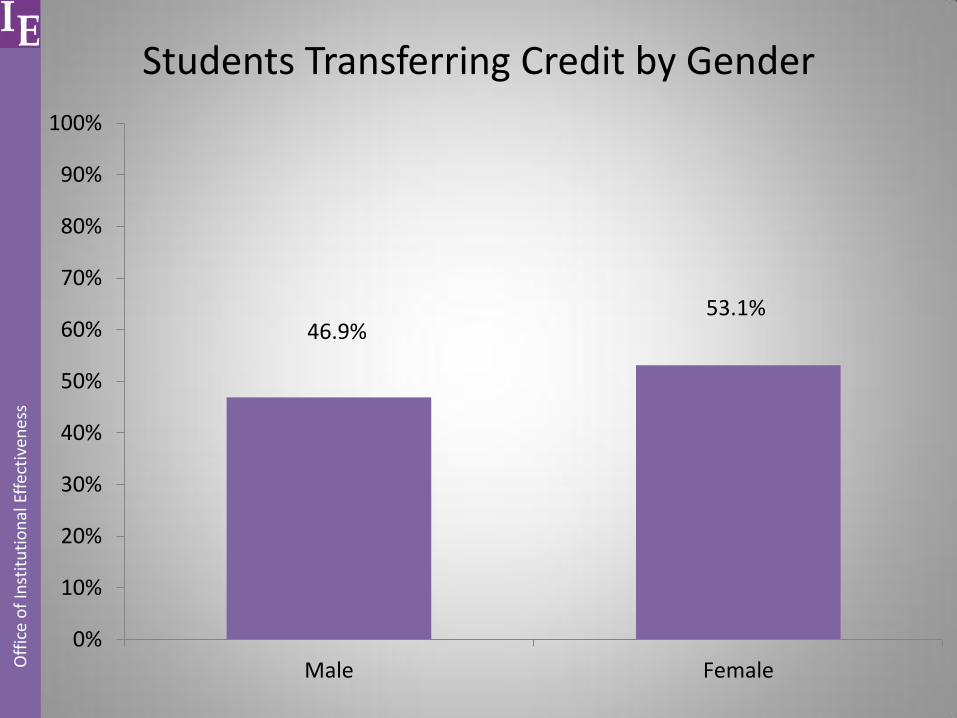

Students Transferring Credit by Gender

46.9% 53.1%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Male Female

O

ffic

e o

f In

stit

uti

on

al E

ffec

tive

nes

s

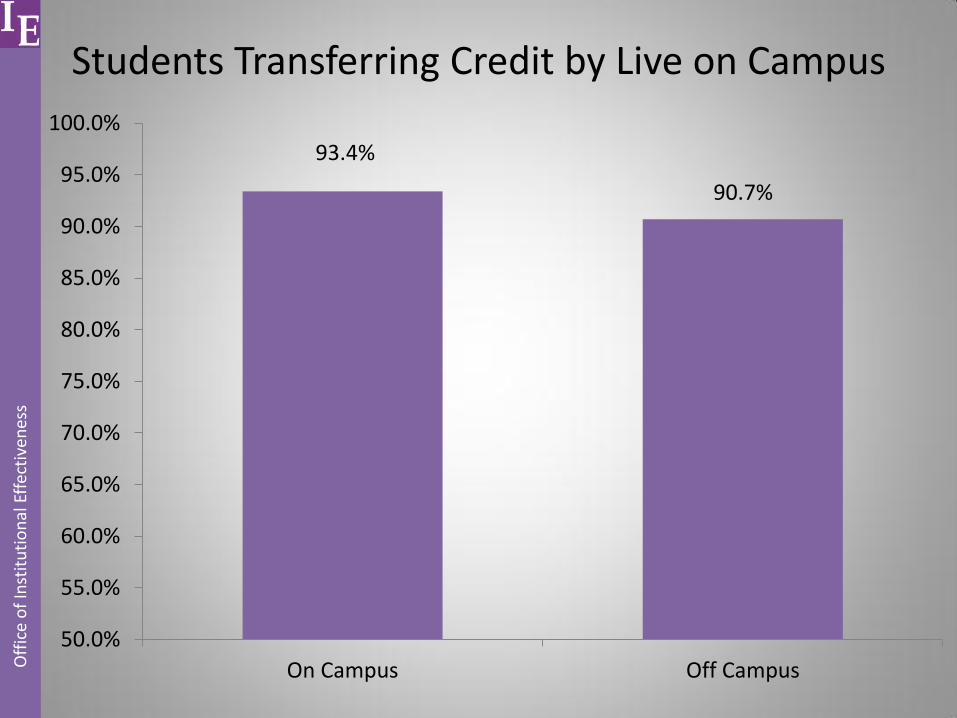

Students Transferring Credit by Live on Campus

93.4%

90.7%

50.0%

55.0%

60.0%

65.0%

70.0%

75.0%

80.0%

85.0%

90.0%

95.0%

100.0%

On Campus Off Campus

O

ffic

e o

f In

stit

uti

on

al E

ffec

tive

nes

s

