Q4 and Full Year 2012 Conference Call · Key P&L Line Items (Adjusted) Q4 2012 Q4 2011 ∆ vs....

58

Q4 and Full Year 2012 Conference Call J 24 2013 January 24, 2013

Transcript of Q4 and Full Year 2012 Conference Call · Key P&L Line Items (Adjusted) Q4 2012 Q4 2011 ∆ vs....

Q4 and Full Year 2012 Conference Call

J 24 2013January 24, 2013

Agenda

Patrick Flanigan VP Investor RelationsPatrick Flanigan, VP, Investor Relations

Bob Hugin Chief Executive OfficerBob Hugin, Chief Executive Officer

Jackie Fouse Chief Financial OfficerJackie Fouse, Chief Financial Officer

Mark Alles, Head of Hematology/Oncology

2

Q&A

Forward Looking Statements and Adjusted Financial Information

This presentation contains forward-looking statements, which are generally statements that are nothistorical facts. Forward-looking statements can be identified by the words “expects,” “anticipates,”“believes,” “intends,” “estimates,” “plans,” “will,” “outlook” and similar expressions. Forward-looking, , , p , , p gstatements are based on management’s current plans, estimates, assumptions and projections, andspeak only as of the date they are made. We undertake no obligation to update any forward-lookingstatement in light of new information or future events, except as otherwise required by law. Forward-looking statements involve inherent risks and uncertainties, most of which are difficult to predict andare generally beyond our control Actual results or outcomes may differ materially from those impliedare generally beyond our control. Actual results or outcomes may differ materially from those impliedby the forward-looking statements as a result of the impact of a number of factors, many of whichare discussed in more detail in our Annual Report on Form 10-K and our other reports filed with theSecurities and Exchange Commission.

In addition to financial information prepared in accordance with U.S. GAAP, this presentation alsocontains adjusted financial measures that we believe provide investors and management withsupplemental information relating to operating performance and trends that facilitate comparisonsbetween periods and with respect to projected information. These adjusted measures are non-GAAP and should be considered in addition to but not as a substitute for the information preparedGAAP and should be considered in addition to, but not as a substitute for, the information preparedin accordance with U.S. GAAP. We typically exclude certain GAAP items that management doesnot believe affect our basic operations and that do not meet the GAAP definition of unusual or non-recurring items. Other companies may define these measures in different ways. Further informationrelevant to the interpretation of adjusted financial measures, and reconciliations of these adjustedfi i l t th t bl GAAP b f d C l ’ b it t

3

financial measures to the most comparable GAAP measures, may be found on Celgene’s website atwww.Celgene.com in the “Investor Relations” section.

Bob Hugin

2012: A Year of Significant Achievements Positioning Us for Sustained Growth

Outstanding financial results:

Strong top- and bottom-line growth increasing global cash flowStrong top- and bottom-line growth increasing global cash flow Continued operating momentum with improving marginsAssertive management of balance sheet and capital structure

Strong performance across commercial metrics:

Growth across product lines driven by increased share and durationLaunches in new indications to serve more patients

Building for the future:

Launches in new indications to serve more patients Expanding access in new geographies

Building for the future:

Key regulatory filings including POMALYST® in US, EU; REVLIMID® MCL in USABRAXANE® positive data in pancreatic cancer and melanomaApremilast pivotal data in psoriatic arthritis and psoriasisAdvancing key early- to mid-stage pipeline programs

5

Advancing Towards the Next Phase of Growth

Maximize Full Potential of our Hematology Franchise1 Maximize Full Potential of our Hematology Franchise1

Expand our Oncology Franchise into New Indications2

Submit Apremilast with Regulators and Prepare for Launch3

Advance Early-Stage Clinical Programs to Key Decision Points4

6

Jackie Fouse

2012 Financial Highlights

Outstanding operating results:Year-over-year product sales grew 15% and fully diluted EPS grew 30%y p g y gImproved adjusted operating margins by 300 bps

Adding value with financial drivers:Adding value with financial drivers:28.6M shares repurchased in 2012 for $2.1B7.5M shares repurchased in Q4 for ~$580M

Excellent performance on operating metrics including:REVLIMID annual growth of 17% Approval for ABRAXANE in NSCLCApproval for ABRAXANE in NSCLC

Investing for the future:Advanced >30 pivotal/phase III trials and accelerated early- to mid-stage pipelineEntered into new collaborations and expanded existing partnerships

8

Components of Revenues

∆ vs. ∆ vs.(in millions) Q4:12

∆ vs.Q4:11 FY 2012

∆ vs.FY11

Total Net Product Sales $1,416 ↑14% $5,386 ↑15%

Collaborative Revenue $2 ↓18% $11 ↓45%

Royalty Revenue $29 ↓23% $110 ↓10%

Total Revenue $1 447 ↑13% $5 507 ↑14%Total Revenue $1,447 ↑13% $5,507 ↑14%

9

Total Product Sales(Growth Rates = Growth vs. Prior Year Period)

$5,386

Q4 Full Year

$1,241

$1,416 $4,673

,

$1,023$3,484

Mill

ions

↑21% ↑14% ↑34% ↑15%↑42% ↑36%

Q4:10 Q4:11 Q4:12 2010 2011 2012

10

2010 and 2011 figures are adjusted

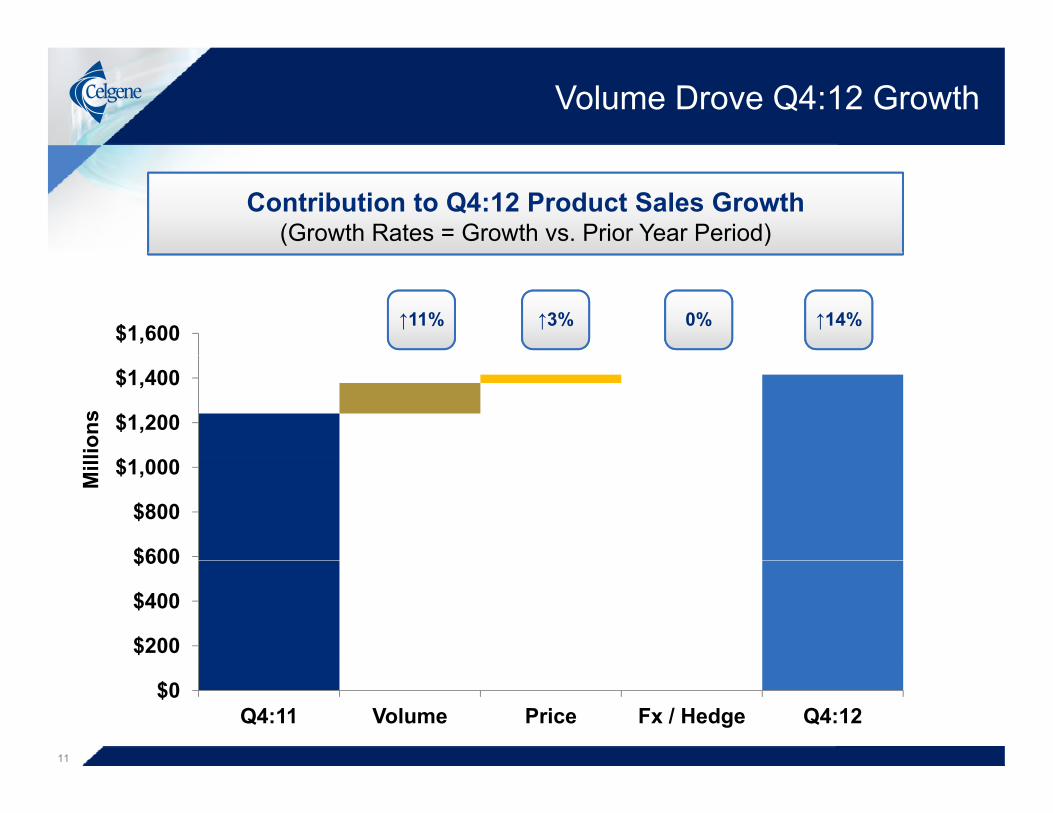

Volume Drove Q4:12 Growth

Contribution to Q4:12 Product Sales Growth(Growth Rates = Growth vs. Prior Year Period)

$1,600 ↑14%0%↑11% ↑3%

$

$1,200

$1,400

lions

$600

$800

$1,000Mill

$200

$400

$600

$0Q4:11 Volume Price Fx / Hedge Q4:12

11

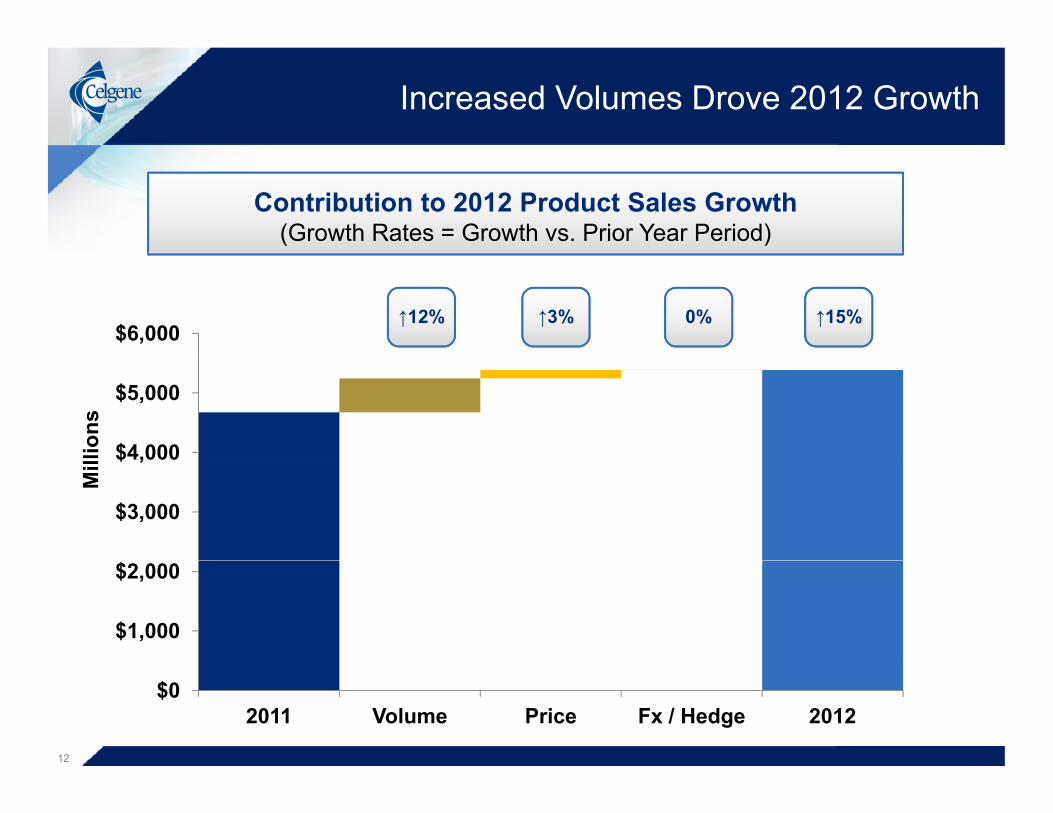

Increased Volumes Drove 2012 Growth

Contribution to 2012 Product Sales Growth(Growth Rates = Growth vs. Prior Year Period)

$6,000↑15%0%↑12% ↑3%

$4,000

$5,000

lions

$3,000

$4,000

Mill

$1,000

$2,000

$02011 Volume Price Fx / Hedge 2012

12

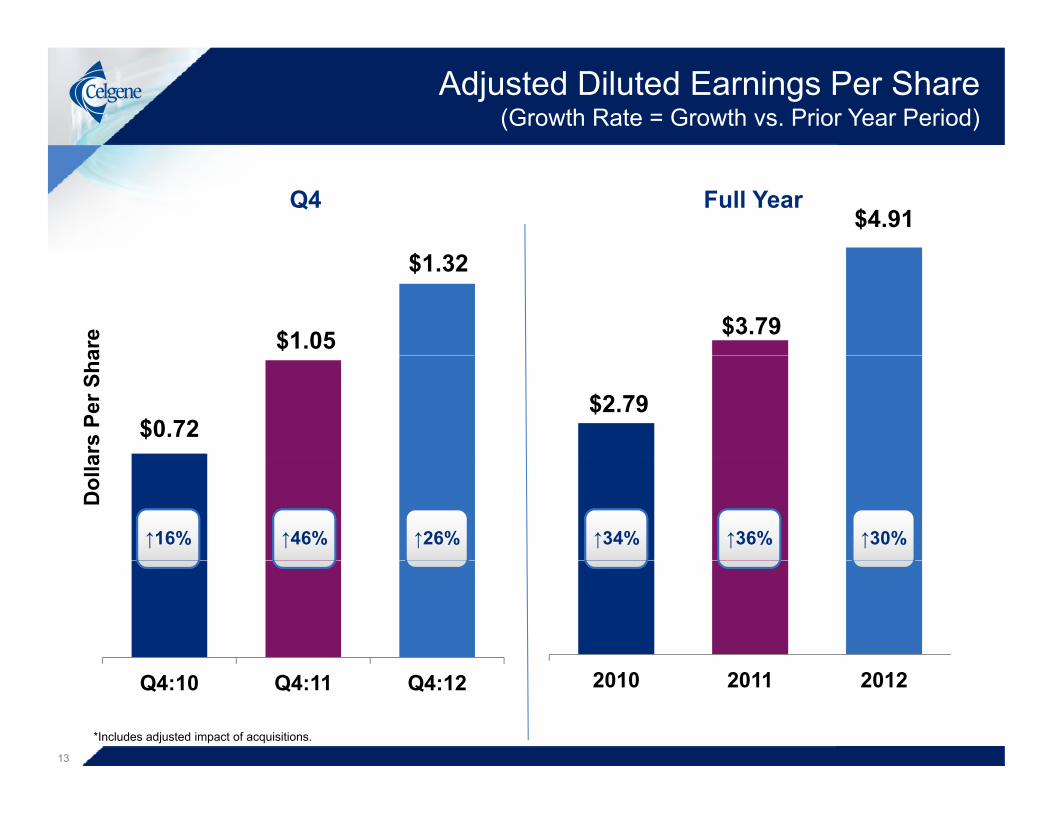

Adjusted Diluted Earnings Per Share (Growth Rate = Growth vs. Prior Year Period)

$

Q4 Full Year$4.91

$1.05

$1.32

$3.79

are

$0.72$2.79

ars

Per S

ha

↑46% ↑26% ↑36% ↑30%↑16% ↑34%

Dol

la

Q4:10 Q4:11 Q4:12 2010 2011 2012

*Includes adjusted impact of acquisitions.

