pulsar II investment insurance planprdlib.convoy.com.hk/prdportal/File/Product and Provider... ·...

53

pulsar II investment insurance plan Product Handbook For Internal Use Only

Transcript of pulsar II investment insurance planprdlib.convoy.com.hk/prdportal/File/Product and Provider... ·...

pulsar II investment insurance planProduct Handbook

For Internal Use Only

Pulsar II Investment Insurance Plan

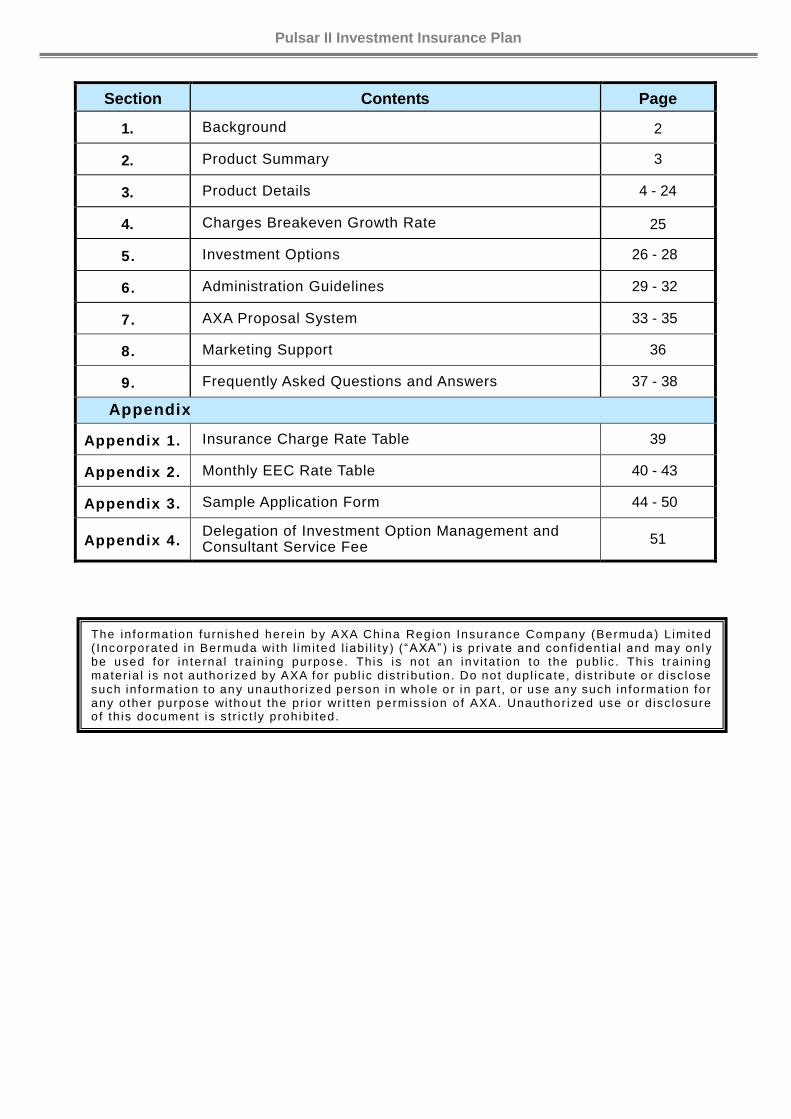

Section Contents Page

1. Background 2

2. Product Summary 3

3. Product Details 4 - 24

4. Charges Breakeven Growth Rate 25

5. Investment Options 26 - 28

6. Administration Guidelines 29 - 32

7. AXA Proposal System 33 - 35

8. Marketing Support 36

9. Frequently Asked Questions and Answers 37 - 38

Appendix

Appendix 1. Insurance Charge Rate Table 39

Appendix 2. Monthly EEC Rate Table 40 - 43

Appendix 3. Sample Application Form 44 - 50

Appendix 4. Delegation of Investment Option Management and Consultant Service Fee

51

The in format ion furn ished here in by AXA China Region Insurance Company (Bermuda) L imi ted ( Incorporated in Bermuda wi th l imi ted l iab i l i t y) ( “AXA”) is pr ivate and con f ident ia l and may only be used for in ternal t ra in ing purpose. This is not an invi ta t ion to the publ ic . Th is t ra in ing mater ia l is no t author i zed by AXA for publ ic d is t r ibut ion. Do not dupl icate, d is t r ibute or d isc lose such in format ion to any unauthor i zed person in whole or in par t , or use any such in format ion for any other purpose wi thout the pr ior wr i t ten permiss ion of AXA. Unauthor i zed use or d isc losure of th is document is s t r ic t ly prohib i ted.

Pulsar II Investment Insurance Plan

All information is for internal use and reference only P.2, total 51 pages

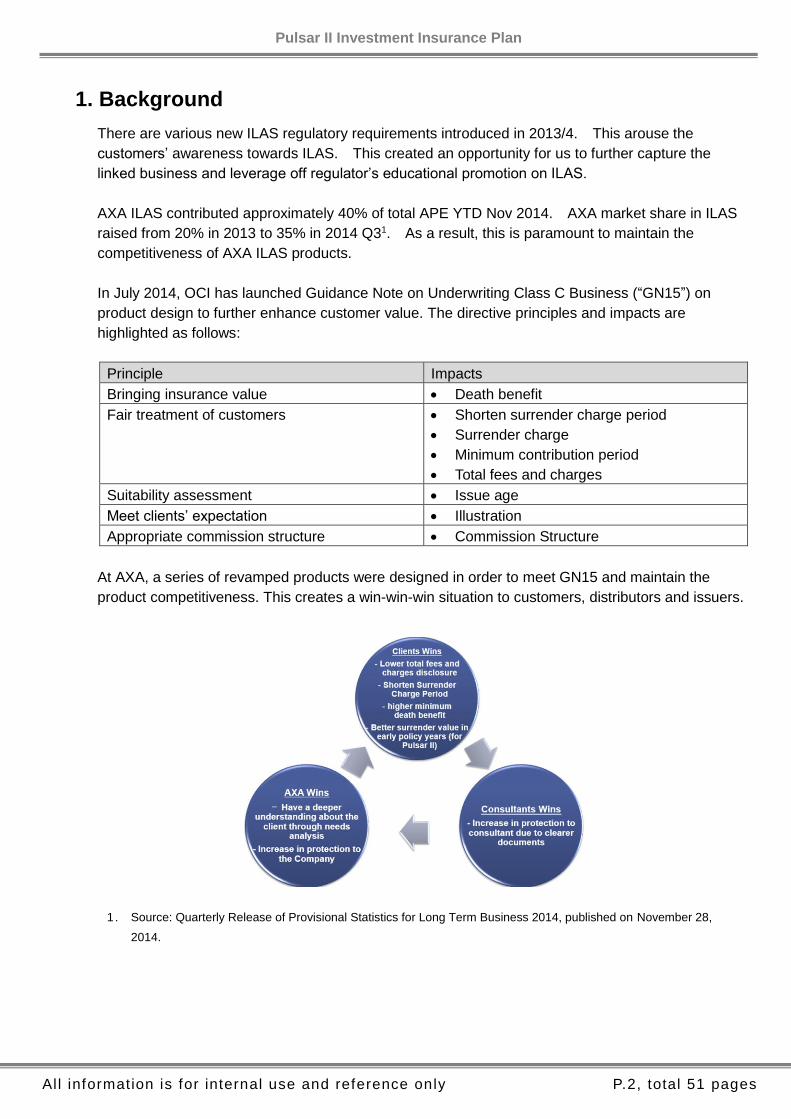

1. Background

There are various new ILAS regulatory requirements introduced in 2013/4. This arouse the

customers’ awareness towards ILAS. This created an opportunity for us to further capture the

linked business and leverage off regulator’s educational promotion on ILAS.

AXA ILAS contributed approximately 40% of total APE YTD Nov 2014. AXA market share in ILAS

raised from 20% in 2013 to 35% in 2014 Q31. As a result, this is paramount to maintain the

competitiveness of AXA ILAS products.

In July 2014, OCI has launched Guidance Note on Underwriting Class C Business (“GN15”) on

product design to further enhance customer value. The directive principles and impacts are

highlighted as follows:

Principle Impacts

Bringing insurance value Death benefit

Fair treatment of customers Shorten surrender charge period

Surrender charge

Minimum contribution period

Total fees and charges

Suitability assessment Issue age

Meet clients’ expectation Illustration

Appropriate commission structure Commission Structure

At AXA, a series of revamped products were designed in order to meet GN15 and maintain the

product competitiveness. This creates a win-win-win situation to customers, distributors and issuers.

1. Source: Quarterly Release of Provisional Statistics for Long Term Business 2014, published on November 28,

2014.

Pulsar II Investment Insurance Plan

All information is for internal use and reference only P.3, total 51 pages

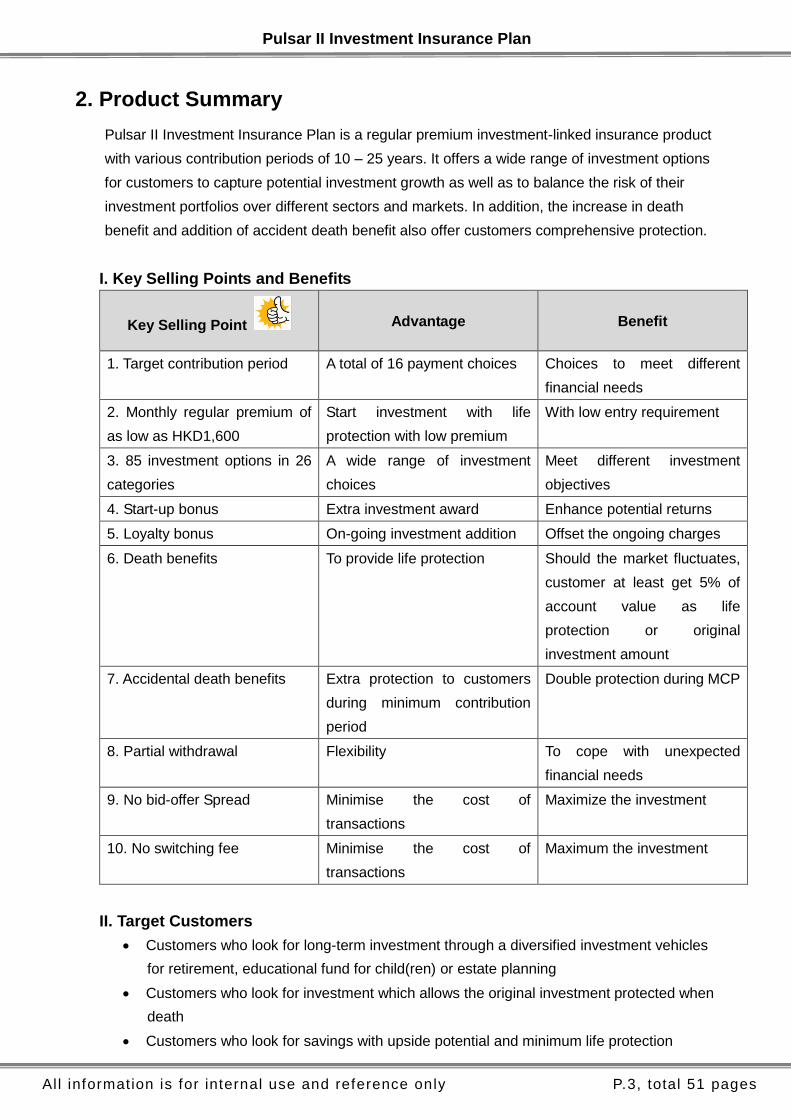

2. Product Summary

Pulsar II Investment Insurance Plan is a regular premium investment-linked insurance product

with various contribution periods of 10 – 25 years. It offers a wide range of investment options

for customers to capture potential investment growth as well as to balance the risk of their

investment portfolios over different sectors and markets. In addition, the increase in death

benefit and addition of accident death benefit also offer customers comprehensive protection.

I. Key Selling Points and Benefits

Key Selling Point Advantage Benefit

1. Target contribution period A total of 16 payment choices Choices to meet different

financial needs

2. Monthly regular premium of

as low as HKD1,600

Start investment with life

protection with low premium

With low entry requirement

3. 85 investment options in 26

categories

A wide range of investment

choices

Meet different investment

objectives

4. Start-up bonus Extra investment award Enhance potential returns

5. Loyalty bonus On-going investment addition Offset the ongoing charges

6. Death benefits To provide life protection Should the market fluctuates,

customer at least get 5% of

account value as life

protection or original

investment amount

7. Accidental death benefits Extra protection to customers

during minimum contribution

period

Double protection during MCP

8. Partial withdrawal Flexibility To cope with unexpected

financial needs

9. No bid-offer Spread Minimise the cost of

transactions

Maximize the investment

10. No switching fee Minimise the cost of

transactions

Maximum the investment

II. Target Customers

Customers who look for long-term investment through a diversified investment vehicles

for retirement, educational fund for child(ren) or estate planning

Customers who look for investment which allows the original investment protected when

death

Customers who look for savings with upside potential and minimum life protection

Pulsar II Investment Insurance Plan

All information is for internal use and reference only P.4, total 51 pages

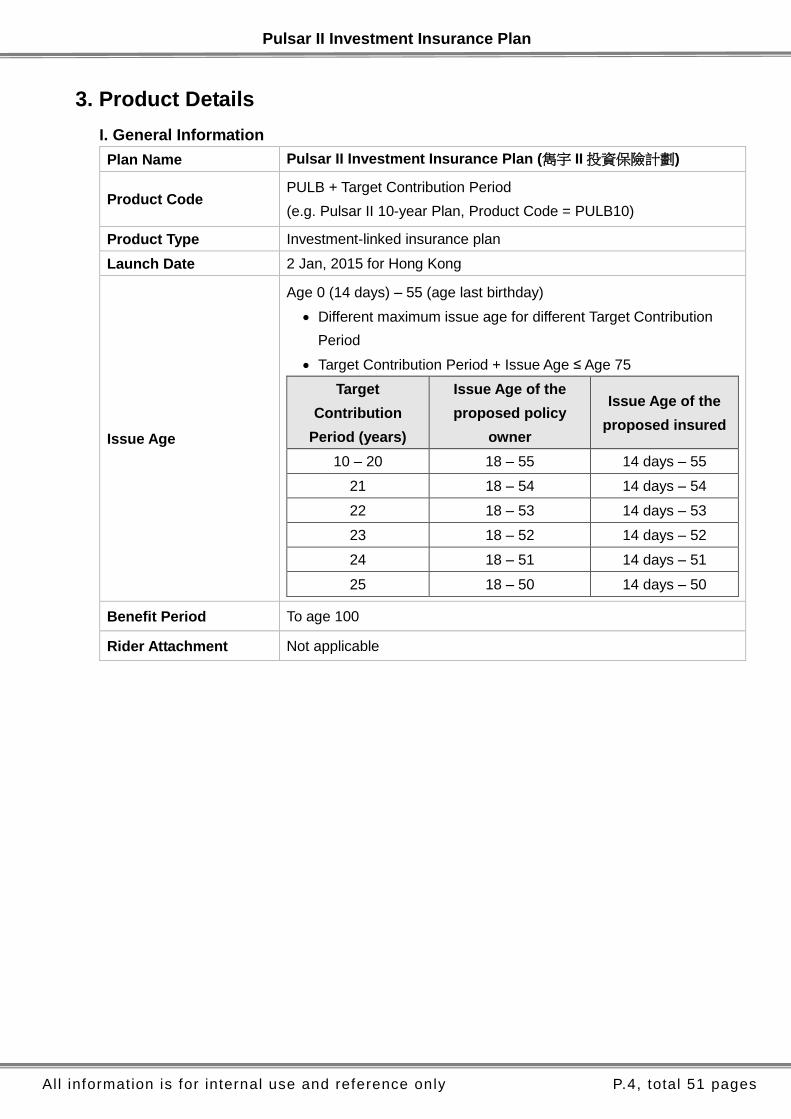

3. Product Details

I. General Information

Plan Name Pulsar II Investment Insurance Plan (雋宇 II 投資保險計劃)

Product Code PULB + Target Contribution Period

(e.g. Pulsar II 10-year Plan, Product Code = PULB10)

Product Type Investment-linked insurance plan

Launch Date 2 Jan, 2015 for Hong Kong

Issue Age

Age 0 (14 days) – 55 (age last birthday)

Different maximum issue age for different Target Contribution

Period

Target Contribution Period + Issue Age ≤ Age 75

Target

Contribution

Period (years)

Issue Age of the

proposed policy

owner

Issue Age of the

proposed insured

10 – 20 18 – 55 14 days – 55

21 18 – 54 14 days – 54

22 18 – 53 14 days – 53

23 18 – 52 14 days – 52

24 18 – 51 14 days – 51

25 18 – 50 14 days – 50

Benefit Period To age 100

Rider Attachment Not applicable

Pulsar II Investment Insurance Plan

All information is for internal use and reference only P.5, total 51 pages

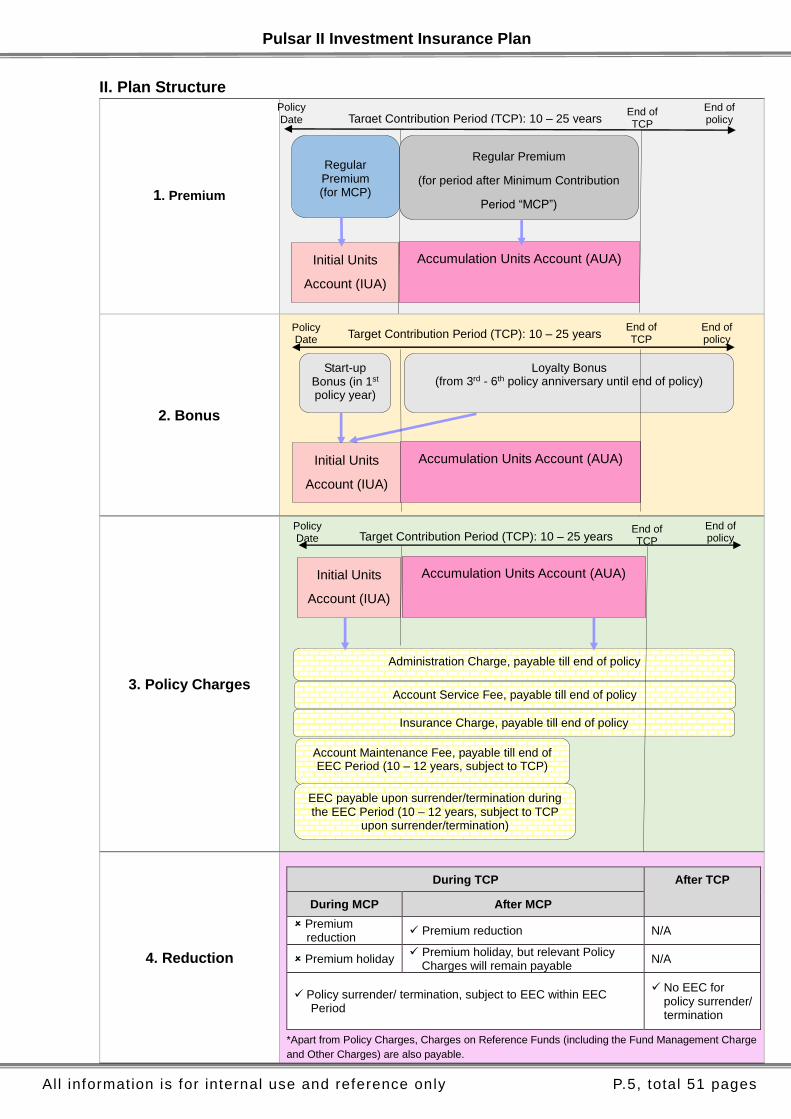

II. Plan Structure

1. Premium

2. Bonus

3. Policy Charges

4. Reduction

*Apart from Policy Charges, Charges on Reference Funds (including the Fund Management Charge

and Other Charges) are also payable.

During TCP After TCP

During MCP After MCP

Premium reduction

Premium reduction N/A

Premium holiday Premium holiday, but relevant Policy

Charges will remain payable N/A

Policy surrender/ termination, subject to EEC within EEC Period

No EEC for policy surrender/ termination

Initial Units

Account (IUA)

Target Contribution Period (TCP): 10 – 25 years

Regular Premium

(for period after Minimum Contribution

Period “MCP”)

End of TCP

Regular Premium (for MCP)

End of policy

Policy Date

Accumulation Units Account (AUA)

Policy Date

Start-up Bonus (in 1st policy year)

Loyalty Bonus (from 3rd - 6th policy anniversary until end of policy)

Target Contribution Period (TCP): 10 – 25 years End of TCP

End of policy

Initial Units

Account (IUA)

Accumulation Units Account (AUA)

Administration Charge, payable till end of policy

Account Service Fee, payable till end of policy

Insurance Charge, payable till end of policy

Account Maintenance Fee, payable till end of EEC Period (10 – 12 years, subject to TCP)

EEC payable upon surrender/termination during the EEC Period (10 – 12 years, subject to TCP

upon surrender/termination)

Target Contribution Period (TCP): 10 – 25 years

Initial Units

Account (IUA)

Accumulation Units Account (AUA)

Policy Date

End of TCP

End of policy

Pulsar II Investment Insurance Plan

All information is for internal use and reference only P.6, total 51 pages

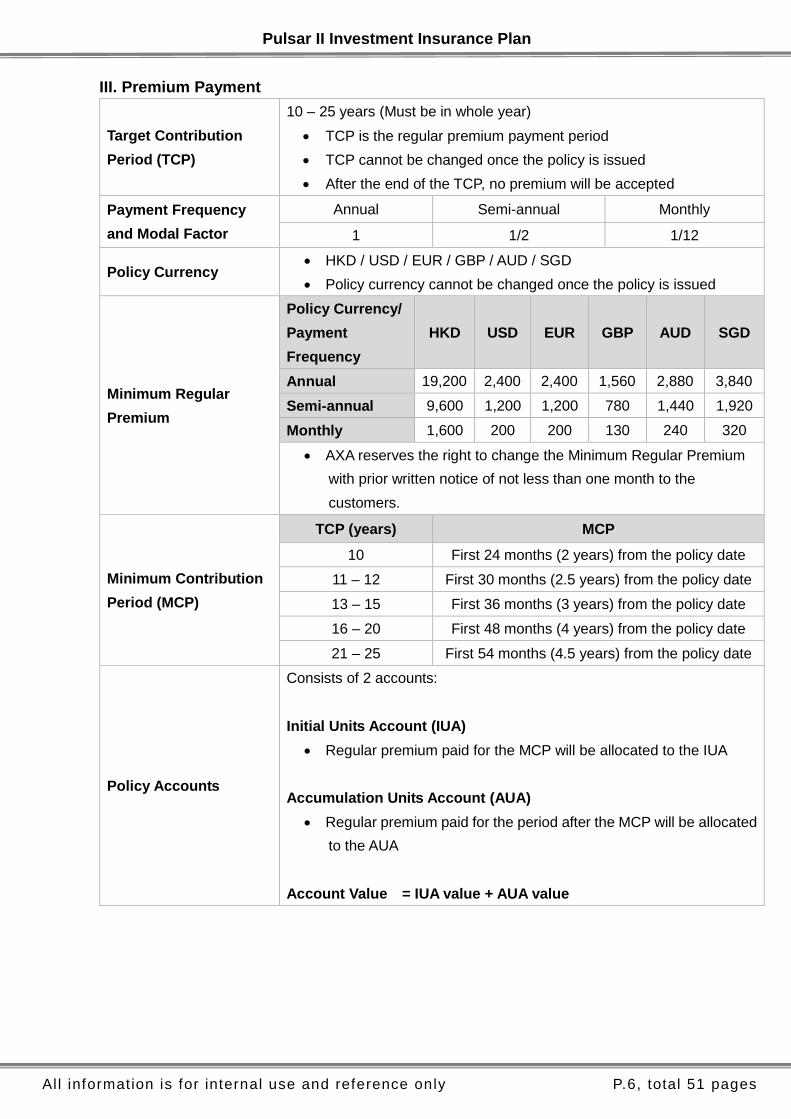

III. Premium Payment

Target Contribution

Period (TCP)

10 – 25 years (Must be in whole year)

TCP is the regular premium payment period

TCP cannot be changed once the policy is issued

After the end of the TCP, no premium will be accepted

Payment Frequency

and Modal Factor

Annual Semi-annual Monthly

1 1/2 1/12

Policy Currency HKD / USD / EUR / GBP / AUD / SGD

Policy currency cannot be changed once the policy is issued

Minimum Regular

Premium

Policy Currency/

Payment

Frequency

HKD USD EUR GBP AUD SGD

Annual 19,200 2,400 2,400 1,560 2,880 3,840

Semi-annual 9,600 1,200 1,200 780 1,440 1,920

Monthly 1,600 200 200 130 240 320

AXA reserves the right to change the Minimum Regular Premium

with prior written notice of not less than one month to the

customers.

