Q2 2011 MOTOROLASOLUTIONS MARKET BAROMETER 2011 HOSPITALITY · How are enterprises and government...

37

PAGE 1 MOTOROLA SOLUTIONS MARKET BAROMETER 2011 HOSPITALITY Q2 2011 BUSINESS AND MARKET INTELLIGENCE MOTOROLA SOLUTIONS

Transcript of Q2 2011 MOTOROLASOLUTIONS MARKET BAROMETER 2011 HOSPITALITY · How are enterprises and government...

PAGE 1

MOTOROLA SOLUTIONSMARKET BAROMETER 2011 HOSPITALITY

Q2 2011

BUSINESS AND MARKET INTELLIGENCEMOTOROLA SOLUTIONS

PAGE 2

MOTOROLA SOLUTIONS MARKET BAROMETER 2011 – HOSPITALITY

MARKET BAROMETER 2011HOSPITALITY

INTRODUCTION

OBJECTIVES AND METHODOLOGY

FIRMOGRAPHICS AND RESPONDENT PROFILE

KEY FINDINGS

IMPORTANCE OF MOBILITY AND INVESTMENT DRIVERS

DEPLOYMENTS

WLAN STRATEGY

BUDGETS AND MOBILE INVESTMENTS

CONCLUSIONS

PAGE 3

MOTOROLA SOLUTIONS MARKET BAROMETER 2011 – HOSPITALITY

The Motorola Solutions Barometer is a market trends study conducted to better understand the changing environment and business strategies concerning mobility in enterprise and government industries.

What are the strategic mobility issues concerning mobility decision-makers? How are enterprises and government segments utilizing mobility and what are the benefits?What are the future mobile technology investment expectations?Which vertical industries and regions are leading in the adoption of mobility solutions?Which applications are most deployed and which are poised for greater adoption?

INTRODUCTION

PAGE 4

MOTOROLA SOLUTIONS MARKET BAROMETER 2011 – HOSPITALITY

MARKET BAROMETER 2011 HOSPITALITY

INTRODUCTION

OBJECTIVES AND METHODOLOGY

FIRMOGRAPHICS AND RESPONDENT PROFILE

KEY FINDINGS

IMPORTANCE OF MOBILITY AND INVESTMENT DRIVERS

DEPLOYMENTS

WLAN STRATEGY

BUDGETS AND MOBILE INVESTMENTS

CONCLUSIONS

PAGE 5

MOTOROLA SOLUTIONS MARKET BAROMETER 2011 – HOSPITALITY

OBJECTIVES AND METHODOLOGYObjectives: Motorola Solutions regularly conducts independent market research to better

understand emerging trends in Enterprise and Government mobility markets. The Motorola Solutions Barometer provides indicators of the opportunities and challenges that mobility poses to Hospitality enterprises by gathering direct feedback from the organizations that are investing and deploying these solutions.

Sampling and Methodology: The survey was conducted in Q4 2010. Respondents were screened for involvement in the decision to invest or purchase mobile and/or wireless technologies, including: wireless networks (WLAN, WiFi), cell phones, smartphones, laptops, netbooks, tablets, rugged laptops, rugged handheld computers, and two-way radio systems.

• Sample: Invitation to participate was sponsored by third party panel provider (ResearchNow). Motorola identity not disclosed. 161 respondents from Hospitality venues across North America and Western Europe completed the survey.

• Metrics: The 2011 Hospitality Barometer probed deployment status and future plans for mobile and wireless technologies in the enterprise. Key metrics included deployment status and planning, mobile employee deployments, WLAN deployment timeline, applications driving investments, and key benefits .

• Technologies: The research examined current and emerging technologies in the hospitality industry and their impact on customer satisfaction. Key technologies include mobile computing, radio, tablets, and WLAN.

PAGE 6

MOTOROLA SOLUTIONS MARKET BAROMETER 2011 – HOSPITALITY

MARKET BAROMETER 2011HOSPITALITY

INTRODUCTION

OBJECTIVES AND METHODOLOGY

FIRMOGRAPHICS AND RESPONDENT PROFILE

KEY FINDINGS

IMPORTANCE OF MOBILITY AND INVESTMENT DRIVERS

DEPLOYMENTS

WLAN STRATEGY

BUDGETS AND MOBILE INVESTMENTS

CONCLUSIONS

PAGE 7

MOTOROLA SOLUTIONS MARKET BAROMETER 2011 – HOSPITALITY

NUMBER OF EMPLOYEES AND REGION

United States 104 64.6%

Canada 6 3.7%

United Kingdom 15 9.3%

France 16 9.9%

Germany 20 12.4%

Total 161 100%

Number of Employees Total North

America Europe

N 161 110 51

250 to 499 5.0 % 4.5 % 5.9 %

500 to 999 13.0 % 12.7 % 13.7 %

1,000 to 1,999 13.0 % 10.0 % 19.6 %

2,000 to 4,999 11.2 % 10.9 % 11.8 %

5,000 to 9,999 16.1 % 16.4 % 15.7 %

10,000 to 49,999 13.7 % 13.6 % 13.7 %

50,000 to 99,999 11.8 % 14.5 % 5.9 %

Over 100,000 16.1 % 17.3 % 13.7 %

Approx. 70% of respondents represent mid- to large companies with at least 2,000 employees.