13

Adjusted Diluted EPS Growth Driven by Increased Operating Income

Contribution to Q4:12 Adjusted Diluted EPS

$1.32($0.05)$0.23$1.05 $0.04 $0.05

Shar

eD

olla

rs P

er

D

Q4:11 Operating Income

Financial Income / Expense

Tax Rate Share Count Q4:12

14

Adjusted Diluted EPS Growth Driven by Increased Operating Income

Contribution to 2012 Adjusted Diluted EPS

$4.91($0.07)$0.85$3.79 $0.11 $0.23

Sha

reDo

llars

Per

D

2011 Operating Income

Financial Income / Expense

Tax Rate Share Count 2012

15

Worldwide Product Sales

Product Sales(in millions)

Q4 2012

∆ vs.Q4:11

FY2012

∆ vs.FY11

REVLIMID Total $1,002 ↑17% $3,767 ↑17%

U.S. $577 ↑18% $2,151 ↑17%

International $425 ↑16% $1,616 ↑17%

VIDAZA® Total $216 ↑14% $823 ↑17%

U.S. $88 ↑3% $327 ↑8%

International $128 ↑23% $496 ↑24%

ABRAXANE Total $106 ↑3% $427 ↑11%ABRAXANE Total $106 ↑3% $427 ↑11%

U.S. $84 ↓9% $334 ↑4%

International $22 ↑90% $93 ↑44%International $22 ↑90% $93 ↑44%

16

Total REVLIMID Sales (Growth Rates = Sequential Quarterly Growth)

$738

$861$795

$934

$820

$970

$855

$1,002

$530

$738

$397

$587

$450

$641

$497

$710

s $363 $397

Milli

ons

2009 2010 2011 2012Q1 Q2 Q3 Q4

+7% +11% +9% +11% +1%+8% +3% +4%+4% +8% +4% +3%-2% +9% +13% +10%

17

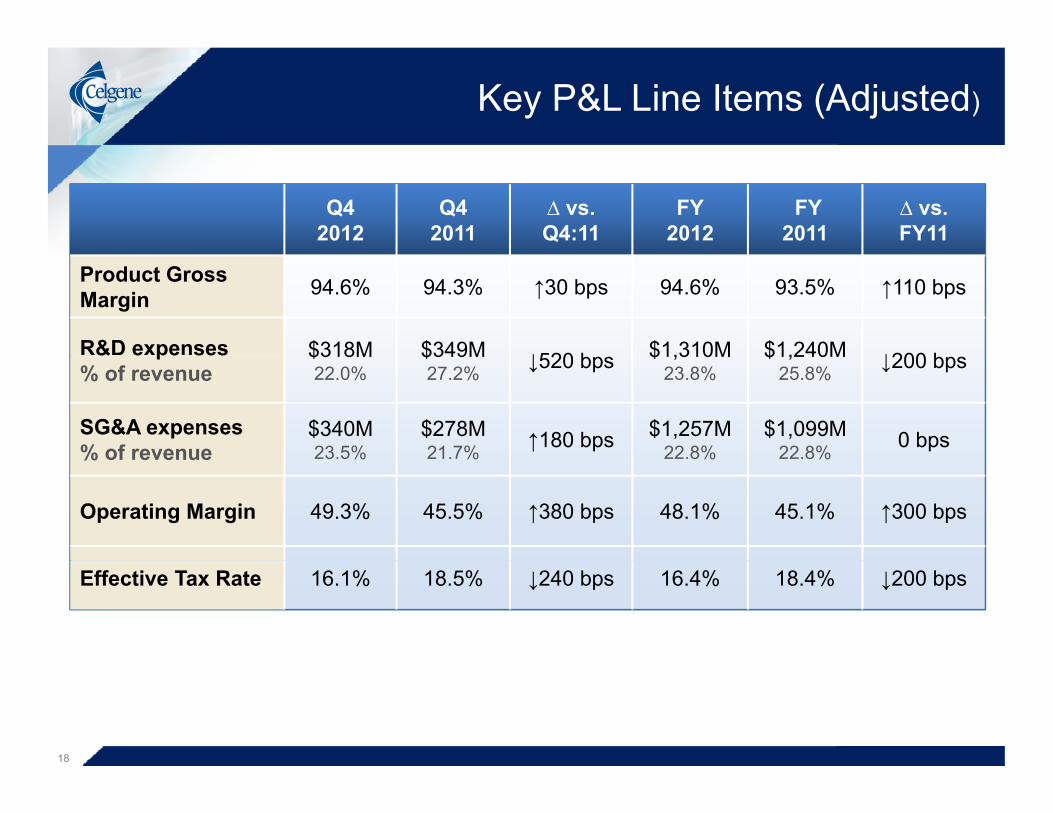

Key P&L Line Items (Adjusted)

Q42012

Q42011

∆ vs.Q4:11

FY2012

FY 2011

∆ vs.FY11

Product Gross Margin 94.6% 94.3% ↑30 bps 94.6% 93.5% ↑110 bps

R&D expenses $318M $349M ↓520 b $1,310M $1,240M ↓200 b& e pe ses% of revenue

$318M 22.0%

$349M 27.2% ↓520 bps $1,310M

23.8%$1,240M

25.8% ↓200 bps

SG&A expenses% of revenue

$340M 23.5%

$278M 21.7% ↑180 bps $1,257M

22.8%$1,099M

22.8% 0 bps% of revenue 23.5% 21.7% 22.8% 22.8%

Operating Margin 49.3% 45.5% ↑380 bps 48.1% 45.1% ↑300 bps

Effective Tax Rate 16.1% 18.5% ↓240 bps 16.4% 18.4% ↓200 bps

18

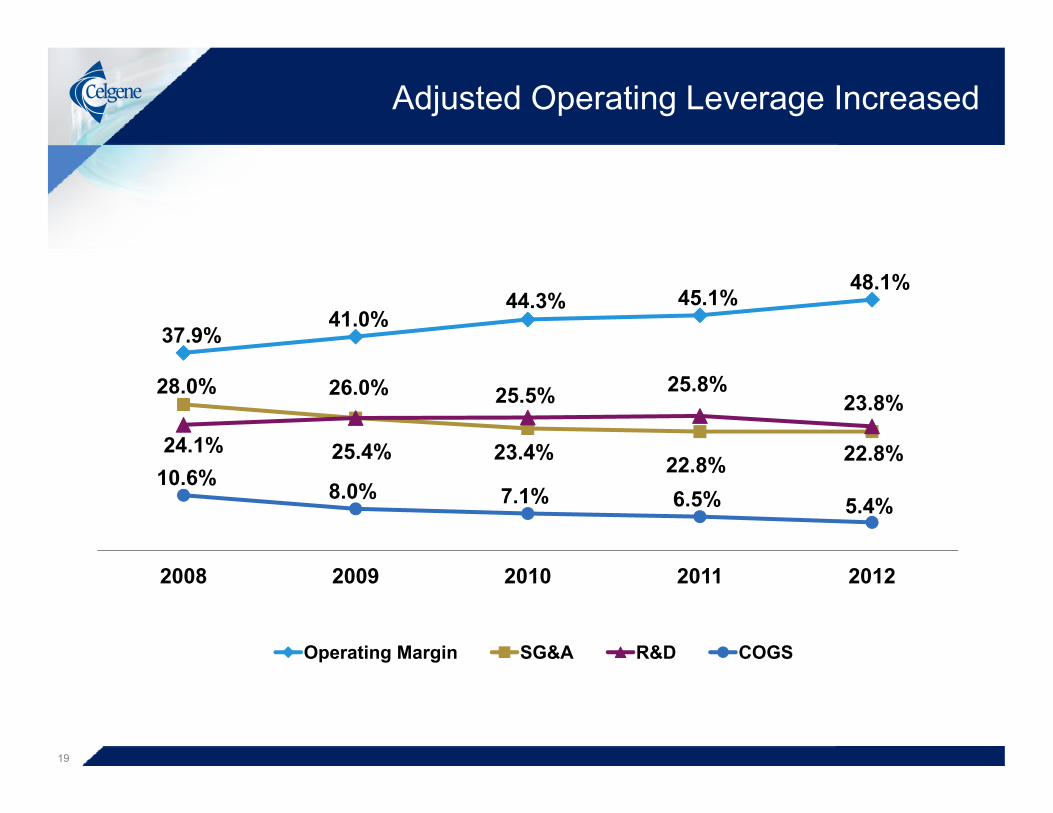

Adjusted Operating Leverage Increased

37.9%41.0%

44.3% 45.1%48.1%

28.0%

25.4% 23.4% 22 8% 22.8%24.1%

26.0% 25.5% 25.8%23.8%

25.4% 23.4% 22.8% 22.8%10.6% 8.0% 7.1% 6.5% 5.4%

2008 2009 2010 2011 2012

Operating Margin SG&A R&D COGS

19

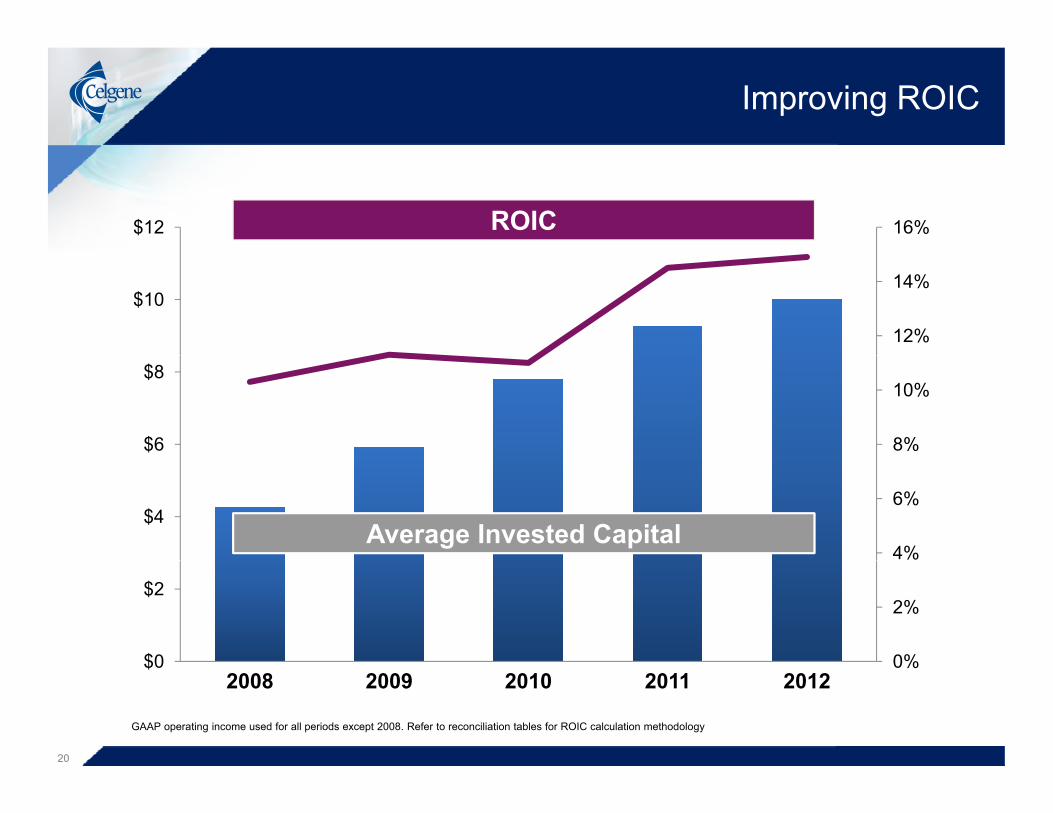

Improving ROIC

16%$12 ROIC

12%

14%$10

8%

10%

$6

$8

4%

6%$4

Average Invested Capital

0%

2%

$0

$2

0%$02008 2009 2010 2011 2012

20

GAAP operating income used for all periods except 2008. Refer to reconciliation tables for ROIC calculation methodology

Cash and Marketable Securities

(in billions) 12/30/12 12/31/11( )

Cash and Marketable Securities $3.90 $2.65

• Cash flow from operations was $2,031M during 20121

• Authorized repurchase of aggregate of $6.5B in common sharesp gg g $– In 2012, purchased 28.6M shares for total cost ~$2.1B– In Q4:12, purchased 7.5M shares for total cost of ~$580M– ~$1.8B remaining under existing stock repurchase program

