Q4 2009 Disclosure Analysisfiles.dlapiper.com/files/upload/ASC_805_and_ASC_810_Q4_Disclosure... ·...

97

PwC Business Combinations and Noncontrolling Interests Q4 2009 Disclosure Analysis An Overview of Results and Observations

Transcript of Q4 2009 Disclosure Analysisfiles.dlapiper.com/files/upload/ASC_805_and_ASC_810_Q4_Disclosure... ·...

PwC

Business Combinations and

Noncontrolling Interests

Q4 2009 Disclosure Analysis

An Overview of Results and Observations

April 2010

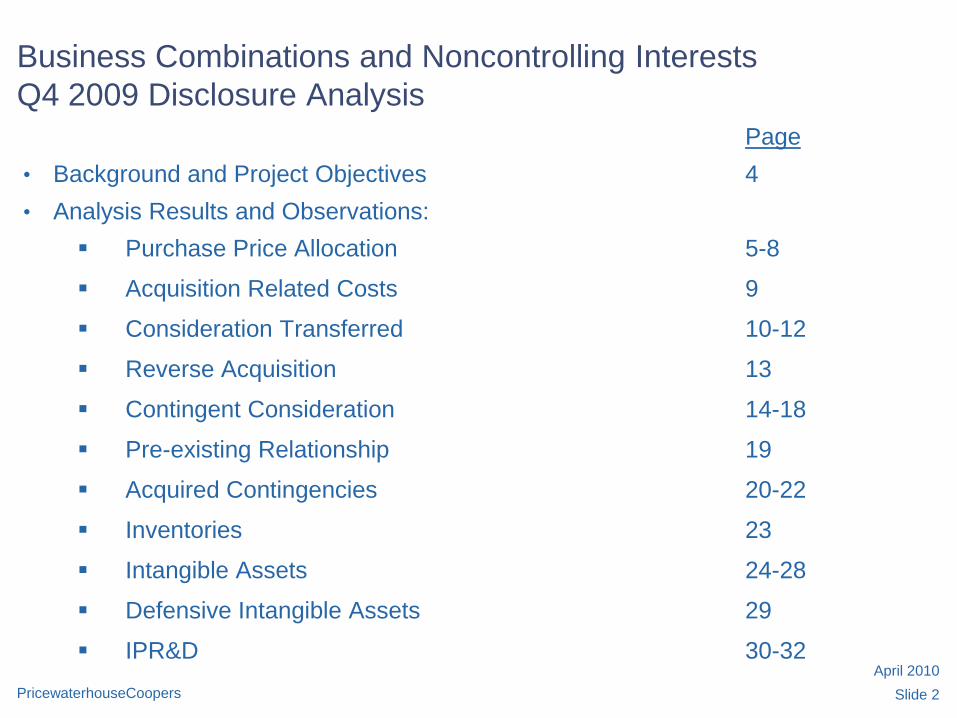

Business Combinations and Noncontrolling Interests

Q4 2009 Disclosure Analysis

Page

• Background and Project Objectives 4

• Analysis Results and Observations:

Purchase Price Allocation 5-8

Acquisition Related Costs 9

Consideration Transferred 10-12

Reverse Acquisition 13

Contingent Consideration 14-18

Pre-existing Relationship 19

Acquired Contingencies 20-22

Inventories 23

Intangible Assets 24-28

Defensive Intangible Assets 29

IPR&D 30-32

Slide 2PricewaterhouseCoopers

April 2010

Business Combinations and Noncontrolling Interests

Q4 2009 Disclosure Analysis

Page

Restructuring Costs 33

Business Combination Achieved in Stages 34

Bargain Purchase Gain 35-36

Actual Results of the Acquiree 37

Pro-forma Revenue and Earnings 38-39

Noncontrolling Interest 40

• Sample Selected 41-43

• Appendix A – Q4 2009 Acquisitions/ Noncontrolling interest

Disclosure Examples:

Table of Contents 45

Disclosure Examples 46-96

Slide 3PricewaterhouseCoopers

April 2010

Background and Project Objectives

Slide 4PricewaterhouseCoopers

• Review of financial statements of 55 public companies who closed deals during the fourth quarter of 2009

• Main objective is to determine how the disclosure requirements of ASC 805 (FAS 141(R)) and ASC 810 (FAS 160) are interpreted in practice

• Not all transactions are material to a buyer and, therefore, some disclosures may be omitted.

• Disclosure excerpts in this analysis are provided solely to increase the awareness and understanding of the types of disclosures that individual registrants have made in particular situations. Because disclosures are specific to the facts and circumstances of the individual registrant to which they relate, there is no suggestion implied by including these disclosure excerpts that they represent required disclosures or are consistent with our views in all circumstances. Accordingly, we make no comments as to the appropriateness, completeness or accuracy of these disclosures.

April 2010

Analysis Results and Observations

Slide 5PricewaterhouseCoopers

Purchase Price Allocation

• 54 companies disclosed the purchase price allocation for the major class of

assets acquired and liabilities assumed and one company did not disclose such

information. This company disclosed that the purchase price allocation was

preliminary and will be adjusted based on valuations completed in 2010.

- 50 companies disclosed the purchase price allocation in the form of a

schedule and 4 companies disclosed such information in narrative form.

- 37 companies disclosed that the purchase price allocation is preliminary, 17

companies did not specify whether the purchase price allocation is preliminary

or final and one company disclosed that the purchase price allocation is final.

April 2010

Analysis Results and Observations

Slide 6PricewaterhouseCoopers

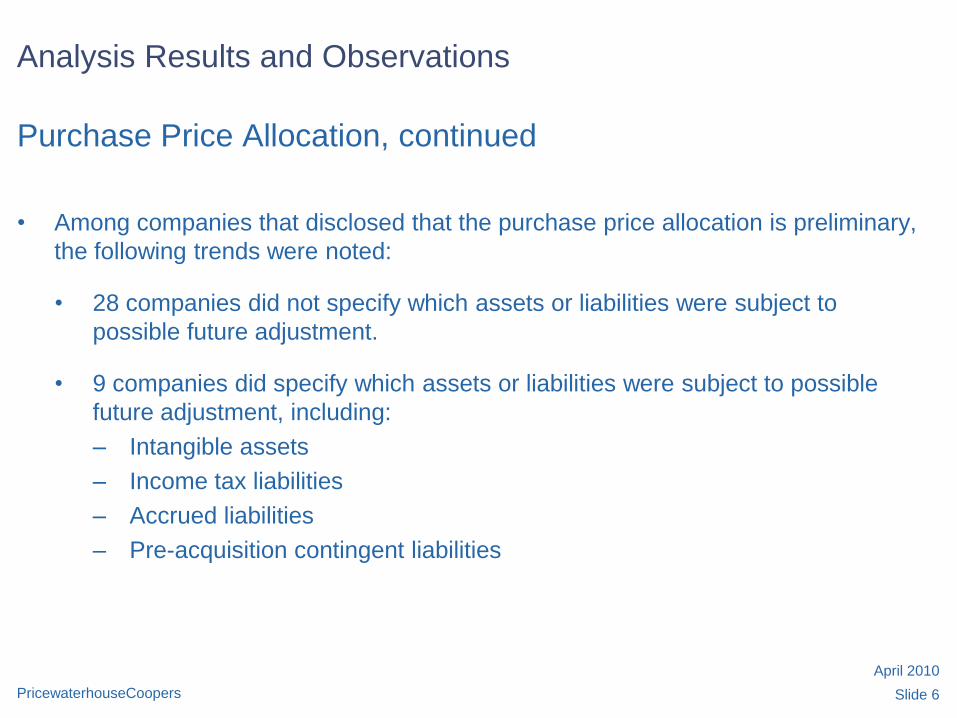

Purchase Price Allocation, continued

• Among companies that disclosed that the purchase price allocation is preliminary,

the following trends were noted:

• 28 companies did not specify which assets or liabilities were subject to

possible future adjustment.

• 9 companies did specify which assets or liabilities were subject to possible

future adjustment, including:

– Intangible assets

– Income tax liabilities

– Accrued liabilities

– Pre-acquisition contingent liabilities

April 2010

Analysis Results and Observations

Slide 7PricewaterhouseCoopers

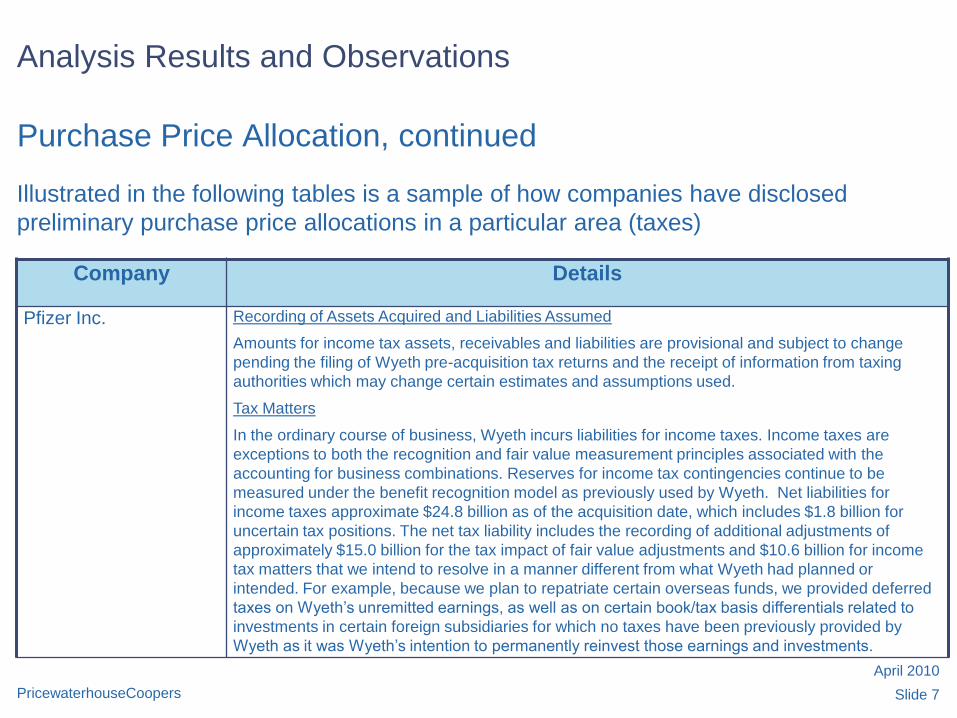

Purchase Price Allocation, continued

Illustrated in the following tables is a sample of how companies have disclosed

preliminary purchase price allocations in a particular area (taxes)

Company Details

Pfizer Inc. Recording of Assets Acquired and Liabilities Assumed

Amounts for income tax assets, receivables and liabilities are provisional and subject to change

pending the filing of Wyeth pre-acquisition tax returns and the receipt of information from taxing

authorities which may change certain estimates and assumptions used.

Tax Matters

In the ordinary course of business, Wyeth incurs liabilities for income taxes. Income taxes are

exceptions to both the recognition and fair value measurement principles associated with the

accounting for business combinations. Reserves for income tax contingencies continue to be

measured under the benefit recognition model as previously used by Wyeth. Net liabilities for

income taxes approximate $24.8 billion as of the acquisition date, which includes $1.8 billion for

uncertain tax positions. The net tax liability includes the recording of additional adjustments of

approximately $15.0 billion for the tax impact of fair value adjustments and $10.6 billion for income

tax matters that we intend to resolve in a manner different from what Wyeth had planned or

intended. For example, because we plan to repatriate certain overseas funds, we provided deferred

taxes on Wyeth’s unremitted earnings, as well as on certain book/tax basis differentials related to

investments in certain foreign subsidiaries for which no taxes have been previously provided by

Wyeth as it was Wyeth’s intention to permanently reinvest those earnings and investments.

April 2010

Analysis Results and Observations

Slide 8PricewaterhouseCoopers

Purchase Price Allocation, continued

Company Details

Watson

Pharmaceuticals Inc.

Long-term deferred tax liabilities and other tax liabilities reflects a deferred tax income

liability representing the estimated impact of purchase accounting adjustments for the

inventory fair value step-up, property, plant and equipment fair value adjustment,

contingencies adjustment and identifiable IPR&D and intangible assets fair value

adjustment. This estimate of deferred tax liabilities was determined based on the

excess book basis over the tax basis resulting from the above fair value adjustments

using an estimated weighted average statutory tax rate of approximately 30%. This

estimate is preliminary and is subject to change based upon management’s final

determination of fair values of tangible and identifiable intangible assets acquired and

liabilities assumed by taxing jurisdiction.

April 2010

Analysis Results and Observations

Slide 9PricewaterhouseCoopers

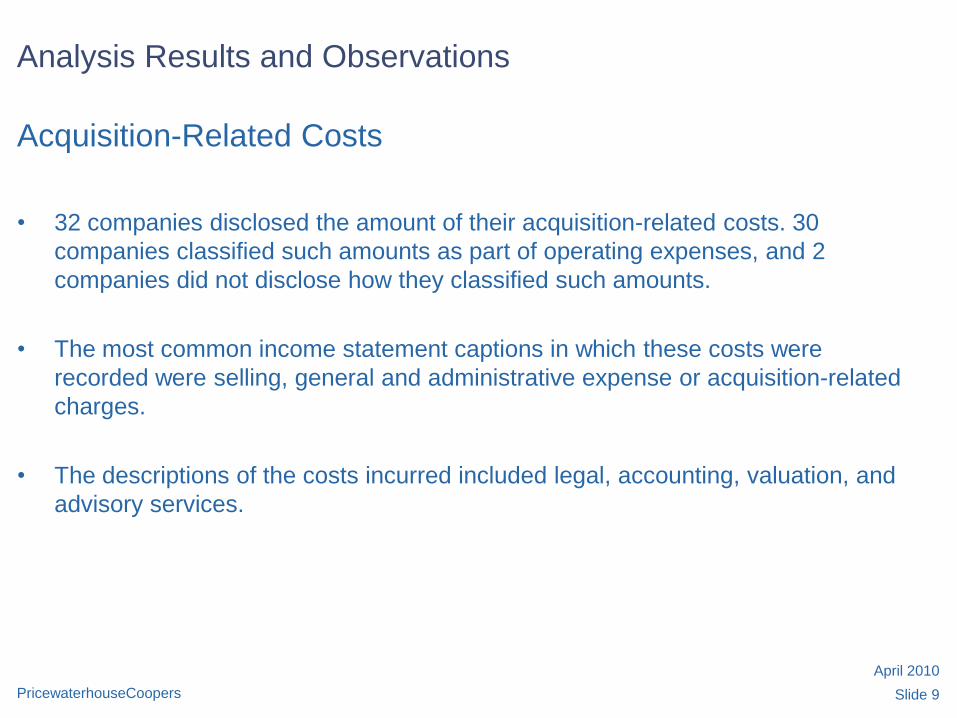

Acquisition-Related Costs

• 32 companies disclosed the amount of their acquisition-related costs. 30

companies classified such amounts as part of operating expenses, and 2

companies did not disclose how they classified such amounts.

• The most common income statement captions in which these costs were

recorded were selling, general and administrative expense or acquisition-related

charges.

• The descriptions of the costs incurred included legal, accounting, valuation, and

advisory services.

April 2010

Analysis Results and Observations

Slide 10PricewaterhouseCoopers

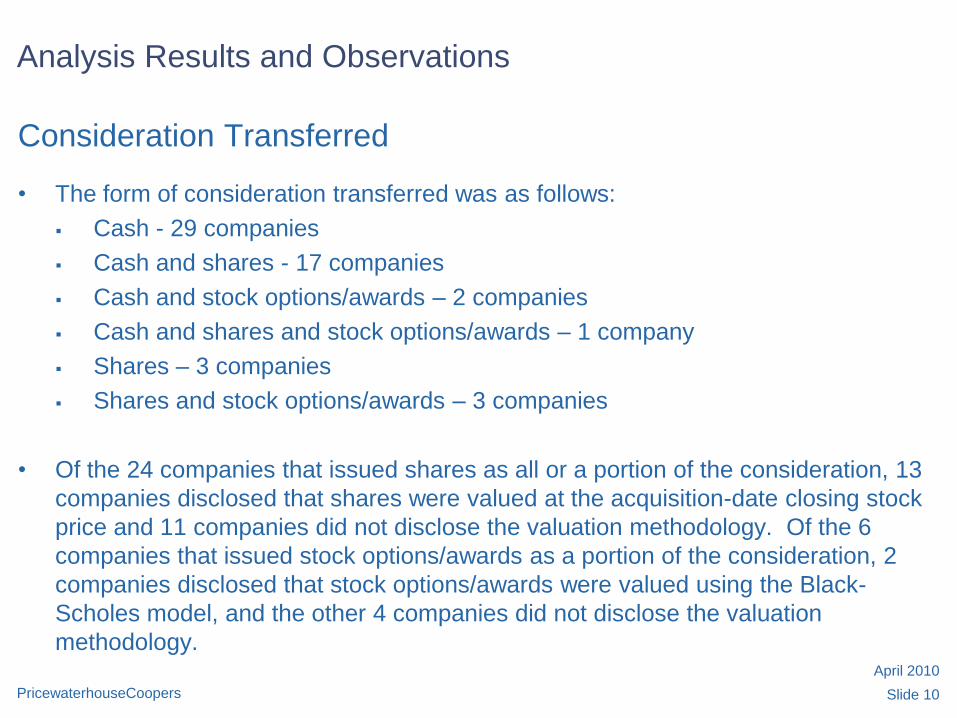

Consideration Transferred

• The form of consideration transferred was as follows:

Cash - 29 companies

Cash and shares - 17 companies

Cash and stock options/awards – 2 companies

Cash and shares and stock options/awards – 1 company

Shares – 3 companies

Shares and stock options/awards – 3 companies

• Of the 24 companies that issued shares as all or a portion of the consideration, 13

companies disclosed that shares were valued at the acquisition-date closing stock

price and 11 companies did not disclose the valuation methodology. Of the 6

companies that issued stock options/awards as a portion of the consideration, 2

companies disclosed that stock options/awards were valued using the Black-

Scholes model, and the other 4 companies did not disclose the valuation

methodology.