Q: “In what country is your organization headquartered?”

Q: “How many full-time employees are employed in your entire organization? Please include employees

at all stores, plants, branches, divisions, and subsidiaries worldwide.”

PAGE 8

MOTOROLA SOLUTIONS MARKET BAROMETER 2011 – HOSPITALITY

HOSPITALITY FOCUS

Total North America EuropeN 161 110 51

Hotel/Spa/Inn 39.1 % 35.5 % 47.1 %Amusement Parks/ Arcades/ Tourist Attraction 10.6 % 10.0 % 11.8 %

Casino 8.7 % 10.9 % 3.9 %Restaurant/Bar -- with Table Service 8.7 % 10.9 % 3.9 %

Restaurant -- Fast Food 8.1 % 10.9 % 2.0 %Sports Arena/Venue 4.3 % 4.5 % 3.9 %

Golf or Ski Resort 1.9 % 1.8 % 2.0 %Movie Theaters 1.9 % 1.8 % 2.0 %

Museums, Zoos and Botanical Gardens 1.9 % 1.8 % 2.0 %National/State/Government monument/park 1.9 % 0.9 % 3.9 %

Other 13.0 % 10.9 % 17.6 %

• The Barometer 2011 includes the responses of 161 decision makers in the Hospitality industry across North America and Western Europe.

• Decision makers who completed this survey represent hospitality enterprises with over four million workers combined.

Respondents represent a wide variety of hospitality enterprises including hotels, tourist attractions, casinos and restaurants.

PAGE 9

MOTOROLA SOLUTIONS MARKET BAROMETER 2011 – HOSPITALITY

TARGET CHARACTERISTICS

US $ equivalent Total N.A. Europe

N 161 110 51

$15M - 49.9 M 12.4 % 11.8 % 13.7 %

$50 - 99.9 M 11.8 % 10.0 % 15.7 %

$100 - 249.9 M 11.2 % 8.2 % 17.6 %

$250 - 499.9 M 12.4 % 10.9 % 15.7 %

$500 - 999.9 M 15.5 % 14.5 % 17.6 %

Over $1 Billion 36.6 % 44.5 % 19.6 %

Q: “Approximately what is your organization’s global annual revenue?”

More than one third of survey respondents represent companies exceeding $1 billion in revenues. Responses come from the executive suite , IT functions and management

closest to day-to-day implementation of mobile solutions.

Senior-most business leader 8.7%

Executive37.3%

Senior-most finance leader 6.2%

Executive in line of business 22.4%

Operations Manager 24.8%

Management43.4%Supply Chain Manager 4.3%

Manager in line of business 14.3%

Senior-most IT DM 4.3%IT

19.2%VP in IT 2.5%

Director in IT 4.3%Manager in IT 8.1%

Q: “Which of the following best describes your role in your organization?”

PAGE 10

MOTOROLA SOLUTIONS MARKET BAROMETER 2011 – HOSPITALITY

MARKET BAROMETER 2011HOSPITALITY

INTRODUCTION

OBJECTIVES AND METHODOLOGY

FIRMOGRAPHICS AND RESPONDENT PROFILE

KEY FINDINGS

IMPORTANCE OF MOBILITY AND INVESTMENT DRIVERS

DEPLOYMENTS

WLAN STRATEGY

BUDGETS AND MOBILE INVESTMENTS

CONCLUSIONS

PAGE 11

MOTOROLA SOLUTIONS MARKET BAROMETER 2011 – HOSPITALITY

KEY FINDINGS: HOSPITALITYHospitality enterprises recognize the increasing importance of mobile technologies (91%) and the competitive advantage for their business (78%). The majority (56%) are planning increased spending on mobile and wireless technologies in 2011 to better equip their workforces.

Elevating the guest experience• Improved guest experience is the top driver for mobility investments, cited by 76 percent of hospitality venues surveyed. • Hospitality decision makers are investing in mobile products to support customer-facing applications that handle wireless

email, guest/attendee check-in, table-side order/payment, event ticketing, among others – all to improve guest services. • 61 percent of respondents plan to deploy some form of video capabilities, including video surveillance, video conferencing

and streaming video in public access areas such as lobbies.• Of hospitality organizations surveyed, 58 percent deploying mobile technology today are seeing improved customer

satisfaction.