$• Issued $1.5B in five- and ten-year bonds• In Q4, paid $121M of up front payments for collaborations and

investments

21

1 net of $190 million of payments related to collaboration agreements

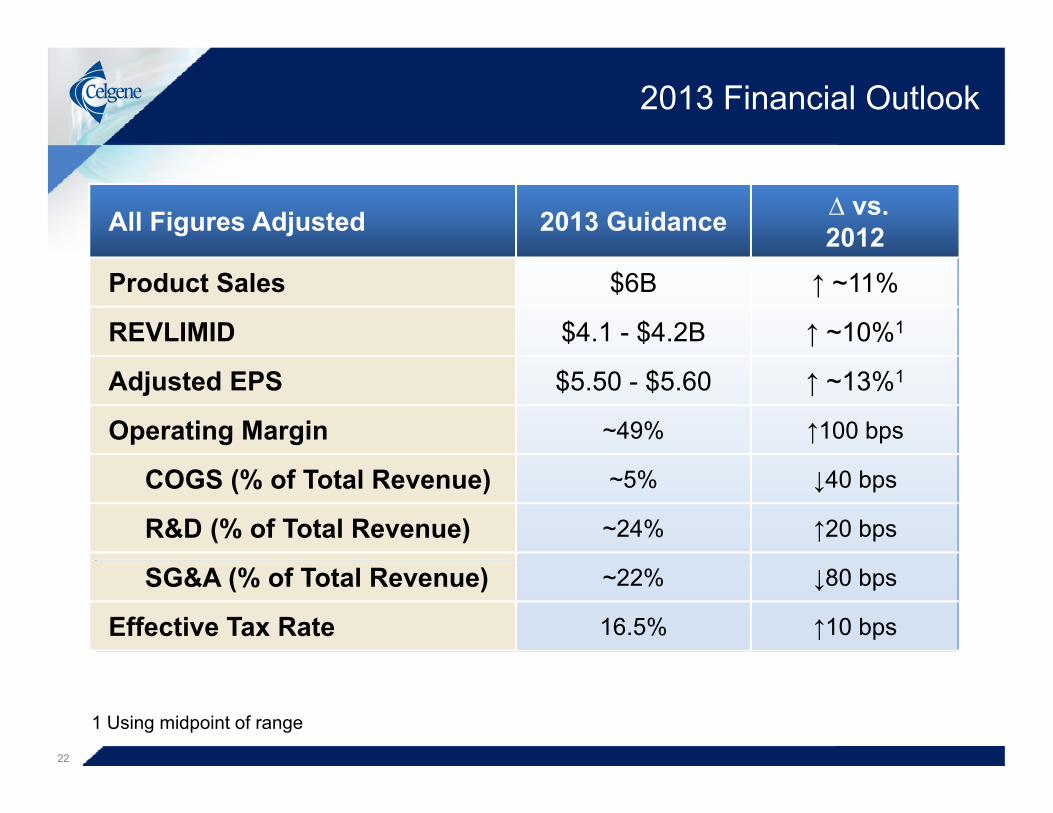

2013 Financial Outlook

All Figures Adjusted 2013 Guidance ∆ vs.2012

Product Sales $6B ↑ ~11%

REVLIMID $4.1 - $4.2B ↑ ~10%1

Adjusted EPS $5.50 - $5.60 ↑ ~13%1

Operating Margin ~49% ↑100 bps

COGS (% of Total Revenue) ~5% ↓40 bps

R&D (% of Total Revenue) ~24% ↑20 bps

SG&A (% of Total Revenue) ~22% ↓80 bps

Effective Tax Rate 16.5% ↑10 bps

1 Using midpoint of range

22

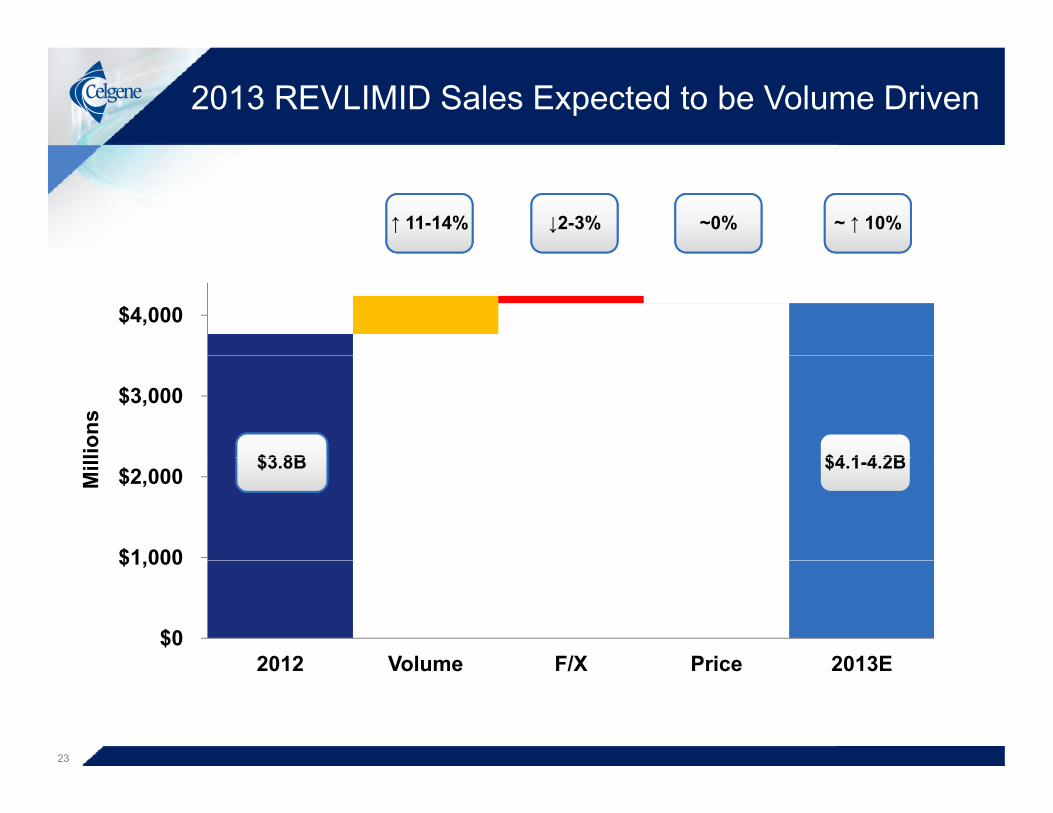

2013 REVLIMID Sales Expected to be Volume Driven

~ ↑ 10%↑ 11-14% ↓2-3% ~0%

$4,000

$3,000

lions

$3 8B $4 1 4 2B

$1 000

$2,000 Mill $3.8B $4.1-4.2B

$0

$1,000

2012 Volume F/X Price 2013E2012 Volume F/X Price 2013E

23

Key Assumptions for 2017 Product Sales Targets

• Strong annual growth in existing franchises• Key approvals: REVLIMID for NDMM (US,EU), MDS (EU), 13% y pp ( , ), ( ),

MCL (US) and POMALYST for RRMM and MF globally• Upside potential: CC-486, CC-292, VIDAZA for AML

13%CAGR

24

Key Assumptions for 2017 Product Sales Targets

• Strong annual growth in existing franchises• Key approvals: REVLIMID for NDMM (US,EU), MDS (EU), 13% y pp ( , ), ( ),

MCL (US) and POMALYST for RRMM and MF globally• Upside potential: CC-486, CC-292, VIDAZA for AML

13%CAGR

+2% points

• ABRAXANE in pancreatic enhances annual growth• Key approvals: pancreatic cancer globally15%

CAGR

+2% points

• Upside potential: melanoma and other cancersCAGR

25

Key Assumptions for 2017 Product Sales Targets

• Strong annual growth in existing franchises• Key approvals: REVLIMID for NDMM (US,EU), MDS (EU), 13% y pp ( , ), ( ),

MCL (US) and POMALYST for RRMM and MF globally• Upside potential: CC-486, CC-292, VIDAZA for AML

13%CAGR

+2% points

• ABRAXANE in pancreatic enhances annual growth• Key approvals: pancreatic cancer globally15%

CAGR

+2% points

• Upside potential: melanoma and other cancersCAGR

+4% points

• Apremilast accelerates annual growth• Key approvals: psoriatic arthritis and psoriasis globally• Upside potential: ankylosing spondylitis and other indications

19%CAGR

Upside potential: ankylosing spondylitis and other indications

26

Key Assumptions for 2017 Earnings Targets

EPS2

($)Hematology

~$12B+

Revenue($B)

25%CAGR1

Oncology

I&I/Other

$12B+

$1.5-2.0B

$1.5-2.0B$13.00 -$14.00

$5 50~$6B

~$8-9B

$1.0-1.25B$0.25-1.0B

$

$8.00 -$9.00

$5.50 -$5.60

$5.3-5.4B

$0.6-0.7B

$6.0-6.5B $8.3-8.8B

2013E 2015E 2017E2013E 2015E 2017E 2013E 2015E 2017E

27

Notes: 1) CAGR calculated using 2013E and 2017 midpoints. 2)Adjusted.

2013E 2015E 2017E

Key Assumptions for 2017 Earnings Targets

EPS2

($)Key Assumptions

25%CAGR1

• Investment in I&I infrastructure

$13.00 -$14.00

$5 50

infrastructure

• Continuous operating margin improvement

$8.00 -$9.00

$5.50 -$5.60

g pthrough 2017

• Tax rate: 16.5%

2013E 2015E 2017E

• Fully diluted sharesoutstanding: 430M

2013E 2015E 2017E

28

Notes: 1) CAGR calculated using 2013E and 2017 midpoints. 2)Adjusted.

2012: Strong Momentum and Investing For The Future

• Performance driven by top line growth and• Performance driven by top-line growth and operating efficiency

• Strength across all operational and financial metrics• Strength across all operational and financial metrics

– Growth rates, Margins, Balance Sheet

• Robust cash flow generation and return of capital to shareholders

R&D i li d l b l i f i i• R&D pipeline and global infrastructure position Celgene well for long-term growth and ongoing P&L leverageg

29

Mark Alles

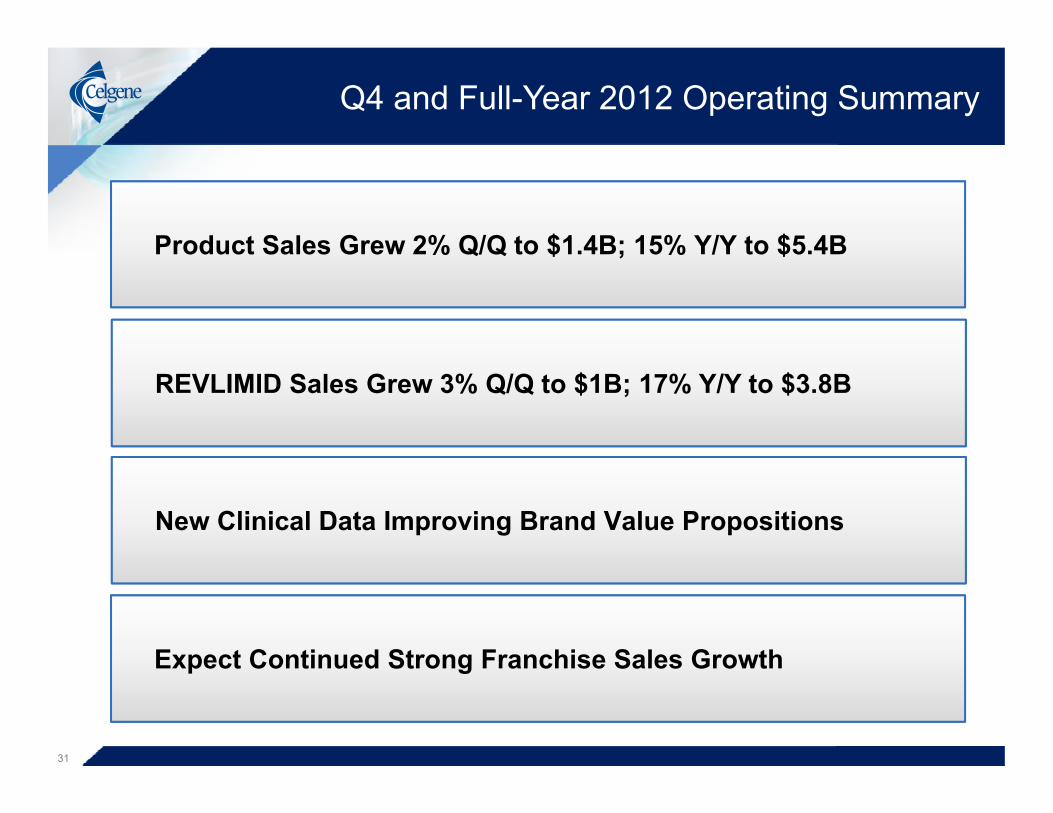

Q4 and Full-Year 2012 Operating Summary

Product Sales Grew 2% Q/Q to $1.4B; 15% Y/Y to $5.4BProduct Sales Grew 2% Q/Q to $1.4B; 15% Y/Y to $5.4B

REVLIMID Sales Grew 3% Q/Q to $1B; 17% Y/Y to $3.8B

New Clinical Data Improving Brand Value Propositions

Expect Continued Strong Franchise Sales GrowthExpect Continued Strong Franchise Sales Growth