April 2010

Analysis Results and Observations

Slide 11PricewaterhouseCoopers

Consideration Transferred

• Of the 6 companies that issued stock options/awards as a portion of the

consideration:

- 2 companies included all of the fair value of the options/awards as

consideration transferred because the outstanding acquiree awards being

replaced were fully vested

- 4 companies allocated the fair value of the options/awards between

consideration transferred (for fully vested acquiree awards that were replaced)

and compensation expense that will be recognized in postcombination

earnings (for unvested acquiree awards that were replaced).

April 2010

Analysis Results and Observations

Slide 12PricewaterhouseCoopers

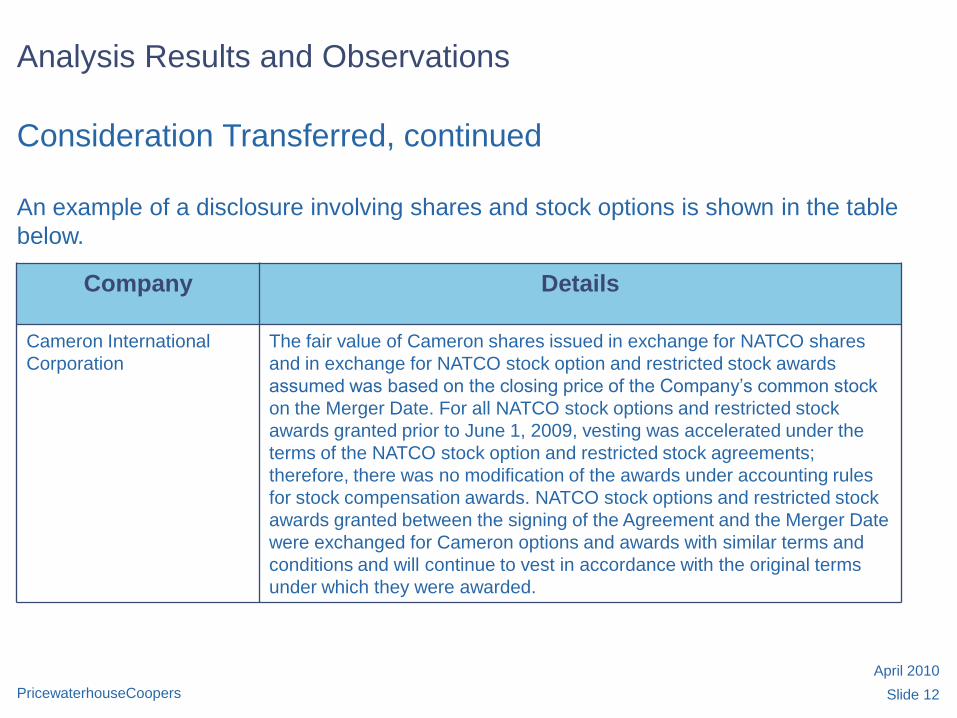

Consideration Transferred, continued

An example of a disclosure involving shares and stock options is shown in the table

below.

Company Details

Cameron International

Corporation

The fair value of Cameron shares issued in exchange for NATCO shares

and in exchange for NATCO stock option and restricted stock awards

assumed was based on the closing price of the Company’s common stock

on the Merger Date. For all NATCO stock options and restricted stock

awards granted prior to June 1, 2009, vesting was accelerated under the

terms of the NATCO stock option and restricted stock agreements;

therefore, there was no modification of the awards under accounting rules

for stock compensation awards. NATCO stock options and restricted stock

awards granted between the signing of the Agreement and the Merger Date

were exchanged for Cameron options and awards with similar terms and

conditions and will continue to vest in accordance with the original terms

under which they were awarded.

April 2010

Analysis Results and Observations

Slide 13PricewaterhouseCoopers

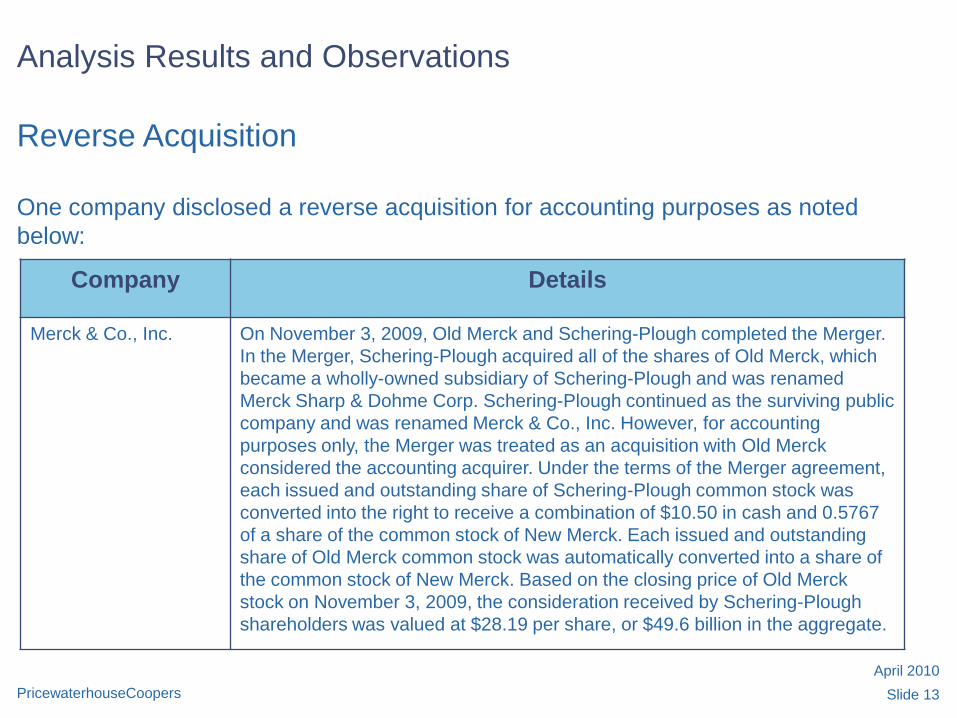

Reverse Acquisition

One company disclosed a reverse acquisition for accounting purposes as noted

below:

Company Details

Merck & Co., Inc. On November 3, 2009, Old Merck and Schering-Plough completed the Merger.

In the Merger, Schering-Plough acquired all of the shares of Old Merck, which

became a wholly-owned subsidiary of Schering-Plough and was renamed

Merck Sharp & Dohme Corp. Schering-Plough continued as the surviving public

company and was renamed Merck & Co., Inc. However, for accounting

purposes only, the Merger was treated as an acquisition with Old Merck

considered the accounting acquirer. Under the terms of the Merger agreement,

each issued and outstanding share of Schering-Plough common stock was

converted into the right to receive a combination of $10.50 in cash and 0.5767

of a share of the common stock of New Merck. Each issued and outstanding

share of Old Merck common stock was automatically converted into a share of

the common stock of New Merck. Based on the closing price of Old Merck

stock on November 3, 2009, the consideration received by Schering-Plough

shareholders was valued at $28.19 per share, or $49.6 billion in the aggregate.

April 2010

Analysis Results and Observations

Slide 14PricewaterhouseCoopers

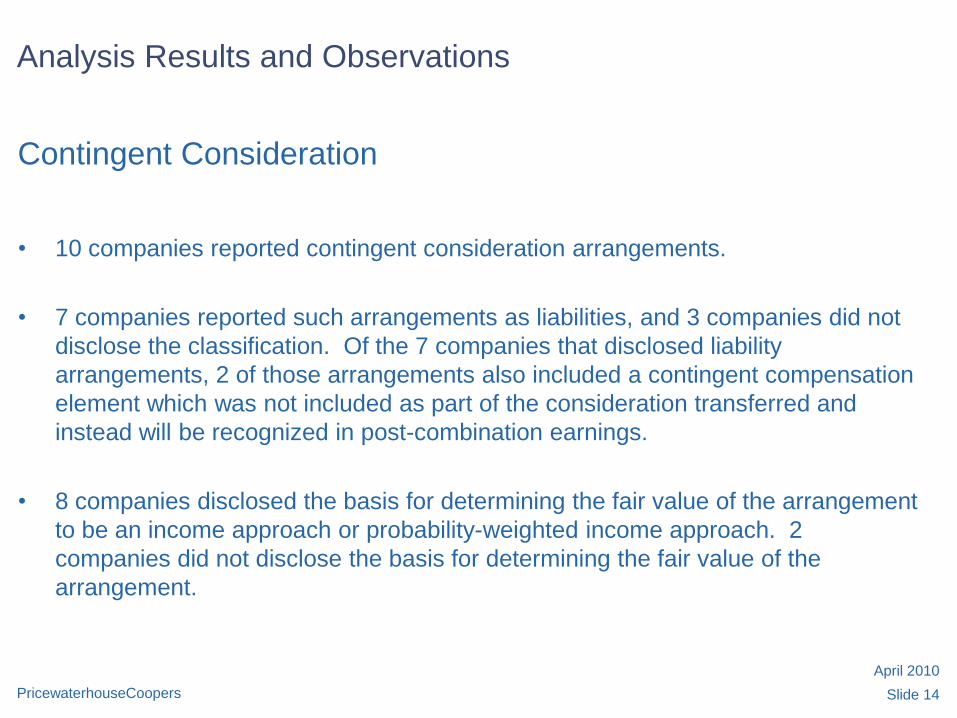

Contingent Consideration

• 10 companies reported contingent consideration arrangements.

• 7 companies reported such arrangements as liabilities, and 3 companies did not

disclose the classification. Of the 7 companies that disclosed liability

arrangements, 2 of those arrangements also included a contingent compensation

element which was not included as part of the consideration transferred and

instead will be recognized in post-combination earnings.

• 8 companies disclosed the basis for determining the fair value of the arrangement

to be an income approach or probability-weighted income approach. 2

companies did not disclose the basis for determining the fair value of the

arrangement.

April 2010

Analysis Results and Observations

Slide 15PricewaterhouseCoopers

Company Contingent

Consideration

Classification

Valuation Methodology

FMC Technologies, Inc. Not disclosed Income approach

MEMC Electronic Materials, Inc. Not disclosed Probability-weighted income approach

Abbott Laboratories Not disclosed Not disclosed

MasTec, Inc. Liability Income approach

Onyx Pharmaceuticals, Inc. Liability Probability-weighted income approach

Cubist Pharmaceuticals, Inc. Liability Probability-weighted income approach

Watson Pharmaceuticals, Inc. Liability Probability-weighted income approach

NetLogic Microsystems, Inc. Liability Probability-weighted income approach

Resources Connection, Inc. Liability Probability-weighted income approach

GSI Commerce, Inc. Liability Not disclosed

Contingent Consideration, continued

April 2010

Analysis Results and Observations

Slide 16PricewaterhouseCoopers

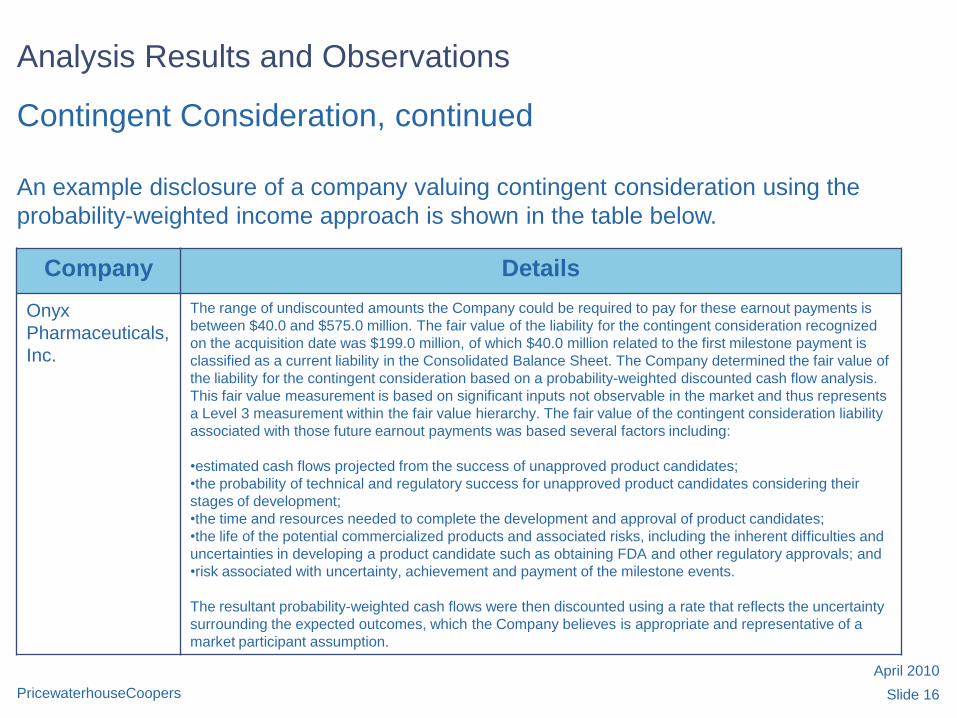

Contingent Consideration, continued

An example disclosure of a company valuing contingent consideration using the

probability-weighted income approach is shown in the table below.

Company Details

Onyx

Pharmaceuticals,

Inc.

The range of undiscounted amounts the Company could be required to pay for these earnout payments is

between $40.0 and $575.0 million. The fair value of the liability for the contingent consideration recognized

on the acquisition date was $199.0 million, of which $40.0 million related to the first milestone payment is

classified as a current liability in the Consolidated Balance Sheet. The Company determined the fair value of

the liability for the contingent consideration based on a probability-weighted discounted cash flow analysis.

This fair value measurement is based on significant inputs not observable in the market and thus represents

a Level 3 measurement within the fair value hierarchy. The fair value of the contingent consideration liability

associated with those future earnout payments was based several factors including:

•estimated cash flows projected from the success of unapproved product candidates;

•the probability of technical and regulatory success for unapproved product candidates considering their

stages of development;

•the time and resources needed to complete the development and approval of product candidates;

•the life of the potential commercialized products and associated risks, including the inherent difficulties and

uncertainties in developing a product candidate such as obtaining FDA and other regulatory approvals; and

•risk associated with uncertainty, achievement and payment of the milestone events.

The resultant probability-weighted cash flows were then discounted using a rate that reflects the uncertainty

surrounding the expected outcomes, which the Company believes is appropriate and representative of a

market participant assumption.

April 2010

Analysis Results and Observations

Slide 17PricewaterhouseCoopers

Existing Contingent Consideration of an Acquiree

• In addition to the 10 companies that disclosed a contingent consideration

arrangement, one other company in the sample disclosed the acquisition of an

existing contingent consideration arrangement to which the acquiree remained a

party from a previous acquisition transaction. This acquired arrangement was

classified as a contingent consideration liability of the acquirer.

April 2010

Analysis Results and Observations

Slide 18PricewaterhouseCoopers

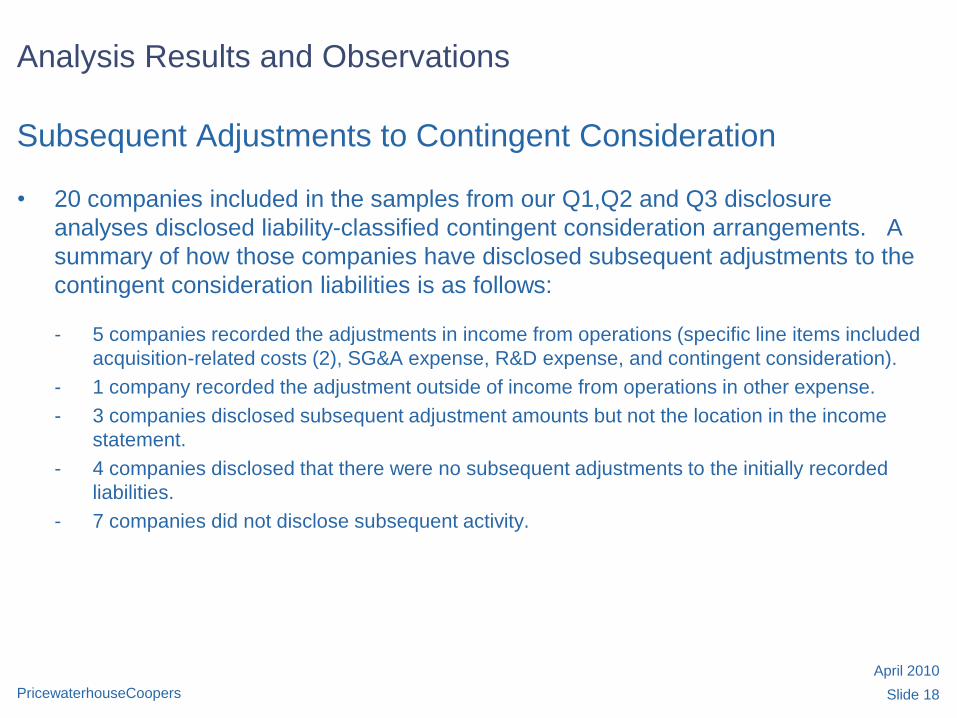

Subsequent Adjustments to Contingent Consideration

• 20 companies included in the samples from our Q1,Q2 and Q3 disclosure

analyses disclosed liability-classified contingent consideration arrangements. A

summary of how those companies have disclosed subsequent adjustments to the

contingent consideration liabilities is as follows:

- 5 companies recorded the adjustments in income from operations (specific line items included

acquisition-related costs (2), SG&A expense, R&D expense, and contingent consideration).