Empowering the mobile worker• 59 percent of respondents currently deploying mobile and wireless technology saw an increase in employee productivity and

efficiency, while 55 percent have seen improved sales results.• Managers, security and customer service associates are the primary users of mobile and wireless devices in the hospitality

companies surveyed – 71 percent of supervisors use smartphones, 52 percent of security use radios, 19 percent of ticketing agents are equipped with VoIP, while 26 percent of property managers have tablets.

• The most popular current applications on two-way radios are project management (51 percent) and collaboration (41 percent). Unified messaging and remote management/monitoring have the highest rate of planned deployments into 2012.

• Among survey respondents, tablets and VoIP handsets are the top two mobile devices planned for new deployments by 2012.

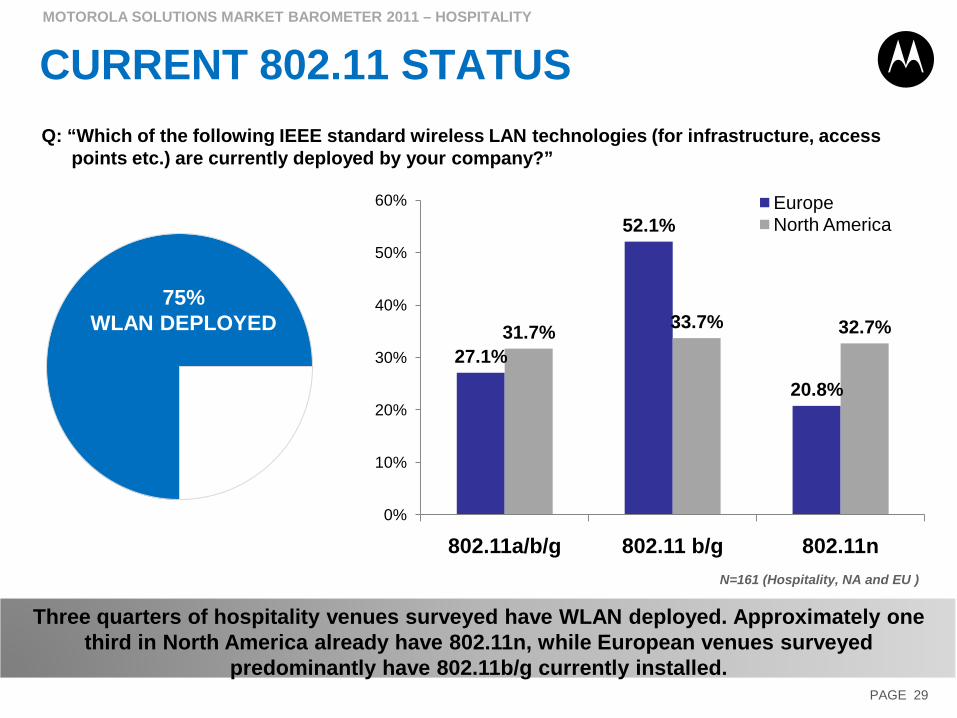

Enabling operational efficiency• 75 percent of hospitality organizations surveyed already have wireless LAN (WLAN) installed in their facilities. In North

America, approximately one third of these venues have 802.11n, while European venues predominately have 802.11b/g. • 42 percent of respondents with existing WLAN expect to be fully upgraded to 802.11n by the end of 2012. • Improving throughput and reliability, and extending range of current wireless data networks are the top three drivers behind

802.11n WLAN adoption – all critical network features to meet greater data volumes and increasing demands for access from the customer and mobile workforce.

PAGE 12

MOTOROLA SOLUTIONS MARKET BAROMETER 2011 – HOSPITALITY

MARKET BAROMETER 2011HOSPITALITY

INTRODUCTION

OBJECTIVES AND METHODOLOGY

FIRMOGRAPHICS AND RESPONDENT PROFILE

KEY FINDINGS

IMPORTANCE OF MOBILITY AND INVESTMENT DRIVERS

DEPLOYMENTS

WLAN STRATEGY

BUDGETS AND MOBILE INVESTMENTS

CONCLUSIONS

PAGE 13

MOTOROLA SOLUTIONS MARKET BAROMETER 2011 – HOSPITALITY

90.6%

AGREE NO OPINION DISAGREE

78.2%

“My organization has a competitive advantage by using mobile and wireless technologies.”

“Mobile and wireless technologies are more important to my organization today than they were last year.”

Hospitality decision-makers overwhelmingly recognize the increasing importance of mobile technologies (91%) and the competitive advantage for their business (78%); the majority

(56%) are planning increased spending on mobile and wireless technologies in 2011.

RISING IMPORTANCE OF MOBILITY“What is your organization’s plan for investing in mobile and wireless technologies in 2011?”