31

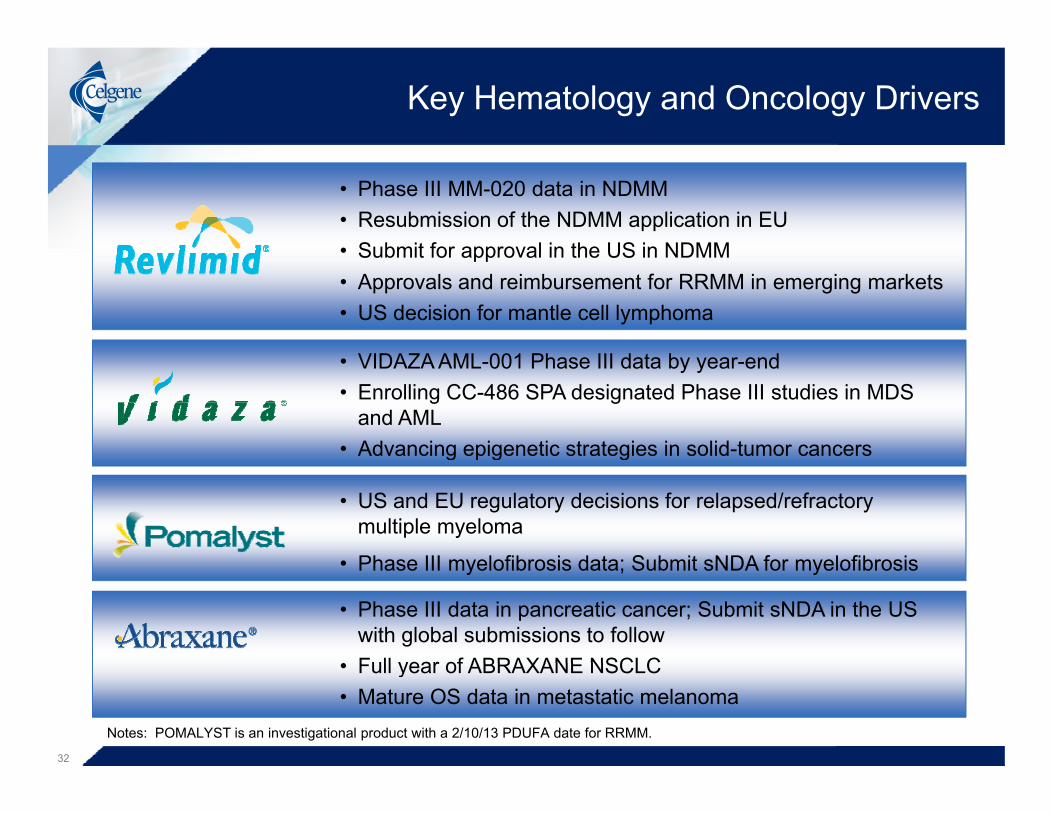

Key Hematology and Oncology Drivers

• Phase III MM-020 data in NDMM• Resubmission of the NDMM application in EU• Submit for approval in the US in NDMM

VIDAZA AML 001 Ph III d t b d

Submit for approval in the US in NDMM• Approvals and reimbursement for RRMM in emerging markets• US decision for mantle cell lymphoma

• VIDAZA AML-001 Phase III data by year-end• Enrolling CC-486 SPA designated Phase III studies in MDS

and AML• Advancing epigenetic strategies in solid-tumor cancers g p g g

• US and EU regulatory decisions for relapsed/refractorymultiple myeloma

• Phase III myelofibrosis data; Submit sNDA for myelofibrosis• Phase III myelofibrosis data; Submit sNDA for myelofibrosis

• Phase III data in pancreatic cancer; Submit sNDA in the US with global submissions to follow

• Full year of ABRAXANE NSCLC• Full year of ABRAXANE NSCLC• Mature OS data in metastatic melanoma

Notes: POMALYST is an investigational product with a 2/10/13 PDUFA date for RRMM.

32

Key Hematology and Oncology Drivers

• Phase III MM-020 data in NDMM• Resubmission of the NDMM application in EU• Submit for approval in the US in NDMM

VIDAZA AML 001 Ph III d t b d

Submit for approval in the US in NDMM• Approvals and reimbursement for RRMM in emerging markets• US decision for mantle cell lymphomaNear-term Milestones• VIDAZA AML-001 Phase III data by year-end• Enrolling CC-486 SPA designated Phase III studies in MDS

and AML• Advancing epigenetic strategies in solid-tumor cancers

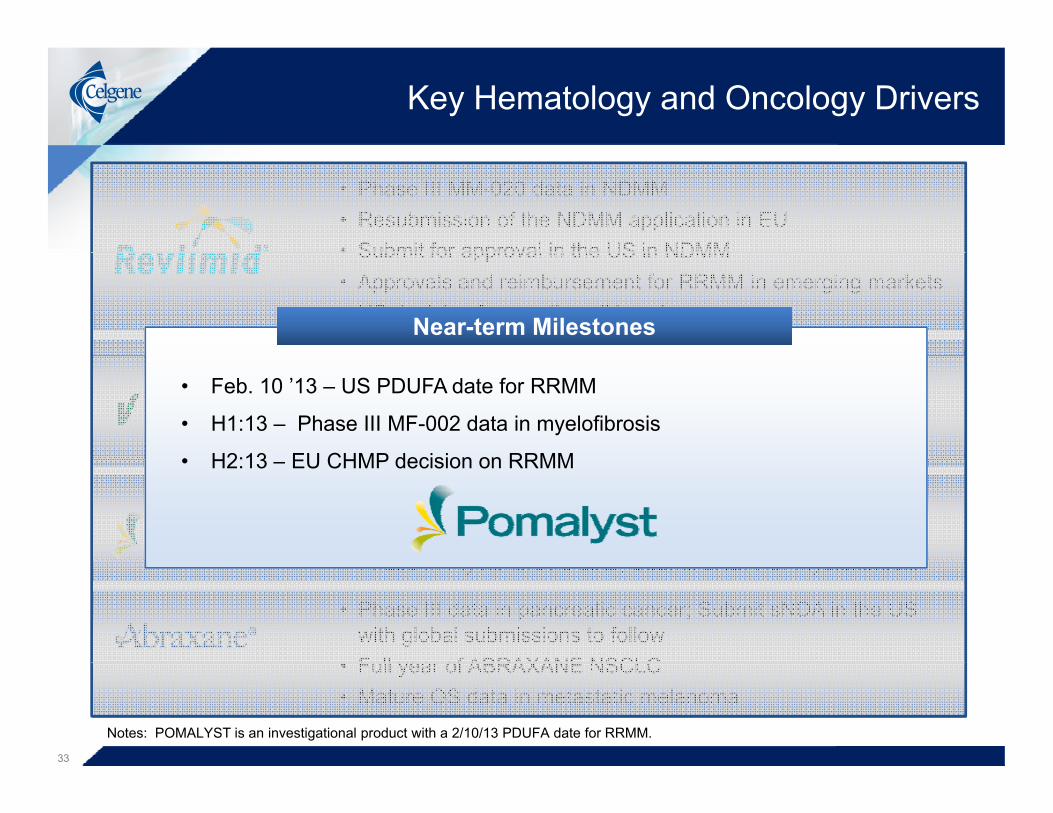

• Feb. 10 ’13 – US PDUFA date for RRMM

• H1:13 – Phase III MF-002 data in myelofibrosis

H2:13 EU CHMP decision on RRMMg p g g

• US and EU regulatory decisions for relapsed/refractorymultiple myeloma

• Phase III myelofibrosis data; Submit sNDA for myelofibrosis

• H2:13 – EU CHMP decision on RRMM

• Phase III myelofibrosis data; Submit sNDA for myelofibrosis

• Phase III data in pancreatic cancer; Submit sNDA in the US with global submissions to follow

• Full year of ABRAXANE NSCLC• Full year of ABRAXANE NSCLC• Mature OS data in metastatic melanoma

Notes: POMALYST is an investigational product with a 2/10/13 PDUFA date for RRMM.

33

Key Hematology and Oncology Drivers

• Phase III MM-020 data in NDMM• Resubmission of the NDMM application in EU• Submit for approval in the US in NDMM

VIDAZA AML 001 Ph III d t b d

Submit for approval in the US in NDMM• Approvals and reimbursement for RRMM in emerging markets• US decision for mantle cell lymphoma

• VIDAZA AML-001 Phase III data by year-end• Enrolling CC-486 SPA designated Phase III studies in MDS

and AML• Advancing epigenetic strategies in solid-tumor cancers

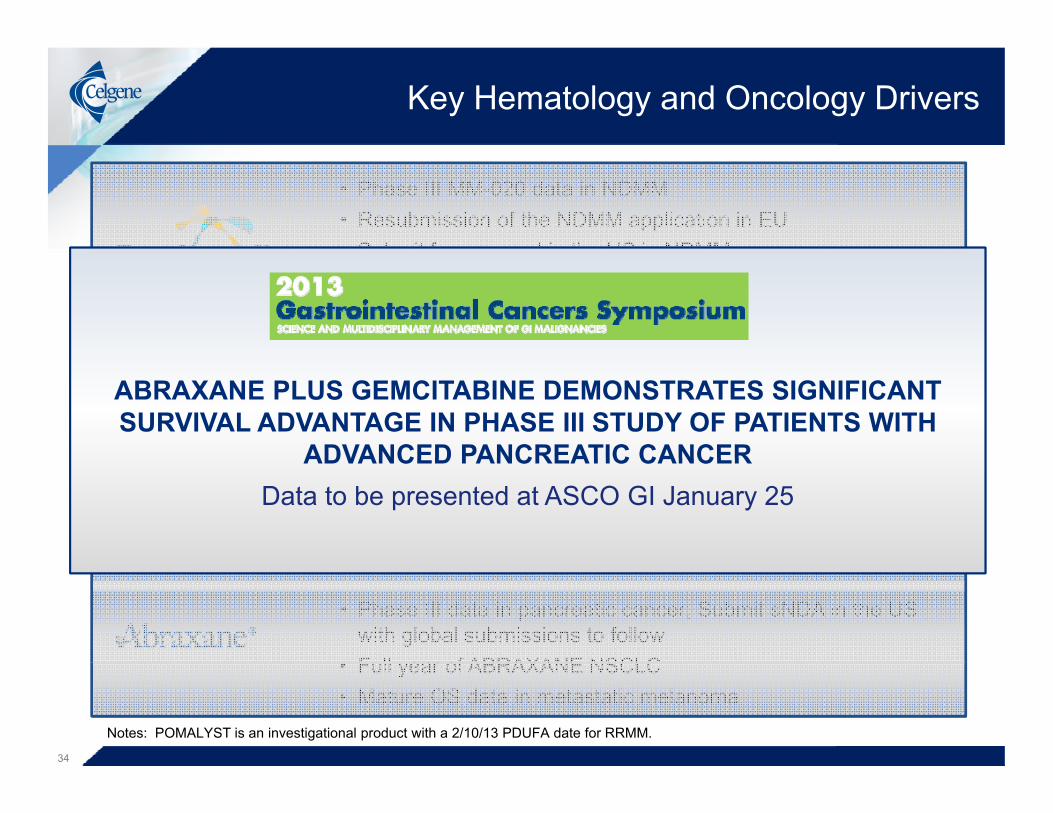

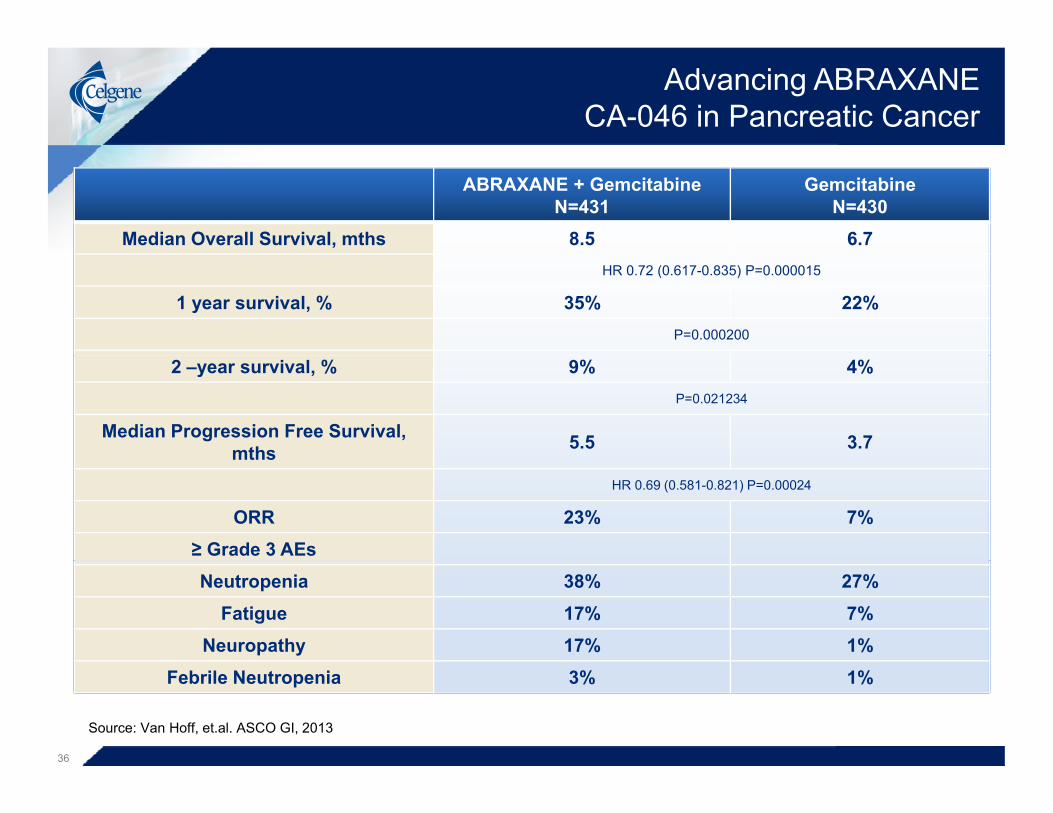

ABRAXANE PLUS GEMCITABINE DEMONSTRATES SIGNIFICANT SURVIVAL ADVANTAGE IN PHASE III STUDY OF PATIENTS WITH

ADVANCED PANCREATIC CANCERg p g g

• US and EU regulatory decisions for relapsed/refractorymultiple myeloma

• Phase III myelofibrosis data; Submit sNDA for myelofibrosis

ADVANCED PANCREATIC CANCERData to be presented at ASCO GI January 25

• Phase III myelofibrosis data; Submit sNDA for myelofibrosis

• Phase III data in pancreatic cancer; Submit sNDA in the US with global submissions to follow

• Full year of ABRAXANE NSCLC• Full year of ABRAXANE NSCLC• Mature OS data in metastatic melanoma

Notes: POMALYST is an investigational product with a 2/10/13 PDUFA date for RRMM.