Minimum Contribution

Period (MCP)

TCP (years) MCP

10 First 24 months (2 years) from the policy date

11 – 12 First 30 months (2.5 years) from the policy date

13 – 15 First 36 months (3 years) from the policy date

16 – 20 First 48 months (4 years) from the policy date

21 – 25 First 54 months (4.5 years) from the policy date

Policy Accounts

Consists of 2 accounts:

Initial Units Account (IUA)

Regular premium paid for the MCP will be allocated to the IUA

Accumulation Units Account (AUA)

Regular premium paid for the period after the MCP will be allocated

to the AUA

Account Value = IUA value + AUA value

Pulsar II Investment Insurance Plan

All information is for internal use and reference only P.7, total 51 pages

Reducing / Increasing

Regular Premium

Reducing Regular Premium:

Allowed after the MCP, customers may reduce the regular premium

to no less than the Minimum Regular Premium

Increasing Regular Premium:

Allowed only if the regular premium has been reduced, customer

may increase it back up to the original regular premium amount

committed at policy issuance

Application for increasing regular premium will be subject to the

underwriting requirements and administrative rules

Except the condition above, customers cannot increase regular

premium. However, customers can apply for a new Pulsar II

policy to increase the regular premium

Important Note

Reduction in regular premium will lead to loss of entitlement to the

Loyalty Bonus and reduction in the Account Value and further lead

to reduction in any applicable Loyalty Bonus

Pulsar II Investment Insurance Plan

All information is for internal use and reference only P.8, total 51 pages

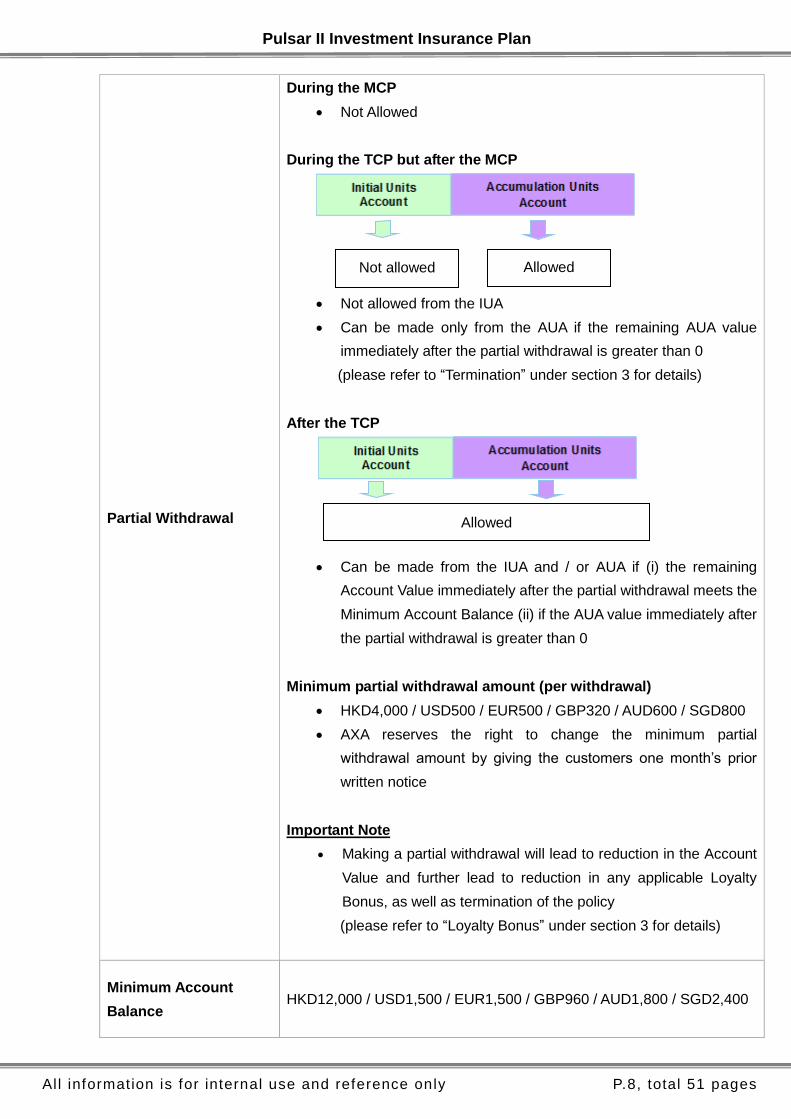

Partial Withdrawal

During the MCP

Not Allowed

During the TCP but after the MCP

Not allowed from the IUA

Can be made only from the AUA if the remaining AUA value

immediately after the partial withdrawal is greater than 0

(please refer to “Termination” under section 3 for details)

After the TCP

Can be made from the IUA and / or AUA if (i) the remaining

Account Value immediately after the partial withdrawal meets the

Minimum Account Balance (ii) if the AUA value immediately after

the partial withdrawal is greater than 0

Minimum partial withdrawal amount (per withdrawal)

HKD4,000 / USD500 / EUR500 / GBP320 / AUD600 / SGD800

AXA reserves the right to change the minimum partial

withdrawal amount by giving the customers one month’s prior

written notice

Important Note

Making a partial withdrawal will lead to reduction in the Account

Value and further lead to reduction in any applicable Loyalty

Bonus, as well as termination of the policy

(please refer to “Loyalty Bonus” under section 3 for details)

Minimum Account

Balance HKD12,000 / USD1,500 / EUR1,500 / GBP960 / AUD1,800 / SGD2,400

Allowed

Allowed Not allowed

Pulsar II Investment Insurance Plan

All information is for internal use and reference only P.9, total 51 pages

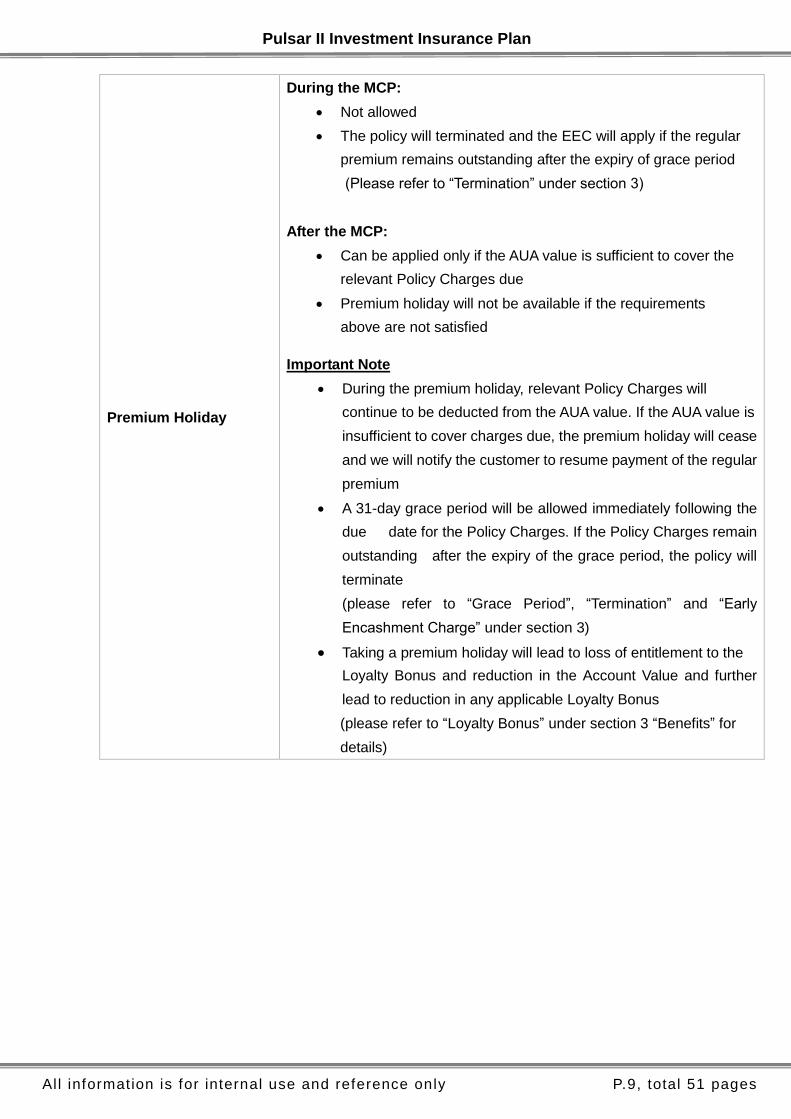

Premium Holiday

During the MCP:

Not allowed

The policy will terminated and the EEC will apply if the regular

premium remains outstanding after the expiry of grace period

(Please refer to “Termination” under section 3)

After the MCP:

Can be applied only if the AUA value is sufficient to cover the

relevant Policy Charges due

Premium holiday will not be available if the requirements

above are not satisfied

Important Note

During the premium holiday, relevant Policy Charges will

continue to be deducted from the AUA value. If the AUA value is

insufficient to cover charges due, the premium holiday will cease

and we will notify the customer to resume payment of the regular

premium

A 31-day grace period will be allowed immediately following the

due date for the Policy Charges. If the Policy Charges remain

outstanding after the expiry of the grace period, the policy will

terminate

(please refer to “Grace Period”, “Termination” and “Early

Encashment Charge” under section 3)

Taking a premium holiday will lead to loss of entitlement to the

Loyalty Bonus and reduction in the Account Value and further

lead to reduction in any applicable Loyalty Bonus

(please refer to “Loyalty Bonus” under section 3 “Benefits” for

details)

Pulsar II Investment Insurance Plan

All information is for internal use and reference only P.10, total 51 pages

IV. Policy Benefits

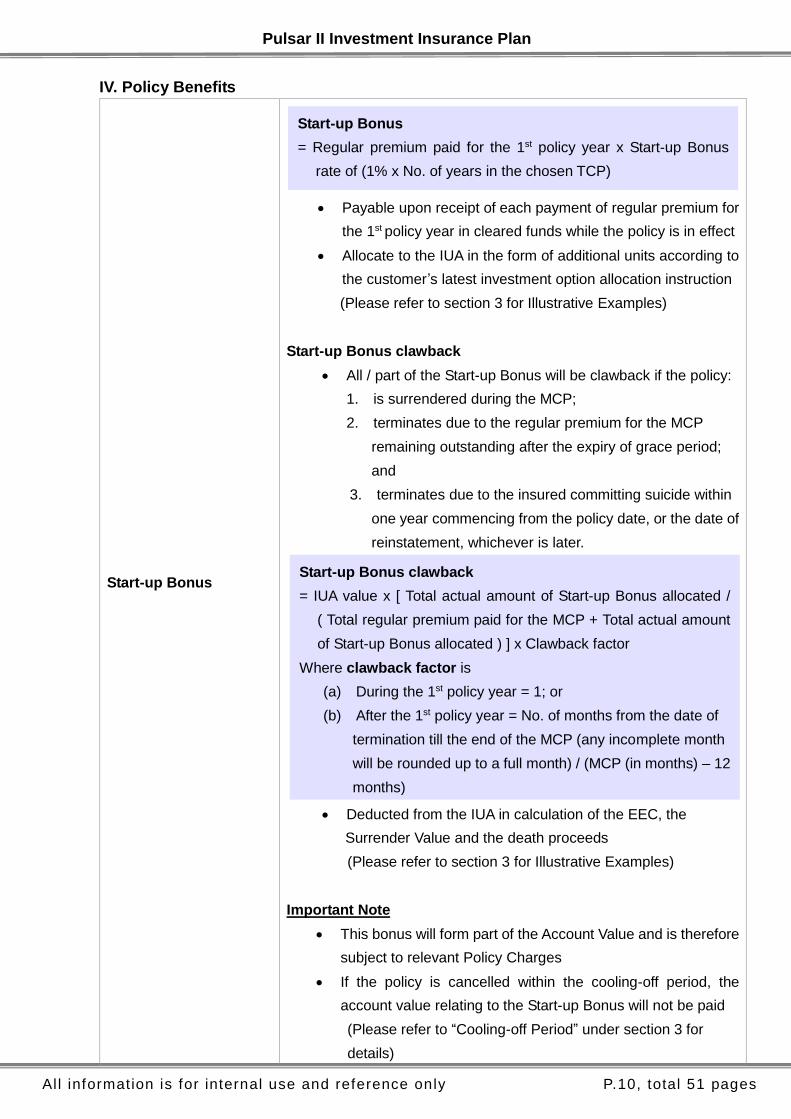

Start-up Bonus

Payable upon receipt of each payment of regular premium for

the 1st policy year in cleared funds while the policy is in effect

Allocate to the IUA in the form of additional units according to

the customer’s latest investment option allocation instruction

(Please refer to section 3 for Illustrative Examples)

Start-up Bonus clawback

All / part of the Start-up Bonus will be clawback if the policy:

1. is surrendered during the MCP;

2. terminates due to the regular premium for the MCP

remaining outstanding after the expiry of grace period;

and

3. terminates due to the insured committing suicide within

one year commencing from the policy date, or the date of

reinstatement, whichever is later.

Deducted from the IUA in calculation of the EEC, the

Surrender Value and the death proceeds

(Please refer to section 3 for Illustrative Examples)

Important Note

This bonus will form part of the Account Value and is therefore

subject to relevant Policy Charges

If the policy is cancelled within the cooling-off period, the

account value relating to the Start-up Bonus will not be paid

(Please refer to “Cooling-off Period” under section 3 for

details)

Start-up Bonus

= Regular premium paid for the 1st policy year x Start-up Bonus

rate of (1% x No. of years in the chosen TCP)

Start-up Bonus clawback

= IUA value x [ Total actual amount of Start-up Bonus allocated /

( Total regular premium paid for the MCP + Total actual amount

of Start-up Bonus allocated ) ] x Clawback factor

Where clawback factor is

(a) During the 1st policy year = 1; or

(b) After the 1st policy year = No. of months from the date of

termination till the end of the MCP (any incomplete month

will be rounded up to a full month) / (MCP (in months) – 12

months)

Pulsar II Investment Insurance Plan

All information is for internal use and reference only P.11, total 51 pages

Loyalty Bonus

Payable every policy year from the respective policy

anniversary according to the chosen TCP while the policy is in

effect

During the TCP but after the MCP

Payable if the regular premium committed at policy issuance

has been fully paid

After the TCP

Payable if the policy remains in effect

TCP (years) Loyalty Bonus payable every policy year

starting from

10 the 3rd policy anniversary

11 – 15 the 4th policy anniversary

16 – 20 the 5th policy anniversary

21 – 25 the 6th policy anniversary

Allocate to the IUA in the form of additional units according to

the customer’s latest investment option allocation instruction

(Please refer to section 3 for Illustrative Examples)

Important Note

Taking a premium holiday / reduction in the regular premium

during the 12 months prior to the relevant policy anniversary

on which the Loyalty Bonus is payable will lead to loss of

entitlement of the Loyalty Bonus. However, it will be resumed

if premium holiday is ceases and regular premium is

resumed / increased to the original amount committed at the

policy issuance during the whole duration of the 12 months

prior to the relevant policy anniversary.

Once the entitlement to the Loyalty Bonus payable on a policy

anniversary is forfeited, no Loyalty Bonus will be paid for that

policy anniversary.

Loyalty Bonus

= The average calendar month-end AUA value for the 12 months

prior to the relevant policy anniversary on which the Loyalty

Bonus is payable x Loyalty Bonus rate of 0.95%

Pulsar II Investment Insurance Plan

All information is for internal use and reference only P.12, total 51 pages

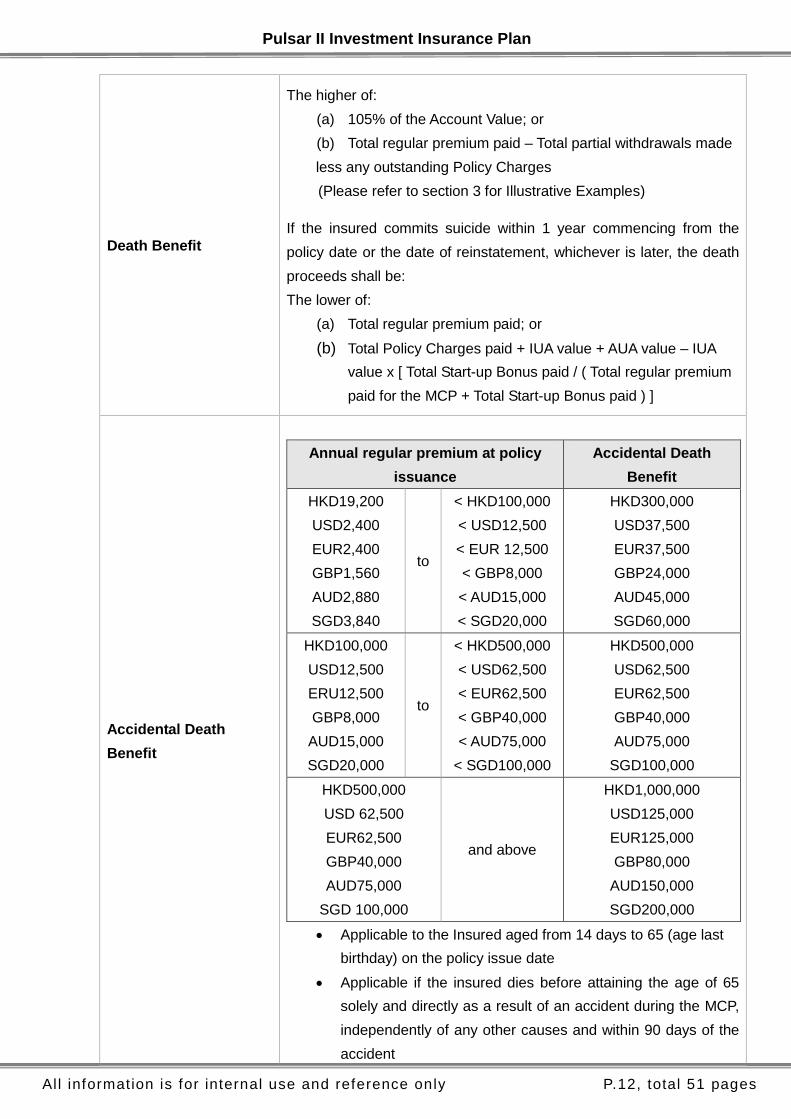

Death Benefit

The higher of:

(a) 105% of the Account Value; or

(b) Total regular premium paid – Total partial withdrawals made

less any outstanding Policy Charges

(Please refer to section 3 for Illustrative Examples)

If the insured commits suicide within 1 year commencing from the

policy date or the date of reinstatement, whichever is later, the death

proceeds shall be:

The lower of:

(a) Total regular premium paid; or

(b) Total Policy Charges paid + IUA value + AUA value – IUA

value x [ Total Start-up Bonus paid / ( Total regular premium

paid for the MCP + Total Start-up Bonus paid ) ]

Accidental Death

Benefit

Annual regular premium at policy

issuance

Accidental Death

Benefit

HKD19,200

USD2,400

EUR2,400

GBP1,560

AUD2,880

SGD3,840

to

< HKD100,000

< USD12,500

< EUR 12,500

< GBP8,000

< AUD15,000

< SGD20,000

HKD300,000

USD37,500

EUR37,500

GBP24,000

AUD45,000

SGD60,000

HKD100,000

USD12,500

ERU12,500

GBP8,000

AUD15,000

SGD20,000

to

< HKD500,000

< USD62,500

< EUR62,500

< GBP40,000

< AUD75,000

< SGD100,000

HKD500,000

USD62,500

EUR62,500

GBP40,000

AUD75,000

SGD100,000

HKD500,000

USD 62,500

EUR62,500

GBP40,000

AUD75,000

SGD 100,000

and above

HKD1,000,000

USD125,000

EUR125,000

GBP80,000

AUD150,000

SGD200,000

Applicable to the Insured aged from 14 days to 65 (age last

birthday) on the policy issue date

Applicable if the insured dies before attaining the age of 65

solely and directly as a result of an accident during the MCP,

independently of any other causes and within 90 days of the

accident

Pulsar II Investment Insurance Plan

All information is for internal use and reference only P.13, total 51 pages

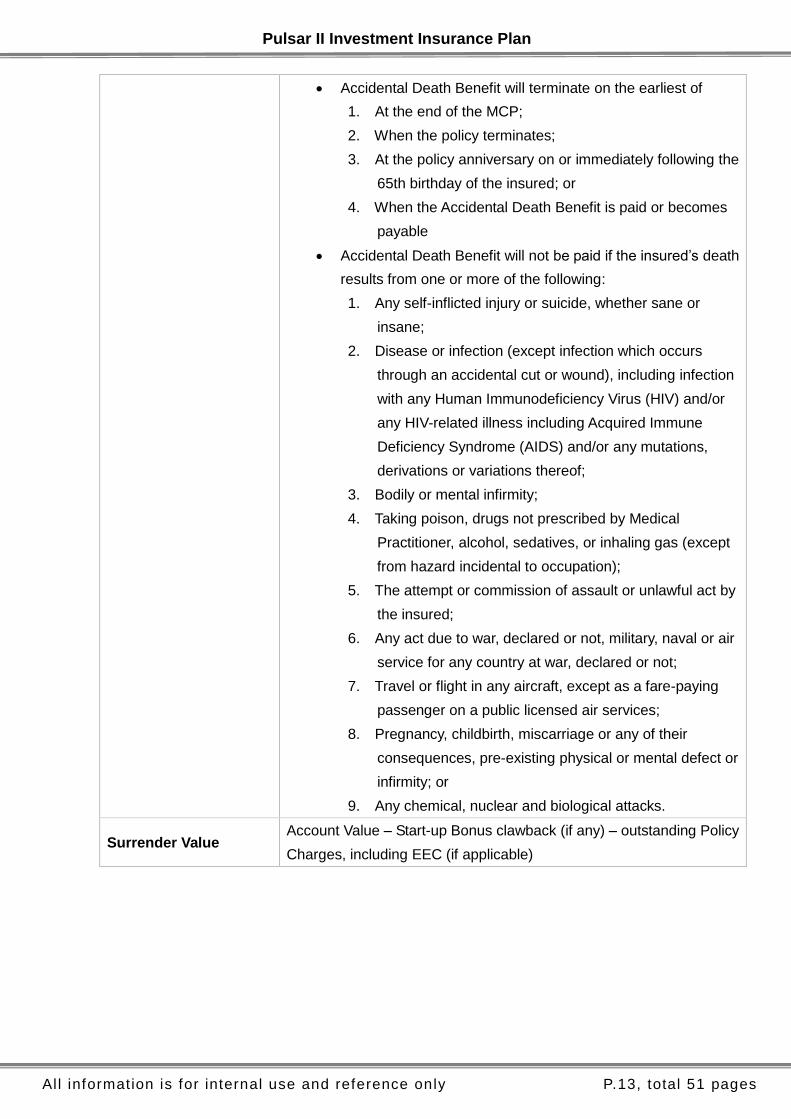

Accidental Death Benefit will terminate on the earliest of

1. At the end of the MCP;

2. When the policy terminates;

3. At the policy anniversary on or immediately following the

65th birthday of the insured; or

4. When the Accidental Death Benefit is paid or becomes

payable

Accidental Death Benefit will not be paid if the insured’s death

results from one or more of the following:

1. Any self-inflicted injury or suicide, whether sane or

insane;

2. Disease or infection (except infection which occurs

through an accidental cut or wound), including infection

with any Human Immunodeficiency Virus (HIV) and/or

any HIV-related illness including Acquired Immune

Deficiency Syndrome (AIDS) and/or any mutations,

derivations or variations thereof;