56.3%

34.5%

INCREASE BUDGET SAME AS 2010NOT SURE DECREASE

N=161 (Hospitality, NA and EU )

PAGE 14

MOTOROLA SOLUTIONS MARKET BAROMETER 2011 – HOSPITALITY

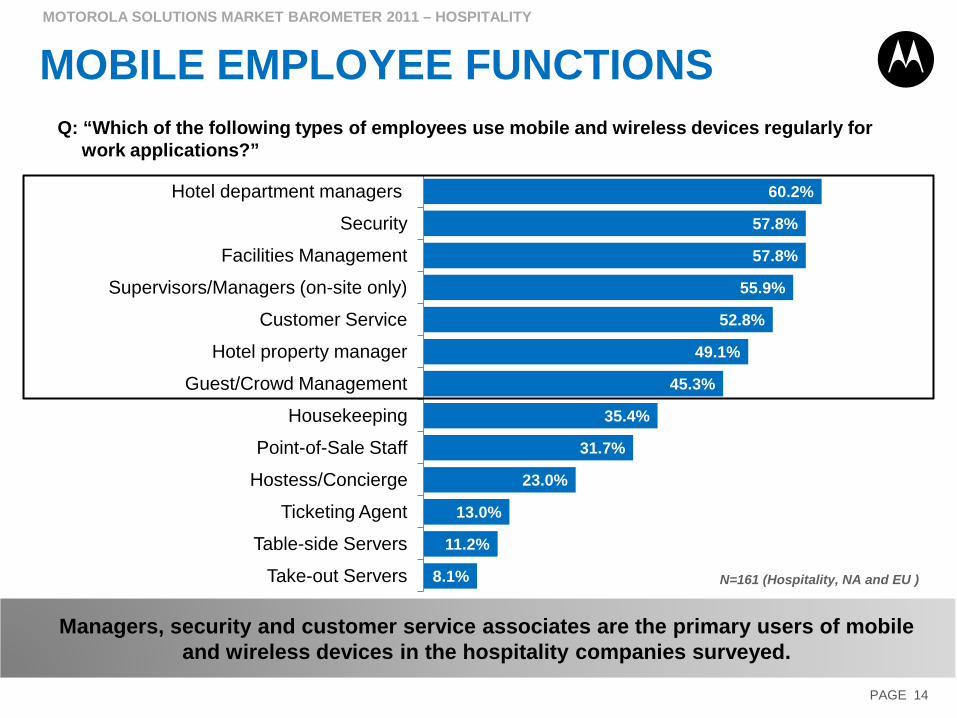

8.1%

11.2%

13.0%

23.0%

31.7%

35.4%

45.3%

49.1%

52.8%

55.9%

57.8%

57.8%

60.2%

Take-out Servers

Table-side Servers

Ticketing Agent

Hostess/Concierge

Point-of-Sale Staff

Housekeeping

Guest/Crowd Management

Hotel property manager

Customer Service

Supervisors/Managers (on-site only)

Facilities Management

Security

Hotel department managers

MOBILE EMPLOYEE FUNCTIONS

Managers, security and customer service associates are the primary users of mobile and wireless devices in the hospitality companies surveyed.

Q: “Which of the following types of employees use mobile and wireless devices regularly for work applications?”

N=161 (Hospitality, NA and EU )

PAGE 15

MOTOROLA SOLUTIONS MARKET BAROMETER 2011 – HOSPITALITY

DEVICES FOR DIFFERENT WORKERS

Smartphone Two-way Radio Portable VoIP Mobile Handset TabletSupervisors/Mgrs (on-

site and travel) 70.7% Security 51.6% Ticketing Agent 19.0% Hotel property manager 25.6%

Supervisors/Managers mobile on-site 59.1% Guest/Crowd

Management 47.2% Table-side Servers 16.7% Table-side Servers 22.2%

Hotel property manager 57.7% Housekeeping 46.4% Take-out Servers 15.4% Point-of-Sale Staff 22.0%Hotel department

managers 53.6% Facilities Management 42.9% Facilities Management 14.3% Supervisors/Mgrs (on-site and travel) 18.5%

Facilities Management 50.5% Hotel department managers 37.1% Hostess, Concierge, 13.5% Hotel department

managers 16.5%

Hostess, Concierge, 45.9% Customer Service 34.9% Customer Service 13.3% Guest/Crowd Management 15.3%

Customer Service 39.8% Hostess, Concierge, 29.7% Hotel property manager 12.8% Housekeeping 12.5%

Security 36.3% Supervisors/Managers mobile on-site 29.5% Supervisors/Mgrs (on-

site and travel) 10.9% Customer Service 12.0%

Point-of-Sale Staff 36.0% Hotel property manager 24.4% Housekeeping 10.7% Supervisors/Managers mobile on-site 11.4%

Guest/Crowd Management 33.3% Point-of-Sale Staff 24.0% Hotel department

managers 10.3% Facilities Management 11.0%

The highest levels of device deployments reflect mobile workers with different needs in different situations. 71% of supervisors use smartphones; 52% of security use radios; 19%

of ticketing agents are equipped with VoIP; and 26% of property managers have tablets.

