Putting the Plan into Planned Giving

91

PUTTING THE “PLAN” INTO PLANNED GIVING Ann E. Casey, CPA Vice President of Finance and Operations at the Madison Community Foundation Theresa A. Zeidler-Shonat, ASA Director of Valuation Services at Smith & Gesteland 1

-

Upload

smith-gesteland -

Category

Business

-

view

1.085 -

download

1

Transcript of Putting the Plan into Planned Giving

PUTTING THE “PLAN” INTO PLANNED GIVING

Ann E. Casey, CPAVice President of Finance and Operations at the Madison Community Foundation

Theresa A. Zeidler-Shonat, ASADirector of Valuation Services at Smith & Gesteland

1

ANN E. CASEY, CPAAnn Casey is Vice President of Finance and Operations for Madison Community Foundation, where shedirects the financial and accounting activities for the foundation's assets, including oversight forinvestment management and policy development. She also assists individuals with planned giving andmajor gifts.

Before joining MCF in 1999, Ann spent nearly 20 years in public accounting as a Senior Tax Manager withboth Ernst & Young and Grant Thornton, focusing on tax planning for entrepreneurial businesses,executives and high net worth individuals.

Beyond her commitment to managing philanthropy through the Madison Community Foundation, Anndemonstrates a commitment to community through her many volunteer activities. She is currently onthe Board of the Wisconsin Planned Giving Council and the Catholic Diocese of Madison Foundation.She is also a public board member of the University of Wisconsin Medical Foundation, as well as itsInvestment and Audit Committees.

Ann holds a BBA in Accounting from UW-Whitewater and a Masters in Taxation from UW-Madison, andcompleted the Strategic Perspectives in Non-Profit Management program at Harvard School of Business.

2

THERESA A. ZEIDLER-SHONAT, ASA

As an Accredited Senior Appraiser in the Business Valuation discipline, Theresa specializes in businessenterprise, equity, and intangible asset valuations for financial reporting, gift and estate tax, tax planning,succession planning, merger and acquisition planning and assessment, divorce and litigation support, andSBA lending requirements.

Theresa has performed valuations for companies in a wide variety of industries that range fromtraditional service and manufacturing industries to service industries to rapidly-changing and high-techindustries and other intellectual-property-intensive industries. Theresa has worked with clients thatrange in size from small family businesses to multi-billion dollar, multi-national firms.

Theresa takes a consultative approach to business valuation. In her role she helps companies understandthe value of their businesses, and gives them the tools and information to understand how their actionscan strengthen their business.

3

WHAT CAN GIVING DO?

Think of all the things that Charitable Giving and Philanthropy

do for our Community…….

4

CLEAN LAKES AND WATER 5

LIBRARIES 6

EDUCATION AND OPPORTUNITY

7

JOB TRAINING 8

PARKS AND PLAYGROUNDS

9

ARTS & CULTURAL ACTIVITIES 10

HOUSING

11

FOOD 12

HOW TO GIVE

• Lifetime gifts• Life Interest Gifts• Planned/Deferred Gifts

13

OUTRIGHT GIFTS

• Cash, Check, Credit card, Text-to-Give• Securities

– Publicly traded stock, mutual funds– Closely-held business interests

• Real Estate, Other property• Retirement accounts, Annuities, Life Insurance

14

DONATE LONG-TERM GAIN PROPERTYSell stock/Gift Cash Gift Stock

Stock Value $50,000 $50,000

Basis 10,000

Long-Term Capital Gain $40,000

Gift to charity $50,000 $50,000

Tax on gain 8,000 0

Tax savings of deduction (15,000) (15,000)

Net cost of gift $43,000 $35,000

15

ORDINARY INCOME

• For property which would result in Ordinary Income when sold:– Charitable deduction reduced, or– Ordinary Income must be recognized

16

ORDINARY INCOME

• Examples:– Short Term gain property– IRAs– S Corps, Partnerships, LLCs– Commercial annuities or insurance– Real estate

17

LIFE INTEREST GIFTS

• Charitable Remainder Trust– Income to individual/remainder to charity

• Charitable Lead Trust– Income to charity/remainder to individual

• Retained Life Interest in Property– Give home to charity; donor may live in home