- 1 company recorded the adjustment outside of income from operations in other expense.

- 3 companies disclosed subsequent adjustment amounts but not the location in the income

statement.

- 4 companies disclosed that there were no subsequent adjustments to the initially recorded

liabilities.

- 7 companies did not disclose subsequent activity.

April 2010

Analysis Results and Observations

Slide 19PricewaterhouseCoopers

Company Description of transaction

Sprint Nextel

Corporation

The acquisition of iPCS resulted in the effective settlement of pre-existing litigation. On

September 24, 2008 the Illinois Supreme Court denied the Company’s petition for

appeal in a contract dispute with iPCS. The decision resulted in a previous ruling being

upheld that required Sprint to cease owning, operating or managing the iDEN network

in parts of certain Midwestern states including Illinois, Iowa, Michigan, Missouri,

Nebraska, Wisconsin and a small portion of Indiana. As a result of the acquisition, all

disputes have been resolved and the Company recorded a $23 million charge as an

increase to operating expenses, representing the estimated fair value of the settled

litigation. Discounted cash flows, an income approach, were primarily used to value

the effective settlement of litigation.

Pre-existing Relationship

• Illustrated in the following table is how one company reported settlement of a pre-existing

relationship.

VMU

Acquisition iPCS Affiliate

Acquisition (in millions) Consideration:

Cash, net of cash acquired $ 265 $ 318 Equity instruments 379 — Settlement of pre-existing litigation — (23 )

Fair value of consideration transferred 644 295 Fair value of Sprint’s equity interest in VMU before the acquisition 57 —

Total $ 701 $ 295

April 2010

Analysis Results and Observations

Slide 20PricewaterhouseCoopers

Company Nature of

Contingency

FAS 5/Fair

Value

Recorded on

acquisition

date

Pfizer Inc. Environmental;

Legal

Fair Value;

FAS 5

Yes (1)

Chesapeake Utilities Corp. Environmental FAS 5 Yes (2)

Hubbell, Inc. Environmental Fair Value

and FAS 5

Yes (3)

Merck & Co., Inc. Not disclosed FAS 5 Yes (4)

Warner Chilcott plc Not disclosed FAS 5 Yes (5)

Acquired Contingencies

• As illustrated in the table, the following companies reported acquired

contingencies.

April 2010

Analysis Results and Observations

Slide 21PricewaterhouseCoopers

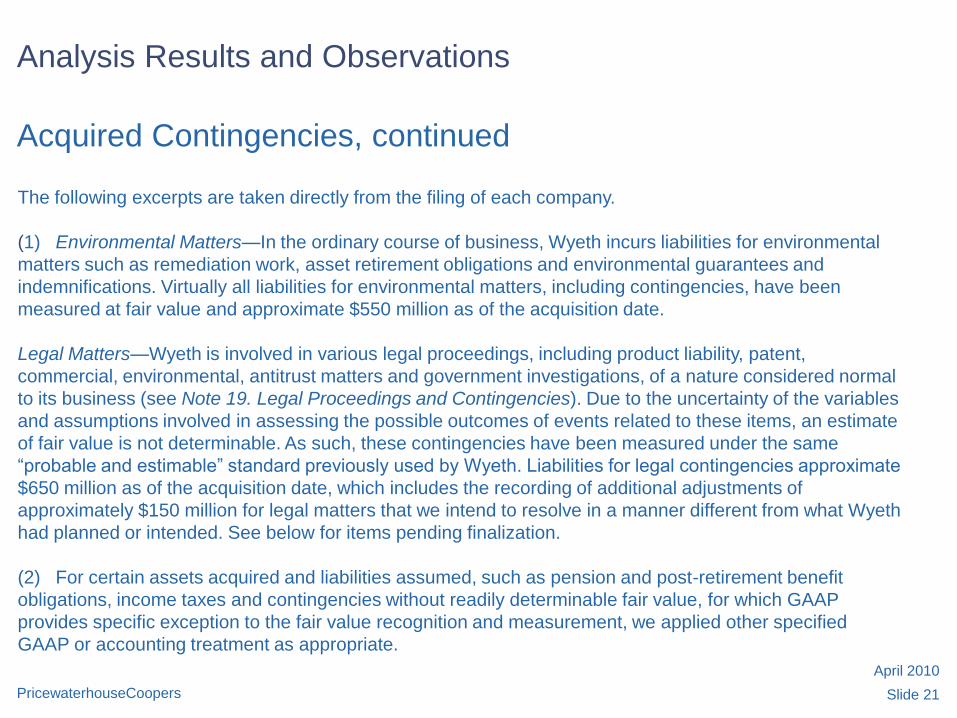

The following excerpts are taken directly from the filing of each company.

(1) Environmental Matters—In the ordinary course of business, Wyeth incurs liabilities for environmental

matters such as remediation work, asset retirement obligations and environmental guarantees and

indemnifications. Virtually all liabilities for environmental matters, including contingencies, have been

measured at fair value and approximate $550 million as of the acquisition date.

Legal Matters—Wyeth is involved in various legal proceedings, including product liability, patent,

commercial, environmental, antitrust matters and government investigations, of a nature considered normal

to its business (see Note 19. Legal Proceedings and Contingencies). Due to the uncertainty of the variables

and assumptions involved in assessing the possible outcomes of events related to these items, an estimate

of fair value is not determinable. As such, these contingencies have been measured under the same

―probable and estimable‖ standard previously used by Wyeth. Liabilities for legal contingencies approximate

$650 million as of the acquisition date, which includes the recording of additional adjustments of

approximately $150 million for legal matters that we intend to resolve in a manner different from what Wyeth

had planned or intended. See below for items pending finalization.

(2) For certain assets acquired and liabilities assumed, such as pension and post-retirement benefit

obligations, income taxes and contingencies without readily determinable fair value, for which GAAP

provides specific exception to the fair value recognition and measurement, we applied other specified

GAAP or accounting treatment as appropriate.

Acquired Contingencies, continued

April 2010

Analysis Results and Observations

Slide 22PricewaterhouseCoopers

(3) Additionally, the Burndy opening balance sheet includes a $6.2 million contingent liability related to

environmental matters. The estimated fair value portion of this liability is $1.6 million, while the remaining

$4.6 million liability was determined using the guidance prescribed under ASC 450, which requires the loss

contingency to be probable and reasonably estimable.

(4) In order to allocate the Merger consideration, the Company estimated the fair value of the assets and

liabilities of Schering-Plough. No contingent assets or liabilities were recognized at fair value as of the

Merger date because the fair value of such contingencies could not be determined. Contingent liabilities

were recorded to the extent the amounts were probable and reasonably estimable.

(5) Liabilities assumed for PGP on October 30, 2009 included certain contingent liabilities valued at

approximately $5 million which were valued in accordance with the FASB ASC 450, ―Accounting for

Contingencies.‖

Acquired Contingencies, continued

April 2010

Analysis Results and Observations

Slide 23PricewaterhouseCoopers

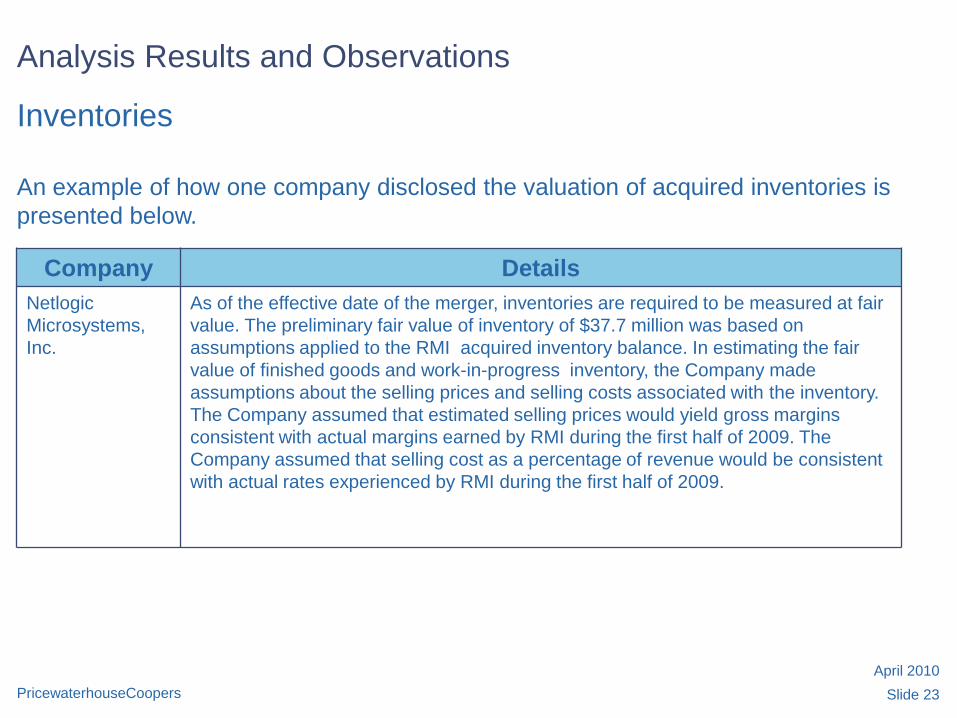

Inventories

An example of how one company disclosed the valuation of acquired inventories is

presented below.

Company Details

Netlogic

Microsystems,

Inc.

As of the effective date of the merger, inventories are required to be measured at fair

value. The preliminary fair value of inventory of $37.7 million was based on

assumptions applied to the RMI acquired inventory balance. In estimating the fair

value of finished goods and work-in-progress inventory, the Company made

assumptions about the selling prices and selling costs associated with the inventory.

The Company assumed that estimated selling prices would yield gross margins

consistent with actual margins earned by RMI during the first half of 2009. The

Company assumed that selling cost as a percentage of revenue would be consistent

with actual rates experienced by RMI during the first half of 2009.

April 2010

Analysis Results and Observations

Slide 24PricewaterhouseCoopers

Intangible Assets

• 52 companies recorded intangible assets as part of their purchase price

allocations.

• Illustrated in the following tables is a sample of how companies valued and will

amortize their intangible assets.

April 2010

Analysis Results and Observations

Slide 25PricewaterhouseCoopers

Intangible Assets, continued

Company Intangible

Assets

Acquired

Valuation Methodology Amortization Method

Broadcom

Corp.

Core technologies Relief-from-royalty method based on market

royalties for similar fundamental

technologies. The royalty rate used is based

on an analysis of empirical, market-derived

royalty rates for guideline intangible assets

Straight-line basis over

their estimated useful life

of 1 to 15 years

Completed

technologies

Multi-period excess earnings approach Straight-line basis over

their estimated useful life

of 1 to 15 years

Customer

relationships

Income approach Straight-line basis over

their estimated useful life

of 4 to 7 years

April 2010

Analysis Results and Observations

Slide 26PricewaterhouseCoopers

Company Intangible

Assets

Acquired

Valuation Methodology Amortization Method

Atheros

Communications,

Inc.

Developed

technology

Income approach – discount rate of 16.5% Straight-line basis over

estimated useful life of 5

years

Customer

relationships

Income approach – discount rate of 16.2% Straight-line basis over

estimated useful life of 7

years

Backlog Income approach – discount rate of 6.9% Straight-line basis over

estimated useful life of

less than 1 year

Intangible Assets, continued

April 2010

Analysis Results and Observations

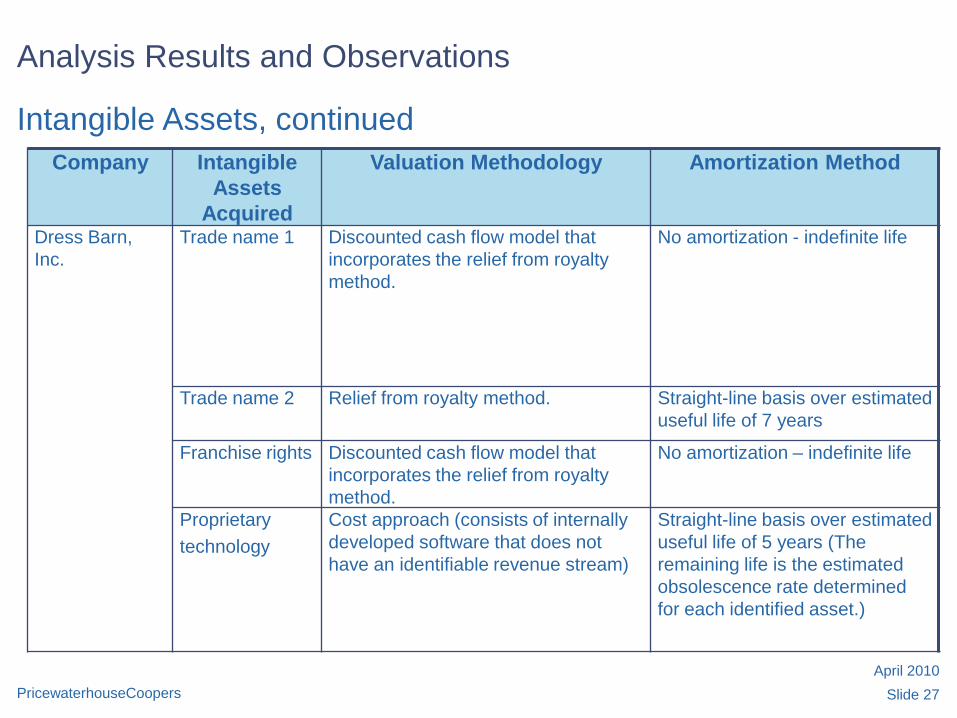

Slide 27PricewaterhouseCoopers

Company Intangible

Assets

Acquired

Valuation Methodology Amortization Method

Dress Barn,

Inc.

Trade name 1 Discounted cash flow model that

incorporates the relief from royalty

method.

No amortization - indefinite life

Trade name 2 Relief from royalty method. Straight-line basis over estimated

useful life of 7 years

Franchise rights Discounted cash flow model that

incorporates the relief from royalty

method.

No amortization – indefinite life

Proprietary

technology

Cost approach (consists of internally

developed software that does not

have an identifiable revenue stream)

Straight-line basis over estimated

useful life of 5 years (The

remaining life is the estimated

obsolescence rate determined

for each identified asset.)

Intangible Assets, continued

April 2010

Analysis Results and Observations

Slide 28PricewaterhouseCoopers

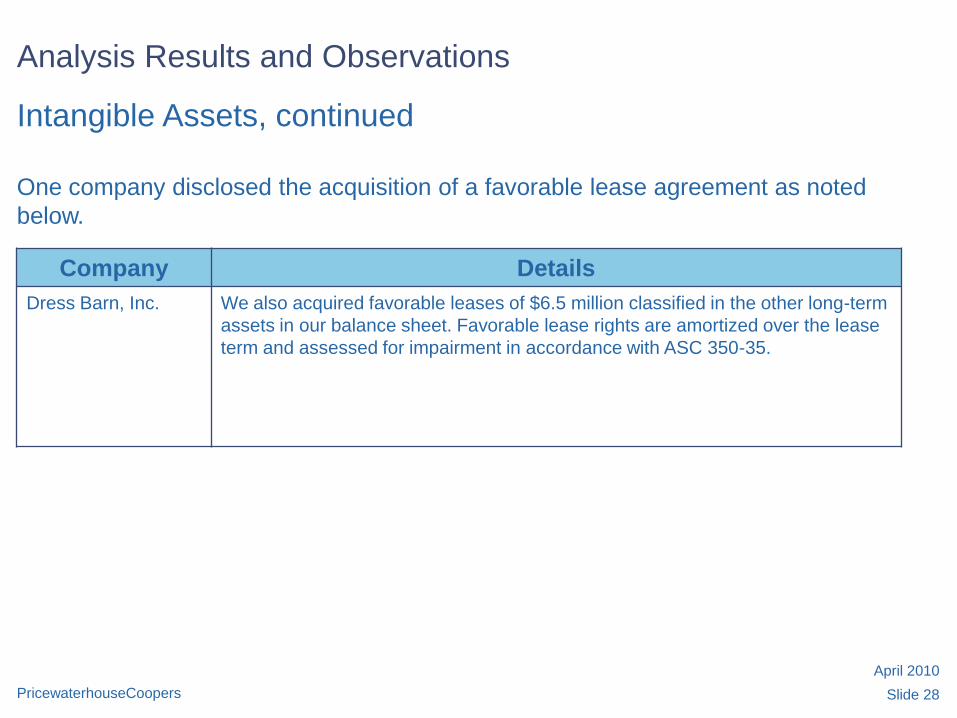

Intangible Assets, continued

One company disclosed the acquisition of a favorable lease agreement as noted

below.

Company Details

Dress Barn, Inc. We also acquired favorable leases of $6.5 million classified in the other long-term

assets in our balance sheet. Favorable lease rights are amortized over the lease

term and assessed for impairment in accordance with ASC 350-35.

April 2010

Analysis Results and Observations

Slide 29PricewaterhouseCoopers

Defensive Intangible Assets

• One company disclosed a defensive intangible asset in the form of a trade name

that was acquired. The asset was valued using the relief-from-royalty method and

was assigned a useful life of seven years, which represents the lifecycle of the

average customer of the brand that is being defended.