% of enterprises deploying the device with each type of worker

xxx xxx

PAGE 16

MOTOROLA SOLUTIONS MARKET BAROMETER 2011 – HOSPITALITY

TOP MOBILITY INVESTMENT DRIVERS

Field-based and customer-facing applications are the top drivers behind investments in mobility products, besides the essential email and contacts apps.

Q: “Which mobile applications are the primary drivers behind your organization's investments in mobile products?”

59.0%

64.6%

65.2%

67.1%

67.1%

68.3%

71.4%

72.0%

72.7%

75.2%

76.4%

Logistics applications

Asset tracking/management

Inventory Management

Asset Maintenance

Industry-specific LOB applications

Security

Personalized contacts and calendar

Field Sales - Sales force applications

Wireless email

Field service applications

Customer-facing applications

N=161 (Hospitality, NA and EU )

PAGE 17

MOTOROLA SOLUTIONS MARKET BAROMETER 2011 - HOSPITALITY

DEVICE DEPLOYMENT DRIVERS

N=148 N=106 N=83 N=61 N=42

Smartphone Tablet Computer Rugged Laptop or Notebook

Rugged Handheld Computer

Rugged WearableComputer

Wireless email 43% Customer-facing applications 33% Line-of-business

applications 19% Inventory Management 25% (Mobile) CRM 21%

Contacts and calendar 31% Field Sales - SFA 25% Facilities

Management 17% Facilities Management 23% Guest/Attendee

Check-In 21%

Field Sales - SFA 27% (Mobile) CRM 22% Guest/Attendee Check-In 16% (Mobile) CRM 23% Labor

management 21%

(Mobile) CRM 27% Line-of-Business apps 21% Table- side Order/

Payment 16% Table- Side Order/ Payment 20% Contacts and

calendar 19%

Field service applications 26% Mobile Point of

Sale (POS) 21% Inventory Management 16% Logistics

applications 20% Security 19%

Customer-facing applications 21% Wireless email 20% Line Busting 16% Line-of-business

applications 18% Voice over WLAN 19%

Line-of-business applications 21% Table-Side Order/

Payment 20% Field service applications 14% Field Sales - SFA 18% Line Busting 19%

Guest/Attendee Check-In 20% Line Busting 19% Food traceability 14% Event Ticketing 18%

Security 18% Contacts and calendar 17% Logistics

applications 14% Line Busting 16%

Which applications are the primary reasons (drivers) for deploying each device?

Deployment of each form factor is driven by specific combinations of applications for which it is best suited.

Includes NA and EU

PAGE 18

MOTOROLA SOLUTIONS MARKET BAROMETER 2011 – HOSPITALITY

BENEFITS

18.6%

24.2%

26.1%

26.7%

31.1%

34.2%

50.3%

54.7%

58.4%

59.0%

Better ergonomics, reduced injuries

Improve greener operations

Lower labor costs via automated processes

Increase customer loyalty

Improve order fulfillment accuracy

Decrease employee/manual errors

Improve guest experience, quality or consistency

Improved business revenues/sales results

Customer satisfaction

Increase employee productivity/efficiency

Q: “Which of the following are the most important benefits realized by your organization due to the utilization of mobile and wireless computing and/or communication products?

Top three benefits from mobile technologies are increased productivity, customer satisfaction and improved revenues.

N=161 (Hospitality, NA and EU )

PAGE 19

MOTOROLA SOLUTIONS MARKET BAROMETER 2011 – HOSPITALITY

MARKET BAROMETER 2011HOSPITALITY

INTRODUCTION

OBJECTIVES AND METHODOLOGY

FIRMOGRAPHICS AND RESPONDENT PROFILE

KEY FINDINGS

IMPORTANCE OF MOBILITY AND INVESTMENT DRIVERS

DEPLOYMENTS

WLAN STRATEGY

BUDGETS AND MOBILE INVESTMENTS

CONCLUSIONS

PAGE 20

MOTOROLA SOLUTIONS MARKET BAROMETER 2011 – HOSPITALITY

DEVICE DEPLOYMENT STATUS

0% 20% 40% 60% 80% 100%

Rugged Wearable Computer

Rugged Tablet Computer

Vehicle-mounted Computer

Two-way radio – vehicle-mounted

Rugged Handheld Computer

Rugged Laptop or Notebook

Netbook

Portable Handset for VoIP or VoWLAN

Tablet Computer

Two-way radio – hand-held

Cell Phone

Smartphone

Laptop/Notebook

Currently Deployed/no Plans Currently Deployed & Plan upgrade/expand New Deployment by 2012

Tablets and VoIP Handsets are the top two technologies planned for new deployments by 2012. Laptops, smartphones and cellphones continue to be supported as indicated by high

rates of planned upgrades (60 -70%).