3. Bodily or mental infirmity;

4. Taking poison, drugs not prescribed by Medical

Practitioner, alcohol, sedatives, or inhaling gas (except

from hazard incidental to occupation);

5. The attempt or commission of assault or unlawful act by

the insured;

6. Any act due to war, declared or not, military, naval or air

service for any country at war, declared or not;

7. Travel or flight in any aircraft, except as a fare-paying

passenger on a public licensed air services;

8. Pregnancy, childbirth, miscarriage or any of their

consequences, pre-existing physical or mental defect or

infirmity; or

9. Any chemical, nuclear and biological attacks.

Surrender Value Account Value – Start-up Bonus clawback (if any) – outstanding Policy

Charges, including EEC (if applicable)

Pulsar II Investment Insurance Plan

All information is for internal use and reference only P.14, total 51 pages

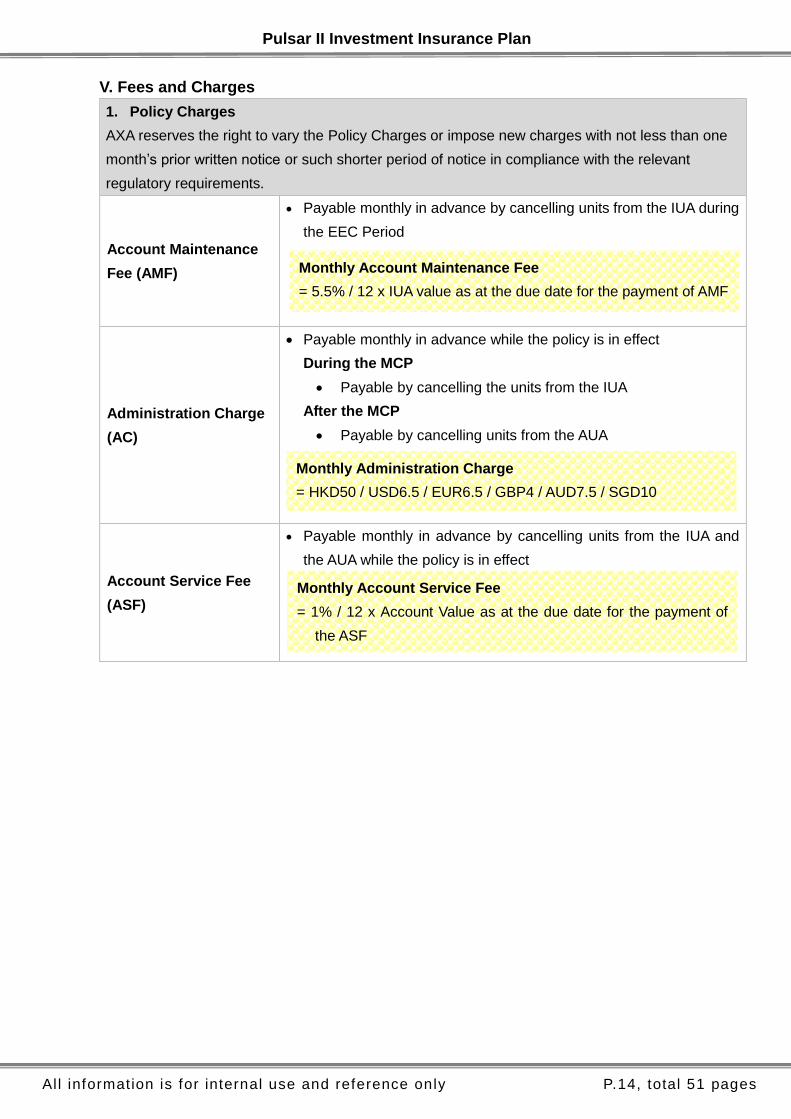

V. Fees and Charges

1. Policy Charges

AXA reserves the right to vary the Policy Charges or impose new charges with not less than one

month’s prior written notice or such shorter period of notice in compliance with the relevant

regulatory requirements.

Account Maintenance

Fee (AMF)

Payable monthly in advance by cancelling units from the IUA during

the EEC Period

Administration Charge

(AC)

Payable monthly in advance while the policy is in effect

During the MCP

Payable by cancelling the units from the IUA

After the MCP

Payable by cancelling units from the AUA

Account Service Fee

(ASF)

Payable monthly in advance by cancelling units from the IUA and

the AUA while the policy is in effect

Monthly Account Service Fee

= 1% / 12 x Account Value as at the due date for the payment of

the ASF

Monthly Account Maintenance Fee

= 5.5% / 12 x IUA value as at the due date for the payment of AMF

Monthly Administration Charge

= HKD50 / USD6.5 / EUR6.5 / GBP4 / AUD7.5 / SGD10

Pulsar II Investment Insurance Plan

All information is for internal use and reference only P.15, total 51 pages

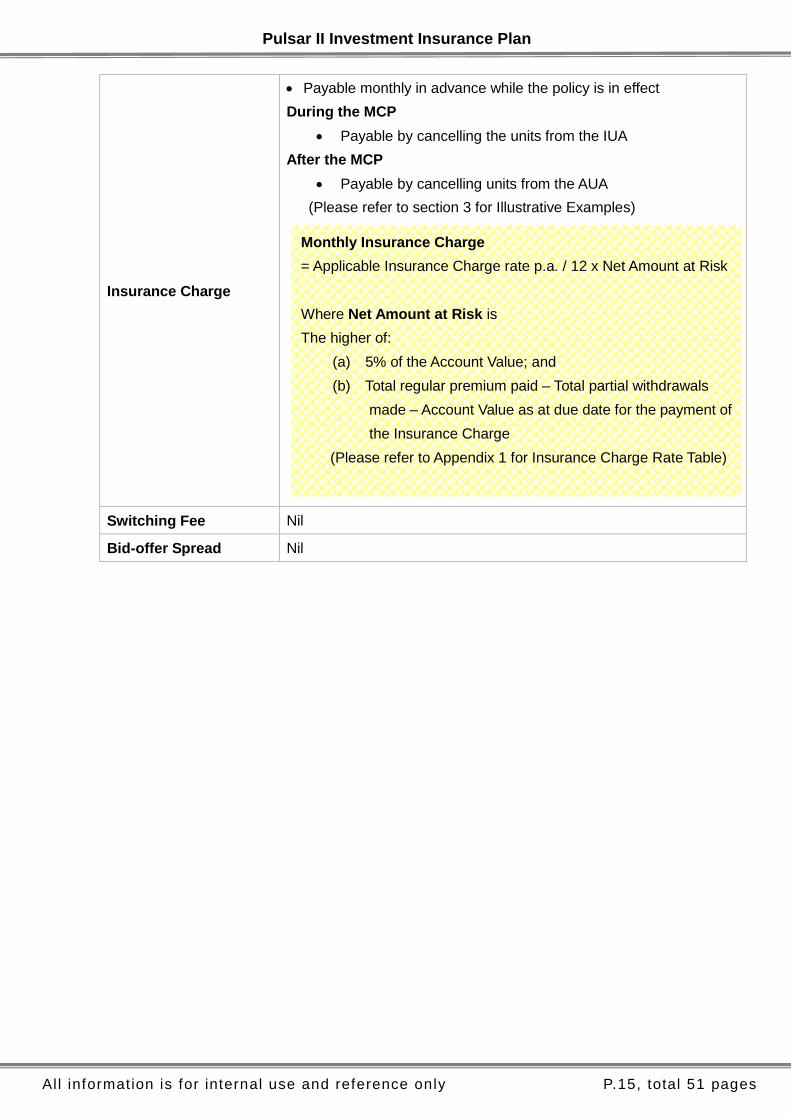

Insurance Charge

Payable monthly in advance while the policy is in effect

During the MCP

Payable by cancelling the units from the IUA

After the MCP

Payable by cancelling units from the AUA

(Please refer to section 3 for Illustrative Examples)

Switching Fee Nil

Bid-offer Spread Nil

Monthly Insurance Charge

= Applicable Insurance Charge rate p.a. / 12 x Net Amount at Risk

Where Net Amount at Risk is

The higher of:

(a) 5% of the Account Value; and

(b) Total regular premium paid – Total partial withdrawals

made – Account Value as at due date for the payment of

the Insurance Charge

(Please refer to Appendix 1 for Insurance Charge Rate Table)

Pulsar II Investment Insurance Plan

All information is for internal use and reference only P.16, total 51 pages

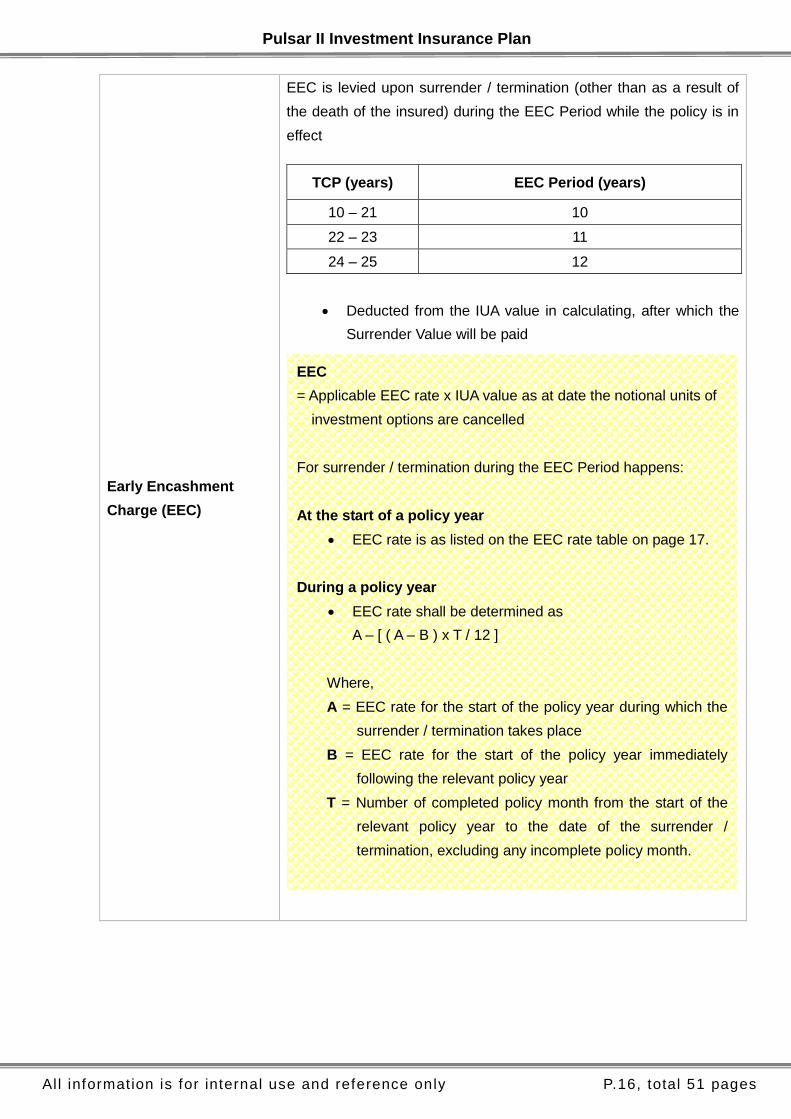

Early Encashment

Charge (EEC)

EEC is levied upon surrender / termination (other than as a result of

the death of the insured) during the EEC Period while the policy is in

effect

Deducted from the IUA value in calculating, after which the

Surrender Value will be paid

TCP (years) EEC Period (years)

10 – 21 10

22 – 23 11

24 – 25 12

EEC

= Applicable EEC rate x IUA value as at date the notional units of

investment options are cancelled

For surrender / termination during the EEC Period happens:

At the start of a policy year

EEC rate is as listed on the EEC rate table on page 17.

During a policy year

EEC rate shall be determined as

A – [ ( A – B ) x T / 12 ]

Where,

A = EEC rate for the start of the policy year during which the

surrender / termination takes place

B = EEC rate for the start of the policy year immediately

following the relevant policy year

T = Number of completed policy month from the start of the

relevant policy year to the date of the surrender /

termination, excluding any incomplete policy month.

Pulsar II Investment Insurance Plan

All information is for internal use and reference only P.17, total 51 pages

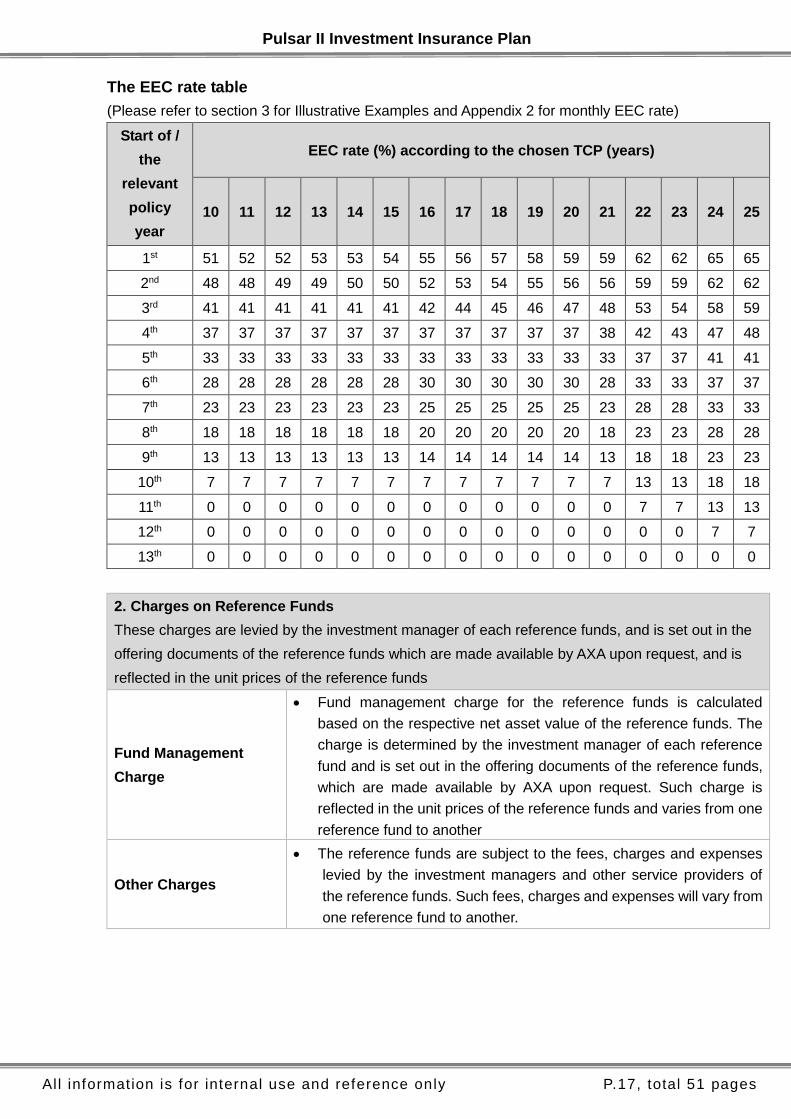

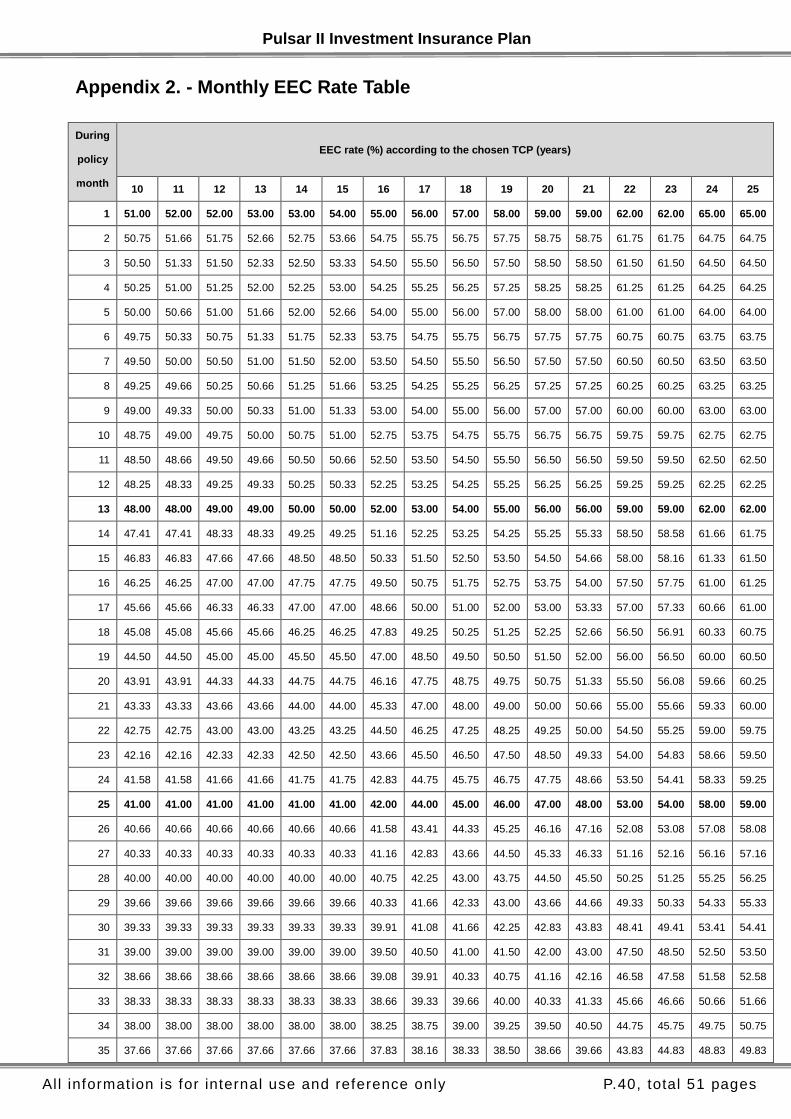

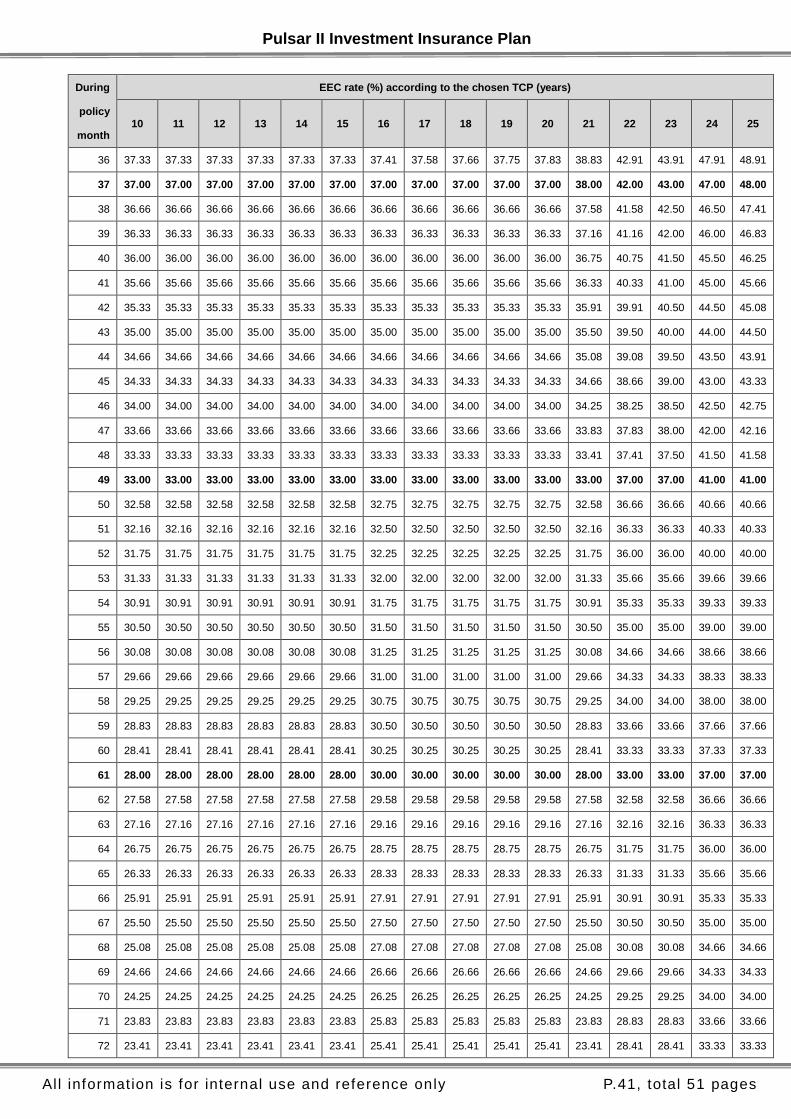

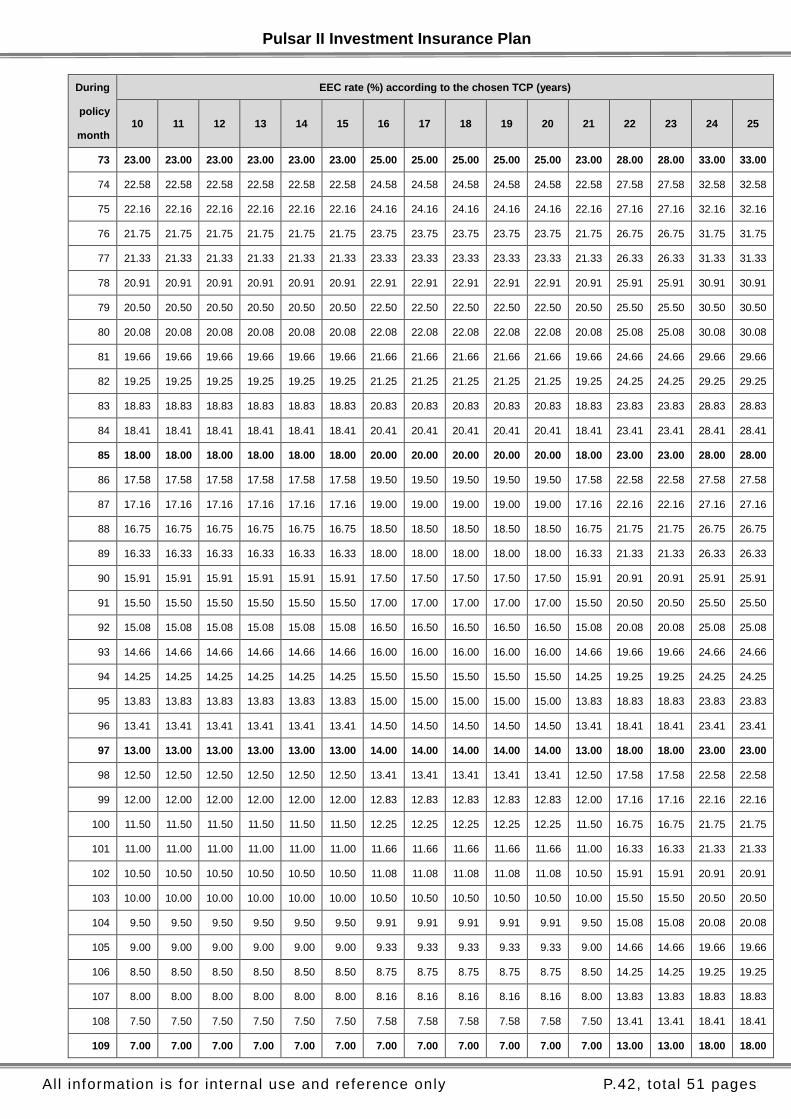

The EEC rate table

(Please refer to section 3 for Illustrative Examples and Appendix 2 for monthly EEC rate)

Start of /

the

relevant

policy

year

EEC rate (%) according to the chosen TCP (years)

10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25

1st 51 52 52 53 53 54 55 56 57 58 59 59 62 62 65 65

2nd 48 48 49 49 50 50 52 53 54 55 56 56 59 59 62 62

3rd 41 41 41 41 41 41 42 44 45 46 47 48 53 54 58 59

4th 37 37 37 37 37 37 37 37 37 37 37 38 42 43 47 48

5th 33 33 33 33 33 33 33 33 33 33 33 33 37 37 41 41

6th 28 28 28 28 28 28 30 30 30 30 30 28 33 33 37 37

7th 23 23 23 23 23 23 25 25 25 25 25 23 28 28 33 33

8th 18 18 18 18 18 18 20 20 20 20 20 18 23 23 28 28

9th 13 13 13 13 13 13 14 14 14 14 14 13 18 18 23 23

10th 7 7 7 7 7 7 7 7 7 7 7 7 13 13 18 18

11th 0 0 0 0 0 0 0 0 0 0 0 0 7 7 13 13

12th 0 0 0 0 0 0 0 0 0 0 0 0 0 0 7 7

13th 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0

2. Charges on Reference Funds

These charges are levied by the investment manager of each reference funds, and is set out in the

offering documents of the reference funds which are made available by AXA upon request, and is

reflected in the unit prices of the reference funds

Fund Management

Charge

Fund management charge for the reference funds is calculated

based on the respective net asset value of the reference funds. The

charge is determined by the investment manager of each reference

fund and is set out in the offering documents of the reference funds,

which are made available by AXA upon request. Such charge is

reflected in the unit prices of the reference funds and varies from one

reference fund to another

Other Charges

The reference funds are subject to the fees, charges and expenses

levied by the investment managers and other service providers of

the reference funds. Such fees, charges and expenses will vary from

one reference fund to another.