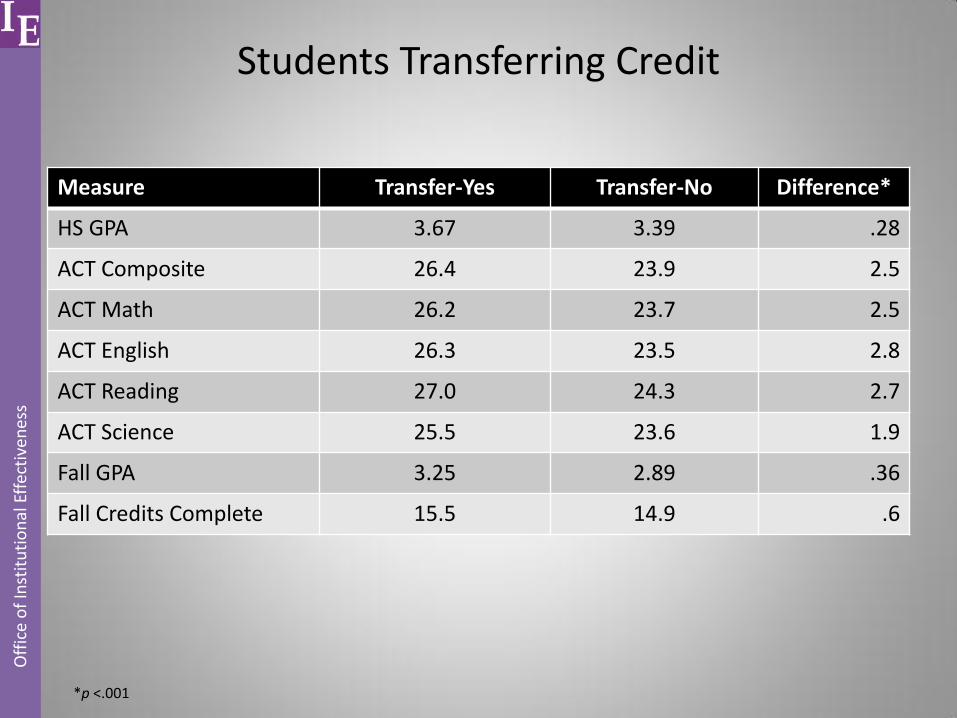

Students Transferring Credit

Measure Transfer-Yes Transfer-No Difference*

HS GPA 3.67 3.39 .28

ACT Composite 26.4 23.9 2.5

ACT Math 26.2 23.7 2.5

ACT English 26.3 23.5 2.8

ACT Reading 27.0 24.3 2.7

ACT Science 25.5 23.6 1.9

Fall GPA 3.25 2.89 .36

Fall Credits Complete 15.5 14.9 .6

*p <.001

O

ffic

e o

f In

stit

uti

on

al E

ffec

tive

nes

s

Students Transferring Credit by F-to-F Retention

89.9% 85.1%

Return-Yes Return-No