Q: “Which of the following mobile and wireless products are currently deployed by your organization for mobile employees and which do you plan to add to your deployments by 2012?”

Total Currently deployed

PlanningNew by

2012

90.7% 8.1%78.3% 13.7%80.1% 9.3%52.2% 14.3%42.2% 23.6%34.2% 29.8%42.2% 16.1%32.3% 19.3%19.3% 18.6%19.3% 14.9%15.5% 18.0%11.8% 18.0%9.9% 16.1%

PAGE 21

MOTOROLA SOLUTIONS MARKET BAROMETER 2011 – HOSPITALITY

EMERGING APPLICATION TRENDS

Currently Using or Deployed

Planning to Deploy by 2012

Applications that require a persistent internet connection. Browser-based Applications* 44.1% 22.4%

SaaS is a cloud deployment of shared and standardized business applications based on a multitenant architecture. Software-as-a-Service (SaaS)* 32.9% 14.9%

Defined as pay-per-use hosting of virtual servers from service providers such as Amazon Web Services, Savvis,

or Rackspace/Mosso or other local service providers..

Cloud Computing or Infrastructure-as-a-service

(IaaS)18.0% 24.8%

conferencing/telepresence, video systems for collaboration. Video capabilities 37.9% 23.0%

Communications technology [voice, video, and data] that is integrated with desktop applications such as presence,

conferencing, and unified messages through an integrated software platform.

Unified communications 27.3% 23.6%

Include RFID, sensors, GPS technologies, and smart cards that collect and transfer data on the condition of

physical assets or people.

Machine-to-Machine (M2M) technologies 21.7% 22.4%

Q: “What is your organization’s level of deployment in the following technologies?”

One third of Hospitality respondents reported already using SaaS applications and 44% indicated they are browser-based applications.* 61% will have some form of video

capabilities deployed by 2012.

N=161 (Hospitality, NA and EU )*These technologies and terminology are rapidly converging.

PAGE 22

MOTOROLA SOLUTIONS MARKET BAROMETER 2011 – HOSPITALITY

VIDEO APPLICATIONS

Q: “What is your organization’s level of deployment in the following technologies?”

10.6%

13.7%

13.7%

15.5%

14.3%

22.4%

21.1%

24.8%

5.0%

7.5%

8.7%

7.5%

9.3%

3.1%

5.6%

3.7%

Immersive videoconferencing (e.g., room-based telepresence)

High definition (HD) in-room videoconferencing

Enterprise IP/digital video for company use (e.g., video training, demos)

Desktop IP videoconferencing

IP video service/streaming for clients/customers (e.g., video feed in a lobby)

Cable or satellite TV service for clients/customers (in room)

Traditional in-room videoconferencing

Video surveillance

Currrent Planned by 2012

Video surveillance, traditional video-conferencing and in-room cable are the top current video deployments. HD and IP video technologies are expected to expand significantly by

2012 reaching levels close to cable/satellite services.

N= 98 (Hospitality, NA and EU)

PAGE 23

MOTOROLA SOLUTIONS MARKET BAROMETER 2011 – HOSPITALITY

APPLICATIONS SOURCING

Current Future Change

Homegrown and/or developed in-house 48.4% 21.7% -26.7%

Custom applications developed by an external developer 38.5% 36.6% -1.9%

Purchase mobile applications off the shelf 47.8% 40.4% -7.5%

Other (please specify) 5.0% 6.8% 1.9%

Don t know 21.7% 34.2% 12.4%

Q: “What is your organization’s primary strategy for acquiring or developing applications for mobile products currently? What is the planned strategy into 2012?”

Preferences for acquiring mobile applications are in flux, reflected by a high number of respondents (34%) who can’t say what the strategy for their organization will be in 2012.

Significantly fewer expect to develop applications in-house.

N=161 (Hospitality, NA and EU )

PAGE 24

MOTOROLA SOLUTIONS MARKET BAROMETER 2011 – HOSPITALITY

APPLICATION DEVELOPMENTQ: “What resources do you work with to develop custom mobile applications or to

customize existing applications?

2.5%

12.4%

13.7%

14.3%

16.8%

19.9%

25.5%

Don t know

By an external developer (off-shore)

Work with Web site design firm

Develop mobile applications on a purchased mobile middleware platform (e.g., Sybase I Anywhere, Antenna …

Work with system integrator to develop (local, regional or national)

Use a mobile extension of an existing packaged application from the vendor (e.g., Siebel, SAP salesforce.com)

By an external developer (local, regional or national)

N=62

When developing custom mobile apps, one quarter of respondents works with an external developer that is local, regional or national, compared to 12% who use off-shore developers.