34

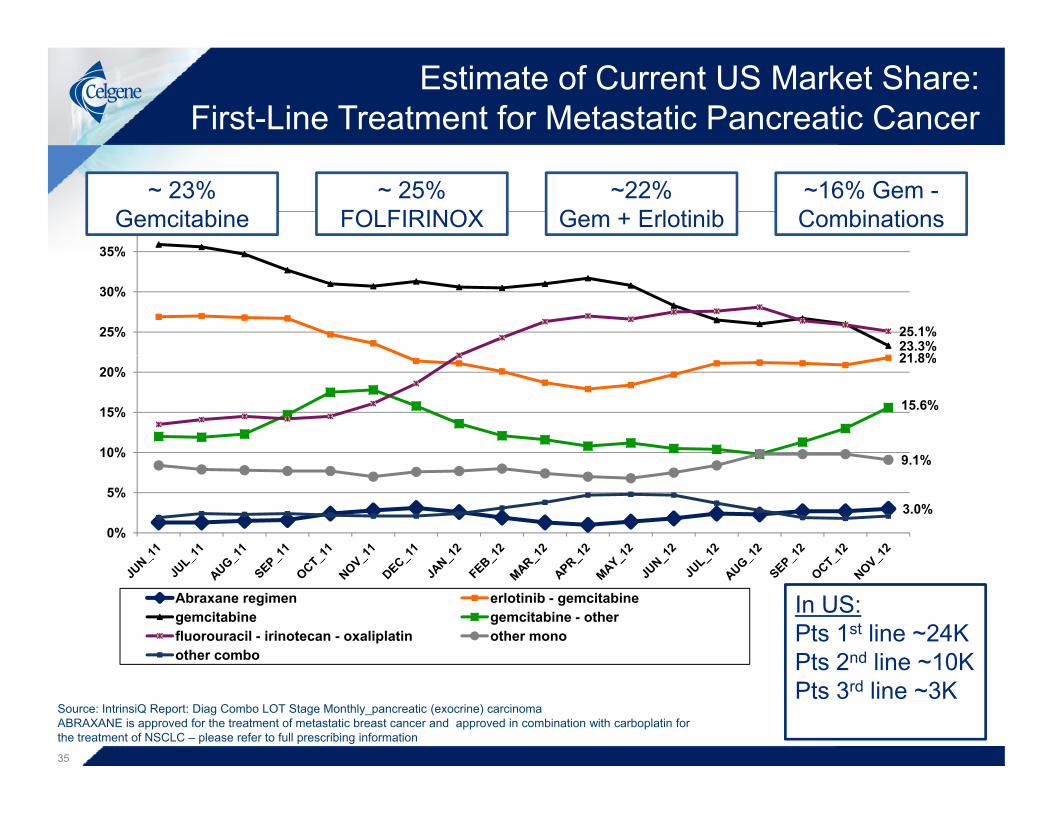

Estimate of Current US Market Share: First-Line Treatment for Metastatic Pancreatic Cancer

35%

40%~ 23%

Gemcitabine~ 25%

FOLFIRINOX~22%

Gem + Erlotinib~16% Gem -Combinations

21 8%23.3%25.1%25%

30%

35%

21.8%

15.6%

9 1%10%

15%

20%

3.0%

9.1%

0%

5%

Abraxane regimen erlotinib - gemcitabinegemcitabine gemcitabine - otherfluorouracil - irinotecan - oxaliplatin other monoother combo

In US:Pts 1st line ~24KPts 2nd line ~10K

Source: IntrinsiQ Report: Diag Combo LOT Stage Monthly_pancreatic (exocrine) carcinomaABRAXANE is approved for the treatment of metastatic breast cancer and approved in combination with carboplatin for the treatment of NSCLC – please refer to full prescribing information

Pts 2 line ~10KPts 3rd line ~3K

35

Advancing ABRAXANECA-046 in Pancreatic Cancer

ABRAXANE + GemcitabineN=431

GemcitabineN=430

Median Overall Survival, mths 8.5 6.7HR 0.72 (0.617-0.835) P=0.000015

1 year survival, % 35% 22%P=0.000200

2 –year survival, % 9% 4%P=0.021234

Median Progression Free Survival, mths 5.5 3.7mths

HR 0.69 (0.581-0.821) P=0.00024

ORR 23% 7%≥ Grade 3 AEsNeutropenia 38% 27%

Fatigue 17% 7%Neuropathy 17% 1%

Febrile Neutropenia 3% 1%

Source: Van Hoff, et.al. ASCO GI, 2013

36

Advancing a Industry Leading Hematology/Oncology Franchise

Global Market Leader in Multiple Myeloma

Global Market Leader in Higher-risk MDSin Multiple Myeloma

Standard treatment for del 5q MDS

in Higher risk MDS

Advancing Clinical Development in AML

Expansion in Metastatic Breast Cancer Approved in R/R PTCL

in the USOpportunities in Lung, Pancreas, Melanoma Global Expansion

Transformed Treatment of Multiple Myeloma

Remains a Standard Relapsed/Refractory

Multiple Myeloma*

Myeloma Therapy

Notes: POMALYST is an investigational product with a 2/10/13 PDUFA date for RRMM.

37

Bob Hugin

Key Milestones – 2013

Product Milestone Expected Timing

• Phase III MM-020 data in NDMM Q1:13

• Resubmission of the NDMM application in EU H2:13• Resubmission of the NDMM application in EU H2:13

• Submit for approval in the US in NDMM H2:13

• Approvals and reimbursement for RRMM in emerging markets Throughout 2013

• US decision for mantle cell lymphoma YE:13

• Regulatory decisions for relapsed refractory multiple myeloma US: Q1:13, EU: H2:13

• Phase III myelofibrosis data H1:13

• Submit sNDA for myelofibrosis H2:13

• Submit sNDA for pancreatic cancer H1:13

• Mature phase III overall survival data in melanoma Mid-13

• FDA decision for pancreatic cancer YE:13/H1:14

Phase III ESTEEM data in psoriasis Q1:13

Apremilast

Phase III ESTEEM data in psoriasis Q1:13

• Submit for approval in psoriatic arthritis and psoriasis Throughout 2013

• Phase III data in treatment-naïve psoriatic arthritis H1:13

• Complete enrollment in Phase III ankylosing spondylitis trial H2:13

39

Appendix

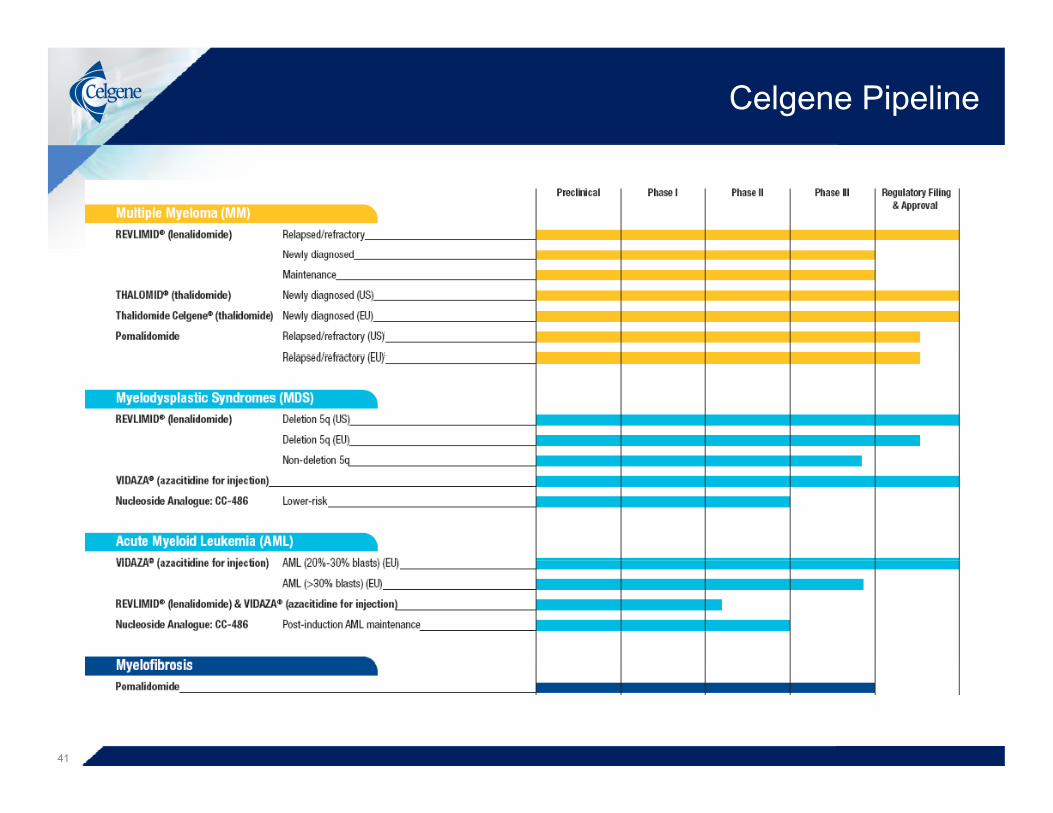

Celgene Pipeline

41

Celgene Pipeline

42

Celgene Pipeline

43

Multiple Myeloma Late Stage Programs

Molecule Revlimid(lenalidomide)

Revlimid(lenalidomide)

Revlimid(lenalidomide)

Revlimid(lenalidomide)

Pomalyst (Pomalidomide)

MM-020 MM-007Trial Name MM-015 CALGB 100104 IFM 2005-02 MM-020FIRST

MM-007OPTIMISMM

Phase Phase III Phase III Phase III Phase III Phase III

dMM & P t ASCT P t ASCTIndication ndMM & maintenance

Post-ASCTmaintenance

Post-ASCT maintenance ndMM RRMM

Target Enrollment 459 460 614 1,623 782

DesignArm A: MPR+R

Arm B: MPRArm C: MP

Arm A: RevlimidArm B: Placebo

Arm A: RevlimidArm B: Placebo

Arm A: Rd to progression

Arm B: Rd fixed

Arm C: MPT

Arm A: PVdArm B: Vd

Arm C: MPT

Primary Endpoint PFS TTP PFS PFS PFS

Completed; Completed; Completed; Enrollment Status Continuing

follow-upContinuing follow-up

Continuing follow-up

complete; Data in Q1:13(E)

Enrolling

44

Multiple Myeloma Late Stage Programs

Molecule Pomalyst (Pomalidomide)

Pomalyst (Pomalidomide)

Pomalyst (Pomalidomide)

MM-003 MM-009 MM-010Trial Name MM-003NIMBUS

MM-009PEXIUS

MM-010STRATUS

Phase Phase III EAP Phase III

Indication RRMM RRMM RRMM

Target Enrollment 426 507

Design Arm A: PdArm B: HiDex Pd Pd

Primary Endpoint PFS Early access

protocol Adverse Events

Status

Enrollment complete; Data

presented at ASH 2012

Enrolling Enrolling

45

MDS/AML/MF Late Stage Programs

Molecule Revlimid(lenalidomide)

Vidaza(azacitidine)

CC-486 CC-486 Pomalyst(pomalidomide)

Quazar AML

Trial Name MDS-005 AZA-AML-001Quazar Lower-

Risk MDSAZA-MDS-003

Quazar AML Maintenance CC-486-AML-

001

MF-002RESUME

Phase Phase III Phase III Phase III Phase III Phase III

Indication Non-del5Q Low Risk/INT-1 MDS AML Lower Risk

MDS

Post-induction AML

maintenanceMyelofibrosis

Target 228 480 386 460 210Enrollment 228 480 386 460 210

Design Arm A: RevlimidArm B: Placebo

Arm A: VidazaArm B:

Conventional C

Arm A: CC-486Arm B: BSC

Arm A: CC-486Arm B: BSC

Arm A: Pomalidomide

Arm B: PlaceboCare

Primary Endpoint

RBC-transfusion

independenceOS

RBC-transfusion

independenceOS RBC-transfusion

independence

E ll t E ll tStatus Enrolling

Enrollment complete; Data

in H2:13(E)Enrolling Enrolling

Enrollment complete; Data

in 2013(E)