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

O

ffic

e o

f In

stit

uti

on

al E

ffec

tive

nes

s

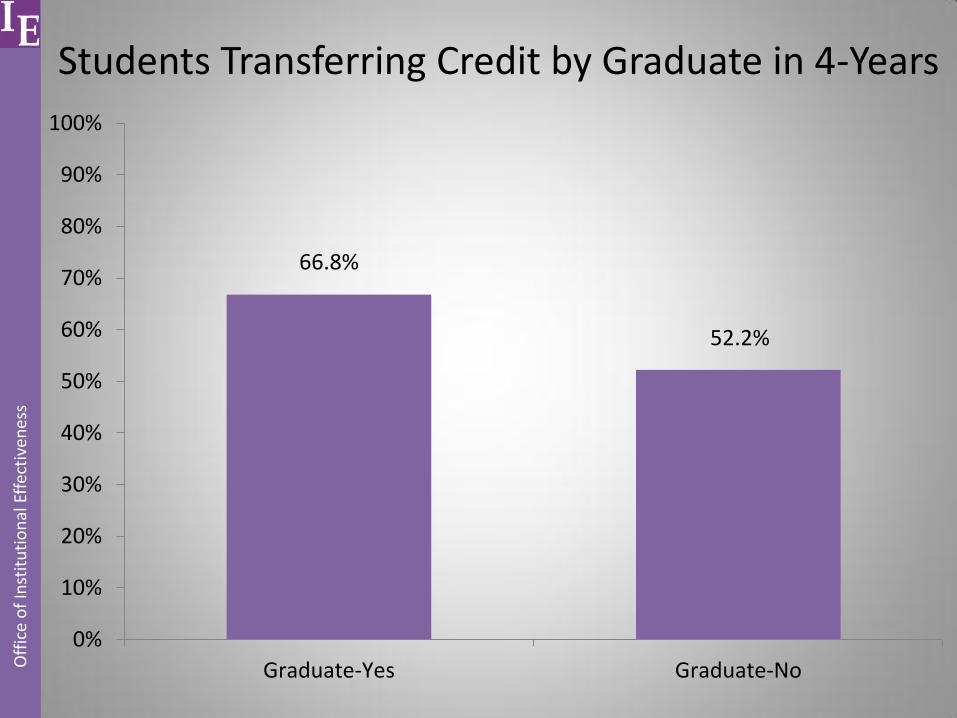

Students Transferring Credit by Graduate in 4-Years

66.8%

52.2%

Graduate-Yes Graduate-No

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

O

ffic

e o

f In

stit

uti

on

al E

ffec

tive

nes

s

Questions

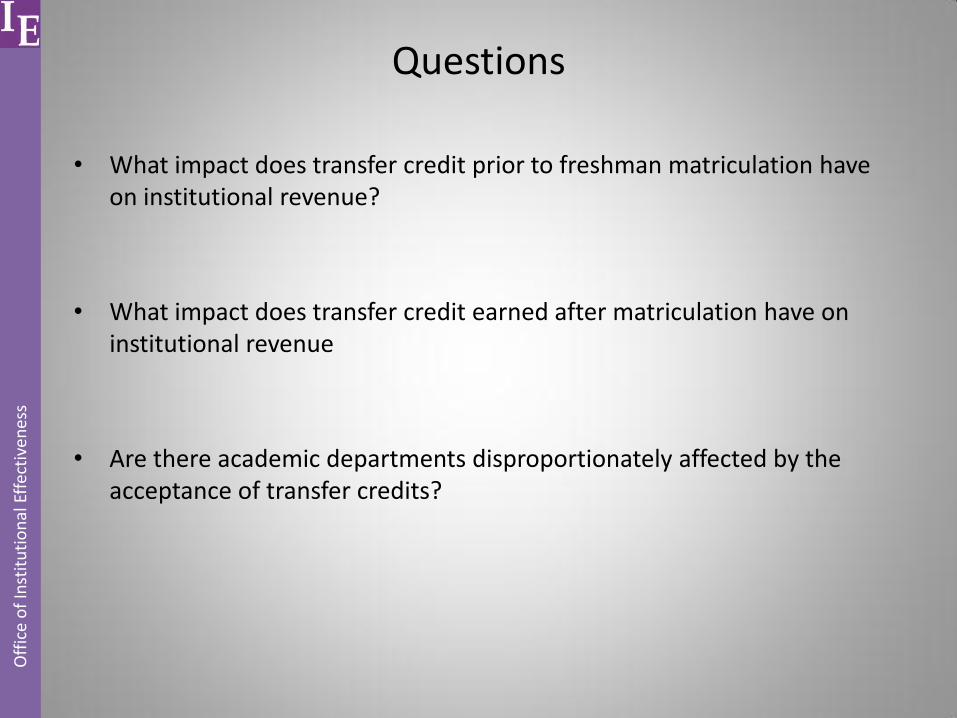

• What impact does transfer credit prior to freshman matriculation have on institutional revenue?