PAGE 25

MOTOROLA SOLUTIONS MARKET BAROMETER 2011 – HOSPITALITY

TYPES OF TWO-WAY RADIO IN USE

Two-way radio handheld

Direct Radio-to-Radio(s) Communication 80.2%

Company-owned and operated system with repeaters and radios 47.2%

Service Provider's repeater/antennae system (Paid

Subscription)26.4%

Licensed (e.g., LMR/PMR) 41.5%

Un-licensed (e.g., FRS) 20.8%

Both. Some unlicensed / some licensed radios.

18.9%

Don’t Know 18.9%

Q: “Which of the following best describes your current two-way radio deployments?

Use of FRS Radio in the Enterprise Use of Repeaters/Radio Antennae Systems

Use of FRS radio in hospitality is prevalent (21% - solely FRS, 19% - in addition to LMR). Nearly one half (47%) of hospitality enterprises operate their own system for at least some

part of their deployments while 26% use a service provider.

PAGE 26

MOTOROLA SOLUTIONS MARKET BAROMETER 2011 – HOSPITALITY

TWO-WAY RADIO DEPLOYMENT PLANS

currently own and operate (no upgrades planned)

30.2%

currently own and operate / plan expansion or

upgrade 23.7%

New deployment by 2012

8.5%

No plans to deploy

Radio/repeater system23.4%

Don't know8.5%

Q: “What are your company’s plans for installing or expanding two-way radio deployments that include a radio repeater and antenna system?”

N=106 (have or plan radio products)

(No radios/ 34% of total)

% among those with current or planned two-way radios any type

Among manufacturers who have or plan to deploy two-way radios, about one quarter (24%) own and operate the radio/repeater system and plan to upgrade by 2012; 30% own and

operate with no plans to upgrade.

PAGE 27

MOTOROLA SOLUTIONS MARKET BAROMETER 2011 – HOSPITALITY

TWO-WAY RADIO: DESIRED APPSQ: “Which of the following applications do you currently have deployed on two-way radios and

which do you plan to deploy by the end of 2012?”

23.4%26.9%

30.5%32.6%33.3%33.7%34.0%34.8%35.1%36.2%

40.6%50.5%

25.5%25.8%21.1%

22.1%15.6%17.3%18.6%17.4%16.5%

21.3%12.5%

5.2%

Remote mgmt/monitoringUnified messaging/voice mail

Knowledge mgmtMulti-media messaging service (MMS)

Calendar/schedulingConferencing

Text messagingPush email

Instant messagingShort messaging service (SMS)

CollaborationProject management

Current Planned by 2012

N=95

(Among respondents with current or planned 2-way radio deployments)

The most popular current applications on two-way radios are project management (51%) and collaboration (41%). Unified messaging and remote management/monitoring have the

highest rate of planned deployments into 2012.

PAGE 28

MOTOROLA SOLUTIONS MARKET BAROMETER 2011 – HOSPITALITY

MARKET BAROMETER 2011HOSPITALITY

INTRODUCTION

OBJECTIVES AND METHODOLOGY

FIRMOGRAPHICS AND RESPONDENT PROFILE

KEY FINDINGS

IMPORTANCE OF MOBILITY AND INVESTMENT DRIVERS

DEPLOYMENTS

WLAN STRATEGY

BUDGETS AND MOBILE INVESTMENTS

CONCLUSIONS

PAGE 29

MOTOROLA SOLUTIONS MARKET BAROMETER 2011 – HOSPITALITY

27.1%

52.1%

20.8%

31.7% 33.7% 32.7%

0%

10%

20%

30%

40%

50%

60%

802.11a/b/g 802.11 b/g 802.11n

EuropeNorth America

CURRENT 802.11 STATUSQ: “Which of the following IEEE standard wireless LAN technologies (for infrastructure, access

points etc.) are currently deployed by your company?”

Three quarters of hospitality venues surveyed have WLAN deployed. Approximately one third in North America already have 802.11n, while European venues surveyed

predominantly have 802.11b/g currently installed.

N=161 (Hospitality, NA and EU )

75%WLAN DEPLOYED

PAGE 30

MOTOROLA SOLUTIONS MARKET BAROMETER 2011 – HOSPITALITY

802.11 N SCHEDULE

28.4%32.6%

14.7%

2.1%

22.1%

13.7%

28.4%

18.9% 17.9%21.1%

0%

10%

20%

30%

40%

50%

Within 12 months By the end of 2012 In 2013 - 2014 2015 or later Not planned / Not applicable

Partial 802.11n

Complete 802.11n

Q: “On what schedule does your company expect to replace its 802.11 a/b/g or 802.11 b/g WLAN deployments with 802.11n?”