Pulsar II Investment Insurance Plan

All information is for internal use and reference only P.18, total 51 pages

VI. Other Information

Cooling-off Period

Customer may cancel the policy within 21 days after the delivery of

the policy / issue of a notice

AXA will refund the amount paid, or less if the value of the

customer’s investment options chosen has fallen at the time when

the cancellation request is received by us and will not be entitled

to the Start-up Bonus

Grace Period

During the MCP

31 days immediately following the due date for the payment

of regular premium

After the MCP

31 days immediately following the due date for the payment

of the Policy Charges if the AUA value is insufficient to cover

the relevant Policy Charges due

Termination

The policy will automatically terminate on the earliest of:

1. When the policy is surrender;

2. On the death of the insured;

3. At the policy maturity;

4. During the MCP, if the regular premium remains outstanding

after the expiry of the grace period; and

5. After the MCP, if the AUA value is insufficient to cover the

relevant Policy Charges due after the expiry of the grace

period

We may terminate the policy at any time if in our opinion the

customer’s ownership of the policy is likely to impose any

regulatory / tax obligation on us that it would not otherwise be

subject to

Surrender Value / Death Benefit (where applicable) shall be paid

Policy Maturity

The policy will mature and terminate on the earliest of:

(a) the Policy Anniversary which falls on the date on which the

insured attains the age of 100 if the date of the 100th birthday of

the insured coincides with such Policy Anniversary, or;

(b) the Policy Anniversary immediately after the date on which the

insured attains the age of 100 if the date of the 100th birthday of

the insured does not coincide with a Policy Anniversary

Surrender Value shall be paid

Pulsar II Investment Insurance Plan

All information is for internal use and reference only P.19, total 51 pages

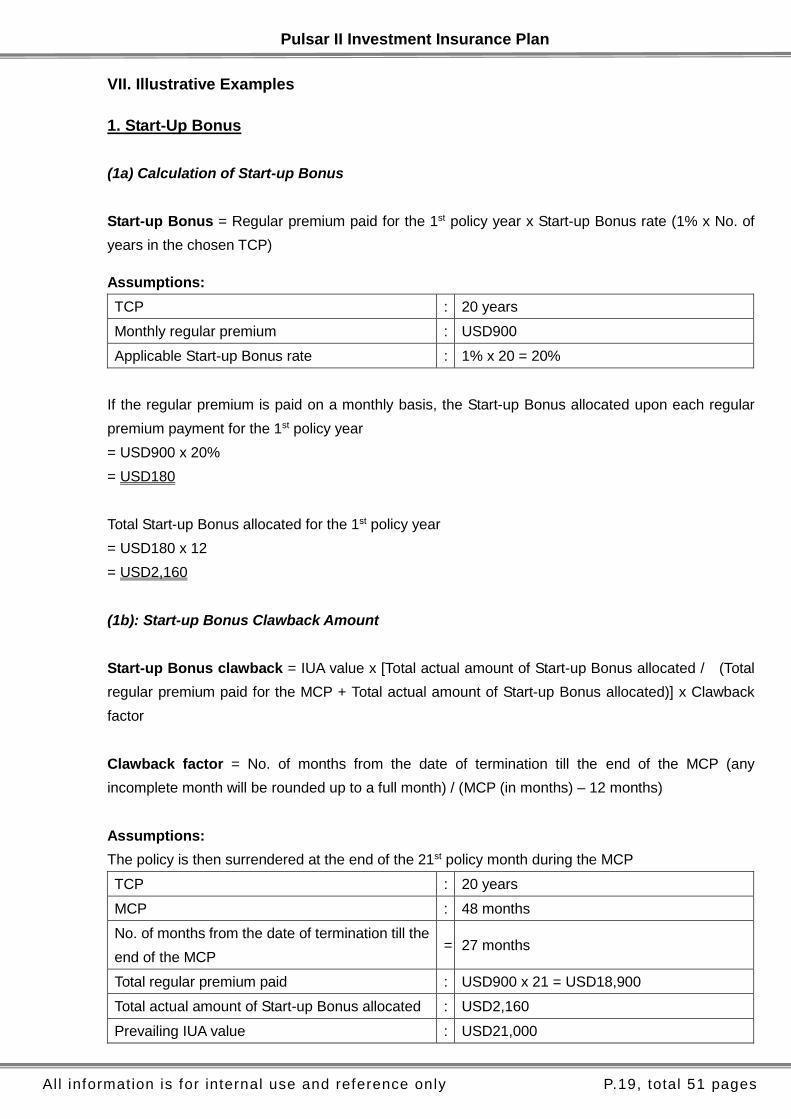

VII. Illustrative Examples

1. Start-Up Bonus

(1a) Calculation of Start-up Bonus

Start-up Bonus = Regular premium paid for the 1st policy year x Start-up Bonus rate (1% x No. of

years in the chosen TCP)

Assumptions:

TCP : 20 years

Monthly regular premium : USD900

Applicable Start-up Bonus rate : 1% x 20 = 20%

If the regular premium is paid on a monthly basis, the Start-up Bonus allocated upon each regular

premium payment for the 1st policy year

= USD900 x 20%

= USD180

Total Start-up Bonus allocated for the 1st policy year

= USD180 x 12

= USD2,160

(1b): Start-up Bonus Clawback Amount

Start-up Bonus clawback = IUA value x [Total actual amount of Start-up Bonus allocated / (Total

regular premium paid for the MCP + Total actual amount of Start-up Bonus allocated)] x Clawback

factor

Clawback factor = No. of months from the date of termination till the end of the MCP (any

incomplete month will be rounded up to a full month) / (MCP (in months) – 12 months)

Assumptions:

The policy is then surrendered at the end of the 21st policy month during the MCP

TCP : 20 years

MCP : 48 months

No. of months from the date of termination till the

end of the MCP = 27 months

Total regular premium paid : USD900 x 21 = USD18,900

Total actual amount of Start-up Bonus allocated : USD2,160

Prevailing IUA value : USD21,000

Pulsar II Investment Insurance Plan

All information is for internal use and reference only P.20, total 51 pages

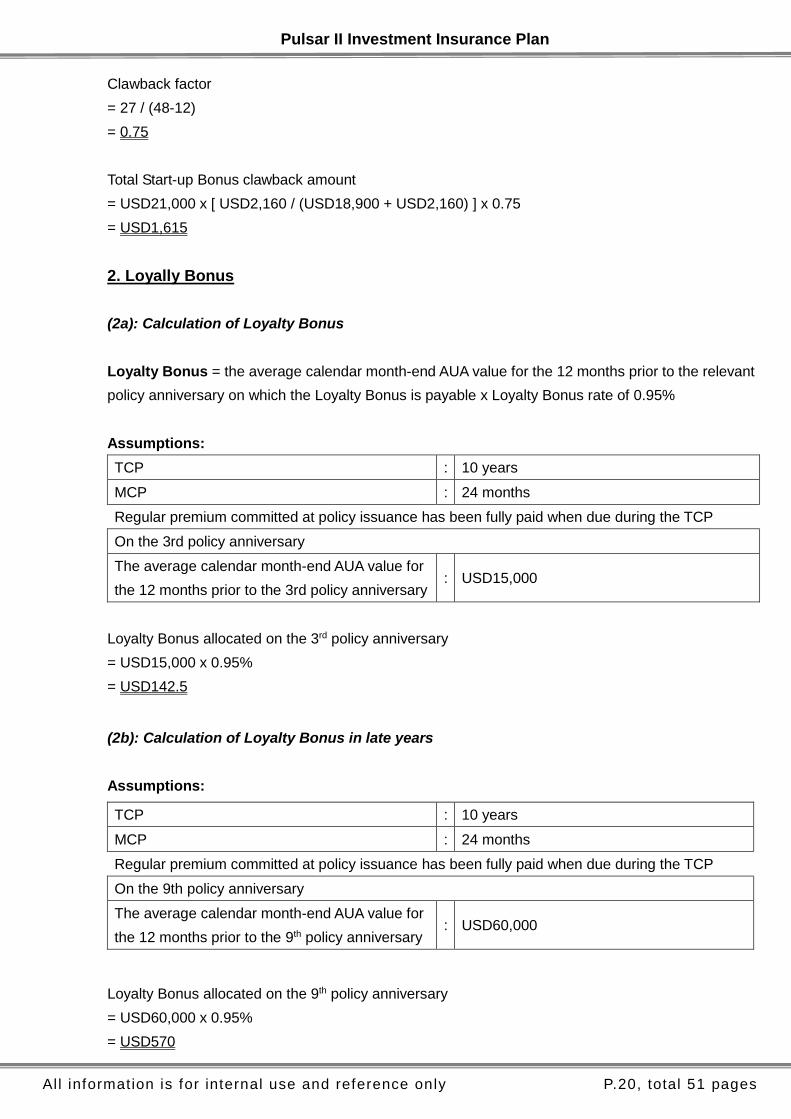

Clawback factor

= 27 / (48-12)

= 0.75

Total Start-up Bonus clawback amount

= USD21,000 x [ USD2,160 / (USD18,900 + USD2,160) ] x 0.75

= USD1,615

2. Loyally Bonus

(2a): Calculation of Loyalty Bonus

Loyalty Bonus = the average calendar month-end AUA value for the 12 months prior to the relevant

policy anniversary on which the Loyalty Bonus is payable x Loyalty Bonus rate of 0.95%

Assumptions:

TCP : 10 years

MCP : 24 months

Regular premium committed at policy issuance has been fully paid when due during the TCP

On the 3rd policy anniversary

The average calendar month-end AUA value for

the 12 months prior to the 3rd policy anniversary : USD15,000

Loyalty Bonus allocated on the 3rd policy anniversary

= USD15,000 x 0.95%

= USD142.5

(2b): Calculation of Loyalty Bonus in late years

Assumptions:

TCP : 10 years

MCP : 24 months

Regular premium committed at policy issuance has been fully paid when due during the TCP

On the 9th policy anniversary

The average calendar month-end AUA value for

the 12 months prior to the 9th policy anniversary : USD60,000

Loyalty Bonus allocated on the 9th policy anniversary

= USD60,000 x 0.95%

= USD570

Pulsar II Investment Insurance Plan

All information is for internal use and reference only P.21, total 51 pages

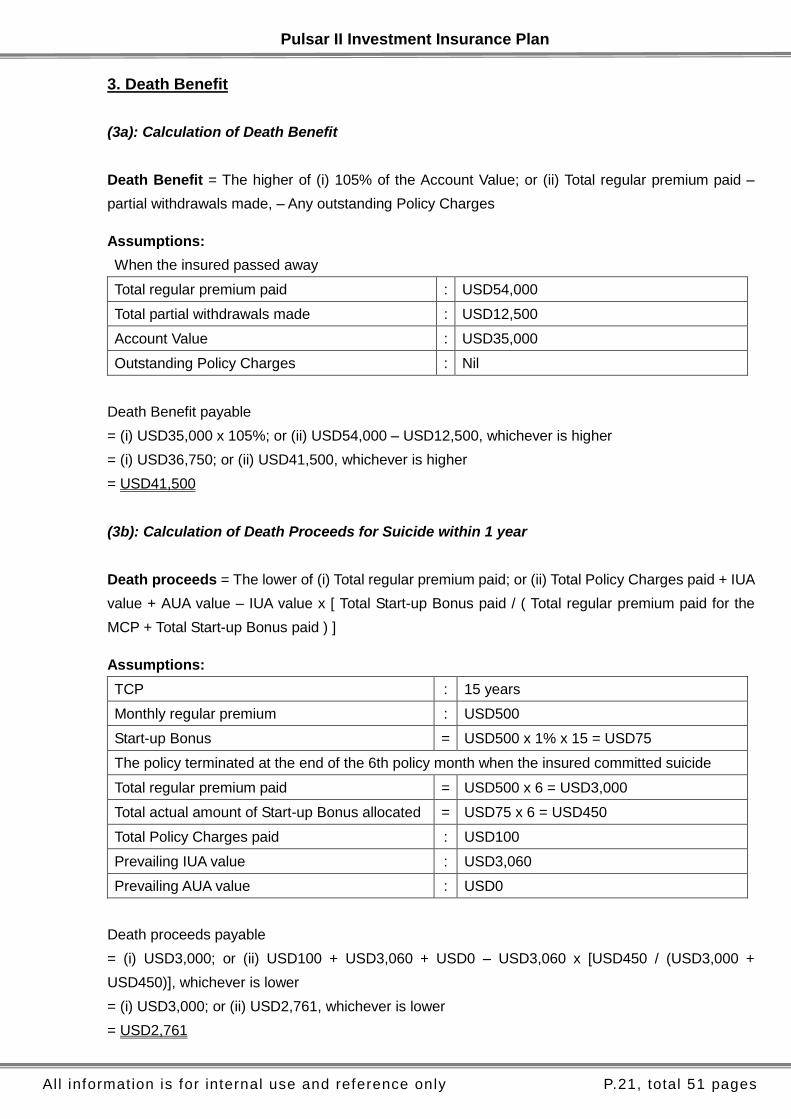

3. Death Benefit

(3a): Calculation of Death Benefit

Death Benefit = The higher of (i) 105% of the Account Value; or (ii) Total regular premium paid –

partial withdrawals made, – Any outstanding Policy Charges

Assumptions:

When the insured passed away

Total regular premium paid : USD54,000

Total partial withdrawals made : USD12,500

Account Value : USD35,000

Outstanding Policy Charges : Nil

Death Benefit payable

= (i) USD35,000 x 105%; or (ii) USD54,000 – USD12,500, whichever is higher

= (i) USD36,750; or (ii) USD41,500, whichever is higher

= USD41,500

(3b): Calculation of Death Proceeds for Suicide within 1 year

Death proceeds = The lower of (i) Total regular premium paid; or (ii) Total Policy Charges paid + IUA

value + AUA value – IUA value x [ Total Start-up Bonus paid / ( Total regular premium paid for the

MCP + Total Start-up Bonus paid ) ]

Assumptions:

TCP : 15 years

Monthly regular premium : USD500

Start-up Bonus = USD500 x 1% x 15 = USD75

The policy terminated at the end of the 6th policy month when the insured committed suicide

Total regular premium paid = USD500 x 6 = USD3,000

Total actual amount of Start-up Bonus allocated = USD75 x 6 = USD450

Total Policy Charges paid : USD100

Prevailing IUA value : USD3,060

Prevailing AUA value : USD0

Death proceeds payable

= (i) USD3,000; or (ii) USD100 + USD3,060 + USD0 – USD3,060 x [USD450 / (USD3,000 +

USD450)], whichever is lower

= (i) USD3,000; or (ii) USD2,761, whichever is lower

= USD2,761

Pulsar II Investment Insurance Plan

All information is for internal use and reference only P.22, total 51 pages

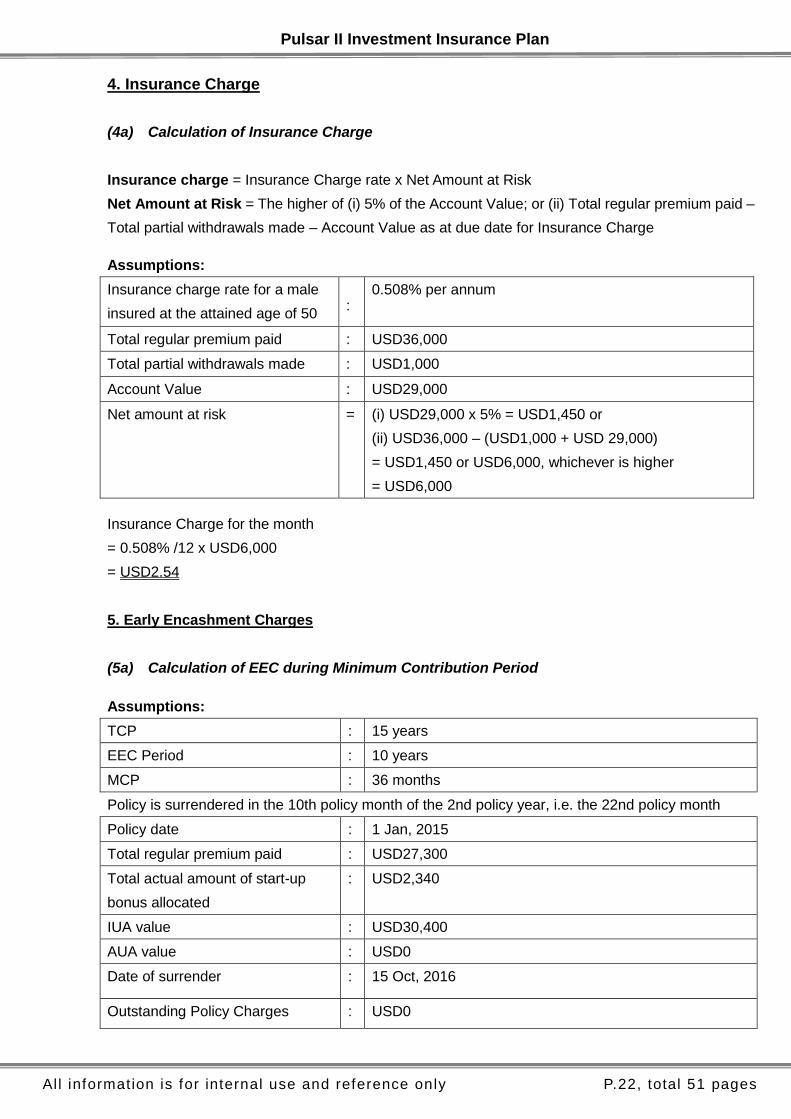

4. Insurance Charge

(4a) Calculation of Insurance Charge

Insurance charge = Insurance Charge rate x Net Amount at Risk

Net Amount at Risk = The higher of (i) 5% of the Account Value; or (ii) Total regular premium paid –

Total partial withdrawals made – Account Value as at due date for Insurance Charge

Assumptions:

Insurance charge rate for a male

insured at the attained age of 50 :

0.508% per annum

Total regular premium paid : USD36,000

Total partial withdrawals made : USD1,000

Account Value : USD29,000

Net amount at risk = (i) USD29,000 x 5% = USD1,450 or

(ii) USD36,000 – (USD1,000 + USD 29,000)

= USD1,450 or USD6,000, whichever is higher

= USD6,000

Insurance Charge for the month

= 0.508% /12 x USD6,000

= USD2.54

5. Early Encashment Charges

(5a) Calculation of EEC during Minimum Contribution Period

Assumptions:

TCP : 15 years

EEC Period : 10 years

MCP : 36 months

Policy is surrendered in the 10th policy month of the 2nd policy year, i.e. the 22nd policy month

Policy date : 1 Jan, 2015

Total regular premium paid : USD27,300

Total actual amount of start-up

bonus allocated

: USD2,340

IUA value : USD30,400

AUA value : USD0

Date of surrender : 15 Oct, 2016

Outstanding Policy Charges : USD0

Pulsar II Investment Insurance Plan

All information is for internal use and reference only P.23, total 51 pages

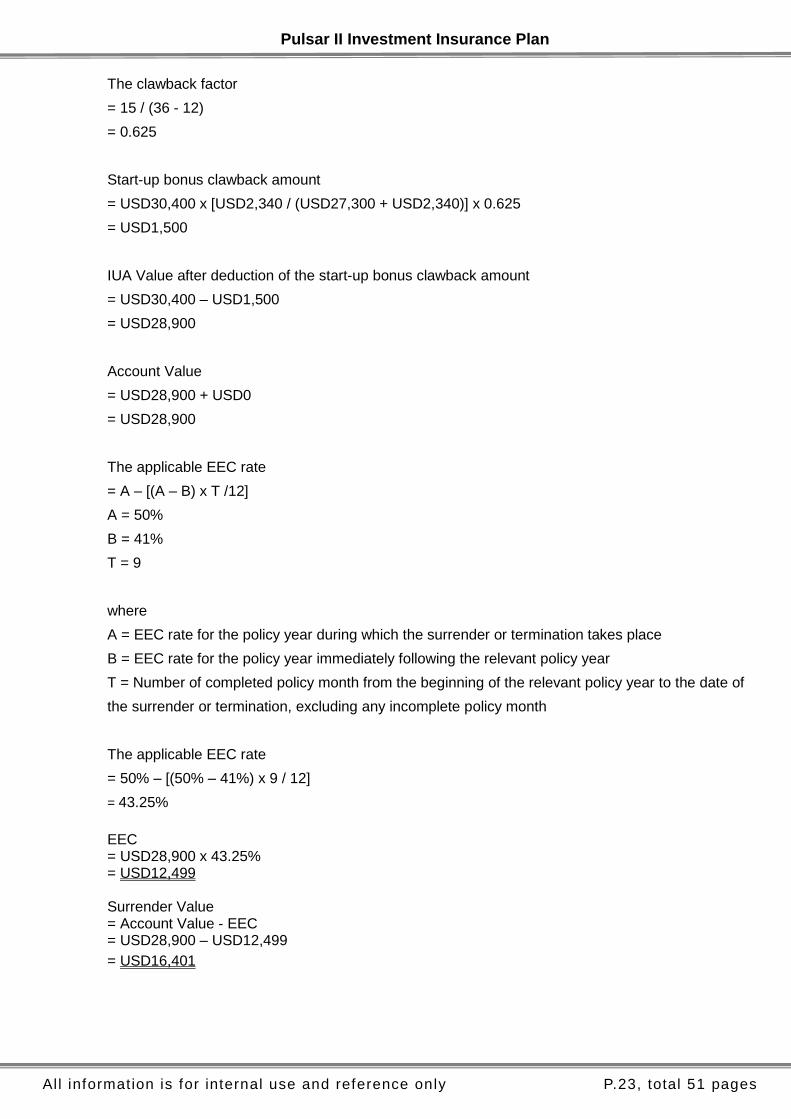

The clawback factor

= 15 / (36 - 12)

= 0.625

Start-up bonus clawback amount

= USD30,400 x [USD2,340 / (USD27,300 + USD2,340)] x 0.625

= USD1,500

IUA Value after deduction of the start-up bonus clawback amount

= USD30,400 – USD1,500

= USD28,900

Account Value

= USD28,900 + USD0

= USD28,900

The applicable EEC rate

= A – [(A – B) x T /12]

A = 50%

B = 41%

T = 9

where

A = EEC rate for the policy year during which the surrender or termination takes place

B = EEC rate for the policy year immediately following the relevant policy year

T = Number of completed policy month from the beginning of the relevant policy year to the date of

the surrender or termination, excluding any incomplete policy month

The applicable EEC rate

= 50% – [(50% – 41%) x 9 / 12]

= 43.25%

EEC = USD28,900 x 43.25% = USD12,499 Surrender Value = Account Value - EEC = USD28,900 – USD12,499