18

CHARITABLE GIFT ANNUITY

• Donor(s) receives lifetime income in return for charitable gift

• Immediate tax deduction• Annuity rate based on age• Annuity payments partially tax-free• Remainder of gift/fund stays with charity

19

CGA SAMPLE RATES

One LifeAGE RATE

60 4.4%

65 4.7%

70 5.1%

75 5.8%

80 6.8%

85 7.8%

90+ 9.0%

Two LivesAGE RATE60/65 4.0%

65/70 4.4%

70/75 4.8%

75/80 5.3%

80/85 6.1%

85/90 7.3%

90/95 8.8%

20

GIVING VEHICLES

Private Foundation– Separate charitable entity– Minimum $3 million - $5 million recommended– Apply for tax-exempt status; annual tax returns– Not really “private”– Annual board meetings, corporate records– Closely-held stock deducted at basis only

21

GIVING VEHICLESDonor Advised Fund

– Component fund within another charity• Community foundations• Commercial investment companies

– Simple to create, low minimums– No separate tax filings or record-keeping– “Recommend” grants and distributions– Can give anonymously

22

AUDIENCE POLL:Do you have Charity in your Estate Plan?

YES

NOT YET

23

LEGACY EXAMPLE

Continue Lifetime Giving

• Add to Donor Advised Fund at CF

• Support ~30 annual charities

• Adjust list as interests have changed

• Payout over 10 years• Report back to family

24

LEGACY EXAMPLE

One Bequest, Many Uses

• College scholarship fund• High school scholarship

fund• Donor advised fund for

children• Immediate grants to 20

favorite charities

25

BEQUESTS

Gift of property or money promised to a person or organization upon your death.

90% of Planned Gifts

• Defined $$ amount• % of estate• Specific asset• Beneficiary

– Bank account– Life Insurance– Retirement Funds

26

BEQUESTSI/we give and bequeath (describe bequest) to Madison

Community Foundation, Madison, Wisconsin, for its charitable purposes as defined in and subject to the provisions of the Madison Community Foundation Trust Agreement as it exists on this date or as they

may be amended in the future. This gift shall be added to the Bob and Sue Smith Donor Advised Fund.

27

WHAT TO GIVE TO CHARITY• During Lifetime – Capital Gain property

– No gain recognized; full FMV deduction– At death, taxable beneficiaries get step-up in basis

• Gain goes away forever

• At Death – Ordinary Income accounts– Taxable beneficiaries would be taxed on income– Charity pays no income tax

28

CHARITABLE GIFT PLANNINGWhat to consider

• Donor considerations– Values and interests– Available assets

Valuation Tax consequences Ease and consequences of transfer

– Income considerations Need for future income Ability to generate income from gift

29

CHARITABLE GIFT PLANNINGWhat to consider

• Non-Profit considerations– Ability to liquidate the gift– Risks/Costs of ownership

Valuation and acceptance costs Holding/liquidation costs Liabilities Tax consequences

– Capacity to honor donor intent Current or new program or initiative? Mission fit or mission drift? Other donor expectations

30

PLANNING PROCESS & TEAM

• Consult with: – Tax Advisor– Attorney– Appraiser– Giving Coordinator at Charity/Charities

31

WHY PEOPLE GIVE• 2014 Study of High Net Worth philanthropy

(household income >$200,000)– 74% belief gift can make a difference– 73% personal satisfaction– 66% supporting the same causes– 63% giving back to the community– 62% serving on a nonprofit’s board or

volunteering for a non-profit

32

BUT WHAT ABOUT TAX BENEFITS OF PHILANTHROPY?

• Only 34% of donors cited tax advantages among their chief motivators for giving.

• Even if they aren’t a primary motivator, tax advantages exist.

• There are also impacts on what you need to include in your tax return.

33

THE KNOWLEDGE CONNECTION

• The study found strong relationships between donors’ knowledge of giving and personal fulfillment from giving.

• Donors who rated themselves “expert” at giving both give more and gain more fulfillment from giving.

34

NON-CASH GIFTS

• Most non-cash gifts have some sort of valuation or appraisal requirement related to taking a charitable deduction on a tax return.

35

WHEN TO DO AN APPRAISAL

• Art work(s) with a total claimed value deduction at or exceeding $20,000 must have a complete, signed appraisal by a qualified appraiser attached to the return;

• Be sure to verify IRS requirements regarding photo-documentation.