% of those who currently have a/b/g or b/g

42% of the currently deployed WLAN base expects to be fully upgraded to 802.11n by the end of 2012.

42.1%

N=95

PAGE 31

MOTOROLA SOLUTIONS MARKET BAROMETER 2011 – HOSPITALITY

WLAN DRIVERS

16.7%

28.2%

32.1%

43.6%

46.2%

56.4%

Adding support for video traffic to our wireless network

Replacing wired primary access with wireless primary access

Adding support for voice traffic to wireless network

Increasing the range of the current wireless network

Improving the reliability of current wireless networks

Increase throughput for current wireless data networks

Q: “What does your organization consider the primary driver(s) for adopting 802.11n? (% among those with current or planned WLAN deployment)

N=78

Improving throughput and reliability, and extending range are the top three drivers behind 802.11n adoption: all are critical network features to meet greater data volumes and

increasing demands for access from the customer and the mobile workforce.

PAGE 32

MOTOROLA SOLUTIONS MARKET BAROMETER 2011 – HOSPITALITY

MARKET BAROMETER 2011HOSPITALITY

INTRODUCTION

OBJECTIVES AND METHODOLOGY

FIRMOGRAPHICS AND RESPONDENT PROFILE

KEY FINDINGS

IMPORTANCE OF MOBILITY AND INVESTMENT DRIVERS

DEPLOYMENTS

WLAN STRATEGY

BUDGETS AND MOBILE INVESTMENTS

CONCLUSIONS

PAGE 33

MOTOROLA SOLUTIONS MARKET BAROMETER 2011 – HOSPITALITY

IT-TELECOM BUDGET

IT-Telecom Budget 2010

IT-Telecom Budget 2011 Change

<$250,000 19.5% 14.9% -4.6%$250,000 - $499,999 11.5% 10.3% -1.1%$500,000 - $999,999 10.3% 9.2% -1.1%$1 mill - $4.9 million 8.0% 12.6% 4.6%$5 mill - $9.9 million 10.3% 5.7% -4.6%

$10 mill - $49.9 million 9.2% 11.5% 2.3%$50 mill - $99.9 million 5.7% 6.9% 1.1%

$100 mill- $499.9 million 10.3% 9.2% -1.1%$500 million + 8.0% 11.5% 3.4%

Total 100.0% 100.0% 0.0%

Q: “What is your organization’s current total annual IT and telecom budget for 2010? and what is the budget planned for 2011?”

IT spending is increasing by approximately 20% overall in 2011 according to the planned spend among hospitality decision-makers surveyed.

N=161 (Hospitality, NA and EU )

2011 Retail IT Spend

2010 Retail IT Spend

+20%

IT Budgets / YoY comparative scale

PAGE 34

MOTOROLA SOLUTIONS MARKET BAROMETER 2011 – HOSPITALITY

5.2%

13.8%

37.9%

32.8%

5.2% 5.2%

10.3%

20.7%24.1%

37.9%

0.0%

6.9%

Increase > 25% Increase 10 to 25%

Increase 5 to 10%

About the same as 2010

Decrease 5 to10%

Don’t Know

North AmericaEurope

MOBILE INVESTMENTS 2011

Q: “What is your organization’s plan for investing in mobile and wireless technologies in 2011?”

56% of hospitality decision makers planned for increases in mobile investments in 2011. Greater average increase is expected in Europe than in North America.

N=161 (Hospitality, NA and EU )

56% overall report increases for 2011

PAGE 35

MOTOROLA SOLUTIONS MARKET BAROMETER 2011 – HOSPITALITY

MARKET BAROMETER 2011HOSPITALITY

INTRODUCTION

OBJECTIVES AND METHODOLOGY

FIRMOGRAPHICS AND RESPONDENT PROFILE

KEY FINDINGS

IMPORTANCE OF MOBILITY AND INVESTMENT DRIVERS

DEPLOYMENTS

WLAN STRATEGY

BUDGETS AND MOBILE INVESTMENTS

CONCLUSIONS

PAGE 36

MOTOROLA SOLUTIONS MARKET BAROMETER 2011 – HOSPITALITY

CONCLUSIONS• Mobility technologies are a

recognizable differentiator for hospitality venues seeking a competitive advantage for their business through increased customer satisfaction.

• Hospitality decision makers realize the increasing importance of mobile and wireless technology to their businesses and have increased their investments in 2011.

• The majority of hospitality venues have deployed wireless LAN technology and are making plans for expansion and upgrades to handle greater data volumes and increasing demands for high-speed access from the customer and mobile workforce.

Insert images

PAGE 37

THANK YOU