April 2010

Analysis Results and Observations

Slide 30PricewaterhouseCoopers

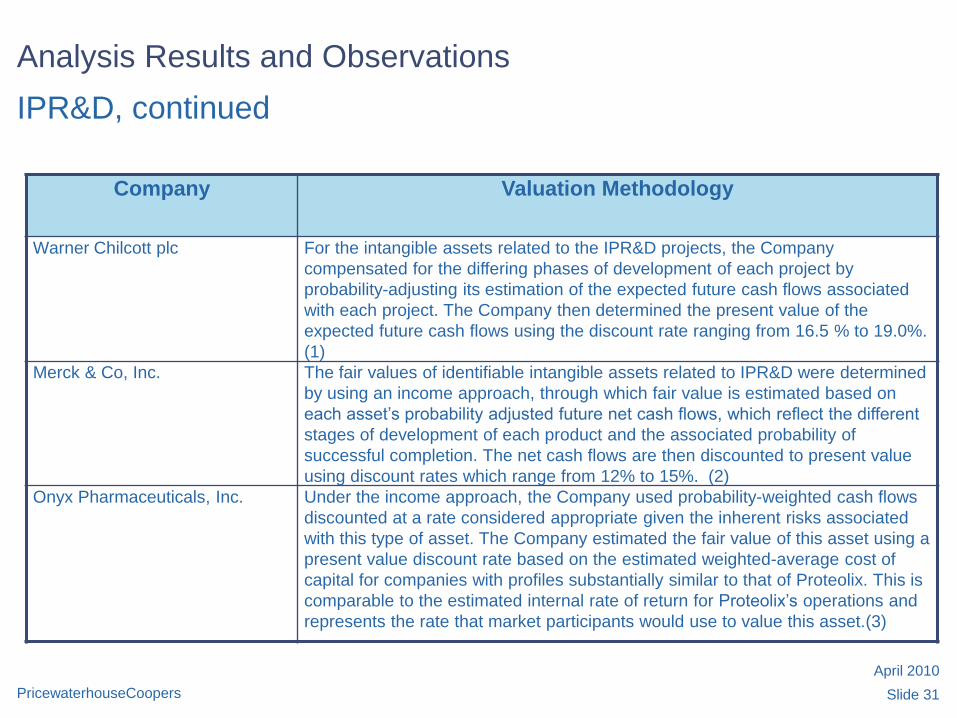

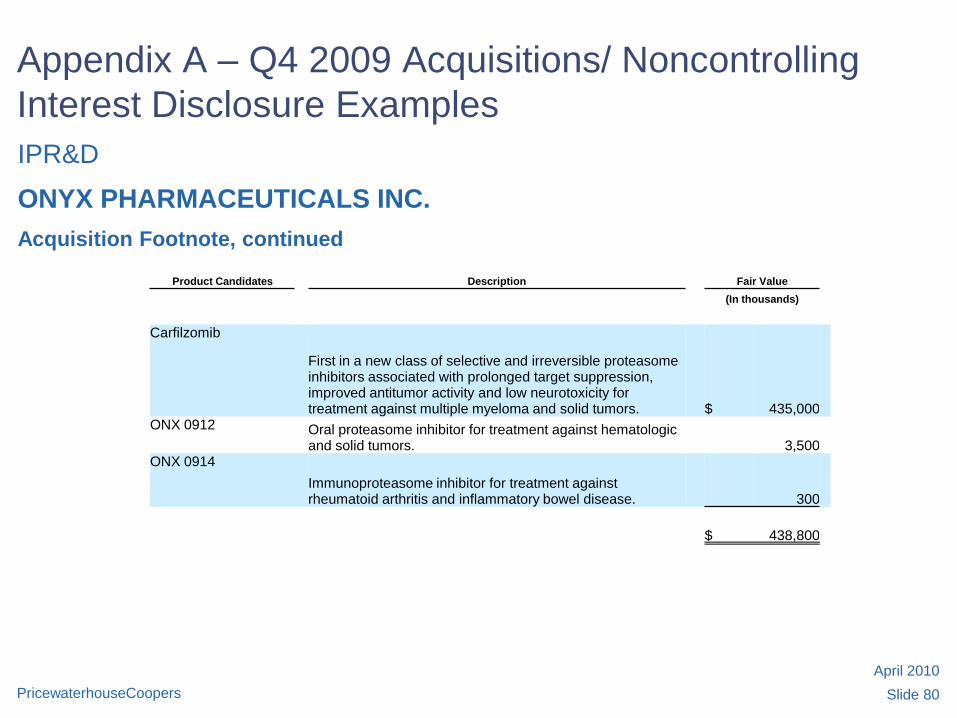

IPR&D

• 13 companies recorded IPR&D as part of their purchase price allocations.

• Illustrated in the following table is a sample of how companies valued IPR&D.

April 2010

Analysis Results and Observations

Slide 31PricewaterhouseCoopers

Company Valuation Methodology

Warner Chilcott plc For the intangible assets related to the IPR&D projects, the Company

compensated for the differing phases of development of each project by

probability-adjusting its estimation of the expected future cash flows associated

with each project. The Company then determined the present value of the

expected future cash flows using the discount rate ranging from 16.5 % to 19.0%.

(1)

Merck & Co, Inc. The fair values of identifiable intangible assets related to IPR&D were determined

by using an income approach, through which fair value is estimated based on

each asset’s probability adjusted future net cash flows, which reflect the different

stages of development of each product and the associated probability of

successful completion. The net cash flows are then discounted to present value

using discount rates which range from 12% to 15%. (2)

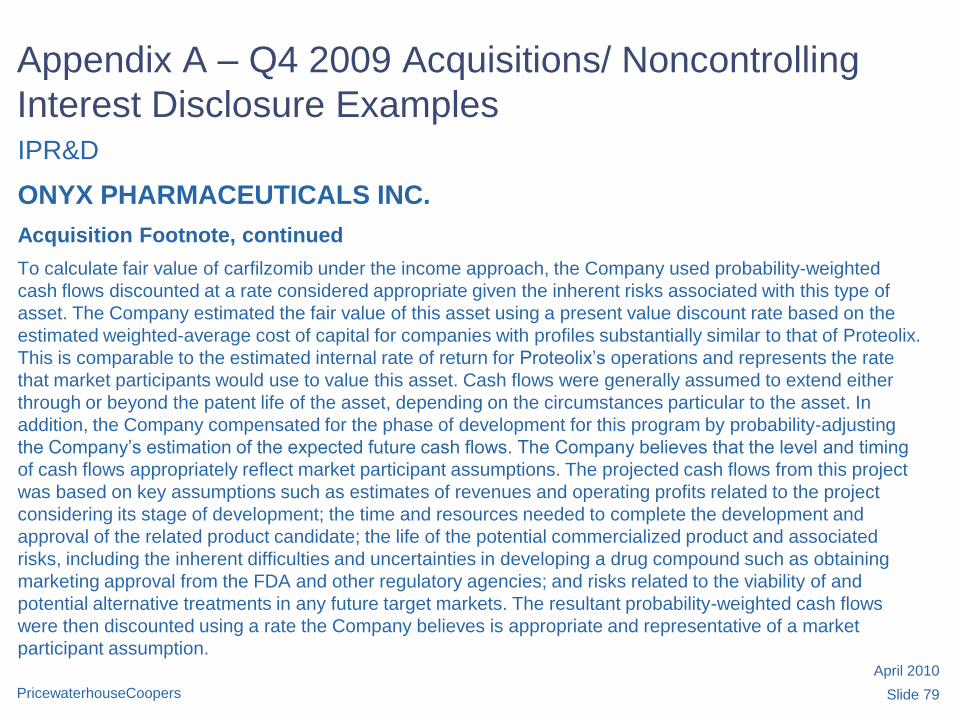

Onyx Pharmaceuticals, Inc. Under the income approach, the Company used probability-weighted cash flows

discounted at a rate considered appropriate given the inherent risks associated

with this type of asset. The Company estimated the fair value of this asset using a

present value discount rate based on the estimated weighted-average cost of

capital for companies with profiles substantially similar to that of Proteolix. This is

comparable to the estimated internal rate of return for Proteolix’s operations and

represents the rate that market participants would use to value this asset.(3)

IPR&D, continued

April 2010

Analysis Results and Observations

Slide 32PricewaterhouseCoopers

IPR&D, continuedThe following excerpts are taken directly from the filing of each company.

(1) The discount rate is based on the estimated weighted-average cost of capital for companies with profiles substantially

similar to that of the acquiree. This is comparable to the estimated internal rate of return for the acquiree’s operations

and represents the rate that market participants would use to value the intangible assets. The projected cash flows

from the IPR&D projects were based on key assumptions such as estimates of revenues and operating profits related

to the projects considering their stages of development; the time and resources needed to complete the development

and approval of the related product candidates; the life of the potential commercialized products and associated risks,

including the inherent difficulties and uncertainties in developing a drug compound such as obtaining marketing

approval from the FDA and other regulatory agencies; and risks related to the viability of and potential alternative

treatments in any future target markets.

(2) Actual cash flows are likely to be different than those assumed. All of the IPR&D projects are subject to the inherent

risks and uncertainties in drug development and it is possible that the Company will not be able to successfully develop

and complete the IPR&D programs and profitably commercialize the underlying product candidates.

(3) Cash flows were generally assumed to extend either through or beyond the patent life of the asset, depending on the

circumstances particular to the asset. In addition, the Company compensated for the phase of development for this

program by probability-adjusting the Company’s estimation of the expected future cash flows. The Company believes

that the level and timing of cash flows appropriately reflect market participant assumptions. The projected cash flows

from this project was based on key assumptions such as estimates of revenues and operating profits related to the

project considering its stage of development; the time and resources needed to complete the development and

approval of the related product candidate; the life of the potential commercialized product and associated risks,

including the inherent difficulties and uncertainties in developing a drug compound such as obtaining marketing

approval from the FDA and other regulatory agencies; and risks related to the viability of and potential alternative

treatments in any future target markets. The resultant probability-weighted cash flows were then discounted using a

rate the Company believes is appropriate and representative of a market participant assumption.

April 2010

Analysis Results and Observations

Slide 33PricewaterhouseCoopers

Restructuring Costs

An example of how one company disclosed the accounting for restructuring

activities is shown below.

Company Details

Netlogic

Microsystems, Inc.

Prior to the close of the acquisition, RMI initiated a restructuring plan where the

employment of some RMI employees were terminated upon the close of the

merger. The Company has determined that the restructuring plan was a separate

plan from the business combination because the plan to terminate the

employment of certain employees was in contemplation of the merger. Therefore,

the full severance cost of $0.9 million was recognized by the Company as

an expense on the acquisition date. The severance costs were comprised of

$0.4 million, which was paid by RMI to the terminated employees prior to the

close, and $0.5 million which was paid after the merger by the Company.

April 2010

Analysis Results and Observations

Slide 34PricewaterhouseCoopers

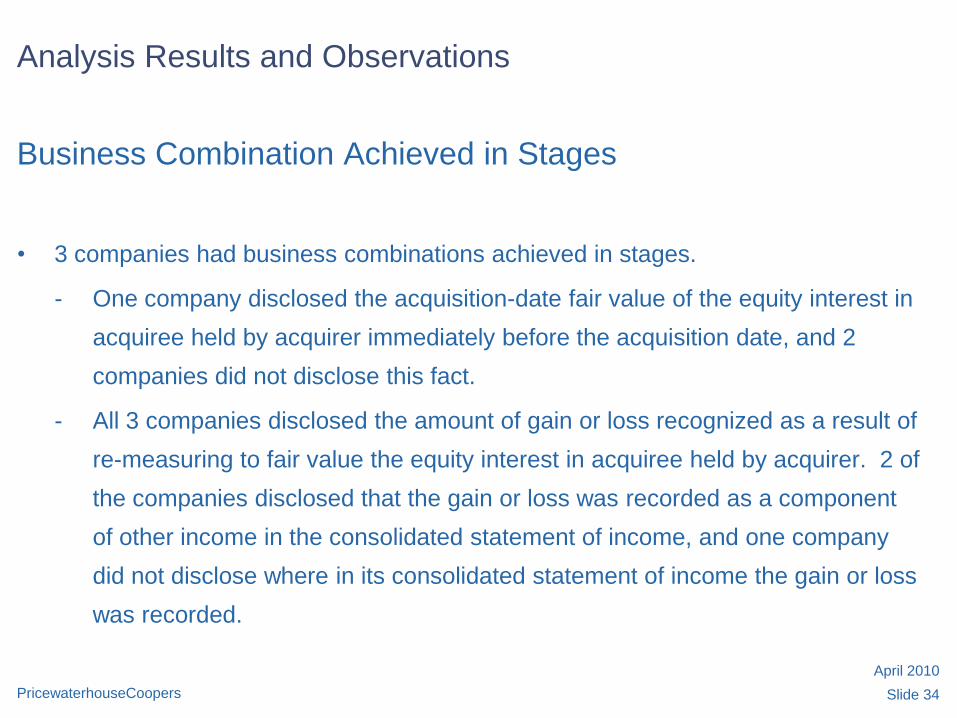

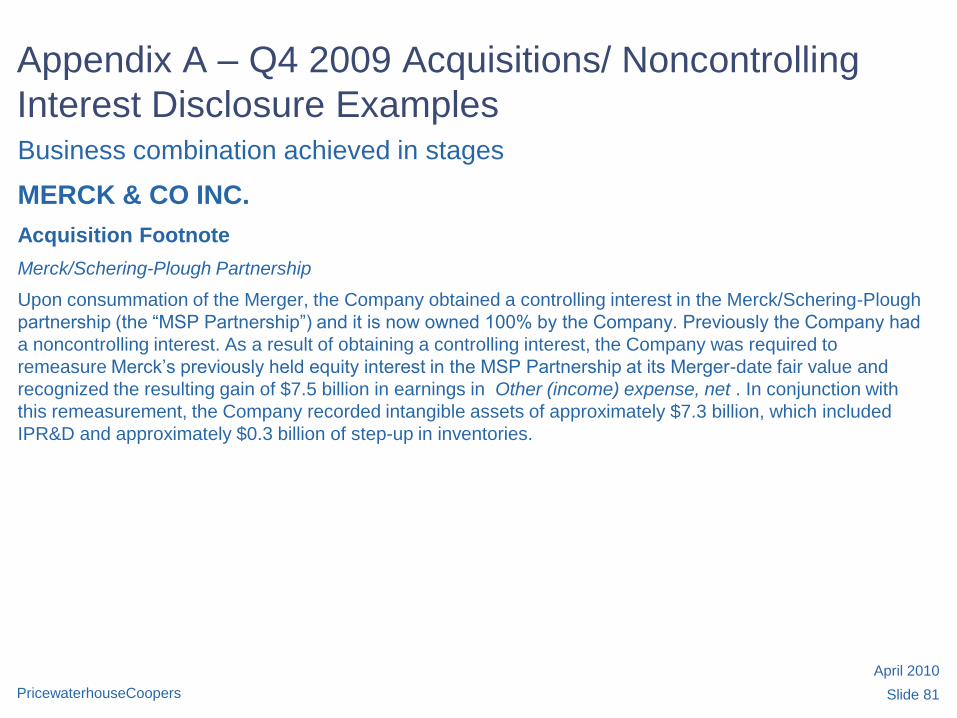

Business Combination Achieved in Stages

• 3 companies had business combinations achieved in stages.

- One company disclosed the acquisition-date fair value of the equity interest in

acquiree held by acquirer immediately before the acquisition date, and 2

companies did not disclose this fact.

- All 3 companies disclosed the amount of gain or loss recognized as a result of

re-measuring to fair value the equity interest in acquiree held by acquirer. 2 of

the companies disclosed that the gain or loss was recorded as a component

of other income in the consolidated statement of income, and one company

did not disclose where in its consolidated statement of income the gain or loss

was recorded.

April 2010

Analysis Results and Observations

Slide 35PricewaterhouseCoopers

Company Reasons why the transaction resulted in a

gain

Amount of gain recognized

Tower Group,

Inc.

Not disclosed As the fair value of net assets

acquired was in excess of the total

purchase consideration, the gain on

bargain purchase of $13.2 million was

recognized in other income.

Bargain Purchase Gain

• As illustrated in the following tables, 2 companies reported a bargain purchase

gain.