36

WHEN TO DO AN APPRAISAL• Any personal property with a claimed

deduction exceeding $250 must include with the return a written communication from the qualified organization containing the name of the organization, the date of the contribution and the amount of the contribution

37

PERSONAL PROPERTY?• General Definition:

– A type of property which can include any asset other than real estate. The distinguishing factor between personal property and real estate is that personal property is movable.

– That is, the asset is not fixed permanently to one location as with real property such as land or buildings. Examples of personal property include vehicles, furniture, boats, collectibles, etc.

38

WHEN TO DO AN APPRAISAL• The donor must have an acknowledgement

stating whether the organization provided any goods or services in exchange for the gift and, if so, a description and a good faith estimate of the value of those goods or services.

39

WHEN TO DO AN APPRAISAL

• Any personal property with a claimed deduction exceeding $500 but less than $5,000, the client must complete Section A of the Form 8283 and attach it to the tax return (this includes donation of household contents exceeding claimed $500)

40

WHEN TO DO AN APPRAISAL• Any personal property with a claimed

deduction of $5,000 or more, Section B of IRS Form 8283 must be completed (including “qualified appraiser’s” and donee’s signatures) and attached to the tax return. A qualified appraisal must be prepared for the donated property.

41

WHEN TO DO AN APPRAISAL• This applies to single items or multiple similar

items of personal or real property.

42

WHEN TO DO AN APPRAISAL

43

• IRS: Appraisal for charitable gift deduction for tax return must be effective as of date of donation or no more than 60 days preceding donation.

POLL QUESTION

How Long do you think a Typical Business Appraisal Process Takes?A. 4 to 6 monthsB. 3 to 6 weeksC. 2 to 3 monthsD. 1 to 2 weeksE. 3 to 4 days

44

Business Interest Appraisal Timeline

45

I.

• Project Scoping and Engagement Letter• This typically takes a few days between initial discussions and the engagement

letter

II.

• Information and Data Request• This length of this step depends on how quickly client responds with requested

information

III.• Initial Modeling and industry research• This portion should take 4 to 6 days to complete

Business Interest Appraisal Timeline

46

IV.• Follow up questions for client• Questions arise during step III. Timing depends on client response time.

V.

• Finish model and finalize report• A few days to a week depending on responses received in Step IV.

VI.• Submit final report to client• In total process typically takes 3 to 6 weeks .

APPRAISAL TIMELINE• Length it takes to complete a business

appraisal can be affected by:– Whether the appraiser can start right away or has

other projects that must be finished before starting yours

– Responsiveness to information requests/follow-up questions

47

APPRAISAL TIMELINE

• You may also need– Real estate appraisal– Machinery and Equipment appraisal– Art or Antiques appraisal

• The timelines for those are different. If they are assets held in the business, these appraisals need to be complete before business appraisal can be finalized.

48

IRS Guidance Regarding Appraisals for non-cash charitable contributions

• IRC Section 170(f)(11)• Section 883 American Jobs Creation Act• Section 1219 of the Pension Protection Act of

2006• IRC Section 6695A

49

WHAT’S NOT DEDUCTIBLE?• A contribution to a specific individual,• A contribution to a non-qualified organization,• The part of a contribution from which the

individual receives or expects to receive a benefit (such as sports tickets or a dinner),

• The value of time or services,• Personal expenses.

