PWC Simularities&diffences full IFRS IFRSforSMEs · Temporary Temporary differences are differences...

3

Œ ˛˝ ”–fi ˝› «·· ˛˝ «fifi»²‹ ‹¿¤»› »”»fifi»… ‹¿¤»›

Transcript of PWC Simularities&diffences full IFRS IFRSforSMEs · Temporary Temporary differences are differences...

êð

×ÚÎ

꼱

®Í

ÓÛ

Ú

«´´

×ÚÎ

Í

Ý«

®®»²

¬¬¿

¨»

Ü»º»

®®»¼

¬¿¨»

êï

×ÚÎÍ º±® ÍÓÛ Ú«´´ ×ÚÎÍ

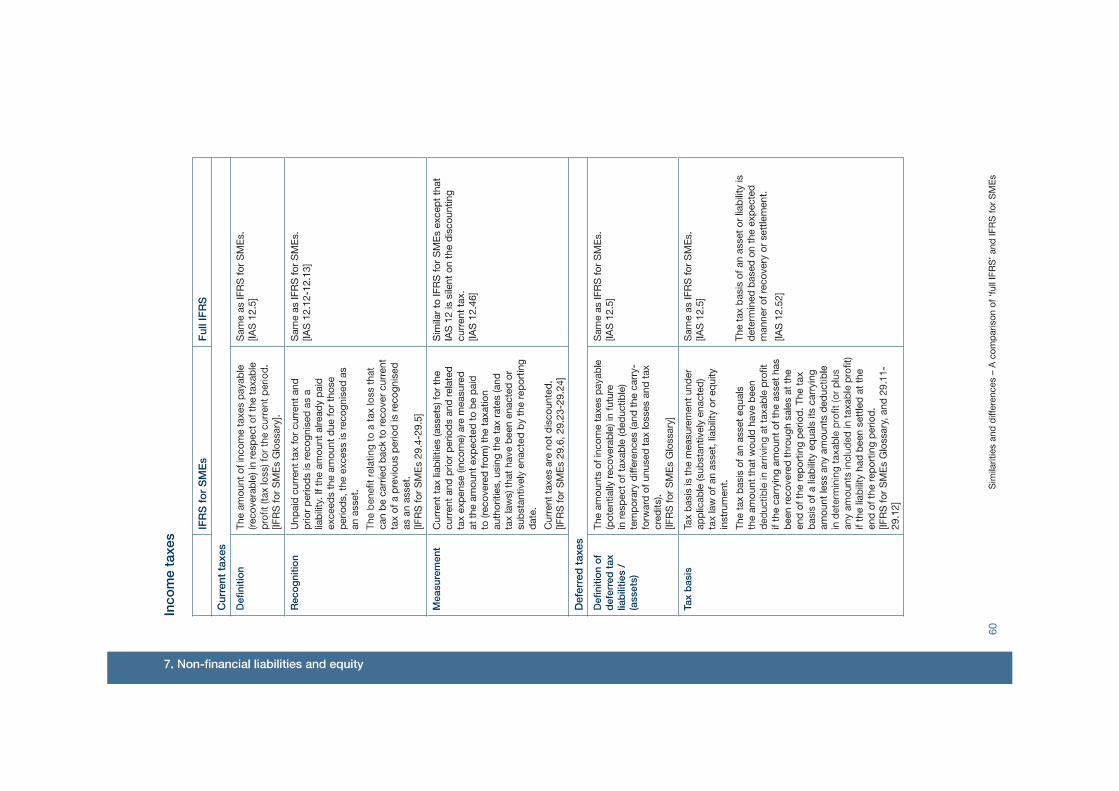

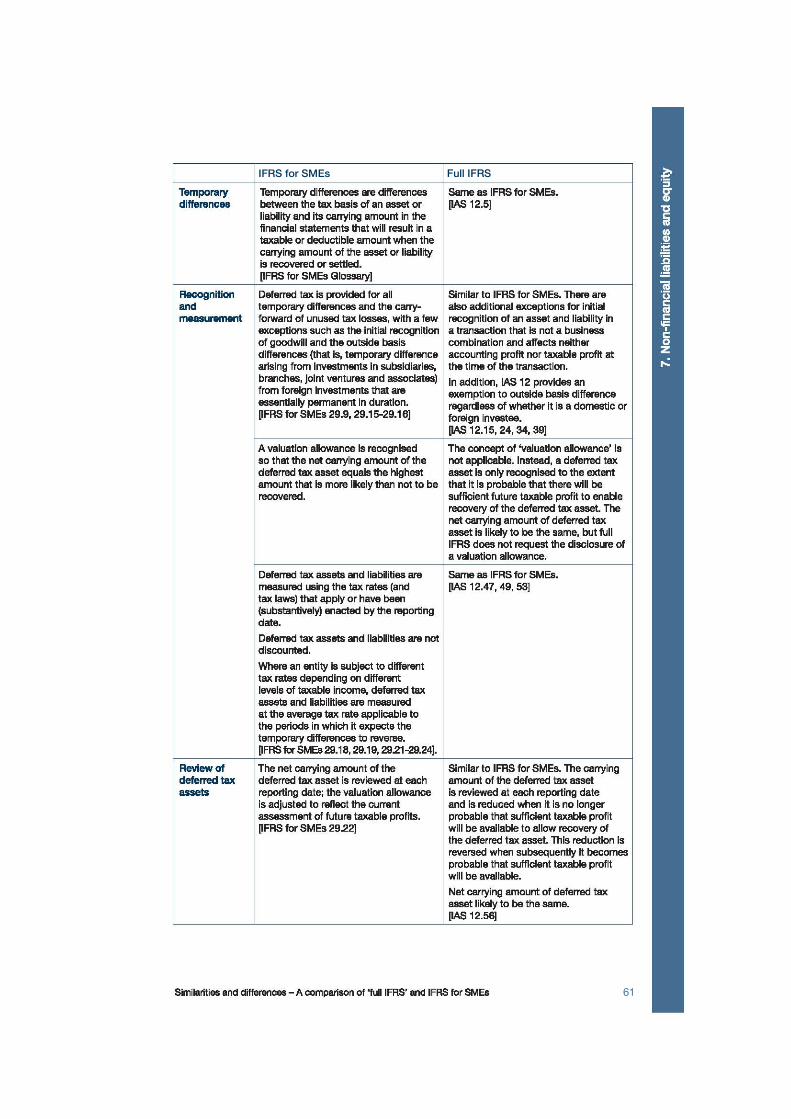

Temporary Temporary differences are differences Same as IFRS for SMEs. differences between the tax basis of an asset or [lAS 12.5]

liability and its carrying amount in the tinancial statements that will result in a taxabie or deductibie amount when the canying amount of the asset or liability is recovered or settled. [IFRS lor SMEs Glossary]

Recognition Deterred tax is provided tor all Similar to IFRS for SMEs. There are and temporary differences and the carry- also additional exceptions for initial measurement forward of unused tax losses, with a tew recognition of an asset and liability in

exceptions such as the initial recognition a transaction that is not a business of goodwill and the outside basis combination and affects neither differences (that is, temporary difference accounting profit nor taxabie profit at arising from investments in subsidiaries, the time of the transaction. branches, joint ventures and associates) In addition, lAS 12 provides an from foreign investments that are exemption to outside basis difterence essentially pennanent in duration. regardiess of whether it is a domestic or pFRS lor SMEs 29.9, 29.15-29.16] foreign investee.

[lAS 12.15, 24, 34, 39]