46

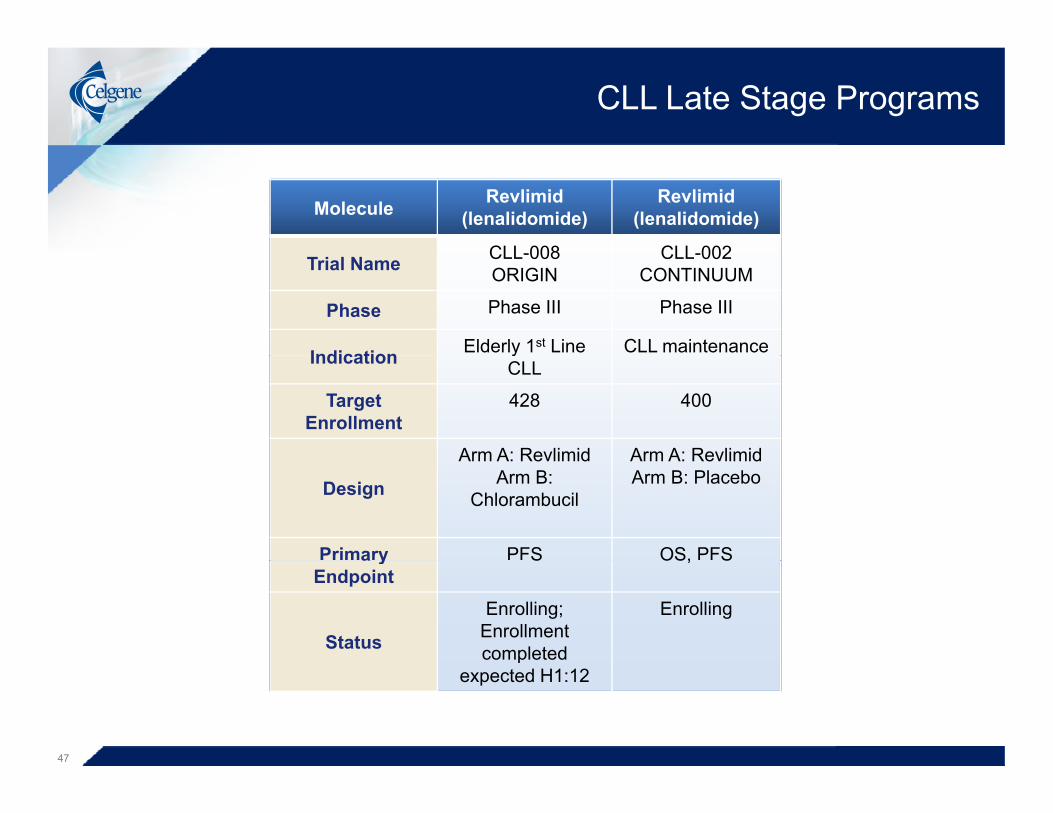

CLL Late Stage Programs

Molecule Revlimid(lenalidomide)

Revlimid(lenalidomide)

CLL 008 CLL 002Trial Name CLL-008ORIGIN

CLL-002CONTINUUM

Phase Phase III Phase III

Indication Elderly 1st Line CLL maintenanceIndication yCLL

Target Enrollment

428 400

Arm A: Revlimid Arm A: Revlimid

Design

Arm A: RevlimidArm B:

Chlorambucil

Arm A: RevlimidArm B: Placebo

Primary PFS OS, PFSa yEndpoint

S OS, S

Status

Enrolling; Enrollment completed

Enrolling

pexpected H1:12

47

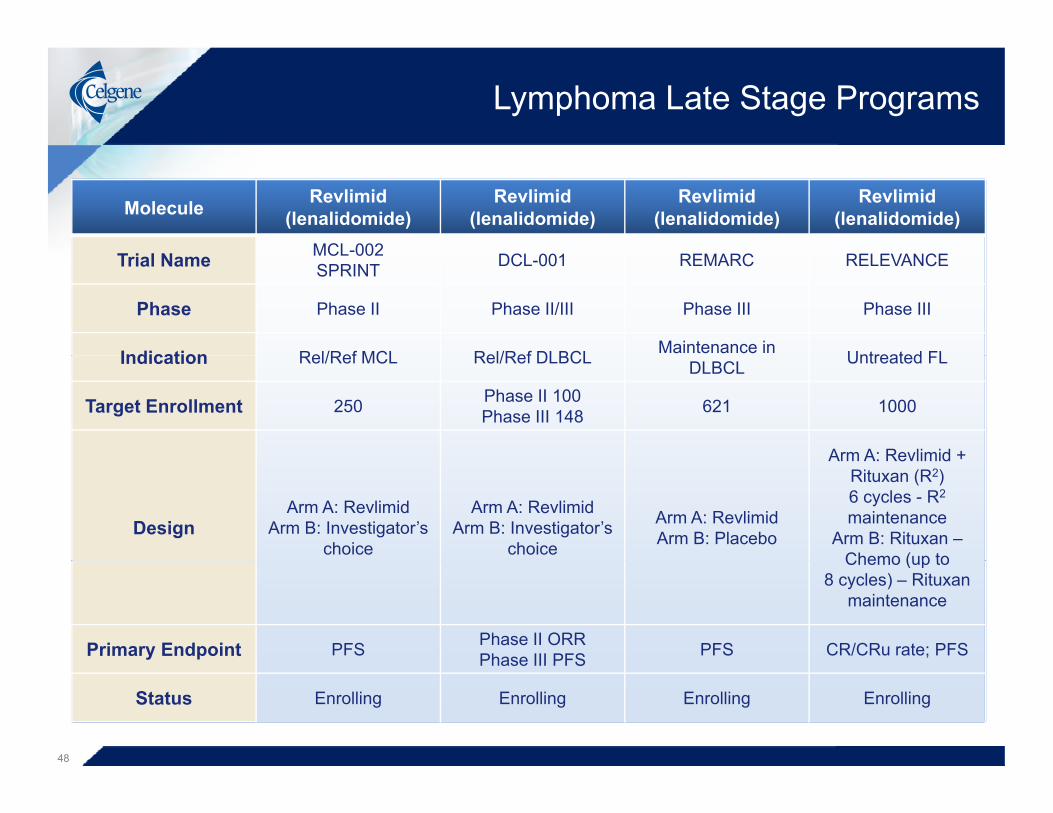

Lymphoma Late Stage Programs

Molecule Revlimid(lenalidomide)

Revlimid(lenalidomide)

Revlimid(lenalidomide)

Revlimid(lenalidomide)

MCL-002Trial Name MCL 002SPRINT DCL-001 REMARC RELEVANCE

Phase Phase II Phase II/III Phase III Phase III

Indication Rel/Ref MCL Rel/Ref DLBCL Maintenance in Untreated FLIndication Rel/Ref MCL Rel/Ref DLBCL DLBCL Untreated FL

Target Enrollment 250 Phase II 100Phase III 148 621 1000

Arm A: Revlimid +

DesignArm A: Revlimid

Arm B: Investigator’s choice

Arm A: RevlimidArm B: Investigator’s

choice

Arm A: RevlimidArm B: Placebo

Arm A: Revlimid + Rituxan (R2) 6 cycles - R2

maintenanceArm B: Rituxan –

Chemo (up toChemo (up to 8 cycles) – Rituxan

maintenance

Primary Endpoint PFS Phase II ORRPhase III PFS PFS CR/CRu rate; PFSPhase III PFS

Status Enrolling Enrolling Enrolling Enrolling

48

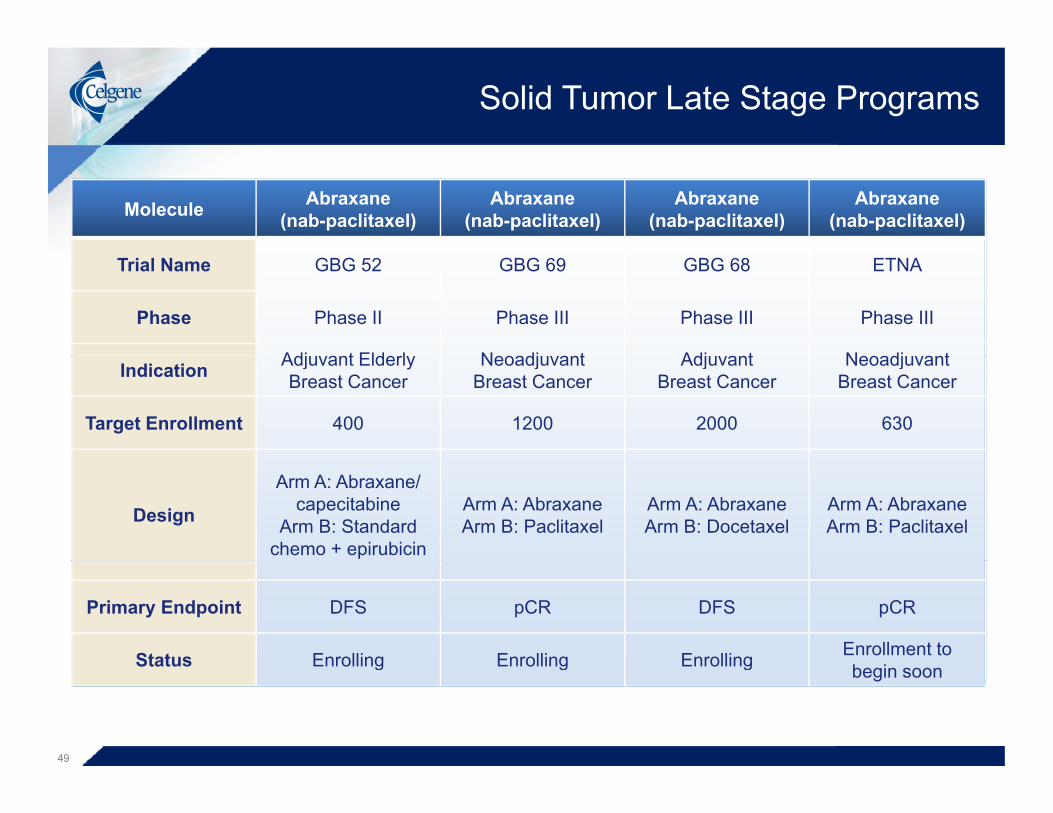

Solid Tumor Late Stage Programs

Molecule Abraxane(nab-paclitaxel)

Abraxane(nab-paclitaxel)

Abraxane(nab-paclitaxel)

Abraxane(nab-paclitaxel)

Trial Name GBG 52 GBG 69 GBG 68 ETNA

Phase Phase II Phase III Phase III Phase III

Adj t Eld l N dj t Adj t N dj tIndication Adjuvant Elderly Breast Cancer

Neoadjuvant Breast Cancer

Adjuvant Breast Cancer

Neoadjuvant Breast Cancer

Target Enrollment 400 1200 2000 630

Design

Arm A: Abraxane/ capecitabine

Arm B: Standard chemo + epirubicin

Arm A: AbraxaneArm B: Paclitaxel

Arm A: AbraxaneArm B: Docetaxel

Arm A: AbraxaneArm B: Paclitaxel

Primary Endpoint DFS pCR DFS pCR

Status Enrolling Enrolling Enrolling Enrollment to Status Enrolling Enrolling Enrolling begin soon

49

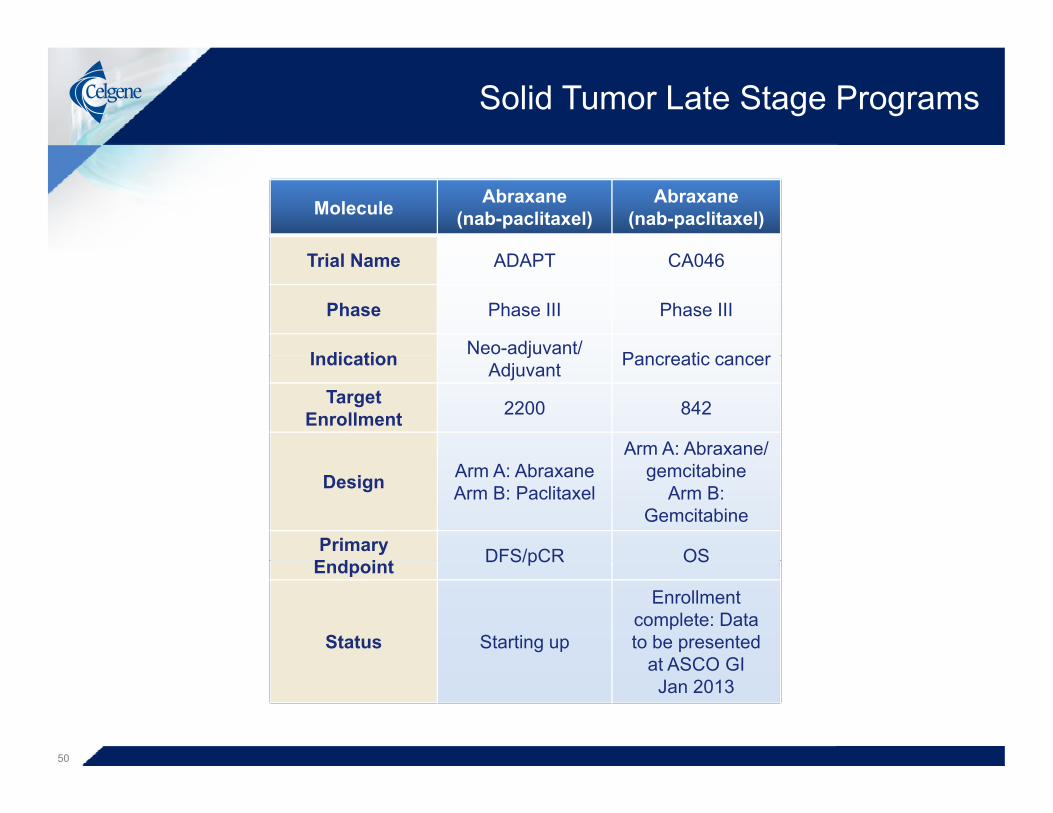

Solid Tumor Late Stage Programs

Molecule Abraxane(nab-paclitaxel)

Abraxane(nab-paclitaxel)

Trial Name ADAPT CA046

Phase Phase III Phase III

Indication Neo-adjuvant/ Pancreatic cancerIndication jAdjuvant Pancreatic cancer

Target Enrollment 2200 842

Arm A: Abraxane/

Design Arm A: AbraxaneArm B: Paclitaxel

gemcitabineArm B:

GemcitabinePrimary

E d i t DFS/pCR OSEndpoint DFS/pCR OS

Status Starting up

Enrollment complete: Data to be presented

at ASCO GIat ASCO GI Jan 2013

50

I&I Late Stage Programs

Molecule Apremilast Apremilast Apremilast Apremilast

PALACE-1 PALACE-2 PALACE-3 ESTEEM-1Trial Name PALACE 1PSA-002

PALACE 2PSA-003

PALACE 3PSA-004

ESTEEM 1PSOR-008

Phase Phase III Phase III Phase III Phase III

I di ti P i ti A th iti P i ti A th iti Psoriatic Arthritis P i iIndication Psoriatic Arthritis Psoriatic Arthritis with skin lesions Psoriasis

Target Enrollment 495 495 495 825

Arm A: Arm A: Arm A:

DesignApremilast 30mg

Arm B: Apremilast 20mgArm C: Placebo

Apremilast 30mgArm B:

Apremilast 20mgArm C: Placebo

Apremilast 30mgArm B:

Apremilast 20mgArm C: Placebo

Arm A: ApremilastArm B: Placebo

Primary Endpoint ACR20 ACR20 ACR20 PASI75

Status

Enrollmentcomplete;

P t d t

Enrollmentcomplete; Top line

Enrollmentcomplete; Top line

Top line data in Jan 2013: Data to b t d iStatus Presented at

ACR 2012

complete; Top line data Sep 2012

complete; Top line data Sep 2012 be presented in

2013

51

I&I Late Stage Programs

Molecule Apremilast Apremilast Apremilast Apremilast

Trial Name ESTEEM-2PSOR-009

PALACE-4PSA-005

POSTUREAS-001 PSOR-010

Phase Phase III Phase III Phase III Phase IIIb

Indication Psoriasis Untreatedpsoriatic arthritis

AnklylosingSpondylitis

Moderate to severe plaque psoriatic arthritis Spondylitis psoriasis

Target Enrollment 413 495 456 240

Arm A: Arm A:Apremilast Arm A:

DesignArm A:

ApremilastArm B: Placebo

Apremilast 30mgArm B:

Apremilast 20mgArm C: Placebo

Apremilast 30mgArm B:

Apremilast 20mgArm C: Placebo

Apremilast 30mgArm B:

Entanercept 50mg

Primary Endpoint PASI75 ACR20 ASAS20 PASI75

Status

Top line data in Jan 2013: Data Enrollment

Complete; Data Enrolling; Data EnrollingStatus to be presented in 2013

Complete; Data expected Q1:13 expected Q1:14 Enrolling

52

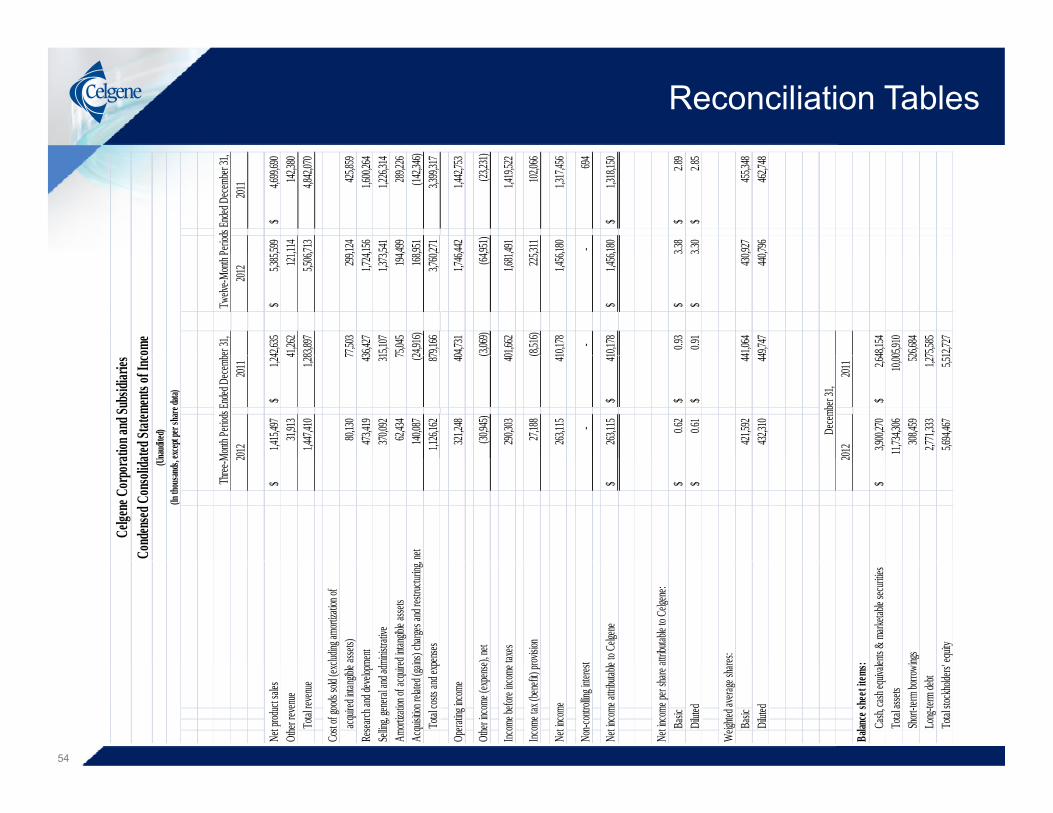

Reconciliation Tables

Reconciliation Tables

2011

,599

4,699,

690$

,11

4142

,380

,71

34,8

42,070

,124

425,85

9

,156

1,600,

264

,54

11,2

26,314

,499

289,22

6

,951

(142,3

46)

,271

3,399,

317

,442

1,442,

753

,951)

(23,23

1)

,491

1,419,

522

,311

102,06

6

,180

1,317,

456

- 694

,180

1,318,

150$

3.38

2.89

$

3.30

2.85

$

,927

455,34

8

,796

462,74

8

Perio

ds En

ded D

ecemb

er 31,

2012

42,635

5,385,

$

41,262

121,

83,

8975,5

06,

77,503

299,

36,

4271,7

24,

15,

1071,3

73,

75,

045194

,

24,916

)168

,

79,166

3,760,

04,731

1,746,

(3,069

)(64

,

01,662

1,681,

(8,516

)225

,

10,178

1,456,

-

10,178

1,456,

$

0.93

3

$

0.91

3

$

41,064

430,

49,

747440

,

48,154

05,910

26,684

75,585

12,727om

e

er 31,

Twelv

e-Mont

h P201

2201

1

1,415,

497

1,24

$

31,913

4

1,447,

410

1,28

80,130

7

473,41

9

43

370

,092

31

62,434

7

140,08

7

(2

1,1

26,162

8 7

321,24

8

4 0

(30,94

5)

(

290,30

3

4 0

27,188

(

263,11

5

4 1

-

263,11

5

41

$

0.62

$

0.6

1

$

421,59

2

44

432

,310

44

2012

2011

3,900,

270

2,64

$

11,734

,306

10,

00

308

,459

5 2

2,771,

333

1,27

5,694,

467

5,51

Decem

ber 31

,

ation

and S

ubsid

iaries

ated S

tatem

ents

of Inc

naud

ited)

except

per s

hare

data)

Month

Perio

ds En

ded D

ecemb

2

$

net

$

$

$

2

$

Celge

ne C

orpo

raCo

nden

sed C

onso

lida (Un

(In th

ousan

ds, e

Three

-M

cludin

g amo

rtizatio

n of

assets

)me

ntmin

istrativ

eed

intangi

ble as

sets

ins) c

harges

and r

estruc

turing

, pen

ses

e), ne

t

taxes

rovisio

n

t e to C

elgene

attrib

utable

to Ce

lgene:

res:

: ents &

mark

etable

secur

ities

ings equ

it y

54

Net p

roduct

sales

Other

reven

ueTo

tal rev

enue

Cost o

f good

s sold

(exc

acquir

ed inta

ngible

Re

search

and d

evelop

mSe

lling, g

eneral

and a

dmAm

ortiza

tion of

acqui

reAc

quisiti

on rel

ated (

gain

Total

costs a

nd exp

Opera

ting inc

ome

Other

incom

e (exp

ense

Incom

e befo

re inc

ome

Incom

e tax

(benef

it) p r

Net in

come

Non-c

ontrol

ling int

eres t

Net in

come a

ttribut

able

Net in

come p

er sha

re a

Basic

Dilute

d

Weigh

ted av

erage

shar

Basic

Dilute

d

Balan

ce sh

eet it

ems :

Cash,

cash

equiva

leTo

tal ass

etsSh

ort-te

rm bo

rrow in

Long-

term

debt

Total

stockh

olders

'

Reconciliation Tables

2011

180

1,318

,150

$

-(26

,688)

-

(1,71

4)

413

9,762

-90

,278

55

3)23

,032

413

104,7

04

-8,7

28

50

911

8,000

50

012

8,479

217

102,7

36

-15

,065

-

9,814

499

289,2

26

374

(147,4

63)

57

75,1

17

-64

4

-

2,036

-(2,

931)

-(69

4)

643)

(293,3

73)

486

1,752

,908

$

.023.8

5$

.91

3.79

$

res t

hat w

e beli

eve

sons

betw

een p

eriod

s and

or

matio

n pre

pare

d in

nd th

at do

not m

eet th

e

eriod

s End

ed D

ecem

ber 3

1,20

12

10,17

81,4

56,1

$

(1,75

2)-

-

-

2,708

12

, 4

-

3,744

(1,

5

24,70

510

2,4

-

-

-

122, 5

62

,497

189,5

26,83

111

6,2

-

-

9,814

-

75,04

519

4,4

24,91

6)16

6,3

-

2, 5

102

-

-

-

-

-

-

-

15,89

8)(19

8,6

73,05

82,1

62,4

$

1.07

5

$

1.05

4

$

ains a

djus

ted fi

nanc

ial m

easu

trend

s tha

t fac

ilitate

comp

aris

ot as

a su

bstitu

te fo

r, the

info

ffect

our b

asic

oper

ation

s an

ent w

ays.

come

er 31

,Tw

elve-M

onth

P20

1220

11

263,1

15

41

$

-

(

-

3,240

-

44

1

26,55

5

2

-

69,15

6

59

,500

6

30,20

7

2

-

-

62,43

4

7

140,0

87

(2

-

-

-

-

-

(82,52

1)

(1 1

572,2

14

4 7

$

1.36

$

1.3

2

$

this

pres

s rele

ase a

lso co

ntaop

erati

ng pe

rform

ance

and t

nside

red i

n add

ition t

o, bu

t no

anag

emen

t doe

s not

belie

ve af

fine t

hese

mea

sure

s in d

iffer

e

ation

and S

ubsid

iaries

AP to

Adj

usted

Net

Inc

exce

pt pe

r sha

re da

ta)

Mon

th Pe

riods

End

ed D

ecem

be2

$

(1)

(2)

(3)

(4)

(2)

(3)

(2)

(5)

(6)

(3)

(2)

(7)

(8)

uctur

ing, n

et:era

tion

(9)

(9)

(10)

(2)

(11

)

(2)

(12)

$

sted:

$

$

acco

rdan

ce w

ith U

.S. G

AAP,

ental

info

rmati

on re

lating

to o

usted

mea

sure

s sho

uld be

con

de ce

rtain

GAAP

items

that

mams

. Othe

r com

panie

s may

def

Celge

ne C

orpo

raRe

conc

iliatio

n of G

AA(In

thou

sand

s,

Three

-M

ble to

Celg

ene -

GAA

P

ments

:s: od

ucts

exite

d or t

o be e

xited

n-core

othe

r rev

enue

s

sold

(exclu

ding a

mortiz

ation

ntang

ible a

ssets)