50

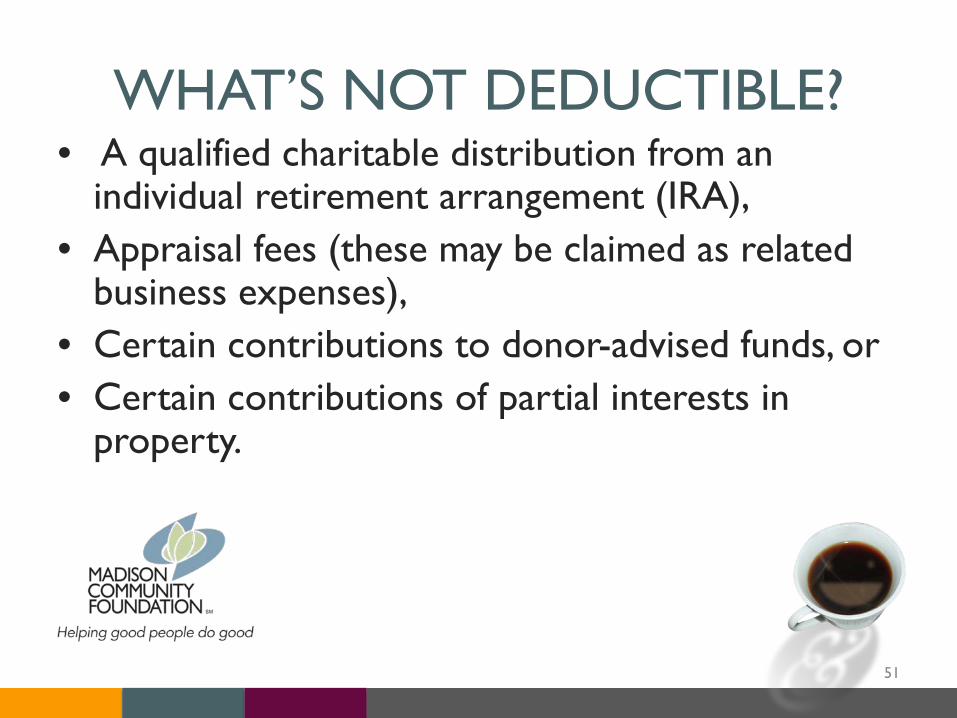

WHAT’S NOT DEDUCTIBLE?• A qualified charitable distribution from an

individual retirement arrangement (IRA),• Appraisal fees (these may be claimed as related

business expenses),• Certain contributions to donor-advised funds, or• Certain contributions of partial interests in

property.

51

WHAT’S NOT DEDUCTIBLE?• One may not deduct a charitable contribution

of a fractional interest in tangible personal property, unless all interests in the property are held immediately before the contribution by the donor or by the donor and the qualifying organization receiving the contribution.

52

WHO CAN AND CAN’T PERFORM APPRAISALS

• The IRS has a requirement that a “Qualified Appraiser” is used.

• The IRS also excludes certain individuals from performing appraisals for tax purposes.

53

WHAT IS A “QUALIFIED APPRAISER?”

• Has an appraisal designation from an appraiser org, or

• Has met certain minimum education and experience requirements;

• Regularly prepares appraisals for which he or she is paid;

54

WHAT IS A “QUALIFIED APPRAISER?”

• Demonstrates verifiable education and experience in valuing the type of property being appraised;

• Has not been prohibited from practicing before the IRS under section 330(c) of title 31 of the United States Code at any time during the 3-year period ending on the date of the appraisal;

• The individual is not an excluded individual.

55

APPRAISER ORGANIZATIONS• Business Appraisals

– American Society of Appraisers (ASA)• Accredited Senior Appraiser (ASA)

– The Institute of Business Appraisers (IBA)• Certified Business Appraiser (CBA)

– National Association of Certified Valuation Analysts (NACVA)

• Certified Valuation Analyst (CVA)

56

APPRAISER ORGANIZATIONS• Machinery and Equipment Appraisals

– American Society of Appraisers (ASA)• Accredited Senior Appraiser (ASA)

– Association of Machinery and Equipment Appraisers (AMEA)

• AMEA accredited or certified

– NEBB Institute• Certified Machinery & Equipment Appraiser (CMEA)

57

APPRAISER ORGANIZATIONS• Art and Antique Appraisals

– American Society of Appraisers (ASA)• Accredited Senior Appraiser (ASA)

– Appraisers Association of America (AAEA)• Certified Member

– International Society of Appraisers

58

APPRAISER ORGANIZATIONS• Real Estate Appraisals

– American Society of Appraisers (ASA)• Accredited Senior Appraiser (ASA)

– National Association of Real Estate Appraisers (NAREA)

– Appraisal Institute• Real estate appraisers must be licensed/certified

in the state in which the property exists

59

WHAT IS AN “EXCLUDED INDIVIDUAL?”

• The donor of the property, or the taxpayer who claims the deduction.