April 2010

Analysis Results and Observations

Slide 36PricewaterhouseCoopers

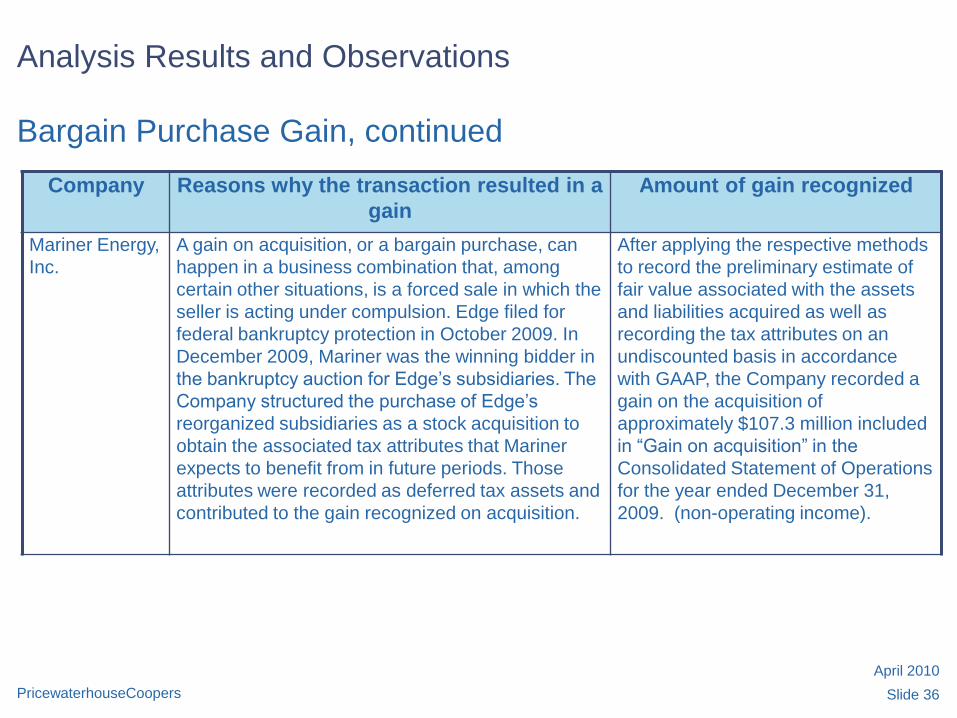

Company Reasons why the transaction resulted in a

gain

Amount of gain recognized

Mariner Energy,

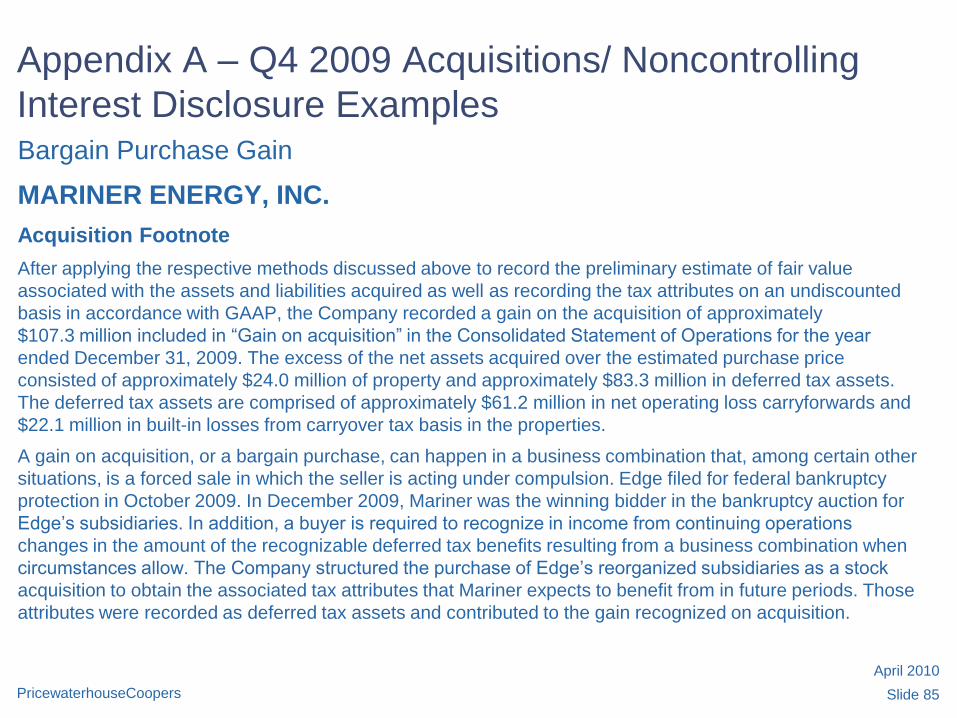

Inc.

A gain on acquisition, or a bargain purchase, can

happen in a business combination that, among

certain other situations, is a forced sale in which the

seller is acting under compulsion. Edge filed for

federal bankruptcy protection in October 2009. In

December 2009, Mariner was the winning bidder in

the bankruptcy auction for Edge’s subsidiaries. The

Company structured the purchase of Edge’s

reorganized subsidiaries as a stock acquisition to

obtain the associated tax attributes that Mariner

expects to benefit from in future periods. Those

attributes were recorded as deferred tax assets and

contributed to the gain recognized on acquisition.

After applying the respective methods

to record the preliminary estimate of

fair value associated with the assets

and liabilities acquired as well as

recording the tax attributes on an

undiscounted basis in accordance

with GAAP, the Company recorded a

gain on the acquisition of

approximately $107.3 million included

in ―Gain on acquisition‖ in the

Consolidated Statement of Operations

for the year ended December 31,

2009. (non-operating income).

Bargain Purchase Gain, continued

April 2010

Analysis Results and Observations

Slide 37PricewaterhouseCoopers

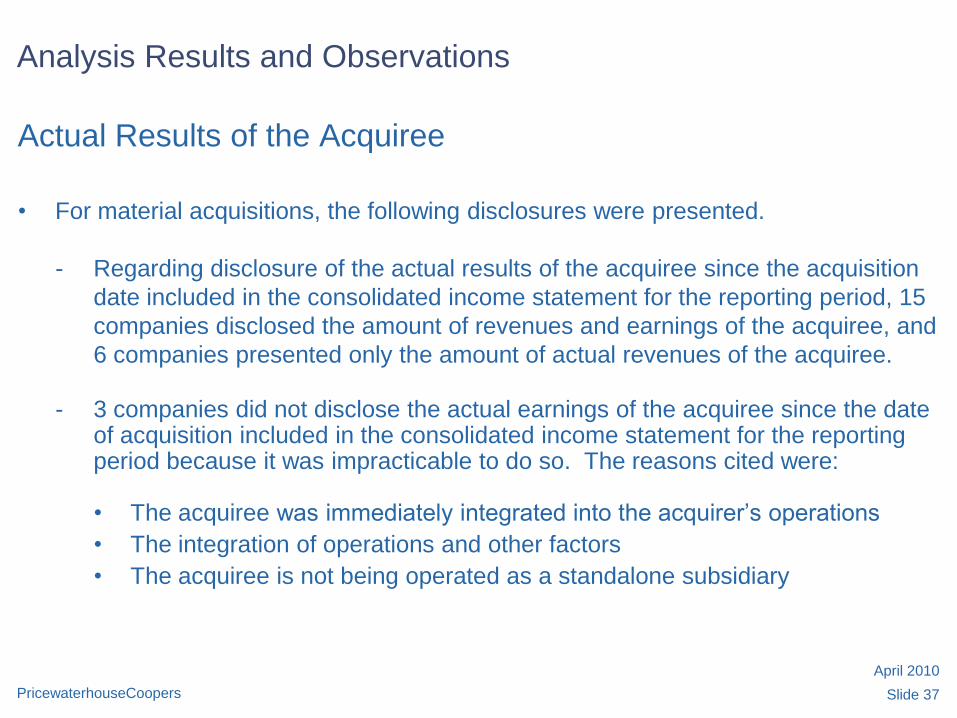

Actual Results of the Acquiree

• For material acquisitions, the following disclosures were presented.

- Regarding disclosure of the actual results of the acquiree since the acquisition

date included in the consolidated income statement for the reporting period, 15

companies disclosed the amount of revenues and earnings of the acquiree, and

6 companies presented only the amount of actual revenues of the acquiree.

- 3 companies did not disclose the actual earnings of the acquiree since the date of acquisition included in the consolidated income statement for the reporting period because it was impracticable to do so. The reasons cited were:

• The acquiree was immediately integrated into the acquirer’s operations

• The integration of operations and other factors

• The acquiree is not being operated as a standalone subsidiary

April 2010

Analysis Results and Observations

Slide 38PricewaterhouseCoopers

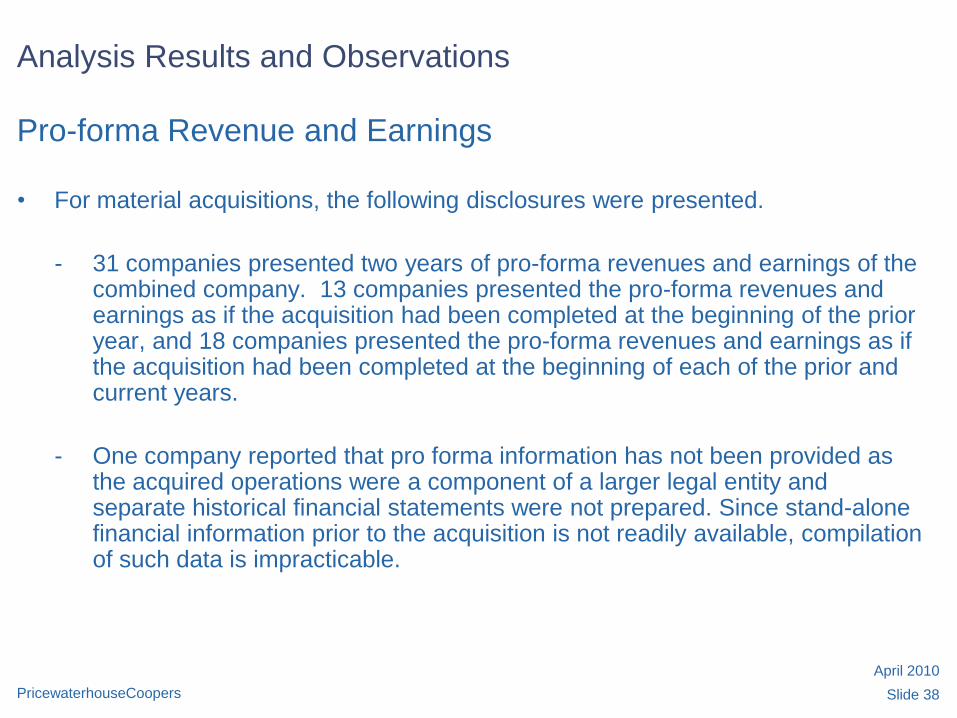

Pro-forma Revenue and Earnings

• For material acquisitions, the following disclosures were presented.

- 31 companies presented two years of pro-forma revenues and earnings of the combined company. 13 companies presented the pro-forma revenues and earnings as if the acquisition had been completed at the beginning of the prior year, and 18 companies presented the pro-forma revenues and earnings as if the acquisition had been completed at the beginning of each of the prior and current years.

- One company reported that pro forma information has not been provided as the acquired operations were a component of a larger legal entity and separate historical financial statements were not prepared. Since stand-alone financial information prior to the acquisition is not readily available, compilation of such data is impracticable.

April 2010

Analysis Results and Observations

Slide 39PricewaterhouseCoopers

Pro-forma Revenue and Earnings, continued

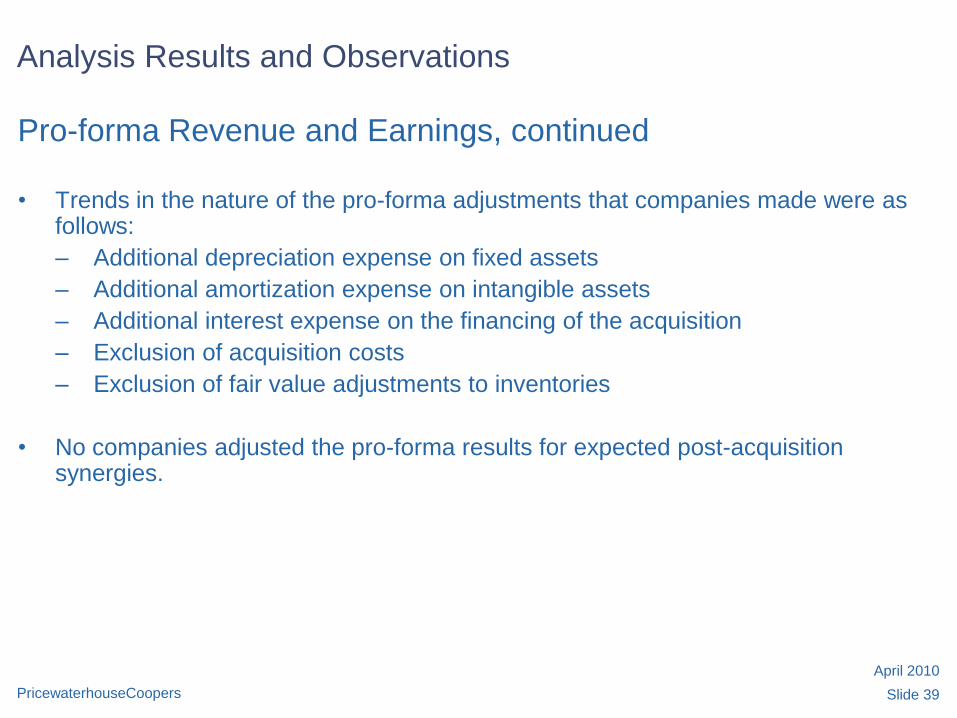

• Trends in the nature of the pro-forma adjustments that companies made were as follows:

– Additional depreciation expense on fixed assets

– Additional amortization expense on intangible assets

– Additional interest expense on the financing of the acquisition

– Exclusion of acquisition costs

– Exclusion of fair value adjustments to inventories

• No companies adjusted the pro-forma results for expected post-acquisition synergies.

April 2010

Analysis Results and Observations

Slide 40PricewaterhouseCoopers

Noncontrolling Interest

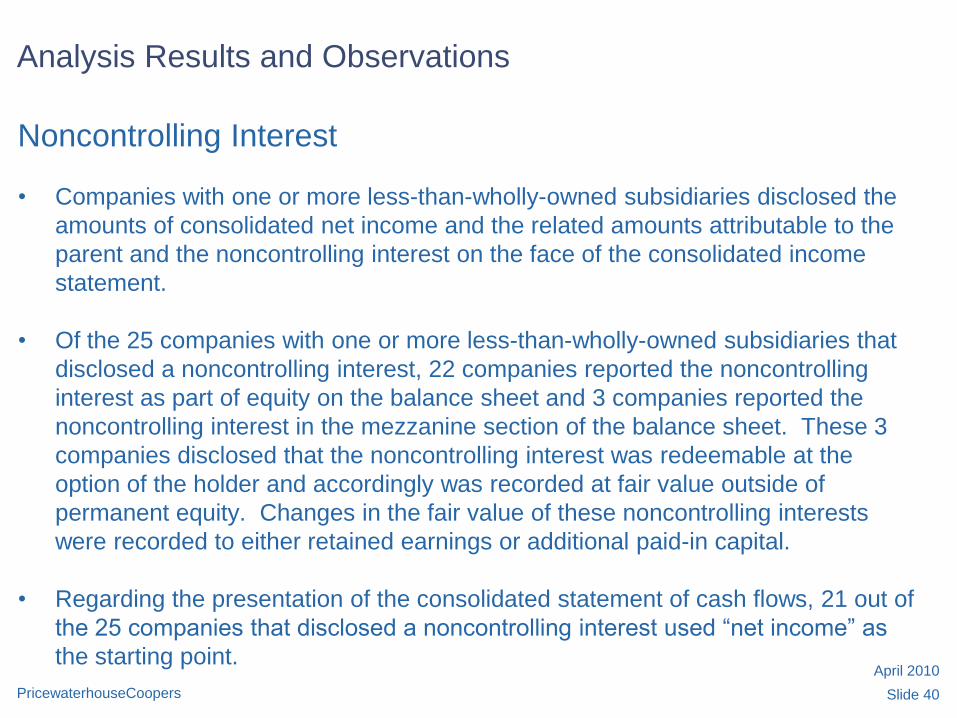

• Companies with one or more less-than-wholly-owned subsidiaries disclosed the

amounts of consolidated net income and the related amounts attributable to the

parent and the noncontrolling interest on the face of the consolidated income

statement.

• Of the 25 companies with one or more less-than-wholly-owned subsidiaries that

disclosed a noncontrolling interest, 22 companies reported the noncontrolling

interest as part of equity on the balance sheet and 3 companies reported the

noncontrolling interest in the mezzanine section of the balance sheet. These 3

companies disclosed that the noncontrolling interest was redeemable at the

option of the holder and accordingly was recorded at fair value outside of

permanent equity. Changes in the fair value of these noncontrolling interests

were recorded to either retained earnings or additional paid-in capital.

• Regarding the presentation of the consolidated statement of cash flows, 21 out of

the 25 companies that disclosed a noncontrolling interest used ―net income‖ as

the starting point.

April 2010

Sample Selected

Slide 41PricewaterhouseCoopers

Company Name Auditor Company Name Auditor Company Name Auditor

Abbott Laboratories D&T Broadcom Corp. KPMG Dress Barn Inc. D&T

Amazon.com Inc. E&Y CA, Inc. KPMG Emerson Electric

Co.

KPMG

Applied Materials Inc. KPMG Cameron

International

Corporation

E&Y Express Scripts Inc. PwC

Arch Coal Inc. E&Y Cavium Networks,

Inc.

PwC Fidelity National

Information Services

Inc.

KPMG

Arrow Electronics, Inc. E&Y Chesapeake Utilities

Corp.

Parente

Beard

FMC Technologies,

Inc.

KPMG

AT&T, Inc. E&Y Cisco Systems, Inc. PwC Green Mountain

Coffee Roasters Inc.

PwC

Atheros

Communications Inc.

PwC Compuware Corp. D&T GSI Commerce Inc. D&T

Ball Corporation PwC Covidien plc D&T Holly Energy

Partners L.P

E&Y

Becton, Dickinson,

and Company

E&Y Cubist

Pharmaceuticals Inc.

PwC Hubbell Inc. PwC

Slide 41

April 2010

Sample Selected

Slide 42PricewaterhouseCoopers

Company Name Auditor Company Name Auditor Company Name Auditor

International

Business Machines

Corp.

PwC Nuance

Communications, Inc.

BDO TeleCommunication

Systems Inc.

E&Y

Intuit Inc. E&Y Onyx Pharmaceuticals

Inc.

E&Y Tellabs Inc. E&Y

Kinder Morgan

Energy Partners LP

PwC Pfizer Inc. KPMG The DIRECTV Group,

Inc.

D&T

Mariner Energy, Inc. D&T Quanta Services Inc. PwC Thermo Fisher

Scientific, Inc.

PwC

MasTec, Inc. BDO Resources Connection

Inc.

PwC Tower Group Inc. Johnson

Lambert

& Co

MEMC Electronic

Materials Inc.

KPMG Scripps Networks

Interactive, Inc.

D&T ViaSat Inc. PwC

Merck & Co. Inc. PwC Sprint Nextel Corp. KPMG Walt Disney Co. PwC

NetLogic

Microsystems Inc.