• What impact does transfer credit earned after matriculation have on institutional revenue

• Are there academic departments disproportionately affected by the acceptance of transfer credits?

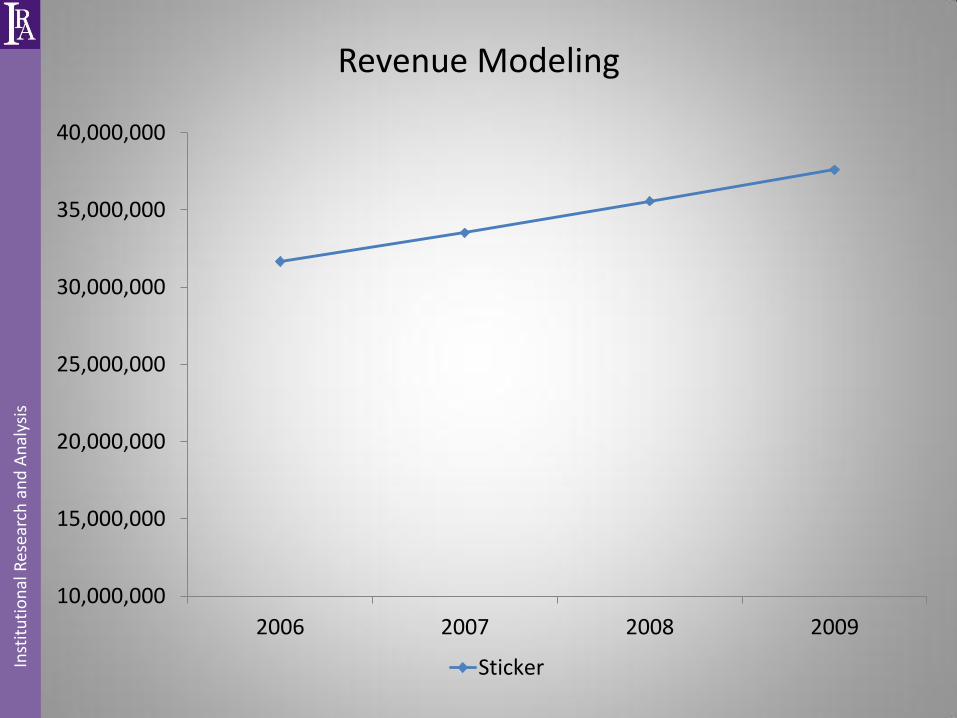

10,000,000

15,000,000

20,000,000

25,000,000

30,000,000

35,000,000

40,000,000

2006 2007 2008 2009

Sticker

Revenue Modeling

In

stit

uti

on

al R

esea

rch

an

d A

nal

ysis

10,000,000

15,000,000

20,000,000

25,000,000

30,000,000

35,000,000

40,000,000

2006 2007 2008 2009

Sticker Attrition

Revenue Modeling

In

stit

uti

on

al R

esea

rch

an

d A

nal

ysis

10,000,000

15,000,000

20,000,000

25,000,000

30,000,000

35,000,000

40,000,000

2006 2007 2008 2009

Sticker Attrition Attrition & Credits

Revenue Modeling

In

stit

uti

on

al R

esea

rch

an

d A

nal

ysis

10,000,000

15,000,000

20,000,000

25,000,000

30,000,000

35,000,000

40,000,000

2006 2007 2008 2009

Sticker Attrition Attrition & Credits Attrition, Credits, Discount

Revenue Modeling

In

stit

uti

on

al R

esea

rch

an

d A

nal

ysis

10,000,000

15,000,000

20,000,000

25,000,000

30,000,000

35,000,000

40,000,000

2006 2007 2008 2009

Sticker Attrition

Attrition & Credits Attrition, Credits, Discount

Attrition, Credits, Discount, FA

Revenue Modeling

In

stit

uti

on

al R

esea

rch

an

d A

nal

ysis

10,000,000

15,000,000

20,000,000

25,000,000

30,000,000

35,000,000

40,000,000

2006 2007 2008 2009

Sticker Attrition

Attrition & Credits Attrition, Credits, Discount

Attrition, Credits, Discount, FA

Revenue Modeling

In

stit

uti

on

al R

esea

rch

an

d A

nal

ysis

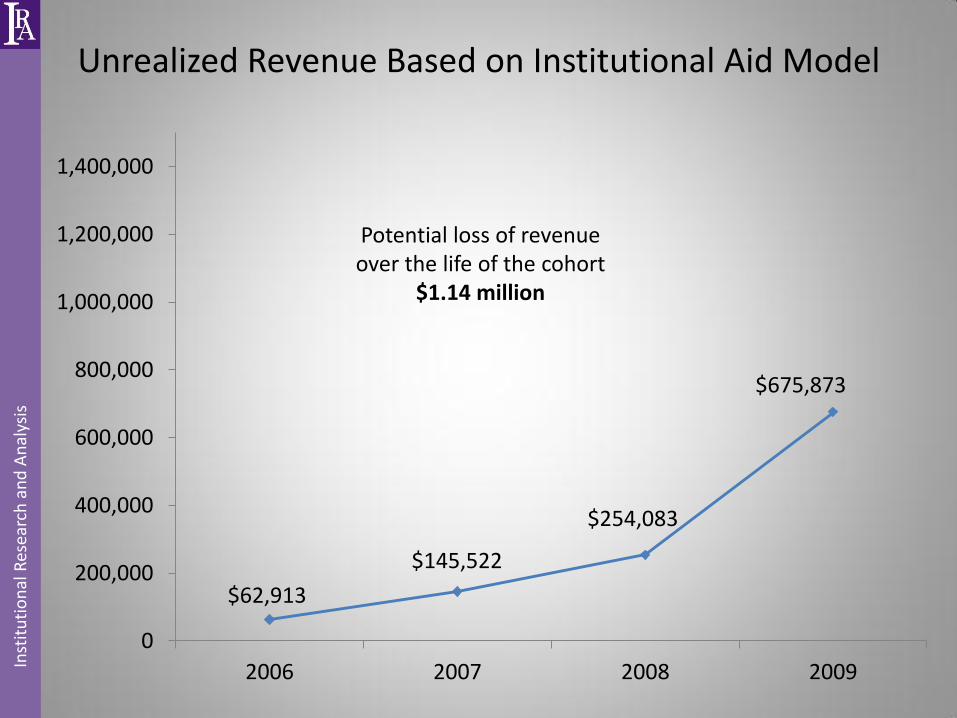

$62,913

$145,522

$254,083

$675,873

0

200,000

400,000

600,000

800,000

1,000,000

1,200,000

1,400,000

2006 2007 2008 2009

Unrealized Revenue Based Model

In

stit

uti

on

al R

esea

rch

an

d A

nal

ysis

$62,913

$145,522

$254,083

$675,873

0

200,000

400,000

600,000

800,000

1,000,000

1,200,000

1,400,000

2006 2007 2008 2009

Unrealized Revenue Based on Institutional Aid Model

In

stit

uti

on

al R

esea

rch

an

d A

nal

ysis

Potential loss of revenue over the life of the cohort

$1.14 million

O

ffic

e o

f In

stit

uti

on

al E

ffec

tive

nes

s

Projected Revenue Loss Pre-Matriculation

O

ffic

e o

f In

stit

uti

on

al E

ffec

tive

nes

s

Freshman Student Outcomes 2006-10

• 3,470 freshman transferred credit pre-matriculation (51%)