:ed

comp

ensa

tion e

xpen

seve

ntory

step-u

pxit

ed or

to be

exite

d

deve

lopme

nt:ed

comp

ensa

tion e

xpen

sen-c

ore ac

tivitie

smp

airme

ntslla

borat

ion pa

ymen

ts

al an

d adm

inistr

ative

:ed

comp

ensa

tion e

xpen

sen-c

ore ac

tivitie

spri

cing s

ettlem

ent

of ac

quire

d inta

ngibl

e asse

ts

lated

(gain

s) ch

arges

and r

estru

fair v

alue o

f con

tinge

nt co

nside

n and

restr

uctur

ing co

sts

(expe

nse),

net

Inc. e

quity

meth

od lo

ssn-c

ore ac

tivitie

sve

stmen

t of n

on-co

re ac

tivitie

s

g inte

rest -

Abrax

is

x adju

stmen

ts

ble to

Celg

ene -

Adju

sted

e attr

ibutab

le to

Celge

ne -A

djus

cial in

form

ation

prep

ared

in a

nd m

anag

emen

t with

supp

leme

ected

info

rmati

on. T

hese

adju

S. GA

AP. W

e typ

ically

exclu

dun

usua

l or n

on-re

curri

ng ite

m

55

Net in

come

attrib

utab

Befor

e tax

adjus

tmTo

tal re

venu

esSa

les of

pro

Abrax

is no

n

Cost

of go

ods

of a

cquir

ed i n

Share

-base

Abrax

is inv

Prod

ucts

ex

Rese

arch a

nd

Share

-bas e

Abrax

is no

nIP

R&D

imUp

front

col

Sellin

g, ge

nera

Share

-base

Abrax

is no

nCa

nadia

n p

Amort

izatio

n o

Acqu

isition

rel

Chan

ge in

fAc

quisit

ion

Othe

r inco

me

Entre

Med

, Ab

raxis

non

Gain

on di

v

Non-c

ontro

lling

Net in

come

tax

Net in

come

attrib

utab

Net in

come

per s

hare

Basic

Dilut

ed

In ad

dition

to fi

nan c

prov

ide in

vesto

rs an

with

resp

ect to

proj

eac

cord

ance

with

U.S

GAAP

defin

ition o

f u

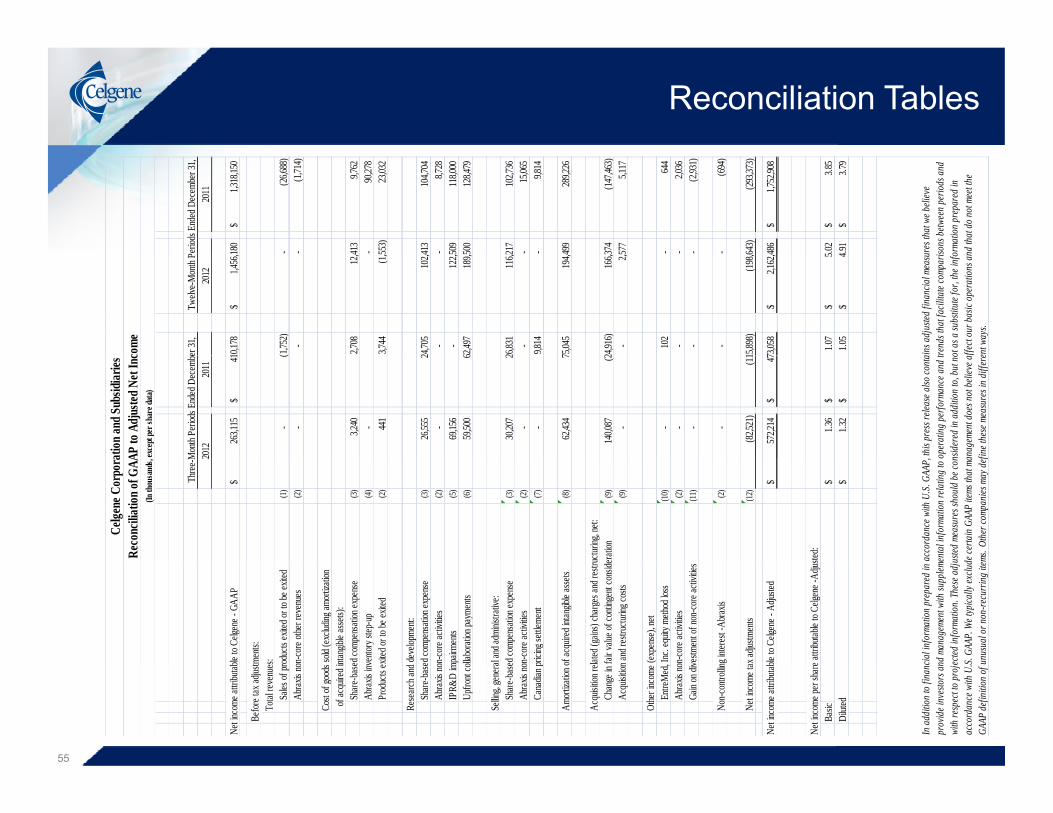

Reconciliation Tables

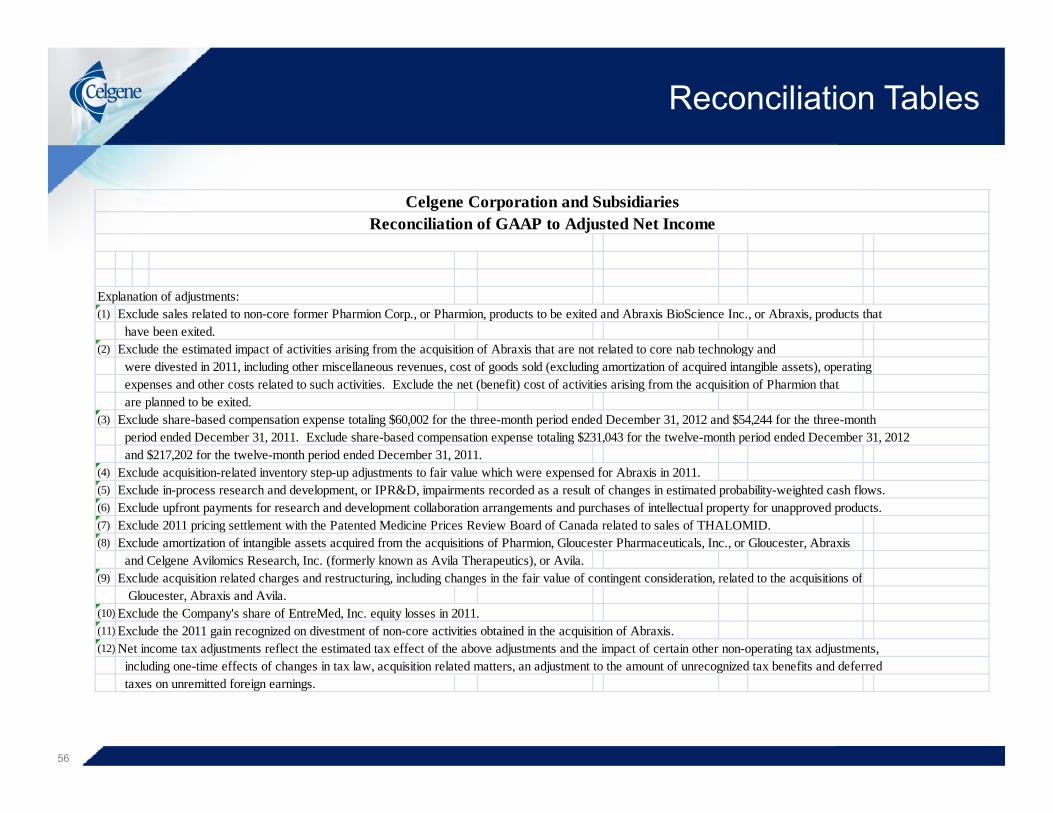

Celgene Corporation and SubsidiariesReconciliation of GAAP to Adjusted Net Income

Explanation of adjustments:(1) Exclude sales related to non-core former Pharmion Corp., or Pharmion, products to be exited and Abraxis BioScience Inc., or Abraxis, products that

have been exited.(2) Exclude the estimated impact of activities arising from the acquisition of Abraxis that are not related to core nab technology andp g q gy

were divested in 2011, including other miscellaneous revenues, cost of goods sold (excluding amortization of acquired intangible assets), operating expenses and other costs related to such activities. Exclude the net (benefit) cost of activities arising from the acquisition of Pharmion that are planned to be exited.

(3) Exclude share-based compensation expense totaling $60,002 for the three-month period ended December 31, 2012 and $54,244 for the three-month period ended December 31, 2011. Exclude share-based compensation expense totaling $231,043 for the twelve-month period ended December 31, 2012

and $217,202 for the twelve-month period ended December 31, 2011. and $217,202 for the twelve month period ended December 31, 2011. (4) Exclude acquisition-related inventory step-up adjustments to fair value which were expensed for Abraxis in 2011.(5) Exclude in-process research and development, or IPR&D, impairments recorded as a result of changes in estimated probability-weighted cash flows.(6) Exclude upfront payments for research and development collaboration arrangements and purchases of intellectual property for unapproved products.(7) Exclude 2011 pricing settlement with the Patented Medicine Prices Review Board of Canada related to sales of THALOMID.(8) Exclude amortization of intangible assets acquired from the acquisitions of Pharmion, Gloucester Pharmaceuticals, Inc., or Gloucester, Abraxis

and Celgene Avilomics Research Inc (formerly known as Avila Therapeutics) or Avila and Celgene Avilomics Research, Inc. (formerly known as Avila Therapeutics), or Avila.(9) Exclude acquisition related charges and restructuring, including changes in the fair value of contingent consideration, related to the acquisitions of

Gloucester, Abraxis and Avila.(10) Exclude the Company's share of EntreMed, Inc. equity losses in 2011. (11) Exclude the 2011 gain recognized on divestment of non-core activities obtained in the acquisition of Abraxis.(12) Net income tax adjustments reflect the estimated tax effect of the above adjustments and the impact of certain other non-operating tax adjustments,

i l di ti ff t f h i t l i iti l t d tt dj t t t th t f i d t b fit d d f d

56

including one-time effects of changes in tax law, acquisition related matters, an adjustment to the amount of unrecognized tax benefits and deferred taxes on unremitted foreign earnings.

Reconciliation Tables

(In thousands, except per share data)

Celgene Corporation and SubsidiariesReconciliation of Full-Year 2013 Projected GAAP to Adjusted Net Income

Low High

Projected net income - GAAP (1) 2,006,000$ 2,058,000$

Before tax adjustments:

Range

Before tax adjustments: Cost of goods sold (excluding amortization of acquired intangible assets): Share-based compensation expense 14,000 14,000

Research and development: Share-based compensation expense 119,000 114,000

Selling general and administrative: Selling, general and administrative: Share-based compensation expense 135,000 130,000

Amortization of acquired intangible assets 265,000 263,000

Acquisition related (gains) charges and restructuring, net: Change in fair value of contingent consideration 11,000 11,000

Net income tax adjustments (185 000) (182 000)Net income tax adjustments (185,000) (182,000)

Projected net income - Adjusted 2,365,000$ 2,408,000$

Projected net income per diluted common share - GAAP 4.67$ 4.79$

Projected net income per diluted common share - Adjusted 5.50$ 5.60$

57

Projected weighted average diluted shares 430,000 430,000

(1) Our projected earnings do not include the effect of any 2013 business combinations, collaboration agreements, asset acquisitions, intangible asset impairments, or changes in the fair value of our CVRs issued as part of the acquisition of Abraxis.

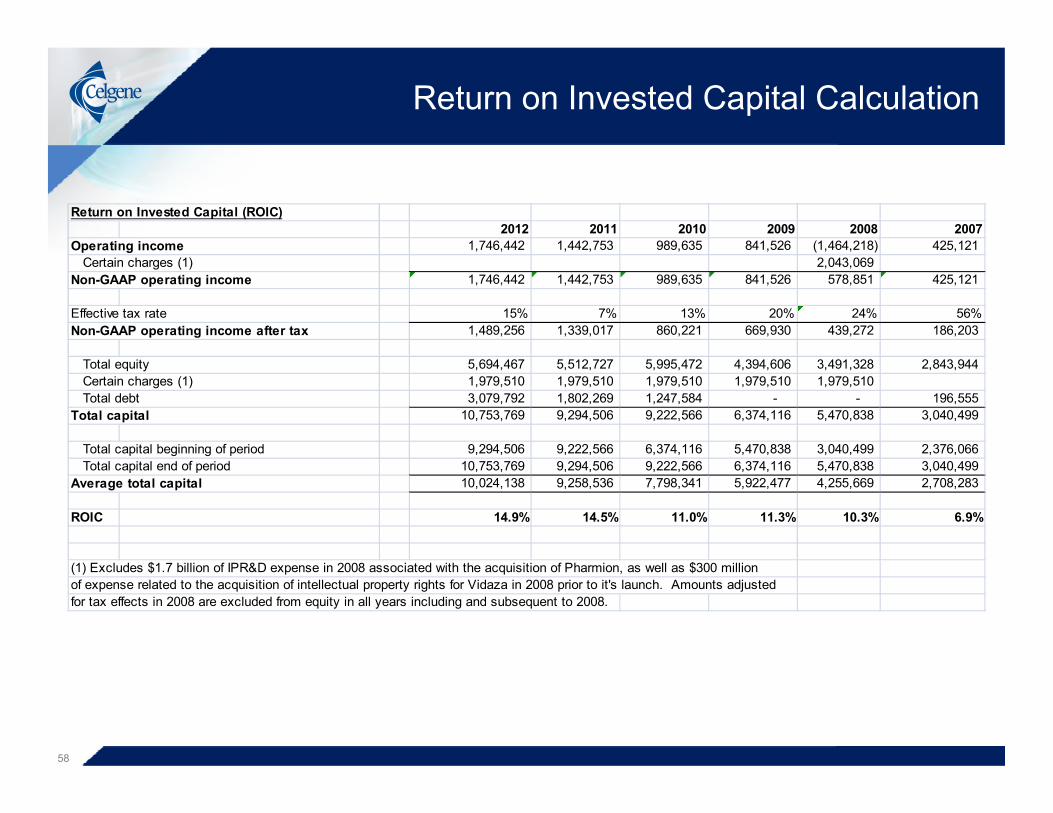

Return on Invested Capital Calculation

Return on Invested Capital (ROIC)2012 2011 2010 2009 2008 2007

Operating income 1,746,442 1,442,753 989,635 841,526 (1,464,218) 425,121 Certain charges (1) 2,043,069

Non-GAAP operating income 1,746,442 1,442,753 989,635 841,526 578,851 425,121

Effective tax rate 15% 7% 13% 20% 24% 56%Non-GAAP operating income after tax 1,489,256 1,339,017 860,221 669,930 439,272 186,203

Total equity 5,694,467 5,512,727 5,995,472 4,394,606 3,491,328 2,843,944 Certain charges (1) 1,979,510 1,979,510 1,979,510 1,979,510 1,979,510 Total debt 3,079,792 1,802,269 1,247,584 - - 196,555

Total capital 10,753,769 9,294,506 9,222,566 6,374,116 5,470,838 3,040,499

Total capital beginning of period 9,294,506 9,222,566 6,374,116 5,470,838 3,040,499 2,376,066 Total capital end of period 10,753,769 9,294,506 9,222,566 6,374,116 5,470,838 3,040,499

Average total capital 10,024,138 9,258,536 7,798,341 5,922,477 4,255,669 2,708,283

ROIC 14.9% 14.5% 11.0% 11.3% 10.3% 6.9%

(1) Excludes $1.7 billion of IPR&D expense in 2008 associated with the acquisition of Pharmion, as well as $300 millionof expense related to the acquisition of intellectual property rights for Vidaza in 2008 prior to it's launch. Amounts adjustedfor tax effects in 2008 are excluded from equity in all years including and subsequent to 2008.

58