PwC Stryker Corp. E&Y Warner Chilcott plc PwC

Slide 42

April 2010

Sample Selected

Slide 43PricewaterhouseCoopers

Company Name Auditor Company Name Auditor Company Name Auditor

Watson

Pharmaceuticals

Inc.

PwC Windstream

Corporation

PwC

Westinghouse Air

Brake Technologies

Corporation

E&Y

Slide 43

April 2010

Appendix A

Q4 2009 Acquisitions/ Noncontrolling Interest

Disclosure Examples

April 2010

Appendix A – Q4 2009 Acquisitions/ Noncontrolling interest Disclosure Examples

Table of ContentsPage

Purchase price allocation 46-50

Acquisition related costs 51-53

Consideration transferred 54-55

Contingent consideration 56-63

Acquired contingencies 64-70

Intangible assets 71-72

Defensive intangible assets 73-74

IPR&D 75-80

Business combinations achieved in stages 81-84

Bargain purchase gain 85

Pro-forma revenue and earnings 86-87

Tax Accounts 88

Noncontrolling interest 89-96

April 2010

Appendix A – Q4 2009 Acquisitions/ Noncontrolling

Interest Disclosure Examples

Slide 46PricewaterhouseCoopers

Purchase Price Allocation

STRYKER CORPORATION

Acquisition Footnote

For all acquisitions, the preliminary allocation of the purchase price was based upon a preliminary valuation,

and the Company’s estimates and assumptions are subject to change within the measurement period as

valuations are finalized. The table below represents the allocation of the preliminary purchase price to the

acquired net assets of Ascent and all other acquisitions completed in 2009 (in millions):

Ascent All Other Total Accounts receivable $ 10.6 $ 0.1 $ 10.7 Inventory 10.3 0.2 10.5 Other current assets 6.3 2.9 9.2 Identifiable intangible assets:

Customer relationship 221.1 9.1 230.2

Developed technology 22.5 18.5 41.0 In-process research and development — 20.2 20.2 Trademarks 5.0 — 5.0 Other — 1.7 1.7

Goodwill 329.1 58.4 387.5 Other assets 22.7 5.2 27.9 Current liabilities (6.3 ) (2.0 ) (8.3 ) Contingent consideration — (45.1 ) (45.1 ) Noncurrent deferred income tax liabilities (96.7 ) (18.5 ) (115.2 ) Other liabilities — (0.5 ) (0.5 )

April 2010

Appendix A – Q4 2009 Acquisitions/ Noncontrolling

Interest Disclosure Examples

Slide 47PricewaterhouseCoopers

Purchase Price Allocation

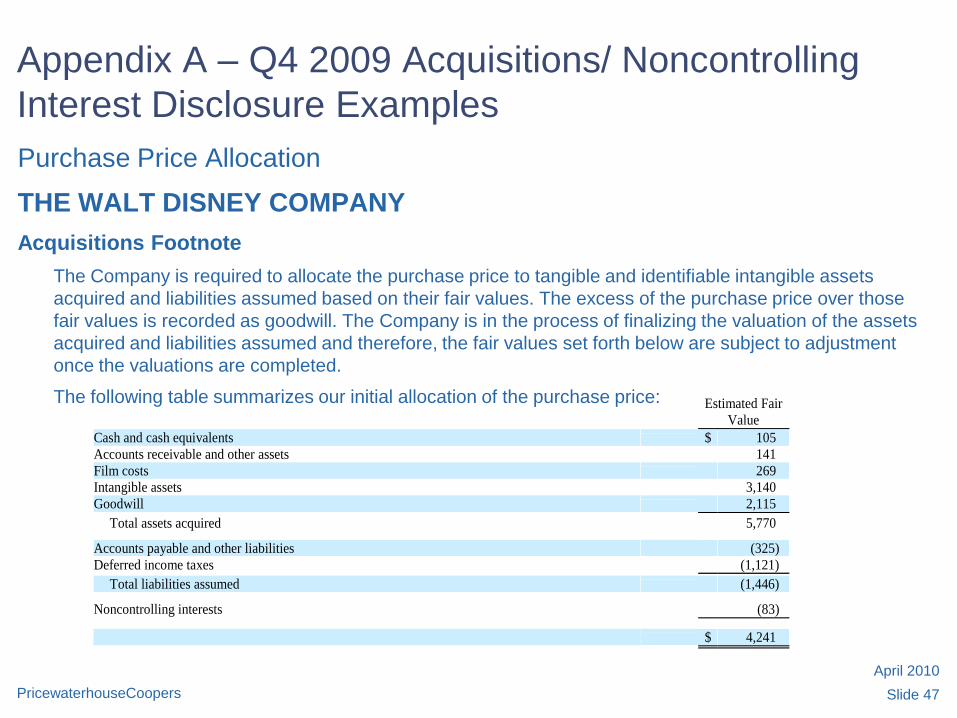

THE WALT DISNEY COMPANY

Acquisitions Footnote

The Company is required to allocate the purchase price to tangible and identifiable intangible assets

acquired and liabilities assumed based on their fair values. The excess of the purchase price over those

fair values is recorded as goodwill. The Company is in the process of finalizing the valuation of the assets

acquired and liabilities assumed and therefore, the fair values set forth below are subject to adjustment

once the valuations are completed.

The following table summarizes our initial allocation of the purchase price:

Estimated Fair

Value Cash and cash equivalents $ 105 Accounts receivable and other assets 141 Film costs 269 Intangible assets 3,140 Goodwill 2,115

Total assets acquired 5,770 Accounts payable and other liabilities (325) Deferred income taxes (1,121)

Total liabilities assumed (1,446) Noncontrolling interests (83)

$ 4,241

April 2010

Appendix A – Q4 2009 Acquisitions/ Noncontrolling

Interest Disclosure Examples

Slide 48PricewaterhouseCoopers

Purchase Price Allocation

TOWER GROUP INC.

Acquisition Footnote

($ in thousands) Level 1 Level 2 Level 3 Total

Assets

Investments $4,734 $ 241,515 $- $ 246,249

Cash and cash equivalents 54,377 - - 54,377

Receivables - - 62,039 62,039

Prepaid reinsurance premiums - - 1,930 1,930

Reinsurance recoverable - - 73,888 73,888

Deferred acquisition costs/VOBA - - 17,149 17,149

Deferred income taxes - - 11,450 11,450

Intangibles - - 11,930 11,930

Other assets - - 21,133 21,133

Liabilities and Stockholders’ Equity

Loss and loss adjustment expenses - - (252,905) (252,905)

Unearned premium - - (98,577) (98,577)

Other liabilities - - (28,814) (28,814)

Net assets acquired 119,849

Total purchase consideration 106,663

Gain on bargain purchase $ (13,186)

April 2010

Appendix A – Q4 2009 Acquisitions/ Noncontrolling

Interest Disclosure Examples

Slide 49PricewaterhouseCoopers

Purchase Price Allocation

SCRIPPS NETWORKS INTERACTIVE, INC.

Acquisition Footnote

On December 15, 2009 we acquired a 65 percent controlling interest in the Travel Channel. The

transaction was structured as a leveraged joint venture between SNI and Cox TMI, Inc., a wholly owned

subsidiary of Cox Communications, Inc. (―Cox‖). Pursuant to the terms of the transaction, Cox contributed

the Travel Channel, valued at $975 million, and SNI contributed $181 million in cash to a newly created

partnership. The partnership also completed a private placement of $885 million aggregate principal

amount of notes (―Senior Notes‖) that were guaranteed by SNI. Cox has agreed to indemnify SNI for

payments made in respect of SNI’s guarantee (see Note 15—Long-Term Debt for additional details).

Proceeds from the issuance of the Senior Notes totaling $877.5 million were distributed to Cox. In

connection with the transaction, SNI received a 65% controlling interest in Travel Channel and Cox

retained a 35% non-controlling interest in the business. This transaction provides a unique opportunity to

meaningfully expand SNI’s portfolio into a lifestyle category that’s highly desirable to media consumers,

advertisers and programming distributors. As part of the transaction, the partnership incurred financing and

transaction related costs of approximately $22.3 million. Approximately $10.2 million of these costs is

included in the caption other costs and expenses and $12.1 million are included in the caption Travel

Channel financing costs in our consolidated and combined statement of operations for the year ended

December 31, 2009. Debt issuance costs of $6.1 million were incurred in connection with the issuance of

the Senior Notes and were capitalized in the caption other assets in our consolidated balance sheet.

April 2010

Appendix A – Q4 2009 Acquisitions/ Noncontrolling

Interest Disclosure Examples

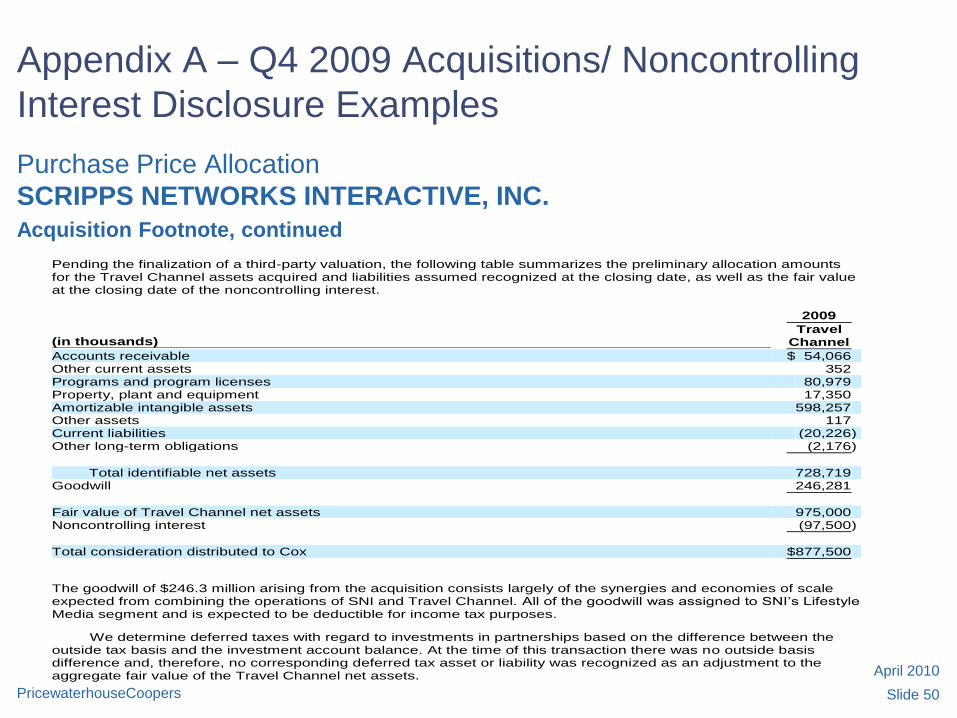

Slide 50PricewaterhouseCoopers

Purchase Price Allocation

SCRIPPS NETWORKS INTERACTIVE, INC.

Acquisition Footnote, continued

Pending the finalization of a third-party valuation, the following table summarizes the preliminary allocation amounts for the Travel Channel assets acquired and liabilities assumed recognized at the closing date, as well as the fair value at the closing date of the noncontrolling interest. 2009

(in thousands) Travel

Channel

Accounts receivable $ 54,066 Other current assets 352 Programs and program licenses 80,979 Property, plant and equipment 17,350 Amortizable intangible assets 598,257 Other assets 117 Current liabilities (20,226 ) Other long-term obligations (2,176 )

Total identifiable net assets 728,719 Goodwill 246,281

Fair value of Travel Channel net assets 975,000 Noncontrolling interest (97,500 )

Total consideration distributed to Cox $ 877,500

The goodwill of $246.3 million arising from the acquisition consists largely of the synergies and economies of scale expected from combining the operations of SNI and Travel Channel. All of the goodwill was assigned to SNI’s Lifestyle Media segment and is expected to be deductible for income tax purposes.

We determine deferred taxes with regard to investments in partnerships based on the difference between the outside tax basis and the investment account balance. At the time of this transaction there was no outside basis difference and, therefore, no corresponding deferred tax asset or liability was recognized as an adjustment to the aggregate fair value of the Travel Channel net assets.

April 2010

Appendix A – Q4 2009 Acquisitions/ Noncontrolling

Interest Disclosure Examples

Slide 51PricewaterhouseCoopers

Acquisition Costs

EXPRESS SCRIPTS INC.

Acquisitions Footnote

For the year ended December 31, 2009, we incurred transaction costs of $61.1 million related to the

acquisition which are included in selling, general and administrative expense. In accordance with the

accounting guidance for business combinations which became effective in 2009, the transaction costs were

expensed as incurred.

April 2010

Appendix A – Q4 2009 Acquisitions/ Noncontrolling

Interest Disclosure Examples

Slide 52PricewaterhouseCoopers

Acquisition Costs

SCRIPPS NETWORKS INTERACTIVE INC.

Acquisitions Footnote

As part of the transaction, the partnership incurred financing and transaction related costs of approximately

$22.3 million. Approximately $10.2 million of these costs is included in the caption other costs and expenses

and $12.1 million are included in the caption Travel Channel financing costs in our consolidated and combined

statement of operations for the year ended December 31, 2009. Debt issuance costs of $6.1 million were

incurred in connection with the issuance of the Senior Notes and were capitalized in the caption other assets

in our consolidated balance sheet.

April 2010

Appendix A – Q4 2009 Acquisitions/ Noncontrolling

Interest Disclosure Examples

Slide 53PricewaterhouseCoopers

Acquisition Costs

PFIZER INC.

Acquisition-Cost Footnote

We incurred the following costs in connection with our cost-reduction initiatives and the Wyeth acquisition:

YEAR ENDED DECEMBER 31,

(MILLIONS OF DOLLARS) 2009 2008 2007 Transaction costs(a) $ 768

$ — $ —

Integration costs and other(b) 569

49 11 Restructuring charges 3,000 2,626 2,523

Restructuring charges and certain acquisition-related costs 4,337 2,675 2,534 Additional depreciation—asset restructuring 241

786 788

Implementation costs 250 819 601 Total $ 4,828

$ 4,280 $ 3,923

(a) Transaction costs represent external costs directly related to effecting the acquisition of Wyeth and primarily include expenditures for banking, legal, accounting and other similar services. Substantially all of the costs incurred are fees related to a $22.5 billion bridge term loan credit agreement entered into with certain financial institutions on March 12, 2009 to partially fund our acquisition of Wyeth. The bridge term loan credit agreement was terminated in June 2009 as a result of our issuance of approximately $24.0 billion of senior unsecured notes in the first half of 2009. All bridge term loan commitment fees have been expensed, and we no longer are subject to the covenants under that agreement (see Note 9D: Financial Instruments: Long-Term Debt).

(b) Integration costs represent external, incremental costs directly related to integrating acquired businesses and primarily include expenditures for consulting and systems integration.

April 2010

Appendix A – Q4 2009 Acquisitions/ Noncontrolling

Interest Disclosure Examples

Slide 54PricewaterhouseCoopers

Consideration Transferred

ATHEROS COMMUNICATIONS INC.

Business Combinations Footnote

Under the terms of the merger agreement, the Company paid an aggregate of $113,627,000 in cash

($70,701,000 net of cash acquired) and exchanged 4,500,000 shares of the Company’s common stock and

equivalents for 32,503,000 of Intellon’s outstanding common stock and equivalents, valued at $140,348,000 to

Intellon shareholders upon closing, resulting in total acquisition consideration of $253,975,000. The Company

issued to Intellon employees on December 15, 2009, options to purchase 631,000 shares of the Company’s

common stock, 189,000 restricted stock units (―RSUs‖) of the Company’s common stock and 16,000 restricted

stock awards with an aggregate value of approximately $18,183,000, in exchange for their options to purchase

shares, restricted stock units, and restricted stock awards of Intellon. Of this amount, 272,000 stock options

and 28,000 RSUs were earned prior to the acquisition date, and therefore, the Company recorded $5,189,000

as part of the acquisition consideration. The remaining 359,000 stock options, 161,000 RSUs and 16,000

restricted stock awards will result in compensation expense of $12,994,000, which will be recognized over the

remaining vesting period of these equity awards, which ranges from one day to four years, subject to

adjustment based on estimated forfeitures. Additionally, on December 15, 2009, the Company issued 356,000

restricted stock units of the Company’s common stock to employees of Intellon valued at $11,456,000, subject

to adjustment based on estimated forfeitures, and will recognize this amount as compensation expense over a

period ranging from one to four years. The value of the Company’s common stock and equivalents issued was

determined based on the Company’s closing share price on December 15, 2009 (the acquisition date), or

$32.18 per share.

April 2010

Appendix A – Q4 2009 Acquisitions/ Noncontrolling

Interest Disclosure Examples

Slide 55PricewaterhouseCoopers

Consideration Transferred

WINDSTREAM CORPORATION

Acquisitions Footnote

In accordance with the D&E Merger Agreement, D&E shareholders received 0.650 shares of Windstream

common stock and $5.00 in cash per each share of D&E Common Stock. Windstream issued approximately

9.4 million shares of its common stock valued at approximately $94.6 million, based on Windstream’s closing

stock price of $10.06 on November 9, 2009, and paid $56.6 million, net of cash acquired, as part of the

transaction. Subsequently, Windstream repaid outstanding debt of D&E totaling $182.4 million including

current maturities.