• The donee of the property.• A party to the transaction in which the donor acquired the

property being appraised, unless the property is donated within 2 months of the date of acquisition and its appraised value is not more than its acquisition price. This applies to the person who sold, exchanged, or gave the property to the donor, or any person who acted as an agent for the transferor or donor in the transaction.

60

WHAT IS AN “EXCLUDED INDIVIDUAL?”

• Any person employed by any of the above persons. For example, if the donor acquired a painting from an art dealer, neither the dealer nor persons employed by the dealer can be qualified appraisers for that painting.

• Any person related under section 267(b) of the Internal Revenue Code to any of the above persons or married to a person related under section 267(b) to any of the above persons.

• An appraiser who appraises regularly for a person in (1), (2), or (3), and who does not perform a majority of his or her appraisals made during his or her tax year for other persons.

61

THE VALUE OF YOUR GIFT MAY NOT BE WHAT YOU THINK IT IS…

62

Fair Market Value

“The price at which the property would change hands between awilling buyer and a willing seller when the former is not under anycompulsion to buy and the latter is not under any compulsion to sell,both parties having reasonable knowledge of relevant facts. Courtdecisions frequently state in addition that both the hypotheticalbuyer and seller are assumed to be able, as well as willing, to tradeand to be well informed about the property and concerning themarket for such property.”

63

Source: IRS Revenue Ruling 59-60

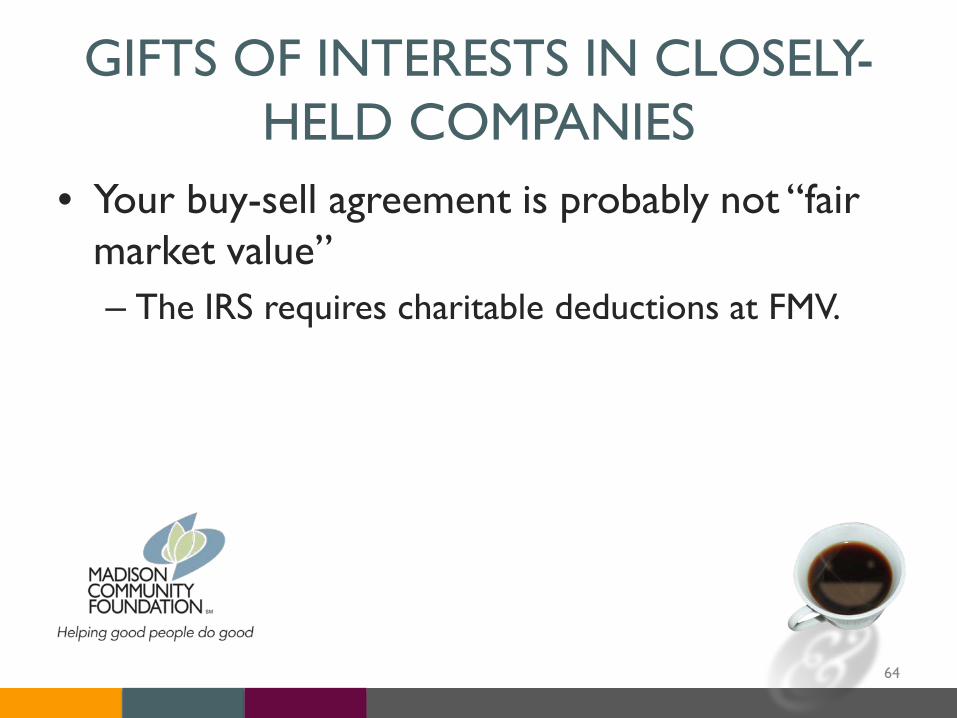

GIFTS OF INTERESTS IN CLOSELY-HELD COMPANIES

• Your buy-sell agreement is probably not “fair market value”– The IRS requires charitable deductions at FMV.

64

GIFTS OF INTERESTS IN CLOSELY-HELD COMPANIES

• Market participate considerations?– Value of ability to control the company (discount

for lack of control)– Opportunity cost of investment (discount for lack

of marketability/non-liquidity)

65

Point in time Measurement• Value Changes over time• “Valuation Date” is important

66

Intangible Assets

• Intellectual Property (IP)• Marketing Intangibles (Trademarks)• Artistic Intangibles• (there are other intangible assets that are

harder to gift)

67

Art and Antiques• Auction prices may not be FMV

– Typically auction prices include both buyer and seller fees

• Your insurance appraisal is replacement cost, not FMV

• eBay isn’t a good source for value estimates, either

68

IRS Restrictions on Charitable Deductions for Intangibles

• The taxpayer’s initial deduction for contributions of certain intellectual property may be the lesser of the taxpayer’s basis in the property or the fair market value of the property.

69

IRS Restrictions on Charitable Deductions for Intangibles

• Transfers of property are not deductible:– If the transfer is of a partial interest in property.– To the extent that consideration is received for

the transfer.– If the transfer is inadequately substantiated.– To the extent the property is overvalued.

70

IRS Restrictions on Charitable Deductions for Intangibles

• The fair market value of a patent must take into account factors such as whether the patented technology has been made obsolete by other technology; any restrictions on the donee’s use of, or ability to transfer the patented technology; and the length of time remaining before the patent’s expiration.

71

LIMITATIONS ON DEDUCTIONS• If the donor contributes personal property

that has a fair market value less than the donor's basis in the item, the claimed deduction is limited to the fair market value.

• Donor cannot claim a deduction for the difference between the basis and the fair market value.

72

LIMITATIONS ON DEDUCTIONS• If the donor contributes property with a fair

market value that is more than the donor's basis, the donor may have to reduce the fair market value by the amount of appreciation (increase in value) when figuring the deduction to be claimed.

• Different rules apply to figuring the deduction, depending on whether the property is ordinary income property or capital gain property

73

LIMITATIONS ON DEDUCTIONS

• Donation of self-created works: Since the 1970s, an artist may not claim the fair market value of self-created works donated by the maker to a qualifying nonprofit organization. The artist may only claim the cost of materials used in creating the works.

74

MAKE SURE YOU AREN’T GIFTING A PROBLEM

• Are there restrictions on transfer?• Check your buy-sell agreement and other

corporate documents– Can an organization outside of company

management own company equity?

75

MAKE SURE YOU AREN’T GIFTING A PROBLEM

• Illustrative Example of a problem…• Robert Rauschenberg’s Canyon

– A work of art in the estate of art dealer Ileana Sonnabend

76

THE CANYON PROBLEM

Image from MOMA.org 77

THE CANYON PROBLEM

Image from MOMA.org 78

THE CANYON PROBLEM

Image from MOMA.org

Taxidermied Bald Eagle

79

THE CANYON PROBLEM

• Under US law it can’t be sold because it contains a taxidermied bald eagle.

• Actually, most people can’t even own it, much less sell it.

80

THE CANYON PROBLEM

• Violation of:

– 1940 Bald and Golden Eagle Protection Act

– 1918 Migratory Bird Protection Act

81

THE CANYON PROBLEM

• Criminal Penalties for Anyone who:– “take, possess, sell, purchase, barter, offer to sell,

purchase, or barter, transport, export, or import, at any time or any manner… alive or dead, or any part, nest, or egg thereof…”

82

THE CANYON PROBLEM

• Sonnabend had an exemption to own the work based on a notarized statement that the bald eagle was stuffed by one of Roosevelt’s Rough Riders prior to passage of the laws

83

THE CANYON PROBLEM

• However, it couldn’t be sold or possessed by anyone else.

• How could it have a fair market value if it is illegal to have a market for it?

• Three separate appraisers valued it at $0

84

THE CANYON PROBLEM

• The IRS disagreed and said it was worth $65 million

• They imposed penalties• It went to tax court

85

THE CANYON PROBLEM• The ultimate resolution?• The IRS agreed to drop fines and taxes• However, the work had to be donated to a US

Institution and the estate could not claim a charitable deduction on it

• It is in MoMA’s collection today

86

WHAT’S NEXT?• Think about what

you want to support

• Think about which of your assets is best gift to support it (hint: it may not be cash)

• Talk to your legal and tax advisors

87

WHAT’S NEXT?• Talk to the giving

coordinator at the charities you want to support

• Line up the appraisals you’ll need

• Feel good about supporting the things that matter to you

88

Questions?

89

Theresa Zeidler-Shonat, ASADirector of Valuation Services

Smith & Gesteland, LLP608.828.3154

Ann Casey, CPAVice President Finance and Operations

Madison Community Foundation608.232.1763

90

91