A valuation allowance is recognised The concept of 'valuation allowance' is so that the net canying amount of the not applicabie. Insteac:l, a deferred tax deferred tax asset equals the highest asset is only recognised to the extent amount that is more likely than not to be that it is probable that there will be recovered. sufficient future taxabie profit to enable

recovery of the deferred tax asset. The net carrying amount of deferred tax asset is likely to be the same, but tuil IFRS does not request the disclosure of a valuation allowance.

Deferred tax assets and liabilities are Same as IFRS for SMEs. measured using the tax rates (and [lAS 12.47, 49, 53] tax laws) that apply or have been (substantively) enacted by'lhe reporting date.

Deferred tax assets and liabilities are not discounted.

Where an entity is subject to different tax rates depending on different levels of taxabie income, deferred tax assets and liabilities are measured at the averags tax rats applicable to the periods in which it expects the temporary differences to revSrs&.

pFRS lor SMEs 29.18, 29.19, 2921-29.24].

Review of The net carrying amount of the Similar to IFRS for SMEs. The carrying deferred tax deferred tax asset is reviewed at each amount of the deferred tax asset assets reporting date; the valuation allowance is reviewed at each reporting date

is adjusted to reflect the current and is reduced when it is no longer assessment of futura taxabie profits. probable that sufficient taxable profit pFRS lor SMEs 29.22] will be available to allow recovery of

the deferred tax asset. This reduction is reversed when subsequently it becomes probable that sufficient taxable profit will be available.

Net carrying amount of deferred tax asset likely to be the same. [lAS 12.56]

Similarities and differences - A comparison of 'fuIIIFRS' and IFRS tor SMEs

êî

×ÚÎ

꼱

®Í

ÓÛ

Ú

«´´

×ÚÎ

Í

Ѭ¸

»®

¬±°

·½