April 2010

Appendix A – Q4 2009 Acquisitions/ Noncontrolling

Interest Disclosure Examples

Slide 56PricewaterhouseCoopers

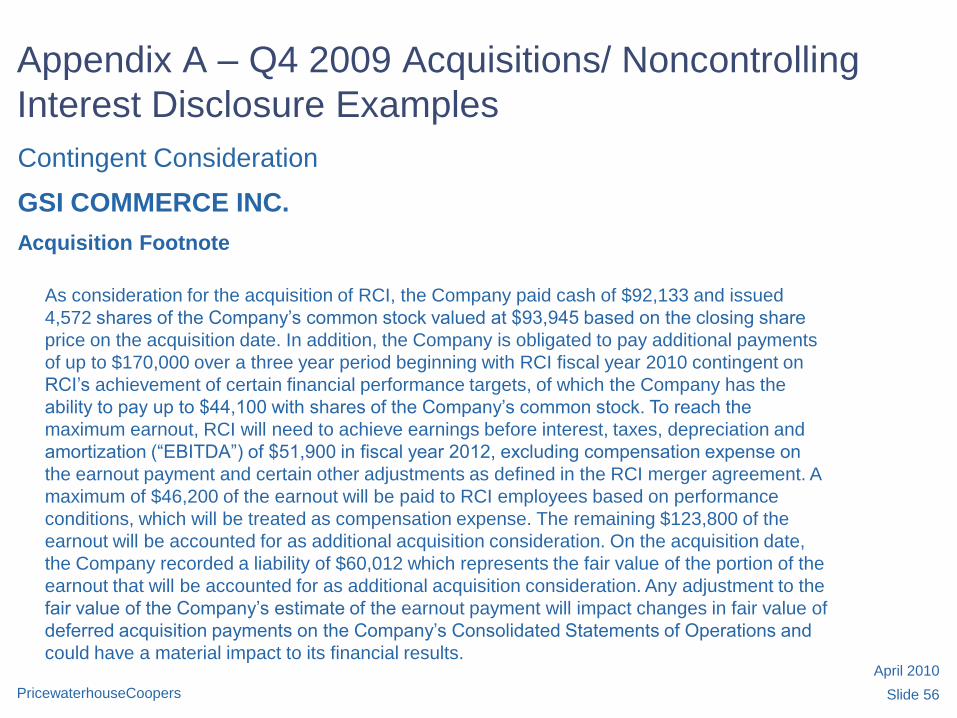

Contingent Consideration

GSI COMMERCE INC.

Acquisition Footnote

As consideration for the acquisition of RCI, the Company paid cash of $92,133 and issued

4,572 shares of the Company’s common stock valued at $93,945 based on the closing share

price on the acquisition date. In addition, the Company is obligated to pay additional payments

of up to $170,000 over a three year period beginning with RCI fiscal year 2010 contingent on

RCI’s achievement of certain financial performance targets, of which the Company has the

ability to pay up to $44,100 with shares of the Company’s common stock. To reach the

maximum earnout, RCI will need to achieve earnings before interest, taxes, depreciation and

amortization (―EBITDA‖) of $51,900 in fiscal year 2012, excluding compensation expense on

the earnout payment and certain other adjustments as defined in the RCI merger agreement. A

maximum of $46,200 of the earnout will be paid to RCI employees based on performance

conditions, which will be treated as compensation expense. The remaining $123,800 of the

earnout will be accounted for as additional acquisition consideration. On the acquisition date,

the Company recorded a liability of $60,012 which represents the fair value of the portion of the

earnout that will be accounted for as additional acquisition consideration. Any adjustment to the

fair value of the Company’s estimate of the earnout payment will impact changes in fair value of

deferred acquisition payments on the Company’s Consolidated Statements of Operations and

could have a material impact to its financial results.

April 2010

Appendix A – Q4 2009 Acquisitions/ Noncontrolling

Interest Disclosure Examples

Slide 57PricewaterhouseCoopers

Contingent Consideration

NETLOGIC MICROSYSTEMS INC.

Acquisition Footnote

The Company may be required to issue up to an additional 1.6 million shares of common stock and pay up to

an additional $15.9 million cash to the former holders of RMI capital stock as earn-out consideration based

upon achieving specified percentages of revenue targets for either the 12-month period from October 1, 2009

through September 30, 2010, or the 12-month period from November 1, 2009 through October 31, 2010,

whichever period results in the higher percentage of the revenue target. The additional earn-out consideration,

if any, net of applicable indemnity claims, will be paid on or before December 31, 2010.

Fair Value of Consideration Transferred:

Issuance of Netlogic common stock to RMI preferred shareholders $ 188,527

Payments to RMI common shareholders in cash 12,582

Acquisition-related contingent consideration 9,679

Other adjustments (837)

Total $ 209,951

April 2010

Appendix A – Q4 2009 Acquisitions/ Noncontrolling

Interest Disclosure Examples

Slide 58PricewaterhouseCoopers

Contingent Consideration

NETLOGIC MICROSYSTEMS INC.

Acquisition Footnote, continued

In accordance with ASC 805 Business Combinations, a liability was recognized for the estimated merger date

fair value of the acquisition-related contingent consideration based on the probability of the achievement of the

revenue target. Any change in the fair value of the acquisition-related contingent consideration subsequent to

the merger date, including changes from events after the acquisition date, such as changes in the Company’s

estimate of the revenue expected to be achieved and changes in its stock price, will be recognized in earnings

in the period the estimated fair value changes. The fair value estimate assumes probability-weighted revenues

are achieved over the earn-out period. Actual achievement of revenues at or below 75% of the revenue range

for this assumed earn-out period would reduce the liability to zero. If actual achievement of revenues is

at or above 100% of the revenue target, the RMI stockholders will receive the maximum consideration of 1.6

million shares and $15.9 million in cash. If the amount of revenue recognized is greater than 75% but less

than 100% of the revenue target, the RMI stockholders will receive an earn-out consideration that increases

as the percentage gets closer to 100%. A change in the fair value of the acquisition-related contingent

consideration could have a material impact on the Company’s statement of operations and financial position in

the period of the change in estimate.

April 2010

Appendix A – Q4 2009 Acquisitions/ Noncontrolling

Interest Disclosure Examples

Slide 59PricewaterhouseCoopers

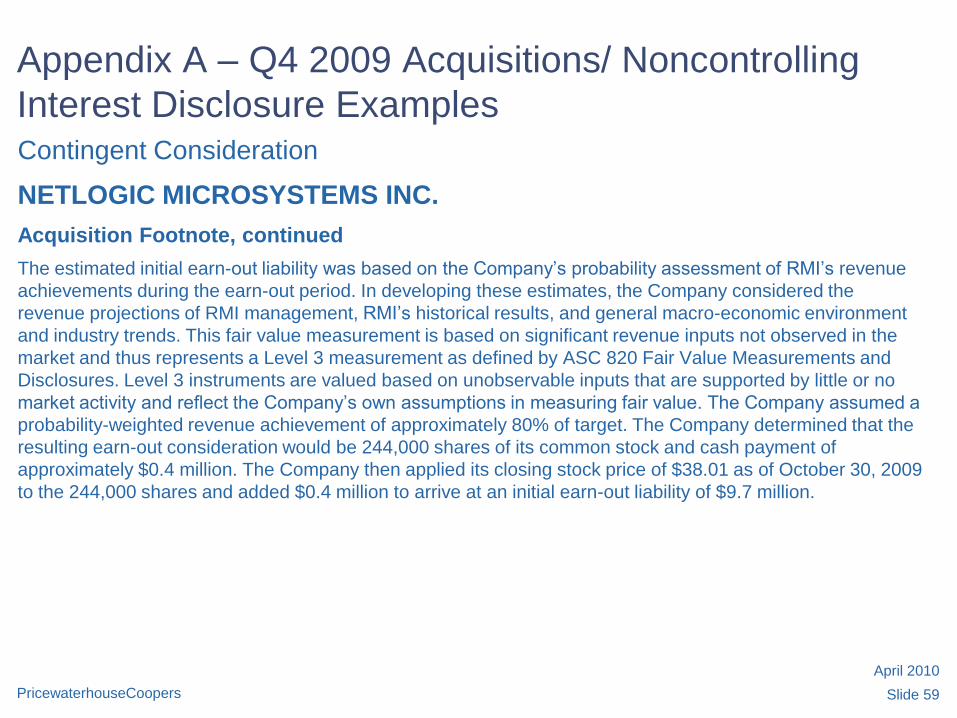

Contingent Consideration

NETLOGIC MICROSYSTEMS INC.

Acquisition Footnote, continued

The estimated initial earn-out liability was based on the Company’s probability assessment of RMI’s revenue

achievements during the earn-out period. In developing these estimates, the Company considered the

revenue projections of RMI management, RMI’s historical results, and general macro-economic environment

and industry trends. This fair value measurement is based on significant revenue inputs not observed in the

market and thus represents a Level 3 measurement as defined by ASC 820 Fair Value Measurements and

Disclosures. Level 3 instruments are valued based on unobservable inputs that are supported by little or no

market activity and reflect the Company’s own assumptions in measuring fair value. The Company assumed a

probability-weighted revenue achievement of approximately 80% of target. The Company determined that the

resulting earn-out consideration would be 244,000 shares of its common stock and cash payment of

approximately $0.4 million. The Company then applied its closing stock price of $38.01 as of October 30, 2009

to the 244,000 shares and added $0.4 million to arrive at an initial earn-out liability of $9.7 million.

April 2010

Appendix A – Q4 2009 Acquisitions/ Noncontrolling

Interest Disclosure Examples

Slide 60PricewaterhouseCoopers

Contingent Consideration

FMC TECHNOLOGIES, INC.

Acquisition Footnote

Direct Drive Systems, Inc. (“DDS”) and Multi Phase Meters AS (“MPM”)—

The acquisition-date fair value of the consideration transferred totaled $213.7 million which consisted of the

following:

The contingent consideration arrangement requires us to pay additional consideration to MPM’s former

shareholders in 2013 and 2014, based on a multiple of 2012 and 2013 earnings before income taxes,

depreciation and amortization (―EBITDA‖), less net interest-bearing debt. We estimated the fair value of the

contingent consideration using a discounted cash flow model. The key assumption in applying the income

approach was a discount rate of 3.48% and 4.10% for 2012 and 2013, respectively, which reflects our debt credit

rating. We have estimated that the total undiscounted payment required under the contingent consideration

arrangement will approximate $64.6 million, with no set maximum payment. The fair value measurement is based

on significant inputs not observable in the market and thus represents a Level 3 measurement as defined by the

FASB. As of December 31, 2009, there were no changes in the range of outcomes for the contingent

consideration.

(In millions) DDS MPM Total

Cash

$ 120.4 $ 33.1 $ 153.5

Earn-out contingent consideration — 56.1 56.1

Debt assumed — 4.1 4.1

Total $ 120.4 $ 93.3 $ 213.7

April 2010

Appendix A – Q4 2009 Acquisitions/ Noncontrolling

Interest Disclosure Examples

Slide 61PricewaterhouseCoopers

Contingent Consideration

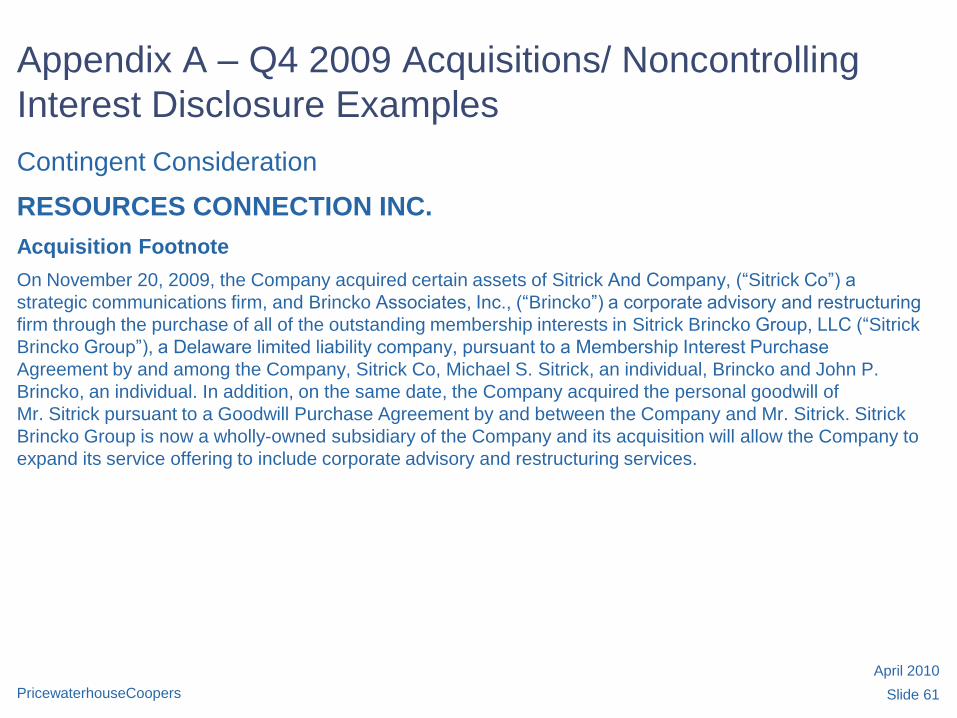

RESOURCES CONNECTION INC.

Acquisition Footnote

On November 20, 2009, the Company acquired certain assets of Sitrick And Company, (―Sitrick Co‖) a

strategic communications firm, and Brincko Associates, Inc., (―Brincko‖) a corporate advisory and restructuring

firm through the purchase of all of the outstanding membership interests in Sitrick Brincko Group, LLC (―Sitrick

Brincko Group‖), a Delaware limited liability company, pursuant to a Membership Interest Purchase

Agreement by and among the Company, Sitrick Co, Michael S. Sitrick, an individual, Brincko and John P.

Brincko, an individual. In addition, on the same date, the Company acquired the personal goodwill of

Mr. Sitrick pursuant to a Goodwill Purchase Agreement by and between the Company and Mr. Sitrick. Sitrick

Brincko Group is now a wholly-owned subsidiary of the Company and its acquisition will allow the Company to

expand its service offering to include corporate advisory and restructuring services.

April 2010

Appendix A – Q4 2009 Acquisitions/ Noncontrolling

Interest Disclosure Examples

Slide 62PricewaterhouseCoopers

Contingent Consideration, continued

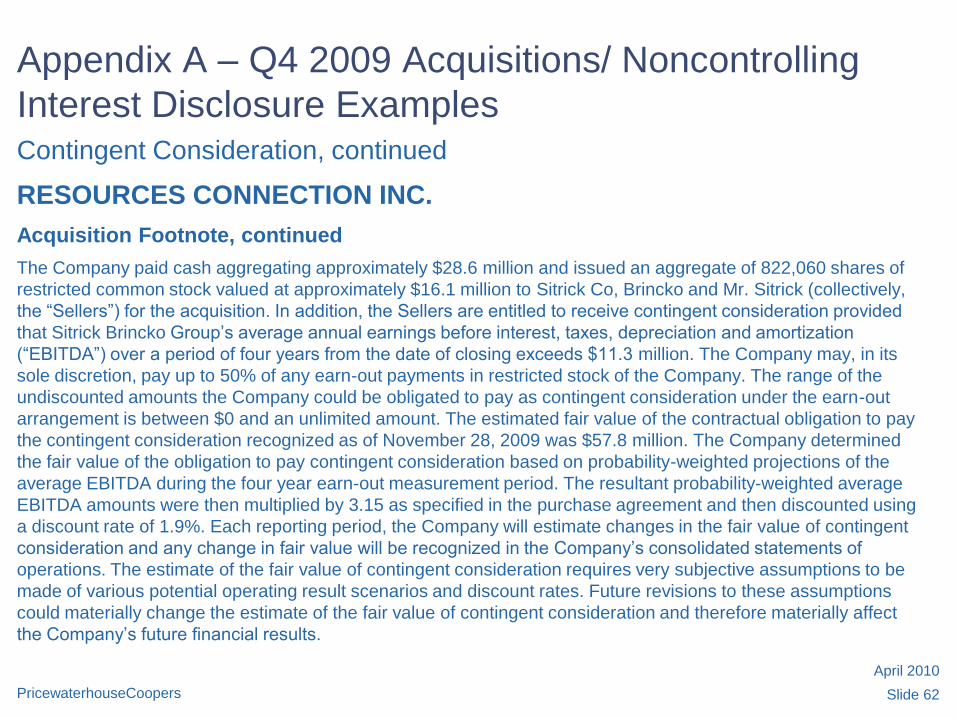

RESOURCES CONNECTION INC.

Acquisition Footnote, continued

The Company paid cash aggregating approximately $28.6 million and issued an aggregate of 822,060 shares of

restricted common stock valued at approximately $16.1 million to Sitrick Co, Brincko and Mr. Sitrick (collectively,

the ―Sellers‖) for the acquisition. In addition, the Sellers are entitled to receive contingent consideration provided

that Sitrick Brincko Group’s average annual earnings before interest, taxes, depreciation and amortization

(―EBITDA‖) over a period of four years from the date of closing exceeds $11.3 million. The Company may, in its

sole discretion, pay up to 50% of any earn-out payments in restricted stock of the Company. The range of the

undiscounted amounts the Company could be obligated to pay as contingent consideration under the earn-out

arrangement is between $0 and an unlimited amount. The estimated fair value of the contractual obligation to pay

the contingent consideration recognized as of November 28, 2009 was $57.8 million. The Company determined

the fair value of the obligation to pay contingent consideration based on probability-weighted projections of the

average EBITDA during the four year earn-out measurement period. The resultant probability-weighted average

EBITDA amounts were then multiplied by 3.15 as specified in the purchase agreement and then discounted using

a discount rate of 1.9%. Each reporting period, the Company will estimate changes in the fair value of contingent

consideration and any change in fair value will be recognized in the Company’s consolidated statements of

operations. The estimate of the fair value of contingent consideration requires very subjective assumptions to be

made of various potential operating result scenarios and discount rates. Future revisions to these assumptions

could materially change the estimate of the fair value of contingent consideration and therefore materially affect

the Company’s future financial results.