= USD16,401

Pulsar II Investment Insurance Plan

All information is for internal use and reference only P.24, total 51 pages

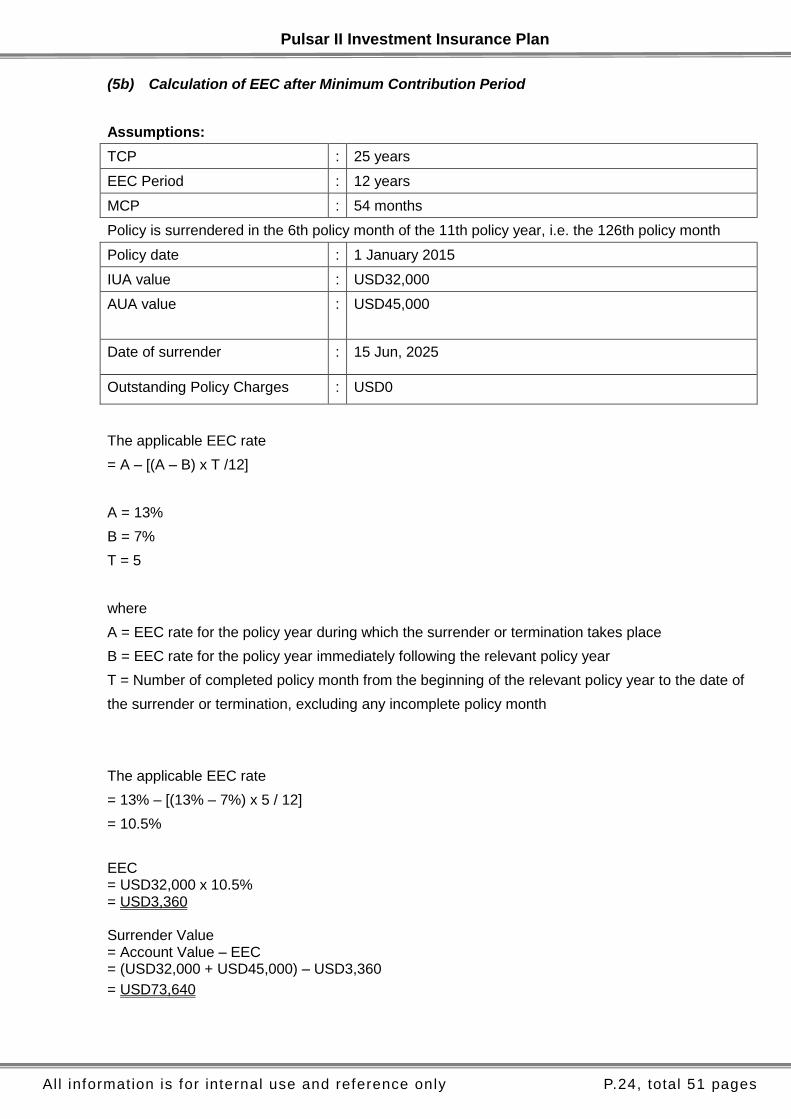

(5b) Calculation of EEC after Minimum Contribution Period

Assumptions:

TCP : 25 years

EEC Period : 12 years

MCP : 54 months

Policy is surrendered in the 6th policy month of the 11th policy year, i.e. the 126th policy month

Policy date : 1 January 2015

IUA value : USD32,000

AUA value : USD45,000

Date of surrender : 15 Jun, 2025

Outstanding Policy Charges : USD0

The applicable EEC rate

= A – [(A – B) x T /12]

A = 13%

B = 7%

T = 5

where

A = EEC rate for the policy year during which the surrender or termination takes place

B = EEC rate for the policy year immediately following the relevant policy year

T = Number of completed policy month from the beginning of the relevant policy year to the date of

the surrender or termination, excluding any incomplete policy month

The applicable EEC rate

= 13% – [(13% – 7%) x 5 / 12]

= 10.5%

EEC = USD32,000 x 10.5% = USD3,360 Surrender Value = Account Value – EEC = (USD32,000 + USD45,000) – USD3,360

= USD73,640

Pulsar II Investment Insurance Plan

All information is for internal use and reference only P.25, total 51 pages

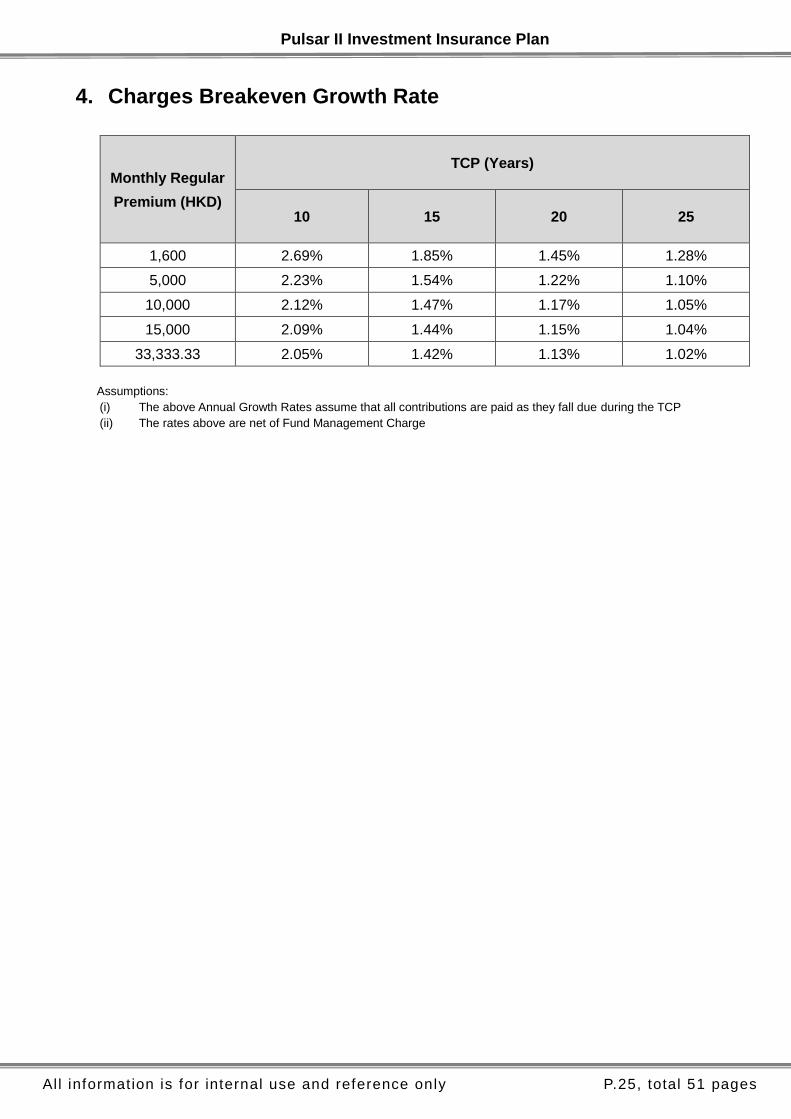

4. Charges Breakeven Growth Rate

Monthly Regular

Premium (HKD)

TCP (Years)

10 15 20 25

1,600 2.69% 1.85% 1.45% 1.28%

5,000 2.23% 1.54% 1.22% 1.10%

10,000 2.12% 1.47% 1.17% 1.05%

15,000 2.09% 1.44% 1.15% 1.04%

33,333.33 2.05% 1.42% 1.13% 1.02%

Assumptions:

(i) The above Annual Growth Rates assume that all contributions are paid as they fall due during the TCP

(ii) The rates above are net of Fund Management Charge

Pulsar II Investment Insurance Plan

All information is for internal use and reference only P.26, total 51 pages

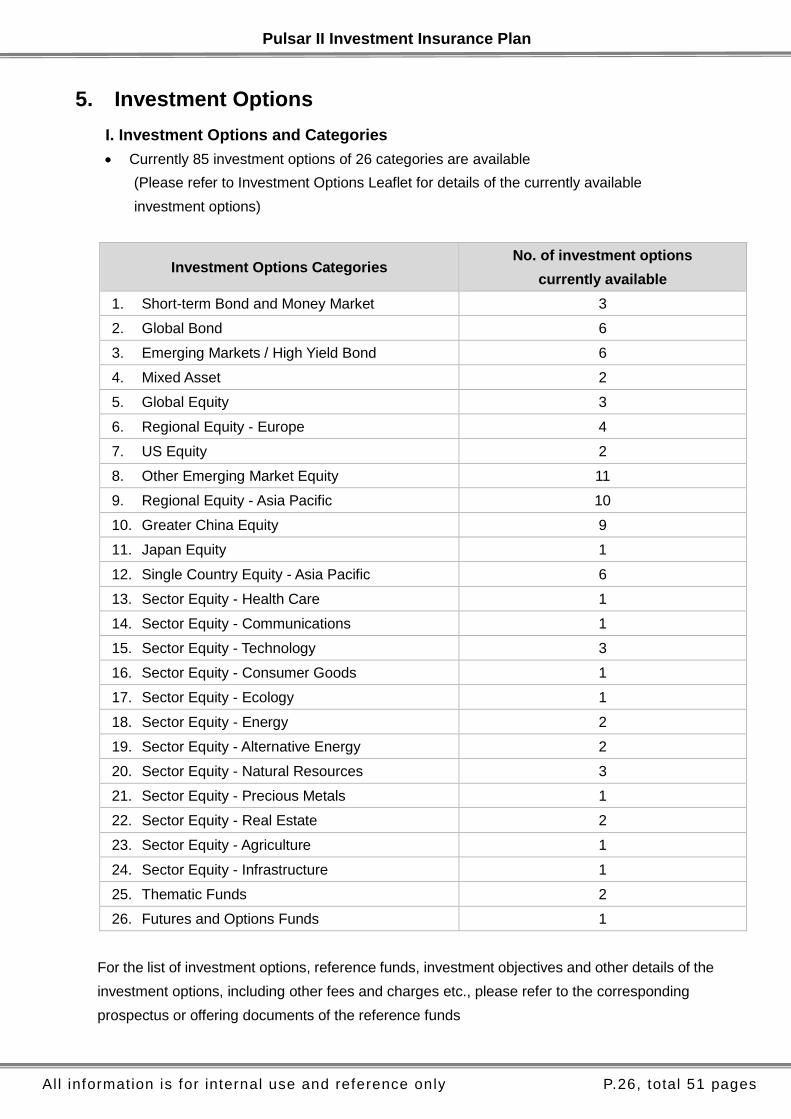

5. Investment Options

I. Investment Options and Categories

Currently 85 investment options of 26 categories are available

(Please refer to Investment Options Leaflet for details of the currently available

investment options)

Investment Options Categories No. of investment options

currently available

1. Short-term Bond and Money Market 3

2. Global Bond 6

3. Emerging Markets / High Yield Bond 6

4. Mixed Asset 2

5. Global Equity 3

6. Regional Equity - Europe 4

7. US Equity 2

8. Other Emerging Market Equity 11

9. Regional Equity - Asia Pacific 10

10. Greater China Equity 9

11. Japan Equity 1

12. Single Country Equity - Asia Pacific 6

13. Sector Equity - Health Care 1

14. Sector Equity - Communications 1

15. Sector Equity - Technology 3

16. Sector Equity - Consumer Goods 1

17. Sector Equity - Ecology 1

18. Sector Equity - Energy 2

19. Sector Equity - Alternative Energy 2

20. Sector Equity - Natural Resources 3

21. Sector Equity - Precious Metals 1

22. Sector Equity - Real Estate 2

23. Sector Equity - Agriculture 1

24. Sector Equity - Infrastructure 1

25. Thematic Funds 2

26. Futures and Options Funds 1

For the list of investment options, reference funds, investment objectives and other details of the

investment options, including other fees and charges etc., please refer to the corresponding

prospectus or offering documents of the reference funds

Pulsar II Investment Insurance Plan

All information is for internal use and reference only P.27, total 51 pages

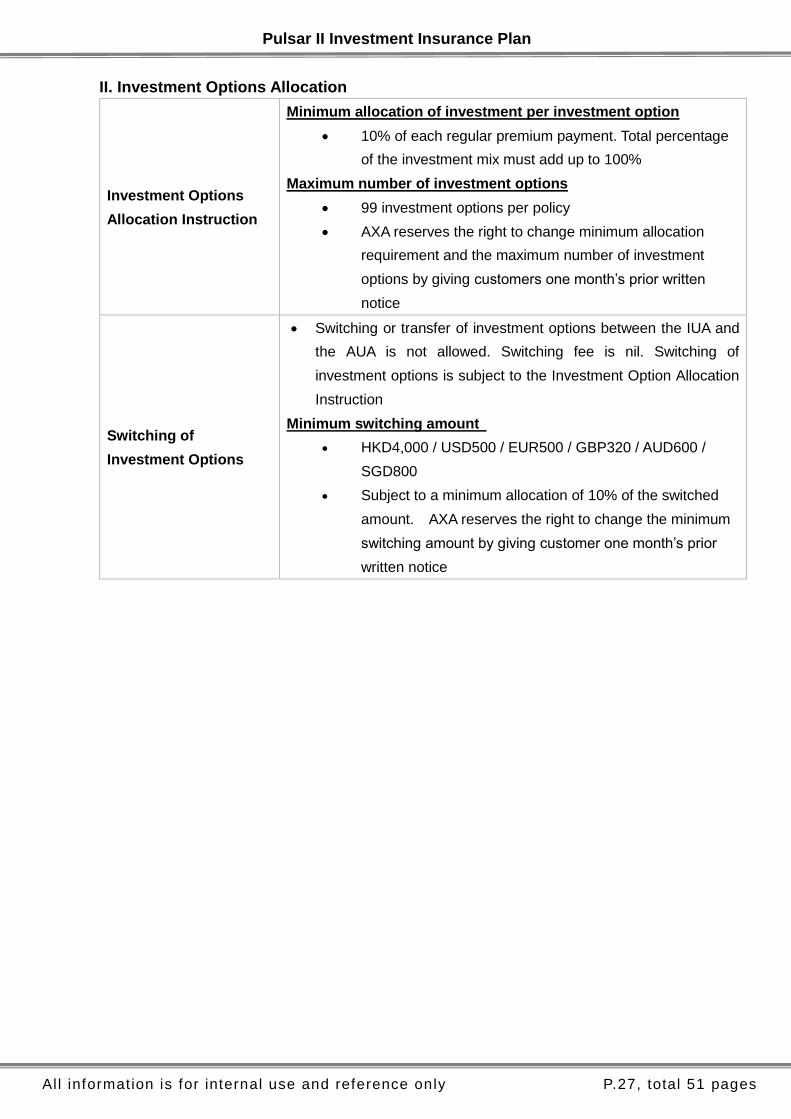

II. Investment Options Allocation

Investment Options

Allocation Instruction

Minimum allocation of investment per investment option

10% of each regular premium payment. Total percentage

of the investment mix must add up to 100%

Maximum number of investment options

99 investment options per policy

AXA reserves the right to change minimum allocation

requirement and the maximum number of investment

options by giving customers one month’s prior written

notice

Switching of

Investment Options

Switching or transfer of investment options between the IUA and

the AUA is not allowed. Switching fee is nil. Switching of

investment options is subject to the Investment Option Allocation

Instruction

Minimum switching amount

HKD4,000 / USD500 / EUR500 / GBP320 / AUD600 /

SGD800

Subject to a minimum allocation of 10% of the switched

amount. AXA reserves the right to change the minimum

switching amount by giving customer one month’s prior

written notice

Pulsar II Investment Insurance Plan

All information is for internal use and reference only P.28, total 51 pages

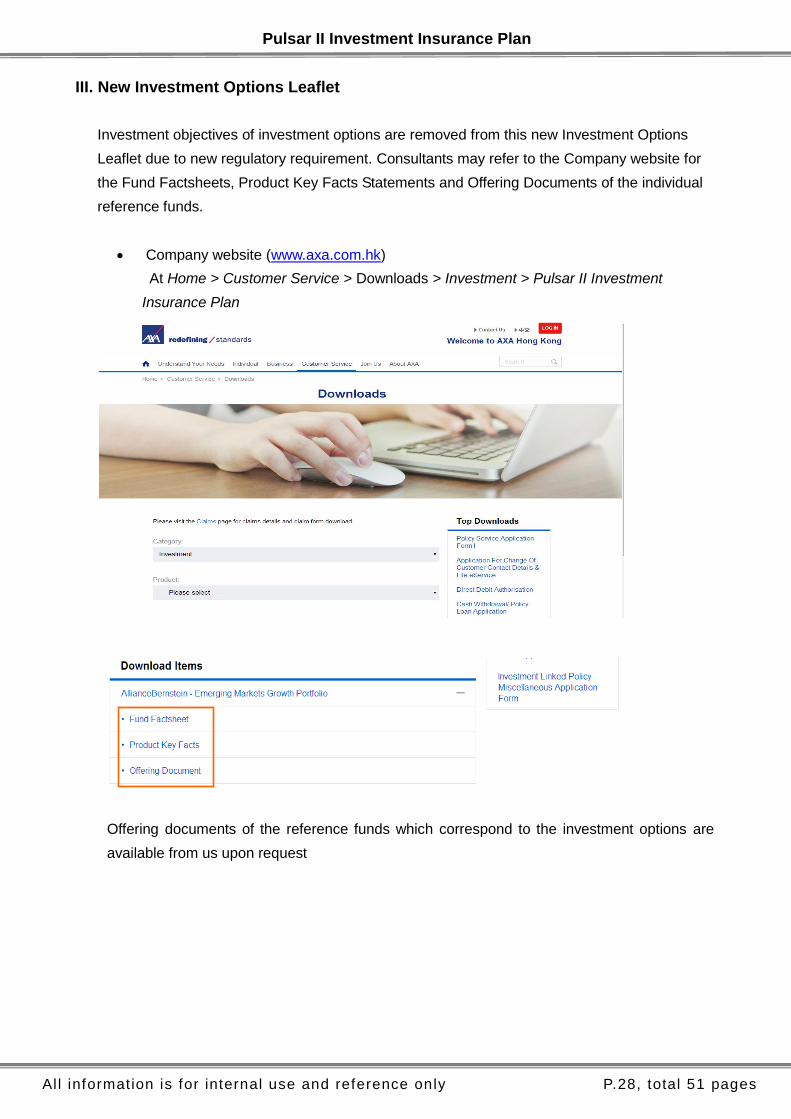

III. New Investment Options Leaflet

Investment objectives of investment options are removed from this new Investment Options

Leaflet due to new regulatory requirement. Consultants may refer to the Company website for

the Fund Factsheets, Product Key Facts Statements and Offering Documents of the individual

reference funds.

Company website (www.axa.com.hk)

At Home > Customer Service > Downloads > Investment > Pulsar II Investment

Insurance Plan

Offering documents of the reference funds which correspond to the investment options are

available from us upon request

Pulsar II Investment Insurance Plan

All information is for internal use and reference only P.29, total 51 pages

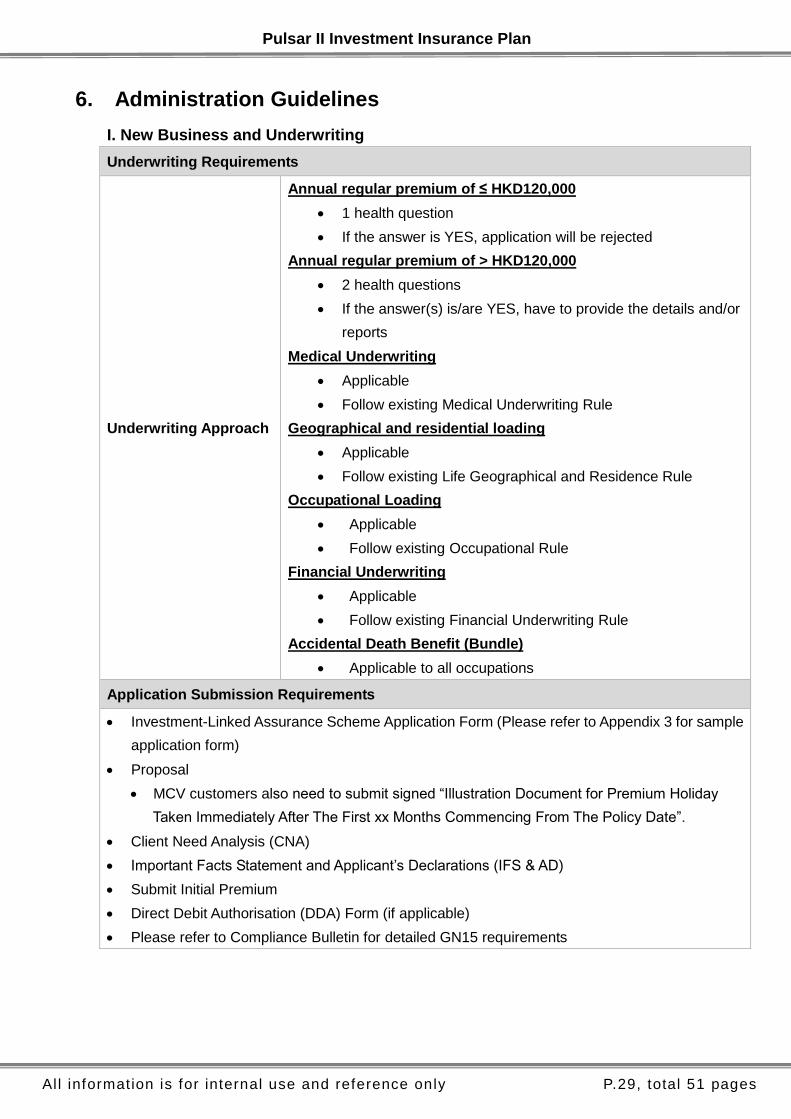

6. Administration Guidelines

I. New Business and Underwriting

Underwriting Requirements

Underwriting Approach

Annual regular premium of ≤ HKD120,000

1 health question

If the answer is YES, application will be rejected

Annual regular premium of > HKD120,000

2 health questions

If the answer(s) is/are YES, have to provide the details and/or

reports

Medical Underwriting

Applicable

Follow existing Medical Underwriting Rule

Geographical and residential loading

Applicable

Follow existing Life Geographical and Residence Rule

Occupational Loading

Applicable

Follow existing Occupational Rule

Financial Underwriting

Applicable

Follow existing Financial Underwriting Rule

Accidental Death Benefit (Bundle)

Applicable to all occupations

Application Submission Requirements

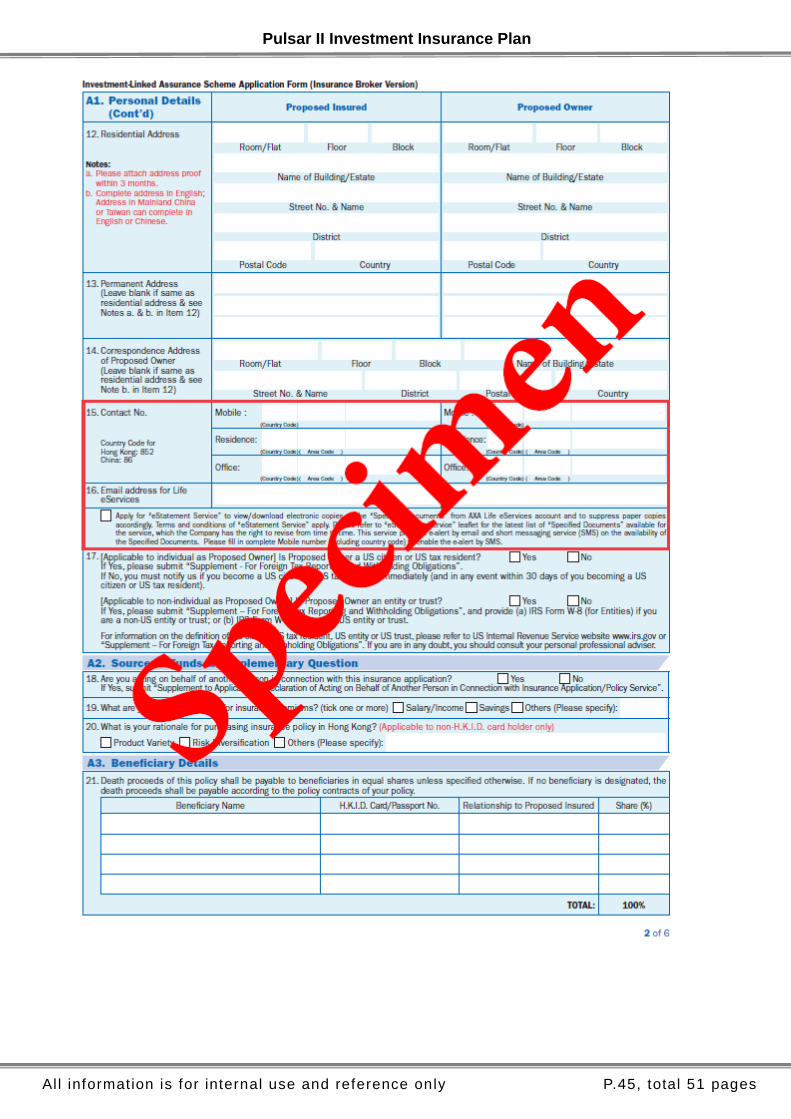

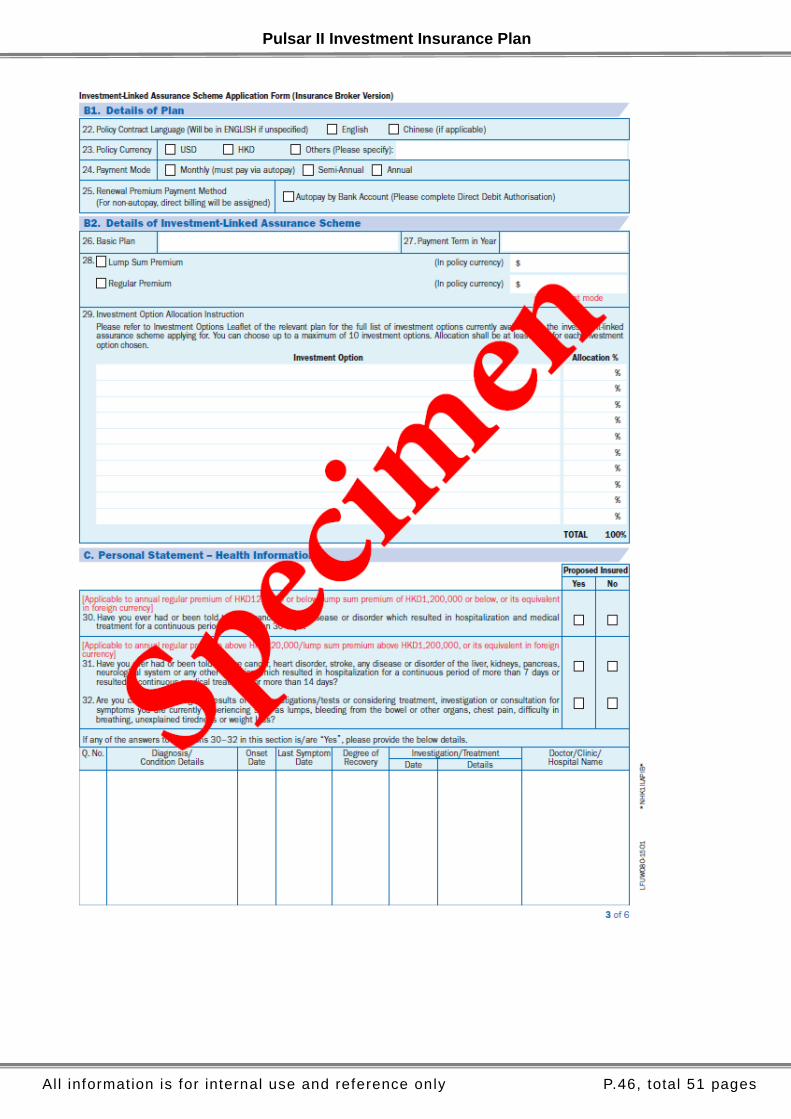

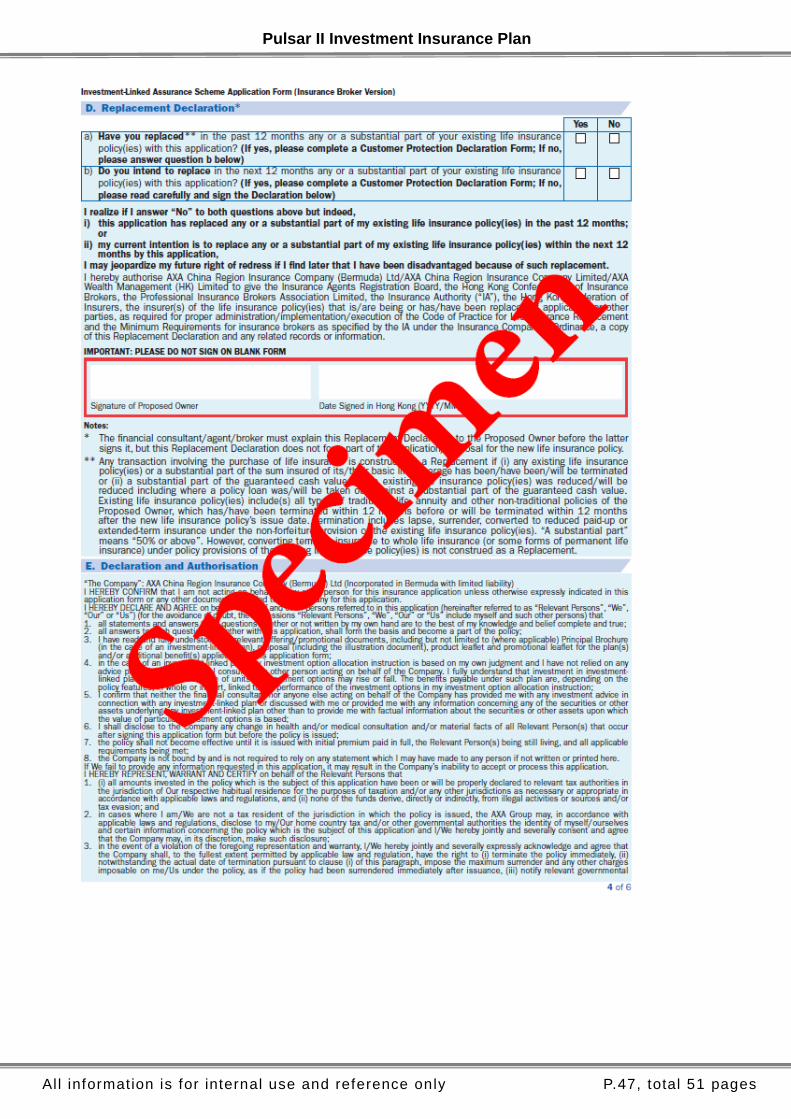

Investment-Linked Assurance Scheme Application Form (Please refer to Appendix 3 for sample

application form)

Proposal

MCV customers also need to submit signed “Illustration Document for Premium Holiday

Taken Immediately After The First xx Months Commencing From The Policy Date”.

Client Need Analysis (CNA)

Important Facts Statement and Applicant’s Declarations (IFS & AD)

Submit Initial Premium

Direct Debit Authorisation (DDA) Form (if applicable)

Please refer to Compliance Bulletin for detailed GN15 requirements

Pulsar II Investment Insurance Plan

All information is for internal use and reference only P.30, total 51 pages

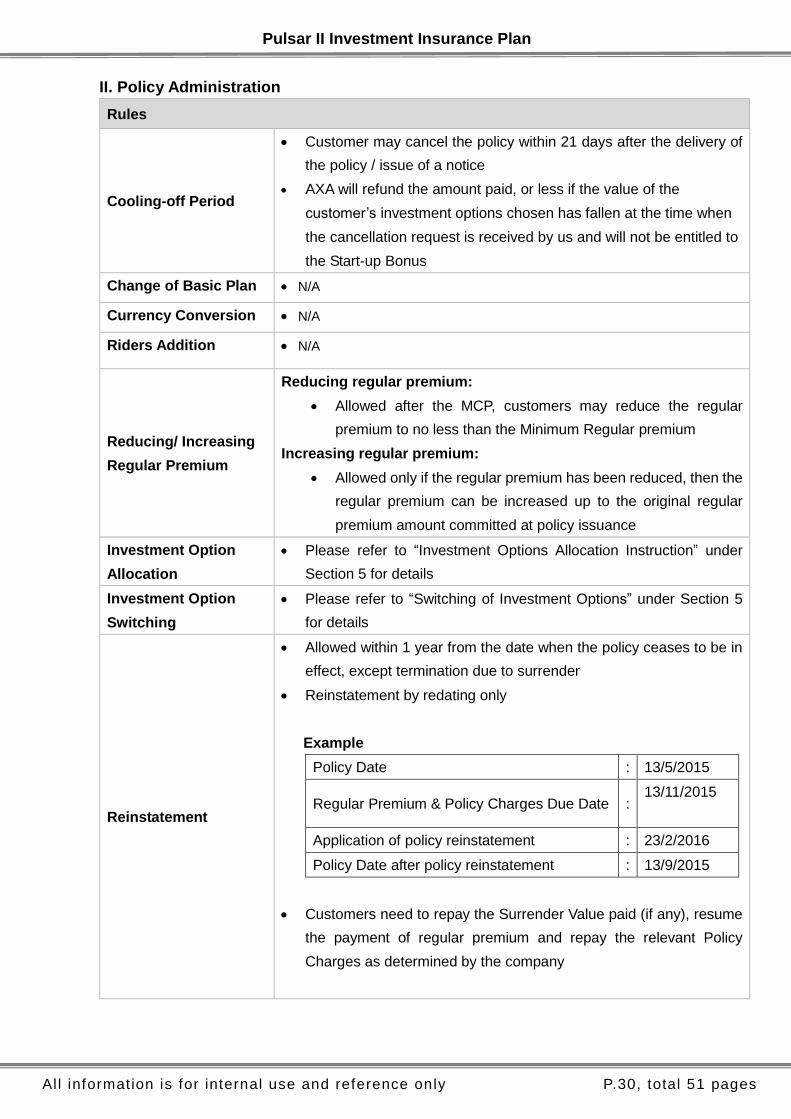

II. Policy Administration

Rules

Cooling-off Period

Customer may cancel the policy within 21 days after the delivery of

the policy / issue of a notice

AXA will refund the amount paid, or less if the value of the

customer’s investment options chosen has fallen at the time when

the cancellation request is received by us and will not be entitled to

the Start-up Bonus

Change of Basic Plan N/A

Currency Conversion N/A

Riders Addition N/A

Reducing/ Increasing

Regular Premium

Reducing regular premium:

Allowed after the MCP, customers may reduce the regular

premium to no less than the Minimum Regular premium

Increasing regular premium:

Allowed only if the regular premium has been reduced, then the

regular premium can be increased up to the original regular

premium amount committed at policy issuance

Investment Option

Allocation

Please refer to “Investment Options Allocation Instruction” under

Section 5 for details

Investment Option

Switching

Please refer to “Switching of Investment Options” under Section 5

for details

Reinstatement

Allowed within 1 year from the date when the policy ceases to be in

effect, except termination due to surrender

Reinstatement by redating only

Example

Policy Date : 13/5/2015

Regular Premium & Policy Charges Due Date : 13/11/2015

Application of policy reinstatement : 23/2/2016

Policy Date after policy reinstatement : 13/9/2015

Customers need to repay the Surrender Value paid (if any), resume

the payment of regular premium and repay the relevant Policy

Charges as determined by the company

Pulsar II Investment Insurance Plan

All information is for internal use and reference only P.31, total 51 pages

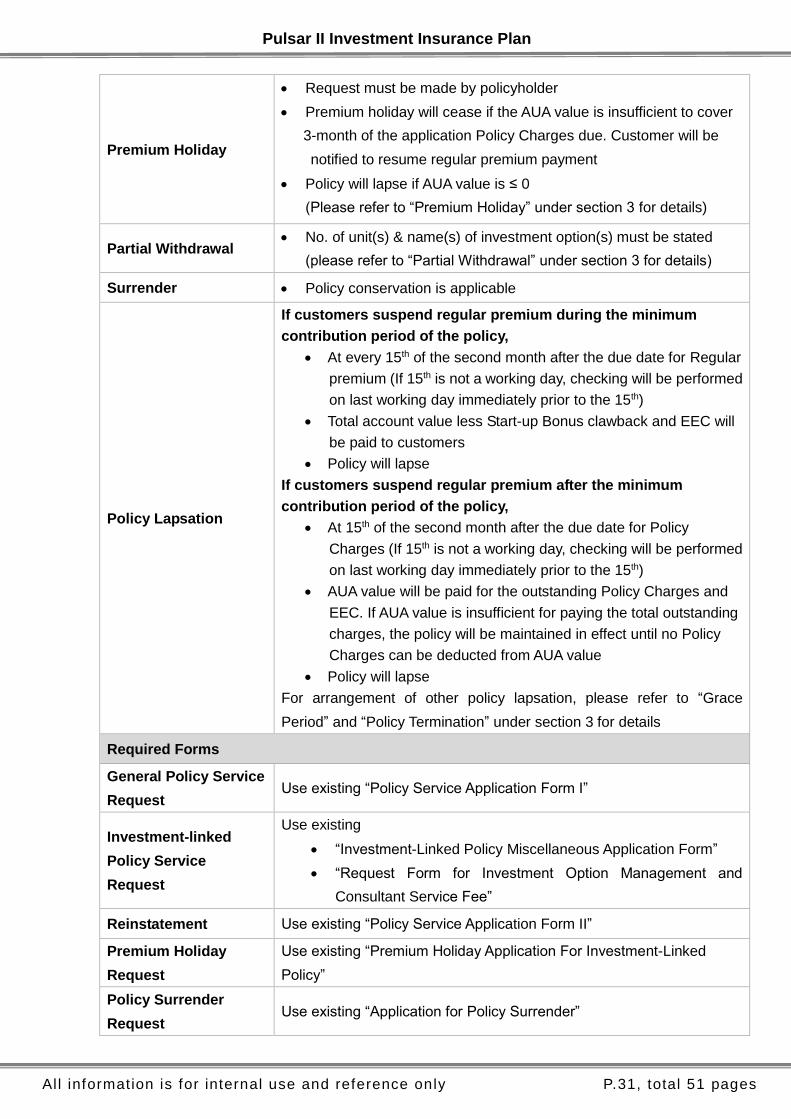

Premium Holiday

Request must be made by policyholder

Premium holiday will cease if the AUA value is insufficient to cover

3-month of the application Policy Charges due. Customer will be

notified to resume regular premium payment

Policy will lapse if AUA value is ≤ 0

(Please refer to “Premium Holiday” under section 3 for details)

Partial Withdrawal No. of unit(s) & name(s) of investment option(s) must be stated

(please refer to “Partial Withdrawal” under section 3 for details)

Surrender Policy conservation is applicable

Policy Lapsation

If customers suspend regular premium during the minimum

contribution period of the policy,

At every 15th of the second month after the due date for Regular

premium (If 15th is not a working day, checking will be performed

on last working day immediately prior to the 15th)

Total account value less Start-up Bonus clawback and EEC will

be paid to customers

Policy will lapse

If customers suspend regular premium after the minimum

contribution period of the policy,

At 15th of the second month after the due date for Policy

Charges (If 15th is not a working day, checking will be performed

on last working day immediately prior to the 15th)

AUA value will be paid for the outstanding Policy Charges and

EEC. If AUA value is insufficient for paying the total outstanding

charges, the policy will be maintained in effect until no Policy

Charges can be deducted from AUA value

Policy will lapse

For arrangement of other policy lapsation, please refer to “Grace

Period” and “Policy Termination” under section 3 for details

Required Forms

General Policy Service

Request Use existing “Policy Service Application Form I”

Investment-linked

Policy Service

Request

Use existing

“Investment-Linked Policy Miscellaneous Application Form”

“Request Form for Investment Option Management and

Consultant Service Fee”

Reinstatement Use existing “Policy Service Application Form II”

Premium Holiday

Request

Use existing “Premium Holiday Application For Investment-Linked

Policy”

Policy Surrender

Request Use existing “Application for Policy Surrender”

Pulsar II Investment Insurance Plan

All information is for internal use and reference only P.32, total 51 pages

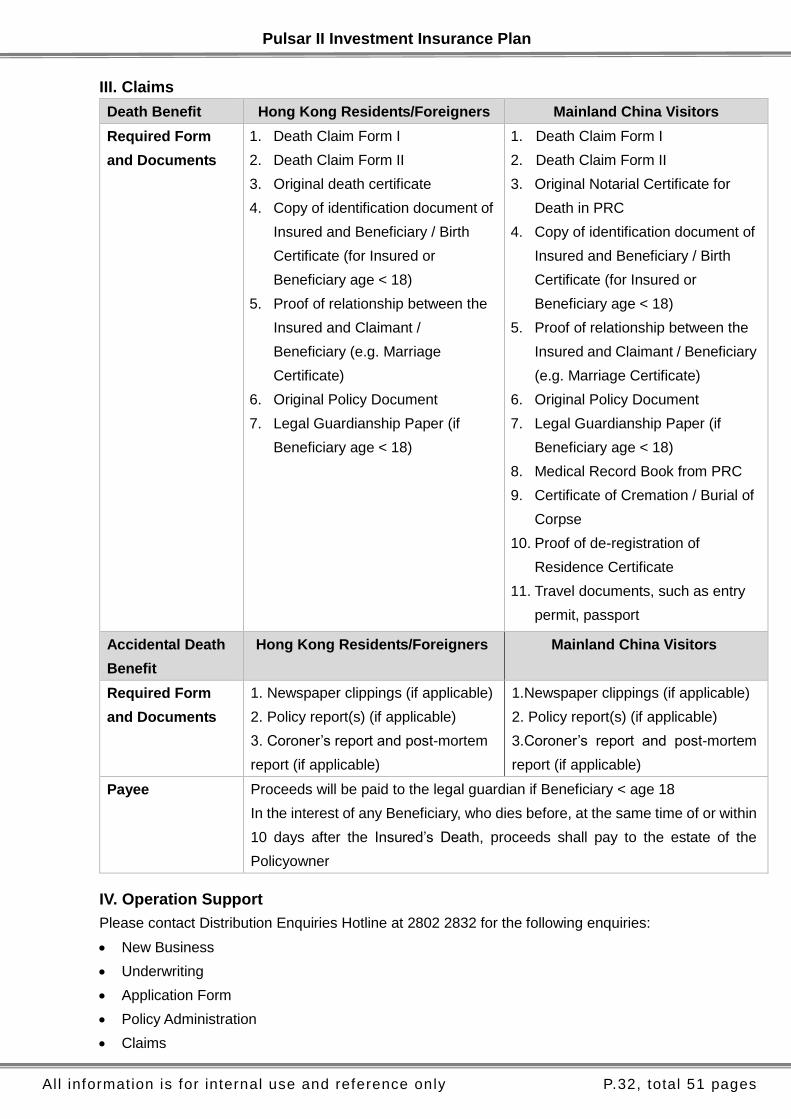

III. Claims

Death Benefit Hong Kong Residents/Foreigners Mainland China Visitors

Required Form

and Documents

1. Death Claim Form I

2. Death Claim Form II

3. Original death certificate

4. Copy of identification document of

Insured and Beneficiary / Birth

Certificate (for Insured or

Beneficiary age < 18)

5. Proof of relationship between the

Insured and Claimant /

Beneficiary (e.g. Marriage

Certificate)

6. Original Policy Document

7. Legal Guardianship Paper (if

Beneficiary age < 18)

1. Death Claim Form I

2. Death Claim Form II

3. Original Notarial Certificate for

Death in PRC

4. Copy of identification document of

Insured and Beneficiary / Birth

Certificate (for Insured or

Beneficiary age < 18)

5. Proof of relationship between the

Insured and Claimant / Beneficiary

(e.g. Marriage Certificate)

6. Original Policy Document

7. Legal Guardianship Paper (if

Beneficiary age < 18)

8. Medical Record Book from PRC

9. Certificate of Cremation / Burial of

Corpse

10. Proof of de-registration of

Residence Certificate

11. Travel documents, such as entry

permit, passport

Accidental Death

Benefit

Hong Kong Residents/Foreigners Mainland China Visitors

Required Form

and Documents

1. Newspaper clippings (if applicable)

2. Policy report(s) (if applicable)

3. Coroner’s report and post-mortem

report (if applicable)

1.Newspaper clippings (if applicable)

2. Policy report(s) (if applicable)

3.Coroner’s report and post-mortem

report (if applicable)

Payee Proceeds will be paid to the legal guardian if Beneficiary < age 18

In the interest of any Beneficiary, who dies before, at the same time of or within

10 days after the Insured’s Death, proceeds shall pay to the estate of the

Policyowner

IV. Operation Support

Please contact Distribution Enquiries Hotline at 2802 2832 for the following enquiries:

New Business

Underwriting

Application Form

Policy Administration

Claims

Pulsar II Investment Insurance Plan

All information is for internal use and reference only P.33, total 51 pages

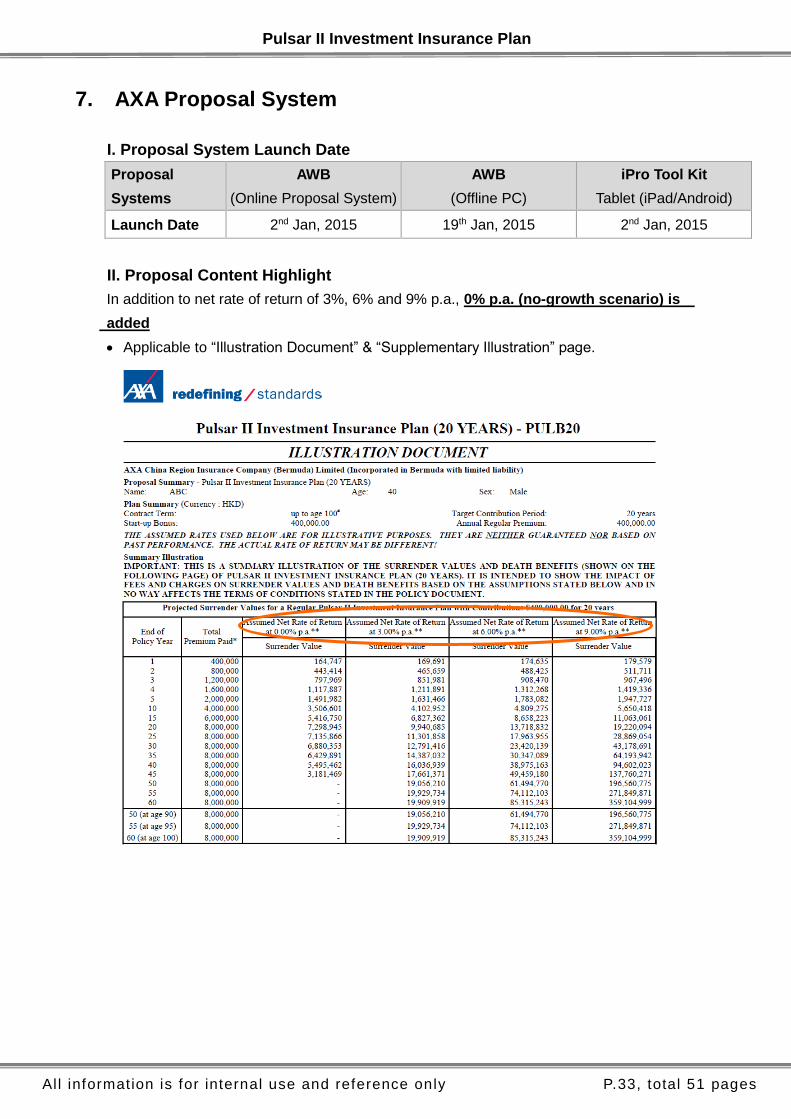

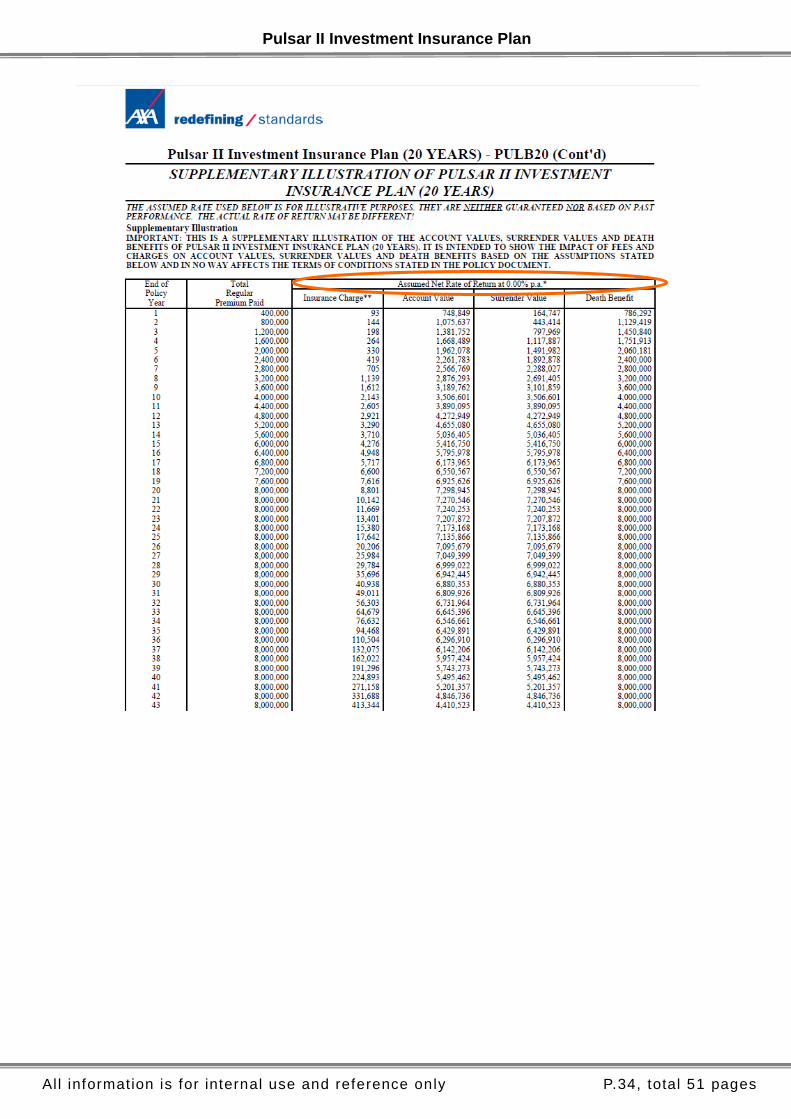

7. AXA Proposal System

I. Proposal System Launch Date

Proposal

Systems

AWB

(Online Proposal System)

AWB

(Offline PC)

iPro Tool Kit

Tablet (iPad/Android)

Launch Date 2nd Jan, 2015 19th Jan, 2015 2nd Jan, 2015

II. Proposal Content Highlight

In addition to net rate of return of 3%, 6% and 9% p.a., 0% p.a. (no-growth scenario) is

added

Applicable to “Illustration Document” & “Supplementary Illustration” page.

Pulsar II Investment Insurance Plan

All information is for internal use and reference only P.34, total 51 pages

Pulsar II Investment Insurance Plan

All information is for internal use and reference only P.35, total 51 pages

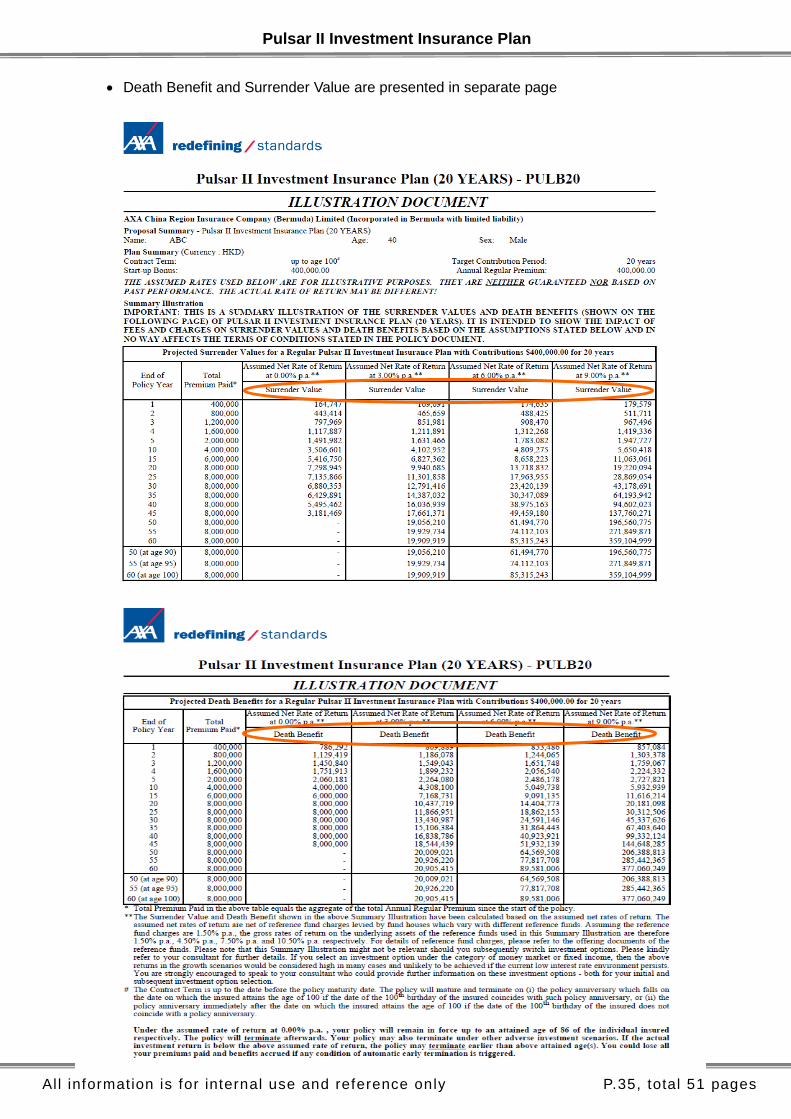

Death Benefit and Surrender Value are presented in separate page

Pulsar II Investment Insurance Plan

All information is for internal use and reference only P.36, total 51 pages

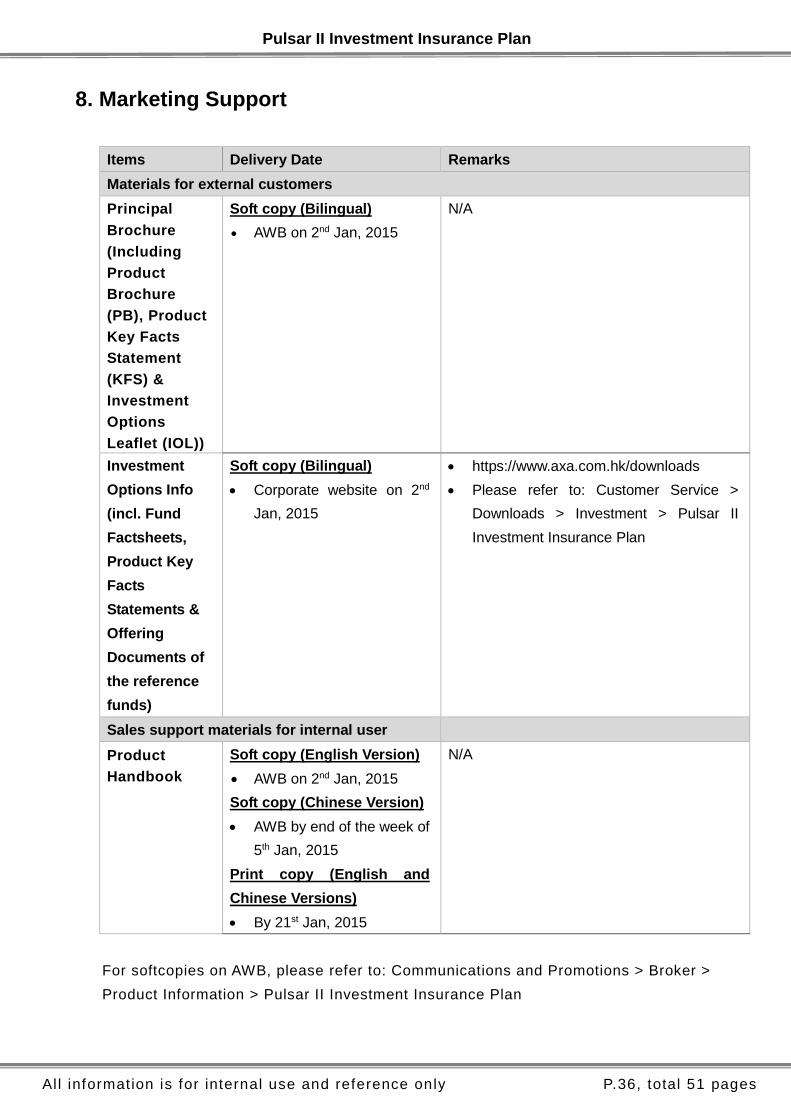

8. Marketing Support

Items Delivery Date Remarks

Materials for external customers

Principal

Brochure

(Including

Product

Brochure

(PB), Product

Key Facts

Statement

(KFS) &

Investment

Options

Leaflet (IOL))

Soft copy (Bilingual)

AWB on 2nd Jan, 2015

N/A

Investment

Options Info

(incl. Fund

Factsheets,

Product Key

Facts

Statements &

Offering

Documents of

the reference

funds)

Soft copy (Bilingual)

Corporate website on 2nd

Jan, 2015

https://www.axa.com.hk/downloads

Please refer to: Customer Service >

Downloads > Investment > Pulsar II

Investment Insurance Plan

Sales support materials for internal user

Product

Handbook

Soft copy (English Version)

AWB on 2nd Jan, 2015

Soft copy (Chinese Version)

AWB by end of the week of

5th Jan, 2015

Print copy (English and

Chinese Versions)

By 21st Jan, 2015

N/A

For softcopies on AWB, please refer to: Communications and Promotions > Broker >

Product Information > Pulsar II Investment Insurance Plan

Pulsar II Investment Insurance Plan

All information is for internal use and reference only P.37, total 51 pages

9. Frequently Asked Questions and Answers

Q1. Why Pulsar II consists of 2 accounts?

A: Pulsar consists of 2 accounts – IUA and AUA – in order to provide financial flexibility to

our customers. Regular premiums contributed for the minimum contribution period of the

policy will be allocated in the form of units to the “Initial Units Account”; any premiums

contributed thereafter will be allocated to the “AUA”.

If a customer suspends premium payment or makes withdrawal at the early stage of the

policy, the account value may not be sufficient to maintain the policy in effect. Hence, the

IUA is there to form the basis of Pulsar II policy such that the policy can be in effect for

the longest possible period. After the minimum contribution period, customer is allowed

to go on a premium holiday and may withdraw account value from the AUA in order to

accommodate their emergency cash needs during the TCP.

Q2. Apart from regular premium, can customers make any additional investment

contribution by paying lump sum premium?

A: No. Lump sum premium is not available in Pulsar II.

Q3. If a Pulsar II policy is surrendered before the end of the TCP, will the Start-up

Bonus paid to the policy be clawed back?

A: If the policy is surrendered during the MCP within the TCP, start-up Bonus paid to the

policy will be clawed back. However, if the policy is surrendered after the MCP before the

end of the TCP, start-up Bonus paid to the policy will not be clawed back. However,

during the EEC period, the Account Value relating to the Start-up Bonus will be subject to

an EEC when calculating the Surrender Value. After the EEC period, no EEC will be

charged. In the event that the policy is surrendered during the Minimum Contribution

Period, the Start-up clawed back will be deducted from the IUA value in calculation of the

EEC and the Surrender Value.

Q4. Can customers withdraw Account Value from the IUA during the TCP?

A: During TCP, no withdrawal from IUA is allowed. However, customers are allowed to

withdraw account value from the AUA only during the TCP, subject to a minimum

withdrawal amount of HKD4,000 / USD500 / EUR500 / GBP320 / AUD600 / SGD800 per

withdrawal. If withdrawal is made from the IUA during the TCP, policy termination will be

triggered and EEC will apply.

Q5. What should be noted about exercising a Premium Holiday?

A: Premium Holiday can only be taken after the Minimum Contribution Period of the policy.

During the Minimum Contribution Period, if the relevant regular premium due is not paid

after the expiry of the grace period, the policy will terminate and the EEC will apply.

Pulsar II Investment Insurance Plan

All information is for internal use and reference only P.38, total 51 pages

During Premium Holiday, Policy Charges will remain payable while regular premium

payments are suspended. This will lead to a reduction in the total amount of premiums

paid and affecting the account value, the death benefit and Loyalty Bonus will thus be

reduced accordingly.

Consultants should remind their customers that premium holiday is a short-term solution

for them to deal with financial difficulties only.

Q6. After the cessation of Premium Holiday, is customer allowed to pay back the

premiums suspended during the Premium Holiday?

A: After the cessation of Premium Holiday, customer is required to resume regular premium

only. No premiums suspended during the Premium Holiday is required to pay back.

Q7. If the total Account Value drops and becomes insufficient to cover the relevant

Policy Charges due during the Premium Holiday due to market fluctuations, will

the policy terminate?

A: If the total Account Value drops and becomes insufficient to cover the relevant Policy

Charges due during the Premium Holiday due to market fluctuations, the policy may not

terminate within the 31-day grace period. Regardless of a Premium Holiday has been

taken or not, the policy will terminate if the Policy Charges due remain outstanding after

the expiry of a grace period.

Q8. After going on Premium Holiday and resumed regular premium payment for

consecutive 12 months, is customer allowed to get back the Loyalty Bonus?

A: After taken a premium holiday at any time during the 12 months prior to the relevant

policy anniversary on which the Loyalty Bonus is payable, the entitlement to the loyalty

bonus on such policy anniversary is no longer retrieved.

However, if subsequently the payment of the regular premium is resumed, the

entitlement to the Loyalty Bonus will be resumed.

Q9. If wrong information was given in health declaration during application, how will

the death claim be handled?

A: We will rescind policy and reject death claim in terms of material non-disclosure. Total

premium paid less any deduction of the amount by which the value of investment has

fallen when rescission decision is made, will be refunded.

Q10. If answer(s) to the underwriting question(s) is/ are Yes, will the application be

rejected or be applied the loading?

A: Yes. It is subject to the underwriting decision.

Pulsar II Investment Insurance Plan

All information is for internal use and reference only P.39, total 51 pages

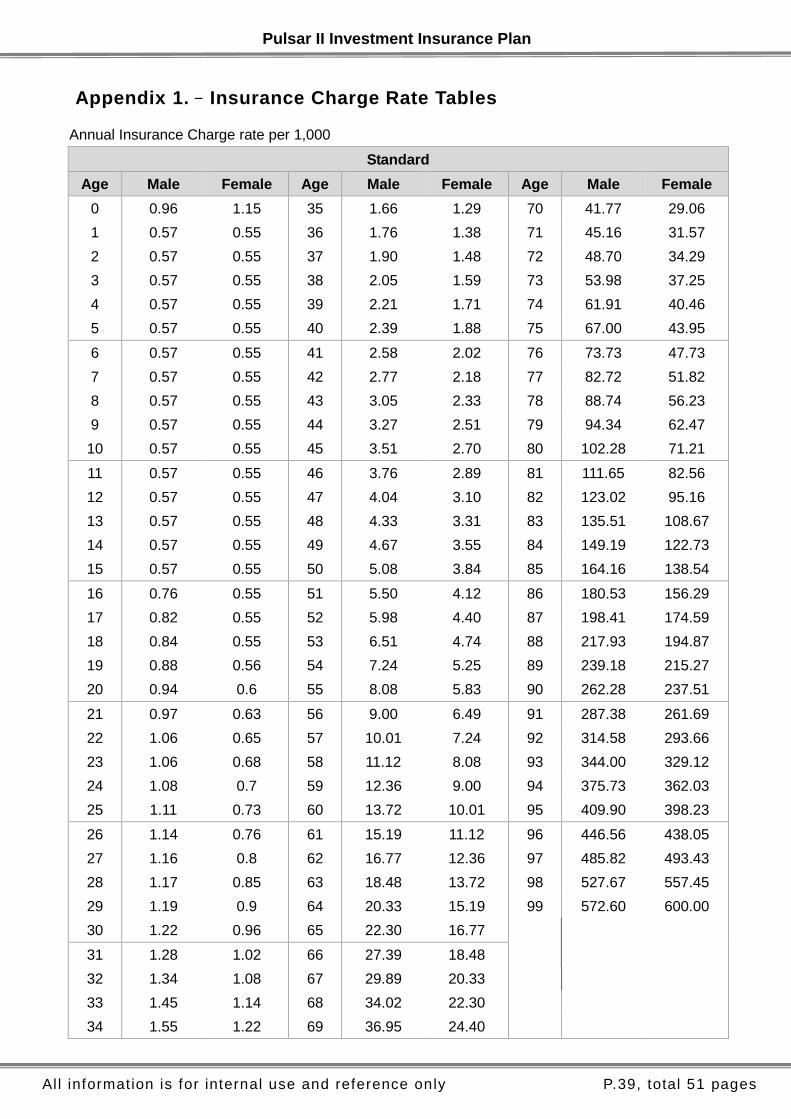

Appendix 1.– Insurance Charge Rate Tables

Annual Insurance Charge rate per 1,000

Standard

Age Male Female Age Male Female Age Male Female

0 0.96 1.15 35 1.66 1.29 70 41.77 29.06

1 0.57 0.55 36 1.76 1.38 71 45.16 31.57

2 0.57 0.55 37 1.90 1.48 72 48.70 34.29

3 0.57 0.55 38 2.05 1.59 73 53.98 37.25

4 0.57 0.55 39 2.21 1.71 74 61.91 40.46

5 0.57 0.55 40 2.39 1.88 75 67.00 43.95

6 0.57 0.55 41 2.58 2.02 76 73.73 47.73

7 0.57 0.55 42 2.77 2.18 77 82.72 51.82

8 0.57 0.55 43 3.05 2.33 78 88.74 56.23

9 0.57 0.55 44 3.27 2.51 79 94.34 62.47

10 0.57 0.55 45 3.51 2.70 80 102.28 71.21

11 0.57 0.55 46 3.76 2.89 81 111.65 82.56

12 0.57 0.55 47 4.04 3.10 82 123.02 95.16

13 0.57 0.55 48 4.33 3.31 83 135.51 108.67

14 0.57 0.55 49 4.67 3.55 84 149.19 122.73

15 0.57 0.55 50 5.08 3.84 85 164.16 138.54

16 0.76 0.55 51 5.50 4.12 86 180.53 156.29

17 0.82 0.55 52 5.98 4.40 87 198.41 174.59

18 0.84 0.55 53 6.51 4.74 88 217.93 194.87

19 0.88 0.56 54 7.24 5.25 89 239.18 215.27

20 0.94 0.6 55 8.08 5.83 90 262.28 237.51

21 0.97 0.63 56 9.00 6.49 91 287.38 261.69

22 1.06 0.65 57 10.01 7.24 92 314.58 293.66

23 1.06 0.68 58 11.12 8.08 93 344.00 329.12

24 1.08 0.7 59 12.36 9.00 94 375.73 362.03

25 1.11 0.73 60 13.72 10.01 95 409.90 398.23

26 1.14 0.76 61 15.19 11.12 96 446.56 438.05

27 1.16 0.8 62 16.77 12.36 97 485.82 493.43

28 1.17 0.85 63 18.48 13.72 98 527.67 557.45

29 1.19 0.9 64 20.33 15.19 99 572.60 600.00

30 1.22 0.96 65 22.30 16.77

31 1.28 1.02 66 27.39 18.48

32 1.34 1.08 67 29.89 20.33

33 1.45 1.14 68 34.02 22.30

34 1.55 1.22 69 36.95 24.40

Pulsar II Investment Insurance Plan

All information is for internal use and reference only P.40, total 51 pages

Appendix 2. - Monthly EEC Rate Table

During

policy

month

EEC rate (%) according to the chosen TCP (years)

10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25

1 51.00 52.00 52.00 53.00 53.00 54.00 55.00 56.00 57.00 58.00 59.00 59.00 62.00 62.00 65.00 65.00

2 50.75 51.66 51.75 52.66 52.75 53.66 54.75 55.75 56.75 57.75 58.75 58.75 61.75 61.75 64.75 64.75

3 50.50 51.33 51.50 52.33 52.50 53.33 54.50 55.50 56.50 57.50 58.50 58.50 61.50 61.50 64.50 64.50

4 50.25 51.00 51.25 52.00 52.25 53.00 54.25 55.25 56.25 57.25 58.25 58.25 61.25 61.25 64.25 64.25

5 50.00 50.66 51.00 51.66 52.00 52.66 54.00 55.00 56.00 57.00 58.00 58.00 61.00 61.00 64.00 64.00

6 49.75 50.33 50.75 51.33 51.75 52.33 53.75 54.75 55.75 56.75 57.75 57.75 60.75 60.75 63.75 63.75

7 49.50 50.00 50.50 51.00 51.50 52.00 53.50 54.50 55.50 56.50 57.50 57.50 60.50 60.50 63.50 63.50

8 49.25 49.66 50.25 50.66 51.25 51.66 53.25 54.25 55.25 56.25 57.25 57.25 60.25 60.25 63.25 63.25

9 49.00 49.33 50.00 50.33 51.00 51.33 53.00 54.00 55.00 56.00 57.00 57.00 60.00 60.00 63.00 63.00

10 48.75 49.00 49.75 50.00 50.75 51.00 52.75 53.75 54.75 55.75 56.75 56.75 59.75 59.75 62.75 62.75

11 48.50 48.66 49.50 49.66 50.50 50.66 52.50 53.50 54.50 55.50 56.50 56.50 59.50 59.50 62.50 62.50

12 48.25 48.33 49.25 49.33 50.25 50.33 52.25 53.25 54.25 55.25 56.25 56.25 59.25 59.25 62.25 62.25

13 48.00 48.00 49.00 49.00 50.00 50.00 52.00 53.00 54.00 55.00 56.00 56.00 59.00 59.00 62.00 62.00

14 47.41 47.41 48.33 48.33 49.25 49.25 51.16 52.25 53.25 54.25 55.25 55.33 58.50 58.58 61.66 61.75

15 46.83 46.83 47.66 47.66 48.50 48.50 50.33 51.50 52.50 53.50 54.50 54.66 58.00 58.16 61.33 61.50

16 46.25 46.25 47.00 47.00 47.75 47.75 49.50 50.75 51.75 52.75 53.75 54.00 57.50 57.75 61.00 61.25

17 45.66 45.66 46.33 46.33 47.00 47.00 48.66 50.00 51.00 52.00 53.00 53.33 57.00 57.33 60.66 61.00

18 45.08 45.08 45.66 45.66 46.25 46.25 47.83 49.25 50.25 51.25 52.25 52.66 56.50 56.91 60.33 60.75

19 44.50 44.50 45.00 45.00 45.50 45.50 47.00 48.50 49.50 50.50 51.50 52.00 56.00 56.50 60.00 60.50

20 43.91 43.91 44.33 44.33 44.75 44.75 46.16 47.75 48.75 49.75 50.75 51.33 55.50 56.08 59.66 60.25

21 43.33 43.33 43.66 43.66 44.00 44.00 45.33 47.00 48.00 49.00 50.00 50.66 55.00 55.66 59.33 60.00

22 42.75 42.75 43.00 43.00 43.25 43.25 44.50 46.25 47.25 48.25 49.25 50.00 54.50 55.25 59.00 59.75

23 42.16 42.16 42.33 42.33 42.50 42.50 43.66 45.50 46.50 47.50 48.50 49.33 54.00 54.83 58.66 59.50

24 41.58 41.58 41.66 41.66 41.75 41.75 42.83 44.75 45.75 46.75 47.75 48.66 53.50 54.41 58.33 59.25

25 41.00 41.00 41.00 41.00 41.00 41.00 42.00 44.00 45.00 46.00 47.00 48.00 53.00 54.00 58.00 59.00

26 40.66 40.66 40.66 40.66 40.66 40.66 41.58 43.41 44.33 45.25 46.16 47.16 52.08 53.08 57.08 58.08

27 40.33 40.33 40.33 40.33 40.33 40.33 41.16 42.83 43.66 44.50 45.33 46.33 51.16 52.16 56.16 57.16

28 40.00 40.00 40.00 40.00 40.00 40.00 40.75 42.25 43.00 43.75 44.50 45.50 50.25 51.25 55.25 56.25

29 39.66 39.66 39.66 39.66 39.66 39.66 40.33 41.66 42.33 43.00 43.66 44.66 49.33 50.33 54.33 55.33

30 39.33 39.33 39.33 39.33 39.33 39.33 39.91 41.08 41.66 42.25 42.83 43.83 48.41 49.41 53.41 54.41

31 39.00 39.00 39.00 39.00 39.00 39.00 39.50 40.50 41.00 41.50 42.00 43.00 47.50 48.50 52.50 53.50

32 38.66 38.66 38.66 38.66 38.66 38.66 39.08 39.91 40.33 40.75 41.16 42.16 46.58 47.58 51.58 52.58

33 38.33 38.33 38.33 38.33 38.33 38.33 38.66 39.33 39.66 40.00 40.33 41.33 45.66 46.66 50.66 51.66

34 38.00 38.00 38.00 38.00 38.00 38.00 38.25 38.75 39.00 39.25 39.50 40.50 44.75 45.75 49.75 50.75

35 37.66 37.66 37.66 37.66 37.66 37.66 37.83 38.16 38.33 38.50 38.66 39.66 43.83 44.83 48.83 49.83

Pulsar II Investment Insurance Plan

All information is for internal use and reference only P.41, total 51 pages

During

policy

month

EEC rate (%) according to the chosen TCP (years)

10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25

36 37.33 37.33 37.33 37.33 37.33 37.33 37.41 37.58 37.66 37.75 37.83 38.83 42.91 43.91 47.91 48.91

37 37.00 37.00 37.00 37.00 37.00 37.00 37.00 37.00 37.00 37.00 37.00 38.00 42.00 43.00 47.00 48.00

38 36.66 36.66 36.66 36.66 36.66 36.66 36.66 36.66 36.66 36.66 36.66 37.58 41.58 42.50 46.50 47.41

39 36.33 36.33 36.33 36.33 36.33 36.33 36.33 36.33 36.33 36.33 36.33 37.16 41.16 42.00 46.00 46.83

40 36.00 36.00 36.00 36.00 36.00 36.00 36.00 36.00 36.00 36.00 36.00 36.75 40.75 41.50 45.50 46.25

41 35.66 35.66 35.66 35.66 35.66 35.66 35.66 35.66 35.66 35.66 35.66 36.33 40.33 41.00 45.00 45.66

42 35.33 35.33 35.33 35.33 35.33 35.33 35.33 35.33 35.33 35.33 35.33 35.91 39.91 40.50 44.50 45.08

43 35.00 35.00 35.00 35.00 35.00 35.00 35.00 35.00 35.00 35.00 35.00 35.50 39.50 40.00 44.00 44.50

44 34.66 34.66 34.66 34.66 34.66 34.66 34.66 34.66 34.66 34.66 34.66 35.08 39.08 39.50 43.50 43.91

45 34.33 34.33 34.33 34.33 34.33 34.33 34.33 34.33 34.33 34.33 34.33 34.66 38.66 39.00 43.00 43.33

46 34.00 34.00 34.00 34.00 34.00 34.00 34.00 34.00 34.00 34.00 34.00 34.25 38.25 38.50 42.50 42.75

47 33.66 33.66 33.66 33.66 33.66 33.66 33.66 33.66 33.66 33.66 33.66 33.83 37.83 38.00 42.00 42.16

48 33.33 33.33 33.33 33.33 33.33 33.33 33.33 33.33 33.33 33.33 33.33 33.41 37.41 37.50 41.50 41.58

49 33.00 33.00 33.00 33.00 33.00 33.00 33.00 33.00 33.00 33.00 33.00 33.00 37.00 37.00 41.00 41.00

50 32.58 32.58 32.58 32.58 32.58 32.58 32.75 32.75 32.75 32.75 32.75 32.58 36.66 36.66 40.66 40.66

51 32.16 32.16 32.16 32.16 32.16 32.16 32.50 32.50 32.50 32.50 32.50 32.16 36.33 36.33 40.33 40.33

52 31.75 31.75 31.75 31.75 31.75 31.75 32.25 32.25 32.25 32.25 32.25 31.75 36.00 36.00 40.00 40.00

53 31.33 31.33 31.33 31.33 31.33 31.33 32.00 32.00 32.00 32.00 32.00 31.33 35.66 35.66 39.66 39.66

54 30.91 30.91 30.91 30.91 30.91 30.91 31.75 31.75 31.75 31.75 31.75 30.91 35.33 35.33 39.33 39.33

55 30.50 30.50 30.50 30.50 30.50 30.50 31.50 31.50 31.50 31.50 31.50 30.50 35.00 35.00 39.00 39.00

56 30.08 30.08 30.08 30.08 30.08 30.08 31.25 31.25 31.25 31.25 31.25 30.08 34.66 34.66 38.66 38.66

57 29.66 29.66 29.66 29.66 29.66 29.66 31.00 31.00 31.00 31.00 31.00 29.66 34.33 34.33 38.33 38.33

58 29.25 29.25 29.25 29.25 29.25 29.25 30.75 30.75 30.75 30.75 30.75 29.25 34.00 34.00 38.00 38.00

59 28.83 28.83 28.83 28.83 28.83 28.83 30.50 30.50 30.50 30.50 30.50 28.83 33.66 33.66 37.66 37.66

60 28.41 28.41 28.41 28.41 28.41 28.41 30.25 30.25 30.25 30.25 30.25 28.41 33.33 33.33 37.33 37.33

61 28.00 28.00 28.00 28.00 28.00 28.00 30.00 30.00 30.00 30.00 30.00 28.00 33.00 33.00 37.00 37.00

62 27.58 27.58 27.58 27.58 27.58 27.58 29.58 29.58 29.58 29.58 29.58 27.58 32.58 32.58 36.66 36.66

63 27.16 27.16 27.16 27.16 27.16 27.16 29.16 29.16 29.16 29.16 29.16 27.16 32.16 32.16 36.33 36.33

64 26.75 26.75 26.75 26.75 26.75 26.75 28.75 28.75 28.75 28.75 28.75 26.75 31.75 31.75 36.00 36.00

65 26.33 26.33 26.33 26.33 26.33 26.33 28.33 28.33 28.33 28.33 28.33 26.33 31.33 31.33 35.66 35.66

66 25.91 25.91 25.91 25.91 25.91 25.91 27.91 27.91 27.91 27.91 27.91 25.91 30.91 30.91 35.33 35.33

67 25.50 25.50 25.50 25.50 25.50 25.50 27.50 27.50 27.50 27.50 27.50 25.50 30.50 30.50 35.00 35.00

68 25.08 25.08 25.08 25.08 25.08 25.08 27.08 27.08 27.08 27.08 27.08 25.08 30.08 30.08 34.66 34.66

69 24.66 24.66 24.66 24.66 24.66 24.66 26.66 26.66 26.66 26.66 26.66 24.66 29.66 29.66 34.33 34.33

70 24.25 24.25 24.25 24.25 24.25 24.25 26.25 26.25 26.25 26.25 26.25 24.25 29.25 29.25 34.00 34.00

71 23.83 23.83 23.83 23.83 23.83 23.83 25.83 25.83 25.83 25.83 25.83 23.83 28.83 28.83 33.66 33.66

72 23.41 23.41 23.41 23.41 23.41 23.41 25.41 25.41 25.41 25.41 25.41 23.41 28.41 28.41 33.33 33.33

Pulsar II Investment Insurance Plan

All information is for internal use and reference only P.42, total 51 pages

During

policy

month

EEC rate (%) according to the chosen TCP (years)

10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25

73 23.00 23.00 23.00 23.00 23.00 23.00 25.00 25.00 25.00 25.00 25.00 23.00 28.00 28.00 33.00 33.00

74 22.58 22.58 22.58 22.58 22.58 22.58 24.58 24.58 24.58 24.58 24.58 22.58 27.58 27.58 32.58 32.58

75 22.16 22.16 22.16 22.16 22.16 22.16 24.16 24.16 24.16 24.16 24.16 22.16 27.16 27.16 32.16 32.16

76 21.75 21.75 21.75 21.75 21.75 21.75 23.75 23.75 23.75 23.75 23.75 21.75 26.75 26.75 31.75 31.75

77 21.33 21.33 21.33 21.33 21.33 21.33 23.33 23.33 23.33 23.33 23.33 21.33 26.33 26.33 31.33 31.33

78 20.91 20.91 20.91 20.91 20.91 20.91 22.91 22.91 22.91 22.91 22.91 20.91 25.91 25.91 30.91 30.91

79 20.50 20.50 20.50 20.50 20.50 20.50 22.50 22.50 22.50 22.50 22.50 20.50 25.50 25.50 30.50 30.50

80 20.08 20.08 20.08 20.08 20.08 20.08 22.08 22.08 22.08 22.08 22.08 20.08 25.08 25.08 30.08 30.08

81 19.66 19.66 19.66 19.66 19.66 19.66 21.66 21.66 21.66 21.66 21.66 19.66 24.66 24.66 29.66 29.66

82 19.25 19.25 19.25 19.25 19.25 19.25 21.25 21.25 21.25 21.25 21.25 19.25 24.25 24.25 29.25 29.25

83 18.83 18.83 18.83 18.83 18.83 18.83 20.83 20.83 20.83 20.83 20.83 18.83 23.83 23.83 28.83 28.83

84 18.41 18.41 18.41 18.41 18.41 18.41 20.41 20.41 20.41 20.41 20.41 18.41 23.41 23.41 28.41 28.41

85 18.00 18.00 18.00 18.00 18.00 18.00 20.00 20.00 20.00 20.00 20.00 18.00 23.00 23.00 28.00 28.00

86 17.58 17.58 17.58 17.58 17.58 17.58 19.50 19.50 19.50 19.50 19.50 17.58 22.58 22.58 27.58 27.58

87 17.16 17.16 17.16 17.16 17.16 17.16 19.00 19.00 19.00 19.00 19.00 17.16 22.16 22.16 27.16 27.16

88 16.75 16.75 16.75 16.75 16.75 16.75 18.50 18.50 18.50 18.50 18.50 16.75 21.75 21.75 26.75 26.75

89 16.33 16.33 16.33 16.33 16.33 16.33 18.00 18.00 18.00 18.00 18.00 16.33 21.33 21.33 26.33 26.33

90 15.91 15.91 15.91 15.91 15.91 15.91 17.50 17.50 17.50 17.50 17.50 15.91 20.91 20.91 25.91 25.91

91 15.50 15.50 15.50 15.50 15.50 15.50 17.00 17.00 17.00 17.00 17.00 15.50 20.50 20.50 25.50 25.50

92 15.08 15.08 15.08 15.08 15.08 15.08 16.50 16.50 16.50 16.50 16.50 15.08 20.08 20.08 25.08 25.08

93 14.66 14.66 14.66 14.66 14.66 14.66 16.00 16.00 16.00 16.00 16.00 14.66 19.66 19.66 24.66 24.66

94 14.25 14.25 14.25 14.25 14.25 14.25 15.50 15.50 15.50 15.50 15.50 14.25 19.25 19.25 24.25 24.25

95 13.83 13.83 13.83 13.83 13.83 13.83 15.00 15.00 15.00 15.00 15.00 13.83 18.83 18.83 23.83 23.83

96 13.41 13.41 13.41 13.41 13.41 13.41 14.50 14.50 14.50 14.50 14.50 13.41 18.41 18.41 23.41 23.41

97 13.00 13.00 13.00 13.00 13.00 13.00 14.00 14.00 14.00 14.00 14.00 13.00 18.00 18.00 23.00 23.00

98 12.50 12.50 12.50 12.50 12.50 12.50 13.41 13.41 13.41 13.41 13.41 12.50 17.58 17.58 22.58 22.58

99 12.00 12.00 12.00 12.00 12.00 12.00 12.83 12.83 12.83 12.83 12.83 12.00 17.16 17.16 22.16 22.16

100 11.50 11.50 11.50 11.50 11.50 11.50 12.25 12.25 12.25 12.25 12.25 11.50 16.75 16.75 21.75 21.75

101 11.00 11.00 11.00 11.00 11.00 11.00 11.66 11.66 11.66 11.66 11.66 11.00 16.33 16.33 21.33 21.33

102 10.50 10.50 10.50 10.50 10.50 10.50 11.08 11.08 11.08 11.08 11.08 10.50 15.91 15.91 20.91 20.91

103 10.00 10.00 10.00 10.00 10.00 10.00 10.50 10.50 10.50 10.50 10.50 10.00 15.50 15.50 20.50 20.50

104 9.50 9.50 9.50 9.50 9.50 9.50 9.91 9.91 9.91 9.91 9.91 9.50 15.08 15.08 20.08 20.08

105 9.00 9.00 9.00 9.00 9.00 9.00 9.33 9.33 9.33 9.33 9.33 9.00 14.66 14.66 19.66 19.66

106 8.50 8.50 8.50 8.50 8.50 8.50 8.75 8.75 8.75 8.75 8.75 8.50 14.25 14.25 19.25 19.25

107 8.00 8.00 8.00 8.00 8.00 8.00 8.16 8.16 8.16 8.16 8.16 8.00 13.83 13.83 18.83 18.83

108 7.50 7.50 7.50 7.50 7.50 7.50 7.58 7.58 7.58 7.58 7.58 7.50 13.41 13.41 18.41 18.41

109 7.00 7.00 7.00 7.00 7.00 7.00 7.00 7.00 7.00 7.00 7.00 7.00 13.00 13.00 18.00 18.00

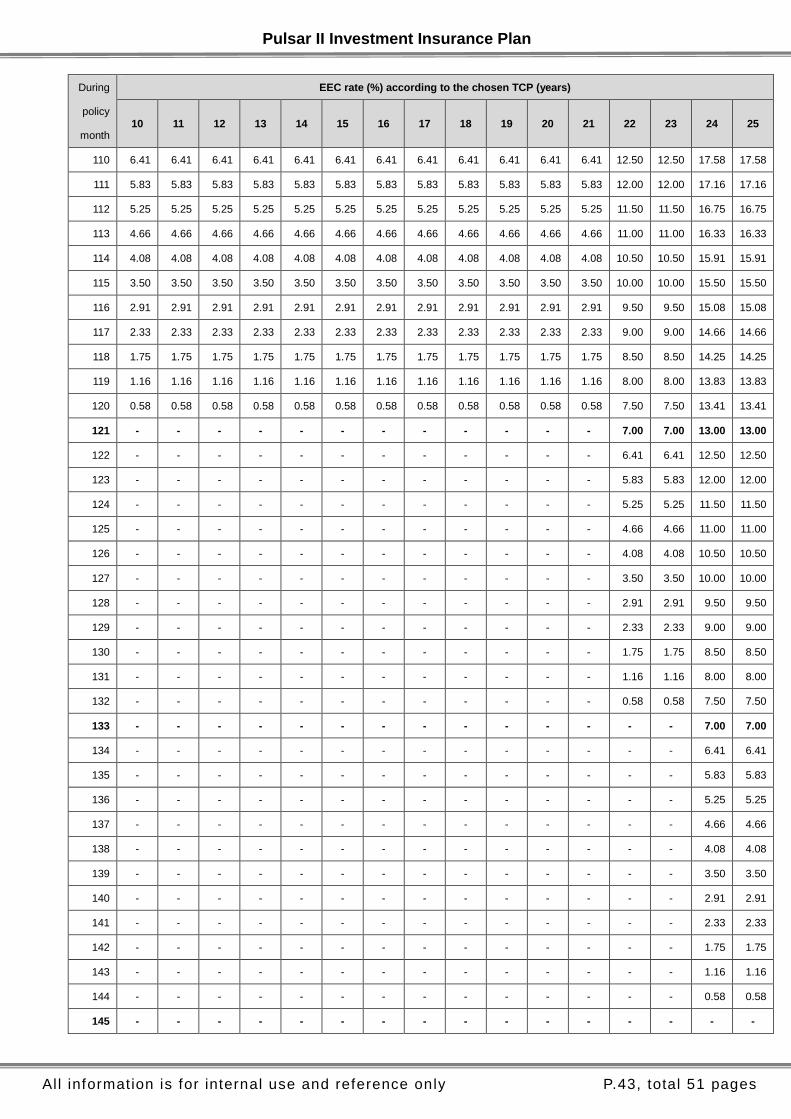

Pulsar II Investment Insurance Plan

All information is for internal use and reference only P.43, total 51 pages

During

policy

month

EEC rate (%) according to the chosen TCP (years)

10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25

110 6.41 6.41 6.41 6.41 6.41 6.41 6.41 6.41 6.41 6.41 6.41 6.41 12.50 12.50 17.58 17.58

111 5.83 5.83 5.83 5.83 5.83 5.83 5.83 5.83 5.83 5.83 5.83 5.83 12.00 12.00 17.16 17.16

112 5.25 5.25 5.25 5.25 5.25 5.25 5.25 5.25 5.25 5.25 5.25 5.25 11.50 11.50 16.75 16.75

113 4.66 4.66 4.66 4.66 4.66 4.66 4.66 4.66 4.66 4.66 4.66 4.66 11.00 11.00 16.33 16.33

114 4.08 4.08 4.08 4.08 4.08 4.08 4.08 4.08 4.08 4.08 4.08 4.08 10.50 10.50 15.91 15.91

115 3.50 3.50 3.50 3.50 3.50 3.50 3.50 3.50 3.50 3.50 3.50 3.50 10.00 10.00 15.50 15.50

116 2.91 2.91 2.91 2.91 2.91 2.91 2.91 2.91 2.91 2.91 2.91 2.91 9.50 9.50 15.08 15.08

117 2.33 2.33 2.33 2.33 2.33 2.33 2.33 2.33 2.33 2.33 2.33 2.33 9.00 9.00 14.66 14.66

118 1.75 1.75 1.75 1.75 1.75 1.75 1.75 1.75 1.75 1.75 1.75 1.75 8.50 8.50 14.25 14.25

119 1.16 1.16 1.16 1.16 1.16 1.16 1.16 1.16 1.16 1.16 1.16 1.16 8.00 8.00 13.83 13.83

120 0.58 0.58 0.58 0.58 0.58 0.58 0.58 0.58 0.58 0.58 0.58 0.58 7.50 7.50 13.41 13.41

121 - - - - - - - - - - - - 7.00 7.00 13.00 13.00

122 - - - - - - - - - - - - 6.41 6.41 12.50 12.50

123 - - - - - - - - - - - - 5.83 5.83 12.00 12.00

124 - - - - - - - - - - - - 5.25 5.25 11.50 11.50

125 - - - - - - - - - - - - 4.66 4.66 11.00 11.00

126 - - - - - - - - - - - - 4.08 4.08 10.50 10.50

127 - - - - - - - - - - - - 3.50 3.50 10.00 10.00

128 - - - - - - - - - - - - 2.91 2.91 9.50 9.50

129 - - - - - - - - - - - - 2.33 2.33 9.00 9.00

130 - - - - - - - - - - - - 1.75 1.75 8.50 8.50

131 - - - - - - - - - - - - 1.16 1.16 8.00 8.00

132 - - - - - - - - - - - - 0.58 0.58 7.50 7.50

133 - - - - - - - - - - - - - - 7.00 7.00

134 - - - - - - - - - - - - - - 6.41 6.41

135 - - - - - - - - - - - - - - 5.83 5.83

136 - - - - - - - - - - - - - - 5.25 5.25

137 - - - - - - - - - - - - - - 4.66 4.66

138 - - - - - - - - - - - - - - 4.08 4.08

139 - - - - - - - - - - - - - - 3.50 3.50

140 - - - - - - - - - - - - - - 2.91 2.91

141 - - - - - - - - - - - - - - 2.33 2.33

142 - - - - - - - - - - - - - - 1.75 1.75

143 - - - - - - - - - - - - - - 1.16 1.16

144 - - - - - - - - - - - - - - 0.58 0.58

145 - - - - - - - - - - - - - - - -

Pulsar II Investment Insurance Plan

All information is for internal use and reference only P.44, total 51 pages

Appendix 3. – Sample Application Form

Pulsar II Investment Insurance Plan

All information is for internal use and reference only P.45, total 51 pages

Pulsar II Investment Insurance Plan

All information is for internal use and reference only P.46, total 51 pages

Pulsar II Investment Insurance Plan

All information is for internal use and reference only P.47, total 51 pages

Pulsar II Investment Insurance Plan

All information is for internal use and reference only P.48, total 51 pages

Pulsar II Investment Insurance Plan

All information is for internal use and reference only P.49, total 51 pages

Pulsar II Investment Insurance Plan

All information is for internal use and reference only P.50, total 51 pages

Pulsar II Investment Insurance Plan

All information is for internal use and reference only P.51, total 51 pages

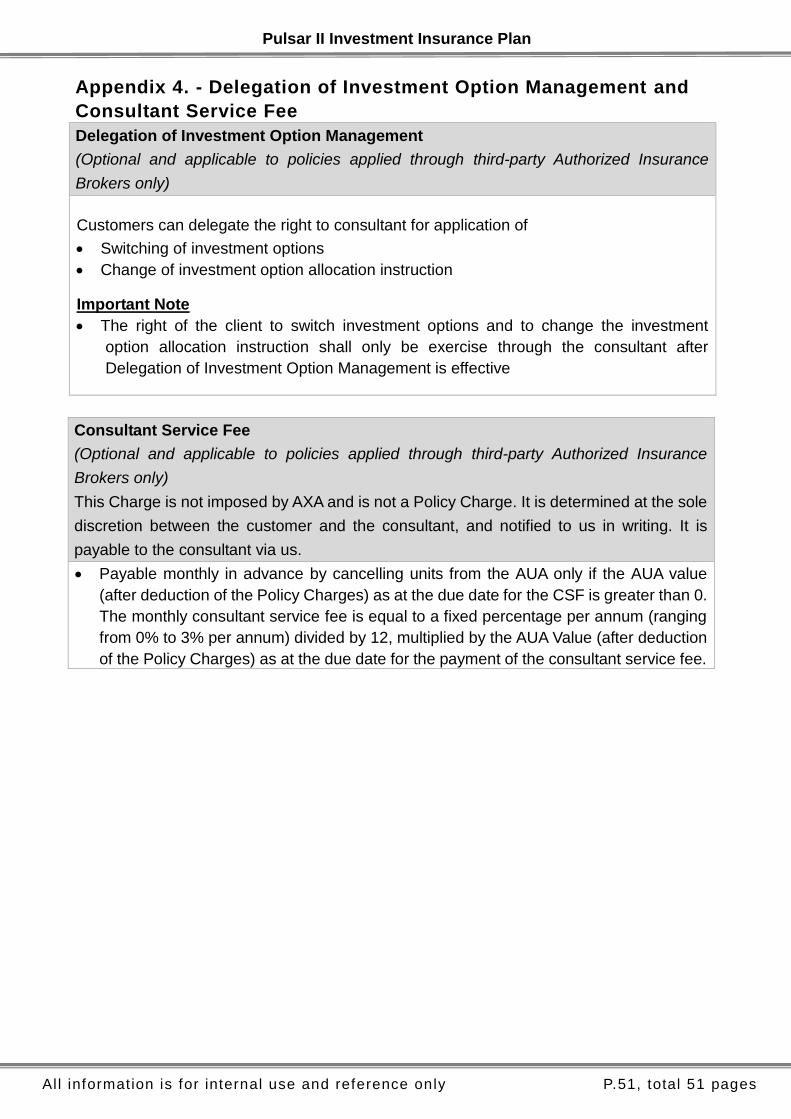

Appendix 4. - Delegation of Investment Option Management and

Consultant Service Fee

2. Delegation of Investment Option Management

3. (Optional and applicable to policies applied through third-party Authorized Insurance

Brokers only)

Customers can delegate the right to consultant for application of

Switching of investment options

Change of investment option allocation instruction

Important Note

The right of the client to switch investment options and to change the investment

option allocation instruction shall only be exercise through the consultant after

Delegation of Investment Option Management is effective

4. Consultant Service Fee

5. (Optional and applicable to policies applied through third-party Authorized Insurance

Brokers only)

This Charge is not imposed by AXA and is not a Policy Charge. It is determined at the sole

discretion between the customer and the consultant, and notified to us in writing. It is

payable to the consultant via us.

Payable monthly in advance by cancelling units from the AUA only if the AUA value

(after deduction of the Policy Charges) as at the due date for the CSF is greater than 0.

The monthly consultant service fee is equal to a fixed percentage per annum (ranging

from 0% to 3% per annum) divided by 12, multiplied by the AUA Value (after deduction

of the Policy Charges) as at the due date for the payment of the consultant service fee.

Prepared by Life Product Development

January 2015