PUNE ICAI'S HELPDESK EMAIL ID support@puneicaiPUNE ICAI'S HELPDESK EMAIL ID [email protected]....

20

Transcript of PUNE ICAI'S HELPDESK EMAIL ID support@puneicaiPUNE ICAI'S HELPDESK EMAIL ID [email protected]....

Computers make it easier to do a lot of things, but most of the things they make it easier to do don't need to be done. - Andy Rooney

News Letter Pune Branch of WIRC of ICAI/June 2015

SEMINAR ON �NITTY-GRITTY OF PRIVATE LIMITED COMPANIES UNDER THE COMPANIES ACT, 2013�

CA. Neeraj SharmaSpeaker

CA.Kusai GoawalaSpeaker- Lecture meet on Schedule II

of Companies Act-2013

INTENSIVE COURSE ON INFORMATION SYSTEM AUDIT OF BANKS

CISA. Mahesh KVSpeaker

CA. Rajendra PonksheSpeaker

Mr. Sunil BakshiSpeaker

CA. Shirish PadeySpeaker

Global certification program on QuickBooks

CS. Milind KasodekarSpeaker

CA. C. V. ChitaleSpeaker

CS. J. SridharSpeaker

Adv. Vasant KarjatkarSpeaker

Adv. R. V. Daravade Speaker

Mr. Sachin DedhiaSpeaker

LECTURE MEET ON PROPERTY TRANSACTION & IT's DOCUMENTATION, STAMP ACT & REGISTRATION

Workshop On IT SECURITY IN CA's OFFICE, CYBER CRIME

INVESTIGATIONS & DIGITAL FORENSICS

2

In the old days, people robbed stagecoaches and knocked off armored trucks. Now they're knocking off servers. - Richard Power

News Letter Pune Branch of WIRC of ICAI/June 2015

Dear Members,

The principle �Change is the only constant� stimulates and inspires us to face the challenges of the fast changing world of post globalization era. Pune Branch is also changing to serve you better with effect from

th13 June, 2015.

The pace of the information technology revolution is phenomenal since last few years. For keeping in tandem with the latest facilities for effective communication and further comfortable platform for members and students, Pune Branch has revamped its website which is being launched on 13th June, 2015. The Branch is also launching its first ever mobile app (for three platforms viz. Android Platform, Windows Platform, & IOS (Apple) Platform) on the same date. We do hope that the members and students will find the new website and mobile app more user friendly and helping in terms of efficient services from the Branch.

One more initiate to address the insufficient connectivity through telephonic channel at the Branch will be a dedicated email id [email protected] where you can send email for any of your query/enquiry. You will immediately get response by email with a ticket number assigned to your query/enquiry which will be replied by the concerned department within given specified time frame. This will help in saving your valuable time in unproductive phone dialing in futile.

The Branch activities during May, 2015 both for members and students provided as usual important inputs through various programmes organized and coordinated by the Branch.

The CPE programmes for members covered plethora of programmes like lecture meets, workshops, intensive courses, seminars etc. The variety of subjects' covered were Property Transactions & its Documentation, Stamp Act & Registration, IT Security in CA's Office, Cyber Crime Investigations & Digital Forensics, Nitty-Gritty of private limited companies under the Companies Act, 2013, Intensive Course on Information System Audit of Banks, Black Money & Imposition of Tax Bill 2015 and Introduction of GST, Global certification program on Quick Books, Schedule II of Companies Act-2013, IFRS, Foreign Contribution Regulation Act, Professional Opportunity as Insurance surveyor & Loss Assessor, Forensics/Fraud Investigation, Income Computation and Disclosure Standards (ICDS), Service Tax input Credits, CARO under Companies Act-2013, Practice Development Skills etc. The annual

event of Direct and Indirect Taxes Refresher Course has started from th30 May, 2015.

Another important programme in May, 2015 was meeting organized by Grievance Redressal Forum, for Members & Students held by Deputy Secretary &In-charge of Members, Students & Firms Section (Decentralized Office) of WIRC of ICAI.

The hectic and unending work schedules of CA profession need to be compensated by inculcating some healthy habits and hence, the Branch has organized Yogasana and Pranayam classes on every Sunday morning at Branch.

The students programmes comprised of Seminar on "Depreciation - Schedule II" and "CARO 2015" - Decoding the new regulations, Seminar on Accounting Standards- 28,30,31,32, Industrial visit to John Deere John Deere India Private Limited, Sanaswadi, Pune, and an Educational visit to National Research Centre for Grapes, Manjri, Pune.

The month of June, 2015 will also be a busy month here at Branch with plethora of programmes lined up; the details of the same are published elsewhere in this Newsletter and also available on the website.

Dear members and students I appeal you all to visit the new website as well download the mobile app of the Branch and please post your feedback with constructive suggestions if any for further betterment in providing effective services. As well please opt for sending your enquiries/queries through email to [email protected].

Before concluding this communiqué, I pray for the smooth onset of the monsoon season that is knocking at present Kerala State's doors.

Thank you!

Plot No. 8, Parshwanath Nagar, CTS No. 333, Sr. No. 573, Munjeri, Opp. Kale hospital, Near Mahavir Electronics, Bibwewadi, Pune 411 037

Tel: (020) 24212251 / 52

Web: www.puneicai.org

Email: [email protected]

PUNE BRANCH OF WIRC OF ICAI

3

In a few minutes a computer can make a mistake so great that it would have taken many men many months to equal it. - Anonymous

News Letter Pune Branch of WIRC of ICAI/June 2015

7th June to 5th July, 2015(Every Sunday for

5 Days)

Advanced Excel for CA Members-2015 [Batch 2]

IIFA Campus: 917/15 A, Vikas A,

Ganeshwadi, Behind British

Library, FC Road, Shivajinagar, Pune

411004.

9.00 AMTo

5.00 PMRs. 4,200/-

8th June to 12th June,2015

workshop for students on English Speaking and Presentation Skills

ICAI Bhavan,Bibvewadi,

pune-37

8.00 AM To

10:00 AMRs. 500/-

9th June,2015Lecture Meet on "Gearing up for GST"

ICAI Bhavan,Bibvewadi,

pune-37

5:00 PMTo

7:00 PMRs. 200/-

11th June, 2015Lecture meet on Transfer pricing -Recent Development

ICAI Bhavan,Bibvewadi,

pune-37

5:00 PM To

7:00 PMRs. 200/-

16th June, 2015Lecture meet on Enq uiries u/s 83 & 88 of Maharashtra Co-op Act

ICAI Bhavan,Bibvewadi,

pune-37

10:00 AM To

12:00 PMRs. 200/-

13th June,2015Certificate Course on International Taxation -

9.30 AM To

5.30 PMRs. 25000/-

13th & 14th June,2015REGIONAL AUDITING CONCLAVE Hotel Aurora Towers

9.30 AM To

5.30 PM

Rs. 1,800/-Registration up to 7th June, 2015-

Early Bird Fee: Rs. 1,500/-

17th June,2015Educational Visit to National Stock Exchange (NSE)

National Stock Exchange (NSE) in

Mumbai- Rs. 200/-

19th & 20th June,2015Intensive Course on Package Scheme of Incentives - 2013

ICAI Bhavan,Bibvewadi,

pune-37

9.00 AM To

5.00 PM

RS. 1500/-per Member: Registration up to 10th June, 2015-Early Bird Fee: Rs. 1,200/- per

Member

20th June,2015DIRECT TAXES' REFRESHER COURSE (DTRC) -2015[ Day-3]

MES Auditorium,Bal Shikshan School,

Kothrud, Pune

9.30 AMTo

1.00 PMRs. 300/-

NA

30 Hrs

2 Hrs

2 Hrs

2 Hrs

20 Hrs

12 Hrs

NA

12 Hrs

3 Hrs

4

If computers get too powerful, we can organize them into a committee. That will do them in. - Bradley'sBromide

News Letter Pune Branch of WIRC of ICAI/June 2015

20th June,2015Convocation for CA Students

Mahatma Phule Sanskrutik Bhavan,

Wanowarie, Pune - 40

9.00 AMTo

2.00 PMNA

21st June,2015Seminar on Auditing in SAP Enviournment

ICAI Bhavan,Bibvewadi,

pune-37

9.00 AMTo

5.00 PMRs. 600/-

23rd June,2015Lecture Meet on Issues in Domestic Transfer pricing

ICAI Bhavan,Bibvewadi,

pune-37

5.00 PM To

7.00 PMRs. 200/-

27th & 28th June,2015

WORKSHOP ON IT SECURITY IN CA's OFFICE, CYBER CRIME INVESTIGATIONS & DIGITAL FORENSICS-[Batch 3]

IT Center, ICAI Bhavan,Bibvewadi,

pune-37

9:30 AMTo

6.00 PM

Rs.2400/- per Member & Rs.3370/-(Inclusive

of Service Tax) For Non Members

27th June,2015DIRECT TAXES' REFRESHER COURSE (DTRC) -2015[ Day-4]

MES Auditorium,Bal Shikshan School,

Kothrud, Pune

9.30 AM To

1.00 PMRs. 300/-

27th June,2015

Seminar on "Recent Amendments in Provisions of sec 263 Regarding Revision of Asst orders by CIT"

ICAI Bhavan,Bibvewadi,

pune-37

3 PM To

6 PMRs. 300/-

25th June to 1st July,2015 Foundation Day Activities Under Finalization - -

4th & 5th July, 2015 National Tax ConventionSiddhi Banquet

Hall, Near Mhatre Bridge, Erandwane,

Pune

9.30 AMTo

6.00 PM

Rs: 2500/- per Member, Registration up to 20th June, 2015

Early Bird Fee: Rs. 2,000/- per Member

10th July,2015INDIRECT TAXES' REFRESHER COURSE (DTRC) -2015[ Day-5]

MES Auditorium,Bal Shikshan School,

Kothrud, Pune

9.30 AMTo

1.00 PMRs. 300/-

11th July,2015INDIRECT TAXES' REFRESHER COURSE (DTRC) -2015[ Day-6]

MES Auditorium,Bal Shikshan School,

Kothrud, Pune

9.30 AMTo

1.00 PMRs. 300/-

NA

6 Hrs

2 Hrs

12 Hrs

3 Hrs

3 Hrs

NA

12 Hrs

3 Hrs

3 Hrs

5

One machine can do the work of fifty ordinary men. No machine can do the work of one extraordinary man. - Elbert Hubbard

News Letter Pune Branch of WIRC of ICAI/June 2015

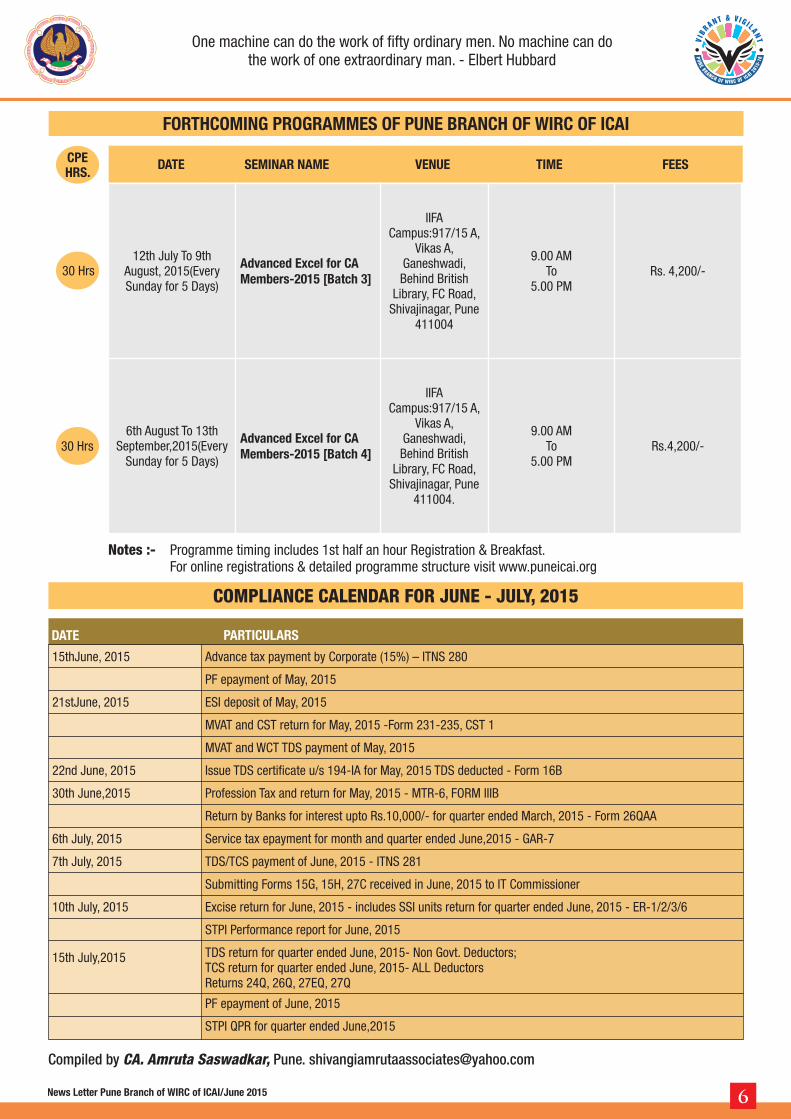

12th July To 9th August, 2015(Every Sunday for 5 Days)

Advanced Excel for CA Members-2015 [Batch 3]

IIFA Campus:917/15 A,

Vikas A, Ganeshwadi, Behind British

Library, FC Road, Shivajinagar, Pune

411004

9.00 AMTo

5.00 PMRs. 4,200/-

6th August To 13th September,2015(Every

Sunday for 5 Days)

Advanced Excel for CA Members-2015 [Batch 4]

IIFA Campus:917/15 A,

Vikas A, Ganeshwadi, Behind British

Library, FC Road, Shivajinagar, Pune

411004.

9.00 AMTo

5.00 PMRs.4,200/-

30 Hrs

30 Hrs

COMPLIANCE CALENDAR FOR JUNE - JULY, 2015

15thJune, 2015 Advance tax payment by Corporate (15%) � ITNS 280

PF epayment of May, 2015

21stJune, 2015 ESI deposit of May, 2015

MVAT and CST return for May, 2015 -Form 231-235, CST 1

MVAT and WCT TDS payment of May, 2015

22nd June, 2015 Issue TDS certificate u/s 194-IA for May, 2015 TDS deducted - Form 16B

30th June,2015 Profession Tax and return for May, 2015 - MTR-6, FORM IIIB

Return by Banks for interest upto Rs.10,000/- for quarter ended March, 2015 - Form 26QAA

6th July, 2015 Service tax epayment for month and quarter ended June,2015 - GAR-7

7th July, 2015 TDS/TCS payment of June, 2015 - ITNS 281

Submitting Forms 15G, 15H, 27C received in June, 2015 to IT Commissioner

10th July, 2015 Excise return for June, 2015 - includes SSI units return for quarter ended June, 2015 - ER-1/2/3/6

STPI Performance report for June, 2015

15th July,2015 TDS return for quarter ended June, 2015- Non Govt. Deductors;TCS return for quarter ended June, 2015- ALL DeductorsReturns 24Q, 26Q, 27EQ, 27Q

PF epayment of June, 2015

STPI QPR for quarter ended June,2015

Compiled by CA. Amruta Saswadkar, Pune. [email protected]

6

DATE PARTICULARS

Those parts of the system that you can hit with a hammer are called hardware; those program instructions that you can only curse at are called software. - Anonymous

News Letter Pune Branch of WIRC of ICAI/June 2015

WELCOME JUDGEMENT OF PUNE ITAT IN CASE OF SERUM INSTITUTE CA. Jatin [email protected]

Welcome Judgement of Pune ITAT in case of Serum Institute: Provisions of 206AA does not override the provisions section 90(2) of ITA, 1961

Recently, in case of DDIT(IT-II), Pune Vs. Serum Institute of India Limited, 'ITA no 1601 to 1604/Pn/2014', Honorable Pune Bench of Tribunal has held that section 206AA of ITA, 1961 does not override to DTAA provisions to the extent that, DTAA is more beneficial to assessee. The said verdict is welcomed, as Honorable Pune bench has resolved heavy contravention ever since Finance Act 2009.

A) Facts of the case:

a) Assessee is a company engaged in the business of manufacture and sale of vaccines, and it is a major exporter of the vaccines.

b) In the course of its business activities, assessee made payments to non-residents on account of interest, royalty and fee for technical services which are subject to withholding of Tax u/s 195 of ITA, 1961

c) The assessee deducted tax at source on such payment in accordance with the tax rates provided in the Double Taxation Avoidance Agreements (DTAAs) with the respective countries as the same was lower & therefore taking benefit of provisions of section 90(2).

d) Revenue noted that payment in case of some of the non- residents, the recipients did not have Permanent Account Numbers (PANs).

e) As a consequence, Revenue treated such payments, as cases of 'short deduction' of tax in terms of the provisions of section 206AA of the Act.

f) As per provisions of section 206AA if the recipient of any sum or income fails to furnish his PAN to the person responsible for deduction tax at source, the tax shall be deductible at higher of

- the rate specified in the relevant provisions of the Act or

- at the rates in force or

- at the rate of 20%.

g) On the strength of section 206AA of the Act, Revenue treated payments to those non-residents who did not furnish the PAN as cases of 'short deduction' being difference between 20% and the actual tax rate on which tax was deducted in terms of the relevant DTAAs.

h) On appeal to CIT(A), it was held in favour of assessee stating that 206AA does not override the provisions of section 90(2) of ITA,1961.

B) Issue put before Honorable Pune Bench:

Whether section 206AA would override the provisions of section 90(2) of ITA, 1961 and thereby, DTAA in a situation where non-resident taxpayer did not furnish PAN, and hence, a minimum withholding tax rate of 20% irrespective of the rate provided in the DTAA?

C) Contentions of Appellantst1 Contention

- Provisions of section 206AA are not applicable to payments made to non-residents as the provisions of section 139A(8) of the Act read with rule 114C(1) of the Income-tax Rules, 1962, non- resident taxpayers were not required to apply for PAN.

- Since, there was no obligation to obtain PAN, section 206AA of the Act would not be applicable, as it prescribed that the taxpayer shall furnish PAN, and this would be possible only where the taxpayer was required to obtain PAN in the first place.

nd2 Contention

- As per section 90(2) of the Act, provisions of the Act are applicable to the extent that they are more beneficial to the taxpayer. Since section 206AA of the Act prescribed the higher rate of withholding tax, it would not be beneficial to the taxpayer vis-à-vis the rates prescribed in the DTAAs.

D) Contention by Revenuest1 Contention

- Revenue relied on provisions of 206AA, memorandum of FA 2009 and Press release of CBDT no 402/92/2006 stating that section 206AA is applicable to Non-residents and it will override section 90(2) of the Act and therefore the tax deduction was liable to be made @ 20% in absence of furnishing of PANs by the recipient non-residents.

nd2 Contention

- CIT(A) had himself concluded that section 206AA of the Act required even the non-resident recipients of income to obtain and furnish PAN to Tax Deductors and hence, 206AA of ITA, 1961 is applicable to non residents also.

E) Ruling of Honorable Pune Bench

- The Honorable Supreme Court in the case of Azadi Bachao Andolan and Others vs. UOI, (2003) 263 ITR 706 (SC) has upheld the proposition that the provisions made in the DTAAs will prevail over the general provisions contained in the Act to the extent they are beneficial to the assessee.

- SC also hold that charging section 4 as well as section 5 of the Act which deals with the principle of ascertainment of total income under the Act are also subordinate to the principle enshrined in section 90(2)

- However, the provisions of Chapter 7 XVII-B governing tax deduction at source are not subordinate to section 90(2) of the Act. Section 206AA is not a charging section but is a part of a procedural provisions dealing with collection and deduction of tax at source. The provisions of section 195 of the Act which casts a duty on the assessee to deduct tax at source on payments to a non-resident cannot be looked upon as a charging provision.

7

If you tried to read every document on the web, then for each day's effort you would be a year further behind in your goal. - Anonymous

News Letter Pune Branch of WIRC of ICAI/June 2015

- The reliance is also placed on the Honorable Supreme Court in the case of CIT vs. Eli Lily & Co., (2009) 312 ITR 225 (SC) observed that the provisions of tax withholding i.e. section 195 of the Act would apply only to sums which are otherwise chargeable to tax under the Act.

- The reliance is also placed on the Honorable Supreme Court in the case of GE India Technology Centre Pvt. Ltd. vs. CIT, (2010) 327 ITR 456 (SC) held that the provisions of DTAAs along with the sections 4, 5, 9, 90 & 91 of the Act are relevant while applying the provisions of tax deduction at source.

- Therefore, in view of the aforesaid schematic interpretation of the Act, section 206AA of the Act cannot be understood to override the charging sections 4 and 5 of the Act.

- Thus, where section 90(2) of the Act provides that DTAAs

override domestic law in cases where the provisions of DTAAs are more beneficial to the assessee and the same also overrides the charging sections 4 and 5 of the Act which, in turn, override the DTAAs provisions especially section 206AA of the Act.

- Therefore, appeals of revenue are dismissed.

F) Key Take Away:

- Section 206AA of ITA, 1961 being procedural section cannot override section 90(2) of ITA, 1961 being charging section.

- 206AA is not applicable to Non-Residents.

- The with holding of tax can be made at beneficial rate of DTAA even if non resident does not have PAN in India.

INDIRECT TAX APPLICABILITY TO SOFTWARE INDUSTRY CA. Roopa [email protected]

CA. Madhukar N. [email protected]

In this article the paper writers have sought to examine the various kinds of software transactions and indirect taxes implications. Inspite of earning billions in CFE, the bane of the software industry in India in addition to no / part or delayed refund, has been imposition of multiple levies which has lead to double taxation especially with VAT and service tax being levied on same base amount. However all transactions are not liable for both ST and VAT.

Background

The aspect of ascertaining the applicability of indirect taxes under Central Excise, Customs, VAT or Service Tax is important. Before getting into the aspect of ascertaining the taxation, one has to firstly understand whether software is goods?

The Hon'ble Supreme Court in Tata Consultancy Services Vs State Of Andhra Pradesh 2004 (178) ELT 0022 (S.C.), held that Computer software in canned form or of the shelf software does have the attributes of having utility, capable of being bought and sold, capable of being transmitted, transferred, delivered, stored and possessed, which are the attributes of goods and thus it is goods is in its marketable form. From the said decision it is now well settled that 'software' is goods. In the case of Infosys Technologies Ltd., Vs. CCE 2009 (233) ELT 56 (Mad), held that even customized software is goods.

The High Court in ISODA case(2010 (020) STR 0289 Mad)upheld the constitutional validity of service tax on Information technology software service stating that not in all the cases of software related transaction there is sale. There may be also service element, what is intended to be taxed on the services involved in the transaction. It further said whether the transaction to be treated as Sale or Service has to be decided on a case to case basis based on terms and conditions between parties.

Central Excise and Customs on Software

Software on a CD or any other media is covered under the Central Excise Tariff Act, under the chapter heading (hereinafter referred as heading) 8523. The Chapter Notes to Chapter 85 read with the section 2(f)(ii) of the Central Excise Act, the activity of recording any phenomenon on a media would be deemed manufacture. Even reproduction of developed software into number of CDs would also be considered as deemed activity of manufacture.

Excise duty is applicable on packaged software at 12.5%. Customised software is exempted from excise duty vide notification 12/12-CE.

When software is imported on a media it is treated as goods and import duties applicable to same. BCD is free, CVD [equal to excise duty on like goods manufactured in India] is 12.5% for packaged software and nil for customized software. SAD is nil for Information technology software, other than that on floppy disc or cartridge tape vide notification 21/12-Cus.When BCD and CVD is nil, SAD is also nil vide notification 21/12-Cus for customized software. SAD is also nil for all pre-packaged goods intended for retail sale in relation to which it is required, under the provisions of the Legal Metrology Act, 2009 or the rules made thereunder or under any other law for the time being in force, to declare on the package thereof the retail sale price of such article. If it is required to declare RSP onpre-packaged goods [on software] intended for retail sale as per Legal Metrology Act, then SAD is exempted.

Service Tax

Under negative list based taxation, service tax is levied on all services other than those mentioned in negative list or a subject matter of exemption. The definition of service covers any activity done by one person to another for consideration. The term service is defined to include declared services. This has covered specified services relating to information technology software. Also covers temporary transfer of any intellectual property right as a service. Service tax rate is 12.36%.

Levy of VAT on software

In order to constitute a sale liable to VAT, tax there should be transfer of property in goods from one person to another for cash, deferred payment or other valuable consideration. By valuable consideration we mean something which could be measured in terms of money. The VAT is imposed as per rates set out in Section 4(1)(a) and (b) given in Schedules to Act.

On a perusal of schedule 3 of KVAT Act 2003, it sets out Exim scrips, ��..copyrights, patents and the like including software licenses by whatever name called. The applicable rate is 5.5%.

VAT vs Service tax on software

Where there is a program sold on media without reservation [source code etc also transferred] then it is plain and simple sale with no service being involved. Not liable to service tax. Once software is goods, transfer of right to use the same for consideration should be subject matter of VAT going by Article 366(29A) of Constitution of India.

8

There might be new technology, but technological progress itself was nothing new and over the years it had not destroyed jobs, but created them. - Margaret Thatcher

News Letter Pune Branch of WIRC of ICAI/June 2015

The deemed sale entry covers transfer of right to use goods. In many cases the copyright or the intellectual property right relating to the software sold continue to vest with the seller. This does not affect the nature of the transaction from being a sale for the purposes of the VAT Act, though it should.

The same transaction could also be taxable to service tax, under another declared services entry of transfer of goods by way of hiring, leasing, licensing or in any such manner without transfer of right to use such goods if the developer is merely permitting to use the software [which is goods] subject to conditions and restrictions as to its usage/replication imposed in this regards.

Where there is no involvement of transfer of right to use, then there may not be transfer of title in goods nor a deemed sale of goods. There must be a transfer of right to use any goods and when the goods as such is not transferred, the question of deeming sale of goods does not arise and the transaction would be only a service and not a sale.

There is a finer distinction between the applicability of VAT and service tax. In the case of VAT there would be �transfer of Right to Use the Goods�. Whereas under the service Tax, what is levied is �temporary transfer/enjoyment of the goods�.

Again taking conservative view most people in software industry, are charging both VAT and Service Tax usually where software is given by means of a license.

Indirect Taxes on Models prevalent in software industry

The industry has the following types of transactions:

a. Canned or off the shelf software: Development, upgradation, etc., done before release is for oneself. This can be construed only as sale of goods liable to sales tax. Where a master is copied, the duplication has been considered to be manufacture. Therefore liable for excise duty @ 12.5%[if off the shelf packaged software]. If imported same impact.

b. Customised Software: When one sells customised software to the customer as per their needs it is a sale liable to VAT. It is also subjected to service tax. Not liable to Excise duty. If software developed by seller then not liable for service tax also as it is a �literary work��.

c. Electronic download: The software are not given on media CD or in hard form, instead it is permitted to be downloaded from internet and license is provided separately to use it, here it is considered as service. The VAT authorities are contending that 'right to use goods' comes within the ambit of deemed sale definition, taxed under sales tax. At present there is double taxation, with both VAT/sales tax and Service Tax being charged.

d. Sale of licenses: This is a deemed sale of right to use the software liable for sales tax. It could also be liable to service tax.

e. Customisation on software owned by customer: This is working on the program owned by the client where the property of the developed program is always the property of the customer. VAT/ Sales tax is not payable on same. Service tax liable.

f. Software developed as per customer specification: The customer gives specifications and company develops to the needs of the customer. Since the company does not retain rights and completely given to the customer with source and object codes, there is no service, it is only sale of goods subject matter of only sales tax.

g. Software works contract- Option 1- IPR with Developer: Customer is intending to develop the software wherein they seek services of software company to develop on continuous consultation with the customer, where the original software belongs to the customer. In this process the Intellectual Property of the final product may go to the customer, but the intermediate programs would be that of software company, which can be used by them for other developments. This involves providing of both services as well as goods (as firstly the property in software developed comes to development company and later transfers to that extent to the customer. In addition to this they also provide services of incorporation, implementation etc.,). This could be considered as works contract under sales tax and service tax department is treating it as service. Both sales tax and service tax is being paid by the industry in this case as well.

h. Option- 2- IPR with Customer: Similar to the previous one, except that all the intellectual property in all the work would belong to the customers and in no part it would become the property of the service provider. As and when codes generated they belong to the customer. This is merely a service of software development provided to the customer and therefore it is subject matter of only service tax. However it should be appropriately supported by documents to mitigate the local VAT authorities queries.

i. Software Consultancy: The customer engages professional as consultants, developers who would work only under supervision or control of the customer with no responsibility on them to deliver any specific software work. It is only service liable to service tax.

IDT implications of various revenue models

1. Access of Software on Subscription basis: When access to software is given, without any license to use, only liable to service tax under Information technology software services and there maybe no VAT liability.

2. Software patches: As a part of upgradation or AMC, any further software patches are provided, then as also involving sale of goods by sales tax authorities. Therefore the same would be subject matter of sales tax as well in addition to service tax.

3. Implementation of software/installation: There is no transfer of property in goods nor a right to use goods. Merely an implementation service, subject matter of only service tax.

4. Testing: It is a pure service, as there is no transfer of right to use the software. Liable only to service tax.

5. Debugging: Only if there is a transfer of software, it is liable to sales tax. Debugging not involving additional software addition would be liable to only to Service tax.

6. Maintenance of software: This maybe a works contract or a service contract. If works contract liable for both. If pure service contract, it is not liable to sales tax.

7. Software on server / cloud: This is a new methodology where the control and possession of the data/ programs being accessed remain with the service provider [ ISP] which maybe hosted on the server of the vendor in or outside India. The contract allows the customer to access the site and enjoy certain privileges. This would be liable only to service tax.

8. Manpower supply within India or outside India: Software engineers with specific skills/ qualification provided within India, it is liable to service tax. When sent abroad, where they are

9

The most overlooked advantage to owning a computer is that if they foul up there's no law against whacking them around a little. - Porterfield

News Letter Pune Branch of WIRC of ICAI/June 2015

employed by foreign companies and they perform software related services there. As there is no transfer of property in goods [software] in both scenarios, it is not liable to sales tax. Service tax may also not be applicable, as services are done outside India.

9. Software Development outside India: The Indian company gets software development contract. Its engineers go abroad to render services on the foreign clients' site. There is no VAT/CST or service tax liability as the activities are done completely outside India.

The above models are merely indicative and there could be many more permutations and combinations. The indirect tax implications may need to be examined separately, depending on the activities done as per agreement between the parties.

Conclusion

In this article the paper writer has sought to examine the applicability of various taxes to software along with possible exemptions/exclusions. There is overlap between various levies and in absence of any clarity, the assessee may continue to pay multiple taxes, which would be finally borne by the end customer. It is hoped that under GST law, there would be some mechanism to ensure that taxes are not paid on more than 100% of base amount charged towards software by assessee.

For further clarifications host on [email protected] or [email protected].

EXPORT PROMOTION SCHEME UNDER FTP 2015-20: MEIS & SEIS CA. Swapnil [email protected]

Foreign Trade Policy 2015-20 is announced by Hon'ble Minister of stCommerce & Industry Mrs. Nirmala Sitharamonon 1 April 2015. In

New Foreign Trade Policy Government has also introduced Two New Export Promotion Scheme � Merchandise Exports from India Scheme (MEIS) & Service Exports from India Scheme (SEIS), in order to accelerate growth of Indian manufactures and Service provider who are exporting their goods and services to outside India and contributing inflow to Foreign Exchange in country.

Earlier in FTP 2009-14, there were many Export Promotion schemes having different criteria and conditions. However in FTP 2015-20, erstwhile five export promotions schemes w.r.t Exports of Goods are merged in to Merchandise Exports from India Scheme (MEIS). As well Served from India Scheme is replaced with Service Exports from India Scheme (SEIS) for Promoting Export of Services.

Applicability: Benefit under MEIS & SEIS is applicable for Exports undertaken from 1st April 2015

1) Merchandise Exports from India Scheme (MEIS): Benefit of MEIS is eligible to Export of Notified Goods and Export to Notified Market of such goods. Appendix 3B of Foreign Trade Policy 2015-20 gives list of Notified Goods, Specified Market & rate of reward on such goods. Rate of Reward under this scheme varies in the range of 2% to 5% on Realised FOB value of exports in free foreign exchange.

2) Service Exports from India Scheme (SEIS): Benefit of SEIS is eligible to Export of Notified Services as per appendix 3D of Foreign Trade Policy 2015-20. It is applicable to Service provider located in India and Service is to be provided from India to any other country or to consumer of any other country. Also Service provider should have active IEC Code at the time of rendering of services. Rate of Reward under this scheme varies in the range of 3% to 5% on Realised FOB

value of exports in free foreign exchange.

Some of Important provisions governing MEIS & SEIS is explained as under:

1) Nature of Reward: Rewards under MEIS & SEIS will be provided in the form of Duty Credit Scrip. Duty credit scrip can be used for payment of duties on goods procured domestical ly/ imported. Duty Credit Scr ip is freely transferable. Therefore if Exporter is not in position to use the Duty Credit Scrip, he can sold the same in open market.

2) Usage of Duty Credit Scrip: Duty Credit Scrip under MEIS & SEIS can be used for

Payment of Customs Duties for import of inputs or Capital goods, except items listed in Appendix 3A.

Payment of excise duties on domestic procurement of inputs or goods, including capital goods as per Department of notification.

Payment of service tax on procurement of services as per Department of Revenue notification.

Payment of Customs Duty and fee as per paragraph 3.18 of this Policy.

Procurement of Goods from Private/Public Bonded warehouse

3) Ineligible categories under MEIS: The Following exports categories/sectors shall be ineligible for Duty Credit Scrip under MEIS Scheme.

a) EOUs / EHTPs / BTPs/ STPs who are availing direct tax benefits; Supplies made from DTA units to SEZ, Deemed Exports, Exports made by units in FTWZ; SEZ/EOU /EHTP/BPT/FTWZ products expor ted through DTA units.

b) Export of imported goods covered under paragraph 2.46 of FTP; Goods which are restricted or prohibited for export

c) Exports through trans-shipment, Export products which are subject to Minimum export price or export duty.

d) Diamond Gold, Silver, Platinum, other precious metal in any form including plain and studded jewellery and other precious and semi-precious stones.

e) Products wherein precious metal/diamond are used or

10

Computers are magnificent tools for the realization of our dreams, but no machine can replace the human spark of spirit,

compassion, love, and understanding. - Louis Gerstner, CEO, IBM

News Letter Pune Branch of WIRC of ICAI/June 2015

Articles which are studded with precious stones.

f) Ores and concentrates of all types and in all formations, Red sanders and beach sand.

g) Crude / petroleum oil and crude / primary and base products of all types and all formulations.

h) Cereals of all types, Sugar of all types and all forms, Export of milk and milk products, Export of Meat and Meat Products.

4) Ine l ig ib le Categor y under SEIS : The Fo l lowing categories/sectors shall be ineligible for Duty Credit Scrip under SEIS Scheme:

a ) E x p o r t Tu r n o v e r o f u n i t s o p e r a t i n g u n d e r STPI/SEZ/EOU/EHTP/BTP schemes or supplies made to such units

b) Equity or dept participation, donations, receipt of repayment of loan

c) Foreign Exchange Remittance relating to Financial Service Sector : Raising of Foreign Curreny loan, Export proceeds realization of clients; Issuance of Foreign Equity through ADRs / GDRs or other similar instruments; Issuance of foreign currency Bonds; Sale of securities and other financial instruments; Other receivables not connected with services rendered by financial institutions

d) Foreign Exchange earned from Contract/Regular Employment abroad

e) Payments for services received from EEFC Account

f) Foreign exchange turnover by Healthcare Institutions and Educational Institution from equity participation, donations etc.

g) Foreign Exchange earnings for services provided by Airlines, Shipping lines service providers plying from any foreign country X to any foreign country Y routes not touching India at all.

h) Service providers in Telecom Sector.

i) Exports of Goods.

5) Cenvat Credit/Drawback: Cenvat Credit is available of ACD, BED, Service Tax paid through Duty Credit Script. Also drawback of the same can be claimed as per DOR Rules including drawback of BCD.

6) Benefit to Supporting Manufacturer: Supporting manufacturer can also claim rewards under MEIS subject to condition that he obtain Disclaimer Certificate from the company / firm who has realized the foreign exchange directly from overseas.

7) E-Commerce: MEIS Benefit is also available to Export of goods through courier or foreign post offices using E-Commerce, of goods notified in Appendix 3C. MEIS reward in such case is available on FOB value upto Rs. 25000 per consignment

8) Requirement of minimum NFE earning for SEIS: Service provider should have minimum Net Foreign Exchange earnings of US$15,000 in preceding financial year. For Individual Service Providers/Sole proprietorship, such minimum net free foreign exchange earnings criteria would be US$10,000 in preceding financial year.

In order to Boost �Make in India, Digital India and Skill India� campaign on Government, Ministry of Commerce and Industry has announced Foreign Trade Policy 2015-20. With new simplified Export Promotion Scheme MEIS & SEIS, government has definitely bring smile on face of Exporter. It is hoped that Industry and Business will take maximum benefit under these Scheme and thereby India's manufacturing/Service sector will boost which will increase their Exports and Foreign Exchange Reserves.

Net Foreign Exchange = Gross Earning of Foreign Exchange - Total Payment/Expenses in Foreign Exchange

(Note: If exporter is a manufacturer of goods as well as service provider, then the foreign exchange earnings and Total expenses / payment shall be taken into account for service sector only )

ARM'S LENGTH PRICE COMPUTATION - A NEW MILESTONE WITH FEW MORE BOUNDARIES CA. Meghnand M. [email protected]

With the intention of aligning transfer pricing regulations in India with international practices and reducing litigations on some of the repetitive issues considerably, Finance Minister of India, Mr. Arun Jaitley, in his Budget speech during July 2014, had announced the introduction of the 'range concept' for determining the arm's length price (ALP) and allowing the use of multiple year data for comparability analysis.

Consequently, section 92C(2) of the Income Tax Act, 1961 was amended to allow taxpayers to determine the ALP in relation to international transactions or specified domestic transactions (SDTs) in the prescribed manner. However, since then, there was no apparent clarity on the use of multiple year data or the range concept.

With the above backdrop, on 21 May 2015, the Central Board of Direct Taxes (CBDT) has released long awaited draft rules of the proposed application of range concept and use of multiple year data for computation of ALP. The draft rules are made open for public comments now.

Currently, the Income Tax Act, 1961, provides that when more than one price is determined using the most appropriate method, the arm's length price will be the arithmetic mean of such prices and the variation, if any,

should not exceed 1% for wholesale traders and 3% in other cases. Further, current rules require that the data to be used for determining an arm's length price compulsorily must pertain to the year in which the international transaction has been entered into, unless the taxpayer can provide evidences that the data for the prior two years has a bearing on the determination of transfer price. The above mechanism created significant issues for taxpayer, because some industries may be cyclical, prices are generally set based on the past year's data, and current-year data may not be available at the time preparing documentation.

The proposed mechanism and conditions released by the CBDT, under which 'multiple year data' and 'range computation' would be used for determination of ALP, shall be as under:

Multiple Year data

a. The multiple year data would be used only in cases where the method used for determination of ALP is Transactional Net Margin Method (TNMM), Resale Price Method (RPM) or Cost Plus Method (CPM); and

11

Any science or technology which is sufficiently advanced is indistinguishable from magic. - Arthur C. Clarke

News Letter Pune Branch of WIRC of ICAI/June 2015

b. The multiple year data should comprise three years including the current year i.e. (year in which transaction has been undertaken) and its use for above mentioned methods shall be mandatory;

c. In case of non-availability of data for 3 years for any of the following reasons: -

Data of the current year of the comparables may not be available on the databases at the time of filing of returns of income by taxpayers;

A comparable may fail to clear a quantitative filter in any one out of the three years; and

A comparable may have commenced operations only in the last two years or may have closed down operations during the current year.

Range Concept

a. The �range� concept shall be used only in cases where the method used for determination of ALP is TNMM, RPM or CPM;

b. A minimum of 9 entities are required to be selected as comparable entities for the tested party, based on the similarity of their functions, assets and risks (FAR) with that of the tested party;

c. 3-year data of these 9 entities (or more) would be considered and the weighted average of such 3-year data of each company would be used to construct the data set. In certain circumstances, data of 2 out of 3 years could also be used. Thus, the data set or series would have a minimum of 9 data points;

d. For calculating the weighted average, the numerator and denominator of the chosen Profit Level Indicator (PLI) would be aggregated for all the years for every comparable entity and the margin would be computed thereafter; and

e. The data points lying within the 40th to 60th percentile of the data set of series would constitute the range.

f. In case the transfer price of the tested party falls outside the range arrived at, the median of the range would be considered as the ALP.

g. There would not be a separate tolerance band once the range is allowed.

In cases where 'range' concept does not apply, the arithmetic mean concept would continue to apply in the same manner as it applied before the amendment to the income tax law along with benefit of tolerance range, which should not exceed 1% for wholesale traders and 3% in other cases.

It is worthwhile to note that use of range application and multiple year data for determination of ALP is a prevalent mechanism internationally. The OECD guidelines 2010 advocates the use of multiple year data in paragraph 3.77 as under:

"Multiple year data will be useful in providing information about the relevant business and product life cycles of the comparables. Differences in business or product life cycles may have a material effect on transfer pricing conditions that needs to be assessed in determining comparability. The data from earlier years may show whether the independent enterprise engaged in a comparable transaction was affected by comparable economic conditions in a comparable manner, or whether different conditions in an earlier year materially affected its price or profit so that it should not be used as a comparable."

Similarly, the OECD guidelines 2010 also advocates the use of range concept in paragraph 3.57 as under:

�It may also be the case that, while every effort has been made to exclude points that have a lesser degree of comparability, what is arrived at is a range of figures for which it is considered, given the process used for selecting comparables and limitations in information available on comparables, that some comparability defects remain that cannot be identified and/or quantified, and are therefore not adjusted. In such cases, if the range includes a sizeable number of observations, statistical tools that take account of central tendency to narrow the range (e.g. the inter quartile range or other percentiles) might help to enhance the reliability of the analysis.''

Moreover, the concept of inter-quartile range is generally practised in countries such as Australia, Denmark, France, Germany, Italy, Korea, Netherlands, Spain, Sweden, the United Kingdom, the USA ,etc. However, there are certain divergences between the rules proposed by CBDT and the practices in other developed and developing countries, which are as under:

1. There is no such specification in the OECD guidelines or in other country regulations for the use of multiple year data and range concepts, while applying specific benchmarking methods � TNMM, RPM or CPM. In the proposed rules, the range benefit is not made applicable to the genuine cases where sufficient comparable transactions are available and related party transactions are benchmarked using Comparable Uncontrolled Price (CUP) method.

2. There is no such guideline which restricts the use of range concept on the basis of number of comparables to be selected as comparable entities of the tested party. For example, as per the US transfer pricing guidelines no adjustment will be made to taxpayer transfer pricing results if those results are within and arm's length range derived from two or more comparable uncontrolled transactions.

3. It is important to note that the inter-quartile range prescribed in the draft rules released by the CBDT is 40th to 60th percentile of the data set of series. On the other hand, it is pertinent to note that the inter-quartile range internationally practised is 25th to 75th percentile of the results.

4. Also, regarding the requirement of minimum 9 comparables, there are industries in India such as manufacturing, specific services etc. wherein it would be difficult for the Indian taxpayer to identify a good comparable set comprising of 9 or more comparable companies. Therefore, these companies would be deprived from the benefit of applying the range concept while determining the ALP.

5. The proposed rules are restricting the range benefit to 40th - 60th percentile of the data set of series as compared to the 25th - 75th percentile of the results, which is typically practised internationally.

Nevertheless, the application of �arm's length range� and �use of multiple year data� concepts are constructive and will go a long way in reducing transfer pricing litigations surrounding these issues in India. Regarding some of the concern areas as aforesaid, taxpayers and consultant communities should submit their comments and suggestions to the CBDT and it is also expected from the CBDT side that they will share the thought process / supporting research carried out while introducing such restricting conditions. All in all, this is an interesting phase in Indian transfer pricing space.

12

Never let a computer know you're in a hurry. - Anonymous

News Letter Pune Branch of WIRC of ICAI/June 2015

BLACK MONEY ACT TO BRING ACHE DIN!! CA. Mrudula S. [email protected]

To unearth the black money stashed overseas, the Black Money (Undisclosed Foreign Income and Assets) and Imposition of Tax Act, 2015('The Act') received President's assent on 26 May 2015 and the same has now been enacted. "The world is no longer willing to tolerate tax havens which thrive in secrecy," stated the Finance Minister just before the Bill was approved. He said the government is also trying to squeeze out black money being parked in property and gold, without causing any shock.

Stated below are few things one must know about the Act:

Effective date:

The Act shall come into force on 1 April 2016 i.e., tax year2015-16.

Tax payers covered:

The Act will be applicable to all tax payers who are resident in India as per the provisions of the Income- tax Act. The Act however, excludes category of �resident but not ordinarily resident� from its ambit.

Scope of the Act:

The Act proposes to include undisclosed foreign income/asset which is defined to mean: (a) undisclosed income from source located outside India, and (b)value of undisclosed asset (including financial interest in any entity) located outside India which is held in the name of the taxpayer/where the taxpayer is a beneficial owner.

Undisclosed foreign income/value of undisclosed foreign assets shall be taxable at30% on gross basis i.e. without any benefit deduction/allowance/set of losses as provided under the Income- tax Act.

Foreign income shall be considered as�undisclosed� if the same is not reported in the return of income (ROI) of the relevant year, or in respect of which ROI was to be furnished, but was not filed within the stipulated time under the provisions of Income- tax Act. Foreign asset is �undisclosed� if the taxpayer is not able to explain the source of investment in such asset or explanation offered, in the tax authority's opinion, is not satisfactory.

Undisclosed foreign asset will be chargeable to tax on the basis of fair market value, which will be determined in accordance with the prescribed rules and the same will be taxable in the year in which it comes to the notice of the tax authorities.

Assessment

ROI is not required to be filed under the Act. The Act calls for direct assessment of undisclosed foreign income/asset on the basis of information received from any sources. In such a case, the Act imposes to follow the principles of natural justice, such as, issue of notice, granting an opportunity of hearing to taxpayer, furnishing documentary evidences etc.

Subsequent thereto, the tax authority is required to pass a final order, in writing with in two years from the end of tax year in which the notice was issued.

The Act states remedial measures such as appeal etc. along the lines of the provisions of the Income-tax Act. The Act also lays down guidelines on rectification / revision of tax authority's orders, provisions for recovery for arrears etc.

Interest levy

Interest shall be levied if ROI has not been furnished, or in case of default on

compliance with advance tax liability under the provisions of the Income-tax Act, in relation to the undisclosed foreign income.

Penalties and prosecution:

The Act mentions stringent provisions with respect to penalties of upto 300% of tax determined and criminal prosecution which could result in up to 10 years of imprisonment, depending on the severity of the offence.

Heavy penalty of 10 Lakh rupees shall be payable if any resident person fails to file the ROI who, at any time during the year, held/ had beneficial interest in any overseas assets (including financial interest in any entity or earned income from source outside India. Also, it has now been made clear that the penal provisions will not be applicable to those having aggregate balance equivalent to 5 lakh rupees in all bank accounts abroad.

Additional penalties could be levied based on the amounts involved and the proposed legislation indicates that prosecution may not be 'compounded', which means a payment cannot be made in order to avoid prosecution.

One time window for compliance

The Act provides for a one time limited period opportunity for taxpayers to declare any undisclosed foreign income/asset which he has acquired from income chargeable to tax under the provisions of the Income-tax Act.

The Taxpayer will need to file declaration in prescribed form before the specified tax authority within a stipulated time period, and pay tax at 30% of the value of asset, and an equal amount of penalty. In such cases, no prosecution proceedings will be initiated. Such person will enjoy exemption from levy of wealth tax for past years in relation to the declared assets.

The Taxpayer is not eligible for one time declaration (a) if in relation to the undisclosed foreign asset including (bank account whether having any balance or not) located outside India, any proceeding under the provision of the Act is pending for any past year; or (b) where information in respect of such assets has been received by competent authority from other country under an agreement, or (c)prosecution proceedings have been initiated under certain specific statutes.

Tax experts fear that there has been no statutory amendment to address concerns to protect bonafide cases of returning non- residents or expatriates and their family members from rigour of the provisions of the Act. The relief is in the form of statement of FM that Innocent taxpayers like NRIs, students, professionals, taxpayers who regularly travel abroad will not be targeted. One will have to wait for CBDT to come up with clarifications providing adequate guidelines to protect these cases. Further, in the context of one time voluntary declaration facility, one will have to wait for the notification of rules and forms and the available window period and specified due date.

It is now for the government to ensure that the new laws are implemented transparently and are not applied selectively through misuse of the implementation machinery.

Indeed, after this assault on black money held abroad begins to bear fruit, due attention needs to be given to tax evasion within the country which is an equally big menace. If all goes well, together all this would be a big feather in the Modi government's cap and shall bring Ache Din for Indians!!

13

Rules of technology: The first rule of any technology used in a business is that automation applied to an efficient operation will magnify the efficiency. The second is that

automation applied to an inefficient operation will magnify the inefficiency-Bill Gates

News Letter Pune Branch of WIRC of ICAI/June 2015

PROCEDURE FOR OBTAINING REFUND OF EXCESS DUTY PAID IN THE SELF ASSESSMENT ERA UNDER CUSTOMS REGULATIONS

CA. Atish [email protected]

14

Introduction

The Central Indirect Regulations such as Central Excise and Service Tax have adopted the self assessment mechanism long back wherein the revenue authorities have no role to play at the time of clearance of goods or rendition of service. However, the Central Government has taken more than a decade to introduce the same self assessment mechanism under the Customs Regulations.

In the recent past, the self assessment mechanism was introduced w.e.f. 08.04.2011 under the Customs Regulation considering the time consumed in assessing each and every bill of entry and the delay caused to the importer in clearance of the consignments. Accordingly, the importer of the goods can file a bill of entry under Section 17(1) of the Customs Act, 1962 based on the self assessment without any intervention of the proper officer of customs.

However, while introducing self assessment mechanism under Customs Regulations only the provisions of Section 17 have undergone a change to give effect and the corresponding relevant provisions under Section 47 of the Customs Act, 1962 have been retained as such without any amendment in line with the amendment in Section 17(1). Therefore, even still today an importer even under self assessment mechanism has to obtain an out of charge order from a proper officer of customs under Section 47 of Customs Act, 1962 as it was required prior to self assessment mechanism.

Therefore, a question arises whether the self assessment introduced under the Customs Regulations is really a self assessment in complete sense or it is an assessment made by the importer or assessment made by customs authorities?

In this regard, one can argue that the order passed under Section 47 is merely a clerical/administrative order in as much as he is merely ensuring that the duty is paid properly as per the assessment of bill of entry and the prohibited goods are not cleared by the importers. Hence, the proper officer giving out of charge for the imported goods is not validating the assessment done by the importer under Section 17(1). Hence the said bill of entry is not an order of a proper officer.

In this regard, the Hon'be High Court of Madras in case of Best & Crompton Engineering [1997 (93) ELT 21 (Mad)] has held that the order passed under Section 47 is not merely a clerical/administrative order but is a quasi judicial order. Further the said view of Hon'ble High Court was further agreed by the Hon'ble High Court of Kerala in case of Arvind Export (P) Ltd. [2010 (253) ELT A81 (Ker)].

Therefore, as per the provisions of Section 17(1) read with Section 47 of Customs Act, 1962, a self assessed bill of entry becomes and order of proper officer and can be appealed against appellate authorities.

Obtaining refund of excess duty paid under self assessment

As discussed above, even under self assessment era, the self assessed bill of entry would amount to order passed by proper officer, the refund of erroneous duty paid would be available only by getting the said order of proper officer set aside by appropriate appellate authority as per the decision of Hon'ble Supreme Court in case of Priya Blue Industries Ltd. [2004 (172) ELT 145 SC].

However, recently it was observed that an appeal filed by an importer against an erroneous self assessed bill of entry filed under amended Section 17(1) has been rejected by the Commissioner (Appeals), Mumbai only on the ground that the self assessed bill of entry filed under Section 17(1) is not an order passed by a proper officer of customs. Therefore, the appeal against the self assessed bill of entry is not maintainable before the Commissioner (Appeals) under Section 128 in as much as self assessed bill of entry is not an appealable order.

Therefore, an importer has option to file an application for amendment under Section 149 of the Customs Act, 1962 to rectify any mistake in the bill of entry based on the documents available at the time of importation. Further the Section 149 does not prescribe any time limit within which the importer has to file an application for amendment. Therefore, the importer can file an application for amendment as and when noticed by the importer.

However, it is observed that the applications of the importer for seeking amendment in the bill of entry under Section 149 are not entertained by the officer of customs and they take a lot of time to pass an order either allowing or rejecting the application of the importer. Based on the outcome of the order of the customs officer under Section 149 the importer can file a refund claim in case the application is allowed or in case of an order passed rejecting the amendment in the bill of entry, the importer will have to pursue the appellate remedy as prescribed under the Customs Regulations against the said rejection order.

Further, assuming the interpretation of the Commissioner (Appeals), Mumbai is correct and no appeal maintainable against the self assessed bill of entry, the importer can directly file a refund claim of excess duties paid on account of erroneous bill of entry without challenging the self assessed bill of entry. In such cases, the refund claim may be allowed by the customs officer in light of the decision of Hon'ble Delhi High Court in case of Aman Medical Products Ltd. [2010 (250) ELT 30 (Del)].

Conclusion

Considering above said 3 alternatives for obtaining refund and no clarity as to which is most appropriate and fastest way to obtain the refund of excess customs duties paid by the importer erroneously.

ANNOUNCEMENTThe Committee on Financial Markets and Investor's Protection (CFM&IP) of ICAI conducts

Certificate Course on Forex and Treasury Management (FXTM) in Pune.

Schedule of Classes: 8/9, 22/23 Aug, 5/6, 19/20 Sept & 3 Oct 2015

Members of Institute of Chartered Accountants of India (ICAI) and the Students who have passed the CA Final Examination are eligible to pursue this Course.

Registration is open on first come first serve basis. Few Seats Left. Please

register early. Classes will be held on alternative weekends: Saturday from 2.00 p.m. to

7.00 p.m. | Sunday from 9.00 a.m. to 2.00 p.m. Course fee: Rs. 17,500/- per member ( including course material, snacks

and examination fee for the first attempt) For more information, updates and for making online payment

please visit: http://www.icai.org/post.html?post_id=3552&c_id=266

Details are as follows:

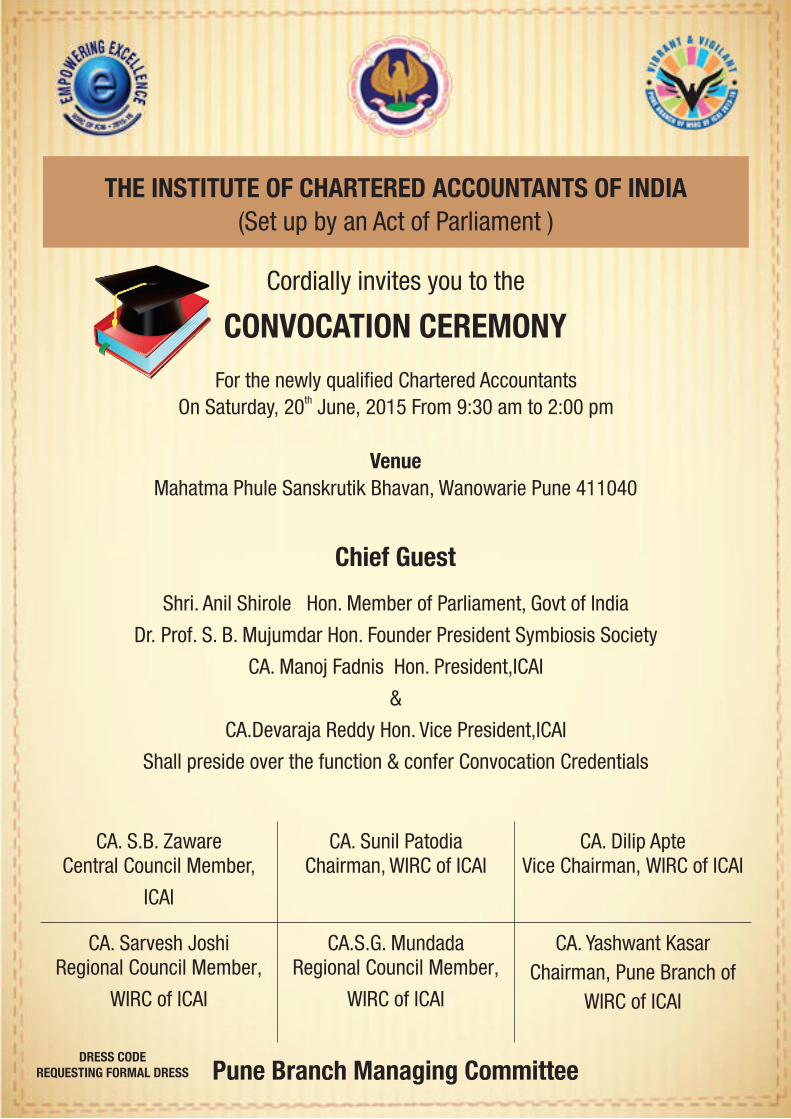

THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA(Set up by an Act of Parliament )

Cordially invites you to the

CONVOCATION CEREMONYFor the newly quali�ed Chartered Accountants

thOn Saturday, 20 June, 2015 From 9:30 am to 2:00 pm

VenueMahatma Phule Sanskrutik Bhavan, Wanowarie Pune 411040

Chief GuestShri. Anil Shirole Hon. Member of Parliament, Govt of India

Dr. Prof. S. B. Mujumdar Hon. Founder President Symbiosis Society

CA. Manoj Fadnis Hon. President,ICAI

&

CA.Devaraja Reddy Hon. Vice President,ICAI

Shall preside over the function & confer Convocation Credentials

CA. S.B. ZawareCentral Council Member,

ICAI

CA. Sunil PatodiaChairman, WIRC of ICAI

CA. Dilip ApteVice Chairman, WIRC of ICAI

CA. Sarvesh JoshiRegional Council Member,

WIRC of ICAI

CA.S.G. MundadaRegional Council Member,

WIRC of ICAI

CA. Yashwant KasarChairman, Pune Branch of

WIRC of ICAI

Pune Branch Managing CommitteeDRESS CODEREQUESTING FORMAL DRESS

Information technology and business are becoming inextricably interwoven. I don't think anybody can talk meaningfully about one without the talking

about the other-Bill Gates

News Letter Pune Branch of WIRC of ICAI/June 2015

u laat tr ig on nso !!C !u laat tr ig on nso !!C !

CA. Prakash Kulkarni(Corporate Social Responsibility)

CA. B. M. Pensalwar (Co- Operative Society, Maharashtra)

CA. Manish Toshniwal(Library)

CA. C. D. Upasani(Make in India Initiative)

CA. Chandak Anand S(Administration & Co-ordination)

CA. Vishnu Bangad(Study Circle Co-ordination)

CA. Malkar Prasad(Corporate & Alled Laws)

CA. Bhattad Vishal(Swachha Bharat Abhiyan)

CA. Nandkishor Malani(Branch Co-ordination)

CA. Rajesh Agrawal(Corporate Social Responsibility)

CA. Yogesh Poddar(Grievances)

CA. Suhas Deshpande(CPE)

CA. Dinesh Gandhi(Co-Operative Society, Maharashtra)

CA. Balasaheb Ekatpure(Accounting standards

for Local Bodies)

CA. Akshay Oke(IND AS - IFRS)

CA. Tarun Lohia(Information Technology)

CA. Vishnu Bhutada(Corporate Social Responsibility)

CA. Bankhele Vikas(International Taxation)

CA. Ashokkumar N.Pagariya(Students Committee)

PUNE MEMBERS CO-OPTED ON WIRC COMMITTEES

16

CA. Subodh Shah(International Taxation)

CA. C. V. Chitale(Capacity Building for Members in Practice)

CA. Nachiket Deo(Ind AS (IFRS) Implementation)

CA. Parag V. Kulkarni(Young Members Empowerment)

CA. Khushbu Jain(State Task Force of WomenMembers Empowerment)

PUNE MEMBERS CO-OPTED ON ICAI COMMITTEES

The new information technology... Internet and e-mail... have practically eliminated the physical costs of communications-Peter Drucker

News Letter Pune Branch of WIRC of ICAI/June 2015

WELL FURNISHED & AIR CONDITIONED OFFICE FOR SALE / RENT IN SADASHIV PETH

Area : 1350 Sq Feet Carpet area

Keshav Prasad Housing Society730, Sadashiv Peth, Kumthekar Road

Pune - 411030Contact Person: Mr. Nitin Shah | Mobile No: 9822044166

17

CA. Sarvesh JoshiRegional Council Member

WIRC

We Congratulate CA. Sarvesh Joshi,Regional Council Member, WIRC

for being Co-Opted as Technical Director of Suvarnayug Sahakari Bank Ltd. Pune

CA. Radhesham Agrawal(Student Co-Ordinator)

CA. Anand Jakhotiya(Chairman, Pune Branch of WICASA)

Pravin Babar(Joint Editor, Pune WICASA)

Vaibhav R. Pingale(Vice-Chairman, Pune WICASA)

Anchila T. Ojha(Secretary, Pune WICASA)

Anand Gupta(Treasurer, Pune WICASA)

Rupendra N. Tholiya(Joint Secretary, Pune WICASA)

PUNE WICASA MANAGING COMMITTEE 2015 - 16

CA. Sunil R. Karbhari(Accounting Standards for Urban Local Bodies)

CA. Khushbu Jain(Young Member Empowerment

Committee)

PUNE MEMBERS CO-OPTED IN SUB GROUPS OF WIRC

Information technology has been one of the leading drivers of globalization, and it may also become one of its major victims-Evgeny Morozov

News Letter Pune Branch of WIRC of ICAI/June 2015

CA. Dilip SatbhaiSpeaker- Lecture meet on Foreign

Contribution Regulation Act

CA. Bhupendra BhandariSpeaker- Lecture meet on "Professional

Opportunity as Insurance surveyor & Loss Assessor"

CA. Sandeep BaldavaSpeaker- Lecture Meet on "Forensics/Fraud

Investigation"

CA.C.D.UpasaniSpeaker

CA.Vishwajeet HonapSpeaker

CA. Harshvardhan PatilSpeaker

SERIES OF LECTURE MEETS ON IFRS

DIRECT TAXES' REFRESHER COURSE (DTRC) -2015

SEMINAR ON INCOME COMPUTATION AND DISCLOSURE STANDARDS (ICDS)

CA. Chetan DagaSpeaker

CA. Pritam MahureSpeaker- Lecture Meet on the

"Service Tax input Credits"

CA. Nilesh KhandelwalSpeaker

CA. Kusai GoawalaSpeaker- Lecture Meet for CA

Members- CARO under Companies Act-2013

Inaugural CA. Amey KunteSpeaker

CA. Tarun GhiaSpeaker

18

It's hard to pay attention these days because of multiple effects of the information technology nowadays. You tend to develop a faster, speedier mind,

but I don't think it's necessarily broader or smarter-Robert Redford

News Letter Pune Branch of WIRC of ICAI/June 2015

GRIEVANCE REDRESSAL FORUM MEETING WITH WIRC OFFICIALS

CA. Sagar ShahSpeaker

CA. Rupal HariaSpeaker

CA. Jatin LodayaSpeaker

"Educational visit of Chartered Accountants studentsNational Research Centre for Grapes�

Industrial visit of Chartered Accountants studentsat John Deere Factory

WORKSHOP ON PRACTICE DEVELOPMENT SKILLS

Yogasana and Pranayam Classes

19