• The average number of credits transferred per student: – Mean – 13.1

– Median – 10.0

– Mode – 4.0

– Interquartile range – 13

– Range – 79.0

• Total credits transferred – 45,599

• The average number of ‘entities’ transferring credit from – 1.31

O

ffic

e o

f In

stit

uti

on

al E

ffec

tive

nes

s

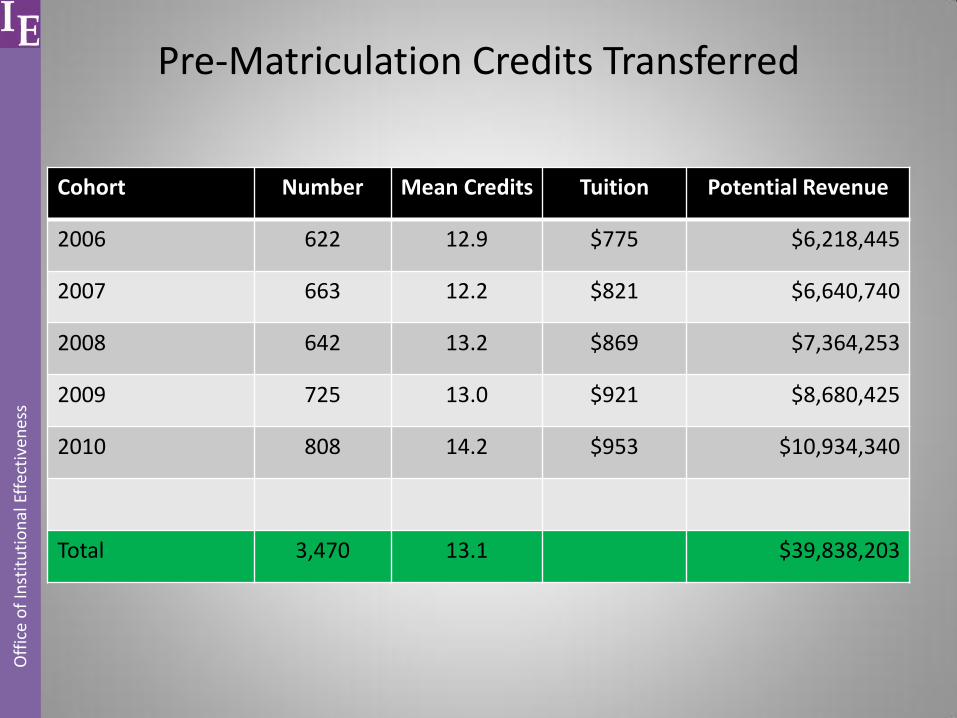

Pre-Matriculation Credits Transferred

Cohort Number Mean Credits Tuition Potential Revenue

2006 622 12.9 $775 $6,218,445

2007 663 12.2 $821 $6,640,740

2008 642 13.2 $869 $7,364,253

2009 725 13.0 $921 $8,680,425

2010 808 14.2 $953 $10,934,340

Total 3,470 13.1 $39,838,203

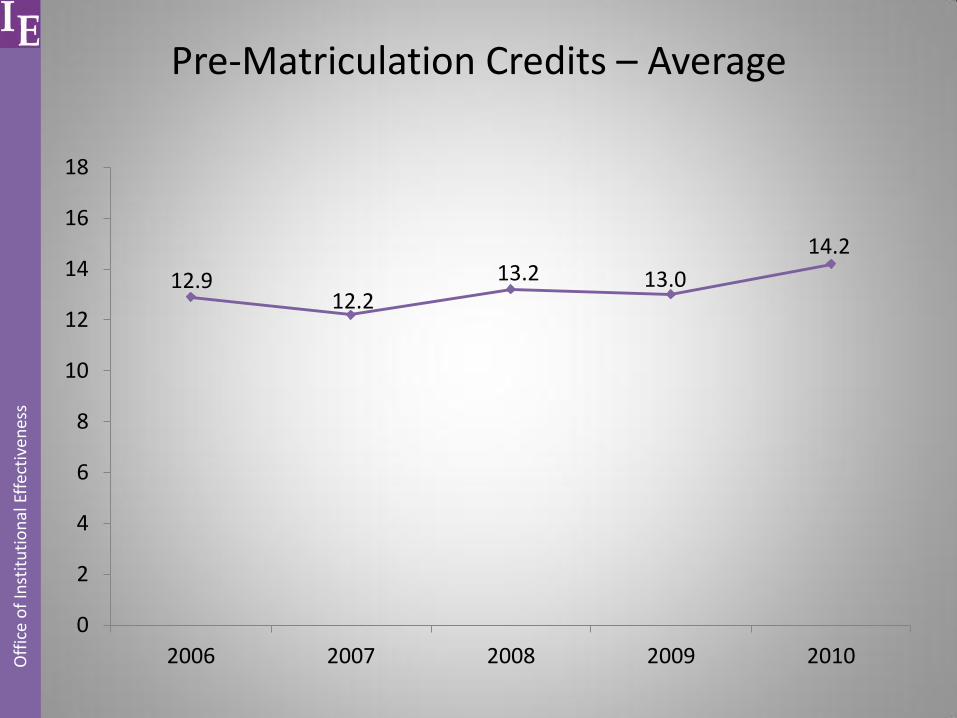

12.9 12.2

13.2 13.0

14.2

0

2

4

6

8

10

12

14

16

18

2006 2007 2008 2009 2010

Pre-Matriculation Credits – Average

Off

ice

of

Inst

itu

tio

nal

Eff

ecti

ven

ess

622 663 642

725

808

0

100

200

300

400

500

600

700

800

900

1,000

2006 2007 2008 2009 2010

Pre-Matriculation Credits – Headcount

Off

ice

of

Inst

itu

tio

nal

Eff

ecti

ven

ess

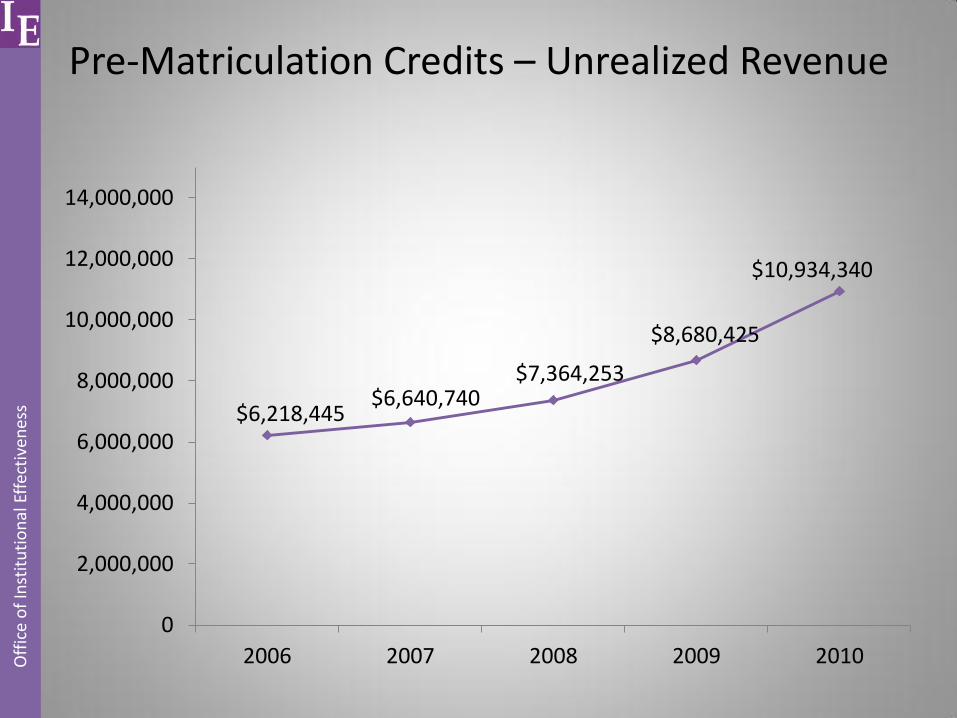

$6,218,445 $6,640,740

$7,364,253

$8,680,425

$10,934,340

0

2,000,000

4,000,000

6,000,000

8,000,000

10,000,000

12,000,000

14,000,000

2006 2007 2008 2009 2010

Pre-Matriculation Credits – Unrealized Revenue

Off

ice

of

Inst

itu

tio

nal

Eff

ecti

ven

ess

O

ffic

e o

f In

stit

uti

on

al E

ffec

tive

nes

s

Projected Revenue Loss Post-Matriculation

O

ffic

e o

f In

stit

uti

on

al E

ffec

tive

nes

s

Post-Matriculation Transfer Trends 2004-07

• 1,220 undergraduate students transferred credit post-matriculation

• The average number of credits transferred per student: – Mean – 7.5

– Median – 5.0

– Mode – 3.0

– Interquartile range – 6.0 (3.0 to 9.0)

– Range – 33.0

• Total credits transferred – 9,150

• Students transferring credit post-matriculation (24%)

O

ffic

e o

f In

stit

uti

on

al E

ffec

tive

nes

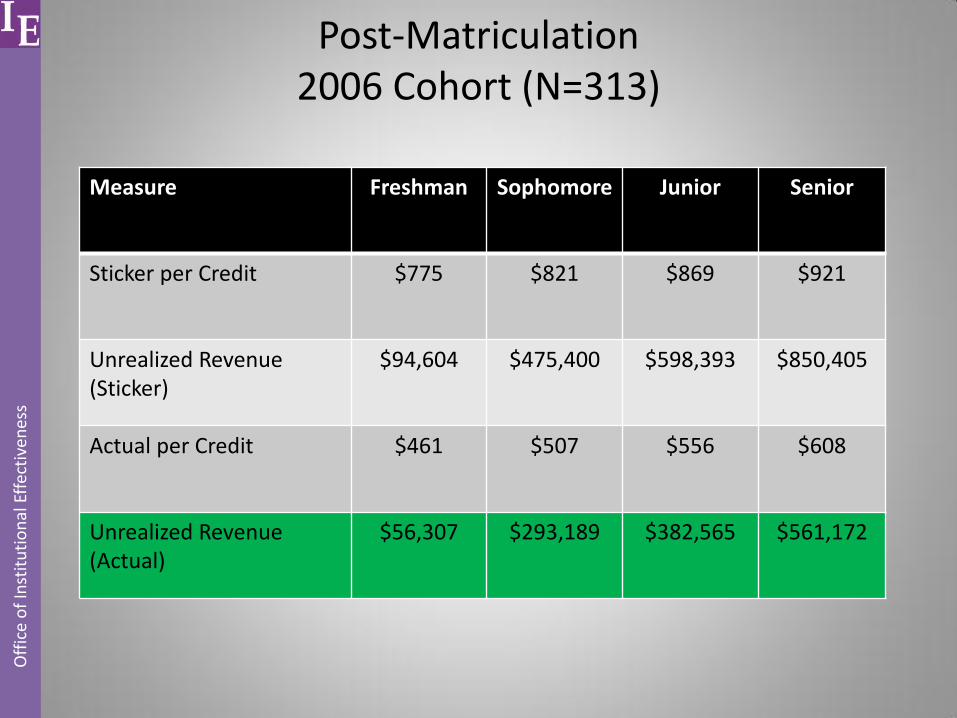

s Post-Matriculation

2006 Cohort (N=313)

Measure Freshman Sophomore Junior Senior

Sticker per Credit $775 $821 $869 $921

Actual by Percentage .595 .618 .639 .660

Actual per Credit $461 $507 $556 $608

Credits Transferred (Avg) .39 1.85 2.20 2.95

O

ffic

e o

f In

stit

uti

on

al E

ffec

tive

nes

s Post-Matriculation

2006 Cohort (N=313)

Measure Freshman Sophomore Junior Senior

Sticker per Credit $775 $821 $869 $921

Unrealized Revenue (Sticker)

$94,604 $475,400 $598,393 $850,405

Actual per Credit $461 $507 $556 $608

Unrealized Revenue (Actual)

$56,307 $293,189 $382,565 $561,172

O

ffic

e o

f In

stit

uti

on

al E

ffec

tive

nes

s

Projected Revenue Loss Academic Departments

O

ffic

e o

f In

stit

uti

on

al E

ffec

tive

nes

s

Core Curriculum

• Three Overarching Objectives

– Liberal learning

– Moral and ethical development

– Career preparation

O

ffic

e o

f In

stit

uti

on

al E

ffec

tive

nes

s Academic Department Transfer Activity

2007-10

Core Requirement Headcount Credits Average

Social Analysis 936 4,235 4.5

Natural Sciences 777 4,010 5.2

Literature and Writing 772 3,434 4.4

Mathematics 703 3,611 5.1

Human Diversity 421 1,614 3.8

Historical Studies 407 1,624 4.0

Language and Culture 350 1,969 5.6

Quantitative Reasoning 321 1,247 3.9

Implications

• Student outcomes

• Dollars and ‘sense’

• Curriculum ‘should’ trump finances

• Entrepreneurial spirit

Discussion