April 2010

Appendix A – Q4 2009 Acquisitions/ Noncontrolling

Interest Disclosure Examples

Slide 63PricewaterhouseCoopers

Contingent Consideration, continued

RESOURCES CONNECTION INC.

Acquisition Footnote, continued

In addition, under the terms of the Membership Interest Purchase Agreement and Goodwill Purchase

Agreement, up to 20% of the contingent consideration is payable to the employees of the acquired business at

the end of the measurement period to the extent certain EBITDA growth targets are met. The Company will

record the estimated fair value of the contractual obligation to pay the employee portion of contingent

consideration as compensation expense over the service period as it is deemed probable that such amount is

payable. The estimate of the fair value of the employee portion of contingent consideration payable requires

very subjective assumptions to be made of future operating results, discount rates and probabilities assigned

to various potential operating results scenarios. Future revisions to these assumptions could materially change

the estimate of the fair value of the employee portion of contingent consideration and therefore materially

affect the Company’s future financial results.

April 2010

Appendix A – Q4 2009 Acquisitions/ Noncontrolling

Interest Disclosure Examples

Slide 64PricewaterhouseCoopers

Acquired Contingencies

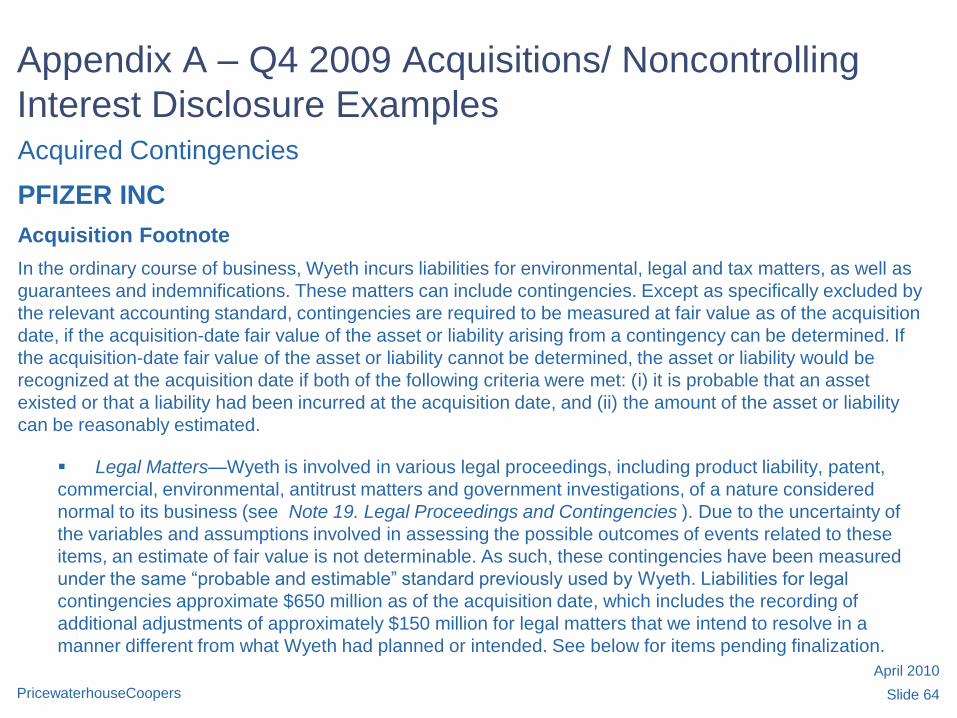

PFIZER INC

Acquisition Footnote

In the ordinary course of business, Wyeth incurs liabilities for environmental, legal and tax matters, as well as

guarantees and indemnifications. These matters can include contingencies. Except as specifically excluded by

the relevant accounting standard, contingencies are required to be measured at fair value as of the acquisition

date, if the acquisition-date fair value of the asset or liability arising from a contingency can be determined. If

the acquisition-date fair value of the asset or liability cannot be determined, the asset or liability would be

recognized at the acquisition date if both of the following criteria were met: (i) it is probable that an asset

existed or that a liability had been incurred at the acquisition date, and (ii) the amount of the asset or liability

can be reasonably estimated.

Legal Matters—Wyeth is involved in various legal proceedings, including product liability, patent,

commercial, environmental, antitrust matters and government investigations, of a nature considered

normal to its business (see Note 19. Legal Proceedings and Contingencies ). Due to the uncertainty of

the variables and assumptions involved in assessing the possible outcomes of events related to these

items, an estimate of fair value is not determinable. As such, these contingencies have been measured

under the same ―probable and estimable‖ standard previously used by Wyeth. Liabilities for legal

contingencies approximate $650 million as of the acquisition date, which includes the recording of

additional adjustments of approximately $150 million for legal matters that we intend to resolve in a

manner different from what Wyeth had planned or intended. See below for items pending finalization.

April 2010

Appendix A – Q4 2009 Acquisitions/ Noncontrolling

Interest Disclosure Examples

Slide 65PricewaterhouseCoopers

Acquired Contingencies

PFIZER INC

Acquisition Footnote, continued

• Environmental Matters—In the ordinary course of business, Wyeth incurs liabilities for environmental

matters such as remediation work, asset retirement obligations and environmental guarantees and

indemnifications. Virtually all liabilities for environmental matters, including contingencies, have been

measured at fair value and approximate $550 million as of the acquisition date.

April 2010

Appendix A – Q4 2009 Acquisitions/ Noncontrolling

Interest Disclosure Examples

Slide 66PricewaterhouseCoopers

Acquired Contingencies

HUBBELL INC.

Acquisition Footnote

The Company assumed Burndy’s pre-exisiting contingent liabilities as part of the acquisition. These contingent

liabilities consisted of contingent consideration related to an acquisition Burndy completed in 2008 as well as

environmental liabilities. The undiscounted fair value related to the contingent consideration liability was

$5.6 million since it is highly probable that the required earning targets will be achieved. Additionally, the

Burndy opening balance sheet includes a $6.2 million contingent liability related to environmental matters. The

estimated fair value portion of this liability is $1.6 million, while the remaining $4.6 million liability was

determined using the guidance prescribed under ASC 450, which requires the loss contingency to be probable

and reasonably estimable.

April 2010

Appendix A – Q4 2009 Acquisitions/ Noncontrolling

Interest Disclosure Examples

Slide 67PricewaterhouseCoopers

Acquired Contingencies

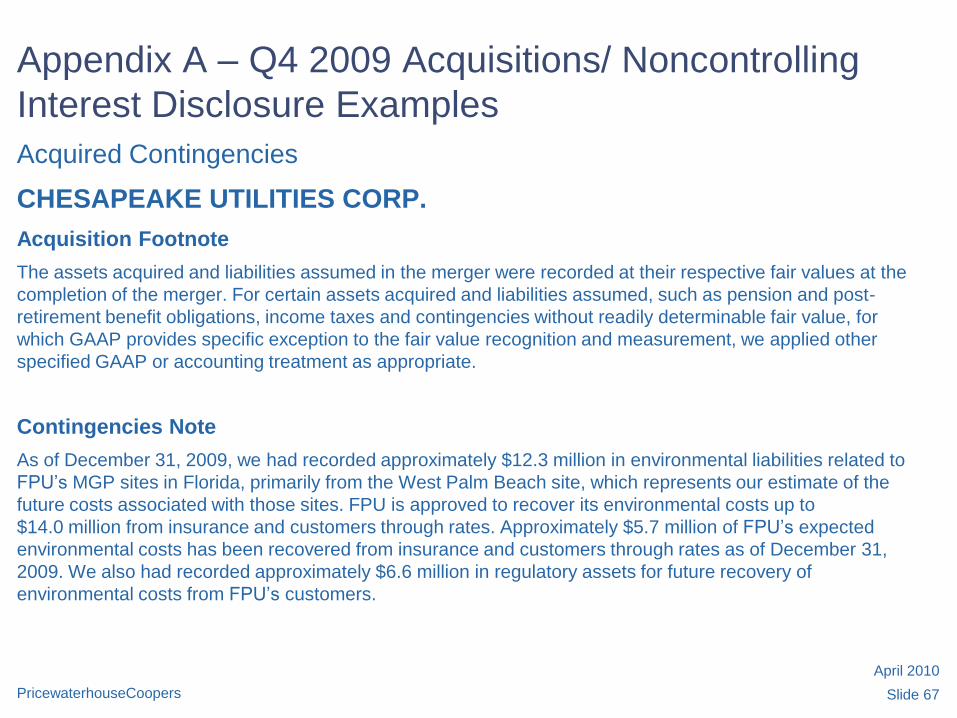

CHESAPEAKE UTILITIES CORP.

Acquisition Footnote

The assets acquired and liabilities assumed in the merger were recorded at their respective fair values at the

completion of the merger. For certain assets acquired and liabilities assumed, such as pension and post-

retirement benefit obligations, income taxes and contingencies without readily determinable fair value, for

which GAAP provides specific exception to the fair value recognition and measurement, we applied other

specified GAAP or accounting treatment as appropriate.

Contingencies Note

As of December 31, 2009, we had recorded approximately $12.3 million in environmental liabilities related to

FPU’s MGP sites in Florida, primarily from the West Palm Beach site, which represents our estimate of the

future costs associated with those sites. FPU is approved to recover its environmental costs up to

$14.0 million from insurance and customers through rates. Approximately $5.7 million of FPU’s expected

environmental costs has been recovered from insurance and customers through rates as of December 31,

2009. We also had recorded approximately $6.6 million in regulatory assets for future recovery of

environmental costs from FPU’s customers.

April 2010

Appendix A – Q4 2009 Acquisitions/ Noncontrolling

Interest Disclosure Examples

Slide 68PricewaterhouseCoopers

Acquired Contingencies

CHESAPEAKE UTILITIES CORP.

West Palm Beach, Florida

We are currently evaluating remedial options to respond to environmental impacts to soil and groundwater at

and in the immediate vicinity of a parcel of property owned by FPU in West Palm Beach, Florida upon which

FPU previously operated an MGP. Pursuant to a Consent Order between FPU and the FDEP, effective

April 8, 1991, FPU completed the delineation of soil and groundwater impacts at the site. On June 30, 2008,

FPU transmitted a revised feasibility study, evaluating appropriate remedies for the site, to the FDEP. On

April 30, 2009, FDEP issued a remedial action order, which it subsequently withdrew. In response to the order

and as a condition to its withdrawal, FPU committed to perform additional field work in 2009 and complete an

additional engineering evaluation of certain remedial alternatives. The scope of this work has increased in

response to FDEP’s demands for additional information.

The feasibility study evaluated a wide range of remedial alternatives based on criteria provided by applicable

laws and regulations. Based on the likely acceptability of proven remedial technologies described in the

feasibility study and implemented at similar sites, management believes that consulting/remediation costs to

address the impacts now characterized at the West Palm Beach site will range from $7.4 million to

$18.9 million.

April 2010

Appendix A – Q4 2009 Acquisitions/ Noncontrolling

Interest Disclosure Examples

Slide 69PricewaterhouseCoopers

Acquired Contingencies

CHESAPEAKE UTILITIES CORP.

West Palm Beach, Florida

This range of costs covers such remedies as in situ solidification for deeper soil impacts, excavation of

superficial soil impacts, installation of a barrier wall with a permeable biotreatment zone, monitored natural

attenuation of dissolved impacts in groundwater, or some combination of these remedies.

Negotiations between FPU and the FDEP on a final remedy for the site continue. Prior to the conclusion of

those negotiations, we are unable to determine, to a reasonable degree of certainty, the full extent or cost of

remedial action that may be required. As of December 31, 2009, and subject to the limitations described

above, we estimate the remediation expenses, including attorneys’ fees and costs, will range from

approximately $7.8 million to $19.4 million for this site.

April 2010

Appendix A – Q4 2009 Acquisitions/ Noncontrolling

Interest Disclosure Examples

Slide 70PricewaterhouseCoopers

Acquired Contingencies (included in purchase price allocation)

CHESAPEAKE UTILITIES CORP.

Acquisition Footnote

(in thousands)

October 28,

2009

Purchase price $ 75,699

Current assets 26,761

Property, plant and equipment 141,907

Regulatory assets 17,918

Investments and other deferred charges 3,659

Intangible assets 4,019

Total assets acquired 194,264

Long term debt 47,812

Borrowings from line of credit 4,249

Other current liabilities 17,504

Other regulatory liabilities 19,414

Pension and post retirement obligations 14,276

Environmental liabilities 12,414

Deferred income taxes 20,850

Customer deposits and other liabilities 15,467

Total liabilities assumed 151,986

Net identifiable assets acquired 42,278

Goodwill $ 33,421

April 2010

Appendix A – Q4 2009 Acquisitions/ Noncontrolling

Interest Disclosure Examples

Slide 71PricewaterhouseCoopers

Intangible Assets

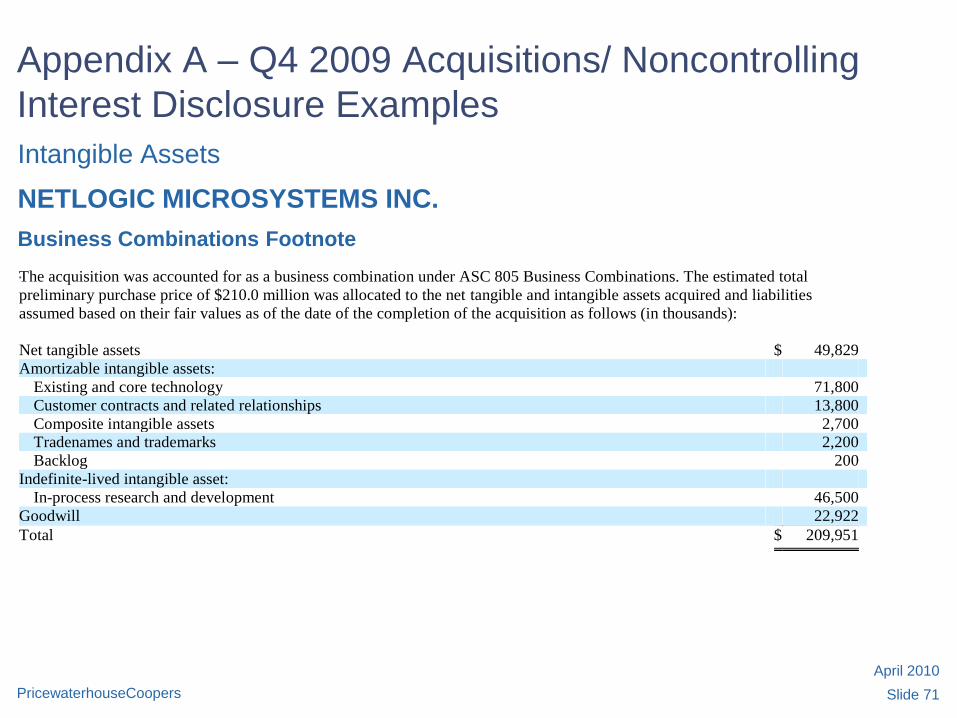

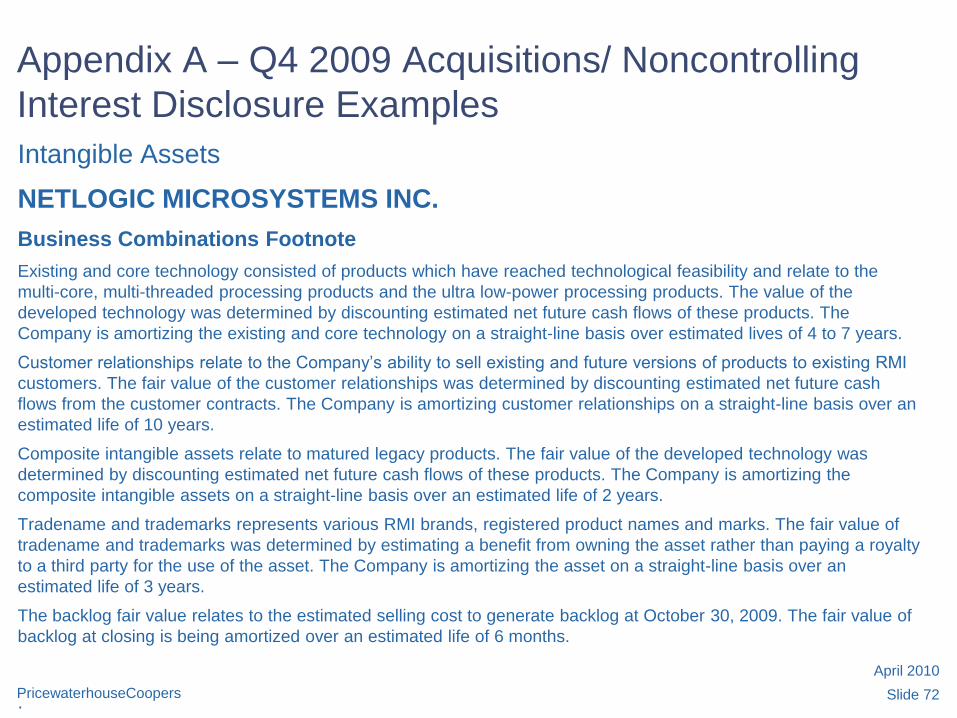

NETLOGIC MICROSYSTEMS INC.

Business Combinations Footnote

.The acquisition was accounted for as a business combination under ASC 805 Business Combinations. The estimated total

preliminary purchase price of $210.0 million was allocated to the net tangible and intangible assets acquired and liabilities

assumed based on their fair values as of the date of the completion of the acquisition as follows (in thousands):

Net tangible assets $ 49,829

Amortizable intangible assets:

Existing and core technology 71,800

Customer contracts and related relationships 13,800

Composite intangible assets 2,700

Tradenames and trademarks 2,200

Backlog 200

Indefinite-lived intangible asset: